")

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

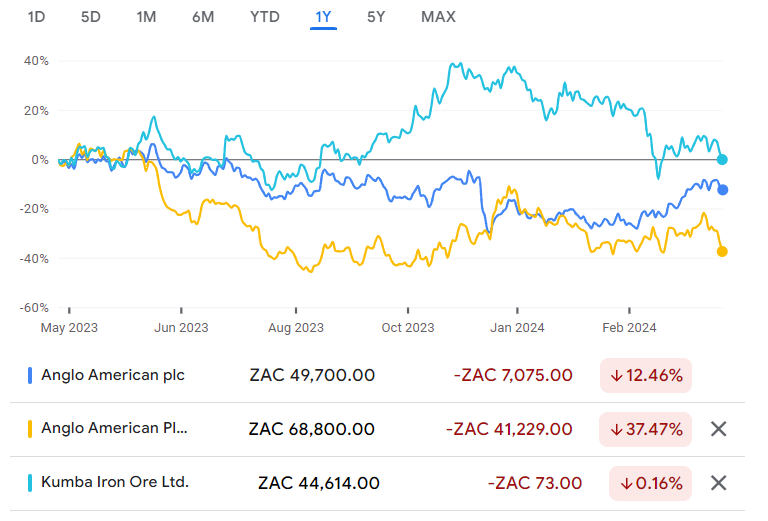

Anglo American’s board rejects the BHP proposal (JSE: AGL | JSE: BHG)

Let the games begin…

The board of Anglo American has unanimously rejected the proposal put forward by BHP. Apart from the structural complexities in the proposal that the board doesn’t like, the main reason is that they believe that the proposal undervalues Anglo American and its prospects.

The copper assets are the focus of course, with the chairman of the board commenting that shareholders still stand to benefit from the full impact of the investments in copper. I’m sure BHP would agree with that statement, behind closed doors at least, as why else do they want to acquire Anglo?

They also describe the BHP proposal as being opportunistic. I think just about every successful acquisition in history that creates shareholder value has been opportunistic, otherwise what’s the point?

Right now, there’s no firm offer on the table. At this stage, the board of Anglo recommends that shareholders take no action in relation to the proposal.

Here’s what it looks like when deals start being thrown around in the market:

The question is: will BHP put in a firm bid and on what terms? Or will another bidder with a taste for copper emerge?

Finbond: are they profitable? (JSE: FGL)

The trading statement has left more questions than answers

Finbond released a trading statement dealing with the year ended February 2024. It notes that HEPS will increase by at least 20% vs. the headline loss per share of 15.1 cents for the year ended February 2023. This isn’t as simple as it sounds.

Firstly, they refer to HEPS rather than a headline loss. Secondly, “at least 20%” is the minimum required disclosure under JSE rules, so the improvement could be vastly higher. Thirdly, they only made a loss per share of 2.3 cents in the interim period, so there’s a chance that they have swung into the green.

It’s frustrating when companies make things obscure. It really wouldn’t have taken much effort to release a clearer trading statement.

Impala Platinum commences a retrenchment process (JSE: IMP)

PGM prices just aren’t giving the sector any relief

Job losses in the mining sector are becoming a worrying trend, with PGM prices putting great pressure on local operations. This impacts jobs both at the mines and the corporate head office. As sad as this is, the decision taken by companies is always on the basis of rather cutting 3 jobs than shutting down a company and losing 10 jobs in the process.

The maths isn’t quite that severe in this case, with Impala Platinum looking to potentially reduce labour costs by 9% across Impala Rustenburg, Impala Bafokeng and Marula, along with a 30% reduction in costs at head office. In total, 3,900 positions could be affected.

Remember, this is the same company that got into a bidding war for Royal Bafokeng Platinum and won. Here we are with retrenchments just a short while later.

Invicta to combine KMP with Kian Ann (JSE: IVT)

The group is looking to strengthen its international holdings

Invicta holds KMP Holdings (a leading supplier of aftermarket heavy-duty diesel engine parts) through Invicta Global Holdings. KMP is based in the UK and US and services a global client base in over 150 countries. Invicta also has a 48.81% stake in Kian Ann Engineering based in Singapore.

Although this transaction means that Invicta is effectively diluting its interest in KMP, the group has taken the decision along with the other shareholders in Kian Ann that KMP would be better off within that entity, benefitting from the procurement and manufacturing network of Kian Ann.

To achieve this, Invicta Global Holdings will sell the shares in KMP Holdings to Kian Ann for roughly R300 million. Invicta originally paid around R270 million back in 2022. The uplift is almost entirely thanks to the rand though, as the base selling price now vs. the purchase price then is only different by around £200k.

KMP will also repay shareholder loans and claims of around R156 million to Invicta. Considering that KMP made net profit of around R31 million for the year to March 2023, it feels like Invicta is getting paid a strong multiple here, particularly for a business that hasn’t delivered exciting earnings growth in the past few years.

Hopefully, combining it with Kian Ann will change that.

Oasis Crescent: the property fund without debt (JSE: OAS)

As a Shariah-compliant fund, this is an unleveraged play on property

Oasis Crescent Property Fund is a fascinating thing. This is basically what you get when you strip leverage out of property returns entirely, as the fund cannot have any debt as a Shariah-compliant structure. Despite not using leverage, the fund proudly notes a unitholder return of 10.3% per annum since inception compared to inflation of 5.6%.

