Africa Finance Corporation has closed a US$150 million senior loan to Kamoa Copper to support the expansion of the Kamoa-Kakula Copper Complex in the DRC. Production started in July 2021 at the project which is situated on the western edge of the Central African Copperbelt, and it is currently undergoing a third phase of expansion which includes a 33% increase in production capacity and the construction of a 500,000 tpa copper smelter.

Egyptian fintech Connect Money has raised US$8 million in a seed funding round. Investors included DisrupTech Ventures, Algebra Ventures, Lorax Capital Partners, One Stop Capital and MDP. The funding will be used to expand in the Egyptian market and in other African countries such as Kenya and Morocco.

HostAfrica has acquired Nigerian web design agency Naijawebhost. Financial terms were not disclosed. This is the second acquisition in Nigeria for the South African firm, in 2021, the company acquired DomainKing.

African Export-Import Bank (Afreximbank) is providing Zimbabwe’s CBZ Bank US$80 million in debt through a $60 million line of credit, plus a $20 million Afreximbank Trade Facilitation Programme facility.

Eos Capital, through its Euphrates Agri Fund, has partnered with Africa Venture Partner Projects and Oyeno Poultry Industries to invest in Namibia’s Kadila Poultry Farming. The undisclosed funding will be used to construct a 6-house broiler farm between Windhoek and Okahandja with a capacity to produce 400 tons of poultry meat per month.

Africa Oil Corp and BTG Pactual Oil & Gas have reached agreement to consolidate their shareholding in Prime Oil & Gas Coöperatief (a 50:50 joint venture between the two firms which owns an 8% participating interest in the Chevron operated petroleum mining lease (PML) 52 (Agbami field) and petroleum prospecting license (PPL) 2003 plus a 16% participating interest in the TotalEnergies operated PML 2 (Akpo field), PML 3 (Egina field), PML 4 (Preowei field) and PPL 261). BTG Pactual Holding will be amalgamated into a newly created Africa Oil subsidiary in return for shares in Africa Oil. Upon completion, BTG will own c.35% of Africa Oil.

Gibb River Diamonds has acquired two uranium projects – the Erongo Project and the Kunene Project – which consist of six Exclusive Prospecting Licenses covering 1,828km². Financial terms were undisclosed.

Humanitarian organization, CARE, has announced a strategic partnership and investment in Ugandan fintech, Ensibuuko. Financial terms were not disclosed, but the partnership will see CARE acquire Ensibuuko’s proprietary Chomoka application, a digital solution for savings groups.

Following the December 2023 update, Marula Mining Plc has confirmed that it is seeking to list on the Growth Enterprise Market Segment of the Nairobi Securities Exchange in July 2024 following its recent investment in the Larisoro Manganese Mine located in Samburu County.

Phatisa and Finnfund have exited their investment in Sierra Leone’s Plating Naturals to PaLenDu, an affiliate of the Dutch Dekker Group. No financial terms were disclosed. The duo first invested in the palm oil producer’s predecessor entity (Goldtree) in 2011. At the time, this was a brownfield investment aimed at rebuilding a palm oil mill in Daru which had been destroyed during the civil war. Planting Naturals now owns over 5,500 ha of its own plantations and produces over 7,000 tonnes of sustainable crude palm oil annually.

Carlyle announced the acquisition of a portfolio of gas-weighted exploration and production assets based in Italy, Egypt and Croatia from Energean. The portfolio includes interests in Cassiopea, Italy’s largest gas field in terms of reserves, and Abu Qir, one of the largest gas producing hubs in Egypt. No financial terms were disclosed.

The Fidelity Bank Plc Rights Offer of 3,200,000,000 ordinary shares of 50 kobo each at ₦9.25 per share, opened on Thursday 20 June. The offer is scheduled to close on 29 July.

In times of uncertainty and volatility, when the business landscape is fraught with challenges, and opportunities seem elusive, business owners face a daunting task – navigating through the storm and steering their companies towards stability and growth. Amidst the chaos, getting a business valuation may seem like a low priority, especially if you’re not actively considering selling your business. However, what many business owners fail to realise is that a comprehensive valuation can provide much-needed clarity and insight, serving as a strategic compass to help guide your business through turbulent waters.

In this article, we explore why getting a business valuation is essential, especially in times of uncertainty, and how it can empower you to make informed decisions and chart a course towards resilience and success.

Gaining clarity amidst uncertainty

Knowing where you stand is crucial as a business owner. A business valuation offers a clear, objective assessment of your company’s financial health, performance and potential, cutting through the noise and providing a beacon of clarity amidst the uncertainty. By crunching the numbers and analysing key metrics, a valuation reveals the true value of your business, helping you understand its strengths, weaknesses, and opportunities for improvement.

Mitigating risks and identifying opportunities

Uncertainty often brings with it a host of risks and challenges, from economic downturns to industry disruptions and changing consumer behaviours. A comprehensive valuation helps you to identify and mitigate these risks by highlighting potential vulnerabilities and areas of concern. At the same time, it uncovers hidden opportunities for growth and innovation, enabling you to capitalise on emerging trends and market shifts.

Building resilience and adaptability

In turbulent times, adaptability is key to survival. A business valuation provides valuable insights into your company’s ability to weather storms and adapt to changing circumstances. By understanding your business’s strengths and weaknesses, you can proactively implement strategies to enhance resilience and agility, ensuring that your company remains competitive and sustainable in the face of uncertainty.

Securing stakeholder confidence and trust

Whether it’s investors, lenders or business partners, stakeholders value transparency and reliability. A business valuation demonstrates your commitment to sound financial management and responsible stewardship of resources, instilling confidence and trust among stakeholders. By providing an objective assessment of your company’s value and potential, a valuation enhances your credibility, making it easier to secure financing, attract investors and forge strategic partnerships.

Preparing for the future

Uncertainty is inevitable, but preparation is key to success. A business valuation serves as a strategic tool to prepare your business for the future, enabling you to develop contingency plans, scenario analyses and strategic initiatives that mitigate risks and capitalise on opportunities. By understanding your business’s true worth and potential, you can make informed decisions that position your company for long-term success and sustainability.

Getting a business valuation is not necessarily about preparing for a sale; it’s about equipping yourself with the knowledge, insights and strategies needed to navigate uncertainty and chart a course towards resilience and success.

Andrew Bahlmann is the Chief Executive: Corporate & Advisory | Deal Leaders International.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Webber Wentzel and RBB Economics recently advised on two transactions that featured unprecedented levels of antitrust scrutiny across multiple African countries. The first transaction involved Dutch brewer, Heineken‘s acquisition of a controlling interest in Namibia Breweries, and the flavoured alcoholic beverages, wine and spirits operations of Distell. The second transaction involved Dutch coatings manufacturer, Akzo Nobel (which manufactures the well-known Dulux paint brand) acquiring Japanese coating manufacturer, Kansai Paint’s two African entities, one of which owns the Plascon brand.

Navigating complex regulatory requirements, each merger underwent competition assessment before various competition authorities in over 20 jurisdictions, a process that spanned at least 18 months from the risk assessment phase to litigation. The in-depth scrutiny and rigorous assessments by African competition authorities signal a positive welcome to the modernisation of African antitrust regimes. This mirrors the evolution of European competition law three decades ago, and we anticipate this positive trend to solidify further.

These transactions serve as useful case studies that offer insights into critical procedural and strategic considerations, which are important for businesses to keep in mind for future transactions that require merger filings across Africa.

