The African continent is home to a rapidly growing and vibrant start-up sector, with new players aggressively seeking to disrupt traditional industries and challenge the status quo. Funding for start-ups in Africa has reached an all-time high, with more than US$4 billion being raised to date in 20221, of which the lion’s share was raised in Africa’s ‘big four’ countries: South Africa, Kenya, Nigeria and Egypt. By way of example, Kenya alone attracted more venture funding in the first three months of 2022 ($482 million) than it did in all of 2021 ($412 million)2. While only attracting approximately 1% of global venture capital funding in Q1 of 2022, it is likely that African start-ups’ share of global venture funding will continue to rise.

African start-ups are solving real-world problems and are often aimed at addressing basic societal needs. They often involve innovative digital solutions to everyday problems within fintech, agritech and edtech, to name a few. This contrasts with start-ups in developed economies, which typically search for digital solutions to improve and refine efficiencies of existing applications.

OPPORTUNITIES AWAIT

It is predicted that the population of Africa will double by 2050, when it is projected that Africans will comprise more than 25% of the global population3. Africa, at present, has the youngest population on Earth, with a median age of 18.8 years, compared to the global median of 31 years4, and may, in a conducive environment, be expected to benefit from a substantial demographic dividend in future. A younger population that is open to advances in technology can stimulate entrepreneurial growth and investment in non-conventional businesses and assets, while also providing a dynamic market within which new start-ups can flourish. These factors set the stage for African entrepreneurs to develop and scale attractive African start-ups.

Africa is, however, faced with numerous challenges, some of which have plagued the continent for decades. However, such challenges also present opportunities to start-ups. By way of example, despite having 60% of the world’s arable land, Africa is a major importer of food and relies heavily on the likes of Ukraine, Russia and other exporters for basic foodstuffs and agricultural inputs. The war in Ukraine continues to threaten agricultural supplies to much of the continent, driving up prices and placing additional pressure on already strained businesses and consumers. Agritech start-ups are endeavouring to address these basic needs and bring much needed relief to African consumers, whilst capitalising on the extensive commercial opportunities. AgriProtein and Twiga Foods are examples of two African start-ups that have already made inroads within the Agritech space. AgriProtein diverts organic waste from landfills and transforms this into feedstock for animals, while Twiga Foods connects farmers with vendors via its distribution and logistics technology.

With more than half of all Africans owning a smartphone, many entrepreneurs are launching mobile-first businesses, enabling an extensive and rapid reach to large audiences. In the fintech space, such businesses serve to broaden access to traditional financial services, including mobile-based money transfers, payments and micro-lending.

HOW TO STIMULATE GROWTH IN AFRICAN START-UPS?

A starting point should be the establishment of in-country and regional policy frameworks, and a regulatory environment that promotes agriculture, fintech and other essential industries and removes the perennial credit, land tenure, market, and technology barriers that have beleaguered these sectors and basic services for decades5. Africa, as a resource rich and culturally diverse continent, desperately needs innovation and technology to harness the resources and human capital that are readily available.

African countries are becoming increasingly open to entrepreneurship and innovation. Governments are expanding investment initiatives that support start-up growth, and are creating policies to make it easier to do business in Africa. In order for these start-ups to thrive, they require access to sustainable and timeous funding. Such funding avenues include:

• Venture capital – generally for early-stage start-ups with limited to no track record; • Grants from governments and other institutions – bodies promoting local investment and entrepreneurship, enabling job creation; • Mezzanine finance – flexible, with a hybrid nature, combining debt and equity finance, generally available for start-ups in a more developed stage of their life cycle, with financiers able to participate in future upside through an equity share; and • Senior debt – available to more mature businesses, once start-ups have proven operational cash flows and accumulated assets and recurring contracts with customers.

Following successful fundraising and investment, start-ups, such as the African Leadership Academy which, to date, has raised more than $80 million in funding6, have set the stage for other success stories within Africa. This particular start-up seeks to “transform Africa by developing a powerful network of over 6,000 leaders who will work together to address Africa’s greatest challenges, achieve extraordinary social impact and accelerate the continent’s growth trajectory”. The awareness that is created by these start-ups is essential for continued investment into Africa.

POSITIONING FOR FUTURE SUCCESS

According to the e-Conomy Africa 2020 report, Africa’s internet economy is one of the largest overlooked investment opportunities available7. The current growth in African start-ups provides a glimpse of a future in which Africa continues to gain recognition as a global investment destination.

Whether you are an African start-up seeking capital, or an investor wishing to invest in an African start-up, a prudent first step would be to find a trusted advisor who is familiar with the African business landscape, to help navigate any potential pitfalls en route to future success.

1) https://thebigdeal.substack.com/. Published on 4 October 2022. 2) https://venturesafrica.com/africans-tech-space-is-thriving-amidst-a-global-meltdown/ 3) https://www.economist.com/special-report/2020/03/26/africas-population-will-double-by-2050 4) https://www.statista.com/statistics/1226158/median-age-of-the-population-of-africa/ 5) https://www.weforum.org/agenda/2022/05/averting-an-african-food-crisis-in-the-wake-of-the-ukraine-war/ 6) https://startuplist.africa/startup/african-leadership-academy 7) https://www.businessinsider.co.za/the-start-up-ecosystems-in-africa-is-s-an-overlooked-investment-opportunity-vc-fund-2022-6

James Moody is a Corporate Financier | PSG Capital

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication

There has been speculation around what has happened to the (new) Companies Amendment Bill. In this article, we consider some of its key features, should it be promulgated in its current form.

Status Quo

On 1 October 2021, the Department of Trade, Industry and Competition (DTIC) published the latest draft of the Companies Amendment Bill (Amendment Bill) in Government Gazette No.45250, which contains some departures from the prior version, published on 21 September 2018. The public was afforded a 30- day period to submit any comments in relation to the Amendment Bill and, since then, there has been media speculation as to the delay in its much-anticipated promulgation. Desmond Ramabulana, the DTIC’s Head of Commercial Law and Policy, provided useful insights regarding the progress of the Amendment Bill by confirming, in a comment to journalist Ann Crotty in June, that the DTIC is analysing the comments received last year and, once complete, the Amendment Bill will be referred to cabinet for parliamentary introduction. When questioned by the Financial Mail as to the expected timing of this process, Ramabulana indicated that “there are no timelines that can be pre-empted, but the department is aiming to make sure this bill [is] referred to Parliament within this financial year.”

The Amendment Bill aims to accomplish three noteworthy policy goals, namely:

(1) improving the ease of doing business with regard to certain provisions of the Companies Act No.71 of 2008, as amended (Companies Act);

(2) enabling greater wage ratio transparency at the firm level; and

(3) addressing true or beneficial ownership of companies, so as to confront money laundering apprehensions.

Some of the key amendments in the amendment bill

I) Enhanced transparency on disclosure of remuneration An amendment that would likely have attracted significant public comment is the director’s remuneration report for state-owned and public companies. The Amendment Bill, in clause 6, entrenches principle 14 of the King IV Code (Principle 14) by introducing a requirement for public and state-owned companies to prepare a remuneration policy for directors and prescribed officers. Notably, the Amendment Bill, in section 30A(2), extends Principle 14 by requiring that the remuneration policy be approved by shareholders, by way of ordinary resolution at the annual general meeting (AGM), and every three years or whenever any material change is made.

S30A(3) of the Amendment Bill states that the company’s remuneration policy must be detailed in a remuneration report, which must include:

(a) a background statement; (b) the aforesaid remuneration policy; (c) the implementation report, detailing the remuneration received by directors and prescribed officers; (d) total remuneration and benefits of the highest remunerated employee; (e) total remuneration of the employee with the lowest remuneration; and (f) the average remuneration of all employees; median remuneration of all employees; and the remuneration gap, reflecting the ratio between the total remuneration of the top five percent of highest paid employees and the remuneration of the lowest paid employees of the company.

As per s30A(6) of the Amendment Bill, the remuneration policy and implementation report, whilst both forming part of the remuneration report, must be approved independently by ordinary resolution of shareholders.

S30A(7) of the Amendment Bill states that if the remuneration policy is not approved at the AGM, changes cannot be made thereto, and it must be presented at the next AGM or general meeting until approval is obtained. S30A(9) of the Amendment Bill states that if the implementation report is not approved, the remuneration committee (or the responsible directors’ committee) must, at the next AGM, present to shareholders the details of how their concerns were considered, and the non-executive directors who serve on the aforesaid committee shall be required to step down for re-election every year that the implementation report is rejected.

In our view, it is likely that public comment focused on the approval processes for the remuneration policy report and implementation report, as contemplated in terms of sections 30A(2), (4), (6) and (7) and (9) of the Amendment Bill, as well as the insertion of section 30A(3) (e) and (f) above, dealing with, inter alia, the total remuneration of the employee with the lowest remuneration in the company and the average remuneration of employees, median remuneration of employees, and the remuneration gap between the highest and lowest paid employees, respectively.

II) Financial Assistance A long-awaited change in the Amendment Bill is clause 11 thereof, which amends s45 of the Companies Act by inserting a new section, 2A. S2A specifies that the provisions of s45 of the Companies Act will not apply to a company that gives financial assistance to, or for the benefit of, its subsidiaries. This amendment arises from the notion that the protections currently provided for in s45 of the Companies Act need not regulate the provision of financial assistance between a holding company and its subsidiary. This amendment will ameliorate the unnecessary inter- group compliance burden that s45 of the Companies Act currently gives rise to.

