Share incentive schemes have, for some time, become a key mechanism to attract, retain and reward top talent. This holds true not only for listed companies, but also for unlisted companies – including those in the private equity sector.

Fund managers often want to incentivise key management in their portfolio companies with an equity slice in the business, thereby creating an alignment of interests to grow profits and, ultimately, returns.

The fortunes of participants in share incentive schemes have, unfortunately, been somewhat mixed over the years, given the volatility in macro-economic conditions, as well as the impact of ‘big bang’ events, such as the 2008 global financial crisis and the more recent COVID-19 pandemic. Many incentive schemes have ended up under water, leaving fund managers to consider what, if anything, can be done to reset these schemes to deliver the incentives that they sought to achieve.

Given the complexity of the relevant legislation, the tax consequences of amending and resetting incentive schemes need to be carefully considered. As a starting point, it is important to understand whether the scheme is ‘restricted’ or ‘unrestricted’. Broadly speaking, a ‘restricted’ equity scheme is one in which the participants are restricted from selling their equity shares (either for a period of time or as an outright prohibition), and/or where the participants may, for any reason, be forced to sell their equity shares at less than market value (for example, if they are dismissed).

In contrast, an ‘unrestricted’ scheme is one in which the participants are able to freely sell their equity shares, and where the participants cannot be forced, under any circumstances, to sell their equity shares at less than market value. Pre-emptive rights (also referred to as rights of first refusal) in favour of other participants or other shareholders that are exercisable at market value, as well as forced sales at market value, do not taint the shares as restricted for tax purposes.

From the participants’ perspective, the distinction between a restricted and unrestricted share scheme is fundamental, as each one is taxed differently. In an unrestricted scheme, the scheme shares are treated as having ‘vested’ in the participants’ hands upfront (at least for tax purposes), with any difference between the market value of such shares and the consideration paid therefor being subject to income tax. All future growth in these scheme shares would then typically be subject to capital gains tax (CGT), not income tax. Conversely, restricted scheme shares are only treated as ‘vesting’ for tax purposes on the earlier of disposal or when all the restrictions attaching to the share are lifted, with the difference between the proceeds/market value (as the case may be) of the shares and the initial consideration paid therefor being subject to income tax at such time only.

Resetting restricted and unrestricted share schemes that are currently underwater may also result in varied tax implications. For example, swapping one restricted share for another restricted share of a different class (with enhanced or reset participant rights) would not necessarily result in any immediate tax consequences for the participants. Instead, the newly acquired restricted shares would simply be subject to income tax upon disposal or vesting, as the case may be. Swapping an unrestricted share for another unrestricted share of a different class would, on the other hand, typically result in the value of the newly issued share being subject to income tax in the participants’ hands upfront. This is clearly not ideal from a cash flow perspective, but at least all future growth in these newly acquired shares would be subject to CGT, not full income tax.

Ad hoc special dividends may, in some cases, be used as a mechanism to reset scheme values, as these dividends would simply be subject to dividends tax at 20%, not full income tax. Obviously, however, this would move the cash flow burden to the company itself, which may be undesirable.

Like many areas of tax, the rules governing share schemes are complicated, and very widely drafted. Resetting these schemes, although done with the best of intentions, can result in very costly and unintended consequences if not carefully navigated.

Brian Dennehy is Director of Tax | Webber Wentzel

This article first appeared in Catalyst, DealMakers’ quarterly private equity publication.

The universe of Exchange Traded Funds (ETFs) is broad, offering investors many different ways to invest in the market.

Not only are there various different sector and weighting methodologies available, but Satrix ETFs offer South African investors a way to make perhaps the biggest decision of all: offshore vs. local exposure.

As we reflect on ETF performance in 2023, Siyabulela Nomoyi of Satrix joined The Finance Ghost to look at topics like:

Offshore vs. local performance and the impact of the start date for that analysis, including the currency effect;

The importance of understanding the underlying stocks in an ETF and their relative valuations; and

Relative performance of local ETFs.

The Ghost couldn’t help but slip in his ongoing request for a retail sector ETF, an index that the JSE really needs to add to the local market.

To understand more about ETFs and how they can be used in your portfolio, enjoy this podcast brought to you by Satrix.

Disclosure Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this podcast (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Is the Ascendis story coming to an end? (JSE: ASC)

A consortium led by Carl Neethling might be taking the company private

Hot on the heels of its trading statement, Ascendis announced that a consortium led by Carl Neethling is in discussions with the company regarding a potential take-private. The crummy news for minority shareholders is that if there is an offer, it is “not expected to be at a significant premium” to the current traded price of 69 cents a share.

No formal offer has been made at this stage. It’s very unusual to see an offer at a low premium, so it will be interesting to see how this plays out.

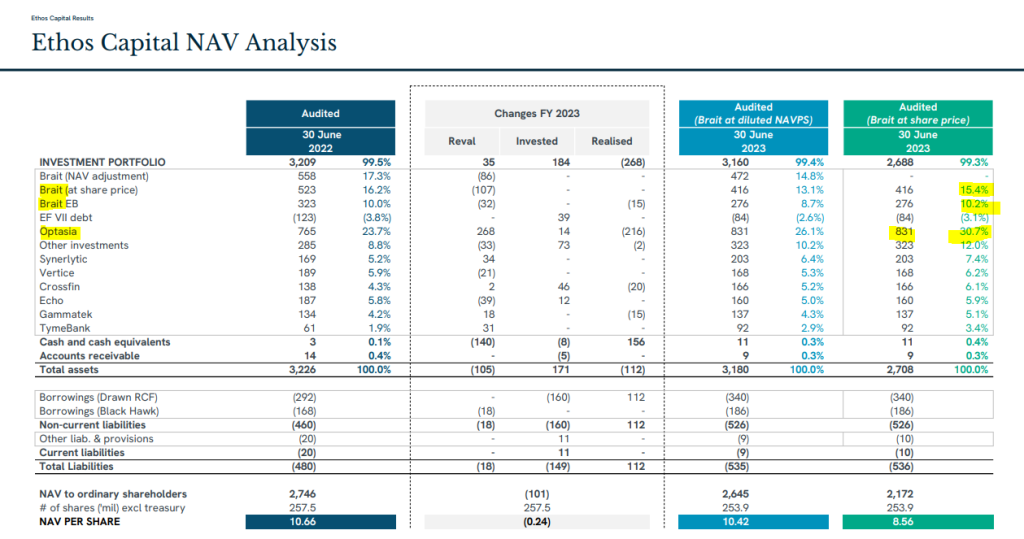

Net asset value per share inches higher at Ethos Capital (JSE: EPE)

Pressure on the Brait share price has let the team down

For the year ended June 2023, the net asset value per share of Ethos Capital increased by a paltry 0.8%. This is based on the Brait share price rather than Brait’s underlying net asset value. MTN Zakhele Futhi hasn’t helped either, with major drops in the listed portfolio that offset the 14% return in the unlisted portfolio.

