The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, we recap a busy couple of days:

Aveng’s poor recent results and the volatility in the share price around the time of the earnings release.

Curro’s solid year-on-year growth, driven mainly by pricing increases in tuition fees.

Libstar’s substantial drop in HEPS, with mushroom production as the biggest problem after the Shongweni facility was destroyed.

Transpaco’s encouraging trading statement, putting another tick in the box for the packaging sector this year.

Standard Bank’s massive jump in earnings, with the African regions shining through.

Various mining sector updates that are almost all negative, including Thungela, Exxaro, Sibanye, Gold Fields and Master Drilling.

Attacq posts the Waterfall deal circular (JSE: ATT)

Here’s a good example of how corporate finance works

Attacq’s proposed transaction with the Government Employees Pension Fund (GEPF) has been in the news for a while now. It did great things for the share price, much to my enjoyment as a shareholder. The GEPF is taking a 30% stake in the Waterfall portfolio and the price on the table is effectively a lower discount (15%) to the net asset value than the listed share trades at. This triggered a value unlock for shareholders.

To get the deal across the line, Attacq needs shareholder approval. This means that a circular has to be sent to shareholders. You’ll find it here.

Other than the price, another highlight of the deal is that the proceeds from the sale will help Attacq reduce its gearing ratio from 38.1% to 26.3% based on December 2022 numbers. This is achieved without losing control of the Waterfall business, as Attacq will retain a 70% shareholding in it and will manage the properties for a fee.

Assuming the transaction goes ahead, the net asset value per share based on December 2022 numbers would be R16.779. Attacq is trading at R8.40. You don’t need to get the calculator out to see why the investment by the GEPF at a 15% discount to adjusted NAV of the portfolio is a good one.

The cost of the deal to Attacq is R11.3m, with Java Capital getting R5m for the corporate finance work and ENSafrica taking home R2.1m on the legals. EY gets nearly R1.8m as the reporting accountant.

Castleview to move higher in the Collins structure (JSE: CVW | JSE: CPP)

Transactions like this aren’t unusual in the listed space

Castleview Property Fund currently holds 25.7% in Collins Property Projects, a subsidiary of Collins Property Group (previously called Tradehold). This is where the logistics and industrial portfolio with a net asset value of around R3.6bn is held.

To make life simpler for Collins and to give it 100% control of its major operating subsidiary, the 25.7% stake will be acquired by Collins Property Group in exchange for the issue of listed shares to Castleview. This is effectively just a swap to the top, giving Castleview a 21.78% stake in Collins.

The issue price is R13.64 per share, which is much higher than the traded price of R7.35 because this is more like a NAV-for-NAV deal that is designed to avoid hurting Collins shareholders. If Collins was acquiring the underlying stake at NAV and issuing shares at a discount, it would be extremely damaging for existing shareholders.

This is a Category 2 transaction for Castleview and for Collins and so no shareholder approval is needed for either listed company.

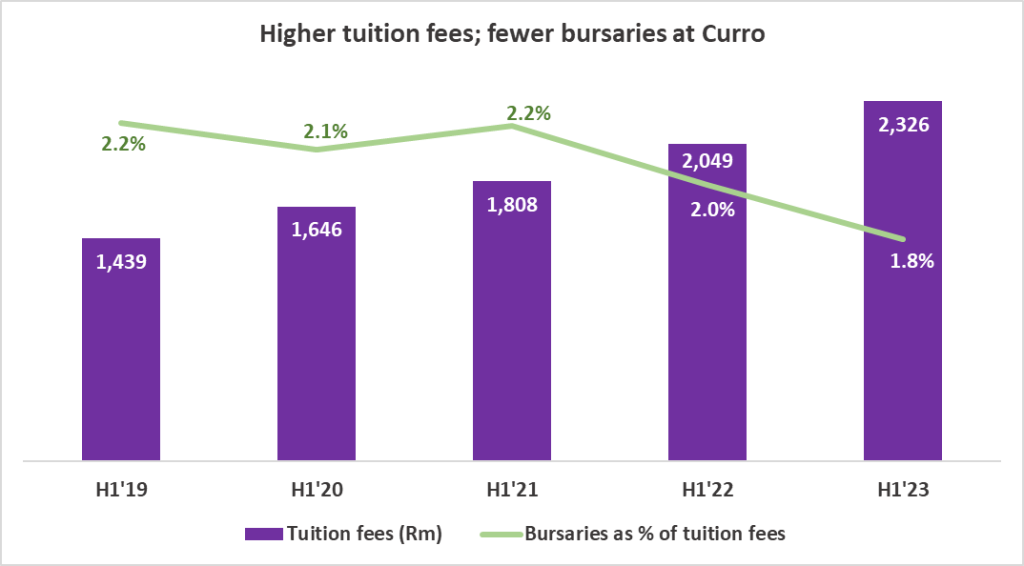

Curro’s interim report is out: insert A+ puns here (JSE: COH)

Recurring HEPS is up by 36%

After 25 years of trying to plug the gap between government schools and very expensive private schools, Curro has released a set of numbers that looks strong. Weighted average learner numbers increased by 3%, revenue was up 16% (thanks to tuition fee growth of 14%) and recurring HEPS jumped by 36%. Recurring HEPS is the right metric because the base period included subsidy income received by Meridian.

It does give a sense of inflationary pressure on middle-income households in this country that tuition fees grew by 14%, while obviously noting that learner numbers are part of that. Still, tell us again about that average inflation number? Despite this, credit loss provisions were flat year-on-year, which actually suggests an improvement in credit quality considering the jump in revenue.

Despite the big jump in earnings, cash from operating activities only increased by 2% because of tax and interest payments along with working capital requirements.

The group reports its various income sources in great detail, allowing me to create this chart of the day:

Curro is a business, so being able to reduce the percentage allocated to bursaries is actually good for shareholders. Welcome to the inevitable emotional conflict that comes with investing in private school education.

If you would like to attend the Unlock the Stock session featuring Curro that is scheduled for 31 August at midday, then register at this link. It gives you a wonderful opportunity to ask questions directly to the management team, brought to you by A2X.

