This is a good example of the value that can be found on the local market

Full credit to those who bought Calgro M3 recently. The share price is up 44.9% this year, helped along by a combination of strong core results and a major share buyback programme. When a company is trading at a low valuation, share buybacks are a very powerful tool.

For the six months ended August, HEPS is between 73.18 cents and 84.58 cents, an increase of between 28.4% and 48.4%. This was driven by solid revenue growth (13.5%) and extensive share repurchases, representing 18.6% of opening share capital. The average repurchase price of R2.63 per share is way below Monday’s closing price of R4.55 per share.

Importantly, cash generated from operations is in line with profit after tax.

Detailed results are expected to be published on 16 October.

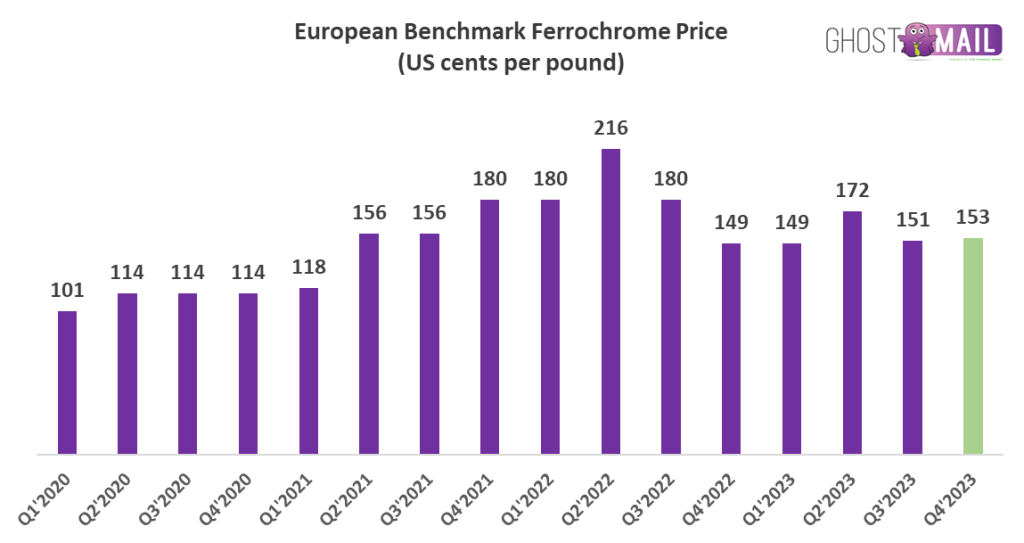

The company announces the benchmark ferrochrome price each quarter

Merafe announced that the European benchmark ferrochrome price for the fourth quarter of 2023 is 153 US cents per pound, up 1.32% from the preceding quarter.

To give you a better idea of the trend in the price during and after the pandemic, I pulled together this chart:

Over three years, the share price is up 230%! The picture is much less exciting over five years, with the stock down 24%.

Nampak has completed the debt restructuring (JSE: NPK)

This is a short, sweet and very important update

With the rights offer now out of the way and the equity side of the balance sheet brought to where it needs to be, Nampak has announced that the debt restructuring has been finalised with effect from 29 September.

Financials for the year ended September are due for release on 4 December.

Pick n Pay gets absolutely slaughtered (JSE: PIK)

Gradually, and then suddenly…

The Ernest Hemingway quote about bankruptcy refers. Although Pick n Pay is far from bankrupt, the group is making losses. Yes, headline losses. This is astonishing, with years of dicey strategy and the absolute strength of Shoprite combining to really hurt shareholders.

Next time you think grocery stores are defensive, just remember this chart:

CEO Pieter Boone is the fall guy, getting fired with immediate effect after 2.5 years in the job. I personally think that Boone’s strategic moves have been in the right direction, trying to address issues that were there long before his time. Anyway, every war has its casualties.

Speaking of long before his time, Sean Summers (who was famously caught for speeding in his Ferrari back in the 2006 bull market) is back in the top job, having run the group for 11 years in a previous stint. He was in charge at Pick n Pay when it was the grocery market leader in South Africa. Many disappointed customers later, that is certainly no longer the case.

I really do wish him luck. He inherits a mess. The core business is no Ferrari, with Pick n Pay SA managing growth in the 26 weeks ended 27 August of just 0.3%, or 0.8% on a like-for-like basis. That is truly awful compared to Shoprite. Boxer SA grew sales 16.1% overall or 4.2% on a like-for-like basis, with even Boxer’s like-for-like performance starting to give investors grey hairs now. A Ferrari F1 pit strategy, more like it.

The star of the show remains the clothing business, up 13.8%.

It’s so bad that the company now expects to report a loss even after adjusting for abnormal costs. Notably, they include diesel for load shedding as an abnormal cost. In other words, Pick n Pay is now making losses before load shedding.

Make no mistake: Shoprite is going in for the kill. Its opponent is a bloody mess who has dusted off an old-school coach to try and turn the fight around. I suspect that Summers is in for a shock when he sees how different the landscape is to when he was living the dream with Ferraris, lots of electricity and an environment of economic growth.

Schroder European Real Estate refinances debt (JSE: SCD)

It really is tight out there for property funds

Schroder European Real Estate has given us a strong indication of how difficult the debt markets are for property companies at the moment. To improve the margin on the five-year debt by 15 basis points, the company has included two unencumbered industrial assets in the security package. This also helped extend the facility by €4.5 million to €13.8 million.

The fixed rate on the facility is 5.3%, being the five-year euro swap rate (3.3%) plus the margin of 2.0%. The Dutch industrial portfolio to which the debt relates is yielding 6.2%. Shareholders are making a margin, but it really doesn’t leave any room for error, does it?

The company’s third party debt is €85.5 million across seven loan facilities, with a loan-to-value ratio of 31%, or 23% net of cash.

The weighted average loan term has increased by nine months to 2.6 years and the blended all-in interest rate is up 30 basis points to 2.9%. There are two more debt expiries due in 2024, so hold on to your seats.

Southern Palladium submits a Mining Right application (JSE: SDL)

This is a critical milestone for the project

Southern Palladium has submitted the Mining Right application to the Department of Mineral Resources and Energy for the 70% owned Bengwenyama Platinum Group Metals project. This is the next major step, kicking off many more workstreams if all goes to plan.

Resource modelling with results of the ongoing drill programme is also underway. The company recently increased the total Mineral Resource by 34%.

Trustco loses its battle with the JSE (JSE: TTO)

The Financial Services Tribunal has now put this issue to bed

This has been a long and protracted battle that has done nothing to win over the hearts of investors. In fact, it goes all the way back to a transaction in 2015!

In simple terms, the CEO of Trustco provided a loan to a private company that was reflected as an equity loan. These were the facts made available to shareholders at the time of approving an acquisition of the company from the CEO, which is clearly a related party transaction. The terms of the loan subsequently changed, which meant it was classified as debt rather than equity. The problem here is that Trustco never disclosed this fact to shareholders.

In other words, the net asset value of the company was nothing like the disclosure initially made to shareholders.

After much legal wrangling, the Financial Services Tribunal dismissed Trustco’s reconsideration application. This has therefore allowed the JSE to publicly censure the company.

The share price is down over 91% in the last five years, so there really isn’t much to love here.

Little Bites:

Director dealings:

In a pretty big show of faith, Alan Pullinger used the gross vested amount of share awards to buy R67 million worth of shares in FirstRand (JSE: FSR). He will settle the tax amount separately, which is why this is notable. There was also a prescribed officer (Emmarentia Brown) who took the same approach, with a purchase of R15.8 million in shares.

Stephen Koseff has sold shares in Investec (JSE: INP | JSE: INL) worth £1.2 million.

A prescribed officer of ADvTECH (JSE: ADH) has sold shares worth R850k.

Des de Beer has bought shares in Lighthouse (JSE: LTE) worth R614k.

Heriot Investments has transferred an 18.67% stake in Texton Property Fund (JSE: TEX) to subsidiary Thibault REIT, which is being listed on the Cape Town Stock Exchange. I’m envisaging layers of discounts here, as Texton is already at a very discounted price to book multiple.