CONSIDERATIONS FOR NAVIGATING COMPLEX MERGERS ACROSS AFRICA

Early risk assessment

The first step is for a business’ economics and legal team to conduct a preliminary risk assessment as soon as practicable, to identify potential substantive regulatory concerns, as well as to inform and develop a merger clearance strategy. This analysis should include identifying jurisdictions that may raise competition risks, public interest issues (such as job losses), and any potential structural and behavioural remedies.

The order of merger filings

To make informed filing decisions, parties must weigh the economic and commercial importance of the deal in each jurisdiction, the competition authority’s appetite to engage in substantive economic analysis, the complexity and resolution of competition issues, and the likelihood of public interest issues arising. While South Africa remains the likely focal point for the foreseeable future, the Common Market for Eastern and Southern Africa (COMESA) regional competition authority is playing an increasingly crucial role, due to its authority to assess the effects of a merger across 21 countries. Following Webber Wentzel and RBB Economics‘ extensive engagements with COMESA, it was observed that although the COMESA centralised filing process has cost-saving benefits, parties should expect increased complexity in the investigation process that follows. COMESA is adopting an increasingly rigorous approach when assessing the merger parties’ economic arguments and analysis. Allowance also needs to be made for the fact that COMESA has to engage with and secure input from all local authorities within the member states affected by the transaction, making for a lengthy and complex process. Some affected member states are inclined to request that the merger be referred to them. Typically, COMESA denies these requests and seeks to accommodate the concerns on the part of local competition authorities by allowing them to send information requests (while keeping COMESA in copy), and to hold meetings with the merger parties subject to a reporting obligation.

Managing the timing of multi-jurisdictional mergers

Ensuring a smooth timeline for a multi-jurisdictional merger across Africa requires meticulous time management. Firstly, factor in the extended review periods required by each jurisdiction where merger filings are required. Secondly, advisors must dedicate time and effort to collecting and analysing significant volumes of information and data, as well as engaging extensively with multiple stakeholders within the merger parties’ businesses (including the head office and local operations teams) to provide comprehensive and accurate responses to the various information requests from the competition authorities. It is also essential to build timing buffers into one long stop date to allow for unexpected delays, particularly in African countries where comprehensive information and data may not be readily available from the merger parties’ local operations.

Address any potentially negative optics/preconceptions upfront

Competition authorities are highly sceptical of transactions that involve well-known brands that appear to create or strengthen structural presumptions of market power. Early engagements with authorities can assist to: (i) shift the debate towards substantive rather than ostensible issues; (ii) establish the authority‘s appetite for more objective economic analysis; and (iii) ascertain the need for a remedy if these presumptions seem insurmountable.

Build a strong merger rationale

At the outset, merger parties should develop and test a coherent and consistent strategic justification for the proposed transaction. It is advisable to involve the advisory team in conceptualising and testing the transaction rationale. In Webber Wentzel and RBB Economics‘ experience, a poorly articulated strategic justification (or no genuine justification at all) can unhelpfully detract from the substance of a case.

Have the right team to co-ordinate the various overlapping processes

Mergers spanning multiple African countries create a complex web of overlapping filing deadlines. This requires an advisory team with the depth of experience and size to prepare simultaneous submissions. The team must be prepared to meet specified deadlines and attend in-person meetings, site visits and public hearings across several jurisdictions.

Ensure consistency in merger filings

Competition authorities in Africa don’t operate in silos; they share information and reference each others justifications and decisions for guidance when evaluating mergers. This collaboration has several implications, but most importantly, it means that submissions across jurisdictions must be consistent in their content and underlying data. This ensures a clear and unified picture for the competition authorities involved. Among these regulators, COMESA and the South African, Namibian and Botswanan Commissions, in particular, are known for their active information exchange (while adhering to confidentiality restrictions).

Increasing levels of scrutiny from competition authorities

African mergers are being confronted by an ever-increasing level of scrutiny, necessitating a well-developed response strategy. Beyond the initial submissions, competition authorities are also increasingly inclined to conduct in-depth assessments and investigate complex theories of harm. This includes non-horizontal theories of harm initiated by third parties, such as customers and intervenors. Furthermore, authorities are no longer prepared to rely only on information provided by merging firms and will look to corroborate or refute these with evidence from third parties (or desktop research).

Public interest is becoming more relevant

African competition authorities are following in the footsteps of South African precedent. They are seeking to negotiate public interest commitments (such as moratoriums on job losses and requiring local procurement and supply commitments). Unfortunately, this is the case even when they are dealing with mergers with very limited competition concerns. It is helpful to consider, well in advance, how you plan to address anticipated requests for public interest commitments. It should also be borne in mind that conceding to proposals in one country might invite requests for similar remedies in other countries, which can become costly and difficult to implement.

Remedy design should align with the economic evidence

When designing a remedy, it is vital to consider its substance, implementation, commercial feasibility, and flexibility across jurisdictions. Remedies in multi-jurisdictional transactions may have a geographical component because of the businesses’ cross-border operations and the market definition adopted in the filing (e.g. regional markets may require regional remedies). Furthermore, African competition authorities are becoming increasingly aware of how a remedy in one country affects another, and they might adjust your proposed remedies accordingly.

While Africa continues to offer attractive commercial opportunities, if regulatory approvals are required to realise these opportunities, it is important to heed the necessary procedural and strategic considerations. Securing and retaining legal advisors with experience in multi-jurisdictional African filings from the very beginning is crucial. Their expertise can streamline the efficiency of the approval processes. Furthermore, securing legal advisors at an early stage also ensures that your internal strategic documents align with the narrative required to support approval for the merger filing.

Martin Versfeld is a Partner and Lebohang Makhubedu, a Senior Associate | Webber Wentzel. Patrick Smith is a Partner, Ricky Mann, an Associate Principal, and Daniela Lamparelli, a Senior Associate | RBB Economics

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Absa flags a drop in profits (JSE: ABG)

A slow pre-election period in South Africa didn’t help matters

Absa has released a voluntary trading update for the six months to June 2024. It’s voluntary because the move in earnings is less than 20%, so this isn’t a mandatory trading statement.

As we saw in Nedbank, conditions in South Africa in the pre-election months this year weren’t conducive to growth. Consumers have been under pressure and large corporates have been playing a game of wait-and-see.

In an Absa-specific issue, they have a very strong base effect for these earnings. This simply means that the first half of 2023 was much stronger than the second half, so the basis for comparison (1H24 vs. 1H23) gives the growth rate a steep hill to climb.

Unfortunately, the hill is simply too steep. They expect headline earnings to decline by mid- to high single digits for the period. Return on equity is expected to drop from 15.7% to 14.0%. That’s not good.

If we dig deeper, we find low single digit revenue growth. Interestingly, net interest income is up high single digits vs. non-interest revenue decreasing by low single digits. Not only is insurance income under pressure (as we saw at Nedbank), but so is trading income. Although these announcements are light on details, at this point it looks like Absa has underperformed its green competitor.

The expense pressures are visible at Absa as well, with expense growth in the high single digits. This means we are in negative jaws territory, with a drop in pre-provision profit. At least the credit loss ratio is in line with the base period, so no further pain there.

There are other problems that have carried through from the second half of 2023, like hyperinflation accounting in Ghana and further losses on the Nigerian currency that has inflicted so much pain.

As a silver lining, Absa expects to declare a flat interim dividend despite the drop in earnings.

Guidance for the full year is mid-single digit revenue and expense growth, leading to a fairly similar cost-to-income ratio to 2023’s level of 53.2%. They expect return on equity of 14% to 15% vs. 14.4% last year. In other words, the tough base in 1H23 that wasn’t repeated in 2H23 will help when viewing 2024 on a full year rather than interim basis.

