In the current economic environment, and in pursuance of various commercial goals, business owners frequently sell their business interests.

The sale of shares in a business, whether to reinvest in a more profitable business, withdraw one’s interest from the business sector, or simply sell the interest to one’s best advantage, can be structured in various ways.

From a tax perspective, the capital gains tax consequences arising from the disposal of a business interest (i.e., the disposal of shares) become relevant. Several variations of sale agreements can be entered into with the consideration being received by the seller at different stages of the transaction, depending on its nature and content. This article will focus specifically on the tax consequences that will be incurred depending on the timing of the receipt of the consideration.

Receipt of proceeds on the date of sale

From a tax perspective, the disposal of a business interest will typically be deemed to take place once all the suspensive conditions have been lifted. Therefore, where a business interest is sold and the seller receives the full proceeds (the consideration) in the same year, capital gains tax will be payable in the year of assessment in which the asset is disposed of.

In considering the amount of tax to be paid, the identity of the holder of the shares should be considered. The sale of capital assets by a company attracts capital gains tax at an effective rate of 21.6%, which is slightly higher than the effective rate of 18% applicable to individuals but lower than the effective rate of 36% pertaining to trusts. Typically, however, in the context of a trust, the capital gain can be distributed to the beneficiaries of the trust and, therefore, taxed at the marginal tax rates of those beneficiaries, which in the case of natural persons will, again, be 18%.

Receipt of proceeds over time

The sale of shares that is subject to a suspensive condition can only be said to be disposed of once the underlying conditions are all met. Where all the conditions are met in year one but the consideration is payable in annual instalments over a period of, for example, four years, tax will remain payable on the full amount in year one. This is so because the suspensive conditions underlying the agreement would have been met and, therefore, irrespective of when the consideration for such disposal is received, the full tax amount will be due in the first year of assessment.

The receipt of consideration in instalments over time does not suspend the capital gains tax consequences where all the underlying conditions of the agreement are met. Accordingly, because the tax is triggered on the entire proceeds in the first year, it could potentially lead to cashflow problems for the seller while the balance of the proceeds remain outstanding.

On the contrary, where a portion of the proceeds of the transaction is subject to a suspensive condition which will be fulfilled over time, the capital gains tax will likely become payable in differing parts. For illustrative purposes, let’s assume that some conditions are required to be met in year one, after which 70% of the consideration is payable, with the remaining 30% to be paid in year two, upon fulfilment of further conditions. In this scenario, capital gains tax will be payable on 70% of the consideration upon fulfilment of the stipulated conditions for year one, with capital gains tax being payable on the remainder in year two, provided that the remaining conditions are met. In this scenario, typically, the cashflows and the tax liability will be aligned.

Receipt of proceeds: initial and contingent consideration

Where the sale of shares is subject, in part, to an earn-out-clause, the capital gains tax consequences could be spread over multiple years of assessment. In such instances, a portion of the proceeds will be fixed, with the remainder portion being subject to variable metrics.

Should the fixed consideration received in year one be less than the base cost of the shares, a capital loss will be realised; however, the remainder portion of the proceeds does not accrue to the taxpayer in the same year of assessment. Accordingly, the capital loss determined must be disregarded and can only be taken into account in future years of assessment, once a capital gain is realised on the disposal of the asset as a whole. If, after all the proceeds have been settled, no capital gain is realised, then the capital loss can be utilised in the same year of assessment against other capital gains.

As is demonstrated by the above examples, there is often a mismatch between commercial and tax considerations underlying transactions. Often, there is a general misunderstanding that the payment of the tax will coincide with the receipt of the sale proceeds. This is not always the case and, therefore, care needs to be taken in the conclusion of sale transactions to ensure that there is no mismatch between the tax payment and the receipt of the cash proceeds. Alternatively, where such a mismatch cannot be avoided commercially, planning for the cashflow to settle the tax liability timeously will be extremely important.

Angelique Stronkhorst is a Consultant and Bobby Wessels a Manager in Corporate and International Tax | AJM.

This article first appeared in DealMakers, SA’s quarterly M&A publication DealMakers is SA’s M&A publication www.dealmakerssouthafrica.com

Nine months into the financial year, Harmony is on track to meet full year guidance

In the latest quarterly result, Harmony focuses on the year-to-date numbers as there are now three quarters out of the way. Although gold revenue is only partially in the company’s control, it increased by 11% year-on-year. A 13% increase in the average gold price was the magic here, with a 2% increase in production if we allow for the closure of Bambanani at the end of FY22.

With only an 8% increase in group all-in sustaining costs (AISC), group operating free cash flow increased magnificently by 49%. This biggest driver was a 94% increase in South African underground operating free cash flow that enjoyed higher recovered grades.

Net debt to EBITDA has improved to 0.5x from 0.6x at the end of the prior quarter.

The company is on track to meet FY23 production, cost and grade guidance.

When looking at Harmony, don’t forget that the company has strategically decided to increase exposure to copper. One wonders if the name Harmony Gold will be changed at some point in future.

Lesaka Technologies is still loss-making (JSE: LSK)

There’s a long way to go here, as profits aren’t sufficient to cover finance costs

Lesaka is in the process of a turnaround, which included the recent acquisition of the Connect Group. Although such a large acquisition obviously did wonderful things for revenue, the reality is that there is still an attributable net loss. In fact, it is bigger in the latest quarter ($5.8 million) that it was a year ago ($3.3 million).

If you make several adjustments, including casually ignoring the net interest expense, you’ll arrive at a positive operating income number. In other words, the group doesn’t have sufficient profits to cover the debt on the balance sheet after the acquisition of Connect Group.

With a market cap of R3.5 billion, the market seems to still believe in the long-term story of taking FinTech services to mass market consumers.

A little ray of sunshine (JSE: SSU)

Southern Sun released solid numbers and fell 1.8% anyway in the market sell-off

Nothing with substantial exposure to South Africa was spared on Wednesday. As commentators on Twitter lamented the volumes on the market, South African equities were wiped out amid concerns about our country. It’s hard to argue at this point.

Southern Sun tried its best to cast some light on a dark day, releasing numbers that reflect a strong return to profitability. There is noise in the numbers (a separation payment this year from Tsogo Sun Gaming and an insurance payout in the prior year), so adjusted HEPS is probably the most sensible measure here. For the year ended March, that metric has increased to between 27.0 and 32.0 cents vs. the prior period headline loss of 8.0 cents.

