If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Corporate finance corner (M&A / capital raises)

Prosus has announced the acquisition of the remaining 33.3% stake in iFood from Just Eat for €1.5 billion in cash. There’s a potential further payment of up to €300 million if the food delivery sector “re-rates” its multiples in the next 12 months. The announcement doesn’t indicate how this is calculated, but it basically protects the seller if the market recovers. The loss attributable to Just Eat was a meaty €62 million in the six months to June 2022. Grossed up for the shareholding, this implies that the group lost around €185 million in that period. You certainly need to place a lot of value on hopes and dreams to be investing in this stuff.

The latest company to annoy the Takeover Regulation Panel (TRP) is Emira Property Fund, although it appears to be a minor transgression. In mid-July, Emira announced a firm intention to make a general offer to the shareholders of Transcend Residential Property Fund. Marketing materials were subsequently released that included views that were not included in the firm intention announcement. The TRP directed Emira to remove these materials from social media. Takeover law is enshrined in the Companies Act and the TRP is one of our strongest regulators in South Africa. When a company is under offer, the regulations become critical.

Financial updates

Standard Bank announced results for the six months ended June 2022. It has been a wonderful time for the banks, with record headline earnings of R15.3 billion, up 33% on the prior period. Return on equity (ROE) improved from 12.9% to 15.3% (the target by 2025 is to reach 17% – 20%). Net asset value grew by 15% and there’s a tasty interim dividend of 515 cents per share, representing a payout ratio of 55%. Margin growth is very important and the banks measure this as either “positive jaws” or “negative jaws” – with the positive variant describing a scenario where income growth exceeds expense growth. In such a scenario, margin expands. Positive jaws in this period was 450 basis points, reflecting the difference between income growth and expense growth. Looking ahead, income growth for the rest of the year is expected to be strong (double digits in net interest income and single digits in non-interest revenue), with ongoing positive jaws and a credit loss ratio in the lower half of the through-the-cycle range of 70 to 100 basis points. The share price is up around 14.5% this year.

Aveng has released a trading statement for the year ended June 2022. Headline earnings per share (HEPS) is expected to fall by between 74% and 78%, with the company pointing out significant non-recurring gains of R868 million in the prior period. Headline earnings (vs. earnings) usually adjusts for such issues, but not all non-recurring items can be adjusted in HEPS. The company provides a view on normalised earnings per share in an attempt to show the true underlying performance of the business. Normalised basic earnings per share is expected to be between 76% and 92% higher than the comparable period. In cases like these, I tend to just focus on the actual HEPS range given and I ignore the percentage movements. HEPS was between 226 and 261 cents, so the Price/Earnings multiple is somewhere around 7x.

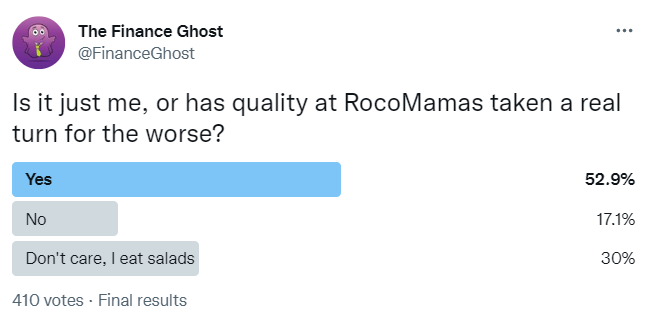

People with a taste for profits will be happy to learn that Spur’s HEPS for the year ended June 2022 increased by 31% to 144.22 cents. There is no debt on the balance sheet and the cash position is up by R29.8 million to R290.7 million. With 631 restaurants across 15 countries, Spur managed to grow solidly throughout the year with a fairly similar growth rate in the first half (H1) and second half (H2). A dividend of 78 cents per share has been declared and the share price closed at R21.50. Looking ahead, the group has flagged macroeconomic issues and rising inflation as concerns. I would perhaps argue that a more stressful country may push more parents to use Spur as Friday night childcare while sipping a cold ale! RocoMamas is where my concern lies, where sales were up 25.3% (vs. say 30.1% in Spur itself, or 31.4% in Panarottis). All these numbers look amazing of course, but remember the base period had Covid lockdowns. My recent experience at RocoMamas was disappointing and a poll I ran on Twitter suggests that I’m certainly not the only one feeling this way:

Afrimat will host a pre-close briefing session related to the interim results for the six months ending 31 August 2022. It will take place on 26 August and those who are keen to attend the virtual event should contact Keyter Rech Investor Solutions for details.

Operational updates

Purple Group (the controlling shareholder in EasyEquities with a 70% stake) has announced that EasyEquities has partnered with an e-wallet provider in the Asia Pacific region to launch investing services within that application. The user base is described as “tens of millions of users” which sounds like a very large market indeed. The launch is planned for September and the counterparty has asked to remain unnamed until the launch. Like a ghost, really.

Share buybacks and dividends

Much like those who smoke every day, British American Tobacco is still busy with share buybacks every day.

Karooooo has confirmed that the interim dividend is R10.053 per share and that it will be paid on 12th September.

Notable shuffling of (expensive) chairs

There was no shuffling on Friday.

Director dealings

A director of Thungela has acquired shares in the company worth nearly R100k.

A Dis-Chem director has sold shares in the company worth R24.6 million. That buys a few nice things.

Des de Beer continues to buy shares in Lighthouse Properties, this time with a R1.1 million purchase.

The interim CFO of AngloGold Ashanti exercised share options and promptly sold the whole lot, putting R382.5k in his pocket.

An executive director of Trematon has bought shares in the company worth R53k.

An entity related to the CEO of Industrials REIT sold shares worth just over £5.2 million. The proceeds will be used as partial repayment of a £6.5 million debt owed by the CEO’s related entity to a subsidiary of the REIT. The loans were made between 2015 and 2017 as part of a company share purchase plan. The balance of the loan will be repaid in the next seven working days. After this sale, the CEO will still hold around 4.55% of the issued share capital.

Unusual things

The Takeover Regulation Panel (TRP) is being kept very busy lately. Aside from the usual regulatory issues related to offers in the market, the TRP also deals with complaints and allegations of misconduct or breaches of takeover law. Complaints have been related to transactions involving a share repurchase in African Phoenix Investments, a general offer from Peresec Prime Brokers and Zarclear Holdings, a share repurchase by Zarclear, the mandatory offer in EnX Group and the scheme of arrangement involving African Phoenix and Zarclear. The complaints boil down to one thing: parties acting in concert and failing to disclose this. There are other elements to the complaint, like the independent expert not considering the potential liability of African Phoenix in respect of the Extract Group mandatory offer. The first decision for the Executive Director of the Panel is whether the complaints are “frivolous or vexatious” – in this case, the decision has been made that there is reasonable suspicion of an infringement and that this deserves a proper investigation. It’s important to note that no adverse findings have been made at this stage. All that has happened is the decision to take a closer look.

