The huge drop in the share price isn’t anything sinister

I must say, I had lost track of the date of the Zeda spin-off. While reading about the exchange control approval that has been obtained for Barloworld’s special dividend of 550 cents, I noticed that the share price had fallen 17%.

Having questioned my sanity for a moment, I realised that Zeda made its debut on the market on Tuesday. It lives and breathes, trading under the ticker JSE:ZZD.

As for Barloworld, the reason for the drop is that the group is essentially significantly smaller now, as Zeda has been unbundled to its shareholders. If you add up the value of your shiny new shares in Zeda and the shares that you still have in Barloworld, it will make a lot more sense.

Change of guard at Gold Fields

Chris Griffith steps down after the Yamana transaction failed

We will never know what the boardroom conversations sounded like, but we do know that Chris Griffith has stepped down as CEO of Gold Fields. The announcement doesn’t even attempt the niceties of “seeking new opportunities” or “broadening his horizons” – instead, it thanks him for his leadership and then reminds everyone that the Yamana deal failed.

The next man in this (particularly) hot seat is Martin Preece, EVP of Gold Fields South Africa, who has been appointed as interim CEO. Preece has been with the company for six years.

It looks like Griffith and Preece have a busy December ahead, as the official handover date is 31 December.

Ouch.

Less comedy (and tragedy) ahead on the JSE

Finally, the listing of Nutritional Holdings is being terminated

In a move that is very long overdue, the JSE is terminating the listing of Nutritional Holdings with effect from 19 December. This mess of a group has delivered comedy and tragedy in almost equal measure, stumbling from one crisis to the next.

This doesn’t give the current shareholders a solution. In fact, it makes the situation even worse, as JSE regulations will no longer apply. Nutritional Holdings will be a public unlisted company, which means it is still regulated by the Companies Act but not by any stock exchange.

The lucky shareholders now hold unlisted shares in a company that can barely string together enough financial information to complete the audits for recent financial years.

With liquidation hearings scheduled for January and February 2023, there might be a short and painful ending to this story anyway.

Orion Minerals secures $87 million funding package

Definitive agreements signed with subsidiaries of Triple Flag Precious Metals Corp

In a major step for Orion, $80 million worth of funding has been raised against the delivery of 87% of future gold and silver by-product production, with the stream rate reducing to 50% after certain milestones. This shows you how specialised junior mining funding is. At the time of delivery, Orion will receive payments of 10% of the delivered value at spot prices.

There’s another $7 million to be advanced against 0.8% of gross revenue from future mineral sales.

This comes after the news of a R250 million convertible loan with the IDC, which is currently at the stage of definitive agreements being drafted and negotiated.

The two sources of funding will be used to complete a feasibility study for early mining at Prieska and enable commencement of mine dewatering.

RMB Holdings updates the market on its value unlock

With interim results now available, value investors got their calculators out

The devil is most certainly in the detail, but orderly wind-downs can offer delicious returns. Anyone who bought shares in Etion at the right time will confirm this. With a drop in the share price of over 10% in response to results, it’s not clear that the market is seeing a juicy outcome for RMB Holdings.

Are they missing a trick?

To help you decide, there are brand new results available. They highlight that since September 2020, a shareholder return of 46.5% has been delivered. That’s way above the market return available over a two-year period but also isn’t lifechanging stuff.

To demonstrate the power of closing the discount to net asset value (NAV), the NAV per share is down 10% over the past year and the share price is up 33%. I must highlight that the NAV includes a huge special dividend of 147.1 cents paid after the end of the reporting period.

If we adjust for that, the “current” NAV is 96.9 cents and the share price is 52 cents.

Herman Bosman has moved on as CEO and financial director, with Brian Roberts (the current CEO of RMH Property) stepping up to the top job. This tells you where the bulk of the remaining value lies: the property portfolio.

Not a pyramid scheme

Vodacom has closed the deal for a 55% interest in Vodafone Egypt

If my own experience with my local Vodacom tower is anything to go by, load shedding is causing a lot of pain to the network. I’m sure Vodacom’s board is only too happy to be taking a 55% stake in Vodafone Egypt, where they hopefully have a lot more electricity than we do.

With the seller of the stake in Egypt being wholly-owned subsidiaries of Vodafone Group Plc, that company’s stake in Vodacom has increased from 60.5% to 65.1%. There was also a cash portion to the deal worth R10.8 billion.

A trading update from Vodacom is expected at the end of January, which will include an update on the medium-term growth outlook.

Little Bites:

Director dealings:

The Mouton family (across several trusts etc.) have loaded up on Curro shares worth nearly R7 million

You know it’s getting bad when several Nampak directors have headed for the exit with parts of their shareholdings. From the CEO’s sale of R985k down to much smaller sales by prescribed officers, it really isn’t looking good for this company.

The CEO of FirstRand has put a collar structure in place over R50.3 million worth of shares, with a put strike price of R55.82, a call strike price of R75.06 and an expiry date in December 2023. The current traded price of FirstRand shares is just over R61.

A prescribed officer of Impala Platinum has disposed of shares worth R1.05 million

A director of Raubex has bought shares worth R247k

The CEO of Calgro M3 has bought shares worth R353k

Via their shared investment vehicle, key directors of Ninety One have acquired shares worth £31.3k

Merafe has announced the European benchmark ferrochrome price for the first quarter of 2023. At 149 US cents per pound, this price is a rollover from the fourth quarter of 2022.

Delta Property Fund has announced an agreement to sell the Beaconsfield property in Kimberly for R22.1 million. This will reduce the loan-to-value by just 10 basis to 58.1%, so there isn’t much to get excited about here.

The shareholders of RCL Foods voted almost unanimously in favour of the resolutions required to unwind the B-BBEE Structure.

Glen Anil Development Corporation has agreed a deal with an associate of a director of Purple Group. The deal is complicated enough that I didn’t just box it under the other director dealings, as the director of Purple only holds an 18.1% stake in Serialong Financial Investments, the company selling the shares. The initial deal is worth R24.3 million and increases Glen Anil’s stake in Purple to 1.2%. The price of 202.08 cents per share is significantly higher than the closing price of 170 cents. The parties have also entered into option agreements that give Glen Anil the ability to buy another 31 million shares over the next few years at strike prices ranging from 175 cents to 310 cents.

Allan Gray is trying hard to get out of the way of Nampak, but it still owns a whopping 16.44% in the company. The share price has nearly halved in the past month on news of the pending rights offer.

Featuring two special guests who bring loads of real-world experience to the table in this industry, our latest bizval webinar was packed with insights into the world of online retail.

