Creditor Beware That Your Guarantee Or Suretyship Is Still Intact

Written agreements are important in business and obviate the need to resolve disputes by weighing one person’s word over another’s. Amendments to agreements are often just as important as the original agreement itself. They are used to add forgotten provisions, address a need that became apparent after the entering into the original agreement or change original terms and conditions as a result of changed circumstances, in order to reflect more correctly the intention of the parties.

To remember that an agreement has been amended and to assist with the implementation of the agreement after an amendment, the signed amendment often gets attached to the original agreement. However, there are instances where an agreement is amended several times and, over time, it becomes inefficient, impractical or confusing to follow which terms are still binding. In these circumstances, it is preferable to consolidate all the changes into one document and fully amend and restate the original agreement. A consolidation and restatement does not create a new contract, but rather the original agreement is merged into one document.

If the performance of the obligations of one party to the original agreement (debtor) are secured by a third party (guarantor) in the form of a guarantee or a suretyship in favour of another party to the original agreement (creditor), that security will constitute the giving of financial assistance by the guarantor to the debtor. Such financial assistance must be given in accordance with the requirements of the Companies Act, 2008. The rationale for the requirements of the Companies Act is mainly to ensure that the company giving the financial assistance can indeed afford to give such assistance.

In terms of section 45(3) of the Companies Act, the board of a company may not authorise any financial assistance unless the particular provision of financial assistance is:

• approved by a general or specific special resolution of the shareholders of the company, adopted within the previous two years; and

• the board is satisfied that (a) immediately after providing the financial assistance, the company would satisfy the solvency and liquidity test; and (b) the terms for giving the financial assistance are fair and reasonable to the company.

If the guarantee or suretyship is given without complying with the Companies Act, the board resolution approving the financial assistance and the guarantee or suretyship agreement for the provision of such assistance is void, to the extent that the provision of that assistance is inconsistent with the requirements of section 45 of the Companies Act.

Accordingly, whenever an original agreement is amended, a determination must be made as to whether new financial assistance resolutions are required. This determination would be particularly important if an amendment to the original agreement changes; for example, the financial exposure of the debtor, the material rights and obligations of the debtor, or the introduction of a new debtor, as these types of changes will consequently increase the financial exposure and/or obligations of the guarantor to the creditor in the event of default by the debtor.

In a situation where an original agreement has been amended a number of times, or materially amended once, and the parties elect, for convenience or other reasons, to conclude a consolidated, amended and restated agreement, the creditor must:

• assess whether the financial exposure of the debtor has increased and/or material obligations of the debtor have changed that will result in an increase in the debtor’s financial exposure; and

• if the debtor’s financial exposure has increased or will increase as a result of the modified obligations, request new financial assistance resolutions by the board of the guarantor and, to the extent necessary, new shareholder resolutions approving the assistance.

If the creditor does not make the assessment, or does, but incorrectly arrives at the conclusion that new financial assistance resolutions are not required when, in fact, they are, the guarantee or suretyship in respect of only that portion of the increased financial exposure or obligations will be void. A creditor may, therefore, inadvertently find itself with security that is no longer sufficient to cover its full risks under the original agreement.

Whilst concluding a consolidated, amended and restated agreement may be appealing, require minimal effort and negotiation, and can be signed fairly quickly (in certain instances) it may be sensible for the parties and beneficial for the creditor to terminate the original agreement that has been amended numerous times and conclude a new agreement, for the following practical reasons:

• unless there is a fundamental reason why it would not be ideal for the parties to enter into a new agreement, concluding a new agreement will help frame the creditor’s mind and influence it to make certain that the new agreement and security package is valid and enforceable;

• continuously amending, consolidating and restating an agreement may result in a creditor not applying its mind to whether it should request new financial assistance resolutions because, for all intents and purposes, the original agreement will be continuing, and it may not be immediately apparent that new resolutions are required. This risk may be more prevalent in large organisations where the individual negotiating the consolidated, amended and restated agreement is different from the one that negotiated the numerous prior amendments; and

• in the event that new financial assistance resolutions were required pursuant to prior amendments but never obtained, concluding a new agreement will ensure that the new agreement is not tainted by any prior non-compliances, provided that when concluding the new agreement, there is full compliance with the Companies Act.

In large finance deals, a failure to obtain fresh financial assistance resolutions (if they were required) as a result of an amendment to an agreement may have huge financial implications for the creditor, should it need to enforce its security. Furthermore, there is a risk that the creditor may only become aware of the error and the invalidity of a portion of its security many years down the line, when the debtor’s obligations under the original agreement mature and the debtor is unable to perform. Without considering any remedies that a creditor may have, there is also a risk that a guarantor may very well apply and succeed in setting aside the security (or a portion thereof) on the basis that it was given in contravention of the Companies Act.

Gabi Mailula is an Executive in Corporate Commercial | ENSafrica.

This article first appeared in DealMakers, SA’s quarterly M&A publication

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Anglo taps the green market

Bankers always find a way to make money – welcome to the world of sustainability-linked finance

Unless you’ve lived under a rock for literally your entire life, you’ll know that money drives behaviour. People like nice things and nice things require money, so financial incentivisation is largely what makes the world go around. There are even those who claim not to be driven by money at all, offering consulting services to those who want to live the same way…

When the world’s most important capital allocators talk, the bankers listen. If there is a mandate to invest in projects with a sustainability angle, you can be sure that investment bankers will find those projects, structure them accordingly and only eat tofu in the week that the deal closes, in case there are any vegans on the credit committee.

Anglo American is raising €745 million through its inaugural sustainability-linked bond. The financing cost is 4.75% per annum and the debt matures in 2032.

Will the money be used for green projects? Possibly, but not necessarily.

What makes it linked to sustainability, then? Well, unless Anglo meets targets related to greenhouse gas emissions, fresh water usage and job creation, a penalty rate will apply. The rate increases by 40 basis points per annum for each target that isn’t met.

So, the lenders make more money if Anglo is less sustainable? Yes. Welcome to where investment bankers meet ESG. In theory, the rate is cheaper to start with because of the ESG targets, which encourages the behaviour.

In practice, I continue to be incredibly skeptical of this area of finance.

FirstRand puts in a solid performance

If Twitter is anything to go by (as well as my own experience), FNB needs to wake up

Under Michael Jordaan’s leadership some years ago, FNB positioned itself as the bank for tech-savvy people.

Why? Because tech-savvy people have money. It’s hard to be an Apple enthusiast if you can barely afford the fruit, let alone the iPhone.

A banking client base tends to be sticky, so the benefits are felt for years on end. I’ve noticed a clear trend on Twitter though of people who are very upset with FNB’s offering. If you’ve ever been through their FICA process that makes you feel like a criminal just for having an account with them, you’ll know what I mean.

We can’t see it in the FirstRand numbers, though. Not yet at least. Return on Equity (ROE) for the year ended June 2022 at 20.6% is lovely and the annual dividend at 342 cents per share is the highest in the group’s history. There’s a special dividend of 125 cents per share on top of that, just as an added sprinkling of joy for shareholders.

With only a 6% increase in pre-provision operating profit, the top-line growth and expense management was decent but not spectacular. The earnings growth was really driven by a far healthier credit environment, with the impairment charge down by 48%.

If you’re wondering about the split, FNB contributed 60% of normalised earnings, RMB was good for 25% and WesBank was 5%.

The group is looking to win more market share in lower-risk business. Lower-risk clients tend to be more discerning though (at least in retail banking), so they will need to improve the service experience. On the corporate side, growth in advances picked up in the second half of the year, most likely as a result of inflated balance sheets due to working capital pressures.

Despite this good news story, the share price is only 6.5% higher this year. It is trading at similar levels to November 2019. As the net asset value per share is R29.389, the share price of R65.44 is a Price/Book multiple of 2.23x. Based on ROE of 20.6%, the effective ROE (as you are paying a premium for the “E” – the equity) is 9.2%.

This is expensive in my view for a banking group, so the market is pricing in a lot of growth. This would explain the sideways share price this year.

Metair? Met Eish.

