In any commercial enterprise with multiple shareholders, disputes are bound to arise. Such disputes may result in the interests of some shareholders being unfairly prejudiced. Section 163 of the Companies Act 71 of 2008 (the Act) plays a critical role in safeguarding the interests of shareholders against such prejudice.

S163(1), otherwise known as the ‘oppression remedy’, states that:

‘A shareholder or a director of a company may apply to a court for relief if- a) any act or omission of the company, or a related person, has had a result that is oppressive or unfairly prejudicial to, or that unfairly disregards the interests of, the applicant;

b) any act or omission of the company, or a related person, has had a result that is oppressive or unfairly prejudicial to, or that unfairly disregards the interests of, the applicant;

c) the powers of a director or prescribed officer of the company, or a person related to the company, are being or have been exercised in a manner that is oppressive or unfairly prejudicial to, or that unfairly disregards the interests of, the applicant’.

Recent court judgments have highlighted several key issues, including locus standi, shareholder litigation, and the meaning of ‘prejudice’ in the context of s163.

Locus standi

It is often minority shareholders – prejudiced by the decisions of the majority – who approach the courts seeking relief in terms of s163. This often leads to the misconception that, in the case of shareholders, only minority shareholders have locus standi (the standing) to apply for relief in terms of s163. This is incorrect.

In the recent Van Der Watt v Schoeman and Others ruling, the court considered the applicability of s163 in instances where there is a deadlock in shareholder voting power.1 In this case, the two shareholders had equal voting rights, as each held 50% of the shares in the company. A dispute arose between them in respect of the management of the company, with one shareholder (the Applicant) accusing the other (the Respondent) of excluding her from the affairs of the company. The applicant approached the court for relief, claiming that her exclusion was oppressive and constituted unfairly prejudicial conduct.

The Respondent argued that the oppression remedy does not apply to a shareholder that is not an oppressed minority, and that as a holder of 50% of the voting rights, the Applicant had no standing to seek relief under s163. In rejecting this interpretation, the court considered the wording of s163, its purpose, and whether a deadlock between shareholders may satisfy the requirements of s163.

The court first examined whether s163 contains any wording that specifies what kind of shareholder may apply for relief. In this regard, the court held that there is nothing in the wording of s163 that suggests that the remedy is only limited to the prejudicial conduct of a majority shareholder, or that only minority shareholders may seek relief. All that is required of a shareholder to be entitled to ask for relief under s163 is to simply be a shareholder.

Secondly, the court examined the purpose of s163 and referred to Benjamin v Elysium Investments (Pty) Ltd, where it was held that:

‘It is a question of fact whether the affairs of a company are being conducted in a manner oppressive to some part of the members’.2

While the above remark was made in relation to the oppression remedy under the old Companies Act, it is clear that determining whether an act constitutes prejudicial conduct is an objective exercise that has little to do with the number of shares that a shareholder owns.

Thirdly, the court considered whether a deadlock can result in prejudicial conduct that satisfies the requirements of s163. The court found that if a deadlock unjustly impacts a shareholders’ ability to exercise an element of control in the company, then it constitutes prejudicial conduct that falls within s163.

It is evident from this judgment that the oppression remedy is not only available to minority shareholders. A shareholder prejudiced due to a deadlock in voting rights is just as entitled to relief. A majority shareholder may, of course, simply exercise their voting power to eliminate the prejudicial conduct.

In Briers and Another v Dr J Bruwer and Assoc no.78 Inc, the court had to determine locus standi where a shareholder had instituted legal proceedings for s163 relief, and then ceased to be a shareholder while the matter was still before the court.3 The court found that locus standi is established at the inception of the legal proceedings, and that an applicant is not stripped of that right by a subsequent buyback of their shares while the matter is still before the court.

The meaning of ‘prejudice’ in s163

To succeed with a claim for s163 relief, a shareholder must first prove that there is prejudicial conduct. The ruling in Edmunds and Another v Supreme Mouldings Investments (Pty) Ltd places emphasis on the meaning of ‘prejudice’.4

Two minority shareholders approached the court with allegations of prejudicial conduct and asked the court for an order directing that the company buy them out.

The dispute arose when the company, through the majority shareholder, entered into a guarantee and cession agreement in favour of a bank, standing good for the debts of two of its subsidiaries. This transaction, which amounted to financial assistance in terms of section 45 of the Act, was concluded without the minority shareholders’ participation and without passing the necessary resolutions. The effect was to create a contingent liability of R10m in the books of the company.

The minority shareholders argued that should the bank call upon the guarantee and cession, it would result in a diminution of their shareholding in the company. They claimed that this constituted conduct that is unfairly prejudicial.

In its ruling, the court emphasised the effect of the conduct, rather than whether the act itself was irregular. It is not enough that the applicants allege oppressive conduct; the conduct must have actually resulted in unfair prejudice. In the case of a guarantee that had not been called on by the bank, the shareholders were deemed to have failed to show any clear diminution in the value of their shares and, by extension, any discernible prejudicial effect. S163 relief was denied on the basis that no actual prejudice had resulted.

It is important for shareholders who seek relief under s163 to be mindful of the requirements that they must satisfy in order to be entitled to relief. The judgments also serve as a caution to companies and shareholders that, once a shareholder has instituted proceedings for s163 relief, a subsequent buyback of the aggrieved shareholder’s shares is not a shortcut to put an end to the matter.

1.(3393/2022) [2023] ZAECQBHC 61. 2.1960 (3) SA 467. 3.(19726/2023) [2024] ZAWCHC 76 (30 May 2024). 4.(2021/36175) [2023] ZAGPJHC 635 (5 June 2023).

David Hoffe is a Partner, Siyabonga Nyezi an Associate, and Ashishaa Kasipersad a Candidate Attorney | Fasken.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Attacq and Hyprop have completed their African deals (JSE: ATT | JSE: HYP)

Time will tell whether being in Africa via Lango Real Estate is a better outcome

Investing in a particular region through another structure or with a partner is mainly a capital allocation decision. Holding assets directly in that region is an operational decision as well as a capital allocation decision, as there is far more risk involved. As for the potential for additional reward, well, it’s not always there despite the higher risk.

Attacq and Hyprop have had enough of holding directly in the rest of Africa, hence why they did the deals to sell the direct exposure in Ghana and Nigeria and accept shares in Lango Real Estate instead. Both deals fulfilled their conditions precedent in the same week, so the story going forward will be one of hoping that the Lango structure turns out to be a better decision than holding properties directly.

It’s go-time for the Capital & Regional deal (JSE: CRP | JSE: GRT)

Growthpoint has thrown its weight behind the deal with NewRiver

At last, after many extensions to the deadline for a firm offer to be made, we have a deal on the table for Capital & Regional, Growthpoint’s listed subsidiary in the UK market.

NewRiver’s bid has found favour with Growthpoint, which means shareholders in Capital & Regional are on their way to receiving 31.25 pence per share in cash and 0.41946 NewRiver shares. This is effectively a premium of 21% to the “undisturbed closing price” of Capital & Regional before news of a potential deal broke.

It’s a fairly light premium because of the share-for-share element, which allows existing shareholders to cash out a portion of their exposure and roll the rest into the merged entity. Capital & Regional shareholders will have 21% in the enlarged entity. The combined group will have a coherent strategy focused on UK shopping centres with anchor tenants having a value-focused strategy and thus making them more defensive (e.g. affordable grocery stores).

Growthpoint will vote in favour of the deal, with an eventual holding of around 14% in the enlarged group if all goes ahead. Growthpoint will receive £50.7 million in cash as part of the deal, which should go a long way towards improving the balance sheet at the property juggernaut.

What worries me is that I couldn’t find any evidence of a commitment to NewRiver listing on the JSE in place of Capital & Regional. This is problematic for many Capital & Regional shareholders who can’t just roll their listed exposure on the JSE into listed exposure in the UK. The announcement notes that further details for South African shareholders will be in the scheme document.