In other news related to Texton Property Fund (JSE: TEX), the company has withdrawn the option for shareholders to choose to receive shares in lieu of a cash dividend. This is based on “current market conditions” which can only be a reference to the huge discount to NAV. Investors are tired of being diluted at huge discounts.

To give you an idea of how complicated large mining debt packages can be, Gold Fields (JSE: GFI) has entered into a sustainability-linked syndicated revolving credit facility agreement of up to A$500 million, with a A$100 million “accordion option” that allows the facility to be enlarged. There are no fewer than 10 banks in the loan syndicate, with Commonwealth Bank of Australia having acted as mandated lead arranger and bookrunner. The bank also acted as sustainability coordinator, as there are sustainability-linked KPIs for the term of the facility (five years).

The payments dates for the capital reduction tranches in Grindrod Shipping (JSE: GSH) are 26 October and 11 December. The first payment is $1.01598 per ordinary and the second is $0.63193 per ordinary share.

AECI (JSE: AFE) announced the appointment of Rochelle Gabriels as group CFO, joining from a senior finance role at Imperial (now part of DP World).

Labat Africa (JSE: LAB) is late in releasing its annual report and is in the naughty corner with the JSE.

Sebata Holdings (JSE: SEB) declared a special dividend of 25 cents per ordinary share. The share price closed 9.5% higher at R2.20.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Ascendis is still loss-making (JSE: ASC)

A delisting without a premium to shareholders will upset a lot of minority holders

The Ascendis share price hasn’t really gone anywhere this year. Neither has revenue, which is slightly down in the year ended June 2023. Gross profit margin fell by 145 basis points to 39.4% and the operating loss has improved from R758 million to R286 million.

That’s still a big loss when your market cap is R424 million.

The headline loss per share is -41.5 cents and the tangible net asset value per share is 81 cents. The share price closed at 67 cents on Friday.

It was a watershed year for the group, with the rights offer closing in August 2022, the Pharma business disposed of in October 2022 and the senior debt fully repaid in March 2023. The company notes that many operational improvements will only bear fruit in the 2024 financial year, which is why talk of a delisting doesn’t win any popularity contests among shareholders.

When you look at the individual business units, performance can vary wildly. The Consumer Health business declined 18% and the Medical Devices segment grew by 20%.

The good news is that the balance sheet is in much better shape, with cash reserves of R102 million and net working capital of over R300 million.

Delta Property makes a tiny dent in its debt (JSE: DLT)

This balance sheet elephant is being eaten spoon-by-spoon

Delta Property Fund has a loan-to-value ratio of 61.36% and a vacancy rate of 32.9%. These are metrics that usually end in financial disaster. The company is desperately trying to offload properties, but it’s really tough in this environment.

The latest announcement deals with the sale of two properties in Bloemfontein for a combined value of R26.1 million. The company is trying to exit Bloemfontein in its entirety. These proceeds will reduce the loan-to-value by just 15 basis points to 61.22% and vacancy levels by 60 basis points to 32.3%.

Kibo Energy has released interim results (JSE: KBO)

The focus isn’t on the financials, but rather on the corporate activities

Kibo Energy is putting together a portfolio of renewable energy assets. This isn’t just rooftop solar for residential complexes. The company is involved in all kinds of things, ranging from plastic-to-syngas through to biofuel and long duration storage.

The company is big on narrative and low on financial results right now, which is why much of the corporate activity has been around agreeing with debt holders to extend the term of the debt and/or convert the loans into equity.

Looking deeper, the company is busy with an optimisation study and laboratory test results at the ICON Park project, which focuses on plastic-to-syngas. The bio-methane Southport project in the UK has been delayed. There is also a dispute related to Shankley Biogas, with settlement negotiations underway.

Moving onto biofuel, there is currently a due diligence programme underway by TANESCO regarding a project in Tanzania. If all goes well, this will end in a power purchase agreement.

In long-duration energy storage, the company is busy with two projects and is targeting the South African market for obvious reasons.

Subsidiary Mast Energy Developments (MED) is another focus area, with a joint venture being put in place with an institutional investor. The completion date has been extended twice, so hopefully nothing falls over there.

As you can see, this is very much a set of promises rather than current financial results. At a share price of 2 cents a share, speculators only need apply.

Orion Minerals looks back on the year ended June (JSE: ORN)

It’s been a period of solid progress, with the share price up 26% over 12 months

This period was a big one for Orion Minerals, with the strategic funding package coming into play. This includes a convertible loan from the IDC, an early funding arrangement with Triple Flag Precious Metals and an equity investment from Clover Alloys as cornerstone investor.

With money in the bank, full focus is on developing the projects. At the Prieska Copper Zinc Mine, the mine development and construction phase has commenced. An updated Bankable Feasibility Study is the goal here, with substantial progress made. At the Okiep Copper Project, the granting of a mining right was achieved. This was the prerequisite for confirmation drilling and metallurgical sampling to complete the Feasibility Study.

There are a couple of other early stage projects within the group, but Prieska and Okiep are the focus areas for investors.

The focus isn’t on the financials at this stage in the life-cycle. Still, it’s worth noting that the operating loss increased from A$15.5 million to A$17.1 million.

Things have been quieter at Renergen (JSE: REN)

Do you remember when there were practically weekly updates from the group?

It feels like Renergen has been lying low lately. The share price is down around 30% this year and the days of regular updates (arguably too regular) seem to be behind us. The company does need to release quarterly updates though, with the second quarter highlights released to the market on Friday.

LNG production has increased by 88% vs. the previous quarter, so that’s good news. The other good news is that the environmental authorisation for the Virginia Phase 2 Gas Project has been received.

The focus, of course, is on helium production (or lack thereof at the moment). The company previously announced a leak in the helium cold box module prior to initial performance testing. The cold box has been successfully repaired off-site and has been delivered back to the site. The performance test is scheduled for November 2023, so there will hopefully be exciting news about the helium soon.

The cold box issue has not impacted phase 2 of the project, as they are being run in parallel.

The company also mentions “new gas anomalies” that have been identified from a drilling and exploration perspective. The announcement doesn’t really give the non-geologists any information on whether this is a big deal or not.

For the speculators out there, one wonders whether a good outcome from the November testing might inject some life back into this share price?

Rex Trueform moves into school sports streaming (JSE: RTO)

This is infinitely more interesting than acquiring another property

The recent acquisitive activity at Rex Trueform has been as exciting as watching a Rugby World Cup minnow get given an absolute hiding. I’m not sure whey they are so keen on acquiring properties in this market.

There’s now a far more interesting deal on the table, with the acquisition of a 35% stake in ITV Africa for R18 million, payable in cash. The company uses and distributes products, software and hardware related to sports broadcasts and streaming services. The words “artificial intelligence” get used a lot. The business was only founded in 2020, so it’s absolutely remarkable how valuable it became in such a short space of time.

And in case you’re wondering whether this is some kind of tech play that never makes money, the business generated a profit of R15.7 million in the year ended February 2023. This sounds like a smart deal for Rex Trueform and is a much, much better use of capital than buying properties.

Weirdly, Sasfin’s results are late (JSE: SFN)

We normally only see delays in results from messy small caps

Sasfin is by no means the poster child for success on the local market. The market cap is R700 million and the share price has shed over a quarter of its value in 2023. Still, it’s unusual to see a company of this magnitude miss the deadline to release financial results.

Sasfin’s results for the year ended June will only be published on around 13 October because of a delay in finalisation of the audit. That reason won’t exactly give investors a warm and fuzzy feeling either.

The company has at least indicated that headline earnings moved in the correct direction, notwithstanding higher impairments and costs. It would be very concerning if a banking group couldn’t grow earnings in this environment of higher interest rates and inflation.

Telemasters has swung into a profit (JSE: TLM)

But this is still a really marginal business

Telemasters Holdings has a market cap of R44.8 million. It doesn’t trade terribly often, as liquidity in a company like this is almost non-existent. The share price has barely gone anywhere for 5 years.

Nonetheless, I’m giving the results for the year ended June some airtime to show you how marginally profitable a business model can be.

This technology group (mainly connectivity and communications from what I can see) generated R64.2 million in revenue this year and an operating profit of just R2.3 million. In the prior year, revenue was R65 million and the loss was R500k.

Why is this company listed? I genuinely have no idea.

