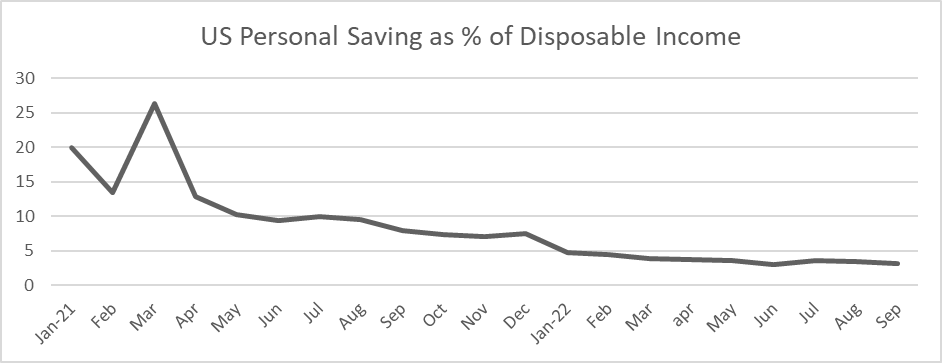

Hyprop reports improved trading conditions

The retail-focused property fund has released a pre-close update

With a retail portfolio in South Africa and Eastern Europe, Hyprop has been thrilled to see the return of shoppers to the malls without masks on their faces. Let’s face it – shopping with masks was no fun at all.

In a pre-close update, the company kicks off with the balance sheet and notes that 84.4% of shareholders (including yours truly) elected the dividend reinvestment plan. This represented a value of R844 million, which had to be reduced on a pro-rata basis to R500 million. There’s also strong demand for the company’s debt, with a bond auction of R785 million in November being 1.4x oversubscribed.

Around 80% of debt is hedged against interest rates, which is important as those rates are on the up in South Africa and Europe.

The group’s loan-to-value ratio is 38.2%.

Looking at the South African performance at tenant level, tenant turnover for the four months to October is 16.9% higher than the previous year. Trading density (which takes into account the trading space) is up 15.7%. Foot count is running 7.1% higher than the comparable period in 2021, so the combination of more shoppers and high inflation is definitely helping.

With a vacancy rate in October of just 1.3%, the situation looks far better than the October 2021 (2.6%) and 2020 (3.3%) numbers.

In Eastern Europe, turnover is up 8.4% year-on-year and trading density is up 8.9%. Foot count is 10.9% higher. Vacancies at 0.5% are actually higher than in October last year, when they were 0.3%. Still, that’s a low vacancy rate regardless.

The African portfolio isn’t a happy story, with Hyprop still trying to exit its investment in the Ikeja City Mall in Nigeria. In Ghana, the deteriorating economy means that a term sheet to sell the properties fell through.

Overall, it sounds like the most important parts of the portfolio are doing well.

