Accelerate Property Fund is to proceed with a R50m fully underwritten renounceable rights offer to raise required working capital. The company will issue 71,428,571 shares for a subscription price of 70 cents per Rights Offer share in the ratio of 6 Rights Offer shares for every 100 APF shares held. The subscription price represents a discount of 31.14% to the 30-day volume weighted average price on 9 December 2022.

In an off-market block trade, AltX-listed Heriot REIT, the company which in 2022 undertook an unsuccessful take private of Safari Investments RSA, has acquired 20 million Safari shares. The shares, purchased from SA Corporate Real Estate, at R5.60 per share was for a total consideration of R112m. Following the acquisition, Heriot and its concert parties collectively hold a 47.1% stake in Safari.

Renergen, an emerging integrated renewable energy producer, has announced plans to list on the Nasdaq Stock Market later this year to raise additional funding for the second phase of its Virginia Gas Project.

As part of its capital optimisation strategy, Investec Ltd this week acquired on the open market a further 476,138 Investec Plc shares at an average price of 518 pence per share (LSE and BATS Europe) and 440,987 Investec Plc shares at an average price of R110.00 per share (JSE).

Chrometco, Efora Energy and New Frontier Properties updated shareholders on their suspension status. Chrometco remains suspended due to the late publication of the provisional annual financial statements for the year ended February 2022. The company is struggling to appoint new auditors due to two subsidiaries within the group being in Business Rescue. Efora is yet to publish its consolidated annual financial results for the year ended February 2021 citing delay in the finalisation of subsidiary Afric Oil’s results which has since been sold. New Frontier Properties were suspended for the late publication of the 2020 financial statements.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Glencore this week repurchased 18,000,000 shares for a total consideration of £98,14 million. The share repurchases form part of the second phase of the company’s existing buy-back programme which is expected to be completed by February 2023.

Investec continued with its repurchase programme, repurchasing 510,006 shares for a total consideration of R55,8. The shares will be cancelled and reinstated as authorised but unissued shares.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 23 to 27 January, 2023, a further 2,979,757 Prosus shares were repurchased for an aggregate €229,3 million and a further 464,150 Naspers shares for a total consideration of R1,6 billion.

Three companies issued profit warnings this week: Italtile, Sea Harvest and RCL Foods.

Three companies issued or withdrew cautionary notices. The companies were: Lux Holdings, African Equity Empowerment Investments and Ellies.

Environmental, social and (ESG) review, in broad terms, refers to the examination of a company’s environmental, social and governance practices, their impact, and the company’s performance against benchmarks. The implementation of ESG practices has swiftly risen up the corporate agenda as a mainstream issue in the last few years, and has profoundly reshaped business models globally.1

As a ripple effect of this, ESG factors are now steadily gaining importance in mergers and acquisitions(M&A) transactions, and are predicted to become embedded across M&A in the coming years.2 South African businesses are, therefore, advised to harness this global appetite for ESG by taking into account such considerations in their M&A transactions, as a means to achieve maximum value and monitor risks. In doing so, South African businesses will be set to unlock competitiveness and profitability, and attract investment.3

An overview of ESG factors

The most prevalent ESG factors which have prompted many businesses worldwide to focus on environmental impacts and risk management practices include:

1) Environmental factors, such as climate change, energy, water scarcity and usage, biodiversity, destruction of natural habitats, environmental pollution and waste management;

2) Social factors, such as employment and labour issues, employee benefits, diversity, health and safety, human rights, community relations, and the manner in which broad- based black economic empowerment is advanced; and

3) Governance factors, such as corporate structure and management, strategic direction and oversight, compliance, anti-bribery and corruption, board composition and executive compensation.4

Growing pressure to support the inclusion of ESG in M&A transactions

Investors believe that companies with strong ESG initiatives are more lucrative investments, pose less risk, and are better positioned for the long term. If a company fails to consider all important ESG aspects, it risks reputational damage. Globally, we have witnessed growing regulatory frameworks which now prescribe intensified accountability for ESG in M&A transactions, such as the new efforts to enhance disclosure of ESG factors in M&A transactions in the United States.5

Locally, the regulation of ESG principles has already been adopted for pension funds, insurers and the Public Investment Corporation.6 However, recently, there have been widespread voluntary ESG initiatives, which indicate that South Africa has been taking steps to follow international ESG trends in M&A. These initiatives include:

• the revised draft Code for Responsible Investing in South Africa (CRISA) 2.0, which stipulates that investment activities must reflect the integration of material ESG factors and which should also reflect in due diligence investigations;7 and

• the Johannesburg Stock Exchange (JSE) Sustainability and Climate Change Disclosure Guidance document, which caters to the growing expectations from various stakeholders on businesses to report on respective impacts on the environment, people and financial performance, incorporating both global and local context to help companies understand how the various standards relate to one another.8

Businesses also ought to take heed of the final guidelines on the considerations to be taken into account when considering the impact on the public interest, published by the Competition Commission in 2016. These guidelines consider the social aspect of ESG. It is typically a conscientious process. For instance, in the merger where ECP Africa Fund IV LLC & ECP Africa Fund IV A LLC sought to acquire Burger King (South Africa) RF (Pty) Ltd and Grand Foods Meat Plant (Pty) Ltd, the Commission initially prohibited the merger on public interest grounds that the shareholding of historically disadvantaged persons in Burger King would decrease from more than 68% to 0% as a result of the merger.9 The Commission prohibited the merger on such grounds for the first time ever. It saw parties having to go back to the drawing board to reconsider public interest concerns, which were later addressed by the parties and accepted by the Commission. This case serves as a pertinent example of the importance of considering social wellbeing and economic needs of South African communities in relation to ESG. Seemingly, investors are taking ESG risks into account now more than ever, due to global pressures as well as increasing shareholder, employee and consumer activism.

ESG considerations in M&A due diligence and M&A agreements

Due diligence allows the buyer in the M&A process to confirm undisclosed details about a selling company’s financials, contracts, personnel and customers. The buyer is then able to derive a complete picture of the business or company being acquired. In light of the ESG-focused shift in the market, we urge buyers to broaden the scope of their due diligence to include performing targeted ESG investigations, in order to identify ESG-related risks which may influence a target’s price and overall deal structure. Once fully aware of the potential liabilities and risks of a transaction, companies may mitigate ESG risk through the transaction agreement. A focus on ESG can be a competitive advantage for businesses, private equity funds and many other strategic acquirers. By integrating ESG considerations into each stage of the deal, this will inform the buyer of any potential impact of the merger or acquisition on its sustainability strategy and the long-term value of the combined entity.

Red flag checks may include assessing the future fitness of the target and relevant assets, and media scans to understand any major ESG-related risks. Thereafter, the buyer can look to address any ESG risks in the transaction agreement through specific indemnities, targeted representations and warranties addressing ESG matters, or through various pre-closing conditions or post- closing covenants by the seller/s. If an issue cannot be addressed pre- or post-closing, such as non-compliance with ESG-related regulations, the buyer may wish to negotiate a reduction in the purchase price to reflect the risk assumed.10

Conclusion

Although ESG is still in its budding phase in South African M&A, it is critical that investors, companies, private equity funds and other strategic acquirers follow in the footsteps of global majors in the widespread incorporation of ESG factors in M&A. Any delay in doing so may result in companies risking reputational damage in the long run and losing out on access to capital and lucrative opportunities often offered by ESG compliance.