I must point out here that the unlisted portfolio is the opinion of management, whereas the listed portfolio is the opinion of a market. You can figure out for yourself which one carries more weight. It does help that there was an equity deal in Optasia that helps confirm the value of the largest of the unlisted investments, driving a small uplift in the average valuation multiple in the portfolio.

Here’s the summary of net asset value per share, in which I’ve highlighted Brait and Optasia to show the combined contribution of 56.3% to group assets.

If you want to dig into this in great detail, you’ll find the results presentation at this link.

The current share price is R4.25, so the discount to the NAV per share of R8.56 is over 50%.

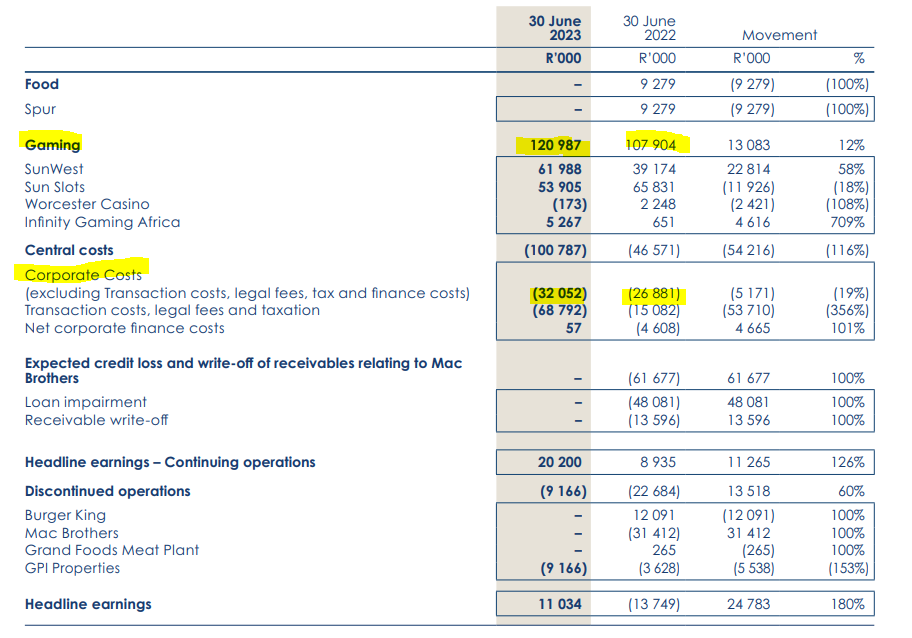

You have to read Grand Parade’s numbers carefully (JSE: GPL)

There are many once-offsand distortions

Grand Parade’s numbers are tricky. There has been a great deal of corporate activity, including the unbundling of the stake (steak?) in Spur and various restructuring transactions. The base period includes a number of discontinued operations, like Burger King and the disaster that was Mac Brothers.

The split between continuing and discontinued operations doesn’t even tell the right story, as Spur gets included in continuing operations and so do loans to Mac Brothers.

To help you look through the noise, I’ve included this table showing the contributions to headline earnings. Gaming grew by 12%, with around half of that amount in absolute terms going into increased corporate costs.

The group is now exclusively focused on the gaming sector, including “robust oversight” of its existing gaming investments, whatever that practically means.

Investment flows at Old Mutual are a sign of the times (JSE: OMU)

Inflation and high interest rates are eating into savings

Old Mutual has released results for the six months ended June. This includes the adoption of IFRS 17, which means major distortions and accounting restatements.

I’ll try and ignore the IFRS nonsense and focus on the operational metrics instead. Life APE sales excluding China grew by 14%. They were only up 1% including China, as the base period included product sales that were subsequently discontinued in anticipation of regulatory channels.

The value of new business margin increased to 2.6%, putting it within the medium-term target range of 2% to 3%.

Although gross flows grew by 17%, net client cash outflows of nearly R7.3 billion were worse than the prior period because clients needed to access their funds to survive these economic conditions. Despite this, funds under management grew by 6% to R1.3 trillion, supported by equity market performance.

Return on group equity value was only 10.5%, which is way below the performance of banking groups in South Africa. Return on embedded value in the Life and Savings business was 13.9%. The group uses a couple of other metrics, like return on net asset value of 11.9% and core return on net asset value of 13.1%.

I don’t really care which of those metrics you use, performance is still well below our local banks. Growth also isn’t exciting, with results from operations at Old Mutual only up by 3%. In this environment, would you rather be lending money to consumers or hoping they save and invest with you?

The group equity value per share is R18.806 and the share price is R12.10, so the market is quite correctly valuing Old Mutual at a discount. This discount is why the year-to-date share price performance of over 15.5% actually beats local banks. Like everything in investing, it comes down to valuation.

The Rebosis fire sale continues (JSE: REA | JSE: REB)

The selling price is way below the recent valuation

As you are probably aware by now, Rebosis is in business rescue and has been executing a “public sale process” to try and sell as many properties as possible to pay down the debt.

The latest such sale is to Katleho Property Investments, a subsidiary of Heriot Investments. The portfolio being sold is four office buildings, three of which are in Ekurhuleni and the other is in Midrand. The portfolio was valued at R291 million on 1 April 2023.

Perhaps that was an April Fool’s valuation, as the actual selling price is R160 million. Based on net operating income, the implied yield is a whopping 26.8%. Rebosis has practically given these properties away. A desperate seller is a terrible thing.

Unless you’re the buyer, of course.

York Timber has given far more detailed guidance (JSE: YRK)

At least cash from operations is positive, if we are looking for silver linings

York Timber has released an updated trading statement that gives a much tighter range for HEPS. Importantly, it also gives guidance for EBITDA and cash from operations.

