Tradehold has declared a special dividend of R4.34 per share. The funds are part of the cash consideration of £102,5 million received from the sale of its shareholding in Moorgarth earlier this year.

Labat Africa has advised it has issued a further 22,606,003 new shares for cash. The shares were issued under the company’s General Authority approved by shareholders in May. The company has issued 39,281,862 new shares under this authority representing a cumulative 23.13% of Labat’s issued share capital.

Super Group has proposed an odd-lot offer to shareholders holding a total of 49,014 Super Group shares, representing 0.014143% of the total issued share capital of the company. The offer will be priced at a 10% premium to the 10-day VWAP of the ordinary share at the close of business on Friday, 2 December 2022.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Glencore this week repurchased 19,080,000 shares for a total consideration of £96,93 million. The share repurchases form part of the second phase of the Company’s existing buy-back programme which is expected to be completed over the period from August 4, 2022, to February 14, 2023.

South32 has this week repurchased a further 2,470,909 shares at an aggregate cost of A$9,19 million.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period October 24-28, a further 5,601,358 Prosus shares were repurchased for an aggregate €237,02 million and a further 1,019,972 Naspers shares for a total consideration of R1,84 billion.

British American Tobacco repurchased a further 1,100,544 shares this week for a total of £37,01 million. Following the purchase of these shares, the company holds 215,471,108 of its shares in Treasury.

Only one company issued a profit warning this week: AH-Vest.

Five companies issued or withdrew cautionary notices. The companies were: Trustco, Afristrat Investment, Grand Parade Investments, Finbond Group and Luxe.

Yet another quiet week on SA’s exchanges – one would be forgiven for thinking the migration of Corporate SA to the coast was already underway:

RMB Corvest, Rand Merchant Bank’s (RMB Holdings) private equity arm, has invested an undisclosed sum in Sedgeley Energy, a solar photovoltaic solutions provider based in Namibia. The deal provides Sedgeley Energy with liquidity required to support its long-term growth plans.

Shoprite has invested an undisclosed sum in local SA tech startup Omnisient. The investment was made in an undisclosed expansion round with participation from Buffet Investments, KLT, One5 and ENL. Omnisient enables businesses to use consumption data to create new revenue streams.

The sale by Tradehold of its rental enterprise to Dulu Holdings, announced to shareholders in September this year, has been terminated following the non-fulfilment of various conditions precedent.

Unlisted Companies

Sika South Africa, a manufacturer and distributor of a range of construction chemicals, has acquired a majority stake in Italian manufacturer Index Construction Systems and Products. The deal expands Sika’s bitumen product range and boosts its position not only in Italy but also in Europe.

The Industrial Development Corporation has increased its shareholding in Mozal Aluminium from 24% to a 32.45% equity stake.

In a tech-themed Ghost Global this week, we bring you fresh updates on Amazon, Meta and Alphabet.

No need to book a game drive – all you have to do is watch the markets to see three of the Big Five American information technology companies making moves this week. Alphabet, Amazon and Meta all announced earnings, and each had something different to say about the future of the never-dull tech industry.

For research on global stocks that will help you trade and invest with confidence, subscribe to Magic Markets Premium for R990/year or R99/month.

Alphabet sticks to a slow and steady strategy

Google’s parent company, Alphabet Inc., released its financial results for the third quarter ended September on Thursday. They reveal that total revenue rose by only 6% year-over-year to $69 billion, which is a little meh compared with the 41% increase in the third quarter of 2021. Still, growth is growth, however aggravatingly slow.

Your favourite ghost is rather bearish on Alphabet, as the way people are searching is changing. With an ever-increasing number of platforms and apps that can do everything, the need to “Google” it could diminish over time. On the plus side, absolutely nobody chooses to “Bing” it unless they open Microsoft Edge because they weren’t concentrating properly.

Within Search, Google is the ultimate. The question mark is over Search as a business over the next decade. This quarter makes that view look a little silly though, with Search advertising revenue significantly higher year-on-year. The same can’t be said for YouTube Ads, with even the best social media and content platforms coming under pressure as people get tired of yet another Monday.com ad.

This makes the Search result even more impressive in the global context. Still, the longer-term worries remain.

A deeper dive into Alphabet’s financials for Q3 reveal that its Cloud segment is the fastest-growing business by revenue, yet losses just keep mounting. With its revenue up by 37,6% year-on-year to $6.9 billion, it just goes to show that there’s a bright side to every pandemic (in this case, the fact that millions of companies were practically forced to adopt cloud tech overnight). The problem is that providing this service is costly and Google Cloud is still sub-scale, so losses increased from $644 million to $699 million.

With such little growth, operating margin fell from 32% to 25%. Ouch.

In an attempt at growth beyond its core business, Alphabet welcomed a new family member to the table with the acquisition of cyber-security company Mandiant for a total purchase price of $6.1 billion. This move sees the tech pioneer adding over 2 600 employees to its workforce. Clearly someone’s feeling optimistic about the future, global recession be damned.

Amazon struggles to see the forest for the trees

Diehard Tolkien fans aren’t the only ones upset by Amazon’s new Rings of Power series – the shareholders who helped pay for it are grumbling too. It turns out big budgets (in this case, a whopping $500 million) don’t impress fans as much as the little things, like actually reading the books and sticking to well-established lore. From a shareholder perspective, it must be more than a little annoying to see such large amounts of money squandered on a sub-par spinoff that no-one asked for in the first place.

To add insult to injury, Amazon’s free cash flow decreased significantly, from an inflow of $2.6 billion for the trailing 12 months ended September 2021 to an outflow of $19.7 billion for the trailing 12 months ended September 2022. This is a cause for concern in an inflationary environment, as money is no longer “free” and the market is placing far more scrutiny on return on investment. Although Amazon is profitable (in this quarter at least), the company is investing more than its cash profits in infrastructure (and possibly the desecration of the works of more genre-defining authors).

Following this downward trend, net income decreased to $2.9 billion for Q3, compared to $3.2 billion in Q3 2021. Net income is being impacted by substantial swings in the value of the investment in Rivian, causing wild quarter-on-quarter moves as the volatile market treats Amazon’s income statement with even less respect than Tolkien’s story received. In the third quarter, the Rivian investment was responsible for a $1.1 billion valuation gain.

For the nine months ended September 2022, the group is sitting on a loss of $3 billion. With Halloween in the bag and the rest of the holiday season looming, Amazon may be banking on a Christmas miracle to turn a slow start to the year around and enable it to report a profit when the annual financials come out.

The truth of it is that the Rivian share price will play a substantial role in where net profit for the year ends up. This is what happens when listed companies make risky bets.

The other major driver of reported earnings is the strength of the dollar. To show how severe the impact is, net sales in Q3 were up 15% as reported and 19% on a constant currency basis. US tech giants are all being hurt by the currency.

Meta-morphosis: Zuckerberg says “Don’t worry, I have a plan.”

For those who want a detailed report on Meta’s latest earnings and what it means for the investment thesis, The Finance Ghost and Mohammed Nalla covered the stock in Magic Markets Premium this week.

Moving on to a summarised view of the third-quarter results, we have to dig deep to find anything to like about these numbers.

It’s certainly impressive that Facebook’s daily users rose by 3% (you read that right – more people are joining or at least using Facebook) to reach a total of 1.98 billion worldwide. Speaking of impressions: ad impressions across the company’s Family of Apps, which includes Facebook, Messenger, Instagram and WhatsApp, increased by 17%, while the average price per ad decreased by 18%. This represents a significant increase in demand for advertising on the platform, which is likely due to the continued growth of the user base. In addition to heightened price sensitivity among advertisers, the decrease in price per ad also confirms that Reels is proving to be dilutive to revenue.