A decent year for Choppies – but not on a per-share basis (JSE: CHP)

The rights issue in mid-2023 means there are many more shares in issue than before

For equity investors, it’s obviously really important to consider a company’s financial performance. It’s even more important to look at that performance on a per-share basis. It’s great having a delicious cake, but not if you only get a crumb or two vs. an entire slice. Similarly, a vast increase in the number of shares without a high enough jump in profits means that profits per share will deteriorate.

This is why the industry standard in South Africa is Headline Earnings Per Share, or HEPS.

The performance for the 12 months to June 2024 at Choppies is a perfect example of why this is so important. Profit for the period was up 9.3%, yet HEPS fell by a nasty 20.7%. The difference here is the number of shares in issue this year vs. the comparable period.

Another important element to the performance is the Kamoso acquisition, which played a major role in group revenue being up 31.7%. Without that acquisition, it would’ve been 12% higher. Excluding acquisitions and looking at performance on a like-for-like basis is important in understanding the true underlying performance.

Other important points to note are that gross profit margin and operating profit margin both deteriorated year-on-year, as you can see by comparing the modest growth in profit to the large increase in revenue. Net finance costs also played a role here, with the acquisition of Kamoso as a driver of higher finance costs.

The good news is that there’s a final dividend of 1.4 Thebe per share vs. nothing in the comparable period.

A far less shiny period for Gemfields (JSE: GML)

Revenue at core operations has dipped

Recent auction results at Gemfields haven’t been fantastic. Those results aren’t even in the numbers for the six months to June though, with a trading statement for that period reflecting a significant decrease in earnings before the recent auction pressures are even seen in the results.

For the six months to June, internal production challenges were a bigger issue than a decrease in market demand. HEPS is down by 21% as reported or 48% on an adjusted basis. The difference between HEPS and adjusted HEPS is the fair value loss on Sedibelo, the PGM asset that Gemfields has now written down to zero. That speaks volumes about the current sentiment towards the PGM sector.

Kagem Mining, the emeralds operation, achieved revenue of $51.9 million vs. $64.6 million in the comparable period. Montepuez Ruby Mining (self-explanatory) saw revenue decrease from $80.4 million to $68.7 million. Combined with inflationary cost pressures at both operations and increased finance costs, this is why earnings are down. It also didn’t help that luxury jewellery business Faberge saw revenue decrease from $8.4 million to $6.6 million.

This isn’t a happy start to the financial year, especially considering the recent dip in demand. All eyes will be on the remaining auctions this year, with management putting forward a cautiously optimistic tone around market conditions.

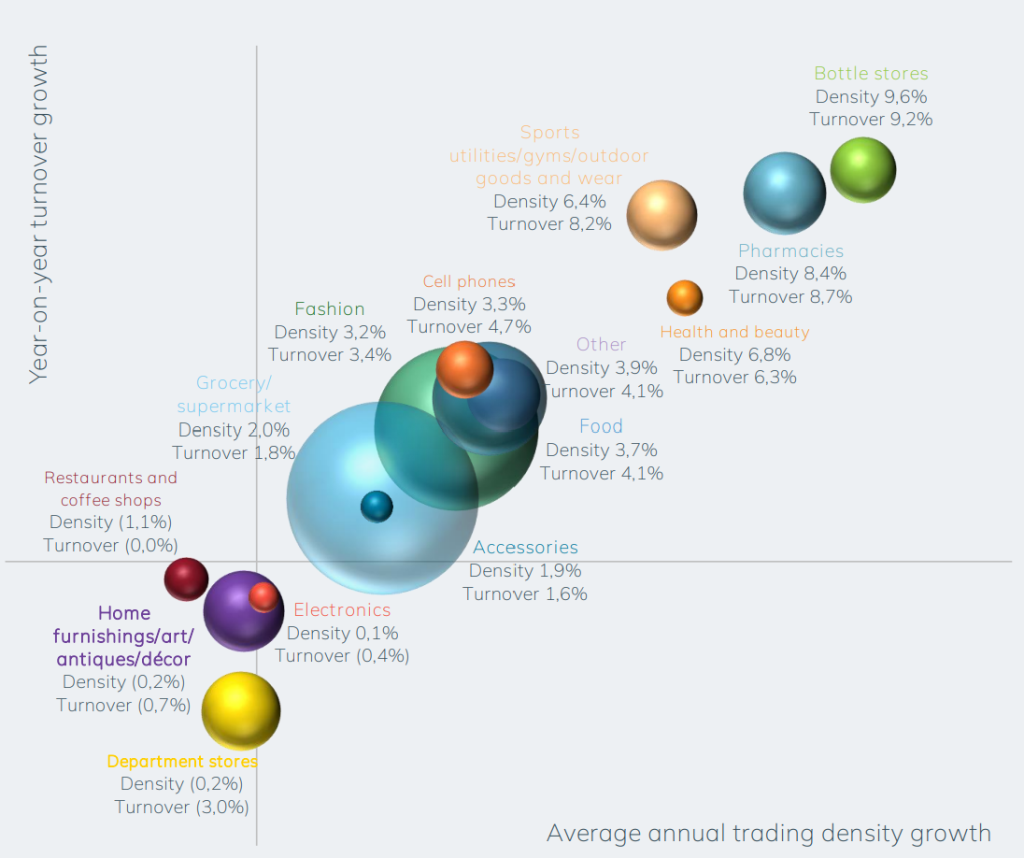

Vukile’s pre-close presentation for the interim period is a great read. You can find the full presentation here.

My favourite chart in the deck is from the South African portfolio review, showing the growth in turnover and trading density for major retail categories. Note how strong it looks for pharmacies and health and beauty in particular, with that combo making a strong case for what the current performance at the likes of Clicks and Dis-Chem must be:

It’s fun to compare this to where the growth is being experienced in the Spanish portfolio, with fashion and homeware as the largest categories but health and beauty once again coming through as the best source of growth:

The great thing about the markets is that you can learn something about retail by reading a presentation by a property fund!

Vukile is on a strong footing for the coming push into Portugal. After a very strong base period, growth in funds from operations per share is expected to be 2% to 4% for the full year and the dividend per share should be 4% to 6% higher. They will give a further update at the interim results.

Nibbles:

Director dealings:

An associate of the CEO of Sirius Real Estate (JSE: SRE) sold shares worth over R2.1 million.

A non-executive director of Anglo American (JSE: AGL) bought shares worth over R580k. Separately, three non-executive directors accepted shares worth over R710k in lieu of fees.

A director of Bell Equipment (JSE: BEL) and her spouse sold shares worth nearly R40k. A director of a subsidiary sold shares worth R200k and a different director sold shares worth R254k. Unlike the recent selling we’ve seen at Bell, these directors aren’t part of the Bell family.

A non-executive director of Metrofile (JSE: MFL) bought shares in the company worth R200k. This adds to some of the other recent buying we’ve seen from the CFO.

An associate of two directors of Astoria (JSE: ARA) entered into a CFD trade worth over R31k.

The minor children of the founder of WeBuyCars (JSE: WBC) have bought shares in the company worth R9.6k – gotta teach them young!

Orion Minerals (JSE: ORN) is paying the advisor on the recent capital raising project in shares rather than cash. Although the shares are being issued at quite a discount to the current market price, cash preservation is more important. The amount being settled is around A$10.6k.

MC Mining (JSE: MCZ) announced that the share options previously granted ex-CEO Godfrey Gomwe have now lapsed. There were 8 million share options, so that makes a difference to shareholder dilution.

Cilo Cybin (JSE: CCO), the recently listed special purpose acquisition company, is still in negotiations to acquire Cilo Cybin as its first “viable asset” – the technical term for the type of deal that a SPAC needs to do for the listing to become permanent.

The Trader’s Handbook is brought to you by IG Markets South Africa in collaboration with The Finance Ghost. This podcast series is designed to help you take your first step from investing into trading. Open a demo account at this link to start learning how the IG platform works.

