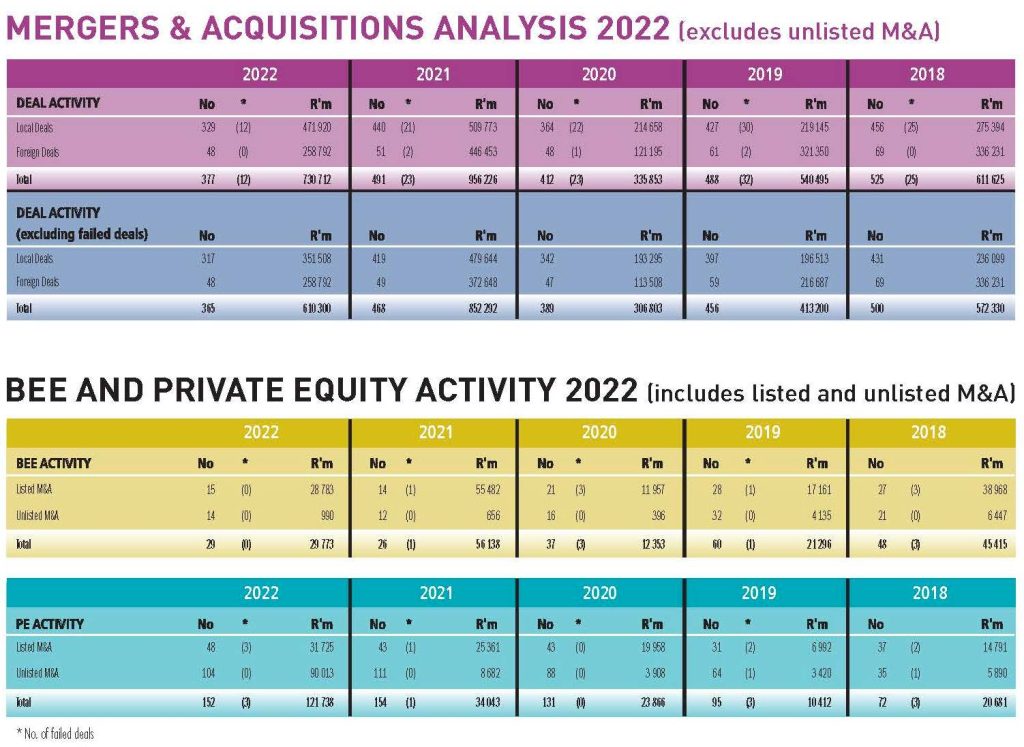

Facts are facts, and while they can be dressed up or down, they reflect the naked truth – dealmaking in South Africa is in steady decline. All but for a slight correction in 2021, due to the release of deals delayed by pandemic lockdowns, the effect of the political and energy related woes faced by ‘SA Inc’ on investor confidence is clearly seen in the number of local M&A deals captured for 2022 – down 7% on the numbers recorded in 2020 and that at the height of the COVID-19 pandemic! The start of 2023 offers insight as to what is to be expected – only four deals were announced during January, this compared with the 26 announced in January the previous year.

The take private of Mediclinic International, shortlisted for the Brunswick DealMakers Deal of the Year 2022, was the largest deal by value for 2022 at £2,05bn (R41,8bn). Gold Fields’ unsuccessful acquisition of Canadian Yamana Gold would have taken top spot at R103bn. The fact that, of the top 10 deals by value for 2022, only three were by SA companies, speaks to the decline in dealmaking in the listed space.

50% of deals used for league table purposes in 2022 fell into three categories. Deals in the Real Estate sector dominated representing 21% of the deals recorded valued at R93,6bn followed by Resources & Energy at 15% (this sector was the highest by value at R203,5bn). Tech deals represented 14% of transactions recorded valued at R39bn.

Behind the scenes – in what DealMakers categorises as general corporate finance activity, companies focused on value creation for shareholders by undertaking share repurchase programmes (R265,9bn versus R115,3bn in 2021) and the distribution of special dividends and unbundlings (R464,2bn versus R63bn in 2021) – most notable being the unbundling by Rand Merchant Investment of its stakes in Momentum, Metropolitan and Discovery, and PSG Group’s distribution of its stakes in its listed portfolio (also shortlisted for Deal of the Year 2022). For the most part, the uptick in the number of listings recorded reflects the growing number (19) of secondary listings undertaken by JSE-listed companies on A2X. But part of the picture is also the increased opportunities now available for domestic investors in the form of new disrupters and innovators.

Private equity continues to be an important driver in the dealmaking space across the continent. In South Africa, two sizeable transactions were recorded: Digital Realty’s acquisition of a majority interest in Teraco Data Environments (R56bn), and the exit by Actis and Mainstream from Lekela Power (R25bn) – the 2022 winner of the DealMakers Private Equity Award.

Given that more than 50% of adults in sub-Saharan Africa remain unbanked, the scope for investment in the fintech space is compelling, and as this number decreases, so the number of opportunities will grow.

Also on the radar of institutional investors are the venture capital alternative investment asset class – although the tough macroeconomic environment and associated rising interest rates will likely curb fundraising outcomes.

The winners of the platinum medal subjective awards are as follows:

Ince Individual DealMaker of the Year

(L-R) Arie Maree (Ansarada), Marylou Greig (DealMakers), Johan Holtzhausen (PSG Capital) and Andile Khumalo (Ince).

Brunswick Deal of the Year – Sanlam Allianz joint Venture

L-R Arie Maree (Ansarada), Iris Sibanda (Brunswick) and the local advisory teams to the deal – Standard Bank, J.P. Morgan, Webber Wentzel, Bowmans and PwC.

Exxaro BEE Deal of the Year – Shoprite Checkers’ evergreen B-BBEE transaction

Arie Marie (Ansarada), Sacha Allie (RMB), Mzila Mthenjane (Exxaro) and Warran Dukas (Shoprite).

Catalyst Private Equity Deal of the Year – Actis exit of Lekela Power

Marylou Greig (DealMakers), Arie Maree (Ansarada), David Cooke (Actis) and Michael Avery (Catalyst).

Business Rescue Transaction of the Year – CIG and CONCO

Marylou Greig (DealMakers), Arie Maree (Ansarada), Martin Liebenberg (Metis), Dean McHendrie (Birkett Stewart McHendrie), Josh Cunliffe (Metis) and Gerhard Albertyn (Metis).

2022 M&A award winners (listed companies)

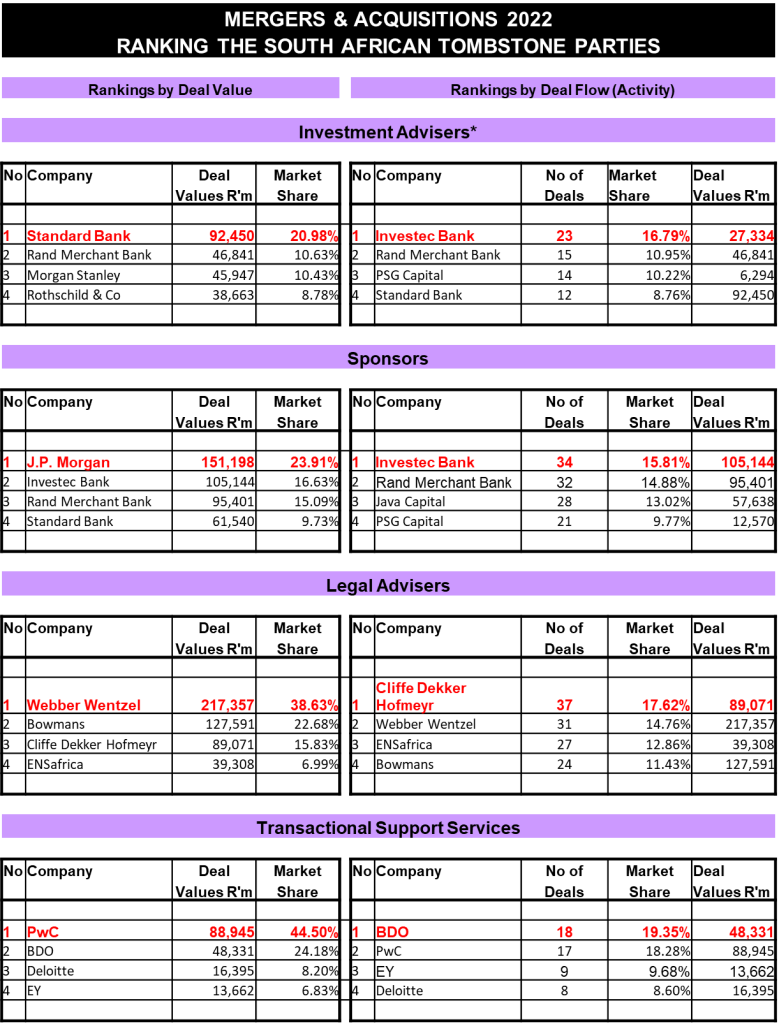

The category of Investment Adviser (by deal value) was won by Standard Bank. (L-R) Arie Marie (Ansarada), Marylou Greig (DealMakers) and Khutso Manthata (Standard Bank).

The category of Investment Adviser (by deal flow) was won by Investec Bank. (L-R) Arie Marie (Ansarada), Marylou Greig (DealMakers) and Marc Ackermann (Investec Bank).

J.P. Morgan was the winner of the Sponsor category (by deal value). Olwethu Matoti, Otsile Matheba (A2X), Thembeka Mgoduso, Athi Ayabulela Noah and Thusani Tshivhase (J.P.Morgan).

The Investec team received the award for top Sponsor (by deal flow). L-R: Rob Smith, Buhle Sithole, Otsile Matheba (A2X), Masetshaba Mabaso and Monica Griessel.

Top Legal Adviser (by deal value) was won by Webber Wentzel.

