The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this week’s episode of Ghost Wrap, we catch up on the public holiday week and the start of the new week across various sectors:

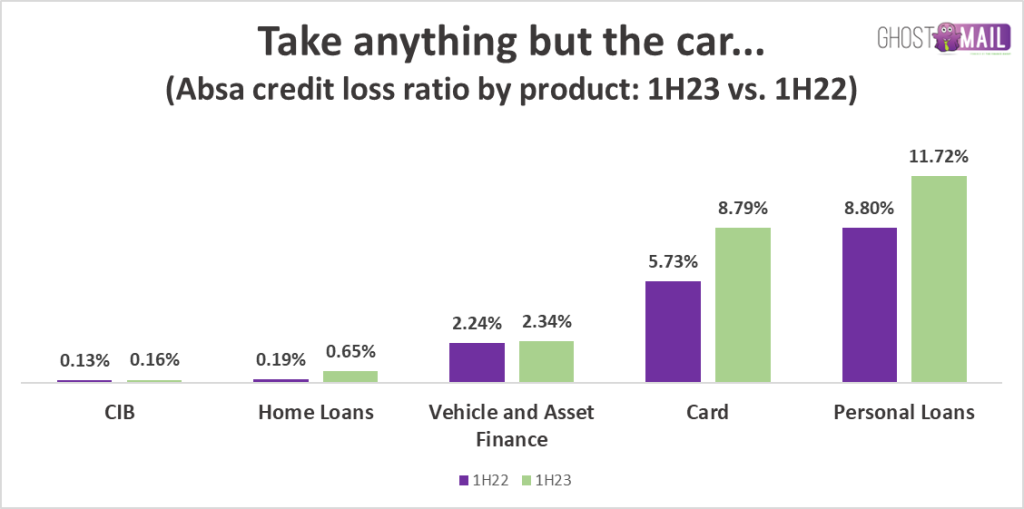

In banking, Nedbank and Absa both released earnings that reflect a deteriorating credit outlook, particularly in retail banking in portfolios like home loans.

In mining, the cycle has turned ugly for most players, with Exxaro, Northam Platinum, Sasol and Glencore as the latest examples.

In telecoms, Vodacom’s fibre ambitions have hit a regulatory hurdle and MTN seems to have put together an exciting Fintech deal with Mastercard, announced alongside its earnings

In building materials and home improvement, Cashbuild is taking a lot of strain and Italtile is also in the red, with consumer discretionary spending disappearing into inflationary pressures and higher interest payments.

Finally, Nampak needs a R1bn rights offer to appease its lenders, along with disposals of non-core assets worth R2.6bn.

The strong share price rally over the last three months looks to be fading

Absa’s share price is up around 12% over the past 12 months, mainly a function of its relative valuation and some relief in the pain of load shedding. It closed as high as R189.45 at the end of July, with that price point as a rapidly diminishing memory with the price closing at R177.76 on Monday after the release of results.

With operations in 15 countries, Absa is a meaty operation. It also has complications like various African exposures, some of which have bitten the group recently as currency and fiscal volatility plays out in the region.

For the six months to June, HEPS on a normalised basis (adjusting for the separation from Barclays, which is a sensible adjustment) only increased by 2.7%. This is despite total income increasing by 12.8% and the cost-to-income ratio improving from 51.2% to 49.8%.

The only explanation can therefore be the credit loss ratio. Sure enough, it has jumped from 0.91% to 1.27%. This means that impairments were 60% higher at a whopping R8.3 billion as the group made provision for these economic conditions. Pre-provision operating profit was up 16%. It’s tempting to think that this tells you what would’ve happened in a consistent economic environment, but this level of growth is also a function of a higher rates environment. You can’t have higher rates without a deteriorating credit outlook.

Return on equity has fallen from 17.5% to 16.7%.

Unsurprisingly, loans to CIB (corporate and investment banking) customers were up 11%, which is higher than growth in loans and advances in the retail and small business books. Corporate balance sheets are in much better shape at the moment than individual borrowers.

To give an idea of just how bad it is getting out there, home loan impairments were up 258% as the credit loss ratio jumped from 0.19% to 0.65%. If you could accurately mark-to-market your property investment right now, I’m quite sure your share portfolio would be the last thing keeping you out at night.

The pain in the property market hasn’t even begun yet. Watch this space.