Raven Property Fund was set up to hold properties in Russia, which seemed like a good idea until war broke out. After needing to sell its stake in those properties, the listed vehicle will be disappearing from the JSE. It’s hardly a loss, as the share price chart looks like the company traded once in the past 3 years!

As we head into the back part of the year, we are seeing that data is getting more scrambled across the globe, which could only mean that volatility is going to be the rule rather than the exception. The team from TreasuryONE explains.

Last week, we saw US CPI coming in better than expected, with the number printing at 8.5%. Other data out of the US in the last couple of weeks also tended to beat expectations to the positive side.

While the number is still high, many analysts believe that the US has reached peak inflation and that the hawkish narrative by the Fed could be slowed down and that we are in line for a 50 basis point hike rather than the 75 basis point hikes that analysts in the market have punted. The immediate reaction to the number was for the US dollar to weaken, which was good news for EM currencies like the rand.

This all points to the narrative that there could be a soft landing in the US economy.

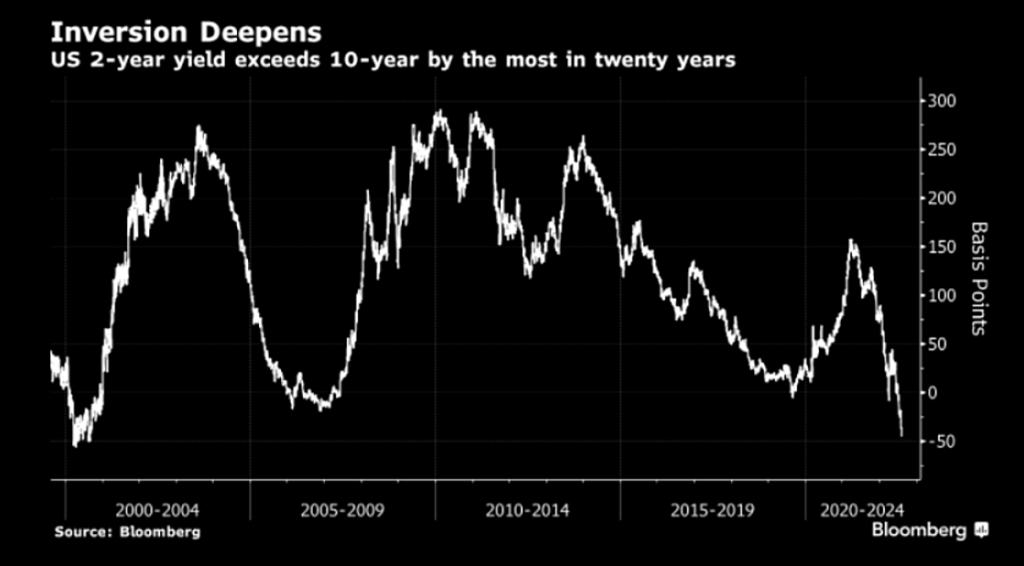

However, the story in the bond market is a little bit different. For a six-week period now, yield curves are inverted. Yield curve inversions, which are rare, are viewed as a good recession predictor because they suggest that investors believe – with the interest rate on long-term bonds being lower than the rate on short-term bonds – that economic growth is slowing.

With bonds seeing troubled times ahead, it only adds to the volatility pot and data being scrambled.

The rand, which touched the R17.00 level not too long ago, traded all the way down to R16.14 in the wake of the data release. Still, the rand, for one, ran too far too quickly, and the second part of the rand bounce back has been weak data out of China, with Chinese data disappointing the market and the Chinese Central Bank cutting interest rates unexpectedly. The Chinese economy is still battling a real estate slump and strong COVID controls which will weigh down any significant growth.

This brought about the market running back to the US dollar, with the US dollar trading below the 1.02 level against the euro, after comfortably trading above that mark after the CPI number. There seems to be a definite divergence between the US and Chinese economies, and that data divergence could set the tone for volatility going forward.

The rand enjoyed the “good” CPI data out of the US but sank back to the R16.40 level after the Chinese data misses. We expected the rand to trade around that level until the release of the FOMC minutes on Wednesday.

The key message from those minutes was that the Fed will continue to hike rates for as long as inflation remains above the 2% target. The pace and size of the hike could slow depending on fresh data in the coming months.

The rand lost ground and remained weak on Thursday, trading around the R16.80 mark. We saw a full reversal since the US CPI numbers, when the rand enjoyed a sell-off in the dollar.

If you enjoy these updates, you’ll love the upcoming webinar with TreasuryONE. Join us at 9am on Thursday, 25th August for a look at inflation and the threat of recession. Attendance is free! You just have to register at this link.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Corporate finance corner (M&A / capital raises)

Although it was obvious from yesterday’s announcement with the results of the meeting, Fortress has confirmed in a separate announcement that the attempt to collapse the dual-share structure has failed. Although over 60% of the FFA and FFB shareholders voted in support of the deal, it needed 75% approval as a special resolution. Fortress needed to meet the minimum distribution requirement of a REIT by 31 October 2022 and cannot do so due to the Memorandum of Incorporation and the rules for distributions. The company is now meeting with the JSE to figure out the way forward, as a REIT has never lost that status before on the JSE.

Tsogo Sun Hotels has achieved resounding shareholder approval for the proposed transaction to commercially separate from Tsogo Sun Gaming and sell a hotel. The name has now formally been changed from Tsogo Sun Hotels to Southern Sun Limited, with new JSE share code SSU. The confusion of having two listed companies called “Tsogo” is finally behind us.

Financial updates

Adcock Ingram has released a further trading statement for the year ended June 2022. In mid-July, the company guided earnings growth of “at least 20%” – the minimum disclosure under JSE Listings Requirements rules to trigger a trading statement. Things are a little better than that, with HEPS expected to be between 23.5% and 24.0% higher, coming in at between 500 cents and 502 cents. The share price is just over R51, so the Price/Earnings multiple is slightly over 10x.

