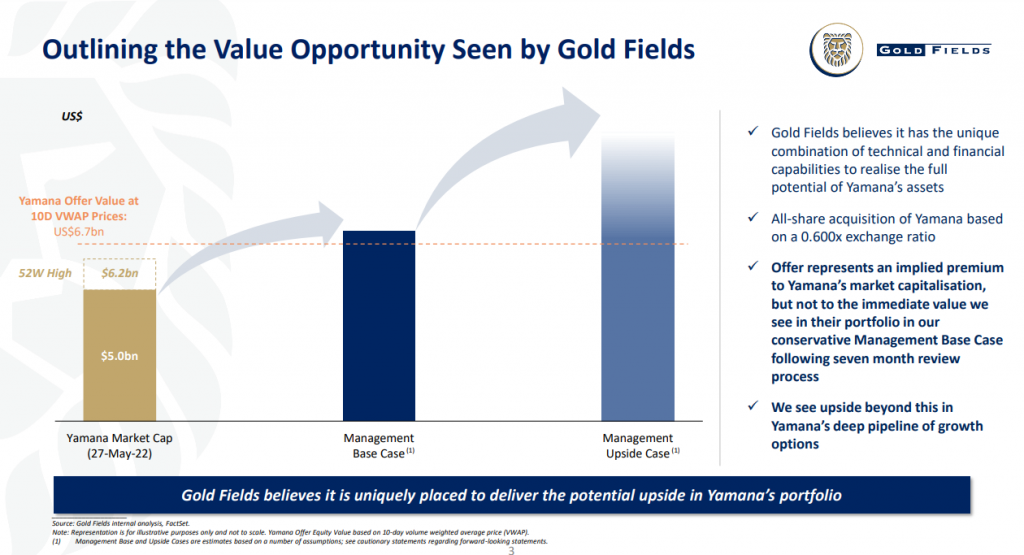

Gold Fields really upset the market at the end of May when the company announced the major acquisition of Yamana Gold, an offshore business trading at a much higher multiple than Gold Fields. To help cheer shareholders up, the company has announced an update on its dividend and listing strategies, as well as rationale of the deal. The first bit of good news is that the revised dividend policy is to pay 30% to 45% of normalised earnings each year, with the 2023 payout ratio expected to be at the top end i.e. 45%. Another important update is that Gold Fields will list on the Toronto Stock Exchange as part of this deal, which will hopefully attract international investors. In terms of Yamana itself, Gold Fields sees this as a strategic fit that will bring high-quality, long-life assets into the group in attractive jurisdictions. There are still major shareholder approvals required (two-thirds of Yamana Gold shareholders and at least 75% of Gold Fields shareholders), so the deal is by no means a certainty. To help get it across the line, Gold Fields has released a detailed presentation that you can find at this link. As a Gold Fields shareholder, I’m hoping this chart from the update comes to fruition:

Capital & Regional Plc has completed the £21.65 million sale of the Walthamstow residential development to Long Harbour. This project is found at a community shopping centre in London. The proceeds will be used to reduce debt. This is a classic “precinct” strategy, with the residential development expected to drive stronger performance at the retail centre. The share price showed its appreciation with a 7.6% rally.

Super Group has raised R500 million in a debt issuance under its Domestic Medium-Term Note Programme on the JSE. It could’ve raised far more if it wanted to, as bids of over R1.7 billion were received for the tranches.

FirstRand is in the process of proposing a scheme of arrangement with a standby general offer to holders of the B preference shares in the bank. If you are the proud owner of such a preference share, I suggest you refer to this circular for more information.

Sebata Holdings is now trading under cautionary after noting that the company is in negotiations for a potential disposal of one or more businesses.

Earnings updates

None – come back tomorrow!

Share buybacks and dividends

As there were no other buybacks or dividends, I may as well remind you that British American Tobacco and Glencore are buying back shares on a daily basis.

Notable shuffling of (expensive) chairs

The expensive chairs stayed where they were today.

Director dealings

The ex-Naspers financial director (who still sits on the board) exercised share options and disposed of shares to the value of over R149 million. To put that number in perspective, if he invests it in fixed income instruments at just 7% per year, the interest would be R200k per week in round numbers. Aah well, back to work the rest of us go.

Capitalworks is a long-standing partner of listed food business RFG Holdings. After the private equity investment house bought R195k worth of shares at the end of June, it has topped up the position with a further purchase of nearly R154k. This is announced on the market because two of the RFG Holdings directors are from Capitalworks.

There’s yet another purchase of shares in Kaap Agri by one of the directors, this time to the value of nearly R72k.

The financial director of Dipula Income Fund has bought nearly R54k worth of Dipula B ordinary shares.

The management team of The Foschini Group has been granted chunky forfeitable share awards, which is a common long-term incentive mechanism. Buried deep in the announcement is a note that the company secretary sold a batch of shares previously granted, putting over R233k in the bank in the process.

Unusual things

Renergen is still using SENS to provide an unofficial online course to anyone who wishes they had studied engineering. The latest update is the introduction of “gas to plant” at the Virginia Gas Project, which sets the scene for final commissioning workstreams over the coming weeks. Commercial operation is anticipated once customer sites are ready to begin accepting product, which Renergen expects towards the end of July 2022.

If you would prefer to study geology online rather than engineering, Orion Minerals is an ongoing source of technical updates about the Prieska project. I usually skip to the quote from the CEO, which is the only bit I really understand. In this case, he continues to sound very happy. Orion is working on an early production strategy at Prieska and latest drilling results seem to be supportive of this.

Old Mutual’s shareholding in Quilter has now moved below the 5% mark, a symbolic step in the Old Mutual story after Quilter was separated from Old Mutual in 2018, rebranded and listed as a UK wealth investment business.

Pembury Lifestyle Group has renewed its cautionary announcement as the company is still trying to pull enough money together to just settle the bills from its auditors. Once that is sorted out, audits need to be done for the 2019 – 2021 financial years. A property in Northriding that was originally built as a school has now been converted to a commercial building, which should provide the cash flows needed to pay the auditors. The designated advisor and company secretary have also resigned, so things are just going SO well there.

Mauritian investment company Lonsa Group has acquired window and door manufacturer Swartland through its Lonsa Everite special purpose vehicle for R1.3 billion, cementing a platform to build a leading building materials group in Sub-Saharan Africa within the next five years.