Jubilee Metals pushes forward with chrome and copper (JSE: JBL)

With PGM prices under pressure, diversification is very helpful

If you’ve been following recent mining updates, you’ll know that the PGM players have been under immense pressure. Focusing on a single commodity (in this case the PGM basket gets treated as one exposure) is dangerous and leads to volatile earnings. This is what Jubilee Metals is trying to avoid.

For context to how volatile mining can be, we can look at the Jubilee share price over the past few years. After it went crazy in 2021 and traded above R4 a share, it’s all the way down at R1.60. A negative move in the mining cycle and a general shift away from riskier equities has not been kind to investors. Having said that, it’s still up over 250% with a five-year lens!

The company cannot control the share price but it can control its strategy. In an update to investors, Jubilee noted the continued expansion of the chrome operations at a time when chrome prices are supportive of this decision. The company is actively seeking additional chrome processing partnerships to increase production.

On the copper side, the roll-out in Zambia is ahead of schedule with commissioning of the Roan upgrade scheduled for October 2023. Jubilee is also busy with refining process trials to find better ways to recover copper from historical tailings materials. This is a major opportunity in Zambia and the CEO’s commentary around the trials is bullish.

Kore Potash affirms ongoing governmental support (JSE: KP2)

This might help settle the serves among investors

Kore Potash has been in the process of negotiating the required construction contracts for the Kola project for what feels like forever. Along the way, there’s been some awkwardness with the government of the Republic of Congo, which didn’t do anything to improve the growing nervousness among investors.

The company seems to be on the front foot now, announcing the receipt of a letter from the Ministry of Mines of the Republic of Congo that affirms ongoing support for the project. Of course, this is by no means a guarantee that the government won’t get jittery again if there are further delays.

Kore Potash is dealing with numerous moving parts here. The planned timeline is that the Engineering, Procurement and Construction (EPC) contract will be finalised by January 2024, with the financial proposal in place a few weeks later.

As the company is in the process of raising more funding to help it reach that date, this letter is critical.

After presumably a number of awkward boardroom discussions, RMB Holdings has released an announcement about the Atterbury loan problem and has withdrawn its cautionary announcement. Instead of trading with caution, you can now trade with confusion.

Atterbury owes R487m to RMB Holdings. R162m will be repayable by the end of December 2023, unless Atterbury can’t afford that repayment, in which case it’s repayable in June 2024. Interest is payable at JIBAR plus 2.75%.

The remainder of the loan (R325m) will be settled at the same time that the R162m is settled, by the issuance of shares in Atterbury to RMB Holdings, calculated based on June 2023 NAV. This would increase RMB Holdings’ shareholding from 27.5% to 38%.

In case the R162m is not repaid by June 2024, then the entire amount (i.e. plus the R325m) becomes payable immediately, along with interest.

Ok. Great. But if Atterbury doesn’t have R162m in 2024, then how exactly would they suddenly find the R487m? They will be in the exact same position that we find ourselves in today, having bought themselves nearly another year and given themselves the option to part-settle in equity.

Either the market is a lot smarter than I am (very possible) or people didn’t read properly (always plausible), with the share price up 7% for the day. It doesn’t sound to me like this is a win for RMB Holdings but I’m happy to be corrected.

From bad to worse at Salungano (JSE: SLG)

The signs of trouble were there when directors resigned in July

Things are now going very badly for Salungano, with the listing having been suspended by the JSE for the company’s failure to publish its financials for the year ended March. If that wasn’t bad enough, a mining contractor of Wescoal Mining (a wholly-owned subsidiary of Salungano) has taken legal steps to liquidate that subsidiary, with a notice of opposition to the application due to be heard this week.

In response, Salungano has launched a court application to place Wescoal Mining in business rescue. This includes the mining operations at the Khanyisa and Elandspruit mines.

Dear, oh dear. The share price has lost over half its value this year and shareholders are now stuck.

Thungela: a perfect example of mining cycles (JSE: TGA)

The interim dividend has dropped by 83% year-on-year

Coal prices have not been a happy story this year, leading to a sharp drop in year-on-year profitability at Thungela. HEPS has plummeted from R67.23 to R22.46 and the interim dividend per share is down at R10 from R60 last year. This means that the payout ratio has also come down significantly when expressed in terms of HEPS. Thungela has declared 33% of adjusted operating free cash flow as a dividend.

Despite this, adjusted EBITDA margin is still at 31% which is hardly a low level. It just looks ugly compared to 64% last year.

The group gives an optimistic view that the current pressure on the coal price won’t last, with ongoing demand for coal and underinvestment in most of the world in coal supply (except for China, India and Indonesia). None of this really helps if we can’t get the coal to our ports, with Transnet Freight Rail again covering itself in glory with a 13% deterioration in the coal run rate year-on-year. Things at least got better towards the end of the period after a terrible first quarter with derailments.

The acquisition of the Ensham business in Australia for R4.1bn is expected to close at the end of ths month. To put that number in perspective, Thungela has R13.6bn in net cash and is about to pay a dividend of R1.4bn.

The market reacted positively to the update, with Thungela closing 4.8% higher.

Little Bites:

Director dealings:

Value Capital Partners has board representation on Altron (JSE: AEL) and has bought another R14.9m worth of shares in the company.

A director of AngloGold (JSE: ANG) has bought $121k worth of shares in the company (in the form of American Depository Receipts).

The selling of shares by directors and associates of Argent Industrial (JSE: ART) continues, this time to the value of R350k.

Emira wants to buy the rest of Transcend (JSE: EMI | JSE: TPF)

And they aren’t prepared to pay a premium for it

With a bid-offer spread as wide as the moon and practically zero liquidity, shareholders in Transcend only have one realistic way to exit their positions: sell to Emira. This is because Emira holds 68.15% of the shares in issue, so it can easily block an offer from anyone else.