With HEPS down by 74%, this was a period that Metair could never have imagined

Metair’s major customers in South Africa are Toyota and Ford. One of them got flooded to the point of shutting down production for a few months and the other one struggled to get semiconductors (microchips), with a major impact on production. Just to make the recipe even spicier, the Turkish energy business operates in a hyperinflationary economy.

It’s hard to make money off that base. It’s also really difficult to achieve meaningful financial reporting, as the level of “normalisation” in the numbers is extraordinary.

One thing we all understand is the concept of dividends. Needless to say, there isn’t one for Metair shareholders based on this period.

A business insurance claim of R360 million was recognised as income in the six months ended June 2022, of which R150 million has been received. The insurance is capped at R500 million, a number that Metair expects to reach in the second half of the year.

Although revenue only fell by 2%, EBITDA was down by 57% and net debt increased from R2 billion to R2.4 billion. Metair notes that most of the South African debt is classified as current and that there is a “technical covenant breach” – this means that your bankers stop inviting you to their box at the rugby and instead take you to the basement boardrooms for a tough conversation.

Discussions with funders are described as being “positive” and Metair doesn’t believe that they will recall the debt, so the trips to the basement have been fruitful. I also can’t see that the bankers pulling the plug, as the issues here were clearly based on freak events that hit the business simultaneously. The best outcome for the banks and certainly for shareholders is to help the group get back on its feet and service the debt.

Clearly, the focus is on cash generation and preservation. All non-essential capex has been deferred. If you’re planning to wait for a Metair dividend, I suggest that you stand in a few Home Affairs queues to practice your patience.

Little Bites

Discovery Health CEO Dr. Jonathan Broomberg has bought shares in Discovery worth R987k.

City Lodge has released an updated trading statement for the year ended June 2022 and as expected, things look a lot better. The base period was destroyed by Covid, with the company still trying to recover from that pain. The previous trading statement was more conservative, noting that HEPS will show an improvement of at least 75%. The latest guidance is that the loss will be between 87% and 93% smaller, coming in at -90.9 cents. On a share price of R4.28, that’s clearly still a material loss. I look forward to the detailed results being released.

Remgro’s trading statement for the year ended June 2022 reflects headline earnings per share (HEPS) growth of between 120% and 130%. Before you get excited, the reason I’m even mentioning this update is that it means very little in the Remgro context. As an investment holding company, the focus is on net asset value (NAV) per share. The group uses HEPS in the context of deciding whether a trading statement is necessary, as this is what the JSE rules require. Investors should wait for the release of full results rather than trying to read anything into this trading statement.

Texton’s trading statement is more useful, although it is also far less promising. Distributable income for the year ended June 2022 is expected to be between 43.35% and 49.31% lower. There will at least be a dividend at a decent payout ratio (75% – 85%) as the board is committed to retaining REIT status.

SA Corporate Real Estate released results for the six months ended June 2022. Distributable income is up 5.2% and the net asset value (NAV) per share is 4.8% higher at 412 cents. Including derivatives, the loan-to-value (LTV) ratio is 37.8%, down slightly from 38.5%. At a closing price of R2.14 the fund is trading on a discount to NAV of 48%.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Balwin benefits from semigration

Demand has been boosted for apartments in the Western Cape and KZN regions

I’ll be honest, I’m surprised that people have been semigrating to KZN. Perhaps the warm sea more than offsets the numerous problems that the battered province has experienced.

In the six months to August, Balwin recognised 8% more units in revenue and managed to achieve an uptick in gross margin as well. Although there is a healthy book of pre-sold apartments, Balwin does note that rising interest rates are likely to cause a slowdown in sales growth.

HEPS is expected to be 45% to 50% higher in this period, implying a range of between 36.18 cents and 37.43 cents. The share price closed 8% higher at R2.70. For reference, that’s where it was trading in April 2020 when government was still trying to restrict chicken sales at Woolies.

Growthpoint: there’s a problem in Sandton

With Office vacancies even worse in FY22 than FY21, some creative ideas are needed for the space

Whenever I see an update from Growthpoint, I always make sure that I read about the V&A Waterfront. This is South Africa’s premier tourist destination, so it’s a great barometer for the post-Covid recovery. Distributable income from this magnificent property was just R364.9 million in FY21 and has come in at R566.7 million for FY22. The vacancy rate has dropped from 3% to 1.6%.

At the other end of the spectrum, the Office portfolio has seen vacancies increase from 19.9% to 20.7%. Retail improved from 6.2% to 5.5% and Industrial came in at 5.7%, a solid improvement from 9.4% last year.

Growthpoint’s biggest headache is clearly the office buildings, with the company noting that this sector remains oversupplied. I genuinely believe that hybrid working is here to stay, so there has been a structural decrease in demand. They would be better off converting half those offices to padel courts.

Looking at other key indicators:

SA REIT Funds From Operations (FFO) increased by 13.7%

The loan-to-value (LTV) ratio decreased to 37.9% vs. 40% in the prior year

Net asset value per share increased by 6.7% to R21.58 (vs. the current share price of R13.00)

The dividend per share is 8.4% higher at 128.4 cents

Motus operandi

Motus is acquiring an aftermarket parts business on an EBITDA multiple of 6.5x – 6.9x

Motus has been trading under cautionary since June. Unlike some companies in the market (Zeder / Onelogix come to mind), the company actually gets on with things after releasing a cautionary.

Although we still don’t know who Motus wants to acquire, we do have a few more details now:

The target is an aftermarket parts business

Motus will be acquiring 100% in the business

Due diligence is underway (as are negotiations) and should be concluded by 3 October

The company is in a faraway land (a “foreign jurisdiction in which Motus operates”)

The purchase price is between R3.7 billion and R3.9 billion, representing an EBITDA multiple of 6.5x to 6.9x

The business is apparently “asset light” which I find interesting – this means that it generates a return off a relatively modest balance sheet. I guess that when compared to the core Motus business of car dealerships, that is possible.

What I don’t understand is that the cautionary announcement has been lifted, even though we don’t have detailed terms yet. I wouldn’t have done that, personally. There’s no guarantee of a deal at this stage and we don’t know who the counterparty is.

Motus’ market cap is R23 billion, so this isn’t such a small deal that it can be ignored as irrelevant.

Bonjour, DSTV

Groupe Canal+ seems to be far more interested in economic rights than voting rights

French media company Groupe Canal+ SA clearly sees value in the MultiChoice business, despite the challenges it faces in retaining premium subscribers. Canal+ has acquired even more shares, taking the stake to 26.26%.

This has become a serious investment now.

My understanding is that South African regulation limits foreign shareholders from holding more than 20% of the voting rights in an entity holding a commercial broadcasting licence. This means that Canal+ holds a 26.26% economic interest and a much lower voting interest, as the calculation has proportional elements to it.

It’s not clear what is going on here and the market doesn’t seem to be pricing in a buyout offer (probably because of the cap on voting rights), with the share price down by around 6% this year.

Perhaps all the programmes will soon have French names? At least Carte Blanche will avoid any rebranding fees.

Cement volumes drop in South Africa

In the five months to August, PPC’s group revenues increased by 9%.

This wasn’t thanks to South Africa, where cement sales volumes fell by 1%. An increase in average selling price by 5% saved the local result, with net debt decreasing from R1.2 billion in March to R1 billion at the end of August.

No, the real winner was Rwanda, with the East African country achieving 16% growth in volumes. It also helps that 70% of cement sales in Zimbabwe were in foreign currency, as this enabled a $4.4 million dividend to be upstreamed in June. Another dividend is expected at the end of the year.

As a reminder of what hyperinflation looks like, PPC Zimbabwe increased US$ prices by 5% in March, then another 2% in April and finally by a further 5% in August!

Little Bites

Des de Beer is still buying shares in Lighthouse Properties, this time worth nearly R1.7 million.

After being part of the campaign to save Ascendis, Carl Neethling has been appointed as acting CEO and Chief Transition Officer of the group, with this appointment expected to last for around 9 months, much like a pregnancy. He will earn R1 per month, so it’s about as financially beneficial as a pregnancy as well.