I’ll start with HEPS, which is shouting timberrrrrr all the way down from 53.30 cents to a loss of between 73.27 cents and 77.00 cents for the year ended June. If we strip out various items (including biological asset fair value movements), we find EBITDA coming in between 58% and 63% lower than the comparable period. Cash from operations is also on the right size of zero at least, despite being between 48% and 53% lower.

Even without the biological asset fair value movements that cause big swings in earnings, this was a poor period for York.

Wesizwe Platinum nosedives (JSE: WEZ)

The headline loss is much higher than the comparable period

With unprotected strike action and ongoing pain in the PGM sector, this was never going to be a happy financial update from Wesizwe Platinum. Still, the extent of the loss is quite breathtaking, especially as this is an interim period.

For the six months to June, the headline loss per share has vastly deteriorated, coming in at between 59.22 cents and 60.04 cents. The loss in the comparable period was just 4.09 cents.

Keeping in mind that the share price is only 76 cents, this isn’t looking good.

Little Bites:

Director dealings:

I usually ignore sales by directors related to vesting of share options. Half of the Woolworths (JSE: WHL) announcement related to those types of sales. The other half was very interesting, with a director of the holding company selling shares worth R1.7 million and a director of the operating subsidiary selling shares worth a massive R19.1 million,

A director of Liberty Two Degrees (JSE: L2D) has sold shares worth R1.57 million.

A director of Novus (JSE: NVS) has sold shares worth R608k.

I’m not sure these are director dealings in the truest sense of the word, so I’m showing them separately. Three directors of Nampak (JSE: NPK) were announced as having followed their rights in the rights offer. Andre van der Veen (part of A2 Investment Partners) is obviously the largest, with an investment of over R72 million.

Heriot Investments has been busy. Not only has the company bought the Rebosis properties at a bargain price, but it has also transferred a 10.02% stake in Safari Investments (JSE: SAR) to its subsidiary, Thibault REIT Limited. This is only relevant because Thibault has applied for a listing on the Cape Town Stock Exchange.

AYO Technology (JSE: AYO) renewed its cautionary announcement related to the settlement agreement with the PIC. The company says that the parties have made significant progress in finalising the terms of the settlement agreement to ensure compliance with the JSE Listings Requirements.

Conduit Capital’s (JSE: CND) disposal of subsidiaries CRIH and CLL continues to hang in the balance, with the closing date for fulfilment of conditions extended yet again, this time to 31 October.

Basil Read (JSE: BSR) is currently in business rescue. The CEO of the company has resigned, so that doesn’t do much to help with stability. An acting appointment has been made internally.

Sable Exploration and Mining (JSE: SXM) has a share price of just 6 cents per share. It’s therefore not ideal that the headline loss per share for the six months ended August is between 65 cents and 75 cents per share! It’s worse than the comparable period, despite the company claiming that the loss has decreased. The maths is not mathing at this company.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

AngloGold begins its new corporate life (JSE: ANG)

Will the primary listing in the US make a difference in years to come?

AngloGold is a company with a rich history in South Africa. This makes it historically significant that the primary listing has been moved to the New York Stock Exchange, with only a secondary listing maintained on the JSE (and A2X and the Ghana Stock Exchange for that matter).

Although this sounds like semantics and even the stock ticker on the local market hasn’t changed, it signals intent to take a global gold story to a US investor base. The headquarters are now in Denver, Colorado, though it obviously retains a large corporate office in the City of No Water. I mean, the City of Gold. I mean, Joburg.

Headline loss narrows at Ascendis (JSE: ASC)

But it’s still a loss

I can finally call Ascendis by its correct name, rather than the very cheeky “Descendis” that I used for a long time when the thing was in a death spiral. Although the company is still loss-making, the trajectory of the losses is firmly in the right direction.

In a trading statement for the year ended June 2023, the company noted that the headline loss per share from continuing operations will be between -37.4 cents and -45.7 cents. This is an improvement of between 69.5% and 62.7% vs. the comparable period.

The headline loss from total operations is between -35.7 cents and -43.6 cents, an improvement of between 55.8% and 46.0%.

Bytes is achieving double-digit growth (JSE: BYI)

The market really liked this story

Bytes closed 9.5% higher on the news that trading conditions are solid, with the operations in the UK and Ireland growing gross invoiced income, gross profit and adjusted operating profit. In other words, things are heading firmly in the correct direction thanks to market share gains in private and public sector work.

Both gross profit and adjusted operating profit grew “comfortably in double digits” in the six months to August. Net cash at the end of the period was £51.3 million, net of £30 million worth of dividends in the period. The company has seasonal cash conversion and expects a strong second half.

Detailed results are due for release on 25 October.

Equites brings more capital home (JSE: EQU)

The company has sold a distribution warehouse in the UK

The property in question has a lease in place with Tesco Distribution until December 2023. That isn’t a typo. The lease is right on the cusp of expiring and the tenant hasn’t committed to a new lease, so Equites was staring down the barrel of a potentially significant vacancy.

A European logistics income fund is clearly feeling less worried, swooping in to buy the property for £29.75 million. This drops the loan-to-value ratio at Equites by 170 basis points, increases the weighted average lease expiry (obviously) and unlocks net cash proceeds of R684 million. Other than the reduction of debt in the UK, Equites is going to bring the capital back to South Africa to support the local development pipeline.

Equites claims that an internal rate of return of 12.1% was achieved on the property (measured in pounds and net of debt). The selling price is a 16.2% premium to the latest book value but I wouldn’t put much focus on that, as UK property prices have been heavily written down as yields have increased in the UK.

The property contributed £2.476 million to distributable income for the year ended February 2023, so the price is a yield of 8.3%.

Grindrod Shipping acquires Taylor Maritime’s ship management businesses (JSE: GSH)

This is part of the strategy of central management of a larger fleet

Grindrod Shipping announced the acquisition of 100% of two ship management companies. Taylor Maritime is the sole owner of one of the companies and part owner of the other. In case you’ve forgotten, Taylor Maritime also holds the vast majority of shares in Grindrod Shipping.

The acquisition price is between $11.75 million and $13.5 million, depending on how the earn-outs play out. The payment structure is a mix of cash and shares, payable over two years.

The company says that this will increase ship management income fees, “unlock synergies” (that dirty M&A term) in the commercial deployment of the dry bulk fleet and achieve savings on the technical side.