In this webinar, we featured two pioneers in the direct-to-consumer retail space. Michael Dixon from Desray Fashions and Justin Blake of Silvery shared their unique insights into how they built their successful businesses.

This deal includes the receipt of $30 million in funding

Back in August, Aspen announced an agreement with the Serum Institute of India that would allow Aspen to manufacture, market and distribute four routine vaccines in Africa under license from Serum.

Before you wonder about whether this is a Covid product long after Covid has gone away, you can feel better about the fact that these are Pneumococcal, Rotavirus, Polyvalent Meningococcal and Hexavalent vaccines.

I’m no doctor, but ctrl-F “Covid” in the announcement yields no results, so that’s good news.

To help fund this 10-year deal with Serum, Aspen had been negotiating for funding with the Bill & Melinda Gates Foundation and the Coalition for Epidemic Preparedness Innovations (CEPI).

The exciting news is that $30 million in funding will be received ($15 million from each of those parties), which supports this initiative and creating regional vaccine manufacturing capacity that would put Africa in a better position going forward for future public health emergencies.

The restructuring of Ellies is an expensive process

There are glimmers of hope in the operations, although they are still making losses

Ellies has released a trading statement for the six months ended October. The headline loss per share is expected to be between -4.17 cents and -4.99 cents, which gives an interesting range vs. the loss of -4.36 cents in the comparable period.

The restructure process has had an impact of R18 million, which equates to -2.24 cents per share. This suggests that things are looking better at operational level, albeit still a loss-making reality.

This is confirmed by the further commentary, which notes revenue up by 5.6% and gross profit marginally higher than the comparable period. Operating costs (excluding retrenchment costs) have been contained below inflation.

Ellies has signed a term sheet with its bankers to restructure the working capital facilities. There are other negotiations to “support the business” in areas of substantial growth for products and services, which probably means the introduction of strategic partners – we can’t be sure until any proper details are announced though.

Interim results are expected to be released on 14 December.

The share price has been ugly this year, losing half its value in largely one-way traffic:

Northam juices up the Royal Bafokeng offer

Cash is king and Northam is putting more of it on the table

NB: this is not an increase to the offer price for Royal Bafokeng Platinum. Instead, Northam Platinum is increasing the cash element of the offer and reducing the share-based element accordingly.

The overall impact is that the cash portion of the offer has increased from R10 billion to R17 billion. Expressed on a per-share basis, the cash consideration is now between R92.48 and R172.70 per share, depending on the level of acceptances.

The total offer price is R172.70, which is unchanged as highlighted above.

The trick here is that if Impala Platinum doesn’t accept the offer for its current shareholding in the company of 40.71%, then all other shareholders that accept would be paid R172.70 in cash.

Northam is trying hard to outfox Impala Platinum in this deal and a greater cash component is another step in that direction.

PBT pulls off a smart deal with Sanlam

The keys to the B-BBEE funding structure have been passed to the right place

PBT Group is a successful tech consulting company that should be running a tight balance sheet, as this is essentially a management consulting model that focuses on selling time.

Despite this, the need to have the right empowerment credentials is a reality in the South African business landscape, so investors have been forgiving of a preference share funding structure that saw PBT Group providing funding to Yonex Investments (a B-BBEE investment entity).

In a smart move, PBT Group has managed to offload this preference share to Sanlam Investment Management for R53.3 million. This is a perfect example of capital allocation discipline, as PBT Group should be chasing a return on capital that is much higher than the yield on the preference share. In contrast, Sanlam Investment Management is looking for yield instruments that offer diversified exposure.

In other words, the deal makes sense for all involved, as Sanlam is a far better owner of these preference shares.

Prior to the disposal, PBT will receive a dividend of R1.4 million on the preference shares. A special distribution of R31.5 million will be paid to PBT shareholders after this deal closes. If you’re wondering where the rest of the money went, it’s important to note that a prior special dividend was higher than the value of non-core asset disposals that had been achieved by that time. There’s effectively a catch-up process underway here.

Importantly, PBT Group still holds R133.1 million in non-core assets. With a market cap of under R1 billion, that’s a substantial special dividend if PBT can get the remaining assets sold.

The Competition Commission has ruled on Shoprite – Massmart

Shoprite can buy most of the intended stores, but not all of them

In an important step for Massmart’s balance sheet, Shoprite has been given the green light to acquire most of the stores that were part of the initial proposed transaction to acquire the heavily loss-making cash and carry business from Massmart.

The competition authorities determined that 15 stores should be excluded from the deal, so Massmart will need to try and sell them off separately.

Shoprite is allowed to acquire 42 Cambridge Food and Rhino Cash and Carry stores, two Fruitspot facilities, the Massfresh Meat business and 12 Masscash Cash and Carry stores.

The effective date of the transaction is 9 January 2023.

I remain a bit skeptical of this deal from a Shoprite perspective. The stores will obviously be renovated and rebranded as Shoprite (and probably Usave) stores, so this was really a process of just securing the sites. Still, it seems like an expensive exercise just for that, as the stores would’ve likely gone bankrupt anyway and the space would’ve become available for “free” from a Shoprite perspective.

Little Bites

Director dealings:

An executive of Gold Fields sold shares worth a meaty R9.6 million.

A director of Stor-Age has acquired shares worth R116k.

Althea Grewar sold shares in Luxe Holdings worth R12 million and we have to assume that the buyer is Mohamed Holdings, which now owns 34.99% of the company.

A director of Sable Exploration and Mining has sold shares worth R808k, with PBNJ Trading and Consulting having increased its stake in the company to 38.4% and having triggered a mandatory offer a well. We can’t be sure if PBNJ bought the shares sold by this director but it seems likely.

Marshall Monteagle PLC released results for the six months to September 2022, reflecting an increase in revenue of 53% and a jump in profit before tax on trading and property operations of 77%. Net of revaluations and other moves, the group is in a loss-making position. The headline loss per share of $0.069 is down from the profit of $0.01 per share in the comparable period. Despite this, there’s a dividend of $0.019 per share.

The general offer by Heriot to purchase Safari shares was accepted by holders of 7.6% of Safari shares in issue. Heriot and its concert parties now hold 40.7% of total Safari shares in issue.

Tharisa released the results of the private placement of bonds related to the Karo Platinum Project. The company was looking to raise $25 million and managed to attract applications of $31.8 million for the bonds being listed on the Victoria Falls Stock Exchange. This is a great result in the strategy to fund this open-pit PGM asset located in the Great Dyke in Zimbabwe.

After announcing that current CFO Charl de Villiers will be taking the top job at Libstar as CEO from January, Terri Ladbrooke as been appointed as interim CFO. This is an internal appointment.