(Peterdy, “A Framework for Understanding and measuring how sustainably an organisation is operating” 2022 (https://corporatefinanceinstitute.com/resources/knowledge/other/ esg-environmental-social-governance/) accessed on 20 October 2022)

(Deloitte, “Unlocking transformative M&A value with ESG” 2022 (https://www2.deloitte.com/us/en/pages/mergers-and-acquisitions/articles/unlocking-transformative-m-and-a- value-with-esg.html) accessed on 20 October 2022)

(Kim, Mallia-Dare “ESG: Creating value and mitigating risk in mergers & acquisitions” 2022 (https://www.millerthomson.com/en/publications/articles/esg-mergers-acquisitions/) accessed 20 October 2022

(Davis, Kitcat “Environmental, Social and Governance Law South Africa”, 2021 (https://iclg.com/practice-areas/environmental-social-and-governance-law/south-africa) accessed on 19 October 2022)

(Gez, Pullins, Druehl, Ali “SEC Proposes Amendments to Rules to Regulate ESG Disclosures for Investment Advisers and Investment Companies” 2022 (https://www.whitecase.com insight-alert/sec-proposes-amendments-rules-regulate-esg-disclosures-investment-advisers-investment#:~:text=On%20May%2025%2C%202022%2C%20the%20US%20 Securities%20and,disclose%20extensive%20climate-related%20information%20in%20their%20SEC%20filings.2 (2022 accessed 20 October 2022)

(Davis, Kitcat, 2022)

(Second Code for Responsible Investing in South Africa, 2022 (https://integratedreportingsa.org/ircsa/wp-content/uploads/2022/09/CRISA2.pdf.) accessed 20 October 2022)

(Roy, “JSE ESG standards lift the game for SA companies” 2022 (https://www.dailymaverick.co.za/article/2022-08-10-jse-esg-standards-lift-the-game-for-sa-companies/) accessed 20 October 2022)

(ECP Africa Fund IV LLC; ECP Africa Fund IV A LLC And Burger King (South Africa) RF (Pty) Ltd; Grand Foods Meat Plant (Pty) Case no. IM053Aug21 para 4)

(Kim, Mallia- Dare, 2022)

Roxanna Valayathum is a Director and Shanna Eeson a Candidate Attorney | Cliffe Dekker Hofmeyr.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Travis Robson (CEO of Trive South Africa) takes a deeper look into meeting the needs of the modern investor.

We aren’t strangers to change. From the market crash in 2008 to the Steinhoff saga, investors have become more desensitised towards change and have adapted to the new worldinvesting order. But what does this mean for an FSP, and how do we stay up to date with the behavioural changes we see in the lives of modern investors?

As CEO of an FSP, I’ve always believed that it’s essential to have a thorough understanding of your business and industry, which allows you to build your business and unique selling points (USPs) around the needs of your target market; something needs to set you apart from the crowd and propel you into the mind of your target market.

To get there, you first need to understand your target market.

Over the years, I have gained extensive industry knowledge through customer engagement and direct research, which led me to identify two key segments: the Alpha Trader and Investing Potential. Using these two categories, we can recognise and meet their needs.

Alpha Traders are the confident group of investors who constitute the largest trading segment in South Africa. Research shows that this group is not beholden to one broker and that members usually have around 2 – 3 different broking accounts, with a propensity to manage these accounts online. This group is taking control of their investment journey and is no longer relying as heavily on traditional brokers as they did in the past. As a result, these investors have impeccably high standards for the service and do-it-yourself technology their broker provides. Seeing as there is typically minimal relational activity between the brokerage and these investors, they would soon change their broker if their service needs are not being met or if they feel that the commissions and fees charged by the brokerage do not allow them to maximise their investment portfolio.

Investing Potential is the group of upcoming investors soon taking over or falling into the Alpha Trader group. We identified this group of investors as young, tech-savvy investors with more advanced insight and technology experience as they have grown up with the latest tech at their disposal. As these tech-savvy investors enter the market, their main focus and decision-making factors focus on pricing, quality of tech and a sense of community or partnership with their brokerage.

What Does The Research Show?

This shift in focus waves goodbye to the old tactics of ‘selling’ a product to a ‘customer’. With a wide range of brokers available and communication capabilities at an all-time high, we see the power tables turn in South Africa as consumers now have the final say in whether your product is industry-worthy.

This highlights the massive industry changes that have happened over the years. We currently see that the share dealing market is in a growth phase and are finding new entrants that are disruptive to previous traditional telephone broking environments. While these disruptors might have done a great job of serving as a gateway for new investors, there is still a large portion of investors whose needs aren’t being met entirely.

As the market has grown and segmentation occurred, execution-only broking is experiencing significant growth because increasing investment in digital platforms results in a wider product offering.

However, it’s important to remember that growing market share means growing customer segmentations. Whilst some investors use gateway brokerages to enter the market, they typically outgrow the ‘milkshake and slushie phase’ and search for a more sophisticated product that grants access to a wide range of local and global products at a competitive rate. Encapsulating these features is something that local brokers have either struggled with or offered at such a premium that a large part of the market share is not interested.

Identifying and Meeting The Need

Considering all this information we uncovered during our research, we’ve identified the following as some of the predominant ‘needs’ that the modern South African investor’s focus has shifted to:

Next-generation tech that allows the investor to plan, execute and monitor their investments.

A wide range of local and global products under one umbrella that’s easily accessible through the platform.

Partnership or a sense of community facilitated by their brokerage makes the investor feel valued and not like just another number in the bunch.

Trust in a brand with a strong reputation that is monitored and compliant with local laws and legislation.

But how does one practically add value to the modern South African investor’s life with so many different offerings up for grabs?

The simple answer is to understand that their needs are ever-changing and to keep a two-way communication flow between you (the brokerage) and your customer (the investor).

Trive South Africa has tapped into the comms flow in the investment world and built our offering around these four specific needs whilst maintaining healthy and necessary flexibility.

On a practical level, we’ve implemented the following strategies to meet the modern South African Investor’s needs:

Quality and Functioning of Next-Generation Tech Trive SA has partnered with a well-respected third-party platform provider, allowing our clients to access a multi-asset investment platform with a simple interface, quick trading options and web functionalities. Not only does this allow us to offer our clients the benefits of a fully customisable and rich trading experience, but it also empowers them to take back control of their investment journey by allowing them to choose what they would like to see and when they’d like to see it.

Providing a Wide Range of Products In today’s world, the client is spoiled with choice and as such a range of markets and instruments is essential for the client, as they would like to trade all their products on one trading portal with one provider. Therefore, Trive SA provides a one-stop shop for every client’s investment needs. From tax-free savings accounts (TFSA) to over 2800 JSE listed and offshore shares, ETF investment opportunities and leveraged products, Trive South Africa offers it all at highly competitive fees and commissions.

Investor and Brokerage Partnerships Whilst clients from ‘traditional’ brokers still value ‘personal service from the broker’, we also see an uprise in need for partnership amongst younger investors. This may be because high-standard services were inclined to good impressions, thus allowing the customers to repurchase with assured satisfaction and expectations of a similar level of service and information. For example, Trive SA has a whole Sales Trading and Research & Education Team supplying our customers with information and a two-way comms channel, positioning ourselves as their partner.

Building Trust and Reputation As a new entrant into the South African market, we understand that building a solid relationship and trust in our brand will take time and hard work. To assist with these efforts, we have taken every possible step to provide our customers with a credible, FSCA-regulated service. We can also leverage the expertise of a strong holding company, Trive Financial Holdings, based in the Netherlands.