Roxanna Valayathum received the award on behalf of Cliffe Dekker Hofmeyr for Top Legal Adviser (deal flow) from Marylou Greig.

The award for Transactional Support Services Adviser (by deal value) was presented to PwC. Anneke du Plessis received the award from Hoosain Karjieker (Mail & Guardian).

Nicky Theori received the award for the top Transactional Support Services Adviser (by deal flow) on behalf of BDO from Hoosain Karjieker (Mail & Guardian).

Top Legal Advisers in unlisted M&A

This is the first time awards for unlisted M&A have been awarded.

Top Legal Adviser (by deal value) in unlisted M&A went to Bowmans. Ryan Wessels accepted the award.

Top Legal Adviser (by deal flow) went to Bowmans. Lerato Thahane accepted the award.

Top BEE Advisers in 2022

DealMakers recorded 29 BEE deals during 2022 in the exchange-listed and unlisted M&A space. The top two BEE deals by value were the disposal of 40m Shoprite Checkers shares (a 5.7% stake) to the Shoprite Employee Trust and Anglo American Platinum’s replacement ESOP representing a 2% stake in Amplats to B-BBEE employees.

Irshaad Paruk accepted the award on behalf of RMB for the top BEE Adviser (by deal value) from Marylou Greig.

RMB was awarded top BEE Adviser (by deal flow). Krishna Nagar accepted the award.

Sally Hutton received the award on behalf of Webber Wentzel for top BEE Legal Adviser (by deal value).

Webber Wentzel was awarded the top BEE Legal Adviser of the Year (by deal flow). Ziyanda Ntshona accepted the award.

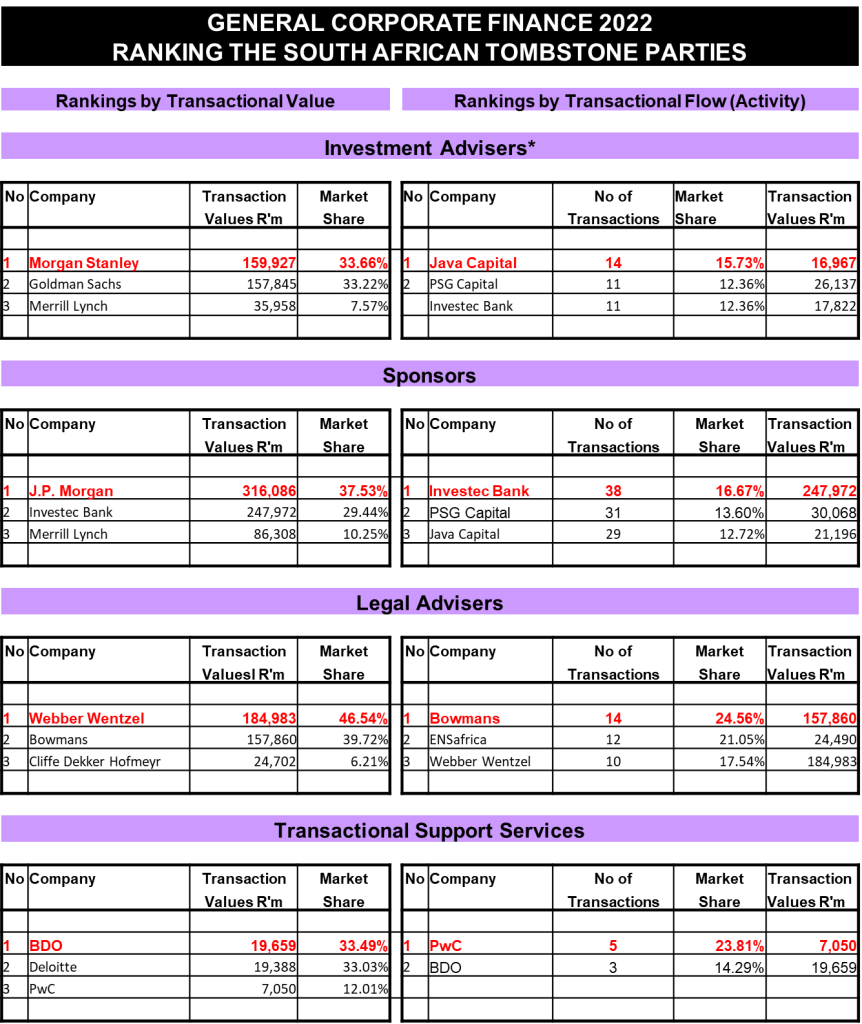

2022 M&A League Tables: SA advisory firms (in relation to exchange-listed companies)

*Investment Advisers include Financial Advisers and all others claiming this category.

2022 General Corporate Finance League Tables: SA advisory firms (in relation to exchange-listed companies)

*Investment Advisers include Financial Advisers and all others claiming this category.

Sable Exploration and Mining is to undertake a fully underwritten rights offer. The company will offer 52,210,464 ordinary shares, in the ratio of 12 new shares for each existing share at a price of R1 per share. The company aims to raise R52,2 million. The offer will be underwritten by James Allan, a director of the company.

Castleview Property has issued 47,839,506 shares at an issue price of R6.48 per share for an aggregate R310 million. The purpose of the issue is to build cash reserves for liquidity management purposes.

Salungano shareholders have been informed that RBFT Investments, which currently holds 18.1% of the issued shares in the group, wants to increase its shareholding and to ultimately delist the company from the JSE. RBFT proposes to acquire on the open market up to 60 million Salungano shares at R1.40 per share. RBFT Investments says the bid is an exempt partial offer and should not be construed as a general offer by RBFT.

Balwin Properties is to take a secondary listing on A2X with effect from 28 February 2023.

Capital & Counties Properties plc will trade on the JSE under its new name Shaftesbury Capital plc with effect from 9 March 2023. The share code will change from CCO to SHC and the company will remain listed in the same sector subsequent to the name change.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Finbond repurchased 45 million shares in the period 14 – 16 February 2023, representing 4.95% of the company’s issued share capital. The shares were repurchased at a price of R0.26 per share for an aggregate R11,7 million. Of the shares repurchased, 25 million will be delisted and cancelled while the remainder will be held as treasury shares which will, following the repurchase represents 9.81% of Finbond’s issued share capital.

South32 has increased its share repurchase programme by c. $50 million in anticipation of a stronger outlook for commodity prices in the second half of its financial year. This will enable the company to return $158 million to shareholders before September 2023. This week the company repurchased a further 1,119,759 shares at an aggregate cost of A$5,1 million.

Spear REIT repurchased 6,941,385 at an average price of R7.62 per share representing 2.83% of the issued ordinary share capital. The shares were repurchased during the period 1 July 2022 to 17 February 2023.

Glencore this week repurchased 11,576,699 shares for a total consideration of £59 million. The share repurchases form part of the second phase of the company’s existing buy-back programme which is expected to be completed this month.

Investec repurchased a further 909,645 Investec shares for a total consideration of R104,28 million. The shares were repurchased during the period 13 February to 17 February 2023. In addition, the company announced that it had repurchased over the period 30 November 2022 to 20 February 2023, 945,321 preference shares for R89,48 million.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 13 to 17 February 2023, a further 2,629,344 Prosus shares were repurchased for an aggregate €74,37 million and a further 317,713 Naspers shares for a total consideration of R1,09 billion.

Seven companies issued profit warnings this week: Aveng, Discovery, Jasco Electronics, Sibanye-Stillwater, Sasfin, Choppies Enterprises and Quantum Foods.

Four companies issued or withdrew cautionary notices. The companies were: Conduit Capital, Brikor, Coronation Fund Managers and Choppies Enterprises.

DealMakers is SA’s M&A publication. www.dealmakerssouthafrica.com

Sibanye-Stillwater which has a 19.9% stake in Australian retreatment mine New Century Resources, has made an unsolicited offer to acquire the remaining stake. The reason given for the offer is that Sibanye is unhappy with the company’s strategic direction and this tailings retreatment and recycling mine fits nicely into Sibanye’s ‘circular economy’ strategy. At an offer price of A$1.10, representing a large premium, the company will pay up to A$120 million (R1,5 billion) if the deal is accepted.

Delta Property Fund’s announced deal to dispose of a property situated at the corner of CJ Langehoven and Cape Road, Gqeberha has been terminated. The sale of the property to Rivadex has been cancelled due to the purchaser’s inability to meet their obligations relating to the cash disposal consideration of R38 million.

Planet42, the car subscription startup addressing transport inequality by putting cars in the hands of people who are unable to access traditional bank credit, has raised $100 million in combined equity and debt funding. The $15 million equity round was co-led by Naspers and ARS Holdings with participation from existing and new shareholders.

Anglo American’s EBITDA is 30% off its record year (JSE: AGL)

Despite this, return on capital employed is still way above the through-the-cycle target

In a year that Anglo American will probably remember for the commissioning of the Quellaveco copper project in Peru, profitability was still fantastic even if the year-on-year story is annoying for investors. Mining companies are cyclical and 2021 was a record year, so consecutive record years was probably too much to hope for.

With production challenges in 2022, the production cost per unit didn’t go in the right direction for several commodities. Compared with a decrease in commodity prices in some cases, earnings came under pressure.

Despite a 30% drop in EBITDA, return on capital employed of 30% is way above the through-the-cycle target of 15%.

Although net debt increased to $6.9 billion as the group invested in its operations, this is still less than 0.5x underlying EBITDA, which is a manageable level.