Obviously, this was driven by improved conditions in the travel industry. It’s also exciting to note that demand for conferencing and events has increased. The one exception is Sandton, which is performing below pre-Covid levels as companies adopted a hybrid working culture during the pandemic and have stuck with it.

Net debt is down at R1.3 billion. For reference, the group market cap is R6.6 billion.

The share price has fully recovered to pre-Covid levels, though it does seem to be running out of steam:

TFG lost R1.5 billion in turnover this year to Eskom (JSE: TFG)

Where else could the R200 million in power backup capex have been spent?

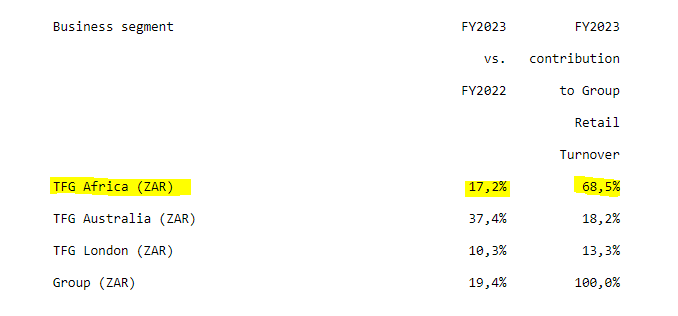

The Foschini Group (TFG) achieved retail turnover growth of 14.3% in the fourth quarter of 2023. It’s important to understand where the group makes its money, so here’s a snippet with TFG Africa optimistically highlighted in yellow as a symbol of my desire for electricity:

As we dig into the South African numbers, turnover growth was 6.0% excluding Tapestry Home Brands, which reflects a likely drop in volumes based on where inflation has been. So, it makes sense to see such high revenue growth at group level when you take the major acquisition into account, as South Africa was up 15.6% without that adjustment.

That’s still an impressive number when you consider the substantial impact of load shedding, something that is only getting worse. Significant power cuts over the festive period led to markdowns of inventory as sales didn’t meet expectations, so gross margins fell 2.1% in TFG Africa for the full year compared to the prior year.

Good news in my view is the split between cash and credit sales growth, with the former up 17.8% in TFG Africa and the latter only up by 9.6%.

At first blush, it looks like TFG London performed poorly with a turnover decline of 5.2% in the fourth quarter. The group expected this, as a strategic decision has been made to make the business smaller and more profitable. The profits are what actually count.

TFG Australia managed 6.7% growth in local currency in the fourth quarter.

I was quite pleased to see online retail turnover increasing its contribution to group turnover. I firmly believe that many of the consumer habits created during the pandemic will stick around, so this supports my thesis. Online sales contributed 10.8% to group turnover vs. 10.5% a year ago. The country-level contribution still varies wildly, with TFG Africa at 3.5%, TFG London at 49.6% and TFG Australia at 6.4%.

TFG loves a good bolt-on acquisition and the latest example is the acquisition of Street Fever, a group operating through the Sneaker Factory brand. All conditions have been met and the deal has closed.

The group is treating 2024 as a year of “consolidation and focusing on improving operating leverage” – in other words, taking a defensive approach in response to local operating conditions. There is also a high base effect in both offshore businesses, with sales down year-on-year in April in both London and Australia.

The share price is down 14.6% this year, reflecting the broader problems in our economy.

The only transaction in Transaction Capital was the sell button (JSE: TCP)

A 35% drop in the share price says as much about SA Inc. as it does about the company

The last time we were this upset as a country, Donald had dropped the bat and we walked away empty-handed from a Cricket World Cup. That trauma feels very mild compared to the current cocktail of doom being served up by Eskom and its effect on our economy. It’s like a cancer that is growing in intensity by the day, with many victims along the way.

Having been smashed by 35% on Wednesday after releasing results, Transaction Capital is now way down at R7.11. For reference, my average in-price is R12.23 and that was after adding to my position at a similar level to where the directors recently bought shares. I would also point out that if you show me someone who has never suffered a loss in the market, I’ll show you a liar. I’ll take this one (and of course several others) on the chin.

This is where the “be greedy when others are fearful” approach really gets put to the test. It’s also where a banking concept called “value at risk” becomes extremely important. Adding to a position is great if you believe in the long-term story, but you also have to be aware of exposure in relation to the rest of a portfolio. Until Transaction Capital settles and starts delivering meaningful and sustained share price gains, I can’t see myself buying more.

With that out of the way, Transaction Capital’s results for the six months to March reflect a 355% decrease (not a typo) to a loss of 183.3 cents per share vs. earnings of 71.9 cents a share in the comparable period.

Even if you use core earnings (management’s view on things), this dropped by 48% and return on equity came in at a paltry 7.3%. This is officially lower than Sasfin’s levels and that’s quite the benchmark for underperformance.

The market is panicking about the balance sheet and whether we are headed for another Ascendis / EOH situation. Management has made strong statements like the balance sheet being “sufficiently capitalised” and “debt covenant levels remaining intact” – the first part being the key.

There are no cross-default clauses at subsidiary level, so the real question is whether SA Taxi could go to zero and what value would then be left in the rest of the group. The group has thrown the kitchen sink at the SA Taxi numbers, taking huge restructuring provisions in one shot. Another big claim is made that “Mobalyz” (the new name for SA Taxi) should settle into “sustainable and predictable profitability during the 2024 financial year” – management won’t say things like this lightly.

Of course, as Shakespeare reminds us, that by which we call a rose by any other name would still smell as kak. We need more than a rebrand here.

With core attributable earnings at Nutun up by 15% and core attributable earnings at WeBuyCars down by 22%, it’s not like the combined impact in the rest of the business is fantastic either. In case you’re wondering, the WeBuyCars issue is a margin problem rather than a volumes problem, with Transaction Capital noting a high base effect.

