Development Partners International, British International Investment, South Suez and other investors have made a US$165 million equity investment into the parent company of Egypt’s discount retailer, Kazyon. The funding will be used to accelerate the retailer’s expansion plans across Africa.

Chariot and Vivo Energy announced a new partnership agreement to implement a gas-to-industry business in Morocco; create a jointly owned SPV for the purchase, transportation and distribution of natural gas to end-users and put in place a long-term gas sales agreement for a portion of the future gas production from the Anchois development project.

A Tunisian startup, Drest.tn, that specialises in online sales of lifestyle products has raised US$336 000 from 216 Capital Ventures, which will be used to expand further into the African Market.

The Rohatyn Group, which recently acquired the business of Ethos Private Equity, has invested in the Kenstra Group, which operates in the East Africa paper and print sectors. Financial terms were not disclosed.

Nomba, a Nigerian payment service provider, announced a US$30 million pre-Series B investment led by Base 10 Partners. Other investors included Partech, Khosla Ventures, Helios Digital Ventures and Shopify.

The International Finance Corporation (IFC) is backing Equatorial Coca-Cola Bottling Company’s sustainability strategy with a €64 million financing package. The company plans reductions in its water and energy footprint through the replacement of production lines, reduction of raw materials, solar panel installations and other changes. The financing package is made up of a €52 million loan from the IFC, concessional finance totalling €8,5 million from the Canada IFC Blended Climate Finance Program and €3,5 million from the Alafaq Aljadida Middle East and North Africa (MENA) Private Sector Development Program.

There’s no room for error with skinny margins in the poultry industry

This sector isn’t for chickens. When you’re dealing with very small net profit margins, the law of small numbers means that modest changes in ratios further up the income statement (e.g. a seemingly innocent drop in gross margin) can have a massive percentage impact at net profit level.

This leads to earnings volatility and a potentially wild ride for investors. In a country like South Africa that dishes up so many challenges, it’s more like riding a wild stallion than just an erratic donkey.

After alerting the market to its current troubles in January, Astral has updated its guidance with a trading statement for the six months ended March 2023. HEPS is expected to decrease by between 87% and 92%. The only positive here is that this means that the company is still profitable, if only just!

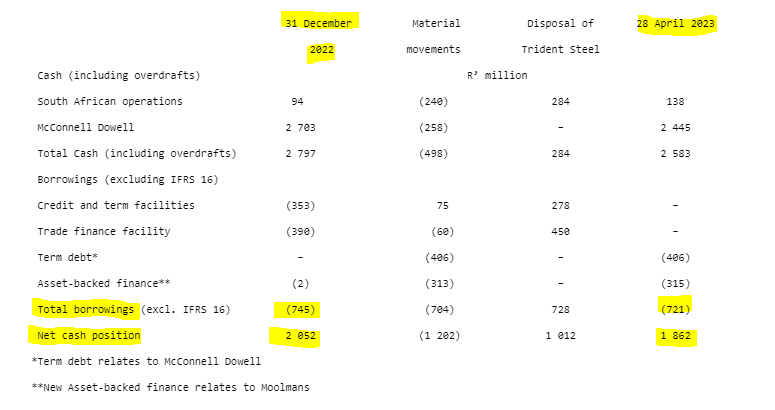

Aveng banks the Trident Steel disposal (JSE: AEG)

There’s no feeling quite like money in the bank, right?

It’s one thing to agree to a transaction. It’s quite another to open up the online banking platform and see cold, hard cash in the account. This is especially true when the inflow is over R1.2 billion!

Aveng’s disposal of Trident Steel was a “locked box” deal based on the 30 June 2022 balance sheet. This means that the balance sheet is frozen in time for purposes of the deal value. The alternative is to work with a post-completion adjustment, which adjusts the purchase price for the state of the balance sheet when the asset finally changes hands.

This was perhaps a “semi-locked box” if such a thing exists, as there are working capital adjustments that applied. There was also a “ticking fee” which is an interesting thing that is a sign of the times in terms of the cost of funding. This fee increases the selling price based on how long it takes the deal to complete.

With all said and done, Aveng has received just over R1.22 billion. R700 million was the actual purchase price, R264 million was net cash retained by Aveng, R75 million was the ticking fee and R183 million was the return of additional liquidity that was previously provided to the business to fund growth.

Be careful here, as some of this cash was obviously already inside the Aveng group. It’s not as though a fresh inflow of R1.22 billion took place at group level. This was the total amount received by the Aveng group holding company, with a smaller (but still very important) amount received on a net group basis.

You should also take note that Aveng has provided a loan of R210 million to facilitate a 30% subscription in the equity of the business that is reserved for B-BBEE participation. Remember, R700 million was the actual purchase price, hence 30% is R210 million. Interest is payable on the loan of 17%, which is a much better return than Aveng has historically achieved for shareholders!

The intention is to find a B-BBEE party who can come into the deal and take Aveng out within 12 months.

