The well-balanced MSCI All Country World Index (ACWI) captures opportunities by optimising on long-term returns, while also managing risk.

This index achieves this through broad market exposure, which also shields investors from concentrated risk, whether by market, region, or currency.

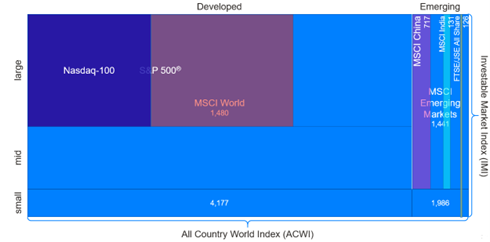

The MSCI ACWI includes both developed and emerging markets in one single index. The index is composed of large- and mid-cap stocks across 23 developed and 24 emerging market countries. With over 2 900 constituents, the index covers approximately 85% of the global investable equity opportunity universe, drawing diversified regional revenue, and can serve as a building block in investors’ overall asset allocation strategy. This index provides exposure to economies that may experience faster growth, yet higher volatility.

The below chart shows how broad the index is and how it compares to the universe of shares from other major indices.

Figure 1: Source – Satrix, MSCI, December 2023

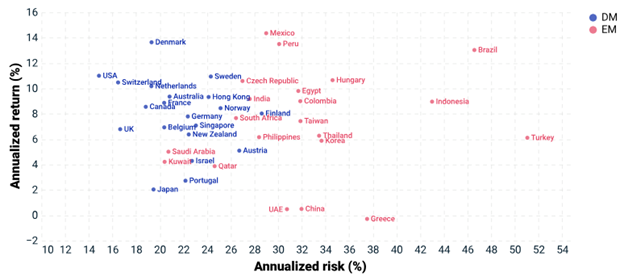

To understand the opportunities in broad market exposure, the chart below shows the annualised returns of regions included in the MSCI ACWI, with data from 1988 to end of December 2023.

Figure 2: Source – MSCI, January 1988 to December 2023 Monthly USD returns DM: Developed Markets EM: Emerging Markets

There is also a clear difference in risk profiles, depending on the region, and a big dispersion in market returns. Rolling the dice by choosing only one or two regional exposures in the hopes of achieving high returns, while minimising capital loss, is a risk. Regional market returns can contrast each other, and this is where the MSCI ACWI index provides investors with a broader exposure – to all the opportunities within markets scattered across the chart.

Growth in different regions

In the above graph there is a clear indication of a difference in risk profiles, depending on the region, while there is a big dispersion in market returns as well. Frequent political turmoil, monetary policies, and volatile currencies can be attributed to emerging markets being on the higher end of the risk scale. However, these regions provide a diversified and entirely different opportunity set compared to developed markets.

An interesting example of this is the luxury-led French market (developed) in comparison to South Africa’s resources-led market (emerging); each with their own factors, opportunities, and limitations.

The International Monetary Fund has revised its growth estimates for Asia, with China and India accounting for most of the upward revision. The MSCI All Country World Index provides investors with an opportunity to diversify across traditional developed market regions and high-growth emerging market regions. Over 60% of its exposure comes from its US constituents, which generate around 45% of its revenues. China accounts for 10% of revenue exposure, with Japan at 5%. India comes in at 3% and South Korea at 3% as well.

The Satrix MSCI ACWI ETF

Investors looking to access the broad range of companies from developed and emerging markets within a single fund can do so via the new Satrix MSCI ACWI ETF that listed on the JSE main board on 22 February 2024. This local ETF offers an efficient and low-cost investment that captures thousands of stocks across many jurisdictions, all in a single trade. The fund is non-distributing, with a TER of 0.35%, and is priced in rands.

SatrixNOW is a no-minimum online investing platform from Satrix that allows you to buy and sell ETFs directly.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Alphamin releases detailed results (JSE: APH)

The catch-up quarter was highly lucrative

Investors had a good idea of what was coming in the results for the first quarter of the year, as Alphamin had already released several key metrics. Full results are now available, showing a quarter-on-quarter increase of 1% in production. That’s not the exciting part. The juicy bit is that sales volumes are up 102% i.e. have doubled, as the business could catch up on sales that didn’t happen in the three months to December due to infrastructure issues.

Tin pricing did the company a favour as well, up 7% vs. the preceding quarter. When this is combined with the sales volumes, it won’t surprise you to learn that EBITDA is up 156% vs. the preceding quarter. These numbers helped reduce net debt from $73 million to $28 million over the past three months. It also helps fund a final dividend of CAD$0.03 per share (Alphamin is listed in Canada).

And in case you’re wondering whether this result is just a function of a super soft base, it’s worth pointing out that net profit is up 25% year-on-year.

The Mpama South plant is ready for a ramp-up in tin concentrate production during May 2024, so that should bring another significant boost to Alphamin.

The share price is up 28% in the past 12 months and a rather ridiculous 404% in the past five years.

Astral Foods is celebrating vastly better numbers (JSE: ARL)

The poultry industry really deserved a break

Astral Foods has some excellent news for investors. For the six months ended March 2024, the company achieved an eyewatering increase in HEPS. The percentage growth, for what it’s worth, is between 435% and 445%!

It’s a lot more useful to know that HEPS increased from 163 cents to between 874 cents and 891 cents per share. When you see a move like this, you have to go back a few periods to give it more context. In doing so, you’ll find that earnings have been exceptionally volatile, as the industry has had to manage everything from avian flu through to lockdowns.

Here’s a summary of HEPS for the past few interim periods:

March 2024: 874 – 891 cents

March 2023: 163 cents

March 2022: 1,420 cents

March 2021: 597 cents

If you enjoy rollercoasters, now you know which sector to look at.

BHP comments on the Samarco settlement (JSE: BHG)

The company has responded to press speculation

The Samarco dam failure in 2015 really was a disaster in every sense of the word. It led to incredible heartache in the area and has cost many billions of dollars for BHP and Vale, the joint investors in Samarco.

There is regular speculation in the press around the progress in settling with the Brazilian State and Federal Government and other public entities. BHP tends to respond to speculation by issuing SENS announcements and clarifying the situation.