And if you’re wondering about other products, here are some credit loss ratios to put it all in perspective:

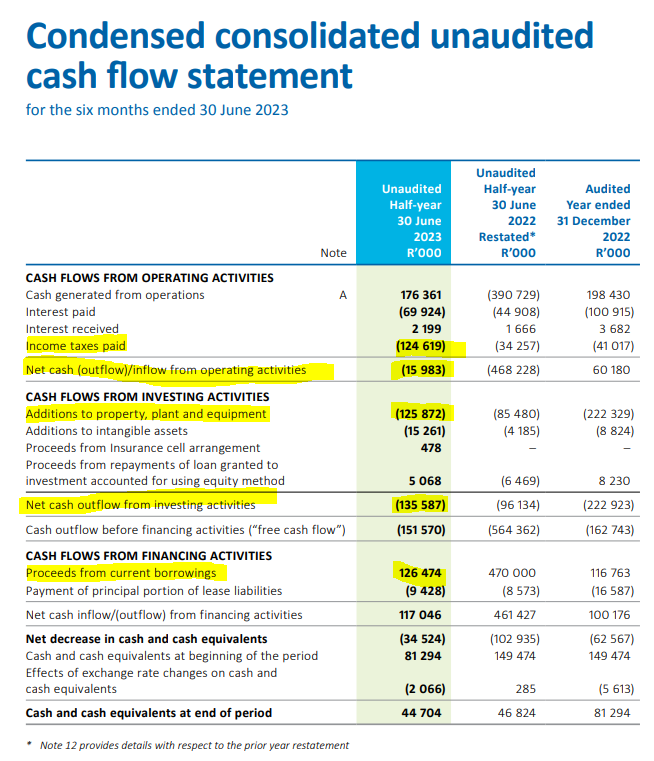

Hulamin: does it ever generate free cash flow? (JSE: HLM)

Earnings don’t help if the cash doesn’t reach shareholders

For the six months to June, Hulamin managed to grow normalised HEPS by 94% to 70 cents. That sounds delightful, especially on a share price of R2.92 (down 7.89% for the day).

Why did the share price drop sharply? The answer can be found on the cash flow statement.

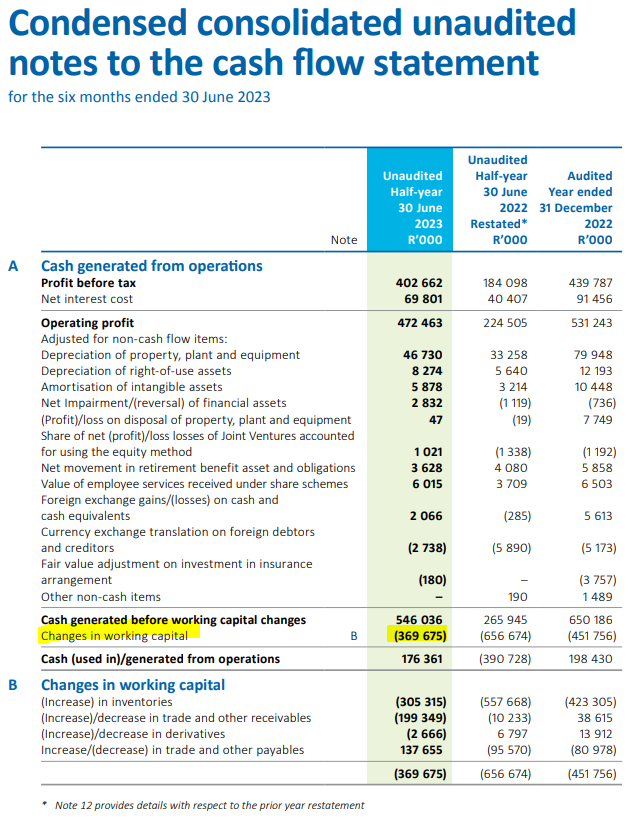

The first problem is the big jump in working capital, which eats up a big chunk of cash from operations:

The next problem is that once you take off tax, there isn’t even a positive balance before we deal with capital expenditure of R125.8m. This is why the group keeps funding its growth using current borrowings rather than internally generated cash flows:

If you look carefully, that issue isn’t unique to this period either. With no dividend declared for this period and a clear issue in how the business is funding its growth, I’m not surprised that the market got spooked by the release of detailed results.