For fun, I decided to do a long-term chart of Anglo American against competing mining giants Glencore and South32:

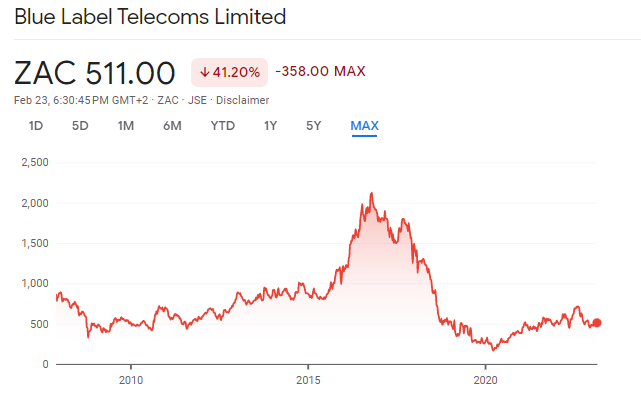

Blue Label rallies 5.4% as the market unpacks the story (JSE: BLU)

These earnings are about as complicated as it gets

At varsity, I remember thinking to myself: “This scenario is ridiculous, this could never happen in real life, Wits is just trying to hurt us.”

Then along came Blue Label Telecoms, with numbers that are so complicated that even Wits lecturers would be impressed.

The problem is that the management team has historically been spectacularly good at losing money for shareholders through misguided and risky transactions. Instead of sticking to the core business, they do all kinds of crazy things. One such thing was to try and resurrect Cell C, which led to a recapitalisation of that company last year. If you truly understood that deal, hats off to you.

Although Cell C has been a financial disaster throughout its life, the current strategy is probably the most sensible we’ve seen. The company is focusing on being the technology that sits between the tower infrastructure (hellishly expensive to own) and companies like Capitec that want to act as Mobile Virtual Network Operators by selling Capitec-branded airtime etc.

If you think Discovery’s numbers are all over the place in terms of normalisation numbers, these are even more intense. Core headline earnings were 3.94 cents per share for the six months ended December, unless you exclude the Cell C recapitalisation, in which case that number would be 51.72 cents.

Likewise, if you ignore several of the matches along the way, the Proteas have been world cup champions several times. Sadly, that trophy cabinet is bare, much like the core headline earnings number at Blue Label.

Here is a short story about the company’s capital allocation track record:

Discovery: where “normalised” is a stretch (JSE: DSY)

Regular readers will already know where this is going…

You may recall a recent earnings update from Discovery that asked investors to casually ignore interest rates, as apparently they have no impact on operations. With the release of results for the six months ended December 2022, Discovery continues to push this narrative.

HEPS as reported fell by 9%. But if you “normalise” those earnings, they increase by 30%. Considering that HEPS is already designed to exclude most of the usual noise found in company earnings, a swing of that magnitude between reported earnings and normalised earnings is extraordinary.

For a company that isn’t affected by interest rates, the term is used no fewer than 53 times in the interim earnings booklet. As another fun statistic, “normalised” appears 51 times. I’ll leave it to you to make your mind up about this.

Distell earnings feel the pressure (JSE: DGH)

Heineken is buying a business that will need to watch its costs carefully

Inflationary environments are tricky things. Top line growth can look great, but profitability is what matters. Some companies can increase prices ahead of inflationary pressures and others simply can’t.

In the six months ended December, Distell’s revenue was up 15.9%. That sounds great, until you see that EBITDA only increased by 0.6% thanks to energy cost pressures and supply chain costs, among other things.

Forex movements had a significant impact here. For example, if you strip them out, headline earnings increased by 8.3% vs. 3.0% as reported.

The lesson here? Be careful of assuming that every industrial/FMCG company benefits from inflation. The analysis is far more complicated than that.

Gold Fields: thank goodness for that break fee (JSE: GFI)

Even the payout ratio is above the usual range thanks to that windfall

With gold production lower and revenue taking a knock as well, this should’ve been an unpleasant period for Gold Fields. Thanks to the gorgeous break fee of $267 million from Yamana though, it was far better than would otherwise have been the case.

The break fee was actually $300 million, but $33 million had been spent on transaction costs. If you’ve ever wondered why bankers fight to get advisory mandates, now you know.

The break fee was such a boost to the balance sheet that the dividend payout ratio for the period was 47%, which is higher than the usual range of 30% to 45%.

With the break fee now in the past, the group will have to focus on the far less lucrative business of trying to get gold out of the ground. With a gold price that appears to be fully committed to inflicting pain on investors, that’s not easy.

Harmony’s earnings are higher, but… (JSE: HAR)

Be careful of the base effect here

For the six months ended December, Harmony’s production costs were between 2% and 10% higher. I’m surprised that Harmony can’t give a tighter range than that, considering that this financial period closed nearly two months ago. Nevertheless, higher underground recovered grades and modest increases in the average gold price helped offset this.

HEPS is expected to be between 10% and 30% higher than the comparable period. Before you get too excited, I must remind you that HEPS in the six months ended December 2021 (i.e. the comparable period) had fallen by 65%. There’s definitely a base effect at play here.

Still, the company expects to achieve its production and cost guidance for the full year. That’s a bit of good news.

Momentum Metropolitan lives up to the name (JSE: MTM)

Earnings look much better in the latest period

For the six months ended December, Momentum Metropolitan expects normalised HEPS to be between 40% and 55% higher.

This solid outcome was driven by the normalisation of the mortality experience in a post-COVID world, as well as improved investment returns. Most of the business operations were positive contributors in this period, other than Momentum Insure which the company notes had a challenging period.

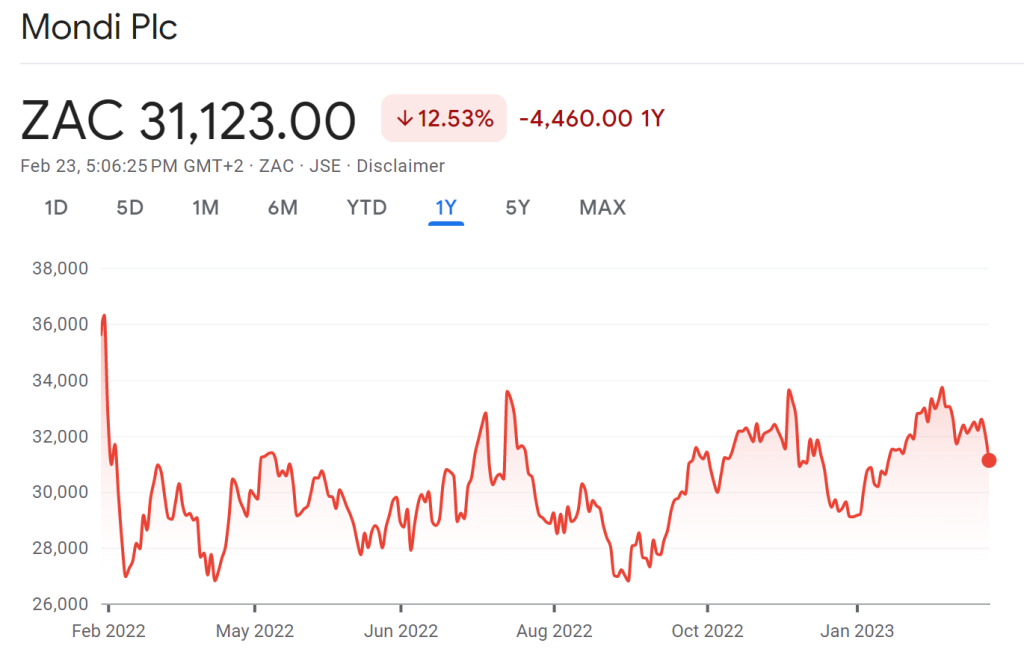

Mondi signs off on a monster year (JSE: MNP)

Cyclical businesses print cash under the right conditions

In the year ended December, Mondi achieved incredible numbers if you exclude the Russian operations. That’s obviously a simplification of note, but you can’t exactly blame Mondi for what happened there.

Without Russia, group revenue increased by 28% and operating profit jumped by 85%. The numbers get even prettier the further down you look, with profit before tax up 119%.

Even including Russia, HEPS increased by 70% year-on-year. This was a massive year for Mondi.

The dividend is only 8% higher than last year, which tells you a lot about how cautious a cyclical business needs to be.

You can see the severe drop in the share price as the conflict broke out in Ukraine, a drop that Mondi is still trying to recover from:

Quantum Foods is now loss-making (JSE: QFH)

This environment is terrible for eggs

Here are the two numbers you need to know from Quantum Foods: in the four months ended January, egg selling prices increased by just 3.9% and feed costs were 25.7% higher. You don’t need an A for maths to realise that this is a major problem. The egg business is expected to report significant losses for the six months ending March.

Across the rest of the business, load shedding is a huge issue. Quantum’s energy costs are up by more than 42% thanks to the need for generators and associated diesel costs.

Probably the only good news at the moment is that Quantum didn’t have to deal with avian flu. We shouldn’t jinx it.

The balance sheet is healthy, which is just as well when the company expects to report a loss for this period. This is despite achieving positive EBITDA, although we don’t know how positive that line in the financials will be.

The net profit is what matters anyway. It will be burning bright red for the six months to March.

Deloitte settles with Tongaat Hulett (JSE: TON)

The auditors are making this problem go away

Without admitting any guilt, Deloitte has agreed to pay R260 million to Tongaat Hulett to settle claims linked to Deloitte’s audit of the company between 2012 and 2018.

The Business Rescue Practitioners have decided to accept the settlement and move on. This makes sense, given Tongaat’s broader balance sheet pressures.

I have no idea what Deloitte’s fees would’ve been over that period, but it would be fascinating to compare the two numbers.

Meanwhile, the date for the publication of the Business Rescue Plan has been extended to 28 February.