Aveng’s share price closed over 5% higher as the market celebrated the news that Aveng no longer has any legacy South African debt. At one point, it peaked at R3.3 billion! It certainly hasn’t been all good news lately, as the McConnell Dowell subsidiary in Australia has had to increase its debt to R406 million in respect to a project guarantee call. That debt is expected to be settled in full by June 2024.

It’s a complicated story, so I’ve included this table from the announcement with my highlights on it to guide you:

In one pocket and out the other, basically.

Calgro M3 puts out a strong trading statement (JSE: CGR)

The market liked it, closing 7% higher on the day

For the financial year ended February 2023, Calgro M3 delivered a strong performance across both its divisions and it shows in the numbers. HEPS will be between 147.90 cents and 158.46 cents, reflecting growth of between 40% and 50%. With the share price having closed at R3.00 on the day, it trades on a P/E multiple of roughly 2x!

It’s going to take time for Calgro M3 to trade at a higher multiple, as investors have been burnt before by erratic earnings. For value investors who love digging into stocks at low multiples, this surely has to be on the research list.

This is especially true when the construction and handover of properties was in line with expectations in 2023, with the company talking about “sustainable returns” in the year to come. Another useful update is that a new burial product has been introduced in the Memorial Parks business, with more success than the previous efforts. The Memorial Parks segment delivered its best final quarter to date.

The company also managed to effect a major share repurchase on a single day, with shares worth R15.4 million repurchased at R2.20 per share. This was through the JSE order book, so the seller wasn’t aware (in theory at least) that Calgro was on the bid. In practice, brokers sometimes do some work behind the scenes to get the trades away for their respective clients.

This repurchase represents 4.99% of issued share capital at the time that the general authority for a repurchase was granted. Up to another 10.73% of shares may be repurchased under the existing authority, which is valid until the next AGM.

That seller must be mildly irritated about the share price movement since that sale, though I would caution that the bid-offer spread can be horrific in illiquid stocks, especially when trying to sell a significant volume of shares.

CMH is still purring like a V8 (JSE: CMH)

For how long can this continue?

CMH has been one of the unlikeliest winners of the aftermath of the pandemic. At a time when people lost their jobs or took pay cuts after companies dug into reserves to survive the worst lockdowns, CMH has somehow been finding a way to make an absolute fortune. This is despite consumers paying far more for petrol and food.

I understand that supply chain constraints were rather useful in boosting car prices, but a chart like this is just ridiculous:

At revenue level, the sale of vehicles is still the bulk of the business, contributing 92% of revenue. Car hire made a huge comeback in the past financial year, with revenue up 82%. Thanks to economies of scale in that business as it bounced back, car hire profits more than doubled from R116 million to R269 million.

This is where we get to the most interesting thing about CMH. Because of the vast difference in segmental margins, car hire may only contribute 7% of revenue but it also contributes 43% of profit before tax!

A recovery in tourism helps the car rental business. The ongoing collapse of Uber in South Africa certainly helps too, with no shortage of complaints on Twitter about how erratic the service has become. Still, I am amazed that car sales are holding up like this, as I expected that side of the business to suffer.

After a couple more interest rate hikes, we will surely see a slowdown in performance.

The dividend declared per share has increased by only 6.7%, despite the company choosing to focus on dividends paid this year (a timing thing) which was 67% higher. Nothing like a factor of 10x difference when trying to drive a particular narrative, right?

With HEPS up 23.2% and the dividend declared up by 6.7%, management is getting tighter with cash. I would be doing the same if I was in their position.

MTN Uganda releases quarterly results (JSE: MTN)

The results of the African subsidiaries are always worth reviewing

MTN Uganda is nowhere near as important as MTN Nigeria that I covered a few days ago, but it’s still worth looking at the underlying numbers.

For the quarter ended March, revenue grew strongly across all the major lines: service revenue +15.8%, data revenue +25.7% and fintech revenue +20.7%. In contrast to what we’ve seen elsewhere in telecoms, EBITDA margin actually expanded by 40 basis points to 52.0%.

Capital expenditure fell by 16.3%, driving a huge drop in capex intensity (capex divided by revenue) of 600 basis points to 15.2%. This is now within MTN Uganda’s target range, so the base period was simply an outsized capex number. That bodes well for free cash flow generation, although capex intensity is expected to rise over the medium-term as investment is accelerated.

Rebosis shows the value of a working email address (JSE: REA)

No, really. It helps when people can contact you.

Rebosis is in business rescue and “rescuing” a property fund isn’t exactly rocket science. There are buildings and there is debt against them. The only way to try and save any kind of equity for shareholders is to try and sell off the portfolio at maximum prices and settle the debt. If there’s a sliver of value left after that, shareholders would get something.

To achieve this, you need a slick sales process. It didn’t get off to a great start, with a truly embarrassing announcement in April that the email address for prospective buyers to register their interest didn’t work for a couple of days. Thankfully, it seems as though buyers had enough perseverance to resubmit their interest, as a “number of participants” have been given access to the virtual data room. Site visits will also be made possible for qualifying potential buyers.