In fact, Meta reckons it will take over 18 months for Reels to be accretive to revenue. Switching people away from Feed and Stories into short-form videos is necessary to fight TikTok, but it is hurting the business.

Revenue fell by 4% to $27.7 billion in the most recent quarter, but the company claims that this figure would have been $1.8 billion higher if foreign exchange rates had remained constant. We’ll take their word for it, noting that revenue is 2% higher on a constant currency basis.

Most investors have lost faith (and money) in the company formerly known as Facebook – or perhaps they’ve lost faith in its leader and his hell-bent metaverse crusade. At a time when the core business is under macroeconomic pressure and facing considerable internal change (the impact of Reels), Zuck is going full throttle on his investment in the Metaverse and capex in general.

At some point, you have to wonder if poor Mark is in on the joke or if we should tell him that very few investors really care about the metaverse. Either way, investors are running out of patience and terrified of the free cash flow trajectory, sending the share price down 25% (again) after this earnings release.

The share price has lost over 72% of its value this year. There’s nothing to like about that.

For research on global stocks that will help you trade and invest with confidence, subscribe to Magic Markets Premium for R990/year or R99/month.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Dis-Chem is still growing into its share price

Earnings are much higher, yet the share price is flat over the past year

The trouble when something is priced for perfection is that the share price tends to go sideways in good times and downwards in bad times. No matter how good the underlying company is, an overpriced share turns it into a mediocre investment.

In the six months to August, Dis-Chem group revenue increased by 9.3%. Retail revenue grew by the same percentage, with comparable store growth of 3.6%. This modest rate was significantly impacted by Covid vaccines in the base period. The rest of the growth came from new pharmacies and the acquisition of 15 Baby Boom stores, extending Dis-Chem’s baby retail leadership position.

Wholesale revenue was up 10.6%. As much of this revenue is earned from Dis-Chem’s own stores, the more important growth measures are sales to independent pharmacies (15.8%) and TLC franchises (22.5%).

With a total income margin of 31.7%, the group has exceeded the 30% total income margin threshold eighteen months sooner than anticipated. Retail total income margin has increased to 30.2% and wholesale has increased to 8.3% if you exclude a once-off gain.

Excluding the Medicare and Baby Boom acquisitions, expenses grew by 15.5% overall and 14% in the retail business. Higher fuel prices led to increased delivery costs vs. the prior comparable period.

Net financing costs decreased by 8.3% from the prior comparable period, partially thanks to R125 million in capital repayments on the Absa loan. A new term loan facility from Standard Bank of R455 million was used to acquire warehouse properties.

Working capital initiatives reduced inventory days and increase creditor days, both of which help unlock cash in the business.

Capital expenditure was R690 million of which R576 million was to maintain the existing infrastructure and purchase warehouse properties, with R114 million used for new stores and IT enhancements.

An interim dividend of 28.11861 cents per share was declared, up 44.3% year-on-year and representing a consistent payout ratio as headline earnings per share (HEPS) grew by the same percentage.

The share price closed at R33.06, down just over 2% for the day.

Two more of MTN’s African subsidiaries have reported numbers

MTN Rwanda and MTN Uganda have added their voices to the MTN story this week (well, sort of)

After strong results from key subsidiaries MTN Nigeria and MTN Ghana, we now hear from two of the smaller businesses in the group.

Well, in theory at least. I wish I could give you an update on MTN Rwanda but sadly the quarterly reports page gives a lovely, yellow-themed 404 error message

Thankfully, the team at MTN Uganda appears to know how websites work. A cursory glance shows that although MTN Uganda is growing, we aren’t seeing the EBITDA margin expansion that is evident in the larger African subsidiaries.

In the nine months year-to-date, mobile subscribers increased by 9.2%, active data subscribers grew 28.8% and active fintech users increased by 19.4%. It therefore won’t surprise you that service revenue (still by far the largest component) was only up 11.5%, compared to 29.8% growth in data revenue and 23.2% growth in fintech revenue.

Something that may surprise you is that fintech revenue is larger than data revenue. This tells you so much about the role that smartphones play in Africa. They are effectively banks in the pockets of the people.

With EBITDA only 9.5% higher, EBITDA margin contracted by 100 basis points to 50.7%. That’s not good directionally of course, but is still a very high margin.

With capital expenditure up by 20% as the investment in Uganda continues, free cash flow was only 5.1% higher.

Pepkor guides solid HEPS growth

With results due on 22 November, the market has been given an early look

Pepkor announced in a trading statement that HEPS for the year ended September 2022 is expected to be between 18.6% and 28.6% higher.

This implies a range of between 160.5 cents and 174.1 cents, which puts the company on a Price/Earnings multiple of between 14.5x and 13.3x.

There is some noise in these numbers, like the recovery of exposure to certain loans going back to the Steinhoff debacle. This contributed around 12 cents per share to HEPS, which is significant.

Although Pepkor received insurance proceeds for damage to fixtures and fittings during the riots, this doesn’t impact HEPS as capital items are excluded. It does impact earnings per share (EPS), as the damage was in the base period and the recovery was in this period, driving a swing in earnings that isn’t reflective of the underlying business performance.

The group also announced the appointment of Sean Cardinaal as COO, having served as managing director of Ackermans from 2011 to 2016 before taking on the COO role for Pepco Group in Europe (a subsidiary of Steinhoff).

Little Bites:

Director dealings:

The CFO of ADvTECH exercised share options and immediately sold the shares for R740k

Des de Beer has acquired a further R892k in shares in Lighthouse Properties, adding to his long list of recent purchases in the company

Impala Platinum reminded the market that the Competition Tribunal process re: the offer to Royal Bafokeng Platinum shareholders is still underway. The company believes that the longstop date (by which time the approval must be obtained for the deal to continue) of 22 November is still achievable. Implats reserves the right to extend that date and it wouldn’t be the first extension in this process.

ISA Holdings released a further trading statement that reflects expected growth in HEPS of between 30% and 50% for the six months ended August.

Tradehold’s disposal of rental properties to Dulu Holdings did not meet the conditions precedent in time and hence the disposal has been terminated.

The CFO of Etion Limited has resigned from the company and will serve a notice period until the end of January. With this group in the process of being unwound in a value unlock strategy, no mention is made in the announcement of a successor.

If you are interested in climate reporting, you’ll be interested to see that Anglo American Platinum has released its first ever climate change report. You’ll find it here>>>

Accenture, Ferrari and Sysco. These are the stocks that Garth Mackenzie chose to discuss with me based on our recent research in Magic Markets Premium.

Garth is a keen Magic Markets Premium subscriber. In fact, he’s even called it a “no-brainer” to subscribe on several occasions. Having listened to all the podcasts and read all the reports in the Premium library, there were three stocks that really caught his eye.

In yet another appearance on his terrific podcast series Talking with Traders, Garth asked me to run through the investment thesis for Accenture, Ferrari and Sysco.

This is a great show that gives you just a small taste of what you would find inside Magic Markets Premium for just R99/month or R990/year.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Capital & Counties brings news from the West End

Even in a trendy London area, valuations are down over the past three months

The latest trading update by Capital & Counties covers the period from 30 June to 31 October (though the valuation date for the properties was 30 September).

The macroeconomic environment in the UK has hurt valuations, with a 2% decline from June to September. This is being driven by valuation yields rather than underlying rental income, as Covent Garden is experiencing rental growth. For pre-Covid context, the valuation is 25% below 31 December 2019 levels.

