Huge Group decided to use SENS to tell us that they have a new corporate identity and website. Isn’t that exciting? More importantly, Huge is going to buy the remnants of the Virgin Mobile South Africa business, which entered business rescue in 2020. Huge wants the software and technology platform in order to create a Platform-as-a-Service business targeting organisations wanting to operate as mobile virtual network operators. This effectively bails out post-commencement creditors of Tethys (the entity holding the business). No indication of price has been given.

Irongate has achieved the final legal steps needed for the acquisition by Charter Hall, with the scheme set to become effective on Friday, 15th July. If you’re an Irongate shareholder, you’ll be receiving some cash this month!

Insimbi Industrial Holdings is rationalising its operations and has decided to either sell or close Insimbi Plastics. These decisions are never easy. Labour unions have already been consulted and Insimbi will now look for a buyer of the assets or the business. If someone buys the business, one would hope that the jobs will be saved.

Raubex and Bauba Resources have released the joint circular to shareholders regarding Raubex’s general offer of R0.42 per share and the potential delisting of Bauba from the JSE. If you’re interested, you can find the circular here.

Buffalo Coal Corp is one of those zombie companies on the JSE that simply never trades. With control of the company having changed hands, Investec has demanded full repayment of all outstanding loans. This is an amount of nearly R54 million. The new owner (Belvedere Resources) would need to provide the funding required to settle this and will be making a proposal to Investec.

Earnings updates

Trellidor has released a trading statement for the year ended June 2022. The Labour Court judgement against Trellidor has driven the board to provide for a financial impact of R32.1 million, which is terrible for a group with a market cap of R271 million. This is because the company had to reinstate 42 employees with back-pay to January 2017. Trellidor has lodged an appeal to the Constitutional Court, which has not yet responded to the appeal. The amount is so high that Trellidor didn’t pay an interim dividend and had to secure bank funding to cover the full cost. Importantly, Trellidor remains both liquid and solvent despite this. Headline earnings per share (HEPS) is expected to be at least 50% lower because of this issue. Interestingly, the share price has hardly dropped since March when the news of this judgement broke, possibly due to low liquidity in the stock. Another argument is that major shareholders may believe strongly in the appeal to the highest court in the land.

Mantengu Mining has released results for the year ended February 2022. There’s been no revenue for the past two years as this entity is just a “cash shell” on the JSE. The company is in the process of acquiring Langpan Mining Company in a reverse takeover, a common use for a cash shell. This is a quicker way to list a business than going the route of a new listing.

Share buybacks and dividends

Naspers and Prosus have gotten off to a good start with their respective share repurchase programmes that kicked off at the end of June. Naspers has repurchased R1.25 billion worth of shares and Prosus has repurchased $276.5 million in shares. It’s a pity that the share prices are up so sharply in the past month, as the repurchases could’ve been done at a far lower price.

There’s a dividend from Nampak, but only if you have access to the VIP section of the bar. This is where the preference shareholders hang out. They usually get their dividends before ordinary shareholders. In exchange for that higher level of certainty around the yield, they give up the upside exposure that ordinary shareholders enjoy. The company has two different preference shares in issue, paying 6% and 6.5% per annum respectively.

Notable shuffling of (expensive) chairs

With PPC under pressure, it’s worth noting the appointment of Daniel Smith as a non-executive director and member of the strategy and investment committee. Smith was the Head of Corporate Finance for Standard Bank, so he certainly knows his way around complicated deals. He is part of the team at Value Capital Partners, the investment firm that has recently been buying more shares in PPC.

Director dealings

Here’s a very important one: an entity associated with the CEO of Tsogo Sun Hotels has bought shares in the company worth R330k. Are things finally turning positive for the tourism industry? In case you clicked on the link to the website and you think I’ve lost my mind, take note that the company is now trading as Southern Sun.

There are tiny purchases by a director of Afine Investments, though that may just be a function of the huge bid-offer spread that plagues small caps on the JSE. I tend to highlight even small purchases in companies like these.

Directors of Kaap Agri are still buying shares, with transactions this time to the value of R155k.

I tend to ignore scenarios where directors are given shares in the company as part of their remuneration. In the case of Lewis, it’s worth mentioning that directors have the option to invest a portion of their net bonus in shares (over and above the usual share-based awards). Several directors have elected to do so.

Unusual things

Some companies release the statement that will be made by the chairman at the AGM. Sirius Real Estate is one such company. The statement usually recaps the prior year’s result and gives a short update on the current environment. Sirius is trading “in line with expectations” and is working on “asset recycling” opportunities – selling properties for cash – in order to reduce the level of debt. The chairman reminds us that a large percentage of tenancy agreements include inflation indexations, which means inflationary increases can be passed on to tenants. The share price is down over 40% this year, the fault of a silly market last year rather than the company doing anything wrong.

You may not be aware that companies also use the JSE to issue debt instruments, not just equity instruments. The Investec Property Fund has a Domestic Medium Term Note Programme and announced yesterday that it has complied with all financial loan covenants. These are the “promises” made to noteholders, relating to metrics like interest cover and loan-to-value ratio. I’m sharing this update to give you a sense of the different types of capital that can be raised on our market.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Companies do a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

I co-host these events with Mark Tobin, a highly experienced markets analyst who combines an Irish accent with deep knowledge in the Australian market (I know, right?) and the team from Keyter Rech Investor Solutions.

You can find all the previous events on the YouTube channel at this link.

The latest event saw Tharisa plc’s executives presenting their business. This is a genuinely interesting mining group, with co-production of platinum group metals (PGMs) and chrome concentrates.

Sit back, relax and enjoy this video recording of our session with Tharisa plc:

The red hat is a familiar sight in South African clothing retail. Mr Price has been on a major acquisition spree recently, so the company is on the radar of investors (and I entered a long position based on recent share price weakness as well). The release of Mr Price’s integrated annual report gave Ghost Grad Jordan Theron a good reason to dig in.

Since its first store opened in 1987, Mr Price has won the hearts of many South Africans. This has been further cemented by their reputation for great value and sponsorship of various sporting events and teams such as the Comrades and Team South Africa at the 2021 Tokyo Olympics.

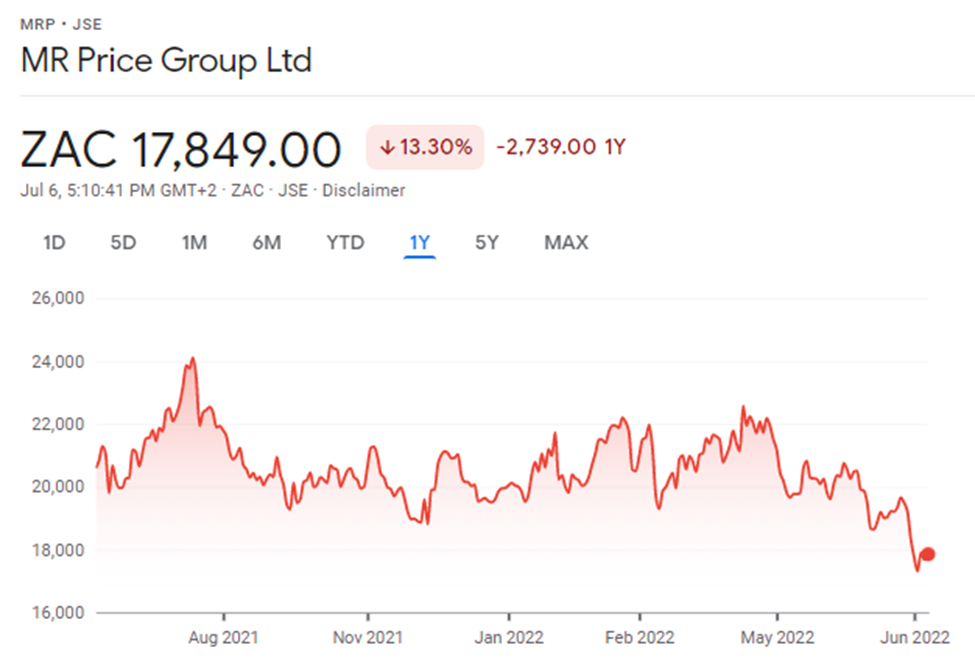

The share price itself is in need of some sponsorship, down 13.3% over the past year:

A podium-worthy CAGR

Feel-good sponsorships aside, this is a serious business and Mr Price has produced a 36-year sales CAGR (Compound Annual Growth Rate) of 17.5%. This is a remarkable performance, particularly over such a long period. If the US market wasn’t on fire right now, this kind of growth rate would even get US growth investors excited!