Italtile is facing a perfect storm (JSE: ITE)

New builds and renovations just aren’t happening in this environment

Much like sector peer Cashbuild (JSE: CSB), Italtile is really struggling in these conditions. Just think logically about your own financial situation and level of confidence in our country right now: are you willing and able to invest heavily in a new property or a major renovation? What about your friends? That’s what I thought.

With massive inflation in basic living costs alongside the impact of higher rates on the cost of debt, disposable income is thin on the ground. To make it worse, Italtile has flagged increased competition from global players as another major challenge.

Despite price inflation of 6.7% in Italtile’s retail business, like-for-like turnover fell by 0.3% in the year ended June. This means that volumes tanked by 7%. On the manufacturing side, sales increased by 4.1% despite volumes dropping. Manufacturing businesses have high levels of operating leverage (fixed costs), so sales growth below inflation will lead to an ugly result in operating profit when full details are released. The final segment is the import business, which suffered a drop in sales of 4%.

Across the group, gross margin fell by 240 basis points. That’s significant.

Against this backdrop, it’s probably a pretty good outcome that HEPS is down by “only” 11% to 16%. This is a range for HEPS of 127.8 cents to 135.3 cents. The share price closed 1.22% higher at R12.40.

Lighthouse is still paying out more than earnings (JSE: LTE)

And once again, there’s a scrip dividend alternative on the table

Lighthouse Properties reported 0.62 EUR cents of distributable earnings per share for 1H23. Despite this, the dividend is 1,350 EUR cents per share, so that’s a payout ratio of 218%. You won’t see that every day.

Despite clearly supplementing the dividend from retained earnings, the distribution is actually down 16.9% year-on-year.

Full-year guidance has been reduced from 2.8 EUR cents per share to 2.7 EUR cents per share, a result of Hammerson (JSE: HMN) reducing its dividend payout ratio. Assuming this is achieved, it would utilise the remaining distributable retained earnings.

MTN announces earnings, with the market’s focus firmly on Fintech (JSE: MTN)

A deal with Mastercard has shone the light on what the Fintech business is worth

The telecoms space has been very tough recently and arch-rival Vodacom has suffered a setback in its bid to become a fibre powerhouse, with the Competition Commission trying to block the deal with Vumatel and Dark Fibre Africa. MTN must be glowing about having such positive news to share against this backdrop.

The good news isn’t to be found in the earnings. Although MTN’s service revenue increased by 16.5% and EBITDA was up by 12%, HEPS could only increase by 7.1% and there is no interim dividend, although I think the market was only realistically expecting a final dividend anyway. MTN has committed to a minimum of 330 cents per share for the full year.

Instead, the good news was firmly in the announced Mastercard transaction, with MTN Group Fintech being valued at $5.2bn. With a group market cap of around R244bn, I’m not sure many people had put a valuation of roughly R100bn just on the Fintech business. It makes a world of sense for both parties, with the market celebrating this news with a 4.9% rally in the share price. The announcement didn’t give any further details and we also don’t know what Mastercard’s stake will be. All we know is that MTN will retain control of its Fintech business.

The balance sheet is becoming a concern again, with holding company leverage up from 0.8x at the end of December 2022 to 1.5x at the end of June. The group level debt isn’t an issue at all. The problem is that MTN cannot get all of its cash out of Nigeria and Ghana, so the problem is where the debt is rather than the overall quantum of group debt.

Without the Mastercard news, the share price would be singing a different tune at the moment.

Nampak needs a R1bn rights offer to survive (JSE: NPK)

Shareholders must wait until 2027 to earn “economic profits”

There’s a lot to unpack here. Let’s start with the debt refinancing.

All but one small lender have now agreed to a debt refinancing package for Nampak, which means they are happy to keep the company alive subject to conditions including an equity capital raise and the disposal of non-core assets. The banks love this because they are the only ones who will actually earn economic profits from Nampak: a return commensurate with the level of risk. Equity holders won’t be so lucky, although it gets even more technical than that. I’ll come back to this later.

The revised debt structure envisages R5.1bn in debt at Nampak Products Limited and R286m as well as $34.6m at Nampak International. There is also over R1.9bn in debt related to Angola and Nigeria that will be housed in an intermediate holding company. Within this package is a mix of term debt (repaid over an agreed period) and revolving debt (more like an access bond on your home that gives ongoing access to debt). This is important to give Nampak some ongoing balance sheet flexibility.