Rough diamond sales at De Beers are looking even rougher (JSE: AGL)

The narrative is now a “U-shaped recovery”

The problems in the diamond industry continue. Although De Beers (part of Anglo American) is quick to point out that this time of year is a quieter period for rough diamond sales, the reality is that the issue is clear to see.

In Cycle 5 last year, they sold $456 million in diamonds. This year, it’s down at $315 million. That isn’t explained by seasonality. The seasonal effect is seen by comparing cycle 5 this year to the immediately preceding cycle 4, which was $383 million.

Although De Beers is trying to pick out hopeful statements like a resurgence in demand for natural diamonds in the US, they are also expecting a protracted U-shaped recovery in demand, with one of the factors being China. The factor they love ignoring, of course, is lab-grown diamonds.

In a U-shaped recovery, rather than a V-shaped recovery, the period at the bottom is longer. Buckle up.

Pick n Pay is lining up its rights offer (JSE: PIK)

Shareholders have approved various related resolutions

There isn’t much good news at Pick n Pay, but at least shareholders are in agreement with the recapitalisation plan. The various resolutions required to prepare for the rights issue achieved a very high approval rate at a general meeting.

The plan remains to pursue a rights issue of up to R4 billion in mid-2024, along with a separate listing and public offer of Boxer towards the end of 2024.

Primeserv’s earnings jump is matched by the dividend (JSE: PMV)

On big moves in HEPS, it’s always good to look at the payout ratio as well

Primeserv has released its results for the year ended March 2024. This is a staffing, recruitment, functional outsourcing and training business and it doesn’t get much attention on the local market, with a market cap of under R200 million.

This financial year was a good one, with revenue up 18% and HEPS up by a meaty 40% to 32.68 cents. Share buybacks were a significant help here. Importantly, the dividend followed suit, up 39% to 12.5 cents. Although that’s a modest payout ratio, it’s still good to see a similar growth rate in the dividend vs. HEPS as this speaks to the cash quality of earnings.

You won’t find too many listed companies that have performed with this level of consistency, as though there was no pandemic in the middle:

Sephaku’s numbers look as strong as the cement (JSE: SEP)

There’s a substantial jump in profits

Sephaku Holdings has released results for the year ended March 2024. They have two underlying businesses: Métier (a subsidiary) and Dangote Cement (an associate referred to as SepCem).

At group level, this has been a year of green numbers everywhere you look. HEPS has jumped from 9.66 cents to 25.71 cents, so that’s a strong positive move.

If we look deeper, we find that margins have improved at both Métier and SepCem, which supercharges the growth in EBITDA. At Métier, EBITDA increased 35.7% to R133 million and margin expanded by 150 basis points to 11.5%. At SepCem, EBITDA grew by 29.4% to R361 million and margin expanded by 140 basis points to 12.8%.

Notably, the SepCem numbers are for the 12 months to December 2023, as the companies don’t have the same year-end.

It’s particularly encouraging to see that revenue at Métier is above FY19 levels for the first time, with plant expansion leading to a recovery in volumes above pre-pandemic levels. In a year where volumes increased 11% and prices were up 9%, Sephaku can smile about the numbers at its subsidiary. As a very happy resident of Cape Town, it also doesn’t shock me to see that much of the boost to Métier’s business is coming from the Western Cape.

As part of the results presentation, the company gave an indication of performance in the first quarter of the new financial year. Revenue is only up 2.2% year-on-year, as we’ve seen a sluggish environment. This aligns with what the banks have been saying about the pre-election period.

Sephaku’s performance this year will depend greatly on whether we see a GNU-inspired acceleration in investment in South Africa.

In a separate announcement, Sephaku noted that Métier has agreed to buy a property in KZN for R21 million. They have been the tenant for 17 years and the lessor was not going to renew the lease due to an intention to sell. As this is a strategically important site, it makes sense to buy it.

Little Bites:

Director dealings:

A non-executive director of Bytes (JSE: BYI) bought shares worth £50k.

A director of a major subsidiary of Insimbi (JSE: ISB) sold shares worth R147.4k.

A director of Copper 360 (JSE: CPR) bought shares worth R69.6k.

A director of RH Bophelo (JSE: RHB) bought shares in the company worth R12k.

A director of Afine Investments (JSE: ANI) dug around in the couch for some coins and bought shares in the company worth R3.4k.

OUTsurance (JSE: OUT) has a programme in place that allows directors of OUTsurance Holdings (which holds the operations) to swap their shares for shares in OUTsurance Group (the listed company). In the latest examples of these trades, OUTsurance has now increased its stake in OUTsurance Holdings from 90.20% to 90.45%. They’ve issued more shares in the group company to pay for it though, so there’s a dilution of other shareholders. In other words, this is a structural thing that comes out in the wash.

Capital Appreciation (JSE: CTA) has repurchased R56.8 million worth of shares between September 2023 and June 2024, representing 3.6% of shares in issue. The average price paid was R1.21.

At a general meeting of shareholders, AYO (JSE: AYO) obtained approval for the resolutions related to the specific repurchase of shares from the GEPF.

In the extremely unlikely event that you are a shareholder in Globe Trade Centre (JSE: GTC), be aware that there is a dividend of PLN 0.22 per share coming.

For those interested in how BHP (JSE: BHG) is thinking about its decarbonisation strategy, there’s a presentation on this topic available here.

The market may be unpredictable, but your investment strategy doesn’t have to be. Investec Investment Management experts share their insights on what approaches are winning, common mistakes investors make, and why staying the course is important. All this and more in the latest episode of Investec’s No Ordinary Wednesday podcast.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Attacq gives the market a pre-close update (JSE: ATT)

Guidance for growth in distributable income per share is unchanged

Attacq has released a pre-close update that is filled with useful information about how the portfolio is performing. To read the entire presentation, you’ll find it here. It includes some helpful case studies on how they use active asset management techniques to increase the values of properties.

Perhaps the most important news is that the guidance for distributable income per share growth is unchanged at between 10% and 12.5%. The dividend payout ratio is expected to be 80%. Overall, things are going well in the portfolio.

The retail-experience hubs (which the rest of us just call shopping malls) experienced an improvement in the occupancy rate from 95.9% as at June 2023 to 96.1% as at May 2024. The exposure to Pick n Pay across the portfolio is 2.7% of rental income, which equates to 1.3% of Attacq group rental income. All leases are with corporate stores rather than franchise stores and at this stage, it doesn’t look like any changes will be made to the space in the leases. Trading density in the overall portfolio (sales per square metre) increased by 4.6% to R3,999/sqm.

The collaboration hubs (offices to the rest of us plebs) saw occupancies increase from 83.9% to 86.5%. That’s still not great but at least it’s trending in the right direction.

The logistics hubs (thank goodness for an easy name) reported a drop in occupancy from 100% to 94.1%. These properties tend to have few tenants occupying large spaces, so the timing of literally one lease can have quite an impact on occupancy levels.

There’s still a lot of development underway in the portfolio, including the Ellipse Waterfall residential development. They have already sold 90.9% of the units. They did need to reconfigure phase 3 though to move from larger units into more 1-bed and 2-bed units to improve saleability. The residential property game isn’t easy. Just read a Balwin update if you don’t believe me.

In Rest of Africa, discussions with Actis regarding the disposal of 50% of Gruppo have been terminated. We know this from Hyprop, which sits alongside Attacq in Ikeja City Mall. There’s a discussion to dispose of Ghana and Nigeria to a single suitor.