Whilst we believe that we are stepping in to fill the gap and meet the needs of the modern South African investor, we understand that this relationship and development will be an ongoing task that will require a lot of introspection and research to ensure we’re heading in the right direction. But, with our fantastic, diverse team and the global group backing us, we believe Trive is always keeping an ear to the ground and has the resources to adapt with our investment partners.

There’s “cautious” optimism for diamond demand at De Beers

AngloAmerican shareholders continue to benefit from the rock that everyone wants

Diamonds. Sparkly things that have been the downfall of many. These rocks benefit from a wonderful marketing campaign by De Beers over the years, positioning them as the best way to show how much you love someone (and to what extent your credit card is part of your life).

For Anglo American shareholders, that’s just fine thank you very much. De Beers gives a solid underpin to the Anglo business, with totally different fundamentals to the other commodities in the group.

Based on the latest sales cycle, the management team was happy with consumer demand over December. Bulk diamond purchasers (or “sightholders” as De Beers calls them) have been careful with their planning for this year given the broader macroeconomic conditions. In a recession, even love gets cheaper.

Given the reopening of China, there is “cautious optimism” for diamond demand this year.

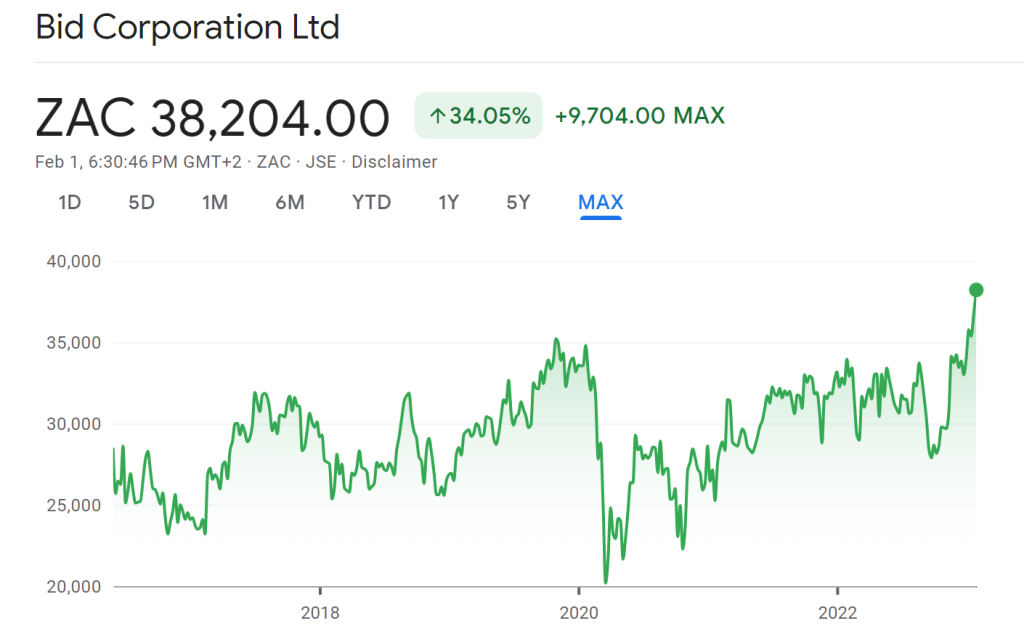

Bidcorp stuns the market – in a good way

A share price jump of over 6% was the reward for punters

Bidcorp is in the food service game, with a wide range of customers in the restaurant and hospitality industry. It’s a wonderful business model, with Sysco as a great example in the US of a similar business.

Despite all the ingredients for a disaster, ranging from consumer pressure through to high energy costs causing margin compression for restaurants, Bidcorp has been riding a wave of consumer demand in the aftermath of the pandemic. Financial pressure or not, people just cannot handle being stuck at home anymore.

After releasing a positive update in November, the momentum continued over the festive season and even into January. Europe has been having a far better winter than anyone expected, so that certainly helped. The lifting of lockdowns in China will be a major boost as well.

For the six months ended December, headline earnings per share (HEPS) will be between 43% and 49% higher year-on-year, implying a range of between 960 and 980 cents. For context, the previous record interim performance was only 714 cents per share, achieved in 2019.

The share price is now at its highest levels since being unbundled from Bidvest. I think you would be quite brave to buy this chart, with a meteoric increase of over 35% since October when the worst was expected for a European winter:

Ellies is paying top dollar to stay relevant

Or is that top rand?

Ellies has a core business has that been dwindling. The company didn’t make it a secret that alternative energy is where its future lies, an industry that Eskom is doing its very best to support.

The problem is that Ellies needed to make an acquisition in this space. With these companies currently all the rage, the risk of overpaying for an asset was always there. With a deal now announced, we have confirmation that a significant multiple is being paid.

With most industrial companies on the JSE trading at mid-single digit Price/Earnings multiples, it’s worrying to see Ellies agree to pay a 10x multiple for Bundu Power, an alternative energy (i.e. generators / solar etc.) business that is expected to make profit after tax for the year ending February 2023 of R20.4 million.

The value of net assets in the business is R48.7 million and Ellies is paying R202.6 million, so there’s a very large goodwill payment here. This means that either Ellies loves the brand (unlikely I would think) or is desperate to get a foothold in this industry (bingo).

Don’t get me wrong: it just might work. Ellies brings a distribution network and Level 2 B-BBEE status, both of which are valuable in South Africa. Perhaps more importantly, there’s a deal structuring trick that has been used here to give Ellies shareholders some protection.

Of the purchase price, only R72.6 million is payable when the deal closes. The remaining R130 million has been structured as three earn-out payments over the next three years. There would typically be earnings targets attached to these payments, though the announcement doesn’t give those details at this stage.

This is a category 1 transaction for Ellies, so a detailed circular will be released and shareholders will need to vote on the deal. If I was an investor in Ellies, I would give the earn-out structure a careful read.

Glencore’s production is higher in Q4

The fourth quarter saw sequential improvement across most commodities

Full year production numbers for 2022 were in line with revised guidance issued in October, so there were no major shocks in the final weeks of the year. Although the fourth quarter was better than the third quarter (a “sequential improvement”), the full year was a mixed bag.

On a like-for-like basis, group production fell by 7% due to abnormally wet weather. Due to a number of disposals and acquisitions, the reported percentage differs significantly from the like-for-like number.

Production challenges aside, Glencore is up nearly 40% over the past 12 months as the commodity cycle played out in its favour.

Harmony reports better production numbers

With the substantial positive momentum in the gold price, this came at the right time

Thanks to improved underground recovered grades in the second quarter, production increased vs. the first quarter of the financial year. This means that Harmony is on track to achieve full-year production guidance, which is exactly what shareholders want to see when the gold price is finally doing the right things.

All-in sustaining costs for the first half of the year were in line with guidance at below R900,000/kg. The gold price per kilogram is currently nearly R1,080,000/kg.

Since the recent lows in September 2022, the share price has skyrocketed 85%. It is nearly 14% up over twelve months.

MTN Nigeria continues to grow

As the most important African subsidiary, this is material to MTN

Nigeria is a good country when you can operate at high margins and enjoy decent growth rates. It’s a terrible place to try and extract money from, as evidenced by the challenges that the likes of Nampak and MultiChoice have been having. MTN is no stranger to those challenges, though a great run during the pandemic means that MTN’s holding company debt has been brought under control and repatriation from Nigeria is less of a key dependency.