This is the structure that would be in place after a successful implementation of a rights offer and asset disposal plan. The rights offer is to raise R1bn, which is hugely dilutive on a market cap below R600m. The non-core asset disposal plan is even more ambitious, with plans to sell R2.6bn worth of assets. Even if they get this right, the net debt to EBITDA ratio will be below 3x by FY24 (which is high) and below 2x by FY25 (manageable but still high).

With all said and done, Nampak would be a R10bn revenue business consisting of Bevcan SA, Bevcan Angola and Divfood. EBITDA margin would be between 10% and 12%. Working capital would sit at between 19% and 21% of turnover and the annual capex bill is expected to be R250m although it will be higher in the immediate future based on existing projects.

To get it done, Phil Roux has now been appointed as the CEO. He has a ton of experience in the FMCG sector.

We can now deal with the “economic profits” concept raised earlier, which is a measure of returns generated by Nampak vs. the weighted average cost of capital (WACC). The goal of simply being profitable is reserved for useless state-owned enterprises like SAA. A private company needs to not just be profitable, but generate an attractive return on capital. Simply, if I asked you to invest R1m in a project that makes annual profit of R100, would you do it? Of course not.

Nampak only expects to generate Return on Invested Capital (ROIC) ahead of WACC by FY27. In other words, from a theoretical standpoint, Nampak actually shouldn’t exist as a company until that point.

There’s a final step in this dance. There are many companies out there that can’t beat their weighted average cost of capital. As a result, they trade at a discount to net asset value (NAV), as shareholders aren’t prepared to pay the NAV in exchange for sub-par returns. This means that if the plan works, Nampak should theoretically trade at 1x NAV or higher by FY27. That’s a bit like a pull-to-par concept in fixed income investing.

If you want to have a punt here, make sure you’ve done the proper analysis and that you correctly take into account the huge rights offer on the table. Personally, I’ll wait until after the rights offer to even consider an entry here. If for any reason they can’t raise the capital, Nampak would likely face an existential crisis and that almost never ends well for shareholders.

Northam adds to the woes in the PGM sector (JSE: NPH)

Platinum counters got absolutely smashed on Monday

The bottom 10 of the top 100 shares on the local market was dominated by PGM companies taking the top spots. Impala Platinum closed 9.8% lower, Anglo American Platinum was down 9%, Northam dropped 7.5% and Sibanye took a 6.6% bath, shielded to some extent by gold exposure.

Although PGM prices dipped and that always causes the share prices to follow suit, it’s likely that part of the market capitulation was linked to the release of results by Northam Platinum for the year ended June. Despite a 13% increase in production from own operations and a 16.1% increase in sales revenue despite a 6.9% decrease in the basket price, there was a drop in HEPS of between 2.5% and 12.5%.

The EPS story is incredibly bad, with huge impairments on the investment in Royal Bafokeng Platinum and the Eland operation.

Net debt was R9.4 billion at year-end, with R9 billion received subsequent to year-end from the disposal of the stake in Royal Bafokeng Platinum. In other words, Northam Platinum is ready to tackle the deteriorating cycle with almost no debt on the balance sheet.

That’s just as well, because PGM markets are looking increasingly weak and the market is starting to show signs of panic. Here’s a chart of the three pure-play counters in the sector, showing that what goes up often comes down in mining:

Sanlam needs to unwind its pre-Covid B-BBEE deal (JSE: SLM)

If a deal is going to fail, rather fail quickly

On my birthday in 2019, Sanlam executed a B-BBEE deal and didn’t give me a single share as a present. In the end it doesn’t matter, because the structure isn’t going to work.

The shares were issued at R70 each (a discount of nearly 10% at the time). Sanlam is now trading at R65, with the pandemic and general SA issues having put the structure into a hole that it won’t dig its way out of in time.

The external funding party is Standard Bank. If the covenants in the structure are breached, Standard Bank would likely require the structure to dispose of a large block of Sanlam shares, which would be a substantial overhang on the share price. To avoid this, Sanlam is going to buy the preference shares from Standard Bank, effectively turning this into an internally funded structure.