In anticipation of the potential loss of REIT status, Fortress REIT Limited has changed its name to Fortress Real Estate Investments Limited

Mantengu Mining has concluded its rights offer to raise R15 million, with 77.69% of the new shares being allocated to the underwriters. This means that other shareholders didn’t exactly fight each other to get to the front of the queue, with applications for only 22.31% of the available shares.

In a role that might not be the easiest to fill based on everything going on with the company, Conduit Capital is looking for a new non-executive director and Chairperson of the Audit and Risk Committee, after Nonzukiso Siyotula resigned from the role.

Rodger Walters has been appointed as an independent non-executive director of RECM and Calibre Limited and as the chairman of the Audit and Risk Committee. He is currently the CFO of ASISA (the Association for Savings and Investment South Africa).

Luxe Holdings renewed the cautionary announcement related to a potential disposal of assets to Go Dutch in a cash deal.

Another company that renewed its cautionary is Afristrat, which is currently in a fight for its life with its balance sheet. I can’t give you the website because it appears to have been hacked and redirected.

Sebata Holdings released results for the six months to September. Revenue is up 26% and the headline loss per share improved from -132.25 cents to -5.27 cents. The website hasn’t worked for as long as I can remember.

With some sparkling alliteration, Chris Gilmour digs into credit demand by South African consumers.

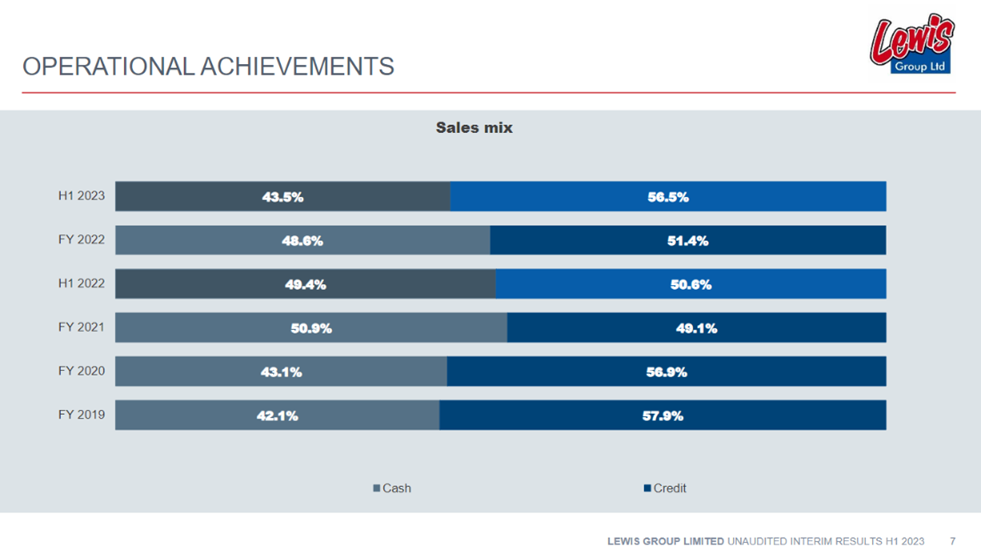

Just when you thought South African consumers had become so debt-averse that this trend would carry on ad infinitum, lo and behold Lewis Stores made abundantly clear that their customers have a preference for credit over cash once more.

In the latest interim results from Lewis to end September 2022, there was a distinct change in the composition of cash:credit sales. From being nearer 50:50 cash:credit, the interim 2023 figures saw a big jump in credit sales to 56.5%:

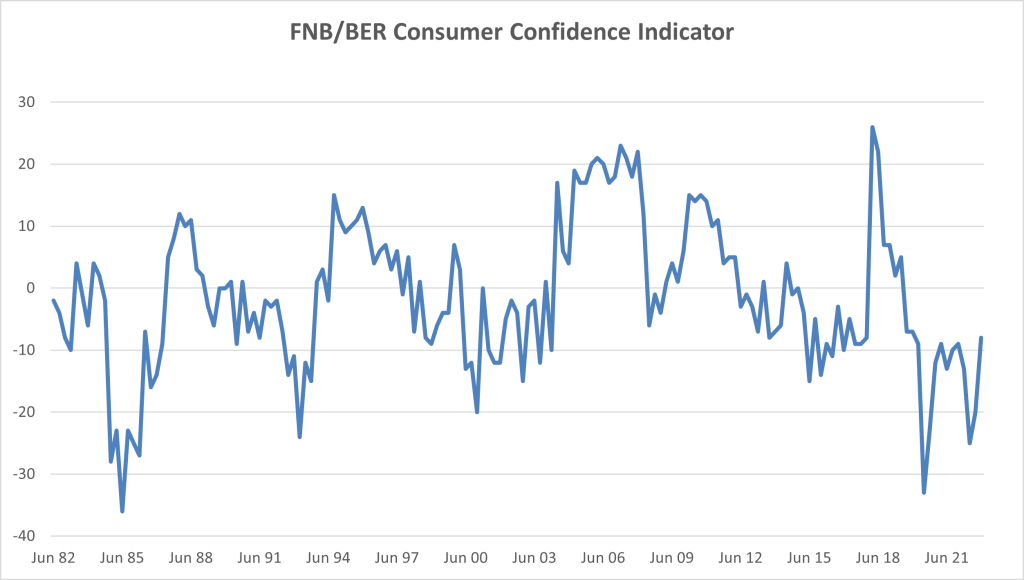

And the latest consumer confidence indicator from the Bureau for Economic Research in Stellenbosch also suggests that consumers became more confident in the final quarter of 2022:

“The FNB/BER Consumer Confidence Index (CCI) recovered from -20 to -8 index points during the fourth quarter of 2022. Although the index remains in weak terrain relative to its long-term average, it has regained all the ground lost during the first half of 2022. The rebound in consumer sentiment shows an improved willingness to spend among consumers, but consumers’ ability to spend would also need to improve in order to translate into a significant increase in consumption.”

In other words, what the BER is suggesting is that, provided consumers have the wherewithal to spend, they will now be more inclined to do so.