Lonsa Everite Proprietary Limited (“Lonsa Everite”), together with Legacy Africa Capital Partners (“LACP”) and Swartland management, have acquired 100% of the issued shares in Swartland Investments and Swartland Insulation (“Swartland”), as well as the freehold properties from which Swartland operates and is adjacent to, from Swartland Group Proprietary Limited and a third-party seller.

The transaction value of circa R1.3 Billion was funded through a combination of Lonsa Group Limited, Lonsa Everite and LACP shareholder equity, a vendor deferred payment agreement and R660 million of debt financing provided by Nedbank Limited.

The acquisition, after receiving approval from all relevant competition authorities and reaching financial close, became effective on 1 July 2022 and includes all of Swartland’s existing operations and assets, as well as the recently established insulation manufacturing business.

Swartland is an industry leading manufacturer and supplier of wooden doors and windows, aluminum doors and windows, garage doors as well as XPS insulation and cornices, and operates in Southern Africa, the United Kingdom and the United States of America. You can see the product range at this link.

With well-known brands such as COL, Kenzo and Hydro, Swartland is a notable and complementary addition to Lonsa Everite’s existing Nutec and AAC brands, significantly widening the Lonsa Everite offering of building material supplies.

In addition, the acquisition rationale was further strengthened through strategic initiatives and synergies identified by Lonsa Everite. This includes expansion of both Lonsa Everite and Swartland’s footprint in the rest of Africa, optimisation of Swartland’s distribution capabilities by leveraging off Lonsa Everite’s established distribution network, providing a greater basket of goods to building supply retailers through complementary products from both Lonsa Everite and Swartland and expansion of Swartland’s route to market utilising e-commerce platforms such as Takealot and others to come.

Robin Vela, Chairman of Lonsa Everite, said:

”The acquisition of Swartland talks to our strategic objective of establishing the Lonsa Everite Group as the preeminent industrial building materials manufacturer and distributor on the African Continent. This will be achieved through a combination of astute acquisitions, leveraging and realising synergies between group entities and organic growth. Both Lonsa Everite and Swartland are highly cash generative, profitable businesses with long established brands (over 80 and 70 years respectively) presence in the South African building materials market. We have only just gotten started and there is more to come.”

Kgosi Monametsi, Managing Director of Legacy Africa Capital Partners, commented:

‘We are delighted to again have partnered with Lonsa Group Limited and Everite Management in this transaction. The investment into Swartland is not only a financially attractive one but also fulfills our Funds objectives from a transformation perspective as well as the contribution to society more broadly as Swartland is a significant employer and job creator.”

Jurgen Stragier, Chief Executive of Lonsa Everite, added:

“Following the acquisition of Everite in May last year by the consortium led by Lonsa Group Limited, the business has developed an ambitious growth strategy, starting with the acquisition of other leading building material businesses with respectable heritage and strong brands. Swartland is certainly among the top of this select grouping of companies, and Lonsa Everite is excited at the prospect of growing a bigger and better Group through this acquisition. It provides a strong starting point for what will be a leading building materials Group in Sub-Saharan Africa within the next 5 years, driven by great people delivering great products to the market.”

Lonsa Everite was advised by Birkett Stewart McHendrie (BSM), a South African corporate advisory firm with a boutique culture that specialises in M&A, restructurings and distressed advisory, transaction services and capital raising. The founding partners have worked together since 2012, completing sophisticated financial advisory services for clients ranging from family businesses, private equity funds and JSE-listed companies through to large multinationals. You can find out more about BSM at this link.

Learn more about Lonsa Everite:

Lonsa Everite was incorporated as a special purpose acquisition vehicle in 2020 when Lonsa Group Limited (“Lonsa Group”), LACP and Everite Management acquired the business and assets of Everite Proprietary Limited (“Everite”) from Group Five Limited. Lonsa Group is a Mauritius incorporated investment vehicle established in 2004 with interests in the energy, industrials, logistics and property sectors in Southern Africa. Everite was established in 1941 and is the leading industrial manufacturer of a range of niche building products for the South African building industry’s commercial, industrial and residential market sectors. Everite is known for its comprehensive range of Nutec Roofing and Cladding Solutions, which includes fibre cement roofing, cladding, ceilings and building columns amongst others. Everite is also the license holder for various leading alternative building systems and technologies.

Learn more about Swartland:

Swartland was established in 1951 and operates as a multifaceted building supplies manufacturer. Swartland is one of the largest manufacturers of quality windows and doors in the South African building industry. Their national distribution footprint comprises 7 depots and more than 42 031m² of warehouse space, situated in all major economic centers in South Africa. Swartland also own the Boskor Sawmill in Tsitsikamma which supplies FSC certified pine timber. This has allowed for synergies within the business as Swartland can now ensure a constant and quality supply of pine to their various product lines. It also allows them to secure the best cut of the timber which was not a guarantee. Swartland manages its own distribution network with a fleet of c. 50 trucks which can deliver to hardware retail chains around sub-Saharan Africa. Swartland also exports products to the UK and US markets.

Swartland’s product offering includes wooden doors and windows, aluminium doors and windows, garage doors and automation, XPS insulation and cornices and skirtings, finishes, par awnings and finished products.

Learn more about LACP:

LACP was founded in September 2018 and is a private equity fund management business. LACP is the manager of Legacy Africa Capital Partners Fund I and is part of Legacy Africa Fund Managers. LACP is a 100% black-owned and managed company comprising a team of deal principals with a long history of private equity investing. The firm seeks to provide capital to entrepreneurial, unlisted companies seeking expansion or buy-out capital to introduce black shareholding to drive growth.