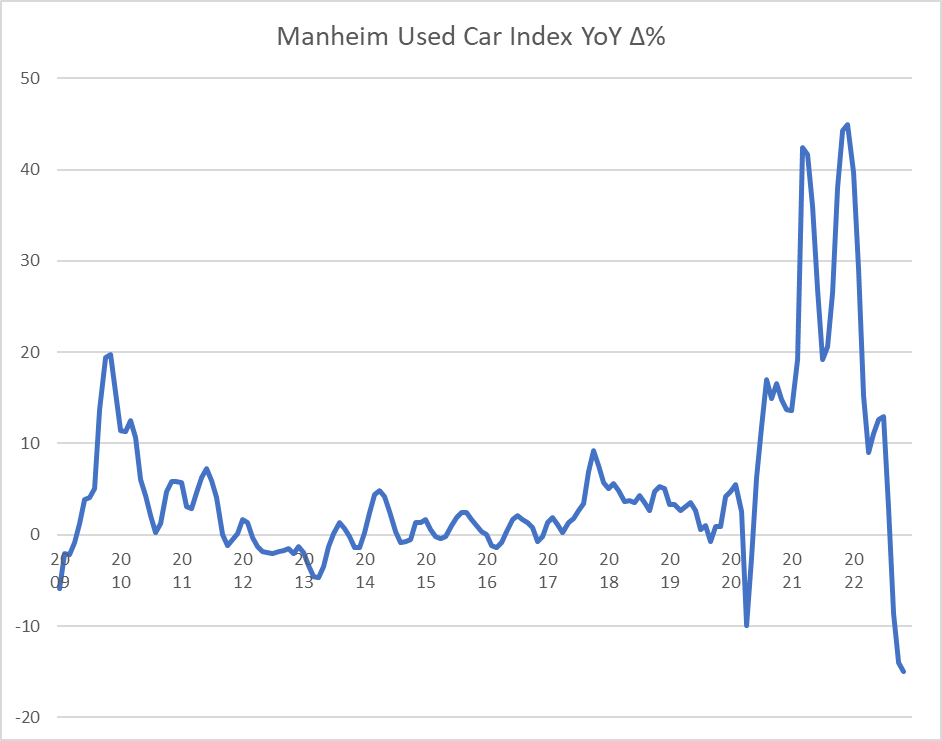

Metair has proven its mettle

Floods, hyperinflation and supply chain challenges – it’s been quite a year

Metair has really been through the most this year. With key operations as far apart as KZN and Turkey, the group has somehow been hit by natural disasters and hyperinflation in the same year. If they didn’t have bad luck at Metier, they would have no luck at all.

In the Automotive Components vertical, the flooding at Toyota’s factory caused havoc in the middle of the year. Production levels resumed during September and stabilised at pre-flood levels. An insurance claim of R400 million has been received thus far and the final claim is under review, with a cap of R500 million. At Ford, production of the next-gen Ford Ranger commenced in mid-November and Metair subsidiaries have entered production and ramp-up phases. Costs of R475 million related to the new Ranger will be incurred in FY22, of which at least 35% will be capitalised.

Despite all these issues and delays, volume expectations over the model lives remain unchanged. The company expects OEM production volumes to be over 700,000 units from 2023, provided supply chains are stable.

To put the importance of a new model into perspective, Metair expects the revenue from the new Ford model to be R46 billion over the model life, if I interpret the announcement correctly.

In the Energy Storage business, margins were impacted by extremely high inflation in Turkey and Romania. The costs are being recovered from customers, but there was a time lag. It all comes down to this quarter, which is the most volume sensitive for the business. It’s a mixed bag of expectations, with the Turkish business expected to be 17% higher, Romania down by 15% and South Africa flat.

Hyperinflation in Turkey is a mess, requiring Metair to apply the painful and complicated hyperinflation rules in IAS29.

Looking at the balance sheet, supply chain challenges have necessitated a larger holding of inventory on the books to allow for potential shipping delays and increases in airfreight costs.

Finally, efforts to achieve a “value unlock opportunity” have not been successful, mainly due to the overall investment climate in Eastern Europe which has obviously been negatively impacted by the war in Ukraine. For now, Metair will focus on running the businesses as best it can.

This share price chart gives you a great visual of how wild this year has been for the company:

Disaster at Murray & Roberts

The Clough deal is dead and the share price has tanked

Just when there was some solid momentum in the strategy to save Murray & Roberts’ balance sheet, there’s a new disaster for shareholders in the form of a 21% drop in the share price thanks to the Clough deal falling over.

The buyer needed to put in an interim loan facility of A$30 million to avoid Clough being placed under voluntary administration. For whatever reason, the parties couldn’t agree on the terms of the loan and so the transaction has collapsed and the buyer has walked away.

With Clough in urgent need of capital, the directors have no choice but to place the company under voluntary administration in Australia. Murray & Roberts has also placed its Australian investment holding company into voluntary administration.

The only other investment in Australia is RUC Cementation, which has a net asset value of $85 million and which has not been placed into administration.

Other than the interest in RUC and a guarantee to Clough USA (related to the old buyout of minorities) of A$3 million, Murray & Roberts has no residual exposure to Australia.

Voluntary administration appears to be quite similar to business rescue, with the goal of preserving the company. That certainly doesn’t mean that any equity value will be preserved.

Green bank, green share price performance

Like the other banks, Nedbank is enjoying these trading conditions

In a pre-close update covering the 10 months to October, Nedbank noted that the company is performing in line with the guidance given during August.

Net interest income is increasing by low double digits, supported by an increase in average interest earning banking assets of mid-single digits. Solid loan growth is being experienced across the corporate, business banking and retail books. Of course, the other factor here is net interest margin (NIM), which improves as interest rates increase.

The credit loss ratio is within the 80bps to 100bps guidance provided for full year 2022. There is some pressure coming through from the corporate book, including stressed borrowers in sectors like commercial property, aviation and agriculture.

Non-interest revenue (NIR) grew by high single digits. This has been a mixed bag, with solid performance in businesses like insurance and pressure in trading income and asset management income. Due to delays in closure of renewable energy deals, there is risk of Nedbank missing guidance for NIR.

As I’ve written about before, the key metric to watch is positive jaws, as this means that margins are heading the right way. The good news is that this is indeed the case for Nedbank.