This leaves major shareholders in Transcend stuck in an illiquid rut and unable to realise the value of their stake. It’s therefore not surprising that holders of 18.61% in the company have already given irrevocable undertakings to accept Emira’s offer of R6.30 per share, even though this implies no premium to the current traded price. This represents 58.41% of the voting class (as Emira can’t vote), so this proposed scheme of arrangement is already a long way down the road towards 75% approval.

With Transcend’s net asset value (NAV) per share as at March 2023 of R8.23, the offer price is a 23% discount to NAV. This is unfortunately what happens when there is only one obvious buyer for the stake and no liquidity to offer people an alternative way to exit. When buying stocks in a takeout basket and hoping for a premium, this is important to take into account.

As a final comment on this price, this discount to NAV isn’t terribly different to other takeout prices we’ve seen on the JSE. Where there has been a premium offered to shareholders, it’s because the traded discount to NAV was much higher.

Libstar suffers a substantial drop in earnings (JSE: LBR)

Here’s another casualty of this operating environment

With a drop in the share price this year of over 30%, the market has been pricing in terrible numbers at Libstar. With the release of a trading statement for the six months to June, we now know just how tough it has been. The numbers seem to be in line with what the market expected, as the share price hardly moved in response.

Revenue growth was just 4% and selling price inflation and mix contributed 10.7% to growth. This immediately tells you that volumes were down, in this case by 6.7%.

Part of the drop in volumes is because Libstar discontinued certain unprofitable lines in the retail business, so that’s technically a good thing. The destruction of the Shongweni mushroom production facility in the second half of 2022 certainly wasn’t a good thing, obviously leading to a sharp drop in fresh mushroom production. Excluding the impact of these issues, retail volumes would’ve been up by 1%.

The industrial and export channels didn’t do well for various reasons.

With lower volumes in a manufacturing company, you would expect to see a drop in gross profit margin. This has played out here, with gross profit down by 5.6% despite revenues up 4%. Gross margin was consistent with the second half of 2022 at least.

The same can’t be said for diesel costs. The company spent R8m in H1’22, R31m in H2’22 and a whopping R45m in this period. Pricing increases could only partly mitigate this impact.

Against this backdrop, normalised EBITDA (a good proxy for operating profit) fell by between 17.3% and 19.3%. This is before we consider net finance costs, which jumped by 71% because of higher interest rates.

HEPS has dropped by between 54.9% and 59.8%, so this is a period that Libstar will want to forget. Normalised HEPS from continuing operations fell by between 42.4% and 47.5%.

Detailed results are due on 12 September. The company has noted that initiatives around the strategic direction will be shared at the same time.

Sibanye’s HEPS has approximately halved (JSE: SSW)

All the PGM players are in the same boat, as one would expect

Sibanye-Stillwater is shielded to a small extent from the decline in PGM prices by its gold exposure. It’s nowhere near enough to stop the pain though, with HEPS for the six months to June down by between 48% and 53%. With a 22% drop in the average rand basket price for PGMs, they never stood a chance, even with the base period including the horrors of the industrial action in the gold business.

On top of the negative move in the cycle, Sibanye has had to content with other issues like a shaft incident at Stillwater.

Sibanye cannot control market prices for commodities but can control production. Local PGM production was flat (a solid outcome), Stillwater’s PGM production was down 11% because of the operational issues and local gold increased by 233% because the base period was a catastrophe.

The share price is down 34% this year, though it remains a ridiculous 285% higher over five years. Mining cycles are wild things.

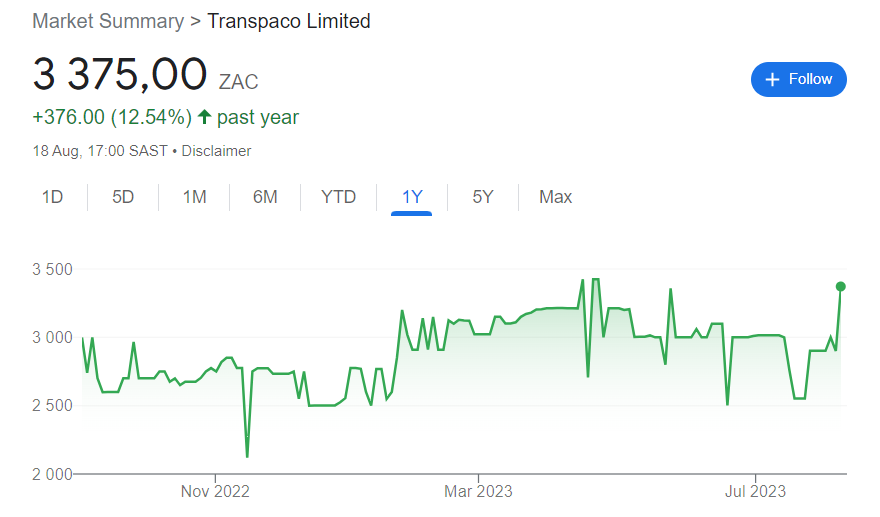

Transpaco: low on stock liquidity, high on earnings growth (JSE: TPC)

This small cap is heading in the right direction

With a market cap of under R900 million and a wide bid-offer spread, Transpaco has a share price chart that is typical of a stock with low liquidity. Whenever you see long horizontal lines, it’s because the stock is thinly traded:

This doesn’t mean that the company isn’t growing. In a trading statement for the year ended June 2023, Transpaco announced that HEPS will increase by between 16% and 22%. This means a range of 554 cents to 582 cents.

The share price is around R29, so that’s a Price/Earnings multiple of roughly 5x.

Little Bites:

Director dealings:

With results now released and Standard Bank (JSE: SBK) no longer in a closed period, a couple of prescribed officers and an associate of a director collectively sold shares worth around R12.8m.

The same is true atInvestec (JSE: INP), where a director and a prescribed officer collectively sold R2.8m worth of shares.

Des de Beer has bought another R6m worth of shares in Lighthouse (JSE: LTE).

A director of Santova (JSE: SNV) sold shares worth R426k.

AngloGold (JSE: ANG) shareholders have said yes to the proposed reorganisation of the company, which effectively internationalises the holding structure of the group.

