The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I recapped five important stories on the local market:

Bell Equipment can take a bow, with a trading statement showing very strong earnings growth and a few weeks left this year to still achieve a further positive earnings surprise.

MTN is a casualty of African currency weakness, which makes it vulnerable to further dollar strength and a slow Chinese recovery – complicated look-through exposures that are important to understand.

AVI is achieving reasonable revenue growth at the moment, with a focus on margins paying off for the company.

Truworths has demonstrated just how tough the SA consumer retail environment still is, with the UK business saving the day.

De Beers has experienced another sharp drop in sales, with a perfect storm of macroeconomic challenges and cheaper lab-grown diamonds clearly visible in the numbers.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

AngloGold’s production rises sequentially (JSE: ANG)

Annual production guidance for 2023 has been affirmed

AngloGold owns a number of mines and they don’t all improve at the same time, but the direction of travel at group level is positive. Production in the third quarter was 3% higher than the second quarter. They had to grind it out the hard way though, with higher ore tonnes processed and a lower overall recovered grade.

This is good news with more international eyes on the company, as the primary listing was moved to the New York Stock Exchange on 25 September.

The other piece of good news is that production is expected to increase further into the final quarter of the year, thereby helping the company achieve full-year guidance.

Before you get too excited, the nine-month view still reflects a 3.2% drop in production year-on-year.

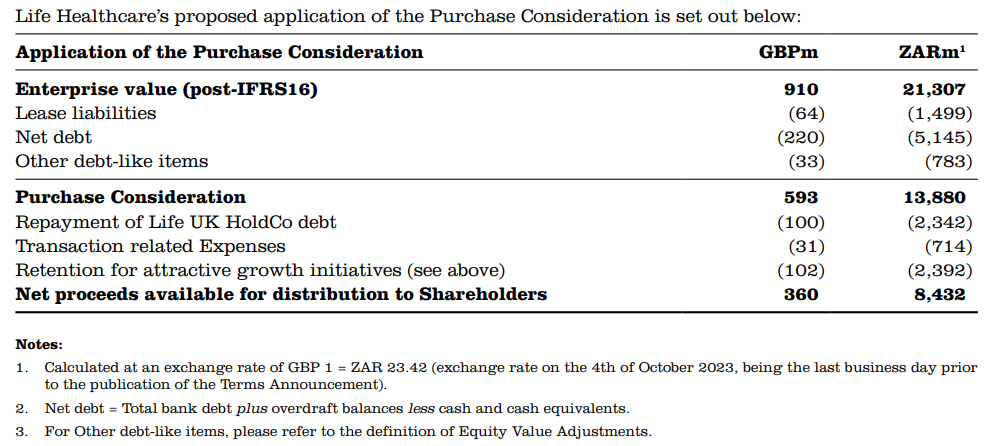

Life Healthcare releases the Alliance disposal circular (JSE: LHC)

The deal was first announced in early October

Life Healthcare is selling its investment in Alliance Medical Group. This is a Category 1 deal that requires shareholder approval. The purchaser is iCON Infrastructure.

Alliance Medical Group has significant capex needs going forward, so Life Healthcare shareholders have dodged that bullet at a time when money is expensive. The cash will be used to reduce group debt, so this transaction makes a significant difference to the balance sheet vs. what might have been. The net proceeds from the transaction after offshore debt and expenses are estimated to be GBP360 million, or around R8.4 billion. The plan is to distribute this to shareholders within three months of completion date.

You may find this cash flow waterfall rather interesting:

Goldman Sachs and Barclays Bank acted as joint transaction advisors, earning GBP 10 million each in the process. Tough life.

If you’ve ever wondered how the relationship between doctors and hospitals works, here’s an interesting paragraph from the circular:

Doctors may have rental agreements in place where they practise, but do not otherwise work under contracts with Life Healthcare. To assist with the retention and motivation of doctors, Life Healthcare allows doctors to make equity investments in some of the operating companies where they practise. Life Healthcare also maintains a medical advisory committee at each of its hospitals, which provides an opportunity for doctors to be involved with the management and monitoring of the quality of care at the respective hospital. Life Healthcare has historically experienced low rates of turnover of doctors at its facilities.

Multichoice is getting burned by African forex (JSE: MCG)

If money needs to be remitted from Nigeria, life becomes painful very quickly

Much like MTN or Nampak, Multichoice is suffering because of what is going on in African currencies. A trading statement for the six months to September confirms this problem.

In fact, the board has now approved something called “adjusted core headline earnings per share” (yikes!) to show the operating performance with losses incurred on cash remittances from the Rest of Africa markets in the group. Simply, the quoted exchange rate and the actual rate at which cash can be remitted are two different things.

On a constant currency basis and despite significant investment in Showmax and a 16% increase in local content investment, trading profit is expected to be between 7% and 12% higher. But after forex losses, trading profit as reported is between 16% and 21% lower than previously reported.

Core HEPS is down between 3% and 8%. This excludes the losses on cash remittances from Nigeria. To put those losses in perspective, they came in at R0.5 billion which also happens to be the extent of additional investment in Showmax. These forex issues are a big problem.

Adjusted core HEPS is between 22% and 27% higher, but that must be because the base period had even worse cash remittance losses than this period.

Finally, HEPS in the same way that everyone else reports it will be a bigger loss than in the comparable period. After reporting a headline loss per share of 58 cents in the comparable interim period, the loss should now be between 287 cents and 291 cents.

Even the Rugby World Cup probably won’t save the result for the second half of the year. It’s all about the Nigerian currency and ever Pieter-Steph du Toit can’t tackle that problem.

Novus expects a massive increase in HEPS (JSE: NVS)

But take note that this is off a low base

Novus has released a trading statement dealing with the six months to September. The base period saw HEPS of only 2.89 cents, with this period reflecting at least a 500% increase on that number. This implies HEPS of at least 17.34 cents for the six months.

The current share price is R4.12.

PPC guides a swing into profits in the interim period (JSE: PPC)

PPC Zimbabwe has been the major positive shift in this period

For the six months to September 2023, PPC will report HEPS of between 25.5 cents and 26.5 cents. The prior period was a loss of 6 cents per share, though this number has been restated for certain accounting errors in the timing of impairments.

The big swing into profitability is a result of PPC Zimbabwe performing well in this period vs. the prior period when it had an extended kiln shutdown. PPC Zimbabwe has also changed its functional currency from the Zimbabwean dollar to the United States dollar, with a positive impact this period.

Little old Primeserv has grown earnings rather nicely (JSE: PMV)

With a market cap under R150 million, this isn’t exactly a widely-followed stock

Primeserv has been around for 25 years on the JSE, yet you’ve perhaps not even heard of it. The group is involved in businesses like outsourcing and staffing services, as well as training.