The current status is that BHP, Vale and Samarco have submitted a non-binding, indicative settlement proposal. Although the total amount under the proposal is $25.7 billion, this includes amounts already invested to date. The present value of BHP’s share of remaining payments is within the provision of $6.5 billion already on the BHP balance sheet as at 31 December 2023.

No final agreement has been reached yet among the parties.

Kore Potash is close to concluding the EPC contract (JSE: KP2)

The big meeting in Beijing is in early May

Kore Potash is as close as they’ve ever been to getting the all-important Engineering, Procurement and Construction (EPC) proposal for the Kola Potash project in the Republic of Congo across the line. The counterparty is PowerChina International Group and an immense amount of effort has been put into this from both sides.

The proposal was received by Kore Potash on 6 February and the parties have been negotiating since then. A meeting is set for Beijing in early May to hopefully get this thing finalised. It all sounds very James Bond, doesn’t it?

I’ll tell you what isn’t very James Bond: a cash balance of only $1.4 million. Kore Potash recently raised funding to try and get the company to the point where the contract is signed. Without the EPC contract, there’s no funding available for the next step. Thankfully, the Summit Consortium has been on the hook since April 2021 to provide funding as soon as the EPC is finalised, with a promise to put the financing in within six weeks of the execution of the contract.

And on top of all of this, the management of Kore Potash has needed to keep relations with the government of the Republic of Congo nice and friendly. This includes local ceremonies attended by dignitaries. When you dedicate your life to junior mining projects in Africa, you’ve decided to play business on hard mode.

It would be lovely to see this go ahead. Hopefully, May will see the finalisation of that contract.

Raubex’s numbers are significantly better than expected (JSE: RBX)

Despite the Beitbridge Border Post project being in the base year, there’s still solid growth

Raubex took a conservative stance on its prospects for the year ended February 2024. The Beitbridge Border Post project was in the base period and not in this one, so there was doubt over whether Raubex could grow vs. that base. The company tried hard to manage investor expectations accordingly.

As recently as March, Raubex had indicated HEPS growth of between 0% and 10% for the year, which was already a solid outcome for the group. The latest trading statement is far more exciting than that, reflecting HEPS growth of between 15% and 25%. This really is an impressive outcome, with full details due to be released on 13 May.

HEPS will be between 451.7 cents and 491 cents for the full year and the current share price is R30.50.

Little Bites:

Director dealings:

The CFO of Thungela (JSE: TGA) implemented a collar hedge structure with a put strike price of R131.93 and a call price of R175.45 with expiry in April 2026. That put price (which gives downside protection) is very close to the current price of R130.33 per share. The hedge relates to a position of 250,000 shares, which is worth nearly R33 million.

Astoria Investments (JSE: ARA) released its numbers for the quarter ended March 2024. The quarterly updates are basically just the movement in net asset value (NAV) and other financial metrics, without much commentary on underlying assets. Measured in dollars, the net asset value per share has dipped 2.9% in the past 12 months. The decrease is nearly 7.7% over three months. Most of the assets are in rands, so the dollar-based reporting hurts the NAV. In rands, it’s actually up over 12 months! The NAV per share is currently R13.8502 and the share price is R8.19.

Ibex Investment Holdings (JSE: IBX), formerly Steinhoff Investment Holdings, announced the repurchase of its listed preference shares. The prefs will be repurchased for R93.50 plus a dividend for the period from 1 January 2024 until the scheme is implemented. The scheme consideration is a 7.13% premium to the 30-day VWAP and gives holders a chance to monetise their shares in this highly illiquid structure. This really does show you the importance of understanding complex capital structures. Steinhoff ordinary shareholders saw their value disappear, whereas preference shareholders have come out in one piece.

Ellies (JSE: ELI) announced that the court application to liquidate Ellies Holdings is still underway. Subsidiary Ellies Electronics remains in business rescue and is continuing to trade, with the proposed business rescue plan due to be published by 10 May 2024. At subsidiary level, there is still a reasonable prospect of Ellies Electronics being rescued.

Salungano (JSE: SLG) announced that Robinson Ramaite has had his period of appointment as the group CEO extended until 1 April 2026. He was initially appointed on 1 March 2022 for a two-year period.

Fortress Real Estate (JSE: FFB) announced that GCR Ratings has upgraded its national scale long-term issuer rating from AA-(ZA) to AA(ZA) and affirmed its national scale short-term issuer rating at A1+(ZA). The rating outlook is Stable. Property funds require significant levels of debt to generate decent equity returns, so this is important stuff.

Cashbuild (JSE: CSB) announced the appointment of Hanré Bester as the CFO of the group. He is currently the CFO of Pinnacle Micro.

Tectonic shifts in demographics will change the way we think about retirement planning. Structured products can play a key role in navigating these changes.

Global demographic shifts are increasingly under the spotlight and investment professionals and investors alike are having to think about what this means for their portfolios.

For a while the demographic shift of people living longer and having fewer children has been associated with Asian countries such as Japan, South Korea and China, as well as parts of Southern and Eastern Europe, but it’s becoming clear that most countries are going through this shift, including many emerging market countries.

Since the 1950s the global total fertility rate (the average number of babies born per woman) has fallen from 5 to about 2.3. This is close to what is known as the replacement rate of 2.1 (the fertility rate required for the population to remain stable over time) and many countries are well below that. According to United Nations data for 2023, Italy (1.3), Japan (1.3) and China (1.2) are well below the replacement rate, but emerging economies such as India (2), Bangladesh (1.9) and Iran (1.7) are also below the replacement rate (South Africa is at 2.3).

Many of the countries with the lowest fertility rates also have the highest median ages, based on Central Intelligence Agency (CIA) figures: Japan, Germany and Italy all feature in the top 10, though India (143rd), South Africa (144th) and Bangladesh (145th) still have young populations. It’s clear though that for most countries, median ages will continue to rise.

Reassessing the old models

As these trends deepen and societies continue to grow older, so the traditional models for pensions and other forms of contractual saving will need to be reassessed. Much of the industry is built on the idea of inflows coming from the incomes of younger workers, which then provides the base for the drawings by older retirees.

However as the proportion of younger, working-age investors and pension fund members falls, and the number of retirees grows (and live longer) so the ability of traditional retirement vehicles to support retirees diminishes.

Policymakers around the world are having to grapple with these problems and find solutions, including potentially raising the retirement age of workers.

