Hudaco has released results for the six months ended May 2022 and they look juicy, with revenue up 11.8% and HEPS up by a substantial 25.1%.

It’s great to see the short-form announcement include a comparison of key financial line items to pre-Covid numbers. For example, revenue is 19.1% higher than the comparable period in 2019 and operating profit is 52.2% higher, so there’s through-the-cycle operating leverage here that shouldn’t be ignored. In other words, revenue grew faster than costs.

In case you aren’t familiar with Hudaco, this is a South African group that imports and distributes automotive, industrial and electronic consumable products. There are parts of the business that would compete with Invicta, for example. There are also consumer-facing parts of Hudaco, like recently-acquired CADAC (yes, the gas braai company – although many would argue that “gas braai” is an oxymoron).

I’ve written many times this year about how supply chain pressures are driving inflated balance sheets. In other words, more investment in inventory is needed. This either drives demand for debt from banks (which has not been as high as I expected) or a decision to retain more cash rather than pay higher dividends, which is the route most companies have taken. I guess they are nervous of banks after some of them behaved like such pigs in the pandemic (I’ve heard some frightening stories of opportunistic behaviour).

Hudaco has gone the route of adding debt, with bank borrowings up R266 million to R860 million. There’s plenty of internal reinvestment as well, with cash from trading of R558 million supporting a R459 million reinvestment in working capital.

Hudaco’s business model is hungry for working capital, not for fixed assets. This gives the group a lot of flexibility, as the balance sheet can shrink or grow in response to market trends and levels of demand.

With headline earnings per share (HEPS) of 857 cents, Wednesday’s closing price of R149 is a Price/Earnings multiple of 8.7x on an annualised basis i.e. by doubling the interim earnings. That’s a really quick-and-dirty approach, usually only useful in deciding whether to scratch deeper into a potential investment.

With a share price up more than 16% this year, that’s probably all the evidence you need to justify doing more research into Hudaco and forming a view.

PBT Group is a really interesting business that gives local investors a way to access themes like “big data” right here on the JSE. The share price is up nearly 10% this year, significantly bucking the bear market trend.

PBT describes itself as a “technology agnostic data specialist organisation” – although this may sound like the usual corporate marketing gumph to you, there’s a critical point here: PBT isn’t tied to any particular technology provider or product. The group provides specialist services that clients can use whether they are running on AWS, Azure or anything else.

Around 91% of revenue is earned from time and material fees, with 9% from projects and fixed-price contracts. The latter has reduced significantly from 25% of group revenue in 2019.

This model does a great job of keeping the till ringing, with strong organic revenue growth. The management team here knows what they are doing, with cost management leading to EBITDA margin expansion.

To put some numbers to it, revenue jumped by 24% in the year ended March 2022, coming in at R975.7 million. Operating profit grew by 45%, as the group achieved higher operating margins.

Here’s something you won’t see every day: earnings before interest, taxes, depreciation and amortisation (EBITDA) of R138.6 million was converted into R135.8 million in cash from operations. That is a near-perfect cash conversion performance, which speaks to high quality earnings and a business model that is a well-oiled machine.

Headline earnings per share increased by 64% to 82.89 cents, so yesterday’s closing price is a Price/Earnings (P/E) multiple of 10.25x. On a normalised HEPS basis (75.56 cents), the P/E is 11.25x.

The total dividend for the year was 57 cents per share, so the yield is 6.7%.

Looking at divisional insights, the South African business has a strong pipeline across its service offerings. A shortage of local skills remains a hindrance though, with the PBT Cloud Academy trying to play a role in addressing this.

The group says that its European business is “starting to fulfil its anticipated potential” and described the United Kingdom business as being an “outstanding contributor” – this is all good stuff. PBT is even starting to service US-based clients from the European operation.

The business in Australia is focused on the healthcare industry, with a team based in Melbourne that is servicing clients in Australia and even in the UK.

PBT isn’t the most liquid counter around, yet it is a favourite among small cap investors who want to buy exposure to a growth industry at a reasonable multiple. The P/E isn’t cheap anymore, but the business is doing a good job of justifying why. This is a great example of the opportunities on the JSE that not enough people talk about.

Sibanye Stillwaterintends to exercise its pre-emptive right to increase its shareholding in Finish mining and battery chemical company Keliber Oy from 30.29% (acquired in February 2021) to 50% plus one share at a cost of €146 million. The company will also make a voluntary cash offer to the minority shareholders of Keliber (excluding the state-owned Finnish Minerals Group) for a total consideration of €196 million. If successful its shareholding in Keliber will increase to 86.1%.

Alviva’s empowerment partners Tham Investments and DY Investments 3 have issued a non-binding expression of interest to acquire the remaining 81.4% of the company at an offer price of R25 per share (representing a 30% premium to its 30-day VWAP of R19.50) in a potential deal valued at R2,4 trillion. The consortium has received an offer of funding from Absa.

