")

In this edition of Ghost Bites:

- Bidcorp is growing despite global conditions

- British American Tobacco is on track for the lower end of guidance

- Plenty of dealmaking at Burstone, but where’s the growth?

- A flat period at Invicta – but for a specific reason

- Momentum’s Capital Markets Day makes for good reading

- Santova: good business, tough environment

- Telkom is brimming with confidence

Bidcorp is growing despite global conditions (JSE: BID)

There is plenty of resilience in this business

Bidcorp is a genuinely excellent business. With global food service operations built through a combination of organic growth and bolt-on acquisitions, the company is one of the best examples of a South African operation that successfully grew offshore.

In a trading update for the ten months to April 2026, Bidcorp has shown revenue growth of 5.1% and trading profit growth of 7.0%, both in constant currency. This margin uplift was achieved through gross margins rising by 20 basis points, an important offset to operating cost pressures.

Due to the extent of offshore earnings, the currency moves play a big role here. As reported in rands, revenue growth was 3.8% and trading profit growth was 6.1%.

HEPS increased by 7.1% in constant currency, or 6.6% in rands. It’s not an outcome that will make you rich, but it’s a commendable performance in a difficult market.

The strength of the balance sheet allowed Bidcorp to repurchase 0.7% of shares in issue during this period for around R1.3 billion. The share price is down 12% over the past 12 months and is currently stuck in a range, so taking advantage through share buybacks seems sensible to me:

Digging deeper, the UK business continues to face a “very negative” macro environment. Gross margin is up in that business, but operating costs are a concern due to wage inflation among other factors.

In Europe, they’ve enjoyed strong performance in places like Italy and Eastern Europe. The Western European markets faced an increasingly competitive environment. Like so many regions, “Europe” is an umbrella term for countries that have very different underlying characteristics.

Australia’s income was flat for the period, with weak consumer sentiment making that market treacherous. New Zealand saw a recovery though.

In the emerging markets business, there was a strong performance in Latin America, South Africa and other countries like Malaysia. China remains difficult, while the Middle East was obviously impacted significantly by events in Iran. Interestingly, Bidcorp has flagged a return to “more normal” levels of activity in the Middle East.

And finally, you guessed it – there’s a mention of AI! Bidcorp has created a Digital Acceleration Office in Amsterdam to drive investment in digital platforms and AI enhancements. There really are two types of companies out there at the moment: those that want to still exist in 10 years, and those that want to die. Bidcorp is in the former bucket.

Ghost Bite: Bidcorp is a company I’ve always wanted to own, but the valuation has been very hard to justify. The stock has returned next to nothing over three years. The Price/Earnings multiple is now in a far more reasonable range of mid-teens, so I’m keeping a keen eye on this one.

British American Tobacco is on track for the lower end of guidance (JSE: BTI)

For those willing to buy it, this stock has been a strong performer

British American Tobacco is “firmly on track” to deliver their guidance for the year. In practice, this means the lower end of the medium-term guided range of 3% to 5% revenue growth.

Global cigarette industry volumes are expected to be down 2.5% in FY26 vs. the previous expectation of 2%. Being in a dying industry, literally, is quite the growth headwind. To offset this trend, the New Category growth at the company is in the mid-teens (ahead of their previous expectations).

British American Tobacco is essentially running on a treadmill set to a high pace, something that most of its historical customers can only dream of doing. It’s all about generating profit growth in excess of revenue growth, with adjusted diluted earnings per share targeted to grow by between 5% and 8% (they are at the bottom of this range as well for FY26).

Cash returns to shareholders are a function of cash conversion and the strength of the balance sheet. British American Tobacco needs to run a leveraged balance sheet to juice up the returns to investors, with a target corridor of 2x – 2.5x net debt to adjusted EBITDA. Once again, they expect to be in this range by the end of the year.

The total return on the stock of 25% over the past 12 months is much better than you’ll find in many other companies. Over three years, the total return of 92% is even more impressive.