In this fireside chat, Wichard Cilliers and Andre Botha of TreasuryONE made themselves available to answer any questions that attendees wanted to ask in the session.

Starting with China and ending with the Big Mac Index, we discussed everything from the rand and the South African trade deficit through to the Fed and consumer confidence.

This is a wonderful learning opportunity, brought to you by TreasuryONE

Along with the release of its interim results, MTN announced it had signed a memorandum of understanding with Mastercard. Following a bespoke process to identify and potentially introduce strategic minority investors into the US$5,2 billion (enterprise value) MTN Group Fintech business, the company will, following the completion of the due diligence exercise, close a deal with Mastercard.

RMB Corvest (FirstRand) in partnership with Umoya Capital Partners, has acquired a significant minority stake in SANTS Private Higher Education Institution. Programmes offered by SANTS focus on quality at an appropriate cost, with an emphasis on ease of access and customer service for potential educators. Since its establishment in 1997, SANTS has presented various programmes and qualifications to more than 40,000 educators in South Africa.

The R8 billion BEE deal announced by Sanlam in October 2018 with SU BEE Investment SPV for a 5% stake (111,349,000 new shares) in the company is being unwound. The shares were issued at the time at R70 per share representing a 9.88% discount – the share has traded for the most part below this level thanks to the pandemic and economic fragility of the country. The deal funded via a combination of preference shares and external funding is unlikely to provide the beneficiaries with any benefit and as such Sanlam has taken the decision to unwind the deal. The company will acquire the preference shares held by Standard Bank (the external funder) and secured by 85 million Sanlam shares for R2,4 billion, funded from existing cash resources.

Unlisted Companies

Sylvania Platinum, a low-cost PGMs producer listed on the London Stock Exchange’s Alternative Investment Market, has announced a joint venture (JV) in SA between its local unit and Limberg Mining, a subsidiary of ChromTech Mining. The JV will process PGM and chrome ores from historical tailings dumps and current arisings from the Limberg Chrome mine in the Western Limb of the Bushveld Complex. The JV will trade and operate under the name Thaba Joint Venture. Sylvania will initially fund the R600 million start-up costs and will provide c.US$5 million in the form of a loan for working capital.

Vitruvian Medical Diagnostics, a medical technology startup developing low-cost diagnostic assistance tools for medical laboratories, has raised US$1,25 million in a recent Seed Extension II funding round. The round was led by 27four Investment Managers’ social impact fund, the Nebula Fund. The investment will be used to scale growth by increasing the team and driving growth in new technologies.

Air Products South Africa, via its subsidiary Weldamax, has added to its gas and welding portfolio with the acquisition of a controlling interest in EWN&S. The acquisition will add a further four sales outlets to the existing 13 countrywide outlets. Financial details were undisclosed.

These earnings got hammered with a vengeance (JSE: AEG)

Aveng’s updated trading statement shows how bad things are

The Aveng share price has been weird for the past week. It started moving higher out of nowhere, then gave up all those gains after the updated trading statement was released. If punters were speculating on the release of favourable information from the company, they got it wrong.

With operating losses at both McConnell Dowell in Australia and Moolmans locally, this period is a useful reminder of how risky construction really is. For the year ended June, the headline loss per share is between 761 cents and 749 cents. The share price is only R8.16, so another year like this and there really wouldn’t be much left to this group. As you would expect, the share price has halved over the past year as these losses were priced in.

Detailed results will be out on 22 August.

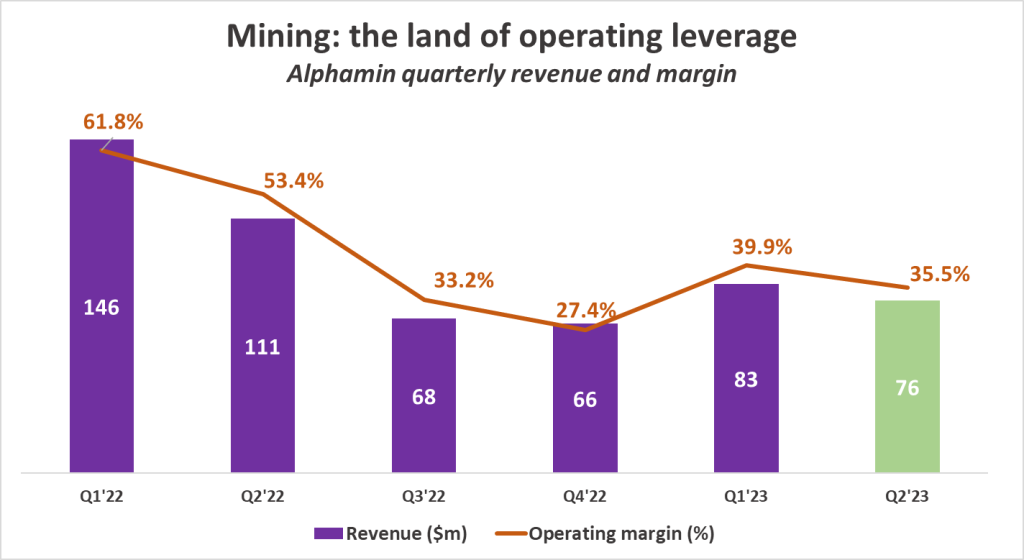

Alphamin released its quarterly financials (JSE: APH)

This is a great candidate for my chart of the day

Mining is a great way to learn about operating leverage, or the impact of fixed costs on margins. Simply, when times are good, they are really good when you have a lot of fixed costs. When they are bad, well, you know the rest.

Here’s a chart of what that looks like, thanks to tin miner Alphamin releasing its quarterly financials:

DRDGOLD’s revenue grows slightly ahead of costs (JSE: DRD)

This means that HEPS is moving in the right direction

For the year ended June, DRDGOLD managed to grow its revenue by 7%.

Although gold sales at Ergo Mining fell by 5% despite a 21% increase in yield (with throughput as the problem), this was more than offset by a 16% increase in the rand gold price. At Far West Gold Recoveries, that gold price increase was the saving grace as yield fell by 8% and sales fell by 15%.