This still isn’t a great outcome for Sanlam shareholders obviously, as Sanlam is effectively investing in itself at an underlying price that made sense a few years ago but not anymore. Still, Deloitte has opined that the deal is fair to shareholders of Sanlam. This was the major condition to the deal as this is a small related party transaction.

Sasol’s HEPS disappointed the market (JSE: SOL)

Sasol hasn’t escaped the broader challenges for the mining sector this year

Practically every mining update in the past couple of months has followed the same playbook: commodity price pressure, some kind of production challenges (usually Eskom), issues with Transnet putting a dampener on sales volumes and inflationary impacts on mining costs that are squeezing margins.

Sasol is no different, with adjusted EBITDA for the year ended June 2023 down by between 2% and 16%. The group always focuses on reporting core HEPS, with that metric down by between 25% and 39%. This implies a range of between R41.14 and R51.14. The share price closed 5.4% lower at R254.50 a share, implying a Price/Earnings multiple of between 5x and 6.2x.

Shaftesbury gives you a UK property debt data point (JSE SHC)

Well, sort of

Shaftesbury owns a solid portfolio of properties in London’s West End. The company has raised 10-year debt funding from an existing lender and this gives us a view on the UK yield curve for property debt. Unfortunately, the company reports a blended rate alongside existing loans that mature in 2030 and 2035, so you would need to go do some digging if you want to really figure out the answer here.

For most of us, it’s just good to know that the blended rate of the new financing package plus the existing debt is 4.7%. If I understood the announcement correctly, the weighted average cost of debt for the entire fund will be 4.2% once the proceeds from this debt will be used to repay an unsecured facility.

4Sight dishes up a dividend (JSE: 4SI)

The share price jumped accordingly – with decent volumes to boot!

Diversified technology group 4Sight Holdings is barely on anyone’s radar. The share price started the year at 25 cents and is now at 39 cents, a juicy 56% return. Every now and then, local small caps pay off.

In the six months to June, revenue jumped by 37.1% and operating profit more than doubled, growing by 121.1%. By the time we reach HEPS, it nearly tripled with a 197.2% increase.

There’s a dividend per share of 2.5 cents, which is a yield of 6.4% on the day’s closing price. Not a bad yield for an interim dividend, is it?

Little Bites:

Director dealings:

A founding director of Famous Brands (JSE: FBR) has taken out a loan from a financial institution and has agreed to hedge R11.6m worth of shares in Famous Brands. The put strike price on the collar is R59.54 which is very close to the current price of R60.21. The call strike price is R74.88. Expiry is August 2025. This is known as a collar structure.

It’s a tiny trade, but a director of Dis-Chem (JSE: DCP) sold shares worth R2.5k.

Trencor (JSE: TRE) is a legacy structure the directors hope to start winding up after December 2024. The latest net asset value per share has been announced as R8.05 and the share price is R6.80.

Jubilee Metals (JSE: JBL) is attracting seasoned executives to the business, like Neal Reynolds who has now been appointed as the CFO. He has previously held various senior roles in the sector.

It seems as though British American Tobacco’s (JSE: BTI) debt tender offer is going well, with the company announcing early results. As part of that announcement, the company announced that the maximum aggregate purchase price was being increased in certain debt pools.

There’s no liquidity in this stock, so Deutsche Konsum REIT (JSE: DKR) only gets a mention down here to help you compare the numbers to other European property funds you might be holding. In the first nine months of the financial year, rental income increased by 6% but funds from operations fell by 15% because of the cost of debt and inflationary pressures on costs.

There was a time when South Africa, along with other emerging markets, was considered a new frontier for growth.

But over time, South Africa has lost much of its lustre and in the midst of globally high interest rates, an energy crisis and a number of questionable policy mis-steps, investor optimism has been diminishing.

Several reports on global investor trends show that investing behaviour is changing and according to the 2023 EY Global Wealth Research Report, 57% of high net-worth individuals feel unprepared to meet their financial goals – citing market volatility as a primary reason.

This report also details interesting differences between younger investors and baby boomers, however, despite the differences in investment appetites, 73% of all respondents report changing investment behaviour because of a decline in portfolio values.

Other interesting finds are that the appetite for advice is growing, and that investors have acted in similar proportions in response to market volatility, moving to active investments and seeking safety with increased allocation toward savings or deposits.