Here’s what a very painful ride looks like:

Universal Partners reports a drop in NAV per share (JSE: UPL)

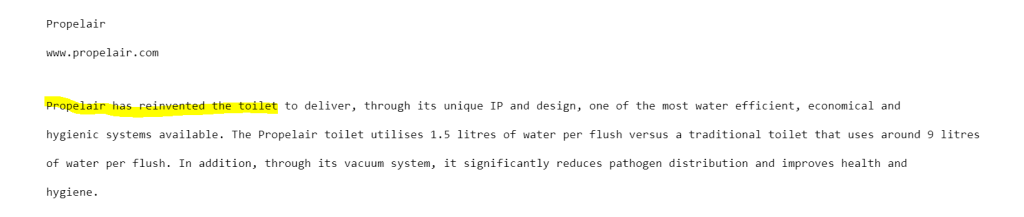

Transaction Capital may be in the toilet, but this crowd has reinvented it

The JSE is nothing if not an entertaining place. One of the investments in the Universal Partners stable is a business called Propelair. It makes some pretty bold claims:

Jokes aside, Universal Partners has an incredibly interesting portfolio that includes various growth businesses in Europe and particularly the United Kingdom.

One of the them is Dentex Healthcare Group, a dental practice consolidation group focused on the UK. Through a merger with Portman Dental Care, Universal Partners has taken cash off the table and now holds a stake in a much larger business.

There’s also an accountancy and payroll company in the UK called Workwell, which Universal Capital has supported in executing a couple of bolt-on acquisitions. None of the services are sexy, but they are effective.

A more exotic business is SC Lowy Partners, a specialist financial group covering high-yield and distressed debt market-making and investment management. This literally couldn’t be more different to a vanilla accounting business.

That’s not all, folks. There is also Xcede (a global recruitment specialist) and of course Propelair, the toilet innovators mentioned at the start.

This investment holding company’s net asset value (NAV) per share has decreased year-on-year from GBP 1.458 to GBP 1.420. That’s roughly R33.80 per share, with the price currently trading at R24.00 per share. This is a discount of below 30%, which is actually rather good for a group like this.

Little Bites:

Director dealings:

An associate of a director of Ascendis Health (JSE: ASC) has bought shares in the company worth just over R92k.

In a move that might be more interesting than it sounds, PSG Konsult (JSE: KST) wants to change its name to PSG Financial Services Limited. This is a nod to the existing service offering and might be a clue to ambitions to broaden that offering further.

Go Life International (JSE: GLI) is the penny stock you’ve probably never heard of. You haven’t missed out, since it spectacularly destroyed shareholder value and trades (very rarely) at one cent per share. The company has announced a specific issue of shares for R4.75 million, the proceeds of which will be used to settle creditors. Management reckons there are “sound prospects” yet when I tried to access the website link they provided, I found a GoDaddy domain parking page. There really are some inexplicable zombies on the JSE. PS: I eventually found the right website.

Equites joins Redefine in the property naughty corner (JSE: EQU)

A sell-off in the share price greeted the news of a nasty drop in net asset value per share

Sentiment in the property sector isn’t great at the moment. Property valuations are under pressure in this environment and that’s not good for the share prices, which are usually valued on a combination of yield and a reference to net asset value (NAV) per share.

After Redefine released results that upset the market, Equites Property Fund followed suit and fell nearly 6.5% on the day. Despite distribution per share growth of 4.1%, the market looked at the drop in NAV per share of 10.5% and acted accordingly.

The pain was especially felt in the UK portfolio, where values fell by 21.4% on a like-for-like basis because logistics yields shifted outwards by a huge 175 basis points from 3.25% to 5.00%. An increase in the South African portfolio value of 4.3% looks a little odd in that context (shouldn’t our yields also be higher?), but that local performance managed to turn a gaping wound into a bad scratch instead.

I’ve written on this topic a few times in Ghost Mail, but it is worth repeating here: property funds may offer inflationary protection in cash distributions as rentals increase, but they don’t help you with property values as the yields move higher and the values come down accordingly.

In a much simpler explanation that brings it closer to home (literally): what happens to the price of your house when interest rates have moved higher? If you aren’t sure, pour yourself a strong one before phoning an estate agent.

Industrials REIT releases the circular for the Blackstone deal (JSE: MLI)

As we already knew, the board is recommending the cash offer

An acquisition process is highly regulated and full of paperwork. You can expect to see several complicated announcements as Blackstone’s buyout offer for Industrials REIT goes through the motions.

This is especially true as the process is playing out in English law, which from my observations is even more complicated than our local takeover law. If they can go to such lengths in that country to recognise a new king, then you can imagine what a takeover process looks like.

The important point is that the directors of Industrials REIT unanimously recommend the deal to shareholders in the circular. It would be a surprise if it doesn’t get approved by shareholders.

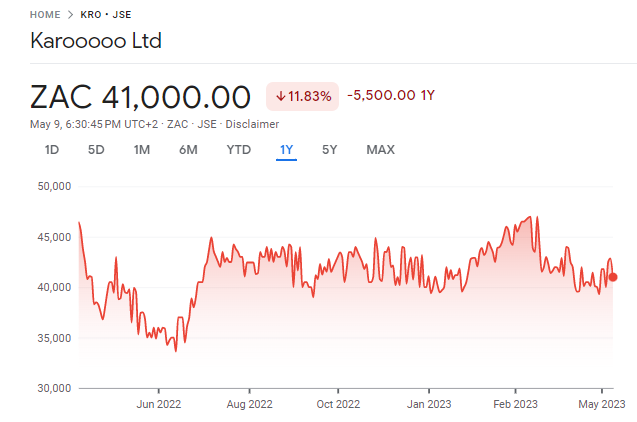

Karooooo is growing, but not as quickly (JSE: KRO)

The world’s most stubborn traded range continues

If ever you wanted an illiquid stock where you could just patiently sit on the bid or offer to try and capture the spread, you could do far worse than Karooooo:

With more sideways action in the share price than a Monster Energy drifting competition, Karooooo has released its results for the quarter and year ended 28 February 2023. The numbers aren’t going sideways even if the share price is, with subscribers up 13% year-on-year.

There’s a concern about the rate of growth, with subscriber growth in Q4 2023 coming in 31% slower than in Q4 2022. This is measured based on the number of net new Cartrack subscribers (38,471 in this quarter vs. 55,587 a year ago).

Total revenue increased by 22% on a constant currency basis and subscription revenue only increased by 16% on a constant currency basis, as the group has increasingly moved away from the focused model that made me buy shares in the first place.

The core business (Cartrack) grew operating profit by 28% for the full financial year and expanded its operating margin from 27% to 30%. That is the gem in this group.