As for the identify of the buyers, this is of course a secret. The fund has indicated that “several listed and unlisted retail-focused property groups” have indicated interest in properties in the fund. That’s no surprise, as Rebosis is a desperate seller and every buyer loves a desperate seller.

Little Bites:

Director dealings:

GMB Liquidity Corporation is happily mopping up further shares in Grand Parade Investments (JSE: GPL), with several trades worth over R1.75 million in total.

An associate of a director of Astoria (JSE: ARA) has bought shares worth R1.06 million.

A number of Brimstone (JSE: BRN) directors have cashed in on a specific repurchase of N ordinary shares by the company that were granted as part of a forfeitable share plan. This looks to me like a liquidity mechanism for management to sell shares at the 30-day VWAP.

It sounds like a small change, but Tsogo Sun Gaming Limited (JSE: TSG) is looking to change its name to Tsogo Sun Limited. In case you aren’t concentrating, the drop of “gaming” from the name signifies the diversified holdings in various entertainment offerings. Well, that’s according to the company at least. I suspect that is says more about the future strategy than the current portfolio.

In case you’re following the progress of Castleview Property Fund (JSE: CVW) as essentially a listed shell for a much larger transaction, you’ll be interested to know that shares worth nearly R270 million have been issued to the subscribers under a specific issue of cash at R6.48 per share. A further R40 million in shares is expected to be issued in July 2023.

The new CFO of Accelerate Property Fund (JSE: APF) has been announced. Marelise de Lange has prior experience as CFO of Texton Property Fund, Rebosis Property Fund and Delta Property Fund. I guess that’s an interesting path, if nothing else. The most recent role was as CFO of Delta, so that fund is now looking for a new CFO.

Anglo American looks to raise 10 year USD debt (JSE: AGL)

Here’s your latest data point on the USD yield curve

I find major debt raises very interesting, particularly at the moment when the yield curve is all over the place. The latest example is Anglo American and its intention to raise $900 million in senior notes due in 2033. In other words, this is highly secured funding (from the perspective of the lenders) that Anglo will be able to use for a period of 10 years.

The company is offering to pay 5.5% on these notes, though what usually happens is that pricing is discovered through a bidding process and the final rate is sometimes adjusted. The mechanism to do this is to issue the notes at a discount or premium, depending on where the pricing ended up vs. the 5.5% coupon.

Time will tell whether there is sufficient appetite at Anglo’s intended price.

Choppies clarifies its position (JSE: CHP)

The company has reminded shareholders that it doesn’t own Choppies South Africa

Choppies is upset about an article in the Financial Mail that the company believes made it sound like the listed group could be in discussions with potential acquirers.

The point that the company has clarified is that Choppies South Africa was sold by the group more than three years ago. The new owner was only allowed to use the name for three years, a period that has already expired obviously.

In other words, any speculation related to Choppies South Africa has nothing to do with the listed company.

Ellies needs to be patient for Bundu (JSE: ELI)

The fulfilment date for conditions precedent has been extended

Fun fact: deals take a long time to close. They usually take longer than people expect, which is a great source of annoyance for everyone involved, especially those who are waiting to be paid a success fee. Yes, I speak from experience here!

The latest example is the Ellies acquisition of Bundu Power for up to R202.6 million, a significant deal for Ellies that has come at a premium valuation multiple. Ellies is rather desperate to evolve its business and Bundu Power has found itself in the right darkness at the right time, with Eskom doing wonderful things for the shareholders of that business.

There’s been quite a delay in the implementation of the deal, although no details are given on the source of the delay. The original date for fulfilment of conditions precedent was 30 April 2023, which has clearly come and gone. This has been extended to 31 August 2023.

A windfall for Gold Fields (JSE: GFI)

The company announced a new partnership in Canada

Before getting into the details of this story, I just have to point out this chart and how ridiculous the volatility actually is when it comes to gold miners:

Gold might be a source of returns that aren’t correlated with the rest of the market, but there is absolutely nothing steady about them. The recent chart looks like Zoom in the pandemic!

The latest news from Gold Fields is a partnership with Osisko Mining to develop and mine the Windfall project in Canada. Let’s hope that the name is a sign of things to come, as the investment for a 50% stake is C$600 million and that’s before any of the capital expenditure related to the project.

There are also a couple of exploration projects as part of this deal, with Gold Fields committing to fund the first C$75 million worth of development expenditure on them before the 50-50 split kicks in for remaining expenses.

The Windfall project has a life-of-mine of 10 years (which Gold Fields thinks is conservative) and an all-in sustaining cost (AISC) of $758/oz, which would make it one of the lowest cost mines in the portfolio.

And let’s face it: Canada is a low-risk jurisdiction in which to mine gold, which certainly doesn’t hurt the story.