Attacq’s gearing ratio is 25.4% and gross interest bearing debt has reduced slightly R5.78 billion. The weighted average cost of debt is 10%.

Overall, things are looking good at Attacq.

Brait needs time to exit its portfolio (JSE: BAT)

At R50m a year in fees, the management company won’t complain of course

Brait owns Virgin Active, a stake in Premier (now separately listed) and New Look, a UK retailer. Eventually, Brait is looking to offload these stakes and return capital to shareholders. In the meantime, there are large management fees, a highly painful rights offer and all the other usual joys to deal with for Brait investors.

It’s easy to point to the five-year share price performance of -96% and blame COVID. Fair enough – nobody saw that coming and gyms were absolutely brutalised by it. But over 3 years, the share price is down 71%. That’s a lot harder to justify.

Speaking of Virgin Active, Brait’s results for the year ended March reflect annualised run rate EBITDA for the health club group of £80 million, up from £33 million a year ago. Take careful note of the currency there. Yes, Virgin Active is far bigger than just South Africa. In fact, Southern Africa is 34% of group revenue, with the next largest being Italy (28%) and the UK (24%). Asia Pacific is also meaningful at 14%. Recent membership growth looks decent across the board as people return to offices and thus to gyms.

Premier is separately listed now so the performance is already known to the market. The group is doing very nicely indeed, with results for the year showing 19% EBITDA growth and a decrease in leverage, along with the declaration of a maiden dividend. Brait will justify hanging onto this asset for as long as possible, I assure you.

New Look is only 7% of Brait’s total assets and that’s just as well, as revenue declined by 8.8% in the past year. Despite this, Brait managed to increase the value of New Look in the Brait balance sheet by lifting the valuation multiple from 5.0x to 6.5x. You can think for yourself whether that sounds logical.

With Virgin Active needing to recover further before Brait is prepared to sell that asset, despite Brait’s apparent approach of increasing valuation multiples when companies go backwards, the group has taken steps to recapitalise the balance sheet (yes, a painful rights offer) and extend the maturity date for the exchangeable bonds.

And of course, The Rohatyn Group will keep earning a R50 million annual advisory fee for the pleasure of all this, along with a new incentive mechanism capped at R50 million based on sharing in increases in Brait’s market cap.

Perhaps the exercise bicycles at Virgin Active should have a pre-set gradient profile based on the Brait share price? Looks like a proper workout to me:

Exxaro saw reduced demand from Eskom (JSE: EXX)

Production as a whole is well down on the end of 2023

Exxaro released a pre-close message dealing with the six months to June 2024. Average benchmark coal and iron ore prices are down vs. the second half of 2023, which is never great news for a commodities business.

Total coal production is down 14% and sales volumes are down 12% vs. 2H’23, with reduced demand from Eskom at Grootgeluk as a major driver. It seems as though this was more of a first quarter issue, with improvements in the second quarter.

It does help cash flow that capex for the six months should be 33% lower, with reduced sustaining capex at Grootgeluk.

Exxaro’s balance sheet remains strong, so the income statement is unlikely to tell a happy story for this period but the overall financial position isn’t a concern.

Interim results are due for release around 15 August.

KAP continues to get klapped by Safripol (JSE: KAP)

When the most important division is hurting, nobody is smiling

KAP is a good example of how a group can be diversified across a number of businesses, yet heavily impacted by just one of them. Even diversified groups are very rarely an even split across the underlying operations. In KAP’s case, the problem child is Safripol and the state of play in the polymer industry.

Although five out of six divisions improved their performance for the 11 months to May 2023, this was more than offset by the negative move at Safripol. This is why HEPS is not expected to differ by 20% or more from the prior period, despite the weak base. EPS will improve sharply because of the impairment of Unitrans in the base period. Remember, HEPS isn’t affected by impairments.

We may as well start with Safripol, where weak domestic and export margins are a major issue. Although domestic sales volumes increased, export volumes were down because of the weak margins. The cyclical downturn in the polymers sector on a global basis is really impacting this business.

In some good news at least, PG Bison’s new R2 billion MDF line in Mkhondo was completed almost a month ahead of schedule after three years of construction. The group has invested a fortune in this initiative and is no doubt excited to show investors why. Other good news is that the appointment of a new CEO at Unitrans and a “rationalisation” of the executive committee (i.e. major changes) have resulted in improved performance.

Over at Feltex, new vehicle assembly volumes and price adjustments supported a “pleasing” performance – words that KAP hasn’t been able to say about Feltex in a while. There’s also a positive story at Restonic, with market share gains, production efficiencies and cost savings.

And at Optix, subscriber numbers increased and the order book and sales pipeline remained positive.

Net debt at the end of this financial year should be in line with the prior period. For balance sheet flexibility, KAP has raised a R3 billion revolving credit facility. This will refinance pending maturities and give them flexibility to pay down debt after the commissioning of major projects.

You won’t find too many share prices that can trade in such stubborn ranges for extended periods, clearly inspired by natural beauties like table mountain:

Nedbank updates the market once more (JSE: NED)

Shareholders certainly can’t claim that they aren’t being kept informed

Not even a month after releasing a voluntary trading update dealing with the first four months of the year, Nedbank has now gone the route of a pre-close update that focuses on the first five months, with expectations for performance going forward.

I love disclosure by companies, so by all means keep it coming Nedbank!

The challenging levels of economic activity in the four month period extended into May, with consumers under pressure and slow growth in credit and transactional revenue. Unsurprisingly, the bank has pointed to the formation of the GNU and the improved investor confidence as a result, which should trickle down into the economy.

Over five months, headline earnings growth is expected to be around mid-single digits. Expense management has helped here, as top-line growth has been subdued.

Net interest income (NII) growth was below mid-single digits, with particularly slow growth in loans in Corporate and Investment Banking (CIB). This doesn’t surprise me at all, as corporates sit on their hands just before elections. Net interest margin is down slightly from FY23 levels. Although management expected growth in NII above mid-single digits, they have now tempered those expectations to below mid-single digits for the interim and full year period.

Looking at impairments, the credit loss ratio has improved but remains above the through-the-cycle target range of 60 to 100 basis points. They expect to be within range for the full year. Nedbank Wealth is below the target range and CIB is within its target. The elevated ratio is because of the Retail and Business Banking (RBB) book, which is above its target range of 120 to 175 basis points. Yes, the different divisions have different target ranges as they take on different risks (and price them accordingly).

Non-interest revenue (NIR) growth was also below mid-single digits, impacted by insurance income that fell year-on-year. This was driven by a more cautious approach in personal loans, which earn both NII as well as insurance premiums on related credit life products. Guidance for NIR growth of above mid-single digits remains in place for the interim and full year periods.

Associate income related to the investment in ETI will be down roughly 31% for the half year, driven by a non-recurring benefit in the base period. There’s no change to expectations here vs. when the four-month numbers were released.

Expense growth is above mid-single digits, with an expectation of expense growth of mid-to-upper single digits for the half year and full year. That’s a concern based on revenue growth, as banks don’t want to be in a negative jaws position (where margins go backwards).

Headline earnings growth has slowed from H2’24 but is still expected to be positive from what I can see. Importantly, return on equity (ROE) – the key metric for banks – has increased vs. the comparable period.

Results for the interim period are due for release on 6 August.

At RECM and Calibre, Goldrush will hope that load shedding stays away (JSE: RACP)

The gaming business suffers when there’s no electricity

Over 96% of the total assets at RECM and Calibre can be attributed to the 59.4% stake in Goldrush, so that’s clearly where the focus of the group is. The year ended March 2024 was difficult, as parts of it were hit by terrible levels of load shedding.

