")

BHP looks to China as a “stabilising force”

If detailed reporting makes you happy, this quarterly update is for you

BHP’s quarterly reports are enough to get the heart racing of any Excel enthusiast, with literally pages upon pages of detailed production disclosures.

For the rest of us who just want a vague idea of what’s going on, the key point is that production guidance for the 2023 financial year remains unchanged. There are some good bits (like record production at Western Australia Iron Ore) and some disappointing bits (Escondida copper in Chile and BHP Mitsubishi Alliance both trending to the low end of their ranges).

In some operations, unit cost guidance has been increased due to wet weather and inflationary pressures. Remember, high rainfall isn’t good news for miners, with coal mining in Queensland having been affected by this.

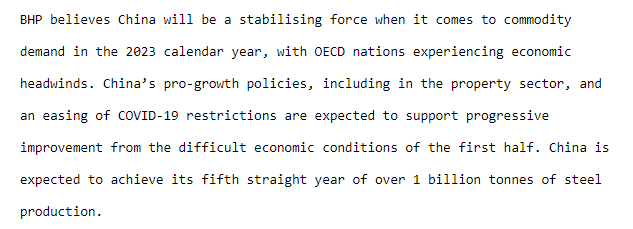

Here’s perhaps the most important comment of all, which I’ve decided to include in full:

Kore Potash quarterly review

If you ever fancied working in the Republic of Congo, perhaps read this first

Other than arguments with the Minister of Mines in the Republic of Congo (which included the arrest without charge of two senior employees of the company in that country), Kore Potash’s focus has been on securing the financing required for the Kola Potash Project in that country.

The SEPCO Electric Power Construction Corporation is negotiating contractual terms with Kore Potash for the Engineering, Procurement and Construction (EPC) proposal. Once this is in place, a financial proposal is expected from the Summit Consortium.

The company has $5 million in cash after investing nearly $1.1 million in exploration this quarter.

There’s never a dull moment when doing business in Africa, especially in the mining industry and especially in a country like the Republic of Congo.

Spar tries to take some of the heat off the share price

The market liked it, with a 3.9% rally

If you’ve been following the Spar updates, you’ll know that the management team is leaving amid allegations of poor corporate governance and even fictitious and fraudulent loans.

Spar has moved to reassure the market, with three important points raised:

- Allegations of discrimination against retailers were investigated by a law firm (one that I’ve never heard of) and the allegations were unfounded. Spar is in a mediation process with the retailers that lodged claims.

- In an example of a professional services firm that I have heard of, PricewaterhouseCoopers notified Spar of a loan that is a reportable irregularity. Upon further investigations, it was found to be a an “isolated matter” that occurred five years ago with a total value of R11 million.

- Among the significant changes to the board, the retirement of Brett Botten as CEO is “pursuant to his request to the board for an early retirement”.

Look, I would also retire early instead of dealing with this kind of pain. The announcement of a new Group CEO will be made in due course.

Is this enough to give investors confidence in the company once more? I suspect that many will wait to find out who the new CEO is before taking a longer term position.

Woolworths is continuing to deliver its turnaround

But watch out for load shedding costs and pressure on gross margin

It’s been a huge year for Woolworths, with share price growth of 27.5%. For longer term holders, the picture looks less like fancy Belgian yoghurt and more like old polony, with total growth of around 4% over five years.

Markets are all about timing. Don’t let anyone tell you otherwise.

The reason that Woolworths has done well in the past year is that the management team is doing the right things. They are reducing trading space, taking Woolworths back to its roots and reducing exposure to Australia, a country where we shouldn’t play cricket or try and own retail businesses. Country Road seems to be an exception. David Jones certainly wasn’t.

For the 26 weeks ended 25 December 2022, group turnover is up by a whopping 16.3% in constant currency terms and 18.5% as reported. There were substantial lockdowns in the base period in Australia, so this isn’t a fair indication of group performance.

A better comparison is to use the last 6 weeks of the period, in which sales increased by 8.8%. Woolworths sounds happy with Black Friday and festive season trade.

As we are seeing in many retailers, consumers have returned to bricks-and-mortar stores and online shopping has slowed down. Without a doubt, some of the changed behaviour will stick and most retailers have reported online sales that are still way ahead of pre-pandemic levels. Woolworths has highlighted the return to stores in Australia in particular, though the base effect of hectic lockdowns would be highly relevant here.

Online sales at group level now contribute 10.9% of total turnover vs. 13.7% in the prior period.

Looking deeper, Fashion Beauty Home sales in South Africa were up 11.2% and accelerated to 12% in the final six weeks. Price movement was 10.8%, so inflation helps here alongside some volume growth. Space was reduced by 2.2%, so trading density (sales per square metre) has definitely improved. Online sales in this segment grew 4.5% and contribute 4.2% of South African sales.

Food is where much of the pressure has been thanks to competitors taking a bite out of Woolworths’ customer base, especially as they trade down in search of value. This has forced Woolworths to become more competitive on price, evidenced by price movement of 6.8% vs. food inflation of 8.4%. Sales were up 5.4% on a comparable store basis, which suggests a drop in volumes. As trading space is increasing, total growth was higher at 7.6%. Online sales grew by 22.7%, now contributing 3.6% of local sales as Woolworths Dash gets some traction in the market.

The Woolworths Financial Services book is 17.2% larger, suggesting that Woolworths has been more willing to give credit. With an annualised impairment rate of 5.5% vs. 4.0% in the prior period, that willingness does come at a cost.

In Australia, Country Road Group is the business that Woolworths is holding on to and sales grew by 25.5%. Again, the base effect skews this. In the last six weeks of the period, growth was 8.5% despite trading space decreasing by 5.5%. Online sales contributed 26.1% to total sales vs. 33.8% in the comparable period.

Woolworths has agreed to sell its stake in David Jones and that deal should be completed by the end of March. With sales performance in those six weeks of just 2.3%, shareholders won’t be sad to see this one go.

The expected increase in HEPS for the 26 weeks ended 25 December 2022 is between 70% and 80%, coming in at between 285.9 cents and 302.8 cents.

The market celebrated these numbers with a jump in the share price of nearly 4.8%.

Little Bites:

- Director dealings:

- An associate of a director of Afrimat has sold shares in the company worth R3.85 million.

- On the 1st of February, history will be made on the JSE when Fortress REIT Limited will no longer be a REIT. The name change is coming. The biggest question is what other changes are coming, particularly to the shareholder register? Personally, I’m not sure that losing REIT status is the end of the world here, but time will tell.

- Shareholders have voted in favour of Aveng’s proposed sale of Trident Steel, which isn’t a surprise based on the pricing achieved.

- Trematon owns 50% in a property in Woodstock that is being sold to a coffee shop for R16.25 million. As tiny as this deal is, it’s a small related party transaction and that means an independent expert needs to be appointed to opine on the fairness of the deal.

Covid: The Fall of Mankind…

Nice one.