Exxaro has released financial results for the six months to June 2022, reflecting revenue growth of 48% and a 77% jump in net operating profit. Cash from operations was a huge R9.4 billion (vs. nearly R4 billion in the comparable period) and dividends from equity-accounted investments brought in another R3 billion. HEPS is only up by 26% though, as equity-accounted income from Sishen Iron Ore fell by 51% and this is reported below the operating profit line. The interim dividend is 23% lower than last year, coming in at R15.93 per share. The group derives 97% of its revenue from coal, which is why the earnings look so good for this period. Of course, it just wouldn’t be a coal industry announcement without a Transnet bashing section, so here it is in all its glory:

“Locomotive unavailability remains a huge challenge, which combined with cable theft, vandalism and sabotage of rail infrastructure, is impacting our logistics chain.”

Exxaro interim earnings release, 18 August 2022

Curro has released results for the six months ended June 2022. Average learner numbers increased by 7% (now over 70,000) and revenue was up 15% (13.3% from tuition fees as a combination of inflationary increases and learner growth, along with 21.4% growth in ancillary revenue). Margins have expanded based on this revenue growth, with EBITDA up by 20%. It gets better the further down you look, with recurring HEPS up by 31%. There’s no interim dividend though, with management electing to wait for a final dividend. The credit loss provision was higher in this period than the comparable period, with R175 million in debtors from actively enrolled accounts and a substantial R74 million from inactive accounts. The real hangover of the pandemic is found in that debtors balance, with many families losing their income for reasons beyond their control. I will never forget the stupidity of extended lockdowns.

Grindrod’s incredible share price run continues, closing over 8% higher after releasing a great update. This year, the share price has considerably more than doubled! This has been a combination of delivering a focused strategy and benefitting from Transnet’s incompetence, with the Maputo port becoming rather popular for South African exporters. Maputo Port volumes grew 30% in the six months to June 2021, driving earnings growth of over 100% in Grindrod’s Port and Terminals business. Over $110 million has been invested in the port to upgrade the infrastructure for greater chrome and ferro-chrome capacity, rail offloading facilities, road upgrades and berth rehabilitation. Even in Richards Bay, volumes were up 28%. This isn’t just a Maputo story. In the logistics side of the business, the shipping and container depot businesses performed well despite KZN’s best efforts to wash the containers into the sea. Interim insurance proceeds of R100 million were received to replace damaged equipment and infrastructure. Grindrod Bank is performing solidly, which is important as that business is being sold to African Bank for R1.5 billion. The other businesses planned to be sold are Marine Fuels, the private equity portfolio and the property exposure on the KZN north coast, which has been an albatross for Grindrod shareholders. With all said and done, core headline earnings (Port and Terminals, Logistics, Bank and Group) came in at between R514 million and R544 million in this period, up between 49% and 58%. Grindrod is absolutely cooking!

Grindrod Shipping released results for the second quarter of the year, giving us a six-month view to June 2022. The group has announced its highest quarterly dividend ever of $0.84 per share. Supply is being constrained by minimal ordering of new vessels because of concerns over environmental regulations and the prices of new builds, so existing operators are charging high rates. In fact, the daily rate for handysize and supramax/ultramax vessels was significantly higher in this quarter than in the first quarter. At this stage, bookings for the third quarter are at fairly similar rates to the average over six months, which means they are down on second quarter rates. The dry bulk market has also experienced limited impact from higher inflation levels and interest rates. HEPS of $2.78 for the quarter is 186% higher year-on-year. The share price closed 15.8% up on this news, taking the year-to-date performance to around 30%! There has been much volatility along the way.

Aside from Caxton and CTP Publishers and Printers fighting with Mpact on SENS, the business is actually doing really well. For the year ended June 2022, HEPS is expected to be 94.5% – 110.8% higher, coming in at between 146.7 cents and 158.9 cents. Results are expected on 12th September. The share price has put in a respectable performance this year, up around 12%.

Blue Label Telecoms has released a trading statement for the year ended May 2022. HEPS is 34% – 38% higher than in the prior year. The expected range is between 115.62 cents and 119.06 cents. With a share price of R7 just after the announcement came out, that’s a trailing Price/Earnings multiple of around 6x. There is still much debate in the market over the ongoing attempts to keep Cell C alive.

Workforce Holdings released a trading statement for the six months to June 2022. The outsourcing, recruitment, training and other services offered by the company led to HEPS of between 14.04 cents and 15.16 cents, an increase of between 25% and 35% vs. the comparable period.

Randgold & Exploration Company has released a trading statement for the six months ended June 2022. A headline loss of 14.90 cents per share is a considerable deterioration from the loss of 7.37 cents in the comparable period. The share price closed over 19% lower, though this is mainly a reflection of the extent of the bid-offer spread.

Buffalo Coal Corp released interim results for the six months ended June 2022. Revenue was up 7% and the loss from operations decreased by 92%. It was still a loss though, in this case R3.5 million off a revenue base of R187 million. No dividends have been declared.

Operational updates

Thungela and Transnet have concluded an amendment to the long-term agreement in which Transnet gives below-par service to Thungela (and others) and gets lambasted for it over SENS on a regular basis. In early April, Transnet issued a Force Majeure notice to the Coal Export Parties (CEPs) based on issues outside of its control, like people stealing infrastructure (among other things). Transnet wanted to use these circumstances as a trigger to terminate the agreement, with the CEPs said no to. Instead, the parties went into a period of negotiation. The parties have now reached agreement on minimum rail capacity as well as rail tariffs, including performance penalties. Thungela does not believe that this agreement will have a material impact on the recently published operational outlook.

Share buybacks and dividends

Tsogo Sun Gaming has declared a final dividend of 19 cents per share for the year ended March 2022. Don’t spend it all at once!

EnX Group is paying a R1.50 special dividend, which is chunky when the share price is R7.20. The last day to trade is 30th August and payment will be made on 5th September.

Aside from a few changes to board committees here and there, no exciting chairs were shuffled.

Director dealings

An associate of Des de Beer continues to buy shares in Lighthouse Properties, this time to the value of R1.8 million.

Unusual things

The Nutritional Holdings soap opera continues. The company has now identified the parties in the liquidation proceedings. Anthony Richard Pinfold is the former director who initiated the applications (there are two – one for Nutritional Holdings and one for Nutritional Foods) and if I understand the announcement correctly, Ontario Private Equity is the shareholder contesting the application. For Nutritional Holdings, a liquidator has been appointed and an application has been made to set aside the final liquidation order. For Nutritional Foods, the matter has been postponed to February 2023.