First production from this asset is expected in 2025.

Impala Platinum’s production is under pressure (JSE: IMP)

We now have data for the nine months to March

Impala Platinum sources its production in various ways, ranging from managed volumes through to joint ventures. When all of that rolls up to the top, total 6E group production volumes fell by 9% for the nine months and sales volumes were 5% lower.

The blame has been laid squarely at the door of “load curtailment” which appears to be the mining industry’s way of describing Eskom’s ongoing failure to do anything useful for South Africa.

Things are tough at the moment for Implats. Full year production is likely to be at the lower end of guidance and unit costs are expected to be at the top end of provided guidance. And against this backdrop, the company is still trying to get the Royal Bafokeng Platinum deal across the line!

Kibo Energy releases interesting test results (JSE: KBO)

Could biofuel be a realistic alternative to conventional coal?

Kibo Energy is hoping to supply solid biofuel as an alternative to conventional coal, targeting international companies in the manufacturing industry.

The company has put its biofuel through testing by accredited laboratories and results are encouraging, with the selected biomass even outperforming conventional coal on some metrics.

After all the manure we’ve dealt with from Eskom, imagine a world where it runs on the stuff? Just kidding – I don’t think that Kibo’s biofuel is made from manure. I stand behind the rest of the sentence, though.

Renergen releases its annual report (JSE: REN)

This is a good opportunity to recap the key points about the company

At this stage, the revenue number in Renergen is a little pointless. Although the company is now selling liquefied natural gas (LNG), revenue of R12.7 million for the year is absolutely insignificant in the context of the Virginia project’s long-term story around helium in particular.

There were a major of key strategic developments in the past financial year, ranging from the successful equity due diligence by the Central Energy Fund through to credit due diligence by the US International Development Finance Corporation and Standard Bank.

I must pause there to point out the importance of the US relationship to Renergen at a time when our government is cozying up to Russia far more than the West. You simply cannot ignore the impact and risks of geopolitics. Renergen is looking to raise capital on the Nasdaq, so there are equity and debt capital raises underway with US counterparts. Critically, a significant source of future demand is the US, particularly given the initiatives in that country to onshore semiconductor (computer chip) production in response to risks around China and Taiwan.

Like I said, you cannot ignore geopolitics with something as strategically important as helium. Risks in Taiwan will drive demand from the US, provided we don’t sour our relations with the West.

As the company works towards commercial operation of the all-important Phase 2 project by 2026, there will be no shortage of volatility. If you want to gain a better understanding of the investment story, my Ghost Stories podcast with CEO Stefano Marani from February 2023 will be useful:

Take note that it was recorded before the details of the IPO were announced. Renergen is looking to raise $150 million during 2023 and doesn’t envisage needing more equity capital for the year after the IPO.

Textainer Group: watch the trend (JSE: TXT)

This is as cyclical a business as you’ll find

In the shipping business (and the related container business that Textainer is in), you need to constantly keep an eye on the numbers. This is the furthest thing from a buy-and-hold industry, as shipping is incredibly cyclical. We’ve seen Grindrod Shipping selling ships to pay down debt and we can now see revenue falling off its peaks at Textainer.

The biggest difference is actually the gain on sale of containers, which was significantly lower in this quarter than in prior quarters. Income from operations was just over $100 million in this period vs. $114 million in the comparable quarter last year. Net income attributable to common shareholders was $53.6 million vs. $72.7 million.

Average fleet utilisation has dropped to 98.8% from 99.7% a year ago.

Against headline earnings of $1.22 per share, the board has declared a dividend of $0.30 per share.

Little Bites:

Director dealings:

Des de Beer has bought R4.85 million worth of shares in Lighthouse Properties (JSE: LTE).

An associate of a director of Rex Trueform (JSE: RTN) has bought N shares worth R214k. N shares in African and Overseas Enterprises (JSE: AON) – part of the same overall group – were also bought with a value of R152k.

A non-executive director of Capitec (JSE: CPI) has entered into a huge hedging trade over shares worth R1.46 billion. The put strike price is R1,461 and the call strike is R2,517 per share. The average expiry date on the derivatives is just over 3 years.

If you are a shareholder in Absa (JSE: ABG), then you will be interested to know that the circular related to the B-BBEE transaction has been posted. I still think this was a huge missed opportunity to give retail investors another structure to invest in on the market.

The delisting of Jasco Electronics (JSE: JSC) is taking longer than planned because of delays in obtaining a compliance certificate from the Takeover Regulation Panel.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

This year, Unlock the Stock is delivered to you in proud association with A2X, a stock exchange playing an integral part in the progression of the South African marketplace. To find out more, visit the A2X website.

In this eighteenth edition of Unlock the Stock, TWK Investments returned to the platform to talk through a tough recent financial period, with particular focus on the long-term prospects of the company.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions. Watch the recording here:

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Glencore’s dealmaking prowess, with the Teck Resources board pressured into giving the company a chance and Glencore executing an unrelated deal in Brazil for aluminium and bauxite assets for good measure.