I had to dig deep into the investor relations sections of the websites to find this information: Truworths has achieved a 19-year sales CAGR of 15.3% and The Foschini Group has managed 13.2% over a 17-year period. These obviously aren’t directly comparable to the period given by Mr Price, but it’s still interesting to compare them.

Mr Price is hugely popular among shoppers

Over 3 months, Mr Price’s resonance with customers drove customer engagement to such a level that the group is the most shopped fashion retailer in the country, with 5.7 million shoppers. With approximately 35% of South Africa’s population living in rural areas where even Mr Price may not have a presence, this is a particularly impressive statistic in terms of share of (realistic) total addressable market.

Clothes, yes, but also cellphones

The financial services and telecoms segment at Mr Price grew operating profit by 85% in the last financial year. Although this segment may be small, the cellular side of the business grew by 32%. In years gone by, the cellular division barely got mentioned in annual reports.

These days, investors know that clothing retailers have tapped into the lucrative cellphone market. It’s all about having an attractive retail footprint and enough trust from customers to bring them additional products.

Second only to Takealot

Mr Price makes wonderful profits and Takealot still doesn’t. In fact, Takealot even made a loss during the pandemic, which was surely a golden period for online shopping. If you think that Takealot operates in a competitive vacuum and that profits are guaranteed to come, think again.

Mr Price has moved strongly into the online space through capital investments and acquisitions. The group’s share of online traffic is 13.3%, which is second only to Takealot among omni-channel and pure-play retailers. This puts Mr Price ahead of Woolworths and The Foschini Group.

Moving along the LSM curve

In South African retail, a group like Shoprite has shown us the value of operating throughout the LSM curve (i.e. having lower-income and higher-income store formats). Mr Price has made a strong move into the premium market segment, which we know is lucrative in this country.

Mr Price agreed to acquire a 70% stake in Blue Falcon, which owns the Studio 88 Group, from RMB Holdings for R3.3 billion. The deal was announced in mid-April. This is a strategic move to “buy” market share in the more premium and ever-expanding Athleisure segment. Studio 88 is South Africa’s largest independent retailer of branded leisure, lifestyle and sporting apparel, with footwear also included under their umbrella.

Riots, unrest and unhappy things

An assessment of Mr Price wouldn’t be complete without a look at how the group handled the period of despair in 2021 when riots broke out mainly in KwaZulu-Natal. This is the province in which Mr Price has its primary distribution centre.

The riots resulted in 539 stores temporarily closing during that week and 111 remaining closed due to damage. There were 96 stores reopened by end of the 2022 financial year, with five reopening in 2023 and ten in 2024.

After enduring this disaster, Mr Price received R296 million from SASRIA for stock, cash, and fixed asset losses as well as R92 million in business interruption insurance which somewhat mitigated the negative impact.

The future

It’s easy to be pessimistic about South Africa. Mr Price thankfully doesn’t feel that way and is ambitiously growing in the local market, through a combination of acquisitions and organic initiatives.

It’s always a risky strategy, as acquisitions are notoriously difficult to integrate and companies tend to overpay for businesses that they want. Only time will tell how this plays out.

Over the past 10 years, Mr Price has only delivered a share price CAGR of 4.1% which is disappointing. With a goal to become Africa’s largest retailer, could the next 10 years will look different?

Nampak has lost 40% over the past 6 months as the market got jittery about the turnaround story and the exposure to African economies in a risk-off environment. There’s some relief for investors, with the company announcing that funders have agreed to extend the deadline for a R1 billion net interest-bearing debt reduction to 1 April 2023. In simple terms, this gives the company more time to solve its balance sheet problems. The share price only closed 2.5% higher on this news, admittedly on a bright red day for the JSE.

Blue Label Telecoms is in the process of recapitalising Cell C, a company that has never managed to sustainably compete against the leading mobile giants in this country. One of the steps is a compromise offer being made to holders of Cell C’s first priority senior secured notes. The notes have a face value of $184 million and carry a rate of 8.625%. After a quorum wasn’t achieved for the first meeting, an adjourned meeting was held on Tuesday and the resolutions were passed in favour of the offer. Blue Label hopes to close the recapitalisation transaction in late July. Please take note of the director dealings below as well.

Irongate has managed to leap over another hurdle in the process of Charter Hall acquiring and delisting the fund. The Supreme Court of New South Wales has given the nod of approval to the scheme. All conditions have now been satisfied and the implementation date is 15th July. We will shortly bid farewell to this listed property business.

Earnings updates

Tin miner Alphamin has announced record quarterly tin production and has given Q2’2022 EBITDA guidance of $66.5 million. This is the company that reminds us in every single announcement that it produces 4% of the world’s mined tin from its operations in the Democratic Republic of Congo. In the quarter ended June 2022, production volume was 4% higher than in the three months ended March 2022 and sales volume was down 3%. EBITDA was down by a whopping 32% quarter-on-quarter though, as the tin price achieved dropped by 19%. Net cash increased by 6% to $138 million. An interim dividend of 38.13 cents per share has been declared. The company is exploring the Mpama South project, which would take Alphamin’s production to around 6.6% of the world’s mined tin.

Share buybacks and dividends

There’s an interesting scenario playing out at Datatec. The cash dividend is 111 cents per share and the current share price is R43.01, so that’s a 2.6% dividend. There’s a scrip dividend alternative though, which means investors can elect to receive shares instead of cash. Here’s the fun thing: the scrip alternative is based on the ratio that 111 cents bears to the 30-day volume weighted average price up to 4th July, which is only R36.77 per share because it shot up recently based on the announcement to sell Analysis Mason. This has made the scrip dividend far more attractive than it would usually be, effectively being issued at a 14.5% discount to the current market price.

Another scrip dividend decision is facing shareholders of Accelerate Property Fund. If I understand the announcement correctly, the difference between the cash dividend and the scrip dividend is substantial. The final price for the scrip dividend will be announced on 12th July.

Not all buybacks relate to ordinary shares. We’ve seen banks mopping up preference shares on the market, as this has become a less desirable source of capital for financial institutions. Investec has gone the route of a general buyback, repurchasing just over 3% of the issued preference share capital. The aggregate value of repurchases was R90.5 million.

Notable shuffling of (expensive) chairs

After the tragic passing of founder David Kan, Mustek has needed to make big decisions about who will take the company forward. With Hein Engelbrecht now appointed as group CEO, additional appointments include Neels Coetzee as the head of the largest operating company in the group and Shabana Ebrahim as Group Financial Director. It’s really not an easy situation for the team at Mustek and I wish them well.

Director dealings

With Blue Label Telecoms busy trying to rescue Cell C, certain directors seem to be voting with their money and in a way that shareholders won’t like seeing. The spouse of an independent director sold shares worth over R40k and an entity related to a different director sold shares worth over R292k.