In August 2021 Datatec announced it was to undertake an evaluation of strategic options and initiatives to unlock shareholder value. An update in May disclosed that negotiations were underway regarding Analysys Mason (AM). This week the company, via its UK subsidiary, announce the disposal of its 71.2% stake (diluted from 79.4% prior to completion) in AM for £136,1 million. The deal with Bridgepoint Development Capital will see BDC also acquire a 21.4% stake of AM from management.

Anglo American has agreed to lead the latest investment round of Sanergy, an organic waste upcycling business with operations in Kenya. Sanergy manages waste by upcycling it into high value agriculture and energy products – such as insect-based protein for animal feed, organic fertiliser for regenerative farming and biomass fuel for sustainable, localised power sources.

RMB Holdings is to sell the A ordinary shares (37.5% stake) in Atterbury Europe plus the shareholder loan claims to existing shareholder Brightbridge for R1,75 billion, to be settled in cash. The aim is to return the proceeds to shareholders in the form of another special dividend.

Texton Property Fund is to sell Hermanstad Industrial Park in Pretoria to Property Genius and Cream Magenta 228 at a premium to its disclosed book value. With a focus on repurposing its office assets, the disposal further reduces the company’s exposure to industrial assets in its direct property portfolio. The proceeds of the R133,5 million deal will be used to repay debt and to further invest in its SME strategy.

Motus has issued a letter of intent for potential acquisition of 100% of the shares in an Aftermarket Parts business for cash.

Etion is to sell its subsidiary Etion Connect, a provider of carrier-grade passive connectivity equipment and solutions that enable telecommunications networks to function, connecting communities, businesses and government with mission-critical connectivity access. The business will be acquired by a newly formed entity Etion Telecommunications (representing management and third party equity partner) for R71,5 million.

Massmart has announced the acquisition of appliance brand Eiger to add to its private product portfolio. The acquisition follows Massmart’s analysis of South Africa’s appliance market.

The deal announced in February between Ascendis Health and Apex Management Services for the sale by Ascendis of the assets through which Ascendis Medical operates has been terminated by mutual agreement.

The October 2021 deal between Acension Properties (Rebosis Property Fund) and Ulricraft (Vunani Capital Partners) has been terminated. Although the conditions precedent of the R3,35 billion deal whereby Ulricraft was to acquire a portfolio of rental enterprises at a blended yield of 9.4%, was extended to allow Ulricraft to obtain finance it was unable to do so within the required period.

Unlisted Companies

ZenysisTechnologies, a data integration and advanced analytics company headquartered in Cape Town and San Francisco, has closed a US$13,3 million series-B round led by the Steele Foundation for Hope.The funds will be deployed towards building partnerships with governments and local institutions to manage complex linkages between climate change and human health in Africa, Asia and South America.

Eco (Atlantic) Oil & Gas via its subsidiary Azinam, has signed a farmout agreement for the acquisition of an additional 6.25% participating interest in Block 3B/4B offshore South Africa. The interest will be acquired from the Lunn Family Trust, a shareholder of Riocure. The block is located lies120-250kms offshore South Africa in the Orange Basin. The consideration payable is US$10 million (R158 million).

The saga with embattled Tongaat Hulett continues with Magister Investments terminating the agreement to underwrite R2 billion of its proposed R5 billion rights offer. The capital raise was to be instrumental in curbing its escalating debt. The company will now establish a restructuring committee and has announced the appointment of non-executive director Piers Marsden as chief restructuring officer to intensify focus on the turnaround of Tongaat.

Prosus has disposed on the open market, 131,873,028 JD.com shares (c.4% stake) it received as an in specie distribution, realising proceeds of c.$3,67 billion. JD.com was considered not part of the group’s core strategic focus.

Adcorp has repurchased an aggregate 1,374,187 shares during the period June 13-24, 2022 for a total value of R8,52 million, funded out of the group’s cash resources. The shares, which represent 1.28% of the issued share capital of the company will be held as treasury shares.

Tiger Brands repurchased a 5,768,836 ordinary shares for a purchase consideration of R898,7 million, representing 3.04% of the total issued shares of the company. The shares were repurchased during the period February 21 to March 31, 2022.

Naspers and Prosus have announced the start of an open-ended share repurchase programme of Naspers and Prosus shares. The programme will run as long as elevated levels of the trading discount to the Group’s underlying net asset value persists. The repurchases will be funded by a reduction in the group’s Tencent stake – an about turn on comments made by Prosus management in April 2021 which stated that it would not dispose of any further Tencent shares for three years.

CA Sales listed on the JSE on June 27, closing the day at R7.54 per share giving the fast moving consumer goods company a market capitalisation of R3,48 billion.