III) Share Repurchase Requirements Another change in the Amendment Bill (which is eagerly anticipated by many), is the proposal to revise s48(8) of the Companies Act by requiring that all share repurchases be approved by special resolution of the shareholders, unless it entails a pro rata repurchase from all shareholders or a repurchase on a recognised stock exchange on which the shares are traded. Accordingly, the present provision of s48(8), which requires compliance with the requirements of s114 and s115 of the Companies Act if the transaction involves an acquisition of the company of more than five percent of the issued shares, will no longer apply. In our view, this amendment is well-supported, as the present provision places a burden on companies to comply with s114 and s115 of the Companies Act (which are not well-suited to share repurchases) which includes, inter alia, the obligation to obtain an independent expert report for repurchases of shares in excess of five percent of any class of shares of the company. If promulgated, it will end the debate as to whether the provision means that such repurchases of shares must be undertaken by way of a scheme of arrangement.

In a judgment that has entrenched the compliance burden, on 8 June 2022, in the matter of First National Nominees (Pty) Ltd and others v Capital Appreciation Limited and Others, the Supreme Court of Appeal confirmed that s48(8)(b) of the Companies Act contemplates that share repurchases in excess of five percent are subject to all of the procedural requirements and rights delineated in s114 and s115 of the Companies Act. Thus, if the proposed amendment to s48(8) is promulgated, it would be a welcomed simplification of what has become a burdensome section which arguably provides little practical benefit to stakeholders.

IV) Beneficial Owners of Companies The Amendment Bill revises s56 of the Companies Act by introducing a definition of “true owner”, and measures what companies will need to adhere to, to establish and report their true ownership. Essentially, “true owner” is defined as the natural person who would, in all circumstances, be considered the ultimate and true owner of the relevant securities, whether due to (directly or indirectly) being entitled to the benefit from the securities, due to (directly or indirectly) being able to direct the registered holder with regards to the securities, or for any other reason.

These amendments identify the true owner of shares of a company by identifying both the beneficial holders and ultimate beneficial owners of its shares. These amendments

(i) oblige all companies to require from their registered shareholders, details of the identity of persons who hold beneficial interests in the companies’ shares; (ii) strengthen the existing provisions relating to companies’ establishing and maintaining a register of the owners of beneficial interests in its shares, and disclosure by shareholders relating to the persons who hold beneficial interests in its shares; and (iii) (iii) require all companies to publish in their audited financial statements, details of all persons who, alone or in aggregate, hold beneficial interests amounting to five percent or more of a particular class of shares.

The proposed definition of “true owner” aligns with the definition of “beneficial owner” in the Financial Intelligence Centre Act No. 38 of 2001. The rationale for the revision is to eliminate company ownership arrangements that are used for illicit and criminal purposes. This is significant in allaying concerns about the potential Grey-listing of South Africa by the Financial Action Task Force.

V) Other Amongst what are regarded as a number of more “technical” changes, other useful changes in the Amendment Bill include:

• Section1: The definition of “securities” has been amended to delete the phrase ‘other instruments’, which removes any ambiguity regarding the scope of securities;

• Section 16(9)(b): This revision clarifies that the period in which the Companies and Intellectual Property Commission (CIPC) should accept a Memorandum of Incorporation (MOI) amendment will be limited to 10 days, subject to a few exceptions;

• Section 38A: This revision provides for judicial intervention, to enable parties to obtain certainty regarding the validity of share issues where the requirements of the Companies Act or a company’s MOI were not strictly adhered to; and

• Section 135: This proposed change clarifies that any utility- related payments made by a landlord to third parties during business rescue proceedings will be regarded as post- commencement financing and will rank before concurrent creditors, but after employees.

Conclusion

After the DTIC has reviewed the public comments, the Amendment Bill’s promulgation will provide significant and, in our view, mostly positive improvements to the Companies Act. In summary, the revision of inter- group financial assistance and share repurchase provisions will improve the ease of doing business.

Significantly, the introduction of the definition of a ‘true owner’ will aid in identifying the beneficial holders and ultimate beneficial owners of a company’s shares. It remains to be seen how industry will react to the more contentious aspects of the Amendment Bill, being the enhanced transparency and approval procedures in relation to remuneration, particularly sections 30A(2)(e) and (f), as well as s30(9). As with any legislative development, the market will no doubt appreciate certainty either way, both as regards the substance of the changes, and the timing.

Anthea Eleftheriadis and Tevin Ramalu are Candidate Legal Practitioners. Supervised by Matthew Morrison, a Director in Corporate and Commercial | ENSafrica.

This article first appeared in DealMakers, SA’s quarterly M&A publication DealMakers is SA’s M&A publication www.dealmakerssouthafrica.com

Andre Botha of TreasuryONE sets the scene ahead of the MPC meeting on Thursday, in which a hike of 75 basis points is expected.

Taking a look at the last couple of weeks and the performance of the rand, it raises the debate of whether there is still some life in the rand rally, or whether we have we done too much in too short a time and a move higher is now more likely than a sustained move lower.

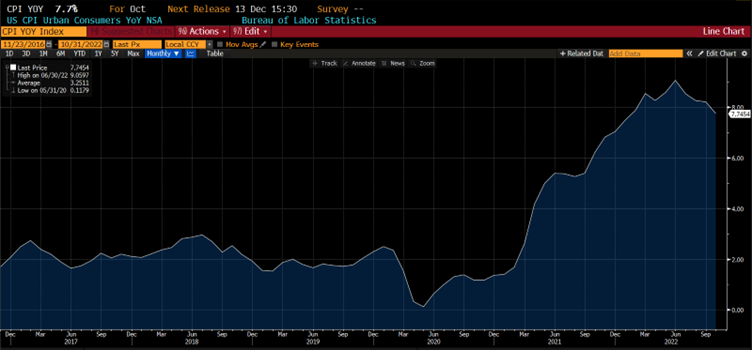

To understand the move lower, we need to understand what has caused the rand and other EM currencies to strengthen as much as they did. As we have become accustomed to over the last year, most of the movement in currency markets is down to the US dollar, and for the most part the Fed, and how they handle the inflation environment currently in the US.

That narrative has not changed in the slightest, as we have seen that inflation printed at 7.7%, which the market has seen as a time for the Fed to start tapering its hawkish talk around interest rates.

US inflation down

The key question to ask is whether we have seen enough of a pullback in inflation to warrant a change of tack by the Fed. The answer is most likely not, as the FOMC minutes will probably indicate.

The minutes will show that the Fed will be headstrong in chasing the 5% Fed funds rate before they start to change its tone regarding interest rates. In saying that, the fact that inflation is coming down will appease the Fed, and the next meeting in December will be key, as any change in stance from the Fed will filter through in that meeting and we could see some action in the back-end of December.

Now back to markets and what has happened in the last week. We have seen the US dollar on the back foot and drifting all the way to 1.0400 against the euro. That has meant that the rand has retraced all the way back to R17.2000 in the wake of the better-than-expected inflation numbers and the current optimism of the Fed pivoting sooner rather than later.

We have seen that the market is skittish on any China Covid news, but the effects of such news are temporary as the optimism outweighs any bad news from China. On the horizon, however, the looming recession is taking centre stage, and it’s only a matter of time before we could see the impact on EM currencies.

Rand enjoying the optimism

Although a lot of attention is being paid to the US Fed minutes, in South Africa we have the MPC meeting this week. We expect the MPC to hike interest rates by 75 basis points on Thursday, mainly in line with the hikes being done by the Fed. The key is what tone the MPC will strike after the announcement as growth in South Africa is anaemic at best and more hikes will hike us into a recession.

The rand has failed to sustain a break below the R17.2000, which leads us to believe that the rand is building a base currently and could look to trade weaker in the short term, where levels above R17.5000 should be used by exporters as we expect the rand to stage a recovery in the second half of 2023.

Visit the TreasuryONE website to learn about market risk and other solutions offered by the group.

African Media Entertainment welcomes back advertisers

The six months ended September 2022 were much stronger for the media assets

In this period, African Media Entertainment’s group revenue increased by 11% and operating profit increased by 22%. It gets better the further down you look, with profit before tax up 38% as the balance sheet also improved.

Regional radio is performing well again, with Algoa FM achieving results 86% above budgeted performance. The great irony is that disasters like water shortages and locust infestations helped the station secure unanticipated campaigns.

The story is similar across the other media assets in terms of performance at or above expectations, with the exception of Moneyweb. The financial media platform is running below budget across digital and radio offerings. A focus on events is part of the strategy to improve the numbers.

The interim dividend of 100 cents per share is 25% higher than last year’s interim dividend.

RFG Holdings is just peachy

This food group has had a solid year, even if the share price has gone sideways

RFG Holdings has released results for the 53 weeks to 2 October. This means there is an extra trading week in this period, which always distorts results. As a further distortion, the acquisition of Today pie was included in this result for eight months, accounting for 2.5% of group revenue growth.

I find it frustrating that the announcement doesn’t give pro-forma numbers based on a comparable 52-week trading period. This is what the grocery retailers do. Although group revenue increased by 21.9%, I know that some of this is due to the extra week.

Margins aren’t impacted by an extra trading week, so growth in group operating margin of 160 basis points is great news. Again, one needs to look deeper though – an insurance settlement of R43.4 million in this segment is a material number vs. operating profit of R574 million.