At the same time, advisers and their clients will also need to re-examine their approach to questions about risk and asset allocation. Given longer lifespans, is it right to de-risk portfolios as investors approach retirement and immediately thereafter? And should investors look to keep a higher weighting in equities at a time when the textbooks tell them to increase their weighting in fixed income, cash and high dividend-paying equities?

Instinctively many investors will want to reduce equity exposure as they approach retirement, but this may not be the best approach if they have a longer life to look forward to in their retirement. Investors will need to look for ways to grow their capital.

Structured products: an investment for managing the demographic shift?

In this environment, structured products have a key role to play. In recent years, investors have been drawn to this particular alternative asset class as an excellent way to reduce volatility in their portfolios in the years just before and after retirement. This is an especially pertinent issue at the moment, with many of the world’s leading indices, including the S&P 500, Nasdaq, Nikkei 225 and Eurostoxx 600 hitting record highs. Structured products can be an excellent tool for hedging the risk of a market sell-off while also allowing participation in the upside.

However, structured products can also help investors negotiate the tectonic demographic shifts discussed above. By incorporating structured products into portfolios well into retirement, investors have a way of managing their risks while also continuing to participate in equity market gains in the future.

Of course, such will depend on the design of products and the underlying investments chosen as reference, as well as the liquidity needs of the investors over the term of each structure (remember structured products don’t pay dividends).

In conclusion, while demographic shifts look set to disrupt traditional retirement planning, structured products could play an increasingly important role in helping investors make the transition to the new retirement world.

Speak to your Financial Advisor for more on retirement planning

About the latest Investec Structured Product:

The Global Accelerator offers 140%* geared exposure to world equity markets in USD up to a maximum return of 56% over the term of approximately 5 years. 100% of investors’ initial capital is protected at maturity (subject to credit risk). Investec is the promoter of the Global Accelerator.

The board of Anglo American has unanimously rejected the proposal put forward by BHP. Apart from the structural complexities in the proposal that the board doesn’t like, the main reason is that they believe that the proposal undervalues Anglo American and its prospects.

The copper assets are the focus of course, with the chairman of the board commenting that shareholders still stand to benefit from the full impact of the investments in copper. I’m sure BHP would agree with that statement, behind closed doors at least, as why else do they want to acquire Anglo?

They also describe the BHP proposal as being opportunistic. I think just about every successful acquisition in history that creates shareholder value has been opportunistic, otherwise what’s the point?

Right now, there’s no firm offer on the table. At this stage, the board of Anglo recommends that shareholders take no action in relation to the proposal.

Here’s what it looks like when deals start being thrown around in the market:

The question is: will BHP put in a firm bid and on what terms? Or will another bidder with a taste for copper emerge?

Finbond: are they profitable? (JSE: FGL)

The trading statement has left more questions than answers

Finbond released a trading statement dealing with the year ended February 2024. It notes that HEPS will increase by at least 20% vs. the headline loss per share of 15.1 cents for the year ended February 2023. This isn’t as simple as it sounds.

Firstly, they refer to HEPS rather than a headline loss. Secondly, “at least 20%” is the minimum required disclosure under JSE rules, so the improvement could be vastly higher. Thirdly, they only made a loss per share of 2.3 cents in the interim period, so there’s a chance that they have swung into the green.

It’s frustrating when companies make things obscure. It really wouldn’t have taken much effort to release a clearer trading statement.

Impala Platinum commences a retrenchment process (JSE: IMP)

PGM prices just aren’t giving the sector any relief

Job losses in the mining sector are becoming a worrying trend, with PGM prices putting great pressure on local operations. This impacts jobs both at the mines and the corporate head office. As sad as this is, the decision taken by companies is always on the basis of rather cutting 3 jobs than shutting down a company and losing 10 jobs in the process.

The maths isn’t quite that severe in this case, with Impala Platinum looking to potentially reduce labour costs by 9% across Impala Rustenburg, Impala Bafokeng and Marula, along with a 30% reduction in costs at head office. In total, 3,900 positions could be affected.

Remember, this is the same company that got into a bidding war for Royal Bafokeng Platinum and won. Here we are with retrenchments just a short while later.

Invicta to combine KMP with Kian Ann (JSE: IVT)

The group is looking to strengthen its international holdings

Invicta holds KMP Holdings (a leading supplier of aftermarket heavy-duty diesel engine parts) through Invicta Global Holdings. KMP is based in the UK and US and services a global client base in over 150 countries. Invicta also has a 48.81% stake in Kian Ann Engineering based in Singapore.

Although this transaction means that Invicta is effectively diluting its interest in KMP, the group has taken the decision along with the other shareholders in Kian Ann that KMP would be better off within that entity, benefitting from the procurement and manufacturing network of Kian Ann.

To achieve this, Invicta Global Holdings will sell the shares in KMP Holdings to Kian Ann for roughly R300 million. Invicta originally paid around R270 million back in 2022. The uplift is almost entirely thanks to the rand though, as the base selling price now vs. the purchase price then is only different by around £200k.

KMP will also repay shareholder loans and claims of around R156 million to Invicta. Considering that KMP made net profit of around R31 million for the year to March 2023, it feels like Invicta is getting paid a strong multiple here, particularly for a business that hasn’t delivered exciting earnings growth in the past few years.

Hopefully, combining it with Kian Ann will change that.

Oasis Crescent: the property fund without debt (JSE: OAS)

As a Shariah-compliant fund, this is an unleveraged play on property

Oasis Crescent Property Fund is a fascinating thing. This is basically what you get when you strip leverage out of property returns entirely, as the fund cannot have any debt as a Shariah-compliant structure. Despite not using leverage, the fund proudly notes a unitholder return of 10.3% per annum since inception compared to inflation of 5.6%.

Sometimes, not having debt is actually pretty useful, even in property. Just ask executives of REITs in the past couple of years, particularly those with significant exposure to office property.

For the year ended March 2024, Oasis Crescent grew its distribution including non-permissible income by 12.9% to 112.2 cents per unit. Investors pay up for this thing, as that’s only an earnings yield of 5.4% based on the current share price. Remember, most investors in a Shariah-compliant structure can’t use many of the fixed income alternatives, like money market and other accounts.

The share price is flat over 5 years despite some volatility along the way.