Source: FNB/BER; Gilmour Research

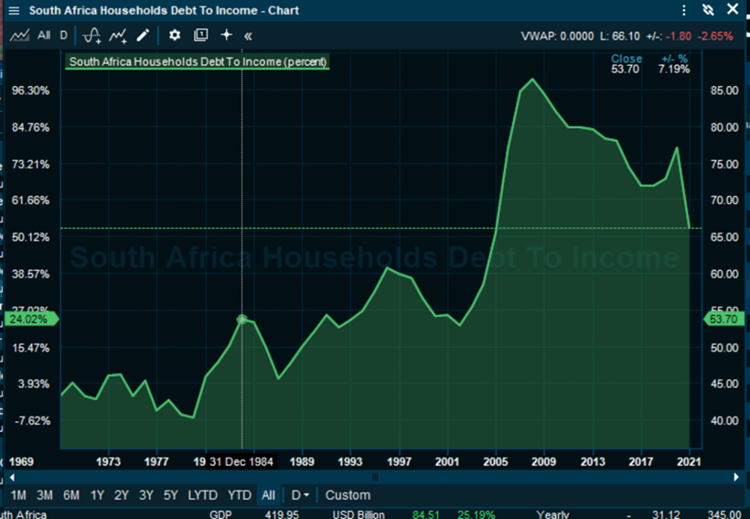

This is not to suggest for a moment that Lewis or any other credit retailer for that matter is about to embark on a program of reckless credit-granting. Far from it, in fact. The credit application decline rate at Lewis improved to 35.8% (previous year 39.1%). Over the years, Lewis and others have learned a lot more about their customers’ spending patterns and have adopted very conservative credit-granting procedures. And for quite some time, South African consumers generally have expressed a preference for cash purchases over credit, as household debt to disposable income has declined progressively. Over the past thirteen years, household debt to disposable income has declined from 85% to nearer 65%.

Thus there is probably some capacity for consumers to take on extra debt, provided they are comfortable in their ability to repay it.

The statistics from the National Credit Regulator (NCR) are seriously lagged – the Q3 figures will only be available by early January – and so it’s not possible to draw any high-level conclusions about consumers’ willingness and/or ability to take on more credit at this point in time.

This comes as South African GDP growth surprised on the upside last week, with Q3 growth beating all estimates, coming in at 4.1% year-on-year and 1.6% quarter on quarter. Admittedly, the figures were helped by a bumper agricultural harvest coupled with a low base of comparison in Q2 . But nevertheless it’s a good outcome and suggests that SA won’t enter recession next year like many of its developed economy trading partners. Obviously the high incidence of rotational power cuts (loadshedding in Eskom-speak) may well dull GP growth in Q4 but across the spectrum, consumers and industry are making plans to combat loadshedding.

But we have to be realistic about the impact of higher credit sales. There can be no doubt that in a “normal” economy, furniture & appliance retailers much prefer credit sales to cash sales. It reminds me of a comment that JD Group CFO Gerard Volkl made at a presentation to the effect that “if we could just find a way of offering consumer finance without having to worry about this pesky furniture, it would be so much easier.”

Lewis CEO Johan Enslin pointed out at the results presentation that a credit sale is, on average, four times more profitable than a cash sale, even allowing for the fact that the group has to wait many months for the proceeds to arrive. This is not surprising, considering that the maximum interest rate allowed under the National Credit Act is the repo rate plus 21%.

Up until now, consumers have been wary of taking on more debt and understandably so at these kind of interest rates.

So, provided the retailer is happy that the consumer can afford to take on more debt and the consumer is happy to assume more debt, there does appear to be a bit of capacity for improving retail sales growth, even in a rising interest rate environment.

This article reflects the independent views and opinions of Chris Gilmour, which are not necessarily the same as The Finance Ghost’s opinions on these stocks. For equity research on South African retail and other stocks, go to www.gilmour-research.co.za.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

A smell at Spar that is worse than the polony

Equites’ latest property deal with Shoprite in their joint venture

Absa’s impressive update with ROE running ahead of Nedbank and Standard Bank

Italtile’s insights into the state of South African consumers

How it is all going down to the wire at Fortress

Sanlam’s mixed bag of results for the 10 months to October

Transnet’s negative impact on Thungela and Kumba

A record year for Gemfields

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

Production is lower in 2022, with Quellaveco still in ramp-up phase

Anglo American is an interesting, complicated group that has exposure to a variety of commodities including PGMs, iron ore, nickel and copper. Don’t forget that De Beers (the diamond giant) is in there as well. The management team talks about the group being a “resilient business through the cycle” – a clear nod to diversification.

In the latest update, Anglo American has advised that production should be down around 3% this year, with unit costs up by 16%. That’s an unhappy story as input cost pressures combine with production decreases to create a nasty outcome.

The situation should improve in 2023, with production expected to increase by 5% and unit costs expected to increase by only 3%. Capital expenditure is anticipated to be around $0.8 billion higher than in 2022 as the Woodsmith project picks up.

In 2024, production is expected to increase by 5% and capex would return to current levels. The expectation for 2025 is flat production (i.e. similar to 2024) and ditto for capex.

Woodsmith is the group’s next major greenfield project after Quellaveco, bringing a diversified source of income in the production of Poly4, the low carbon fertiliser. Speaking of copper project Quellaveco, that operation increases Anglo’s global production base by 10% and is expected to be highly margin accretive over the next decade.

Other than the immediate pressures, the group sounds bullish about its prospects.

Anglo American Platinum faces operational pressures

2022 production is expected to be within guidance, but beyond that looks tricky

At Anglo American Platinum, the good news for 2022 is that refined PGM production is 3.8 million ounces, smack in the middle of the guided range of 3.7 million to 3.9 million. The bad news is that because of inflationary pressures, the unit cost of R15,300 per ounce is higher than the guidance of R14,000 to R15,000.

There is a build up in work-in-progress inventory because of loadshedding and the delay in the Polokwane smelter rebuild. This inventory will be refined in 2023, which will give some benefit to the next financial year and 2024 as well.

Looking at the medium-term guidance (2023 – 2025), the business is clearly under pressure. Drilling initiatives have reflected a reduction in higher-grade ore volumes at Mogalakwena. There are also lower volumes expected from Amandelbult, with infrastructure closures, challenging geological ground conditions and the pending end to the life-of-mine of the current opencast operations. The company also expects to receive lower purchase-of-concentrate volumes than previously anticipated.

The production forecast for 2023 and 2024 is 3.6 million to 4.0 million ounces. It was previously between 3.8 and 4.2 million ounces for 2023 and between 4.1 and 4.5 million ounces for 2024, so this is a significant drop. It gets worse in 2025 (a new forecast), with production estimated at 3.3 million to 3.7 million ounces.

With ongoing inflationary pressures on top of production challenges, the unit cost guidance for 2023 is between R16,000 and R17,800 per PGM ounce.

This isn’t great news for shareholders at all, with a 7.3% drop in the share price on Friday as a result.

ARC gives an update on its investments

With investments like rain and TymeBank, this is always worth a read

The updates on each underlying company don’t go into much detail, but there’s enough to get a good sense of how the portfolio is doing.

African Rainbow Capital Investments (ARC) is split into a diversified investments portfolio and a financial services portfolio, so I’ll stick to that approach for this update.