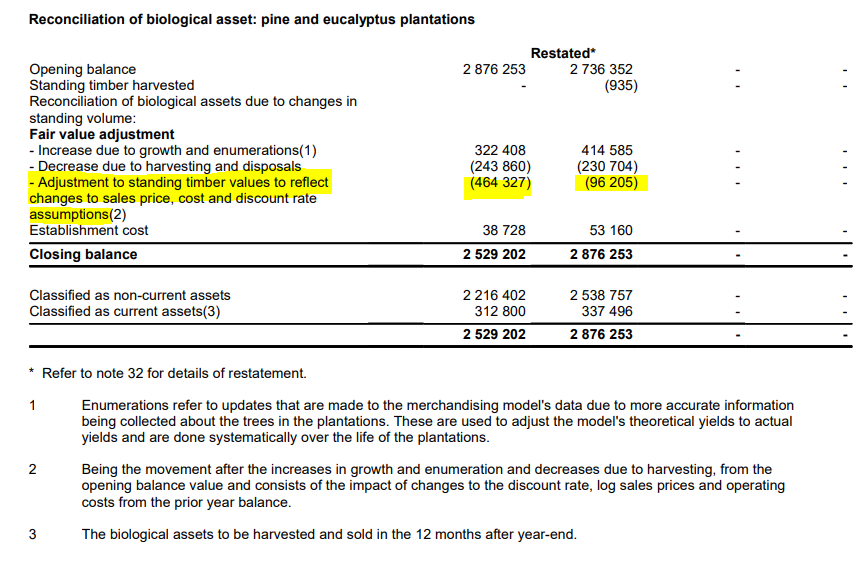

We now have full details on York Timber (JSE: YRK)

Fair value movements on biological assets cause huge swings

The financial results of York Timber tend to be very volatile. Although the actual business fundamentals aren’t exactly consistent either, the biggest source of volatility is the fair value movements on the biological assets i.e. the value of the trees themselves.

For example, the comparable period showed a fair value profit of R90.8 million and this period was a loss of R384 million. This gets recognised in cost of sales and thus affects gross profit, which is why that line swung from R590 million last year to a loss of R36 million this year. It also gets included in headline earnings.

To understand more about the fair value adjustment, we can refer to the notes to the financials. You’ll note that harvesting and disposals tend to be consistent, but the adjustment to values based on underlying assumptions was much worse this year.

The underlying assumptions that drive the fair value include log prices, operating costs, the costs to sell the logs, the discount rate and the volumes over the cycle of the trees. The discount rate is priced off the 10-year yield curve, which is why an increase in fixed income yields has a negative impact on equity values.

Moving on, the tough result for the year ended June 2023 hasn’t been helped by a drop in revenue of nearly 9.5%. Leaving aside the biological asset valuations, the drop in cash generated from operations of 50% shows that the core business is struggling. The change in biological asset valuation is simply the present value of the future expectations of the business, so there’s a double-whammy effect when things aren’t going well.

The share price is down roughly 20% this year.

Little Bites:

Director dealings:

An executive director of Medscheme, a major subsidiary of AfroCentric (JSE: ACT) has sold shares worth R254k.

A prescribed officer of ADvTECH (JSE: ADH) has sold shares worth R205k.

The CEO of Libstar (JSE: LBR) has bought shares in the company worth just under R50k.

Wesizwe Platinum (JSE: WEZ) released results for the six months to June 2023. The biggest movements have been in foreign denominated loans. The headline loss per share was 59.63 cents, much higher than 4.09 cents in the comparable period. The share price is 67 cents a share.

London Finance & Investment Group (JSE: LNF) has practically zero liquidity on the local market. I’ll therefore just give it a cursory mention, with headline earnings of 4.4p per share vs. a loss of 1.4p in the comparable period. A final dividend of 0.60p (roughly 14 ZAR cents per share) has been recommended for shareholder approval.

Finbond (JSE: FGL) announced that the acquisition of a 49% stake in Trustco Finance Namibia has once again had the fulfilment date extended, this time to 31 October.

OUTsurance Group (JSE: OUT) has received SARB approval for the special dividend, with a planned payment date of 16th October.

Buka Investments (JSE: BKI) hasn’t really done anything yet as a listed company. This is why the results for the six months to August reflect an operating loss of R1.7 million and no revenue. The listing has been suspended since February, as the company has not met the requirements for listing. Assets need to be injected into this cash shell to meet the requirements and the board hopes to announce a final transaction within the next four months. The ambition remains to grow into a sizable fashion business.

In a quarterly progress report, suspended company Conduit Capital (JSE: CND) noted that the financials for the year ended June 2022 (not a typo) should be finalised by October 2023. The company also announced that the 30% shareholding in Oraclemed Investments and related claims will be sold for R9 million.

Steinhoff (JSE: SNH) is a step closer to disappearing from the market, with the expiry of the two-month creditor opposition period. No opposition was filed. The listings in Frankfurt and on the JSE will now be terminated, with the latter subject to SARB approval.

Nonkululeko Dlamini has left the CFO role at Transnet to take up the CFO role at Telkom (JSE: TKG). Her previous experience also includes being acting CFO at Eskom and CFO at the IDC. It’s like playing state-owned bingo.

Sable Exploration and Mining (JSE: SXM) released interim results. There’s no revenue at all and the loss was R3.1 million, worse than a loss of R2.4 million in the comparable period. The company only has assets of R1.4 million. The company is in the process of being recapitalised via a rights issue.

Afristrat Investment Holdings (JSE: ATI) is a long and sorry tale of corporate pain. If you want to see how bad it is, you can read the latest quarterly progress report. The new news seems to be that Getbucks Limited (now called GetB) has been placed into liquidation. I’ve long since given up trying to even find a website for the company.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Afrimat released a voluntary trading update (JSE: AFT)

And the fact that it is “voluntary” tells you that this is a modest change in earnings

At a time when most mining and resources companies are reporting a major decline in earnings, Afrimat has reported a positive move in HEPS for the six months ended August. Although it is only a move of between 2% and 7%, it’s still a really great outcome compared to so many others in the sector.

The group’s strength lies in its diversity of commodity exposures, with the benefit clearly visible in this period.

Results are due around 26 October 2023.

Attacq shows the power of a focused strategy (JSE: ATT)

Distributable income per share has grown sharply and more growth is expected

With so many property updates recently coming into the market, the trend for me is clear. Broad exposure in this economy is very problematic. Focused exposure is still working.

Attacq’s Waterfall City area is doing the things, with the group reporting distributable income per share up by 14.5% for the year ended June 2023. Waterfall City is 57% of distributable income and grew by 27.6%. As you might be aware, the Government Employees Pension Fund has invested R2.7 billion directly into that portfolio. It’s like an oasis in the desert of Gauteng.

There’s other stuff in the portfolio as well, not least of all a 6.5% interest in MAS offshore. With MAS cutting its dividend, that’s not an ideal situation. The other headache is the business in the Rest of Africa, with the disposal of the interest in Ikeja City Mall hanging in the balance as the buyer is struggling to raise the funds.

I do wonder about the commentary about how “business diversification” will be a focus area going forward, with opportunities “complementary to the real estate portfolio” – whatever that may mean.

The dividend actually increased by 16%, ahead of distributable income as the dividend includes trading profit generated from the sale of sectional title units.

The loan to value ratio has increased by 10 basis points to 37.3%.

Notably, over 25% of the total energy mix is from renewable sources.

The really impressive part is that distributable income per share is anticipated to increase by between 8% and 10% in FY24. This assumes no dividend from MAS.

The share price closed 3% higher, putting it on a yield of just 6.8%.

Positive momentum continues at Barloworld (JSE: BAW)

This is another perfect example of why I prefer industrials in this environment

Barloworld has released a voluntary update for the 11 months to August 2023. Revenue from continuing operations is up by 15%, EBITDA is up by 13% and operating profit from core trading activities is up by 18%. Happiness all round, with the joy continuing on the net debt line which has dropped from R7.5 billion to R6.3 billion.

Equipment southern Africa grew revenue by 34% and operating profit by 17.3%. Operating margin fell 60 basis points due to the mix effect in favour of machine sales. Working capital increased to support demand but is expected to improve by year-end. The Bartrac joint venture grew profits by 56%. The blemish on these numbers is a drop in the firm order book from R5.7 billion to R3.7 billion.