Reinet enjoyed an uplift this quarter in the fund (JSE: RNI)

The fund numbers are a precursor to the listed group numbers

Between December 2023 and March 2024, Reinet fund saw its net asset value per share increase by 7.9% in euros. That’s a very strong quarter! The fund holds the investments in Pension Insurance Corporation and British American Tobacco amongst others.

This isn’t exactly the same thing as the group net asset value per share, but it’s always a good directional indication of how the listed NAV has performed in a given period.

Junior miners are generally loss-making for obvious reasons, but investors are getting impatient

Renergen is right on the cusp of becoming a producer of helium rather than a promiser of it. Getting across that line has proven to be really difficult though, with a few technical issues along the way that have irritated the market. This is why the share price has shed half its value over the past 3 years. It’s also way down from the peaks above R43 per share, currently trading at R12.50.

The bears in the market don’t need much to set them off when it comes to Renergen, with the latest trading statement adding fuel to the fire. The headline loss per share for the year ended February 2024 will be between 72.7 cents and 76.7 cents vs. a headline loss of 19.89 cents in the prior period. This deterioration is due to the downtime experienced during the maintenance cycle.

Sibanye wants to equity-settle its convertible bonds (JSE: SSW)

Currently, settlement would be in cash

In 2023, Sibanye-Stillwater placed $500 million in bonds due November 2028 with a coupon of 4.25%. The proceeds were used to fund the Reldan acquisition, with the remainder retained for general corporate purposes.

The bonds are currently cash-settled instruments, which is a drag on the Sibanye balance sheet. It significant reduces the flexibility of the company. To try and address this, shareholders are being asked to approve that the bonds can be converted into ordinary shares at a price of R24.5792 per Sibanye share. The current share price is R22.19. That might not sound like an issue right now, but remember these bonds will exist until 2028. By then, one would certainly hope that the share price has moved higher.

This is a material drag on the share price, as a conversion of all the bonds would represent 13.21% of shares in issue!

It sounds highly punitive, but remember that Sibanye raised debt at a lower rate than would otherwise have been the case without the conversion. This is a typical mezzanine funding structure. Such structures are more expensive than vanilla senior debt by design, which is why they are only used when senior debt isn’t a viable alternative.

Little Bites:

Director dealings:

A director of Sabvest Capital (JSE: SBP) has bought shares worth R1.7 million.

Aside from a trade related to share options that was included in the same announcement, a prescribed officer of Capitec (JSE: CPI) has bought shares worth R1.67 million.

Alphamin (JSE: APH) has declared a dividend of 41.78220 cents per share, payable on 24 May. The current share price is R15.89.

As Eastern European property fund MAS (JSE: MSP) continues to navigate a very difficult funding environment, the company announced that €40.2 million worth of notes have been issued in a private placement. They are due 2029 and carry a rate of 6.50%. They were issued as an exchange for existing notes due 2026 with a rate of 4.25%. The rate is higher obviously, as is to be expected in this environment, but at least the maturity is three years later.

It is no surprise whatsoever that Sasfin’s (JSE: SFN) disposal of the Capital Equipment Finance and Commercial Property Finance businesses to African Bank for a very lucrative price received almost unanimous approval from Sasfin shareholders.

A subsidiary of Sephaku Holdings (JSE: SEP) has repurchased a further 2.72% of its issued shares for R7.2 million. The average price paid was R1.04 and the current share price is R1.10.

Absa (JSE: ABG) announced that Deon Raju has been appointed as the Group Financial Director. He’s been at Absa since 1999 and his most recent role was Group Chief Risk Officer, held since June 2021.

Anglo American Platinum (JSE: AMS) has announced the appointment of Sayurie Naidoo as CFO of the group. She has been with Anglo American for over 15 years

Kibo Energy (JSE: KBO) remains stuck on R0.01 per share despite regular SENS announcements. The latest one is that the Pyebridge project has passed the requirements to retain the Capacity Market contract that makes gross margin of £308k per year. The site has secured further contracts to ensure minimum annual gross margin of £817k until 2028. The 2nd phase at Pyebridge is in preparation phase and will be funded by RiverFort under the new funding agreement. Based on the absolute lack of action in the Kibo share price, RiverFort seems to be getting the bulk of the economic benefits from Kibo’s subsidiary Mast Energy Developments.

Putprop (JSE: PPR) has proposed an odd-lot offer. This is a classic case of where it makes sense, as those holding fewer than 100 shares each make up a whopping 52% of the total number of shareholders in the company. They hold just 0.01% of shares in issue. This means that the compliance burden far outweighs the benefit of such a widely held register. The price will be a 5% premium to the 30-day VWAP as at 3 June 2024.

Due to elevated cost of living pressures, fashionistas around the globe are having to tighten their belts. Make no mistake – those belts are still designer. Consumers are just getting smarter at paying less for them.

As a fashion enthusiast on a budget, I never thought the day would come where I would be able to afford anything from the lauded house of Prada. And yet, this week, I made a personal dream come true when I bought myself a beautiful pair of Prada sunglasses. How is this possible on a writer’s earnings? The answer is simple: I got them secondhand.

Yes, thanks to a lot of patient searching and the miracle of the internet, I bought a pair of designer sunglasses for approximately 25% of the price that I would have paid in-store. They are in perfect condition and their authenticity has been verified. All I had to do was to wait for someone to pay the full price for them first, and then decide to sell them.

If this is your first introduction, then welcome to the wonderful world of secondhand luxury.

Macklemore and me

The year was 2012, and American hip-hop duo Macklemore and Ryan Lewis’s saxophone-driven earworm, “Thrift Shop” had just landed. As someone who had just discovered the magic of charity shops and flea markets, I felt that the song had been written for me. My thrifting habit, which had started as a way to access affordable clothing as a broke student, had quickly morphed into the understanding that I could get branded, better-quality clothing at cheaper prices than the new stuff at the mall, if only I was willing to dig for the gems inbetween rails of mediocre hand-me-downs.

Sure, sometimes I would come across an item of clothing that was stained, that smelled funny or that needed a bit of repair. But with a little bit of elbow grease and a lot of OMO, I found that I could restore practically any item of clothing to its former glory – and then revel in that glory knowing that I had paid peanuts for it.

