Listen to the latest episode of Ghost Wrap here:

Emira wants to buy the rest of Transcend (JSE: EMI | JSE: TPF)

And they aren’t prepared to pay a premium for it

With a bid-offer spread as wide as the moon and practically zero liquidity, shareholders in Transcend only have one realistic way to exit their positions: sell to Emira. This is because Emira holds 68.15% of the shares in issue, so it can easily block an offer from anyone else.

This leaves major shareholders in Transcend stuck in an illiquid rut and unable to realise the value of their stake. It’s therefore not surprising that holders of 18.61% in the company have already given irrevocable undertakings to accept Emira’s offer of R6.30 per share, even though this implies no premium to the current traded price. This represents 58.41% of the voting class (as Emira can’t vote), so this proposed scheme of arrangement is already a long way down the road towards 75% approval.

With Transcend’s net asset value (NAV) per share as at March 2023 of R8.23, the offer price is a 23% discount to NAV. This is unfortunately what happens when there is only one obvious buyer for the stake and no liquidity to offer people an alternative way to exit. When buying stocks in a takeout basket and hoping for a premium, this is important to take into account.

As a final comment on this price, this discount to NAV isn’t terribly different to other takeout prices we’ve seen on the JSE. Where there has been a premium offered to shareholders, it’s because the traded discount to NAV was much higher.

Libstar suffers a substantial drop in earnings (JSE: LBR)

Here’s another casualty of this operating environment

With a drop in the share price this year of over 30%, the market has been pricing in terrible numbers at Libstar. With the release of a trading statement for the six months to June, we now know just how tough it has been. The numbers seem to be in line with what the market expected, as the share price hardly moved in response.

Revenue growth was just 4% and selling price inflation and mix contributed 10.7% to growth. This immediately tells you that volumes were down, in this case by 6.7%.

Part of the drop in volumes is because Libstar discontinued certain unprofitable lines in the retail business, so that’s technically a good thing. The destruction of the Shongweni mushroom production facility in the second half of 2022 certainly wasn’t a good thing, obviously leading to a sharp drop in fresh mushroom production. Excluding the impact of these issues, retail volumes would’ve been up by 1%.

The industrial and export channels didn’t do well for various reasons.

With lower volumes in a manufacturing company, you would expect to see a drop in gross profit margin. This has played out here, with gross profit down by 5.6% despite revenues up 4%. Gross margin was consistent with the second half of 2022 at least.

The same can’t be said for diesel costs. The company spent R8m in H1’22, R31m in H2’22 and a whopping R45m in this period. Pricing increases could only partly mitigate this impact.

Against this backdrop, normalised EBITDA (a good proxy for operating profit) fell by between 17.3% and 19.3%. This is before we consider net finance costs, which jumped by 71% because of higher interest rates.

HEPS has dropped by between 54.9% and 59.8%, so this is a period that Libstar will want to forget. Normalised HEPS from continuing operations fell by between 42.4% and 47.5%.

Detailed results are due on 12 September. The company has noted that initiatives around the strategic direction will be shared at the same time.

Sibanye’s HEPS has approximately halved (JSE: SSW)

All the PGM players are in the same boat, as one would expect

Sibanye-Stillwater is shielded to a small extent from the decline in PGM prices by its gold exposure. It’s nowhere near enough to stop the pain though, with HEPS for the six months to June down by between 48% and 53%. With a 22% drop in the average rand basket price for PGMs, they never stood a chance, even with the base period including the horrors of the industrial action in the gold business.

On top of the negative move in the cycle, Sibanye has had to content with other issues like a shaft incident at Stillwater.

Sibanye cannot control market prices for commodities but can control production. Local PGM production was flat (a solid outcome), Stillwater’s PGM production was down 11% because of the operational issues and local gold increased by 233% because the base period was a catastrophe.

The share price is down 34% this year, though it remains a ridiculous 285% higher over five years. Mining cycles are wild things.

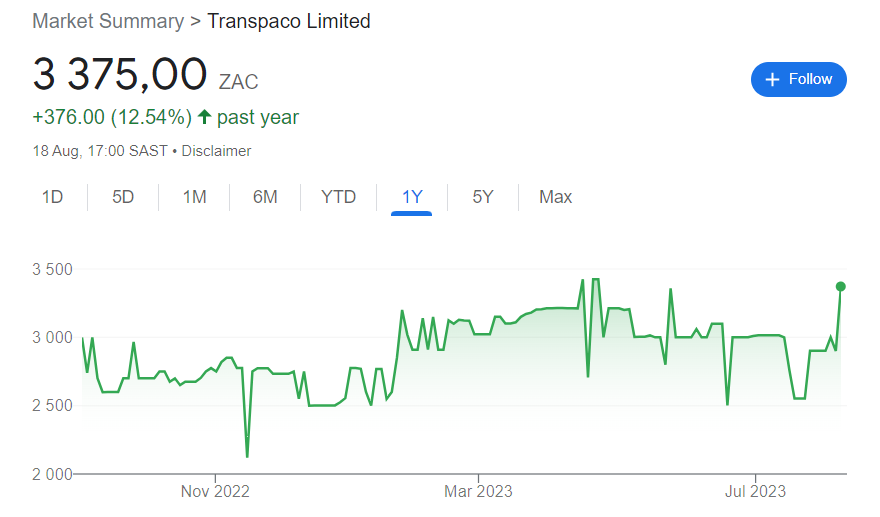

Transpaco: low on stock liquidity, high on earnings growth (JSE: TPC)

This small cap is heading in the right direction

With a market cap of under R900 million and a wide bid-offer spread, Transpaco has a share price chart that is typical of a stock with low liquidity. Whenever you see long horizontal lines, it’s because the stock is thinly traded:

This doesn’t mean that the company isn’t growing. In a trading statement for the year ended June 2023, Transpaco announced that HEPS will increase by between 16% and 22%. This means a range of 554 cents to 582 cents.

The share price is around R29, so that’s a Price/Earnings multiple of roughly 5x.

Little Bites:

- Director dealings:

- With results now released and Standard Bank (JSE: SBK) no longer in a closed period, a couple of prescribed officers and an associate of a director collectively sold shares worth around R12.8m.

- The same is true at Investec (JSE: INP), where a director and a prescribed officer collectively sold R2.8m worth of shares.

- Des de Beer has bought another R6m worth of shares in Lighthouse (JSE: LTE).

- A director of Santova (JSE: SNV) sold shares worth R426k.

- AngloGold (JSE: ANG) shareholders have said yes to the proposed reorganisation of the company, which effectively internationalises the holding structure of the group.