Equipment Russia is obviously finding life really difficult, with revenue down 46%. Thanks to the revenue mix shifting in favour of aftermarket services which are much higher margin than new machinery, operating profit only fell by 8.7%. They’ve obviously also made progress in reducing costs. Operating margin grew from 11.3% to 19.2%. The Russian business is self-sufficient in terms of funding.

Equipment Mongolia grew revenue by 48.1% and improved margins as well, though the announcement doesn’t indicate to what extent.

Ingrain’s business is ultimately consumer-facing, so this is predictably where the pressure is. Revenue is up 12.1%, with export volumes and higher prices offsetting flat domestic sales. EBITDA is down 19.2% unfortunately, with an operating margin of 8.2% vs. the prior period of 12.4%.

As I’ve become used to with Barloworld, the balance sheet has been well managed.

Burstone needs a strong second half (JSE: BTN)

Negative reversions in SA and higher interest costs everywhere are hurting

In case you weren’t paying attention to the market, Investec Property Fund changed its name to Burstone Group after buying out the Investec property management company at an eyewatering valuation.

For the six months ending September, Burstone expects distributable income per share to be 4% to 5% lower. For the full year, they hope to achieve low single digit growth. That would be a pretty big turnaround, with much of it attributable to the timing of interest rate increases in the base year.

In South Africa, the year-on-year change in weighted average cost of funding is 40 basis points. In Europe, it’s 100 basis points (a huge move on a base of 2.1%).

The loan-to-value ratio is around 42%. Assets of R950 million were sold at a 1.5% discount to book value. The management company was acquired for R850 million (I told you it was eyewatering) and other investments in assets were R250 million.

Looking deeper, the South African portfolio is delivering like-for-like net property income growth of 2%, with negative reversions of 7%. The Pan European Logistics Platform is growing at 7% to 8% on the net property income level, with positive reversions, but earnings are expected to drop by 10% in rands (15% in euros) because of the impact of funding costs. Burstone’s share in the platform has increased from 64.15% to 83.15%, so there’s an increase of 18% in distributable earnings attributable to Investec despite the underlying platform suffering a drop.

No detailed commentary has been given about the Irongate fund management platform in Australia, other than the assets performing “well in a tough market” – read into that what you will.

Detailed results are due on 16 November.

Net of impairments, Capitec is less efficient (JSE: CPI)

I am questioning the way the market calculates the efficiency ratio

Capitec has released results for the six months to August and that’s always a big deal. Remember, this bank is priced for serious growth, so you would expect to see very strong numbers.

Net interest income is up by 17% and non-interest income grew by 25%. So far, so good. The fastest growing income line is actually funeral plan income, up 59%.

Credit impairments shot up by 62%, which isn’t unexpected in this environment. This means that net income only increased by 10%.

Operating expenses were up 14%, so operating profit before tax was just 6% higher. This means that operating margin has deteriorated. But if you read the commentary, you’ll see that the cost-to-income ratio has improved from 41% to 38%. Now, that’s only true if you ignore the impairments. On that basis though, the group would be incentivised to show efficiency gains by simply extending poor-quality loans and growing pre-impairment income.

Headline earnings per share grew by 9% and the interim dividend increased by the same amount.

The net asset value per share is R339.95 and the share price is R1,751. Does that premium to book sound right to you on growth of 9%, well below other banks in the peer group?

The market is desperate for any good news though, so the share price increased by 6.4%. I can only assume that people liked the dividend growth.

Emira’s occupancy and reversions have improved (JSE: EMI)

The company has released a pre-close update

In an update dealing with the five months to August, Emira announced that the local portfolio of retail, industrial and office properties has a total vacancy rate of 4.3%, which is better than 4.7% at March 2023. The focus has been on retaining tenants, with negative reversions of 5.5%. Again, that’s better than the 2023 number of -8.4%. The weighted average lease expiry is 2.6 years and the average annual lease escalation was 6.5%.

Looking deeper, retail vacancies increased from 3.1% to 3.3%. Reversions improved from -5.5% to -2.4%. Both trading density and footcount improved within the portfolio.

In the office portfolio, vacancies were up from 12.5% to 12.7%. Reversions improved from -14.8% (!) to -7.5%, a reminder of how bad things were and how tough they still are. With mainly P- and A-grade properties, it also gives a clue into how rough things must be for low quality office space.

Industrial vacancies went in the right direction, down from 2.1% to 90.6%. Reversions were still negative though, coming in at -6.4% vs. -6.5% in 2023.

The residential portfolio is a mix of directly held and indirectly held properties, as Emira has a 68.15% economic interest in Transcend. Across the residential portfolio, vacancies were 3.1% vs. 2.6% at March 2023. Residential units are being sold off, but disposals by Transcend are at a slower pace than budgeted because of the impact of higher interest rates. Emira has made an offer to Transcend shareholders to take the company private at R6.30 per share, so hopefully interest rates don’t cause too much pain to that value unlock strategy.

Notably, Emira’s disposal of Enyuka closed in July 2023 for aggregate proceeds of R641.5 million. A vendor loan of R130 million was provided to the purchaser, so proceeds of R511.5 million were realised.

The US portfolio is performing in line with expectations, although vacancies increased from 2.6% to 3.9%.

Emira’s loan-to-value ratio has improved from 44% at the end of March 2023 to 42% in August 2023. Once the Transcend offer closes, this is expected to increase to between 43% and 44%.

Results for the six months to September are due on 16 November.

This is hopefully the final loss-making year for EOH (JSE: EOH)

The first half of the year was impacted by debt levels

EOH would like you to concentrate on operating profit, as this is the performance before we consider the balance sheet. On that metric, there’s an increase of between 20% and 50% for the year ended July 2023, a very wide range to be giving the market two months after the end of the period.

The headline loss per share improved by between 53% and 62%. It’s still a loss though of between 17 cents and 21 cents, with the benefit of the equity capital raise only felt in the second half of the year.

For me, the biggest concern is that revenue from continuing operations only grew by between 2% and 4%. Although there was a big jump in operating profit, there were lots of other movements and once-offs. Investors cannot do well over the long term unless EOH starts producing better revenue growth, as this performance is below inflation.

To justify attention from investors in a high yield environment, EOH needs to show real growth in revenue growth i.e. ahead of inflation.

Results will be published on 18 October.

HCI gives an update on Namibian oil (JSE: HCI)

This is a classic junior resources situation, where updates are full of technical terms

In case you haven’t been following the HCI story, the company is a 49% shareholder in Impact Oil and Gas. This is a UK-based company that is a 20% participant in a block in offshore Namibia and a 18.89% participant in another block.

If you want to read the full announcement regarding drilling results, you’ll find it at this link.

In summary, the CEO is “very pleased” with the results. I usually skip to the management commentary in these announcements, as I didn’t study geology or mining engineering.

Heriot REIT’s floating rate debt is biting (JSE: HET)

The good news is that distributable earnings per share still went up

This was an important period for Heriot REIT, with the consolidation of Safari Investments (JSE: SAR) and thus the inclusion of investment property valued at R3.7 billion. This also contributed to the 22% uplift in net asset value per share, as the company was able to recognise an unrealised bargain gain.

To Heriot’s credit, the metric they focus on is distributable earnings per share. They’ve grown this by 4.2%, which is considerably lower than the growth in net operating income of 13.8%. This is because of the 350 basis points increase in the repo rate during this reporting period, with Heriot having only floating rate facilities. The timing of balance sheet movements means that Heriot’s average cost of borrowings increased by 239 basis points to 8.68%, leading to a lower distributable earnings per share than would otherwise have been the case.

The office segment is still struggling, with the company noting negative reversions and muted demand. The rest of the portfolio is doing better.

Very encouragingly and in stark contrast to the highly negative guidance given by other major property funds, Heriot is expecting the distribution per share for the year ending 30 June 2024 to increase by between 3% and 7%. This assumes a further increase in rates of 50 basis points in the next year.

The share price closed 10.20% higher at an implied yield of 7.9%.