Value Capital Partners is an investor in PPC and the investment principals sit on the board as non-executive directors. This means that whenever the investment fund increases its stake, it shows as a dealing by an associate of directors. The fund has bought shares in PPC worth nearly R9 million.

A director of Trematon is buying shares in the company, admittedly in relatively small transactions. The latest purchase is only worth R28k. It’s an illiquid share with a wide bid-offer spread though, so the director seems to have standing bids in the market that are being hit from time to time.

Unusual things

Aveng’s McConnell Dowell business has been in dispute with a customer since March 2016. This is a great reminder of how slow a legal process is. In great news for Aveng, the claim has been settled and payment of R282 million has been received. This cash has been retained by McConnell Dowell. Separately, the company repaid R275 million in debt in June, taking the total debt reduction over the past financial year to R350 million. If the Trident Steel deal goes ahead, Aveng would settle remaining debt in South Africa and would have a stronger financial position. Aveng dropped 5% on the day and has lost 44% of its value this year, as the market has lost all interest in marginal plays.

We all know that it’s practically impossible to only buy what you actually went to Dis-Chem for. There are many things about the pharmacy group that most people don’t know, so Ghost Grad Karel Zowitsky took a closer look.

Dis-Chem listed in 2016 at a valuation that was simply far too high, so investors suffered years of disappointment.

The recent story looks a little different, with the share price trading 20% higher than the levels at the start of 2020.

To show you how important it is to avoid frothy IPOs (new listings), here’s a chart of Dis-Chem vs. Clicks over the past five years:

Dis-Chem recently released its integrated annual report along with the audited annual financial statements for the year ended 28 February 2022. This typically doesn’t give any new price sensitive information, as the results are announced earlier than the release of full reports. For those willing to dig deeper and learn about the company, there are usually some interesting nuggets that can help flesh out an investment thesis (or give you more reasons to avoid the company).

It’s a bit like shopping at Dis-Chem – the more you look, the more you find!

The underlying numbers look good for the latest financial year. Revenue grew by 15.7% to breach the R30 billion mark for the first time in the group’s history and operating profit grew by 21.6%.

Let’s take a deeper look at the business.

Pharmacy-first approach

It’s important to understand that Dis-Chem believes in a pharmacy-first approach. This strategy ensures that there is a dispensary in every store along with the front shop. Conversely, Clicks was a health and beauty retailer that subsequently added pharmacies to the stores, so the DNA of the groups is different.

The dispensary is the biggest driver of footfall, with more than 2.6 million scripts filled in an average month. This is not the main driver of profit, as dispensed medicine has a regulated Single Exit Price that doesn’t provide the juiciest of margins, making Dis-Chem reliant on the front shop (the rest of the store) to achieve a healthy gross margin overall.

The exact same strategy applies to Clicks and even the little pharmacy up the road from you.

To make the economics even trickier, pharmacists are the highest earners among customer-facing retail store staff – and by a significant margin. The combination of low-margin products and expensive staff is why pharmacist groups try everything possible to optimise store schedules. If you’ve ever wondered why you sometimes wait 30 minutes in a queue for a pharmacist, now you know.

The reason you struggle to go into Dis-Chem for “just one thing” is because the store is designed that way. The idea is to tempt you en route to the dispensary with all the front shop items. Now you also know why the dispensary is always furthest from the entrance!

Organic products and inorganic growth

When a company is following an “inorganic” growth strategy, it is growing through acquisitions. This is what sets Dis-Chem apart at the moment, as competitor Clicks is following more of an organic growth path while experimenting with new things, like a dedicated baby store format.

If we turn the clock back a bit, we find an acquisition that was a clear show of strategic intent by Dis-Chem. The Baby City acquisition(at a ticket price of R430 million) became effective on 1st January 2021. A quick walk around the store is a great way to delay any plans to have a baby, as the costs of having a little person are incredible. My mother can wait longer to become a grandma! (note from The Ghost – as the parent of a toddler, I can confirm this!)

Baby City is a strong business with a solid footprint and reputation among parents. A key benefit of the Dis-Chem acquisition is that the Dis-Chem loyalty programme can now apply at Baby City as well. The financial pressures of having a baby are significant and parents tend to look for every saving opportunity.

Integrated reports tend to provide plenty of information about stakeholders like the community, so it’s worth mentioning that the Dis-Chem Foundation is a beneficiary of the loyalty programme. The Foundation has been around since 2006 and a portion of the purchase value each time a card is swiped is donated to it, providing funding for projects that provide people with water, food, shelter, and warmth.

Moving on, October 2021 saw Dis-Chem seal the deal on Pure Pharmacy Holdings (trading as Medicare Health) by acquiring 100% of the outstanding share capital for R282 million. The acquisition provides control over 48 Medicare stores, which are now being rebranded into Dis-Chem stores, giving a healthy boost to Dis-Chem’s footprint with an additional 17,721m² of floor space. Importantly, this gives Dis-Chem access to areas in which it was previously under-represented.

It is difficult to grow a pharmacy footprint organically, as obtaining regulatory approvals to open a pharmacy is a lengthy and tricky process. This is the main reason why South Africa still has many independent pharmacies. An acquisition of a chain of pharmacies is gold for the likes of Dis-Chem, with a few hoops to jump through along the way with the Competition Commission.

In November 2021, Dis-Chem acquired 25% of the issued share capital inKaelo for R192 million, a group that owns AskNelson (a psychological wellbeing platform often utilised by organisations to provide support for their staff), occupational health clinics as well as gap and primary health insurance products.

This acquisition solidified an interesting partnership between Dis-Chem and Kaelo that saw the launch of Dis-Chem Health, a provider of three products: primary healthcare insurance, gap cover, and accident cover. The group notes that there are currently 12.4 million employed, yet not medically insured people in South Africa, which provides a strong case for affordable medical insurance.

Dis-Chem is following an aggressive expansion strategy and investors should keep an eye on it. Year-to-date, Dis-Chem has lost 7.5% of its value and Clicks is down 12%. There’s no medicine for a bear market, sadly.

It seems like deals are falling over left and right in this environment, both locally and offshore. The latest example is Texton Property Fund, whose sale of the Foretrust and Loop Street properties is no longer going ahead. The intended buyer (Stonehill Property Group) was unable to fulfil the necessary conditions for the deal, despite an extension that was granted from 12th April until 30th June.

Another example is Delta Property Fund, which has seen the sales of Fort Drury and Sediba for a combined price of R76.5 million fall over. On the plus side, the fund has announced an unrelated disposal of three properties (two in Sunninghill and one in Port Elizabeth) for R76 million. Delta really needs this to go through, as it would reduce the loan-to-value (LTV) from 57.0% to 56.9% and vacancy levels by 30 basis points from 31.3% to 31.0%. Those are still frightening numbers.

Hyprop and Attacq are co-invested in the Ikeja City Mall in Lagos, Nigeria. The funds are in the process of selling the property and the necessary application has now been made to the country’s competition authorities. The longstop date for the transaction (i.e. the date by which it needs to be completed) has been extended to 31 December 2022.

Kibo Energy has agreed a three-month extension for the redemption of convertible instruments. The redemption date is now 30 September 2022 and covers notes to the value of just over £0.65 million

Earnings updates

Salungano Group (previously Wescoal) has released results for the year ended March 2022. The group met the 8mt production target for the year and secured its first coal exports, as it looks to diversify from our part-time electricity provider Eskom. The group wants to become a diversified investment company, with agriculture and renewables in the cross-hairs. This kind of behaviour usually terrifies investors. Despite revenue increasing by nearly R1.24 billion, operating profit increased by just R3 million. There is once again no dividend for shareholders.

If you would like to take a detailed look at PPC’sresults for the year ended March 2022, the annual financial report is now available at this link.