Keen to learn more about the battery metals strategy at Sibanye? The company released a presentation that you’ll find here.

Stefanutti Stocks is selling its businesses in Mozambique and Mauritius to a privately owned group for a total of $13.5 million (subject to adjustments). The proceeds will be used to reduce debt as part of the restructuring plan.

Pan African Resources is a rock solid miner. For the year ended June 2022, record gold production was achieved (up 1.9%) and profit after tax was slightly higher for the year, which is a lot more than its competitors can say. Net debt reduced by a whopping 66.7%, which is why the company can pay a dividend and execute a share buyback programme. For some variety in the story, the first commercial harvest at the Barberton Blueberry project was achieved!

The High Court has granted the provisional liquidation order against Constantia Insurance Company Limited, which contributes almost all of Conduit Capital’s revenue. This is what desperation from investors looks like:

Welcome to the new Ghost Bites. Startups are all about experimentation and this one is no different. After much introspection, I felt that it was time for a change.

When I first built The Finance Ghost as a concept and a brand, it was all about delivering great insights in a fun and accessible way. Merging the InceConnect and weekly Ghost Mail publications was incredibly tricky and I feel that I swung too far towards “the news” rather than “the stuff you won’t read elsewhere” – and we all know which one is better.

So here we are. It’s time to have fun again!

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Ghost Bites will still be a daily article. It will still focus on JSE news and will cover the biggest and most interesting news rather than all the news. If you got bored reading about British American Tobacco’s daily buybacks, imagine how I felt writing about them!

Don’t worry – if there’s a story you should know about on the JSE, chances are good that it will be in Ghost Bites.

But if you’re wondering what the exchange rate will be for your next dividend from Richemont, then you won’t find it here anymore. I’m only going to focus on the juicy stuff.

ARC needs a new performance benchmark

Rain has surpassed R1 billion EBITDA and Fledge Capital achieved a 78% IRR on the disposal of WeBuyCars to Transaction Capital

At the moment, ARC’s performance benchmark is on par with using me as a benchmark for the 100 metre sprint. It’s hardly difficult to outperform.

All they need to do is beat a 10% hurdle and they will earn performance participation shares in the investment manager. Based on how things are going with interest rates, you’ll soon be able to beat that with a decent fixed deposit.

Thankfully, shareholders will have the opportunity to approve a new fee structure at the AGM. This will be based on actual costs incurred by the asset manager plus a 5% profit margin. Here’s the bad news though: the 10% hurdle is the new structure. The previous structure had no hurdle whatsoever!

With ARC’s share price down by nearly a third over five years, the money has been made by the investment manager rather than the shareholders.

The intrinsic net asset value (INAV) per share increased by 14.7% in the year ended June 2022. As always, there were significant movements within the portfolio that I highlight below.

The fundsold Afrimat shares for R740 million and pumped R362 million into Kropz Plc during the period, funding the operational cash shortfall at Elandsfontein. R56 million was invested in Rain this year, which isn’t much when you consider that the spectrum auction participation was R1.43 billion. Rain achieved its budgeted EBITDA of R1 billion for the year ended February 2022.

On the financial services side (and remember that ARC Fund holds 49.9% in ARC Financial Services), ARC FS acquired 37.33% of Crossfin for R415 million and invested an additional R303 million into TymeBank. You may recall that TymeBank also received $142.5 million from Tencent and other investors. Tyme Global received $37.5 million as part of the same process.

Here’s another fun fact: Fledge Capital (another ARC investment) achieved a 78% IRR on its disposal of WeBuyCars to Transaction Capital. As private equity investments go, that’s phenomenal.

Attacq’s dividend is back

Gearing is down and a dividend of 50 cents per share has been declared. Exposure to Cell C is the blemish on this result

I hold Attacq in my portfolio. It hasn’t delivered the share price recovery I hoped for in the past year or so, with a flat performance. A distribution of 50 cents per share was still largely ignored by the market, with the share price closing at R6.74.

The balance sheet is healthier (gearing is down to 37.2% from 43.3%), with the proceeds of R850 million from the sale of the Deloitte head office and R444.5 million from the Equites transaction used to reduce debt. The net asset value (NAV) is up to R17.49. You don’t need to get the calculator out to see that the discount to NAV is large.

As a reminder, Attacq is synonymous with Waterfall City in Midrand. It also holds a 6.5% stake in MAS P.L.C. and some investments in Africa that it is trying hard to sell, along with co-investor Hyprop. Ironically, that’s the other property fund in my portfolio.

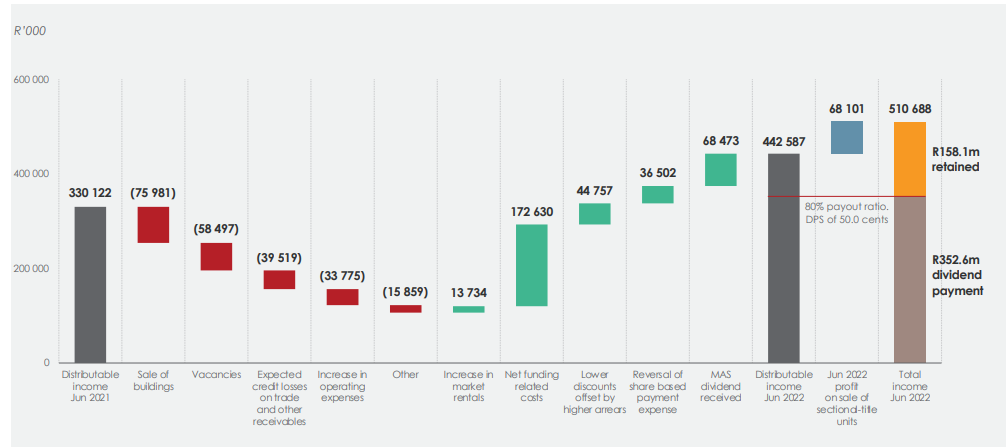

Attacq breaks down its distributable income by portfolio. Waterfall City contributed 32.3 cents per share out of 62.8 cents. Speaking of waterfalls, the company included this waterfall chart in its result:

Here’s a final fun fact: 83% of rand-denominated debt is hedged for interest rate risk, vs. 76.2% last year. This makes sense in the current environment.

One of the blemishes in the result is the exposure to Cell C and its office / warehouse campus, a large property that houses a telecoms company that has caused a lot of financial pain for people over the years. Speaking of Cell C, CEO Douglas Stevenson had to postpone the results announcement and roadshow because he has an upper respiratory tract infection.

I think most Cell C investors over the years would’ve happily swapped their exposure for such an infection.

Labat: the most confusing SENS headline

Labat has put together a joint venture to get more cannabis from Kenton-on-Sea to the global market

Labat’s share price closed 17.6% lower yesterday and I fear it was mostly due to extreme confusion around this SENS announcement:

Read it again. Slowly. And again…

The problem is that they tried to squeeze everything into the headline, like a tweet that should’ve been a thread. SENS needs to introduce threads.

What Labat is actually doing is setting up a distillate facility at the Sweet Waters facility in the Eastern Cape. One of the counterparties is Caliboyz Holdings, which sounds like a Chris Rock movie. Based in California, the company is involved in the design and manufacture of cannabis extraction and manufacturing facilities.

Most of the product will be exported.

Say cheeeeeeeese

Lancewood is the standout performer in Libstar’s results

Libstar’s revenue grew by 9.6% in the six months to June 2022 and EBITDA was only up by 4.6%, so margin deteriorated. Food producers are under a lot of pressure at the moment.

The Perishables category was the big winner, up 14.6% thanks mainly to a strong performance by Lancewood cheese. Normalised EBITDA in this category was up 27.8%.

In Groceries, revenue was up 2.2% and EBITDA fell by a nasty 17.7% because of supply chain challenges and increased logistics costs.

If you ever wondered about the impact of inventory pressures, supply chain issues and inflation on the balance sheet and the ability to generate cash, here’s a very good example of the pain it causes:

Libstar has been repositioning its portfolio towards value-added food products. The Household and Personal Care (HPC) division is performing better these days but is still being “evaluated” – a nice way of saying that Libstar would sell the division if someone would take it.