And unlike Nampak and MultiChoice, MTN operates at exceptional margins in Nigeria that make it worth the risk. In 2022, service revenue grew by 21.5% and EBITDA grew by 22%, so margins expanded even further to a whopping 53.2%.

The company is investing just as quickly as it is growing earnings, with capital expenditure up 23.5%. The useful thing about MTN Nigeria is that there’s a strong case to be made for in-country investment, rather than trying to get all the cash back to South Africa for other purposes. This helps mitigate some of the repatriation issues.

Capital intensity (capital expenditure as a percentage of revenue) increased from 24.7% to 25.1%. This is a key ratio for telcos, as high capital expenditure is part of the game and is obviously a drag on free cash flow available to shareholders.

MTN Nigeria is separately listed on the Nigerian Stock Exchange and is up more than 18% over the past year.

Vukile gives an update on festive trading

Vukile offers a unique combination of South African and Spanish exposure

In Vukile’s South African portfolio, footfall was higher than last year by 8%, with township and community malls outperforming the likes of regional malls. Despite the obvious issues around load shedding, trading density was up across the local portfolio by mid-to-high single digits. Trading density for grocery (+8.5%) was well ahead of clothing (+4.8%), which ties in with recent updates we’ve seen from retailers.

In Spain, the Castellana portfolio also showed improvement in all major metrics, with footfall running ahead of even pre-pandemic levels. It seems as though growth was strong across all major categories.

This bodes well for Vukile, with a share price chart that has lost momentum in its recovery:

Little Bites:

Director dealings:

A director of PSG Konsult has disposed of a sizable number of shares, worth R7.75m

A director of Stefanutti Stocks has bought shares worth just over R160k.

A director of Invicta has bought listed preference shares in the company worth R136k

Those interested in Kibo Energy should refer to the detailed operational update released by the company, which gives extensive details on the various energy projects in the group. Overall, management seems happy and expects to see projects achieve revenue generating status in the next 12 to 24 months.

Gemfields has record-high net cash on the balance sheet

There’s even some good news from Fabergé

After record combined auction and Fabergé revenues in 2022, the balance sheet at Gemfields has more net cash than ever before – $104 million, to be exact! This excludes another $55 million in auction receivables.

The group’s market cap is only R4.5 billion, so a huge chunk of the value sits in cash.

Luxury jewellery business Fabergé has historically been a financial drag on the business. It has now achieved the lowest annual funding required, which means it’s still hurting the company but is on the right path.

The market continues to value this company at a very modest multiple, not least of all because of the risks of mining in Mozambique in a region that has been dealing with terrorist activity.

Hudaco’s earnings are going up

A trading statement delivered good news for shareholders

For the year ended November 2022, Hudaco’s earnings did the right things. Headline earnings per share (HEPS) is expected to be between 20% and 24% higher year-on-year, coming in at between R19.77 and R20.37 per share.

At a closing price of R145 (flat for the day), the Price/Earnings multiple is around 7.25x at the midpoint of the earnings guidance.

The share has been range-bound for a year now, up just 6.4%. Difficult operating conditions in South Africa keep the multiples for industrial companies low, especially in light of load shedding (pun intended).

Renergen looks to the US market

The group is preparing for further equity raises

With helium production now underway, Renergen is clearly worried about whether the local market will provide sufficient capital for the next phases of development.

The plan is to potentially offer American Depositary Shares on the Nasdaq in 2023, which means that Renergen will look to tap the US market for capital. This won’t impact the local listing, though shareholders will need to approve the listing of additional shares.

The company already applied to the SEC in late 2022, so that regulatory approval process is underway but isn’t completed yet. The company has reminded shareholders that the SEC may not approve the listing, which would scupper this plan.

Sea Harvest Group: not the catch of the day

The fuel price is really hurting this business

Sadly, boats need fuel to run. That’s not great news when fuel costs have gone through the roof.

For the year ended December 2022, Sea Harvest Group expects HEPS to decline by between 32% and 35%, coming in at between 102 cents and 107 cents. The share price closed 5.3% lower at R10.47 in response to this news.

A 10% drop in hake volumes as a result of quota losses was more than offset by pricing gains thanks to firm demand for the product. Despite an effort to control costs, there was nothing that the company could do about a R240 million impact from fuel price increases. When combined with once-off acquisition costs for the MG Kailis deal and other issues like higher interest rates and load shedding, profitability could only head in one direction.

Shoprite achieves 46 months of market share gains

Shoprite is still my pick in the retail industry in 2023

For the six months ended 1 January 2023, Shoprite managed to post seriously impressive growth. Even if we exclude LiquorShop to try and adjust for the base effect of lockdowns, group sales growth was 15.6%. Even the furniture business managed to achieve growth of 8.6%, so Shoprite really has done well here.

Like-for-like growth in Supermarkets RSA was 11.1%, a really strong performance vs. a base period where like-for-like growth was 11.3%. On a two-year basis, that’s impressive. The underpin in this period was a record Black Friday and festive season, capping off 46 months of uninterrupted market share gains.

Selling price inflation was 9.4%, which means there was volume growth in the business as well. The difference between like-for-like growth and selling price inflation is volume growth.

The growth is happening across the group, with Checkers and Checkers Hyper up 16.9% and Shoprite and Usave growing by 15.1%. The group’s greatest strength is that it resonates with consumers of all income levels.

It’s not all rainbows. Gross margins are slightly down, driven by fuel price pressures in supply chain and the need to be aggressive on price to support this sales growth.

The pressures further down the income statement are a lot more worrying. For example, employee costs experienced a “notable increase” because of increases in the minimum wage, the employee incentives from government coming to an end and other factors as well.

There’s also a whopping figure of R560 million spent on diesel for generators over this period. This only covers load shedding stages five and six, which happened right at the end of the period. What does this mean for retailers if these stages become the norm?

A positive impact will be the receipt of a R245 million insurance claim, offset to some extent by an additional R90 million in the cost of cover.

The stores bought from Massmart have been integrated into the group and rebranded into Shoprite, Usave and Cash and Carry stores as required. The acquisition was effective from 9th January.

Transpaco jumps 9.6% on strong earnings

Be careful though: illiquid stocks can post big daily moves

In a trading statement for the six months ended December, Transpaco’s HEPS is expected to be between 41.3% and 48.6% higher. This is a range of between 309 and 325 cents per share for the interim period.

So, how do you work out a Price/Earnings (P/E) multiple from this update?

You have to be careful of doubling this result, particularly given the tricky conditions that everyone is operating in at the moment. Also, doubling an interim number means you are actually looking at a forward Price/Earnings multiple rather than a trailing multiple.

Ideally, you want to use the last twelve months’ numbers, which is what LTM stands for on trading systems.

The manual way to do this is to take the prior year’s HEPS and subtract the prior interim period’s HEPS from that number, thereby isolating the second half of the prior year. You then add it to this interim period to arrive at HEPS over the last twelve months.

The FY22 result was 475.5 cents and the interim number was 218.8 cents, so the second half of the year (H2) saw HEPS of 256.7 cents.

Adding it to the current guidance for H1 of FY23 gives us a range of between 565.7 cents and 581.7 cents in HEPS over the last twelve months. At the midpoint and using the latest closing price of R28.51, that’s a Price/Earnings multiple of just under 5x.

And there we go – now you know how to work out a LTM P/E multiple! Those acronyms aren’t so hard, once someone explains them.