The bank is on track to beat the 2019 level of earnings and is focused on achieving a return on equity (ROE) above the 2019 level of 15% by the end of 2023. The longer-term goal is over 18%.

Nampaking another punch to shareholders

After suffering a huge knock, Nampak shareholders have taken another 8.5% smack

The market hated the news of a rights offer last week, a necessary step in giving Nampak’s balance sheet some breathing room. The market clearly didn’t like these results either, with the share price coming under further pressure.

For the year ended September, revenue increased by 21% and trading profit increased by 13%. That sounds rather good, until you read further down the income statement. Operating profit before net impairments fell by 4% to R1.2 billion, which isn’t pretty but is clearly still a large, positive number. The result was helped along by strong volumes in beverage cans and the liquid paper business.

By the time you get to attributable profit though, you’ll instead find a loss of R147 million vs. a profit of R207 million in the comparable period. Ignoring impairments, headline earnings came in at R229 million vs. R402 million in the prior year. Detractors included foreign exchange losses, higher interest rates and increased impairments.

With all this noise in the numbers, another useful metric is cash generated from operations before working capital changes. This fell by 11% to R1.5 billion.

Although Nampak managed to comply with its major debt covenants (net debt : EBITDA and EBITDA : interest), the problem is that a major facility (R1.35 billion) is repayable soon (March) and the group can’t cover that repayment without an equity capital raise. This is partially because efforts to dispose of certain assets were unsuccessful.

The proposed rights offer is for R2 billion, with the excess to be used in the business and to pay advisory fees to the bankers etc.

The share price chart makes for an unpleasant sight:

There’s nothing salty about Oceana’s earnings

Despite a stronger second half, the dividend is still slightly lower

For the year ended September, Oceana grew its revenue from continuing operations by 12% and operating profit by 11%, so margins came under a bit of pressure. The benefits of financial leverage were felt further down the income statement, with headline earnings per share (HEPS) from continuing operations up by 17% to 626 cents.

Looking at the full group, revenue was up 11% but operating profit only increased by 6% and HEPS increased by 10% to 606.2 cents. From this, you can immediately see that the discontinued operations are loss-making (group HEPS of 606.2 cents vs. HEPS from continuing operations only of 626 cents).

The dividend has come under some pressure, with a decrease of 3% to 346 cents per share. This is likely due to a significant drop in cash generated from operations which fell by 33% because of increased canned fish and fishmeal inventory levels. When the business is sucking up cash, there’s less available for shareholders. A mitigating factor was a 12% decrease in capital expenditure.

It could certainly have been a lot worse, with the second half benefitting from a normalising supply chain in key businesses and favourable fishing conditions in the US.

Keep an eye on the balance sheet – net debt to EBITDA has increased from 1.5x to 1.7x. This is due to higher working capital requirements and the transaction of USD-denominated debt at a weaker exchange rate. Gross debt reduced by 6% in South Africa and 7% in US dollar terms, so any dollar weakness will help this ratio going forward.

Tharisa announces record profits

Record output is being achieved at a time when the commodity market is strong

Mining houses can’t control commodity prices. The most they can do is control production and look to capitalise on favourable conditions. With record earnings, Tharisa has done exactly that.

For the year ended September, revenue increased by 22.7% and EBITDA was up 12.9%, with clear cost pressures despite the company’s best efforts. Net profit increased by 35.6%.

Cash conversion was under pressure in this period, decreasing by 11.1% despite the increases in profitability.

The company reports in dollars and releases a press release based on rands, so the correct way to report the dividend is in dollars. At 7 US cents per share, the dividend is lower than 9 US cents in the comparable period.

Strategically, construction at the Karo Platinum Project in Zimbabwe has commenced and funding is well underway, with a goal of doubling Tharisa’s output in less than 24 months’ time.

York Timber taps the market

The company will raise R250 million through a heavily discounted rights offer

With a current market cap of R860 million, York Timber’s raise of R250 million is substantial. The share price has lost around 32.5% of its value this year, with only a 2% drop in response to the news of this capital raise.

The good news in this rights offer is that the money isn’t being raised to pay back the banks, as has been the case with most recent capital raises on the JSE. Instead, the capital will be used to procure more timber externally and invest in manufacturing plants, thereby allowing the harvesting age on the escarpment plantation to increase from 20 years to 23 years.

The company believes that this will enhance shareholder returns in the medium- to long-term. That would be nice, as York has historically struggled to give much love to shareholders.

The underwriter is A2 Investment Partners, the activist investment that has been involved in York for a while now. The underwritten portion is expected to be somewhere between R111 million and R160 million, subject to A2 not breaching the 35% threshold and needing to make a mandatory offer. An underwriting fee of R4.78 million will be paid to A2 for this.