Netcare is on track to meet FY23 guidance (JSE: NTC)

And encouragingly, margins are going in the right direction– with adjustments

Paid patient days at Netcare are expected to increase by 6.8% for the year ending September. Revenue is expected to be 9% to 10% higher, which is enough for positive operating leverage. I must point out that Netcare reports operating margin on a truly ridiculous basis, as they exclude diesel costs. We would all love to pretend that load shedding doesn’t exist, wouldn’t we?

On this “normalised” basis which I disagree with wholeheartedly, margin is up by between 125 and 175 basis points vs. FY22 at 17.2%.

If you need an indication of what adulting is like at the moment, maternity days are down (apparently in line with global trends) and the mental health segment is the fastest growing in terms of paid patient days (even after adjusting for the Akeso Gqeberha facility). What a world we live in.

Netcare is hoping to achieve 100% of its energy needs from renewable sources by 2030. Including a new power agreement, there are initiatives and plans in place to achieve 26%.

We’ve already heard from Astral Foods (JSE: ARL) and Quantum Foods (JSE: QFH) about the extent of the bird flu outbreak currently in South Africa. This is a very serious issue, affecting supply of chicken and eggs and likely to lead to price inflation in a type of protein that is a staple for South Africans.

At RCL Foods, the outbreak has affected 11 of the 19 sites in the inland region. Around 410,000 birds have been culled, with an estimated financial impact of R115 million.

Schroder’s NAV per share goes backwards (JSE: SCD)

The macroeconomic trends in Europe aren’t pretty for property

Schroder REIT announced a reduction in NAV per share of 1.8% this quarter. The trend this year has been negative, with property valuations under pressure as yields in Europe have increased. This is despite Schroder enjoying 100% indexation of rentals to inflation, giving us a timely reminder that property as an inflation hedge is a very dubious thesis.

The portfolio loan-to-value ratio is 31% based on gross asset value and 23% net of cash. This is roughly in line with March levels.

The market gave Spar’s update the thumbs up (JSE: SPP)

The group is clawing its way back from the abyss

I’ll start with the trading update for the 47 weeks to 25 August, in which group turnover grew by 10.6%.

Southern Africa was good for 5.9%, with grocery up 8.1% (below inflation of 10.1%) and TOPS down by 0.6% vs. a very high base. The combined Southern Africa result for grocery and liquor is 7.0%. They reckon it would’ve been 9% without the disastrous SAP implementation. What’s that saying about if my aunt had a certain something, she would be my uncle?

Turnover at Build it fell by 3.6%, because South Africans aren’t building it unless “it” is a solar installation. The pharmaceutical business grew 19.9% at least.

BWG Group in Ireland and South West England grew turnover by 8.5% in local currency. In Switzerland, turnover fell 3.4% in a challenging environment. In Poland, turnover increased by 5% in local currency. The rand is a great big stinking you-know-what, so all those numbers look much stronger when converted to rand.

I think that what the market focused on is the paragraph dealing with Poland, with Spar noting that it will engage in a process to dispose of that interest. It’s been an absolute disaster and Spar is stretched too thin, with the market appreciating the maturity of a decision to rather focus. This is especially important when you consider that the group is in breach of a leverage covenant that lenders have waived for now.

With a new management team in place, this is firmly a turnaround story that the market will watch closely. Where do you reckon this one is headed?

Investors are trying to flee Trellidor (JSE: TRL)

If there was decent liquidity, I think the share price would be a lot lower

Trellidor has released results for the year ended June. Revenue fell by 2.1% and believe me, that’s the most enjoyable number you’ll read about.

If we adjust for the costs of the extremely punitive Labour Appeal Court judgement, earnings per share was 3.7 cents this year vs. an adjusted base of 25 cents. Reported earnings per share last year was 0.4 cents because of that judgement, so the market was certainly expecting an uplift. The problem is that a return to previous levels of operating profitability now seems like a pipe dream, as the operations are really struggling and there was a massive 81.3% increase in net interest.

Unsurprisingly, there is no dividend.

If I’m going to highlight one silver lining, it may as well be that cash from operations of R39 million was in line with the prior year. Inventory levels were reduced in the second half of the year.

The share price has tanked 29% in the past five days.

Little Bites:

Director dealings:

The CFO of Sirius Real Estate (JSE: SRE) has bought shares worth £85.7k.

AEEI (JSE: AEE) has finally announced a resolution to the situation in BTSA. A subsidiary of AEEI holds 30% in BTSA and will dispose of that stake (structured as a share buyback) for R290 million. This has been the subject of a long dispute and arbitration, with the relationship between the parties having broken down.

The CFO of Stadio Holdings (JSE: SDO) will step down at the end of December to take a “career break” – the search is underway for a replacement.

Holders of Steinhoff preference shares (JSE: SHFF) should note that the company has released a cautionary announcement around a transaction related to these shares.

Mining exploration company Southern Palladium (JSE: SDL) has released its financial report for the year ended June. The income statement isn’t the focus area during the exploration phase, but it’s still worth noting a headline loss per share of A$0.08. This is better than the headline loss per share of A$0.18 in the comparable period. The group is focused on its 70% interest in the Bengwenyama Platinum Group Metal project and exploration to support a prefeasibility study and the lodgement of a mining right application.

Buka Investments (JSE: BKI) has announced that the headline loss per share for the six months ended August will be between 10.5 cents and 12.5 cents, which is much larger than the loss in the corresponding period of 6.72 cents.

RMB (FirstRand) via its Family Office Group Solutions business, has acquired a 20% stake in Genfin Holdings for an undisclosed sum. Genfin’s subsidiaries include Genfin Business Finance, which delivers alternative lending solutions for SMEs and Kanga Finance, a developmental credit provider. The equity investment and bespoke debt funding solution will be used to provide further growth capital to its subsidiaries.

African Infrastructure Investment Managers (Old Mutual) is to double its equity commitment to NOA Group having first invested $90 million (R1,6 billion) into the vertically integrated energy platform in November 2022. NOA aims to develop, finance and operate a portfolio exceeding 2.5 GW of renewable energy assets over time.

Invenfin, the venture capital arm of Remgro, has made a further investment of US$1,5 million in Root. Founded in SA in 2016, Root offers a low-code platform that empowers modern digital insurance products designed for direct, affinity, and embedded distribution at scale. The end-to-end insurance platform helps companies sell digital insurance products in Africa, the UK and in Europe. Funds will be used to accelerate its expansion plans in Europe and the UK.

Singapore-based Grindrod Shipping, 83% owned by Taylor Maritime Investments Ltd, a subsidiary Grindrod Shipping Pte Ltd, has entered into two agreements to acquire Taylor Maritime Management from Taylor Maritime Group and to buy Tamar Ship Management from Taylor Maritime Group and Temeraire Holding. Under the terms of the transaction, Grindrod Shipping Pte Ltd and Island View Ship Management Pte Ltd have agreed to acquire the companies for c.US$11,75 million with a maximum value not exceeding $13,5 million. The transaction will be financed via a combination of cash and the allotment of new Grindrod Shipping shares. The acquisition is subject to certain conditions and is expected to close before mid-October.

An agreement to settle the dispute between African Equity Empowerment Investments (AEEI) and BT Communications Services South Africa (BTSA) has finally been reached and AEEI will dispose of its 30% stake in BTSA for R290 million. The stake was sold in 2008 by BT Group plc (BT) for R27 million to AEEI as its BEE shareholder with BT holding an option to repurchase the stake upon the occurrence of certain events. In 2021 a dispute arose over the call option which has been the subject matter of an arbitration ever since. AEEI has “taken the decision to preserve shareholder value by unlocking cash reserves for growth and to limit further advisory and legal costs”.

Equites Property Fund subsidiary, Equites International, has disposed of a property currently let to Tesco Distribution, located on Dodwells Road in Hinckley, UK to Relif UK IB.V. The purchaser, part of the Realterm Europe Logistics Income Fund, will acquire the property for a purchase consideration of £29,75 million. The transaction is a category 2 transaction and so does not require approval by shareholders.

Currently in business rescue, Rebosis Property Fund is to dispose of a further four office properties to Katleho Property Investments for an aggregate consideration of R160 million. The properties were valued at R291 million in April 2023. The beneficial shareholder of Katleho is Heriot Investments.