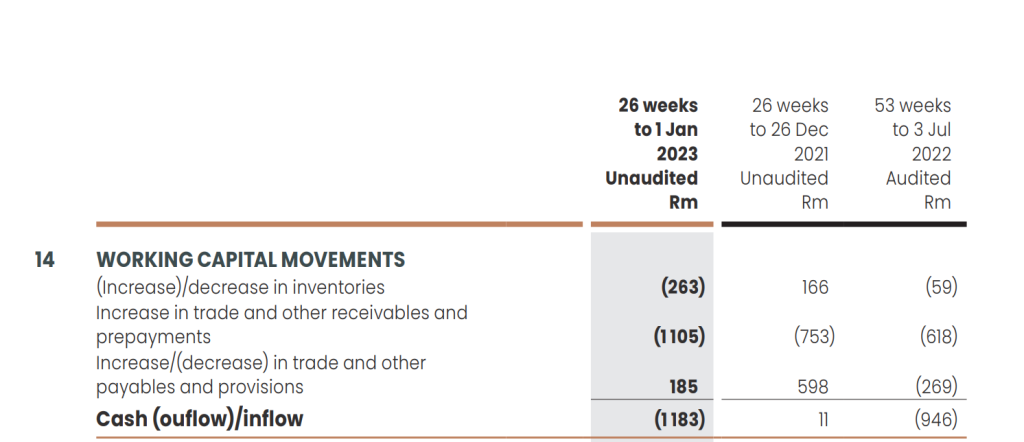

Truworths’ earnings are higher, but watch the cash (JSE: TRU)

Thedividend payout ratio has come down in this period

You can tell quite a lot from the dividend payout ratio, actually. When management is confident, they tend to pay higher dividends. When conditions are tricky or the business is proving to be cash hungry, the payout ratio is moderated.

In the 26 weeks ended 1 January 2023, the revenue and gross margin story at Truworths was very promising. At a time when some competitors went backwards, Truworths grew sales by 13.1% and maintained gross margin at around 53.5%.

Despite this, EBIT only increased by 5.6%. This tells us that there were pressures in operating costs, with operating margin falling from 26.5% to 24.7%. If you dig further into the results, you’ll see that bad debts were a contributor here, which is worrying for the credit retailers.

HEPS increased by 10.3% and the interim dividend was only 6.7% higher, which is where the lower payout ratio is visible. A driver of this might have been the sharp drop in cash generated from operations, which fell from R2.8 billion to R1.7 billion despite the increase in earnings.

To find the source of the cash pressure, you need to go to note 14 in the financials, where you’ll see that aside from investment in inventory, the pressure is from a higher investment in trade receivables i.e. credit sales to customers:

The Truworths share price is up 13.6% this year, as value investors climbed into this retailer that was trading on a modest multiple.

Little Bites:

Director dealings:

As a Transaction Capital (JSE: TCP) shareholder, it’s not great seeing David McAlpin (who runs the all-important Nutun business, previously called Transaction Capital Risk Services) selling shares worth over R5.2m.

Adv. JD Wiese (a non-executive director of Invicta and Christo Wiese’s son) bought preference shares in the company worth R430k (JSE: IVTP),

Family members of the CEO of Spear REIT (JSE: SEA) have acquired shares worth roughly R116k.

A director of Dipula Income Fund (JSE: DIB) has acquired shares worth R82.4k.

A director of Kaap Agri (JSE: KAL) has bought shares worth R76.6k.

Directors of Nictus (JSE: NCS) have bought shares worth around R30k.

As part of broader director appointments, the managing partner of Sanlam Private Equity (Paul Moeketsi) has been appointed to the board of Life Healthcare (JSE: LHC). I never ignore private equity appointments to a board.

If you are a shareholder in Redefine Properties (JSE: RDF), you’ll want to flick through the pre-close presentation available at this link.

Altron’s (JSE: AEL) sale of its ATM hardware and support business is taking longer than planned, with regulatory approval from the Namibia Competition Commission still outstanding.

In bad news for Delta Property Fund (JSE: DLT), the intended sale of the Cape Road property for R38 million has been cancelled as the purchaser couldn’t put the money together.

A director of Sable Exploration and Mining (JSE: SXM) has agreed to follow his rights for R3.67 million and underwrite a further R2.48 million worth of shares. The company is looking to raise R52.2 million in total.

Choppies (JSE: CHP) renewed its cautionary announcement linked to the potential acquisition of 100% in a Botswana based FMCG company.

Trematon’s (JSE: TMT) disposal of the Woodstock Hub property has been determined as fair by the independent expert, so the R16.25 million deal will go ahead.

The plans by I Group Investments to use the Castleview Property Fund (JSE: CVW) vehicle as a listed shell are continuing, with a specific issue of shares to related parties of R310 million.

In the week of the one-year anniversary of Russia’s invasion of Ukraine, it is worth pondering the impact this event has had on the global economy and how it is likely to play out in the future. Chris Gilmour digs in.

Without wishing to labour the point, and without indulging in whataboutism, let me be clear that I view Russia’s invasion as being an act of naked aggression that goes entirely against all norms of a rules-based society. And if Russia succeeds in Ukraine, that won’t be the end of the story. Far from it. Moldova, Romania and Poland will be next, regardless of their EU/Nato membership.

To be sure, the Americans have no doubt gotten involved in similar atrocities over the years, such as their involvement in the Balkans, Iraq and Libya to name but a few, but the economic repercussions were relatively contained. This doesn’t make Russia’s involvement any more palatable, however, as two wrongs don’t make a right.

It has been said that when war comes, the first casualty is the truth. And that is very true, from a variety of perspectives. There can be little doubt that Vladimir Putin firmly believes his own rhetoric when he talks about re-incorporating Ukraine into the greater Russia, regardless of the fact that Ukraine has been a sovereign country ever since the fall of the USSR.

Already, this campaign has claimed many lives on both sides.

Russia does not disclose casualties but the Armed Forces of Ukraine estimate that approximately 135,000 Russian soldiers have been killed so far. Ordinarily, this would be regarded as a massive setback for any country, until one realises where those casualties are concentrated amongst the Russian forces. These are not primarily soldiers from Moscow or St Petersburg, but tend to be conscripts from faraway areas of the Russian Federation such as Chechnya for example. Recently, these forces have been augmented by The Wagner Group of mercenaries, which in turn have been recruiting troops from Russian prisons.

Russia, like China and Japan, is suffering from de-population. As a direct consequence of the Lewis Turning Point, there physically aren’t enough people in the country to keep the economy ticking over, nevermind losing them on the battlefield. The stories of Ukrainian children being abducted and taken back to Russia are not just urban legend. This is one of the few ways left for Russia to try to reverse its current de-population trend and only time will tell if it has succeeded.

The one factor that has astonished western military experts about this whole campaign is the relative ineffectiveness of the Russian armed forces. A year ago, most experts would have given Ukraine virtually no chance against the big bad Russian bear. But within days, it became glaringly obvious that the Russian military wasn’t even close to the might of the old Red Army that trundled into Hungary in 1956 and Czechoslovakia in 1968. This is a hollowed-out version that lacks basic logistics capabilities, that has yawning gaps in its non-commissioned officer ranks and where motivation levels among recruits is exceedingly low. Putting these and other factors together adds up to a dismal cocktail.

And yet, Putin keeps throwing ever more manpower against Ukraine. His empty threats regarding nuclear retaliation carry even less weight than they did when first he first uttered them a few months ago. The west realises that he’s just bluffing. But eventually there will come a point where Russia physically runs out of people in the necessary demographic to maintain its presence in Ukraine. That point is perhaps not too far off now.

If this hypothesis is correct, and Ukraine starts making noticeable incremental territorial gains during the spring and summer, we can reasonably expect desperate counter-measures from the Russians. These may include the use of chemical weapons and so-called “dirty bombs”- ordnance wrapped around small pieces of radioactive material.

There is no room for negotiation on either side. Ukraine is determined to have its territory back to pre-2014 levels and is not prepared to discuss the matter. It is particularly keen to have the Crimean Peninsula back. The Russians are equally determined not to give an inch. However, if enough pressure can be brought to bear on Russia in the form of economic sanctions coupled with crushing defeat on the battlefield, it will have no choice but to retreat.

Throughout its long history, Russia has gone to war with many nations, which is hardly surprising, considering its extensive land mass that borders many other countries. And its track record in these wars is not inspiring, other than in World War 2, when it came back after losing many millions on the battlefield to defeat Nazi Germany on the Eastern Front. Russia/the USSR has been beaten in many wars over the centuries. It is not and never has been invulnerable. For the sake of a long-lasting peace, it is important that Russia is soundly defeated in Ukraine.

This article reflects the views and opinions of its author, Chris Gilmour.

AngloGold tanks 7% on a rough day for mining (JSE: ANG)

I’m so glad that I cut my gold exposure a few weeks ago

I’ve given up on gold. After the rally at the start of the year, I decided to recycle my capital into more lucrative investments, like collecting leafblowers or vintage vacuum cleaners. I’m now convinced that almost anything is a better choice than gold miners.

With another horrible day on the market for these miners and a 7% drop at AngloGold after releasing results, nothing here is proving me wrong.

Despite gold production increasing by 11% in 2022 and all-in sustaining costs per ounce only increasing by 2%, adjusted EBITDA was lower. Why? Because the gold price just refuses to do well in a rising rates environment. It has failed as an inflation hedge and gold has limited utility outside of inflation hedging and jewellery.

The positive element to this story lies in free cash flow, which looks much better year-on-year.

I have no regrets in exiting this industry.