HEPS increased by 57.3% and the dividend followed suit, with a similar percentage increase to 45.8 cents per share.

Looking deeper, the good news story comes from regional fresh foods, ready meals, fruit juice and an export business that benefitted tremendously from the failure of last year’s peach crop in Greece, the world’s largest exporter of canned peaches. The weakening of the rand also helped the international business.

The noise in these numbers may explain why the share price doesn’t seem to be excited about the peach crop or the Today Pie business in 2022:

Prosus: the ultimate cash furnace

As conditions worsen in the world of frothy tech startups, Prosus is scaling back

After posting an operating loss from continuing operations of more than R1 billion in the year ended March 2022, Prosus has carried on where it left off with an operating loss of R287 million in the six months ended September 2022. If you prefer using core HEPS from continuing operations to assess performance, you’ll find a profit at least (64 cents) but a year-on-year drop of 54%.

Prosus claims to be reducing its cost base sharply to meet market challenges, so the chickens are coming home to roost here. Prosus made a number of risky investments during the pandemic in a low interest rate environment and in the immortal words of Dorothy, this isn’t Kansas anymore. Rates are much higher and the tech industry has been burning, particularly businesses that don’t have a proper business model.

The company notes that M&A investment of $230 million was considerably lower than in recent periods because of the rise in the cost of capital. It’s amazing what interest rates can do. There’s still plenty of investing through the income statement (as people like to call it), which means absorbing huge operating losses in portfolio companies that are essentially still startups.

Still, you just can’t keep a good venture capitalist down. Prosus committed €1.5 billion plus contingent consideration up to €300 million to acquire the remaining 33.3% stake in iFood from Just Eat Takeaway. In a more conservative move, Indian portfolio company PayU secured approval for the acquisition of BillDesk but didn’t pursue the deal after certain conditions were not met by the long-stop date.

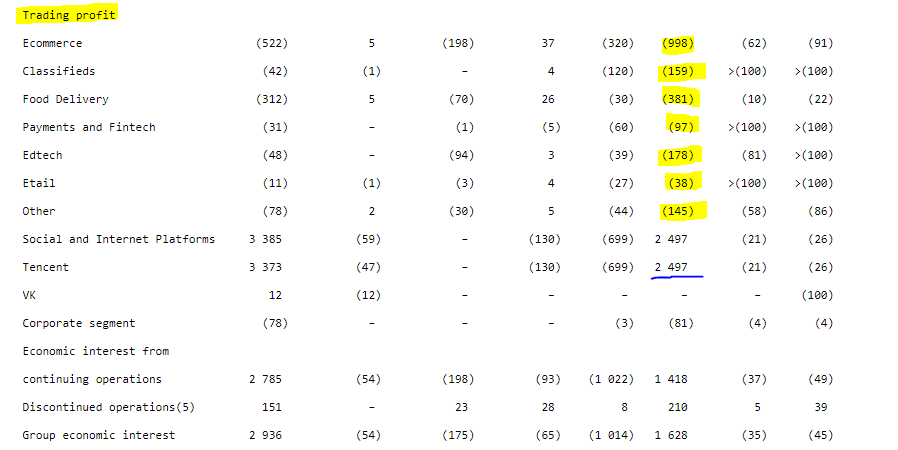

The good news in this result is that the management team is using share buybacks rather than further spiderweb-inspired structures to try and address the discount to NAV. After trimming its position in Tencent, repurchases worth $4.1 billion were executed.

Perhaps a table straight from the result will help you understand the problem with Prosus. You can’t see the headings but I’ve highlighted the trading profit (mainly losses) for this period as reported under IFRS rules. Prosus might be the most efficient furnace in the world, taking profits from Tencent and incinerating them in the rest of the group:

Naspers also released results and the complex group structure means that Naspers is almost perfect repetition of Prosus. There are some key differences though, like Takealot that is owned by Naspers. The online retailer achieved revenue of $433 million and incurred a loss of $13 million, a trading margin of -3% vs. -1% in the prior period.

Takealotta Capital should be the new name for the entire group.

Telkom releases ugly results for the six months to September

Revenue is down 0.7% and HEPS has fallen by a spectacular 51.9%

When people build investment models, they don’t include assumptions like “headline earnings being less than half what they were last year” – yet here we are. Telkom has released terrible numbers and the share price has lost over a third of its value this year. MTN walked away from a potential deal and Telkom’s financial performance has been laid bare, with the combination causing much pain for investors.

Much of Telkom’s revenue base is as modern as a CD player in a car. The company is in a race against time to replace the legacy fixed business as customers migrate to fibre and LTE. One of Telkom’s horses in the race is the Mobile business and a slight increase in revenue of 0.5% is disappointing when customer numbers increased by 10.9%. There is massive competition in that market.

With revenue only 0.7% higher, Telkom was a sitting duck for inflationary cost pressures that have hit other telecommunications players, like Vodacom. EBITDA fell by 17.3% and margin contracted by 470 basis points to 23.4%. An effort was made to contain costs as far as possible, with operating expenditure only 5% higher.

In fibre business Openserve, 46.2% of homes passed by fibre are connected to the network. There is clearly room to grow here. Openserve’s revenue fell by 4.3% because of legacy products, with only 65% of revenue derived from next-generation products.

BCX grew revenue by just 0.8% and Swiftnet, the masts and towers business, suffered a revenue drop of 2.1%.

Here’s the really ugly number: Telkom generated negative free cash flow of nearly R1.9 billion. By shifting consumers to post-paid models, the handset cost is incurred up front and revenue is collected over 24 or 36 months.

Telkom is following a “value unlock” strategy and is looking to sell the investment in Swiftnet partially or in full. Openserve is a legally separated subsidiary of Telkom, opening the door to partnerships in that business i.e. bringing in new shareholders.

Medium-term guidance has been revised, with revenue and EBITDA now only expected to grow by low- to mid-single digit percentages. The board hopes to reinstate its dividend at the end of FY23. With net debt to EBITDA of 1.7x and such a tough free cash flow number in this period, things will have to improve significantly for a dividend to become a reality.

Little Bites:

Director dealings:

A director of a major subsidiary of Santova has sold shares worth just over R2 million.

The CEO of SA Corporate Real Estate has retained shares worth around R3.4 million after a vesting of forfeitable performance shares based on reaching retirement age (the rest of the shares were sold to cover the tax).

Get ready to feel poor: Discovery director Barry Swartzberg has executed options trades to hedge his position in Discovery. The value? Across four options trades, the highest position value is R448 million!

Grindrod has declared a special ordinary dividend of 55.9 cents per share, representing a cash return of 25% of the consideration received from the sale of Grindrod Bank.

In an update to a deal announced back in March 2022 for the sale of Glencore’s Cobar copper mine in Australia, Glencore will receive up to $1.1 billion as originally agreed but with amended payment terms. Glencore will also receive a 1.5% net smelter return life of mine royalty. Of the $1.1 billion, only up to $875 million is payable in cash in the short-term. The rest is payable in equity or in cash depending on average copper prices.

The transition of Rand Merchant Investment Holdings into OUTsurance has taken another big step, with board changes coming on 1 December that will see the OUTsurance executive directors taking over the equivalent roles at RMI level.

NEPI Rockcastle has been in dispute for a long time regarding the discontinued acquisition of two shopping centres in Poland. The company had raised a provision of €37.3 million for this matter and the settlement amount has now been finalised at €16 million. This means that a €21.3 million reversal will come through in the current year distributable earnings, a 10% positive impact on the revised earnings guidance given in November. Based on this, NEPI Rockcastle expects distributable earnings per share to be 48% higher this year.

Deneb Investments released results for the six months ended September and they were heavily impacted by the timing of a Covid insurance claim in this period. Adjusting for that distortion, profit increased by 8% despite revenue increasing by 18%. Gross profit was only up 9%, with margins in the manufacturing segment coming under pressure. If you didn’t dig this deeply into the numbers, then you might’ve seen HEPS up by 59.1% and made a very different assumption about the performance.

Indluplace released results for the year ended September. Revenue fell by 2.9% and operating profit decreased 0.6%. The net asset value per share decreased by 6.5% to R6.37 and the share price closed at R3.00. The dividend increased by 13.6% to 31.95734 cents, so this residential property fund is trading on a yield of 10.65%.

Primeserv released interim results for the six months ended September. Revenue increased by 9% and HEPS jumped by 48%. An interim cash dividend of 2 cents per share has been declared and the share price closed at R1.05.

Anglo American keeps making progress in its carbon reduction and water usage plans. I keep saying this in Ghost Bites: Anglo American walks the talk when it comes to ESG. The latest news is that the company has secured a desalinated water supply for its Los Bronces copper mine in Chile from 2025. Anglo’s goal is to reduce fresh water abstraction in scarce water regions by 50% by 2030. At Los Bronces, Anglo plans to eliminate the use of fresh water entirely. This is the first step in that process, with an added benefit of desalinated water being supplied to nearby communities in addition to the mine (20,000 people).

Kibo Energy has signed a renewed Memorandum of Understanding (MOU) with Tanzania Electric Supply Company (TANESCO) regarding the development of the Mbeya Power Project. This project was first announced in 2018. There’s a lot of “agreeing to agree” here, with the renewed MOU essentially being an agreement between the parties to conclude a Power Purchase Agreement that would see TANESCO buying power from Kibo’s Mbeya project. This flagship project for a steam-powered facility has been revived and gives Kibo another iron in the fire alongside the bio-fuel initiative announced in August 2022.