In this episode of The Trader’s Handbook, The Finance Ghost and Shaun Murison dive deep into one of the most critical aspects of trading: risk management. Building on previous discussions around technical trading indicators, the hosts explore the concept of volatility and its significance in managing risk. They break down strategies like the use of stop losses, the impact of leverage, and the importance of position sizing.

Shaun shares valuable tips on how traders can protect their capital during high-risk situations using tools like guaranteed stop losses and trend lines.

Whether you’re a seasoned trader or new to the markets, this episode provides actionable insights to help you navigate market fluctuations and manage your exposure effectively.

Listen to the episode below and enjoy the full transcript for reference purposes:

Transcript:

The Finance Ghost: Welcome to episode seven of The Trader’s Handbook, my collaboration with IG Markets South Africa. it’s really good to have you here with us. In episode six, we gave you a pretty good taste of some of the technical trading indicators that are used by traders. Particular focus in that show was on moving averages and MACD, which has nothing to do with McDonald’s and everything to do with trying to help you do better in the markets. And Shaun, I think it was really fun to just start chatting through some trading indicators, so we’re going to do some of that today as well.

But we are also going to start out with a discussion on risk management. And that’s because these technical indicators, as great as they are – it’s quite an information download and it’s quite a lot to absorb when you’re listening to a podcast. And that’s why we include the charts in the show notes as well. So if you want to engage with the technical trading content as best you can, then make sure you’ve got the show notes open in front of you so you can actually look at the charts that are being referenced as Shaun walks us through that.

Certainly for the risk management stuff etc. you luckily don’t need any charts in front of you. You can sit back with whatever drink is in your hand. Shaun, you’ve got a coffee in your hand from what I saw there. Thank you for joining us and I look forward to doing this one with you.

Shaun Murison: Great, it’s good to be back.

The Finance Ghost: Risk management, that is pretty much key to the process, isn’t it? We know from the statistics that retail traders generally speaking have quite a tough time with risk management and only a relatively modest percentage of traders are really successful. A lot of that must surely come down to risk management. I think let’s start with just the absolute basics.

People hear market commentators, they read it in the media etc. about market volatility. That is ultimately the focus of risk management. I’ll hand over to you to just walk us through what volatility actually is at the end of the day, and then we can dive into more risk management topics.

Shaun Murison: Yeah, so I think just starting off, risk management is key in trading. I think everyone’s always concerned about when to buy and when to sell, the timing of the market. But if you commit too much money into the wrong trade, you’re going to get yourself into trouble.

So, you need to understand volatility. You need to manage that risk. You can have a strategy where you are right nine out of every ten times, but you could still be loss-making, because if you commit too much money to that one time that you’re wrong, you’re going to give away all your profits.

When we talk about volatility, essentially we’re talking about the range of price movements, whether historical or implied in the future. So if we talk about a share price, commodity price, FX price, whatever you’re trading, small price movements suggest low volatility. A large range of price movements between the high and the low is considered high volatility. When you’re looking at shares, for example, let’s say a share moves 3% in a day between the high and the low. It’s obviously more volatile than a share that moves, on average, about 1% over the course of the day. Higher volatility gives you a higher degree of risk, but also a high opportunity for reward, which still needs to be managed. In a highly volatile market environment, you might consider having smaller positions in the market. In a low volatile environment, you might consider having slightly bigger positions to try and magnify that reward.

The Finance Ghost: This is the old story, right, about how things don’t go up in a straight line. That’s exactly what volatility is. You look at a chart and you see all the little squiggles. Yes, there might be a broader trend, up or down or even sideways. Sideways is also a trend, but it’s not a straight line unless it’s an incredibly illiquid stock that never trades. You get those, but they’re not of any help to traders whatsoever. If you’re looking at a stock that actually has activity in it, you’re going to see lots of up and down moves, and that ultimately is volatility.

Volatility is not just about these black swan events that make it into the headlines, right? It’s not just the big moves, like -20% or -30% in a day because something crazy came out. Recently, we saw Barloworld close 12.5% lower on Friday the 13th – can’t make this stuff up. That was because they just went and released an announcement about some disclosure they’ve had to make around potential export control violations to Russia. This is stuff that’s really, really difficult to manage, these black swan events, and we’ll get to that shortly.

Volatility is more than that. It’s actually all the small moves as well. As you pointed out, it’s the extent of the moves both up and down. It’s how a share price moves over time within a trend. Just back to those black swan events, I’m not sure that Barloworld’s announcement is quite a black swan. I think 12.5% down is a big “owie” as my little guy would say, but it’s not quite a black swan.

As you pointed out before, though, IG does have a guaranteed stop loss for those sort of scenarios. We’ve talked about stop losses before, which are a way to manage your downside risk – basically stem the bleeding at a point in time on the chart. But if a stock really gaps down, and that means that bids just disappear in the market and the only bid is a long way down and someone is willing to sell down there and the stock gaps lower, that can go right past your stop loss, as I understand it, unless you have taken out this guaranteed stop loss. I just want to confirm with you that that understanding is correct. Just practically on the platform, when you’re executing a trade, how do you do this guaranteed stop loss? Is it available on every stock or every index or every asset on the platform? How does it actually work?

Shaun Murison: Just going back to stop losses, for new listeners, a stop loss is obviously just an order to exit the market if it moves unfavourably against you. With a normal stop loss, like you correctly said, sometimes we’ll wake up and the market might just open lower and past our stop loss. If you had bought and you’re looking to sell to somebody, there’s no one to sell to, but your order in the system would be to get me out if it gets to this price or below.

What can happen in that situation is you actually end up losing slightly more than what you expected to lose. We refer to that as slippage. Now, slippage can work in your favour when you’re placing orders as well, but in that scenario, you’d lose slightly more than what you expected. A guaranteed stop loss is a function that IG does offer to say, well, if it does get to this price, even if it gets lower, we honour that price and we’ll get you out of that price. So, very simply, you can just add that to your trade. When you’re placing a trade on the IG mobile app or on the platform, you just choose what type of stop you like.

Now, if you use a guaranteed stop, there is a slight premium associated with that, obviously, because now we’re taking on that risk for you to try stop you from getting that slippage. But it’s a really, really cool feature. It means that you can rest assured that this is how much, in a worst case scenario, if the trade’s going to go against me, how much I’m going to lose, and there will be no surprises on that front.

The Finance Ghost: And in terms of the availability of that guaranteed stop loss, is it available on everything?

Shaun Murison: Yes. Yeah. It’s available across all the different asset classes.

The Finance Ghost: Okay. And that’s on the platform. When you’re putting your normal stop loss in, you have that option on the platform?

Shaun Murison: Yes, when you place the trade, you have an option of three types of stops. There’s a normal stop loss, which we’ve discussed, and I just don’t want to say you’re always going to get slippage. I think if the market’s illiquid or if you’re trading shares, you’re more likely to get slippage because of gap risk. The markets close and open, but some of the continuous markets like forex indices, you’re less likely to get slippage because they are trading pretty much 24 hours with IG.

The Finance Ghost: Yeah. Part of what we’ve discussed in stop losses previously, and I would encourage our listeners to work back through the content, was looking at stuff like the typical range that a stock will trade in, or an asset or an index or forex or whatever the case may be, and using that to inform your stop loss decision, because it doesn’t help to put your stop loss at a point where there might be your typical daily volatility and then you basically just locked in a day’s loss for no real reason, no real benefit. It’s there for risk management, not making sure you lost money on a slightly bad day.

Shaun Murison: Can I just add in there a very, very cool technical analysis indicator? It’s very easy to use.

It’s called average true range. You add that indicator to your chart, it’s going to give you that information. It’s going to show you, on average, how much that particular share or that index or that FX price moves over the course of a day, an hour. All you have to do is just add that indicator to your chart. You look at the value, and then you can really have an expectation of what is a probable move.