Ghost Bite: This stock isn’t for me, but there are many investors willing to pay up for defensive earnings like these. Each to their own. But what do you think?

Plenty of dealmaking at Burstone, but where’s the growth? (JSE: BTN)

When will the platform strategy really start to pay off?

Burstone’s roots lie in financial structuring and the incubation of a property business within a bank. This thinking still comes through strongly in their strategy, as they are focused on building property platforms that are capable of attracting the opium of bankers everywhere: Other People’s Money.

That’s a clever strategy from a return on capital perspective. Earning management fees on capital provided by somebody else is a good way to juice up your return on equity, for example. But investors still want to see growth.

For the year ended March 2026, Burstone’s full year distributable income per share was up by just 2.2%. We can’t really make the excuse that this is a hard currency return, as 80% of the group’s earnings are from South Africa!

The net asset value per share stayed flat at R11.79, with real estate valuation gains offset by non-cash movements. Again, nothing to get excited about here whatsoever.

The local portfolio is doing the heavy lifting, with like-for-like growth in net operating income of 4.2%. Despite negative reversions increasing to 7.9%, the portfolio valuation moved upwards by 5%. They are expecting a strong year again in FY27, particularly thanks to the yields on solar deployment.

They expect to finalise the launch of a “South African Core Plus” property platform within the next three months. They need to get on with it, as the macroeconomics are moving against the property sector at the moment. Another interest rate hike or two won’t be good news for the REITs.

As for Europe, there was a nasty decline in like-for-like earnings of 12.5%. Burstone has launched a European light industrial platform with R2.5 billion in third-party equity commitments. I hope the returns will get a whole lot better going forwards. They are targeting yields of 6.5% to 7.5% on acquisitions, with a cost of funding of between 4.5% and 5.0%.

In Australia, where they are still very early in their journey, investment income from real estate was R27 million. They earned fee income of R9 million. You can contrast this to Europe, where fund and asset management fee income was R111 million.

The group balance sheet has a loan-to-value ratio of 39.6%, which is on the high side. It was 36.3% in the previous financial period.

The guidance for FY27 is distributable income per share growth of 4% to 6%. Thanks to a planned increase in the payout ratio to 92.7%, the distribution per share is expected to grow by 7% to 9%.

Ghost Bite: Burstone is one of the more complicated property models on the JSE. The total return (share price plus dividends) of 19.6% over 12 months appears to be flattering relative to the underlying performance in the business.

A flat period at Invicta – but for a specific reason (JSE: IVT)

Earnings growth is ever so slightly in the green

Invicta’s trading statement for the year ended March 2026 tells a story of a challenging macroeconomic environment and the short-term impact of a major acquisition.

HEPS is only up by between 0% and 2%, with the deal for Spaldings having negatively affected HEPS in this period. Spaldings is trading in line with budget and is expected to be profitable in the next financial period.

If you split out Spaldings and focus on the rest of the business, HEPS would’ve been up by between 6% and 8%.

Ghost Bite: Invicta has smart people running the place. The company offers exposure to the “real economy” across several geographies. I maintain a small long-term position in the company.

Momentum’s Capital Markets Day makes for good reading (JSE: MTM)

You can learn a lot from these events

Momentum hosted a Capital Markets Day on Tuesday that gives investors a huge pack of slides to sink their teeth into. I’ll just touch on a few concepts here.

The Momentum strategy includes six focus areas. As with all great corporate strategies, the targets are both broad and vague enough to give management some wriggle room.

I also had to smile at the progress indicators, which range from “fully confident” down to “de- / reprioritised” – a particularly glowing take on “we didn’t get this one right”. It’s also a scoring system of green / amber / grey! No red detected…

Thankfully, the company is doing well overall, so there are mainly green progress indicators. They are improving collaboration across the various business clusters and unlocking cost savings along the way. They are pushing hard into advice, which I believe is the right strategy in financial services (you always want to own the client). The various initiatives are adding up to a return on equity of 23.3%, which is already well above the FY27 target.

As noted in the results the other day, the value of new business margin is an industry-wide issue at the moment and a key focus area.