Toddler Ghost was raised on Umatie frozen baby foods. I can’t resist highlighting that Libstar has acquired that business. Based on our experience, it should be a winner!

Charl de Villiers will take over as CEO from the 1st of January, as co-founder Andries van Rensburg is stepping down after an incredible run at the helm of this group.

Things have slowed down at Mustek

Mustek remains well ahead of pre-pandemic levels, though

Although revenue at Mustek is up 11.5% for the year ended June, the gross profit margin fell from 14.9% to 14.3% and headline earnings per share (HEPS) is down 19.1%.

The dividend has followed suit, down 15.6% to 75 cents per share. For context, it was 90 cents in 2021, 26 cents in 2020 and 30 cents in 2019.

In other words, the year-on-year picture doesn’t look great but Mustek is still well ahead of pre-pandemic levels.

RFG Holdings is just peachy

RFG closed 8.4% higher on a bright red day for the JSE

Most investors were given a hiding by US inflation numbers. If you hold shares in RFG Holdings, you have something to smile about.

For the 11 months ended August, revenue is up 21.2%, driven by strong international demand for canned fruit and other fruit products. Last year’s peach crop in Greece failed, which makes a big difference in the market as Greece is the world’s largest exporter of canned peaches.

And you thought that economy was all about olive oil and high bond yields, didn’t you?

Input costs for those cans are causing pressure on margins, with the company finding it “challenging to fully recover cost increases” – an issue familiar to all food manufacturers.

The carbohydrate enthusiasts among you will be pleased to know that the pie category is recovering. Vegetable sales have been slower. Clearly, we are eating our problems.

Feedback is critical – let us know if you enjoyed the new Ghost Bites!

Ghost Grads Kreeti Panday and Karel Zowitsky bring us Ghost Global this week and they’ve chosen a wonderful array of companies to cover.

Dave & Buster’s Entertainment

Welcome to America, kids. Each Dave & Buster’s venue has a full-service restaurant and a video arcade!

In the company’s second quarter ended July 2022, the group completed the $835 million acquisition of Main Event, after which Main Event CEO Chris Morris took over as CEO of Dave & Buster’s. The group now owns nearly 150 Dave and Buster’s branded restaurants and over 50 Main Event branded restaurants.

Source: Dave & Buster’s website

The company achieved record Q2 revenue of $468.4 million, up 24% from Q2 2021. Of this, $51.4 million consisted of revenue from Main Event, so it’s not as exciting as it sounds. Adjusted EBITDA was a record $119.6 million, rising 0.3% from the comparable period.

The company has emphasised its efforts to brand its restaurants as an ideal football-watching destination, with a national media campaign that includes partnering with ESPN and driving awareness on platforms such as Twitter, TikTok and YouTube.

The group’s D&B Rewards Program has gained over four million members since its inception in November 2021. Loyalty members comprise 5% of sales year-to-date.

The group is optimistic on future shareholder returns despite macroeconomic factors and has pledged to closely watch costs and capital spending. The share price is flat over the past year and has been range-bound, so the chart isn’t quite as exciting as the venues themselves.

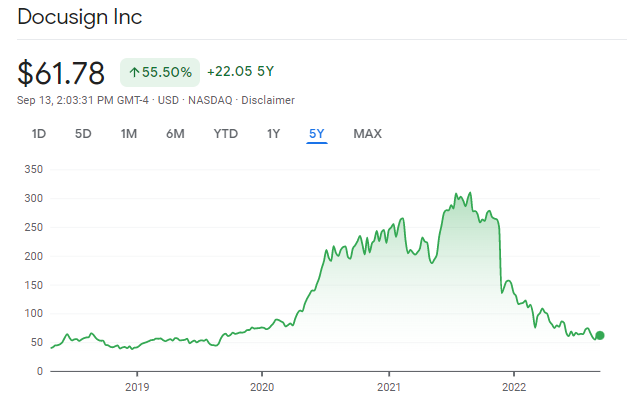

Many new brooms trying to sweep clean at DocuSign

Electronic agreement management company DocuSign has released results for its second quarter ended July 2022. Total revenue increased 22% from the comparable period to $622.2 million. Subscription revenue was up 23% to $605.2 million, while professional services and other revenue was down 11% to $17 million. Billings rose 9% to $647.7 million.

The company’s customer base grew by 22%, adding 44,000 customers and bringing the total to 1.28 million globally.

The company has announced new product capabilities such as an addition to DocuSign eSignature which enables users to send or manage envelopes on another user’s behalf. The company is focused on “integrated and trusted customer partner experiences” and has deployed a strategy of upgrading talent through vigorous training and retention initiatives to achieve this. DocuSign is focused on using the next quarter to drive operating expense reductions and improve operating margins.

The company is also currently undergoing a leadership transition, with 6 out of 8 executive leaders joining in Q2 (perhaps giving new meaning to “upgrading talent”). A search for a new CEO is currently underway, which makes this new executive team sound a bit like a real-life version of Game of Thrones.

Previous CEO Dan Springer resigned after the company lost over 60% of its value within a year, being replaced by Chairman of the Board Maggie Wilderotter in the interim.

GameStop: playing with collectibles

If you’ve ever wondered where you could get your own Thor hammer or Iron Man mask – this is the place. Gamestop is one of the world’s largest video game retailers, selling everything from consoles and games to collectibles for Marvel and Star Wars. Founded in 1984 in the state of Texas, Gamestop is listed on the NYSE, and operates over 4,500 stores worldwide. About 3,000 of these stores are situated in North America with the remainder being found in Canada, Europe, and Australia.

Having a look at the Q2 financials that were released for the period ending 31 July 2022, we see that net sales decreased to $1.136 billion from the prior year’s second quarter of $1.183 billion. Sales from collectibles increased to $223.2 million for the quarter compared to $177.2 million in the prior year, proof that Ghost Grad Karel Zowitsky isn’t the only one who got excited about the Thor hammer that comes with batteries.

Although sales are decent and the company is operating at a gross profit margin of 24.8%, SG&A expenses are sitting at 34.1% of net sales. The maths isn’t your friend here.

GameStop has reported another net loss. The company attributes this to long-term initiatives, which some of these companies like to call “investing through the income statement” – in other words, spending more than they make!

Gamestop’s 52-week range is $19.39 – $63.92, so there’s no shortage of volatility here for the average investor. The $30 mark is a key support and resistance level, depending from which side you are approaching that level. This is fun for swing traders but not for investors!

Cushions to break the fall

Based in Stamford, Connecticut, Lovesac is a furniture company that is most notable for its couches that can be organized in almost any way using their platform called “Sactionals” – essentially bases of the couch on which sides and seats can be added to create a wide variety of different configurations that will fit your home. In addition to couches, Lovesac sells beanbags called Sacs. This product is obviously where the company derives its name from.

Source: Lovesac website

Looking at the Q2 results, we see net sales at $148.5 million, an increase of 45% from the previous Q2 of $102.4 million. The gross profit margin sits at a healthy 54.5%. Operating expenditure increased 42% from $50 million to $71 million but Lovesac still managed to pull off a cool net income of $7.1 million, down 15.7% from 8.4 million in the previous Q2.

Lovesac is listed on the NASDAQ with the ticker LOVE but even these comfortable products couldn’t break the fall of the share price, down nearly 60% this year. The 52-week range is $25.55 – $87.12 which is huge. The price is back where it was in July 2020 when people were staying home and staying safe, buying themselves new furniture to make that process more comfortable.

This is a classic example of a good business that had a silly valuation.

Interested in global stocks? Not sure how to do your own research, or looking to supplement your own process? The Finance Ghost and Mohammed Nalla release a weekly podcast and report on global stocks, available for R99/month or R990/year in Magic Markets Premium. The full library is available, giving you over 45 reports to enjoy!