There is no shortage of leasing demand, with 35 new leases and renewals signed since June.

As a reminder, Capital & Counties is in the process of a merger with Shaftesbury Capital to bring two West End property portfolios into one group. In the meantime, the company has a strong balance sheet (loan to value ratio of 21%) and is focusing on its business, as there isn’t much that it can do about the macroeconomic climate.

MTN Ghana adds to the party with a great result

Another tick in the box for the portfolio of African subsidiaries

Hot on the heels of MTN Nigeria, we have MTN Ghana with a solid quarterly result. Revenue is the highest it has been over the past five quarters, with a strong contribution across Voice, Data and MoMo (the mobile money business).

For the nine months to September, service revenue is up 27.9%, well ahead of subscriber growth (13% in mobile, 18.2% in active data and 16.3% in active MoMo).

If you liked the EBITDA margin in Nigeria, just wait until you see Ghana. The margin is 310 basis points higher at 57.5%, driving a 35.1% increase in EBITDA.

The capex requirement in Ghana is high, like in the other African subsidiaries, as MTN is investing heavily. Year-to-date capex is GHS1.4 billion vs. EBITDA of just over GHS4 billion. Unlike Meta, MTN only invests cash flow that it actually generates!

It’s not all rainbows. Inflation in Ghana was 37.2% in September 2022, so that gives context to these growth numbers. The government is tightening monetary policy and is restructuring its debt with the IMF. This is why MTN Group trades at a modest multiple despite the growth in Africa, as investors have been burnt before by African growth stories that aren’t accompanied by dividends.

For now, MTN is rolling out its networks in these countries with self-funded, in-country cash. Over the next 10 years, I’m bullish on what the company can achieve with a huge smartphone user base.

Octodec’s share price jumps 9.3% after releasing results

Income is up and the balance sheet is improving, but reversions are still negative

Octodec owns a portfolio of 246 residential, retail, office, industrial and specialised properties in Tshwane and Johannesburg. The portfolio is valued at R11 billion and the residential income is a differentiator here on the JSE, contributing 31.7% of rental income. Nearly 55% of income is derived from the CBD areas in those cities.

For the year ended August, distributable income after tax has increased from R358.4 million to R466.1 million. On a per share basis, it has come in at 175.1 cents.

The dividend per share is 130 cents, which now puts the fund on a trailing yield of 13.1% after the share price closed at R9.89.

The net asset value (NAV) per share is R23.28, so the discount to NAV is still huge at 57.5%.

The loan-to-value (LTV) ratio has improved from 43.2% to 39.7%.

Looking deeper into the portfolio, negative reversions are still being experienced in every sector except retail shopping centres. In the offices segment, renewal reversion is -3.7% and new lease reversion is -12.4%.

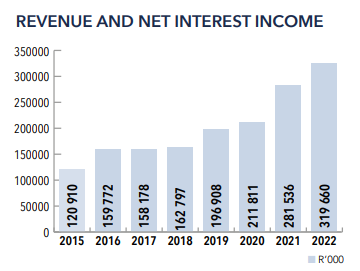

Santova reports another great set of numbers

A jump in HEPS to of 62.4% is more good news for shareholders

Santova has a reputation for being a small cap on a strong growth trajectory. The latest interim results only support that reputation, with revenue up by 13.5%, HEPS up by 62.4% and the net asset value per share increasing by 35.7%.

I decided that the revenue and net interest income chart tells the best story of how this business has benefitted from the supply chain crunch during the pandemic:

Cash generated from operations has increased by 45.5% and return on equity has increased by 720 basis points to 28.2%, so Santova is doing all the right things it seems.

As always, the focus is on the company’s outlook. Shipping rates have declined in 2022 and there is a general cooling off in consumer spending because of inflation. Even then, current shipping rates are up on 2019 pre-pandemic rates and by a huge margin ($4,000 vs. $1,300 – $1,600).

Santova notes that a subdued peak season is anticipated because larger customers are sitting with elevated stock levels, having ordered for Black Friday and Christmas earlier in the year. Smaller customers can now take advantage of decreasing shipping rates.

Finally, the acquisition of A-Link Freight in the US closed in September, shortly after the end of this reported period. Those numbers will be in the next result.

Sasol raises $750 million in convertible bonds

A drop of nearly 8% in the share price would’ve upset shareholders

To refinance debt and for general corporate purposes, Sasol offered $750 million in guaranteed senior unsecured convertible bonds due 2027. That’s a mouthful, isn’t it?

In simple terms:

Debt instruments (“bonds”) that offer protection to investors (“guaranteed senior” tells you that)

The instruments aren’t secured by a specific, valuable asset (“unsecured”)

They carry an equity kicker as they can be converted into shares at some point (“convertible”)

The debt is repayable in 2027 (I think that part is self-explanatory)

When the issuance was announced in the morning, the expected pricing was between 4% and 4.5% per annum. This is because Sasol needed to test investor demand in the market and wasn’t quite sure where the pricing would land.

Whenever you see a convertible instrument, you need to look out for the terms of that conversion. In this case, my understanding is that the conversion is at Sasol’s election (not the investor’s choice) and is convertible into shares or cash. The conversion price was indicated as being at a premium of between 30% to 35% above the volume weighted average price on 1 November. This makes more sense when you remember that the instruments are only due in 2027.

There are also certain events that would allow the holders to trigger a redemption, like a change of control or a delisting of Sasol.

As another important point, shareholders still need to approve the convertibility of the bonds. If that approval isn’t achieved, Sasol can choose to redeem all of the bonds at the greater of 102% of the principal amount or the fair market value.

When it comes to hybrid instruments like these, things get complicated.

By the end of the day, Sasol announced that the bonds were priced at 4.5% per annum and that the conversion price is a a 30% premium. In other words, the market was only interested at the most lucrative end of the range in both cases (the highest yield and lowest conversion price).

The bond issuance gave the market the jitters, with the share price closing almost 8% lower.

Textainer Group banks another good quarter

Despite volatility in shipping, Textainer has achieved steady headline earnings this year

In Textainer, we have another example of a company talking about normalising shipping rates.

Demand for new containers was muted during this quarter as shipping lines have sufficient inventories. Textainer still managed to make money from this by selling old containers.

Income from operations of $123 million was slightly higher quarter-on-quarter and 8% higher year-on-year. Average fleet utilisation was 99.4% in this quarter vs. 99.8% a year ago. Adjusted EBITDA of $192.6 million is 4.6% higher year-on-year.

The shipping game is all about capital management. With less of an opportunity to deploy capital, Textainer is focused on returning capital to shareholders through dividends and share repurchases. The year-to-date repurchases represent 8% of shares outstanding at the beginning of the year.

The balance sheet is strong and 90% of the financing is hedged for rising rates.

A dividend of $0.25 per share has been declared.

The share price is down 3.3% this year and 5% over 12 months.

Little Bites:

Director dealings:

An associate of Piet Viljoen and Jan van Niekerk (Calibre International Investment Holdings) has acquired R31.6 million worth of shares in Astoria Investments

The CEO of AVI exercised share options and immediately sold all the shares for R2.76 million

Des de Beer has bought more shares in Lighthouse Properties, this time to the value of R2.5 million

A prescribed officer of Renergen has bought shares worth R246k

Sibanye-Stillwater has entered into s189 consultations regarding the Beatrix 4 shaft and the Kloof 1 plant, both of which are part of the SA gold operations. The Beatrix shaft is lossmaking and the Kloof 1 plant is experiencing the impact of depleting mineral reserves. This is a significant step, as it could lead to retrenchment of 1,959 employees and could affect 465 contractors. Sibanye hopes to reduce these numbers through measures like natural attrition, retirements, voluntary separation and transfer to vacant positions.