Novus subsidiary Novus Print has concluded an agreement to acquire Pearson plc’s 75% stake in Pearson South Africa for a base consideration of R829,4 million. The remaining 25% stake is held by BEE partners Sphere RB Investments and Pearson Marang Education Trust whose stake will remain in place following the conclusion of the acquisition. Within the Pearson SA stable are the print materials and CAPS-approved textbook publishers Heinemann and Maskew Miller Longman. The acquisition is a category 1 transaction.

Lonmin UK, a wholly owned subsidiary of Sibanye Stillwater has disposed of its majority stake in Lonmin Canada (Loncan) to Ontario-headquartered Magna Mining, valuing Loncan’s assets, which include the Denison project and Crean Hill mine, at C$16 million.

Mondi plc is to sell its Russian pulp, packaging paper and uncoated fine paper mill Mondi Syktyvkar to Augment Investment for a consideration of RUB95 billion (c.€1,5 billion). The category 1 transaction will require shareholder approval. In a separate transaction, Mondi has agreed to acquire the Duino mill near Trieste in Italy from the Burgo Group for a total consideration of €40 million. The containerboard machine in operation at the mill will strengthen the groups backward integration in corrugated packaging.

Fortress REIT shareholders have rejected the proposed scheme by the Board to repurchase all the Fortress A shares held, in consideration for the issue of 3.01281 Fortress B shares for every Fortress A share held. This, despite the fact, that prior to proposing the scheme the company engaged extensively with shareholders of both A and B shares on the need to collapse the dual share structure, warning that failure to do so would lead to the loss of REIT status which requires certain distributions of income.

The acquisition by SGT Solutions (40% owned by Ayo Technology Solutions and 60% held by African Equity Empowerment Investments) of Italian Summer, a company in the power management and backup solutions industry, has been terminated. The reason given for the immediate termination is the unfulfillment of conditions precedent.

Unlisted Companies

Seriti Resources has reached financial close on its acquisition of a majority stake in wind-powered renewable energy company Windlab Africa. The acquisition, through its subsidiary Seriti Green, consists of 100% of Windlab South Africa and 75% of Windlab East Africa. Windlab Africa is valued at c. US$55 million (R892 million). As part of the transaction involving debt and equity, RMB and Standard Bank have each taken a 14.5% stake in Windlab Africa for transaction considerations of US$5,8 million (R95,1 million).

Pretoria-based veterinary pharmaceutical company Afrivet Southern Africa has been acquired by US animal health distributor Bimeda. Afrivet also operates in Zambia and Mozambique while Bimedia has a long-established presence in Africa. Financial details were undisclosed.

City Logistics and private equity firm Clearwater Capital have acquired the Fastway Couriers South Africa franchise, with City Logistics taking the majority 70% stake. Financial details of the transaction were not disclosed.

Sango Capital, a local investment management firm, has acquired a controlling stake in Tunis Stock Exchange-listed Sotipapier, a manufacturer of Kraft paper, test line and flute paper based in Tunisia. The stake was acquired from private equity firm SPE Capital for an undisclosed sum.

Homefarm, a Johannesburg-based agritech startup, has raised c.R1,7 million in a seed funding round. The funds will be used to scale its operations, improve its service offering and roll out its marketing and distribution channels. The startup has as a fully automated indoor farms model which allows people to grow their own food.

Schroder European Real Estate Investment Trust has declared a further special dividend of 0.10 euro cents per share associated with the successful execution of the Paris, Boulogne-Billancourt business plan.

Orion Minerals has undertaken a further share purchase plan providing shareholders with an opportunity to increase their shareholding in the company at the same offer price of A$0.02 per share (R0.22 per share). The capital raise is part of a broader capital raising to underpin the next phase of development of its portfolio of advanced base metal assets in South Africa.

A number of companies announced the repurchase of shares

Naspers and Prosus continued with their open-ended share repurchase programmes. This week the companies announced that during the period 8th to 12th August 2022, a total of 2,431,395 Prosus shares were acquired for an aggregate €153,72 million and 329,534 Naspers shares for R808,21 million.

British American Tobacco repurchased a further 825,000 shares this week for a total of £27,79 million. The number of shares permitted to be repurchased is set at 229,400,000.

Four companies issued profit warnings. The companies were: Santam, DRDGOLD, Sibanye Stillwater and Randgold & Exploration.

Four companies this week issued or withdrew cautionary notices. The companies were: Safari Investments RSA, Alviva, Novus and Aveng.

Galileo Resources plc is to acquire a 29% stake in BC Ventures, the owner of a prospective lithium project near Kamativi in Southwest Zimbabwe and two gold licenses close to Bulawayo. The assets are owned through Zimbabwean subsidiary Sinamatella Investments. Following the Galileo will hold an 80% interest in BC Ventures. The Consideration Shares will be issued at 1.2 pence per share which is a premium of 4.4. The purchase consideration of £6 million will be settled by the issue of 50 million Galileo shares at 1.2 pence per share, a premium of 4.4% to the closing price of 1.15 pence pre share on August 8, 2022. The consideration shares are subject to a 12-month lock up.

Sango Capital, a South African investment management firm, has acquired a controlling stake in Tunis Stock Exchange-listed Sotipapier, a manufacturer of Kraft paper, test line and flute paper based in Tunisia. The stake was acquired from private equity firm SPE Capital for an undisclosed sum.

Kenyan social commerce startup Flo by Saada has been acquired by US-based Elloe. Flo by Saada enables small and medium enterprises to build solutions and process payments through USSD and programmable SMS. Financial details were not disclosed.

Ghanaian cashflow and spend management platform Float has acquired Nigerian cloud-based accounting company Accounteer for an undisclosed sum. The deal is in line with Float’s strategic objective to become the financial operating system for Africa’s SMEs.

IProcure, a Kenyan agritech startup, has raised US$10,2 million in a series B round led by Investisseurs & Partenaires with participation from Novastar Ventures, British International Investment and Ceniarth. The funding will be used to scale into the East Africa region, particularly Uganda and Tanzania and to launch a credit offering for agro-retailers.

Pastel, a Nigerian digital bookkeeping platform for merchants, has raised US$5,5 million in a seed round. The round was led by pan-African venture capital firm TLcom with participation from Global Founders Capital, Golden Palm Investments, DFS Labs, Plug and Play, Ulu Ventures and Soma Cap. Funding will be used to expand its product offering, develop additional finance management features and tools around group savings, loans and payments for small business.