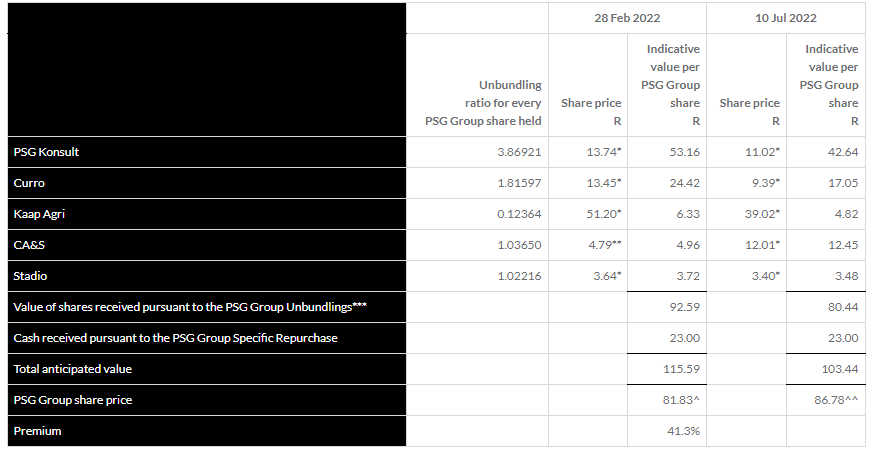

The big moment is here for PSG shareholders, with the restructuring circular now available to shareholders. It deals with the “unlocking of value” for the PSG Group i.e. the unbundling of almost all the assets. This means that 61.1% of PSG Konsult, 63.6% of Curro, 34.7% of Kaap Agri and 47% of CA&S will be unbundled to shareholders. Only a portion of Stadio is destined for PSG shareholders (25.1% of the company), with the PSG founding management holding on to some of their Stadio shares. PSG is proposing that the assets that aren’t unbundled should be sold to the PSG founders for R23 per share. BDO Corporate Finance has already given its opinion as Independent Expert that the terms are fair and reasonable to shareholders. The table below indicates the value being distributed to shareholders. If you want to see how complicated corporate restructurings can become, there’s a 254 page circular for you to sink your teeth into at this link.

Source: PSG website, 10 July 2022

Capital & Counties Properties (Capco) is in the process of proposing a deal with shareholders that would see Shaftesbury merger with Capco. A circular and prospectus have been sent out, as there are so many new shares being issued that this isn’t just a standard acquisition (hence the word “merger”). If you want to see the sheer number of documents required from a regulatory compliance perspective for a deal like this, check out this section on the Capco website. Please also note the earnings update from Capco further down in Ghost Bites today.

Back in November 2021, Vivo Energy announced that Dutch energy and commodity trading company Vitol would be making a cash offer for all the shares it didn’t already own in Vivo. After working through the various shareholder and regulatory approval processes, the offer has now met all conditions. As the effective date is prior to the interim dividend record date, Vivo Energy has declared a special dividend of $0.02 per share. The shares are expected to stop trading on the JSE on 25th July, with the dividend then paid and the listing terminated on 29th July.

Banks have been buying up their issued preference shares in the market, as this has become a less appealing source of capital since Basel rules changed (these are the rules governing the way banks measure their capital adequacy). At one point, banking preference shares were all the rage as a source of funding. FirstRand is the latest bank to make this move, with an offer to repurchase all the “B” variable rate preference shares. This is being structured as a scheme with a standby offer, with means that FirstRand’s ideal scenario is to repurchase all the shares (achieved through a scheme of arrangement), with second prize being a repurchase of shares from any shareholder willing to sell (the standby offer). The repurchase price is a 12.8% premium to the 30-day volume weighted average price.

In case you are keeping an eye on service station forecourts business Afine Investments, you’ll be interested to know that Petroland Group and Terra Optimus now own 6.22% and 5.55% respectively.

Earnings updates

Capital & Counties Properties (Capco) already earned a mention in Ghost Mail this morning for the release of regulatory documents related to the Shaftesbury merger. The company also gave the market an update on its business, headlined by a 5% increase in the value of the Covent Garden estate in the first half of the year. This was driven by a 4% improvement in the estimated rental value (ERV) and a decrease in the cap rate that the property is valued on, reflecting improved leasing activity and market conditions. Sales value is running ahead of 2019 levels and footfall is still recovering. The vacancy rate at 30 June is 2.5%. The loan to value ratio of Covent Garden is 20% and Capco has cash of £139 million and £300 million in undrawn loan facilities. Capco repaid £200 million in loans in the first half. Interim results for the six months to June will be released on 2 August.

PBT Group has released its integrated annual report for FY22. Although there is no change to the previously announced results, the report is a worthwhile read for PBT shareholders because the company does a great job of giving proper disclosures about the business. For example, PBT discloses the percentage of revenue earned from each industry, with financial services now contributing 74% of revenue (way up from 49% in FY19). For more great insights into this company, refer to the integrated annual report at this link.

Brait is firmly on the radar for investors, so it’s worth mentioning that the integrated annual report is now available at this link.

African Dawn Capital has released results for the year ended February 2022. Revenue increased by over 58% and the headline loss per share improved by 12% to -20.3 cents. This group has a colourful history to say the least, including a fight with SARS and failed transactions. Today, the group has a lending business and a platform that claims to increase due diligence efficiency.

Share buybacks and dividends

I don’t mention it every day as it would just become annoying, so this is your occasional reminder that British American Tobacco and Glencore are both busy with share buyback programmes and are releasing daily updates.

Notable shuffling of (expensive) chairs

There was no shuffling today!

Director dealings

Another day, another purchase of shares by a director of Kaap Agri. The latest purchase was to the value of R95k.

Unusual things

BHP is defending a group action claim in the United Kingdom related to the failure of the Samarco dam in Brazil in 2015. I’ve seen offshore media reports that this is a £5 billion claim, so the stakes are high. There is incredible footage of the dam collapsing, which you can find here on YouTube (be warned: many lost their lives and it’s not hard to see how from the video). The UK High Court previously ruled that proceedings in the UK were an abuse of process. The Appeal Court has overturned that ruling, which allows the group action to continue in the UK. This has nothing to do with the merits of the claim and is purely a procedural ruling. BHP is deciding whether to seek permission to appeal to the UK Supreme Court. BHP has already provided £1.5 billion in compensation to over 376,000 people and legal proceedings in Brazil are ongoing.

Imbalie Beauty has released the last integrated annual report that will carry that name, as the company has rebranded to Buka Investments. Covid caused incredible pain for the group’s beauty franchises, leading to a restructure of the group that included the beauty businesses being stripped out along with the debt raised during Covid. The remaining listed shell will focus on investments in the fashion industry.

A couple of weeks ago, Chris Gilmour took a detailed look at the non-discretionary retailers on the JSE. This includes the grocery stores and pharmacy chains. Last week, he began a journey into the discretionary retailers on the JSE, focusing on Woolworths in part 1. This week in part 2, Chris looks at Truworths in detail.

Truworths lags both The Foschini Group (TFG) and Mr Price in terms of vision, entrepreneurial flair and the ability to capitalise on market opportunities.

In part, this is probably due to complacency which has sunk into the organisation over many years. It still persists with an addiction to credit-fuelled growth in its main operations, whilst its competitors have long ago gone the predominantly cash route. And while both Mr Price and TFG have recently embarked upon meaningful acquisitions in order to grow their top lines, Truworths has put its excess cash into share buybacks.