Naspers and Prosus have responded to the press speculation by Asian Tech Press, specifically an article that claimed that a Chinese state-owned investment company is in talks with the group to buy all of its Tencent shares. The companies call the article “speculative and untrue” – so there we have it. In the meantime, the group is busy with a share buyback programme funded by the sale of a small number of ordinary shares in Tencent.

Argent Industrial released a trading statement for the six months ended September 2022. Headline earnings per share (HEPS) is expected to be between 11.2% and 31.2% higher than the comparable period. This implies a range of between 164.7 cents and 194.3 cents for the interim period. The share price closed at R12.99.

Michael Fleming, CFO of Clicks, will be taking early retirement. The announcement is a great reminder of the growth achieved by Clicks, as the market cap increased from R10 billion to R77 billion during his tenure. Gordon Traill has been announced as his replacement, the current chief of support services in Clicks. He has been with Clicks since 2006, when he joined as head of internal audit. This is a great succession planning story.

Alexander Forbes’ acquisition of Sanlam Life’s standalone retirement fund administration business has become unconditional. This increases the number of active members administered by Alexforbes (the official trading name these days).

There’s a mass exodus at Rebosis Property Fund, with five independent non-executive directors (including the chairman) tendering their resignations. As a reminder, the company is in business rescue. The board now has four executive directors and one non-executive director. The board and the business rescue practitioners are considering the composition of the board committees and will provide an update in due course.

Europa Metals has announced its final results for the year ended June 2022. This is an exploration company focused on advancing the Toral project in Spain towards a mining licence application. A $6m farm-in arrangement with Denarius Metals Corp was announced during the year, subject to due diligence and other conditions.

AH-Vest (owner of AllJoy foods) announced results for the year ended June 2022 that saw a 14.4% increase in revenue and a 72.4% decrease in operating profit. HEPS has collapsed by around 80% and the dividend per share has followed suit. The sharp drop in profitability is attributed to higher production and distribution costs due to e.g. fuel price increases.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Adcorp declares an interim dividend

This is the first year-on-year increase in revenue since August 2018

Adcorp’s share price has dropped by 6.5% this year, which has ironically made it a far better investment than many other companies in 2022!

Revenue from continuing operations increased by 3.2% and gross profit increased by 6.3%, so there was margin expansion at that level. The same can’t be said for operating profit, which fell by 0.3% after the group invested in people (especially in Australia).

Headline earnings per share (HEPS) from continuing operations decreased slightly from 25.7 cents to 24.6 cents. Despite the decrease, Adcorp feels confident enough to declare an interim dividend of 12.2 cents per share.

The discontinued operation is allaboutXpert in Australia, which continues to suffer “problems” in general. The loss from discontinued operations is R13.7 million.

Looking at the balance sheet, the net unrestricted cash position fell from R197.7 million to R144.8 million. This decrease was driven by working capital investment, share buybacks and a net dividend during the period.

The group has unrecognised tax losses of R798 million and recognised losses of R238 million. As profitability improves, Adcorp would be able to recognise more of the losses.

In South Africa, Adcorp expects to sustain the progress made in the first half of the year. In Australia, Adcorp expects demand for white collar staff to soften and demand for blue collar contingency staff to stay strong.

Even with solid results, Balwin hits a resistance level again

What will it take for the share price to break higher?

Balwin Properties closed 7% higher on Monday after releasing solid results. Here’s one for the share price chart enthusiasts:

As you can see, the price has been bumping its head on a strong resistance level. I certainly don’t profess to know much about technicals, but I do enjoy seeing these patterns. The results released on Monday took the closing price back to that level but not beyond it.

For the six months to August, Balwin grew revenue by 20% and HEPS by 47% to 36.63 cents. The net asset value increased by 11% to 771.39 cents per share.

With a share price of R2.75, Balwin is trading at a substantial discount to net asset value per share and a modest earnings multiple.

The market is clearly worried about something, despite gross profit margin increasing from 24% to 26% thanks to cost containment measures and better pricing on apartments. The balance sheet has also improved, with the loan-to-cost ratio reducing from 41.2% to 39.7% and a cash balance at the end of the period of R581.2 million.

With a 15-year development pipeline, there’s no shortage of opportunities for the group. There’s even a dividend of 9.9 cents per share, up from 7.4 cents in the comparable period.

Interestingly, Gauteng contributed 62% of apartment volumes in the comparable period and that has dropped to 50% in this period. The contribution by the Western Cape and KwaZulu-Natal increased, with Balwin noting the trend of semigration.

In case you’re curious, one-bedroom units contributed 45% of sales. 35% of sales were two-bedroom units and the remainder were three-bedroom apartments.

The market must be worried about prevailing macroeconomic conditions and the impact of rising interest rates. Balwin highlights these challenges but also notes the healthy pre-sales position of the group, with 1,551 apartments forward sold beyond the reporting period.

As expected, EOH needs to raise equity capital

I’ve been telling you this for a while now

Broken balance sheets either end in business rescue (like Tongaat) or substantial capital raises, like EOH. It’s really as simple as that.

With a market cap of R760 million, EOH is looking to raise R600 million in fresh equity. As dilutive capital raises go, that’s a big one. The structure is R500 million through a rights offer and R100 million through a specific issue of shares for cash to Lebashe Investment Group as the group’s B-BBEE partner.

In addition to raising all-important equity capital, EOH notes that Level 1 B-BBEE credentials will be assured until 2028 through the Lebashe transaction.

With the “correct” capital structure in place, EOH reckons that the business would have generated revenue of just under R6 billion and profit after tax of R112 million at a 2% margin.

2%. Exciting stuff. Still, that’s a far better outcome than Tongaat has managed.

MTN Nigeria reports solid free cash flow growth

I’m still happily holding MTN after reading this

Having lost a quarter of its value this year, MTN has been the victim of general risk-off sentiment in equity markets. If you do detailed work on it, you’ll perhaps agree with me that it doesn’t take heroic assumptions to see value at this level.

The latest news is a quarterly result from MTN Nigeria, which means we now have numbers for the nine months to September 2022. If we look at that period, we see mobile subscribers up by 9.7%, active data users up by 14.6% and fintech subscribers up by 68.7%. MTN’s African growth story continues to do well, with service revenue up by 20.6% and EBITDA 23% higher.

Within service revenue, the year-to-date growth was 4.4% in Voice and 49.1% in Data as the largest sources of revenue (contributing almost 90% on a combined basis). The rest of the business is growing quickly but is much smaller at this stage.

The margins are incredible in the African subsidiaries. In Nigeria, the year-to-date EBITDA margin is 53.6%, 100 basis points higher than the comparable period. Concerns about this margin “normalising” are getting harder to justify, as MTN is doing an excellent job of generating more revenue through smartphones with each passing year.

Rolling out the network requires significant investment, which is why capex is 45.2% higher at N379 billion. For reference, profit after tax over the period is N269 billion. If you’re wondering how those cash flows work, depreciation (a non-cash expense in profit before tax) is N243 million.

Free cash flow is 42.9% higher this quarter and 7.5% higher year-to-date.

Interestingly, because of the government’s initiative to register SIM cards, there was a quarter-on-quarter decline in mobile subscribers. MTN Nigeria expects this to moderate in the fourth quarter of the year.