Although gaming revenue was up 7% for the year (with all four divisions seeing revenue increases), EBITDA (before IFRS 16) was down 2%. Keeping the lights on is expensive – literally. Diesel costs were a major drag here, along with general cost pressures.

Profit after tax fell by 28%, yet the dividend from Goldrush was 20% higher than the prior year. To help you understand the payout ratio, after-tax profit was R97 million and the dividend was R60 million.

Goldrush has been focused on optimising the footprint, with the total number of active gaming positions down by 2.5% at year-end as some limited payout machines (LPMs) were out of commission while being redeployed to more profitable locations.

The major change going forward is that RECM and Calibre will no longer be using investment entity accounting going forward. Recognising that Goldrush is the permanent asset in the group, they will instead switch to publishing consolidated accounts.

Little Bites:

Director dealings:

Sales by Investec (JSE: INL | JSE: INP) executives are common in the market, as they incentivise key staff members with strong share-based awards. To give you an idea, two executives sold shares for a combined total of over R27 million.

A director of a major subsidiary of Stadio (JSE: SDO) sold shares worth R990k.

A director of a major subsidiary of Altron (JSE: AEL) received shares worth R595k in a share-based award and sold the whole lot.

An associate of a director of Astoria Investments (JSE: ARA) bought shares in the company worth R246k.

A director of Copper 360 (JSE: CPR) acquired shares worth R71k.

Watch out for an important announcement by Orion Minerals (JSE: ORN) this week, as the company has requested a trading halt (this is an Australian thing as the primary listing is there and regulated by those rules). This is because they expect to make a material announcement in relation to a proposed capital raising. The halt is until the commencement of trade on 27 June or whenever the announcement is made, whichever is earlier.

Despite the Prudential Authority saying no to Conduit Capital’s (JSE: CND) sale of CRIH and CLL to TMM Holdings, the parties are persevering. TMM is engaging with the Prudential Authority to appeal the decision. In the meantime, the parties have extended the fulfilment date for the conditions to 31 January 2025. TMM has even agreed to pay for R500k worth of CLL’s costs each month from July, with that contribution to be set off against the eventual purchase price. They really want this deal to work.

enX (JSE: ENX) announced that the special distribution of R5.00 per share will be paid on 8th July.

Omnia (JSE: OMN) announced that its special dividend of R3.25 per share has now been approved by the SARB.

I wish I was surprised that Kibo Energy (JSE: KBO) will miss the deadline for publication of its financial results for the year ended December 2023. They are due by 30 June and in reality they will only be done by August. Trading in the shares will be suspended from 1 July as a result. This partially impacts the placing of shares that was recently announced, which will happen in two tranches. The first is on 27 June and the second is once the suspension is lifted.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

In the 36th edition of Unlock the Stock, we welcomed Oceana Group to the platform for the first time. To understand the drivers of the share price performance, The Finance Ghost co-hosted this event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions.

In this piece, Tivon Loubser of Twelve B Fund Managers comments on the ongoing need for solar investment in South Africa and how investors can participate through Twelve B Energy Fund II. For more information on how the team approaches solar, this recent podcast with Tivon is highly recommended:

In the wake of our politically motivated load shedding sabbatical, we seem to be back on track for what has become status quo (albeit under a different guise – Load Reduction). While it would not have come as a surprise to anyone, it does reiterate the dire position of our energy crisis.

In what has been a trying time for South Africa, characterised by little to no growth in our economy, it is tough to find the silver linings. In this case the one silver lining that does come to mind, is the 125% SARS-approved Section12BA tax allowance, and the resulting investments into renewable energy-generating assets. This has served as a catalyst for South Africa’s transition to a low carbon economy, while also reducing reliance on the failing power grid. At the end of 2023, South Africa had an installed capacity of just under 8GW, which accounts for almost 50% of installed capacity on the continent.

A lot of this stimulus has come from foreign direct investment, as well as the private capital markets. In the private market space, at Grovest we pioneered Section 12BA investments through the Twelve B Green Energy Fund. Not only has this made investing in solar accessible to retail investors, but it has also provided a mechanism for businesses and body corporates to finance solar installations at their premises through Power Purchase Agreements (PPAs).

Investing in solar

Investing into the Twelve B Green Energy Fund enables taxpayers, including individuals, trusts, companies and pension funds, to invest in a portfolio of renewable energy-producing assets and benefit from the Section 12BA tax incentive. The Fund also offers bi-annual income distributions, an average annual cash yield of 14.22%, and a targeted IRR of 18%.

There are a number of important caveats to the 12BA allowance. In order to claim the allowance, the money must be invested into renewable energy-generating assets during the period of assessment. Therefore, it is very important to do your homework when choosing which Section 12B fund to invest in. Make sure the respective fund has sufficient deal pipeline to deploy all the raised capital. It is also important to ensure that the fund is using reputable solar installers (Engineering, Procurement and Construction companies – EPC’s). As the solar industry is currently a gold rush, more and more ‘fly by nights’ are popping up, which has resulted in subpar installations, and installations which poser a major fire risk.

Twelve B Green Energy Fund I successfully closed at the end of 2023, and all monies raised were successfully deployed, enabling all investors to claim their full 12BA allowance. Our Fund I portfolio consisted of 10 different projects, creating a strongly diversified portfolio.

Fund II: 30 June closing date

Fund II is closing on the 30th of June, and operates on the same premise as Fund I. The big difference is that we have expanded our network of vetted EPC partners. Extensive due diligence is done on all the prospective EPC partners, ensuring they have all the necessary industry accreditation and a strong track record.

The existing Fund II pipeline is well in excess of R200m, with a number of blue chip off-takers. This bodes well for Fund II, and ensuring all the raised capital is deployed. This is imperative considering the 12BA allowance is going to be sunset on the 28 February 2025.

Further to the financial returns, and the lucrative tax allowance, one of the reasons we at Twelve B are so passionate about this investment is the tangible impact it is having on South Africa. To date we have had countless success stories of businesses and homeowners experiencing increased efficiencies due to the solar installations.

This article includes forward-looking statements which have been based on current expectations and projections about future results, which although the Fund Manager believes them to be reasonable are not a guarantee of future performance.Twelve B Fund Managers (Pty) Ltd is an approved juristic representative of Volantis Capital Proprietary Limited, an Authorised Financial Services Provider FSP No 49836.

This article is not a recommendation by The Finance Ghost regarding this project. Please do your own research and speak to your financial advisor as part of any investment decision.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Ethos will pass the Brait hot potato to shareholders (JSE: EPE | JSE: BAT)

There is very little love for Brait in the market

In a voluntary NAV update, Ethos Capital announced that the net asset value per share has increased by 1.8% over the three months to March, now at R7.44. The share price is R4.25, so the shares trade at a significant discount to NAV per share – a common problem in the market for investment holding companies.

The unlisted portfolio contributed a R0.55 increase in NAV and the listed portfolio suffered a R0.22 reduction thanks to the sell-down in Brait.

Ethos has decided to unbundle Brait ordinary shares as part of the “value unlock” for shareholders. It’s just a pity that there isn’t much value. RMB has agreed to amend existing covenants and extend debt facilities until February 2028, when proceeds from the Brait exchangeable bonds will reduce that facility.

The group is also unwinding the Black Hawk Private Equity structure, which is held by non-executive directors of Ethos and their associates. The shares will be sold back to Ethos for nil consideration, as there is debt associated with the structure. Ethos shareholders are stuck with the guarantee in respect of that debt.