DRA Global has successfully completed the sale of the G&S business to KAEFER Integrated Services. The net proceeds are A$3.4 million and DRA will recognise a pre-tax loss of A$4.1 million on the assets and liabilities sold. There is existing litigation against G&S and DRA has retained this exposure, which is why KAEFER bought the assets and certain liabilities of the business rather than the shares in the entity. Buying the entity vs. buying the business is a key consideration in any acquisition.

Have you ever wondered about the documentation involved in raising debt capital on a public market? If you want to flick through the 121 page thriller that is the Anglo American Euro Medium Term Note Programme offering circular, you’ll find it at this link.

Financial updates

Construction group WBHO’s share price is down nearly 32% this year and almost 45% over five years, so this isn’t a happy story. The share price chart is remarkable, with periods of range trading followed by regular drops that Red Bull would organise an extreme sports event around. In a trading statement covering the year ended June 2022, the group reminded the market of an announcement back in June about the enormous losses in the discontinued Australian operations. It will cost them A$135 million just to shut that business down. From continuing operations (i.e. excluding Australia), HEPS will be between 0% and 5% lower. For total operations, the picture is hideous – HEPS will be between 695% and 700% lower. You won’t see that every day. Full results are expected on Tuesday this week.

Metrofile Holdings released results for the year ended June 2022. The share price is 6.7% lower this year, so there hasn’t been much excitement. This is reflected in the results, with revenue up just 5% (and only 1% if you exclude the acquisition of IronTree) and EBITDA up by a paltry 1%. Although HEPS was only 3% higher, the dividend per share was 20% higher. The company experienced destruction of higher priced boxes when POPIA was implemented, so that didn’t help things. Since the second quarter, the company experienced an increase in intake and reduction in destructions. The largest revenue contributor outside of South Africa is MRM Middle East, which has grown nicely over the past 18 months. The problem is that MRM South Africa revenue decreased by 2% to R539 million and MRM Middle East grew 10% to just R86 million, so it’s a cute business but doesn’t save the group result. The group margin pressure is something to keep a close eye on, as the company attributes this to a higher mix of digital services vs paper services. The paper business carries a higher margin, so this feels like a structural decline in margin. Net debt increased 3% to R446 million after acquiring IronTree for R66 million. HEPS for the year of 30.7 cents puts the group on a Price/Earnings multiple of 10.4x. The dividend yield is 5.6%. In my view, the only reason that anyone buys Metrofile at this valuation is that there is the ongoing possibility of someone swooping in and making an offer for the business.

Lesaka Technologies (previously Net1) has announced fourth quarter and thus full year 2022 results. If you strip out the Connect group, the business only achieved similar revenue to the comparable quarter. It’s actually worse than that, as Connect contributed $86.2 million directly (out of $121.8 million this quarter) and grew the existing business by 23%. In other words, revenue would be lower without Connect, though currency also plays a big role here as on a constant currency basis, the ex-Connect business grew revenue by 35%. Lesaka reports in dollars and earns in rands. The group operating loss of $10.1 million is an improvement on $13.6 million in the comparable quarter but is still nasty. “Segment adjusted EBITDA” (typical of tech companies – splitting out inconveniences like corporate costs and inter-company eliminations) improved to $6.1 million from a loss of $6.7 million. As you can guess, the full-year numbers reflect substantial losses, especially as Connect group was only included from mid-April. To give you an idea of how expensive M&A is, Lesaka spent R65.9 million on the acquisition of Connect. The share price closed 4.4% lower, though there is very little liquidity.

Choppies Enterprises released a trading statement for the twelve months ended 30 June 2022. HEPS will grow by between 81% and 101%, a strong recovery after a highly disrupted Covid year. The share price is down more than 10% this year.

ArcelorMittal South Africa has agreed a payment plan with the Competition Commission, provided for in the 2016 settlement agreement. The remaining portion of the settlement will be payable from 2022 to 2028. The company has put in numerous controls to ensure compliance with competition law going forward.

WG Wearne Limited has been suspended from trading since 2016, so you can forgive yourself for having never heard of the company. The same rules apply as the company catches up on results. It looks very silly, but the company has released a trading statement for the 2018 financial year. The HEPS range hardly matters. The good news is that the company is catching up on its financials.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Operational updates

Brait released a voluntary update to the market based on the upcoming presentation at the RMB Morgan Stanley Conference. The share price closed nearly 6% higher, so the market liked it. The happiest news is in Premier, the FMCG business that seems to be bucking the trend in a market that has seen the likes of Tiger Brands come under pressure. Premier is achieving the holy grail for food manufacturing: volume growth while passing on input price increases to customers. Revenue and EBITDA growth are ahead of budget, with double digit increases for FY23. A recent decrease in key commodity prices is encouraging for inflationary pressures. This business is being prepared for a separate listing, so the good news needs to keep coming. In Virgin Active, clubs in residential areas are performing strongly and inner-city clubs are underutilised, which makes sense given the shift to hybrid work. Overall, the business remains under pressure, especially as consumers in Europe and the UK have been impacted by rising living costs and the clubs in that region are dealing with severe inflation. The South African gyms are achieving membership sales above 2019 levels, though I must point out that many people would’ve cancelled during the pandemic. Finally, at clothing retailer New Look, a shift towards an omnichannel model has helped the business perform in line with expectations since January, after Omicron significantly impacted trading at the end of 2021. Brait needs to pump more money into New Look as part of a deal to extend an operating facility with HSBC, so another R182 million will flow into this business. It carries a 16.5% coupon and ranks ahead of the existing payment-in-kind (PIK) facility. This is essentially a glorified shareholder loan, which isn’t worth much if the business fails. Thankfully, it seems to be turning the corner.

Fairvest released a pre-close presentation for the period ended 30 September 2022. The fund is moving out of industrial, office and residential assets and into retail assets, which is quite the pivot! The entire strategy is built around simplifying the business and reducing risk. In the office portfolio, vacancies have decreased to 15.4% from 16.7%. The industrial portfolio has seen vacancies rise to 4% from 1%. Vacancies in the retail portfolio are stable at 4.8%. Loan-to-value is expected to be below 40% by year-end. 59% of debt is expiring in the next 12 months, so there will be a major focus on the balance sheet.

South32 has announced the dividend that will be payable to investors on the JSE. The final dividend is 241.91510 cents and the special dividend is 51.83895 cents.

With its migration to the Netherlands now achieved, NEPI Rockcastle has declared an interim dividend. The dividend is 22.83 euro cents per share, which at current exchange rates would be around R3.95 per share. The share price closed at R93.27, just over 2% higher.

Notable shuffling of (expensive) chairs

On a day to forget for WBHO after the release of a trading statement reiterating the financial damage from the Australian business, the resignation of an independent director was also announced.

The CEO of Libstar has retired and a new CEO has been appointed. Andries van Rensburg is stepping down from the company he co-founded in 2005, no doubt with many stories to tell. The current CFO, Charl de Villiers, will take the top job from 1 January 2023. He has been with the group since 2017. Cornel Lodewyks has been promoted from managing executive of Lancewood to an executive director position of Libstar. A new CFO will be announced in due course.

Director dealings

The ex-CEO of The Foschini Group, Doug Murray, has “rebalanced a portfolio” in his trust by selling nearly R28 million worth of shares in the company. The share price is up more than 13% this year. What’s the opposite of buying the dip again…?

A director of a subsidiary of Blue Label Telecoms has sold shares worth over R640k. A director of a different subsidiary sold shares worth R578k.

Des de Beer is still mopping up shares in Lighthouse Properties, although this time he could only get his hands on nearly R40k in shares.

A director of recent JSE addition CA Sales Holdings has bought shares worth nearly R20k.

A non-executive director of Capital & Counties Properties now holds 0.04% of shares in issue, having added to the position with further purchases of around £118k.

Unusual things

Here’s something cool: Industrials REIT will be added to the FTSE All-Share Index from 19 September, having now met the eligibility criteria. This is important because it means that index funds will need to buy the stock in order to correctly track the index. The share price closed 2.66% higher, though it should be noted that it was a green day overall on the JSE.