The company has released a trading statement for the six months to September 2023 that reflects HEPS growth of between 20% and 23%. This implies a range of 14.90 cents to 15.30 cents per share for the interim period.

For reference, the share price is R1.26.

Here’s another reminder of how cyclical Sappi is (JSE: SAP)

EBITDA has more than halved year-on-year

Sappi has released results for the quarter ended September 2023 and they are a useful reminder of how cyclical this sector is. Revenue is down 28% year-on-year and EBITDA excluding special items has fallen 57%. The group has even slipped into a headline loss position vs. a strong profit a year ago.

This quarter caps off the 2023 financial year, with full-year results showing a 20% drop in sales and 45% decrease in EBITDA. Headline earnings fell 62%.

Despite this, the full-year dividend was consistent at $0.15 per share.

Aside from geopolitical stability and a global economic downturn, one of the more specific drivers of the drop in performance was an underperforming Chinese economy. Another factor was that inventory destocking at buyers took longer than expected, with Sappi responding by trying to preserve selling prices and margins to the greatest extent possible. There have also been some major restructuring steps taken at some of the European sites.

There were some positives, like South Africa achieving record EBITDA for full year 2023. Also, net debt of $1.09 billion is the lowest level in 30 years!

None of this was enough to offset sharp drops in sales volumes, so Sappi will be hoping for a better year in FY24. Some parts of the business have experienced a structural decline though, like graphic papers where capacity is being reduced. With a strong balance sheet, Sappi sounds confident about its ability to rise to challenges.

Separately, the company announced several changes to the board among independent directors, including the chairman who is retiring after several years in the role.

Sephaku’s profits dipped in a tough environment (JSE: SEP)

Although revenue moved higher, both operations saw a contraction in margin

Sephaku Holdings has released interim financial results for the six months ended September. As I’ve reminded you before, that’s not quite true, as SepCem (one of the two major operations) has a December year-end and so this period for Sephaku Holdings represents the six months to June for SepCem and the six months to September for Metier and the group accounts.

The reason why the year-ends can’t be aligned is that Sephaku only holds a 36% shareholding in SepCem. This means that it equity accounts for the earnings (recognises its share of them) rather than consolidates the entire financial result.

With that out the way, we can note that although revenue grew in both underlying divisions, a contraction in EBITDA margin to 10% at Metier and 8.6% at SepCem means that HEPS fell from 11.26 cents to 7.54 cents, a 33% reduction in profits.

But if you read more deeply, you’ll find that Metier actually grew its profits because EBIT margin was stable even though EBITDA margin wasn’t. Profit after tax increased from R29.5 million to R37.8 million. SepCem is where the real pressure was felt, with equity accounted earnings swinging from a profit of R3.8 million to a loss of R14 million.

The challenge at SepCem will be to achieve price growth to recover input cost increases. This is anything but easy in such a soft market in terms of demand.

Sibanye-Stillwater isn’t shy of deals in tough times (JSE: SSW)

In fact, this is usually the best time to be buying assets

You need a strong stomach to operate in the mining industry. Neal Froneman and the team at Sibanye have been doing this for a long time, so they understand market timing and the value of buying when everyone is bleeding (including themselves).

To this end, Sibanye announced the acquisition of Reldan, a US-based metals recycler. The enterprise value is $211.5 million and the cash purchase price is $155.4 million.

This is part of Sibanye’s “circular economy” strategy of owning recycling and tailings businesses. Reldan is a bit different to the rest of Sibanye’s business, as the company reprocesses waste streams like industrial waste and electronic waste to recycle green precious metals. This means gold, silver, palladium, platinum and copper from waste items like semiconductor scrap and mobile phones!

In 2022, Reldan generated $371 million in revenue, $42 million in EBITDA, $39 million in earnings and $28 million in free cash flow.

This is an interesting diversification strategy!

Truworths is going backwards in South Africa (JSE: TRU)

My bearishness on SA retailers continues

Truworths released a sales update for the 17 weeks from 3 July 2023 to 29 October 2023. Sales increased by 10.9% year-on-year, which sounds decent at first blush. Account sales were 47% of total sales (down from 52% in the comparable period), so most of the growth was in cash sales (up 22.5%) vs. account sales (up just 0.1%).

So then why did the share price drop 3.8% on a day when the All Share only fell 0.3%?

The challenge sits in the South African business. The Truworths Africa division mostly consists of South Africa and saw sales increase by a paltry 1%. Account sales were steady at 70% of total sales and key credit metrics also appear to be consistent. Comparable store sales fell 2.2% despite high inflation of 9%, so volumes were down by double digits. The group expanded into this environment anyway, with trading space up 1.1% and expected to be up by between 1% and 2% for the 2024 financial period.

At least online sales grew locally, up 41% and contributing 4.7% to Truworths Africa’s total sales.

In the UK, the Office business grew sales by 18.9% in pounds, which is obviously a great result in rands – up 38.8%, in fact. This is despite trading space dropping by 5.5% as Office exited all seven of its stores in Germany. The business is expanding overall though, with trading space expected to be up by 9% for 2024.

In the UK, online sales contributed 45% of total sales, up from 41% in the comparable period and thus growing much faster than the bricks-and-mortar business.

The market is clearly worried about the underlying metrics in South Africa, as rand weakness isn’t a good reason to hold Truworths. In fact, it’s a good reason not to hold Truworths because of the impact on South African consumers and inflationary pressures like fuel and food.

Despite this setback, the share price has still been a great performer in 2023 because of the modest valuation, up 34% year-to-date.

Little Bites:

Director dealings:

Des de Beer really opened his wallet this time, buying R13.6 million worth of shares in Lighthouse Properties (JSE: LTE)

An associate of a director of Wesizwe Platinum (JSE: WEZ) sold shares worth R1.75 million.

A director of Old Mutual (JSE: OMU) bought shares worth R624k.

Although a prescribed officer of Capitec (JSE: CPI) exercised options to acquire shares, the options must be exercised within nine months of the strike date and hence I’m not sure this gives us much insight into market timing.

Finbond (JSE: FGL) has posted the circular dealing with the specific repurchase of 38.55% of shares in issue.

Tongaat Hulett (JSE: TON) confirmed that the Secured Lender Group have entered into a transaction to sell their claims and security to a consortium of parties that includes Robert Gumede.

Alexander Forbes and OUTsurance have concluded a binding agreement which will see Alexander Forbes acquire 100% of the shares in OUTvest, a digital wealth platform. The platform integrates automated advice, human advice, administration, and asset management into a digital wealth solution. The disposal by OUTsurance follows a strategic review of OUTvest and the resultant decision to consider a restructuring due to the sub-scale nature of the business. Financial details were undisclosed as the acquisition falls below the threshold for categorisation.