I was not alone in this discovery, of course, and that’s part of the reason why “Thrift Shop” was such a hit. At its core, the song spoke to a generation of young consumers who were rejecting the notions of embarrassment and shame that were previously attached to secondhand clothing. Thrifting became cooler than ever before – a counterculture way of sticking it to big labels while looking fabulous and saving money, all at the same time. Secondhand marketplaces started popping up online, and Instagram pages dedicated to the resale of clothing became a dime a dozen. In no time at all, the thrift shop became a digital entity. Forget about e-commerce. This is recommerce.

In 2023, approximately one third of clothing and apparel items purchased in the US were secondhand. The global secondhand apparel market is currently worth $177 billion, up 28% from 2021. By 2027, the same global market is expected to grow to $350 billion.

That’s a lot of secondhand jeans.

It’s not all grunge though

It might surprise you to learn that of the global secondhand apparel market, about a third is made up of luxury goods. In 2023, Bain & Company estimated that approximately $49.3 billion worth of secondhand luxury goods were sold globally.

The emergence of online resellers like the RealReal and Vestiaire Collective has significantly enhanced accessibility to pre-owned designer items. Consequently, the resale market has expanded twofold over four years, now representing 12% of the value of the new luxury goods market.

In my example of the Prada sunglasses, I paid less for the item than I would in-store, which makes sense to me, because I know that I am buying something pre-owned. What surprised me in my research is that some luxury items can actually fetch a higher price secondhand than they would brand new. For example, certain Hermès items not only retain their value but can command a significant premium on the secondary market. In fact, the brand’s pre-owned handbags can fetch prices up to 25% higher than their original retail value. Likewise, pre-owned timepieces from Rolex and Patek Philippe often sell at average premiums of 20% and 39%, respectively.

A lot of this has to do with the limited release of luxury items. When Hermès only makes 500 of a certain scarf before discontinuing it forever, there is no option to buy a new one in the store. In a classic case of demand surpassing supply, resellers are then free to name their prices.

Most brands experience a decline in resale value, however. Over the past year, the secondhand value of products from Gucci, Balenciaga and Bottega Veneta has decreased by 10%, 14% and 23% respectively. When resold, handbags by Louis Vuitton typically lose an average of 40% of their original value, while Christian Dior’s bags nearly depreciate by half. As you can imagine, this is great news for consumers in the secondhand market.

Can luxury brands get a slice of this pie?

What’s more lucrative for a luxury brand than selling an item once? Selling it twice, of course!

A number of luxury brands have already woken up to the idea that their wares have a significant resale value, and are striving to insert themselves into the circular economy. Some do this by collaborating directly with the resale platforms – Burberry, for instance, has partnered with Vestiaire Collective, while Gucci has sided with The RealReal. Some have gone even further and established their own resale platforms. Rolex is a great example of this. Their certified pre-owned watch programme provides discerning customers with timepieces that have been authenticated and serviced by their own watchmakers, adding a layer of reassurance and trust that might just be enough to lure consumers away from private sales and back into the fold.

The trick to success in this game is volumes. While high-value, low-volume brands like Rolex and Hermès are capable of making a “second profit” off their items, clothing designers and handbag manufacturers are not so lucky. Because their volumes are higher, they would have to repurchase substantial quantities of pre-owned inventory for this approach to be successful in their own stores or on their own platforms, which causes all kinds of other problems for the vast manufacturing capacity they have built to produce new items.

It’s a generational thing

Earlier in this article, I mentioned that the rise in thrifting in the early 2010s was primarily driven by the fact that perpetually-broke Millennials were flocking to thrift stores instead of shopping malls. Now, we’re seeing how the next generation, Gen Z, is embracing secondhand shopping as a result of their strong focus on sustainability.

For better or worse, Gen Z is the generation that was raised with the ever-present threat of global warming and ecological decline in their peripheral vision. All that fear, combined with a healthy dose of greenwashing, has created a generation that has demonstrated a strong preference for sustainable brands, with some showing a willingness to pay as much as 10% morefor an item that they believe to be more sustainable.

Unsurprisingly, 75% of Gen Z consumers also prioritise sustainability over brand recognition when making clothing and apparel purchases. And what’s more sustainable than buying what already exists, instead of creating demand for new items, which require resources to produce? That explains why, according to eBay’s second annual Recommerce Report, a staggering 80% of Gen Z consumers are actively seeking out and purchasing pre-owned items.

I’m not the head of strategy at Prada (thankfully), but if I were, I would be paying particular attention to these statistics and considering what they mean for my brand in the long term. In a recent survey of affluent consumers, those under the age of 40 strongly agreed that buying secondhand was a sustainable choice, with just under half of participants in the same age group reporting that they are currently buying pre-owned luxury goods.

It’s not looking like a particularly bright future for luxury brands that can’t adapt to compete with their own secondhand wares. As for me – I’ll be smiling all summer long as I wear my favourite new sunglasses. And if I get tired of them, I can always just resell them.

About the author:

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

BHP looks to change the mining landscape (JSE: BHG | JSE: AGL)

Does Anglo American’s underperformance make it a sitting duck?

Get the corporate finance notebooks out for this “unsolicited, non-binding and highly conditional combination proposal” that BHP has made to Anglo American. This is the kind of deal that investment bankers dream of, with names like Goldman Sachs and Morgan Stanley on the announcement.

It’s worth saying right up-front that although BHP is listed on the JSE, the company actually wants nothing to do with South African mining risks. For this deal to go ahead, BHP would require Anglo American to unbundle its shares in Anglo American Platinum and Kumba Iron Ore to shareholders.

As Anglo is a UK-domiciled company, that takeover law will apply to this situation. This means that BHP has until 5pm on 22nd May to either announce a firm intention to make an offer, or announce that it doesn’t intend to make an offer.

It didn’t take BHP long to respond, with an announcement that was clearly ready to go. Just two hours later, BHP noted that this is an all-share offer based on the ratio of 0.7097 BHP shares for each ordinary share in Anglo American. Plus, each Anglo shareholder would get the shares in Amplats and Kumba in proportion to the effective interest in those companies.

They do the hard work for you in terms of the maths, showing that this is a premium to the market value of Anglo’s unlisted assets (i.e. excluding Amplats and Kumba) of 31%. It’s a premium of 78% based on the 90-day VWAP.