Europa Metals has signed a definitive agreement with Denarius Metals Corp that would give Denarius the option to acquire up to 80% in Europa’s wholly-owned Spanish subsidiary. This is structured as a two-stage option: one for 51% and another for 29%. If Europa shareholders agree, this would inject an initial $4 million into the Toral project and a further $2 million down the line. Separately to this agreement, Europa has raised £580,000 by issuing shares at a substantial premium (more than 60%!) to the current traded price.

Brikor has released financial results for the six months ended August. Revenue increased by 10% but EBITDA fell by 50%. The group is breakeven at headline earnings level and no dividend was declared.

The best of British and the worst of Silicon Valley. This week, the focus is on iconic British fashion group Burberry and Elon Musk’s controversial approach to his newfound ownership of Twitter.

Burberry banks on British

British luxury fashion and beauty brand Burberry has released results for the first six months of its financial year ended September 2022. Overall, the company had a very successful half-year, with revenue rising by 11% to £1.3 million and adjusted operating profit growing by 21% to £238 million.

This was largely driven by a strong performance in the retail sector, where comparable store sales were up 5% with acceleration in the second quarter vs. the first (11% vs. 1%).

During the period, Burberry focused on expanding its brand through various endeavours such as the launch campaign of its Lola handbag range. Close your eyes vegans – leather goods saw an increase in comparable sales of 11% partly thanks to this.

The company appointed CEO, Jonathan Akeroyd, in March 2022. Akeroyd has been credited with helping to revive Burberry’s fortunes by emphasising its British roots. He has also been instrumental in expanding the company’s product range and increasing its store presence in key luxury locations around the world. These factors have all contributed to Burberry’s strong growth and have positioned it well for continued success in the future.

Burberry has also appointed English fashion designer Daniel Lee as the company’s new creative director. Lee, who was previously the creative director of Italian Fashion House Bottega Veneta, will be responsible for leading the creative vision of the company in line with its vision of modern “Britishness.” In his new role, Lee will be responsible for overseeing all aspects of the brand’s creative output, from design and marketing to product development.

The company has placed a strong focus on achieving top-line growth in recent years. This is evidenced by their aggressive expansion plans and target of £4 billion in revenue within the next 3-5 years. This target is even more ambitious when considering their long-term goal of £5 billion in revenue. It goes to show that the world may have mixed feelings about the Royal House of Windsor, but when it comes to the House of Burberry, things are looking up.

Elon Musk flips the bird

When a company acquisition is formalised by the new owner walking into headquarters carrying a porcelain sink and captioning the resultant tweet “let that sink in”, you know everyone is bound to get nervous.

Ever the showman, Elon Musk has provided the world at large with Days of Our Lives-level drama in his quest to own Twitter – and he doesn’t seem to be slowing down now that he holds the reins. With mass layoffs and controversial changes to the platform being implemented, this past week has been a tumultuous one for the digital soapbox, and the effects are starting to show.

Reports suggest that about a third of Twitter’s Top 100 marketers have not advertised on the social media platform in the past two weeks, presumably concerned about brand association.

Twitter is a platform that relies heavily on advertising for its revenue. In recent years, Twitter has tried to find other sources of revenue, such as subscriptions, but those products have not gained much traction, like Elon’s nosediving paid Blue Tick concept, which allowed people to go wild with pretending to be George Bush (blue tick and all) while tweeting about Iraq.

Twitter’s lack of diversification in its revenue sources could become a serious problem if advertising revenue continues to decrease in the future.

Of course, revenue may not matter at all if there is no-one left in the office to actually keep the platform running. At the moment, about 5 000 employees have either been laid off or have quit since Musk’s hostile takeover. To put that number in perspective: that’s over half of the company’s global workforce. And it’s not just the seat-warmers that are packing up their pot plants. Included in the employees who have resigned are a number of top executives, notably the Head of Integrity and Safety Yoel Roth, Chief Private Officer Damien Kieran and Chief Information Officer Lea Kissner.

Notably, with all these executives, Twitter never managed to eradicate child porn on the platform. Under Musk, it was sorted out within days. I’m no fan of Musk but there’s no disputing that something was very wrong in blue bird world.

Unsurprisingly, all of this commotion has resulted in lawsuits being filed against Twitter. These include alleged violations of the California WARN Act and the Americans with Disability Act. This came after Musk’s announcement that the majority of employees would need to work out of the office for at least 40 hours per week, making it infeasible for many employees with disabilities to continue their jobs.

Looking through the noise, is it all bad?

Breaking labour law is never ok and those lawsuits need to play out in court with compensation for those who deserve it. But if we look at the bigger picture here, Musk is proving that Big Tech has been fat and happy for far too long. Many times, investors have felt their blood boil at the news of another 20% increase in headcount when revenue is barely moving forward. Musk is staging a revolution in Silicon Valley and investors aren’t complaining, with tech layoffs now spreading across the industry.

A cursory flick through the complaints by ex-staff members at Twitter will reveal exactly what was wrong with this industry. While the investment bankers are working 12 hour days (and longer) for their big salaries and bonuses, many in Silicon Valley were goofing off on TikTok and worrying more about pointless committees than getting any work done.

If you don’t believe me, just consider that Twitter is still doing just fine and most of the staff are gone.

The biggest question is around revenue. A company can’t shrink its way into profitability if all the advertisers leave. Personally, whilst I doubt that Twitter will go down as a great investment for Musk, I reckon it will be OK. Most of all, I think it’s the wind of change that tech investors so desperately needed to feel blowing.

If you want to understand more about the issues that have been plaguing the tech industry, Magic Markets Premium has an extensive library of research on this sector. You can get access to research on Apple, Amazon, Meta, Microsoft, Intuit and so many others for R99/month or R990/year.

Is there room to celebrate or is the market getting ahead of itself?

It’s easy to get confused, so let’s clear this up immediately: Bidcorp is the food service business that was unbundled from Bidvest a few years ago. It no longer has anything to do with Bidvest, which is more of an industrial services player.

This is a truly global business, with a low percentage of profits generated in South Africa. The share price has historically traded at a high multiple, which is why shareholders have been on a mostly sideways journey since it listed:

In a trading update for the four months to October, the company surprised the market by talking about “record” results. Against a backdrop of high energy costs and constrained consumer spending, this is a lot better than I was expecting. A jump in the share price of over 5% suggests that I wasn’t the only one who was surprised by this.

This trading period covers the Northern Hemisphere summer, so the worst of the European issues arguably haven’t been felt yet. Still, there’s no denying the resilience in the business model here. Some of this resilience comes from non-discretionary demand from institutional customers, like schools and hospitals. This is obviously far less volatile than demand in the restaurant and entertainment industries.

On a constant currency basis, the group has been running at between 23% and 30% higher than last year’s levels over the past few months. Australasia is the standout region because of the base effect of Covid lockdowns. The Emerging Markets segment has been negatively impacted by China and ongoing lockdowns.

Of course, revenue is only part of the story. Gross margin is critical and the company says that most businesses have been able to pass through inflation increases to date.

The most impressive thing about this result is that operating expenditure increased by 20.8% on a constant currency basis and revenue increased by 25.5%. This is operating margin expansion at a time when most people expected the opposite. EBITDA margin is now ahead of 2019 levels.

As is the norm at this time of the year for Bidcorp, the business has absorbed working capital through buying-in inventory and paying suppliers earlier to secure supply. If you want to understand more about working capital, this recent bizval webinar is really useful. I spoke about working capital from around 12 minutes in:

Finishing off on Bidcorp, the investment in working capital led to a free cash outflow of R2.6 billion. Bolt-on acquisitions in this period came to R292 million. A bolt-on acquisition is a deal to buy a company that slots in very easily with existing operations.

So, has the market gotten too excited here? It all comes down to your view on the European winter. If you believe that the Europeans will get through the current crisis, then Bidcorp’s recent trading update makes a strong case for success.

The share is still trading at a very high multiple though, so be warned.

Coronation takes a big knock to earnings

When equity markets are down, asset managers suffer

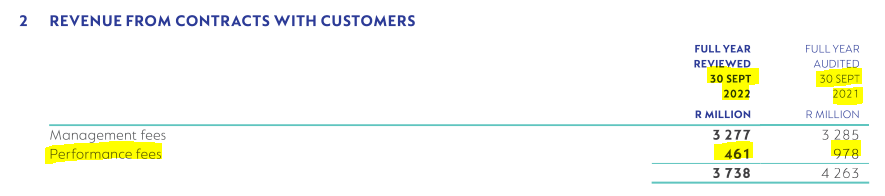

Coronation has R610 billion in assets under management (AUM) after the recent market rally. At the end of September, that number was R574 billion, down 9% year-on-year. Interestingly, average AUM for the year ended September was slightly higher than the prior period, so the earnings drop isn’t because of a drop in AUM.

If you’re wondering why revenue has dropped, you need to find Note 2 in the financial statements. Management fees are consistent, as you would expect when AUM is flat. The year-on-year pain lies firmly in performance fees:

The more concerning statistic relates to net outflows at 6% of average AUM. This means that clients pulled their funds out and either invested them elsewhere or left the market altogether.