Sibanye-Stillwater is to acquire US-based metals recycler the Reldan Group for a cash consideration of US$155,4 million. With its platform and technology capable of processing a variety of waste streams, the acquisition of Reldan enhances Sibanye’s exposure to the circular economy. The deal is expected to be value accretive, positively contributing to Sibanye’s earning and cash flow from day one.

Clientèle has announced it is to merge its business with that of 1Life, an insurer specialising in funeral and underwritten life insurance products. Clientèle will settle the R1,91 billion acquisition price by way of an issue of shares. The consideration shares (117,815,756 translating into a 26% equity stake) will be issued at R16.25 per share which includes a control premium of 6.23%. The acquisition is accretive, resulting in a combined Embedded Value of c.R7,8 billion and almost 1,5 million contracts.

NEXT176, a venture capital business backed by Old Mutual, has announced a R27 million investment in JOBJACK, a South African tech startup offering a recruitment registration platform for entry-level job seekers. NEXT176 led the R45 million pre-Series A funding round. The funding will be used to scale the business by expanding its network of employers and job seekers nationwide.

Sirius Real Estate has disposed of an industrial park in Maintal, in the German region of Hesse for €40,1 million. The disposal represents a net initial yield of 5.7%. In addition, via its BizSpace subsidiary, Sirius has exchanged and completed the acquisition of a £33,5 million portfolio of three assets located in North London from a closed ended fund.

Unlisted Companies

Legacy Africa Capital Partners (LACP), through its LACP Fund I, has acquired a significant minority stake in Welltec, a local financial wellness technology company and provider for responsible credit solutions for consumers. Founded in 2016, Welltec’s digital Credit Gateway platform offers personalised, actionable guidance for consumers. To date, Welltec in collaboration with partners that license its technology services, has restructured some R1 billion worth of credit for over 170,000 consumers.

Twelve years after being acquired by Dimension Data, SYNAQ, South Africa’s cloud-based email security services, has been bought back by its co-founder David Jacobson. Financial details were undisclosed.

Inclusivity Solutions, a Cape Town-based insurtech startup has raised US$1,5 million in a Series A extension round. Impact investor Goodwell Investments led the round, having backed Inclusivity Solutions in previous fund raises. The insurtech which delivers embedded insurance solutions, will use the investment to scale its expansion plans into at least 12 African markets by end 2024. It will also continue to invest in its no-code, open API platform which enables distribution partners and insurers to offer a full range of insurance products in a matter of hours.

Following the results of the scrip dividend election, Hyprop Investments will issue 20,832,563 ordinary shares in the company in lieu of a dividend, resulting in a capitalisation of the distributable retained profits in the company of R499,981,512.

Due to the disposal of two businesses, enX finds itself in the enviable position of having surplus proceeds to the operational requirements of the company and as such, has declared a special distribution of R1.00 per enX share. The distribution of R182 million will be paid to shareholders on 27 November 2023.

Mantengu Mining has issued 10 million shares, representing 6.49% of its issued share capital, to GEM Global Yield at R1.13 per share. The shares were issued to discharge a commitment fee due by the company for access to a share subscription facility of up to R500 million.

Several listed companies reported repurchasing shares this week. They were:

During the period 27 July to 1 November 2023, Ninety One ltd repurchased 8,900,922 ordinary shares, representing 3% of its issued share capital. The shares, which will be cancelled, were repurchased for an aggregate value of R345,6 million financed from excess cash resources.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 30 October – 3 November 2023, a further 3,965,096 Prosus shares were repurchased for an aggregate €107,7 million and a further 343,784 Naspers shares for a total consideration of R1,02 billion.

Glencore intends to complete its programme to repurchase the company’s ordinary shares on the open market for an aggregate value of US$1,2 billion by February 2024. This week the company repurchased a further 10,010,000 shares for a total consideration of £43,8 million.

To better reflect the nature of its business, Go Life International will, subject to shareholder approval, change its name to Numeral. The company is a multi-faceted healthcare company offering a comprehensive product range to address needs from pharmaceutical, generic, nutraceutical, medical consumables through to high-end hospital equipment. If approved, the company is expected to trade under its new name on 12 December 2023.

Four companies issued profit warnings this week: Sephaku, Omnia, TWK Investments and MultiChoice.

Five companies issued or withdrew a cautionary notice: Clientèle, Ayo Technology Solutions, Conduit Capital, Ascendis Health and Tongaat Hulett.

Royal Exchange has received approval from Nigeria’s Securities and Exchange Commission (SEC) to conduct the signing ceremony for its proposed Rights Issue of 4,116,296,059 ordinary shares at 50 kobo per share (on the basis of four new ordinary shares for every five ordinary shares held).

NGX-listed Japaul Gold & Ventures Plc has applied to the SEC to raise capital of ₦20,000,000,000 through the issue of 8,000,000,000 ordinary shares at N2,5k each via special placements. The capital would be used primarily to fund the acquisition of a 50% equity stake in H&H Mines, 100% of Covenant Gems & Gold Minerals and the establishment of a gold refinery to maximise value.

Pharmaceutical manufacturing company, Me Cure Industries Plc, listed 4,000,000,000 ordinary shares of 50 kobo each at a price of ₦2.96 per share on the Growth Board of the Nigerian Exchange this week, adding ₦11,84 billion to the market cap of the West African bourse.

Francophone Africa super app, Gozem has acquired a majority stake in Beninese fintech, Moneex. Financial terms were not disclosed, but co-founders Florent Ogoutchoro and Henry Ukoha will retain an equity stake.

Zambian social enterprise, Good Nature Agro has closed a US$8,5 million Series B round from new investor OikoCredit International and existing shareholders Goodwell Investments and Global Partnerships.

Kenya’s I&M Group has received notice that British International Investment Plc had agreed to sells its 10.13% stake in the company to East Africa Growth Holding, an investment vehicle set up by AfricInvest Fund IV, AfricInvest IV Netherlands and AfricInvest Financial Inclusion Vehicle. Financial terms of the deal were not disclosed.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Alexander Forbes is the buyer of OUTvest (JSE: AFH | JSE: OUT)

This sub-scale business needed a new home

OUTsurance Group is focusing on its core competencies, which is a good thing. OUTvest was a good attempt at getting into the investments game back in 2017, but they didn’t manage to achieve scale in the business. I must give credit to management for recognising that the business was simply too small and difficult to justify continued involvement.

It didn’t take long to find a buyer, with Alexander Forbes jumping in to acquire 100% of OUTvest. There are certain conditions precedent that need to be met for the deal to go ahead, like regulatory approvals. The idea here is that OUTvest will then be part of a full-scale investment house that will allow it to reach its potential.

In the Alexander Forbes announcement about this deal, the company highlights the digital nature of the OUTvest solution and how this is a good strategic fit.

The deal is below the categorisation threshold for both companies, so this is a voluntary announcement and the value hasn’t been disclosed.