I like my money, which is why I keep it far away from Ethos and Brait.

After eight years, Peter Hayward-Butt is resigning as the CEO of Ethos. Over that period, the share price has lost 55% of its value. Anthonie de Beer will take over as CEO.

Concerning metrics in Hyprop’s local portfolio (JSE: HYP)

I get so irritated by the silly things that local management teams have to focus on – like water!

Travelling abroad is a wonderful thing, but it definitely elevates your frustrations with things that don’t work in South Africa. When a property group has to include a paragraph about initiatives for backup potable water in the most important province in South Africa, it really is time to hold our politicians to much higher standards.

Property funds in the UK and Europe aren’t stressing about where the water will come from, that much I can assure you.

Leaving the basics aside, Hyprop took a risk with the Table Bay Mall acquisition (especially at the price they paid) and the dividend suffered for it. They blamed the Pick n Pay issues for the lack of dividend, but Hyprop was the only fund in the market to take that route, so I suspect it was more of a convenient excuse against the backdrop of the balance sheet pressure from the Table Bay Mall deal. Although the mall is in a fast-growing area of Cape Town, I still worry that they’ve overpaid for it. The deal was paid for with R500 million in available cash, R250 million from revolving credit facilities and R900 million from the issuance of DMTN bonds. The group loan-to-value ratio is up from 37.4% at December 2023 to 40.2%.

Looking at the South African portfolio as a whole, tenant turnover only increased by 2.1% year-on-year for the five months to May. This is despite a 5.7% increase in footcount. We are walking around in the malls it seems, but we aren’t buying enough. As a further concern, trading density (sales per square metre) fell in both April and May on a year-on-year basis, as did tenant turnover. That’s not the trend you want to see.

Although they are achieving positive rent reversions in the local portfolio, that situation will change if tenant turnover growth doesn’t turn positive again in the aftermath of the elections.

Compare this to the Eastern Europe portfolio – a land of reliable water supply and consumers with some disposable income. With only a 0.5% increase in footcount, there was an 8.7% increase in tenant turnover. These numbers are based on the four months ended April. Unsurprisingly, there are positive rental reversions in that market.

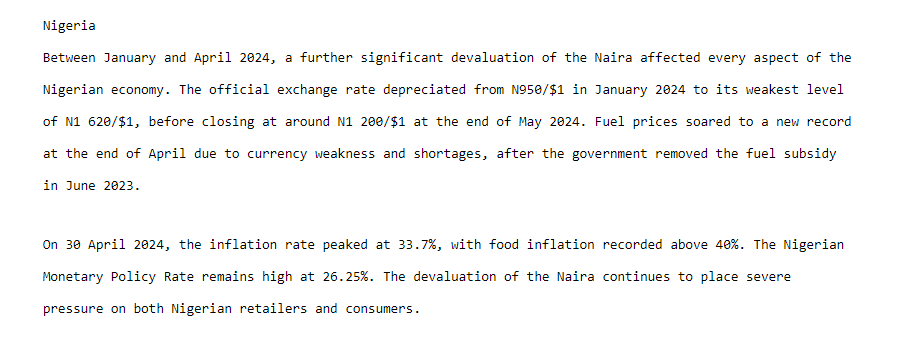

In the sub-Saharan Africa portfolio, Nigeria has been severely impacted by the devaluation of the naira. The political climate in South Africa is full of people arguing that “the markets” don’t matter and that we don’t need a business-friendly GNU. Well, here’s life on the ground when the markets go against you:

Ghana isn’t doing much better, unfortunately.

As a further challenge in Nigeria, the Ikeja City Mall sale didn’t meet the conditions precedent. Hyprop has signed a letter of intent with another party for the entire sub-Saharan Africa portfolio. Fingers crossed.

A dividend for the full financial year will be considered by Hyprop. With not a single mention of Pick n Pay in the pre-close update, that excuse has hopefully run its course now.

A flat profit performance at Invicta (JSE: IVT)

This is despite decent revenue growth

For the year ended March 2024, Invicta reported revenue growth of 7%. That sounds like it should lead to a great result at profit level, but profit was actually 0.5% lower for the year.

One of the reasons is that selling, administrative and distribution expenses were up 10%, with 400 basis points attributable to the acquisition of Imexpart Limited. There were also some asset impairments in this financial year.

A major factor was the significant jump in finance costs from R131 million to R177 million, more than offsetting the growth in equity accounted earnings from Kian Ann, which increased from R152 million to R172 million.

Although HEPS fell by 4% to 470 cents, the group also reports sustainable HEPS with further adjustments for non-trading items. This metric was up 5% to 488 cents, which is why the dividend also increased by 5% to 105 cents per share.

Jubilee is acquiring two more copper assets (JSE: JBL)

The copper strategy in Zambia is going well

Jubilee has significantly increased its copper resource base through two transactions to acquire copper resources that are currently in production (Project M and Project G). The combined value of the deals is $3.85 million. Only $0.25 million is settled in cash, with the rest paid for through the issuance of new Jubilee shares at a 30-day VWAP.

It’s great to see smaller companies being able to use their shares as acquisition currency, as this is one of the key reasons to be a listed company. This is made possible by what the company is achieving in initiatives like the Roan Upgrade.

Jubilee is pushing hard on what it calls its Integrated Copper Strategy in Zambia, which allows for targeting of copper resources ranging from tailings through to near-surface copper reef that is accessible through open-pit mining.

Kore Potash isn’t across the line with PowerChina yet (JSE: KP2)

This is anything but an easy negotiation

Negotiations where so much is on the line are always tricky. Both Kore Potash and PowerChina are heavily invested in the Kola project, with the latter having spent considerable time and resources in putting together the Engineering, Procurement and Construction (EPC) proposal. Of course, for Kore Potash, they are committed rather than just involved in the project. It simply has to work for them.

After meetings in Beijing in May, further important issues were raised around completion and performance guarantee tests. This is because the goal is to achieve a fixed price contract with only minimal variations. This puts the risk on PowerChina. If you’ve followed the South African construction industry, you’ll know that a single bad contract can sink an entire company, so it’s understandable that the parties are taking their time to get this right.

A follow-up meeting has been planned for July 2024.

Another interesting development is that PowerChina has expressed interest in operating the mine after construction, with a draft operating proposal expected to be received in July.

As soon as the EPC is finalised, Kore Potash will need to move forward with raising funds from the Summit Consortium.

The market hated the uncertainty in the news, with the Kore Potash share price closing 22% lower on much higher volumes than an average day of trade, so that wasn’t because of an isolated trade.

The flowery language continues at Orion Minerals (JSE: ORN)

Sometimes it sounds like they are selling tickets to a show

It’s very unusual to see emotive language on SENS. Companies shy away from words like “exceptional” and “outstanding” and with good reason. The use of hype words can turn against you very quickly if things go slower than expected, or aren’t quite as outstanding as was promised.

Nonetheless, Orion has referred to “More Outstanding Hits” – which sounds like a Saturday radio show – at the Okiep Copper Project. Basically, they are excited about the drilling results coming through.

Interestingly, the company notes a slow turnaround time from local laboratories, which gives an idea of the activity in the copper exploration space.

Orion is working to complete the Bankable Feasibility Studies. As the name suggests, these are needed to move forward with financing and further development activities.