RCL Foods announced a “small related party transaction” in terms of which it has extended the provision of management services to Siqalo Foods for a further three years. Siqalo is a subsidiary of Remgro, hence the related party designation.

Chris Gilmour puts on his geopolitical hat and updates us on the sanctions against Russia, the energy crisis facing Europe and the extent of the Ukrainian resistance.

One of the major factors contributing to the current bout of high inflation and interest rates globally is the continuing war in Ukraine. What began as a limited special operation that was only supposed to take three days has turned into a nightmare not only for Ukraine and Russia but for most of Europe and many other parts of the world.

The war grinds on

Over six months later, the conflict has deteriorated into a grinding war of attrition, with seemingly no end in sight. But at least the rationale behind Russia’s invasion of Ukraine is becoming clearer, and Ukraine’s resistance has stiffened to a point that few if any observers thought possible at the outset. The bottom line is that this war could well drag on for years, in which case higher inflation and interest rates are likely to remain a feature of the global economy for equally as many years.

Global recession looms on the horizon and Europe is likely to bear the brunt of it.

The EU has adopted a non-negotiable stance with Russia over its invasion of Ukraine, even going so far as to offer Ukraine EU candidate membership status. It will not soften its stance on Ukraine unless and until Russia withdraws its troops. Russia has retaliated by cutting off gas supplies to Europe. The end result has been a massive rise in European gas prices in the past few months, which have had serious inflationary effects.

Russia’s gas has been supplied to Europe primarily via the Nordstream 1 pipeline, a 1,200km pipeline which lies under the Baltic Sea and connects St Petersburg in Russia to north-eastern Germany. The pipeline is owned and operated by Nordstream AG and its majority shareholder is Gazprom of Russia. Nordstream 2, a parallel pipeline, was supposed to have come on stream last year but was halted by Germany after Russia invaded Ukraine.

An effective Mexican standoff, or gigantic game of “chicken” has arisen between the EU and Russia over its involvement in Ukraine and the supply of gas to Europe. The Europeans are resolute in their resistance to Russia’s aggression in Ukraine and Russia appears equally determined not to supply any further gas to Europe. Currently, Russia’s gas is being flared off near the start of the Nordstream pipeline not far from the Finnish border. The Russians don’t have storage facilities in the area to store the gas and thus their only option if they don’t supply Europe is to flare it off.

In aggregate, Europe’s gas stores are 80% full, which will allow most countries to get to February or March 2023, even if no more Russian gas is supplied.

The EU has also proposed price caps on Russian oil and gas that will remain in place until Russia leaves Ukraine. So a real deadlock has set in.

In the coming northern hemisphere winter, which starts around November and lasts all the way through February, the mood is going to be very sombre indeed. Germany in particular has put all its energy eggs in one basket metaphorically speaking, by using Russian gas to such a great extent. The question isn’t just about whether or not Germans or Dutch, or Belgians or French or whoever are going to freeze in their homes this winter. Supply of gas will be sourced from somewhere, but at a great cost. No, the biggest single concern is industrial supply of energy. The Germans in particular will have to cut back substantially on their manufacturing capability, purely because the costs of doing business with anything other than Russian natural gas will be prohibitive.

This in turn will lead to recession in Germany and any other country in Europe or elsewhere for that matter that relies on the German industrial machine for its existence.

Back to the battlefield

One of the most surprising things about this invasion is how useless the Russian military has turned out to be. I am from a generation that can remember the Prague Spring of 1968, when Soviet tanks rolled into Prague and crushed Aleksandr Dubcek’s attempt at reform of the communist system in Czechoslovakia. And I have seen the newsreels of the 1956 uprising in Budapest fomented by Imre Nagy that was met with the same amount of brute force. Of course these were very different circumstances, as both Czechoslovakia and Hungary were mere satellites of the USSR but the point is that in those days, the Soviets acted quickly and decisively to quell any possibility of insurrection.

That all changed in later years, when the Soviets had to leave Afghanistan after a decade in that country achieving precisely nothing. Probably the closest comparison that can be made with the Ukrainian conflict is what happened in the renegade region of Chechnya, where the capital Grozny was shelled into rubble during the first Chechen war of 1994 to 1996. Although Russia and Chechnya ceased hostilities for a few years, they erupted again in 1999 and lasted for ten years. These were bloody campaigns, with heavy casualties on both sides.

The Russians have adopted their usual strategy of using massive artillery firepower in Ukraine, just as they did in Chechnya and, incidentally, in the Battle of Berlin in 1945. It’s a simple but effective strategy that relies on pulverising the urban infrastructure to rubble before allowing the infantry to go in and take control of the area that is left. That is what they have done in the eastern and southern regions of Ukraine and have used unimaginably large amounts of ammunition. Retired US General Petraeus, interviewed on CNN recently, said that Russia was using as many artillery shells in a single day as the US used in the entire campaign in the first Gulf War. It has been widely reported that Russia was using 40,000 artillery shells per day at the height of hostilities on the eastern front. Apart from depleting the Russian ordnance supply very rapidly, that type of hammering also takes a huge toll on the big gun barrels as well. If not maintained – which is likely the case in Russia – these guns become useless very quickly.

Other analysts have highlighted that Russian ammunition is often dangerously outdated (more than 30 years old) and can be dangerous to handle. It is not known what capability the Russians have to replenish their ammunition supplies on such a scale that is required for further continuous shelling, but the New York Times published an article last week stating that the Russians are sourcing artillery from North Korea. If this is true, it is pretty desperate stuff and is a damning indictment on the inability of Russia to manufacture and supply industrial-scale artillery shells and rockets.

The Ukrainians, conversely, have been having a fair degree of success in recent weeks and months, especially since receiving supplies of the HIMARS multiple rocket launcher system (MRLS) from the US. HIMARS is much more accurate than the Russian MRLS and has the ability to “shoot and scoot” to avoid detection by the Russians. This has allowed the Ukrainians to specifically target Russian-controlled infrastructure in Crimea and other parts of occupied Ukraine with impunity. It has been especially successful in eliminating Russian ammunition dumps at railheads, as well as bridges and other critical infrastructure in southern Ukraine. It seems likely that Ukraine may be on the verge of taking back control of the southern city of Kherson from the Russians. Reports are also coming in that Ukraine is advancing rapidly in the Kharkiv area farther north as well.

This is all good and well and is great for Ukrainian morale. But to be realistic, the chances of physically ejecting the Russians from the eastern areas such as the Donbas is likely to be much more difficult than taking back Kherson. The Russian military cannot be far away from ordering a general mobilization of troops in Russia to bolster its flagging capabilities in Ukraine. However, that will likely be a double-edged sword for Russia. On the one hand, it means they will get more troops virtually overnight. But at the same time, these will be conscripts who really don’t want to fight, many of whom will have friends and relatives in Ukraine. Much of the current Russian military comprises ethnic minorities such as Chechens and Mongols, who are reasonably well paid and are effectively mercenaries.

But will sanctions be effective?

Ukraine’s (and the west’s) greatest hope lies in the effectiveness of sanctions against Russia. If enough economic and financial pressure can be applied via sanctions, Russia will not be able to finance its war in Ukraine for an extended period of time. But sanctions take time to work properly.

Anyone who lived through the sanctions era in South Africa will remember how much nationalistic pride this instilled in certain sections of the community at the outset. A process of inward industrialisation began and South Africa managed to produce a huge amount of its requirements locally. It was far from being an autarky, mainly because it had to import all of its oil, but it became self-sufficient in many other products and services. However, that situation didn’t last and after a while, the corrosive impact of sanctions really began to bite hard.

The same will happen with Russia, but like the situation with South Africa, it will just take time.

We must also not forget that sanctions-busting almost became an art-form for Rhodesians and South Africans in the 1960s, 70s and 80s. Almost anything could be bought and sold, for a price. Who can ever forget that meeting between Gordon Waddell, Harry Oppenheimer’s son-in-law and director of JCI and Anglo American , and his Soviet counterparts at the Bolshoi Ballet production of Boris Godunov in Moscow in November 1980? When questioned about his appearance, Waddell nonchalantly replied that he was “just passing through”. In reality, although the USSR and South Africa were sworn ideological enemies, at a financial level they did a lot of business together.