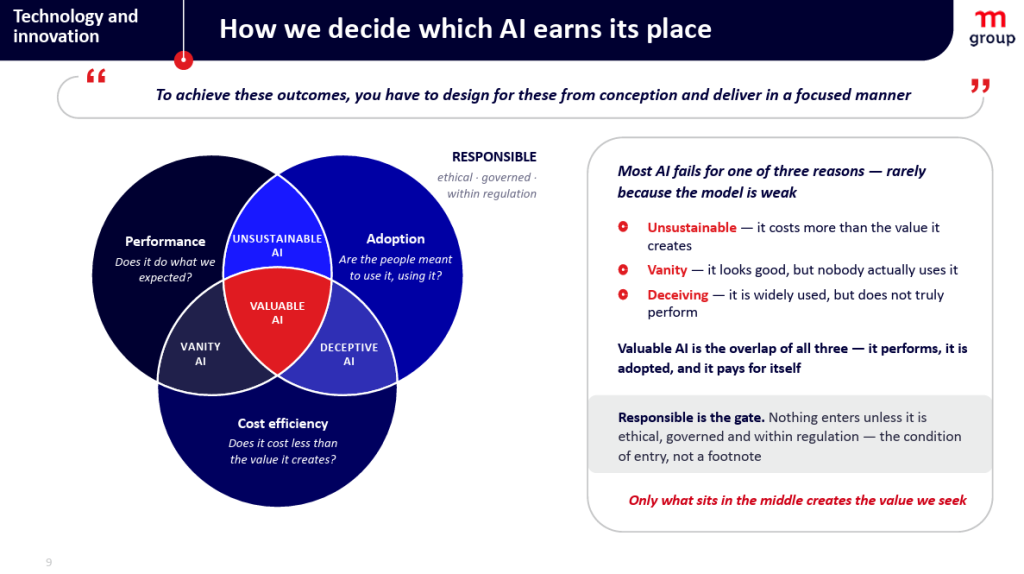

There’s an interesting chart in the deck that shows the use of cash over the past three years. 48% has gone into dividends and 29% into share buybacks. They’ve retained 23% to invest in the underlying business. Shareholders are being richly rewarded here.

But perhaps the most interesting chart of all is this one dealing with AI investment:

Ghost Bite: Capital Markets Days are wonderful things. More companies should do them!

Santova: good business, tough environment (JSE: SNV)

The global trade environment deserves a break

For whatever reason, there’s a delay of almost a week between the release of results by Santova and the related analyst presentation. At least they make up for it by including a huge amount of commentary in the slides.

One of the points they make is that the tariffs in 2025 took container ship orderbooks to lows not seen in more than a decade. This is the important context to Santova’s tale of two halves, with profit down 23.4% in the first six months before they clawed it back to a full-year decrease of only 5% (excluding Seabourne Group).

Seabourne has been fully integrated into Santova’s systems, so investors will be looking for that benefit to come through in FY27. The market understands that the first year of an acquisition is often quite messy.

The deal weights the group exposure even further offshore, with 84.6% of group revenue being generated in foreign lands. Europe was the largest contributor at 46.6%, with the UK up next at 29.5%. Both those regions now reflect the new business model, which includes express courier and fulfilment centres.

Interestingly, this means that Santova is thematically positioned for eCommerce in Europe! They are also pushing into tech-driven supply chain consultancy work, which they justify based on companies deploying AI and focusing more on data analytics. How’s that for a pivot?

Unsurprisingly, the North American business suffered a loss for the year. There’s not much that they could do about the tariffs. With a net profit margin that barely makes it into double-digits outside of Africa, it really hurts when one of the operations is making losses. The group net profit margin for the period was 12.6%.

The business in Africa is the standout, with a net margin of 28.5%!

Ghost Bite: Santova can be thought of as a company that is doing its best in a hostile global trade environment. The lack of a dividend means that there isn’t a yield underpin to the valuation. They focus on buybacks instead, but all they managed to do in FY26 was offset the impact of share options to employees! The concern here remains around flow through of cash to shareholders.