Vodacom: profits almost certainly under pressure

The quarterly update gave no details on profits, but we can reliably guess…

Vodacom’s quarterly update is 17 pages long. A quick CTRL-F for the word “profit” reveals just one mention, in the disclaimer of all places. We know that the telecoms companies are taking strain at the moment thanks to energy backup costs related to load shedding, so this spells trouble in my books.

Another clue about profitability lies in normalised revenue growth of just 4.7% for the group. This excludes the transformative Vodafone Egypt deal, with those numbers consolidated in December. Revenue in South Africa grew by 5%, which we know is well below many of the inflationary input costs. It’s very unlikely that operating margins went in the right direction.

Speaking of the Vodafone Egypt deal, it was worth R43.6 billion and is the largest in Vodacom’s history. They have pyramids in Egypt and they hopefully also have electricity.

MTN gets all the credit for being a FinTech play, but Vodacom is holding its own in that space, with a 30.6% increase in financial services revenue to R2.6 billion. That’s still small compared to group revenue of R30.7 billion, but it makes a meaningful contribution. M-Pesa is Africa’s largest mobile money platform by transaction value, processing $366.7 billion over the past 12 months.

Capital expenditure is a major focus point, as telecoms businesses have a reputation for generating sub-economic returns for shareholders over a long period of time. This is due to the need to continuously upgrade the network to stay ahead of technological developments. In South Africa, capital expenditure increased by 15.6% year-on-year vs. revenue growth of 5.0%.

Can you see the problems yet?

I can, yet the share price is down just 2% in 2023. It trades on a trailing dividend yield of 6.3%. I suspect that “forward dividend yield” is a term that Vodacom investors will learn about in 2023, but perhaps I’m wrong here.

Little Bites:

Aveng announced that its subsidiary Moolmans has entered into a new five-year contract with manganese mining company Tshipi é Ntle, valued at around R7 billion. Significant investment is required against this contract, including major yellow earthmoving equipment that would certainly get Toddler Ghost very excited and screaming “DIGGER!” at every opportunity. Moolmans has been servicing this client since 2011.

In a quarterly activities report, Southern Palladium reminded the market that drilling results to date have been in line with expectations, with some results coming back even better than expected. Phase 1 drilling is underway and the company has $14.2 million in cash.

MC Mining’s quarterly activities report looked at pressure on production from geological conditions and load shedding. It was also an important period for the balance sheet, with a A$40 million rights issue completed. The focus is on the financing of the flagship Makhado Project.

Orion Minerals also released a quarterly report, recapping a period that saw a major funding package signed with Triple Flag Precious Metals Corp. Off the back of that, terms have been agreed with the IDC and definitive agreements are being negotiated. There is now sufficient funding for trial mining at Prieska.

Accelerate Property Fund has more related party weirdness than a hillbilly annual convention. To help clean that up, there’s now a R50 million rights offer. The company already trades at a huge discount to NAV, yet the rights offer is is at a discount of over 31% to the 30-day VWAP. This has been fully underwritten by “U Big Investments” for a juicy fee of R2.5 million.

Zeder has completed the deal to sell its stake in Agrivision Africa, which means that the company has now received the R160 million selling price in cash.

In news that should shock absolutely nobody, Trustco has missed its own deadline of publishing its annual financial statements by 31 January. The auditors are apparently still finishing their work. The company hasn’t given any guidance regarding a new release date.

With just a few weeks to go until the ANSARADA DealMakers Annual Awards, the following deals have been shortlisted for the Brunswick Deal of the Year 2022. The DealMakers Independent Panel have selected these deals from the nominations submitted by the M&A industry advisers. They are, in alphabetical order:

Mediclinic International take private

The offer by Remgro and MSC Mediterranean Shipping (MSC) to Mediclinic shareholders owning the remaining 55.44% stake, provided Mediclinic shareholders with an exit premium of 50% on the six-month average price at the time, valuing the offer at £2,05bn (R41,85bn). In terms of the offer, by special purpose vehicle Manta Bidco, they would receive 504 pence (R102.06) per share in cash, plus the declared final dividend of 3 pence per share.

Local Advisers: Standard Bank, Morgan Stanley, Rand Merchant Bank, Webber Wentzel, Bowmans and Cliffe Dekker Hofmeyr.

PSG Group restructuring, unbundling and delisting

The ever-increasing discounts at which investment holding companies trade marked the catalyst for a transaction which would pursue a value-unlock initiative for shareholders through a restructuring of a nature not seen before in South Africa; one involving six JSE-listed companies, two of which were dual-listed. The value of R115.59 per share was unlocked for exiting shareholders, representing a 41.3% premium to the closing price on 28 February 2022, amounting to c. R22,54bn.

Local Advisers: PSG Capital, Tamela, Cliffe Dekker Hofmeyr, BDO and Deloitte.

Sanlam Allianz joint venture

The deal announced in May 2022 was almost two years in the making, and valued in excess of R33bn. The combined African operations of Sanlam and global integrated financial services group, Allianz creates the premier pan-African, non-banking financial services entity, operating in 27 countries across the continent, with positions strengthened in 12 overlapping countries. The ambition is to be a ‘Top 3’ insurance company in all chosen markets.

Local Advisers: Standard Bank, J.P. Morgan, Webber Wentzel, Bowmans and PwC.

The winner will be announced at the ANSARADA DealMakers Annual Awards on 21 February, 2023 at the Sandton Convention Centre.

South Africa is going through a lot right now. Eskom has finally conceded that loadshedding is going to be worse before our energy security crisis gets better; and the country’s economy is sluggish in shaking off the multiple blows thrown at it, COVID-19, the far-reaching impact of unemployment and increased cost of living. For the South African investor, there are limited options available when it comes to investing locally.

The diversity of your portfolio isn’t limited to having access to a multitude of asset classes or varying investment vehicles but also ensuring that these products work for you – beyond the cycles and market sentiments.

Perhaps the value lies in looking within some of South Africa’s local investment and savings vehicles and considering the likes of a Tax-Free Savings Account (TFSA).

Introduced in 2015 to encourage household savings, the current perception around TFSAs is that they are for the investment novice, newly minted professionals or those who’d like to have some money for a rainy day, tax-free. But this is a myth. A TFSA should, in fact, be a serious consideration for all types of investors – including the astute and experienced. It is an investment vehicle that can be considered as a base product to maximise this tax advantage provided by government. Equally important is understanding the Ts and Cs, fees and the transparency of a TFSA to ensure the highest net return.

After having spent hours conducting research, could you confidently say that you understand the returns, the fees, and the value you’ll get from this investment besides its tax-free appeal? Or that you understand the cumulative impact of these hidden costs on the value of your TFSA in the long-term?

In launching our Tax-Free Savings Account, our approach was simple: we wanted to develop a product that investors can include as part of a holistic investment approach where they can benefit from all the tax breaks available to them, and ensure that even the simplest investment vehicle, like a TFSA, continues to enhance their investment portfolios. But the benefits of a tax-free savings vehicle is negated if investors are paying what they would have saved on taxes, in fees. So, to align with the ultimate objective of encouraging investors to save, we charge zero investment fees on our TFSA. We’ve also made it easy for investors to switch their TFSA from another service provider to ours.