Share buybacks and dividends

Investec has been busy with a buyback programme since approval was granted at the AGM in August 2021. The company has repurchased 3.13% of shares in issue under that approval for a total value of R852 million. The average price paid is R85.24 which compares favourably to the current price of R86.72.

I don’t cover it often as the company gives a daily update of buybacks, but it’s worth reminding you that British American Tobacco is busy buying back its own shares. This is typical of a value stock that is treated by investors as a cash cow with questionable long-term growth prospects.

While I’m at it, I may as well use a quieter day of news on the JSE to remind you that Glencore is buying back shares and releasing daily updates as well.

Notable shuffling of (expensive) chairs

Growthpoint has appointed Andile Sangqu as Lead Independent Director, an important role in corporate governance.

Anglo American has appointed Helena Nonka as Group Director of Strategy and Business Development. I have worked in similar teams in more than one listed company before. These are the teams that deal with large corporate deals and projects that sit outside of business-as-usual for the group. Nonka comes from a similar role at a renewable energy company, which gives some indication of the skills Anglo is clearly looking for.

Director dealings

A non-executive director of Kaap Agri has bought shares in the company worth around R145k.

An associate of a director of Raubex bought shares worth around R1.48 million, yet another one to add to a long list of recent insider purchases at the company. The directors are piling into Raubex shares.

Michiel Le Roux (founder of Capitec) has reminded the rest of us how poor we are. His investment entity has raised around R566 million of loan funding using shares in Capitec as collateral. This comes with a derivative collar structure, which protects Le Roux from the Capitec share price falling below R1,812.58 per share. It also caps his upside on these shares with a call strike price of R3,222.37. The structure’s average expiry date is 3.3 years from now.

Unusual things

Visual International has been sent to the JSE’s naughty corner for failing to release an annual report on time. Based on the financial situation at that group, I think the report is the least of the worries.

There are often announcements that are immaterial to most readers (like low value director dealings, acceptance of share-based awards and changes in non-executive directorships) that don’t make the cut for Ghost Bites, though they may have some relevance to you. Ghost Bites (and Ghost Mail) is never a replacement for your own research into an investment.

Last week, Chris Gilmour took a detailed look at the non-discretionary retailers on the JSE. This includes the grocery stores and pharmacy chains. This week, the focus is on the discretionary retailers, which would include clothing, furniture and perhaps some DIY too. In part 1, Chris focuses on Woolworths.

Included in the discretionary retailer universe are three clothing retailers (Truworths, Mr Price and The Foschini Group), a hybrid clothing and food retailer (Woolworths), a retail conglomerate (Pepkor), a furniture retailer (Lewis Group) and a DIY / Home Improvement retailer (Cashbuild).

What is notable from the outset is how poorly most of these retailers have performed in the past five years on a relative basis, with a few exceptions such as Lewis and Cashbuild. With Woolworths, the pain has largely been self-inflicted with the ill-conceived acquisition of David Jones in Australia. The same goes for Truworths, a really good and well-managed business but one that has a slavish adherence to credit and nothing else. Two retailers, Mr Price and The Foschini Group (TFG), deserve special mention for expanding into the pandemic-induced downturn, rather than just accepting their fate. That strategy is now paying off handsomely for both.

Price

Market cap (R’bn)

Price / Earnings multiple

Revenue (R’bn)

HEPS (5-year CAGR)

Woolworths

5380

56.3

19.1x

78.8

-3.85%

Mr Price

18316

49.3

14.3x

28.1

7.60%

Pepkor

1970

74.6

12.8x

77.3

n/a

TFG

12346

41.1

12.2x

46.2

-1.53%

Cashbuild

25300

6.5

10.3x

12.6

8.70%

Truworths

5218

22

8.3x

17.5

-4.81%

Lewis

4980

3.1

5.9x

7.3

16.2%

Woolworths

Probably the most well-known (and loved) discretionary retailer in SA is Woolworths (Woolies). Based unashamedly on the Marks & Spencer (M&S) brand in the UK, it has been around in SA since the 1930s.

Woolworths management should exit Australia, not just David Jones, and demerge the food and clothing divisions in South Africa into two separate companies. The real beneficiary of this would be the shareholders, who over the past 5 years have experienced substantial value destruction. And despite strong rumours circulating in Australia that Woolworths is indeed considering selling David Jones, the company itself continues to deny this speculation outright.

The plan with David Jones when it was originally purchased was to increase the own-branded portion of the merchandise offering, do more direct sourcing and achieve better stock management with improved information systems, which would in turn increase the gross margin and double the net margin over the following few years. It all sounded like good retailing. Effectively, as management said at the time, they were going to take the Woolworths concept to Australia, using the David Jones brand. Marks and Spencer had worked in the UK, particularly the food offering amongst some strong competitors, so it would seem that Woolworths could do the same in the Southern hemisphere.

That is not what happened in our view. In reality, what happened was almost the opposite. At a time when the department store format around the world is in decline it would seem that Woolworths brought the David Jones department store format to South Africa, turning the clothing, beauty and home business into a department store, which in turn is now struggling.

Woolworths South Africa has for many years had a close relationship with M&S. The two companies have shared suppliers, sourcing skills, technology, product strategy, branding strategy and used to provide graduate trainees with opportunities to work in each other’s companies. If you were to walk into a Woolworths Store in South Africa, you would be forgiven for thinking you were in a Marks and Spencer store. Even the last chairman of Woolworths, Simon Susman, who used to be CEO and head of Foods, has family connections to the founding family of Marks and Spencer.

But we believe that due to the close connection, as well as other factors the businesses are more alike and face similar threats. Due to the competitive nature of the UK retail market, M&S has, we believe, faced tough times sooner than Woolworths. Additionally, Woolworths has been one of the main beneficiaries of the demise of Edgars and the wider Edcon group. This has plastered over the real devastation that is occurring in the retail market for not just Woolworths but other retailers too.

The signs are now there that Woolworths is facing a critical period in its history.

Woolworths South Africa used to be part of a larger retail group, called the Wooltru Group. This retail group included Massmart and Truworths as well. The Wooltru group demerged the subsidiaries as the synergies that the management thought it could achieve were not being achieved. The group had outgrown itself. Investors wanted focused investment and we believe the same still applies today.

In our view, there are no synergies or rationale to keep the food business tied to an ailing department store in Australia and a struggling quasi-department store in South Africa. Investors would most likely value the food business higher if it were not encumbered by the rest of the companies within the group, from which it gains in our view no synergies or benefit.

There is no reason why the Foods business should be retained within the larger clothing retail group, especially since food has been removed from the Australian retail offering. A focused food retailer with the market positioning and customer profile of Woolworths Foods would become one of the most highly rated retail companies in South Africa. As top line growth slows and cash generation increases, it could become a haven for investors in a time when the economy is starting to slow, much the same as the Clicks Group

Woolworths Foods is a hugely aspirational and iconic brand in South Africa and that brand equity has been established over many decades of delivering ultra-high quality foods without ever compromising standards. But new space growth has been tapering off in recent years, with no apparent new growth vector in sight. In a South African economy that is likely to languish for the foreseeable future, our base case scenario is for Foods to become a cash cow for the rest of the business.

This is the least troublesome part of Woolworths’ business and has been so since the company’s genesis. While the clothing division has often got it wrong with respect to fashion, Foods has just kept pumping out healthy growth. However, it may be reaching saturation in a languishing South African economy with no obvious new meaningful growth vectors in sight.

It has always resonated with upmarket shoppers, as it has got the mix right in its stores. The layout is also very clever; shoppers invariably have to walk through the clothing part to get to Food and in the process are susceptible to cross-shopping opportunities.