Bonbell, an Egypt-based restaurant management platform, has closed an initial funding round for $350,000. The investment, from a Canadian angel investor will be used to further develop Bonbell’s app which launched earlier this year. The foodtech startup offers a cloud-based online food ordering and delivery system enabling restaurant managers to handle dine-in orders, table reservations and curb side delivery.

Nigerian TeamApt, a fintech startup operating a business payments and banking platform, has secured an undisclosed sum from venture capital firm QED Investors. The investment will be used to scale the business across Africa.

Lori Systems, a Nairobi-headquartered African on-demand logistics and trucking company has raised an undisclosed sum in a pre-Series B round. The funds, raised from Google and existing investors, will be used to scale new product lines and reach profitability. The company digitises haulage, providing shippers with solutions to manage their cargo and transporters.

The environmental, social and governance (ESG) and sustainability revolution is in full swing. Today’s investors are no longer only looking at financial yields and returns. They are increasingly also factoring in societal, environmental and other non-financial considerations when making investment decisions.

The increased focus on “responsible” investing has been so swift that Bloomberg Intelligence expects ESG assets to account for over one-third of global assets under management by 2025,1 whilst Deloitte believes that ESG-mandated assets are on track to represent half of all professionally managed assets globally by 2024.2

Projections like these, and the ever-increasing ESG and sustainability-related “carrots” and “sticks”, have spurred organisations to integrate ESG considerations into many more business functions.

A practice which has recently started gaining traction, although not yet among South African companies, is the assignment of C-Suite3 level roles focusing solely on ESG and sustainability.

Considering the increase in ESG-related regulation, risks and stakeholder demands, coupled with the already busy workloads of current C-Suite executives, it makes perfect sense for organisations to have a C-Suite executive permanently dedicated to, and taking ownership of, the organisation’s ESG function.

All in the name: chief ESG officer (“cESGo”), chief sustainability officer (“CSO”) or something else?

Unlike CEOs and CFOs, there is not yet a single, universal title for the executive tasked with overseeing ESG and sustainability. The title will likely depend on the organisation’s principal area of focus between the aforesaid. However, given that the “E” in ESG encompasses sustainability and the promotion of environmentally responsible practices, it could be argued that cESGo is the more apt title.

What role will the cESGo play in the organisation?

The role of the cESGo will evolve alongside the definition of ESG itself. Nevertheless, there are a number of duties which are typically viewed as being part of this portfolio. These include:

• along with the board, establishing the organisation’s ESG strategy, goals and initiatives;

• overseeing and bringing together the ESG-related aspects in the different (often siloed) functions of the organisation, such as product, marketing, compliance, risk, etc.;

• monitoring the ESG environment outside of the organisation to discover trends and best practices, as well as to identify potential risks and opportunities applicable to the organisation;

• liaising with external stakeholders and regulators, and introducing their insights to the organisation;

• overseeing and analysing the organisation’s reporting on ESG and sustainability to ensure goals are being achieved; and

• benchmarking competitors.

Does your organisation need a cESGo?

The answer will depend on a host of factors, including the organisation’s size, industry, geographic locations and exposure to ESG-related risks. The organisation’s culture and the brand image it wishes to portray will also be key considerations in this decision.

Organisations who do appoint a cESGo are generally seen to take ESG and sustainability as a strategic imperative, with the areas worthy of board representation. Having the cESGo report directly to the CEO also gives the cESGo the necessary authority and influence to effect timely actions.

However, those organisations who decide against such an appointment do have other options. They could have the current C-Suite executives take on additional ESG-related roles or, alternatively, have their social and ethics committees’ mandates widened to take on more responsibility.

With the ESG and sustainability landscape continually evolving, along with the need for disclosures of same, now may be the perfect time for South African companies to start considering this formal appointment to help them to become more responsible corporate citizens and, as a result, attract additional institutional investor funds.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Corporate finance corner (M&A / capital raises)

Fortress REIT looks set to become engrained in the history of the JSE for potentially being the first listed property company to lose REIT status. At the all-important meeting of shareholders to approve a scheme of arrangement to repurchase all of the Fortress A shares through the issuance of 3.01281 B shares for every A share, the vote went against the scheme. It therefore cannot be implemented and failed by quite some margin actually, with only c.60% approval (a special resolution requires 75%). Even a promotional video with Bruce Whitfield couldn’t save this one, unfortunately. The company has previously warned that failure to pass the resolution would likely lead to loss of REIT status as the requirements related to distributions of income won’t be met.

Aveng has renewed the cautionary announcement related to the potential disposal of Trident Steel. The value is expected to exceed Trident Steel’s net asset value as reported in the 2022 interim financials. The proceeds would be used to settle remaining debt in South Africa, significantly improving the balance sheet in the process. Although I’m not close to the numbers on Aveng, I would imagine that shareholders are really hoping this deal goes through!

Texton Property Fund is pushing forward with its strategy to invest in the US. Texton has committed $5.5 million to GIM Investments PCC for investments in the manufactured housing real estate sector in the US. These are the mobile home parks that represent an interesting asset class (those who listened to Episode 87 of Magic Markets would’ve learnt about this asset class from the team at Westbrooke Alternative Asset Management). The capital will be deployed over two years as and when investments are identified. This makes sense for Texton, as South Africans cannot gain access to this asset class through any other listed vehicles on the JSE. It brings USD-based earnings that are far more resilient to cyclical fluctuations than other property types. With a target net IRR of 14.5%, it also offers returns that are appealing to local investors. This is a category 2 transaction under JSE Listings Requirements and does not require a shareholder vote.

Orion Minerals Limited has closed its Share Purchase Plan, an initiative to raise capital from existing shareholders to supplement the capital raise currently underway with strategic investors. $1.35 million was raised through this initiative, with strong support from South Africa – a reminder that the retail investor base and smaller asset managers shouldn’t be ignored by listed companies. Commitments for around $6 million from other investors had previously been received, with discussions continuing for the remaining $14 million. Discussions are also taking place with banks and development finance institutions, with Orion noting “very positive progress” with a leading development financing agency following a period of due diligence and negotiations.

SilverBridge has announced that the offer from ROX Equity Partners of R2.00 per share for all the shares in SilverBridge has become unconditional. This means that shareholders can go ahead and accept the offer without wondering whether any regulatory or other conditions will be met. The offer closes at midday on Friday, 2nd September.