Cash operating costs increased by 6%, below revenue growth and thus giving margins a move in the right direction. Ergo was the winner here once more, with costs up by 6% vs. Far West Gold Recoveries where they increased by 11%. Although Ergo is far larger than Far West and that’s why the average has come out where it did, there’s obviously some rounding off here in the commentary as well.

Free cash flow in this period was R468.9 million, way down from R871.6 million in the comparable period. The difference lies in much higher investing activities in this period. Importantly, there’s still no debt on the balance sheet.

Exxaro gives us full details on its earnings (JSE: EXX)

When the cycle turns, it can turn quickly

You know the drill by now: commodity prices down, inflationary pressure on costs and infrastructure in South Africa that has more blind spots than Ferrari’s F1 pit strategies. Like so many other mining houses on the local market, Exxaro is having to deal with all these issues.

Exxaro generates 96% of revenue and 90% of EBITDA from its coal business. With coal revenue down 16.4% year-on-year, this was never going to be a pretty result. Very few people realise that Exxaro also has renewable energy investments in the form of wind assets, which recorded a very good six months thanks to a windier period. It’s just too small in the group context to really make a difference.

Where we desperately need the winds of change to blow is at Transnet. You know it’s bad when the results make a comment that Transnet’s performance “did not deteriorate further” – so just being bad, rather than worse, is an achievement.

HEPS fell by 29% for the six months to June and the interim dividend is 1,143 cents per share, down 28%.

Gold Fields: not too bad, actually (JSE: GFI)

In this environment, a small drop in mining is a big win

To give context to the Gold Fields numbers, I am mentioning right upfront that the company has operations in several countries. This gives it some protection from the joy of load shedding (and load curtailment for that matter).

For the six months to June 2023, HEPS came in at $0.51 (because the company is listed in the US and reports in dollars). This is a 12% drop vs. the comparable period. Despite this, the rand dividend has increased by 8% year-on-year to R3.25 per share, which tells you everything you need to know about the exchange rate over the past year.

In terms of other important metrics, gold production fell by 4% and the all-in cost per ounce increased by 3%. The balancing figure that saved the result from a sharper drop is of course the gold price, which was $1,927 in this period vs. $1,851 in the comparable period.

Due to acquisitions and dividends, net debt increased during the period and the net debt : EBITDA ratio is now at 0.42x vs. 0.33x a year ago.

The full year guidance has been maintained for both production and costs. Of course, nobody knows what the gold price will do.

CFO Paul Schmidt has indicated a desire for early retirement (I think the gold price will do that to anyone to be honest), so the company will look for a successor.

Master Drilling is still growing, but for how long? (JSE: MDI)

I suspect there’s a lag effect of the commodity cycle on Master Drilling’s earnings

Master Drilling has released a trading statement because the expected growth in HEPS for the six months to June is between 20% and 30% higher in rands. The company also gives a dollar range for HEPS growth, which is only between 0.7% and 10.7% because of rand weakness.

This is obviously a very strong growth rate, with interim HEPS expected to be between 162.70 and 176.30 cents. The share price is just over R12, so the annualised multiple is around 3.5x. When multiples are low in mining and related companies, warning bells should be going off for you.

Is it correct to annualise the interim earnings? I’m not familiar enough with Master Drilling’s business model to know for sure (and I would welcome any insights here), but logically a drop in commodity prices can’t be good news here. When prices are high, mining exploration is easier to justify. When prices drop, mining houses get tighter on capital expenditure and drilling would suffer.

The share price shows you how cyclical this stock is:

Oceana releases a trading statement (JSE: OCE)

Make sure you have read it carefully

A trading statement is usually big news, but not always. It is triggered by earnings moving by more than 20% vs. the comparable period, whether up or down. That’s a big move, which is exactly why the JSE Listings Requirements make companies give an early warning of a move this size.

Oceana’s trading statement is based on a move in earnings per share (EPS), not headline earnings per share (HEPS). This is a very good time to learn one of the big differences between the two concepts: profits and losses on disposals of assets. HEPS excludes these distortions.

Oceana sold Commercial Cold Storage Group with effect from April 2023, banking a juicy profit of R370 million after tax. This works out to 304 cents per share, which is huge vs. earnings for the year ended September 2022 of 603 cents. It’s therefore not rocket science to figure out that the move will be more than 20% in earnings.

At this stage, no guidance has been given for HEPS. Although this doesn’t necessarily mean that HEPS won’t have a significant move, it does mean that you shouldn’t be interpreting this trading statement as meaning a big jump in the core business.

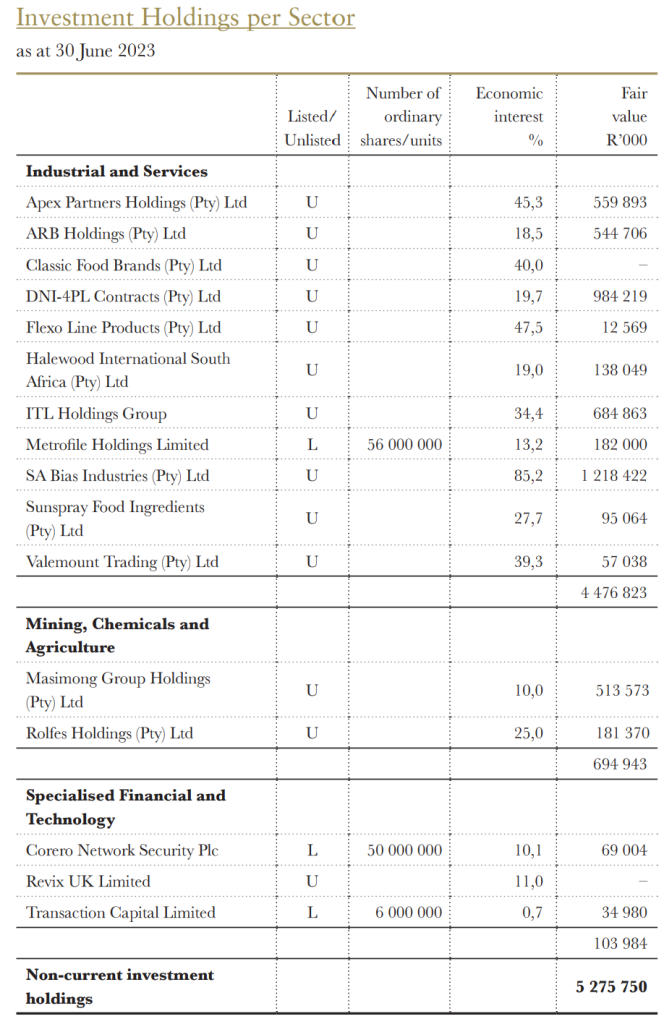

Sabvest’s interim results are always worth a read (JSE: SBP)

