Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

No dividend at AfroCentric (JSE: ACT)

HEPS has fallen sharply

In the year ended June, AfroCentric could only grew revenue by 2%. That’s not going to cut it, with HEPS down by 34%. The dividend of 34 cents a share last year is just a distant memory as no dividend will be declared for the year ended June 2023.

Although once-off restructuring costs were part of the story here, the lack of revenue growth is the real concern. The pharmaceutical cluster normalised after heightened trading during 2022, which explains the year-on-year move. The medical scheme administration business isn’t exactly a rocketship either, but put in a steady performance with a 2.6% increase in revenue.

The strategic focus will be on bedding down the Sanlam relationship after the group took a 60% controlling stake in AfroCentric in May 2023.

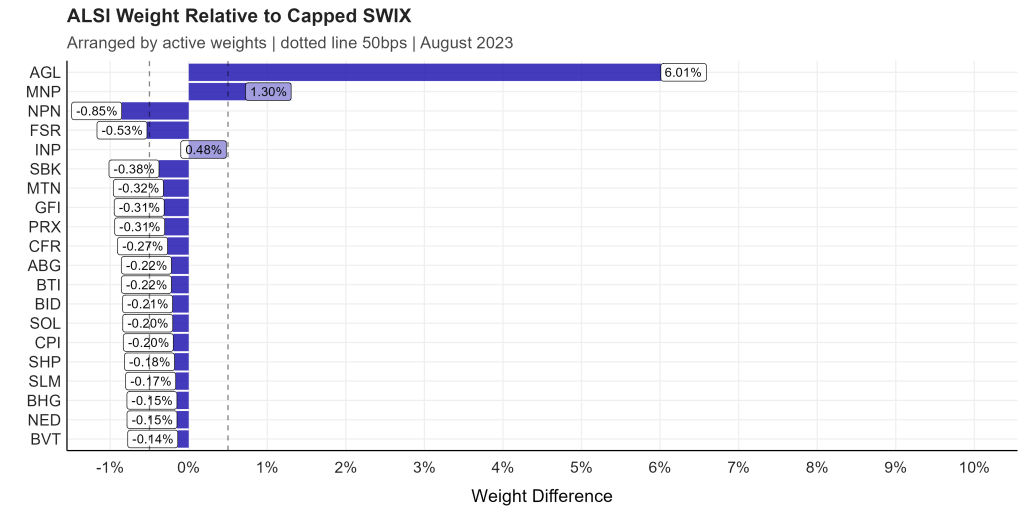

AngloGold sells its stake in Gramalote (JSE: AGL)

Bidders were non-existent, so the joint venture partner is buying it

AngloGold is selling its 50% stake in the Gramalote Project for a total consideration of up to $60 million. The buyer is B2 Gold Corp, which already owns the other half. Both parties wanted to sell Gramalote and couldn’t find any buyers willing to make an acceptable offer, so B2 Gold was basically the only buyer in town for this stake.

AngloGold will receive a payment of $20 million at closing date, with the balance dependent on various project and production milestones at the project. The deal unlocks some cash for AngloGold and allows the group to focus on its core assets.

Fairvest delivers a pre-close update (JSE: FTA | JSE: FTB)

Investors have been brought up to speed on the year ending September 2023

Fairvest has a portfolio with a gross lettable area split of 49.2% retail, 25.8% industrial and 25.0% office. That split would’ve looked good before the pandemic. As we all know though, office property hasn’t been a happy story in the aftermath of Covid. The vacancy rate in that portfolio is 11.5% vs. 4.4% in the retail portfolio and just 1.2% in industrial.

It’s not surprising that recent property disposals have been focused on office properties, although a couple of retail and industrial sales have also been in the mix.

The group level result is vacancies of 5.3%, positive rental reversions of 2.3% and a loan-to-value below 34%. The guided distribution per B share is between 40.5 cents and 42.0 cents. The B shares closed the day at R3.28, so that’s a yield of roughly 12.6% based on guidance.