Back in the mid 2000s, when Simon Susman was CEO, Woolies Foods embarked upon an extensive rollout of standalone convenience stores. And while a number of these stores undoubtedly cannibalised existing stores in close proximity, the fact that the background economy was growing reasonably well meant that lost market share was soon recouped by the cannibalised store.

It is current management’s aim to concentrate its efforts on locating any new retail space in larger shopping centres. This despite the obvious trend that has emerged since the Covid lockdown of consumers preferring local shopping.

Profit margin appears to have plateaued

Ten years ago, in financial 2011, operating profit margin was a relatively low 3.8%. Throughout most of the last decade, this margin increased consistently, as the new store rollout programme matured and as previously franchised businesses were converted to Woolies Food corporate stores. In financial 2021, operating margin was 8% and appears to be stabilising at around that level. Gross profit margin has been very steady between 23.5% and just over 25% in the past decade.

With very little new space growth likely to materialise in the next few years, margins are likely to remain at or around current levels.

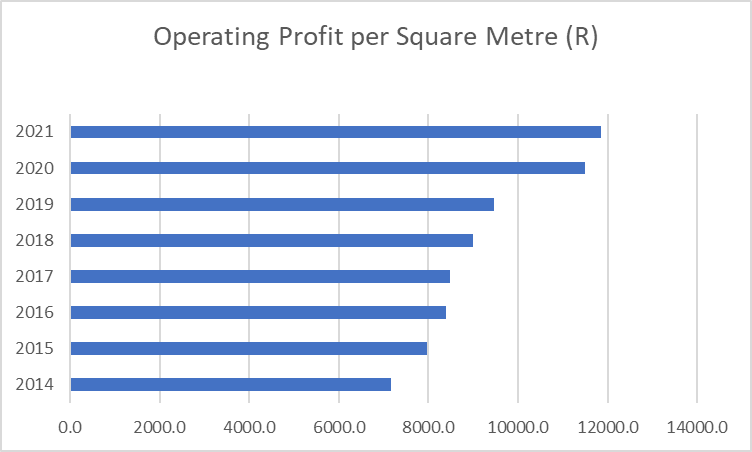

The ability of Woolies Foods to profitably exploit its existing floor space is demonstrated in the following chart of operating profit per square metre. There is a very satisfying upwards trajectory, which has improved noticeably in the 2020 financial year, as square metreage stayed fairly constant.

A league apart when it comes to quality

For many decades, Woolies has been in a league of its own when it comes to high quality food shopping. Other than a handful of specialised independent stores and upmarket Spars, the competition has largely left Woolies’ traditional stomping ground alone. Pick n Pay tried competing on the convenience format not long after Nick Badminton took over as CEO but that challenge didn’t last long, as it was unable to cement long-lasting supplier agreements to supply high-quality convenience and other meals. More recently, Checkers has entered the fray with a degree of success, albeit with an as yet limited offering.

Woolies’ dominance of the convenience food market is based on their ability to source a good range of exclusive suppliers and retain them but also to be able to supply their stores with these items at precisely the correct temperature. It has taken many years to attain this status and new entrants will find the going difficult if they wish to compete.

Often, Woolies’ relationships with its suppliers go back many decades and are established literally with a handshake. Woolies insists on exclusive supply relationships with its suppliers, so there is no possibility of a Woolies’ supplier also supplying Checkers for example, other than in the mainstream national brands arena.

However, a relatively new incipient threat to Woolies’ traditional dominance of the convenience food market may lie in the recent phenomenon of recipe boxes / meal kits. The leaders in the field in Europe and the UK are HelloFresh, Gousto and Mindful Chef but South Africa has recently joined in with operations such as Ucook, Takealot, Netflorist and Daily Dish springing up. Admittedly Woolies has risen to the challenge with its own range of recipe boxes but not surprisingly they tend to be more expensive.

Woolies Foods dominates private label food capacity in SA

South Africa suffers from a dearth of food producers that are prepared to supply food retailers with own-brand or private label products. Woolies has certainly managed to grab the lion’s share of private label capacity in South Africa, with long-standing arrangements between itself and Rhodes Food Group, Libstar and Interfoods for example. Notable among the large local food producers that are unable or unwilling to participate in private label production is Tiger Brands. Tiger steadfastly refuses to produce private label on the grounds that by so doing it would dilute the value of their existing brands.

Home delivery

Home delivery is regarded as a loss leader for many retailers and Woolies is no exception. It may well find that outsourcing its home delivery completely to the likes of a Takealot would make more sense than persevering with in-house capability. M&S has achieved this in its relationship with home delivery specialists Ocado in recent years.

Rest of Africa not a serious proposition for Woolies Foods

The rest of Africa was a growth vector for a number of South African retailers post 1994, although that trend has reversed in the past couple of years, with Shoprite having exited a number of African jurisdictions. Woolies Foods has hardly ever ventured far into Africa, other than into the neighbouring states. To date, only clothing stores have been opened in the rest of Africa (apart from Botswana and Namibia), for the simple reason that the very low tolerance demanded by Woolies for chilled and frozen foods cannot be guaranteed in most African countries, due mainly to erratic electricity supplies.

Woolies can guarantee cold chain to the neighbouring states. If it were to go farther afield to the rest of Africa, it would be an entirely different challenge. So for example, Woolies could deliver certain frozen and long life products into the rest of Africa but they decided against it as they want to bring the full Woolies Food experience or nothing.

And former CEO Ian Moir made it quite clear when he made his ill-fated decision to buy David Jones in Australia: Woolies saw far more growth potential in Australia than in the rest of Africa.

Woolies Food market share is remarkably high

Market share among listed food retailers is estimated at around 10%, making it the smallest of the “big four” – Shoprite, Spar, Pick n Pay and Woolies. Woolies’ perceived grocery universe size is between R350 billion and R400 billion. According to management, market share is growing, though they won’t be drawn on exact numbers.

This is a remarkably high level of penetration, especially considering that Woolies Food is a very upmarket offering, operating in a developing country with the highest rate of persistent unemployment of any country in the world. To increase that market share meaningfully beyond the current level, given the likelihood of a languishing local economy appears highly ambitious.

Woolies’ price points are substantially higher than their competitors.

Woolies Foods price points are substantially higher than those of their JSE-listed competitors and are similarly priced to small-scale artisanal food producers. The reasons is simple: the quality of their foods is much higher than that available at the competition and Woolies’ fresh offering, for example, is preserved much better. For as long as the South African economy was showing even moderate growth, this wasn’t a problem, as Woolies shoppers tend to be willing to pay up for the kind of quality that is conspicuous by its absence at the other large retailers. But with the local economy likely to experience anaemic growth beyond the current year’s bounce-back from the Covid pandemic, the ability of Woolies Foods to carry on charging such ultra-premium prices may be reaching a tipping point.

At this point it is worth reflecting on a paragraph in the 2019 Marks & Spencer annual report:

“In 2018 we acknowledged that our Food business had become too premium and lost some of its broader appeal. While customers still recognised us for quality, the competition had worked hard to match our success by copying our innovation and fresh product ranges and we hadn’t kept up. The challenges were compounded by our outdated supply chain, with excessive waste, poor availability and high operating costs eroding our profits.”

Is Woolies facing similar challenges in SA? Obviously not in cold chain but perhaps in Woolies being perceived as too premium?

Woolies management realised that their pricing in certain categories was simply too high and have partially addressed the problem by significant investment in price in the past couple of years, notably in poultry products.