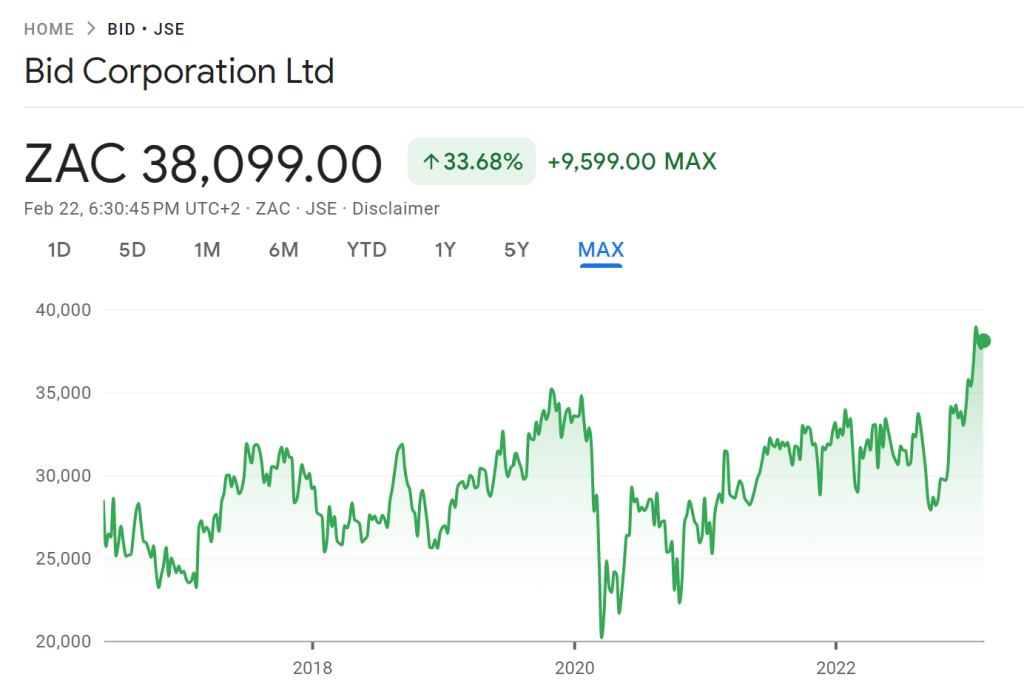

Bidcorp: food service is lucrative (JSE: BID)

The share price has gained another 2% after results were released

The food service industry is a beautiful thing. Restaurants, hotels and even hospitals aren’t going to send someone to the shops to go and buy supplies and ingredients. Instead, they let companies like Bidcorp do the hard work.

This puts Bidcorp at the perfect point in the value chain – literally the shovel in the restaurant gold rush. Restaurants come and go, but Bidcorp doesn’t. The same is true for Sysco ($SYY), the North American equivalent to Bidcorp. We’ve researched this company in Magic Markets Premium, a research platform that you can access at a really affordable rate.

Bidcorp is more than just a restaurant supplier. Only 42% of revenue is from hotels and restaurants, with a further 12% from fast food joints. Other major segments include butcheries, caterers, other wholesalers and healthcare providers.

Another important thing to know about Bidcorp is that the company offers genuinely global exposure to investors, with a small percentage of group revenue (5%) generated in South Africa. As rand hedges go, this is a goodie.

The market knows how good the business is, which is why it trades at such a high multiple that any slowdown in earnings growth gets punished with significant volatility:

Of course, the pandemic drove a massive drop in the share price. Hindsight is perfect, as this would’ve been a good choice to jump into. Recent momentum is sharply upwards and I always get nervous buying a chart like that. Huge climbs tend to correct themselves and consolidate.

Looking at the six months ended December, earnings look fantastic with revenue up 28.1% and HEPS up 45.5%. Cash generated from operations increased by 35.6%. This is why the market has gotten excited.

The “laggard” in this result was the Emerging Markets segment, which includes China that was heavily impacted by lockdowns in this period. Even in that segment, revenue grew 10.2% and trading profit was up 13%. The reopening in China has been part of the recent share price momentum, though it’s worth highlighting that China is also a relatively small contributor to group revenue.

The biggest part of the business actually sits in the UK (25%) and Australia (16%).

Though I would be wary of buying the recent jump, this is one of the ways on the JSE to truly give your money a passport.

Choppies expects a major drop in earnings (JSE: CHP)

Volumes are down and competitors are squeezing Choppies on price

In grocery retail, inflation can either help you or kill you. It all depends on the ability to increase prices, which in turn depends on product quality and the resilience of the customer base.

A less differentiated retailer can get into trouble in these conditions, especially when focusing on lower income consumers who are exceptionally price sensitive.

Choppies has suffered a drop in volumes as a direct result of stiff competition in a tough environment. Pricing increases couldn’t mitigate this impact, which is further proof that Choppies has little ability to hang on to customers for any reason other than price competitiveness.

For the six months ended December, HEPS is expected to be between 29% and 39% lower. Chopped, indeed.

Coronation puts a number on the tax dispute (JSE: CML)

Destination: Constitutional Court

Coronation’s market cap is R10.8 billion. The tax dispute with SARS is estimated to be worth between R800 million and R900 million, based on a decade’s worth of profits being attacked.

That’s not terminal for the company by any means, but it is terminal for the interim dividend.

The fight isn’t over yet. Coronation is going to apply to the Constitutional Court for leave to appeal against the Supreme Court of Appeal judgment.

Although it’s been on a rollercoaster ride this year, the share price is marginally higher year-to-date. Longer term performance is ugly, with a 60% drop over five years.

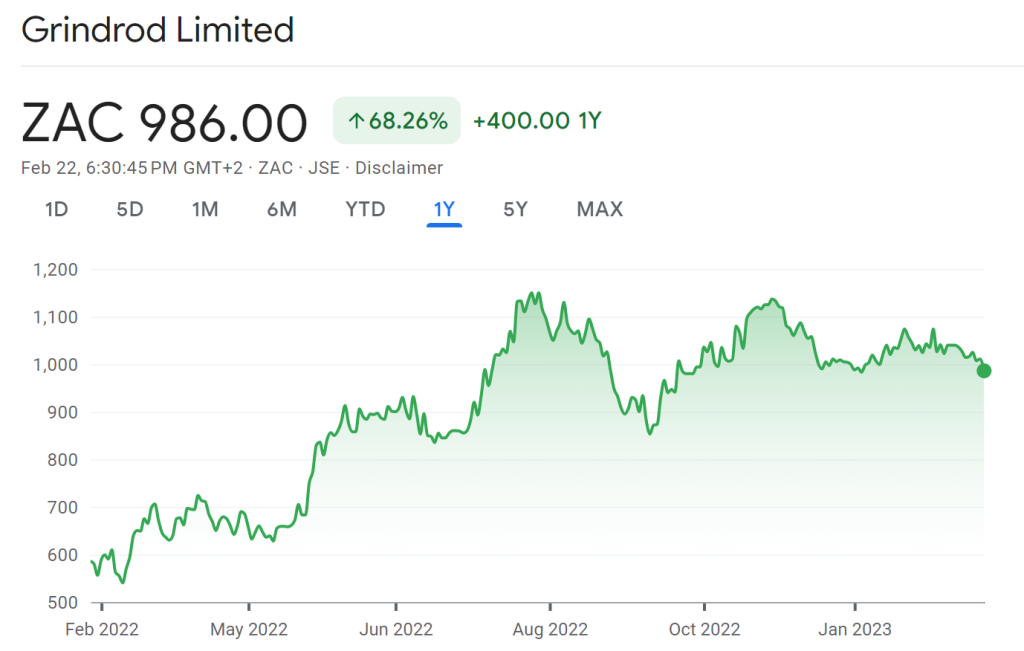

Grindrod continues to grow strongly (JSE: GND)

Although HEPS is up substantially, the market perhaps wanted more

A share price is all about expectations. A share price movement is all about the difference between reality and those expectations. With a 2.5% drop in the price after releasing a trading statement, it seems that the market was hoping for a bit more from Grindrod.

For the year ended December, HEPS will be up between 37% and 43%. Detailed results are due on 2nd March.

After a sharp increase during 2022, the share price seems to have run out of gas:

Sasfin keeps disappointing (JSE: SFN)

In a year that was amazing for banks, Sasfin missed out

If you really don’t like money, you could consider being a long-term investor in Sasfin. Over three years, you would’ve made a whopping 4% in total (plus dividends). In the past year, when other banks have been flying, you would be flat.

In a trading statement for the six months ended December, HEPS is down between 16.8% and 24.7% vs. restated earnings. The restatement had a huge impact on prior period earnings, making them much higher than previously reported.

Not a single Sasfin share changed hands despite the update coming out at 4pm, so that probably tells you everything you need to know.

Standard Bank waves its flag once more (JSE: SBK)

As has been the trend in (most) local banks, earnings are up

In the year ended December, Standard Bank benefitted from the major trends that I’ve been highlighting as bullish for banks: inflation (hence larger balance sheets at corporates and even individuals) and significantly higher interest rates.

We aren’t at the point yet where interest rates are really hurting the credit loss ratio, so banks are performing beautifully (Sasfin excluded).

This trading statement doesn’t give us many details, but we know that HEPS for the year is up between 30% and 35%. Detailed results are due on 9th March.

Little Bites:

Director dealings:

A director of Old Mutual (JSE: OMU) bought shares worth nearly R15k.

Directors of ultra-obscure company Nictus (JSE: NCS) bought shares worth R1.75k.

Kibo Energy (JSE: KBO) sent out a notice for an Extraordinary General Meeting, as the company wants to give the directors the authority to issue a lot of new shares as part of the company’s growth strategy.

Jasco Electronics (JSE: JSC) released results for the six months ended December. It was a very unhappy period in which revenue fell by 14% and the group swung from a profit of R4.7 million to a loss of R23.8 million. The situation is tense, as the company has breached its loan covenants with the Bank of China. CIH is looking to take the group private, so Jasco is likely to leave our market anyway.

Hammerson Plc (JSE: HMN) has had to restate its 2021 financial results based on an accounting interpretation of forgiveness of rental payments during Covid. The property fund’s earnings for FY21 have been restated from £80.9 million to £65.5 million. The change in policy will have a positive impact on FY22 earnings, so watch out for a significant positive year-on-year swing from this change.

The Competition and Markets Authority (CMO) in the UK has approved the merger of Capital & Counties Properties (JSE: CCO) and Shaftesbury without conditions.