Michael Field, GM: Investments at Fedgroup, says that these investor trends have also been observed and reported locally, speaking to a growing investor need for certainty amidst global and local unpredictability.

“What we have seen in the last few months are investors moving towards fixed instruments as investment options, with outflows from variable instruments and assets.”

Data from SARB shows that fixed deposits and notice deposits grew 16.45% over the 18-month period between January 2022 and June 2023. Fedgroup has seen a similar trend over this period, with growth of 33.5% in its Secured Investment product, offering an attractive fixed rate over five years along with capital security and zero fees.

This investor behaviour speaks to a growing, risk-averse trend both locally and globally.

Earlier this year, asset manager Ninety-One, reported a £10.6 billion (about R138bn) in net annual outflows of assets under management (AUM) in May, indicating a preference for the preservation of capital over the potential for higher-than-average returns.

An additional nuance to this behaviour doesn’t just exist in the world of HNWIs (high-net-worth individuals) but amongst middle-income retail investors who are becoming more savvy when it comes to using traditional banking products to save and invest. These investors are also often younger. TymeBank’s Rainy Day Report 2023 shows that from TymeBank’s depositor base, just under 40% of customers between the ages of 26 – 35, used a fixed deposit to save. The trend towards capital preservation, and ensuring that it appreciates, even modestly, is a preferred way to navigate volatility – especially in a market facing national elections next year, along with probable policy changes.

Fedgroup is known for its Secured Investment offering and recently developed additional products to protect and grow investors’ wealth, particularly in its competitive Specialist Endowment Portfolios. These portfolios include a combination of alternatives and traditional underlying assets that are counter-cyclical in nature and designed to smooth volatility and provide balance to investment portfolios.

In response to the growing client need for certainty, Fedgroup has now also launched a Fixed Endowment offering, providing all the tax and estate benefits of the endowment structure along with a market-beating fixed return. Clients and financial advisors have seen the value in this offering and demand has been overwhelming.

So whether the world you’re facing experiences a black swan event, a global pandemic, war in the 21st century, a suspended government in Europe, a coup in West Africa, a local road falling in like you’re living in a Marvel movie, or political battles that now take place in the courtroom instead of the ballot, speak to your financial advisor about how Fedgroup’s Fixed Endowment and its top-performing Secured Investment can offer you certainty so you can be a bit bolder in the world of the upside down.

Disclaimer: you might not want to read this post on an empty stomach! We take no responsibility for any fast food cravings you might develop along the way.

Forget that old paradox about the chicken and the egg. The much more interesting question is which fast food giant came first: McDonalds or Burger King?

In 2015, McDonalds celebrated the 60th anniversary of the opening of businessman and franchisor Ray Kroc’s first McDonalds in Des Plaines, Illinois. As a tribute, they introduced a limited edition menu item: the 1955 burger. This of course was the perfect moment for arch-rival Burger King to ever-so-subtly start rolling out their new tagline: “Since 1954”.

What sounds like a petty little snub was actually a finely orchestrated act of one-upmanship that Burger King had been developing since July of 2014, when they first trademarked “Since 1954”. They secured the trademark, and then waited almost a full year to roll it out.

Why the wait? Well, they needed McDonalds to make their move first. The hubbub around the 1955 burger was the perfect opportunity for Burger King to remind the world at large that actually, they had the headstart when this race began.

All’s fair in mayonnaise and war

Of course, in the greater scheme of things, it hardly matters at all that Burger King opened their restaurant four months before McDonalds opened theirs. At least, that’s the story according to them.

It’s tempting to get into the specifics of second mover advantage, particularly between two businesses that have an almost identical consumer base. Only so much can be attributed to coincidence, after all. McDonalds has the Big Mac, Burger King has the Whopper. McDonalds serves Coke products, Burger King serves the Pepsi line. McDonalds has the McFlurry, Burger King has something called a King Fusion that is so laughably similar to a McFlurry – down to the design of that signature mixing spoon – that you can practically visualise copyright lawyers frothing at the mouth.

Imagine having the advantage of tweaking your competitor’s star product while doing none of the market research yourself. That’s second mover advantage in a nutshell.