Another blemish on the result is that active MoMo wallets have dropped 29.4%, despite growth in registered wallets. The company prioritised enhancements to the control systems and banking interface rather than growth, so growth is expected to return next quarter. The long-term growth story is positive.

Looking at the balance sheet, MTN Nigeria has a net debt to EBITDA ratio of 0.6x. This is a comfortable level of debt.

MTN’s share price only increased by 1% on the day. I’ve noticed that the share price tends to ignore the subsidiary results and then moves sharply when group results are released.

One to watch, I think.

Little Bites:

Director dealings:

An associate of the CEO of Renergen has bought shares worth R145k

Value Capital Partners (an investment firm with representation on the ADvTECH board) has bought shares in the company worth around R3.68 million

An associate of the CEO of Spear REIT has sold shares in the property fund worth R1.5 million

An associate of a director of Standard Bank has sold shares worth R2.75 million

A director of STADIO has sold shares worth nearly R3.5 million

Harry Smit (you may remember that name), the chairman of Ascendis, has bought shares worth nearly R69k

Astoria Investments released results for the quarter (and nine months) ended 30 September. The key metric is net asset value (NAV) per share, which has increased by 3% in USD and 16.7% in ZAR since the beginning of the financial year. There have been no changes in the fair values of underlying assets between June and September. No dividend has been declared as the board is focused on achieving growth in the NAV per share, which has now reached R11.5856 per share. The share price of R7.00 is a discount of nearly 40% to the listed share price.

RECM and Calibre released interim results for the six months to September 2022. The NAV per share has increased by 24% year-on-year. Almost the entire asset value of the group is attributed to its 58.8% stake in Goldrush. The alternating gaming business was more than happy to see the back of Covid, with operations showing a strong recovery. Goldrush achieved its best ever 12-month rolling EBITDA (R397.7 million) by the end of the period. The group values Goldrush on a 7x EBITDA multiple and then adjusts for net debt (a typical market approach).

MC Mining has released its activities report for the quarter ended September 2022. Coal production at Uitkomst was 5% higher year-on-year. The conclusion of a coal sales and marketing agreement facilitates the export of at least 20,000t of API4 coal from Uitkomst on a monthly basis. The access to the export market helped increase revenue per tonne from $108 to $125. Load shedding has adversely impacted production as Uitkomst only has back-up generators for underground mining operations. The other SOE letting the team down (Transnet) caused port backlogs and resulted in elevated inventory levels. The group has $2.2 million in cash and launched a $40 million rights offer that is expected to close in November. The proceeds will be used to develop the Makhado Project.

Having completed the sale of Moorgath Holdings, Tradehold has declared a special dividend of 434 cents per ordinary share. This represents 31.5% of the current market cap.

The sale by Ascendis Health of Austell Pharmaceuticals for R432 million has closed. Ascendis will use the proceeds to settle the majority of the outstanding debt.

Finbond is still in negotiations regarding a potential acquisition in Mexico. The group has renewed its cautionary announcement.

The independent expert on the Famous Brands property transaction (BDO) has opined that the terms are fair to Famous Brands shareholders. This is the key milestone in a small related party transaction.

After significant recent movement on the Grand Parade Investments shareholder register, the company has issued a further cautionary announcement regarding discussions with potential bidders for GPI or its underlying assets.

Grindrod Shipping has published the offer documentation related to the conditional cash offer by a wholly-owned subsidiary of Taylor Maritime Investments. The offer opened on 28 October and will expire on 28 November. The special dividend is scheduled to be paid on 5 December and the results of the offer are expected to be announced on 20 December.

Labat Africa has been issuing shares for cash to expand the cannabis healthcare business and address general working capital needs. The latest issue of 22.6 million shares took place at between 16.83 cents and 19.14 cents per share, above the current traded price of 12 cents per share.

Anglo American is a company that takes sustainability and emissions very seriously. I have a lot of respect for what the company is achieving, as there is far more than just lip service being done here. If you’re interested in this stuff, check out the sustainability report at this link

Lwazi Bam, who was CEO of Deloitte Africa until May 2022, is joining the board of Standard Bank as an independent non-executive director.

With the benefit of Stats SA retail sales growth data, Chris Gilmour digs into the South African retail sector.

I always greet the monthly release of retail sales growth data by Statistics South Africa (StatsSA) with a certain degree of trepidation these days, for a variety of reasons. First and foremost is the gut feel that retail sales growth really should be on a noticeable downwards trajectory, considering the poor state of the ambient economy coupled with the increasing interest rate environment.

But it’s not.

Admittedly, much of the rationale for this lies in favourable base effects from the previous year. Whether these relate to coronavirus restrictions or riots doesn’t make much difference. The second reason is the extent of revisions of data by StatsSA.

I can understand why a so-called “flash” estimate of retail sales might be reviewed and subsequently revised a month later. But I am discovering significant revisions taking place going back 3, 6, 9 and more months prior. This doesn’t instill confidence in the integrity of the data.

And then lastly, most JSE-listed retailers are now exhibiting good growth in sales and HEPS, virtually regardless of sector. Even companies such as Truworths which had been languishing for many years has, all of a sudden, produced record earnings. Having said that, most JSE-listed retailers’ share prices are still languishing well below the levels they were trading at five years ago, with the notable exceptions of Clicks and Lewis.

This used to be a glamour sector on the JSE, but not anymore. The companies are still very high profile and it is superficially easy to draw conclusions about their readiness to compete, based on subjective engagements on a personal level.

The big question now is for how long JSE-listed retailers remain on fairly elevated ratings, given the poor outlook for the consumer economy? The answer to this question is that only the strong and the adaptable will survive and flourish in the difficult years that lie ahead for consumer stocks.

Defensive choices

Let’s start with the defensive retailers: the food and drug retailers.

As previously mentioned, Clicks has been an outstanding performer in the market, even though its actual earnings performance has hardly ever shot the lights out. But it is in the right sector (pharmaceutical retailing and wholesaling) and that is highly resilient to the economic cycle. It’s perhaps not surprising that it remains the most highly rated retail stock on the JSE.

The second most highly rated stock is Dischem, not far behind Clicks. Although as a consumer I find it infinitely more interesting and varied than Clicks as a shopping experience, its fundamental earnings performance has been erratic and its share price isn’t vastly different to where it was five years ago following a clumsy, ham-fisted private placement instead of an IPO.

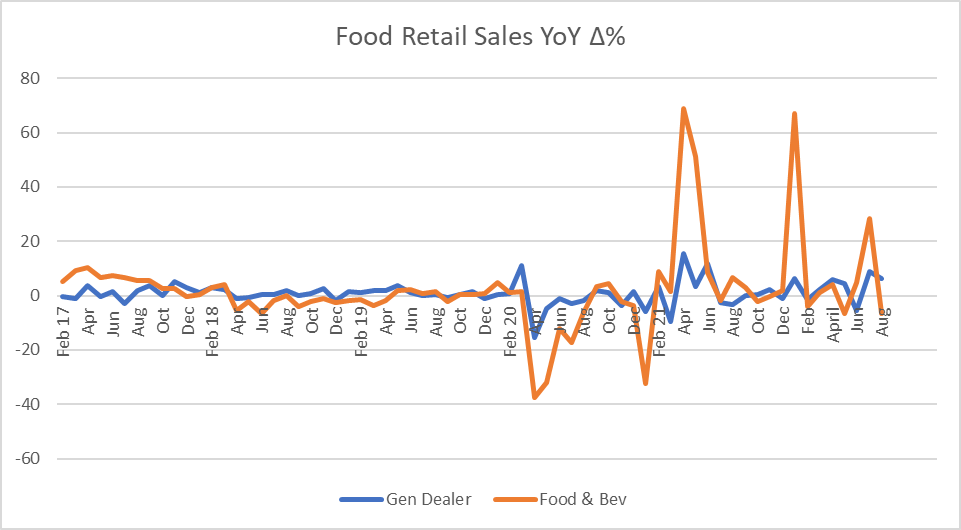

Food retailers in SA should, in the normal course of events, exhibit relatively low and predictable sales growth. That pattern has been thrown into confusion in recent times by the impact of lockdowns and liquor restrictions, as well as the impact of riots in KZN and parts of Gauteng.