Ex-growth under current management

Truworths remains a solid and operationally well-managed business, notwithstanding its ill-conceived foray into the UK retail market with the acquisition of Office six years ago. It remains well-run and offers shoppers a quality experience. However, it has gone ex-growth in recent years and that is unlikely to change under current management direction.

A five-year share price chart certainly tells a story:

Long-time CEO Michael Mark will be retiring this year after over thirty years at the helm of the business. Generally speaking, he has had a good record in running the company, but Truworths now finds itself, in my opinion, at a watershed. Its products, although high-quality in the main, are perhaps priced somewhat too optimistically for the emerging middle-class market.

A generous separation

During the three decades of Michael Mark’s tenure, Mr Price has had four CEOs and TFG has had five. Mark was destined to retire from the job in the middle of last decade and his successor, Jean-Christophe Garbino, was named as CEO-designate and should have succeeded him in 2015. But the arrangement didn’t work out and Garbino abruptly resigned. To this day, no satisfactory explanation has been given for his departure, other than a comment in the Sunday Times from Mark that “it just didn’t work out”.

Garbino received payment in the amount of R25 million as compensation for loss of office on resignation as an executive director of the company on 4 December 2015. By the time he left he had attended three board meetings and received salary and benefits worth R2.2 million. This was a remarkably generous separation package by the Truworths board for someone who had scarcely set foot in the business.

Prior to his extremely short tenure at Truworths, Garbino had spent 22 years at Kiabi, a French budget fashion retailer, the last seven years of which being as CEO of the company. Perhaps his experience at Kiabi would have served him well had he stayed and set Truworths on a potentially different course. But that is in the realms of speculation and we will never know.

Although there has been a temporary improvement in certain of Truworths metrics in financial 2021, thanks to a favourable base effect when making comparisons with 2020, longer-term erosion is still intact.

Unless Truworths can change its top management direction, and quickly, it will likely see its financial metrics deteriorate even further and lose more ground to its competitors. This is reflected in the very poor rating of the share. On a Price/Earnings ratio of only 8.3x, Truworths is the second cheapest share in the retail sector.

The Primark trademark fight

A couple of years ago, Truworths started using the Primark label in South Africa, on the grounds that it hadn’t been used for at least five years by the Irish parent company and thus it had ceased to be protected. And although Truworths has won the first round in court, I believe that Primark will eventually win back its right of use from Truworths. There are at least two relatively recent precedents in SA law that inform us that Truworths is in the wrong.

It is understandable why Truworths wants to use the Primark label. Like Zara and H&M, it is lower-end and appeals to customers who want fashion at an extremely low price. And like Zara and H&M, it would probably gain a loyal following in SA very quickly for all the reasons mentioned earlier. Most importantly, it allows Truworths to gain a foothold in the lower-end fashion segment that is currently dominated by Mr Price and TFG. In so doing, it would be able to increase its top line.

Most, if not all of Primark’s South African customers would be totally oblivious of the fact that there is no relationship between Primark in SA and the real multinational Primark. This might backfire on Truworths in the longer term if South African customers access the genuine Primark website and discover that products shown there are not available in SA.

Source: Primark website

Primark, a subsidiary of Associated British Foods (ABF), first registered its Primark brand in SA in 1976 and to date has never used the trademark in SA. In South African law, a third party such as Truworths can cancel a trademark if it has not been used for five years. In 2018 Truworths filed a cancellation action against Primark’s registration for the Primark trademark on the grounds that this trademark was not subject to use. In the action at the time, Primark’s counter-argument was that, because Primark is an internationally well-known brand, the non-use of the trademark was irrelevant and that Primark’s registration should be protected from cancellation.

However, the Supreme Court of Appeal (SCA) disagreed, finding that although the Primark brand was well-known in the UK and elsewhere, it was not well-known in SA. Therefore it did not qualify for protection if it had not been used for five years.

But there was a sting in the tail that could ultimately be negative for Truworths in the longer term. The SCA commented on Truworths’ dishonest motivations and approach. In the initial court papers, Truworths stated that it only wanted to use the Primark label on some clothing lines without actually opening a chain of Primark stores. It has become clear that Truworths does indeed intend opening a chain of Primark stores. At end-June 2021, 11 Primark stores were operating in South Africa.

A similar legal situation can be found in the case of McDonalds, the well-known multinational fast-food chain in its actions against George Charalambous and his partner Chicken Licken founder George Sombonos. The two Georges attempted to use the McDonald’s trademark in SA in the 1990s on the grounds of non-use of the trademark. While they were partially successful in being allowed to use a slightly different version of the name (MacDonald’s instead of McDonald’s), Charalambous and Sombonos lost on appeal in 1996 and McDonald’s won the rights to use all of their own trademarks in SA.

Closer to Truworths’ business is the case of LA Retail vs the US Polo Association (USPA). LA Retail, a South African apparel producer, had produced copycat versions of the Ralph Lauren-owned Polo brand products in SA for many years. The only difference between Ralph Lauren’s original logo with two polo-playing horsemen and LA’s logo was that in the Ralph Lauren products, the players faced right and in the LA logo they faced left. LA and Ralph Lauren had an agreement going back many decades that they could use this arrangement in SA and both parties appeared to be happy.

But in 2019, the USPA and its SA affiliate Stable Brands (Pty) Ltd won an important legal battle against LA Group in terms of which over 40 LA Group trademarks using Polo in the name were required to be cancelled and expunged in the trademark register in SA.

Although Truworths has won the first round in its attempt to retain the use of the Primark label in SA, it should be noted that Primark intends to take “whatever steps are necessary to protect its trademark and hard-earned reputation” – Primark and ABF are formidable opponents. Not only is Primark a true multinational retailer, but parent company ABF has long-established links in many countries, including South Africa. It knows the South African corporate and legal landscape well and Primark will no doubt be well aware of the potential for its brand in South Africa.

I believe that the fight for Primark’s right of use of trademark in SA is far from overand that ultimately, Primark will win. In this event, Truworths will have to find an entirely new avenue for tapping into the lower-end fashion market. Truworths already has a lower-end fashion chain called Identity that could presumably be used to increase the group’s top line.

It therefore seems surprising that Truworths would want to go the potentially hazardous route of using a multinational brand such as Primark without the owner’s permission.

Next week, Chris will deal with more of the discretionary retailers on the JSE, like Mr Price, TFG and Pepkor.