This is one of the most respected investment holding companies on our market

Unlike some of the other investment companies on the JSE that hold mostly a basket of listed assets, Sabvest gives exposure to assets that you can’t otherwise get. There are thirteen unlisted and three listed investments. The Seabrooke Family Trust has voting control of Sabvest through a special share class and holds a 40.5% economic interest. This has been a lucrative investment vehicle, boasting a 15-year share price CAGR of 17% (excluding dividends).

The net asset value (NAV) per share is up by 10.4% over the past year, which is a decent outcome that has been driven by resilient performance in most of the unlisted investments. The dividend per share is consistent at 30 cents, which is a tiny yield (even when annualised) on a share price of R70. You aren’t buying this thing for the dividend.

The discount to NAV is substantial, with a share price of R70 vs. a NAV per share of R114.65. That’s a discount of 39%, which isn’t materially different to other major funds like Remgro.

If you’ve been following the sad and sorry tale of Transaction Capital, you’ll be wondering what the impact is on Sabvest. Obviously now a much smaller percentage of the portfolio than it once was, the value of the stake is R35m and the total portfolio is worth nearly R5.3bn. If you’re bullish on Transaction Capital, it’s probably too small within Sabvest for this to be the right way to play that view.

If you would like to see the full portfolio, here it is:

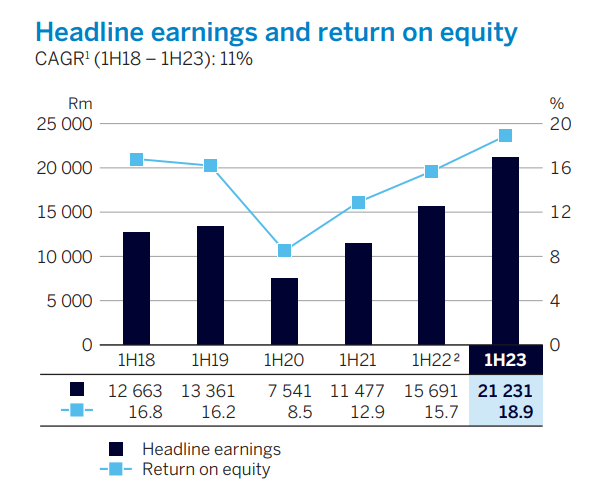

Standard Bank grows its earnings and dividend by 35% (JSE: SBK)

Return on equity has also jumped sharply

Standard Bank is a large beast. There’s far more to the group than just South Africa, with the African regions contributing 44% to headline earnings. Africa grew headline earnings by 65% and achieved return on equity of 28.4%, blowing away the South African result of 17% growth and return on equity of 15.2%. By the way, that South African result is still more than decent!

Income has experienced wonderful growth in a period of higher interest rates and larger balance sheets under inflationary conditions, up 29%. The expense base certainly doesn’t grow by this much, which is why the cost-to-income ratio has improved from 55.5% to 50.5%. That’s not the best in the sector, but it’s not bad. Remember, lower is better on that ratio.

The story of banking this year has been one of impairment provisions, which are measured by the credit loss ratio. This has increased to 97 basis points, which is right at the top of the through-the-cycle range of 70 to 100 basis points. Despite this, the banking business achieved return on equity of 19.0%, much higher than 15.3% in the interim period last year and a genuinely high number.

Net asset value per share is an important driver of the share price, so you always want to see this moving in the right direction. On this metric, Standard Bank achieved growth of 10%.

In good news for those who are barely keeping their heads above water every month, Standard Bank has echoed Nedbank’s view that local interest rates will be flat for the rest of the year.

Speaking of the outlook for the second half of the year, Standard Bank expects ongoing strong revenue growth and positive jaws (income growth ahead of expense growth i.e. further improvement in operating margins). The credit loss ratio is expected to remain in the upper half of the target range, so that suggests it won’t get any worse from the current level.

Shareholders will enjoy an interim dividend of 690 cents per share, a payout ratio of 54%.

Standard Bank must be reading Ghost Mail, because they’ve already done the work for me on a potential chart of the day going back to 1H18! With so many accounting restatements and changes in rules, I won’t try replicate this or add in the second half for each year. This tells a good enough story:

Little Bites:

Director dealings:

We are firmly back into a Des de Beer buying cycle at Lighthouse Properties (JSE: LTE), with the latest acquisition being R6.1m worth of shares.

Senior executives of Karooooo (JSE: KRO) acquired shares worth R1.6m. I was surprised to see that this is a “voluntary disclosure” of this trade. The company’s primary listing is on the Nasdaq and so those rules take precedence, but I didn’t realise that the JSE doesn’t force this disclosure on secondary listed companies.

A director at Acsion (JSE: ACS) bought shares worth R13.3k.

A director of Afine Investments (JSE: ANI) fished some coins out from between the couch cushions and bought shares worth R4.6k.

With the future of the company now secured, the CEO of Royal Bafokeng Platinum (JSE: RBP) will now retire as his fixed term contract expires at the end of August. The current manager of the Styldrift mine will now take over the top job at what will be a subsidiary of Impala Platinum (JSE: IMP). In a cute story, he was a bursary student at Impala Platinum many years ago and was with the company for 13 years! Talk about coming full circle.