The most recent example is the spike in sales in July, followed by a big reversal in August, as shown in the graph below:

Source: Stats SA

Pick n Pay appears to have found a new lease of life under new CEO Pieter Boone. Its interim results two weeks ago were undoubtedly aided by comparison from a soft base in 2021 but nevertheless the group managed to squeeze out some decent sales growth for the first time in years. Their clothing division is really pumping, as is their discounter chain, Boxer.

But can Boone work his magic on the two other elements of the business – QualiSave and the traditional Pick n Pay chain? Only time will tell. The plan is to pit the traditional Pick n Pay chain up against Woolworths Foods at the top end, whereas QualiSave is aimed at the middle market.

Woolworths Foods has definitely lost market share to Checkers in the past year or so and now it’s going to be up against a re-energised Pick n Pay. Provided Pick n Pay can maintain even a slightly favourable price differential between itself and Woolies Foods, chances are it can take market share away.

This just leaves QualiSave. These are smaller Pick n Pay stores where the average number of products on the shelves (stock-keeping units or SKUs) is 8,000. This compares with 3,000 SKUs at a Boxer and 18,000 at a typical Pick n Pay. Just for the sake of completeness, a typical large Tesco in the UK would stock around 45,000 SKUs. QualiSaves should operate on a lower cost model than a traditional Pick n Pay and if that lower cost can be passed onto consumers via lower prices, the re-branding will work. But it will take time for consumer awareness in this regard to catch on.

Spar had its “day in the sun” a few years ago when it bought its Irish, south of England, Swiss and Polish operations. But Spar pricing is perceived to be somewhat more expensive than the average in SA and that could result in a loss in market share over time. Unlike Pick n Pay and Shoprite, Spar doesn’t really have a dedicated discounter brand in SA.

Meanwhile, Shoprite just keeps on pumping out the sales and earnings growth regardless. This is the benchmark by which all food retailers in SA are measured and that situation is unlikely to change anytime soon.

Five years ago I joked with SABC TV interviewer Arabile Gumede that I would rather buy Woolies 250g Chuckles Malted Puffs than Woolies shares. They were both trading at around R60 at the time. Today, the Woolies share price is still pretty much where it was then, perhaps a little higher, but Chuckles are now trading at R75. Go figure.

Clothing retailers

On the clothing front, The Foschini Group (TFG) and Mr Price remain the front-runners in the race to remain relevant in the languishing SA economy. TFG has particular relevance as it has differentiated itself with its quick manufacturing capability that is gradually onshoring an ever-greater proportion of its clothing requirements.

And Woolies? Well, if and when it can do something about disposing of the Australian millstone around its neck, it will have to take a long, careful look at its clothing offering. Still in many ways a glorified department store configuration, is it really best suited to the changing SA consumer economy?

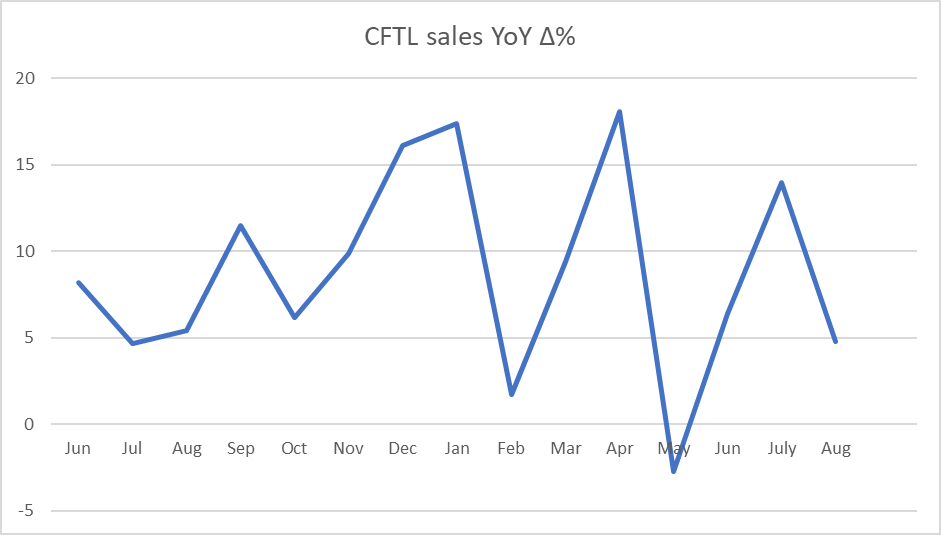

According to StatsSA, the clothing, footwear, textiles and leisure (CTFL) category has been fairly strong for some time now, albeit erratic in nature, as show in the graph:

Source: Stats SA

As is the case with food retailers, where the real battle is at the low end of the social spectrum between the discounters such as Boxer and Usave, so in CFTL the battle is on for the hearts and minds of the low-end consumer in South Africa.

Pick n Pay appears to have found a real niche in its clothing offering and it seems to be taking considerable market share. Mr Price is the acknowledged leader in this area with its fashion at a low price but TFG, as mentioned earlier, is attacking the situation from a different perspective, namely local manufacturing. All three should continue to do well in the SA environment.

It will be instructive to see what kind of sales and earnings growth Truworths manages to squeeze out of its local and UK operations this financial year. Most of its products are in entirely the wrong price points for a languishing economy and as yet it doesn’t have sufficient traction in the low-end segment of the market. Its credit-granting is arguably the best in the business but that is of cold comfort in a market that is increasingly credit-averse.

Is the entire sector too expensive?

So we’re left with a sector that was formerly glamorous in the sense that it contained companies with high sales and earnings growth and high ratings, but which are now just relatively highly rated without necessarily being high growth any more. The foreign fund managers loved the listed JSE retailers because they offered first-world retail management in an environment that looked like an emerging market. And they were primarily responsible for pushing the shares to the dizzy heights that they achieved some years ago. But the local institutions are far closer to the action and are not as easily impressed as their foreign counterparts. The reality is that SA’s GDP growth rate is unlikely to exceed 2% for the foreseeable future, which is a damning indictment on a country with the highest persistent rate of unemployment of any country in the world.

I have always taken the simple view that if a share is rated on a PE of 20x, it should offer HEPS growth of at least 20% per year for the foreseeable future. And yet we have numerous examples on the JSE of shares sitting on PE ratios of 20%+ but where HEPS growth is nowhere near 20% per year.

And while investors love Clicks because of the predictable nature of its business, does it really deserve to be rated on a PE of over 30 times?

So this is the time for highly focused stock-picking to come to the fore. Only highly innovative, nimble retail companies with strong balance sheets will survive intact over the next few years. Already, Edcon and Stuttafords – both unlisted – have hit the buffers and Massmart looks like it’s going the same way.

Shoprite, Mr Price and TFG have been investing heavily through the cycle and will emerge in good shape in my opinion. It looks like Pick n Pay is at long last following suit and also investing heavily.