I would pay close attention to this section of the report if I were you:

To soften the blow of revenue pressure, expenses fell by 12%. This was achieved through a variable expenditure model, which I think means that the top fund managers only earn big bonuses where there are large performance fees. This would certainly make sense. Fixed costs were up by just 2%.

Fund management earnings per share (which excludes any fair value movements) decreased by 18% to 387 cents. Diluted HEPS fell by 25% to 366.3 cents. The final dividend per share is 172 cents, taking the annual total to 386 cents. This is 18% lower than the prior year.

As you can see, Coronation pays out practically its entire fund management earnings per share number as a dividend. The trailing dividend yield is now 11.8% and the share price has lost roughly 40% of its value this year.

There’s momentum at Momentum

A quarterly operational update reveals far higher profits

For the three months ended September, Momentum Metropolitan managed to achieve a huge year-on-year increase in return on equity from 15% to 20.9%. You won’t see a swing like that every day! This was driven by a 73% increase in normalised HEPS.

Of course, there’s a significant base effect here from Covid. An improved mortality experience has assisted the numbers this year, a trend that you’ll also see in the Old Mutual update below.

The value of new business is below the group’s expectations and new business margins have dropped, which isn’t good obviously. The present value of new business volumes has also decreased by 3%, which the group attributes to a high base effect. Another irritation for the management team is that institutional and retail assets under management declined by 3%.

The short-term insurance businesses are under pressure overall. Guardrisk experienced a decline in normalised headline earnings of 13%, though Momentum attributes this to once-offs in the prior period (despite being a headline number). In good news, Guardrisk improved operating profit by 13%. Momentum Insure is where the real pain was felt in this segment of the business, with a loss of R16 million for the quarter because of a high claims ratio of 70% vs. 58% in the prior period. Rather than being due to a specific event, this was because of inflationary pressure on the cost of claims, offset slightly by premium increases on policy renewals.

The share price rallied 4.7% in response to this update.

Old Mutual will be applying for a banking licence

At what point will the banking sector be overtraded?

Before we get into the big news of the banking licence, let’s deal with the rest of Old Mutual’s business.

For the quarter ended September, there’s significant jump in Life APE sales (up 17%) after the Covid disruptions in the base period. Despite a decrease in gross flows of 7%, net client cash flow recovered from the prior period thanks to reduced mortality claims and lower client disinvestments and terminations. Unsurprisingly, funds under management fell by 6% at a time when global markets have come under pressure. Loans and advances were flat year-on-year. Gross written premiums increased by 12%, driven by higher renewal rates and new business sales.

Looking at profits, fewer Covid excess deaths in the current period means that profits in the life insurance business improved. Old Mutual Investments even managed to increase its profits thanks to higher asset-based fees on higher average asset levels despite market troubles. There were issues elsewhere in the group, like net catastrophe losses in the KZN floods.

With that out the way, let’s talk about the banking licence. Old Mutual has received Section 13 approval from the Prudential Authority to proceed with the application for a banking licence. Old Mutual wants to hold the primary relationship with customers who currently make use of existing lending products and other financial services. This will allow Old Mutual to accept retail deposits, which is a cheaper source of funding than most other options.

This isn’t a cheap strategy, as anyone at Discovery will tell you. Old Mutual has budgeted R1.75 billion to build the transactional capability and R830 million has already been incurred, with 10% of these costs capitalised. Launch is expected in the second-half of 2024 and breakeven status is only expected to be achieved within three years of launch. The group is targeting a return of 400 basis points above the cost of equity once the bank has achieved scale.

With savings of more than R700 million achieved in the business, much of the build cost is being achieved through finding efficiencies in the group.

Does the country need another bank? Probably not. Does this mean that Old Mutual won’t make a success of it? Also probably not. This is a huge group with a deep understanding of banking from the previous relationship with Nedbank.

I wouldn’t just ignore this initiative.

Omnia is up on key metrics

All three operating divisions grew revenue and operating profit

For the six months ended September, Omnia put in a strong result under tricky supply chain conditions. A strategy of ensuring supply to customers has paid off, even if it led to huge increases in net working capital.

Group revenue increased by 22.8% and operating profit was 18% higher, so there was some margin pressure. Operating margin fell by 30 basis points from 6.9% to 6.6%. Group HEPS only increased by 3% but adjusted HEPS from continuing operations increased by 32%.

This result came at a cost on the balance sheet, with net working capital increasing sharply from R3.1 billion to R5.2 billion, an increase of 69%. This was a direct result of higher investment in a rising commodity cycle, reflecting the strategy of making sure sales weren’t lost because of shortages.

Looking deeper, the Agriculture segment grew revenue 17% and operating profit 33%. The net working capital pressure in this segment is expected to unwind in the second half of the financial year. The Mining segment grew revenue by 32% and operating profit by 44%. The Chemicals business could only manage 0.3% revenue growth, but operating profit increased rather spectacularly by 108%. This is a direct result of product mix improvement.

The tax dispute with SARS is ongoing. The group has lodged an appeal against the revised assessments following the partial allowance of the objection. With literally hundreds of millions at stake here, this is important.

The outlook is upbeat, with the group noting the potential for significant additional upside within the business. I suspect that the overhang of the tax issue needs to disappear before the market will show Omnia much love.

Pepkor sells a lot of cellphones

7 out of 10 cellphones in South Africa, to be precise

In the year ended September, Pepkor achieved 5.3% growth in revenue. The floods and the change in Flash’s product mix were negatives here, with the group highlighting 8.1% growth excluding those factors. This gives some idea of the underlying momentum in the business.

Normalised HEPS (the right measure in this case) has grown by 15.7% and the dividend increased by 24.9%, so the group is falling more confident and is using a higher payout ratio.

That confidence has been earned, with 4.2% compound annual growth in like-for-like sales over three years. A gain in market share of 123 basis points has been achieved since pre-Covid times.

Distinct from all-important organic growth (215 net new stores opened during the period), the major step of acquiring Avenida in Brazil is working out well so far. Given the disastrous amounts of load shedding we are currently experiencing, exposure beyond our borders isn’t a bad idea. The double-whammy is severe, with the cost of power backup (70% of group stores have backup) and the negative impact on revenue from fewer customers visiting stores during periods of load shedding.

Here’s the most fascinating statistic of all: the group sold 12 million cellphones this year! This is 7 out of 10 handsets sold in South Africa.

Fun stats aside, the outlook for South African retail isn’t great. Load shedding as we head into the peak trading period is an absolute disaster and higher levels of inflation are expected into next year. The good news is that the cost of shipping has reduced.

This is probably why the share price dropped despite the strong growth in earnings, closing nearly 1.6% lower on the day. There’s been plenty of volatility along the way, with a year-to-date result that is rather flat:

Little Bites:

Director dealings:

A director of Mustek has bought contracts for difference (CFDs) on the company’s stock worth nearly R1.2 million

An associate of a director of Afrimat has sold shares in the company worth R3.3 million

An associate of a director of Sea Harvest has acquired shares worth R88.8k

Premier has released its pre-listing statement in all its 288-page glory. If you want to learn about this company that lists Tiger Brands, Pioneer Foods and RCL Foods as its three largest competitors, then you’ll find the document at this link

Tradehold released results for the six months to August 2022. The big news is that the company will be turning into a REIT, having now sold off the UK operations for £102.5 million. This has led to a special dividend to shareholders of R4.34 per share, in addition to the 30 cents per share interim dividend. The remaining assets are a 74.3% holding in the Collins Property Group and full ownership of the Nguni Group and the Tradehold Africa Group. These holdings will be the underpin for Tradehold’s new positioning as an industrial / logistics-focused REIT under the name Collins.

Jubilee has released an update on its operations. The cobalt operation at the Sable Refinery has achieved the production of export grade cobalt and has significantly increased its processing capability through bypassing a traditional, power-intensive smelting process. Targeted cobalt margins at capacity are in excess of 45%. As a reminder that Zambia is one of the friendlier jurisdictions in Africa for mining companies, Jubilee has been awarded a water licence to have its own, dedicated water supply infrastructure for operations at Project Roan. The group’s focus is on taking the learnings from the resource in the South to the resource in the North, which has the potential to far exceed the original stated production target.

Renergen announced the successful placement of shares with investors in Australia, New Zealand and South Africa. A total of R107.6 million was raised at a price of R24.64 per share. This is a 10% discount to the 30-day volume weighted average price (VWAP). The share price has dropped by over 20% in the past 90 days as the market has become jittery about delays to helium production.

Trematon Capital Investments holds a diversified portfolio of property and education assets. For the year ended August, revenue increased by 22% and operating profit increased by 25%. The group has swung from a loss-making position to a profit of R34.5 million. HEPS has increased from 2.1 cents to 8.7 cents, a 314% increase. A capital distribution per share of 40 cents per share has been declared.

Indluplace released a trading statement for the year ended September 2022. With a final dividend of around 18.8 cents per share, the full-year dividend of 31.86 cents per share is 13.6% higher than last year.

Primeserv Group released a trading statement for the six months ended September. HEPS is expected to increase by between 46% and 50%.

Huge Group released a trading statement for the six months ended August. HEPS will be between 12.6% and 31.4% higher than the comparable year and NAV per share is between 19.6% and 39.2% higher.

With Cobus Loubser moving from the CFO role to that of CEO, Curro has announced that Burtie September is the new CFO. He has been with the group since 2016, so this is a solid example of internal succession planning.