Argent Industrial is showing solid HEPS growth (JSE: ART)

Once again, we have an industrial business moving in the right direction

Here’s another example that supports my overall thesis at the moment that industrial businesses are in a better position than consumer businesses. Argent Industrial has released a trading statement dealing with the six months ended September. HEPS is expected to be between between 12.6% and 32.6% higher, so that’s very encouraging.

This is a range of 204.1 cents and 240.4 cents. For reference, the share price is around R15 and was up 3.7% in the aftermath of the earnings release.

Despite a strong year of underlying performance, the share price has been incredibly choppy and is trading slightly below the levels seen at the beginning of 2023. One of the great frustrations in the market is that you can be “right” about the underlying business without getting rewarded by the share price.

AVI is focusing on margins in this environment (JSE: AVI)

Comments at the AGM point to a soft environment, but strong cost control at AVI

At the company AGM, the chairman of AVI gave an update on trading conditions in the first quarter of the year. Revenue is up 5.2% year-on-year, which isn’t much to get excited about. Volume performance is mixed across categories and I&J is still struggling, with poor catch rates and an unfavourable sales mix.

The good news, however, is that gross margins have expanded because of price increases and cost controls. Operating profit growth for the quarter was “pleasing” despite the I&J challenges, with operating margin also expanding. This means that operating profit growth was higher than revenue growth.

Final allocations in the hake long-term rights allocation were made on 1 October. I&J’s quote is materially in line with the allocation initially made in February 2022, with a final reduction of around 5% relative to the rights held before the 2020 fishing rights allocation process began.

At De Beers, rough diamond sales are looking rougher by the day (JSE: AGL)

The lab-grown debate rages on – and my view is unchanged

Anglo American has released the latest sales data at De Beers. Cycle 9 2023 achieves sales of a paltry $80 million, way down from $454 million in Cycle 9 2022 and also lower than $200 million achieved in Cycle 8 2023.

The company keeps trying to convince the market that this is a deliberate decision to hold back on sales while supply and demand equalises.

Let me reframe that for you: we would like to sell more diamonds, but they aren’t moving quickly enough through retail stores and hence we have to hold back on sales because there isn’t enough demand.

I will say it again: lab-grown diamonds are disrupting this market. The 20- and 30-somethings out there want to buy experiences, not things. There are many people who are more than happy with a pretty ring for half the price, with the rest of the budget available for travel or the wedding itself.

As the excellent American Swiss billboard outside Canal Walk screams to people passing by on the highway: diamonds are for everyone.

Will the De Beers marketing machine manage to convince people that mined diamonds are still superior? Or will demand continue dropping, with mined diamonds only finding a market in premium jewellery? And in the interest of giving a balanced view, can lab-grown diamonds stay this cheap, or are they currently running an unsustainable economic model to try win market acceptance before ramping the price?

We can debate it all day long, but the De Beers numbers are telling quite the story.

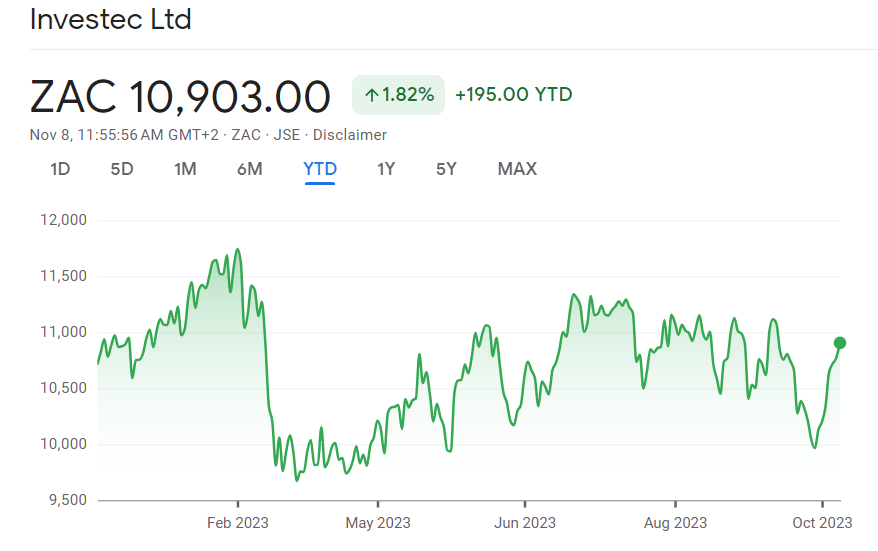

Investec did even better than expected (JSE: INL)

Earnings guidance has been revised higher

Back in September, Investec released a pre-close update for the six months to September 2023 that indicated a HEPS range of 33.8 to 35.8 pence vs. 32.0 pence in the comparable period.

The financial services group has released a further trading statement that now reflects a HEPS range of 36.5 to 37.5 pence. This is obviously great news for shareholders.

The updated guidance means that the growth in HEPS is between 14% and 17.2%. This is measured in GBP, so that’s a hard currency return.

The share price is up roughly 16% over the past 12 months. The year-to-date performance is flat though, with this very interesting chart that shows how many times the price has tried to break higher:

Lesaka reports an operating profit for Q1’24 (JSE: LSK)

This platform is still sub-scale, but there are promising signs here

Lesaka Technologies really is an interesting story. If you want to hear that story directly from the management team, you should watch the recording of the recent Unlock the Stock event featuring the company:

We now have results for Q1’24 and the highlight here is that the company has reported an operating profit. That might sound ridiculous, but there are many nuances to this story. The swing into profitability is a result of cost reduction initiatives in the Consumer business and the contribution from the Connect business that was recently acquired.

Unfortunately, there’s still a very big difference between operating profit ($228k) and the net loss attributable to Lesaka ($5.6 million). The net interest charge of $4.5 million is the biggest driver of that difference, up sharply from $3.6 million in the comparable quarter.

Having reminded you that the overall Lesaka platform is still sub-scale, let’s dig into the segments. The Merchant division (which includes Connect) reported revenue of $121.4 million, up 24% year-on-year. EBITDA margin is 6.6%, which is a structurally low margin because of the way that airtime sales are reported. In the Consumer division, revenue was $15.6 million and adjusted EBITDA margin was 15.9% vs. a loss last year.

Another important point to highlight is that the net loss of $5.6 million includes $5.9 million worth of depreciation and amortisation and $1.8 million in stock-based compensation. This is why cash from operating activities is actually a positive $3.3 million, with a total decrease in cash of $3.6 million in this quarter that takes the cash and cash equivalents balance to $55 million.

The balance sheet will also be helped by the specific repurchase of shares that Finbond is currently busy with, as Lesaka will sell its stake in Finbond back to that company for R64.2 million.

Lesaka sits firmly in the growth stock bucket, requiring you to take a long-term view on financial inclusion and fintech in the township economy in South Africa.