In some cases, these parallels between the two menus are actually deliberate. Some would argue that the most successful feats of Burger King’s strategy come about from directly challenging McDonald’s products. In November 2013, Burger King introduced the Big King sandwich – with two patties, a three-layer bun, and a special sauce – as a less-than-subtle competitor to the Big Mac. When McDonald’s brought back the McRib sandwich, Burger King came up with the BK BBQ Rib as a cheaper alternative. And then in 2018, Burger King took direct aim at McDonalds’ quarter pounder by announcing a double quarter-pound burger.

Flame-grilled guerilla tactics

Of course, there is no point in mentioning the rivalry between McDs and BK without highlighting the absolutely magnificent effect that this has had on Burger King’s marketing strategies.

The intense competition between the two brands has driven Burger King to tactics that make guerilla warfare look like child’s play. One particularly memorable example of their “hacktervising” involves a campaign called the Whopper Detour, a bold stunt that promoted a $1 cent Whopper that could only be ordered through the Burger King app.

The catch? The promotion would only become available if that Whopper was ordered from a McDonalds parking lot! Using geofencing technology, Burger King was deliberately sending its customers right onto the doorsteps of their biggest competitor, actively forcing them to reject those burgers, and then calling them home to their own drive-throughs.

Beyond successfully executing perhaps the most cold-blooded feat of marketing psychology in fast food history, Burger King also achieved over 1.5 million downloads of their app over the course of the campaign. Check out this great video on the topic:

Competition. I’m lovin’ it.

So what have we learned from this article, besides the fact that burger wars are a thing? In short, competition makes businesses better. That’s why every report in the Magic Markets Premium library has a section dedicated to competitors in a particular business’ field.

Think of competition as the ultimate motivator. It’s like an unfriendly nudge to keep businesses on their toes, always looking for ways to make things better – whether it’s juicier burgers or smarter marketing strategies. And guess who benefits the most? Yup, you and me, the customers! We get a whole bunch of choices, better products, and great deals, all thanks to this healthy rivalry. And when businesses win over more customers, that means good things for shareholders.

For the price of one burger per month, you can buy yourself a treasure trove of delicious business insights. With nearly 90 research reports on global stocks available in the library, a subscription to Magic Markets Premium for just R99/month gives you access to an exceptional knowledge base that has been built since we launched in 2021. It’s not quite “Since 1954”, but we’re pretty proud of it just the same.

And if this sector has piqued your interest, you’ll be pleased to know that the research library also includes a report on Yum! Brands from February 2023.

Eastern Platinum gets a boost from chrome prices (JSE: EPS)

Despite the name, around 94% of revenue is from chrome concentrate sales

Eastern Platinum has reported results for the quarter and six months ended June, so you have to be careful when reading the results to see whether you’re looking at a quarterly or interim (six months) number.

Revenue increased by 78.5% year-on-year for the quarter, or 54.9% for the six months. Gross margins also improved, so mine operating income was over three times higher for the quarter. By the time we get to net income attributable to ordinary shareholders, we find a huge jump from $1.2 million in Q2 last year to $7.7 million in Q2 this year. On a six-month basis, it more than doubled from $4.2 million to $9.0 million.

The balance sheet remains a problem though, with a working capital hole of $16.1 million (current assets minus current liabilities). That’s better than it was a year ago (a deficit of $39.5 million) but remains a significant concern. Union Goal has now stopped taking shipments of chrome concentrate due to payment disputes, so revenue since June 2022 has been generated from third-party sales.

Be very careful here, as chrome sales from the retreatment plant are expected to end by early 2024. After that date, PGMs will be the main source of revenue based on the restart of the Zandfontein underground section of the Crocodile River Mine. The company needs to raise additional capital for that project.

The share price has lost over 70% of its value this year. Whistleblower allegations regarding undisclosed related party transactions have been part of the market pressure, with an investigation by a special committee underway.