Ghost Global is a new weekly segment that will be brought to you by the Ghost Grads on a rotational basis. This week, Jordan Theron updates us on earnings from some significant US companies.

Ford: feeling a little fragile?

Ford sold 152,262 vehicles in June, up 31.5% year-on-year. This was due to the increase in truck and SUV deliveries and its new all-electric pickup trucks. Whilst this is positive, US auto industry sales are down 11%, showing difficulties replenishing car dealerships and high levels of inflation forcing buyers out of the market.

For the first 6 months of 2022, sales were down 8% reflecting the current supply chain crisis dogging the global economy. This problem has led to decreasing inventory levels.

Can the old-time heavyweight giant pull its weight with its shiny new F 150 and take on the likes of Tesla, VW, and Toyota? With a YTD share price performance of -46%, they’re going to need to start finding their feet in this increasingly competitive electric car market.

Pass the chips

With the world becoming increasingly reliant on technology, Taiwan Semiconductor Company (TSM) is a stock you should care about even if you don’t own it.

TSM produces semiconductor chips which are used in everything from cellphones and cars to rocket ships. They reported better than expected earnings, with June sales up 18.5% YOY and revenue for the 6 months to June being $34.41 billion.

Even though the stock is down 36% YTD, it has produced a share price CAGR of 17.6% over 5 years.

The threat to TSM is a potential drop in demand for its chips, either due to lower consumer demand or oversupply in the market. TSM has to invest a huge amount of capital in R&D and facilities that manufacture chips (known as a “semiconductor fab”), which leaves the company exposed to supply / demand dynamics. Political tensions with mainland China also can’t be ignored.

With the full June quarter results coming out later this week, this is a stock you will want to keep an eye on.

Warren Buffett and fossil fuels

Its pretty hard to talk about investing in the stock market without talking about the legendary Warren Buffett. From delivering newspapers to becoming the Oracle of Omaha, Buffett has had arguably the largest impact on the investing world of anyone. He is the CEO of Berkshire Hathaway, which recently increased its stake in Occidental Petroleum to 18.7%, an investment valued at around $11 billion after the rapid spike in the oil price. The brent crude oil price has risen from as low as $72/barrel to as high $120/barrel this year.

This rise can be attributed to various factors such as poor energy policies from western countries, an increase in demand after the pandemic and a supply crunch from the conflict in Ukraine. We may be suffering at the pumps, but the big oil companies are printing money at a rate that even Jerome Powell would be impressed by.

Occidental Petroleum is up 110% this year and is trading on a Price/Earnings multiple of around 9x. Despite huge inflationary consequences for consumers around the world from the current oil price, Buffett clearly doesn’t see that trend slowing down. Is he too eager about this cycle, or is he slowly capitalising on an opportunity we are all ignoring due to the new climate change agenda?

Costco is cashing in

The famous value retailer has released strong monthly sales numbers for June, beating expectations with net sales jumping 20.4% YOY to $22.78 billion. This is further proof of the slow and steady winning of market share from its competitors in a difficult economic environment.

The really impressive number is the 18.1% increase in same store sales, which beat Wall Street expectations of 14.1%. With its business model focusing on membership fees to help subsidise great in-store prices, as well as cheaper gasoline (Jordan lives in the US so he’s using the right term here!) to entice customers to purchase more goods, it seems Costco might just have found its sweet spot in this fragile economy.

This recent success has led to speculation about a potential cash dividend to reward shareholders with the balance sheet looking juicier than normal, making this proudly American company one to keep an eye on.

Turmoil at Twitter

Who can forget the buzz created in the streets (both tarred and virtual) by the announcement that Elon Musk offered to buy Twitter for $44 billion?

With an increasingly political and polarizing environment in the US, this created massive waves with most Republicans praising the South African-born Musk’s free speech stance vs the Democrats crying wolf about his increasing global influence due to his enormous wealth and more libertarian approach to public policy.

He has recently notified Twitter of his intention to withdraw his offer due to Twitter’s inability to validate that less than 5% of its accounts are spam or bots. Interestingly, this has resulted in a 2% rise in Tesla stock while leading to a drop in Twitters stock by 5% in day trading and another 5% overnight.

Twitter has become a controversial platform for many reasons which we need not mention, but it should provide for some good entertainment in the coming months with Twitter’s plan to legally bind Musk to his original offer.

Only time will tell what will happen to the public town square of the new world, but for now a cautious approach is best with Twitter stock.

Magic Markets Premium – expand your universe

With the JSE’s listed universe of companies shrinking by the month, learning about global investment opportunities in critical. In Magic Markets Premium, The Finance Ghost and Mohammed Nalla bring you a weekly report and podcast on global stocks. There are around 35 reports already in the library, including three of the companies in this week’s edition of Ghost Global (Ford, TSM and Costco).

For just R99/month or R990/year, you can have access to institutional-quality research that is guaranteed to expand your investment knowledge. Visit the Magic Markets website to subscribe.

You may recall that Remgro and MSC Mediterranean Shipping Company made a rather surprising offer for Mediclinic at the beginning of June. The board of the hospital group told the billionaire families exactly where to put that offer, possibly with medical assistance if needed. Since then, there have been four more proposals of which three were rejected. The fourth one is far more interesting, valuing Mediclinic at 504 pence per share. This is a 35% premium to the price on the day before the initial offer was made. The latest offer is 8.9% higher than the initial proposal. The independent board has noted that if this becomes a firm offer, they would be willing to recommend it to shareholders. As UK law applies here, there is a colourfully-named “put up or shut up” clause (no, really) that requires Remgro and MSC to either make a firm intention offer by 4th August or walk away. Although there is still no guarantee of a deal here, a 8.6% jump in the share price on Thursday shows you how the market feels. At the current exchange rate, that’s a potential offer of R101.20 per share vs. the closing Mediclinic price of R94.90.

This Groupe Canal+ / MultiChoice thing just isn’t going away. The French media company has bought even more shares in MultiChoice, taking its stake to over 20%. We would have called that a “significant minority” stake in my investment banking days, which is the level at which things are starting to get serious. We don’t know what the intention is with this MultiChoice investment, but companies don’t build up a 20% holding with no plan in mind. Canal+ is owned by Vivendi, a listed French media giant with a market cap of €10 billion (around 3.5x the size of MultiChoice).