An awkward disclosure error by Investec (JSE: INP | JSE: INL)

The UK funds under management number actually went the other way

In the trading update released last Friday, Investec disclosed the UK Wealth and Investment funds under management (FUM) number as having increased by 1.3%. This was wrong, as there was actually a decrease of 2.0% since March 2023.

There were positive net inflows, so this is more to do with changes in asset values than anything wrong with the underlying business.

Nampak’s rights offer was heavily supported (JSE: NPK)

Coronation is the only underwriter that received additional shares

The important news for Nampak as a whole is that the company has successfully raised the intended R1 billion in equity at a price of R175 per share. The important news for its shareholders is that if you hoped to get any excess applications through this process, I’m afraid you will be disappointed. Such was the demand for the rights offer (over 138% of available shares) that a couple of the underwriters aren’t even getting excess shares.

Excluding excess applications, 90.08% of shares were subscribed for. Coronation gets first bite at the cherry based on the underwriting agreements, which means the remaining 9.92% all went to them. The other underwriters didn’t get anything and there’s certainly nothing for anyone else who asked for additional shares.

All eyes will now be on whether Nampak can steady the ship.

Vukile releases a fascinating pre-close update (JSE: VKE)

The South African retail portfolio is performing very well

The concept of “property” as an asset class is a dangerous umbrella term. There is a vast difference between an office building in Sandton and a value shopping centre on the edge of a township area or on a busy commuter route. If you need any further proof, you can look at Vukile’spre-close investor presentation.

In the South African portfolio, turnover is 3.6% higher than the comparable period and trading densities are growing across all segments. Vacancies at August 2023 are steady at 2.0% and reversions have improved from 2.3% for the year ended March to 2.4% for the six months to September. Footfall is 107% higher than in FY23.

I really enjoyed this chart in the update, showing the size of each category (the bubble) and the current performance across turnover growth and density growth. Top right is where you want to be. Bottom left is where you don’t want to be. The concerning bubble is Fashion, which is (1) very large and (2) very stagnant:

The performance in the Spanish portfolio also looks very good. Turnover at all the centres is up by strong double digits year-on-year. Unlike in South Africa, Spanish consumers have money for clothes:

Looking at the balance sheet, Vukile held a successful R526 million bond auction in August, so there’s support from the market for this story. The loan-to-value ratio of 44% seems a little high to me in this environment, but the credit rating is strong with a stable outlook.

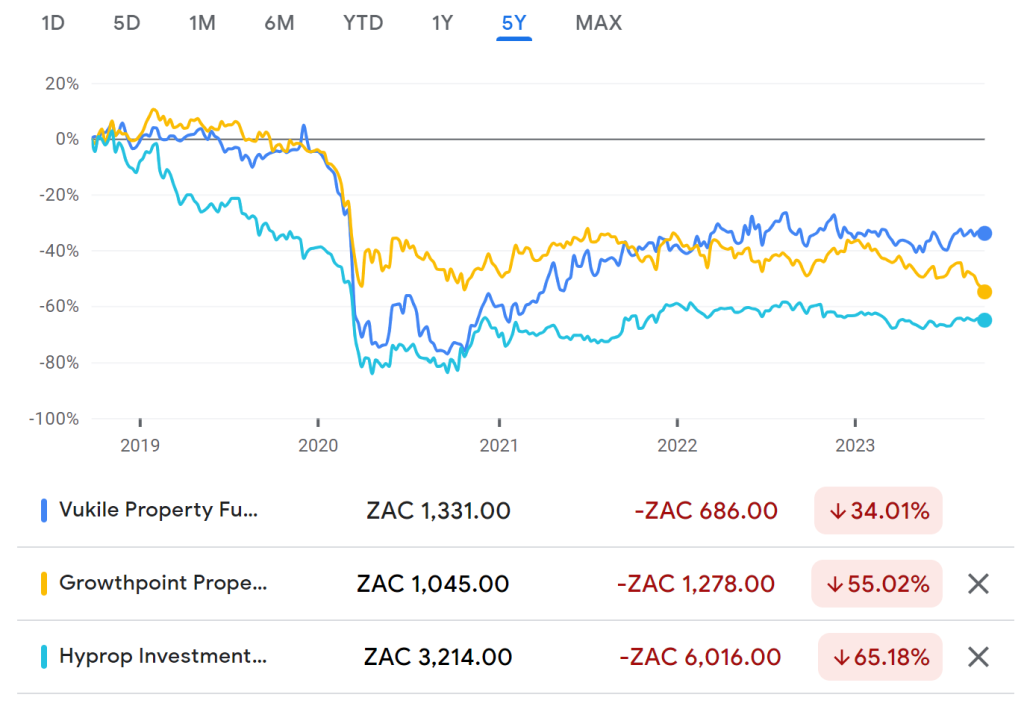

Most importantly, the guidance for FY24 is positive. The dividend per share is expected to grow by 7% to 9%. That is vastly different to what we’ve seen from the likes of Growthpoint and Hyprop.

This is why the chart over the last 12 months looks like this for the three funds:

Sadly, this is what the chart looks like over five years:

Little Bites:

Director dealings:

Des de Beer was clearly feeling flush for the latest purchase of shares, buying R8.2 million worth of shares in Lighthouse Properties (JSE: LTE).

The CEO of Sirius Real Estate (JSE: SRE) sold shares worth £450k. Interestingly, other directors / associates / senior execs bought shares worth a total of £19k.

A non-executive director of Richemont (JSE: CFR) has bought shares worth almost R2.3 million.

An associate of a director of NEPI Rockcastle (JSE: NRP) bought shares worth R1.27 million.

A founder of Brimstone (JSE: BRN) has bought N ordinary shares worth R165.5k.

OUTsurance Group (JSE: OGL) shareholders are looking forward to the final dividend of 78 cents a share and special dividend of 8.5 cents a share that the company has declared. The special dividend requires SARB approval and this approval hasn’t been obtained yet, so this may kick out the date for that dividend. The final dividend is unaffected.

If you’re wondering about your clean-out dividend from Advanced Health (JSE: AVL), there are “unforeseen circumstances” that have delayed the payment to 27 September.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

No interim dividend for Gemfields investors (JSE: GML)

The board keeps reminding investors that 2022 was a standout year

It’s rather interesting to note the words “lab-grown” in the opening paragraph of the Gemfields earnings announcement. Lab-grown diamonds have been a source of much debate out there. Lab-grown gemstones exist as well, yet nobody is really talking about it. There’s an acceptance that the market for gemstones enjoys very different pricing between natural and lab-grown gemstones.