Unlisted Companies

Red Rocket, an independent power producer established in 2012, has received a capital injection of US$160 million from management shareholders vehicle, Bill Kilgore Investments and an international consortium of clean energy investors comprising Inspired Evolution, STOA and FMO, the Dutch entrepreneurial development bank.

The Cape-based payment orchestration platform Revio has raised US$5,2 million in a seed investment round. Fintech fund QED Investors led the round with participation from Partech and existing investors Speedinvest, RaliCap and Everywhere VC. The startup helps merchants optimise their order to cash lifecycle. Funds will be used to scale Revio’s coverage across the continent and expand its capabilities to add value for customers.

Nampak has successfully raised R1 billion by way of a partially underwritten renounceable rights offer. The offer was oversubscribed with gross demand equating to more than 138% of the available rights offer shares. A total of 5,714,286 shares will be issued at R175 per share.

As part of its capital optimisation strategy, Investec Ltd acquired a further 101,332 Investec Plc shares on the open market at an average price of R105.48 per share.

Ascendis Health has advised shareholders that it has initiated a process to investigate and progress a potential delisting of the company from the JSE. Discussions have been entered into with CAN Capital IHC, an entity owned and controlled by Carl Neethling – the current CEO of Ascendis. Shareholders have been warned that while no offer has been made, if any offer is made, it is not expected to be at a significant premium to the current traded price of 69 cents per Ascendis share.

Optasia, a global fintech company in the Ethos Capital Partners stable, may consider a secondary listing on the JSE in the next 18 months as Ethos seeks to exit its investment. In November last year Brait, in which Ethos has an c.12% stake, hinted at the possible listing of Virgin Active in the medium to long term.

Luxe, the jewellery company which owns Arthur Kaplan and NWJ, was suspended by the JSE in August 2022 for failure to release its financial results. The company faced a further blow this week following a high court judgement placing it in liquidation. Earlier this year Luxe, without notifying the market, had its subsidiaries placed in liquidation. The application to have Luxe placed in liquidation was brought about by Richline SA, a jewellery manufacturer.

Several listed companies reported repurchasing shares. They were:

Gemfields has repurchased an additional 5,200,000 ordinary shares at an aggregate price of R3.21 per share. The repurchased shares will be held as treasury shares. The total number of shares in issue including treasury shares is 1,221,918,104.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 18 – 22 September 2023, a further 3,873,865 Prosus shares were repurchased for an aggregate €110,83 million and a further 340,108 Naspers shares for a total consideration of R1,1 billion.

Glencore intends to complete its programme to repurchase the company’s ordinary shares on the open market for an aggregate value of $1,2 billion by February 2024. This week the company repurchased a further 9,650,000 shares for a total consideration of £43,73 million.

South32 continued with its programme of repurchasing shares in the open market. This week a further 735,515 shares were acquired at an aggregate cost of A$2,44 million.

As part of Investec Ltd’s share repurchase programme, the company reported this week that it had repurchased 152,647 shares at an average price per share of R104.63. Since November 21 2022, the company has repurchased 13,78 million shares at a cost of R1,48 billion.

Profit warnings and cautionary notices issued this week

Seven companies issued profit warnings this week: Quantum Foods, York Timber, Sable Exploration and Mining, Wesizwe Platinum, Safari Investments RSA, Buka Investments and EOH.

Seven companies issued or withdrew a cautionary notice: Life Healthcare, Finbond, Ascendis Health, Conduit Capital, Ayo Technology Solutions, African Equity Empowerment Investments and Steinhoff Investments.

AgDevCo, a specialist investor in African agriculture, has invested in East African Magical Farms. The value of the investment was not disclosed but the funding will be used to expand into two additional farms in the Naivasha area in Kenya.

Nigerian fintech startup Risevest has acquired digital trading startup Chaka. Financial terms of the deal were not disclosed. The companies confirmed that both Risevest and Chaka will continue to trade as separate products.

All On announced a US$200,00 investment in Enerplaz PayGo Solutions. Launched in 2021, the clean energy company provides Energy-as-a-Service solutions to MSMEs and residences in the Niger Delta Region.

TotalEnergies EP Angola Block 20 has completed the sale of a 40% stake in Block 20 to Petronas Angola E&P for US$400 million. TotalEnergies will retain a 40% stake alongside Sonangol Pesquisa e Produção S.A. with a 20% stake.

The Emerging Africa Infrastructure Fund has committed €46 million to the upgrade and extension of the Autoroute de L’Avenir. The A1 motorway links Senegal’s capital Dakar, to the Blaise Diagne International Airport and was the first toll motorway in West Africa built under a public-private partnership scheme. The Government of Senegal and Eiffage SA (majority shareholder) own the toll road.

The Companies Act, No. 71 of 20081 (the Act) introduced the social and ethics committee (SEC) concept to South African corporate law, and with effect from 1 May 2012, mandated certain categories of companies to constitute and maintain a SEC.

Initially, some companies constituted SECs merely as a tick-box exercise to comply with the Act, with SEC detractors viewing the committee as a training ground for new non-executive directors (NEDs) and a ‘waiting room’ for NEDs wanting to ‘scale down’ responsibilities. However, the growing importance of stakeholder inclusivity and the widespread acceptance of ESG and sustainability (ESG+S) have placed the SEC and its evolving role in the spotlight.

In recent years, many key South African role players have taken note of the SEC’s increasing importance, including the Department of Trade, Industry and Competition (DTIC). On 1 October 2021, the DTIC published the latest draft of the Companies Amendment Bill for public comment (the Bill).2 The Bill proposed, inter alia, several SEC-related amendments to the Act, which included the following, relating to public companies –

• A SEC report in a prescribed form3 must be presented at public company annual general meetings (AGMs), and must be approved by way of an ordinary shareholders resolution.

• Where the SEC report is not approved, engagement with shareholders who voted against the SEC report will be required and, within a period of four months, a statement on the outcome of such engagement must be published on the company’s website and SENS (if listed). Such statement will also form part of the SEC report to be presented at the company’s next AGM.

• Public company SEC members must be appointed, or reappointed, as the case may be, at each AGM of the company.

• Public company SECs are to include no less than three directors, with the majority of such directors to be independent and not to have been involved in the day-to-day management of the company during the previous three financial years.

• SEC vacancies are to be filled within 40 days.

While there appears to have been little progress in the legislative process, with public comments on the draft Bill still being considered by the DTIC, this is nevertheless a good time to consider further refinements to the SEC construct, including the points highlighted below.

SEC functions

Regulation 43(5) of the Companies Regulations (Reg 43(5)) sets out the statutory functions of the SEC, whilst the King IV Report on Corporate Governance for South Africa, 2016 ‘broadens’ the SEC’s role to include “oversight and reporting of organisational ethics, responsible corporate citizenship, sustainable development and stakeholder relationships”. The matters set out in Reg 43(5)(a) were broad to start off with and have, over time, ‘unofficially’ expanded in scope. Considering that Reg 43(5) has been in effect since 2012, it is proposed that the prescribed matters be formally updated to account for recent developments, such as the increasing imperative of addressing the climate crisis, whilst simultaneously empowering the SEC to provide strategic leadership on these items, instead of limiting itself to mere compliance oversight.

ESG and sustainability

ESG+S has increasingly become a key business imperative for companies to consider and incorporate in their strategies, operations and reporting. In South Africa, much of a company’s responsibility for governing ESG+S practices and related matters falls on the SEC. Despite initially being categorised as non-financial factors, ESG+S has proven to possess rising financial implications for companies (many investors take ESG+S performance into consideration when deciding whether to invest in a company). Given the ever-expanding scope of ESG+S factors for SECs to consider and the increasing amount of time required to be spent thereon, as well as the growing financial implications associated with ESG+S compliance (and non-compliance), it is suggested that greater structure and certainty be given to the SEC’s ESG+S function, either in Reg 43(5) or in the next iteration of the King Code.

Cross committee membership

Cross committee membership encourages pollination of thinking between members of the different board committees and gives such members a deeper understanding of the risks and opportunities faced by the company, as well as the strategies to address these. It might be worth-while to consider the merits of mandated cross committee membership (i.e. for at least one audit committee (AuditCom) or risk committee member to also serve on the SEC).