Bidvest has acquired 100% of BIC Australia, which has nothing to do with those orange pens that most of us held at some point in time in our school careers. For the younger readers, there was a world before iPads believe it or not! BIC Australia is a private company that offers integrated facilities management services. Cleaning services are at the core, with a full range of hygiene, waste and similar services offered. The client base is primarily A-grade offices in New South Wales. The price is based on an enterprise value for BIC Australia of R1.8 billion, which is the value of assets in the business less any excess cash. The actual cash payment would depend on how much debt is in the business vs. equity. Bidvest is paying for this with the proceeds from the bond issuance in October 2021. The management team have signed service agreements and remain committed to the business.

Alexander Forbes announced in March that Prudential Financial (listed on the New York Stock Exchange) had agreed to acquire 14.83% in the company from Mercer Africa, a subsidiary of Marsh McLennan Companies Incorporated (also listed on the NYSE). The deal has closed and the price was R5.05 per share excluding the dividend declared on 6th June and payable on 11th July. Prudential also intended to make a partial offer to other shareholders if the Mercer deal went ahead, which is now the case. A partial offer takes Prudential to a maximum 33% stake in Alexander Forbes, below the 35% threshold that triggers a mandatory offer. ARC Financial Services holds 41.47% of Alexander Forbes and will not accept the partial offer. A circular will be sent out in due course with the terms of the partial offer.

Sirius Real Estate has completed the sale of its £16 million BizSpace Camberwell business park in London. The net initial yield is only 2%, which means the selling price was really high. In fact, Sirius achieved a 94% premium to what it paid for the asset in November 2021! Full marks to Sirius here – the company has made a song and dance about its ability to create value through active management of assets and we’ve seen it come through in this sale.

Life Healthcare has registered a R7 billion Domestic Medium Term Note Programme Memorandum with the JSE. If you’re interested in what a debt raise on the JSE looks like, you’ll find all the documents at this link.

Earnings updates

Deutsche Konsum REIT is one of those almost pointless listings on the JSE, as the stock practically never trades. Nonetheless, the group gives us insights into the convenience retail property market in Germany. That’s rather niche, I know. The fund has acquired six more properties on an initial acquisition yield of 8.6% with a vacancy rate of 1.6%. In the current financial year, the fund has managed to acquire 21 properties at an average initial yield of 8.5%. The fund also managed to sell five properties on which it made a gain. The total portfolio is 179 properties. As Deutsche Konsum offers such interesting exposure to the German market, it’s a pity that there is no trade on the JSE.

Share buybacks and dividends

African and Overseas Enterprises as well as Rex Trueform (separately listed but part of the same group) have declared dividends on their 6% cumulative preference shares. I’m not close to the detail on this group but I did notice that the African and Overseas Enterprises preference shares are “participating” preference shares, which means they can achieve a return above the 6% coupon depending on the terms of the shares and what triggers that participation.

Notable shuffling of (expensive) chairs

There’s another senior change at York Timber, this time with the resignation of the company secretary after a period of 9 years at York.

Woolworths has appointed Nombulelo Moholi as Lead Independent Director. Ms Moholi has served on the board in a non-executive capacity since July 2014.

AngloGold Ashanti has appointed Ian Kramer as Interim CFO after the retirement of Christine Ramon. The company is following a “comprehensive international search process” for a permanent CFO. Kramer is an internal appointment and will no doubt be hoping that the international process comes up empty.

Netcare’s Chair Thevendrie Brewer has resigned as her family have decided to emigrate. I guess load shedding was the last straw. Ms Brewer has been in that role since April 2018 and on the board since 2011. Netcare hasn’t announced a new Chair yet.

Director dealings

An entity related to the CFO of Famous Brands has bought CFDs on Famous Brands worth over R825k. This is a pretty serious punt at the shares and ties up with what I’m seeing from the property REITs who have commented on how “entertainment” tenants are having a far happier time of things at the moment.

The recent insider buying at Raubex has been something to behold. The latest purchase is significant – a R700k acquisition of shares by the recently appointed CEO of the group.

Another company that has seen regular buying by directors is Kaap Agri. The latest purchase is by a non-executive director to the value of R145k.

Value Capital Partners is still piling into PPC shares, with around R9 million worth of shares acquired in the past three days. We know about this because there are directors on the PPC board appointed by Value Capital Partners as an anchor shareholder. The share price had a huge day, closing over 15% higher. Even with that move, it’s still nearly 40% down this year.

Telkom directors received shares in the company and appear to have run for the hills, with major disposals by several directors. The announcement doesn’t say that this sale was a portion of the share-based awards in order to cover taxes payable, so I’ll assume that this was an outright sale because they don’t want the shares. At least I have something in common with Telkom directors, because goodness knows I don’t want the shares either.

Unusual things

I can see that Kibo Energy is one of those companies that will announce every step of its journey in the renewables space, much like Renergen does with its projects. To be fair, investors in these types of businesses tend to hang on every word. In this case, the news is that Kibo has committed to purchase the first two proof of concept CellCube batteries that use fancy technology. Kibo has a strategic framework agreement with CellCube to deploy long-duration energy solutions in Southern Africa.

With Irongate (the old Investec Australia Property Fund) leaving the market as part of the buyout by Charter Hall, Fairvest B shares have been promoted to the FTSE/JSE Capped Property Index. This means that Fairvest will be bought by any ETFs tracking the index.

Although it comes through as director dealings, the disposal of R13.8 million worth of shares in Finbond by Protea Asset Management LLC is actually an unbundling of shares to the underlying investors in that fund. Protea is linked to Sean Riskowitz who sits on the Finbond board.

MiX Telematics has raised a R350 million general credit facility from Investec and an uncommitted general credit facility of $10 million.

In May, a consortium comprising Remgro and MSC Mediterranean Shipping Company proposed to the Board of Mediclinic International a possible cash offer to acquire the Mediclinic shares not already held by Remgro at a price of 463 pence (R88.43) per share. The proposal was rejected on the grounds that the offer significantly undervalued Mediclinic and its prospects. At the time, Remgro which currently holds a 44.6% stake in Mediclinic, said that it would consider its position. This week Mediclinic announced it would progress with talks on the consortium’s fourth proposal which values Mediclinic shares at 504 pence per share – a premium of 23% to the share price of 411 pence on June 7, the day prior to market speculation. In line with regulations, the consortium must make a firm offer by August 4, 2022.

Bidvest has announced the acquisition of B.I.C. Services, a niche integrated facilities management services provider across office, commercial and education sites. The acquisition is for an enterprise value of A$160 million (R1,8 billion). It has been some time since a South African corporate has made an acquisition in Australia, not surprising given the poor track record of those who have gone before.