Financial updates

DRDGOLD has released a trading update for the year ended June 2022. Production was ahead of guidance (183,902 ounces vs. guided 160,000 – 180,000 ounces) and the cash operating cost was only slightly above guidance as well (R600,875/kg vs guided R600,000/kg). Capital investment was R584.1 million vs. guidance of R600 million. Due to the rather tepid performance of the gold price over the past year, headline earnings per share (HEPS) has fallen by between 13% and 33%. This brings it down to 113.6 cents – 147.2 cents vs. a share price of around R10.40. The balance sheet is strong, with no debt at all and cash of over R2.5 billion. During the period, the group generated free cash flow of R871.6 million and paid dividends of R513.3 million. I sold my DRDGOLD position at the start of the year if I recall correctly, which was the right decision as the share price is down more than 20% this year. As the company has thin margins (it reclaims gold rather than mines it), inflationary pressures on costs really hurt the investment thesis unless the gold price performs strongly.

Sibanye-Stillwater released a trading statement for the six months ended June 2022. HEPS is expected to be between 47% and 52% lower than in the comparable period. This has been impacted by factors like the strike at the South African gold operations, suspensions of operations at the Beatrix tailing storage facility for a quarter, flooding at the US PGM operations and lower precious metal prices vs. the comparable period. Production at Stillwater in the US was down by 23% due to the floods. That sounds like a walk in the park vs. the impact on gold production in South Africa, which fell by 77% during the period. The share price was down by around 6% for the day.

Northam Platinum has released a voluntary trading update for the year ended June 2022. It’s been a very busy year of corporate actions for the company, with the acceleration of the Zambezi BEE transaction and the acquisition of a strategic shareholding in Royal Bafokeng Platinum. Although there was a 12.8% increase in sales volumes, there was a 13.4% decrease in the 4E US dollar basket price. Thanks to a weakening of the rand, sales revenue growth ended up in the green, up 4.4%. The group unit cash cost per refined platinum ounce has increased by 18.9%, driven by inflation, more employees in service and lower concentrator feed grades. HEPS is expected to vary by between -7.9% and +2.1% vs. the prior period, so the midpoint is a slight drop. Net debt : EBITDA is at 0.97x, in line with the group’s target of below 1x. Interestingly, the value of net debt is similar to the value of the 34.52% stake in Royal Bafokeng Platinum. Full results will be released on 26th August.

Aspen Pharmacare released a trading statement for the year ended June 2022. Normalised HEPS is expected to increase by between 20% and 25%. This was achieved despite very little revenue growth (1% – 3% as reported or 4% – 6% in constant currency). The HEPS performance has been achieved by higher EBITDA margins (i.e. better operating profits per unit of revenue) and lower net finance charges (if you pay less interest to the bank, you have more earnings left for shareholders). The share price has had a nasty year, down nearly 29%.

Emira Property Fund released financial results for the year ended June 2022. This fund has a portfolio that is diversified across the various types of properties (including residential) and also has a US component to bring an offshore flavour. Distributable earnings were up 3.8% for the year and the final dividend decreased by 5.2%, so the full-year dividend was only 1% higher. The group notes a strong performance in industrial and retail properties, offset of course by the office properties. Although growth in income from the residential portfolio has been marginal, the good news is that vacancies are down significantly. Net asset value (NAV) per share as increased by 7.3% to R16.286, so the share price of R10.70 is a discount to NAV of over 34%. Based on the full year dividend of 119.79 cents, Emira is trading on a yield of 11.2%.

Here’s one for the diaries: Lesaka Technologies (previously Net1) will release results after US market close on 9th September.

Operational updates

None today!

Share buybacks and dividends

It seems like some of the cross-holding between Naspers and Prosus might be reduced. The lock-up on the Prosus shares held by Naspers expired on Wednesday and Naspers has indicated that it intends to dispose of some Prosus shares to fund ongoing repurchases of Naspers shares. Approval from the SARB is required first. If that is obtained (as expected in the coming weeks), it looks like a portion of this odd structure may be unwound.

A director of Santova in Australia exercised share options and promptly sold those shares and a few more, with a total value of nearly R2.9 million.

Unusual things

Mpact has now formally responded to Caxton’s allegations (and insinuations, as Mpact puts it) via SENS. The first point that Mpact confirms is that the Competition Commission is not seeking to impose a penalty against Mpact and that the company has been cooperating transparently since 2016. Mpact goes on to remind the market that Caxton applied to the Commission to file a separate merger notification before an offer was even being made to the Mpact board. I had found that to be a really weird step from Caxton and I wrote about it at the time. Mpact felt that it couldn’t support a joint or separate merger filing decision as the company hadn’t even received an offer. The Commission agreed with Mpact, Caxton took this on review before the Competition Tribunal and the outcome is pending. In that process, a third party made representations that Caxton has tried to get access to. The representations were made available to Caxton chairman Paul Jenkins on a strictly confidential basis. Furthermore, Caxton sent a letter of demand for a shareholders’ meeting that Mpact has rejected as unlawful. One thing is for sure – lawyers are making plenty of money here for the hours of advice. I must be honest, the Mpact announcement reads like it was written by adults whereas the Caxton announcement was like listening to an angry teenager. As for where this will end, that is anyone’s guess. It has become a terribly unhealthy relationship.

Renergen initiated a process to change its auditor, reflecting a desire to have an audit firm that brings more international experience. After a tender process, the audit committee has recommended the appointment of BDO South Africa. Shareholders will be asked to approve this at the AGM.

If you are a shareholder in Jasco Electronics, you should note that the circular for the related party lease agreement has been distributed by the company.

The Softbank Group’s philosophy is to “contribute to people’s happiness” through the information revolution. With a tepid share price performance over the past year, shareholders are probably looking for some of that happiness themselves. Ghost Grad Kreeti Panday takes a closer look.

Japanese multinational conglomerate SoftBank Group, has released results for the three months ended June 2022, reporting a ¥3.16 trillion ($23 billion loss) for the quarter. That’s particularly horrible when compared to the ¥761.5 billion profit made in the comparable period.

Born in the 80s

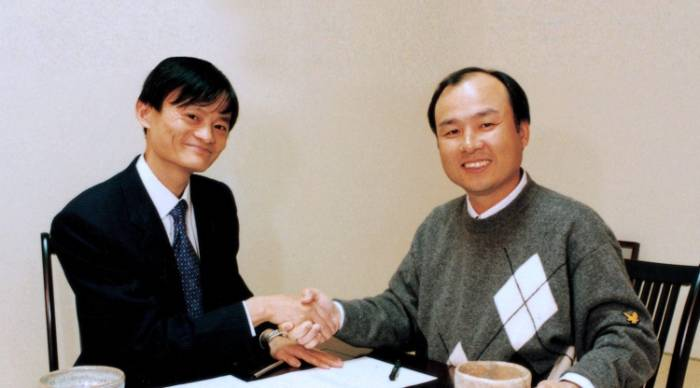

SoftBank was founded in 1981 as a software distribution company. The next step was to launch monthly magazines in 1982, which shows how far this group (and the world) has come. It was only when the internet came around that SoftBank started to do landmark deals, like a joint venture to launch Yahoo! Japan in 1996 and an investment in Alibaba in 2000.