Anglo American’s recent production update and the importance of the Quellaveco asset, along with the year-on-year declines in commodity prices in dollars.

Sibanye-Stillwater’s Keliber project in Finland and the support from the Finnish government in the form of out outsized equity investment in the project.

Smart dealmaking from Capital Appreciation in the acquisition of Dariel Solutions, with a deal structure and valuation that seems to make a lot of sense.

MTN’s quarterly results in Nigeria, showing the importance of reading ALL the way down the income statement.

The Prosus share buyback programme and the ongoing sale of shares in Tencent.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

Glencore is proof that perseverance can work (JSE: GLN)

To the dismay of Teck’s board, its shareholders are taking notice of Glencore

I suspect that “Glencore” is a swearword in the average household of a Teck Resources board member in Canada. After initially approaching the board and then improving its proposal, Glencore suffered a double rejection that led to a letter being released to Teck Resources shareholders.

It seems to have landed, because Teck decided to withdraw its separation proposal. In other words, the Teck board has realised that the Glencore proposal isn’t going to just disappear and that shareholders deserve a chance to consider it. Even if the board won’t take the offer to shareholders with its blessing, Glencore has said more than once that it is willing to make the offer directly to shareholders. This would be a textbook example of an attempted hostile takeover.

Even with all of this going on with Teck, Glencore isn’t sitting on its hands. On the aluminium side of the business, Glencore is agreed to acquire a 30% stake in Alunorte S.A. and a 45% stake in Mineracão Rio do Norte S.A. (MRN) with the counterparty to both deals being Norsk Hydro ASA.

The combined value of those deals is $775 million and the effective date is 30 June 2023. Due to various adjustments that are expected to be made to the price, the expected payment is $700 million.

Alunorte is the world’s largest alumina refinery outside of China, located in Brazil. MRN is an open case bauxite mine located in Brazil. Bauxite is the main ore of aluminium and Alunorte is one of the biggest customers for MRN’s bauxite.

This is another reminder of what a force of nature Glencore actually is. With a market cap of around R1.35 trillion, this is a huge commodity platform business that can pull a few levers and make huge steps in exposure to so-called “transition metals” – with the Teck deal as a particularly large attempt in that space.

Industrials REIT remains defensive (JSE: MLI)

The update for the fourth quarter reflects a healthy business

If you’ve been regularly reading your Ghost Bites, you’ll know that Industrials REIT is currently under offer from Blackstone. This will need to go through a shareholder approval process, along with an extensive regulatory process for a deal of this size.

In the meantime, the company has to stay up to date with reporting requirements. This also helps investors make an informed decision about the offer.

In the fourth quarter of the 2023 financial year (covering the three months to March 2023), the company gave a mix of quarterly and annual numbers for investors to chew on. For example, Industrials REIT achieved 4.8% like-for-like growth in passing rents and 10.6% growth in estimated rental values over the full financial year.

And in this quarter specifically, there was an average uplift in rent of 27% on all lettings signed during the quarter. The supply-demand dynamics remain favourable in this property sector, allowing the company to achieve substantial increases in rent when leases come up for renewal. Through its Industrials Hive platform, the company is focused on having relationships directly with tenants by showcasing its available properties through an in-house web platform.

The sale of the care homes joint venture in Germany was completed in April, so the portfolio is now purely focused on multi-let industrial units. This is part of why it fits so neatly into a portfolio run by the likes of Blackstone.

The loan-to-value (LTV) ratio was 29% on 31 March 2023. The average cost of debt is 2.8% and average maturity is 3.2 years, with loan extensions that could take that to 4.4 years.

MC Mining had a mixed quarter (JSE: MCZ)

Production at Uitkomst was sharply down year-on-year, but exports are here

With “challenging geological conditions” in addition to localised flooding and of course load shedding, MC Mining suffered an 18% drop in production at Uitkomst Colliery, measured on a year-on-year basis. Sales were higher though, with the particularly good news being that a big portion of domestic sales has now been rerouted to export sales after management initiatives in that space.

The company is also busy with the Makhado hard coking coal project, with a detailed implementation plan having been formulated and put into action for the first five years of mining and processing operations.

At the outsourced Vele Aluwani Colliery which was recommissioned in December 2022, mining and processing of coal ramped up and 48,518 tonnes of thermal coal was delivered during the quarter. For context, Uitkomst produced 101,616 tonnes this quarter.

The company had cash of $14.1 million at the end of the quarter vs. $20.2 million at the end of December.

MTN Nigeria and Ghana release results (JSE: MTN)

If you are invested in MTN, you need to follow the subsidiaries in Africa

I always enjoy the release of results by MTN’s African subsidiaries. They tell us so much about business in Africa in general – a high growth region that is fraught with currency risk. Companies that can grow in-country with internally generated cash flows (like MTN) can make it work. Those that are trying to bring the cash home to deal with South African debt are in trouble (like Nampak).