We can’t always tell the future. We don’t know when you’re going to have those black swans or an outsized moves in the market, but you look for what’s probable. And that indicator, average two range, abbreviated to ATR, is something I’d encourage anyone new to technical analysis and charting to just add to a chart and take a look at because it will give you an expectation of how much that market moves on a normal day. If you apply it to a daily chart, over an hour, if you apply to an hourly chart, five minutes.

The Finance Ghost: Yeah, and there was actually a great piece on that in Ghost Mail this past week. What I’ll do is I’ll include that link in the show notes, and I recommend listeners go check it out. That IG Markets Academy is just a wealth of knowledge. And obviously there, first you get to look at Shaun’s very professional photo at the top of the article. But once you make your way past that, you’ll also find some really useful charts. It’s a great read that I highly recommend.

I think let’s talk about leverage, Shaun, because that is really the reason why volatility is so important to traders, even more than investors. And what I mean by that is, for me, for example, coming from an investor background, if I’m just sitting on a stock or an ETF or whatever it is I’m invested in, if it has a really bad day and it’s down 10%, I’m not forced to sell. I’m not sitting there with a leveraged position. I can just hang on to it. I might want to sell if I think it’s going to go much lower. Or I can ride it out and say, actually it looks like it was overcooked.

In fact, if I have a relatively modest position, and I think it was a silly move, then I can jump in and take the opportunity. It happened earlier this year when Cashbuild dished out this absolute gift. There must have been a big seller in the markets, as there was no reason why the share price behaved the way it did. I said thank you very much, and jumped in, and it worked beautifully. But it is less risky when there’s no leverage.

With trading CFDs, there is leverage, and obviously that adds to the risk. It also adds to the potential return. That’s the golden rule of finance. You can’t get the bigger return without taking a little bit more risk. In a risk management show, we need to to at least do a quick recap on leverage. It’s something we have talked about before, so let’s not spend a lot of time on it. I think just a quick recap on how the leverage works in CFDs and then why that is so important in the context of volatility?

Shaun Murison: I think leverage essentially magnifies moves in the market because you’re putting a deposit down for your trade. If you wanted R100,000 worth of shares, you might be asked to put a R10,000 deposit. Your profits or losses are magnified by ten times. It actually enhances that volatility. And the reason you use that magnification is to help you get in and out of the market quickly, because trading is seen as short-term. A 1% move essentially works out to a 10% move if you’re looking at ten times leverage or ten times gearing, so you don’t have to be in the market as long.

You could also use the analogy of putting down a 10% deposit on a property, let’s say a R1,000,000 property and putting down R100,000. The capital gains come from that R1,000,000 property, not from the deposit. That’s essentially how you could look at short-term trading and leverage, because essentially, when you’re buying a house, you are leveraging yourself.

The Finance Ghost: Likewise, if that property goes down 10%, you effectively lost your whole deposit. That’s exactly the point, because the layer of equity in this thing is quite thin. It’s like what happens in a private equity investment. You typically have a lot of debt and a relatively modest layer of equity. If it does well, you shoot the lights out in terms of return on what money you actually put in. But if it does badly, you can effectively wipe out the layer of equity and this leads me directly into my next question. Let’s say you put down R1,000 on a R10,000 position for easy numbers. If it drops 10%, the asset that you invested in has effectively lost your entire R1,000. I understand that. But what happens if it drops 15% and you weren’t sitting with any kind of stop loss? Is there an automatic system on the platform that basically gets you out of the trade before you lose more than your deposit? Or can you actually lose more on that one specific trade than your original deposit, before dipping into the rest of your balance sitting with IG?

Shaun Murison: That’s a very good question, because you always see the headlines, when you talk about derivative trading, CFD training, you can lose more than your deposits, but the answer to that is both yes and no, right? If you’re trading with IG, different brokers might have different models on that, but you are always in your account required to have the deposit or your margin for the trade you have open and any loss that you may be incurring.

So, if you don’t have enough money to cover the deposit in your trade, and because you’re incurring a loss and you don’t have sufficient funds in your account, then we do have an automated system which can close you out of that trade, which should stop you from losing more money – in the negative situation, more than your initial deposit. We talked about things like gap risk and market dislocations, sudden movements, you know, Barloworld 12% lower and things like that, in which situation you’d still get closed out of the trade, but you would lose more than your initial deposit. The good news is, there’s a way of ensuring that you don’t lose more than your initial deposit. And that’s by using what we referred to earlier on as a guaranteed stop loss. Because there, you are guaranteed to get out where your stop loss level is. You will not lose more than your initial deposit for that trade. That’s why I said the answer is yes and no. If you are using things like guaranteed stop loss, then, no, you cannot lose more than your initial deposit on a trade.

The Finance Ghost: Thanks, Shaun. That’s super helpful. I think let’s move on now to another angle to risk that isn’t as commonly considered or talked about, which is an order not filling to the level that you actually wanted it to. Now, I would imagine in something like a pairs trade, which we discussed a couple of shows ago – go back and check that out if you missed it – that can be quite an issue because you suddenly sit with a very different mix of exposure to what you expected.

Let’s say you expected to be long a thousand shares of one thing and short 500 shares of the other. And because of the different prices, you end up with the exact long-short mix you were looking for. If one of those trades doesn’t fill completely, you know, let’s say instead of shorting 500, you could only short 300, or instead of only long 1000, you could only get 800 shares, then suddenly the trade is not actually what you thought it was going to be. Let’s talk through that as a source of risk. Why do trades sometimes not fill? How does this work in practice and what can traders do about it?

Shaun Murison: Look, when you buy, you’ve got to buy from somebody, and when you’re selling, you’ve got to sell to somebody. Maybe the volume or the number of shares you want to buy or sell is not the matching volume on the other side. So that is a risk, that you can’t get the volume of the order that you’re looking for. You might get a partial fill, things like that, but there is an easy way of remedying it if you are trading on the IG platform. You activate the direct market access function, the DMA function, or what we call level one or level two access, and then you can actually see what volume is available on the platform, in the market, in the underlying market before you place your trade. That’s just one way of mitigating that risk.

The Finance Ghost: Yeah. And I mean, there’s not much you can do about it, right? If, as you say, there isn’t someone to sell to or buy from, this market can’t just be made out of thin air. That’s more of an issue on the illiquid stocks, which I guess is part of why you don’t offer every single stock on the platform, because liquidity can be an issue.

Shaun Murison: Exactly. That’s 100% right. It might be an attractive stock, but if no one’s really trading it, then you might get in, but you struggle to get back out of that particular company.

The Finance Ghost: Yeah, absolutely. Look, I think we’ve now dealt with a few things around risk, and there’s really only one more that I want to cover before we have a brief conversation on a couple of technical concepts. That is position sizing, as well as any other risk management tools that you think might be worth discussing.

Let’s do that. Why is position sizing so important as a risk management tool? And do you think there are any others that we maybe should have spoken about on the show that we haven’t touched on?

Shaun Murison: Like I said earlier on about the position sizing, committing too much money to the trade where you’re wrong can wipe out all the profits from the trades where you’re right. That is one of the things that we do see. Bad habits in trading include overtrading and trading too big.

There’s a very simple formula there to help with that position sizing. A stop loss manages the risk on your trade, but you need to decide what your total risk is. How much money are you prepared to commit to any one trade? Is it 1% or 5% low risk relative to high risk?

In that formula I like to give, when you’re looking at shares, you take that total risk and you put it into monetary value, and then you divide that by your risk per share or your stop loss distance, and then that’ll give you a number of how many shares you should trade. So total risk divided by your stop loss distance will give you the number of shares you can trade. Very simple formula. And that should help you with your position sizing, managing your risk within the market.