Telkom is brimming with confidence (JSE: TKG)

Juicy dividends are coming through the system

Telkom has been a superstar of the local market in recent years. If you can believe it, the total return over three years is 135%! This is an incredible reward for those who were willing to take a punt on this turnaround story.

Telkom is different to the leading telcos on the JSE, as the company isn’t generating most of its growth in other countries in Africa. Group revenue was up by just 1.4% in the year ended March 2026, with the good news story in Consumer and even Openserve being partially offset by BCX. Notably, Openserve has contributed positively to growth for the first time in nine financial years!

It’s when you dig into the product-level performance that you’ll see the growth engines really shine through. For example, mobile data revenue was up by 10.5%. Group data revenue (across all business segments) contributes 59.8% of total revenue.

Telkom Consumer is the business that is causing a major headache for competitors in South Africa. With a 31.1% jump in mobile data subscribers and an increase of 10.3% in prepaid service revenue, Telkom is focused on winning in the domestic market. It’s a strategy that works, particularly when they are competing against giants who are giving most of their attention to challenging frontier markets in Africa.

EBITDA was a stronger story than revenue, with that metric up 5.8% as margin expanded to 28.1%. And by the time we reach adjusted HEPS, there’s a 21.5% increase for shareholders to celebrate.

Reported HEPS shows a much higher growth rate, but that’s because of major distortions in the base. When management suggests that you use a lower rate, that’s usually the right approach. The time to be skeptical is when they suggest using a higher rate.

Perhaps the most impressive highlight lies in the cash trend. Free cash flow was up by 10.4%, giving the balance sheet a further boost.

The dividend was up 3.5%, but that growth rate is heavily skewed by the special dividend from the proceeds of the Swiftnet disposal in the prior year. If you look at only the ordinary dividend, the growth rate is a pretty spectacular 66%!

Ghost Bite: The significant jump in the payout ratio is a sign of confidence from management. Telkom is executing successfully on a credible strategy.