Huge has acquired Tethys Mobile, currently in Business Rescue, from shareholders and creditors for an undisclosed sum. Once implemented, Huge will change the name to Huge Digital Enablement. Tethys was SA and Africa’s first mobile virtual network operator when it launched to the market in 2006.

Deutsche Konsum REIT-AG (DKR) has acquired a portfolio of six mainly food-anchored local retail properties in Saxony and Saxony-Anhalt. The properties which have a combined rental area of 9,000sqm were acquired for c.€9,2 million.

Both Delta Property Fund and Texton Property Fund have notified shareholders that property transactions announced in 2021 have been terminated due to the inability of the purchasers to fulfil conditions precedent. Properties in question were the sale by Texton to Stonehill Property Group of the Forestrust and Loop Street Properties for an aggregate consideration of R397 million and the disposal by Delta of the Fort Drury and Sediba properties to Central Plaza Investments 199 for R76,5 million.

Unlisted Companies

Lonsa Everite, together with black-owned and managed South African private equity firm Legacy Africa Capital Partners and Swartland management, have acquired 100% of the issued shares in Swartland Investments and Swartland Insulation, as well as the freehold properties. Swartland is a manufacturer and supplier of wooden and aluminum doors and windows, garage doors as well as XPS insulation and cornices. The business operates in Southern Africa, the UK and the US. The transaction value of c.R1,3 billion was funded through a combination of equity, vendor deferred payment agreement and R660 million of debt financing.

In another deal, Legacy Africa Capital Partners has invested an undisclosed sum in power solutions provider Continuous Power Africa (CPA). The investment will accelerate CPA’s expansion into new markets beyond telecommunications and grow its range of products.

Fintech startup Sava Africa, a local spend-management platform, has raised US$2 million in pre-seed funding. The platform combines bank accounts, mobile wallet, payments, accounting integrations and invoice and expense management tools. The round was led by Quona Capital with participation from Breega, CRE Ventures, Ingressive Capital, RaliCap, Unicorn Growth Capital and Sherpa Ventures. Funds will be used to launch its product in South African and Kenya.

Alaris, which delisted from the JSE in February this year, has expanded its footprint in Europe with the acquisition of Kuhne electronic, a German electronics engineering company. Financial details were undisclosed.

Firering Strategic Minerals plc, an exploration company focusing on critical minerals, has increase its stake in the Atex Lithium Tantalum Project in Côte d’Ivoire from 51% to 77%. A 10% stake was acquired in exchange for 1,158,200 shares valued at €88,672 and a further 16% for €320,000 in cash. The company has an option to acquire the remaining 23%.

Dutch energy and commodity trading company Vitol has entered into a joint venture with the Nigeria Sovereign Investment Authority to invest in a range of high integrity, socially impactful, carbon avoidance and removals projects in Nigeria. The companies will make an initial commitment of US$50 million and will partner with local NGOs.

CFAO Kenya has made an undisclosed investment in OFGEN, a leader of solar PV installation for commercial and industrial use in East Africa.

Autochek Africa, an e-commerce company headquartered in Lagos, has acquired CoinAfrique, a Mauritian-based classified ad marketplace, serving francophone African markets. The deal will accelerate the penetration of Autochek’s auto financing services in French-speaking Africa.

In a non-binding offer, SODIC a real estate and community development company, is to make a cash acquisition of Cairo headquartered state-owned developer Madinet Nasr Housing & Development through a mandatory tender offer. The offer is for an indicative purchase price in the rage of EGP3.20 and EGP 3.40 per share, representing a 28-%36% premium, valuing the company at c.EGP6,18 billion (US$328 million). SODIC will undertake a due diligence.

Paymee, a Tunisa-based fintech startup offering specialising in digitising payment flows that offer online payment acceptance solutions, has raised six-figure funding in a round led by P1 Ventures. Funds will be used to accelerate its product development and offering.

Kenyan startup Duhqa, a last mile end to end supply chain and distribution technology platform enabling manufacturers, retailers and individuals to buy and sell conveniently, has closed a US$2 million seed round from participants CrossFund, Roselake Ventures and Mo Angels, among others. The funds will be used to scale its service offerings in East Africa.

Cameroonian importer and distributor of petroleum products BOCOM Petroleum SA, has secured a €50 million financing package through the International Finance Corporation. The financing will be used to expand access to liquified petroleum gas in Cameroon.

This week was all about repurchases, with companies taking advantage of weaker stock prices to buy back their own shares from the marketplace.

Last week Naspers and Prosus announced the start of an open-ended share repurchase programme of Naspers and Prosus shares. The companies have since announced that during the period 28 June to July 1, 2022, a total of 4,266,596 Prosus shares were acquired for an aggregate €264,3 million and 527,276 Naspers shares for R1,24 billion.

During the period May 27, 2022 to June 30, 2022, Barloworld repurchased 6,004,502 shares for an aggregate value of R548,38 million. The general repurchase represents 3% of the company’s issued share capital. The shares will be delisted and cancelled. Following the cancellation, Barloworld will hold 3,194,290 ordinary shares as treasury shares representing 1.64% of the companies issued ordinary shares.

Investec Ltd has repurchased 942,642 preference shares representing 3.06% of the company’s issued preference share capital. The preference shares were repurchased at prices between R94.33 and R97.79 for an aggregate value of R90,5 million.

Santova has applied to the JSE for the cancellation of 1,329,736 shares held as treasury shares following the repurchase at an average price of R4,24. Following the cancellation of the shares the remaining share capital of the company will be 137,440,516 shares.

This week British American Tobacco repurchased 1,060,000 shares for a total of £37,33 million. The purchased shares will be held in treasury with the number of shares permitted to be repurchased set at 229,400,000.

Glencore this week repurchased 7,860,000 shares for a total consideration of £33,54 million in terms of its existing buyback programme which is expected to end in August 2022.

This week one company issued a profit warning. The company was Trellidor.

One company this week issued or withdrew a cautionary notice. The company was Aveng.

South Africa’s public market is broken. In the past 30 years, the number of listed companies has more than halved from 760 to about 330.

Worryingly, the trend appears to be gaining momentum. No less than 25 delistings occurred in 2021 (with just seven new listings in the same period), and at least a further 21 delistings are already anticipated for 2022 – and we’re only at the beginning of the second quarter.