You asked about other ways of managing risk. Well, we did talk in one of the previous episodes about peer trading, hedging out risks or market-neutral positioning. Another one that I think is often overlooked is don’t overtrade, you don’t always have to be in the market. Sometimes sitting on your hands is actually a trade. Being patient and waiting for opportunity is a way of mitigating risk. It’s okay to miss out rather than lose out sometimes. There are always opportunities arriving in the markets. Just waiting for the best ones, I think, is quite prudent and is a form of risk management.

The Finance Ghost: Yeah. Fantastic. Let’s do today’s little technical section because we have a few minutes left and there’s some good stuff to talk through. Today we’re going to look at trend lines. So that includes trend lines, support lines, resistance lines, all very interesting things. I’ll just let you run through all of them in one shot. What’s nice with these is I think support and resistance lines are something I’ve used with relative success in some of my investing, because it really is one of the easiest things, in my opinion, to see on a chart. If you’ve ever looked at a share price and you’ve wondered why did it move, I don’t know, 6% and not 8%, then you zoom out a bit and you have a look that it stopped at a level that it’s been at before, either up or down. And you see those support and resistance lines, it’s amazing how visible they are on a chart. That for me was the sort of entry point into technical analysis and believing that actually there’s a lot of value in this stuff because support and resistance lines do work.

Shaun Murison: So, yeah, starting off with trend lines. We have talked about moving averages. Moving averages are essentially an automated or dynamic trend line. But a trend line is just drawing a line along the lows, the price. If they’re going higher, it gives you an idea of market direction. We know they’re in an uptrend. Draw it along the top, so the market’s falling, linking lower highs. You can see the market is in the downtrend. A lot of what we do is trying to align our trades in technical analysis with the general trend of a market.

Trend lines are another way of just helping assess general market direction. You can use those for support and resistance, but I think what you’re referring to and what is my preference as well, the most important indicator to me is just a simple horizontal line on that chart.

And that horizontal line marking major turning points in the market, major lows, we call it support when you draw it underneath because it looks like it’s holding up the price and making turning points. We put lines above the tops of that. It looks like a bit of a ceiling because it looks like it’s stopping the price from moving higher. We can sort of get an idea of where buying has come into the market, where selling has come into market, and buying support is an area where buying has come back into the market.

Resistance is an area where selling has entered the market. So that gives us an idea of price expectation. Resistance gives us upside targets if the price is going up. Support gives us a downside target if the price is going down. And if it’s acted as support in the past, we can see that may be a buying opportunity or area where we could look at accumulating that particular share or company or whatever asset class you’re trading.

The Finance Ghost: I think it’s an important risk management tool. It’s not just about what the opportunity is in front of you, but if something has fallen from a resistance line all the way to a support line, and that’s your moment where you decide, okay, I’ll short this thing. You’re not playing the charts at all. You’re literally going short at exactly the point where a bunch of people say, hang on, I’m going to buy this thing now. And as you said from the very beginning, the market is really just this great big voting machine. It doesn’t actually matter whether something is fairly valued or not. It matters how people perceive it and what they are willing to do. And if enough people believe, hey, this is a support line I’m going to buy here, and that’s the exact moment at which you go short, you’re not managing your risk and you’re probably going to have a bad time (on average).

Shaun Murison: One of our earlier mentors said markets always move to where the orders are. And, you know, the support levels often show us where those orders are. Just something I’ve always kept in mind. I believe in support because the price, the balance between buying and selling pressure has changed. In future, we don’t know what’s going to happen, but we’re looking at the probability of what’s happened in the past. And so that to me is where orders are in a place where I can get involved in that market as well.

The Finance Ghost: Yeah. Fantastic. I think this has been a really, really good discussion as usual. We’ve touched on some technical stuff. We’ve touched on some other stuff. I would certainly encourage our listeners to go and check out the other shows in this series. This is now episode seven. There are six other great shows to go listen to, and there will be several more as well. As always, you’re very welcome to let us know what you would like us to cover. You can contact either one of us through the various social media channels or, you know, use the contact form on the Ghost Mail website, for example, or comment on the podcast. We’ll see it wherever you try and put it.

We look forward to doing this again next time, Shaun, and giving more insights. Thank you very much and see you for episode eight.

Investors worldwide are grappling with high investment fees. For example, 34% of global investors surveyed in a recent bfinance Investors’ Costs and Fees poll say their fund servicing costs have increased in the past three years. Yusuf Wadee, Head of Exchange-Traded Products at Satrix*, shares insights on these fee trends and how index-tracking investment product providers balance cost-effectiveness and returns in this high-fee landscape:

“The industry is observing pressure on fees across all asset management sectors. However, index-tracking investment product providers balance cost-effectiveness with consistent performance to provide efficient, accessible, and value-driven index-tracking solutions that stand the test of time. This balance can help investors harness the full power of compounding returns while minimising the erosive effects of high fees.”

Yusuf Wadee

The Widespread Phenomenon of Global Fee Pressures

Ever-reducing asset management fees have become a global phenomenon affecting active management and rules-based investment strategies. Wadee notes, “The fee pressures are playing out almost everywhere in the industry. However, the driving forces behind this trend differ across investment disciplines.”

He says in the active management space, the trend of investment outflows has persisted. This exodus has intensified the downward pressure on fees in this market, particularly given the traditionally higher fee base associated with active management.

Conversely, the indexation space, which includes rules-based strategies, has experienced consistent inflows into our markets. “Here, the fee pressures among competing product providers are more related to players trying to capture more of the market and new inflows via aggressive fee positioning,” he explains.

The Compounding Effect of Fees on Returns

Understanding the long-term impact of fees is crucial for investors. Wadee draws a compelling parallel between the power of compounding returns and the eroding effect of compounded fees.

“Much has been written on the power of compounding. The fact that a simple (but consistent) investment strategy, involving investing early in the market and staying invested, yields profound results after many years is powerful. This is due to the effect of compounding – simply put, you get growth on your growth.”

However, he adds that this same principle works in reverse concerning fees. “The eroding effect of high fees works similarly – but in the opposite direction. The long-term impact of high fees consistently levied year after year on investment portfolios over time is also driven by the same compounding force – the only difference is that the compounding force of higher fees acts in the opposite direction to the compounding of being invested in the market.

Wadee says even minor differences in annual fees can significantly affect wealth accumulation over time.

Balancing Cost Reduction and Performance

In response to fee pressures, Wadee says Satrix has had the benefit of having the first mover advantage in the South African indexation market. As such Satrix has been able to reach, very early on, a significant scale of assets needed to effectively operate an indexation business in what is a very competitive market. “Past a certain scale, indexation firms can extract economies of scale and efficiency benefits that allow us to ensure performance and quality for our investment strategies despite market fee pressures.”

The Case for Index Tracking in a Challenging Investment Landscape

Wadee says index tracking offers significant value to investors in the evolving investment landscape, particularly in the current high-fee environment. For instance, Satrix research shows that in South Africa, almost 90% of active manager returns result from market performance, which they can track using simple, low-cost index tracker funds.

“This raises an important cost-benefit question for investors – how differentiated, consistent, and successful are actively managed funds’ returns versus how much investors are paying in fees to achieve those returns? The higher costs of active management compared to index tracking means that the median performing active fund almost always underperforms an index tracking fund on a net of fees basis.”

Minimising the Effects of Compounding Costs

Wadee emphasises that the impact of fees is less pronounced in index tracking than in active management, particularly over the long term. “The effect of higher costs compounds over the medium to long term and creates a significant headwind for active managers and investors to overcome. In contrast, index tracking’s lower fee structure allows investors to benefit more fully from market returns, minimising the erosive effect of fees on long-term wealth accumulation.”

He says for investors, the message is clear – while low fees are essential, they should consider them in the context of overall value, performance, and alignment with investment goals. “In an environment where every basis point counts, index-tracking investment product providers must strive to optimise their offerings and ensure investors can harness the full power of compounding returns, minimising the erosive effects of fees, and maximise long-term wealth creation potential,” concludes Wadee.