As part of an incredibly complicated sequence of events, Safari Investments (JSE: SAR) shareholders will be asked to vote on the company repurchasing a large number of shares for a total price of R311 million. With a market cap of only R1.8 billion, this is big.

Famous Brands (JSE: FBR) has concluded its transaction to buy property from the group founders for R181 million.

Homechoice (JSE: HIL) is highly illiquid, so I’ve included the trading statement under Little Bites as you would have to make many little bites to build up any kind of position. For the year ended December 2022, HEPS grew by between 30% and 50%. The bid-offer spread is wider than the average highway, so good luck with trading this one.

If you happen to be a Trustco (JSE: TTO) shareholder and would like all the details on the accounting restatements that were necessary after the company lost its dispute with the JSE, then refer to the trading statement that was issued on Wednesday. The net asset value (NAV) per share is much higher in the latest numbers, with the share trading at a large discount to NAV anyway.

Sasol delivered a mixed set of results for the first six months of the 2023 financial year, supported by oil and refining tailwinds offset by lower volumes and higher feedstock costs.

No loss of life since October 2021

~550MW renewable energy power purchase agreements conclude in South Africa

R18 billion spend with black-owned suppliers

Invested R780 million in socio-economic and skills development

Venture Capital Fund launched supporting low carbon strategy

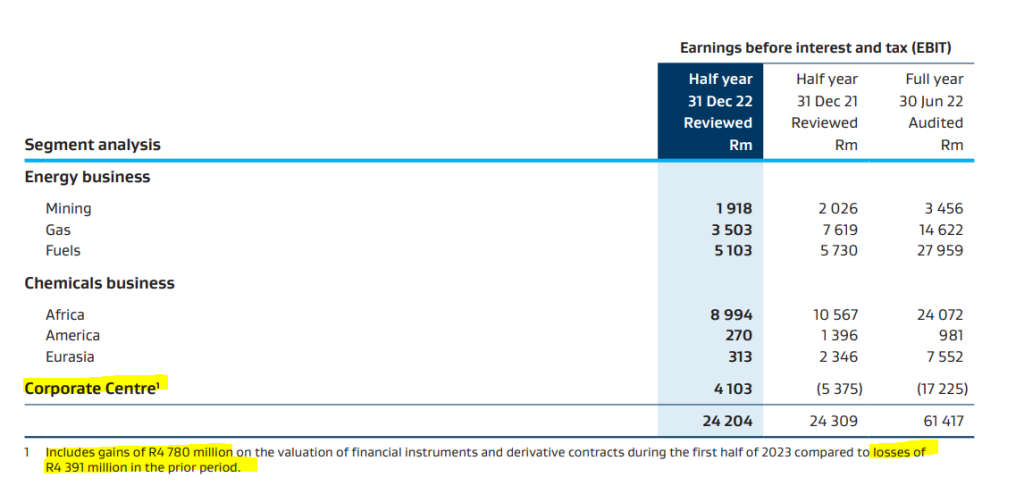

Earnings before interest and tax (EBIT) of R24,2 billion

Core headline earnings per share up 9% to R24,55

Interim dividend of R7,00 per share declared

The impact from the global weaker economic growth, disrupted supply chains, depressed chemical prices and the resultant higher input costs impacted the Chemicals business negatively. Performance of our South African value chain was muted given the scheduled total East factory shutdown at Secunda and operational variability experienced, mainly due to lower productivity and coal quality in our Mining operations, contributing to lower volumes for the six months. The safety of our people and stability of our operations is a key priority. The company will continue to focus efforts on improving business performance to maximise profitability for the full year.

“We navigated several challenges during the period, including safety and operational stoppages at our Mining operations, power supply interruptions which also impacted our suppliers and customers, weaker global economic growth, disrupted supply chains and higher feedstock and energy costs. The last two factors had a particularly severe impact on the profitability of the Chemicals Eurasia and Chemicals America segments,”

said Fleetwood Grobler, President and Chief Executive Officer, Sasol Limited.

Earnings before interest and tax (EBIT) of R24,2 billion remained in line with the prior period, mainly due to a strong pricing environment which was offset by lower volumes and increasing input cost pressures, with declining demand for chemicals globally. Earnings benefitted from gains of R5,1 billion on the valuation of financial instruments and derivative contracts offset by remeasurement items of R6,4 billion.

Remeasurement items include impairments of our Secunda liquid fuels refinery cash generating unit (CGU) (R8,1 billion), South African Wax CGU (R0,9 billion) and China Essential Care Chemicals CGU (R0,9 billion) and a reversal of impairment of our Tetramerization CGU (R3,6 billion) in the United States of America, as well as a profit on partial disposal of an interest in the Area A5-A offshore exploration license in Mozambique (R266 million) and the realisation of foreign currency translation reserves following the liquidation of subsidiaries (R251 million).

“I am excited about the progress we have made towards achieving our 30% greenhouse gas emission reduction target. We have concluded power purchase agreements (PPAs) for the purchase of a significant quantity of renewable energy in South Africa totalling approximately 550 MW. In Mozambique, our gas drilling campaign is progressing ahead of plan, providing us with increased feedstock flexibility up to 2030. Our Sasol ecoFT business is also making good progress, and we have entered into several studies to determine the feasibility of producing sustainable aviation fuel (SAF) from green hydrogen and sustainable carbon sources,” concluded Grobler.

Note: this article was sponsored and written by Sasol

Adcock Ingram has delivered a masterclass here, with great earnings and dividend growth off relatively modest top-line growth.

It’s funny how just one product can cause major swings, with Panado demand normalising and volumes down by 5.4% in the Consumer business as a result. Thanks to average selling price increases of 9.8% though, turnover was higher and trading profit grew by 7.1% as costs were well managed.

In the OTC business, turnover was up 15.3% with volume growth in brands like Allergex. Although gross margin was under pressure from production costs and the weaker currency, trading profit still increased by 8.5%.

The largest segment is Prescription, which increased turnover by 9.4%. Combined with a higher gross margin, the net impact was a substantial 37.4% jump in trading profit.

The disappointing segment was Hospital, which saw turnover decline by 2.2%. Still, with gross margin going in the right direction, trading profit improved by 10%.

As you can see, the trading profit performance was impressive across the board and Adcock Ingram really did a great job here in tricky conditions. With the Single Exit Price increase of just 3.28% this year, cost control will be critical in this industry. The company has warned that gross margin compression is almost unavoidable.

The interim dividend is 20% higher at 125 cents per share and the share price was trading at just under R53.00 in afternoon trade.

Assemble, Avengers! (JSE: AEG)

A 13.4% rally was the reward for punters

I’m old enough to remember when Aveng was trading at one cent per share. Literally. In the heat of the pandemic when the Fed was making it really easy for everyone by letting money fall out of the sky into the economy, the Aveng fans called themselves the Avengers.

It’s worth remembering where Aveng came from:

Buy and hold, they said. It will be fun, they said.

You can’t see it on the chart, but the share price is down 28% over the past year. This is despite Tuesday’s rally. In case you’re wondering what happened to the “one cent” share price, there was a huge share consolidation during the pandemic.

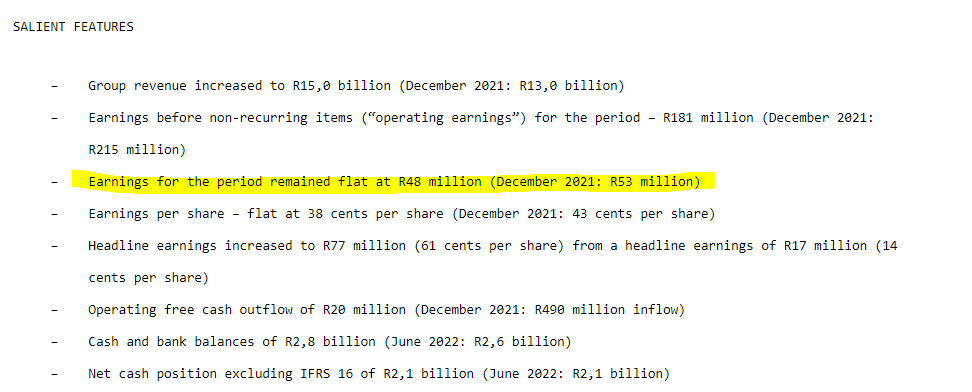

Moving on to results for the six months to December, someone really needs to help Aveng with what “flat” means. When earnings drop from R53 million to R48 million (-9.5%) that’s not “flat”:

Corporate nonsense aside, the business is clearly more profitable and has cash in the bank. The metric they don’t include in the summary is “normalised earnings” which dropped from R82 million to R44 million. So…is it more profitable?

I think the market focused on the debt. R125 million was repaid in the period. There’s another R353 million of “legacy debt” that will be dealt with by the proceeds of the Trident Steel disposal. The trade finance facility will also be settled.

The focus going forward is on McConnell Dowell in Australia and Moolmans in South Africa.

BHP on the wrong end of iron ore and copper prices (JSE: BHG)

Attributable operating profit is down 32%

Managing a mining giant isn’t easy. There isn’t much you can do about commodity prices, so you have to focus on controlling production, expenses and capital allocation.

Despite commodity prices moving against BHP in the six months ended December and revenue dropping by 16%, the company still achieved an EBITDA margin of 54%. Margins were under pressure though, as EBITDA was down 28% year-on-year.

After $3 billion found its way into capital expenditure, there was $3.5 billion in free cash flow for shareholders to enjoy.

Net debt is at $6.9 billion, which is towards the bottom of the target range of $5 billion to $15 billion. An interim dividend of $0.90 per share has been declared, equivalent to a 69% payout ratio.

BHP tells a cautionary tale for the second half of the year, noting a volatile operating environment and a global slowdown in the wake of anti-inflationary policies (i.e. higher interest rates). Much of the commodity demand depends on China.