Before going into the portfolio updates, take note that the lower management and performance fees for the fund were approved by shareholders in November. Although I still don’t like the structure, it’s better than it used to be.

Diversified investments

The only comment on rain is that the business is performing well and the additional spectrum is expected to positively impact the valuation.

At phosphate business Kropz, the Elandsfontein phosphate plant has suffered several setbacks to its commissioning. This caused operational cash shortfalls and ARC increased the convertible loan facility by R550 million as a result, of which R247.5 million has been drawn.

The last of the Afrimat stake was sold in November, generating an internal rate of return (IRR) of 21.72% on that investment. Another disposal of a public company was the 3.2% stake in Capital Appreciation, with an IRR of 12%.

Most of the assets in the ARC Services group of company are being disposed of in line with the carrying value of R291 million.

Bluespec is performing in line with expectations and meeting profit targets. Weelee, the online vehicle bidding platform, is also growing in line with the business plan.

The disposal of Humanstate and Payprop SA for R496 million has been concluded. The IRR on disposal was 20%, excluding any earn-out structures. There is the potential to receive another R52 million over 30 months.

Fledge Capital is in an acquisition phase, having sold its remaining investment in WeBuyCars earlier in the year.

Linebooker is enjoying strong month-on-month volume growth in the online booking platform and the management team is exploring options beyond South Africa.

Financial services

Alexforbes is a publicly listed company and ARC doesn’t go into any details beyond what the company already discloses in its own reporting.

TymeBank always gets a lot of focus and deservedly so, as this is a significant and interesting investment. October saw 228,000 new customers onboarded, a record month for the bank and vastly higher than 130,000 to 140,000 customers per month in the first half of 2022. With the acquisition of Retail Capital, TymeBank is looking to enhance its offering to its business banking clients. Retail Capital is a large SME funder that has disbursed over R5.5 billion to more than 43,000 business owners in the past decade. Notably, Tyme Global has launched GOtyme in the Phillipines.

Crossfin has increased the number of merchants utilising its services and has achieved revenue and EBITDA growth on a year-on-year basis.

In Sanlam, the deal with Absa Investments to create one of South Africa’s largest black-owned asset managers has been concluded. Also related to Sanlam, ARC highlights that Sanlam is looking to take a controlling stake in Afrocentric.

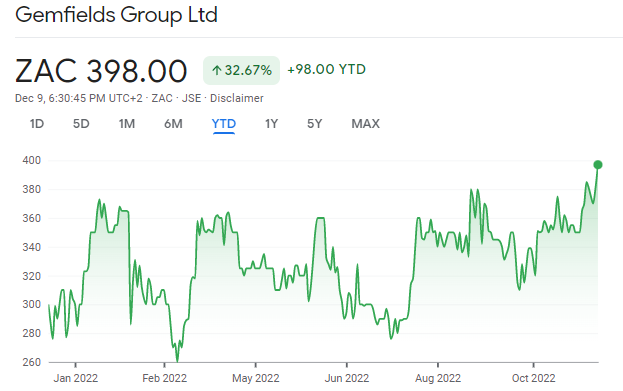

Rubies are red, Gemfields is green

After some major scares this year, Gemfields is at a 52-week high

There’s been no news for a while on the insurgency in Mozambique that got dangerously close to Gemfields’ Montepuez ruby mine. The army was sent in to stabilise the situation and it seems to have worked. Although the risks aren’t gone by any means, the market seems to have relaxed after seeing support from government to protect the mine.

In the latest ruby auction, the company achieved auction revenues of $66.8 million after selling 94% of the lots offered for sale. Over the full year, the 2021 auction revenue record for Montepuez rubies ($147.4 million) was smashed with a performance of $166.7 million.

Looking at the broader group (i.e. including the Kagem emerald mine in Zambia), Gemfields’ auction revenues of $316 million have set a new annual record, up 32% from 2021.

It’s been a year of immense volatility and huge opportunities for traders:

Italtile hints at its performance

Revenue is higher, but retail volumes are surely down

Italtile has updated the market on its sales for the five months to November.

It’s important to understand that the group has manufacturing operations (Ceramic Industries and Ezee Tile Adhesive Manufacturers) as well as retail operations (CTM, Italtile Retail, TopT and U-Light). The integrated supply chain import businesses are Cedar Point, International Tap Distributors and Distribution Centre.

The businesses continue to face serious macroeconomic headwinds. Under considerable pressure from interest rates and inflation, consumers are deferring or scaling down on renovations and new build projects. To make it worse, loadshedding is causing a lot of pain for Italtile in the manufacturing division.

Although the update doesn’t give the percentage increases in selling price inflation, we can safely assume that a 2.3% increase in sales in the Retail division means that volumes are down. This is the case where inflation is higher than the percentage increase in sales. I have the same concern about the integrated supply chain businesses, which are up just 3%.

The Manufacturing division is up 7.8%, a performance that is “primarily due to price increases” (which implies some volume growth at least).

The company expects difficult conditions to persist for the rest of the year and no specific earnings guidance has been given due to the uncertain operating conditions.

Kumba updates production guidance

With issues at Transnet, you can guess in which direction the guidance went

After a tricky first half of the year for Kumba, matters were made more difficult by a two-week strike at Transnet in October. This has a negative effect on throughput, which in turn leads to a build-up of iron ore stockpiles at the mines.

Something has to give somewhere, in this case in the form of lower production due to the lack of storage space. Thankfully, the group has managed to maintain its unit cost guidance for the year despite lower production.

For 2023, production is expected to be 35 – 37Mt, down from 39 – 41Mt. The unit cost is $44 per tonne, achieved through lower anticipated diesel prices and currency depreciation. Of course, if the macroeconomic picture works out differently, then things could get ugly.

There is some light at the end of this railway tunnel. Kumba highlights various steps being taken by Transnet to improve matters, including a major maintenance programme, an extra set of trains, the removal of speed restrictions and the implementation of weather-related mitigations. This supports a production outlook of 37 – 39Mt in 2024 and 39 – 41Mt in 2025.

Still, that’s well down from the 41 – 43Mt previously guided for 2024. Our infrastructure challenges are throttling our economy.