MiX Telematics has published first half results (JSE: MIX)

The results for the first six months of the year look pretty good

MiX Telematics reports quarterly because of the US listing. To make life more complicated, the company reports quarterly numbers under US GAAP and then six-monthly numbers under IFRS, which is the type of reporting that South African investors are accustomed to.

I’ll focus on the interim results reported using IFRS. Total revenue is up 13% in constant currency and subscription revenue is up by the same percentage, with the acquisition of Field Service Management having contributed 490 basis points worth of growth.

But despite revenue of R1.38 billion, profit for the period is only R38 million. These aren’t exactly juicy margins, are they? To be fair, this includes forex losses of R15.9 million and a R10 million charge from the income tax effect of net foreign exchange losses. Even with those adjustments, it’s not a high margin business.

Adjusted EBITDA increased 58% year-on-year to R343 million, with margin up 580 basis points to 24.8%.

It’s good to see that free cash flow of R45 million isn’t terribly different to profit for the period. Cash generated from operations was R270 million, so the business is quite cash hungry in terms of capital expenditure. Of the R224.8 million in capital expenditure in this period, R173.2 million was attributed to in-vehicle devices.

The company recently announced a proposed merger with Powerfleet, which would create a significantly larger business with benefits of scale and an expanded investor base on the Nasdaq. It’s early days for that transaction, as shareholders will need to be convinced of the benefits.

Little Bites:

With the announcement of the merger with 1Life and the broader relationship with Telesure, it’s not great news that the Clientele (JSE: CLI) group CFO is resigning with immediate effect after 11 years with the business. His replacement on an interim basis is Tiffany-Ann Boesch, the former CFO of PPS.

Ascendis Health (JSE: ASC) renewed the cautionary announcement related to the potential take-private by a consortium led by ACN Capital IHC, an entity owned and controlled by Carl Neethling. Discussions are still in progress and it’s quite possible that no deal will take place here, which is why shareholders are advised to exercise caution.

Conduit Capital (JSE: CND) has renewed its cautionary announcement related to the liquidation order against CICL (the main subsidiary in the group) and the impact that this will have on the financial results for the year ended June 2022.

The next time you feel like your personal admin is falling behind, just remember that Go Life International (JSE: GLI) is holding its AGMs for the years 2018 – 2023 on the same day in November!

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Bell Equipment is still growing earnings strongly (JSE: BEL)

This stock has been a great lesson in the importance of valuations, up 44% this year

As a cyclical business with significant operations in South Africa, you don’t need to be much of a business expert to point out some of the risks for Bell Equipment. The good news is that the valuation is so dirt cheap that the excavators feel compelled to try and move it around.

In a trading statement dealing with the year ending December 2023, Bell expects to report HEPS of at least 750 cents. We are weeks away from the end of this period, so that’s a very big show of faith. I also want to give credit to the company for this level of disclosure, as this is the way a trading statement is supposed to be used.

This implies an increase of at least 59% in HEPS, with stronger market demand and a high level of execution by the company in response to that demand.

The share price is R21.85, so the Price/Earnings multiple is not even 3x.

MiX Telematics reports a major year-on-year profit swing (JSE: MIX)

Remember, these results should be read against the backdrop of the potential Powerfleet transaction

MiX Telematics has been busy lately. The proposed merger with Powerfleet was announced in October 2023, with the hope of creating an Internet of Things (IoT) scale player.

Of course, financial reporting requirements don’t just fall away because a deal is underway. The company has released a trading statement dealing with the six months to September 2023, reflecting a return to profitability.

After reporting a headline loss per share of 0.5 cents for the comparable period, HEPS for this period is 7 cents. That’s a very big swing, achieved through a combination of higher revenue and better margins as a result, along with a lower effective tax rate because of the impact of foreign exchange movements on intercompany loan funding.

The share price closed 9.3% higher on a day that was bright red for the JSE.

Has MTN settled in the R90s? (JSE: MTN)

The release of group results didn’t seem to have much impact

For the past week or so, we’ve been digesting the updates from MTN’s African subsidiaries. In most cases, they weren’t great this quarter. Inflation has been hitting those markets hard.

The group results have now been released, kicking off with a reminder that MTN has 290 million customers in 19 markets. The big dream is to turn those customers into fintech payments customers, creating a monster of a financial services business along the way. Execution of that idea isn’t so easy, of course.

Group revenue increased 9% as reported or 14.2% in constant currency. Voice revenue grew 4.3% in constant currency and data revenue was up 23.1% on the same basis. Interestingly, fintech revenue was slightly slower at 22.1% growth (again in constant currency). This is despite a 33.9% increase in fintech transaction volumes.

Group EBITDA before once-offs fell by 13.8% as reported. It increased 6.2% in constant currency, which shows you how severe the currency impact has been. As the share price shows, the market has focused on reported results rather than constant currency performance.

Over the nine months year-to-date, EBITDA fell 2.8% as reported or grew 11.2% in constant currency. Regardless of which of those metrics you use, EBITDA margin has contracted.

The share price got down to R90 before turning up and landing at R95. Here’s a one-year chart:

I must caution that if it breaks below the R90s, it’s entirely plausible that it gets to the R70s before sentiment changes.

What will improve things for MTN? Certainly a drop in inflation in the various African countries will help, along with a weaker dollar. If we are at the top of the hiking cycle in the US, then that should lend some support to a recovery.

It’s also important to understand that South Africa is far from being an exciting story for MTN. Total service revenue increased just 4.1% year-on-year in this quarter, which is better than Q1 and Q2 but still well below inflation. There’s also some sequential improvement in EBITDA margin since the beginning of the year. Overall though, we are a slow growth market. People like MTN because of the Africa story, hence why the recent macroeconomic deterioration has hit the price so hard.

Interestingly, mobile data is now 47.9% of MTN SA’s service revenue.

Finally, I think it’s good news that holding company leverage was still at 1.5x, in line with the June number. The group balance sheet is always a worry as upstreaming cash from the African subsidiaries is difficult.

Omnia expects HEPS to drop (JSE: OMN)

It seems like chemicals businesses are struggling across the board

There are a number of JSE-listed companies that play in the chemicals sector, or at least they have certain segments that do. From what I’ve seen recently, chemicals groups are struggling in general at the moment (there are exceptions of course). Omnia can add its name to the list, with an expected drop in HEPS.

For the six months ended September, the group expects HEPS to have dropped by between 12% and 2%, which means a range of 260 cents to 289 cents for the interim period. For reference, the share price is R57.00.

The pressure was felt more in the agriculture segment than the mining segment, although the commentary in the announcement is incredibly positive for a company that is telling shareholders that earnings are down.