The dilution for any shareholders not following their rights is substantial, with a 33.87% discount to the 30 day volume weighted average price. This is a renounceable rights offer, which means shareholders that don’t want to follow their rights can sell the right (known as a “nil paid letter”) on the open market.

Whatever you do, either follow your rights or sell the right. You’ll find it in your broker account on 4 January. If you do nothing, you will lose money.

Little Bites:

- Director dealings:

- At Lighthouse Properties, directors seem to be nothing if not consistent. Mark Olivier is the latest director mopping up shares on a regular basis, this time worth R715k. Of course, you won’t be shocked to learn that Des de Beer bought another R2.25m worth of shares

- In an unusual trade that I assume is a hedge, a director of Ascendis has sold CFDs on the company’s shares with a total value of around R143k

- A group of directors of Ninety One are part of an investment vehicle that invests in shares in the company, with the latest example being a purchase worth around R9.1m

- A non-executive director of Sibanye-Stillwater has sold shares worth R237k

- A non-executive director of Stefanutti Stocks has purchased shares worth R275k

- A director of Afrimat has bought shares in the company worth R47.5k

- Sygnia jumped 9.8% after releasing results for the year ended September. Despite assets under management and administration falling by 3.8%, revenue increased by 9.7%. HEPS is up 12.1% and the total dividend per share increased by 55.6% to 210 cents.

- Alexander Forbes has released results for the six months ended September. Although operating income from continuing operations increased by 8%, profit from operations fell by 9% because of lower-than-expected market performance and higher operating costs. HEPS from continuing operations fell by 15%. The discontinued operations are doing well ironically, with group HEPS up by 11%. The interim dividend of 15 cents per share is 25% higher than in the prior period. In further bad news for the Sandton property market, Alexander Forbes is targeting a smaller footprint with lower rates that could achieve a 350 basis points reduction in the cost-to-income ratio.

- Sabvest has executed a small investment in Valemont Trading, a business that produces a range of products for the pet market. The company is also the largest manufacturer and distributor of bird seed and related feeder products in the country. Sabvest has acquired a 39.3% equity interest and will also provide additional loans to execute an acquisitive growth strategy. Sabvest doesn’t play silly games, so keep an eye on this space as a platform for growth in this market. The deal value wasn’t announced.

- BHP Group is still dealing with the legal fallout of the Fundão Dam collapse in 2015. With legal proceedings underway in Brazil, there is now a claim in the English courts that BHP is disputing due to the existing proceedings in the country where the disaster happened. BHP and Vale each held 50% of Samarco, the owner of the dam. As Vale hasn’t been named as a defendant to the claim in England, BHP had to file a “contribution claim” with a view to Value contributing to any damages that may be payable under a ruling in that country.

- With Vodafone Group Chief Executive Nick Read stepping down at the end of December, there was some chatter on FinTwit about whether the local CEO might be promoted to the role. At this stage, that’s pure speculation. Still, Vodacom felt the need to announce this change of management at the global mothership.

- Glencore has reached an agreement with the DRC over the company’s past conduct. The DRC will be paid $180 million in settlement. I would just love to know where that money will go.

- Lighthouse Properties has successfully raised R50 million at an issue price of R6.50 per share. This is the same as yesterday’s closing price and in line with where it has been trading for the past few days.

- Jasco Electronics is a rather obscure company with a market cap of just over R50 million. It makes no sense for a company of that size to be listed, so I’m not surprised that a cautionary announcement has now been released regarding an intention to make an offer by Community Holdings, the company’s major shareholder. The idea would be to subsequently delist the company as well. The offer price of 16 cents per share is a 4% premium to the 30-day volume weighted average price (VWAP).

- Most of the shareholders in Datatec elected to receive the special dividend in cash (R2.63bn) rather than in scrip (R137m).

- Grindrod’s special dividend of 55.9 cents per ordinary share has received approval from the SARB.

- At Oasis Crescent Property Fund, unitholders of 32.3% of units elected to receive the cash distribution and the rest elected to receive additional units instead (like a scrip dividend).

- Marshall Monteagle has released a trading statement for the six months to September, reflecting a headline loss per share of $0.069 vs. a profit of $0.072 in the prior period (which isn’t directly comparable because of a change in year-end). The company attributes this to declines in stock market valuations that have subsequently reversed.

- If you’re curious about the process of business rescue, then following Tongaat at the moment will be of interest to you. The next step is for shareholders to vote on the remuneration of the business rescue practitioners in a vote to be held on 9 December.

")

")

")

| Premier)")