Profits have declined at PBT Group (JSE: PBG)

The share price has come a long way off its highs

The PBT Group share price is a good example of why patience can pay off in the markets. Before the pandemic, nobody knew anything about this company. It then exploded onto the scene (and I think launched my career as a ghost to be honest, as writing on this company landed me my first Financial Mail opportunity). After excellent results during the pandemic, reality set in about the sustainable growth prospects and the share price washed away:

In a trading statement for the year ended March, the company has advised that normalised HEPS from continuing operations will be down by between -13% and -7.6%. This is because revenue growth is between -0.1% and 6.1%, with EBITDA expected to be -8.4% to -2.7% lower.

The normalisation adjustment always took into account the treasury shares related to the BEE structure. Those shares have subsequently been classified as ordinary shares in issue, so HEPS from continuing operations without the normalisation adjustment fell by between -26.1% and -21.5%.

The highlight is cash generated from operations, which increased by between 1.2% and 7.5%.

The discontinued operation is PBT Australia, which was disposed of on 30 September 2023.

The PPC CEO doesn’t mince his words (JSE: PPC)

There’s proper tough talk here

If you read PPC’s high level results for the year ended March 2024, you really wouldn’t think that there’s anything to be worried about. After all, revenue is up 20.6%, EBITDA margin expanded by 160 basis points and HEPS swung from a loss of 20 cents to a profit of 19 cents. Bliss, surely, especially when you consider that there’s a dividend of 13.7 cents?

The newly appointed CEO thinks otherwise, noting that “problems are pressing” and that a “meaningful organisational reset and tough decisions” are going to be necessary here. I’m very glad that PPC doesn’t pay my salary, then.

The wording is quite incredible really, with the growth in revenue in the South African and Botswana cement business described as being “marginal” – despite being +5.2%. Materials business did see revenue drop by 6% though. It’s also worth noting that the revenue growth in cement was driven by pricing increases, as volumes were negative.

Of the R502 million increase in trading profit, Zimbabwe contributed R395 million. CEO Matias Cardarelli will clearly be focusing on improving things in the local business, which is exactly why he was the chosen successor. PPC faces major market headwinds like slow economic growth and the problem of imports, so he has his job cut out for him.

Still, I can only admire someone who recognises the problem instead of pretending that it isn’t there. We have far too many executives on the JSE who have become accepting of mediocrity.

I like the new CEO and it will be interesting to see where this story goes

Naspers and Prosus have released results for the year ended March 2024. The group has achieved eCommerce profitability in the second half of the financial year, which is a big deal. They are well ahead of the commitment to be profitable in that business in the first half of the new financial year. The fact that the announcement starts with a note on profitability tells you that the winds of change have blown strongly in the group.

Here’s another indication of the changes: the group invested $571 million in M&A in the year, way below the peak of $6.3 billion in 2022 when the previous CEO was all about tight shirts and loose deals. Management is now trying to rectify significant underperformance in the past couple of years, which is what happens when you deploy most of your capital at the top of the cycle. They have $16 billion in capital on the balance sheet, so discipline with that money is key.

I always like to look at the Naspers results specifically to see what’s going on with Takealot Group, which includes Mr D. For this period, gross merchandise value increased by 3% and revenue was up by 8%. Mr D was profitable for the first time, with a trading profit of $3 million for the year. As for Takealot, it reduced losses by $4 million but still isn’t profitable. I also look at Media 24, which suffered an impairment of R280 million in this period as performance is below expectations.

The offshore assets are obviously where the real value lies in this group.

RCL Foods will let Rainbow go on a high (JSE: RCL)

A trading statement shows that Rainbow has been a helpful contributor in this period

With the unbundling of Rainbow by RCL Foods coming up on 1 July, RCL has released what will be its final trading statement that includes references to Rainbow.

For the year ended June, RCL Foods expects HEPS from total operations (including Rainbow) to be at least 75% higher than the prior period. Rainbow has been a major driver of that performance, as has the grocery business which has enjoyed the demise of load shedding in recent months. The sugar business is also doing well. Baking is facing volume and margin pressures though in an extremely competitive environment.

The announcement notes that Rainbow’s trading performance in the second half of the year was broadly in line with the first half, with an interesting comment that retail and wholesale volumes increased while quick-service restaurant volumes softened. It seems that South Africans are eating at home more often, presumably a combination of affordability and the abundance of electricity. Although feed costs increased in the second half of the year and volumes were under pressure in the external feed business, Rainbow navigated this with lower input costs thanks to breed performance and cost control measures as part of the turnaround strategy.

Little Bites:

Director dealings:

Various top Nedbank (JSE: NED) executives sold shares in the company worth over R31 million.

The CEO of Mr Price (JSE: MRP) received share awards and promptly sold the whole lot for over R19 million. The CFO took the same approach to the value of R2.6 million, as did the company secretary to the value of R1.8 million. The company secretary also sold additional shares worth R56k.

The former CEO of The Foschini Group (JSE: TFG) has sold shares in the company worth R25.8 million.

An associate of directors of Astoria Investments (JSE: ARA) bought shares in the company to the value of R4.4 million and entered into a CFD trade with a value of just under R5 million.

A director of a major subsidiary of Novus (JSE: NVS) received share awards and sold the whole lot for R973k.

Various directors of Anglo American (JSE: AGL) were happy to receive shares in lieu of fees for services rendered, with a total value of around R700k.

A director of Copper 360 (JSE: CPR) acquired shares i the company worth R22.5k.

Adrian Gore has entered into replacement hedging transactions over Discovery (JSE: DSY) shares. There are two distinct tranches. The first is a put – call structure expiring mid-2025 at prices of R113.1836 and R168.5769 respectively. The second is a similar structure that expires in March 2026 at prices of R114.3028 and R184.9017. These structure protect against downside below the put price and give away upside above the call price. The current share price is R135. There are 3,000,000 options in total, so the nominal value being hedged is just over R400 million at current prices.

Trustco (JSE: TTO) has agreed a share repurchase with University of Notre Dame du Lac in the US, which holds 12.8% in Trustco, 0.7% in Trustco Resources and 8.65% in Legal Shield. Each of those entities will repurchase their respective shares from the university. The aggregate value is $5 million. This is a related party deal, so a circular with an opinion by an independent expert will be sent to shareholders in due course.

Tiny little Visual International (JSE: VIS) released a trading statement that reflects HEPS of 3.33 cents for the year ended February 2024. The share price is only R0.03!

Putprop (JSE: PPR) announced the results of the odd-lot offer, in which 4,048 shares in the company were repurchased. This took 362 individual holders off the register, holding 0.01% of the shares in issue.

MC Mining (JSE: MCM) has announced that Godfrey Gomwe is stepping down as managing director and CEO. This comes after the successful offer by Goldway Capital for the company. Don’t feel too sorry for him, as there’s an accelerated vesting of 8,000,000 share options that can be exercised before April 2027. Separately, the company announced the appointment of non-executive director Christine He as interim Managing Director and CEO, effective 1 July 2024.

Ibex Investment Holdings (JSE: IBX) (the old Steinhoff investment vehicle) has announced the placing of up to 400 million Pepkor shares in the market. This represents 10.9% of Pepkor’s current issued share capital. Ibex currently owns 43.7% of issued Pepkor shares. Ibex may increase the size of the placing subject to demand and pricing. Barclays, Investec and JPMorgan are acting as Joint Global Coordinators and will be picking up the phone to qualifying investors to try place the shares.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

A major win for Coronation against SARS (JSE: CML)

And indeed, a win for corporate South Africa

This is the news that many had been waiting for. The Constitutional Court delivered judgment on the landmark tax matter between SARS and Coronation, with Coronation as the victor. This has important ramifications for offshore structures put in place by local corporates.