Safari Investments has posted its response circular to the general offer by Heriot Properties. Safari’s independent board is unanimous in its view that the offer price is unfair but reasonable, which means it is below the fair value of the company but higher than the market price before the offer, particularly in light of the liquidity in the stock and how difficult it is to sell large positions. You can find the circular here. Heriot and its related parties now own 37.49% in Safari.

Afrocentric expects the circular for the partial offer by Sanlam to be posted on 8 December.

Buka Investments expects its headline loss per share for the six months ended August to be between 6.0 and 7.4 cents.

Return on invested capital has shot up and there’s a special dividend

In this snippet, I’ll deal with Barloworld’s results for the year ended September. The news about the unbundling of Zeda (the car rental business) is dealt with further on.

With revenue from continuing operations increasing by 15.4%, Barloworld is doing very nicely. Interestingly, EBITDA margin from continuing operations fell from 12.8% to 12.2%. Inflationary pressures are evident here, with all three of the major segments reporting a decrease in margin. The revenue growth was enough to keep EBITDA moving in the right direction overall, growing by 9.2%.

I’ve often commented on Barloworld’s ability to allocate capital and this period is no exception, with return on invested capital of 16.9% compared to 11.3% in the prior year.

The reward for shareholders is a final dividend of 295 cents per share and a special dividend of 550 cents per share. This is a total dividend of R8.45 on a share price of nearly R108. When net debt drops from R7.6 billion to R4.6 billion, juicy dividends become possible.

Going forward, the group anticipates a tricky operating environment because of inflation. Equipment Southern Africa will benefit from infrastructure and mining investment. Equipment Eurasia is in a tough space for obvious geopolitical reasons, with Barloworld trying to do the best it can for its employees. At Ingrain, local maize prices are expected to remain elevated due to ongoing disruptions to international prices from the conflict in Ukraine.

The Barloworld share price chart shows the substantial drop when war broke out in Ukraine, reflecting market concerns about the Equipment Eurasia business:

Hello, Zeda

Barloworld is finally unbundling car rental businesses Avis and Budget

So, you may be wondering about the Zeda name and how it relates to Avis and Budget. Personally, I think someone just has a sick sense of humour and wanted to create a market that has Zeder and Zeda listed on it to cause maximum confusion. I can’t see any other link!

Nomenclature aside, Barloworld will be unbundling 100% of its car rental group to shareholders. I have great respect for Barloworld’s ability to manage a balance sheet, so I’m a little worried about an announcement that says the unbundling will “unshackle” Zeda “by the umbrella of Barloworld’s capital allocation framework” – a lot of corporate gumpf that make very little sense. Unshackled from perhaps? That’s not good either.

With the name and the confusing wording aside, the part I do understand is the rationale for Barloworld shareholders. This is a non-core asset that doesn’t fit in with the strategy of the rest of the group. Barloworld has taken major steps towards having a more focused group, with the major pillars being Industrial Equipment & Services (the “diggers” that get Toddler Ghost excited) and Consumer Industries, the pillar that was formed through the acquisition of Tongaat Hulett Starch (subsequently renamed Ingrain).

The Avis and Budget businesses collectively offer car rental and fleet solutions. The pandemic caused havoc for the industry but the businesses were able to reduce their fleets and survive the pain. When utilisation rates are high, car rental businesses can actually do rather well.

For the full details, we have to wait for the pre-listing statement that is due to be released on the 28th of November. An unbundling process moves quickly and Barloworld shareholders can expect to see Zeda shares in their portfolios before Christmas.

Ethos Private Equity to merge with The Rohatyn Group

A specialised global asset management firm is acquiring Ethos Private Equity

Established around 20 years ago, The Rohatyn Group now has $6 billion in assets under management (AUM) and 120 employees in 16 cities across the globe. Growing at this pace organically is almost impossible, so I’m not surprised to read that growth has also been achieved through acquiring other general partners (private equity management firms).

Ethos has been around since 1984 and has made over 150 investments in Africa. The combined firms can offer their respective limited partners (private equity investors) a vast array of investment solutions. The enlarged business will have almost $8 billion in AUM.

Importantly, all key members of management will remain in their roles and current incentives will remain unchanged.

Well, not a lot. The listed company needs to give its consent for the cession of the advisory agreement to The Rohatyn Group. This also applies to Brait, as that company is also advised by Ethos and thus needs to consent to the agreement moving to The Rohatyn Group.

This is the critical point to understand: this transaction is for the management company of the funds and not for the funds themselves or the underlying assets.

Naspers’ HEPS swings into the red

But it’s tricky to know which numbers to focus on

As regular readers will know, I tend to ignore Earnings Per Share (EPS) in favour of Headline Earnings Per Share (HEPS). When it comes to Naspers and Prosus, I’m not sure that’s the right approach. The strategy of the group is to make investments in a wide range of technology firms, so ignoring changes in value of the investments perhaps isn’t the best way to do things.

The board would like you to focus on core HEPS, which adjusts for “non-operational” items.

Whichever way you cut it, earnings for the six months to September 2022 are well down. There is some complexity from the Avito business in Russia, which has been classified as a discontinued operation. If we go with management’s view of core HEPS from continuing operations, then the decrease is between 59.7% and 52.3%. HEPS is in the red, between 100.6% and 107.9% lower. Just to close the loop, EPS is between 81.3% and 88.3% lower.

EPS was impacted by a $12.3 billion gain on the sale of a 2% interest in Tencent in the prior year vs. a gain of just $2.8 billion in this period, so that’s a huge year-on-year swing. Impairment charges etc. on investments in associates are $1.8 billion higher in the current period.

Looking at HEPS, lower profitability across the investments has hurt the numbers. Further pressure has come from earlier stage investments in certain companies.

Full results are expected on 23 November.

Netcare is a case study in operating leverage

A small change in revenue makes a big difference in this industry

The hospital industry is famous for high levels of operating leverage. Simply, this means that a high proportion of fixed costs in the business (the hospitals are there whether full or empty) creates an “airline economics” scenario where profitability can swing wildly based on capacity utilisation.

In a market that has largely normalised post-Covid, Netcare’s revenue is up just 2.1%. But here comes the operating leverage: EBITDA is up by 7.4%, operating profit is up 9.9% and net profit is 38.2% higher! The huge jump between operating profit and net profit is because of a concept called financial leverage, which is the effect of having debt in the capital structure. The interest expense doesn’t increase proportionally with revenue.

Speaking of debt, net debt has decreased by 8.6% and net debt to EBITDA is a palatable 1.4x.

I must point out that hospital groups are known for having sub-par returns on capital. For whatever reason, it’s really hard to generate economic profits in this industry (returns above the cost of capital). Case in point: return on invested capital has increased from 7.9% to 8.8%. That’s not exciting.

Adjusted HEPS increased by 23.4% and the dividend per share increased by 47.1% as the group felt more confident to increase the payout ratio.

In FY23, the group anticipates revenue growth of between 9% and 12%. If that materialises, it would drive further margin expansion and improved returns.

Sirius Real Estate grew strongly in the six months to September

Funds From Operations (FFO) increased by 47%

The sharp growth in earnings at Sirius wasn’t matched by an increase in the net asset value (NAV), with only a 1.8% and 2.1% like-for-like valuation increase in Germany and the UK respectively.

These increases make sense in the context of a 2.4% increase in the like-for-like annualised rent roll in Germany and 4.1% in the UK.

At group level, NAV per share increased by 1.8% to 103.9 cents. This is measured in euros, so the rand NAV per share at current exchange rates is R18.28. At a closing price of R17.20, Sirius is trading below the NAV per share (as I predicted would eventually happen despite people getting upset with me about it).

To give some support to the valuation being close to NAV per share, two assets were sold during the period at a 9.4% premium to book value.

Looking at the balance sheet, the weighted average cost of debt fell from 1.4% to 1.3% and the loan-to-value decreased marginally from 41.6% to 41.0%.

Funds From Operations increased by 47% overall and 32.2% on a per share basis, which is similar to the 32.4% increase in the interim dividend per share to 2.70 euro cents.

Sun International shines on Grand Parade

The latest deal takes the stake to 21.1% – a significant minority interest

Sun International has been moving in on Grand Parade and has now picked up a decent chunk of stock from VCP Capital Partners. A 7.8% stake has been acquired for R3.50 per share, with a total deal value of over R128 million. This is almost a rounding error for Sun International.

There are many interesting relationships at play here.

For example, Sun International and Grand Parade are both shareholders in SunSlots, SunWest International and Worcester Casino. It’s also important to note that VCP holds 20.9% in Sun International, so this deal becomes a small related party transaction as Sun International is effectively transacting with a significant minority shareholder.

For the deal to go ahead, an independent expert needs to opine that the terms are fair to the shareholders of Sun International. BDO Corporate Finance has been engaged to provide this opinion. The announcement is inconsistent – it initially says that the opinion has been provided to the JSE and then says that it hasn’t been finalised yet.

This stake in Grand Parade has been built quickly. Prior to this announcement, Sun International held a 13.3% interest in Grand Parade of which the acquisition of 10.6% was announced last week.

Tsogo Sun Gaming: casinos cash in

There’s a big jump in earnings

Although we have to wait for detailed earnings to be released on 24 November, a trading statement from Tsogo Sun Gaming has given us a strong clue that earnings are bouncing back.