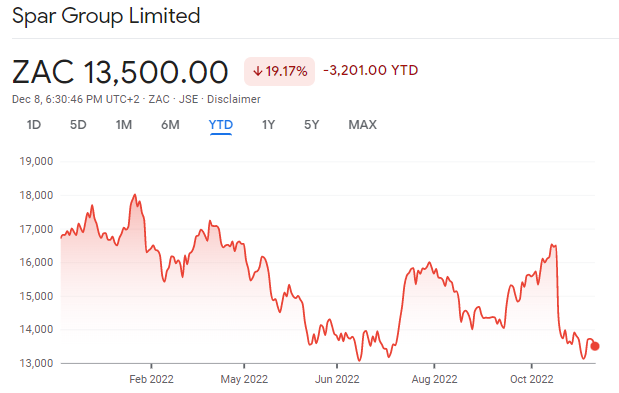

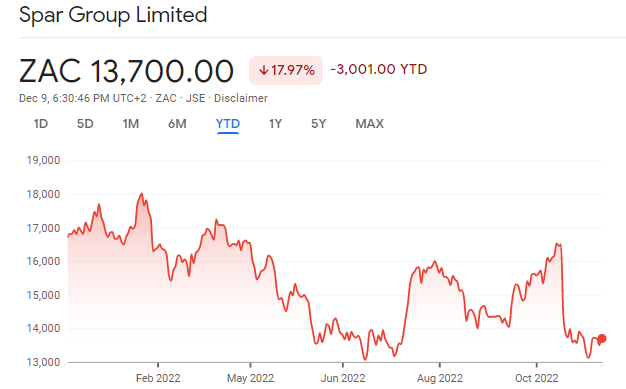

Spar responds to media allegations

The share price is quickly becoming the least of the problems

In an explosive recent piece by Ann Crotty of the Financial Mail, a number of allegations were put forward about governance at Spar. It also highlighted the legal proceedings by the Giannacopoulous Group, which owns 45 Spar stores.

In this edition of My Big Fat Greek Dispute, the article sets out a long-standing dispute between Spar and the Giannacopoulous Group with respect to its guild membership, a prerequisite for owning a Spar store (you need to remember that they are franchises).

A very embarrassing court judgement is quoted, in which high court judge Judy Kollapen talked about a “spectacular failure on the part of the Spar Group” – not what shareholders (or others for that matter) want to read.

The family is now claiming R2.1 billion in damages. That’s a lot. There is also a criminal proceeding underway, with the backing of AfriForum. This is getting very ugly, very quickly.

The governance concerns go deeper than just a legal dispute that hasn’t been given much attention in the company disclosure. There are allegations of fictitious loans and major question marks around Graham O’Connor’s independence as chairman. He was the previous CEO and his family appears to have various commercial interests with Spar.

I won’t reveal more of Ann Crotty’s excellent work in Financial Mail. Being a subscriber to the publication is a worthwhile investment and you can read it there (along with my weekly column in the magazine if you so desire).

On Friday, the retailer responded to the media allegations, the summary being as follows:

The “fictitious and fraudulent loan allegations” relate to what Spar describes as an “isolated matter” – that’s not a great sign

The company refutes allegations of discrimination against retailers based on race or store location, noting that “perfection” (a process of taking legal ownership under a bond i.e. Spar Group taking ownership of a franchise store) is only a method of last resort to protect Spar as a creditor

O’Connor was appointed as chairman after serving as CEO because the board felt this was in the best interest of the company, with a lead independent director appointed to balance this as is suggested under the King Code

Amidst the allegations, O’Connor has stepped down as chairperson of the board and will remain a director. Andrew Waller, the current lead independent director, will serve as interim chairperson.

The share price tells the story here:

Little Bites:

Director dealings:

Having banked a juicy allocation of shares after the Avito disposal, Prosus and Naspers CEO Bob van Dijk exercised his options and disposed of all the shares. CFO Basil Sgourdos sold the shares required to cover the taxes and kept the rest.

A director of Afrimat has sold shares worth around R4.5m

A director of Sea Harvest has acquired shares worth R466k

The chairman of Hulamin has bought shares worth R203k

African Equity Empowerment Investments has provided Premier Fishing and Brands with notice of a firm intention to make an offer to acquire 6.14% of shares in the company. Premier would subsequently delist from the exchange if this scheme of arrangement is approved by shareholders. The offer price is R1.60 per share. In case you’re wondering about that shareholding, AEEI already holds 56.23% in Premier, 34.06% is held by 3Laws Capital and 3.57% is held by Sekunjalo. The 6.14% is therefore held by the general public. With such a tiny free float, there’s really no point in being listed.

Equites has announced the development of a logistics campus for Shoprite, with this particular property being built in the joint venture that the company has with Shoprite (50.1% – 49.9% in favour of Equites). The structure is that the joint venture will acquire an existing warehouse from Shoprite for R90 million and extension land for R75.6 million. This is minor in the context of the development cost, which is over R1 billion! With a 20-year lease and three rights to renew for 10 years each, this substantially increases the weighted average lease expiry period of the portfolio. The initial yield is 7.8% and rentals will escalate at 5%. Equites recently joined us on Unlock the Stock to talk about the strategy and performance, with the recording available for you to watch here:

SA Corporate Real Estate released a pre-close investor presentation. The portfolio has delivered like-for-like net property income growth of 7.3% with the office portfolio as the (predictable) ugly duckling. The vacancy rate in that part of the portfolio is over 20%, expected to reduce to below 17% by the end of December. The negative reversion in the office portfolio is huge at -27.6%! The Industrial portfolio has a vacancy rate of 0.82% and negative reversions of -5%. The retail portfolio has a 3.9% vacancy rate and although there is a slight negative reversion for the year thus far, this is expected to turn positive by December.

After an oversubscribed bookbuild for sustainability-linked notes, Pan African Resources will issue notes to the value of R800 million. Pan African is the first mining company to issue a sustainability-linked bond in the South African market.

Salungano Group released interim results for the six months to September. With the hilariously named Vanggatfontein on care and maintenance and lower demand from Eskom, the company hasn’t put in a good performance. Revenue fell by 13% and the group swung from an operating profit of R190 million to an operating loss of R16 million. The headline loss per share of 19.64 cents is ugly vs. HEPS of 20.69 cents in the comparable period.

Delta Property Fund just can’t catch a break, with an embarrassing announcement that the interim results for the period ended August included an error. These aren’t small errors either, with some line items in the cash flow statement being wrong by over 30%. This shouldn’t be happening in a listed company.

Trustco has renewed the cautionary announcements related to the management agreement and the resources transaction, both of which are making progress.

The JSE has appointed Ms Fawzia Suliman as its group CFO. Many people forget that the JSE is a company that is listed on the JSE! This always confuses newcomers to the market. One is a corporate entity and the other is an exchange, so the company effectively uses its own product in order to be listed.

Ascendis announced that Ms Bharti Harie has been appointed as chairman of the board.

There are wholesale changes to the Grindrod Shipping board as part of the transaction with Taylor Maritime Investments. There are five new appointments to replace the two directors who have stepped down as part of the agreement with Taylor.