Sadly, management continues to be distracted by the Carzuka project, a used car business that should’ve been called bazooka as a fairer reflection of what it does to group profits. The loss this year was R38 million vs. R13 million the prior year as that business scales up.

Record free cash flow for the year of R547 million was achieved vs. R379 million a year before.

Interestingly, there’s been a change in the accounting policy that sees 56% of costs of acquiring a subscriber capitalised rather than 66% a year before. This is a more conservative approach. Although there is no impact on free cash flow, it does mean that adjusted EBITDA is lower than it would’ve been under the old policy.

Can it get any worse for Quantum Foods? (JSE: QFH)

Load shedding, meet bird flu

The poultry industry is seeing absolute flames at the moment. Even Nando’s Peri-Peri isn’t a fair reflection of what’s going on out there.

Back in February, Quantum Foods released a trading statement that reflected an expected decrease in HEPS of at lest 100% for the six months ended March. In other words, the company expected to be loss-making.

An updated trading statement reflects a decrease of between 76% and 87%, which is still horrible but obviously better than expected. Load shedding and consumer pressures are causing havoc for this business and the broader industry.

Just when things were looking up, the second half of April 2023 saw an outbreak of highly pathogenic avian influenza (HPAI) at Lemoenkloof layer farm in the Western Cape. This resulted in 420,000 layers being culled at a cost of R34 million. Competitor farms in the region were also affected, so eggs are likely to be more expensive in the fairest Cape for the rest of the year.

This industry literally cannot catch a break at the moment.

Sibanye is still a rollercoaster (JSE: SSW)

Many hearts (and wallets) have been broken by this stock

If you’re looking for a steady, safe investment that won’t keep you up at night, Sibanye-Stillwater should be at the very bottom of your list. If the company isn’t dealing with a gold strike, it’s dealing with floods. When those disasters are finally gone, PGM prices fall over. It’s wild.

At least the “green” metals are starting to show signs of promise. The Finnish government is supportive of the Keliber project, having agreed to increase their equity stake to 20%. The Rhyolite Ridge JV has received support from the United States Department of Energy through a conditional $700 million loan.

The South African gold operations have returned to profitability, thankfully. It couldn’t have come at a better time, as the PGM operations have suffered a dip in production and a nasty drop in average basket prices.

With all said and done, adjusted EBITDA for the quarter ended March 2023 is down to R7.8 billion from R13.7 billion a year ago. Yikes. It even looks bad compared to the quarter ended December 2022, which came in above R10 billion.

The culprit is the local PGM business, where production was impacted by Eskom load curtailment and copper theft of all things. Adjusted EBITDA fell 43% year-on-year (admittedly vs. a record base period) and the company believes that the outlook for the second quarter is more positive.

The share price closed 11.3% lower on the day.

Steinhoff: what the FAQ? (JSE: SNH)

This frequently asked questions list makes for entertaining (and rather sad) reading

I don’t know how many more times the Steinhoff board needs to tell investors that the thing is worthless. A frequently asked questions (FAQ) list is the latest attempt, which you can find here.

To save you the time, here’s a pretty blunt answer to this ongoing debate:

The document even includes perhaps the most important question of all:

Jokes aside, there is some important deal news from the company. Mattress Firm and Tempur Sealy International have reached a deal that would see Tempur Sealy acquire all the shares in Mattress Firm in a cash and share transaction valued at $4 billion. Steinhoff holds an economic interest of 45% on a fully-diluted basis in Mattress Firm.

$2.7 billion of the price is payable in cash and the rest is in shares in Tempur Sealy. This will give Steinhoff a 7.5% stake in the combined company, which I’m sure makes the debt holders happy. As per the FAQ, this doesn’t exactly help the equity holders, as the price doesn’t differ materially from Steinhoff’s recent disclosures. Sorry to disappoint.

The deal is only expected to close in the second half of 2024 as there is an extensive regulatory process to be followed. The Federal Trade Commission (FTC) has requested additional information and documentary material, so this won’t be a slam dunk.

Vukile chooses more Spain vs. local pain (JSE: VKE)

And City of Joburg is living up to expectations

Let’s start with the bad news, although some on Twitter felt it might be good news.

Vukile Property Fund’s deal to acquire the Pan Africa Shopping Centre is dead. One of the conditions precedent was for the seller to obtain a written amendment to the notarial head lease from City of Joburg (COJ). It’s hard enough to renew a driver’s licence with those people or pay a traffic fine, so I have no idea why anyone thought this would be successful. Unsurprisingly, the initial deadline of November 2022 was pushed out to April 2023 and then missed again.

The deal is off and I wish the seller luck in ever successfully selling this property. Relying on COJ for something is a horrible position to be in.

Perhaps reminded of just how poorly run parts of our country are, Vukile has exercised its call option to acquire more shares in the Spanish subsidiary, Castellana Properties. This is for a meaty amount, coming in at €63.9 million (note the currency). When this is finalised, Vukile will own 99.6% of Castellana.

Little Bites:

Director dealings:

GMB Liquidity (an associate of newly minted Grand Parade Investments (JSE: GPL) director Greg Bortz) is still mopping up shares in the company, this time buying R2.67 million worth of shares.

Two prescribed officers of Capitec (JSE: CPI) have bought shares worth R2.15 million in total.

An associate of Gareth Ackerman has bought shares inPick n Pay (JSE: PIK) worth R627k as the price has continued to slide.

A director of KAL Group (JSE: KAL) has bought shares worth R22.7k.

OUTsurance Group (JSE: OGL) has completed the acquisition of 50% in Youi Holdings (the Aussie business) from Willem Roos, co-founder of the business. Minority shareholdings are a feature of the OUTsurance structure, as OUTsurance Group only owns 89.7% of OUTsurance Holdings, which in turn has bought the 50% stake.

Octodec (JSE: OCT) has announced a new asset and property management agreement with City Property Administration (CPA). As a reminder of how incestuous the property industry actually is, this is a related party deal as the chairman and managing director of Octodec are also shareholders in CPA and directors of that company. CPA also holds shares in Octodec. With more surprising related parties running around than at a hillbilly’s birthday party, an independent expert will need to opine on the agreement and a circular will be released to shareholders.