This picture from the SoftBank website of SoftBank founder Masayoshi Son and Alibaba founder Jack Ma is well worth replicating here:

In 2017, SoftBank launched its first Vision Fund, investing in the types of businesses that get Cathie Wood all hot under the collar. There are now two such technology-focused venture capital funds with investments in over 470 companies in aggregate, consisting of mainly AI-focused unicorns (privately-held companies that have reached a $1 billion valuation). In 2019, SoftBank created the $5 billion SoftBank Latin America fund to invest in similar companies in that region.

What goes up…often comes down

We all know that that 2020 – 2021 saw an incredible bubble in the valuations of futuristic companies that are big on promises and often rather low on cash flows.

It’s only when you see the numbers put forward by SoftBank that you realise the scale of it all. The Vision Funds posted an investment loss of ¥2,9 trillion (around $21.5 billion). Thankfully, the realised loss was across the two funds was just over ¥27 billion ($200 million), so the rest was based on mark-to-market movements and valuation declines in private investments.

Masayoshi Son, has largely blamed the loss on global stock market turmoil and the rapid fall of the yen. Many of the companies that the group is invested in are technology stocks, which have suffered due to Central Banks raising interest rates in response to rising inflation. He has emphasised the defensive and conservative approach that the group has now adopted in its investments following the losses, which is possibly too little too late.

One of the major issues is the drop in IPOs as the listing environment soured. When you’re planning to list a company at a gigantic (and ridiculous) valuation, you better get the timing right. Those days were left behind in 2021 and we won’t see them again unless we return to an environment of incredibly low interest rates and frequent use of the money printing machines.

This isn’t good news for SoftBank. It cannot easily force the founders of unicorns to list into an unsavoury valuation, though this problem fixes itself as these founders burn capital. SoftBank has historically done well from taking profits on IPO that are used to invest in other companies.

Troubles in China

With core investments in the likes of Alibaba, the recent geopolitical climate in China hasn’t done SoftBank any favours. Covid-19 lockdowns have been a problem, tensions between Taiwan and China have flared up and the Chinese Communist Party (CCP) has been taking aim squarely at tech companies. This led to incredible destruction of value at ride-hailing company Didi, in which SoftBank invested $12 billion through Vision Fund 1 in 2017. SoftBank has registered a $9.3 billion loss on that investment.

SoftBank now appears to be losing faith in the Chinese operating environment for tech companies, lowering its stake in Alibaba Group Holding by 38.4% to 14.7% for a gain of $34 billion. At least someone has made a profit on Alibaba shares.

This came after the US Securities and Exchange Commission (SEC) added Alibaba to its delisting watchlist based on the Holding Foreign Companies Accountable Act (HFCAA) – legislation that scrutinises China-based US-listed companies. The sale is seen as a significant move as SoftBank has been considered one of Alibaba’s biggest champions since its initial investment.

Other disposals

SoftBank also sold the remainder of its stake in ride-hailing company Uber between April and July at $41.47 per share. The group invested in Uber in 2018 and again in 2019, becoming its largest shareholder. In 2021, the group sold a third of its stake and has now disposed of the balance.

SoftBank also sold stakes in online residential real estate company Opendoor, US-based cancer care group Guardant Health and Chinese real estate platform Beike.

Getting serious on debt and costs

The loan-to value (LTV) ratio, which the company aims to keep at a maximum of 25%, has been lowered to 14.5% as a result of the group’s “defensive” strategy. SoftBank also intends to keep a cash position sufficient to cover the group’s bond redemptions for at least the next two years.

Earnings per share decreased from ¥437.45 to a loss of ¥1,949.55. Clearly, action is required. Masayoshi Son warned of group-wide cost reduction within the company, announcing that “headcount may need to be reduced dramatically.” The company did not, however, give any indication of the scale of this cost reduction.

There are also executive reshufflings underway. Rajiv Misra, CEO of SoftBank Investment Advisors (which manages Vision Fund 1) and of SoftBank Global Advisors (which manages Vision Fund 2), will be relinquishing the latter role and retaining the former, being described as a “key man” for Vision Fund 1.

Despite all these pressures, the company has authorised a share repurchase programme of ¥400 billion. If there’s one thing tech companies just love, it’s the use of share buybacks.

If you enjoy Ghost Bites, then make sure you’re on the mailing list for a daily dose of market insights in Ghost Mail. It’s free! SIGN UP >>>

Corporate finance corner (M&A / capital raises)

Although I would’ve thought that Mondi has its hands full with an orderly exit from the Russian market, the company clearly isn’t ignoring opportunities to grow elsewhere. Mondi is acquiring the Duino mill near Trieste in Italy for €40 million. Perhaps the group’s favourite corporate development employees were sent on this due diligence and the unlucky others were sent to Russia! The mill currently has one paper machine that produces lightweight coated mechanical paper. Mondi plans to invest €200 million to convert this to production of high-quality recycled containerboard – 420,000 tonnes of the stuff every year. The location near export harbours is the appeal here, as the mill can support Mondi’s corrugated solutions plans in Central Europe and Turkey, in addition to serving the Italian market.

Financial updates

BHP Group has released results for the year ended 30 June. Revenue increased by 14% and HEPS is up by 54% to 439 US cents. Interestingly, the dividend has gone the other way, down by 13% from 200 US cents per share to 175 US cents. This is despite the group achieving record underlying EBITDA margin of 65% and record free cash flow of $24.3 billion for the year. Total dividends for the year represent a 77% payout ratio, well above the 50% minimum payout policy. Net debt has been squashed to just $0.3 billion, way down from $6.1 billion at the end of 2021. The Samarco disaster in Brazil in November 2015 is still haunting the group, with a provision of $1.1 billion raised in this period. The outcome of various legal proceedings and associated negotiations is highly uncertain, so this provision is guesswork at best. The report has loads of details, including the outlook for the various commodities produced by the group. You can read it here.