Clicks will be around forever, though perhaps not on quite such a rarefied PE and the same goes for DisChem.

But beyond this list of six retailers, I can’t say with any certainty that they’ll all be around in ten years’ time.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Glencore’s second half is under pressure

The reason? Weather, industrial action and supply chain issues in Kazakhstan of all places!

Glencore is a giant, with numerous commodities in the group and operations all over the world. This means that each year, some things go badly and others go well. For investors, the outcome is a portfolio effect across a basket of commodities.

For the nine months to September, the strongest production result was in cobalt with a 41% increase. The worst is silver, down 25%.

Zinc has been impacted by supply chain issues in Kazakhstan as a secondary impact of the war in Ukraine. Production is down 18% year-to-date. In Nickel, production is up 15% but guidance for the full year has been decreased because of labour action at two of the mines.

Coal is up 7% year-to-date thanks to higher attributable production from Carrejon, in which Glencore acquired the remaining two-thirds interest in January 2022. Full year guidance has been lowered though, in this case because of severe flooding and higher than average rainfall in Australia. The company expects further disruption in the fourth quarter from the weather patterns.

After an excellent first half of the year, Glencore’s second half isn’t going to be as pretty. Still, the company expects an above-average second half performance. Glencore expects to be at the top-end of the long-term EBIT guidance range of $2.2 billion to $3.2 billion per annum.

Unlike many other resources companies this year, Glencore’s share price is up more than 28%.

Impala Platinum just LOVES load shedding

Here’s a perfect example of how Eskom is breaking our economy

The good news: discussions with the core customer base suggest that PGM demand will rise over the coming year.

The bad news: Eskom.

Yes, poor Impala Platinum (like everyone else) has to navigate the ongoing joy of a power utility that is sometimes just a utility. Or just a liability, actually.

Tonnes milled and 6E in concentrate both increased by 2% year-on-year for the quarter ended September, a decent result under the circumstances. Refined 6E production fell by 5%, with a significant 18% drop in rhodium production. The drop in refined production is thanks mainly to Eskom. This is a perfect example of how load shedding continues to negatively impact our GDP.

The company has maintained its guidance for FY23, as this is only a first quarter production report and it’s too early to justify any changes.

To understand the importance of rhodium in our economy, you should read this excellent article that Greg Salter wrote a few weeks ago.

Industrials REIT: doing what it says on the tin

The impact of a tough base is clear in the growth numbers

As regular readers will know, industrial properties were the darling of the pandemic. The share prices got way too hot and the bump back down to earth has been ugly. Industrials REIT is down almost 40% this year, mainly as a result of a silly valuation coming into this year. As another example, Sirius Real Estate has lost more than 51% of its value.

At operational level though, Industrials REIT continues to do well overall. Tenant demand is strong and the average uplift upon renewal or new letting is at a high of 30%, marking the eighth successive quarter of over 20% uplift.

The business also benefits from the Industrials Hive platform, which gives the REIT more control over the letting process and the ability to showcase its properties in one place.

With the pandemic moratorium coming to an end, the company could take steps to replace non-performing tenancies. This drove a marginal decrease of 0.7% in occupancy and like-for-like passing rent.

The brakes have been applied though, with investment activity on hold as capital values react to macroeconomic conditions. My expectation is that property values fall in this environment, so those who are patient with their capital will be rewarded.

Perhaps the most important metric for investors is the “change in passing rent” or like-for-like growth over the past 12 months. It has dropped every quarter since Q1’22 (8%) until the current level in Q2’23 (2.7%). US analysts would describe this as “lapping tough comps” – in English, this means that performance was so good last year that it’s a tough base against which to compare current growth.

As this market takes a breather and lets the macroeconomic conditions settle, Industrial REIT’s loan-to-value (LTV) ratio of 25% (allowing for unrestricted cash) is good news. The average cost of debt is 2.5% and 90% of the debt is hedged against increases. The average maturity of the debt is 3.5 years and the group is comfortably within debt covenants.

There are likely going to be some difficult times ahead. It seems like Industrials REIT is doing the right things to manage them.

Orion Minerals had a busy quarter of fundraising

The non-binding term sheet from the IDC is the highlight

On a busy day for mining company announcements, Orion Minerals joined the party with a quarterly activities report. This is just a summary of the critical developments over the last three months.

The most important step was the R250 million non-binding term sheet from the IDC. This convertible debt facility will fund early works at the Prieska Copper-Zinc Project. The priority now is taking this to a binding agreement.

The IDC term sheet satisfies a condition to the previously announced A$10 million package from Triple Flag, so it unlocks a large overall funding opportunity.

In other funding news, the IDC also agreed to become a strategic partner in the New Okiep Mining Company by funding a R34.6 million share of the pre-development costs.

Orion also completed a $6 million capital raising and $1.35 million share purchase plan to fund the advancement of the early production plan at the base metal projects in South Africa.

Overall, it was a quarter of extensive fundraising activities to support the company’s journey from being an exploration company to an operating mining company. There’s still a long way to go!

The announcement is incredibly detailed and I would encourage you to read it if you are an investor or interested party.

Tharisa is looking to raise $50 million in a bond issuance

Get ready to learn about the Victoria Falls Stock Exchange

I suspect that the Victoria Falls Stock Exchange (VFEX) has far less liquidity than the natural wonder after which it is named. Some exchanges are purely technical listing venues, offering investors a regulated environment in which to invest rather than a liquid market on which to trade. It all comes down to the types of instruments and the investors that issuers are looking to attract.

Karo Mining Holdings, a subsidiary of Tharisa, will look to raise $50 million in a bond issue on this exchange. This means that the company is raising debt to develop the Karo Platinum Project in Zimbabwe (hence the choice of exchange).

Tharisa owns 70% in Karo Mining which in turn owns 85% of the Karo Platinum Project. The Zimbabwe government owns the other 15%.

The total anticipated capital cost for phase one is $391 million, so the bond will part-fund that plan. The parties expect to break ground in December 2022 and commence production in July 2024.

The minimum amount for the bond raise is $25 million and Arxo Finance (a wholly-owned subsidiary of Tharisa) will subscribe for $10 million of the notes. This effectively means that Tharisa is helping to fund the project, as it should.

If applications are lower than $25 million (i.e. $15 million from third parties), the issue won’t proceed. If excess applications are received, the issuer reserves the right to increase the size of the issuance.

The instrument will pay 9.5% semi-annually with a bullet repayment (i.e. the full capital amount) at maturity, three years from the date of issue.

Little Bites:

Director dealings:

A non-executive director of Bytes Technology Group has acquired shares worth around R233k

Associates of Carl Neethling have acquired shares in Ascendis Health worth just under R4m

Carl Neethling is a busy guy. With the CFO of Ascendis Health having stepped down, he is now taking on that role on an interim basis. He is already the Chief Transition Officer and acting CEO as well! Although these situations aren’t unheard of when a company is undergoing a major change, it will be good to see the management team settle as quickly as possible.

Renergen released results for the six months ended August. This isn’t “big news” because the company is still pre-production, so there are still operating losses. In this period, the operating loss was R30 million vs. a loss of R27.3 million in the prior period. When everything is switched on and the company is operating, the results will be watched closely by the market. The share price is down 24% this year.

Southern Palladium released a quarterly activities report for the three months to September. As this is an exploration company, you need to be a geologist or mining engineer to know what is actually going on here. The company spent $862,000 on exploration in this quarter, which included several drilling projects. As at the end of September, Southern Palladium held $15.9 million in cash.