KAP Industrial Holdings reports a drop in HEPS (JSE: KAP)

Safripol and Restonic had a particularly tough time

KAP Industrial Holdings is a well-diversified business. The downside is that one of the businesses is usually having a tough time, so the company trades in a frustrating price range that now sees it near the 52-week low of R3.68. The price closed at R3.75 after releasing results, down 3.85% on the day.

Revenue increased by 12% in the six months to December. This doesn’t help when operating profit falls by 8%, driven by a 26% decline in Safripol based on lower volumes and pressure in Restonic as well. If you read further down the report, you’ll realise that profitability took a knock across almost the entire business, with revenue up and operating profit either flat or slightly down in several divisions.

With finance costs up sharply, the impact was amplified at HEPS level, down 17% year-on-year.

The cash story is the worst one of all, with cash flow from operations down by 96% due to a R2.2 billion temporary absorption of working capital. Investors will be hoping that “temporary” is the operative word there.

The company describes the near-term outlook as “challenging and uncertain” – but they are confident in the group. Still, there’s no obvious reason why the group’s operating environment should materially improve in the second half of the year, as the macroeconomic pressures aren’t disappearing.

Kumba reports a 46% drop in HEPS (JSE: KIO)

This is despite average realised FOB export prices 13% above the benchmark

Demand for Kumba’s high-grade iron ore helped the company achieve an average price of $113 per wet metric tonne, which is 13% above benchmark prices. With production lower across the group and export sales down by 9%, that wasn’t enough to save this result.

Unit costs increased sharply, driven by inflation and lower production. EBITDA margin fell from 63% to 50%, a situation that would’ve been worse without Kumba’s cost saving efforts.

Free cash flow was 66% lower at R10.4 billion. Total dividends for the year fell by 61% to R40.

With a closing price of R540, this puts Kumba on a trailing dividend yield of roughly 7.4%.

Motus earnings are up, but watch the balance sheet (JSE: MTH)

There’s a lot more debt in the system now

In the six months ended December, Motus achieved revenue growth of 14% and EBITDA growth of 25%. Although operating profit was 22% higher, attributable profit only increased by 9%.

The difference lies in the interest costs (which more than doubled), with Motus having taken on far more debt as part of making strategic acquisitions. Net debt to equity has increased from 30% to 75% and net debt to EBITDA is up from 0.9x to 1.6x. More debt was also required for higher levels of working capital. Of the bank funding (rather than floorplan funding), only 9% is at fixed rates and the rest is floating.

Whilst growth in HEPS of 13% is nothing to get upset about, metrics like free cash flow (down from R2.9 billion to just R425 million) spooked investors. The dividend was up only 9% and investors don’t want to see a dividend growing at a slower percentage than revenue, as it means that the top-line story isn’t being enjoyed by shareholders.

In terms of market share, Motus holds 20.5% share of the retail new car market in South Africa, which contributes 65% to revenue and 78% to operating profit. The company doesn’t disclose the share in the UK and Australia but notes that it maintained market share in those countries.

Growing organically is the “cheap” but difficult way to do it. Motus uses acquisitions to grow faster, with two deals in this period. One was for Motor Parts Direct in the UK, a substantial deal for Motus. The other was a bolt-on acquisition of three Mercedes Benz passenger dealerships and one commercial vehicle dealership.

With the share price down 3%, the market must have a concern or two about this balance sheet. I know that I do.

NEPI Rockcastle: record operating income (JSE: NRP)

Management is bullish about the momentum continuing

Despite the challenging economic background and the obvious problems in Eastern Europe related to Ukraine, NEPI Rockcastle enjoyed resilient consumers in Central and Eastern Europe (CEE) who spent more per visit to the malls. With record net operating income in the year ended December 2022, the management team expects growth to continue.

The company highlights that regional malls play a huge role in CEE, which is different to the high street culture in Western Europe. That sounds rather similar to South Africa!

With a loan-to-value ratio of 35.7%, the NEPI Rockcastle balance sheet is in very good shape.

Distributable earnings per share for the year was 52.15 euro cents, which was 51.5% higher than in 2021. An adjustment is needed for a once-off item, which would see a recurring view on earnings reflecting 20% growth. That’s still impressive.

Sasol was a mixed bag in this interim period (JSE: SOL)

Local supply chain challenges dampened the earnings party

Here’s a little reminder of how crazy things got in the pandemic for Sasol vs. where they are now:

This chart hides the recent momentum, which has been poor to say the least. Sasol has lost 15.7% in the past six months as local operational issues have plagued the company.

We now have results for the six months ended December, a period during which oil prices helped but chemical prices didn’t. Pressure on input costs hit the chemicals side of the business and lower coal quality in the mining business contributed to lower volumes.

This resulted in a flat EBIT performance of R24.2 billion. There were valuation gains on financial instruments of R5.1 billion, more than offset by impairments with Secunda liquid fuels refinery as the main culprit (R8.1 billion).

You have to read really carefully when lookin at Sasol’s numbers, with the hedging at the corporate centre making a huge difference:

The mixed result means that earnings per share was down 3.1% year-on-year, but headline earnings per share (which excludes impairments) more than doubled to R30.90. The group reported core HEPS growth of 9%, coming in at R24.55.

The interim dividend is R7.00 per share, so you don’t get a particularly exciting payout ratio here. Sasol is a hungry animal in terms of capital expenditure and you can see this impact on the cash that eventually finds its way to shareholders. If you read the detailed results, you’ll see that Sasol might end up spending more than guidance on capex this year due to inflationary pressures.

The market was clearly expecting more here, with Sasol down nearly 4% by lunchtime.

Open market bids for Salungano (JSE: SLG)

RBFT Investments wants to increase its stake

RBFT Investments holds an 18.1% stake in Salungano Group and wants to make that bigger. The intent is to eventually acquire all the shares and delist the company. For now, the company wants to acquire up to 60 million shares at R1.40 per share and will be doing so on the open market.

This is an exempt partial offer, not a general offer. If you hold Salungano shares and want the price, you just need to offer the shares on the screen accordingly.

Sibanye wants New Century Resources (JSE: SSW)

Sibanye already holds 19.9% and has made an offer for the rest

Sibanye-Stillwater (which everyone just calls Sibanye) already owns 19.9% in New Century Resources, making it the largest shareholder in the company. New Century is an Australian base metal producer and a top-15 global zinc producer, operating a tailings operation in Queensland.

Sibanye wants to own all of it, which is in line with the company’s “circular economy” strategy that includes a goal to be a global leader in tailings retreatment and recycling.

If all New Century Resources shareholders accept the offer, then Sibanye will need to cough up US$83 million for the deal.

The offer price is A$1.10 per share, a whopping 42% higher than the prior day’s closing price.

Sibanye also released a trading statement and production update for the year ended December, reflecting a drop in HEPS of between 46% and 51%. This reflects the gold sector labour issues in South Africa and the severe weather event at Stillwater. The gold strike had a massive impact, with production down by 50% in that part of the business.

The share price fell 5.5% on the day to close at R39.24. For reference, the 52-week low is R39.24.

Super Group keeps doing well (JSE: SPG)

Another 2% gain takes the year-to-date performance to nearly 23%

For the six months ended December, Super Group’s revenue increased by 34.6% and EBITDA was up 24.2%. This means that margins came under pressure, but it also means that earnings grew considerably.

As we head further down the income statement, it gets exciting again with HEPS up by 30.1%.

The company certainly took advantage of favourable conditions, ranging from strong supply chain demand in South Africa in the transport business and higher revenues per load in Europe through to an increase in new car sales thanks to improved vehicle availability in South Africa and the UK. From an accounting perspective, LeasePlan in Australia was consolidated for the full six months.

Management sounds bullish after this result!

Texton: the market price doesn’t lie (JSE: TEX)

The fund trades at less than a third of NAV

After the initial news broke of the interim dividend becoming only a distant memory, Texton has now released detailed numbers.

The fund is following a rather unusual strategy, with a direct property portfolio valued at R2.2 billion and indirect investments valued at R538.5 million. Essentially, capital has been recycled from the direct portfolio into the indirect portfolio, which is how Texton has gained exposure to the US market.

Although distributable earnings grew by 5.24%, HEPS fell by 28.9% and there is no dividend per share for this period vs. 10 cents in the comparable period. The net asset value (NAV) per share increased by 2.7% to 609.51 cents. The share price trading at just R2 tells the story, less than a third of the NAV per share.

I guess this is what happens when you take shareholder capital and invest it in funds like the Blackstone Real Estate Income Trust instead. I still don’t see a single logical reason why Texton is pursuing this strategy instead of returning capital to shareholders.

The loan to value ratio is at least healthy, coming in at 26.9%.

Tiger Brands is roaring, for now at least (JSE: TBS)

For how much longer can consumers keep this up?

For the four months to January, Tiger Brands managed to increase revenue by a whopping 17%. Here’s the real kicker though: 18% is due to price increases and volumes fell by 1%.

The volume performance obviously varies significantly at category level. Snacks & Treats did well for example, whereas the Baby division reported lower volumes and a drop in market share.

Load shedding cost pressures are still coming for consumers, with costs of R27 million for generators in this period. Tiger Brands hasn’t “yet” recovered this in price, which suggests that food inflation isn’t going anywhere. Each day of stage 6 load shedding costs Tiger Brands R1.5 million in incremental costs.

To prepare for stages 6 – 8 (something most of us are living in denial of), Tiger Brands needs to invest a further R120 million in additional generating capacity. To make it worse, the bulk of this investment would be on diesel and water storage capacity to mitigate the impact of load shedding on the municipal water supply.

The inflation outlook is low double digits in the second half of the financial year. Of course, this depends on Eskom not getting even worse.