Starting with Nigeria, the data story continues with active data users up by 14.7% vs. mobile subscribers up by 9.4%. Active mobile money wallets grew from 2 million to 3.2 million!

Some margin pressure is coming through, with service revenue up by 20.5% and EBITDA up by 17.7%. EBITDA margin fell by 130 basis points to 53.3% – still a huge number.

The story deteriorates thereafter, with profit before tax up by just 8.5% and earnings per share by 3.8%. Why is this the case? The clue lies in the EBITDA acronym – Earnings Before Interest, Taxes, Depreciation and Amortisation.

Depreciation and amortisation increased by 23.4%, a function of MTN’s significant capex investments in the country. Net finance costs are a bigger issue, up by a whopping 42.2% with inflation in Nigeria at a 17-year high and the Monetary Policy Rate in the country up to 18%.

At first blush, it seems as though MTN is cutting back on investment, with capex down by 25.8%, or down by 47.8% excluding right-of-use assets. Accounting weirdness aside, the insight here is that capex has slowed down considerably. If you read through the details of the announcement, you’ll find commentary around a high base for capex and supply chain challenges in this quarter that impacted the capex growth rate. They expect a “ramp-up” in capex during the rest of the year, so it wouldn’t be correct to say that MTN is slowing down on investment in Nigeria. With net debt to EBITDA of 0.2x, there’s still plenty of financial headroom even if finance costs are showing a worrying trajectory.

I would love to give you the details on Ghana but the MTN Ghana investor relations website was down when I tried to access it. I’ll check back in this week to see what I can find.

Reinet gives us a clue about its NAV move (JSE: RNI)

Reinet Fund’s NAV move is a precursor to Reinet Investments

Reinet is an investment holding company that primarily holds shares in Pension Insurance Corporation and British American Tobacco. That’s a defensive portfolio of note.

Like all investment holding companies, the key metric is Net Asset Value (NAV) per share. Before the listed company releases its NAV update, Reinet announces the quarterly NAV of the Reinet Fund, the vehicle through which the investments are held.

These NAVs aren’t exactly the same, as there are balance sheet items at Reinet Investments level that you won’t find in Reinet Fund. It does give a very strong clue as to the percentage movement in the NAV though.

At Reinet Fund level, the NAV has decreased by around 1.3% from December 2022 to March 2023.

Sasol raises more US dollar funding (JSE: SOL)

Sasol is attractive to global lenders and fixed income investors

One should never assume that a successful debt raise is an indication of returns coming the way of equity investors. The metrics involved are completely different, as fixed income is all about debt affordability and equity is all about growth. Still, it’s never a bad thing when a company is appealing to debt providers.

Sasol has raised $1 billion through the issuance of notes (debt instruments) that mature in 2029. The rate is 8.75% per annum, so that gives you an idea of where the dollar yield curve is and the kind of risk premium that Sasol needs to offer.

The orderbook reached over $2.3 billion, so this raise was 2.3x oversubscribed.

Together with the recent extension of its dollar loan maturity, Sasol has full pre-funded the March 2024 bond maturity.

Southern Palladium signs off on a busy quarter (JSE: SDL)

Drilling, drilling and more drilling

Southern Palladium is firmly in drilling and exploration mode. You need to be a geologist to really understand the updates on SENS, so I usually just look for commentary from management around whether the drilling results are in line with expectations or not.

Having done wider drilling in this quarter to figure out which of the four potential development scenarios is the most favourable, the next quarter will be about narrower infill drilling to increase confidence levels from Inferred to Indicated.

As at the end of March, the company held $12.93 million in cash vs. $14.20 million at the end of December 2022.

Little Bites:

Director dealings:

A non-executive director of Hammerson (JSE: HMN) has acquired shares worth £8.9k.

An associate of a director of Ascendis Health (JSE: ASC) has bought shares worth nearly R92k.

African Rainbow Minerals (JSE: ARI) has announced that CEO Mike Schmidt has stepped down after 11 years in the job. He will stay on as Executive of Growth and Strategic Development. The current COO, Phillip Tobias, has been appointed as CEO with effect from 1 May 2023. It’s always good to see internal appointments like this.

The AB InBev (JSE: ANH) dividend has been approved by shareholders. A dividend of €0.75 will be paid to holders on the JSE register on 5th May.

If you are a shareholder in Kibo Energy (JSE: KBO), you’ll be interested to know that subsidiary Mast Energy Developments has released its annual report. Recent activities have focused on the Pyebridge project site, the construction and development of the Bordesley project and the acquisition of two reserve power projects.

In this episode of Ghost Stories, Nico Katzke (Head of Portfolio Solutions at Satrix) returns to the platform for another fantastic discussion on a variety of finance topics, with the key theme being offshore vs. local investment.

With all the stresses that we face every day as South Africans, does it make sense to take money offshore at any cost and at any valuation? Or is there value to be found in the rand and on the local market?