Luxe Holdings doesn’t exactly have the best reputation in the market, so the news of the independent non-executive director resigning isn’t promising. He is also the Chairperson of the Audit and Risk Committee, so there’s another red flag for you.

PBNJ Trading and Consulting has acquired 38.4% of the shares in Sable Exploration and Mining Limited, which means that there is now a mandatory offer process underway. A mandatory offer to all remaining shareholders is triggered whenever a company acquires a stake of more than 35% in a regulated company. At a price of R1 per share (the current market price), this gives shareholders a liquidity mechanism in this incredibly obscure company.

It’s been…a year, hasn’t it? The team from TreasuryONE kicked off December by recapping the major recent moves in the market and the macroeconomic data that makes all the difference. Of course, we looked to the future as well.

In this interactive session, attendees had some really interesting questions that included a few that I needed to answer about equity strategies.

It was a brilliant webinar that I highly recommend making time to watch:

To learn more about how TreasuryONE can help your business navigate these conditions, visit their website.

British American Tobacco: can smokers still afford it?

Big on trademarked ESG-friendly terms, low on volumes

I never cease to be amazed by British American Tobacco’s public relations onslaught. The website looks like a tech company or a special needs school that promises a brighter future:

Of course, this is a cigarette company that is trying hard to figure out how else to make a profit. Because ESG index inclusion is all about intent and meeting rules, rather than a company’s actual value to society, British American Tobacco is a favourite. This is why most of the ESG industry is just window dressing of the worst kind.

The New Category business (vapes etc.) has 21.5 million customers and is still loss-making, with a plan to be profitable by 2025 when the target of £5 billion revenue is met.

The cigarettes make the money, though industry volumes are under pressure because of macroeconomic factors and post-Covid normalisation of consumption. With a core business that is essentially a sunset industry, there’s a major focus on cost savings (£1.5 billion annualised savings by the end of 2022) and pricing initiatives to recover inflationary pressures.

Investors treat British American Tobacco as a cash cow. It manages to grow revenue slightly each year and converts over 90% of adjusted profit from operations into cash.

With a market cap of R1.75 trillion, British American Tobacco is an absolute monster and is used as a defensive stock because the customers are, shall we say, rather sticky. Here’s what that looks like in a tricky market:

Rebosis business rescue update

To meet JSE requirements, a quarterly update on the process is required

The Rebosis business rescue plan was supposed to be released on 1 December, but the practitioners have requested an extension to 20 January. That’s the boring news.

The financial statements are a sticking point, as the annual financials for the year ended August can’t be released until the auditors can make a reliable assessment of the company’s ability to continue as a going concern. That isn’t going to happen until the business rescue plan is approved and the valuations of the properties are completed.

The company also released an operational update that reflects vacancies of 11.8% in the R5.3bn retail portfolio and 26.2% in the R5.9bn office portfolio. The negative reversions on the office portfolio are quite spectacular at -29%.

Government tenants are clearly hard negotiators.

Transnet keeps letting Thungela down

And not just Thungela, but all of us in South Africa who depend on the economy

If it was possible to win a FIFA World Cup through scoring economic own goals, South Africa would put any of the big names to shame. We might even be granted a Cricket World Cup as an adjacent prize, just to make sure we eventually get one of those trophies.

These sporting fairy tales are about as likely as Transnet sorting out its rail business or Eskom keeping the lights on. The frustrations are immense, as we are a resource-rich country at a point in the cycle where it should be our turn to shine.

Instead, the only thing shining is my rechargeable light while I write Ghost Bites late at night.

The pain is made clear by Thungela, our coal superstar that is losing out on exporting coal because of poor rail performance by Transnet Fright Rail. A strike in October by Transnet employees certainly didn’t help either. Because South Africa appears to have angered the ancestors, we also had a derailment on the coal corridor in November that took 10 days to clear.

Mitigating actions included a focus on railing higher-grade products to ports and using trucks to supplement that supply. That’s not cheap when the price of diesel is so high. In the final cruel irony, the price of diesel is partly being driven by demand from Eskom.

Truly, it’s a mess.

Against this delightful backdrop, Thungela’s pre-close statement paints a picture for the year ended December 2022 that remains lucrative. As a regular flick of your light switch will no doubt remind you, there is an energy crisis and we aren’t the only country dealing with it.

This crisis comes through in demand and hence the price for export coal, which has increased from $103.82/tonne to $236.11/tonne. You don’t need your calculator to figure out that this is a big jump. Sadly, thanks to Transnet, export saleable production at 12.8Mt is lower than the revised range of 13.0Mt to 13.6Mt issued in August and 15% lower than the 2021 number.

Lower production has a direct impact on costs per tonne, with the FOB cost per export tonne (excluding royalties) expected to be around R955/tonne (4% higher than the revised range issued in August and 21.7% higher than in FY21). Included in this number is a non-cash charge of R85/tonne related to an increase in environment provisions based on closure estimates.

Including royalties, the cost is expected to be R1,106/tonne vs. R812/tonne last year.

Despite this, Thungela is a cash machine of note, boasting a ridiculous net cash position of R19.8 billion on 30 November compared to R8 billion a year ago. It won’t improve in December because of operational disruptions, which shows how costly the strikes and derailments are.

South Africa desperately needs Thungela, with the company expected to pay taxes and royalties of R4 billion this year.

Headline earnings per share (HEPS) is expected to be at least 97% higher than last year, coming in at a minimum of R131 per share. This is a good time to remind you that Anglo gifted this company to the market at a price of R25 per share in June 2021.

With perfect hindsight of course, that was a forward P/E multiple of 0.2x.

Incredible.

Little Bites:

Director dealings:

One must be careful with reading too much into directors selling off their shares received under performance awards, but I did note that a few Transaction Capital directors didn’t hold on to any of their shares

A prescribed officer of Nedbank and the company secretary have collectively sold shares worth just over R3 million

In a reminder of how much your bank balance sucks in comparison to some of the directors on the JSE, the CEO of Omnia has sold shares worth R15.3 million just to cover the tax on a performance award

There’s always a bigger fish, with Stephen Koseff of Investec fame selling shares worth around R155 million

Sanlam has released the circular for the Afrocentric deal that would see Sanlam taking a stake of between 55% and 64.45% in the company. This is being executed through a partial offer at R6.00 per share. You’ll find the circular here.

Transpaco is executing a specific repurchase of shares worth R42.9 million from a related party to the company’s CEO. As the price has been set at the 30-day volume weighted average price (VWAP), no fairness opinion is necessary. This represents 4.95% of the issued shares of Transpaco.