I still believe that the key difference here is societal pressure to buy diamonds as an engagement present, driving demand for a more affordable solution. The same isn’t true for gemstones, which have always been a genuine “luxury” purchase that isn’t linked to a generally accepted milestone in our lives.

This doesn’t mean that the gemstone market doesn’t have its own challenges. Mining is always tricky, with recent announcements covering the disappointing production quality of emeralds at the Kagem mine and the decision to withdraw from the high-quality auction this year.

Looking at rubies, the company has started production on the second processing plant at Montepuez in Mozambique. This is the single largest ever investment by the group. This is expected to become operational in the first half of 2025 and the company calls it a “gamechanger” for processing the stockpile of rubies.

The year-on-year numbers tell a story of 2022 as a standout period, which is why there was an interim dividend last year that has not been repeated this year. Revenue has dropped by 20.5% and EBITDA has fallen by 30.5%. By the time you reach the bottom of the income statement and adjust for minority interests, profit attributed to the owners of Gemfields fell tremendously by 77%!

Even if you use adjusted HEPS (which excludes the impact of the negative fair value move on the Sedibelo PGM asset), there’s a drop of 54%. Whichever way you cut it, there’s a big drop off here that is a strong reminder that mining companies on a low Price/Earnings multiple can get very ugly. That multiple unwinds quickly as profits fall.

I must however point out that even though 2022 was a stellar year, this performance of HEPS of 0.8 US cents is even well below 2021’s number of 2.0 cents.

The share price is being helped out by rand weakness, as it is currently trading well ahead of 2021 levels:

Investec’s UK business is driving growth (JSE: INP | JSE: INL)

This has been a period of significant corporate activity as well

Investec has released a pre-close update dealing with the six months to September. There’s a significant difference between reported and constant currency numbers, with the bank pointing out 19% depreciation in the rand.

There were also quite a few corporate actions. The merger of Investec Wealth & Investment UK with Rathbones Group was completed recently. The property management company related to Investec Property Fund (now Burstone Group) was sold to that fund at a lucrative price in my opinion. The group has invested R6.7 billion in share buybacks. There are also distortions in the base period, like the distribution of the Ninety One stake.

This means that “adjusted profit” will be all over these results. Thankfully the difference isn’t too big though, unlike at a place like Discovery where the adjustments are huge. At Investec, HEPS is up by between 6% and 12% and adjusted earnings per share is up by between 8% and 14%.

Looking at the operations, the UK business should report adjusted operating profit that is at least 25% higher. The South African business is up by at least 5%, as the local business isn’t growing anywhere near quickly enough to offset the impact of rand depreciation.

Notably, the cost-to-income ratio has dropped below 60% as revenue grew ahead of costs.

The group credit loss ratio is expected to be at the upper end of the through-the-cycle range of 25bps to 35bps. Surprisingly, South Africa is at the lower end of the range of 20bps to 30bps and the UK is at the upper end of the range of 30bps to 40bps. When you dig deeper, this is because of better than expected recoveries in the local business and the interest rate and inflationary pressures in the UK.

Interim results are scheduled for release on 16 November.

Life Healthcare renews its cautionary (JSE: LHC)

Several months later, negotiations for Alliance Medical Group are still underway

Life Healthcare first made an announcement about a potential disposal of Alliance Medical Group back in February 2023. The company wasn’t looking to sell the business, but received interest from the market regardless.

Although it usually takes a while to negotiate a transaction, this one is starting to feel cold. We are now in September and the cautionary has been renewed once again, noting that there has been “significant progress” but there is still no certainly of a transaction on the table.

Bird flu is ripping through the poultry industry (JSE: QFH)

Quantum Foods has slipped into a loss-making position

Bird flu has bucked the semigration trend by moving from the Western Cape to Gauteng. Clearly, nobody warned it about the potholes.

Jokes aside, this is an incredibly serious problem. Quantum Foods’ Lemoenkloof layer farm in the Western Cape was smashed by the virus in April 2023 and now the farms in Gauteng and the North-West province have been affected. The value of the birds affected by the outbreaks is estimated to be R106 million, which is a huge number when you consider the market cap of Quantum Foods at R930 million.

This has triggered the release of a trading statement that reflects headline earnings slipping into a loss for the year ended September 2023. The company hasn’t guided how large the loss will be. The silver lining here is that the farms in the Western Cape and Eastern Cape haven’t been affected by the outbreak.

Of course, this comes after the recent update by Astral Foods (JSE: ARL) that showed how terrible things are in the poultry industry. Load shedding and consumer spending are already disasters. Bird flu is just the nail in the coffin.

Offshore capital allocation is also helping to grow the distributionper share

Spare a thought for Texton. The property fund has 89.3% of its SA portfolio in office properties. Trying to manage that beast in a post-pandemic world is a less appealing role than coaching the Wallabies. Still, with what the company calls an SME-focused strategy, the vacancy rate has dropped from 22.3% to 18.5% in the year ended June 2023. Rental rates are still under huge pressure though, with negative reversion of 14.3% in the office portfolio vs. -2.1% in retail and -8.2% in industrial.

In the UK portfolio, the primarily industrial portfolio features triple net leases and a weighted average lease expiry of over seven years, so this is a predictable income stream (in theory). The decrease in property valuations in the UK in response to pressure from rising rates was largely offset by depreciation of the rand.

The recent focus at Texton has been to invest in offshore funds. I don’t particularly like this fund-of-funds approach as it does little to remove structural discounts to NAV. Nonetheless, Texton has five investments in the US (combined market value R572 million) and one in the UK with a current value of R26.6 million. Rand depreciation obviously helps here.

The group sold five properties this financial year for R447.3 million. Debt was reduced by R420.8 million, of which the company describes R240 million as being a “permanent reduction” in debt. The effective interest rate on the South African debt has increased from 7.44% to 10.77%. In the UK, it jumped from 2.71% to 6.61%. This is why property funds have been under pressure.

The NAV per share has grown by 5.5% year-on-year to R6.1937 cents. The share price is just R2.50, so that’s a substantial discount to NAV of roughly 60%. Texton grew its dividend per share by 13.3% to 19.26 cents, which puts it on a traded yield of 7.7%.

The weak rand has been very helpful for Texton in this period.