If you would like to read the full presentation, you’ll find it here>>>

Gemfields completes its third best year for emeralds (JSE: GML)

It’s just a pity that the final auction of higher quality emeralds won’t work out

At the latest auction of commercial quality emeralds, Gemfields’ offering contained a higher than usual mix of lower value grades. Recent emerald production at Kagem has been of lower quality and quantity than usual, which is why the company has withdrawn from the higher quality emeralds auction scheduled for November.

This means that emerald auctions are now finished for Kagem for 2023, with total auction revenues of $90 million. That’s the third best auction year ever for Kagem, slightly below $92.3 million in 2021 and way below the bonanza in 2022 of $149 million.

That tough base in 2022 has put the share price under pressure recently, with investors realising how quickly the price/earnings multiple is going to unwind this year.

Mondi finds a way out of Russia (JSE: MNP)

The Syktyvkar asset has found a buyer

Mondi’s share price closed 2.6% higher after the market received the happy news that the overhang related to the Russian operation may soon be a thing of the past. It’s been a struggle to sell the Syktyvkar asset, but there’s now a deal with Sezar Invest LLC to dispose of the business for RUB 80 billion. That works out to roughly R16 billion.

The very good news is that regulatory conditions have been met, so this deal is ready to close provided the buyer can make the various payments. There are six monthly instalments to be paid, with the first due at the end of September 2023. The asset will transfer after four payments and the final two will be secured by a letter of credit.

Mondi plans to distribute the proceeds to shareholders once all instalments have been made.

The Russian buyers are absolute winners here, picking up the asset for a profit before tax multiple of 1.7x. Who says that (war) crimes don’t pay?

Oceana gives the market a peek at its performance (JSE: OCE)

Management hasn’t given any overall commentary though

Usually, a voluntary trading update gives the market a useful summary from the management team about the group level performance. This isn’t the case at Oceana, where it dives straight into the segmental performance.

In canned fish and fishmeal (Africa), Lucky Star grew volumes by 8% in the 11 months ended 27 August 2023. In the last five months though, volumes fell 5% because of base effects. Concerningly, margins are under pressure as pricing increases weren’t enough to offset inflationary increases in energy, tin can and other costs. The good news is that local canning production volumes increased by 15%, so there’s a lot of inventory to support demand going forward. Now the company just needs to see more demand!

South African fishmeal and fish oil saw a 32% increase in average rand selling prices over the period. Sales volumes were 8% lower and production volumes fell 24%.

Overall, the local operations incurred costs attributable to load shedding of R28 million.

Moving on to the US, they have electricity there but they also had fewer fish. Based on the 21-week season, landings were 5% lower than the prior period. Not only are there fewer fish, but the fish also had lower fat content, so fish oil yields have dropped. Strong operating inventory levels helped mitigate this impact, with sales volumes up 49% for fishmeal and 28% for fish oil. With major supply problems in Peru, a demand-supply imbalance caused fishmeal prices to rise 9% in dollars and fish oil prices to jump by 38%. With the rand being weaker and the Hurricane Ida insurance proceeds having been received, there’s a good outcome here for Oceana.

In the wild caught seafood division, horse mackerel sales volumes were slightly lower for the 11-month period and hake sales volumes fell by 38% due to a reduction in catch rates and days at sea. The impact of high fuel prices won’t help here either. As a mitigating factor, the weak rand supported export pricing.

Looking at the balance sheet, Oceana took the proceeds of R370 million after tax from the sale of the cold storage business and put them towards settling term debt in South Africa of R550 million. Term debt in the US was successfully refinanced.

Capital expenditure jumped from R154 million to R380 million, with investment in vessels and production facilities after fishing rights were renewed for 15 years. R50 million of a committed R115 million has been spent on the canned meat facility in the St Helena Bay region.

Detailed results are due on 27 November.

A new chapter begins for Prosus and Naspers (JSE: PRX | JSE: NPN)

Bob the Empire Builder is on his way out

With the capitalisation issue to undo the ridiculous cross-holding now complete, Prosus no longer holds any Naspers N ordinary shares. With that deal completed, the share buyback programme has now resumed.