*Satrix is a division of Sanlam Investment Management

Disclaimer

Satrix Investments (Pty) Ltd is an approved FSP in terms of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. Satrix Managers (RF) (Pty) Ltd (Satrix) is a registered and approved Manager in Collective Investment Schemes in Securities.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSPs, their shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Grand Parade’s HEPS is vastly higher, but don’t get excited (JSE: GPL)

The jump is for non-recurring reasons

Grand Parade Investments has released results for the year ended June 2024. HEPS is up by more than sevenfold from 2.56 cents in the prior period to 19.20 cents in this period. And no, this isn’t because the underlying investments are suddenly shooting the lights out.

In fact, profit from equity-accounted investments actually decreased from R121 million to R114 million. Aside from a couple of other line items, the real reason for the improvement in HEPS can be found in operating expenses which decreased from R102 million to R58 million. This is due to the costs of the substantial restructuring transactions in the base period.

The current level of profitability is probably a reasonable approximation of where the group will be going forward. The year-on-year percentage move certainly is not.

Hyprop is a step closer to saying goodbye to the problematic African portfolio (JSE: HYP)

One deal has become unconditional and the other is hopefully nearly there

In early August, Hyprop announced that it was finally getting out of the portfolio in Nigeria and Ghana that had caused many headaches. The disposals of the portfolios in each country were structured as separate deals.

The deal to dispose of the properties in Ghana has become unconditional, so that’s one down at least. The Nigeria deal is in the process of fulfilling its conditions precedent.

Jubilee Metals has secured stable power in Zambia (JSE: JBL)

This is key to the copper strategy

Jubilee Metals’ Zambian copper strategy has an initial processing capacity target of 25,000 tonnes of copper per year. There are two sites to help them get there: the Sable Refinery and the Roan Concentrator. To meet the target, they will have open-pit mining operations and reprocessing of surface waste.

A stable power supply (or lack thereof) has been a significant challenge. Thanks to a recently signed agreement with Lunsemfwa Hydro Power Company, they have been enjoying uninterrupted power for the past week and this will continue into the future with 100% renewable power.

In other important news, the Roan front-end module has achieved its design capacity and the Roan operational team is now running it day-to-day. Munkoyo open-pit operations have been ramping up, with the higher grade ore to be delivered to the Sable Refinery and the rest stockpiled for further processing. And finally, their large waste rock project is set to begin a commercial trial in November this year thanks to Roan’s front-end module.

Jubilee has a very exciting copper strategy and now has the power to implement it, literally.

NEPI Rockcastle looks to tap the bond market (JSE: NRP)

Here’s a good reminder that there’s more to a balance sheet than equity

It’s easy to forget that companies use public markets to raise debt as well as equity. NEPI Rockcastle (JSE: NRP) has delivered a great reminder of that fact, with a plan to raise EUR 500 million under the existing EUR 4 billion medium-term note programme.

Essentially the way this works is that companies go through the pain (and expense) of setting up an umbrella debt programme with a set of rules that the market comes to understand. When they actually need the money, they then raise debt under the programme based on the terms that were already assessed by the market. For the JSE and other public markets worldwide, the debt market is an important part of their business. For corporates, it’s a vital way to spread funding risks and be less reliant on banks.

To add further intrigue to this debt offering, this is a green bond structure, so the money will be used for projects that meet the eligibility requirements based on the green finance framework adopted by the company.

Overall, this is a great example of how the largest funds can really take advantage of the best that debt markets have to offer. The ultimate winner in that is equity holders, as a cheaper cost of debt means more profits for equity investors.

South32 got an important grant from the US government (JSE: S32)

It always helps when the government helps you pay for things

South32 announced that the Hermosa project in Arizona in the US has been selected for a $166 million award from the US Department of Energy (DOE). Hermosa’s project offers the only clear pathway to produce battery-grade manganese from locally sourced ore for the North American electric vehicle battery market.

Energy is always a matter of national importance, so you can understand why the government wants to push things along there. The intention is for the grant to support the development of a commercial-scale manganese production facility, with the DOE providing 30% of the cost of the facility up to a maximum of $166 million.

This means that South32 is still on the hook for the bulk of the cost, as it should be, so they will need to get themselves comfortable with the business case. They are engaging with potential customers and looking for supply opportunities.

In the meantime, they are busy with certain construction projects at the facility, supported by a $20 million grant from the Defense Production Act Investment Program. If you can get the government to help de-risk your project, why not?

And in news from the Taylor zinc-lead-silver project, construction there is progressing as planned. The intention is for this project to have shared infrastructure with the Clark project at Hermosa, which is the subject of the US government support.

Signs of life at Trellidor (JSE: TRL)

Investors will treat this one with caution

Trellidor has been a source of pain for many investors, with the share price having roughly halved in value over 5 years. It’s been a rollercoaster ride of note along the way, with people initially taking the “stay home and stay safe” trend very literally in the pandemic. Those were good times, with the share price trading at around R3.50.

Subsequent labour and supply chain challenges along with demand issues took the share price below R1.20 in early 2024. It closed at R2.06 on Monday, so you can forgive shareholders for having whiplash from this volatility.

In early September, an initial trading statement indicated that HEPS would be at least 22.4 cents, a much better outcome than 4.20 cents in the prior period. The even better news is the updated trading statement, which gives a range for HEPS of between 35.68 cents and 36.52 cents.

Thanks to all the pain previously suffered, investors will take a while to really believe in Trellidor again. The midpoint of the guided range is a Price/Earnings multiple of around 5.7x at current levels.

Texton is still trading at a huge discount to NAV (JSE: TEX)

Share buybacks are the only option here– but the board has other priorities

Texton’s net asset value (NAV) per share is R6.25 and the share price is R3.40. Even if you knew nothing else about the company, your head should already be spinning with thoughts of how share buybacks could make a difference here. If the directors really believe in the NAV, they should be using all excess cash to buy the shares back at what looks like a bargain price relative to the NAV.

The good news is that Texton has been recycling capital, with R71.9 million of non-core assets sold. The bad news is that they love investing in international property investments even though the market simply won’t pay close to NAV for that exposure, with R30.6 million deployed in such investments over the same period as the aforementioned disposals. For reference, R34.2 million was used for capital expenditure in the South African portfolio. Share buybacks? Just over R300k.

The capex is necessary and can be value-adding for investors. As for the international stuff, it speaks volumes that Texton’s board believes more in that opportunity than in simply buying back their own shares at a 45% discount to NAV.

Even more strangely, the dividend per share is up by 4.5%. If nothing else, at least pay a flat or lower dividend and use the excess cash for more buybacks!

Nibbles:

Director dealings:

In the recent Lighthouse Properties (JSE: LTE) bookbuild to raise capital, Des de Beer subscribed for shares worth R15.1 million. An associate of a different director subscribed for nearly R3 million in shares.

An associate of a director of Discovery (JSE: DSY) sold shares worth R11.9 million.

A director of Aspen (JSE: APN) sold shares worth R2.9 million.

The CFO of Metrofile (JSE: MFL) has bought yet more shares, this time to the value of R210k.

A prescribed officer of Thungela (JSE: TGA) sold shares worth R148k.

Due to the vesting of share awards, there was selling by various directors / prescribed officers of Woolworths (JSE: WHL). In several cases, the sales exceeded the amount needed to settle taxes. This counts as a sale in my books, particularly given the current pressures in the business.

Primary Health Properties (JSE: PHP) has been included in various JSE indices. This is important as it means that index tracking funds (like ETFs tracking those indices) will need to buy the shares.

Mantengu Mining (JSE: MTU) has made some major changes to the board. These include Alastair Collins moving from chairman to Chief Legal Officer (you won’t see that career path every day) and Jonas Tshikundamalema appointed as Chairman in his place.

From the garb of the working class to counterculture symbol and onward to wardrobe staple, nothing says “market penetration” like a pair of blue jeans.