Sometimes, not having debt is actually pretty useful, even in property. Just ask executives of REITs in the past couple of years, particularly those with significant exposure to office property.

For the year ended March 2024, Oasis Crescent grew its distribution including non-permissible income by 12.9% to 112.2 cents per unit. Investors pay up for this thing, as that’s only an earnings yield of 5.4% based on the current share price. Remember, most investors in a Shariah-compliant structure can’t use many of the fixed income alternatives, like money market and other accounts.

The share price is flat over 5 years despite some volatility along the way.

Reinet enjoyed an uplift this quarter in the fund (JSE: RNI)

The fund numbers are a precursor to the listed group numbers

Between December 2023 and March 2024, Reinet fund saw its net asset value per share increase by 7.9% in euros. That’s a very strong quarter! The fund holds the investments in Pension Insurance Corporation and British American Tobacco amongst others.

This isn’t exactly the same thing as the group net asset value per share, but it’s always a good directional indication of how the listed NAV has performed in a given period.

Renergen’s maintenance cycle hurts profits (JSE: REN)

Junior miners are generally loss-making for obvious reasons, but investors are getting impatient

Renergen is right on the cusp of becoming a producer of helium rather than a promiser of it. Getting across that line has proven to be really difficult though, with a few technical issues along the way that have irritated the market. This is why the share price has shed half its value over the past 3 years. It’s also way down from the peaks above R43 per share, currently trading at R12.50.

The bears in the market don’t need much to set them off when it comes to Renergen, with the latest trading statement adding fuel to the fire. The headline loss per share for the year ended February 2024 will be between 72.7 cents and 76.7 cents vs. a headline loss of 19.89 cents in the prior period. This deterioration is due to the downtime experienced during the maintenance cycle.

Sibanye wants to equity-settle its convertible bonds (JSE: SSW)

Currently, settlement would be in cash

In 2023, Sibanye-Stillwater placed $500 million in bonds due November 2028 with a coupon of 4.25%. The proceeds were used to fund the Reldan acquisition, with the remainder retained for general corporate purposes.

The bonds are currently cash-settled instruments, which is a drag on the Sibanye balance sheet. It significant reduces the flexibility of the company. To try and address this, shareholders are being asked to approve that the bonds can be converted into ordinary shares at a price of R24.5792 per Sibanye share. The current share price is R22.19. That might not sound like an issue right now, but remember these bonds will exist until 2028. By then, one would certainly hope that the share price has moved higher.

This is a material drag on the share price, as a conversion of all the bonds would represent 13.21% of shares in issue!

It sounds highly punitive, but remember that Sibanye raised debt at a lower rate than would otherwise have been the case without the conversion. This is a typical mezzanine funding structure. Such structures are more expensive than vanilla senior debt by design, which is why they are only used when senior debt isn’t a viable alternative.

Little Bites:

- Director dealings:

- A director of Sabvest Capital (JSE: SBP) has bought shares worth R1.7 million.

- Aside from a trade related to share options that was included in the same announcement, a prescribed officer of Capitec (JSE: CPI) has bought shares worth R1.67 million.

- Alphamin (JSE: APH) has declared a dividend of 41.78220 cents per share, payable on 24 May. The current share price is R15.89.

- As Eastern European property fund MAS (JSE: MSP) continues to navigate a very difficult funding environment, the company announced that €40.2 million worth of notes have been issued in a private placement. They are due 2029 and carry a rate of 6.50%. They were issued as an exchange for existing notes due 2026 with a rate of 4.25%. The rate is higher obviously, as is to be expected in this environment, but at least the maturity is three years later.

- It is no surprise whatsoever that Sasfin’s (JSE: SFN) disposal of the Capital Equipment Finance and Commercial Property Finance businesses to African Bank for a very lucrative price received almost unanimous approval from Sasfin shareholders.

- A subsidiary of Sephaku Holdings (JSE: SEP) has repurchased a further 2.72% of its issued shares for R7.2 million. The average price paid was R1.04 and the current share price is R1.10.

- Absa (JSE: ABG) announced that Deon Raju has been appointed as the Group Financial Director. He’s been at Absa since 1999 and his most recent role was Group Chief Risk Officer, held since June 2021.

- Anglo American Platinum (JSE: AMS) has announced the appointment of Sayurie Naidoo as CFO of the group. She has been with Anglo American for over 15 years

- Kibo Energy (JSE: KBO) remains stuck on R0.01 per share despite regular SENS announcements. The latest one is that the Pyebridge project has passed the requirements to retain the Capacity Market contract that makes gross margin of £308k per year. The site has secured further contracts to ensure minimum annual gross margin of £817k until 2028. The 2nd phase at Pyebridge is in preparation phase and will be funded by RiverFort under the new funding agreement. Based on the absolute lack of action in the Kibo share price, RiverFort seems to be getting the bulk of the economic benefits from Kibo’s subsidiary Mast Energy Developments.

- Putprop (JSE: PPR) has proposed an odd-lot offer. This is a classic case of where it makes sense, as those holding fewer than 100 shares each make up a whopping 52% of the total number of shareholders in the company. They hold just 0.01% of shares in issue. This means that the compliance burden far outweighs the benefit of such a widely held register. The price will be a 5% premium to the 30-day VWAP as at 3 June 2024.

")

")

")