Investors in Ethos Capital (JSE: EPE) should note that an investor update presentation will be made available on Wednesday morning as part of an event scheduled for 9am. I’ll revisit it in Ghost Bites this week.

PSV Holdings (JSE: PSV) is suspended and in business rescue. The updates are always a bit of a soap opera, with the latest news being that DNG Energy will put forward a proposal to recapitalise the company during the next 3 months.

The difference between continuing and discontinued operations is critical

At first glance, Barloworld’s results for the year ended March 2023 don’t look good. HEPS fell by between 4.5% and 6.3%, which suggests that the core operations are struggling.

You need to dig deeper, particularly after the mobility business Zeda was unbundled to shareholders and the Logistics business was sold. When earnings have been sold off or simply passed on to shareholders, then group earnings obviously move lower.

This is why the concept of “continuing operations” is so important, as it tells you about what is left in the group. On that measure, HEPS increased by between 28.5% and 31.0%. That’s more like it!

DRDGOLD reports a huge positive swing in EBITDA (JSE: DRD)

The company has enjoyed a higher gold price

DRDGOLD gives punters an exceptionally leveraged play on gold. This chart of DRDGOLD vs. competitors will show you that if you believe gold is going higher, then picking the company with the highest operating leverage (i.e. DRDGOLD) is the way to go:

The reverse is also true, in case you’re wondering. Get it wrong and DRDGOLD will bite your head off.

The reason for this is that DRDGOLD is a tailings business, so it processes ore that was previously mined to get more gold out of it with modern techniques. This isn’t exactly the most efficient way to find the yellow stuff, so the production cost is high and margins are very thin unless the gold price moves higher. You can see where this is going.

Quarter-on-quarter production increased by 4% and the average gold price received was 11% higher in rand. With all-in costs per kilogram only up by 2% over the same period (thanks to improved yield in the process of extracting the gold), the net result is a 54% jump in adjusted EBITDA!

There is no debt in this business, which is why investors see it as a cash cow during a period in which gold prices are rising.

Eastern Platinum completed a rights offering (JSE: EPS)

Most of the capital was raised in Canada

Eastern Platinum has raised roughly R96.5 million through a rights offering, with the vast majority of the capital (around R94.5 million) being raised on the Toronto Stock Exchange.

Ka An Development Co now owns 49.9% in the company after following its basic rights and exercising what the announcement refers to as a subscription privilege.

Orion gets a step closer to unlocking funding (JSE: ORN)

A crucial condition precedent has been met

Orion Minerals rallied 16.7% on the news that the company managed to repay the Anglo American sefa Mining Fund loan facility. The loan dates back to 2015 and was used for exploration and development of the Prieska Copper-Zinc Project.

Thanks to the share placement with Clover Alloys and major existing shareholders, the company settled the loan and has released the shares held as security against the loan. This is the key in unlocking the IDC convertible loan facility and Triple Flag Precious Metals Corp early funding arrangement, as those shares are needed as part of the related security package.

Drawdown on those packages is expected imminently, with the initial capital earmarked for trial mining, dewatering and feasibility studies.

Redefine gets a bloody nose from the market (JSE: RDF)

A significant drop in the dividend never puts a smile on the faces of REIT investors

Redefine (JSE: RDF) finds itself in the unfortunate position in which a large proportion of its portfolio is in the Office sector, which is still a horrible place to be. 38% of the South African portfolio is Office, with a 14.3% vacancy rate and -12.4% rental reversions in the six months to February 2023.

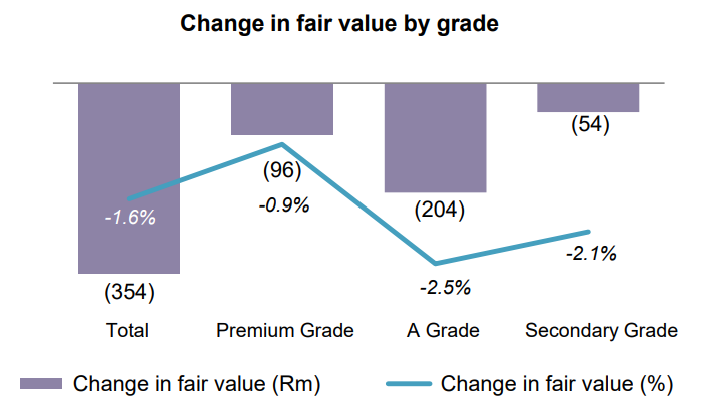

The fair value movements in the Office portfolio make for sad reading regardless of the grade of the property:

In the South African Retail portfolio, reversions were also negative at -3.7%. In other words, new leases are being concluded at lower rates than the expired leases. The vacancy rate of 4.4% is steady year-on-year and the portfolio’s fair value moved higher by R139 million – nowhere near enough to offset the Office move.

Enter the Industrial portfolio: an asset class that is still doing very well. Although vacancies increased from 3.1% to 4.9%, reversions were positive at +1.3% and the total fair value was R141 million higher. In case you’re keeping score, that still doesn’t make up for the Office move.

We can’t just look at the R59.4 billion South African portfolio, as there’s also the R34.7 million portfolio in Poland as part of the Redefine story. 82% of that portfolio is in the Retail sector and only 3% is in Office, with the rest in Industrial – a much better split than in the local business. Metrics are mixed in the overseas business, with reversions still negative as a headache for investors.

If we look at the balance sheet, the SA REIT loan-to-value increased from 40.2% to 40.9% and the weighted average cost of debt in South Africa moved from 8.7% to 9.2%. This really isn’t the right time for debt to be going up, which is part of what the market didn’t like. Although 81.2% of group debt is hedged for an average term of 1.7 years, these hedges can’t be achieved for free and the cost is becoming increasingly more expensive.

With all said and done, distributable income per share was down by 9.2% and the dividend per share fell by 14.2%. The market punished Redefine with a 6.6% drop in the share price.

South32’s Hermosa project gets FAST-41 status (JSE: S32)

Zinc and manganese are of strategic importance

South32 is the proud owner of 100% of the Hermosa project, the only advanced project in the US that could supply two federally designated critical metals: zinc and manganese. With the project now given FAST-41 status, South32 expects a more efficient and transparent process in achieving the federal permits required as the development of the Taylor and Clark deposits continues.