Just read this excerpt and decide for yourself whether it makes sense in the context of these numbers:

“The Group delivered a resilient operational performance with strong sales volumes, market share growth and robust margins. Solid progress was made in the Group’s international expansion efforts, in particular the Mining segment which contributed to profit ahead of expectations. A focus on costs, prudent capital expenditure and stringent working capital management enabled the Group to maintain a robust financial position with a positive net cash balance of approximately R1.6 billion. Omnia continues to maintain a strong balance sheet which allows it to retain optionality in line with its disciplined capital allocation framework.”

There isn’t much in there to explain the drop in HEPS.

Sirius has concluded the sale in Germany and acquisition in the UK (JSE: SRE)

The Sirius model is based on active management of properties

Sirius has been making a real song and dance about the disposal of a property in Germany on a yield of 5.7% and the acquisition of three assets in North London on a yield of 7.3%.

Remember, the yield and the price are inversely related. Selling at 5.7% and buying at 7.3% effectively means selling high and buying low, which is obviously a good approach when recycling capital.

The disposal in Germany was 6% above book value, which also gives the reported net asset value per share some support.

Active asset management is a big part of the promise that Sirius makes to shareholders. The company believes that the newly acquired UK properties should generate a running yield of 10% at maturity, with a current occupancy rate of just under 70%.

The Sirius share price is up 21.7% this year, though it remains miles off the pandemic peaks when people were willing to pay a very silly premium to NAV for Sirius. This share price chart looks more like a tech stock than a property group:

Little Bites:

Director dealings:

Des de Beer was clearly feeling flush for this latest trade, with a purchase of R10.7 million worth of shares in Lighthouse Properties (JSE: LTE).

Here’s one worth paying attention to: Christo Wiese has bought R654k worth of shares in Collins Property Group (JSE: CPP) and an associate of the Collins family bought shares worth R5.9 million.

The company secretary of Growthpoint (JSE: GRT) has sold shares worth R520k. Although these are linked to share schemes, the announcement doesn’t say that this is purely to cover the tax, so it’s a sale in my books.

A senior executive at Pan African Resources (JSE: PAN) has bought shares worth R25k.

STADIO Holdings (JSE: SDO) has appointed Ishak Kula as CFO. He joins from Bud Group, which is a large private company involved in various industrial verticals.

Eastern Platinum (JSE: EPS) has obtained approval from the South African Competition Commission for Ka An Development Co to acquire shares in the company as part of the rights offering announced back in May. The approval is subject to the establishment of a 5% employee share ownership programme in Barplats Mines within six months of Barplats attaining a steady state of certain run of mine tonnages for a period of six consecutive months.

AYO Technology (JSE: AYO) has renewed the cautionary announcement related to the ongoing discussions with the JSE around the settlement agreement with the GEPF and PIC. The point here is that the terms need to comply with JSE Listings Requirements.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Accelerate confirms the terms of the proposed sale of Eden Meander (JSE: APF)

Shareholders will be asked to vote on this transaction

Accelerate Property Fund (JSE: APF) is in my bucket of property funds that I wouldn’t invest in. There have been some strategies followed by the company that have ruled it out for my own money. The share price is down 20% this year and down more than 80% over five years.

As part of an effort to improve the balance sheet, Accelerate identified Eden Meander for a potential disposal to the Sasol Pension Fund and a couple of other investors. This was first announced in August 2023. After a successful due diligence, terms have now been announced to the market.

The property is being sold for just over R530 million, so this is a Category 1 transaction under JSE rules that will result in a detailed circular being sent to shareholders as a precursor to a shareholder vote. Keep an eye out for further announcements in this regard if you are a shareholder.

The announcement irritatingly doesn’t indicate the book value of the property as at the last reporting date. I trawled through the reporting to find it. As at 31 March 2023, the fair value of Eden Meander was disclosed as R522 million. With a sale achieved slightly above book value, I genuinely don’t know why they didn’t highlight this fact in the announcement.

AECI grows group revenue and EBIT by 10% for the nine months to September (JSE: AFE)

But the German business is going from bad to worse

If you’ve been following AECI, you’ll know that AECI Schirm Germany has been a headache. Within group EBIT (not a typo – this is Earnings Before Interest and Taxes) of R1.895 billion for the nine months to September, we find the German business with a loss of R230 million.

Despite this knock, revenue and EBIT both increased by 10% thanks to solid mining explosives sales volumes, a weaker rand and generally improved profitability thanks to new contracts. AECI Mining is the biggest part of the business and grew revenue by 15% and EBIT by 30%.

There were also negatives in places other than the German business, like AECI Agri Health with EBIT down 23% and AECI Chemicals down 18%.

The balance sheet has been well contained, with net working capital down 3% despite the growth in revenue. This is a great example of using creditors to fund debtors and inventory. Also, capital expenditure was 4% lower at just over R1 billion. But due to debt in AECI Schirm and of course higher interest rates overall, net finance costs jumped by 92% to R425 million.

There is still decent coverage here of EBIT to finance costs, but the trajectory isn’t good.

Will things get better in Germany? Despite a turnaround plan that was showing promise, trading conditions have deteriorated even further and AECI isn’t expecting a short-term recovery.

If you would like to dig deeper into this company and review the capital markets day presentation, you’ll find it here.

enX posts strong earnings from continuing operations (JSE: ENX)

The HEPS story looks very different if all operations are included, but this isn’t the most useful view

enX Group operates businesses that produce and market oil lubricants and greases, design and diesel generators, distribute industrial engines, offer cleaner power solutions and import and distribute plastics and speciality chemicals. They are even involved in conveyor belting fabric.

In other words, enX is firmly an industrials play, which has been a better choice this year than being in a consumer vertical. Not all industrial models have worked well though, as Eqstra Fleet Management is being sold by the group for strategic reasons.

Focusing on continuing operations for the year ended August, revenue increased 26% thanks to demand for power solutions and related services, along with the various other products offered by enX. Operating profit is up 31%, despite once-offs in the base period and the current period. HEPS from continuing operations increased by 16%.

Within continuing operations, I have to highlight New Way Power as a major winner in load shedding. Revenue jumped 72% and profit before tax shot up from R10 million to R101 million. That’s what happens when a business suddenly achieves scale, helped by the entry into the provision of solar PV systems back in 2021.

HEPS from total operations is down 38%, but this isn’t because of a poor performance by Eqstra. Instead, it’s because of discontinued operations in the base period that weren’t in this period. enX has been through a period of significant restructuring, so focusing on HEPS from continuing operations is sensible.

After closing some major asset disposals in the past couple of years and paying substantial distributions along the way, there is still excess capital on the balance sheet. enX has declared a special distribution of R1.00 per enX share. The group has been structuring recent distributions as a reduction of capital rather than a dividend for tax purposes.