By far the biggest benefit, however, is the market-beating return that our tax-free savings product offers. With a minimum effective annual return of 10% per annum, integrating a TFSA into your investment portfolio is a no-brainer. What’s more, we’re so confident in the performance of the underlying assets of this offering, that we’re guaranteeing this minimum return until 29 February 2024. And we are confident that these underlying assets will continue to meet or exceed our targeted returns thereafter.

Ours is an account that’s structured using an endowment policy issued by Fedgroup Life Ltd. and is invested in a bespoke selection of underlying funds and a range of cash and debt instruments. In addition to a market-beating return, the Fedgroup TFSA also offers investors additional benefits. In the event of the investor’s death, named beneficiaries receive the proceeds faster and the TFSA doesn’t form part of the investor’s estate for the calculation of executor fees. These unique benefits help investors get the most out of this product and that’s what we want for our investors – the protection and preservation of their money and investments, a sustainable, diverse portfolio and market-beating returns that don’t just look good on paper but also enhance your investment gains.

We put our clients first in a global economy that’s unpredictable, a local one that’s worrisome, and an industry that frustrates through fees, fine print, and convoluted terms and conditions.

There is no reason to make TFSAs so difficult. They are investment vehicles that can help bolster consumer confidence when it comes to investing and enable investors to structure portfolios that deliver and improve with time while serving as an entry point for many who are looking to secure their financial futures.

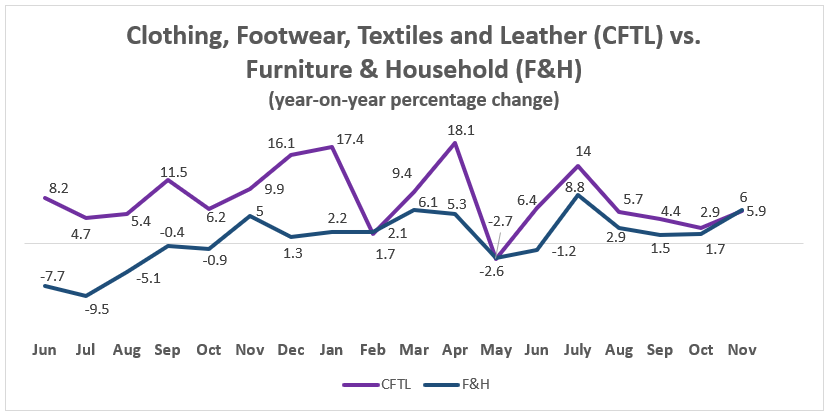

Chris Gilmour digs into the Stats SA November release and finds some surprising numbers.

StatsSA never fails to surprise me with its monthly releases and November 2022 was no exception. The rational person in me was expecting to see a really dull November, given the rising interest rate background. I was expecting to see another big yawnfest of a Black Friday/Cyber Monday at month end. I was completely wrong!

Discretionary retailers in the clothing, footwear, textiles and leather (CFTL) and household furniture and appliances (F&H) had an exceptionally strong month. It will be instructive to observe how December retail sales pan out, given the strength of November’s sales.

The best performing category in November was F&H at 6% year-on-year, closely followed by CFTL on 5.9%. We must bear in mind that November 2022’s figures are being compared against November 2021’s figures, which would also have a relatively strong “Black Friday” component built into them, so it’s not as if there some sort of weak base effect at play.

Far from it, in fact, which makes the November 2022 figures all the more interesting, especially as they arise during a period of sustained rising interest rates.

Source: StatsSA; Gilmour Research

Both of these discretionary categories are depicted in the above graph, which shows that they are both quite volatile, though rarely do they dip into negative territory.

Some of the JSE-listed alternatives

From a JSE perspective, it’s difficult to draw any meaningful conclusions. There is only effectively one furniture retailer left on the JSE – Lewis Group – and its share price languishes at somewhat less than half of its 2018 peak.

The CFTL retailers have had a very mixed picture, with Truworths enjoying a very belated surge after years of doing nothing, while Mr Price and The Foschini Group are demonstrating the benefits of investing through the cycle. But even here, there doesn’t appear to be an appetite for either of them.

Perhaps Truworths is worth having a look at, as its trading pattern is not only the best of the listed CFTL retailers but TRU is also the cheapest share of this universe, on a P/E ratio of only 8.5 vs 10 for TFG and 12.2 for MRP.

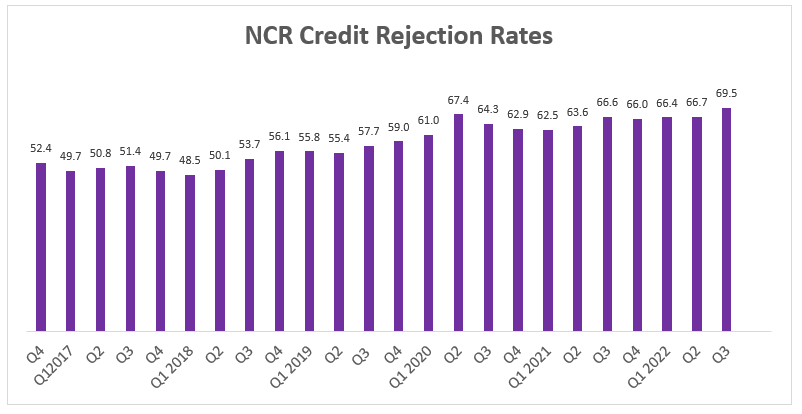

What is happening in credit sales?

At the most recent Monetary Policy Meeting of the SARB held on 26 January 2023, an interest rate hike of 25 basis points was announced. This is a lot lower than the string of 75 basis point hikes that have preceded this and probably signals a peak in the repo rate.

While this is a glimmer of good news for the embattled South African consumer, we must bear in mind that rates can stay at these elevated levels for quite some time, so any real relief may be some way off yet. In recent trading updates from discretionary retailers such as Lewis and Mr Price, it is noticeable that credit sales have increased faster than cash sales, suggesting that consumers are losing their fear of credit.

This is fascinating, as rejection rates for new credit applications have actually increased, according to the National Credit Regulator. This seems counter-intuitive as far as the rational person is concerned and yet the figures do suggest that this is indeed the case:

Source: NCR. Gilmour Research

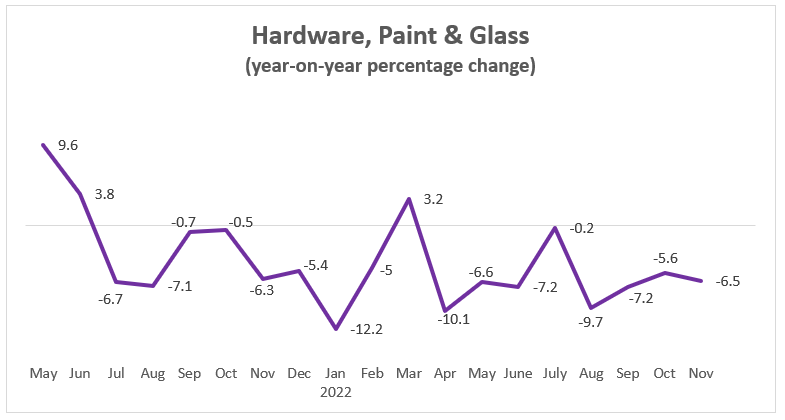

The wooden spoon goes to…

The worst performing sector in November continued to be hardware, paint and glass, a DIY home improvement proxy. There are no signs of a turnaround in this dismal sector, even after many months of secular decline. So, no respite for Cashbuild shareholders:

Source: StatsSA; Gilmour Research

This article reflects the independent views and opinions of Chris Gilmour, which are not necessarily the same as The Finance Ghost’s opinions on these stocks. For equity research on South African retail and other stocks, go to www.gilmour-research.co.za.