The feasibility study for the Taylor zinc-lead-silver deposit is expected to be completed in the second half of the calendar year and early stage work is underway at the Clark battery-grade manganese deposit, with the focus on moving to a pre-feasibility study.

Little Bites:

Director dealings:

Des de Beer has bought another R2.75 million worth of shares in Lighthouse Properties (JSE: LTE).

An associate of a director of Ascendis Health (JSE: ASC) has bought shares in the company worth R211k.

Sanlam’s (JSE: SLM) partial offer to AfroCentric (JSE: ACT) shareholders is now wholly unconditional, with regulatory approvals having been met.

Claims filed by market purchase claimants in relation to Steinhoff’s (JSE: SNH) global settlement will be settled through the Stichting Steinhoff Recovery Foundation on a rolling basis from 10 May 2023.

Jasco Electronics (JSE: JSC) has received the necessary compliance certificate from the Takeover Regulation Panel (TRP) that will enable the offer and delisting to go ahead.

Efora Energy (JSE: EEL) is suspended from trading and released a trading statement noting a headline loss of between 33.51 cents and 34.51 cents. With a suspended price of 12 cents per share, that doesn’t sound good.

This is a voluntary announcement of a typical bolt-on acquisition

The term “bolt-on” acquisition gets used loosely to describe a deal that is typically low on risk, as the acquirer is buying a business that slots quite easily into the existing business. Or bolts onto it, for that matter.

Alexander Forbes has agreed to acquire a 60% stake in TSA Administration, an independent provider of institutional group risk insurance administration services in South Africa. The business has been at it for 25 years and serves over 120,000 insured members.

Alexander Forbes has the option to acquire the remaining 40% stake over a period of five years. This is a good example of an initial position of control, with the ability to take out the minorities over time.

The deal is too small to even be categorised for JSE purposes, so details of the purchase price haven’t been announced.

MTN Rwanda under margin pressure (JSE: MTN)

This subsidiary seems to be struggling more than the others

MTN Rwanda has grown mobile subscribers by 7% and active data subscribers declined by 0.7%. That’s not exactly a high growth story, even if Mobile Money subscribers grew by 17.2% in the latest quarter. MTN Rwanda experienced a 50 basis points drop in customer market share as competition started to bite.

Service revenue was up by 14.9% and EBITDA by only 9.4%, so margin fell by 220 basis points to 45.5%.

The story at profit after tax level is anything but good, with a 32% drop due to increasing financing costs relating to inflation adjustments on lease payments.

Ouch.

Santova investors can’t wait for Monday (JSE: SNV)

Shortly after the close on Friday, Santova released excellent numbers

To say that Santova has been a winner of the pandemic would be an understatement. This small cap now boasts a market cap of over R1 billion and has been executing a strategy to make the most of the gift that was the supply chain crunch of the pandemic.

It’s clearly been working, with share price growth over three years of a whopping 430%. To avoid using the depths of the pandemic as a base for comparison, we can look at a five-year chart that shows growth of over 162%, which is a compound annual growth rate (CAGR) of 21.4%.

This company is a perfect example of why small cap investors get excited about the world. When it works, it works incredibly well.

The company is still growing its earnings strongly, with growth in headline earnings per share (HEPS) for the 12 months to 28 February 2023 of between 19.1% and 24.1%.

I’m sure that Santova investors are looking forward to seeing what the share price action on Monday morning might bring. Based on the midpoint of the earnings guidance, the company is trading on a Price/Earnings multiple of roughly 5x.

Little bites:

Director dealings:

An associate of a director of FirstRand (JSE: FSR) has sold shares worth R6.7m in exchange for units in a unit trust.

A director of a subsidiary of Growthpoint (JSE: GRT) has sold shares worth nearly R1.7m.

You guessed it – Des de Beer has bought another R1.55 million worth of shares in Lighthouse Properties (JSE: LTE).

The chairman of Southern Palladium (JSE: SDL), Terence Goodlace, has resigned from the board based on other board positions and advice received on the number of board positions in the industry that would be appropriate. Mike Stirzaker, an existing director, has been appointed as the interim chairman.

Attention Indluplace (JSE: ILU) shareholders: check your inboxes for the circular related to the offer by SA Corporate (JSE: SAC).

If you are a shareholder in WBHO (JSE: WBO), take note that the circular regarding the B-BBEE transaction has been posted to shareholders.

And in a final circular reference (Excel jokes are always allowable), Premier Fishing and Brands (JSE: PFB) has released the circular regarding the offer by Sekunjalo Investment Holdings.

The small related party transaction atAcsion Limited (JSE: ACS) has received the nod of approval from the independent expert as being fair to shareholders.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

AB InBev is making a strong case for itself as a more defensive stock than the likes of British American Tobacco.

Famous Brands doesn’t think that load shedding is working out well for the group but I disagree – and the latest numbers seem to support my view.

Calgro M3 has released very strong numbers and is using the depressed share price as an opportunity for buybacks.

CMH’s profitability has been a high performance machine of note.

Astral Foods is firmly on the wrong side of load shedding, with narrow margins on a good day turning into nearly no margin at all on a bad day.

Pick n Pay is taking serious strain at the moment and the share price has horribly underperformed Shoprite.

Santova is a great example of what gets small cap investors excited.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

Despite this tricky environment, EBITDA margin expanded slightly

When the going gets tough, the tough reach for a drink with their mates. That’s how it seems at least, with revenue growth at AB InBev of 13.2% in the first quarter and normalised EBITDA growth of 13.6%. Normalised EBITDA margin has expanded by 13 basis points to 33.5%.

Most of the growth was from pricing increases, with volumes only up by 0.9%. If you ever wondered whether beer is price sensitive, you now have your answer.

The share price is up over 17% this year, so this has been a good place to hide this year. I can’t resist drawing a one-year view of beer vs. cigarettes in the form of AB InBev vs. British American Tobacco.

Pick your sinner:

A famously good trading statement (JSE: FBR)

Famous Brands is keeping us fedwhile we are fed up with Eskom

Surprisingly, Famous Brands suggests that load shedding isn’t doing any favours to its growth prospects. I disagree completely. When there’s no power at home, buying food on the way home becomes a whole lot more appealing. I personally think that load shedding is a net positive for the group, at least for now.

For the year ended February 2023, HEPS is up by between 27% and 47%. To be fair, the base period was still impacted by the back-end of Covid.