A2X will, on July 4 2022, welcome Discovery to its bourse. Discovery’s secondary listing will bring the total number of instruments available for trade on A2X to 69 with an aggregate market capital of R4,5 trillion.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

South32 this week repurchased 1,472,651 shares at an aggregate cost of A$6 million.

This week British American Tobacco repurchased 1,423,000 shares for a total of £49,8 million. The purchased shares will be held in treasury with the number of shares permitted to be repurchased set at 229,400,000.

Glencore this week repurchased 8,610,000 shares for a total consideration of £38,8 millionin terms of its existing buyback programme which is expected to end in August 2022.

This week three companies issuedprofit warnings. The companies were: Sable Exploration and Mining, Wilson Bayly Holmes-Ovcon and Visual International.

Four companies this week issued or withdrew cautionary notices. The companies were: Afristrat Investment, Premier Fishing and Brands, Finbond, Ascendis Health and Datatec.

BAOR, a mining company based in Burkina Faso is to acquire the Kouri and Babong gold projects in the country from ASX-listed Golden Rim for an aggregate purchase consideration of US$15,5 million in four staged cash payments over 12 months.

MTN-Halan an Egypt-based fintech, has added a digital offering to its merchant network with the acquisition of B2B e-commerce platform Talabeyah for an undisclosed sum. Talabeyah services the FMCG market, offering supplies directly to small merchants and retailers with next day delivery. The deal enhances MNT-Halan’s breath and scope.

A 30% stake in Kenyan retail chain Naivas Supermarket has been acquired by a consortium of investors led by Mauritian conglomerate IBL Group. The stake was acquire from exiting Amethis, a French fund and the International Finance Corporation.

Spear Capital, the private equity firm headquartered in Harare with a fundraising office in Oslo, Norway, has completed its investment into Associated Foods Zimbabwe. Spear Capital’s investment into the business will be a part buy-out of existing shareholders, part working capital injection and part capital expenditure as well as investment into systems and equipment to improve the manufacturer’s environmental impact.

Afrikamart, the Senegalese agritech startup, has closed a US$850,000 seed round. The platform allows for the sourcing and distribution of fresh produce. The funds, raised from BLOC Smart Africa Fund, Orange Digital Ventures, Launch Africa and Teranga Capital, will be used to scale the business in the West African country.

Kukua, the Nairobi-based edtech startup, has raised US$6 million in a series -A round. Investors included Tencent Investments, Alchimina, EchoVC, FirstMinute Capital and Auxxo Female Capital.

Moringa School, a Kenyan learning accelerator, has raised undisclosed funding from Proparco which will aid in the broadening of subject range and its expansion into Ghana and Nigeria as it prepares for series-A funding next year.

XENO, a Ugandan investment platform assisting individuals across Africa to plan, save and invest via an app, has raised US$2 million in seed funding led by Beyond Capital Ventures. Funds will be used to scale the platform.

DealMakers AFRICA is the Continent’s M&A publication

At the end of 2021, the South African Competition Commission’s (Commission) Burger King merger prohibition set into motion significant changes to competition law in South Africa. This was the first time in 20 years that a merger was prohibited on public interest grounds alone. This was also the first time that the Commission publicly interpreted section 12(3)(e) of the Competition Act (introduced by the Competition Amendment Act 2018). This new provision deals with the promotion of a greater spread of ownership and, in particular, increasing the levels of ownership by historically disadvantaged persons (HDPs) and workers.

The transaction was ultimately approved by the Competition Tribunal (Tribunal), and we hoped that the Tribunal’s reasons would provide some guidance on how the competition authorities should pursue their public interest mandate (and particularly the application of s12(3)(e)). However, since the Commission and merger parties reached agreement on all the proposed conditions before the Tribunal’s reconsideration hearing, the Tribunal’s recently published decision does not offer any further clarity. The Commission’s decision prohibiting the merger (also recently published in Government Gazette No. 46000) does, however, provide some insight into the Commission’s approach to s12(3)(e) of the Competition Act.

One of the main reasons that the Commission prohibited the transaction was the considerable negative effect of the merger on the promotion of a greater spread of ownership. Pre-merger, the target firms were ultimately controlled by an entity with a 68.56% HDP shareholding. In contrast, the merged entity would not have any HDP or worker ownership and, therefore, the Commission held the view that the proposed merger could not be justified on substantial public interest grounds.

Some key observations from the Commission’s prohibition decision are set out below:

• Following amendments to the Competition Act to this effect a few years ago, the Commission reiterated that, even when a merger transaction is not likely to raise competition concerns, competition authorities are obliged to determine whether it can or cannot be justified on substantial public interest grounds. The Commission views the competition assessment and the public interest assessment as co-equal in terms of the Competition Act. It highlighted that the assessment of public interest grounds is not dependent on the outcome of a competitive assessment.