Little Bites:

Director dealings:

Christo Wiese is taking a positive view on the Shoprite (JSE: SHP) share price, selling put options worth R226.4 million at a strike price of R226.45 and buying call options with a strike price of R236.18 for R236.2 million. The current share price is R241. He has basically used the put options (on which he only loses out if the price drops below R226.45) to almost fully fund the purchase of call options that are already in the money. The options expire in December.

An associate of a director of NEPI Rockcastle (JSE: NRP) has bought shares worth R1.5 million.

Finbond (JSE: FGL) has reminded the market of the plan to repurchase a massive 38.55% of shares in issue at a price of 29.11 cents per share. The current traded price is 38 cents per share. The circular for this repurchase will be posted to shareholders after the release of interim results (end of October) and prerequisite important milestones like a firm intention announcement.

Shareholders in Liberty Two Degrees (JSE: L2D) voted almost unanimously in favour of the scheme of arrangement and take-private of the company. It received 99.96% support at the general meeting.

Vukile Property Fund (JSE: VKE) has announced the appointment of a couple of financial heavy-hitters to the board. Jon Zehner joins the board with extensive global investment experience in real estate and James Formby is the former CEO of Rand Merchant Bank. These aren’t the kind of board appointments that you make to improve your lease terms or your occupancy levels. This is deep balance sheet experience.

This wasn’t the only banking-into-commerce announcement of the day. Marna Roets has joined the board of Zeda (JSE: ZZD) after extensive experience in banking, including senior roles in Standard Bank and Barclays Africa.

There’s another delay in the joint venture transaction for Mast Energy Developments, the subsidiary of Kibo Energy (JSE: KBO). The revised completion date is expected around mid-October 2023. The delays seem to be due to statutory processes, so theoretically all should still be fine.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I looked at some of the more interesting stories in a busy few days of news.

Capital Appreciation’s share price has done anything but appreciate this year, with sector peer PBT Group also under pressure.

Mustek is proof of how low expectations can help in this environment.

Bidvest is executing a bolt-on acquisition in Australia, a traditionally tough market for SA corporates.

Hyprop’s outlook for distributable income is as bearish as Growthpoint’s outlook, yet the share price performances are completely different because of relative valuation.

Astral Foods is in a perfect storm for the poultry industry, just like sector peer Quantum Foods.

Trellidor gave earnings guidance that really disappointed the market.

Southern Sun shows that swimming with the tide is much easier than swimming against it, with City Lodge finding things are a lot harder in its traditionally business-focused hotel footprint.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Motherclucker, it’s bad out there for poultry (JSE: ARL)

The Astral Foods update reads like the script of a horror movie

To be quite honest, I’m surprised that the Astral Foods share price only fell by around 11% for the day. There isn’t a single positive thread in the announcement, with problems everywhere you look. Take a swig of your coffee and prepare yourself.

When results were released for the six months to March 2023, it was already made clear to the market that load shedding and these macroeconomic conditions represent serious problems. Things have only gotten worse since then, with load shedding being a R1.9 billion burden for the full financial year ending September 2023 (vs. R741 million in the interim period). This includes R200 million in capital costs to try and address the issue. The rest of the costs include R45 million per month in diesel and other issues like production cutbacks and overtime shifts.

This brings us neatly to the next problem: enormous pressure on chicken prices to consumers. The announcement almost makes it sound like Astral may not be generating much gross profit, let alone net profit. We will need to wait for detailed results to confirm or deny this. Margins on chickens are notoriously thin, so it’s genuinely not impossible for load shedding plus consumer pressures to have smashed gross margin.

And finally, as we reach the end of this horror movie where the frightening character with the chainsaw is waiting behind the door, we find bird flu. In fact, we find the worst bird flu that South Africa has ever witnessed. The total cost of the outbreak is estimated to be R220 million.

It therefore shouldn’t surprise you that headline earnings per share collapsed into a loss of between R18.08 and R18.02. Interestingly, that’s pretty similar to the amount by which the share price dropped on the day of the announcement.

The balance sheet is geared to around 25% and there are no debt covenants. I bet the lenders are starting to wish that they had negotiated a few safety nets for themselves. Things desperately need to change for the poultry industry.

Margins at Choppies have been chopped (JSE: CHP)

It’s very tough out there for retailers

Even beyond South Africa’s borders, things are tough for retailers. It’s incredible to compare the results from Choppies to a company like CA&S Holdings (JSE: CAA), as it shows you how important it is to pick your position in the value chain. CA&S is killing it at the moment in terms of volumes growth, whereas Choppies experienced a drop in volumes on a comparable store basis.

For the year ended June, Choppies grew revenue by 6.4% but saw gross margin decline from 21.6% to 21.1%. Operating margin declined by 36 basis points to 4.26%, with expense growth outpacing revenue growth. Of course, net finance costs also increased.

With all said and done, HEPS fell 7.5% and no dividend was declared in this uncertain environment.

Dividends are back at Discovery (JSE: DSY)

As usual, there are also plenty of accounting adjustments

Discovery is a big fan of releasing “normalised” numbers that tend to look much better than HEPS reported in the good ol’ fashioned way. Before diving into the details, I’ll let you decide based on the share price performance whether the market is terribly interested in management’s view on normalised numbers. Here’s the key statistic: Discovery is currently trading at similar prices to 2015.

For long-term holders, the only benefit to being involved in Discovery has been free smoothies at Kauai.

I will therefore just focus on headline earnings, which increased by 5%. If you are happy to accept normalisation adjustments like removing the effect of interest rates, then normalised HEPS increased 32%.

A dividend of 110 cents has been declared. On the current share price of R147, that’s a yield of just 0.75%.

Another relevant metric is embedded value per share, which is R149.11. Return on embedded value was 13.2%, which I believe is why the share price is quite similar to embedded value. Still, there are other financial institutions I would own long before Discovery.

The Investec – Rathbones deal has completed (JSE: INP)

The bank now has a significant stake in a much larger UK operation

Investec tried bravely to build from scratch in the UK, but eventually the right way to achieve true scale was to combine the business with another decent-sized player. The merger of Investec Wealth & Investment in the UK with Rathbones Group makes all the sense in the world strategically.

The deal has now become effective, which means that Investec holds a 29.9% stake in voting shares and a whole bunch of convertible non-voting shares as well. The economic interest in the enlarged entity is thus 41.25%, so Investec has relinquished control but has gained exposure to a far more established and powerful business overall.

Investec has appointed two non-executive directors of Rathbones has part of the deal.