Advanced Health intends declaring a Clean-Out dividend to shareholders of 20 cents per share. The payout is conditional on the Scheme (the offer to acquire the issued shares of the company by Eenhede Konsultante Eiendoms Beperk at 80 cents per share) being declared wholly unconditional.

Resilient REIT has disposed of 162,431,649 shares in Hammerson plc for an aggregate consideration of R982,2 million. Although Hammerson’s results were well received by the market, the Resilient Board says its priority remains focused on Resilient’s energy initiatives and funding its capital commitments while retaining conservative leverage.

Finbond will ask shareholders to vote on the repurchase from related parties of 38.55% of the total issued Finbond shares. The company will repurchase 220,523,358 shares from Net1Finance and 120 million shares from Massachusetts Institute of Technology at a price of 29.11 cents per share. The shares, if repurchased, will be delisted.

Glencore intends to complete its programme to repurchase the company’s ordinary shares on the open market for an aggregate value of $1,2 billion by February 2024. This week the company repurchased a further 10,010,000 shares for a total consideration of £43,6 million.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 7 – 11 August 2023, a further 2,185,222 Prosus shares were repurchased for an aggregate €145,97 million and a further 272,116 Naspers shares for a total consideration of R930,3 million.

Six companies issued profit warnings this week: Exxaro Resources, Italtile, Northam Platinum, Impala Platinum (update), KAP and Aveng.

Four companies issued or withdrew a cautionary notice: Finbond, Ayo Technology Solutions, Conduit Capital and Trustco.

Africa Finance Corporation has announced a US$95,25 million investment in oil and gas downstream company Mahathi Infra Uganda. The funding will finance, amongst other things, the construction of two self-propelled barges for operation on Lake Victoria. The new barges are expected to have a significant impact with a single barge trip replacing 200 truck journeys on East Africa’s busiest transport route between Kisumu in Kenya to Kampala in Uganda.

Starcore International Mines has acquired EU Gold Mining in a share swap transaction. The deal will give Starcore a stake in the Kimoukro Gold Project in Côte d’Ivoire through a Mineral Property Option Agreement that EU Gold has with K Mining SARL.

Carlyle has announced the sale of Assala Energy in Gabon to Etablissements Maurel & Prom SA, the oil and gas exploration and production company listed on Euronext. Financial terms were not disclosed. Carlyle first invested in Assala back in 2017.

d.light has secured an additional US$125 million in funding through a securitisation facility to scale up its services in Tanzania. The Eastern and Southern African Trade and Development Bank has provided a US$30 million securitisation facility with the capability for d.light to purchase up to $125 million of receivable assets.

Ghanaian agritech company, Oyster Agribusiness, has secured US$310,000 in funding. Root Capital has provided $300,000 in debt and the firm has received grants totalling $10,000 to expand its existing operations.

Ed Partners Africa, the Kenyan non-banking financial institute that provides loans to educational institutions, has raised US$1,5 million in debt funding from Oikocredit.

Firering Strategic Minerals has signed an option deed to acquire up to 28.33% in Limeco Resources – owner of the limestone project 22km west of Lusaka in Zambia. The option is exercisable in two tranches at a total cost of US$5,1 million.

The macro landscape in South Africa is challenged by muted growth, constrained energy availability, rising interest rates and disrupted rail logistics, just to name a few.

While all local companies are affected in one way or another, the industrial sector is particularly exposed, as evidenced by the fact that the JSE FTSE All Share Index has, in aggregate, increased around 33% over the last five years, while a market-weighted average of 44 JSE-listed industrial stocks decreased by approximately 10% over the same period.

This backdrop has translated into significantly lower M&A activity in South Africa. According to DealMakers, there have only been 32 M&A transactions concluded in the first quarter of 2023, compared to 82 transactions in Q1 2022. At this rate, it is almost certain that 2023 will fall short of the 731 deals concluded in 2022, although the RMB Corporate Finance house view is that deal activity is likely to pick up later in this calendar year.

Industrial counters are bearing the brunt of the current economic climate and, looking at valuation levels in the sector, it suggests a buyers’ market. We believe that there are good acquisition opportunities in the sector for those who are willing (and brave enough) to search for them through a ‘value-orientated lens’. Looking at a basket of 44 industrial stocks listed on the JSE, the average PE multiple over the last year is approximately 9x compared to the 10-year average (excluding COVID-19) of approximately 13.5x.

We looked at the work of well-known global value investors to identify some of the key principles that they use in their investment approaches and how they could be applicable in a South African acquisition context.

Understand the importance of market cycles “The pendulum of investment psychology is constantly fluctuating between optimism and pessimism, between greed and fear, between credulousness and skepticism, between risk tolerance and risk aversion.” – Howard Marks, co-founder and co-chairman of Oaktree Capital Management.

Just about everything in the financial world is cyclical – from market liquidity to interest rates to the financial performance in the SA industrial sector. The most basic reason for this is human nature. Undoubtedly, there are also objective drivers that play a part in cycles, such as the COVID-19 pandemic (which, in financial market terms, led to a massive dip and almost as big a jump in very short order), but it is the application of psychology to these drivers that determines the amplitude of cyclical fluctuations.

It feels as though we are in a period where the weak SA economy, together with several objectively negative events, is leading to an abundance of (often exacerbated) bearish news flow. This is driving risk aversion, which in turn creates behaviour from investors and capital allocators that is driving valuations down. Eventually, a point will come where these valuations become attractive enough for the underlying prospects being valued that the contrarians will start knocking at the door and, in time, other capital allocators will follow suit. This behaviour is the catalyst that ultimately leads to an upturn in the cycle, and value-focused capital allocators worth their stripes can identify a cycle and leverage off it.

Behave in a counter-cyclical and contrarian manner “To buy when others are despondently selling, and to sell when others are euphorically buying takes the greatest courage, but provides the greatest profit.” – Sir John Templeton, founder of the Templeton Growth Fund.

