")

AVI is treading water and maintaining flat earnings

But consumer pressures are a bigger problem than load shedding

For the six months ended December, AVI suffered the significant impact of load shedding in its manufacturing operations. Keeping the lights on in a retail store is one thing, but managing an entire manufacturing back-end is something else entirely.

Alternative power solutions added R22 million to operating costs. Although that isn’t a catastrophe for a R25 billion market cap company, it’s still painful. It may be a red herring though, as the bigger problems are in consumer spending.

Volumes are under pressure in some categories, as cutting luxuries from the grocery basket is an easy way to save money. Group revenue increased by 7.2%, with pricing as the bulk of the story here. As is always the case in these types of businesses, category-level performance can vary drastically. For example, I&J fell 2.3% with lower catch rates and other issues, while the fashion brand portfolio grew by 17.4%.

An important update is that the consolidated gross margin increased slightly, a solid outcome in an environment where margin pressure is common. The mix effect will be a major contributor here.

Without I&J, operating profit would’ve been up 8.4%. Including that business, group operating profit could only manage growth of 1.7%.

Below that line, there’s still the pressure from net finance costs, which increased as borrowings and rates were both higher. Inflation leads to bigger balance sheets, which is why I was bullish on banks last year. They sit on the other side of this issue for operating companies.

Overall, headline earnings per share (HEPS) for the period are expected to be between 0% and 1% higher, coming in at between 316.9 cents and 320.1 cents. The share price fell more than 3% on this news, as AVI doesn’t trade at the cheapest multiples around.

MiX Telematics releases strong quarterly results

Shareholders can smile at record subscriber growth and significant margin expansion

For some reason, MiX Telematics doesn’t bother to write a proper SENS announcement to go out with the results. Instead, you have to go digging on the website for the quarterly update. Investor relations laziness aside, the results look good.

With record net quarterly subscriber additions of 44,600, the subscriber base is now over 959,000. Revenue increased by 14% on a constant currency basis and adjusted EBITDA increased from $6 million to $8.4 million for the quarter.

You probably noticed the dollar signs. This is because MiX Telematics is listed on the JSE and the New York Stock Exchange, with the company choosing to report in dollars.

With adjusted EBITDA margin of 22.2% vs. 17% in the prior quarter, there’s good news here for the company. The other good news is that free cash flow is positive again, after timing of investment in inventory worked its way through the system.

In the next quarter, the management team hopes to see further improvement in margins. Heck, they might even make enough money to afford someone who can write a decent summary of the result on SENS.

Shareholders look set to get something OUT

Core earnings at OUTsurance are looking strong

For the six months ended December, the listed group formerly known as Rand Merchant Investment Holdings has released results that are mainly attributable to the OUTsurance business. Having cleaned out almost everything else, the group recently changed its name to OUTsurance Group Limited.

The insurance operations are in Australia (under the Youi brand) and in South Africa under the OUTsurance brand that we all know. In both cases, the performance is good. The reasons vary.

In Australia, fewer natural peril claims have helped alongside premium growth and a more favourable investment environment. Indeed, the only recent disaster in Australia of any consequence was our cricket tour there, which is sadly an uninsurable event.

In South Africa, premium growth was strong and the claims experience was in line with historical levels, so there’s a return to normality.

There are a million distortions in the headline earnings per share (HEPS) number at group level, due to the extensive disposals of assets by the group. The important number is normalised earnings for the insurance businesses that are now the core of the group, which increased by over 20% for the six-month period.

Even Truworths can figure out load shedding

The market doesn’t give Truworths much credit – will this update change that?

You know, it doesn’t seem that hard to think of a solution here. When the power is out, invest in energy backups so your customers aren’t shopping by smartphone torchlight.

Yes?

No?

It depends on which retailer we are talking about. Whilst Mr Price spent its time writing SENS announcements about how bad load shedding is, the likes of Truworths (and The Foschini Group and Woolworths) just got on with it.

With the Truworths numbers now in the wild, there are no excuses left for the shocking numbers from Mr Price. Truworths grew retail sales by 13.0% on a comparable basis for the 26 weeks to 1 January 2023. The growth was strong both locally (13.4%) and in the UK (12.3%).

Yes, there’s a timing impact here. The first part of the 26-week period was much butter than in the last 9 weeks that were hit by load shedding. I suspect that Mr Price would raise this point in its defence, as the Mr Price update only covered the Black Friday and festive season. Still, the gap in performance is so huge that timing alone cannot explain it.