For the six months ended September, HEPS is expected to increase by between 78% and 94% to between 55 and 60 cents per share. This is despite a hotel management contract cancellation expense of R289 million.

I decided to dig into the archives and I discovered that adjusted HEPS for the six months ended September 2019 was 65.3 cents. This means that the company has still not recovered to pre-Covid levels.

Little Bites:

Director dealings:

The CEO of Motus has sold shares in the company worth R4.05 million

Not sure this one is worth a mention but I’ll do it anyway: the CEO of Altron had a quieter day of buying shares, only mopping up R5.4k this time around

In a trading and pre-close update, Fortress REIT (a name that might not be the case forever) confirmed October vacancies in the SA direct logistics portfolio of just 0.1% and vacancies in the Central and Eastern Europe logistics portfolio of 5.5%, down from 8.3% at the end of June. Sadly this only tells part of the story. Office vacancies of 24.6% aren’t doing the group any favours (although this is less than 4% of assets by value) and retail vacancies are steady at 3.6%. The total portfolio vacancy has at least improved from 5.4% at the end of June to 3.9% at the end of October. There is a substantial effort underway to sell non-core assets, with nearly R434 million in net proceeds since the end of June. A further R1.4 billion worth of properties are currently held for sale. Distributable earnings from NEPI Rockcastle are ahead of expectations and the South African portfolio is dealing with higher interest rates than Fortress expected. A shareholder meeting has been demanded by a group of shareholders with a proposal to save REIT status, with the meeting scheduled for January.

PPC has released group results for the six months to September. Although revenue increased by 9% if we exclude Zimbabwe, HEPS fell from 10 cents to 4 cents on that basis. The culprit is higher energy costs and increased competition in the core South African market. Zimbabwe is currently dealing with hyperinflation and contribution to group revenue reduced significantly. The good news is that $4.4 million was paid to the group from Zimbabwe. Further good news is that finance costs fell by 43% thanks to ongoing de-gearing of the group. The shining star was the business in Rwanda, where EBITDA increased by 63% and EBITDA margin improved from 28.4% to 32.3%. When group HEPS falls from 55 cents to a loss of 5 cents, one needs to try find reasons to smile.

Poultry group Astral Foods reported results for the year ended September. Revenue was up 22% and HEPS jumped by 125%. This is typical of poultry businesses that have notoriously volatile net earnings because of the low margin nature of the business model. The total dividend for the period is 97% higher. The outlook is less exciting I’m afraid, with pressure on consumer spending and record high raw material costs that are expected to be repeated in 2023. Load shedding is another major issue, with production cutbacks implemented and significant capital expenditure in diesel generator capacity. The share price is flat this year, having given up all of its recent gains based on the sobering outlook released to the market in recent weeks.

Old Mutual announced that the Bula Tsela B-BBEE scheme was a “resounding success” with an oversubscribed retail offer. I think that the scheme has a decent chance of success because of Old Mutual’s dividend yield, so this is good to see.

York Timber has announced the appointment of Schalk Barnard as CFO. As he was the audit partner on the York audit as an employee of PwC, he has resigned from the firm to take up this role and PwC has had to resign as auditor with immediate effect to avoid a conflict. You don’t see this very often at all!

Brikor has released a trading statement for the six months ended August 2022. It isn’t happy news I’m afraid, with HEPS expected to be between 55% and 145% lower, which means there’s a good chance the company is now loss-making. I would love to include the website link but it appears to be very broken.

Andre Botha (Senior Dealer at TreasuryONE) and George Glynos (Head of Research at ETM Analytics) discuss the probability of a recession in 2023.

Inflation has become a global problem, and in an effort to combat it, we have seen Central Banks hiking interest rates. The question becomes, what is the cost of the hiking cycle? From what we can establish, the Central Banks are hiking into a low-growth scenario which has greatly increased the chances of a recession.

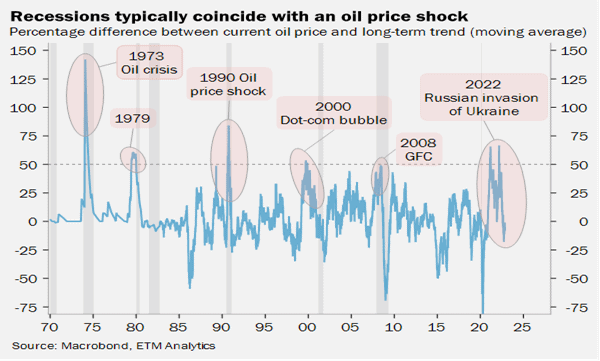

Below are some prominent charts that emphasise the point.

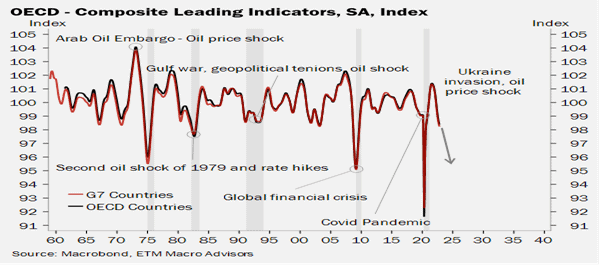

To start with, over the past 50 years, no oil price shock has occurred without a recession in oil-exposed developed economies.

Global leading indicators are turning lower, raising the recession flag. Five times out of eight that the leading indicator has fallen to this levels, worldwide recessions have followed. As central banks continue to raise rates, quantitative tightening has only begun, the full consequences of monetary tightening have not yet materialized, and inflation remains high and detracts from disposable incomes, we anticipate a further decline in the leading indicator.

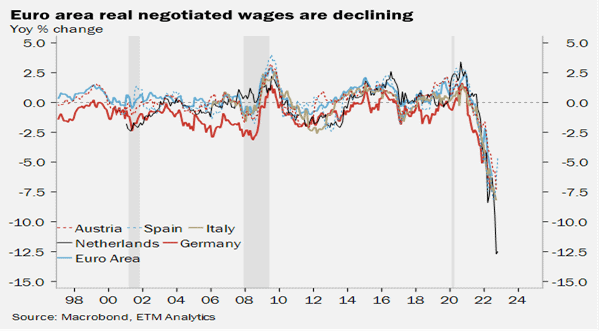

The cost-of-living crisis, especially in the Eurozone, has become extreme. There is no escaping the slowdown that is coming. You can either hike rates to curtail inflation – which will slow growth – or inflation will do it for you. As a result of Europe’s reluctance to raise rates, inflation has become a greater concern. As a result, household disposable income is plummeting, which will have a significant negative impact on consumer spending.

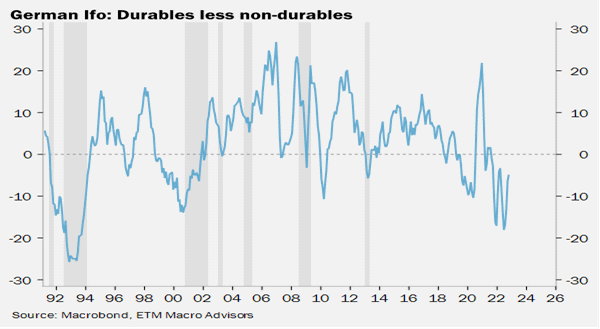

Europe’s biggest economy is under considerable pressure and the demand for durable goods relative to non-durables is well below zero, signaling a constraint on expenditure and consumption on bigger ticket items. Historically, such levels have indicated a recession.

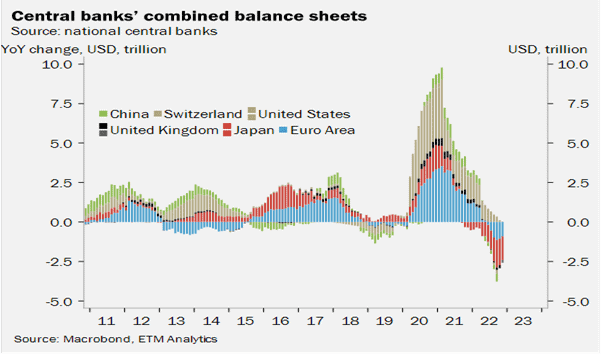

Liquidity is actively being drained from the global economy at a rate not seen since the data started getting captured in 2007. This will have a huge impact on consumption, bank lending, economic growth, and the financial markets.

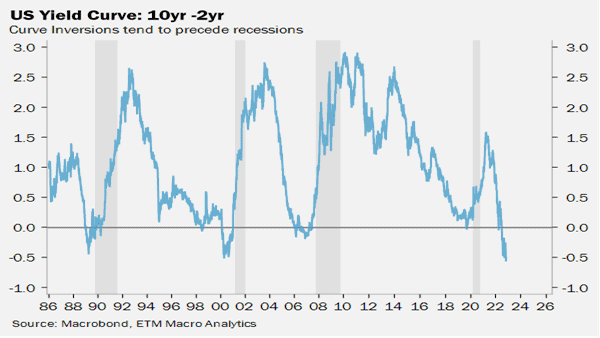

The US yield curve is the most inverted it has been since the 1980s, making it one of the greatest historical indicators of a recession. The Fed believes it can engineer a soft landing. The question to ask is whether the Fed will get it right. The smart money is that they won’t because the global coordination of hikes and inflation makes this time different.