• The Commission noted that s12A(3)(e) of the Competition Act imposes an obligation on the competition authorities to consider the effect of a merger transaction on the promotion of a greater spread of ownership. This provision falls under legislative measures contemplated in s9(2) of the Constitution, which states that: “to promote the achievement of equality, legislative and other measures designed to protect or advance persons, or categories of persons, disadvantaged by unfair discrimination may be taken”.

• While the merger parties argued that empowerment shareholders (in this case, the sellers), were entitled to a return on their investment, in the Commission’s view, a return on investment is a private gain to the empowerment shareholders. Although the Commission agrees with the view adopted in established case law such as Metropolitan / Momentum that a balanced approach needs to be taken when assessing public interest factors, it did not consider a gain to shareholders to be a countervailing public interest ground, weighed against the negative effect of the merger on the promotion of a greater spread of ownership.

In its decision, the Tribunal sets out a summary of the proceedings and arguments put forward by the Commission and merger parties but does not refute or expand on any particular issues. Importantly, though, after agreements were reached between the merger parties and Commission, the merger was ultimately approved by the Tribunal, subject to several conditions, despite the reduction in HDP ownership. This indicates that a more holistic approach may be considered by the authorities, and that some degree of flexibility may be possible. For example, if one public interest element is negatively affected, it could be outweighed by other positive public interest outcomes.

In this merger, several extensive conditions were put forward. For instance, the merger parties committed to investments in South Africa of up to R500m, several supply commitments, and the establishment of an employee share ownership programme which will entitle workers to a 5% stake in the merged entity.

Since s(3)(e) was introduced into the Competition Act, and even more so since the Burger King decision, we have observed that the Commission has approved many mergers subject to conditions aimed at promoting the ownership levels of HDPs and workers. Overall, the Commission’s approach to the application of this section has been in line with its reasoning in the Burger King prohibition. We recommend that parties involved in transactions in South Africa adopt a proactive approach and make realistic assessments of what type of commitments may be required if potential public interest issues (especially involving a reduction in HDP/B-BEE ownership levels) are anticipated.

Daryl Dingley is a Partner and Elisha Bhugwandeen a Senior Knowledge Lawyer | Webber Wentzel

This article first appeared in DealMakers, SA’s quarterly M&A publication

Adding to a significant day of property updates, Hyprop released a pre-close update. The retail-focused fund was hammered by the pandemic, with the share price still 50% off pre-pandemic levels. Let’s take a closer look.

The balance sheet has been a major focus for investors, so it’s not surprising that the announcement starts there. Hyprop has investments in Eastern Europe, so there’s a mix of rand- and euro-denominated debt in the group.

The sale of Delta City Mall in Montenegro was implemented in May 2022 and put €70 million into the bank. Hyprop promptly used this to reduce euro-denominated debt. Along with other repayments, the euro-denominated debt has reduced from €373 million in June 2021 to €110 million currently.

Rand-denominated debt has headed in the other direction, up from R5.1 billion to R6.4 billion. This was driven by the purchase of four Eastern European assets from European investment vehicle Hystead for €173 million.

There’s a short comment on how US dollar-denominated debt in Nigeria hasn’t changed, other than capitalised interest. The group notes the ongoing US dollar illiquidity in Nigeria. If you’re a shareholder in the likes of Nampak or MTN, you should take note of that.

The group loan-to-value (LTV) is around 40% which is uncomfortably high for the complexity and risks of the group. In recent periods, Hyprop disclosed a see-through LTV and a consolidated LTV, due to the Hystead structure. It now only discloses a consolidated LTV, which went as high as 51.7% in June 2020.

The announcement goes into great detail about tenant news at Canal Walk, CapeGate, Rosebank Mall and other centres. One thing I’ll highlight is that Exclusive Books seems to be hanging on, with stores upgraded to the “latest specification” – as a great lover of books, I’m happy to see that!

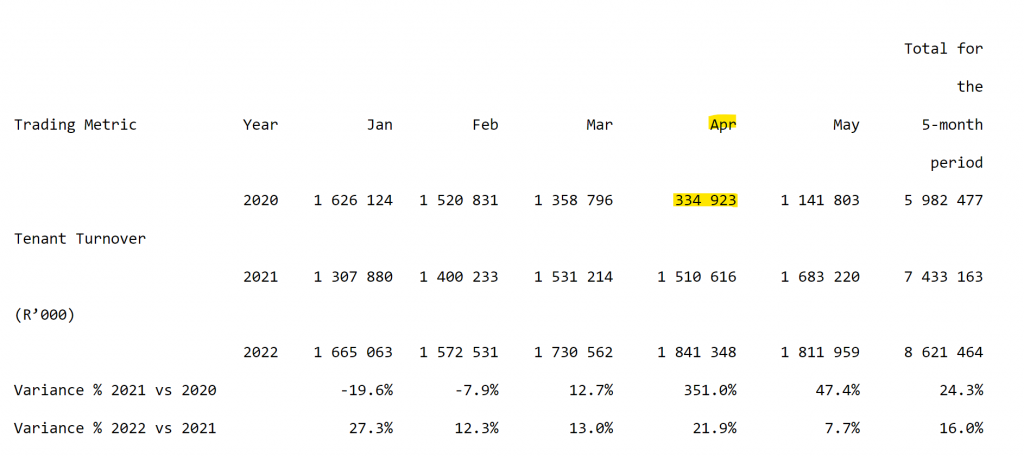

In case you’ve forgotten what happened in March and especially April 2020, here’s a spectacular reminder from the announcement:

I would also like to highlight that although trading density is running higher than February 2020 (rand sales per square metre), foot count is still lower. This is in line with most of the commentary I’ve seen from retail property funds: people are spending more per trip and doing fewer trips.

The trading at entertainment tenants has shown significant improvement. With masks out of the way, that can only improve further from here.

If you’re wondering whether things will go back to normal in retail, the trading metrics in Eastern Europe may help. Masks were burned in March 2022 and everything has improved since then: turnover, trading density and footfall. Recent performance is in line with pre-Covid levels.

That’s really bullish commentary when you consider that the mask mandate has only just been lifted in South Africa. Will we see a strong second half of the year in retail-focused property funds in South Africa?

Hyprop is trying to sell its assets in the rest of Africa, including in Ghana where it is co-invested with Attacq. Currency risks and dollar liquidity are the major issues, as the update makes it sound as though performance at the malls themselves is rather strong. South African businesses in many sectors have learned hard lessons about rushing off into Africa.

With a net asset value (NAV) per share at the end of December 2021 of R58.97 and a current share price of R35.01, the market is putting a 40% discount on Hyprop’s net assets. With masks out of the way, is it finally time to have a punt at Hyprop? The share price is down 9% this year.

Retail-focused fund Hyprop has released a pre-close update with some incredibly interesting insights into the retail property portfolio in Eastern Europe in particular. Although it is obviously a different market to South Africa, the trend in metrics since mask mandates were abolished in March 2022 is quite something to see. I dedicated a feature article to Hyprop that you can read here.

Emira Property Fund’s B-BBEE deal was concluded in May 2017 with Letsema Holdings and Tamela Holdings, each of which held a 2.5% stake in the group after the deal was implemented. 90% of the price was funded by debt (40% from a third party and 50% as a vendor loan from Emira) for a five-year period which expired on 27 June 2022. The deal has been extended to 2027, including the guarantee provided by Emira to the lender. As Letsema is an associate of an Emira director, this is a small related party transaction that requires sign-off from an independent expert. Moore Corporate Services Cape Town has opined that the terms are commercially reasonable. No shareholder approval is required. The group also released a pre-close operational update, which I wrote a feature article on here.

There’s very bad news for Rebosis shareholders, with the property fund announcing that the dream deal to sell a multi-billion rand office portfolio was, in fact, a dream. Ulricraft, a special purpose vehicle spearheaded by Vunani Capital Partners, didn’t meet the deadline to raise the funding for the R3.35 billion transaction to buy the properties on a blended yield of 9.4%. The deadline had already been extended from 22 April to 22 June. The board of Rebosis won’t give another extension, so this deal is dead. Rebosis has promised to communicate a refinancing plan to shareholders by the end of July, as the fund simply isn’t sustainable in current form. The share price of Rebosis ordinary shares (JSE: REA) fell by 35%.

Safari Investments, a REIT (property fund), released results for the year ended March 2022. Property revenue increased by 14% and the group managed to improve its cost to income ratio, which is impressive in this environment. A mythical unicorn emerged a few paragraphs down in the announcement: positive reversions of +1.15%! This means that new leases were signed at a higher rate than the expired leases, which is almost unheard of in the sector currently. The loan-to-value (LTV) is down to 37% and the net asset value (NAV) per share has increased to 855 cents. The share price at R5.70 is a 33.3% discount to NAV. The total dividend for the year of 57 cents per share puts the fund on a yield of 10% on the nose.

If you haven’t been in the markets for a while, you may be shocked to learn that the JSE is listed on the JSE! The JSE as a company is publicly listed on the exchange that it operates and derives revenue from. For the six months ending June 2022, headline earnings per share (HEPS) is between 24% and 32% higher than the comparative period, coming in at between 520.92 cents and 554.53 cents. The group attributes this to higher revenue growth in all segments, active cost management and higher net finance income. The share price was down 6.6% this year before the announcement, so it will be interesting to see how it reacts.