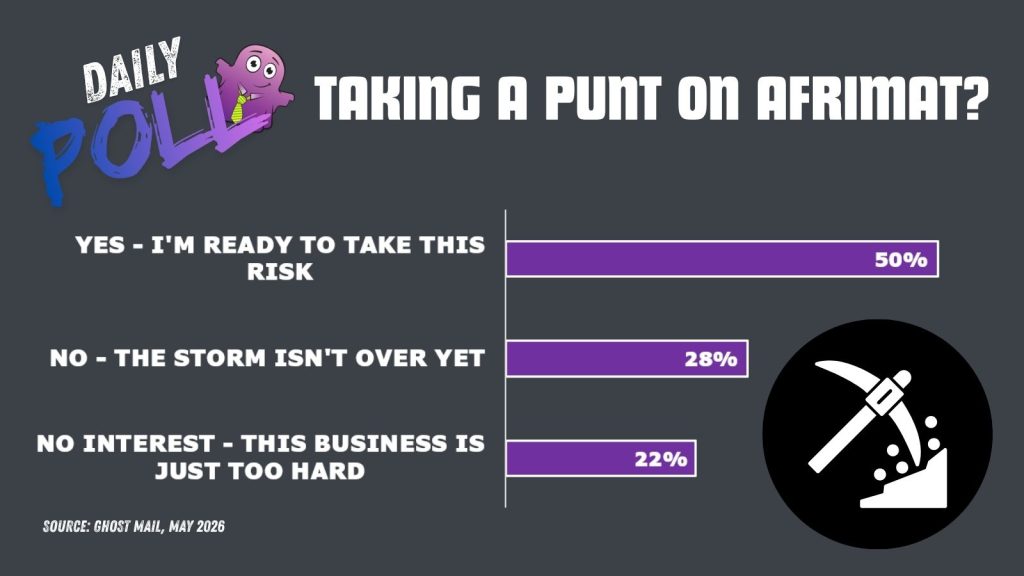

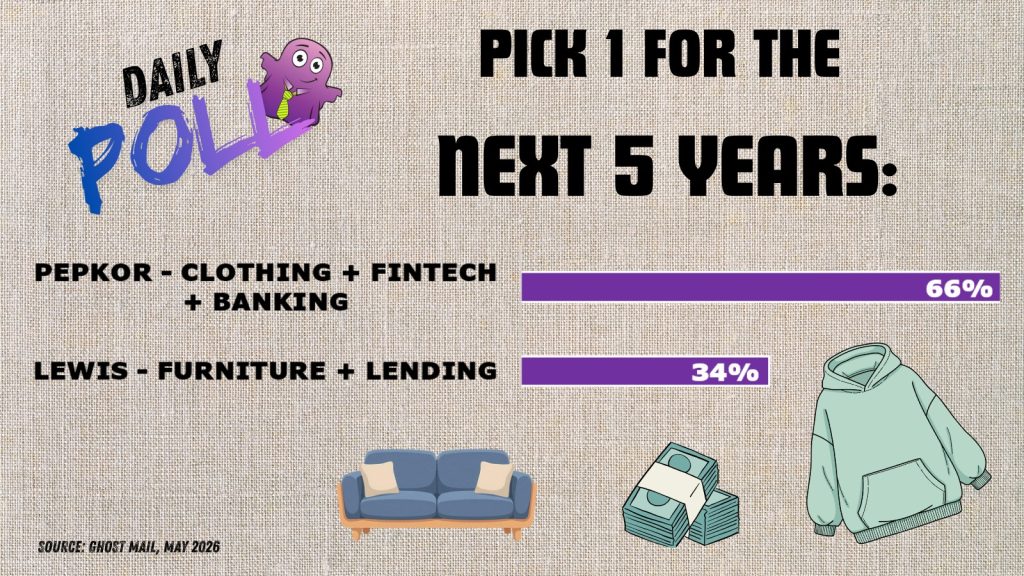

Results of previous poll:

Nibbles:

- Director dealings:

- A director of Richemont (JSE: CFR) has sold shares in the company worth around R7 million.

- A director of a major subsidiary of AVI (JSE: AVI) received share awards and sold the whole lot for R2.7 million.

- A director of Santova (JSE: SNV) exercised options and then sold all the shares for a total of R1.5 million.

- A director of Nampak (JSE: NPK) bought shares worth just over R1 million.

- A non-executive director of Clientèle (JSE: CLI) and immediate family members sold shares worth a total of just over R800k.

- The spouse of a non-executive director of Santam (JSE: SNT) bought shares worth R563k.

- There’s some action at Europa Metals (JSE: EUZ). They are looking to acquire some antimony and gold assets in Austria of all places. Antimony is listed as a critical mineral in the US and Europe, particularly due to its military applications. They are playing firmly into the localisation trend here, with the isolationist policies of global superpowers driving renewed focus on secure supply chains. This would require a raise of A$4 million, accompanied by a listing on the Australian Stock Exchange where you’ll find deep capital pools for mining assets. The current controlling shareholder of these assets, Torey Marshall, will become CEO of Europa Metals if the transaction goes through.

- UK-based property fund Hammerson (JSE: HMN) has priced a five-year EUR350 million bond at around 3.875% per annum (110 basis points over the euro mid-swaps rate). The issuance was five times covered, so there was no shortage of demand. They are partially refinancing some very cheap 1.75% sustainability-linked bonds maturing in June 2027. After this issuance, the weighted average maturity of debt is 4.7 years. The company noted that the FY26 guidance for earnings is unchanged.

- Newpark REIT (JSE: NRL) has renewed the cautionary announcement related to a potential shareholder proposal that “may present an opportunity for shareholders to monetise some or all of their shares”. Practically, this could take many different forms. We will have to wait and see if anything materialises.

- Shareholders of Trematon (JSE: TMT) gave a resounding approval to the deal to sell Club Mykonos Langebaan. That’s a major step forward in the value unlock process.

")

")

")

")

")

")

")