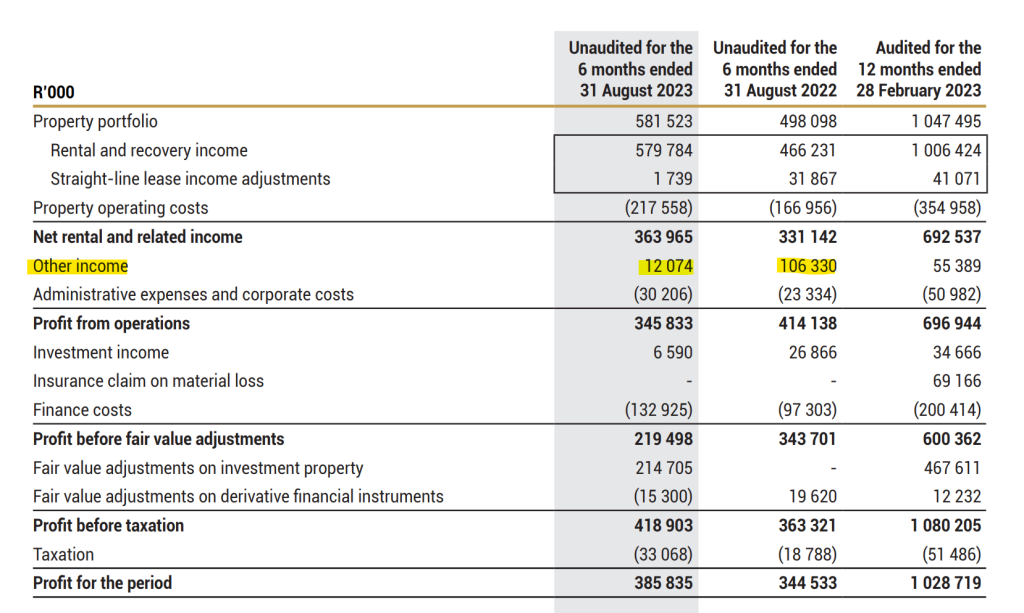

Exemplar REITail reports a 6.5% drop in the dividend (JSE: EXP)

A large insurance claim in the base period has skewed the results

Whenever you are assessing the financial performance of a company, you need to scan the numbers for anything unusual. Here’s a perfect example from Exemplar REITail:

Net rental and related income has moved higher, which is good. The next line your eyes should’ve moved to (in the absence of highlights) is profit from operations, which shows a big negative move. The “other income” line is clearly where the negative shift happens. If you read the notes to other income, you find that R69 million in insurance proceeds were recognised in the base period. Although it doesn’t explain the entire move, it goes a long way towards doing so.

Why isn’t this insurance claim on the line that is literally called “insurance claim on material loss”? Well, if you look in the final column, you’ll see that it was classified there for the full year reporting.

I don’t make the accounting rules. I just try hard to navigate around their weirdness at times.

You may also want to take note of the big jump in finance costs from R97 million to R133 million. This issue is plaguing property funds at the moment, as leverage is a huge part of the business model.

Investors care most about the dividend (down 6.47%) and the net asset value per share (up 13.81% to R14.34). The share price closed at R10.10.

Hyprop achieved the R500 million target for the dividend reinvestment programme (JSE: HYP)

In fact, the reinvestment alternative was oversubscribed

Real Estate Investment Trusts (or REITs) try to find ways to retain equity capital. This is because the REIT rules mean they are always on a treadmill, having to distribute most of their profits to shareholders.

One of the ways to retain capital is a dividend reinvestment programme, which in some respects works like a miniature rights offer. Hyprop has used this with great success in the past and has done it again, retaining R500 million in equity capital through shareholders electing to reinvest at R24 per share. For reference, the current price is R26.76, with the discount used to encourage this election.

Holders of 68.5% of shares chose the reinvestment alternative, which would’ve meant retention of R730.6 million were it not for the self-imposed R500 million limit. This means that each shareholder who elected this alternative will reinvest a pro-rata amount.

MTN Rwanda is moving firmly in the wrong direction (JSE: MTN)

Even East Africa, once a hotbed of potential, isn’t safe from these conditions

MTN Nigeria could win a game “bad things happening to me” bingo

MTN Ghana is growing, but below inflation (only just)

MTN Uganda is doing really well, with earnings growth way ahead of low inflation in the country

This brings us neatly to MTN Rwanda, which is an unfortunate story. EBITDA could only limp 4.7% higher, with EBITDA margin unwinding by 390 basis points to 44.9%. Capital expenditure increased by 11.5%, so pressure on the balance sheet (a feature of telecommunications businesses) is clear to see.

Thanks to the muted EBITDA performance and a sharp increase in net finance costs, profit after tax fell by 25.2%.

The inflation rate is 17.2%, so I think we can all agree that negative real growth is particularly worrying here. As we are seeing elsewhere in the business, another worry is US dollar-denominated expenses, with the company trying desperately to stay ahead of the curve when earning local currency.

MTN Group got down to R90 before turning higher to R97. Let’s see what the share price does when group results come out, as the market usually does a fairly poor job of watching the African results as a pre-cursor to the group performance.

NAV growth and a dividend at Redefine (JSE: RDF)

And perhaps most importantly, a more positive outlook

Redefine is a typical example of a large local REIT with a diversified portfolio. In these conditions, that isn’t necessarily a good thing. Being a focused REIT with a small portfolio does have its perks.

To give you an idea of the spread, 65% of Gross Lettable Area (GLA) is in Gauteng, 14% is in the Western Cape, 6% is in KZN and 8% is spread across the rest of South Africa. The remaining 7% is international.

There’s significant exposure to office property, with R22.2 billion worth of office property out of a total property portfolio of R78.8 billion.

Despite the broad exposure and numerous challenges in the property sector at the moment, the SA REIT GLA vacancy rate improved from 6.8% for the year ended August 2022 to 6.6% for the year ended August 2023.

Loan to value has moved higher, from 40.7% in 2022 to 42% in 2023. Including foreign currency debt and derivatives, the cost of debt has increased by 110 basis points to 7.1%. For those who haven’t had experience with balance sheet structuring and yield curves in different countries, you’ll find it interesting to compare the ZAR cost of debt (8.7%) to the EUR (2.6%) and USD (5.3%) denominated loans.

Focusing on the returns to shareholders this year, the dividend was 1.9% higher at 43.80 cents and the NAV per share has increased by 6.4% to R7.6596. The share price is R3.59, so Redefine is trading on a yield of around 12.2%.

In the outlook section, Redefine has some optimism that the property cycle has bottomed out. The guidance for distributable income for FY24 is between 48.0 and 52.0 cents vs. 51.53 cents in FY23. In other words, sideways or slightly down is still the expectation for the next 12 months, but the worst seems to be behind the sector.

Sibanye strikes a wage deal at Kroondal (JSE: SSW)

The average increase over five years is 6.4% per annum

Sibanye-Stillwater has been having an incredibly tough year thanks to plummeting PGM prices and inflationary pressures in costs. This has driven a need for some restructuring and retrenchment activities at certain mines, which perhaps sends a signal to the unions across the group.

The Kroondal PGM wage negotiation has been concluded without any disruptions. AMCU and the NUM have agreed to a five-year deal with inflation-linked increases similar to those agreed at Rustenburg and Marikana during 2022.

The average increase over the five-year period is 6.4% per annum.

Little Bites:

Director dealings:

Here’s an interesting one: the CEO of Capitec (JSE: CPI), Gerrie Fourie, has sold shares worth R11.5 million.

A director of a major subsidiary of Super Group (JSE: SPG) sold all the shares that vested under a share appreciation rights scheme, coming in at R1.95 million. Where an executive sells all the shares rather than enough to cover just the tax, that’s a genuine sale in my books.

Speaking of sales related to share awards, the selling by Truworths (JSE: TRU) executives continues. The company secretary has sold R1.4 million worth of shares, with part of the reason being a rebalancing of his investment portfolio.

Des de Beer has bought R1.4 million worth of shares in Lighthouse Properties (JSE: LTE)

A director of a major subsidiary of Bell Equipment (JSE: BEL) has bought shares worth R99k.

Go Life International (JSE: GLI), one of the most obscure companies on the JSE, is changing its name to Numeral Limited provided shareholders approve the change.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

This year, Unlock the Stock is delivered to you in proud association with A2X, a stock exchange playing an integral part in the progression of the South African marketplace. To find out more, visit the A2X website.

In the 28th edition of Unlock the Stock, we welcomed Bell Equipment and Calgro M3 to the platform for the first time. The management team gave a presentation on the performance and strategy and took numerous questions from attendees.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions. Watch the recording here:

Mention the name “Craig Warriner” at your next gathering of friends, and you’ll be able to identify the BHI burn victims by the looks on their faces.

While former-insurance-salesman-turned-investment-messiah Warriner whiles away the hours in his specially-requested private jail cell, hoodwinked investors are coming to terms with the fact that they may never see their money again.

Sequestrator Cawood Attorneys is currently picking over the R4.78 million that remains in the BHI account (a shadow of the estimated R3 billion that Warriner lifted from investor pockets). Meanwhile, BHI trustees are considering an application to the high court to have the trust declared a ponzi scheme.

None of this is news to anyone who’s read a financial publication in the last week or so. As South Africans, we aren’t strangers to the concept of ponzi schemes either, what with the ghosts of Mirror Trading International, Krion and Africrypt still looming large in the corners of many a courtroom (editor’s note: not all ghosts are good for you). Which leads us to the same question we always seem to ask when a new ponzi scheme makes the news cycle: how does something like this happen?

What Kool-Aid and cults have in common

If you’ve found yourself in conversations on the subject of BHI recently, you may have encountered or even used the term “drinking the Kool-Aid”. While the product itself may not have made its way onto South African shores (the closest comparison we have locally would probably be something like Drink-o-Pop sachets), our exposure to American-made films and series means that this particular phrase has wormed its way into our lexicon nonetheless.

The meaning is clear though: when someone is “drinking the Kool-Aid”, they are committing to a possibly doomed or dangerous idea because of perceived potential high rewards. In case you’re wondering how such a bleak concept became associated with a sugary children’s drink, I’m happy to inform you – but be warned that the backstory is particularly macabre.

On November 18, 1978, roughly 918 people members of the People’s Temple cult – back then referred to as the People’s Temple Full Gospel Church – committed suicide by drinking cyanide-laced cooldrink at their compound in Guyana. Newspapers picking up the story reported that the compound was strewn with the empty Kool-Aid packets that had been used to create the deadly cocktail. Factually, this was incorrect – cult members had actually used a cheaper knock-off product called Flavor Aid – but that didn’t stop the image of those empty Kool-Aid packets from burning itself into the public subconscious.

Cult members performed what they believed to be “revolutionary suicide” at the instruction of their leader, Jim Jones, who founded Jonestown as a refuge from the perceived threat of fascism in America. The incident became widely known as the Jonestown Massacre.

Personality equals power

To understand how modern-day investors are able to fall into the trap of ponzi schemers, it actually helps to think about Jim Jones. Ask yourself: how did one man convince almost 1000 Americans to not only give him all of their income and assets, but to sell their houses, break ties with their families, quit their jobs and move to a jungle compound in South America?

The answer is the same as it is with many cult leaders: he had a powerfully magnetic personality that drew people to him. Charming on the surface, yet dominant enough to silence those who would try to speak up against him. And he wielded that personality like a superpower, drawing in people from all walks of life until the size of his following alone was enough to start magnetising new recruits.

Does that sound familiar?

Victims of Craig Warriner’s scheme often refer to the fact that he made extensive use of his St Stithians College old boys’ network, and appears to have made multiple donations to the school. By paying above-average commission fees (as high as 5%) to brokers, Warriner created the illusion of a man who was not only very wealthy but magnanimous in his wealth. All he wanted to do was help other people get wealthy. And that carefully constructed facade is all it took to reel in the money.

As much as we hate to admit it, we humans are herd animals. When enough of us start to move in one direction, the rest will start to lift their heads and wonder where we went. If you need clear evidence of this, consider that it is a well-established and studied fact that individual investors will follow the advice of their coworkers, even when the advice given contains no value-pertinent information. We value the advice and recommendations of those around us far more than we trust our own research and – in many cases – our own common sense.

So, what can we take from this article and apply when the Next Big Opportunity comes along?

Beware the charming leader who requires blind obedience. Real genius doesn’t hide its methods. If you’re being persuaded to “just trust” someone, that’s reason enough to do the opposite.

Consider your sources, and then consider them again. Be aware of your own tendency to believe the people around you simply because they are friends or family members. Look past the person making the recommendation and examine the facts in the cold light of day.

Don’t believe the hype. There’s no such thing as an investment that only delivers returns. If you can’t find a trace of a market dip ever, or if the promised returns seem too high to be true, then there’s reason to be cautious.

Remember: if investing was easy, we’d all be living in mansions. As much as you want to believe that there is a shortcut or an undiscovered path to the returns of your dreams, the chances of that being true are not worth risking your hard-earned cash on.

And if you’re currently feeling the BHI burn – my sympathies, friend. Hindsight is frustratingly perfect, isn’t it?

About the author:

Dominique Olivier is a fine arts graduate who recently learnt what HEPS means.Although she’s really enjoying learning about the markets, she still doesn’t regret studying art instead.

She brings her love of storytelling and trivia to Ghost Mail, with The Finance Ghost adding a sprinkling of investment knowledge to her work.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

| Investec | Lesaka Technologies | MiX Telematics)")

")

")