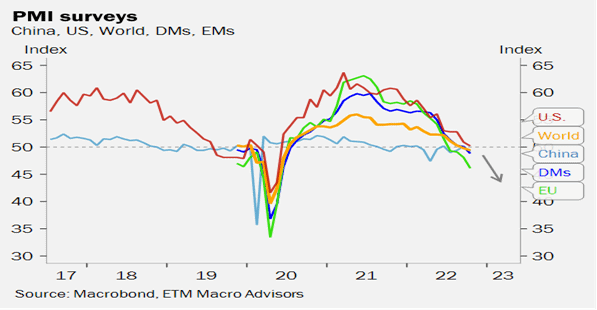

Global PMI readings have all fallen and are looking to dip into contraction territory. Over the weekend, the IMF warned that this would further detract from global GDP growth and that their expectation for global growth in 2023 could be revised down from the 2.7% they had predicted in their previous forecast.

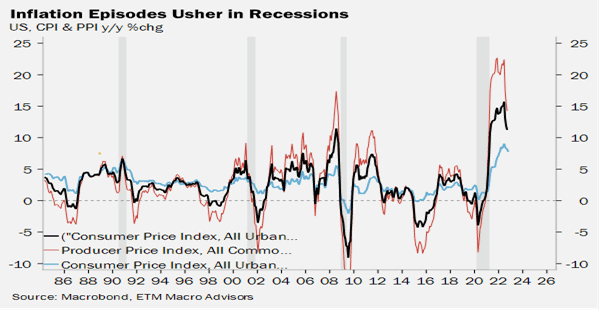

Inflation episodes tend to usher in recessions and this has been the most extreme bout of inflation in many decades.

From the above, we believe that there is a very strong case to be made that a recession is in most likelihood on our doorstep and could be the story of 2023. The warning signs are flickering and there is enough evidence there that a significant slowdown is approaching.

For more information on how TreasuryONE can help you manage market risk alongside other services, visit the website.

The fiscal strategies employed during the pandemic are coming back to haunt some of the world’s most powerful economies. As Chris Gilmour explores, the UK is in for a tough time.

When the Sars-CoV-2 virus struck the western world outside of China about 2.5 years ago, most countries reacted by taking on massive amounts of new debt and applying stimulus measures in order to prevent their economies from stalling.

At the time, I cautioned that these measures would have to be paid for in one way or another once the pandemic had ended and whether that was via massive tax increases or other austerity measures didn’t really make much difference. With the arrival of the Omicron variant of the virus last November, the pandemic has all but disappeared in most western countries, even though it is still alive and kicking in China. Most restrictions have now been lifted, particularly those relating to international travel and life is largely getting back to normal in most countries.

Economic payback

But this is where it gets “interesting”…

The UK had its first real taste of coronavirus payback time last week, when the new chancellor of the exchequer, Jeremy Hunt, unveiled his autumn statement, which is akin to South Africa’s medium-term budget policy statement. In many ways, this can be seen as a worst-case scenario template for many other countries that will probably have to indulge in similar, though perhaps not quite as extreme measures in the not too distant future.

In part, Hunt’s mini-budget was designed to provide clarity on government spending in the wake of the disastrous measures announced by his predecessor, Kwasi Kwarteng, in late September. Kwarteng had attempted, in true libertarian fashion, to spend his way out of the problem with unfunded tax cuts. To add insult to injury, Kwarteng completely ignored the Office for Budget Responsibility (OBR) which was designed in 2010 to help prevent treasury officials doing their own thing regardless of the financial outcome.

In this case, the international bond markets brought Kwarteng’s excesses to heel by trashing the value of UK pensions and in so doing, dropping the external value of sterling to near-parity with the US dollar.

Jeremy Hunt is no rocket scientist; unlike Kwarteng, he doesn’t hold a PhD in economics, but he is regarded as being a safe pair of hands. Last week he had the unenviable task of applying austerity measures to an already crippled economy in the hope that some kind of light will emerge before the next general election in late 2024. And at least this time he has the buy-in of the OBR, which assisted greatly with forecasts.

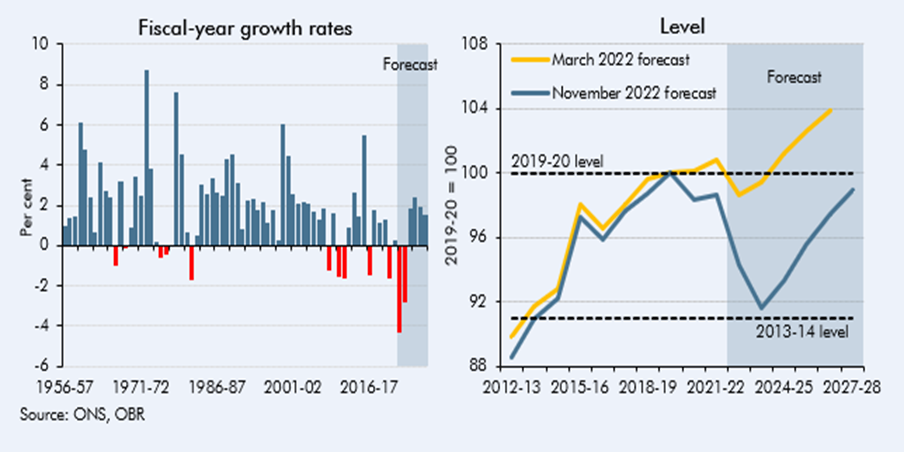

Unfortunately, it makes for dismal reading, as the next few charts from the OBR illustrate.

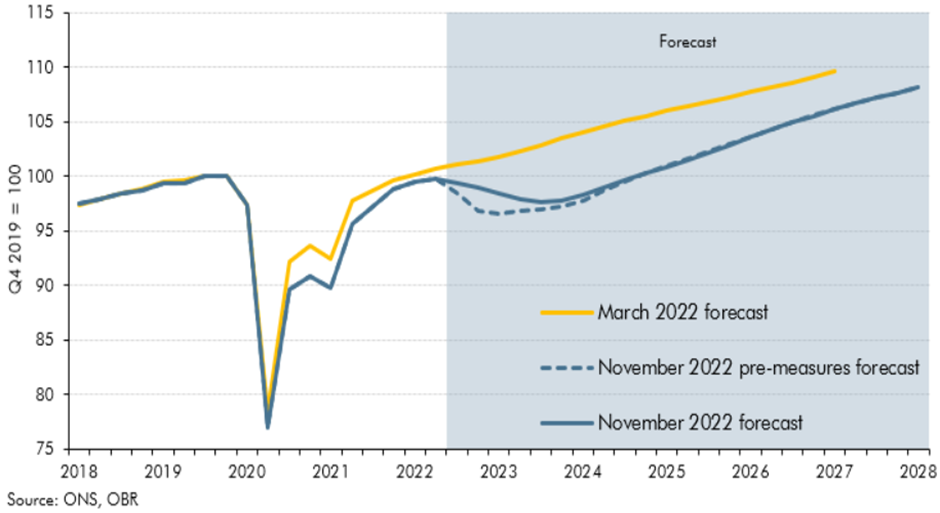

It’s going to be ugly

Alone among the major European economies, Britain’s GDP is still trailing its pre-pandemic levels and it looks like it won’t exceed them until 2025 at the earliest. On a per capita basis, the outlook is even more sobering:

Real household disposable income per person

But that’s not all. The Bank of England’s pessimistic GDP outlook of a few months ago, even before the Truss/Kwarteng circus got into full swing, suggested a 5-quarter recession, lasting until well into 2023.

The OBR now forecasts something that is perhaps slightly shallower than that but nevertheless still prolonged:

Real GDP

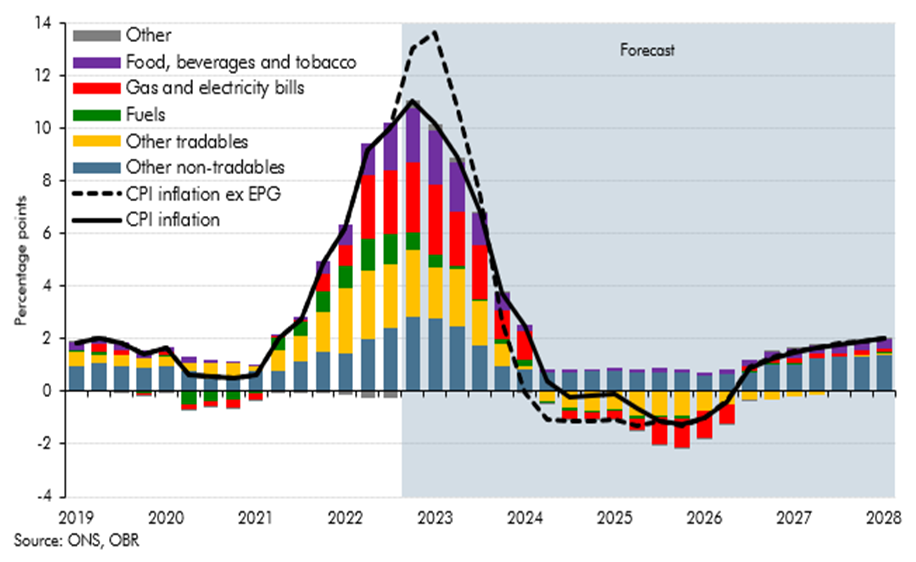

The only metric that looks even remotely optimistic is the one that relates to the root causes of inflation in the UK. Inflation is seen peaking in 2023, coming off sharply in 2024 and actually going negative in 2025/26: