Nobody can accuse Walmart of leaving the market in suspense. After tongues were set wagging by news of a potential offer, the American retail giant has now made a firm commitment at R62 per share.

Note from The Finance Ghost:

The deal has been structured as a scheme of arrangement with a standby general offer that kicks in if the scheme fails. This is interesting, as it means that Walmart is willing to increase its stake in Massmart even if it can’t reach a 100% shareholding and delist the company.

There is significant investment required for Massmart to achieve a turnaround in fortunes. The impact on short-term profitability is likely to be negative, so Walmart is making a significant commitment here. Understandably, that is easier in a private company rather than in the public eye.

PwC is acting as independent expert and has concluded on a preliminary basis that the terms are fair and reasonable.

Full details will be included in the offer circular that is expected to be posted on or about 23 September 2022.

It didn’t take long for Walmart to move from a “potential offer” for Massmart to a firm intention announcement. The deal has been structured as a scheme of arrangement with a standby general offer that kicks in if the scheme fails. This is interesting, as it means that Walmart is willing to increase its stake in Massmart even if it can’t reach a 100% shareholding and delist the company. It’s worth highlighting that if a standby general offer is accepted by 90% of holders, there is provision in the Companies Act to allow Walmart to force the remaining holders to accept the offer. This would be a very weird outcome though, as shareholders would’ve needed to vote down the scheme and then accept the offer in order to create this position, which doesn’t make sense. The announcement notes that Massmart is going to need significant investment in the short-term and that turnaround measures will impact profitability, so my view is that Walmart wants to do this away from the public eye. The scheme consideration and general offer price are both R62 per share, a substantial premium of 68.7% to the 30-day volume weighted average price (VWAP). PwC is acting as independent expert and has concluded on a preliminary basis that the terms are fair and reasonable. One of the conditions to the scheme is that any appraisal rights exercised won’t exceed 5% of ordinary shares. The s164 opportunists in the market may find it tough to make money here, as justifying a higher value for Massmart than R62 per share is going to be extremely difficult based on recent results. In my view, we have a better chance of being Cricket World Cup champions than seeing the share price reach those levels in the absence of this offer. PwC seems to agree.

A chapter has been closed – Barclays PLC no longer holds any shares in Absa. Barclays agreed to sell its remaining 7.44% stake in Absa through an accelerated bookbuild at a price of R169 per share. That’s 4.6% below the current price of R177 per share.

All the way back in November 2020, Pan African Resources announced the acquisition of Mintails, a gold group where the holding company was placed into provisional liquidation in 2018. A definitive feasibility study concluded that the project has compelling economics and a significant impact for the group, with the potential to increase production by 25% through constructing a world-class tailings retreatment operation. The due diligence is in its final stages and the deadline has been extended from 31 August to 30 September.

Mahube Infrastructure is in the process of restructuring and recapitalising its business and has released an important circular. If you are a shareholder, make sure you read it here.

Financial updates

Impala Platinum has released results for the year ended June 2022. It’s been an unhappy time in the PGM sector, with rand revenue per 6E ounce down by 4%. This issue is made a lot worse by lower volumes (also down 4%) and a 17% increase in unit costs per 6E ounce. The safety performance also worsened, with seven fatalities at managed operations – this simply isn’t acceptable. Headline earnings per share (HEPS) fell by 17%. The balance sheet is strong at least, with R26.5 billion in net cash at the end of the period. Free cash flow was R28.8 billion (vs. R38.3 billion in the prior year), net of capital investment of R9.1 billion. The total dividend for the year is 1,575 cents per share, down 28.4% from the prior year. In terms of outlook, the palladium and rhodium markets are expected to remain tight (which is supportive of price) whereas the platinum prospects “remain muted” in the near term. The share price is down more than 23% this year.

African Rainbow Minerals has released results for the year ended June 2022. HEPS has fallen from R66.88 to R57.87, a drop of 13.5%. Despite this, the final dividend is identical to last year at R20 per share, bringing the full year dividend to R32 per share (vs. R30 last year). The coal business was firmly the highlight, swinging from a headline loss of R250 million to headline earnings of R928 million. This is the smallest part of the group though (contributing 8% of earnings), so it couldn’t save a situation where the much larger ferrous and PGM businesses saw earnings drop by 16% and 34% respectively. Net cash improved by R2.97 billion to R11.18 billion. Operationally, the group has concluded the acquisition of the Bokoni Platinum Mine and will now focus on finalising a definitive feasibility study. Development capital of R5.3 billion is expected over three years to ramp up the mine to steady-state production.

Santam has released its interim financial results for the six months to June 2022. Although gross written premium grew by a healthy 23%, the impact of the floods etc. drove a 53% decrease in HEPS. Of gross claims paid of R14.2 billion, R4.4 billion was attributable to the KZN floods. The group targets a net underwriting margin of 5% to 10% and could only manage 2.3% in this period. Despite the pressure, the interim dividend of 462 cents per share is 7% higher than the prior year.

Sanlam has released a trading statement for the six months ended June 2022. The general insurance business has been suffering, driving a decrease in group HEPS of between 2% and 12%. The life insurance business put in good numbers thanks to lower mortality claims as Covid calmed down. The investment management business achieved higher asset-based income. The credit and structuring business enjoyed lower bad debt charges and higher net interest income. General insurance was hit by the floods in South Africa (with a severe impact on Santam) and lower investment return on insurance funds in Morocco. At group level, the lower equity markets over the period and higher project costs contributed to the decrease in earnings.

Fortress REIT released a trading statement that significantly reduces the forecast distributable earnings for FY23. As the property fund is likely to lose its REIT status, it will now pay tax on its profits (an estimated charge of R350 million in FY23). I must point out that shareholders will pay dividend tax rather than income tax on distributions (i.e. a much lower tax rate as the company will pay some of the tax), so the biggest impact is on pension funds and institutional shareholders that are tax-exempt. They now experience genuine tax leakage, which is why I can’t see them sticking around on the shareholder register. The company’s assumption is that it will lose REIT status on 31 October and that retained cash will be used to reduce debt. Losing REIT status gives the fund a lot more balance sheet flexibility. It would be a spectacularly ironic outcome if everyone looks back five years from now and figures out that REIT status did more harm than good! The fund also released its results for the year ended June 2022, showing a 0.6% increase in NAV per share across the aggregate number of FFA and FFB shares in issue. The loan-to-value ratio has increased from 36.7% to 40% over the past year. Vacancies have reduced from 7.4% to 5.4%.

Truworths has released results for the 53 weeks ended 3 July 2022. The group includes “pro forma” numbers which are on a comparable 52-week basis. As a reminder, retailers who report on a 52-week calendar would have a 53-week period every few years. This obviously limits comparability, so the group reports two sets of numbers to help investors. On that comparable basis, retail sales were up 6.6% and HEPS increased by 42.4%. The group managed to expand its gross margin to 53.5%. Cash generated from operations was R3.9 billion and the group used R1.6 billion for share buybacks. Net debt to equity is only 9.2%. The dividend per share is up 44% to 505 cents, of which 205 cents is the final dividend. After a strong recent rally based on the release of a trading statement, the price of R57.74 equates to a dividend yield of 8.7%. Truworths has underperformed for a long time, so the market treats it as a low-growth stock that needs to provide the bulk of the return as a dividend. Depending on your view on its growth prospects, this is either an opportunity or a value trap.

Insimbi Industrial Holdings has released a trading statement for the six months ended August 2022. HEPS is expected to be at least 20% than the comparable period, which is the minimum disclosure required by the JSE to trigger the release of a trading statement. It often happens that the actual increase is a lot higher, though one cannot assume that this is always the case.

Sasfin announced that GCR has affirmed its national scale rating of long-term BBB+(ZA) and short-term A2(ZA), with the outlook improved from negative to stable. This is some relief after a week of terrible PR for Sasfin related to a Daily Maverick investigation on smuggled illegal cigarette funds.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Operational updates

Montauk Renewables has announced the planned construction of a second renewable natural gas processing facility at its Apex landfill gas project in Amsterdam, Ohio. This would increase processing capacity by an estimated 40%. The project is expected to be completed in 2024, with the key driver being forecasted biogas feedstock volumes from the host landfill. The expected capital investment is between $25 million – $30 million over the next 12 to 18 months.

Share buybacks and dividends

It seems that South32 has returned to daily share buybacks, so at least British American Tobacco doesn’t need to feel lonely in its ongoing buybacks.

Glencore has repurchased another £18.2 million worth of shares as part of the buyback programme that will run until February 2023.

Notable shuffling of (expensive) chairs

Altron has appointed a new CEO to replace Mteto Nyati. The new man in the seat is Werner Kapp, who spent 22 years at Dimension Data including a role as CEO of Middle East and Africa. Kapp will take over from 1 October 2022.

The CFO of Huge Group has resigned with effect from 1 September 2022. Yes, that is precisely zero days notice. Why, you ask? I don’t know, but it probably isn’t for good reasons. Either the relationship soured or the company disclosure sucks because the resignation happened a while ago. In the meantime, the Financial Manager at Huge Management (Peter Boyce) will take over as Interim CFO.

Texton has changed its company secretary from one consulting entity to another. As a reminder, a company is allowed to appoint a juristic entity (i.e. a company) as its company secretary.

Director dealings

Prepare yourself to feel poor. Bob van Dijk exercised Naspers share options awarded back in March 2014 and had to sell some to cover the taxes. The sales come to nearly R1.3 billion – that is not a typo! I would like to remind you that this was only a portion of the total options exercised. The total value was over R2 billion. For perspective, that’s the same as Aveng’s market cap!

Directors of Sibanye-Stillwater have bought more shares. CEO Neal Froneman was good for $285k, the Chief Organisational Growth Officer (and his associate) tossed R4.5 million into shares and the Chief Sustainability Officer invested over R992k on the local market and over $46k into Sibanye ADRs in the US. The share price has taken a lot of pain this year and a show of faith from the management team goes a long way towards easing investor concerns.

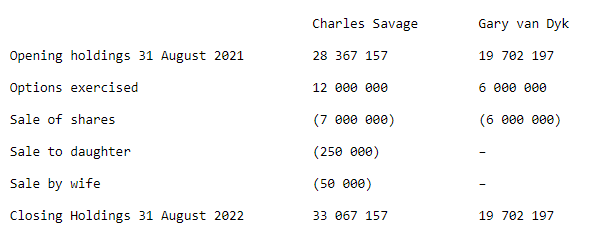

Purple Group announced a sale of shares by Charles Savage as well as the CFO, Gary van Dyk. The group knew that the market would panic on this news, so Purple provided a table showing the movement in their respective holdings this year. The point is that Charles has been a net buyer of shares and Gary is flat:

The CEO of Tradehold (and his wife) have exercised an option to sell shares to Christo Wiese at net asset value per share, which is considerably higher than the current share price. They have exercised this option to the value of over R9.8 million.

A non-executive director of Astral Foods has acquired shares in the company worth R250k.

Unusual things

After 27.14% of the votes were cast against a non-binding advisory vote related to the remuneration policy, Gemfields has invited shareholders to attend a call on 13th September to “express their views” – i.e. complain to the manager.

Majority shareholder Walmart has released details of a firm intention offer to acquire the remaining 47.22% stake in Massmart in a deal worth c.R6,4 billion. The offer of R62 per share represents a premium of 68.7% to the 30-day volume weighted average price as at closing share price on August 26, 2022. Should the scheme not become operative, a standby conditional offer would take effect.

Huge Group has announced a series of agreements for the acquisition of the Interfile Group, a software company which develops and licences its own software. Huge will acquire a 30% stake from the Msemu Investment Trust for R30 million and a 14% stake from Aloecap Private Equity for R14 million. The company is also finalising the acquisition of Gurb Investments’ 25% stake and the founder’s 6%. As part of the transaction Interfile will bring on board a new BEE partner in YW Capital (also acting as transactional adviser to the deal). The management team will hold 5%. Further information in respect of these transactions will be released in due course.

Grindrod Shipping has warned shareholders it is in discussions with LSE-listed Taylor Maritime Investment in relation to a non-binding proposal to acquire the entire issued share capital of the company. The tender offer is for a consideration of US$26 per share representing a cash price of $21 per share in conjunction with a special cash dividend of $5 per share.

Master Drilling Mining Services (MDMS), a subsidiary of Master Drilling, has exercised a call option to acquire a further stake in the A&R Group. In July last year MDMS acquired a 25% stake in the engineering group providing mining solutions, training and products for R78,6 million. MDMS latest acquisition at an estimated cost of R129,4 million will increase its stake in the A&R Group to just above 51%. The purchase price is capped at a maximum of R240,1 million.

Zeder Financial Services, a subsidiary of Zeder Investments, is to dispose of Zeder Africa to ForAfrica Forestry for a disposal consideration of R160 million. Zedar Africa has as its sole asset a 55.62% stake in Agrivision Africa, whose principal activity is the production and milling of agricultural grain produce in Zambia.

Cognition is proposing to sell its 50.01% stake in Private Property to BetterHome Group, ooba and Fledge Capital in a deal worth R150 million. The rational for the sale is the belief that Private Property may benefit from a more industry-aligned shareholder base with the ability to accelerate the growth of its revised strategy.

The April 2022 acquisition by Afristrat Investment of Crosscorn from SATF for a purchase consideration of US$5 million, has been cancelled by mutual consent. The reason for the termination of the deal is that given Afristrat’s recent suspension on the JSE, it is no longer able to issue the shares to satisfy the equity component of the purchase price.

Unlisted Companies

Africa Bank, as the successful bidder, has acquired the majority of financial services provider Ubank’s disclosed assets and liabilities. Ubank has a presence in the mining sector and a distribution footprint that compliments African Bank’s existing national offering and feeds into its push to diversify funding sources. The parties have agreed on a total cash consideration payable of up to R80 million.

Nyanza Light Metals, a manufacturer of titanium dioxide pigment and other co-products, has received an initial US$3 million investment from Lagos-headquartered Africa Finance Corporation which will go towards the completion of its plant in Richards Bay Industrial Development Zone – taking the US$550 million project to financial close in H1 2023.

Barclays plc is to undertake an accelerated bookbuild to dispose of its remaining 7.44% stake (63,072,652 shares) in Absa Group. The shares will be placed at R169 per share for a total consideration of R10,66 billion. Following the sale, Barclays will no longer own any ordinary shares in the Absa Group.

Rebosis Property Fund has entered business rescue following the failure of its turn-around strategy to strengthen the Group’s balance sheet. The group announcement lists restricted timeframes, the impact of a rising interest rate cycle and the delay of rental payments by government departments and municipalities as reasons for the vulnerable financial position it now finds itself.

Altvest Capital which listed on the Cape Town Stock Exchange in May this year has taken a secondary listing on A2X with effect from September 6, 2022. MAS plc indicated this week that it too was aiming to take a secondary listing on the A2X alternative exchange with further details to be provided in due course.

Tsogo Sun Hotels has received confirmation of its name change from the Companies and Intellectual Property Commission. Shares under the name Southern Sun will trade from September 7, 2022.

A number of companies announced the repurchase of shares

Super Group has repurchased 25,025,919 shares in the open market at an average share price of R29.63 per repurchase share. The shares were repurchased between May and August, excluding the closed period, for a total value of R741,5 million. Following the repurchase, the group holds 12,61 million shares as treasury shares representing 3,47% of the shares in issue.

Glencore this week repurchased 7,420,000 shares for a total consideration of £35,8 million. The share purchases form part of the second part of the Company’s existing buy-back programme which is expected to be completed over the period from August 4, 2022 to February 14, 2023.

South32 has restarted its repurchase programme and this week repurchased 990,346 shares at an aggregate cost of A$4,11 million.

Prosus continued with its open-ended share repurchase programme. This week the company announced that during the period 22nd to 26th August 2022, a total of 3,234,455 Prosus shares were acquired for an aggregate €208,14 million.

British American Tobacco repurchased a further 690,602 shares this week for a total of £23,9 million. Following the purchase of these shares, the company holds 207,154, 782 of its shares in Treasury.

Three companies issued profit warnings. The companies were: Trellidor, Mustek and Fortress REIT.

Six companies this week issued or withdrew cautionary notices. The companies were: PSV Holdings, Cognition, Tongaat Hulett, Huge, Grindrod Shipping and Conduit Capital.

Nigerian commercial entity Fidelity Bank has entered into a binding agreement to acquire Union Bank United Kingdom, representing Fidelity Bank’s first foray into international markets. The deal, of which no financial details were disclosed, remains subject to the approval of the UK’s Prudential Regulatory Authority.

Cairo-based private equity firm Ezdehar Management is to acquire a 60% stake in Egyptian grocery retail chain Zahran Market. The stake is to be acquired through its Mid-Cap Fund II for an undisclosed sum. Through the partnership, Zahran Market aims to solidify its position locally and to expand its footprint to the underserved regions of the country.

EFG Hermes’ lifestyle-enabling fintech arm, valU, has acquired Paynas, the Egyptian HR and payroll platform. The transaction furthers valU’s strategy to grow the business and enhance its tech power, increasing its footprint to reach Paynas’ large and growing base of SMMEs.

Africa-focused investment company Tana Africa Capital, together with Sango Capital, a South African investment management firm, has made a minority investment in Sundry Markets, a Nigerian grocery retailer operating through the ‘market square’ brand.

Pezesha, a Kenyan pan-African fintech offering B2B digital lending infrastructure with a focus on providing affordable working capital to financially excluded SMEs, has raised US$11 million in a pre-series A round. The investment, a mix of equity and debt, will be used to scale operations in core markets within the East African region and expand into West Africa. The funding round was led by Women’s World Banking Partners II.

Anchor, the Nigerian banking-as-a-service startup providing the interface, dashboards and tools to help developers embed and build banking products, has raised c.US$1 million in a pre-seed round. Investors included Byld Ventures, Y Combinator, Luno Expeditions, Niche Capital among others. The funding will be used to scale the business.

Egyptian cloud-based subscription management platform SubsBase has closed a seed round of US$2,4 million. The round was led by Global Ventures with participation from HALA Ventures, P1 Ventures, Plus Venture Capital, Plug and Play, Ingressive Capital and Camel Ventures together with several existing investors. Funds will be used to develop SubsBase’s global and regional integration capabilities and build its educational content and business development support for recurring revenue-based businesses.

Edtech startup OBM, Egypt’s education startup, has raised a six-digit figure from EdVentures in a second round of investment. Funds will be used for expansion and the launch of its new application ‘Taleb’.

Grey, a Nigerian-based fintech startup enabling cross-border payments, has raised US$2 million in seed funding in a round supported by Y Combinator, Soma Capital and Heirloom Fund among others.

Omnibiz, a Nigerian retail-tech startup, has raised US$15 million (in debt and equity) in a pre-series A round led by Timon Capital with participation from Ventures Platform, LoftyInc Capital Management, Chapel Hill Denham and others. The funding will be used to accelerate retailer growth and retention.

WamiAgro, a Ghanaian agritech startup, has received c.US$227,000 from impact investment fund Wangara Green Ventures. The investment will be used to offer training, provide input loans and provide access to markets by small-hold farmers across the grains value chains.

For private equity firms in Africa, achieving successful exits is now more important than ever. Why now? Fundraising for PE firms in Africa and across numerous emerging markets has been particularly tough over the last three to five years. While the investment and exit volumes and values for PE rose to all-time highs globally, this was not necessarily the case in Africa.

PE firms have not been under as much pressure to put new capital to work and, in other instances, may not have had capital available for new investments. What capital was available may have been set aside to further invest into existing portfolio companies, whether to make bolt-on investments or to weather the ‘storm’ caused by the impact of COVID-19. PE firms in Africa were and have rightly been more focused on creating value in their existing portfolio companies and getting them ready for an exit.

The economic environment became tougher towards the end of Q1 2022 when compared with Q1 2021, due to the Ukraine-Russia war and the rise in interest rates in developed markets, to levels not seen for many years or even decades. Given this uncertainty, the few possible IPOs being considered have been placed on ‘pause’, waiting for an IPO window to open. The level of interest of trade buyers from developed markets has also reduced, with international PE firms more cautious on the deployment of capital. As noted earlier, local PE buyers have limited ‘dry powder’. For these reasons, the buyer universe is, in our view, more challenging than in 2021, and preparation for an exit is thus more critical than it has probably ever been. PE firms in Africa need to show more successful exits to demonstrate their abilities in value creation, and show a track record of healthy returns to raise capital for new funds.

What exactly is ‘‘Exit Readiness’’ and how can this be best done in these ever-changing times?

The good news is the ‘Exit Readiness’ process has not changed. Rather, it is the environment around it that has changed. Because the environment is so different, PE firms need to re-examine the full range of assumptions around the portfolio companies that they are looking to prepare for exit. We view ‘Exit Readiness’ through five main topics.

Who are the most likely buyers?

Ideally, one should identify five most likely buyers for the portfolio company. Those thought to be the most likely buyers pre-COVID could quite easily be different post-COVID. PE firms need to rerun their buyer screenings to identify those with both the appetite and firepower to pursue a deal. PE firms should create a bespoke series of equity stories that make sense for each buyer, or buyer type, and approach the exit process with increased flexibility and creativity.

What is the equity story?

The current market uncertainties have resulted in an increased dependency on data-driven decision making. PE firms should consider re-writing the equity stories within the current environment, and that expected in the near to medium term. Sellers should consider preparing scenario planning to reassure buyers that they’ve thought through all the potential scenarios and summarised this into a well-developed forecast and plan that provides a clear picture of what is expected to happen, albeit with the flexibility to adjust as required.

Information needs and buyer questions

Identify all the information requirements of all potential ideal buyers. What are the likely key questions that these buyers would have? Information and data required for an exit process can be time consuming to prepare and collect. Periodically refreshing documents will reduce the ‘heavy lift’ required once an exit process is launched. Having a ‘permanent’ virtual data room (VDR) will enable the company to run ad-hoc and confidential exit enquiries. Leading VDR providers have also developed best-in-class lists of information required per sector, transaction type, et cetera, which could be valuable. Clear and simple tracker tools will ensure visibility of progress and accountability for closing information gaps.

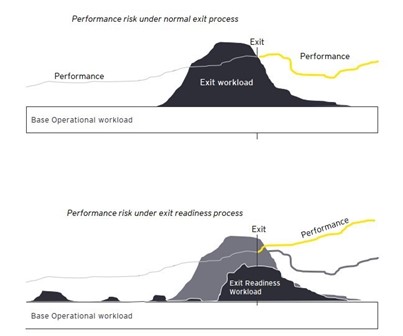

Timetable for preparation

‘Exit Readiness’ will enable the preparation of a detailed exit plan starting from c. 18 months before an actual exit occurs. Importantly, it also reduces the risk of the significant workload required for an exit process negatively impacting the normal day-to-day responsibilities of the management team and distracting them from executing on their operational agenda and strategies. Below is a picture illustrating the performance risk under a normal exit process versus that including an ‘Exit Readiness’ process.

Alignment of stakeholders

‘Exit Readiness’ enables all key stakeholders to become aligned and ready to undertake the exit process. We refer to this alignment as the diamond with four key stakeholders for which alignment is critical. These four stakeholders are the sellers (PE and other shareholders), the management team, advisors and the buyers.

Our annual divestment study shows these aspects of exit preparation make the biggest difference to value:

Identification and “fixing” of key risk areas. Tactics to deal with open or closing out of value eroding issues.

An exit strategy to address the equity cases for each of the most likely buyers.

Evidenced forecasts supported by operational plans and consistent KPIs – at the level of detail required to make them credible to buyers.

Planning for the right due diligence to support operational, commercial and tax/legal/regulatory aspects of your plans – so you get value for them.

EY support through ‘Exit Readiness’ helps you make choices, plan and prioritise, to ensure that business as usual continues alongside the exit.

Three final messages to make your ‘Exit Readiness’ a hugely valuable process:

Prepare for a sale before you need a buyer

Take a buyer’s point of view

Prepare, prepare – and prepare some more

Graham Stokoe is an Africa Strategy and Transactions Partner and Africa Private Capital Leader | EY

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication

The growing importance of Environmental, Social and Governance (ESG) matters to stakeholders necessitates a co-ordinated approach to managing and reporting these issues to the board, which could justify appointing a dedicated ESG Manager.

Companies’ boards of directors should be fully aware by now that (i) investors are increasingly looking to invest in companies that are better positioned on ESG issues, (ii) lenders are becoming increasingly aware of the potential impact of significant ESG risks on the creditworthiness of businesses, and (iii) shareholders, customers and civil society are increasingly pushing the ESG agenda. Therefore, it follows that a negative response to the effect that a company’s operations have on ESG will impact the relationship which that company will have with its stakeholders.

Stakeholders now expect company boards to be more conscious of, and report in increasing detail on, how they are fulfilling their ESG responsibilities. This has also become a regulatory issue. In February 2022, the EU published a proposed Directive on Corporate Sustainability Due Diligence (EU Directive), which will apply not only to companies operating in the EU, but also to non-EU companies active in the EU that meet certain criteria, including South African subsidiaries.

The EU Directive requires companies to integrate the implementation of the due diligence policy into the corporate strategy, the compliance of which must be overseen and monitored by the board. Furthermore, the EU Directive provides that, when fulfilling their duty to act in the best interests of the company, directors must consider the consequences of their decisions on sustainability matters. To ensure that executives deliver on strategic ESG objectives, some companies are now looking at introducing ESG KPIs aligned to executive compensation.

However, the practicalities of data collection, data analysis and reporting, including what needs to be reported on, how much detail is required, and who is responsible for co-ordinating ESG compliance in an organisation, still contains many grey areas. Recommendations such as the recently launched JSE Sustainability Disclosure Guidance, GRI Sustainability Reporting Standards, and the Taskforce on Climate-related Financial Disclosures’ recommendations provide general guidelines on disclosure and reporting (much of it on climate change commitments). But to ensure that they are meeting their responsibilities, boards need a practical checklist to track ESG performance and evaluate the ESG impacts of their company’s operation against the set strategic goals.

Who is responsible for reporting to the board on ESG?

This is a critical question. Some companies have an ESG manager who reports to the Social and Ethics Committee and/or an ESG and Sustainability Committee on various ESG aspects. In other companies, different areas of responsibility are reported separately; for example, issues to do with gender and race are reported to the Social and Ethics Committee by the Human Resources Manager; ethics/ procurement by the Procurement Manager; and diversity/inclusion by the Transformation Executive. Alternatively, responsibilities such as the monitoring and reporting of specific ESG-related risks, such as the supply chain risks and ESG and sustainability reporting, is delegated to a different board committee, such as the Audit and Risk Committee.

The lack of integration and a siloed approach to these issues is not ideal. In some international companies, a Chief Sustainability Officer (CSO) with executive seniority has been appointed, and South African companies may follow this trend. In a recent report, the Institute of International Finance and Deloitte surveyed over 70 financial services companies to determine the role of the CSO as a co-ordinator of ESG within the company. In the report, it was found that companies who have given the CSO strong executive support and a broad strategic mandate derive more benefits because of the greater integration of ESG matters and the ability to deliver ESG commitments in a coherent manner for commercial gain.

Covering all three – E, S and G

Initially, much of the focus has been on how companies measure and report on their goals to reduce emissions of greenhouse gases. This has broadened, with companies now reporting on other environmental issues, such as water consumption, and effluent and air emissions.

Equally detailed measurement and reporting is increasingly required for social aspects, which should include not only interaction with employees and surrounding communities about health and safety, but also transformation and training goals. This extends to ethics, including how the company procures goods and puts measures in place to prevent or address corruption. Similarly, governance reporting is expected to move beyond listing who attended board meetings and how much they earn, to demonstrating what difference the leadership of the company has made, how independent it is, and how it has demonstrated its ethical stance. In so doing, it demonstrates its commitment to ensure that the negative impact of the company’s operations in respect of ESG factors is reduced.

How do directors know that they have fully discharged their ESG responsibilities?

The starting point is to set specific strategic goals, either as a percentage (e.g. 30% of top management to be female by 2025) or measured from a base year (e.g. to reduce 2019’s levels of water usage by 30% by 2025), and to introduce short-term and long-term goals in order to monitor the progress and stress test the achievement of the set strategic goals.

To provide effective oversight, the directors need to understand the consequences of their decisions on sustainability. They must fully under-stand what the risks are, and the challenges in meeting these set targets, and closely monitor the progress, including identifying specific issues that are blocking progress. In this regard, companies will have to upskill their directors by employing a variety of methods, such as providing specialised board training for the directors on ESG matters and/or appointing directors with ESG expertise. In addition, the directors must understand their various stakeholders’ interests on specific ESG issues, as stakeholders are increasingly demanding answers from directors on these issues. Even if company policy is that directors should not respond to any questions on matters related to the company, in certain circumstances, directors may be at risk if they do not speak out. Directors must be made aware that they may be required to speak on certain topical ESG issues in relation to the company’s operations or, at the very least, explain the company’s ESG strategic goals, and should be provided with relevant holding statements on these goals.

The ESG Manager or the CSO may be tasked with ensuring that the relevant and useful ESG information is provided to the directors and included in the company’s integrated report, to give it prominence alongside financial reporting. Such a functionary would be instrumental in ensuring that relevant and useful ESG information collected across the various departments is provided to the directors or the relevant board committees in a co-ordinated fashion. This person will be able to assist the board in interpreting the issues raised, pressure test the goals, and monitor the progress in achieving them.

Nomsa Mbere and Safiyya Patel are Partners | Webber Wentzel

This article first appeared in DealMakers, SA’s quarterly M&A publication

The team from TreasuryONE takes a look at the market environment ahead of the release of non-farm payrolls on Friday.

In the last couple of days, we have seen a flight to safety again as the US dollar came charging out the blocks after the hawkish statement from Fed Chair Jerome Powell at Jackson Hole on Friday. Although the speech was only a matter of minutes, some of the key takeaways from the speech were that the Fed will focus on data but that there is no pivot in sight.

The market took this as a very hawkish signal, and we have seen the US dollar trading below parity against the Euro with only brief moments of the dollar trading above parity. This is in stark contrast to the previous time that the US dollar broke below parity, where the snapback was swift and sudden.

Refer to the below EUR/USD graph, with the momentum well against euro strength currently:

The flight to the US dollar was evident as commodities like gold, normally associated with a safe haven play, were also sold off in the wake of Fed Chair Powell’s speech. It seems that the old adage: “buy dollars, wear diamonds” is certainly true for now.

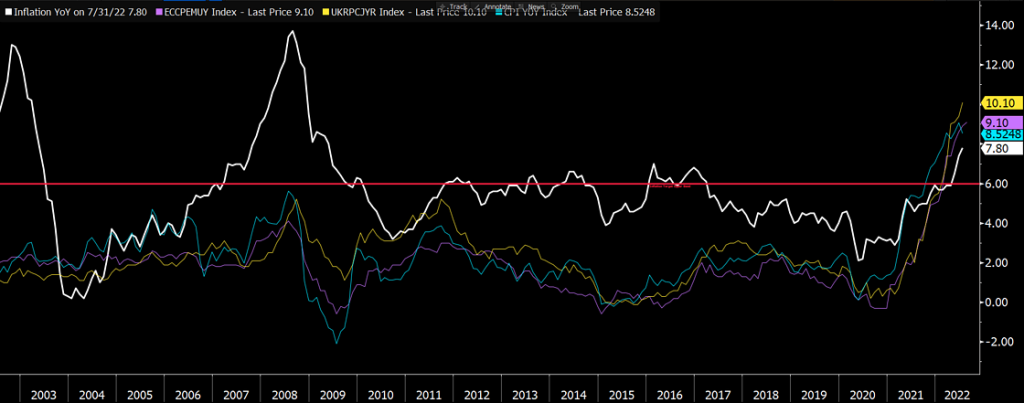

The Eurozone will come under renewed pressure in the short term, especially in relation to the energy crisis that is gaining speed as winter approaches. With energy consumption costs soaring, and with inflation printing higher at 9.1% vs 9.0% expected, we could see the euro under pressure.

The below graph shows the Eurozone inflation (in purple) versus some peer countries. We can also see South Africa’s inflation (in white) still below the US, Eurozone and the UK.

With the Fed still taking centre stage, we expect a lot of volatility around the non-farm payroll number out on Friday, with markets waiting anxiously for the number. We expect the US dollar to remain on its firming path should the number exceed expectations. Should the number miss expectations, we could see a bit of a relief rally in EM currencies in the short term.

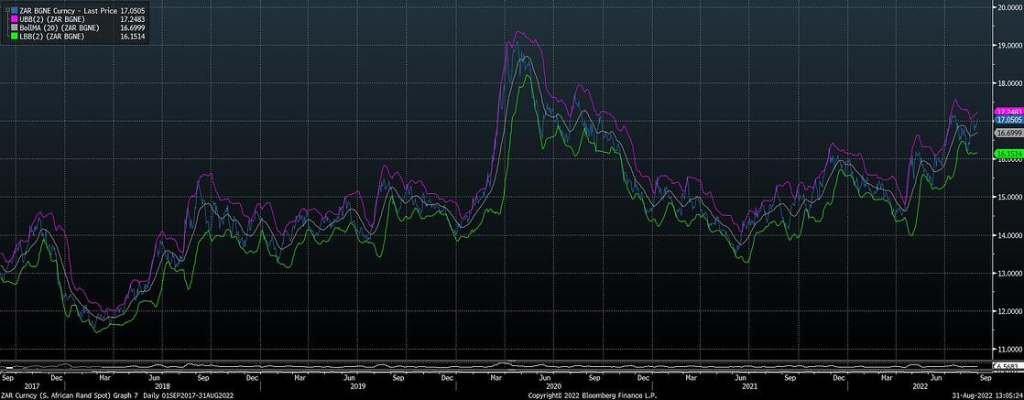

Speaking of EM currencies, the rand has broken above R 17.00 in the wake of the flight to the US dollar and could be under more pressure should we have a positive US non-farm number. In the past few trading sessions, the rand has followed the US dollar, which will influence any rand moves in the short term.

See below the current USDZAR chart, the rand still comfortably within the R17.30 to R16.50 range.

Huge Group has announced the acquisition of Interfile Group, a solid business with 80% of its revenue earned on an annuity basis. The group offers operational and hosting services, transactional services (bill presentment, SMS, email and payment), call centre services, consulting services and maintenance services. At its core though, Interfile is a software company that implements business process solutions for clients including government departments, municipalities and private sector organisations. The claim to fame is that Interfile built the eFiling system for SARS in 2003. Over the last five years, Interfile has paid dividends of over R65 million. There are synergies with certain Huge Group companies like Glovent Solutions. YW Capital, an equity advisory and investment house, will be coming on board as the new empowerment partner. YW Capital has an investment portfolio that exceeds R450 million. Huge will acquire 30% from Msemu Investment Trust for R30 million and 14% from Aloecap for R14 million. An agreement is being finalised with Gurb for a further 25% and with the founder of the business for 6%. Ultimately YW Capital will hold 25% in the business and the executive management team will hold 5%. This values the group at around R100 million vs. 2022 profit after tax of R27.3 million, so that’s an attractive deal for Huge at a Price/Earnings multiple of less than 4x! It’s certainly a…huge step forward from the Adapt IT debacle.

Altron is in the process of selling Altron Document Solutions to Bi-Africa Investment Holdings. One of the conditions is an approval from the Zimbabwe Competition and Tariff Commission. In a surprise to absolutely nobody, the deal is being delayed because that approval is outstanding. The deadline for fulfilment of conditions has been extended from 31 August 2022 to 28 February 2023.

Although it didn’t come out on SENS, Barclays Plc announced on the LSE that it will be selling its remaining 7.4% shareholding in Absa through an accelerated bookbuild. This means that institutional investors will be approach to take up the stock. The bank is doing well at the moment, so there should be solid demand.

Tradehold shareholders have approved the disposal of its interest in Moorgarth Holdings to Moorgarth Group Holdings for £102.5 million.

Yet another executive of SilverBridge Holdings has accepted the offer from ROX Equity Partners of R2.00 per share. The closing date for the offer is 23 September.

Afristrat’s problems just seem to be going from bad to worse. With the shares suspended from trading on the JSE, the company can’t go ahead with acquiring a distressed loan asset pool of $5 million in exchange for the issuance of shares. The deal is off.

Financial updates

Woolworths released results for the 52 weeks ended 26 June 2022. It’s an unusual one, as the Fashion Beauty Home (FBH) segment has a good story to tell year-on-year and the Food segment reported a decline in profits. The group level result is a combination of South Africa and Australia where lockdowns were terrible for the first half of the year, so group turnover growth of 1.7% isn’t a very helpful metric. The more useful number is 4.9% growth in the second half of the year. The market definitely noticed the balance sheet recovery, with Woolworths moving from net borrowings of R1.1 billion to net cash of R229 million. This was achieved through a strong working capital performance, capex discipline and cash received from all underlying subsidiaries including David Jones. This supported a whopping 247.7% increase in the dividend. Looking deeper, FBG grew full year turnover by 5.4% despite trading space declining by 4.5%, so Woolworths is focused on trading density (sales per square metre). Gross profit margin in this business expanded by 210 basis points to 47.6% and operating margin moved from 8.4% to 11.9%. In Food, sales were up 4.2% and price movement was below inflation, reflecting price investment by Woolworths. Gross profit fell by 50 basis points due to growth in online sales, supply chain costs and price investment. Full year profit fell by 3.9% with an operating margin of 7.3%. In Australia, the focus is on the second half of the year where David Jones grow turnover by 2.6% and Country Road Group grew by 9%. The share price closed 4.8% higher on a day when the market was very jittery, so that’s a solid outcome.

Discovery released a trading statement for the year ended June 2022. The group talks about a “pivot to growth” and that was reflected in headline earnings growth of between 70% and 80%, although core new business annual premium income only increased by 6%. The huge increase in profit was in Discovery Life as the pandemic gently fell away, with the most impressive core business growth in Discovery Health with 20% and VitalityHealth with 27%. Discovery Insure was severely impacted by adverse weather and recorded a loss. Pressure in the Chinese investment market drove a reduction in profitability at Ping An Health Insurance. Discovery Bank put in a “strong performance” although very few details are given. Full year results will be released on 7th September and will be very interesting. The share price has fallen 15% this year.

Murray & Roberts has released results for the year ended June 2022. Revenue increased by 36.5% to R29.9 billion and EBIT was over 30% higher at R705 million. The order book is slightly lower year-on-year but “near orders” (which the company describes as having more than a 95% chance of being secured) skyrocketed from R11.1 billion to R60.4 billion. Although continuing HEPS jumped from 16 cents to 58 cents, net debt is higher (R1.1 billion vs. R0.7 billion) and there is no dividend. The Energy, Resources & Infrastructure platform boasts by far the largest order book in the group. In stark contrast, the Power, Industrial & Water platform remains loss-making. Overall, the company is happy with the group order book and notes that operating margin is expected to improve from FY24.

Trellidor released an updated trading statement for the year ended June 2022. The previous update was released on 6 July and noted that due to the Labour Court judgement and related provision of R32.1 million, HEPS would be down by at least 50% vs. the prior year. There were plenty of other challenges in this period, leading to a 1% drop in turnover and a reduction in trading margin due to raw material and freight inflation. The company notes that steel prices increased by more than 80% in the past two years and that supply chain constraints have persisted. The original trading statement didn’t tell the full story, as HEPS is expected to drop by at least 95% and may even slip into the red. HEPS in the comparable period was 40.80 cents and the Labour Court judgement is a 24.9 cents per share impact, so the rest is attributable to the far more worrying operational issues that aren’t about to disappear. It’s never nice to see a company taking such a tough knock.

Aspen released its results for the year ended June 2022 and the market approved, with the share price nearly 6% higher in late afternoon trade. This is a classic example of grinding out a great profit performance despite tepid revenue growth (just 2%). Normalised EBITDA from continuing operations was up 11% and HEPS from total operations increased by 31%. The dividend is 24% higher at 326 cents per share. Make sure you read the operational update further down in Ghost Bites that deals with the news of a ten-year vaccine deal with Serum Institute of India.

Motus released results for the year ended June 2022 and fell 4.4% on the day, so that’s not ideal. The amount of leverage in this result is something to behold, with revenue only up 5% and HEPS up by 72%. Here’s an interesting one though: free cash flow from operations actually declined by 18.1%. Despite pressures on cash flow from working capital requirements, the dividend is 71% higher at 710 cents per share (of which the interim dividend was 275 cents). Based on the closing price, Motus is trading on a dividend yield of 6%. Net debt to EBITDA is only 0.8x, so the balance sheet remains strong. South African vehicle sales have been better than predicted and Motus increased market share from 20.2% to 22.4%. Motus maintained market share in the UK despite sales in that market falling by 18.2%. Share was also maintained in the Australian market, which fell by 2.1%. For context, the SA operations contributed 66% of group revenue and 81% of group operating profit.

Cashbuild released results for the year ended 26 June 2022. Revenue fell by 12% (despite selling price inflation of 7.2%) and even the gross margin came under pressure, dropping from 26.9% to 26.3%. Thankfully, operating expenses also fell by 13%, so operating profit was down by 16% in a result that could’ve been a lot worse. HEPS is down by 33%. Of the 36 stores that were looted, 28 have reopened, 3 were permanently closed and 5 are in the process of being rebuilt or possibly closed. Trading conditions remain challenging, with revenue down 3% year-on-year in the six weeks subsequent to period end. A final dividend of 677 cents per share has been declared, taking the dividend for the year to 1,264 cents. After closing 8% lower at R226.99 per share, Cashbuild is trading on a trailing dividend yield of 5.6%.

Mustek released a trading statement for the year ended June 2022. The period ended in the worst way possible, after founder David Kan sadly passed away in May. HEPS is expected to be between 15% and 25% lower than in the comparable period, coming in at between 331.36 cents and 375.54 cents. For context, the 2019 result was HEPS of 139.32 cents, so Mustek is still running way ahead of pre-pandemic levels. The share price is up more than 80% over 3 years and is still in the green in 2022, a commendable performance.

Clientele Life has released results for the year ended June 2022 and has put in a solid performance, with the dividend 9% higher at 120 cents per share. This stock trades based on dividend yield, with a share price of just R11.50 (and thus a dividend yield of 10.4%). Everything is managed tightly, so insurance premiums up by 1% for the year aren’t an issue when operating expenses fell by 6%. HEPS increased by 12%, driven mainly by 15% increase in net profit in Clientele Life.

DRA Global has released results for the six months to June 2022. Revenue is down 16.2% and the company has swung into a loss. The net cash balance has fallen from A$118.4 million to A$72.5 million. Although there is no dividend, the company did manage to complete the share buyback programme. The core businesses in the EMEA and AMER regions are performing well, with APAC anticipated to become profitable in the second half of the financial year. Fixed-price contracts in the APAC region have been a major drag on profitability and their terminations are being commercial resolved. On a headline earnings level, the group recorded a small profit in this period, down 83%! The share price is down more than 40% this year.

Anglo American has announced the rough diamond sales value for the seventh sales cycle of 2022. It has come in at $630 million, slightly below $638 million in the sixth cycle. Usual seasonal trends mean that the next few cycles will be affected by the temporary closure of polishing factories for the Diwali holidays.

Randgold & Exploration Co Limited has released financials for the six months to June 2022. The numbers are a little pointless, as all the cash is sitting in investment funds and there has been significant expenditure on litigation. There are currently no operations.

African Bank has a CET1 ratio of 38%, which means that the bank is exceptionally well capitalised. It’s no wonder that this bank is on the acquisition trail, having risen from the ashes. This equity buffer is around three times higher than where banks usually operate.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Operational updates

In addition to the financial results dealt with above, Aspen announced a collaboration agreement to manufacture and make available four Aspen-branded vaccines for Africa. Before you panic and wonder why anyone cares about Covid vaccines anymore, you’ll be pleased to learn that these are routine vaccines (pneumococcal / rotavirus / polyvalent meningococcal / hexavalent) which means that people still want them. This is a ten-year agreement with Serum Institute of India, the world’s largest vaccine producer. Aspen will manufacture, market and distribute the Aspen-branded vaccines across most of the continent, excluding certain markets where parties already hold rights to these vaccines. With 99% of vaccines in Africa currently imported, Aspen anticipates receiving grant funding from the Bill & Melinda Gates Foundation and the Coalition for Epidemic Preparedness Innovations (CEPI) to support African regional manufacturing capacity.

Karooooo (the owner of Cartrack) is clearly excited about the milestone of 1,600,000 subscribers, releasing an announcement that this number has been reached. The results for the second quarter are in line with “management’s expectations” and results will be out on 12th October.

Delta Property Fund released a voluntary pre-close update for the six months ended 31 August 2022. The group has been focused on disposing of non-core assets, which are largely vacant. 26 assets have been earmarked for disposal with an aggregate value of R767 million. During the period, disposals worth R259.2 million were executed. The proceeds are used to reduce debt. The vacancy rate of 33.9% is enormous and will only improve to 32.1% based on the disposals already agreed (property transfers are underway). It gets worse the more you look, as month-to-month leases are 12.3% of the total. The disposal of the non-core holding in Grit Real Estate Income Group is also a priority. This disaster of a fund has lost 94% of its value over 5 years.

Rebosis Property Fund has announced that Phahlani Mkhombo and Jacques Du Toit have been appointed as the joint business rescue practitioners of the company. In reality, they are now in charge of the group.

Share buybacks and dividends

In the past few months (other than during closed period), Super Group repurchased shares worth R741.5 million. This represents 6.7% of issued share capital.

Glencore is also back at it, with a repurchase of around £17.65 million.

Notable shuffling of (expensive) chairs

Ms Dimakatso Quocha has joined the board of African Media Entertainment, bringing with her extensive experience in the ICT and broadcasting sector.

DRA Global has appointed Michael Sucher as CFO, having been the Acting CFO since May. He has been with DRA since 2021 and held previous roles at BHP and South32.

Director dealings

A prescribed officer of Harmony Gold sold R8.1 million in shares all the way back in MARCH and the company has only announced it now due to an “administrative oversight” – this attention to detail (i.e. lack thereof) might explain the recent financial performance.

A director of a subsidiary of Stefanutti Stocks has acquired shares in the company worth more than R91k.

A director of Equites Property Fund has pledged further shares as security for a loan from Investec. Many people don’t realise that directors in listed companies are often sitting with leveraged positions, especially in the property sector.

A director of a subsidiary of RFG Holdings has disposed of shares worth over R381k.

A director of a subsidiary of Renergen has sold shares worth nearly R175k.

A director of Redefine Properties has bought shares in the company worth around R1.29 million.

A prescribed officer of Adcorp has sold shares worth around R1.7k. I hope he doesn’t spend it all at once.

Mediclinic has published the circular related to the offer by Remgro and MSC Mediterranean Shipping Company, acting through Manta Bidco Limited. The independent Mediclinic directors consider the terms to be fair and reasonable, having taken advice from both Morgan Stanley and UBS (thereby racking up a bill that would make some medical specialists blush). You’ll find the scheme document at this link and all related documents at this link.

Mahube Infrastructure is in the process of restructuring and recapitalising its business. Shareholders are also being asked to approve the revised investment policy. The JSE has granted a dispensation for the rule to dispatch a circular within 60 days of the announcement. A circular will be issued to shareholders before 5 September 2022.

Financial updates

Conduit Capital’s journey to zero (or pretty close) continues, with the Prudential Authority lodging an application to the High Court to place Constantia Insurance Company Limited into liquidation, with a court date in September. This subsidiary represents 94.4% of the revenue of the consolidated group. With 200,000 shares bid and over 2.5 million shares offered, those stuck in the structure are trying to get out.

Harmony Gold fell by 11% after releasing results for the year to June 2022 that reflected the full extent of the pain. Although revenue increased by 2%, production profit fell by 20%. Operating cash flow decreased by 55%. Guidance for next year doesn’t look like much to get excited about, with production in a similar range to this year and all-in sustaining cost “below R900,000/kg” vs. R835,891/kg this year. The final dividend of 21 cents per share is a small consolation prize for a share price that has fallen more than 28% this year.

Master Drilling released interim results for the six months to June 2022. On a USD basis, revenue was up 34% and profit increased by 47.9%, so that’s a fantastic set of numbers. Headline earnings per share (HEPS) is measured in ZAR and was up 55.5%. The accounting earnings growth hasn’t fully translated into cash earnings growth, with net cash from operating activities only up by 19%. The committed order book is $242.7 million. To put that into perspective, revenue for this period was $96.5 million. Master Drilling doesn’t typically declare interim dividends and this period is no different. The share price is up more than 50% in the past 12 months as activity has picked up significantly in the mining sector. This is about as close to “shovels in the gold rush” as you can get.

STADIO Holdings (and yes, they insist on capital letters) released solid results for the six months to June 2022. When you’ve grown HEPS by 18%, you’re allowed to take the upper case route. That result has been driven by 11% growth in student numbers, which led to 13% revenue growth. It’s worth noting that STADIO negotiated the early settlement of the CA Connect acquisition (a runaway success) through issuing Milpark shares, thereby diluting its interest in Milpark from 87.2% to 68.5%. STADIO only pays annual dividends rather than interim dividends, so there’s no dividend for this period. Despite the world returning to normal, contact learning student numbers fell by 4% and distance learning increased by 14%, with distance learning now contributing 85% of the student base. Back in 2017, it was only 80%. STADIO has no debt and a cash balance of R167 million, so the group really is in a strong position. This is a classic case of a great story that has already been priced in, as the share price is down over 5% this year. In today’s edition of Bad Conclusions, we also note that STADIO’s students are learning less and eating more:

Old Mutual released results for the six months to June 2022 and the market hated them, sending the share price down over 6.5% by afternoon trade. That’s a little embarrassing when the first line of the announcement talks about a “strong set of results” – well, the market says otherwise. The words “more than offset” are also frequently used, mainly because the bad news tended to outweigh the good news. Net client cash flows fell by 27% and funds under management dropped by 7%. Value of new business fell by 4%. The highlight was probably Life APE sales, up 15%. Thanks to the pandemic mostly disappearing from our lives, results from operations increased by 87%. Adjusted headline earnings would’ve been up 19% if income from Nedbank was excluded from the prior period, as Old Mutual unbundled the stake in November 2021. That doesn’t seem terrible on an overall basis, but the market looked through the net result to the underlying performance and clearly had different expectations. The interim dividend of 25 cents per share (44% of adjusted headline earnings) is below the dividend policy (ordinary dividend cover of 1.5x to 2x of adjusted headline earnings over a financial year) and many in the market had hoped for more. The share price is down nearly 17% this year.

Kaap Agri has released a voluntary trading update for the ten months ended July 2021. The agriculture industry has been impacted by higher fertilizer and fuel costs due to the conflict in Ukraine, as well as logistical issues related to the floods. The Agri trade business achieved real growth of 16.6% vs. the prior period and the Retail trade business grew turnover by 1.6% excluding the acquisition of PEG Retail Holdings. Margins in both businesses have improved relative to the prior period. Kaap Agri notes “severe fuel volume decreases” in the broader industry based on high fuel prices, as consumers have been forced to reduce travel. The impact on Kaap Agri’s fuel business has been a reduction in volumes of only 2.8% (excluding PEG), which is good under the circumstances. As the PEG acquisition became effective on 1 July, only one month of its performance is included in the numbers for the 10 months ended July 2022. Those operations have exceeded expectations. Kaap Agri reports recurring HEPS as the most meaningful measure of profitability, with that measure expected to be between 15.3% and 21.3% higher in the year ended September 2022.

Super Group released results for the year ended June 2022. Revenue increased by 17% and EBITDA was up by a substantial 69.8%. In a rather unusual shape to the income statement, the impact on HEPS was lower than on EBITDA, with that metric up by 33.4%. Cash generated from operations was up by 38%, which is always an important line to consider. The dividend is 34% higher at 63 cents per share. The share price has lost more than 16% this year.

Transpaco has released results for the year ended June 2022. HEPS is 41% higher at 475.5 cents and the total dividend per share is 215 cents. This result was made possible by revenue growth of 12.5% and operating profit growth of 35.1%, with operating margin expanding from 79% to 9.6%. The Plastic division contributed 58% of group operating profit and grew operating profit by 31%, with the Paper and Board division contributing 31% of group operating profit and growing its profit by a meaty 44%. The rest of the operating profit came from properties and group services, in case you were doubting your maths. The share price is up 48.5% this year.

Brimstone Investment Corporation released results for the six months to June 2022. I only ever look at the intrinsic net asset value (INAV) per share, as this is an investment holding company and the consolidated results reflect the roll-up of underlying companies, which makes it difficult to draw meaningful conclusions. One such conclusion is that Brimstone continues to disappoint investors, with INAV per share down by 18.4% year-on-year. No interim dividend has been declared, so there is nothing to ease the burn for investors. The share price is flat this year and the bid-offer spread is even wider than the frowns on the faces of investors.

Lewis Group has been upgraded by Global Credit Ratings (GCR) from A(za) to A+(za) for its long-term rating. The short-term rating has been affirmed at A1(za) and the outlook is stable. GCR noted Lewis’ resilient performance through the pandemic and its strong operating margin that the rating agency expects to continue trending upwards. Despite many reasons to feel good about the business, the share price is flat year-to-date.

Equites Property Fund has also announced an update from GCR, affirming its existing ratings and revising its outlook to positive.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Operational updates

Southern Palladium presented at the 2022 Africa Down Under event and has made the presentation available online. It has useful information on the PGM value chain in South Africa and the drilling plans for the company. You can find it here.

MC Mining Limited has announced updates for its Makhado project, Vele Colliery and Greater Soutpansberg Projects. The company is facing a decision around whether to move the Vele coal processing plant and modify it at Makhado, or construct a bespoke coal processing plant at Makhado. At this stage, the most attractive project NPV (net present value) is to move the Vele plant to Makhado. The construction of a bespoke plant gives almost the same return and retains the optionality around the Vele asset. The company has initiated discussions with BOOT (build, own, operate, transfer) funders. Other exploration assets in Limpopo (like the Greater Soutpansberg Projects) are longer-term opportunities.

Share buybacks and dividends

Last week, Prosus repurchased shares with a total value of nearly $208 million.

Lighthouse Properties is offering shareholders a scrip dividend of 1.625 EUR cents per share or a cash distribution of 1.462 EUR cents per share (a 10% discount to the scrip option). A scrip dividend means that shareholders receive shares in the company instead of cash. Lighthouse is incentivising shareholders to take the scrip option, as this helps the fund retail cash.

Reinet shareholders have approved a dividend of €0.28 per share and the exchange rate for the conversion to rand will be announced on 6th September.

AngloGold Ashanti has appointed Ms Gillian Doran has the CFO with effect from 1 January 2023. Ms Doran is currently the CFO of Aluminium within the Rio Tinto Group, based in Montreal.

Mpact has appointed a new independent non-executive director, which is particularly important given the battle that the company is having with Caxton & CTP, an activist shareholder in the company. Alethea Conrad has been appointed to the board and brings 16 years of experience at Oceana Group.

The company secretary of Calgro M3 is stepping down and being replaced by Juba Statutory Services. This is the only official company role that can be filled by a legal entity (obviously with a suitably qualified person behind it) rather than a warm body.

Director dealings

The directors of Sibanye-Stillwater are buying the dip, with Neal Froneman himself picking up over $682k in shares. Admittedly, that is relatively small change for him, dwarfed even by the Chief Regional Officer: Americas buying $731k in shares. A non-executive director bought nearly R2m worth of shares on the local exchange.

The group CFO of Famous Brands doesn’t mess around when it comes to investment positions in the company. He has bought contracts for difference (a leveraged position) with exposure of nearly R1.05 million.

An associate of a director of NEPI Rockcastle has bought shares in the company worth over R3.7 million.

A director of a subsidiary of Stefanutti Stocks has bought shares worth nearly R184k.

A director of ISA Holdings increased his exposure to the company through a transaction further up in his personal investment holdings. In other words, there was no changing of hands of the shares in the listed company. The look-through exposure increased.

Unusual things

Tsogo Sun Hotels will trade under its new name, Southern Sun Limited, from 7th September.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

– Massmart | Implats | Truworths | Santam | Fortress")