The G7 recently managed to institute a policy whereby Russian oil will be subject to a price cap, with estimates of that cap being between $40 and $60 per barrel. Currently, Russia is receiving a shade under $100 per barrel for its Urals crude and even the heavily-discounted oil that it sells to China and India is going for around $70 per barrel.

Trying to calculate a breakeven cost of production for Russian crude is tricky, as it emanates from a variety of locations, although the Urals in Siberia is the main region. Officially, Russian oil companies mention a figure of between $4 and $8 per barrel as being their estimated cost of production, but this seems ridiculously low. IHS Markit estimates a figure of around $44/barrel.

The mechanism for prosecuting these sanctions is via global shipping insurance. The plan is to ensure that no Russian oil cargoes will be insured by the cartel that runs global shipping insurance. That can even be extended to ports as well. But as illustrated earlier, there are many ways to skin a cat and the Russians will presumably already have alternative shipping plans ready.

Russia’s potential Achilles Heel: the permafrost

Russia is a major player in global energy markets, being one of the world’s top three crude producers, along with Saudi Arabia and the United States. Russia relies heavily on revenues from oil and natural gas, which in 2021 made up 45% of Russia’s federal budget.

In 2021, Russian crude and condensate output reached 10.5 million barrels per day (bpd), making up 14% of the world’s total supply. Russia has oil and gas production facilities throughout the country, but the bulk of its fields are concentrated in western and eastern Siberia. In 2021 Russia exported an estimated 4.7 million bpd of crude, to countries around the world. China is the largest importer of Russian crude (1.6 million bpd), but Russia exports a significant volume to buyers in Europe (2.4 million bpd).

Russia is the world’s second-largest producer of natural gas, behind the United States, and has the world’s largest gas reserves. Russia is the world’s largest gas exporter. In 2021 the country produced 762 billion cubic metres (bcm) of natural gas, and exported approximately 210 bcm via pipeline.

The bulk of Russian oil and gas comes from the far east of this enormous country, specifically Siberia, where the ground is referred to as permafrost. Permafrost is what it sounds like; it rarely gets unfrozen and that impacts pipelines, both oil and gas, though in different ways. Russian oil from Siberia freezes if it doesn’t keep moving, due to the fact that all crude oil contains an element of water and the water freezes at a much higher temperature than oil.

Russian oil companies have to ensure that their pipelines are insulated so as to avoid freezing, especially in harsh winter conditions.

Thus unlike more “normal” oil producers such he US or the Gulf states, Russia can’t just cap its wells during times of lower demand. To do so would result in frozen and burst pipes and in a worst-case scenario, destroyed oil wells. So it’s imperative for Russia that oil continues moving, even if only slowly. That is one of the reasons why it has offered such attractive discounts to countries such as India and China.

Gas is somewhat different. The permafrost in which the bulk of Russian gas is found is warming up in the summer months and the gas pipelines are now encountering subsidence that is adversely affecting them. Maintaining these pipelines under changing conditions is an expensive exercise.

The bottom line: Europe is feeling major pain

However this conflict eventually pans out, there is going to be major pain in Europe, especially during the winter months of 2022 going into 2023. Even if a few rogue states such as Hungary and Italy break ranks with the EU, the majority will go along with the EU decision to rapidly wean the area off Russian energy as quickly as possible.

Recession has probably already arrived in Europe as it has, technically, in the US. Higher energy prices are going to be a feature of life for ordinary people and businesses for the foreseeable future. Business will be able to source alternative energy supplies, but at a prohibitive cost in the main. Certain governments will attempt to soften the pain with so-called price caps for its consumers, such as the measures mentioned in the UK’s new Truss administration’s speech last week. But the damage has been done and trying to reverse this – which is ultimately what is required if inflation is to be tamed – is impossible at least in the short term.

For its part, Russia is likely to continue looking stupid on the battlefield. Its military is but a shadow of the former mighty Soviet military machine and nothing is going to change there. Sanctions will eventually bite hard into the Russian economy but they will take time and during that time there is always the possibility that the EU’s cohesion and resolve will further break down.

Russian people are no strangers to hardship and there is little doubt that they will just suck it up. They have no choice under the Putin autocracy. The Kremlin has no intention of relenting, not even when the world demonstrably sinks into prolonged recession. In the long term, provided sanctions do work, then Russia will eventually be beaten into submission. At that point it will no longer be able to finance its aggression in Ukraine or any other part of eastern Europe for that matter.

But by then, the world will be a very different place and fossil fuels may no longer be of such great economic importance.

In an unusual outcome, Transaction Capital’s share price closed 0.78% higher on Friday despite a significant capital raise that saw shares in issue increase by approximately 5%. Having originally intended to raise R1 billion, the company raised R1.28 billion at a price of R35.50 per share, a 4.7% discount to Friday’s closing price. Usually, the share price drops when a capital raise is executed, as investors are diluted at a discount. The fact that the bookbuild was oversubscribed is another strong show of faith in the company.

As we’ve seen with a few banks, FirstRand has made the move to acquire its preference shares from shareholders. This is no longer an attractive source of funding under new banking regulations. FirstRand took the route of a scheme of arrangement, as the ideal outcome was to acquire all the outstanding shares. Having been approved by shareholders, the final amount of R100 per share plus a pro rata dividend will be paid on 26th September.

There’s action on the shareholder register at Fortress REIT. After Allan Gray increased its stake in Fortress A shares to over 5%, we now see Peresec holding 5.4% of Fortress B shares. This is the prime broking business at Peresec, which means it is probably linked to structures put in place with hedge funds or similar institutional players. There are going to be intriguing movements in this share register as we get closer to Fortress losing REIT status.

MTN has upsized its debt capital markets bond auction, which means that investor demand was strong. The initial plan was to raise R2 billion, with an option to increase it to R2.5 billion. The notes on offer varied in tenor (three, five and seven years) with a preference for longer dated notes. The auction on 6 September was massively oversubscribed, with R5.431 billion in investor interest, all within or tighter than price guidance. MTN decided to issue R2.565 billion in notes as follows: R540 million in three-year, R1.04 billion in five-year and R984 million in seven-year notes. This has improved MTN’s ratio of non-rand to rand debt and has improved the debt maturity profile, all while achieving better pricing along the curve. Post-settlement holding company leverage is unchanged at 0.8x and non-rand debt will only be 33% of group debt vs. 42% when interims were released.

Value Capital Partners has sold shares in Super Group and now only holds 0.33% of shares outstanding.

Having underwritten the recent capital raise, Calibre Investment Holdings now holds 11.7% in Ascendis Health.

At PPC’s annual general meeting, the company withdraw the resolution that would give the directors a general authority to issue shares for cash. The board has noted that any potential issue of shares will be put to shareholders for a vote. After an incredible recovery run in 2021, the share price is down over 51% this year.

Financial updates

FirstRand released a further trading statement for the year ended June 2022. The range for headline earnings per share is between 576.6 cents and 600.6 cents, representing an increase of between 20% and 25%. The share price has been very volatile this year, currently showing a 6% gain in 2022. Full results will be released on 15th September.

Bell Equipment released its interim results for the period ended June 2022. Revenue is up 10%, operating profit is up 15% and net profit has increased by 20%, a perfect example of how leverage works in a business (a percentage change in revenue drives a larger percentage change in profits). HEPS has increased by 19%. The number that sticks out is the net cash flow for the period, which has gone from a R264.2 million inflow in the prior period to a R176.7 million outflow in this period. The biggest swing in cash was in working capital, with the business absorbing nearly R1.1 billion in working capital in this period. The company attributes the higher inventory levels to a planned increase in production volumes, as well as poor performance from certain component suppliers that has now forced Bell to hold higher levels of components. This sounds to me like a structural increase in working capital. No interim dividend has been declared.