For the six months to March, Tiger Brands expects solid operating income growth. I’m once again surprised by the company’s ability to keep growing earnings in this inflationary environment.

At what point will consumers simply break? Or will the pain keep going elsewhere, like into discretionary retailers?

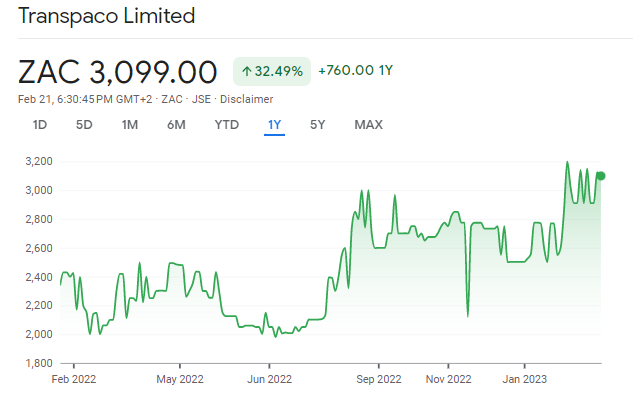

Transpaco reports a major jump in HEPS (JSE: TPC)

The dividend isn’t far behind, up more than 41%

Transpaco isn’t the most liquid stock around, so the share price chart includes those typical horizontal periods where not much happens in the share price:

Still, the 32% gain over the past year has been backed up by earnings. For the six months to December, HEPS increased by 45% to 316.7 cents and the dividend increased by over 41% to 85 cents per share. This was achieved off revenue growth of 19.8%, so this is a perfect example of operating leverage (a percentage change in revenue leading to a higher percentage change in profits because of fixed costs in the structure).

Operating margin expanded from 9.0% to 10.0%. Those aren’t the biggest margins around, but at least they are heading in the right direction.

To add to the happy news, the gearing position (level of debt) improved.

Little Bites:

Director dealings:

Two directors of Spar (JSE: SPP) sold shares worth a total of R1.27m that vested under a conditional share plan, but the announcement doesn’t specify whether this was just the portion to cover taxes.

An associate of a director of Newpark REIT (JSE: NRL) has acquired shares worth R21k.

An associate of a director of Tradehold (JSE: TDH) has acquired shares worth R13k.

Steinhoff (JSE: SNH) has agreed to settle litigation in Europe for EUR202 million. The share price dropped another 3% to 31 cents, which means it is now only 31 cents too expensive.

Shareholders of Premier Fishing and Brands (JSE:PFB) have approved the acquisition of an additional equity stake in Talhado Fishing Enterprises.

The publication of the Rebosis Property Fund (JSE: REB) business plan has been postponed for the fifth time. It is now expected by 3rd March.

Before I delve into production numbers at Anglo American Platinum (Amplats), I have to point out the relationship between the PGM prices and the USD/ZAR cross. The dollar basket price per PGM ounce fell by 8% and the rand basket price increased by 2%. Our currency depreciation obviously lends a helping hand to the Amplats business.

Despite this, production issues and lower volumes meant a 24% decrease in revenue. Those fixed costs sadly don’t disappear just because production is lower, so adjusted EBITDA fell by 32% and EBITDA margin decreased from 65% to 57%.

Headline earnings per share fell by 38% and net cash fell by 43%. With that combination, it’s perhaps not surprising that the dividend fell by 62%.

The share price only fell by 2% as these results were well telegraphed to the market ahead of time.

CA Sales Holdings jumped 7.5%

This FMCG group released exciting numbers

In a trading statement covering the year ended December 2022, CA Sales Holdings indicated that HEPS would be up between 29% and 34%. That’s a juicy growth rate by any standards, with an expected HEPS range of 76.89 cents to 79.87 cents.

After the share price closed 7.5% higher at R7.05, this is still only a Price/Earnings multiple of around 9x at the midpoint of guidance.

City Lodge is profitable again

But HEPS looks a little light vs. the share price

In case you’ve been living under a rock, the tourists are back and the good times are flowing. City Lodge is thrilled to see the end of COVID, with numbers that are back in the green.

If we exclude the once-off settlement for business interruption insurance, then City Lodge achieved HEPS for the interim period of between 12.6 cents and 14.5 cents. That’s a vast improvement from the loss-making comparable period that was ruined by the pandemic.

Still, with a share price of R4.81, that doesn’t seem like a particularly great outcome. Even if we double this period, a simplification of note when you consider an ongoing month-on-month recovery (mitigated to some extent by recognising that the summer holidays must be the best time for this business), then it’s on an annualised Price/Earnings multiple of 17.8x.

Hmmm….that’s rather a lot, isn’t it?

The share price closed 2.8% lower after this announcement.

A positive Mpact

A 6.5% rally rewarded shareholders on Monday

For the year ended December, revenue from continuing operations was up 7%. The underlying operations did even better than this, as the base period included the major distribution agreement that Mpact terminated. Without that impact, revenue would’ve been up by 15% and volumes by 6%, so the benefit of higher pricing is clearly visible.

The volume growth was all in the Paper business, as the Plastics business saw flat volumes year-on-year across most of that division.

The joys of operating leverage are being felt here, with earnings before interest and tax (EBIT) up by 23% year-on-year. The “I” in “EBIT” is a bit painful though, with net finance costs of R180 million in 2022 vs. R140 million the year prior, driven by increased average net debt and higher interest rates.

Due to capital expenditure and increased working capital, net debt increased from R1.756 billion to R2.327 billion.

Looking ahead, Mpact will be investing R1.2 billion in its Mkhondo Paper Mill in response to growth in demand from the South African export fruit sector. Mpact hasn’t been shy to invest in its operations in general, including in major solar projects.

In case you’re wondering about discontinued operations, the Versapak business is held for sale. The company reported 20% growth in revenue and a strong improvement in profitability from net earnings of R2 million to R65 million. This is encouraging for potential offers that Mpact might receive.

I would really love to tell you what the HEPS increase will be. Sadly, the formatting of the SENS announcement was a complete disaster, so I’ll just include it here for you to decide for yourself:

Either way, earnings are up strongly and the market liked that, even if nobody was quite sure how to read this.

Murray & Roberts says bye-bye to Bombela

Strong shareholder support was achieved

This is a short update for Murray & Roberts, but one that is too important to be buried in the Little Bites. The company desperately needs to make progress on fixing its balance sheet, with the disposal of Bombela Concession Company firmly part of that strategy.

At the general meeting of shareholders to vote on the deal, it received overwhelming support, with 99.988% of votes cast in favour of the transaction.

Clearly, this deal is moving forward.

No dividend at Texton

There’s an abundance of caution here

If you invest in a property fund, it’s usually because you want to earn a dividend. Sorry for you if Texton was your fund of choice, because the old dividend of 10 cents per share is but a distant memory. For the six months to December, there is no interim dividend at all.

This is despite an increase in distributable earnings of 5.2%.

The board wants to “conserve cash” and “manage its balance sheet liquidity through the current interest rate environment” – so time will tell how this plays out.

WBHO updates its earnings guidance

There is a strong year-on-year improvement in profitability

Construction group WBHO has finished its work on the accounting impact of the Australian tax position on the 2021 numbers.

Based on this calculation, HEPS from continuing operations is expected to be between 800 cents and 828 cents for 2022 vs. 591 cents in the comparable period, an increase of between 35% and 40%.

Little Bites:

Director dealings:

A director of a subsidiary of Tharisa has sold shares worth R221.5k

A prescribed officer of Barloworld has bought shares worth R142k.

An associate of a director of Huge Group has bought shares worth R58.2k.

If you are an Alviva shareholder, keep an eye on your trading account on 6th March. That’s when the cash from the implementation of the Alviva delisting should be yours for the taking.

Spear REIT repurchased 2.83% of shares in issue between July 2022 and February 2023, at an average price of R7.62 per share. The current share price is R7.13, so ongoing buybacks will hopefully continue to bring the average repurchase price down.

The City of Johannesburg Valuation Appeal Board has upheld the municipal valuation proposed by the city for Sandton City, so the rates bill for Liberty Two Degrees is higher than they would like. With a provision needing to be recognised for arrear rates and interest, the impact on the year ended December 2022 is 2 cents per share. On a closing share price of R4.45, that’s not a huge impact on the yield.

Jasco Electronics Holdings increased 9% despite reporting a headline loss from continuing operations of between -6.3 cents and -6.5 cents. For those looking for silver linings, at least the order book is a lot healthier.

In the latest episode of Ghost Stories, Renergen CEO Stefano Marani took a break from a busy capital raising schedule to have an in-depth conversation with The Finance Ghost. After the first half of the show focused on the background to the project and the importance of helium to the global economy, the second half looked at the capital raising strategy.

Topics covered in the show include:

Stefano’s background in investment banking in the pre-GFC days, with the events of 2008/2009 leading to a career shift and the eventual investment in what would become Renergen.

The future-proof nature of helium, including several examples of industrial and technological applications for which there is no known substitute.

The importance of government support over the lifetime of this project.

South Africa’s geographical and geopolitical positioning, both of which are helpful to Renergen.

The logistical challenges around transportation of liquid helium.

Renergen’s plan to self-power its operations, making it grid agnostic in a country that we know doesn’t have enough electricity.

The Cryo-Vacc and the helium tokens – what happened to these headline grabbers?

The group structure and the way this drives the capital raising strategy with asset-specific funding partners.

An overview of Phase 1 vs. Phase 2 of the project.

The use of accelerated bookbuilds and why they are a necessity in South Africa vs. rights offers.

The capital raising strategy going forward, including the pursuit of a full listing on a US exchange rather than an OTC listing.

The likelihood of achieving meaningful liquidity in the US vs. what a company like Karooooo has experienced on the Nasdaq.

And on a fun note – the positive social impact of Renergen’s sponsorship of local rally racing.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")