Notably, the HEPS number doesn’t include a R75 million liquidation dividend received from the disaster that was Gourmet Burger Kitchen in the UK.

Full results are due on 22 May, in which we will be able to get further details on the performance.

Gold Fields reflects on a largely flat quarter (JSE: GFI)

If you focus on sequential quarters though, it’s anything but flat

This operational update from Gold Fields is a fun example of why you need to be clear on what numbers you are looking at and what you are comparing them to.

On a year-on-year basis, things look alright at Gold Fields. Production was flat, all-in sustaining cost (AISC) was flat and all-in cost (AIC) was 2% higher because of capital expenditure at Salares Norte, a project which is now 90.3% complete. First production at that project is expected during Q4 2023.

The story is different on a quarter-on-quarter basis i.e. compared to the immediately preceding quarter. Production dropped 4% on that basis, AISC was up 8% and ASC was up 3%. Things aren’t as good as they were at the end of 2022, that’s for sure. The pressure seems to mostly be in Australia.

After paying a significant dividend, net debt to EBITDA has increased from 0.29x at the end of 2022 to 0.36x at the end of March 2023.

Production and cost guidance is unchanged for the full year.

KAL shareholders can be thankful for the PEG fuel deal (JSE: KAL)

Formerly called Kaap Agri, the group is operating in a tough environment

South Africa is already a volatile place to do business and that’s before you layer on the complexities of the agriculture sector. A quick look at KAL Group’s performance for the six months to March shows recurring HEPS growth of 8.7% and a similar increase in the dividend, which is hardly a tough result in this environment. The important thing is to look deeper in understanding this number,

Whenever a major acquisition has been executed, you need to look at how the business would’ve performed without that acquisition. This is a comparable view that tells you a lot about sustainable performance, as the major jump from an acquisition is only felt in the period in which the acquisition is first brought into the numbers. After that, it’s all about sustainable earnings.

KAL Group certainly doesn’t try to hide this, making it clear early on that the result was helped by the including of PEG, a fuel retail business that the company recently acquired. To give you a sense of how important it was, group revenue increased by 68.4% overall and 11.8% on a comparable basis.

Excluding fuel, inflation was 12.1%. This suggests that volumes in the rest of the business came under pressure, which makes sense in this environment.

When buying a business, you’re buying the revenue and the expenses. Before you get too excited about that jump in revenue, take note that expenses increased by 72.9% because of the acquisition. Encouragingly, like-for-like expenses were only 0.4% higher. The group has done an exceptional job of managing costs, especially with R35 million of loadshedding expenses. Without the loadshedding costs, like-for-like expenses actually fell by 2.0%.

Looking deeper at major divisions excluding fuel, Agrimark (by far the largest contributor in the group) reported operating profit growth of 1.2% and Agrimark Grain’s profits fell by 11.3%.

The balance sheet reflects a higher net debt position because of the PEG acquisition and inflationary pressures on working capital. When combined with an environment of higher rates, finance costs shot up from R60 million to R152 million.

As commendable as the group’s efforts have been in managing costs, the reality is that the story wouldn’t have been so pretty without the major strategic acquisition. It will be interesting to see how the shape of the group plays out going forward.

Mondi reports a softer quarter (JSE: MNP)

The company calls it a “stable” period, but supply-demand seems to be shifting

Mondi is a highly cyclical business that is impacted by many factors that are far outside of its control. These include market selling prices and levels of demand across various products.

Despite volatility in individual variables, underlying EBITDA from continuing operations was flat vs. the final quarter of 2022, after excluding fair value gains on forestry. This is a non-cash item and I would also happily ignore it.

Worryingly, this quarter displayed lower average selling prices and softer demand. Thankfully, input prices were also lower, which is why EBITDA has turned out ok on a net basis.

The CEO notes that trading in the second quarter is experiencing “subdued” demand with lower average selling prices. Input costs are also reducing, so the overall narrative remains positive and the company is still focused on expansion.

In case you’re wondering, the Russian operations generated €123 million in EBITDA in this quarter and the sale of this division is sitting with Russian authorities for approval. I’m very glad that I don’t need to attend those meetings.

Pick n Pay’s comparable HEPS drops 16.3% (JSE: PIK)

The last thing you want to be running is fridges during load shedding

Is grocery retail defensive? Well, sort of. Even in periods without load shedding, the low net margins in grocery stores and the significant variance in gross margin at product level create a recipe for far more erratic earnings movements than most people think.

Simply, if net margin is 3% and gross margin moves by a rather innocent looking 100 basis points further up, you’re looking at a 33% move in net profit if all else holds equal.

In the 52 weeks to 26 February, Pick n Pay reported 8.9% growth in turnover and an improvement in gross margin to 19.6%. Under normal circumstances, that would be a solid outcome. Instead, with trading expenses up 11.9% thanks to load shedding and general inflationary pressures, the impact on pro forma trading profit is a 4.9% decrease. This just gets worse as you head down the income statement, leading to a drop in pro forma headline earnings per share (HEPS) of -16.3% and a similar decrease in the dividend, as the payout ratio has been held steady. More on that later.

What is “pro forma” HEPS, I hopefully hear you ask? Pick n Pay reports this number to strip out the impact of business interruption insurance proceeds (the insurance was received in a different period to the losses suffered) and hyperinflation gains and losses in Zimbabwe. I agree with these adjustments and Pick n Pay makes its dividend decisions based on this definition of HEPS, so this is what I would focus on.

If we dig into the expense growth, we find a perfect storm of diesel generator costs for load shedding (R430 million net of electricity savings or R522 million before the saving, which shows how much more expensive it is) and incremental costs in implementing the all-important Ekuseni strategic plan. The group-wide cost saving initiatives are the only reason that costs didn’t completely run away from Pick n Pay, with R800 million worth of savings in FY23.

There are some highlights, like 20.2% sales growth at Boxer and 15.3% sales growth from standalone Pick n Pay Clothing stores, with 58 new stores opened in this financial year. On-demand sales (Pick n Pay ASAP!) more than doubled.

I flagged earlier that the payout ratio is changing. Going forward, the payout ratio of 76% (1.3x cover) will change to between a 56% and 67% payout (1.5x to 1.8x cover). In other words, Pick n Pay needs to retain more of its earnings to facilitate the Ekuseni plan. If you’ve been keeping an eye on how well Shoprite has been doing, you’ll know exactly what that is so important.