We must fix this situation and arrest this delisting trend. Everyone involved in investment banking needs to realise that this trend is a threat to their livelihoods. This is now a matter of urgency, because it is likely that the local public markets will enter something akin to a death spiral, where an ever-diminishing pool of very large listed companies is matched by an ever diminishing pool of ever larger asset managers, sucking the oxygen out of the market and stifling new entrants – both new listed companies and new investors.

Dynamic, lively public markets are required, not only to provide savings and investment opportunities, but also to underpin the growth and investment that is so desperately needed to support South Africa’s economic development and, of course, all-important job creation. It goes without saying that a public market in a death spiral will eventually also offer meagre opportunity to investment bankers.

While at a micro level, the JSE itself is an easy target for ascribing the blame for this crisis, the real structural cause has less to do with listing red tape, supposed high costs, or cyclical share prices, and everything to do with the systematic institutionalisation of the country’s savings and investment industry over the past three decades.

Investment on the JSE has become increasingly exclusionary.

Of course, the imperative to fix the delisting crisis in this country goes beyond providing investors with access to a diversity of investment options; the capital needs of the businesses themselves must be met by the public markets too. For the private investor in South Africa, opportunities to provide primary capital to newly listed companies have become increasingly few and far between. And the habit of companies and their advisors to structure listings to avoid the obscure JSE Listing Requirement 5.18 appears partly to blame.

Simply put, Requirement 5.18 states that if an offer of shares to the public is oversubscribed, the allocation of the available shares must be done equitably. It was created to ensure that when a general offer is made, like an initial public offering (IPO), large institutions don’t have an unfair advantage over smaller institutions, or the investor in the street. This is in line with the financial sector’s own charter to which all banks and many other advisors are party, and which has, as one of its objectives, the realisation of a more equitable financial sector – especially in terms of promoting the interests of those who have historically been excluded.

All of which begs the question: Why is Requirement 5.18 so obscure that the only people aware of its existence are regulatory managers studying towards their JSE sponsor executive exam?

The answer is that JSE Listing Requirement 5.18 has not been applied to any new listings for at least the past decade. It was last applied three times in 2010 and just once in 2012.

If the financial services sector deliberately excludes the public from most primary capital raising opportunities, largely for reasons only of timing and convenience, then they should not wonder why there is not a pool of smaller investors available to provide the oxygen that the market so desperately requires.

This exclusionary trend has also been driven by institutional investors who have what is known as an ‘acceptable limit’ on the size and liquidity of the companies targeted for investment by their asset managers – which generally translates to the largest 80 to 120 companies only. That’s not to say that those institutional investors are solely to blame, however, as it is the regulations within which they operate that are at the heart of the problem.

For example, a unit trust fund is typically required to return cash to an investor within 24 hours of receiving a request to withdraw funds. Delivering on this high liquidity expectation is a challenge for most funds. Not only is the minimum settlement period for disinvestment from a large liquid listed entity three business days, but selling out of a position in a smaller listed company can easily take as long as a week or two. This inherent liquidity mismatch exists in every collective investment scheme and is replicated across other types of institutional funds.

This size and liquidity bias means that the larger the fund gets, the fewer individual counters it can consider for investment. This compounds the death spiral as funds have been getting larger and, as a result, the number of counters in their acceptable investment universe has been shrinking.

The economics of personal stockbroking have also collapsed, and many stockbrokers have spent the last decade transforming into regulated wealth managers, which has involved moving most of their clients into index benchmarked model portfolios or institutionally managed collective investment schemes, with the remainder moved on to no-service, no-advice, secondary trading-only digital platforms.

Add to this the fact that an ever-increasing proportion of investing is now index-linked, and it is clear that South Africa’s financial sector has firmly turned away from both direct investment by smaller investors and investment into smaller listed entities.

It’s obvious that a massive bias in favour of ‘the large and the liquid’ has been designed into our entire institutional savings industry. That means that any company outside of the top 120 listed on the JSE receives very little interest from our institutional investors. The same institutional investors have, in turn, assimilated many small direct investors, in part through gatekeeping the access to tax incentives.

The solution: De-institutionalise our markets.

Irrespective of the answers to these questions, the reality we must face is that South Africa’s capital market is simply no longer fit for purpose, especially for a resource rich economy. This is clear when you compare the South African market to those in the UK, Canada and Australia.

As is the case in this country, individuals in those countries are given tax incentives to save. These range from tax deductions on pension contributions to deferment of capital gains tax in collective investment schemes. In South Africa, we have gone one step further and introduced tax free savings accounts that attract no tax at all.

The difference, however, is that South Africans are only able to access these tax incentives if they save in an institutional fund and pay an institution to manage the assets.

In contrast, UK, Australian and Canadian individual investors have the option of benefitting from these tax breaks through self-directed, self-invested or self-managed investment accounts, in which they can hold a wide range of assets, including stocks and shares.

By compelling South Africans to access these incentives only through institutions, we have choked off access to capital for smaller listed companies. Is it any wonder, then, that smaller companies don’t perceive any benefit to listing, or staying listed, on the JSE?

It is clear that any solution has to start with de-institutionalising our savings market. This demands a primary focus on the ‘bottom of the pyramid’, namely the general public. Meaningful incentives to save are needed, but in a way that gives individuals the right to choose where and how they save and invest. Most individuals will continue to save through institutions, but we must remove the monopoly that institutions currently enjoy on the access to tax incentives, if we are to save the very market on which they depend.

In 1992, the Jacobs Committee laid the basis for the next three decades of financial sector reform in South Africa. It proposed much of the legislative and regulatory scaffolding on which our savings industry now rests. Importantly, it investigated the ‘attainment of a level playing field for competing financial intermediaries (i.e. banks, life assurers and asset managers) in the country’. It did not, however, include consideration of the same levels of fairness for private direct investors and, as a result, it has inadvertently contributed to the steady shrinkage of the JSE that we have seen ever since.

The time has come for another Jacobs Committee, this time to investigate levelling the playing field between institutional and direct investors, with the objective that both should at least be afforded the same investment opportunities, be taxed on the same basis, and have the ability and incentive to support new listings of smaller companies seeking access to equity capital.

The time has come to de-institutionalise our stock exchange and get the investing public back into the public market. If we don’t, we may well end up with a bourse comprising only 120 or so large, liquid companies. And that will certainly be of no benefit to anyone.

Paul Miller is a Director of AmaranthCX.

This article first appeared in Catalyst, DealMakers’ private equity magazine.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")