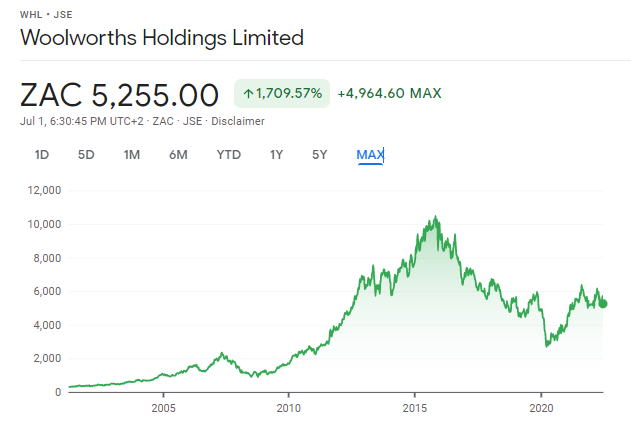

Although it may seem silly to draw such a long-dated share price chart, it does tell the story of this business in different economic conditions. Importantly, it also shows the value destruction after the acquisition of David Jones in 2014:

Next week, Chris will deal with more of the discretionary retailers on the JSE, like Truworths and Mr Price.

Ghost Global is a new weekly segment that will be brought to you by the Ghost Grads on a rotational basis. This week, Kreeti Panday updates us on earnings from some significant US companies.

Nike: direct-to-consumer is working

Nike has released results for the year ended March 2022, celebrating the group’s 50th anniversary.

Revenue has dropped 1% in the fourth quarter, largely blamed on macroeconomic challenges. The recent Covid-19 lockdown has caused difficulty for the company, with sales in Greater China dropping by 19% compared to the previous year’s period. Supply chain disruptions caused a rise in Nike-owned inventories of 30% compared to the prior year, as well as a 12% decline in wholesale revenue.

Despite this, Nike is still optimistic on the strength of its brand as a driver for consumer demand. Nike claims to be the no. 1 brand for athletes and sport in the 12 key cities around the world, specifically citing the fact that the Jordan brand has surpassed $5 billion in revenue.

Their Consumer Direct Acceleration strategy has also been kicking in. This is a strategy focused on direct consumer relationships i.e. owning the customer experience rather than selling through third-party retailers. Direct revenues were up 14% and the number of Nike-owned stores was up 10%. Nike has put a lot of emphasis on their effort to become more digitally connected with Nike Digital now comprising 24% of total brand revenue. The company believes that their increasing digital engagement, including Nike app downloads, is leading to more repeat buyers and higher buying frequency which will ensure long-term growth.

However, high inflation levels have led to concerns of lower consumer demand in favour of cheaper alternatives.

FedEx reports highest ever annual revenue

FedEx has closed its financial year ended March 2022 with highest ever revenue of $93.5 billion, an 11% increase from last year.

The really impressive thing is that operating margin managed to expand in the fourth quarter, despite challenges caused by labour shortages as well as external factors including Covid-19 lockdowns in Asia and geopolitical uncertainties in Europe.

FedEx is currently readying the company for a leadership transition, with Don Colleran moving into a CEO advisor role in September before his retirement in December after a 40-year tenure at FedEx. He will be replaced by Richard Smith, who has held numerous positions at FedEx since joining in 2005, including the position of CEO of FedEx Logistics.

FedEx has expressed concerns of slower inventory restocking leading to lower freight demand. The group also expects lower B2C (Business-to-consumer) volumes as consumers take any opportunity to leave their houses and venture into stores in the absence of Covid-19 restrictions.

Bed, Bath & Beyond a disaster

Bed, Bath & Beyond has released Q1 2022 results during a year in which many investors have pulled the plug. The share price is down over 65% this year and expectations for results were neither high nor were they met.

Revenue fell from $1.95 billion in Q1’21 to $1.46 billion in Q1’22, less than the expected $1.51 billion. The group also struggled with supply chain issues, with a 15% increase in inventory compared to the previous year. The turnaround strategy includes aggressive actions on costs and reduced capital expenditure. However, the outlook is stark as comparable sales continue to trend in the range of negative 20%.

The company announced a change in CEO from Mark Tritton to Sue Gove, previously an Independent Director and Chair of the Strategy Committee, as well as a change in the Chief Merchandising Officer position.

Hennes & Mauritz – you know the brand, you just don’t realise it

H&M probably rings a bell, doesn’t it? The Swedish retailer released results for the first six months of the financial year with sales in physical stores experiencing a steady increase in the second quarter. Majority-owned Sellpy (an ecommerce platform for second hand sales) has doubled sales in the last quarter.

The Russia-Ukraine war has caused a halt in sales in Russia, Belarus and Ukraine, which explains 500 basis points of the expected 6% decrease in sales for June. Rising inflation rates are also a cause of concern for H&M, as sales have also not yet reached pre-pandemic levels.

H&M has implemented a sustainability-focused strategy, aiming to halve carbon emissions while doubling sales by 2030.

BlackBerry is still out there, even if BBM isn’t

Canadian group BlackBerry (now primarily a cybersecurity company for anyone having flashbacks of typing their BBM messages with the edge of their fingernails) reported a gross margin of 62% in Q1 results. The company achieved a 19% increase in revenue from IoT (Internet of Things).

The type of work in this space includes designing a Digital Cockpit for the new Renault Jiangling, an electric sedan. This Digital Cockpit will make use of augmented reality, artificial intelligence, and hologram functions. BlackBerry expects growth of 8 – 12% in this area over the next three years.

BlackBerry achieved a 6% increase in revenue from cybersecurity. Developments in this space include joining forces with Google to create Chrome Enterprise Management. This will aid the growing number of devices running Google Chrome OS and Chrome browser. BlackBerry also develop software products and provide professional services.

If you are interested in global investment opportunities, then the depth of analysis in Magic Markets Premium will be incredibly valuable to you. For just R99/month, you will receive a weekly report and podcast covering a global stock. There are already nearly 35 reports in the library, including the likes of Nike and FedEx mentioned here in Ghost Global. With my Magic Markets partner Mohammed Nalla, I’m so proud to bring institutional-quality research to a retail audience at an affordable price. Visit the Magic Markets website to subscribe.

City Lodge Hotels punters will be pleased to know that the sale of the East African operations has become unconditional, which means there are no further hurdles in the deal. The effective date was 30 June and the proceeds will be received “imminently” – great news for the City Lodge bank account. The share price is down 29% this year and hasn’t shown signs of turning, despite a promising recent update from the company regarding occupancies.

Mondi has completed the sale of its Personal Care Components business to Nitto Denke (a Japanese diversified manufacturer) for an enterprise value of €615 million. Mondi is focused on growing in sustainable packaging and this business wasn’t seen as a strategic fit going forward.

Heriot REIT and Safari Investments are still sorting out finer details of the offer that Heriot is making to shareholders of Safari. The Takeover Regulation Panel has granted an extension for the offer circular to be posted by 29 July.

Earnings updates

Lesaka (previously Net1 – and now with a beautiful website instead of Net1’s hideous effort that looked like it was built using DOS) has released Connect Group’s financial statements for the 2021 and 2022 financial years. Remember, Lesaka just acquired this group for around R3.7 billion. Revenue was up 22% to R5.1 billion and gross profit grew 37% to R570 million. EBITDA was 26% higher at R382 million, outperforming the EBITDA that was “warranted” in the agreements i.e. promised by the sellers to the buyer. If you are interested in learning more, the company is hosting a webcast on 7th July that you can sign up for here.

Primeserv’s release of results has been slightly delayed. The numbers for the year ended March 2022 will be released on Friday, 8th July.

Share buybacks and dividends

Barloworld has given an update on its share repurchase programme. Over the course of June, Barloworld repurchased shares worth nearly R550 million at an average price of R91.33. This represents around 3% of shares in issue, with the authority from the AGM in February allowing for a further 7% of shares in issue (at the time of the AGM) to be repurchased. This has been a very tough year for Barloworld, with the share price down nearly 43% after a significant destruction of value in Russia that was obviously beyond the group’s control.