The one-year chart of these rivals is incredible:

Little Bites:

Director dealings:

Des de Beer is still buying up shares in Lighthouse Properties (JSE: LTE), this time to the value of R402k.

Impala Platinum (JSE: IMP) has acquired a further 0.12% in Royal Bafokeng Platinum (JSE: RBP), taking the stake to 45.20%.

Spar (JSE: SPP) is still in the process of finding a new CEO. Until that happens, Mike Bosman will continue as Executive Chairman of the group.

Aspen (JSE: APN) released a vague announcement about an exclusive distribution agreement with Amgen for a period of five years. The announcement doesn’t give a single number to help investors understand the impact. Unless you’re a medical doctor familiar with the products, this is a prime example of a company using SENS as a public relations tool rather than an investor communication platform.

In case you are closely following the Steinhoff (JSE: SNH) restructuring process or simply looking for a document to help you fall asleep at night, take note that the updated WHOA Restructuring Plan has been published.

Gold Fields has partnered with Osisko Mining to develop the Windfall project in Québec, Canada. The companies will develop and mine the underground Windfall Project. Gold Fields has acquired a 50% interest in the feasibility stage for a cash payment of C$300 million with a further cash payment of C$300 million payable on issuance of key permits. Under the partnership Gold Fields has also acquired a 50% up-front vested interest in Osisko’s highly prospective Urban Barry and Quévillon district exploration camps – in exchange Gold Fields will fund the first C$75 million in regional exploration on the properties over the first seven years, thereafter exploration spend will be shared.

Glencore has announced the purchase of an 30% equity stake in Alunorte and a 45% stake in Mineracão Rio do Norte for a combined equity value of c.US$775 million. The acquisitions from Norwegian Norsk Hydro are inter-conditional. The Brazilian acquisitions provide Glencore with exposure to lower-quartile carbon alumina and bauxite – enhancing Glencore’s capability to supply the materials in the ongoing energy transition.

In February Sibanye-Stillwater, which had a 19.9% stake in Australian retreatment mine New Century Resources, made an unsolicited offer to acquire the remaining stake. The takeover offer of A$1.10 per share saw Sibanye’s stake increase to 87.64% by March 21, 2023. The company will now acquire all remaining shares that have not been validly accepted in the offer. Sibanye has been unhappy for some time with New Century Resources’ strategic direction. The transaction is valued at A$120 million (R1,5 billion).

Unlisted Companies

Local real estate company Only Realty Property Group has acquired a majority stake in Leadhome, a tech-driven, full service real estate agency.

Castleview Property Fund has issued 41,67 million shares in terms of its specific issue of shares for cash announcement in February. The shares were issued to related parties – associates of I Group Investments, the ultimate holding company of Castleview – at R6.48 per share for an aggregate amount of R270 million. The company expects to issue the remaining 6,17 million shares representing an aggregate value of R40 million during July 2023.

Erin Energy – suspended in April 2018 when the company filed for bankruptcy in the US – has had its secondary listing removed by the JSE. The move by the JSE is based on the failure of the company to make any meaningful progress on the completion of the liquidation proceedings and addressing the various non-compliances with the Listing Requirements since its suspension. The last day to trade (off-market) will be 9 May 2023, following which investors will remain shareholders in an unlisted company.

Shareholders in Tsogo Sun Gaming have been asked to approve the change in the company name to Tsogo Sun Limited. In 2019 the company changed its name from Tsogo Sun Holdings Limited to Tsogo Sun Gaming Limited. The Board believes that given the trademark used is Tsogo Sun in its marketing material and in its domain name this would be more appropriate.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Calgro M3 has advised it has repurchased an aggregate of 7 million shares, representing 4.99% of the issued ordinary share capital of the company. The shares were repurchased at R2.20 per share for an aggregate value of R15,4 million. The shares will be delisted and cancelled. The company may repurchase a further 15,1 million shares in terms of the General Authority granted at the company’s annual general meeting.

South32 has increased its share repurchase programme by c. $50 million in anticipation of a stronger outlook for commodity prices in the second half of its financial year. This will enable the company to return $158 million to shareholders before September 2023. This week the company repurchased a further 3,101,096 shares at an aggregate cost of A$12,9 million.

Glencore this week repurchased 12,800,000 shares for a total consideration of £60,27 million. The share repurchases form part of the second phase of the company’s existing buy-back programme.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 24 to 28 April 2023, a further 2,439,269 Prosus shares were repurchased for an aggregate €163,6 million and a further 309,350 Naspers shares for a total consideration of R992,9 million.

One company issued a profit warning this week: Astral Foods and one company issued or withdrew a cautionary notice: Ellies.

Development Partners International, British International Investment, South Suez and other investors have made a US$165 million equity investment into the parent company of Egypt’s discount retailer, Kazyon. The funding will be used to accelerate the retailer’s expansion plans across Africa.

Chariot and Vivo Energy announced a new partnership agreement to implement a gas-to-industry business in Morocco; create a jointly owned SPV for the purchase, transportation and distribution of natural gas to end-users and put in place a long-term gas sales agreement for a portion of the future gas production from the Anchois development project.

A Tunisian startup, Drest.tn, that specialises in online sales of lifestyle products has raised US$336 000 from 216 Capital Ventures, which will be used to expand further into the African Market.

The Rohatyn Group, which recently acquired the business of Ethos Private Equity, has invested in the Kenstra Group, which operates in the East Africa paper and print sectors. Financial terms were not disclosed.

Nomba, a Nigerian payment service provider, announced a US$30 million pre-Series B investment led by Base 10 Partners. Other investors included Partech, Khosla Ventures, Helios Digital Ventures and Shopify.

The International Finance Corporation (IFC) is backing Equatorial Coca-Cola Bottling Company’s sustainability strategy with a €64 million financing package. The company plans reductions in its water and energy footprint through the replacement of production lines, reduction of raw materials, solar panel installations and other changes. The financing package is made up of a €52 million loan from the IFC, concessional finance totalling €8,5 million from the Canada IFC Blended Climate Finance Program and €3,5 million from the Alafaq Aljadida Middle East and North Africa (MENA) Private Sector Development Program.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")