Farmers, cowboys, rock stars, celebrities, presidents and you and I – everyone’s got at least one pair of jeans in their cupboard. They’re comfy, stylish, and go with pretty much anything. How did a singular item of clothing manage to make its way into wardrobes on every continent in the world? If you believe the popular myth peddled by Levis, jeans were invented by their founder, Levi Strauss, during the American gold rush in the late 1800s. While Levi’s isn’t lying about that story, they aren’t giving us 100% of the facts either.

Putting the blue in blue collar

Here are some quick facts about jeans to get us started. First of all, every pair of jeans in the world is made of cotton. Well, mostly cotton – in some cases, elastane or spandex is added to the fabric to create more stretch, but the dominant fibre must be cotton. All denim is created through generally the same process: cotton fibre is spun into yarn. Half of the yarn is dyed, while the other half is left white. These two yarns are then woven together in a tight pattern, which creates the hardiness that denim is known for.

While many people associate the word denim with the colour blue, denim actually refers to the type of weave, not the colour of the end product. In other words – any colour denim is as genuine as the blue kind, as long as the weave is correct.

Research shows that fabric for jeans actually got its start in two 17th century cities – Genoa, Italy, and Nîmes, France. The word “jeans” might even come from the French word for Genoa, “Gênes.” In Nîmes, weavers tried to recreate the hardy “Gênes” fabric but ended up making something slightly different, a durable twill fabric known as denim (short for “de Nîmes,” or “from Nîmes”).

The fabric from Genoa was a fustian material, similar to corduroy, and was affordable, making it perfect for work clothes. In fact, the Genoese navy outfitted all of their sailors in jeans because they could wear them wet or dry (I can’t think of a worse fate than being made to perform manual work while wearing wet jeans). Denim from Nîmes, on the other hand, was tougher and considered higher quality, and was therefore often used for smocks or overalls.

The German and the gold rush

As you can see, denim had been in production for quite some time before Levi Strauss entered the picture. In 1851, the young Mr. Strauss left Germany and headed to New York to join his older brothers, who ran a goods store there. Having quickly picked up the tricks of the trade, he set out for San Francisco 1853 to start his own dry goods business. Ever heard of selling shovels in a gold rush? From the sounds of it, that may be quite literally what Levi Strauss was doing.

Around this time, Jacob Davis, a tailor who regularly bought fabric from Levi’s store, came up with an idea. A common problem that many of Davis’ customers faced was that their pants would tear from hard wear. After being asked to mend many of these pairs of torn pants, Davis noticed that they often tore in the same places. In 1872, Davis wrote to Strauss, suggesting they team up to patent and sell clothing reinforced with rivets. These copper rivets were meant to strengthen areas that took a lot of wear, like pocket corners and the bottom of the button fly. Strauss liked the idea, and in 1873, they secured US patent No. 139,121 for their “Improvement in Fastening Pocket-Openings.”

Davis and Strauss played around with different fabrics at first, even trying out brown cotton duck, a heavy-duty material (not a waterfowl). But they quickly realised denim was a much better fit for work pants, so they made the switch. In the beginning, Strauss’ jeans were just tough pants for factory workers, miners, farmers, and cattlemen across the North American West. The jeans of this era were 100% a logistic solution for those who did hard manual jobs – accordingly, they were worn baggy and loose, kind of like dungarees without the bib. In fact, Levi Strauss didn’t even call them “jeans” until 1960 – before that, they were known as “waist overalls.”

Blue jeans and big screens

After James Dean rocked jeans in Rebel Without a Cause in the 1950s, they became a symbol of youth rebellion. By the 1960s, wearing jeans was becoming more mainstream, and by the 1970s, they were a staple for casual wear in the US. Distressed denim took off in the punk movement during the ’70s, where early punks ripped up their clothes to show their anger toward capitalism and corporate greed. Safety pins became a statement, encouraging people to resist the fashion trends that fueled big corporations.

Of course, it didn’t take long for those same corporations to catch on and start selling pre-ripped clothes with safety pins already attached, watering down the original punk message. Denim became a key part of this rebellious style, with both men and women wearing torn jeans and jackets, often accessorised with pins, badges and bold slogans. The trend resurfaced in the ’90s with grunge fashion, where loose-fitting ripped jeans, flannel shirts, and layered T-shirts became the go-to look. This anti-conformist style even helped shape the casual chic trend that carried into the 2000s.

A look to die for

In the Soviet Union, jeans were seen as the ultimate symbol of the Western way of life. “Jeans fever” officially kicked off in 1957 during the World Festival of Youth and Students. While jeans weren’t officially banned, they were hard to find because the Soviet government saw them as a symbol of rebellion. Soviet youth wanted to copy the style of Western film and rock stars, but the government resisted producing or supplying jeans, since that would mean giving in to capitalist market demands.

People went to extreme lengths to get their hands on real Western-made jeans, sometimes even resorting to violence and illegal activities. This led to the rise of black markets and the bootlegging of jeans, which became a significant part of Soviet cultural history. The US jeans brand Rokotov and Fainberg is actually named after two Soviet men, Yan Rokotov and Vladislav Faibishenko, who were executed for, among other things, trafficking in jeans.

A runway/runaway success

Today, jeans are far more than the rugged workwear Levi Strauss and Jacob Davis envisioned – they’re a global cultural staple. From casual Fridays at the office to high fashion runways, jeans have found their way into every corner of society, defying the boundaries of class, geography, and fashion trends. They have transcended their practical beginnings to become a symbol of effortless cool, rebellion, and self-expression.

However, this long-standing reign may be facing a new challenge. As the athleisure trend continues to gain momentum, more people are turning to sportswear and activewear for everyday outfits. The rise of stretchy, breathable fabrics and the appeal of comfort-driven style means that jeans are no longer the default choice for many. With yoga pants, leggings, and joggers increasingly taking centre stage, jeans may no longer enjoy the monopoly they once did in our wardrobes.

Even so, denim’s remarkable market penetration remains a testament to its staying power. While trends may shift and new contenders emerge, jeans have proven they can adapt and evolve. Whether they will continue to dominate or share space with the rising athleisure movement remains to be seen, but one thing is certain: jeans have cemented their place in fashion history, and they’re not disappearing anytime soon.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

At Clientèle, perhaps its best to focus on the dividend (JSE: CLI)

IFRS 17 has severely impacted comparability of the numbers

The transition in accounting rules from IFRS 4 to IFRS 17 has been a difficult thing for life insurance groups. Comparability is severely limited in these cases, at least in the transition year itself. For example, just moving from IFRS 4 to IFRS 17 suddenly increased the net asset value at Clientèle by R2.2 billion. Despite the jump in net asset value, HEPS fell by 4% year-on-year, largely influenced by a major swing in the effective tax rate due to deferred tax assets.

TL;DR: it’s complicated.

When the numbers get this tricky, I try and look for something simple to latch onto. Cash is always a good one, so the dividend being flat at 125 cents per share is probably the best metric to consider here. I also wouldn’t ignore profit before tax increasing by 47% thanks to a solid performance from the underlying operations.

The share price has been choppy in recent times, delivering a return of only 6.7% in the past year. If you add on that dividend though, it looks vastly better, as the trailing dividend yield is a substantial 10.5%. Sometimes, the dividend is an almost immaterial component of total return. At Clientèle, that definitely isn’t the case. This is a perfect example of a company that is offering a substantial dividend and decent prospects of underlying growth.

Fairvest expects to exceed distribution guidance for the B shares (JSE: FTA | JSE: FTB)

Key metrics are moving in the right direction

Fairvest has released an update dealing with the trading period that ended in August. This is a pre-close update, as the financial year ends in September.

With 69.1% of revenue coming from the retail sector, Fairvest’s exposure is mostly in the right place. They are sitting with 18.8% of revenue in the office sector and 12.1% in industrials.