Caxton and CTP Publishers and Printers released its results for the year ended June 2022. This is a complicated group with several investments in addition to its operating entities, so one has to be quite careful in choosing which lines to use in assessing financial performance. Although HEPS has more than doubled to a 10-year record high of 157 cents, the net asset value per share is only 9.9% higher at R18.87 per share. A major driver of revenue was the return of retailer advertising spend in local newspapers, which creates demand for advertising brochures. The packaging side of the business also did well, as the alcohol and quick-service restaurant industries recovered. There has been a deliberate move in recent years to replace declining publishing earnings with the growing packaging business. The business maintained its margins despite pricing pressures, though it notes that this required a “transparent and flexible approach” with customers and that pricing reviews took place on a more regular basis. As for the strained relationship with Mpact, Caxton notes that it “continues to persevere in efforts to obtain clarity regarding competition related issues as between Mpact and Golden Era, Mpact’s major customer and competitor and co-accused in a cartel case still pending before the Competition Tribunal” – a far more mature statement than the drivel put out by Caxton in its last announcement on this matter. As a reminder, Caxton holds a 34% stake in Mpact and has made noise about working towards control of the company, though nothing formal has happened in that regard. Caxton has declared a dividend of 50 cents per share. The share price closed 5.6% higher at R9.94.

York Timber released a trading statement for the year ended June 2022. Detailed results are coming on 20 September. In the meantime, investors can chew on the news of HEPS decreasing by between 73% and 80%. Ugly, isn’t it? Cash generated from operations is expected to be between 50% and 55% lower than the previous year, which is worse than the drop in EBITDA of between 30% and 35%. So not only are earnings significantly down, but there’s pressure on cash flow generation as well. The share price is 33.5% lower this year.

The ARC Fund Partnership is returning nearly R20 million in capital to listed group ARC Investments. This will meet the operational cost requirements of the listed company for the next three years. Structurally, ARC Investments is a limited partner in the ARC Fund, which is an en-commandite partnership (typical of private equity structures).

For shareholders in Blue Label Telecoms, here’s one for the diary: the webcast of the Cell C annual results for 2021 and interims for the six months to June 2022 will take place on 14 September at 2pm. Here’s the link to register.

In the very unlikely event that you are a shareholder in suspended company WG Wearne Limited, you should note that the financial results for 2017 have been restated. This is because the 2018 audit is currently underway (that isn’t a typo). It never ceases to amaze me how messy things can get among the worst companies on the JSE. Don’t ever make the mistake of assuming that an investment in a publicly listed company is always less risky than a private company.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Operational updates

None today!

Share buybacks and dividends

Having now sold its stake in Atterbury Europe Holdings for R1.75 billion and as part of a strategy to realise its entire portfolio over the next four to five years, RMB Holdings has declared a dividend of R2 billion. This equates to 141.67283 cents per share, of which 17.98676 cents is a return of capital (and therefore not subject to dividends withholding tax) and the rest is a normal dividend on which tax is payable. The share price closed at R1.94. Yes, 74% of the market cap is going to be returned to shareholders through this distribution.

Anna Dimitrova will join the board of Vodacom as a non-executive director. From 1 November, she will take the role of Group Financial Controller for Vodafone Group plc, having worked in the group for over 20 years. Vodafone is the controlling shareholder of Vodacom.

Kathleen Bozanic has resigned as an independent non-executive director of DRA Global. The reason given is that she has been appointed as the CFO of another company.

Anthony Ball did not make himself available for re-election at the PPC AGM.

Simon Fifield has been appointed as an independent non-executive director of Redefine. He is currently the CEO of Newpark REIT, a role he will relinquish on 1 November 2022.

Linda de Beer is stepping down from the board of Tongaat Hulett after three years, with effect from 30 September. The reason given is that there are increasing demands on her time from other roles.

Director dealings

One of Dr Christo Wiese’s investment entities has acquired shares in Brait worth R22.4 million after the close out of a single stock futures contract. The share price is down by around 16% this year.

Entities related to Wiese have piled into Shoprite exposure, buying shares in the open market worth R1.75 million and single stock futures contracts with exposure of over R224 million!

A non-executive director of CA Sales Holdings has acquired shares in the company worth over R560k.

Calibre Investment Holdings (an associate of two of the directors of Astoria) has acquired shares in the company worth over R41.5k.

Unusual things

The JSE has paved the way for actively managed ETFs (like Cathie Wood’s ARK structures in the US). This would allow fund managers to have a collective investment scheme structure that is listed on the JSE rather than accessible as a unit trust. It will be very interesting to see what happens here, as it could make life a lot easier for retail investors! If you’re interested, you’ll find the approved amendments to the JSE Listings Requirements at this link.

The trading halt on MC Mining shares on the Australian Stock Exchange has been lifted, after being put in place in response to substantial share price action despite no new updates being in the market.

With a market cap of R26 billion, Transaction Capital is now raising R1 billion through a placing with institutional investors. The group currently holds 74.9% in WeBuyCars and is looking to acquire another 15%. This brings the put and call arrangement forward, as Transaction Capital is keen to deploy more capital into a business that it knows and loves. Interestingly, the remaining 10% is held by the founders (5% each) and they will defer their put options (the right to sell) to the 2027 and 2028 financial years, but not later than 2030. Transaction Capital will forego its call option on the remaining shares, so these shareholders could technically elect to remain in WeBuyCars forever. The capital will also be used for the GoMo business that will be housed in SA Taxi (refer to the snippet in the operating updates section below for more details). Some capital will be leftover for general group purposes. The announcement came out after market close, so you can expect to see share price pressure on Friday morning.

As part of its repurchase programme to try and undo some of the discount to net asset value that the management team so successfully created over time, Prosus has sold 1,115,000 shares in Tencent, reducing the total ownership in the Chinese tech giant to 27.99%. Another 192 million shares are being moved from certificated form into the dematerialised format in Hong Kong, which would pave the way for further sales in an “orderly way” over time. Whilst it makes sense from a finance theory perspective to sell the Tencent shares and repurchase the discounted Prosus and Naspers shares, it also increases the concentration of non-Tencent assets in the group, most of which really aren’t attractive in my view.

Absa has confirmed that Barclays holds just 0.02% of the issued share capital of our local bank. As for why there is still a small shareholding left, I can only assume that the bank holds it on its balance sheet as part of a hedge for a derivative structure somewhere or perhaps in a securities-related book. Either way, the strategic stake is gone.

The potential take-private of OneLogix is really dragging on now. The first announcement about a potential deal came out in December 2021. Since then, “negotiations have been in progress” and there’s still no guarantee of any kind of offer on the table. The financial performance of the company deteriorated sharply in recent times and of course the conflict in Ukraine came as a shock, so there are some reasons why it should be taking this long. Still, this is a case of you-know-what or get off the pot.

If you are a tax professional or you are interested in this field, you’ll want to read PSG’s announcement about the apportionment of tax cost for the unbundled shares. If you don’t fit into those categories, watching your grass grow will be a more entertaining use of time.

Financial updates

Tongaat Hulett released an update that ticked practically every box: debt restructuring, trading statement, operational update and further cautionary! I decided to put it in the financial section, as Tongaat’s terrible financial situation is driving all this news. There is R6.3 billion of excess debt in the South African operations, which is simply unsustainable. This number is R800 million worse than a year ago, as 2022 saw a significant cash outflow due to operating conditions. Net debt is R6.6 billion, of which R5.4 billion is owed to South African lenders and the balance is trade finance owed to the South African Sugar Association. There’s another R1 billion in debt in the African operations. To make it worse, there is a working capital shortfall in the 2023 financial year as existing headroom on the debt isn’t enough to fund the milling season. The board is currently considering options including an equity capital injection at various levels in the group or a disposal of some or all of the African operations. To keep the lights on while everyone figures this out, the lenders are working with Tongaat to structure a suitable facility. The banks are clearly scared here, as they haven’t invoked the interest rate ratchets on the debt (a penalty rate for breaching covenants). Tongaat is also negotiating with other potential lenders to secure a further R750 million. Although HEPS hardly matters right now, the range for the year ended March 2022 is -676 cents to -632 cents per share. The prior period was originally reported as -631 cents but was subsequently restated to -440 cents per share.