Sasol has announced an update to the sale of its 30% interest in The Republic of Mozambique Pipeline Investments Company, also known as ROMPCO. I am quite sure that a few laughs have been had around the coffee machine about that name. Interestingly, a deal was originally announced in May 2021 that would’ve seen the stake sold to a consortium comprising Reatile Group and a fund managed by African Infrastructure Investment Managers. The other shareholders in ROMPCO quickly romped their way to exercising a pre-emptive right to buy the stake, effectively shutting out the consortium. The deal has now closed, with an initial payment of R4.1 billion and a further R1 billion payable if certain milestones are achieved by June 2024. Sasol retains a 20% stake in ROMPCO and agreements related to the pipeline and the transport of gas to Secunda are unaffected. This is great news for the Sasol balance sheet and takes the company a step closer to rewarding shareholders with dividends once more.

Argent Industrial has released results for the year ended March 2022. Revenue increased by 23.7% and EBITDA by 32.2%. HEPS was a whopping 55.7% higher at 339.2 cents. A final dividend of 42 cents per share was declared. At a closing price of R14.21, Argent is trading on a Price/Earnings multiple of just 4.2x. This R800 million market cap industrials group is looking interesting! It owns an array of businesses including Xpanda, American Shutters, JetMaster and many others.

Irongate shareholders voted almost unanimously in favour of the deal with Charter Hall. This is a key milestone of course, with a few regulatory approvals to go before Irongate shareholders get paid out and the company delists.

Recently-listed Southern Palladium has awarded a drilling contract to Geomech Africa, with the phase 1 programme to commence in mid-July 2022. The results will be used in pre-feasibility studies, which in turn will be used for a mining right application. Phase 2 drilling will be over a wider area and will be used for more accurate life-of-mine planning. The goal of Phase 2 would be to upgrade the project to Inferred Mineral Resource status. If you have any interest in junior mining (whether financial, intellectual or both) then you’ll want to keep an eye on updates from this company.

In case you’ve ever wondered how much money Magda Wierzycka and her husband Simon Peile have made from Sygnia, here’s a clue: through a restructuring of the family’s investment interests, nearly R831 million worth of Sygnia shares have changed hands. Very importantly, this isn’t a sell-down of the stake in Sygnia – it’s only a restructure, so don’t panic! I’m just including it here to give you an idea of what serious wealth really looks like.

Sable Exploration and Mining has released a trading statement for the year ended February 2022, noting that the loss per share will be between 127 cents and 155 cents. They describe this as a “decrease in the loss” from the 76.21 cents loss reported in the prior year. This kind of maths is why you need to stay in school, kids.

Salungano Group (previously Wescoal) released a trading statement for the year ended March 2022. HEPS has swung massively into the green, from a loss of 2.87 cents to a profit of between 5.70 and 6.60 cents. There’s not much trade in the stock and it closed yesterday at R1.46, with this announcement coming out after the close.

In a trading statement covering the six months to the end of February 2022 (yes – this is long overdue), Trustco noted that net asset value per share has increased from 1.48 cents at the end of August 2021 to between 3.95 and 4.25 cents. Just four hours later (presumably after a hugely productive afternoon), the company then released results confirming this number as 4.13 Namibian dollars, so the trading statement was incorrect to refer to those numbers as being cents rather than NAD. It’s also ridiculous to see a trading statement coming out four hours before results.

York Timbers has been dealing with a strike by NUMSA employees at its Escarpment operations since 25th April. The Labour Court confirmed the strike as being unprotected on 7th June, leading to ultimatums to return to work as well as disciplinary proceedings. Investors will be more interested to know that operations have been reinstated, though not yet at full capacity.

Marcel Golding has entered into agreements to buy shares in two listed companies in which he is a director. There’s an agreement to buy R15.4 million worth of shares in Rex Trueform in February 2023 at a price of R18 per share (current price R14.90). There’s also a future purchase of nearly R10 million in shares in African and Overseas Enterprises at a price of R27 per share (current price R16.96). I’m not close to the details of what is going on here but as director dealings go, these are big ones.

The CEO of Fairvest’s family trust has bought another R1.5 million worth of shares in the property fund.

Capitalworks is a long-standing partner of RFG Holdings (known to many as Rhodes Food Group) and holds a large stake in the group. Shares worth another R195k have been added to the position. This is tiny in the world of private equity but it does indicate ongoing commitment to the business.

A private entity related to two Brimstone directors (including CEO Mustaq Brey) has bought shares in Brimstone worth nearly R53k. It’s not an amount to get excited about but it’s still a positive signal, as I guess they could’ve punted on crypto instead (or just spent it on a nice holiday).

Speaking of small director purchases, a director of Kaap Agri has bought shares worth around R90k in the company.

Yet another example is the CEO of Spear REIT, who bought another R95k worth of shares for his kids.

Andre du Plessis has retired from his position as CFO of Capitec, which opened the door for Grant Hardy to be appointed as his successor. Hardy will take over from 1 July and his bank account will no doubt thank him.

A prescribed officer of Thungela has sold shares in the company worth nearly R143k.