Between March (the interim period) and August, vacancies decreased from 4.7% to 5.3%. Rental reversions (the rate on new leases vs. the expired lease) were positive 4.3%, which is also higher than the interim period at 3.1%. This has contributed to the happy news that Fairvest is expected to exceed the guided distribution per B share of between 41.5 cents and 42.5 cents.

Even the office portfolio is heading in the right direction, with vacancy rates down from 12.6% in the interim period to 10.7% at the end of August. They’ve been working hard on that portfolio and I think the work-from-home trend is well and truly dead for most companies.

Investec expects HEPS to be rather flat in the interim period (JSE: INL | JSE: INP)

The UK business underperformed the local business

Investec has released a pre-close trading update dealing with the five months to August. In both countries of operation, the UK and South Africa, the period was impacted by uncertainty ahead of elections. Since then, it’s been a story of improved activity and an expectation of reduced rates that has now materialised.

For the six months to September, Investec expects pre-provision adjusted operating profit to be between 6.7% and 12.9% higher. This was assisted by an improvement in the cost-to-income ratio, as revenue growth was ahead of costs. Both net interest income and non-interest revenue seemed to do well, although trading income was down year-on-year. It’s interesting to see Investec highlight that although there was decent demand for loans out there, they also saw elevated repayments in a higher interest rate environment. Perhaps the biggest operational highlight was that funds under management in Southern Africa increased by 10.7%.

Unfortunately, HEPS will be -1.4% to +3.5% vs. the prior period, so that’s a pretty flat performance at the mid-point. One of the reasons for the flat HEPS performance is the cost of corporate activity and other strategic actions, along with the amortisation of intangible assets related to the Rathbones business combination in this period. Remember, HEPS may exclude impairments but it doesn’t exclude amortisation.

The credit loss ratio is around the upper end of the through-the-cycle range of 25 basis points to 45 basis points, with a fairly consistent credit position vs. the end of the previous financial year.

Looking deeper, the Southern African business achieved growth in adjusted operating profit of at least 15% compared to the prior period. The credit loss ratio is below the midpoint of the through-the-cycle range of 15 basis points to 35 basis points. Return on equity should be close to the upper end of the 16% to 20% target.

The UK business has a far less compelling year-on-year story to tell, with adjusted operating profit down by between 5% and 11%. The credit loss ratio is above the guided range of 50 basis points to 60 basis points, with specific impairments having been suffered. Return on tangible equity is between 13% and 14%, within the target range of 13% to 17%.

This means that group return on equity is between 13% and 14%, within the target range of 13% to 17% but at the lower end of it. Group return on tangible equity came in between 15.5% and 16.5%, which is in the middle of the 14% to 18% target range.

MTN moves forward with the proposed extension to the B-BBEE deal (JSE: MTN)

If shareholders don’t approve the extension, there is very little value in the scheme

As previously announced, MTN is looking to extend the MTN Zakhele Futhi scheme by a period of three years. This is quite simply to buy time for the MTN share price to hopefully recover, creating more equity value in the B-BBEE scheme. There is a great deal of debt in the scheme (like in most B-BBEE deals), with the recent pressure in the MTN share price leading to a situation where the B-BBEE scheme was underwater for a while and due to expire worthless.

Thankfully, a recent uptick in the MTN price has put the scheme back in the green, but not by much. I agree with MTN that it is not in the best interests of the B-BBEE shareholders to allow the scheme to expire in November as was originally the plan. If shareholder don’t vote in favour of the extension, the current MTN share price suggests that each MTN Zakhele Futhi shareholder would only receive R3.51 in value once all the MTN shares are sold and the debt is settled.

With MTN Zakhele Futhi currently trading at R10, the market is clearly pricing in a successful extension.

The circular with the details of the extension and the notice of the general meeting can be found at the bottom of the page at this link.

Orion has released its detailed annual report (JSE: ORN)

The company has had an incredibly busy year

Orion Minerals has released full details for the year ended June 2024. Enthusiasts of junior mining will enjoy working through the full report. Orion gained a lot of respect from me this year for choosing to include retail investors in its capital raise. Far too many listed companies just run off to institutions when they need money.

The group’s main activities relate to the Prieska Copper Zinc Mine and the Okiep Copper Project. At the former, they are busy with the development of key infrastructure to support mining operations. At the latter, they are earlier in the process with the current priority being to complete the bankable feasibility study this year.

There is a third project that is even earlier in the process called the Jacomynspan Nickel-Copper-PGE project. They are in discussions with potential users of the metal vapour powder products that they think can be produced from that project.

With trial mining underway at the Prieska Copper Zinc Mine, this was a hugely important transition period for the company.

Renergen has resumed LNG production (JSE: REN)

Annual maintenance has been completed

Production at Renergen is always a contentious issue, considering just how long it took for the helium production to come online. You can almost hear a sigh of relief when there’s good news around the operations, as many shareholders are still licking their wounds.

The good news is that the annual maintenance of the entire plant is now complete, with the plant started earlier this week and LNG production resumed. The helium module is being started and will be brought down to temperature to recommence filling. Perhaps the important nuance here is that they haven’t actually started filling helium again just yet.

Importantly, the maintenance was managed entirely by Renergen’s internal team rather than any OEM contractors.

Nuggets:

Director dealings:

The group company secretary of Sun International (JSE: SUI) has sold shares worth nearly R1.7 million.

Wesizwe Platinum (JSE: WEZ) released a trading statement dealing with the six months to June. HEPS will be between 1.40 cents and 13.32 cents vs. a loss of 59.63 cents in the comparable period. When the guided range is that wide, you can see that they are at a point where the layer of profits is terribly thin. The increase was mainly due to unrealised forex gains on foreign loans.

SAB Zenzele Kabili (JSE: SZK), the B-BBEE structure linked to AB InBev (JSE: ANH), has released earnings for the six months to June. This was the scheme where nobody wanted to listen to sensible views during the pandemic. Even the directors tried to tell the market to stop buying shares so far above the value of what they were actually worth. Due to the level of debt in the structure vs. the performance in AB InBev, here’s what it looks like when investors choose to mistrust experienced views and the numerous analysts who were quoted in the media trying to warn people to stop buying this structure at crazy levels:

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Bytes is growing, but just watch those margins (JSE: BYI)

The market liked this update, with the price closing 9.5% higher

Bytes Technology has released an update for the six months ended August 2024. The highlights are that gross invoiced income and adjusted operating profit grew by 13.5%, with the market showing its appreciation for that number. The net cash position at the end of the period was £71.5 million. This is after paying £35.3 million in dividends.

They are generally more cash generative in the second half of the year than the first half, so keep that in mind when results come out on 15 October.

But perhaps the bigger thing to keep in mind is that gross margin has been a pressure point in recent periods and that seems to have continued over these six months, with gross profit only up by 9%. That’s well below the growth in gross invoiced income, which is precisely the challenge.

Clientèle’s numbers aren’t as bad as they thought (JSE: CLI)

Accounting changes are having a major impact here

Clientèle has released an updated trading statement dealing with the year ended June 2024. Their first trading statement noted an expected drop in HEPS of between 33% and 53%. The updated number is a drop of between 30% and 35%, so they’ve ended up right at the bottom of that initially guided range. That’s a good thing, I guess.

Much of this is because of the significant changes to accounting rules in this space thanks to the introduction of IFRS 17. Without that impact, earnings would not differ by more than 20% to the comparable period.

Detailed results are due for release on Friday 20th September, so we will shortly have full numbers.

Discovery delivered a much better set of numbers (JSE: DSY)

Discovery SA and Vitality were the stars

We already knew that these numbers would be good, as Discovery released quite a detailed update dealing with the year ended June 2024. Full results are now available for those who want to really dig in.

The numbers look a lot better than usual at Discovery, with normalised headline earnings up by 15% at group level. Without the normalisation, headline earnings is up by 7%. The really strong contributions came in from Discovery SA and Vitality Global, with normalised profit from operations up by 16% and 57% respectively. Sadly, Vitality UK was down by 14%.