Qualifications, skills and experience

The Bill proposes that the Minister may prescribe the minimum qualification requirements for SEC members. Considering the wide ambit of the SEC’s mandate, it may make sense to prescribe the qualification requirements for a minimum portion of the SEC, with it being sufficient for other members to have SEC-relevant experience. This approach will help to ensure that the SEC comprises a mix of relevant qualifications, skills and experience.

Despite not having been promulgated yet, the Bill’s proposed amendments to the Act should be welcomed. However, to truly ensure the SEC’s future relevance, key aspects, such as its functions and members’ competence requirements, would need to be updated.

1.Section 72 of the Act, read with Regulation 43 of the Companies Regulations, 2011 (‘Companies Regulations’) provides for the establishment of SECs. 2.The 2021 draft contained some departures from the prior version, published on 21 September 2018. 3.The SEC report must detail (i) how the SEC performed its functions; (ii) how the SEC fulfilled its mandate; and (iii) that there were no instances of material non-compliance to report.

Johann Piek is a Director | PSG Capital

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Share incentive schemes have, for some time, become a key mechanism to attract, retain and reward top talent. This holds true not only for listed companies, but also for unlisted companies – including those in the private equity sector.

Fund managers often want to incentivise key management in their portfolio companies with an equity slice in the business, thereby creating an alignment of interests to grow profits and, ultimately, returns.

The fortunes of participants in share incentive schemes have, unfortunately, been somewhat mixed over the years, given the volatility in macro-economic conditions, as well as the impact of ‘big bang’ events, such as the 2008 global financial crisis and the more recent COVID-19 pandemic. Many incentive schemes have ended up under water, leaving fund managers to consider what, if anything, can be done to reset these schemes to deliver the incentives that they sought to achieve.

Given the complexity of the relevant legislation, the tax consequences of amending and resetting incentive schemes need to be carefully considered. As a starting point, it is important to understand whether the scheme is ‘restricted’ or ‘unrestricted’. Broadly speaking, a ‘restricted’ equity scheme is one in which the participants are restricted from selling their equity shares (either for a period of time or as an outright prohibition), and/or where the participants may, for any reason, be forced to sell their equity shares at less than market value (for example, if they are dismissed).

In contrast, an ‘unrestricted’ scheme is one in which the participants are able to freely sell their equity shares, and where the participants cannot be forced, under any circumstances, to sell their equity shares at less than market value. Pre-emptive rights (also referred to as rights of first refusal) in favour of other participants or other shareholders that are exercisable at market value, as well as forced sales at market value, do not taint the shares as restricted for tax purposes.

From the participants’ perspective, the distinction between a restricted and unrestricted share scheme is fundamental, as each one is taxed differently. In an unrestricted scheme, the scheme shares are treated as having ‘vested’ in the participants’ hands upfront (at least for tax purposes), with any difference between the market value of such shares and the consideration paid therefor being subject to income tax. All future growth in these scheme shares would then typically be subject to capital gains tax (CGT), not income tax. Conversely, restricted scheme shares are only treated as ‘vesting’ for tax purposes on the earlier of disposal or when all the restrictions attaching to the share are lifted, with the difference between the proceeds/market value (as the case may be) of the shares and the initial consideration paid therefor being subject to income tax at such time only.

Resetting restricted and unrestricted share schemes that are currently underwater may also result in varied tax implications. For example, swapping one restricted share for another restricted share of a different class (with enhanced or reset participant rights) would not necessarily result in any immediate tax consequences for the participants. Instead, the newly acquired restricted shares would simply be subject to income tax upon disposal or vesting, as the case may be. Swapping an unrestricted share for another unrestricted share of a different class would, on the other hand, typically result in the value of the newly issued share being subject to income tax in the participants’ hands upfront. This is clearly not ideal from a cash flow perspective, but at least all future growth in these newly acquired shares would be subject to CGT, not full income tax.

Ad hoc special dividends may, in some cases, be used as a mechanism to reset scheme values, as these dividends would simply be subject to dividends tax at 20%, not full income tax. Obviously, however, this would move the cash flow burden to the company itself, which may be undesirable.

Like many areas of tax, the rules governing share schemes are complicated, and very widely drafted. Resetting these schemes, although done with the best of intentions, can result in very costly and unintended consequences if not carefully navigated.

Brian Dennehy is Director of Tax | Webber Wentzel

This article first appeared in Catalyst, DealMakers’ quarterly private equity publication.

The universe of Exchange Traded Funds (ETFs) is broad, offering investors many different ways to invest in the market.

Not only are there various different sector and weighting methodologies available, but Satrix ETFs offer South African investors a way to make perhaps the biggest decision of all: offshore vs. local exposure.

As we reflect on ETF performance in 2023, Siyabulela Nomoyi of Satrix joined The Finance Ghost to look at topics like:

Offshore vs. local performance and the impact of the start date for that analysis, including the currency effect;

The importance of understanding the underlying stocks in an ETF and their relative valuations; and

Relative performance of local ETFs.

The Ghost couldn’t help but slip in his ongoing request for a retail sector ETF, an index that the JSE really needs to add to the local market.

To understand more about ETFs and how they can be used in your portfolio, enjoy this podcast brought to you by Satrix.

Disclosure Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this podcast (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Is the Ascendis story coming to an end? (JSE: ASC)

A consortium led by Carl Neethling might be taking the company private

Hot on the heels of its trading statement, Ascendis announced that a consortium led by Carl Neethling is in discussions with the company regarding a potential take-private. The crummy news for minority shareholders is that if there is an offer, it is “not expected to be at a significant premium” to the current traded price of 69 cents a share.

No formal offer has been made at this stage. It’s very unusual to see an offer at a low premium, so it will be interesting to see how this plays out.

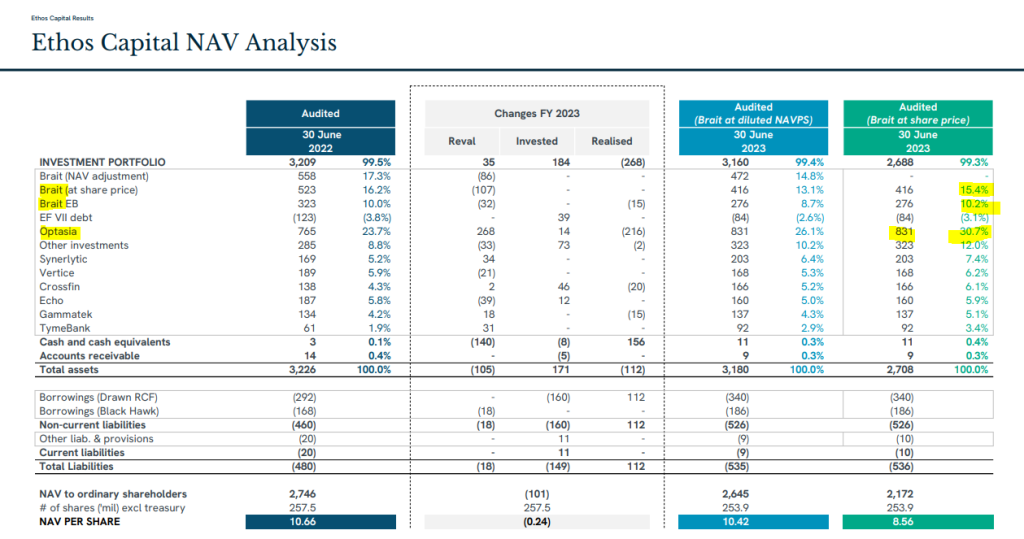

Net asset value per share inches higher at Ethos Capital (JSE: EPE)

Pressure on the Brait share price has let the team down

For the year ended June 2023, the net asset value per share of Ethos Capital increased by a paltry 0.8%. This is based on the Brait share price rather than Brait’s underlying net asset value. MTN Zakhele Futhi hasn’t helped either, with major drops in the listed portfolio that offset the 14% return in the unlisted portfolio.

I must point out here that the unlisted portfolio is the opinion of management, whereas the listed portfolio is the opinion of a market. You can figure out for yourself which one carries more weight. It does help that there was an equity deal in Optasia that helps confirm the value of the largest of the unlisted investments, driving a small uplift in the average valuation multiple in the portfolio.