Emira’s financial year will close at the end of June 2022. Ahead of that, the group has updated the market on progress since the interim results that covered the six months to December 2021. Property’s recovery has had a wobbly this year, so investors are watching the sector closely.

Emira holds assets in South Africa and in the USA. There are direct and indirect holdings. To make it easier, the fund discloses the information for each segment of the portfolio separately.

The fund has extended it’s B-BBEE transaction to 2027. In this article, I focus on the pre-close update and the metrics in the property portfolio. If you want more details on that extension, you’ll find them as part of Ghost Bites here.

Before delving into the details, it’s worth noting that the loan-to-value (LTV) ratio has increased from 41.8% at December 2021 to 42% at May 2022. Dollar-denominated debt has increased to $73 million after an acquisition in the US (further details below).

Emira has refinanced R1.3 billion in maturing debt facilities this year and has unutilised facilities of R370 million along with cash of R50.6 million in the bank.

Direct local portfolio

The direct local portfolio is 74% of the fund’s investments, so the South African macroeconomic picture is important for Emira. Thankfully, vacancies reduced from 6.1% at the end of December 2021 to 5.5% by the end of May 2022. The focus is on retaining clients, with an 82% retention rate over the 11 months to May 2022.

Tenants still have the upper hand in negotiations, with weighted average reversions for the period at -12.8%. That’s better than -14.1% in the six months to December.

Weighted average lease expiry is 2.7 years and average annual escalations are 6.7%.

Emira has recycled almost R270 million in capital by disposing of four properties.

In the retail portfolio (49% of the direct portfolio), vacancies fell from 3.6% to 3.3% and 90% of maturing leases were retained. Weighted average reversions improved slightly in recent months, coming in at -14.4% for the 11 months to May. This is a portfolio of grocer-anchored neighbourhood centres, which is one of the better places to be right now. It shows how tough things still are.

This brings us neatly to the office portfolio, which is 30% of the direct portfolio. There’s a surprisingly good story to tell here, with vacancies improving from 18.2% for the six months to December to 16.6% for the 11 months to May. Only 65% of maturing leases were retained and the weighted average lease expiry is 2.7 years, so Emira will be desperately hoping that people return to work soon. Reversions were actually rather good at -11.4% vs. -16.9% in the interim period. That’s lower than the retail portfolio!

In the industrial portfolio, which is 19% of the direct local portfolio,vacancies fell from 2.6% to 1.9%. Industrial is still the best place to be in property. 81% of maturing leases were retained at a weighted average negative reversion of -12.6% (worse than -11.7% in the interim period), which is a real surprise relative to the office portfolio.

There’s only one directly held residential property in the portfolio: The Bolton. Occupancy increased from 92.2% at the end of December to 98.6% by the end of May.

Enyuka

Emira is disposing of its shares and claims in Enyuka for R638.6 million, which is 5% of Emira’s investment portfolio value. Many conditions still need to be fulfilled, including the biggest one of all: the buyer confirming finance.

Vacancies in the Enyuka portfolio are stable at 3.2%.

Transcend Residential Property Fund

Transcend is separately listed on the JSE, with a share price down around 17% this year. This is a small fund with a market cap of less than R1 billion. Emira holds 40.69% of the shares in issue and it contributes 4% of Emira’s investment portfolio value.

USA

The portfolio in the US of A is 17% of Emira’s portfolio value and comprises 12 equity investments into open air retail centres. These are grocer-anchored properties, so they feel a bit like Emira’s local retail portfolio.

Emira bought the twelfth property in this period at a cost of $18.45 million for a 49.5% equity interest.

Ten of the investments are paying dividends again and the eleventh is expected to resume dividends later this year. The final property needs to find a tenant to replace Dick’s Sporting Goods before dividends are likely.

In closing, Emira’s share price is only slightly down this year as well as over the past 12 months. It remains over 30% down from pre-pandemic levels. Although the LTV remains on the high side, Emira has demonstrated an ability to recycle capital. This may be one to keep an eye on.

With no real data out of the market last week, the main event of last week was the testimony by Fed Chair Jerome Powell to Congress. TreasuryONE expected the market to be very cautious around the testimony and with no other significant events last week, the market traded relatively flat for most of the week.

Much of the Fed Chair’s testimony has been available for some time. With little to no new information, it’s easy to see why the market didn’t react much to the testimony.

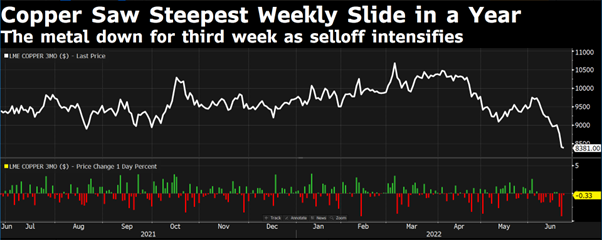

One of the highlights of the meeting was Fed Chair Powell’s statement that whilst raising interest rates aggressively will fight inflation, there is a real risk of rising unemployment rates as the economy slows. There have been forecasts for a recession and the copper price, one of the leading signs of a recession, entered a bear market last week.