Losses narrow at MC Mining (JSE: MCZ)

The headline loss per share has improved by 55%

MC Mining has reported a loss for the year ended June 2023 of $4.4 million. Non-cash charges within that number are $3.7 million, so the cash loss is much smaller.

Although revenue increased by 91%, cost of sales grew by 96%. Margins are very thin, with gross profit of $3.6 million off revenue of $44.8 million. To add further pressure to the income statement, the company has been staffing up for the Makhado project. This has a five-year implementation plan and an estimated post-tax IRR of 37%.

The existing operations clearly can’t afford to fund the development of Makhado, which is why the company raised net proceeds of $21.4 million in a rights issue in November 2022.

The share price has been hammered this year, down 40%.

Remgro isn’t mincing its words about this environment (JSE: REM)

This is “probably one of the most difficult business environments” since Remgro’s inception

Johann Rupert isn’t called “Rupert the Bear” for nothing. There’s always a pragmatic and realistic undertone to company announcements in his stable, with the Remgro announcement being no different. Despite the intrinsic net asset value increasing 16.6%, the introductory paragraph doesn’t exactly inspire hope in the economy.

This was a year of dealmaking for the group, including transactions related to Mediclinic and Distell / Heineken. There were also changes to OUTsurance Group, Grindrod Shipping and Grindrod. In case you need a reminder of how ridiculously expensive these transactions tend to be, the detailed results disclose “abnormal merger integration and deal compensation costs” of a whopping R619 million at Distell just on the Heineken deal.

Remgro has reflected results from Heineken Beverages for two months of this financial year and things aren’t off to a great start. Even excluding amortisation and depreciation related to the acquired assets, Heineken Beverages contributed a loss of R19 million based on the consumer environment, load shedding and supply chain challenges. Ouch.

Touching on some of the private companies in the portfolio, Siqalo Foods saw a 14.2% decrease in headline earnings based on a drop in volumes in this environment and a 17.6% increase in input costs. My bearishness on consumer-facing stocks continues.

Lending money remains a decent activity in this environment, with Business Partners contributing R72 million to headline earnings vs. R70 million in the comparable period. The modest increase is thanks to higher interest rates, offset to an extent by credit impairments.

The fibre assets are the subject of a potential transaction with Vodacom, one which the competition authorities are not very keen on. CIVH saw a major jump in headline earnings from R47 million to R206 million, thanks to improved performance in the business. It’s not hard to see why Vodacom is hot for this deal.

I also have to highlight TotalEnergies, where headline earnings dropped from R1.076 billion to R54 million. Negative stock revaluations were part of the problem. Even without that, earnings fell 29.5% due to higher input costs and supply chain challenges. Oil isn’t always lucrative!

Long story short, intrinsic net asset value (NAV) per share increased by 16.6% to R248.47. The current share price of R157 is a discount of 36.8% to intrinsic NAV. The ordinary dividend is up by 60% to 240 cents.

Trellidor is a disaster (JSE: TRL)

Earnings have come in way lower than I expected

When Trellidor released a trading statement at the beginning of September that flagged an increase of at least 20%, it was clear that this was not the actual percentage growth that would be coming. FY22 was a shocking year, so earnings needed to be multiple times higher than in that year, not just 20% higher.

The good news is that earnings are indeed multiple times higher, with HEPS of between 4.16 cents and 4.24 cents vs. 0.40 cents in the base period. The very bad news is that this is nowhere near enough, as 2021 saw HEPS of 40.8 cents and 2020 was 13.8 cents. In other words, earnings are less than a third of what they were in 2020!

The share price plummeted 24.6%, which is what happens when there are desperate sellers in an illiquid stock. But even at R1.87, the earnings multiple is clearly ridiculous and the company cannot justify anything close to that level.

If you read the reasons for the earnings drop, there’s very little happy news here. Household budgets are under pressure and consumers are focusing on basics like electricity and water solutions, nevermind security. In the UK, customers focused on in-store shop fittings based on regulatory changes, not security. When you combine these revenue pressures with increased input cost pressures and the adverse Labour Court Judgement that saw the reinstatement of 42 employees with full backpay and benefits, Trellidor really is facing huge problems. As final insult to injury, increases in debt and prevailing interest rates drove a substantial increase in net finance costs.

One thing is for sure: the doors are a much safer investment than the company itself.

Little Bites:

Director dealings:

Normal programming appears to have resumed, with Des de Beer buying R1.9 million worth of shares in Lighthouse (JSE: LTE).

I generally avoid commenting on director sales related to vesting of share options, as that isn’t usually useful information for investors. The approach taken by a director of major subsidiaries at Novus (JSE: NVS) is worth highlighting though. He received R691k worth of shares and only sold R74k worth of shares. That’s a solid retention of shares.

Fred Robertson and various associated entities bought N shares in Brimstone (JSE: BRT | JSE: BRN) worth roughly R390k.

Collins Property Group (JSE: CPP) is in the process of taking its stake in Collins Property Projects to 100% by flicking U Reit Collins (a subsidiary of Castleview Property Fund JSE: CVW) to the top. In other words, Collins will issue shares to pay for the acquisition, taking the subsidiary of Castleview to a 21.78% holding in Collins group. To execute this transaction, some amendments to authorised share capital will be required and a circular has been sent to shareholders.

If you are interested in Omnia (JSE: OMN), then the presentation at the RMB Morgan Stanley Off Piste conference is a useful way to learn more about the company. You can find the deck at this link.

Microcap Telemasters Holdings (JSE: TLM) released a trading statement dealing with the year ended June. HEPS has swung from a loss of 3.73 cents to earnings of 0.81 cents. The share price is only 95 cents!

Rex Trueform (JSE: RTO) has been investing in property recently, with another deal now notched on its belt. There are various properties involved with a total value of R51.5 million, of which R44.5 million is being funded by debt. The acquisition yield is 9.5%. The rationale here is that Rex Trueform’s subsidiary is already occupying part of the properties for operational purposes, so they are securing that occupancy and earning a rental yield on the rest.

Shareholders of Kore Potash (JSE: KP2) approved the resolutions required for the issue of shares under the current capital raising efforts.

In a bid to double its facilities management operations in Australia, Bidvest has acquired Consolidated Property Services (CPS) for an undisclosed sum from private shareholders. CPS provides integrated property services to more than 145 sites across Victoria, New South Wales and South Australia. With current management having signed services agreements the company says the deal will be earnings and return accretive to Bidvest.