If this deal goes ahead, Anglo and BHP shareholders would be invested in a very large combined entity that has iron ore, metallurgical coal, potash and copper. BHP’s various global listings (including on the JSE) would be retained. BHP also notes that Anglo shareholders would be able to determine how much exposure they want to Amplats and Kumba, unlike the current situation where you can’t own Anglo’s copper and diamond assets without also getting exposure to the PGMs and iron ore.

Speaking of diamonds, BHP doesn’t sound very keen on De Beers. They note that it would be subject to a strategic review post completion. One wonders if we could see a separate listing of De Beers at some point.

Notably, there is still no firm intention to make an offer at this stage. There will need to be a due diligence process first.

Yet another solid period at Clicks (JSE: CLS)

The valuation is always a debate, but this is a quality company

Clicks is one of the most solid retailers you’ll find in South Africa. The health and beauty category is a particularly great place to play, with the pharmacy offering ensuring there is footfall in the stores, while the small appliances also play an important role for group sales and margin.

For the six months to 29 February 2024, Clicks group retail turnover by 12.4%. Wholesale wasn’t nearly as exciting (UPD has strategically stepped away from certain contracts that are less profitable), so group turnover growth came in at 9.0%. I must also point out that UPD had certain systems implementation considerations to manage at the distribution centre, but the platform is apparently now ready for growth.

Underpinning this growth is a footprint of 900 stores and 11 million Clicks ClubCard loyalty programme members. You may also recall that Clicks acquired Sorbet, with that business contributing solid franchise fees to the Clicks group.

Operating profit increased by 13.5% and operating margin expanded by 30 basis points to 8.5%, primarily due to the increased mix of retail vs. wholesale. Retail costs were up 14.8%, but 300 basis points was due to acquisitions and there was also a considerable contribution from new stores. Comparable retail costs grew 8.7%. Distribution costs were up 10.8% due to the systems implementation and associated employment costs.

By the time you reach the bottom of the income statement, diluted HEPS was up 13%. Share buybacks were a great help here, as headline earnings (total, not per share) increased 10.5%. Those buybacks are made possible by Clicks having such a cash generative business, with cash from operations of R1.1 billion vs. capital expenditure of R314 million. They are ramping up heavily for 2024, with planned capital investment of R920 million. Although Clicks highlights the risk of a return of load shedding, they are accelerating their store expansion plan to between 50 and 55 stores for the 2024 financial year.

On the working capital front, overall group net working capital days improved from 47 days to 44 days. Retail inventory days improved from 85 days to 82 days, but UPD increased from 48 days to 61 days due to an increase in stock ahead of the single exit price increase. In other words, this is strategic buying of stock.

There is an aggressive push underway by Clicks. They’ve invested in the wholesale business and they are planning a lot of new stores. This is going to hurt the grocery chains, as Clicks products are some of the juiciest margin categories in retail.

Coronation releases earnings for the March period (JSE: CML)

They really put in the minimum required effort with this disclosure

I find lazy disclosure on the market very frustrating. For example, Coronation notes that assets under management were R631 billion as at the end of March 2024. The announcement doesn’t give the comparable number a year ago, so you have to go digging for it. The March 2023 number was R623 billion. Perhaps growth of just 1.1% in 12 months is the reason they make you go digging.

Then, instead of reminding the market of the per share impact of the tax provision in the comparable period, they simply point out that earnings across all metrics will be vastly higher because of the base effect. How much work would it have been to just show the comparable number without the tax problem?

I went back into the old report and found that fund management earnings per share (their preferred metric) excluding the tax charge was 191.5 cents. For this period, it’s expected to be at least 175 cents. In other words, even with adjusting for the tax charge, the business is going backwards.

Standard Bank gives a quarterly update (JSE: SBK)

Currency movements led to flat headline earnings

Each quarter, Standard Bank has to disclose financial information to the Industrial and Commercial Bank of China to assist that entity with its reporting on its investment in Standard Bank. To ensure all shareholders have the same level of information, Standard Bank also releases a quarterly earnings update on SENS that includes some important commentary.

Earnings in the banking activities grew by mid-single digits for the first quarter of the period. Although credit impairment charges were higher as expected, there was solid growth in the lending activities in particular. Operating expenses were flat year-on-year, leading to margin expansion.

In the Insurance and Asset Management segment, earnings fell year-on-year due to losses linked to market movements.

Group headline earnings ended up flat year-on-year, with the good news story in banking offset by the insurance and asset management result as well as negative movements in average currencies relative to the rand.

The group remains committed to positive jaws this year (i.e. income growth ahead of expenses growth) and return on equity inside the target range of 17% to 20%.

Little Bites:

Director dealings:

Adding to the recent purchases in the company, another director of OUTsurance (JSE: OUT) has bought shares – this time to the value of R14.9 million.

A director of Italtile (JSE: ITE) has sold shares worth R112k.

In news that doesn’t come as a surprise if you’ve been following the recent corporate activity around MC Mining (JSE: MCZ), Nhlanhla Nene (yes, the ex-Minister of Finance) is stepping down as chairman of the company.

Following the joint announcement by Canal+ and MultiChoice which set out the terms of the mandatory offer, Canal+ has notified shareholders that it has, this week, acquired a further 3,374,668 MultiChoice shares in open/off market transactions. Canal+ now holds an aggregate of c.41.60% of the MultiChoice shares in issue. The shares were acquired at an average price per share of R116.57, below the mandatory offer price of R125.00 per share, for an aggregate R394,48 million.

RMB Holdings had declared a gross special dividend of 3,5 cents per share from proceeds of the Divercity Property share disposal. The special dividend will return R48,75 million to shareholders.

Coronation Fund Managers has repurchased 65,699 shares at R33.62 in terms of its Odd-lot offer to shareholders and 141,105 shares in terms of the specific offer. The repurchased shares will be cancelled and delisted. The total issued ordinary share capital of Coronation will be reduced to 249,592,298.

Marula Mining, which has investments in South Africa, Tanzania, Kenya and Zambia, took a secondary listing on A2X on April 25, 2024. The company has a primary listing on the Apex segment of the Aquis Stock Exchange Growth Market based in London. It is seeking to move its primary listing to the Main Market of the LSE and will also take a secondary listing on the Kenya Securities Exchange in late April/early May.