If you are a shareholder in Industrials REIT, please be aware that you need to choose whether to receive the next distribution in cash or in shares. The default selection is cash, so you need to act if you would prefer to receive more shares. Companies usually do this in an effort to preserve cash, as they would rather issue more shares than pay cash out of the group. Interestingly though, as the group is trading at a discount to net asset value, the board notes that it may execute buybacks to match the level of shares issued, so as to not dilute shareholders. This makes me wonder what the point of the scrip dividend is. I’m sure the answer lies somewhere in the circular which was distributed to shareholders on Friday, so make sure you read it if you are invested here.

Telemasters Holdings has announced a dividend of 0.5 cents per share. The share closed at R1.10 on Friday, so this dividend isn’t going to set anyone’s pants on fire.

Notable shuffling of (expensive) chairs

Following the tragic loss of iconic founder David Kan, Mustek has appointed Hein Engelbrecht as the new CEO. This secures continuity for the group, as Engelbrecht has been with the group for well over two decades.

York Timber has announced the permanent appointment of Gerald Stoltz as CEO of the group. This means that a new CFO will need to be appointed and the company will make an announcement in due course.

Shortly after leaving Altron as its CEO, Mteto Nyati has been appointed as an independent non-executive director at Massmart. He has plenty of experience in turnaround stories, so this is a solid appointment to the board for the struggling retailer. Massmart’s share price is down 42% this year as the group has struggled to find any success with formats like Game.

Director dealings

Back in June 2019, Famous Brands was trading at around R85 per share. The former CEO of Famous Brands and son of the founder entered into a collar structure around that time. This is a put option at R74.62 and a call option at R120.22, typically put in place as a defensive play for executives. The holder of the collar structure relinquishes the upside over R120.22 per share and is protected below R74.62 per share. With the share price at R58.70 on Friday, the put was exercised and the counterparty is now the proud owner of R14.2 million worth of shares at a price of R74.62, 27% above the market price. These structures are usually fully hedged by the counterparty (often a bank), with the bank locking in a margin in the pricing of volatility at the time of entering the collar.

An executive director has bought shares in CMH worth over R2.6 million. That’s a pretty big play at this point in the cycle, particularly with rising rates and clear pressure on consumers. The share price is up around 6% this year and 13.8% over the past 12 months. It does pay a large dividend, though.

An independent director of AngloGold Ashanti has bought shares in the company worth $80k (R1.3 million) – I’m glad he sees some value in the group. It would be nice if my gold shares eventually showed me some love.

A director of Kaap Agri has bought shares in the company worth R94k.

An associate of an executive director of Trematon has bought shares in the company worth R62.4k.

Unusual things

JP Morgan has reduced its stake in Clicks from 10.04% to 6.93%. I usually ignore institutional changes, but this one is notable because the Clicks share price is almost entirely supported by its offshore investor base. Local investors scratch their heads about the Clicks valuation on a regular basis. To see an international investor selling down like this is relevant, particularly in light of our current challenges with load shedding. What will it take to spook offshore investors?

The JSE has released a list of companies in the naughty corner for not submitting annual financial statements on time. Luxe Holdings, Chrometco, Brikor, African Dawn Capital and Sable Exploration and Mining are all in detention. In the case of African Dawn, the company confirmed in a separate announcement that the delay relates to a dispute with SARS and the impact this has on the financial statements.

There are often announcements that are immaterial to most readers (like low value director dealings, acceptance of share-based awards and changes in non-executive directorships) that don’t make the cut for Ghost Bites, though they may have some relevance to you. Ghost Bites (and Ghost Mail) is never a replacement for your own research into an investment.

PBT Group released its results for the year ended March 2022 and they tell a wonderful story. By operating in the big data and cloud computing industry, PBT enjoys incredibly high organic demand for its services. Swimming downstream is always so much easier than upstream. Margins are higher and all of it lands in the bank account, with near-perfect conversion of EBITDA into cash from operations. To understand more about this result and the business, read this feature article.

Industrials group Hudaco has released its results for the six months ended May 2022 and they are worth paying attention to. Operating leverage is clearly visible here, as strong revenue growth looks even better once you reach the bottom of the income statement. The balance sheet is growing in response to pressures on supply chains, but Hudaco has enough flexibility in its operating model to handle this with relative ease. To learn more about Hudaco, you should read this feature article.

Exxaro released a pre-close update for the six months ended 30 June. The API4 coal export price index has averaged around $270 per tonne vs. $151 in the six months ended December 2021. Total production is up 1% vs. the preceding six months and sales volumes are down 3%, which means the company has mostly taken advantage of the pricing but it could’ve been a lot better. Logistical constraints were the major issue, with export volumes down 27%! The ongoing pressures on local ports can only be good news for Grindrod, which has enjoyed incredible growth in its Mozambique port and terminals business (refer to this feature article for more information on that). To give an idea of just how bad Transnet is, the Mpumalanga export rail performance declined from 15 trains per week in 2021 to 8 trains per week this year. In good news for cash flows, capital expenditure is around 47% lower.

Sibanye-Stillwater must’ve been pleased to announce something unrelated to strikes or floods. The group already holds a 30.29% stake in Keliber (a Finnish mining and battery chemical company) and intends to exercise a pre-emptive right to increase the shareholding to 50% plus 1 share, which will set Sibanye back €146 million. In addition, Sibanye will make a voluntary cash offer to the minority shareholders of Keliber, other than the Finnish Minerals Group (a state-owned holding and development company). This would take the stake to over 86% if minorities accept the offer, which would come at a further investment for Sibanye of €196 million. A capital raise will then be executed with a potential equalisation mechanism that would get Sibanye to an 80% holding anyway, with a maximum possible cheque from Sibanye of €104 million for the raise. The total potential investment is thus €446 million, with a maximum of €250 million being in equity and the rest being in debt. Keliber is aiming to be the first fully integrated lithium producer in Europe, so this deal is core to Sibanye’s “green metals” strategy. Sibanye hopes to close the deal by February 2023. The share price is down over 15% this year, so Sibanye shareholders (like me) will be pleased to see positive momentum.

Alviva jumped by over 16% on the news that it may join the long list of companies that have departed from the JSE. The company has received an expression of interest from a consortium looking to buy the remaining shares in Alviva that they don’t already own. The consortium comprises major shareholders and empowerment partners of Alviva with an existing stake in the company of 18.6% of shares in issue. Key managers at Alviva have been invited to participate in the consortium as well. A cash offer of R25 per share will be made to shareholders, representing a premium of 30% to the 30-day volume weighted average price. Absa will be providing funding to the consortium. At this stage, there is no firm offer. If discussions between the parties reach that point, a firm intention announcement will be released.

Sabvest Capital has acquired a look-through interest of 18.95% in Halewood South Africa by participating in a consortium that bought the entire company from UK holding company Halewood International. This is a manufacturer of alcoholic and non-alcoholic beverages including Red Square and Caribbean Twist. There’s also a drink called Buffelsfontein, which sounds like it hurts the next morning. Sabvest’s investment is held through its 41.03% interest in Masimong Beverage Holdings and RMB has come in as a co-investor. The share price closed 8.8% higher on a day that burned bright red on the JSE, taking the year-to-date performance to a highly impressive 34%. This investment group is a lovely reminder that there is plenty of money to be made in the local market if you know where to look.

Datatec has withdrawn its cautionary announcement and released all the relevant details of the disposal of Analysys Mason for up to £210 million. The purchaser is Bridgepoint Development Capital. Datatec’s share of this number is approximately 38% of Datatec’s market cap and the proceeds will be paid to shareholders as a special dividend. This is a substantial value unlock, which is why the share price jumped 22.5% on the day. A deal of this size has many hoops to jump through, so the various approval processes will now get underway.