We covered topics including:

Why local vs. offshore is such an important (and emotive) topic for South Africans.

Has the rand really been as bad as people think?

The extent of offshore exposure that can already be obtained through investing on the JSE.

The attractiveness of local yields.

The importance of valuation in any assessment, as things aren’t usually as good or as bad as they seem.

The recovery of China and the impact this has on local commodity players and luxury businesses.

Is “home bias” an issue for South Africans, or do we ironically suffer from the reverse?

The volatility paradox and how rand volatility interacts with volatility of other asset classes in investment funds.

The value of letting data drive our decisions.

For more from the Satrix – Ghost Mail partnership, visit this link to find various podcasts and articles.

Grindrod Shipping reduces debt through ship sales (JSE: GSH)

In such a cyclical industry, timing is everything

With things having slowed down in the shipping industry and interest rates on the rise, it made sense for Grindrod Shipping to sell off some ships and reduce debt with the net proceeds.

There were four such sales in March and April, with total net proceeds of $26.6 million. The cash was used to reduce senior secured debt in the group.

Kibo Energy is a good example of dilution in action (JSE: KBO)

Always look out for convertible instruments

When a company has issued warrants or convertible debt, there is risk of dilution for ordinary shareholders.

A warrant is just a type of option, allowing the holder to exercise the right to receive shares directly from the company (i.e. new shares) for a pre-determined price. Warrants can be used as part of start-up capital raising to create an equity kicker for early-stage investors to get them across the line.

A convertible loan does what it says on the tin: this is a debt instrument that can be converted into equity (shares) at the option of the holder.

The latest announcement dealing with equity conversions is a reminder that Kibo has dilutive structures in place, something that investors should be aware of when investing.

Kore Potash quarterly review (JSE: KP2)

This is a useful summary of progress at the Kola Project

The focus is still on finalising the terms of the Engineering, Procurement and Construction (EPC) contract. Kore Potash’s counterparties to this contract are PowerChina and SEPCO, who are working on guarantees to support the EPC contract.

Importantly, Summit Consortium has confirmed that the financing proposal for Kola will be provided within six weeks of the EPC terms.

As at 31 March, the company had $3.8 million in cash.

Life Healthcare: enough volatility to send you to the ER (JSE: LHC)

Here’s a lesson in investing in “safe” assets, like hospital groups

Life Healthcare is currently weighing up its options to sell its offshore business, Alliance Medical Group. Unsolicited proposals were received that the board can’t ignore, driving a need to engage with the potential offerors.

The company has renewed its cautionary announcement in this regard. Caution indeed, as just a cursory glance at this share price chart will reveal:

Fully licensed and shovel ready (JSE: MCZ)

MC Mining updated the market on the Makhado project

In MC Mining’s case, the shovels would be building the project rather than taking hard coking coal out of the ground. The good news is that an estimated 650 permanent jobs are expected to be created at full production. A detailed execution plan for the next five years has been put together based on the bankable feasibility study for Makhado and a great deal of subsequent work.

Various tender processes for contractors are underway and are expected to be concluded in the third quarter. Funding arrangements are expected to be concluded at around the same time.

It’s a long process, even once a project is “fully licensed and shovel ready” as the company puts it.

Orion Minerals reflects on the past quarter (JSE: ORN)

Copper and zinc prices are volatile as always, but the outlook remains strong

So-called “junior” mining companies are risky things. While they are running around trying to piece together funding for projects, metal prices can change and so can sentiment. It helps when there is a solid long-term story, as is the case with a metal like copper.

The past quarter was critical for Orion, with Clover Alloys coming in as the cornerstone equity investor. Together with other equity investors, this puts the company in a position to access the Triple Flag Precious Metals ($87 million) and IDC facilities (R250 million).

Scalable dewatering of the underground operations is set to start this quarter.

Renergen’s trading statement isn’t important (JSE: REN)

The share price isn’t being driven by current financial results

With Renergen having been firmly in development phase, the current financial results don’t tell you much about the long-term prospects or what the share price should be doing.

Still, I should mention that a trading statement has indicated a headline loss per share of between -22.6 cents and -17.1 cents for the year ended February 2023. That’s an improvement on the prior year of between 18% and 38%.

The royal saga continues (JSE: RBP | JSE: IMP)

Although Northam Platinum pulled its offer, the TRP complaints are unresolved

I’m tired of reading about this deal, so I can only imagine how tired those involved are. The management team at Royal Bafokeng Platinum is particularly gatvol, with the company having been under offer for over 18 months. Operating in a tough environment with that level of uncertainty really isn’t easy, something we are starting to see in the numbers.

Northam Platinum is no longer interested in making an offer to shareholders. This doesn’t mean that the saga is over, as a Takeover Regulation Panel (TRP) Compliance Certificate cannot be issued until complaints are resolved. A couple of complaints are causing major headaches, with the company trying to resolve them.