Exxaro Resources released a trading statement for the six months to June 2022. Thanks to a strong performance in the coal business despite logistical and other challenges, HEPS is expected to be between 18% and 32% higher. Share buybacks have also helped drive this result, with the downer being lower income from the equity-accounted investment in Sishen Iron Ore. EBITDA increased by between 131% and 157%, reflecting the performance of the coal business (income from investments is not included in EBITDA). The HEPS range is R32.11 to R35.93 and the share price was up 6% in afternoon trade to R217.

Santam released a trading statement for the six months to June 2022. Due to lower underwriting results and investment income, it doesn’t make for pretty reading. HEPS has fallen by between 43% and 62%. Net underwriting margin was positive but below the target range, impacted by adverse weather conditions and the KZN floods, with some of this impact mitigated by reduced Covid-19 business interruption claims provisions. The share price is flat over the past 12 months, with recent momentum firmly negative.

Truworths released a trading statement for the 53-week period ended 3 July 2022. Remember, retailers typically report based on weeks rather than calendar years, which leads to a 53-week reporting period every few years. This obviously has an impact on comparability, as it is rather flattering to have another week of trade in your numbers (unless you are Massmart in which case less is more). At Truworths, HEPS growth on a comparable 52-week basis is between 38% and 43%, an impressive result and the highest ever HEPS achieved by the group. The share price is up more than 21% in the past 30 days after the company indicated to the market that a big result was forthcoming.

KAP Industrial Holdings released an updated trading statement for the year ended June 2022. The news has gotten even better. The original trading statement noted HEPS from continuing operations of “at least 64.5 cents” and now that the company has more certainty over its results, that has been updated to a range of between 70.7 cents and 78.1 cents. This is an increase of between 64% and 82%. With discontinued operations included, the range increases to between 71.4 cents and 78.8 cents. The share price is flat this year, currently trading at R4.26.

HomeChoice International has released results for the six months ended June 2022. The most impressive thing about these numbers is the 29.5% increase in operating profit off modest revenue growth of just 4%. Although retail sales fell by 10%, loan disbursements increased by 33.1%. Headline earnings per share (HEPS) increased by 16.6%. An interim dividend of 64 cents per share has been declared, up from 47 cents in the comparable period. Weaver Fintech (which recently acquired PayJustNow) contributed 84% of group profit, so just be well aware of what you are investing in here. This group has become a financial services player that also happens to sell products in a digital-first strategy (30% of HomeChoice Retail sales are digital). Notably, the gross margin in the retail side of the business expanded by 320 basis points.

Transpaco released a trading statement for the year ended June 2022. HEPS has increased by between 38% and 45%, coming in at between 464 cents and 488 cents per share. The share price was 3.5% higher in afternoon trade, admittedly on very thin volumes. At around R24 per share, the Price/Earnings multiple is around 5x.

Trencor released results for the six months to June 2022 and you may be shocked to see a big ol’ zero as the profit or loss attributable to shareholders. This means that the costs of maintaining this cash shell are less than R500k, or they would round up to a loss of at least R1 million. Trencor is just the old holding company for Textainer, the shipping container business that Trencor unbundled to shareholders as part of a restructuring process. Trencor is sitting on cash that will be distributed to shareholders once certain indemnities expire in December 2024. The net asset value per share is R7.07 and the share price is R5.39. The trouble is that if the indemnity is triggered (which Trencor believes is a remote possibility), it looks like all the cash would be gone.

Capital & Counties Properties has confirmed the exchange rate applicable to the dividend. South African shareholders will receive 12.67712 ZAR cents per share before withholding taxes of 20% are applied.

EnX Group’s special dividend of R1.50 per share has still not received approval from the SARB. The company has reminded the market that a finalisation announcement (with dates for payment) will only be released once approval is obtained.

In the past week or so, Prosus repurchased shares to the value of $157 million and Naspers repurchased shares to the value of R808 million.

Notable shuffling of (expensive) chairs

The CFO of Sirius Real Estate is taking 12 months paternity leave following the birth of his first child. He has formally left that role, with a plan to return as Group FD in September 2023. Alistair Marks, the Chief Investment Officer and former CFO, will step in as interim CFO while the group looks for a permanent replacement. Kudos to a corporate exec for prioritising what he believes to be more important than anything else – far too many people put work above everything else until it is too late!

As part of releasing its results, BHP also announced two executive leadership changes. Edgar Basto has been appointed as Chief Operating Officer and Geraldine Slattery has been appointed as President Australia. I’ve always felt that the American convention of appointing a “President” sounds a bit awkward. Other options are usually “Country Head” or similar. Either way, there’s no shortage of talent at an organisation the size of BHP.

Following the retirement its Chairman, Raubex has appointed Les Maxwell (currently the lead independent director of the board) as the Acting Chairman.

Director dealings

A prescribed officer at Capitec has exercised share options and disposed of shares worth over R30 million. Nice life.

The company secretary of Vukile Property Fund has sold shares in the company worth R505k.

The company secretary of Thungela has bought shares in the company worth R257k.

Someone has clearly been running a campaign for company secretaries to open trading accounts, because the company secretary of Sygnia exercised employee share options and promptly sold nearly the entire amount (R238k)

Unusual things

Industrials REIT made a whoopsie in its recently reported numbers. A change in the number of diluted shares (those that would be in issue assuming all outstanding share options are exercised) means that diluted NAV per share is lower by 2 pence per share vs. what was reported (coming in at £1.76 per share). The total accounting return noted by the company of 25% should actually be 23.6% based on this correction. It’s uncommon to see corrections after the annual report was published.

Quilter Plc also released a correction to numbers – it’s so odd to see two proper companies with mistakes in their numbers on the same day! Quilter’s recent announcement disclosed incorrect numbers for HEPS for the comparable period. The correct year-on-year comparison is HEPS of 11.7 pence in this interim period vs. 1.4 pence in the comparable period.

Pembury Lifestyle Group is another example of a JSE-listed company that can’t even afford its audit fees, let alone anything else. The company is suspended from trading and needs to publish its financial statements going back to 2019. The proposed audit fee for the three years is R4 million. Pembury cannot afford that, so it reached out to previous auditors Moore to work out a deal based on different auditors at subsidiary and group level. Pembury still owes money to Moore as well as Abacus, another previous auditor. It’s all a bit of a nightmare. To make it worse, the CEO passed away suddenly in May and both the Designated Advisor (the title given to the advisor playing the role of JSE Sponsor for an AltX-isted company) and company secretary resigned. Some of the directors previously involved with the turnaround have agreed to return to the board. Talk about running a gauntlet!

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")