The full impact of this matter was R794 million, which Coronation had provided for in full. This is a great windfall for shareholders, especially as the SARS fight had ruined the Coronation dividend for a year. Investors will be very happy to see this cash kept within the company (and hopefully paid out as a dividend) rather than paid to the tax authorities.

Insimbi is selling two underperforming businesses (JSE: ISB)

And there’s an innovative structure to help the buyers pay for them

In listed companies, we are quite accustomed to seeing asset-for-share transactions. In these deals, the companies buy assets (usually private companies) and pay for them by issuing shares to the sellers. In Insimbi’s latest announced deals, they are doing things the other way around.

The core outcome here is the disposal of the AMR Booysens Business and the AMR WR Business, both of which are underperforming. The trick is that the disposals are linked to specific repurchases of shares from shareholders who are related to the buyers of these businesses. Effectively, most of the proceeds from the specific repurchases of shares will be used to pay Insimbi for the businesses.

In both underlying transactions, the repurchase price is R1 per share. Insimbi closed at R0.80 on Friday but has a 52-week high of R1.35, so the repurchase price isn’t as silly as it may look. This is an illiquid stock where the price can move significantly in a single day.

The repurchases represent 11.41% of Insimbi’s total shares in issue, with a total value of R43.05 million. Insimbi will get back R30 million for the disposals, so the shareholders in question are pocketing a net R13 million from these transactions. Frustrating as that may sound, these businesses are currently making losses, so shareholders need to think about the long-term picture.

This is certainly an interesting structure, with Mazars Corporate Finance appointed as independent expert to opine on the deal. The opinion will be included in the circular.

Motus gave an important strategic update (JSE: MTH)

Proper capital markets days are thin on the ground in SA, so pay attention when you see them

Listed companies need to meet a minimum disclosure requirement under regulations, but nothing stops them from going beyond that. Although very few take the route of hosting capital markets days and really talking to the market, there are those that do. This is to be applauded, with Motus as the latest such example.

The full presentation is available here and I recommend checking it out.

The group targets 65% of EBITDA in South Africa and 35% from international operations. They also target 50% of EBITDA from vehicle sales and the other half from non-vehicle sales. In both cases, they are currently in line with these targets, so no major changes are expected there.

The acquisitive activity has been focused on building out the international arm of the business, which makes sense when the group has its roots in South Africa and has roughly 20% market share in its home market for vehicle sales. Beyond the UK and Australia in terms of vehicle sales, the business that really has them excited is the aftermarket parts business in the UK and Asia. They call this the best growth potential for the group.

Of the many slides in the deck, one that jumped out at me deals with a structural shift in the South African car parc. That’s not a typo – this is the correct term for the total number of vehicles on the road in a given country or segment. With owners keeping their vehicles for longer (and often financing them over a longer term), there’s more demand for value-added products and services. This is a great opportunity for Motus, with strategies in place to develop products (e.g. telemetry) and markets like insurance. They even manage to bring the buzzwords like AI and machine learning into it!

Overall, the flavour of the strategy is to build annuitised revenue streams that are less cyclical than new car sales. Aftermarkets parts and value-added services sit squarely in this strategy.

Remgro has confirmed that Mediclinic is still very boring (JSE: REM)

Margins are down and earnings are flat

Hospital groups generally confuse me from an investment perspective. Although you would expect them to be licences to print money, the reality is that return on capital tends to be sub-par. Despite this, Remgro was happy to take Mediclinic private along with its consortium partners. The latest numbers for Mediclinic (covering the year to March 2024) have done nothing to convince me that this sector is interesting.

Group revenue may have increased by 5% at Mediclinic, but adjusted EBITDA was down 2%. Adjusted EBITDA margin contracted from 15.8% to 14.7%, with margins in both Switzerland and South Africa going the wrong way. At least margins in the Middle East were slightly up. Adjusted earnings came in flat in dollar terms for the year.

The second half was an improvement on the first half of the year, so perhaps some of that momentum will be carried forward. Even then, I just don’t see the appeal of hospital groups as equity investments.

Spear is recycling R160 million worth of capital (JSE: SEA)

The buyer for this property is The City of Cape Town

Spear REIT is selling 100 Fairway Close for R160 million to The City of Cape Town, which also happens to be the current tenant. This is an exit from a commercial office building, which Spear is happy to do as part of optimising the portfolio in the context of the pending Emira Western Cape portfolio implementation.

This also creates further headroom on the balance sheet, which is important as part of the broader funding and planning around the Emira deal. After this disposal, Spear’s loan-to-value will be between 23% and 23.5%. The strategic target for the loan-to-value ratio is between 38% and 43%, with management looking to operate at 39% on a go-forward basis after the Emira acquisition.

The yield for the disposal is 9.8%. This reflects some of the challenges in the office sector, even in Cape Town. The price of R160 million is identical to the value at which the assets were carried as at February 2024, the date of the last published annual financial statements.

Vunani suffers a sharp decline in profits (JSE: VUN)

The fund management and insurance businesses are to blame

Vunani had a year to forget for the 12 months to February 2024. HEPS has plummeted from 30.1 cents to just 7.4 cents. Despite this, the final dividend was only slightly down from 11 cents to 9 cents.

The decrease in profits wasn’t because of some kind of non-operating adjustment. Alas, operating profit tumbled from R124.6 million to R55.2 million. A combination of a drop in income and an increase in operating expenses did the damage.

If you look at the segmental results, there’s still no turnaround in sight for the institutional securities broking business, which made a loss of R12.4 million this year after a loss of R9 million in the prior year. Insurance also swung into losses, with a result of negative R7.6 million vs. positive R10.3 million in the prior year. A blow was also dealt by the fund management business, which saw profit drop from R21.2 million to R9.5 million.

It was only the asset administration business that made a decent, consistent contribution. Profit was R34.6 million this year vs. R33.7 million in the prior year.

If Vunani was serious about creating shareholder value, they would’ve at the very least walked away from the institutional securities broking business by now. Instead, they are willing to still carry those losses for some reason, which really doesn’t work when the rest of the group also goes the wrong way.

Little Bites:

Director dealings:

There are some very large disposals of Dis-Chem (JSE: DCP) shares by directors and prescribed officers. An associate of director Stanley Goetsch sold shares worth R165 million. Saul Saltzman sold shares worth R38.4 million. Christopher Williams sold shares worth R51 million. They sure weren’t shy to take advantage of the recent rally in the shares.

A director of Investec (JSE: INP | JSE: INL) sold shares worth £1.34 million.

As part of the related party deal for Novus (JSE: NVS ) to acquire Bytefuse, an associate of the CEO of Novus received R10.8 million in Novus shares in exchange for the shares in Bytefuse.

Jan Potgieter, ex-CEO of Italtile (JSE: ITE), sold shares worth R2 million.

An associate of a director of Safari Investments (JSE: SAR) purchased shares worth R1.1 million.

A director at City Lodge (JSE: CLH) sold shares in the company worth R132k.

In a trading statement for the year ended March 2024, Marshall Monteagle (JSE: MMP) flagged a major jump in HEPS from negative 4.4 US cents to positive 5.8 US cents.

Castleview Property Fund (JSE: CVW) released a trading statement for the year ended March. It reflects the final dividend per share as being 42.147 cents per share. This is well more than double the comparative period, but Castleview went through so much restructuring that I wouldn’t put too much focus on the year-on-year move.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

| Pick n Pay | Primeserv | Sephaku)")

")

")

")