Here’s the summary of net asset value per share, in which I’ve highlighted Brait and Optasia to show the combined contribution of 56.3% to group assets.

If you want to dig into this in great detail, you’ll find the results presentation at this link.

The current share price is R4.25, so the discount to the NAV per share of R8.56 is over 50%.

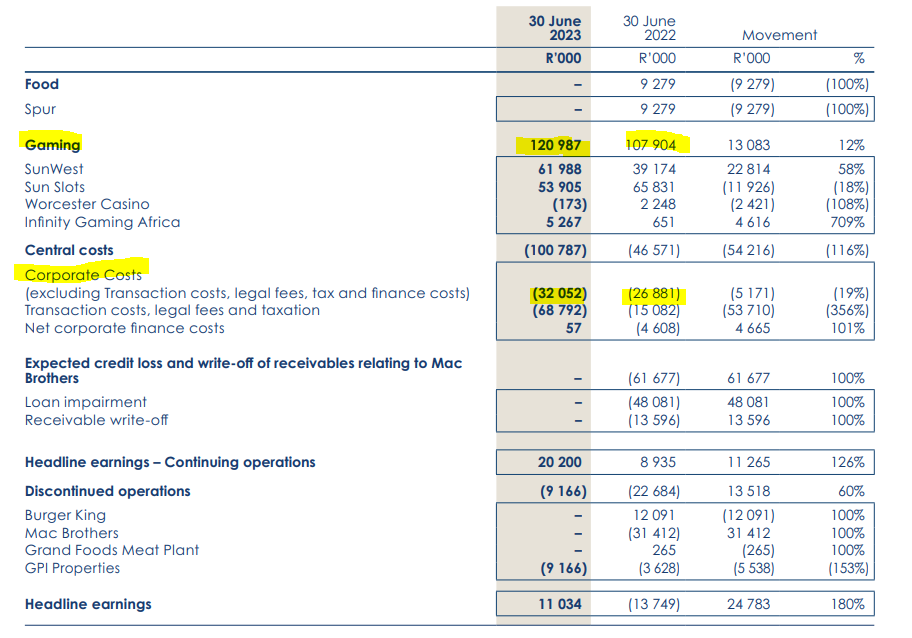

You have to read Grand Parade’s numbers carefully (JSE: GPL)

There are many once-offsand distortions

Grand Parade’s numbers are tricky. There has been a great deal of corporate activity, including the unbundling of the stake (steak?) in Spur and various restructuring transactions. The base period includes a number of discontinued operations, like Burger King and the disaster that was Mac Brothers.

The split between continuing and discontinued operations doesn’t even tell the right story, as Spur gets included in continuing operations and so do loans to Mac Brothers.

To help you look through the noise, I’ve included this table showing the contributions to headline earnings. Gaming grew by 12%, with around half of that amount in absolute terms going into increased corporate costs.

The group is now exclusively focused on the gaming sector, including “robust oversight” of its existing gaming investments, whatever that practically means.

Investment flows at Old Mutual are a sign of the times (JSE: OMU)

Inflation and high interest rates are eating into savings

Old Mutual has released results for the six months ended June. This includes the adoption of IFRS 17, which means major distortions and accounting restatements.

I’ll try and ignore the IFRS nonsense and focus on the operational metrics instead. Life APE sales excluding China grew by 14%. They were only up 1% including China, as the base period included product sales that were subsequently discontinued in anticipation of regulatory channels.

The value of new business margin increased to 2.6%, putting it within the medium-term target range of 2% to 3%.

Although gross flows grew by 17%, net client cash outflows of nearly R7.3 billion were worse than the prior period because clients needed to access their funds to survive these economic conditions. Despite this, funds under management grew by 6% to R1.3 trillion, supported by equity market performance.

Return on group equity value was only 10.5%, which is way below the performance of banking groups in South Africa. Return on embedded value in the Life and Savings business was 13.9%. The group uses a couple of other metrics, like return on net asset value of 11.9% and core return on net asset value of 13.1%.

I don’t really care which of those metrics you use, performance is still well below our local banks. Growth also isn’t exciting, with results from operations at Old Mutual only up by 3%. In this environment, would you rather be lending money to consumers or hoping they save and invest with you?

The group equity value per share is R18.806 and the share price is R12.10, so the market is quite correctly valuing Old Mutual at a discount. This discount is why the year-to-date share price performance of over 15.5% actually beats local banks. Like everything in investing, it comes down to valuation.

The Rebosis fire sale continues (JSE: REA | JSE: REB)

The selling price is way below the recent valuation

As you are probably aware by now, Rebosis is in business rescue and has been executing a “public sale process” to try and sell as many properties as possible to pay down the debt.

The latest such sale is to Katleho Property Investments, a subsidiary of Heriot Investments. The portfolio being sold is four office buildings, three of which are in Ekurhuleni and the other is in Midrand. The portfolio was valued at R291 million on 1 April 2023.

Perhaps that was an April Fool’s valuation, as the actual selling price is R160 million. Based on net operating income, the implied yield is a whopping 26.8%. Rebosis has practically given these properties away. A desperate seller is a terrible thing.

Unless you’re the buyer, of course.

York Timber has given far more detailed guidance (JSE: YRK)

At least cash from operations is positive, if we are looking for silver linings

York Timber has released an updated trading statement that gives a much tighter range for HEPS. Importantly, it also gives guidance for EBITDA and cash from operations.

I’ll start with HEPS, which is shouting timberrrrrr all the way down from 53.30 cents to a loss of between 73.27 cents and 77.00 cents for the year ended June. If we strip out various items (including biological asset fair value movements), we find EBITDA coming in between 58% and 63% lower than the comparable period. Cash from operations is also on the right size of zero at least, despite being between 48% and 53% lower.

Even without the biological asset fair value movements that cause big swings in earnings, this was a poor period for York.

Wesizwe Platinum nosedives (JSE: WEZ)

The headline loss is much higher than the comparable period

With unprotected strike action and ongoing pain in the PGM sector, this was never going to be a happy financial update from Wesizwe Platinum. Still, the extent of the loss is quite breathtaking, especially as this is an interim period.

For the six months to June, the headline loss per share has vastly deteriorated, coming in at between 59.22 cents and 60.04 cents. The loss in the comparable period was just 4.09 cents.

Keeping in mind that the share price is only 76 cents, this isn’t looking good.

Little Bites:

Director dealings:

I usually ignore sales by directors related to vesting of share options. Half of the Woolworths (JSE: WHL) announcement related to those types of sales. The other half was very interesting, with a director of the holding company selling shares worth R1.7 million and a director of the operating subsidiary selling shares worth a massive R19.1 million,

A director of Liberty Two Degrees (JSE: L2D) has sold shares worth R1.57 million.

A director of Novus (JSE: NVS) has sold shares worth R608k.

I’m not sure these are director dealings in the truest sense of the word, so I’m showing them separately. Three directors of Nampak (JSE: NPK) were announced as having followed their rights in the rights offer. Andre van der Veen (part of A2 Investment Partners) is obviously the largest, with an investment of over R72 million.

Heriot Investments has been busy. Not only has the company bought the Rebosis properties at a bargain price, but it has also transferred a 10.02% stake in Safari Investments (JSE: SAR) to its subsidiary, Thibault REIT Limited. This is only relevant because Thibault has applied for a listing on the Cape Town Stock Exchange.

AYO Technology (JSE: AYO) renewed its cautionary announcement related to the settlement agreement with the PIC. The company says that the parties have made significant progress in finalising the terms of the settlement agreement to ensure compliance with the JSE Listings Requirements.

Conduit Capital’s (JSE: CND) disposal of subsidiaries CRIH and CLL continues to hang in the balance, with the closing date for fulfilment of conditions extended yet again, this time to 31 October.

Basil Read (JSE: BSR) is currently in business rescue. The CEO of the company has resigned, so that doesn’t do much to help with stability. An acting appointment has been made internally.

Sable Exploration and Mining (JSE: SXM) has a share price of just 6 cents per share. It’s therefore not ideal that the headline loss per share for the six months ended August is between 65 cents and 75 cents per share! It’s worse than the comparable period, despite the company claiming that the loss has decreased. The maths is not mathing at this company.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")