Many investors tend to be trend followers, which is what creates market cycles. Highly successful capital allocators are the opposite. As the cycle corrects itself, a big part of effective capital allocation lies in buying companies when everyone is against them and their prospects, and selling companies when everyone loves them. Of course, this is a difficult and scary thing to do, but it can be very rewarding when done right.

We had a conversation with the CEO of a well-known manufacturing company, who told us how one of their main global competitors went from half its size to almost double its size in less than seven years, and how a substantial part of the growth resulted from two large acquisitions when the market was close to its lowest level.

If you consider the recent acquisitions in the South African cement industry (Afrimat acquiring Lafarge South Africa and Huaxin Cement acquiring Natal Portland Cement), one could argue that these were contrarian moves, where the rest of the market was seeing limited growth in the short term.

Buy at an acceptable margin of safety “Confronted with the challenge to distil the secret of sound investment into three words, we venture the motto – ‘Margin of safety.’” – Benjamin Graham, renowned value investor, lecturer, financial securities researcher, and mentor to Warren Buffet.

Margin of safety is effectively value investing’s credo – buying something for less than it’s worth. One can achieve a margin of safety when a company or stock is bought at a price sufficiently below its intrinsic value, allowing for human error, bad luck, or extreme volatility in a complex, unpredictable and rapidly changing world. This largely describes the South African industrial sector at present, characterised by potentially undervalued businesses, presenting an opportunity to buy at an acceptable margin of safety.

Looking at Afrimat’s acquisition of Lafarge South Africa at an enterprise value of approximately R800m, Chronux Research calculates that Afrimat is effectively acquiring Lafarge South Africa’s materials businesses at a 3x EV/EBITDA multiple and getting the cement business for free. Afrimat is known for acquiring good assets that need a little bit of work at a low price, having done something similar with Diro Iron Ore (now Demaneng Resources) a couple of years ago, and it shows with its market cap having increased around approximately 215% since July 2016 to R9,1bn.

Search for quality and avoid too much leverage “Using leverage is like playing Russian roulette – it means that you are inevitably going to get a bullet in the head.” – Ray Dalio, founder of Bridgewater Associates.

An important part of being able to take advantage of contrarian opportunities, even if acquired at a low multiple, is to ensure that the company has the runway to withstand stress. Even though one may be acquiring a business, believing in the long-term industry and company prospects, change often takes a long time. One needs to ensure that the business can keep the lights on, especially if things get worse. From an acquisition perspective, this entails two key points: i) buying high-quality businesses that are in strong fundamental positions and ii) not over-leveraging them.

Reunert is a very good example of this. The company’s market capitalisation has been mostly stable over the last five years, but came under pressure in mid-2022, dropping to R5,8bn. Notwith-standing this, Reunert continued to operate its solid portfolio of assets efficiently, and continued making strategic acquisitions in line with its long-term strategy. Most recently, it has acquired defence component manufacturer, Etion Create, and technology-focused consulting agency, IQbusiness, without materially leveraging its balance sheet. Its market capitalisation has since strengthened to R9,3bn.

Think long-term expected value “The single greatest edge an investor can have is a long-term orientation.” – Seth Klarman, founder and CEO of the Baupost Group.

Often, when allocating capital, companies are too focused on the next year’s earnings. Acquisitions should be made that will maximise expected value, even if that means the lowering of near-term earnings. We frequently see too much emphasis being placed on the near-term EPS accretion or dilution when companies are considering acquisitions. This then deters companies from taking a long-term perspective and making contrarian plays when times are challenging.

These principles may seem simple, but it is often said that (value) investing is simple, not easy – implying that human nature often intervenes to the detriment of investing (or in the case of M&A, acquisition) success.

When it comes to industrial companies, while we have a firm belief in the longer-term prospects of the sector, we expect deal flow in the short term to remain muted, given concerns around ‘forecast error’ because of all the macro challenges. The implementation of transactions is also taking longer to conclude; in many instances, due to longer and more difficult negotiations on risk and reward, including valuations and warranties, allied with longer regulatory approval processes.

As a result, we think that there will be fewer, but better, long-term acquisitions made, as buyers seek to identify opportunities that tick boxes along the lines of the five principles covered above. Deal flow is likely to be driven by:

• Consolidation and bolt-on acquisitions: we continue to see consolidation as bigger companies with stronger balance sheets look to integrate the value chain to manage costs and enhance margins and cash flows;

• Delisting transactions: there have been many delistings off the JSE in the past couple of years, and it has been particularly busy in the industrial sector (Imperial, Value Logistics, Onelogix, Afrox and Rolfes Holdings, to name a few). We see this trend continuing, given the ‘value trap’ that we’re seeing in the small and mid-cap industrials sector; and

• International M&A: large multinational industrial companies looking to strategically expand into the African continent often see South Africa as the launch pad for such a regional expansion, and we see a surprising amount of inbound interest as a result. The logistics sector is currently particularly active in this regard, with Taylor Maritime Investments’ acquisition of Grindrod Shipping and AP Moller Capital’s acquisition of Vector Logistics as prime examples. There are also South African operators looking to expand into broader Africa and offshore to diversify regional exposure and look at growth opportunities, like Omnia, which recently established a joint venture between its mining focused subsidiary, BME, and PT Multi Nitrotama Kimia, an Indonesian explosives and blasting services provider. In our view, these cross-border deals are expected to continue.

Alex Volschenk is a Lead Banker in the Automotive, Logistics and Industrials Sector and Cara Pardini a Corporate Finance Transactor | RMB.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, we recap a busy couple of days:

It’s hard to find companies doing well in this environment, but Grindrod is one of them – if only the share price would notice!

As expected, there’s a further trading statement from Impala Platinum about just how bad things are.

Merafe is doing very well, bucking the trend in the mining industry and continuing to trade at a dirt cheap multiple.

In property, the trajectory locally and in Western Europe (represented by Resilient) is completely different to Central and Eastern Europe (NEPI Rockcastle)

Base effects are important, as evidenced by looking at Santam and Sun International’s latest numbers and comparing their through-the-cycle returns.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")