Sibanye-Stillwater has reached a five-year wage settlement agreement with AMCU at the Rustenburg and Marikana PGM operations. This concludes the wage negotiation process, as agreements were reached with NUM and UASA in September. The agreement is consistent with the previous five-year offer, with average annual increases of 6% and above (subject to a few specific rules). This was a far smoother process than the disastrous labour action in the gold operations. With all benefits, Sibanye’s wage bill is expected to grow at 6.3% per annum over the next five years.

Northam Platinum’s credit rating has been upgraded by GCR and the outlook is Stable. The company has refinanced its R4 billion revolving credit facility maturing in September 2024 with a new five-year facility of R5.705 billion. This is at a better rate than before by 15bps, ranging from JIBAR + 2.40% to JIBAR + 2.80% depending on the level of utilisation. The company also settled the R3 billion bridge facility with a final maturity date of December 2022, replacing it with a five-year term loan of R2.445 billion that matures in August 2027. The rate is JIBAR + 2.50%. Overall, Northam has R9.15 billion in banking facilities. As a final update, Northam has settled all amounts owing to Royal Bafokeng Holdings and therefore owns an unencumbered 34.52% stake in Royal Bafokeng Platinum.

Finbond has released results for the six months ended August. As highlighted before, regulatory changes in the US have had a significant negative impact on profitability. Despite strong growth in loans and advances and even a 2.8% increase in the NAV, HEPS has decreased by 35.9% to a loss of 8.2 cents vs. a loss of 6 cents last year.

aReit Prop released results for the nine months ended September. After a third quarter dividend of 9.64 cents per share, the year-to-date dividend is 20.34 cents per share. The net asset value per share is 935.2 cents and the share price is R7.00.

In an exceptionally weird situation, Kibo Energy once again had “technical difficulties” at the AGM that means most of the largest shareholders were unable to cast their votes. This was already an adjourned AGM, so they went ahead anyway with the AGM and withdrew the resolutions that were outside of the ordinary course of business. They will be dealt with in an extraordinary general meeting.

GMB Liquidity has further increased its position in Grand Parade Investments, taking the stake to 30.23%.

AH-Vest, the owner of All-Joy foods, has a market cap of just R40.8 million. As you might imagine, there’s far more liquidity in the tomato sauce than in the stock. For the year ended June, the company expects to report HEPS of between 1.72 cents and 2.32 cents. That’s a drop of between 68.5% and 76.5%! The company attributes the decline to credit loss provisions that need to be raised on receivables more than 60 days past due. There are also cost pressures throughout the supply chain.

In Ghost Global this week, we bring you the latest news on Hasbro, Goldman Sachs and Volvo.

If you’ve been in the markets in 2022, you’ll know that it’s hardly been a game. It’s been more painful than a family fight after a long night of playing Monopoly, which brings us neatly to Hasbro as our first company in this week’s global update.

For research on global stocks that will help you trade and invest with confidence, subscribe to Magic Markets Premium for R990/year or R99/month.

It’s a kind of Magic

In the quarter ended September, Hasbro managed to miss expectations that weren’t terribly demanding. The pandemic is but a distant memory now, as are the toy sales to parents who were desperate to entertain the kids during lockdown.

Revenue is down 15% to $1.68 billion and adjusted operating profit fell by 31% to $271 million. Not such a monopoly, after all.

The problem is consumer price sensitivity in an inflationary environment where people are trying to afford fuel, nevermind games. This drives increased promotions and puts pressure on gross margins.

As highlighted in Magic Markets Premium some months ago (and not because of the similar name), the best business in the group is Magic: The Gathering. This collectable card game has been popular for three decades and continues to grow its loyal fan base, having become Hasbro’s first $1 billion brand. Hasbro’s revenue growth in the upcoming quarter is expected to be relatively flat, with Magic contributing one of the few positive stories.

The release of blockbuster movies is also important, as Hasbro manufactures toys under licence from studios. Marvel Studios’ Black Panther: Wakanda Forever in November should help, along with six more blockbuster films in 2023.

Finally, Hasbro intends to focus on high-margin pre-school brands including Peppa Pig and Play-doh.

The share price has lost 35% this year. It will be interesting to see how the company performs over the all-important festive season.

Goldman Sachs: a painful point in the cycle

There are several major banks in the US. Even in such illustrious Wall Street company, Goldman Sachs stands out as the most iconic investment bank of all.

At this stage in the cycle, that’s not necessarily a good thing.

For investment bankers to make the kind of bonuses that keep Porsche’s income statement ticking over, there needs to be capital markets activity. Bankers need IPOs and mergers in order to earn juicy advisory fees. After a red hot period during the pandemic as vast liquidity hit the market, there has been a harsh return to reality.

Third quarter revenue is down 12%, though at $11.98 billion there is still no shortage of cash to help pay for impressive office buildings. Revenue is 1% higher than in the second quarter, so there’s a modest sequential uptick.

The Investment Banking segment took the most pain, with net revenues down 57% to $1.58 billion. This is purely because liquidity has dried up and markets have been in the doldrums, so those who didn’t list or raise capital during the pandemic aren’t about to rush into that bloodbath. The situation is worsening this year, with revenue down 26% vs. the second quarter.

The much larger Global Markets segment grew by 11% to $6.2 billion, benefitting from a higher interest rate environment and the knock-on effect for certain products. As a partial offset, there was lower revenue in cash products, equity financing and derivatives. Revenue was 4% lower than in the second quarter.

The Asset Management segment couldn’t escape the broader pressures of the market, with revenue down a nasty 20% to $1.82 billion. It’s almost impossible to grow asset management earnings in a falling market, as net inflows would have to be gigantic to counter the effect of a smaller base on which to earn fees. The good news is that revenue is 68% higher vs. the preceding quarter, so there are signs of improvement.

The Consumer and Wealth Management segment grew revenue by 18% to $2.38 billion, driven by higher deposit spreads and credit card balances. In this part of the bank, higher interest rates are helpful. As balances and average rates have grown, revenue is also 9% higher than in the second quarter.

The share price is down 14% this year. That’s a decent result, as JPMorgan has lost over 22% this year.

For truck sakes

We end off this week with Volvo, a group that manufactures far more than just soccer mom cars.

With an increase in net sales of 35%, it’s interesting to note that Volvo sells more trucks than passenger vehicles. The net order intake for trucks increased by 27% to 64,700 vehicles, with the need to replace ageing trucks as a major driver of demand. Fully electric trucks increased by 307%, albeit off a small base.

In passenger vehicles, deliveries rose by 21% to 53,300 vehicles.

With production and delivery records tumbling for Volvo this quarter, the ongoing challenges in supply chain remain a massive irritation. As lovely as the growth in sales looks, the impact gets blunted by a 34% increase in operating expenses. Operating margins have dropped from 11% to 10.3%.

Impressively, more efficient working capital means that return on capital employed has improved from 25.6% to 27.4%. That’s good going in this environment.

Volvo hasn’t been immune to other geopolitical issues, with construction equipment deliveries down 7% because of market declines in China. The war in Ukraine resulted in substantial impairments of assets relating to Russia.

There’s a significant own goal as well, harking back to Volvo violating EU competition rules and needing to pay a lofty fine. That opened the floodgates for private damages claims from customers and other third parties, with Volvo unable to estimate the potential liability at this stage.

Volvo’s share price is down 16% this year, a far better outcome than many other manufacturers. For example, Ford is down more than 42%!

For research on global stocks that will help you trade and invest with confidence, subscribe to Magic Markets Premium for R990/year or R99/month.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")