Ellies has applied to the JSE for the voluntary suspension of its shares. The company commenced with voluntary business rescue proceeding earlier this year, subsequently entering liquidation following the announcement by the business rescue practitioner that there was no reasonable prospect of the company being rescued. The suspension of trading is effective immediately.

A number of companies announced the repurchase of shares:

British American Tobacco has commenced its programme to buyback ordinary shares using the £1,57 billion net proceeds from its sale of ITC shares. The company will buy back £1,60 billion of its ordinary shares – £700 million in 2024 and the remaining £900 million in 2025. This week the company repurchased a further 840,000 shares at an average price of £23.33 per share for an aggregate £1,96 million.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 15 to 19 April 2024, a further 4,451,758 Prosus shares were repurchased for an aggregate €128,06 million and a further 331,645 Naspers shares for a total consideration of R1,07 billion.

Following market speculation, Anglo American (Anglo) has confirmed that on April 16, 2024, it received an unsolicited, non-binding and highly conditional combination proposal from BHP. The proposal comprises an all-share offer for Anglo American by BHP and would, according to Anglo American, be preceded by separate demergers by Anglo American of its entire shareholdings in Anglo American Platinum and Kumba Iron Ore to Anglo American shareholders. In addition, shareholders of Anglo would receive 0.7097 shares for each ordinary Anglo share. Based on closing market prices of 23 April 2024, the proposal represents a total value of c. £25.08 per Anglo ordinary share including £4.86 in Anglo Platinum shares and £3.40 in Kumba shares, valuing Anglo’s share capital at £31,1 billion. The two parts of the proposal would be inter-conditional. Anglo has a primary listing on the LSE and secondary listings on the JSE, BSE, NSE and the SIX Swiss Exchange. The combined entity would retain BHP’s global listings on the ASX, LSE, JSE and NYSE. Anglo is taking the proposal under advisement.

Trustco has advised that it will acquire a further 1,135 shares in Namibian entity Legal Sheild Holdings from Riskowitz Value Fund. Prior to the acquisition, Trustco holds an 80% shareholding in the investment entity which holds Trustco Insurance, Trustco Life and Trustco’s real estate portfolio. Trustco will issue 400 million new shares at R1.17 per share (Trustco’s share price is currently trading at R0.20 per share). The shares will be issued in two tranches – 200 million shares are due after the effective date and the second tranche 12 months after the issuance of the first.

On March 8, 2024, Mondi plc announced it would make an offer to acquire DS Smith. Having completed a due diligence and following the announcement on April 16, 2024, of a competing bid by International Paper Company, Mondi has decided that an all-share merger would not be in the best interests of its shareholders.

Unlisted Companies

Local cybersecurity distributor Maxtec Peripherals has been acquired by UK headquartered QBS Technology as part of that company’s expansion strategy within the META region. Maxtec provides a distribution platform for African Cybersecurity Channel Partners to provide Software, Hardware, Managed Services and Rental Financing across all verticals. For Maxtec, the deal will facilitate further expansion into new territories and sustain growth in existing regions.

TransPerfect, the world’s largest provider of language and AI solutions for global business has announced the acquisition of South Africa-based Content Lab, a provider of audiovisual localisation services for media and entertainment clients. Content Lab will be renamed TransPerfect Media South Africa. Financial terms were undisclosed.

Sintana Energy and Namibia’s Crown Energy have entered into a definitive agreement for the acquisition by Sintana of up to a 67% stake in Giraffe Energy Investments. Giraffe is the owner of a 33% interest in Petroleum Exploration License 79 which governs blocks 2815 and 2915. The agreement sees Sintana acquire an initial 49% for a cash consideration of US$2 million and retain an option to increase the stake to 67% anytime over the next five years for US$1 million.

Trident Energy has announced agreements with Chevron and TotalEnergies to acquire stakes in operational fields within the Republic of Congo. TotalEnergies EP Congo has agreed to acquire an additional 10% interest in the Moho license from Tident and sell its 53.5% stake in the Nkossa and Nsoko II licenses. Trident has also reached an agreement to acquire the entire issued share capital of Chevron Overseas (Congo) which holds a 31.5% non-operated working interest in the Moho-Bilondo, Nkossa, Nsoko II fields and 15.75% operated interest in the Lianzi field. Upon completion, Trident will hold an 85% working interest in the Nkossa and Nsoko II fields, a 15.75% working interest in the Lianzi field. Triden will also retain a 21.5% working interest in the Moho-Bilondo field.

Globeleq has completed the acquisition of a 48.3% equity stake in the 25 MWp Winnergy solar PV plant in Egypt from Enerray, Enerray Global Solar Opportunities and Desert Technologies. Financial terms were not disclosed.

AIM-listed Ariana Resources has entered into a conditional merger agreement to acquire 100% of Rockover Holdings, owner of the Dokwe Gold Project in Zimbabwe. Ariana currently holds circa 2.1% of Rockover. The all-share merger will see existing Ariana shareholders hold a 62.5% stake in the merged entity with existing Rockover shareholders holding the remaining 37.5%.

Egypt’s Bokra has raised US$4,6 million in a pre-seed round led by DisrupTech Ventures and SS Capital. The Cairo-based fintech is looking to become the first platform to offer goal-based investment and saving products through asset backed securities, thereby revolutionising wealth management in the MENA region.

Reuters announced that sources have indicated that International Resources Holding has offered to buy a majority stake in Vedanta Resource’s Zambian copper assets. The mining investment firm is reported to be looking to expand its Zambian mining business following the successful acquisition of a 51% stake in Mopani Copper Mines earlier this year.

Khawarizmi Ventures has led a US$1 million pre-seed investment in Egyptian HRtech, bluworks. Other investors included Camel Ventures, Acasia Ventures and various angel investors. The startup, founded in 2022, develops SaaS solutions to manage the lifecycle of blue-collar employees in industries such as retail, F&B, facility management, healthcare, education and construction.

Impact investor, Renew Capital has invested in Kenyan B2B platform Farm to Feed. The tech-enabled platform finds new uses for surplus and less-than-perfect produce. The size of the investment was not disclosed.

Egypt’s Waffarha has raised a seven-figure seed round led by Value Makers Studio. The fintech will use the funding to enhance existing technology, hire new talent and expand its footprint in Saudi Arabia.