Merafe Resources has announced the benchmark ferrochrome price for the third quarter of 2022. The price of $1.80 per pound is a 16.7% decrease from the second quarter. The share price has gained over 36% this year and only lost 3.7% despite this announcement. With Eskom as a major risk for the group, there’s rigorous debate on Twitter about whether this company is truly a bargain. On a trailing Price/Earnings multiple of 2.4x, there’s a pretty big margin for error built into the valuation.

Pan African Resources closed 5% higher on a day that was red for the gold miners. The group has completed a definitive feasibility study on the Mogale Gold Tailings Storage Facilities that form part of the Mintails Mining assets near Krugersdorp. The highlight is that the project has the potential to increase the group’s current production by at least 25%. The real ungeared internal rate of return (IRR) is estimated to be 20.1% based on a gold price of $1,750/oz and an exchange rate of R15.50 to the dollar. Construction capex would be R2.5 billion with an estimated payback period of 3.5 years post commissioning. The construction period would be between 18 and 24 months.

Lighthouse Properties has released a pre-close update related to the six months ended 30 June. In April and May, turnover in the portfolio exceeded the 2019 pre-Covid turnovers by 5.1%. That’s a major turnaround from the relative performance of -6.1% in the first quarter of 2022. Notably, France is still running well below pre-Covid levels, with the uptick coming from Iberia and Slovenia. Vacancies increased slightly from 5.1% at December 2021 to 5.2% at May 2022. The share price is down around 24% this year.

When it comes to pre-close updates in the property sector, Resilient chose to play its cards close to its chest. In a very brief update, the fund noted that the South African portfolio achieved comparable sales growth of 9.7% for the five months ended May 2022. A positive reversion of 2.8% was achieved overall (i.e. new leases were signed at higher rates than existing leases), though Resilient does note that leisure-related tenants experienced negative reversions. There is still pressure on those tenants, but the removal of the mask mandate should help with that. The fund is busy with solar installations at various malls in South Africa and construction work at properties in France.

MAS Real Estate received strong support from shareholders to acquire six properties in Romania and extend its development joint venture with Prime Kapital. This is critical for the fund’s pipeline of acquisition opportunities in the region.

In an unusual combination of Lord of the Rings and general flatulence, Gandalf has struck gas in the Free State. Renergen is every geek’s dream, using names from Star Wars and Tolkien’s finest to refer to elements of its projects. Gandalf is a new gas blower and gas was intersected at 480 metres from the surface. Further drilling to 1,200 metres is expected to be complete by August. Separately, the company reiterated that the Phase 1 plant is making progress and so are the customer sites, so synchronisation of the project timelines should be achieved. There has been a cautious approach taken in testing, which has delayed things by a few weeks. In this case, “safety first” is definitely the name of the game. Renergen made significant progress with capital raising activities in the last quarter (both debt and equity), as detailed in the company’s quarterly report that you can read here.

Anglo American has a zero emissions haulage solution called nuGen, which sounds more like a USN product designed to help you get ready for summer. Names aside, Anglo has agreed non-binding terms to combine this with First Mode, the company that partnered with Anglo to build the technology. In other words, Anglo would take an equity stake in this business, which would remain independent and would operate under the First Mode name. Anglo needs to decarbonise its fleet of around 400 ultra-class mine haul trucks. This also requires investment in critical supporting infrastructure. Anglo has held 10% in First Mode since 2021 and will move to a majority holding under this deal. First Mode would offer similar services to other third parties, so Anglo effectively creates a profit centre out of decarbonising its fleet and helping others do the same. Clever stuff!

Wilson Bayly Holmes – Ovcon, which most of us simply know as construction group WBHO, released a trading statement for the year ended 30 June 2022. WBHO has withdrawn funding from the Australian operations and they have been placed into administration, a painful decision no doubt. The group provided A$119 million to settle obligations on that side of the pond and expects to be better off than this estimate by at least A$23 million. WBHO is also negotiating an exit on an amicable basis from the contract related to the Western Roads Upgrade. But by the time you take into account other costs to close the Australian business, the original A$119 estimate actually goes the other way, with an updated figure of A$135 million. WBHO can fund this from current resources and a three-year term loan facility. In the local business, revenue in Building and Civil Engineering is expected to be 5% lower and in the Roads and Earthworks division will be at least 11% lower. In both cases, operating profit is higher (by 8% and 4% respectively). The situation in the UK isn’t pretty, with revenue down by 25% and profit by 40%. There’s also no real improvement in the steel industry, with the Construction Materials segment revenue 15% higher and operating profit 48% lower. Across major areas of the business, the order book is considerably higher than a year ago and the balance sheet is in decent shape. Excluding the Australian operations, HEPS is expected to be at least 3.6% lower for the year ended June 2022.

Christo Wiese has entered into a derivative structure related to Shoprite shares. He’s sold puts at a strike price of R198.87, which means that he receives a premium and would need to buy the shares at that level if the counterparty so chooses. Wiese has also bought calls at R217.94, which means he has paid a premium to be able to buy the shares at that level if he so chooses. The maturity date is 15 December and 10,000 contracts were entered into for both trades, so the call exposure is higher than the put exposure. The current traded price is around R197.88, so my interpretation is that Wiese is happy to buy at this level anyway (hence the sold puts) and is looking for leveraged upside based on the share price increasing from here this year. You gotta risk it to get the biscuit, as they say.

Crookes Brothers has released results for the year ended March 2022. The agriculture group reports “operating profit before biological assets” which is interesting, as it tries to show the operating profit without the significant swings in the value of the “living” assets in the group. That number increased by 18% and the profit after biological asset fair value adjustments fell by 39%, so that gives you an idea of the volatility in that fair value measurement. Headline earnings per share fell by 16% to 229.6 cents. The Price/Earnings multiple is thus 18.2x but it hardly matters as there is almost no liquidity in the stock.

After a huge director dealings announcement related to Marcel Golding earlier this week, an associate of a different director bought shares in both Rex Trueform and African and Overseas Enterprises. The amounts were only R48.5k and R86k respectively, but it’s interesting to note this activity.

A director of Thungela has acquired shares in the business worth R195k.

Trustco has issued a cautionary announcement, so now you have to be cautious of a potential deal in addition to being skeptical of their accounting policies. An independent third party is having a serious look at the option to become up to a 70% shareholder in Meya Mining for $50 million. This potential deal is at term sheet stage and Trustco hopes to finalise agreements by the end of July.

Nictus has declared a final dividend for the year of 3 cents per share. This little company has a market cap of only R36.8 million and liquidity is practically non-existent. The spread is the size of the moon, with the best bid at R0.39 and the best offer at R0.92 per share. It’s worth noting that in the year ended March 2022, HEPS fell by 48.84% to 9.43 cents.

Eastern Platinum Limited has announced Wanjin Yang as its new CEO. The company is working towards restarting underground operations at the Zandfontein section of the Crocodile River Mine. An independent competent person’s report on the mine has been filed.

Bauba Resources, which Raubex is in the process of mopping up the minorities in, has announced that Nuco Chrome has been granted a mining right valid for a period of eight years. It will allow for the mining of chrome, cobalt, copper, gold, nickel and platinum groups metals in an area near Rustenburg.

Sable Exploration and Mining has released results for the year ended February 2022. The headline loss per share has been confirmed as -141.76 cents. The net asset value per share is -598.1 cents. So, in case you were curious, this isn’t exactly a financial powerhouse.

Property developer Visual International has reported a loss for the period ended February 2022 of R7.9 million. The announcement claims that this is an improvement from a loss of R7 million, proof once more that in the bottom of the dustbin on the JSE, the sponsors (or designated advisors for AltX companies) don’t even read announcements properly before releasing them. The auditors have raised a material uncertainty about the company’s ability to continue as a going concern.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")