Zeder Investments subsidiary Zeder Financial Services, which holds a 92.98% stake in the Capespan Group, is to dispose of Capespan excluding its pome fruit primary production operations and the Novo fruit packhouse. The acquirer, 3 Sisters, is a special purpose acquisition vehicle owned and funded by Agrarius Agri Value Chain, which is administered and driven by 27four Investment Managers. Zeder will receive R511,39 million for its stake while minority shareholders will receive R38,6 million for a 7.02% interest. As part of the disposal, Zeder will conclude a strategic relationship with Capespan in respect of the marketing and distribution of Pomme Farming Unit’s crops.

The mandatory offer of R6.41 per enX share by African Phoenix Investments to minority shareholders closed on 15 September 2023 with acceptances in respect of 0.27% (495,846) of the company’s issued share capital. African Phoenix now holds a 49.07% stake in enX.

Mondi plc has entered into an agreement to sell its last remaining facility in Russia to Moscow-based real estate development company Sezar Group. In August 2022 the company announced the sale of Mondi Syktyvkar to UK’s Augmented Investments for a purchase consideration of €1,5 billion. However, the deal failed in June this year due to “lack of progress” in gaining the necessary approvals to complete the transaction. Sezar will pay a total cash consideration RUB80 billion (c. €775 million/R15,7 billion). Mondi intends to distribute the net proceeds from the disposal to shareholders.

OUTsurance has exercised an option to acquire, for A$42,5 million (R518,5 million), the remaining 2.65% stake in Youi held W Roos, a member of the team which started Youi in 2008. The company acquired the first 2.65% stake in March this year for A$36 million.

Telemedia, a subsidiary of Rex Trueform, has entered into two agreements to acquire properties. The Telelet portfolio, consisting of eight properties, will be acquired for R50 million and the acquisition of 27 Landau Terrace in Melville, a related party acquisition from the Bretherick Family Trust, for R1,5 million.

AngloGold Ashanti has agreed to sell its 50% indirect interest in the Gramalote Project in Columbia to Canadian miner B2Gold for a total consideration of up to $60 million (R1,1 billion). AngloGold Ashanti will receive a cash payment of $20 million at the transaction close with the balance dependent on project construction and production milestones. The Gramalote project is a joint venture between the two companies.

Unlisted Companies

Saint-Gobain Construction Products South Africa, the subsidiary of the French headquartered leader in light and sustainable construction, is proposing to acquire local specialist epoxy, polyurethane flooring and construction solutions company Technical Finishes SA. Financial details were undisclosed – the deal is pending regulatory approval.

Quilter plc is to launch an odd-lot offer to shareholders holding fewer than 200 ordinary shares in the company on 28 April 2023 and who will still hold those shares on 10 November this year. This applies to approximately 134,000 (67%) of the company’s shareholders, representing 1.21% of the total number of shares in issue. If all shares eligible to participate are tendered, Quilter will pay out £16,1 million for 17 million shares based on a price of 90.1 pence per share which represents a 5% premium to the market price.

OUTsurance will pay shareholders a special dividend of 8.5 cents per share payable on 9 October 2023.

A further 31,096,000 shares have been issued by Kore Potash following the approval by shareholders of the issue in respect of the conversion of convertible loan notes into equity by its chairman David Hathorn.

Argent Industrial has repurchased a further 325,487 ordinary shares representing 0.58% of the issued share capital of the company for an aggregate R5,11 million. The company is entitled to repurchase a further 10,82 million shares in terms of the general authority granted at the last annual general meeting.

Glencore intends to complete its programme to repurchase the company’s ordinary shares on the open market for an aggregate value of $1,2 billion by February 2024. This week the company repurchased a further 9,650,000 shares for a total consideration of £44,13 million.

South32 continued with its programme of repurchasing shares in the open market. This week a further 5,605,784 shares were acquired at an aggregate cost of A$18,68 million.

The JSE has warned Labat Africa that it may face suspension and possible removal of its listing from the bourse if it fails to release its Annual Financial Statements before 30 September 2023.

Three companies issued profit warnings this week: York Timber, Southern Sun and Astral Foods.

Two companies issued or withdrew a cautionary notice: PSV and African Equity Empowerment Investments.

Turaco has acquired MicroEnsure Ghana (to be rebranded as Turaco Ghana) from MIC Global. Financial terms were not disclosed. The deal sees the tech-enabled insurance company expand its footprint in Africa and will now operate in four countries – Kenya, Uganda, Nigeria and Ghana.

Incofin’s Rural Impulse Fund has sold its 28% equity stake in Rwanda’s Unguka Bank to LOC Holdings. Financial terms were not disclosed. Incofin first invested in the microbank over a decade ago and has help the company increase its total assets from US$14 million to $29 million.

Kuwait’s Foreign Petroleum Exploration Company (KUFPEC) has acquired a 40% stake in Egypt’s Nile Delta offshore Block 3 from Shell’s BG International. No financial terms were disclosed.

Lupiya, a Zambian neobank, has announced a US$8,25 million Series A funding round. The round was led by Alitheia IDF Fund and included INOKS Capital SA and the German Investment Bank KfW DEG.

Nigerian auto-tech firm Fixit45 has raised US$1,9 million to drive growth in its existing business and expand into Kenya and Uganda. The pre-seed round was led by Launch Africa Ventures with participation from Soumobroto Ganguly, David DeLucia and a number of angel investors.

Ghanian agritech Complete Farmer has raised US$10,4 million in equity and debt in a pre-Series A. The $7 million in equity was raised from The Acumen Resilient Agriculture Fund, Alitheia Capital via its Munthu II Fund, Proparco, Newton Partners and VestedWorld Rising Star Fund. Sahel Capital’s SEFAA Fund, Alpha Mundi Group’s Alpha Jiri Investment Fund and Global Social Impact Investments provided the $3,4 million debt funding.

Automotive technology platform Mecho Autotech has secured a US$2,4 million pre-Series A funding round. The Nigerian company raised the funds from Global Brain Corporation, Ventures Platform and Uncovered Fund.

Côte d’Ivoire SaaS e-commerce platform ANKA has raised a US$5 million pre-Series A extension round of debt and equity led by the IFC with participation from Proparco and the French Public Investment Bank. The $3,4 million equity investment from the IFC marks its first investment into the African creative sector.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")