There’s progress in the deal to sell PresMed Australia

Back in December, Advanced Health told the market that it had agreed with a consortium of management and medical shareholders, alongside a major private equity backer, to sell its 56.44% stake in PresMed Australia for R522 million. The proceeds will be used to settle debt and support the working capital requirements of Advanced Health’s South African operations.

BDO Corporate Finance has been appointed as independent expert, with that report due to be included in the circular that will be distributed to shareholders. Another important step is that the TRP has been provided with the proof of funds for the consortium, a requirement under takeover law.

The various conditions need to be met by no later than 30 April, so things are heating up in this transaction. Irrevocable undertakings have been received from holders of 68.23% of the share capital of Advanced Health, so the deal looks to be in with a good chance of success.

Record tin production at Alphamin

Margins are juicy even with tin prices under pressure

Alphamin mines around 4% of the world’s tin, a little factoid that the company reminds us of in every announcement.

For the year ended December, the group achieved record tin production of 12,493 tonnes, up 14% from the prior year. In the fourth quarter, production of 3,113 tonnes was ahead of guidance of 3,000 tonnes.

The estimated EBITDA for the full year of $222 million is also a record.

The tin price moved severely over the year, with the average price for the full year at $30,636/tonne and the Q4 price at $21,436/tonne. The current price is around $30,000/tonne, so there’s been a significant recovery in the price this year, which is encouraging for the ongoing development of the Mpama South project.

Importantly, the EBITDA margin in Q4 (when prices were low) was a meaty 41%. When mining goes well, it really goes well!

The full year dividend was CAD$0.06 per share (roughly R0.78 per share). At a share price of R13.00, this isn’t an example of a mining business on a high dividend yield.

The group had net cash of over $109 million on the balance sheet as at the end of December.

Capital & Counties updates the market on 2022

London’s West-Endis experiencing strong demand

In a story that we are seeing from the European property funds overall, Capital & Counties has confirmed that rental demand at properties is strong but valuations are going sideways because of higher yields being demanded by investors.

If you’ve ever run a valuation in your life, you’ll know that a 19 basis points move to a yield of 4.07% is significant. This can offset some really juicy underlying tenant demand.

Net debt at Capco has increased from £599 million to £622 million, with net debt to gross assets increasing from 24% to 28%.

The proposed merger with Shaftesbury is expected to close during the first quarter of 2023.

Italtile: it still hurts

The share price seems to know this already

Unless you’re a hedge fund manager looking to add to your short book, Italtile really hasn’t offered much since the middle of the pandemic. As people returned to work and interest rates went crazy, the thought of spending money on holidays (or even petrol) started to take preference over any plans to renovate the bathroom.

In a trading statement, Italtile has guided that headline earnings per share (HEPS) for the six months to December 2022 will drop by between -8.1% and -5.5%, coming in at between 77.1 and 79.3 cents.

The share price was flat on the day, with a recent downward trend clearly visible in this chart:

Nampak is doing its best, but it isn’t enough

The rights offer has dropped from R2 billion to R1.5 billion

Despite revenue growth of 20% in the three months to December 2022, Nampak’s operating profit is down because of foreign exchange losses.

I’ve beaten this drum many times: running a relatively low margin business with a complicated African treasury is exceptionally hard. Of the cash transfers in the period of R452 million, 68% was from Nigeria at a “significant cost to operating income” – i.e. transferred at a rate that is far more onerous than the quoted rate in the market, due to shortage of foreign currency.

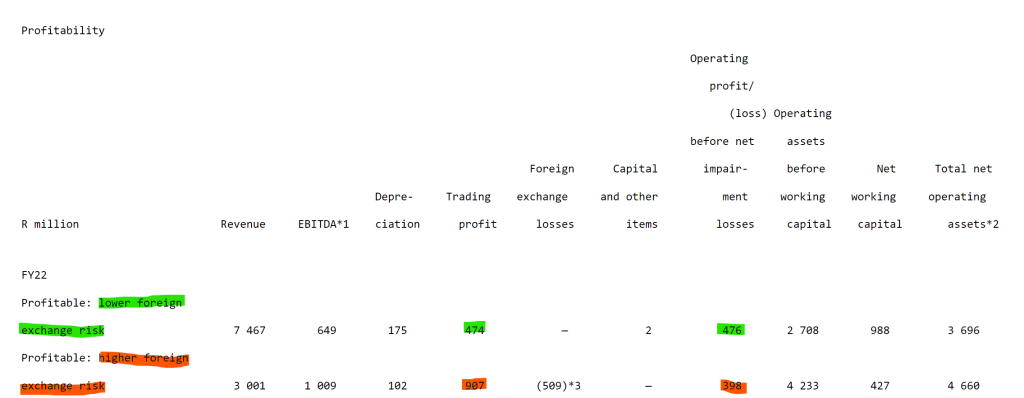

Here’s another view on why operating in risky jurisdictions should only be attempted with very juicy margins:

For those with dodgy eyes, it says that Nampak makes only R474 million in trading profit from jurisdictions with lower foreign exchange risk and R907 million from jurisdictions with higher risk. By the time the forex losses are factored in, the latter number has plummeted to R398 million.

The sad thing is that trading profit increased by a higher percentage than revenue, so all the pain is being felt due to either forex losses or issues further down the income statement (higher net finance costs as well as a higher effective tax rate that have both negatively impacted net profit).

The management team has been focused on the balance sheet and rightly so, unlocking a net working capital and liquidity improvement of R500 million. For this reason, the proposed rights offer has decreased from R2 billion to R1.5 billion.

Interestingly, Nampak notes that the operations can handle load shedding up to stage 4, with anything beyond that level causing trouble. I think we can all relate to that.

A new equity funding package is being negotiated with the lenders who require Nampak to execute a rights offer with net proceeds of at least R1.35 billion. A number of shareholders have pushed against the order of events, saying that the terms of the funding should be finalised before the rights offer is launched.

Nampak has committed to give details of the funding package before the rescheduled extraordinary general meeting on 8th March.

Pan African Resources drops more than 6% after an update

Production came under pressure in the first half of the year

For the six months ended December, Pan African Resources managed to make significant progress on its renewable energy strategy. Aside from solar projects, there was also the issuance of a $47.3 million sustainability-linked bond that will help fund the Mintails project.

The problem lies in the production numbers, not the strategic initiatives. Load shedding and difficult weather conditions put the business under pressure, particularly at Barberton Mines. Production for the period fell by 14.6%, a significant drop from what was admittedly record production in the prior year.

Despite this, production guidance for the full year has been maintained. There’s a big catch though: this guidance is “subject to consistency in Eskom’s electricity supply” – and this probably explains the share price drop.

Investors will also take note of a significant jump in net debt, which is attributed mainly to capital expenditure and the payment of a dividend.

Pepkor is flattered by Avenida, with SA businesses under pressure

The company joins the Mr Price WhatsApp group of like-for-like pain

With Pepkor adding its voice to the retail sales updates over the festive period, we now have a proper overview of what happened in the sector. Revenue increased by 6.5% at group level, but we have to dig deeper to really unpack it.

The number to look for is like-for-like sales, particularly with the major acquisition of Avenida in these numbers. Sure enough, like-for-like fell by 1.4%. This is despite 70% of stores being able to trade with backup power, so there’s more to the festive retail story than just load shedding.