Old Mutual has seen value in Spar despite a horrible year and no shortage of bad press, taking the stake to 5.23% despite a share price chart that reminds me of last week’s polony that fell down the back of the shelf:

Spear REIT announced that the sale of 15 on Orange for R246 million has received approval from the Competition Commission, which means the disposal has met all outstanding conditions and can go ahead.

Sebata Holdings has released a trading statement for the six months ended September, with the headline loss per share improving substantially to between 5.25 cents and 5.36 cents (vs. 132.25 cents last year). I would love to hyperlink it, but the website doesn’t work.

Nictus released its financial statements for the six months ended September, with revenue down by 1.34% to R18.8 million (this company is tiny) and a headline loss of 2.03 cents, which is at least better than a loss of 2.94 cents in the comparable period

Randgold & Exploration Co released a trading statement for the year ended December 2022, in which the loss per share has more than doubled because of further operating expenditure incurred by the company.

Anglo American is to go ahead with a deal first disclosed in June which will see the miner combine its nuGen™ Zero Emissions Haulage Solution (ZEHS) with US specialist engineering company First Mode (the company that partnered with Anglo to develop ZEHS). In addition, Anglo will provide equity funding of US$200 million into First Mode which will accelerate the development and commercialisation of ZEHS. On completion of the transaction, the business will be valued at US$1,5 billion and Anglo American’s stake in First Mode will increase from 10% to a majority shareholding.

Jasco Electronics is in discussions with its major shareholder, Community Holdings No 1 (CIH) with regards to its intention to make a general offer to minorities to acquire the remaining shares in Jasco. The purchase offer per share of 16 cents represents a 4% premium on the 30-day VWAP of Jasco shares on 2 December 2022.

Sabvest Capital has acquired a 39.3% equity interest in Valemount Trading, a manufacturer and distributor of products for the local pet market, from R & K Trust. The equity purchase consideration will be determined in accordance with an earnings and cash/debt formula calculated on 28 February 2023.

The Premier board and its shareholders (Brait) have decided not to proceed with the initial public offer and listing of the company on the JSE due to current unfavourable capital market conditions. Rather, as noted in the pre-listing statement, Titan and RMB will, in specified proportions, acquire the unlisted ordinary shares in Premier from Brait for an aggregated consideration of R3,5 billion by way of a private sale of shares.

The deal between Murray & Roberts and Webuild announced in early November has been terminated. M&R was to dispose of its interest in Clough Australia. In terms of the deal Webuild would inject A$30 million into cash strapped Clough to avoid placing the company under voluntary administration. The implementation of the loan did not take place resulting in Clough being placed into voluntary administration.

Unlisted Companies

Montfort Group, a global commodity trading and related-asset investment company, has entered the local energy market with the acquisition of a 49% stake in New Age Energy, a B-BBEE company focused on the reliable import, export and distribution of safe and high-quality energy products. The new partnership will see Montfort introduce its brand, products and services to the South Africa market.

CodiumX, an IT investment group headquartered in Johannesburg, has acquired a stake in local data analytics company Intellinexus. The deal will help the company achieve its ambitious target of five to 10 times growth over the next two years through organic growth and acquisitions.

Swiss media group Ringier is to acquire almost all outstanding shares in Cape-headquartered Ringier One Africa Media (ROAM) from co-shareholders SEEK, and minority shareholders Jabavu and Ceatonia. The deal strengthens Ringier’s long-term investment in certain digital marketplaces in sub-Saharan Africa

Connect, a UK cloud communications expert has acquired Pivotal Data and illation as it seeks to increase its presence in the South African market. Financial details were undisclosed.

Atlantis Foods, SA’s frozen seafood distribution company, has acquired Snoek Wholesalers in a deal which will scale the company’s operations and revenue. Snoek Wholesalers represents global brands such as Marfrio and Leroy in SA and sources fish from Peru and China for processing.

Host Africa, the Cape-based hosting business leading in Cloud Server solutions in South Africa, has acquired Kenyan hosting company EAC directory. Financial details were not disclosed.

Automation startup Synatic has raised US$2,5 million in a seed extension round to grow its footprint in the US in preparation for a Series A round. The round was led by Allan Gray E-Squared Ventures and UW Venture. Synatic provides complete solutions for the data integration market, offering a low-code/no-coder/your-code solution to simplify the integration of internal and external data sources.

South African venture capital fund management firm Fireball Capital has, alongside a fund advised by the Development Partners International Fund, invested in Ukheshe International, the UK-headquartered fintech enabler.

Lighthouse Properties’ offer to shareholders to acquire new Lighthouse shares has closed with the company issuing 7,692,308 new shares at R6.50 per share. The R50 million capital raise will provide the company with additional liquidity primarily for capital expenditure at its shopping centres.

York Timber intends to raise R250 million by way of a partially underwritten renounceable rights offer of 142,857,142 ordinary shares at a price of R1.75 per share. A2 Investment Partners will underwrite between R111 million and R160 million of the offer for a fee of R4,78 million. The proceeds of the offer will be utilised to preserve the timber volumes by procuring more timber externally and will be applied towards capital investment in manufacturing plants.

In terms of the scrip distribution alternative, Datatec will issue 3,171,196 new Datatec shares resulting in a capitalisation of distributable retained profits of R137 million.

Oasis Crescent Property Fund will issue 901,099 new units in terms of its scrip distribution alternative resulting in a capitalisation of distributable retained profits of R21,08 million.

As part of its capital optimisation strategy, Investec Ltd acquired on the open market a further 1,359,287 Investec Plc shares at an average price of 500 pence per share (LSE and BATS Europe) and 1,716,167 Investec Plc shares at an average price of R104.32 per share (JSE). Since October 3rd the company has purchased 12,58 million shares.

Transpaco has announced its intention to repurchase 1,56,000 shares from Samuel Abelheim Holdings at R27.48 per share for an aggregate of R42, 87 million, to be drawn from cash resources. The repurchase, which represents 4.95% of the issued share capital of the company, is a related party transaction and thus requires the approval of shareholders.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Glencore this week repurchased 16,100,000 shares for a total consideration of £89,20 million. The share repurchases form part of the second phase of the company’s existing buy-back programme which is expected to be completed by February 2023.

South32 has this week repurchased a further 1,021,256 shares at an aggregate cost of A$4,09 million.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period November 28 – Dec 2, a further 5,156,456 Prosus shares were repurchased for an aggregate €315,53 million and a further 850,610 Naspers shares for a total consideration of R2,21 billion.

British American Tobacco repurchased a further 580,373 shares this week for a total of £19,77 million.

Two companies issued profit warnings this week: Marshall Monteagle and Sebata.

Three companies issued or withdrew cautionary notices. The companies were: Jasco Electronics, Murray & Roberts and Jasco Electronics.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")