Sahel Capital, through its Social Enterprise Fund for Agriculture in Africa fund, announced a US$600,000 term and working capital loan for Persea Oil & Orchards. The Kenyan avocado oil processor provides an off-take market for avocado farmers and produces cold-pressed organic extra virgin avocado and crude oil.

Merger regulation continued to feature prominently in many African jurisdictions in 2023, with many transactions requiring approval. Most were uncontentious, but there were some high-profile cases that encountered headwinds. Notably, the proposed acquisition by AkzoNobel of Kansai affected a number of African countries, and was reviewed by many competition regulators across the continent. The parties were direct competitors, and the deal was closely scrutinised over many months.

The transaction was approved in Nigeria, Tanzania Mozambique and Namibia, but it was prohibited in South Africa and Botswana. COMESA conditionally approved the deal in Malawi, Burundi, Kenya, Rwanda and Uganda, but prohibited it in Eswatini, Zambia and Zimbabwe. In South Africa, the decision to prohibit the transaction was taken on reconsideration by the Competition Tribunal, and handed down in November 2023. Because the parties again failed to obtain approval, AkzoNobel and Kansai have mutually agreed not to proceed with the merger.

PUBLIC INTEREST

South Africa continues to focus on public interest considerations in mergers, an aspect that has gained considerably in importance since legislative amendments aimed at promoting economic transformation, amongst other things, came into force in 2019. In October 2023, the South African Competition Commission issued a draft of amended public interest guidelines relating to merger control for comment, although, in practice, they have been applying these principles for some time. While employment issues have been in focus for some years, the competition authorities are now intent on ensuring that historical injustices are rectified.

In accordance with the amendments, when reviewing mergers, they now seek to ensure that small and medium-sized enterprises (SMEs) have an equitable opportunity to participate in the economy, and that mergers promote a greater spread of ownership; in particular, increasing the ownership stakes of historically disadvantaged persons (HDPs) and workers. Foreign to foreign transactions are also viewed through this lens, with a number of mergers being approved subject to conditions to achieve these outcomes.

South Africa is not alone in seeking public interest benefits pursuant to mergers. For example, in the Heineken / Distell merger (which was reviewed in a number of African countries), South Africa imposed public interest conditions, including the requirements to maximise procurement from SMEs and HDPs, and to put an employee share ownership scheme in place. Botswana required the parties to set up a distribution development programme to absorb a suitable Botswanan citizen-owned company into the merged entity’s supply chain. Namibia imposed a condition regarding retrenchments, as well as a condition encouraging local production.

PROHIBITED PRACTICES

A number of African countries were active in investigating prohibited practices. Kenya investigated cartels in the manufacturing and agriculture sector. Pursuant to the investigation, nine steel manufacturers were penalised for engaging in price fixing. Morocco investigated nine fuel companies for anti-competitive practices in the markets for the supply, storage and distribution of gasoline and diesel.

A settlement agreement was concluded, where the companies were required to pay a $180,000 fine. Namibia has recently launched an investigation into fishing vessel owners and operators for the alleged fixing of quota usage fees that are paid to fishing rights holders. An important case in South Africa is the forex bank cartel case, which has been ongoing for many years, though the substantive case is yet to be heard.

There have been numerous interlocutory skirmishes, most recently before the Competition Appeal Court (CAC) in November 2023, pursuant to which the CAC has dismissed the case against 14 banks – leaving only five banks still to face the music – although an appeal by the Commission cannot be ruled out. Kenya is also investigating banks for the fixing of foreign exchange trades.

DIGITAL MARKETS

Digital markets continue to be in the spotlight globally, and Africa is no exception. In late 2021, the regulators in Kenya, Nigeria, Egypt, Mauritius and South Africa began a discussion on the topic, and in 2023, this grouping expanded. Pursuant to a dialogue, these countries, as well as COMESA, The Gambia, Morocco and Zambia, agreed to set up a working group to collaborate on competition issues in digital markets, amongst others.

The working group is committed to expanding and deepening the dialogue on this topic amongst African competition authorities. The African Competition Forum undertook training on complex digital investigations, focusing on the characteristics of digital markets, amongst others. Mozambique is also looking into digital markets and has recently published a Decree that approves the Regulations on the Registration and Licensing of Intermediary Providers of Electronic Services and Digital Platforms Operators.

South Africa is particularly focused on this area. In 2023, the Competition Commission concluded its Online Intermediation Platforms Market Inquiry and published its findings and proposed remedial actions. Shortly thereafter, it launched a further market inquiry into Media and Digital Platforms, which is ongoing. After a first round of questions, the Commission recently issued a Further Statement of Issues, and will shortly begin public hearings.

Market inquiries are a popular tool in South Africa. In addition to the digital markets inquiries mentioned above, the Commission is currently conducting a market inquiry into Fresh Produce, and in April 2023, it issued draft terms of reference in relation to a Steel Market Inquiry. Other countries are starting to follow suit, and Seychelles is set to undertake a comprehensive market inquiry into the grocery retail sector.

COMPETITION LEGISLATION DEVELOPMENTS

Uganda has been considering competition legislation for a number of years and, in August 2023, the legislation was finally passed by the legislature. Although the bill envisaged that the Act be administered by an independent competition authority, President Museveni required that this be reconsidered. The Act was passed on the basis that administration fall under the relevant ministry, but on the understanding that there would, in future, be an amendment making provision for an independent competition authority to be established.

In February 2023, the African Union (AU) Heads of State formally adopted the Protocol to the Agreement establishing the African Continental Free Trade Area on Competition Policy (Competition Protocol) at the 36th Ordinary Session of the Assembly of Heads of State and Government of the AU. The Competition Protocol aims to create an integrated and unified continental competition regime which covers all aspects of competition law, including merger control, prohibited practices, and abuse of dominance. The Competition Protocol must still be ratified by 22 of the member states before it can enter into force.

CONCLUSION

It can be seen that competition law is alive and well in Africa, and constantly developing. Companies doing business in Africa will need to keep abreast of these developments to ensure that they stay on the right side of the various competition laws across the continent.

Lesley Morphet is a Partner and Nolukhanyo Mpisane a Candidate Attorney | Fasken (Johannesburg)

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")