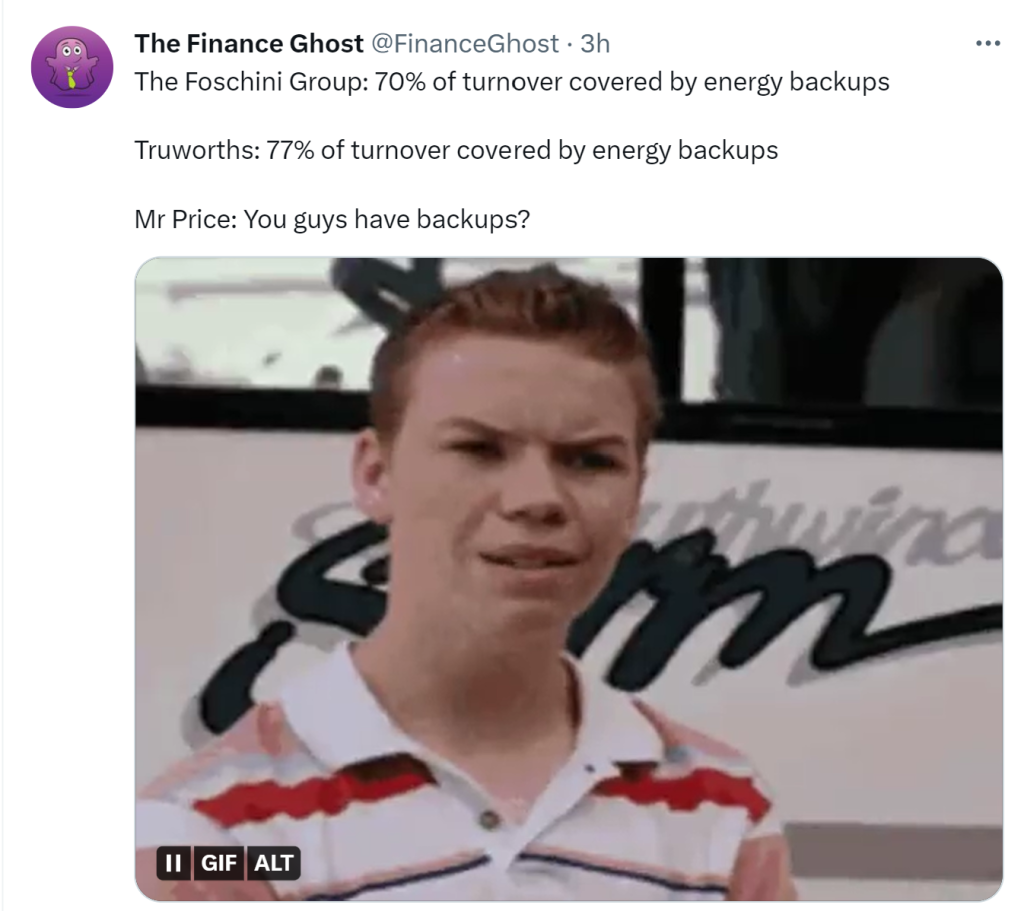

Perhaps the extent of backup power has something to do with it? I’ll just defer to my Twitter here:

The numbers look good even as you dig deeper, with healthy growth across account (16.0%) and cash (9.9%) sales. Account sales contributed 51% of group sales. With inflation of 13.3%, I must highlight that volumes seem to have dipped slightly. Still, that’s decent in this environment.

In the UK where they have lots of electricity and not a lot of sunshine, retail sales at the Office segment were up by 12.3% in local currency. Online sales contributed 44% of total revenue, down from 47% in the comparable period. There was a nifty acceleration in that business, with sales up 15.1% in the last nine weeks of the period.

Trading space increased by 0.8% in Truworths Africa and was reduced by 3.8% in Office.

Headline earnings per share (HEPS) for the 26 weeks to 1 January 2023 are expected to be between 8% and 11% higher, coming in at 485 to 498 cents. Famous for trading on a modest multiple, the Truworths share price increased by over 4%.

Little Bites:

- Director dealings:

- An associate of the CEO of Spear REIT sold shares worth R309k and an associate of the CFO sold nearly R3.4m worth of shares – are interest rates starting to bite?

- A director of Dipula Income Fund bought shares worth over R207k and an associate of a different director bought shares worth R1.44m.

- A director of EOH has bought shares worth just under R100k.

- Anglo American continues to make progress in having more efficient heavy machinery in its operations. You may recall the hydrogen mining truck that caused quite a buzz when it was launched. Now, we have an LNG dual-fuelled vessel, the first of ten such vessels that Anglo will use in its chartered fleet in 2023 and 2024. As part of the goal to achieve carbon neutrality by 2040, these vessels will cut CO2 emissions by 35% vs. conventional marine fuel vessels. The maiden voyage is a haul of iron ore from Kumba.

- Here’s an unusual one for you: the CEO of AECI has accelerated his retirement by a few months, leaving to pursue other interests. A current independent non-executive director has been appointed as CEO while the group looks for a successor. This isn’t exactly a great handover, is it?

Two things that bugs me this morning.

One, is’t there any opportunity for M&A in the vehicle tracking & recovery industry. With Cartreck , Nestar & Telematics being significant players with ambitions for global growth. Especially those that are listed in Nasdaq?

Secondly, ?Henry Laas and the Murray and Roberts board turning down the company being bought by the Germany company ( being a major shareholder at the time) should they not fall into the sword since the share has nosedived since then. Where’s the accountability from a fiduciary duty point of view?