That’s not the biggest news that the company released on Monday. No, that honour definitely goes to the “mutual agreement” that will see CEO Bob van Dijk step down as CEO. He will remain as consultant to the group until September 2024, although it’s hard to imagine why based on his track record.

Having been CEO of Naspers since 2014 and of Prosus since it listed in 2019, Bob earned an absolutely eyewatering amount of money while presiding over perhaps the most convoluted corporate structure in South African history.

His successor on an interim basis is Ervin Tu, the Chief Investment Officer at Naspers. Tu is an ex-Goldman Sachs and Softbank dealmaker and is based in San Francisco, so you can be sure that he loves a good revenue multiple when buying businesses.

Will it simply be more of the same for the company? Time will tell.

Volumes under pressure at RFG Holdings (JSE: RFG)

This is example number 593 of consumers cutting back

For the 11 months to the end of August, RFG grew revenue by 10%. Price inflation was 13.5%, so volumes were down. There were also forex movements and mix changes (as well as the acquisition of Today), so the group helps us out by confirming that volumes actually fell by a substantial 7.7%. The good news is that the first half of the year was a decline of 8%, so the second half has improved to a decrease in volumes of 6%.

Canned fruit and vegetables are under particular pressure based on consumer demand. The pie category is doing well thanks to the Today business. Overall, regional revenue is up 11% for the period with huge inflation of 16.4% and volumes down 6%.

In the international segment, revenue grew 6.7% but volumes fell 12.9% as the world normalised after the Greek peach crop failure in 2021. Operational pressures at the Cape Town port are a serious concern, with shipping lines bypassing the port in some cases due to waiting times.

And of course, against this backdrop of lower volumes, there is still load shedding to contend with.

Results for the year ending September will be released on 22 November.

Zeder sells most of Capspan to Agrarius (JSE: ZED)

The pome farming unit isn’t part of the deal

Zeder has been talking about a value unlock for as long as I can remember. The disposal of the 92.98% stake in Capespan is part of that strategy, even though Zeder is hanging onto the pome farming unit and will put in place a deal with Capespan for marketing and distribution of the related crops.

The minority shareholders in Capespan are also selling, so the buyer is getting 100% of Capespan. Speaking of the buyer, you’ve likely never heard of Agrarius Sustainability Engineered, a JSE-listed special purpose investment vehicle with a R10 billion Shariah-compliant note program. Managed by 27four Investment Managers, this is a good example of how the JSE offers various different listing structures.

Zeder’s interest in Capespan was valued at R1.046 billion as at February 2023. The disposal value is only R511 million but Zeder is quick to point out that this is in line with the previously reported value excluding the pome unit that is being retained. Zeder plans to distribute the proceeds to shareholders once the cash is received, with an effective date for the disposal expected to be in January 2024.

Little Bites:

- Director dealings:

- Three directors of property fund MAS (JSE: MSP) collectively bought shares worth R3.66 million.

- The CEO of African Rainbow Minerals (JSE: ARM) bought shares worth R3.1 million.

- The spouse of a co-founder of Mr Price Group (JSE: MRP) bought shares in the company worth R924k.

- Brimstone (JSE: BRT) co-founder Fred Robertson bought N ordinary shares in the company worth around R112k.

- Quilter (JSE: QLT) is making an odd-lot offer. It’s an unusual one, as the threshold for the offer is a holding of 200 shares rather than 100 shares. The company is offering a 5% premium to the market price to be calculated based on the 5-day VWAP until 20 October, but don’t get too excited. There’s another unusual twist in the tale, with the offer only being eligible to shareholders who held fewer than 200 shares on 28 April 2023 and who will still hold those shares on 10 November 2023. Based on how I read this offer, opportunistic plays to buy up 199 shares and lock in some beer money won’t work.

- The mandatory offer by African Phoenix and concert parties to shareholders in enX Group (JSE: ENX) at a price of R6.41 per share was unlikely to be a showstopper when the current share price is R8.10. Indeed, only holders of 0.27% of the issued shares were happy to accept that price, taking the offerors to a collective holding of 49.07% in the company. It’s a very thinly traded stock, which must be why some people were happy to take the liquidity opportunity and move on.

")

")

")

")

")