The chart below shows that copper is presently trading at a 16-month low:

The IMF has reduced the US growth rate from 3.7% to 2.9% for 2022, so the US should still avoid a recession. The report also highlighted that there is a high degree of uncertainty in the outlook of the US economy. It’s very uncommon for the market to run on second- or third-level data during times of uncertainty, especially now with inflation and interest rates.

That was the case on Friday when the University of Michigan 12-month CPI number dropped slightly from 3.3% in the previous month to 3.1%. This caused some of the markets to run as the US dollar lost some ground and risky assets like the rand and stock indices had a decent Friday afternoon.

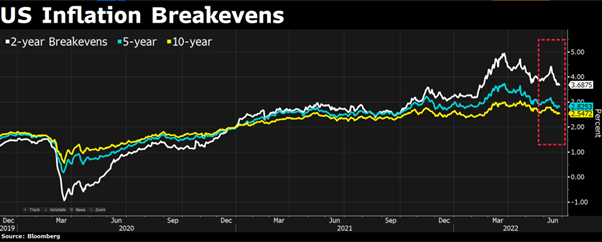

As shown in the chart below, inflation breakeven rates in the 2-year, 5-year and 10-year space have started to turn down once again:

With this in mind, the more aggressive rate hikes that the US market is pricing may also self-correct. The question is, at what interest rate will the US economy collapse?

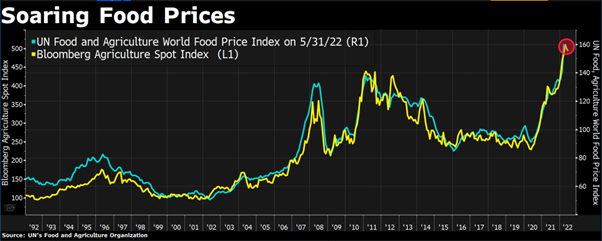

Food price inflation will be a major source of concern around the world. Food prices skyrocketed following Russia’s invasion of Ukraine, as the fear of shortages had a significant impact. This could also be a turning point for several other countries, as crop estimates from throughout the world are higher than expected. Brazil and Australia, in particular, are having bumper crop years.

This will help to reduce inflation significantly.

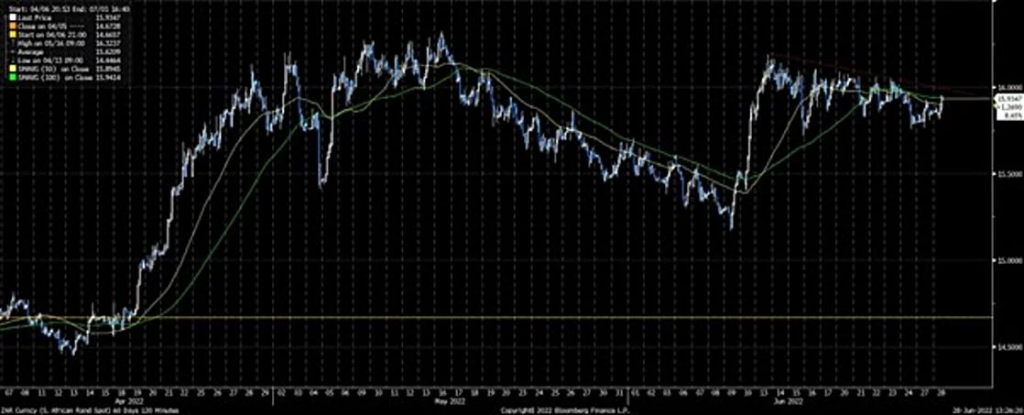

The rand closed last week at R15.80 after spending the majority of the week around the R16.00 level. The US dollar also slipped to 1.055 against the euro after threatening to break below 1.04 earlier in the month. For now, the USD/ZAR seems to be stuck within a short-term range of R15.70 to R16.10:

Looking ahead to this week, most of the risk is concentrated on Wednesday with speeches by both Fed Chair Jerome Powell and ECB Chief Christine Lagarde. Much of the focus will be on interest rates and inflation, with German CPI due on Wednesday and the EU inflation figure due on Friday.

We expect the rand to stay within tight ranges for the early part of the week, with Wednesday being the big day for emerging markets movements as any hawkish/dovish talk by both Central Banks leads to movement in the currency market.

A keen eye will also be given to the commodity space, with a commodity sell-off also a good indicator of expected recessions, which could be negative for the rand should that happen.

For assistance with managing market risk and many other services ranging from treasury solutions through to robotic process automation, visit the TreasuryONE website.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")