The poor result in clothing was driven by Ackermans, where like-for-like sales nosedived by 8%. That’s a really ugly outcome in an inflationary environment of around 5%, implying that volumes fell by approximately 13%.

Across Mr Price and Pepkor, along with cash vs. credit sales at Lewis, we now have pretty clear evidence that lower income earners are being hammered by current economic conditions. Still, that’s not the only reason for the pain. At Mr Price, I think that the brand isn’t resonating with customers anymore. In Ackermans, Pepkor admits that the merchandise mix wasn’t aligned to the brand promise of “unbeatable value” – and in fashion, that’s a major issue. Markdowns have been implemented, which means gross margins are going to take strain.

There’s some hope in January at least, with the back-to-school rush driving strong sales at Pepkor’s core value brands. This is a necessity though, with parents likely making sacrifices elsewhere to afford school clothes.

The rest of the group posted positive like-for-like growth, with Avenida up 6.8%.

The DIY / building material format within the group performed decently in the broader economic context. The Building Company managed to grow 1.8%. The performance has deteriorated in January, with general iffyness around load shedding not helping matters.

I can’t help but wonder how Pick n Pay Clothing is performing in this environment. One of the best success stories to come out of Pick n Pay in recent years, the value-driven offering has resonated with customers and taken market share. We don’t get to see detailed numbers unfortunately, as the division gets bundled into the broader (and much larger) Pick n Pay business.

A management band-aid at Spar

The group is casting the net wide for a new CEO

With the…sudden retirement of the CEO of Spar, the company has found itself without anyone at the helm. As a temporary measure, non-executive chairman Mike Bosman will now become Executive Chairman (and Spar even uses capital letters here to make this significant upgrade even clearer). He has resigned from the board of AVI after 13 years to make sure he can deliver this role.

With the…sudden retirement of the CEO of Spar, the company has found itself without anyone at the helm. As a temporary measure, non-executive chairman Mike Bosman will now become Executive Chairman (and Spar even uses capital letters here to make this significant upgrade even clearer). He has resigned from the board of AVI after 13 years to make sure he can deliver this role.

Bosman will have his hand held sweetly by the Board Chairman’s Committee, to “strengthen governance” in the aftermath of a really embarrassing period for the company. Lead independent director Andrew Waller will be the chair of that committee.

While Spar fights to regain any level of respect in the market, the search for a new CEO is underway and the company hopes to make an announcement within three months.

The CEO of Tongaat heads for the exit

But the business rescue practitioners are running the show now anyway

Things seem to keep getting worse at Tongaat, with CEO Gavin Hudson retiring from the top job. He joined in the aftermath of the accounting irregularities and tried to steady the ship, but a cocktail of a pandemic, civil unrest and floods made it an almost impossible task.

Tongaat is in business rescue and the plan is expected to be published before 28 February, with the company’s “core team of executives” working with the business rescue practitioners.

The reality is that Hudson’s departure probably doesn’t make a huge difference at this stage, as the business rescue practitioners are in charge of the company’s affairs.

Little Bites:

Director dealings:

A trust linked to directors of Ninety One has acquired shares worth around £86k.

A director of Mustek has sold shares worth around R875k

It’s such a tiny amount that it probably doesn’t matter, but an associate of a director of Ascendis Health bought shares worth nearly R4k

Safari Investments is currently under offer from Heriot REIT at a price of R5.60 per share. Before the latest block trade, Heriot and its concert parties collectively held 40.7% of the total Safari shares in issue. After a deal with SA Corporate Real Estate Limited (also at R5.60 per share), Heriot and its concert parties now own 47.1% in Safari.

Trustco doesn’t seem to be getting anywhere in court. After the High Court dismissed Trustco’s review application regarding the JSE’s decision around Trustco’s financial statements, the company applied for leave to appeal to the Supreme Court of Appeal. This application was dismissed with costs. I’m no lawyer, but I assume they will give up now.

By Duma Mxenge, Business Development Manager at Satrix

The global move to a gig economy has accelerated in recent years as workers exit formal employment in favour of flexible freelance work or take on freelance assignments in addition to their main jobs. In fact, online platform Statista expects gig workers to gross over USD455 billion globally in 2023.

With this economy growing so rapidly, asset managers and financial advisers need to think smart when developing and recommending financial solutions to this growing market segment. Most importantly, we must remember that gig workers’ earnings may vary wildly from one month to the next.

Income volatility and inadequate savings to pay for unexpected expenses stand out as the main financial challenges facing South Africa’s gig workers, described by Oxford Languages as “individuals who do temporary or freelance work, often as independent contractors engaged on an informal or on-demand basis”.

Many traditional investment products are designed with those in formal employment in mind. For example, retirement annuity products and pension funds assume that clients can afford a fixed monthly contribution, plus an annual increase. These products can present difficulties for gig workers due to their uncertain earnings.

In additional, research by the United States based Commonwealth (assisted by Green Dot, Gig Wage and Steady) found that most gig workers had no savings for emergency expenses, observing that financial ‘blows’ of USD1,000 to fix a vehicle or make up a rent payment were often insurmountable. As such, the starting point for a gig-worker-appropriate financial solution is a product that allows for irregular cash savings and gives workers access to that money in the event of an emergency.

Although cash savings can be accumulated in a bank account, it makes sense for gig workers to consider money market funds that allow them to earn ‘better than bank’ interest rates while avoiding the price uncertainty that goes hand-in-hand with stock market investments. As the gig worker accumulates sufficient savings and his or her earnings become more stable, the adviser may suggest lump sum or once-off investments in a range of discretionary investment products.

South African gig workers can choose from hundreds of collective investment schemes such as unit trusts and exchange traded funds (ETFs), which allow them to build a savings portfolio with exposure to any asset class, both locally and offshore.

An individual with volatile income should not neglect saving for retirement. After building an adequate emergency fund, equivalent to around six months of average income, the gig worker can begin contributing to a retirement annuity offered by one of the country’s Linked Investment Service Providers (LISPs). Retirement annuity products are also available on the SatrixNOW investment platform. These retirement annuities are balanced funds and they allow flexibility in contributions introducing gig workers to a highly-regulated retirement fund industry.

The gig economy carries significant risks and a high level of uncertainty. This uncertainty makes it difficult for gig workers to choose investment products for housing emergency funds or securing retirement. Satrix believes that gig workers should approach financial advisers to assist in managing uncertain cashflows, and over time build the necessary exposure to savings, retirement funds and discretionary investments.

Asset managers and financial advisers can work together to ensure that gig workers benefit from sound financial advice and the investment returns on offer to appropriately match the needs of the client.

Satrix is the leading provider of index-tracking investment products and exchange traded funds (ETFs) in South Africa, with over R160 billion in assets under management invested in the range of ETFs, index-tracking unit trusts, life pooled and segregated portfolios that are specifically tailored for client-specific mandates or retail funds.

It pioneered index investing in South Africa, launching the flagship Satrix 40 ETF as the first locally listed ETF in November 2000. The business services the institutional, intermediary, and individual investor markets. Satrix has proven expertise in risk management, portfolio analysis and index construction.

A core part of the Satrix purpose is to drive the democratisation of investments for all South Africans, where SatrixNOW, the no-minimum amount online investing platform, is a key enabler to provide access for South Africans to “Own the Market”.

For more info on ETFs, unit trusts and retirement annuities, visit the Satrix website.

Disclosure Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")