For example, there is a fight underway around the accelerated vesting and issuance of shares to the CEO and COO who announced their retirements. They were then given contracts to stick around until the corporate action is concluded. Northam Platinum believes that this is a “frustrating action” under Takeover Law and the matter has gone as far as the High Court. The problem is that the High Court process has the potential to really drag on, which would then delay the issuance of a compliance certificate by the TRP. Royal Bafokeng is considering other steps that would resolve this matter.

There were other issues as well. Northam Platinum made a complaint about the independence of the Royal Bafokeng directors, with that complaint dismissed by the TRP and then the Takeover Special Committee (TSC) in the appeal process. There were also concerns around the level of disclosure by the valuation independent expert in terms of valuation ranges. This was subsequently resolved, although the ranges are now so out of date that they are actually pointless.

Meanwhile, Impala Platinum has extended the longstop date to 31 May. The language in that company’s announcement is starting to sound very frustrated and impatient.

Somehow, I don’t think that Northam Platinum is on the Christmas card list for either Implats or Royal Bafokeng.

Steinhoff: worthless, but willing to share (JSE: SNH)

The speculative punts on this share price continue

Steinhoff closed 20.8% higher on Wednesday. You may be mistaken for thinking that there’s a good reason for this.

Instead, there’s just the usual activity in this share price of speculators playing a game of musical chairs. When the music stops, those who didn’t get out with a profit will be left as the proud owners of unlisted instruments in a worthless company.

In case you think that this is just me being painful about Steinhoff, here’s the company literally telling you that there is no value:

In simple terms, the company is worthless and hence creditors didn’t mind making space for shareholders to receive 20% of nothing. Ask yourself this: if there was any value here at all, why would creditors give some of it up after shareholders voted against the restructuring plan?

Little Bites:

As part of significant changes to its board, Grand Parade Investments (JSE: GPL) has also announced the appointment of a new chairman.

Heriot Investments and related parties (including Heriot REIT – JSE: HET) now hold 56.8% of the shares in Safari Investments (JSE: SAR).

The CFO of AECI (JSE: AFE) has resigned for personal reasons. An internal promotion has been made on an interim basis.

The delisting of Jasco Electronics (JSE: JSC) was approved almost unanimously by shareholders at a general meeting.

Oando PLC (JSE: OAO) looks set for an offer and delisting process. In case you’re interested, the company released a very long announcement about taking delivery of electric buses (a perfect example of SENS being used as a public relations platform) and also released financials for the year ended December 2021, so it has nearly caught up.

Efora Energy (JSE: EEL) has been suspended for a long time. The company seems to be making some progress in addressing the backlog of financial reporting, but there’s still a long way to go in finishing audits etc.

Capital Appreciation has acquired 100% of Dariel Solutions, the holding company of Dariel Software. The R131,2 million purchase price will be settled through cash (R85,3m) and Capital Appreciation shares (25,243,779 shares at R1,52 each, totalling R38,4m).

Unlisted Companies

The UK’s Card Factory, has acquired 100% of SA Greetings Corporation for £2,5m in cash. SA Greetings is a wholesaler of greeting cards and gift packaging. It operates 24 “Cardies” stores and owns a roll-wrap production facility.

Convergence Partners has acquired a stake in 42Markets, a financial and capital markets fintech investment group, for US$10 million. The investment was made through the recently closed, US$296 million, Convergence Partners Digital Infrastructure Fund. The capital will be used to speed up the development and expansion of its portfolio companies (Mesh, Andile and FXFlow).

Consumer rewards app, Maholla, has raised US$1,5 million in seed funding. Investors include the Buffet Group, Castleton Capital, Praesidium Capital Management and Galloprovincialis. Moholla’s app rewards users for scanning any receipt from any store. It then links the retail-agnostic shopping data to the consumer and provides a real-time understanding of what consumers are purchasing in SA.

The PBT special dividend of 75 cents per share (a total gross distribution of R156,9 million) has been approved and will be paid on 15 May.

Distell and Heineken have announced that all the scheme conditions have been completed and Distell will delist from the JSE on 28 April.

Kibo Energy issued a total of 794,893,911 new shares following a warrant conversion and convertible note conversion. 284,524,625 shares were issued for the warrants and 510,369,286 shares issued for the convertible loan note conversion.

The Jasco Electronics shareholders have approved the delisting resolution and the offer has become unconditional. The finalisation date announcement is expected to be released in early May.

The Kal Group (previously Kaap Agri) will repurchase and delist 247,843 shares following the release of the odd-lot offer results.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 17 to 21 April, a further 2,651,096 Prosus shares were repurchased for an aggregate €185,26 million and a further 566,392 Naspers shares for a total consideration of R1,9 billion.

Two companies issued profit warnings this week: Coronation Fund Managers and Renergen.

Three companies issued or withdrew cautionary notices: Trustco, Life Healthcare and Afristrat Investment.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")