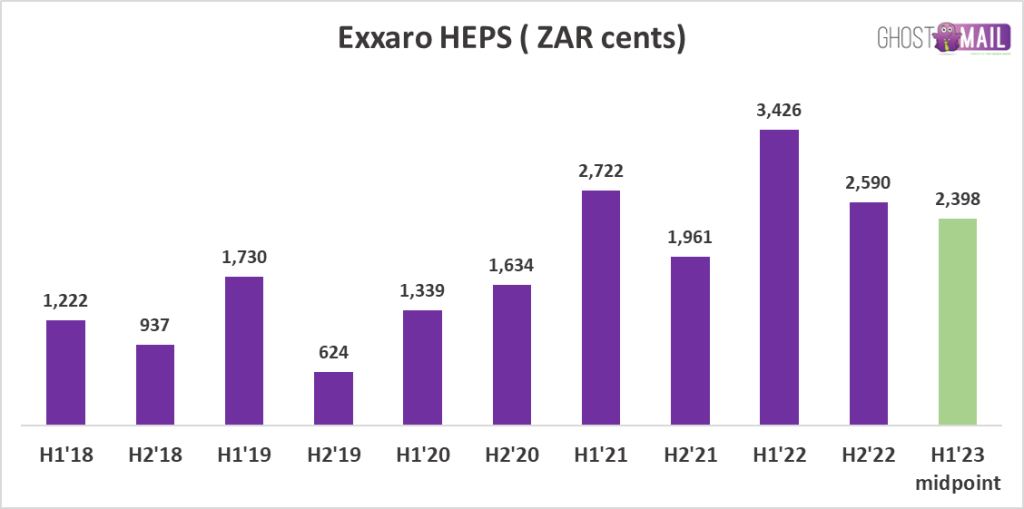

Exxaro flags a drop in earnings (JSE: EXX)

Like most of the mining sector companies, earnings went the wrong way this year

The story of the mining sector this year is one of lower commodity prices, production challenges thanks to Eskom and distribution problems thanks to Transnet. We are a resource-rich country that is exceptionally good at scoring own goals.

Exxaro hasn’t escaped this unfortunately. With coal prices and volumes have dropped, earnings could only go in one direction.

Headline earnings per share (HEPS) is expected to drop by between 23% and 37%, which means an earnings range of between R21.58 and R26.38. This is for the six months to June.

Using the midpoint of that guidance, here’s a chart of earnings at Exxaro in recent years:

As I always remind you: if you want a low-stress investment that you can buy and forget about, stay as far away from mining as possible.

Here’s what the share price has looked like over the past five years:

The return does not reflect the dividends along the way, which are typically the biggest component of the total return in a mining house like this.

Finbond proposes a huge special repurchase (JSE: FGL)

The Massachusetts Institute of Technology (yes, that MIT) wants out

In case you’re wondering quite why MIT has a big stake in Finbond, you aren’t alone. MIT must be wondering much the same thing in terms of how it all went so wrong. The famous education institution invested in a local fund that didn’t work out. When the fund was unwound, they ended up holding shares directly in Finbond (and a few other companies too).

Net1 Finance Holdings also wants to exit its stake in Finbond, with these two investors collectively holding 38.55% of Finbond’s total issued ordinary shares.

This is a huge stake to try and sell, which is why the parties have agreed an exit price of 29.11 cents per share. That’s quite a bit lower than Friday’s closing price of 35 cents, although I think they would be a lot worse off if they tried to sell on the open market. Finbond doesn’t have nearly enough share price liquidity for an exit of a stake that size to be possible.

Finbond has enough cash or existing debt facilities available for this repurchase, which comes to just under R100 million. The company likes the deal because it can take shareholders off the register at a significant discount to the current share price. Whether or not the market will support this allocation of capital is a different question.

As this is a repurchase from a related party, a circular will be sent to shareholders. If the repurchase isn’t approved, I genuinely don’t know how MIT and Net1 will sell their stakes.

Little bites:

Director dealings:

A director of Argent Industrial (JSE: ART) has sold shares worth roughly R400k.

A director of Altron (JSE: AEL) has bought shares worth nearly R158k.

Quite hilariously, a director of Afine Investments (JSE: ANI) bought shares worth R380. No, there isn’t a “k” missing there. 95 shares at R4 each!

Those following Novus Holdings (JSE: NVS) will want to know that A2 Investment Partners now holds 28.20% of the issued share capital in the company after Caxton and CTP (JSE: CAT) sold out completely. Will we see a takeout offer at some point?

Grindrod Shipping’s (JSE: GSH) extraordinary general meeting went to plan, with almost unanimous approval for a $45 million capital reduction. In other words, a large cash payout to shareholders is coming up, which is part of why the share price closed over 9% higher on Friday.

Cognition’s (JSE: CGN) sale of its head office for R11.875 million has met all required conditions, so the transaction will now be implemented. It may sound like a silly update, but the market cap is under R200 million so this is a material unlock of cash.

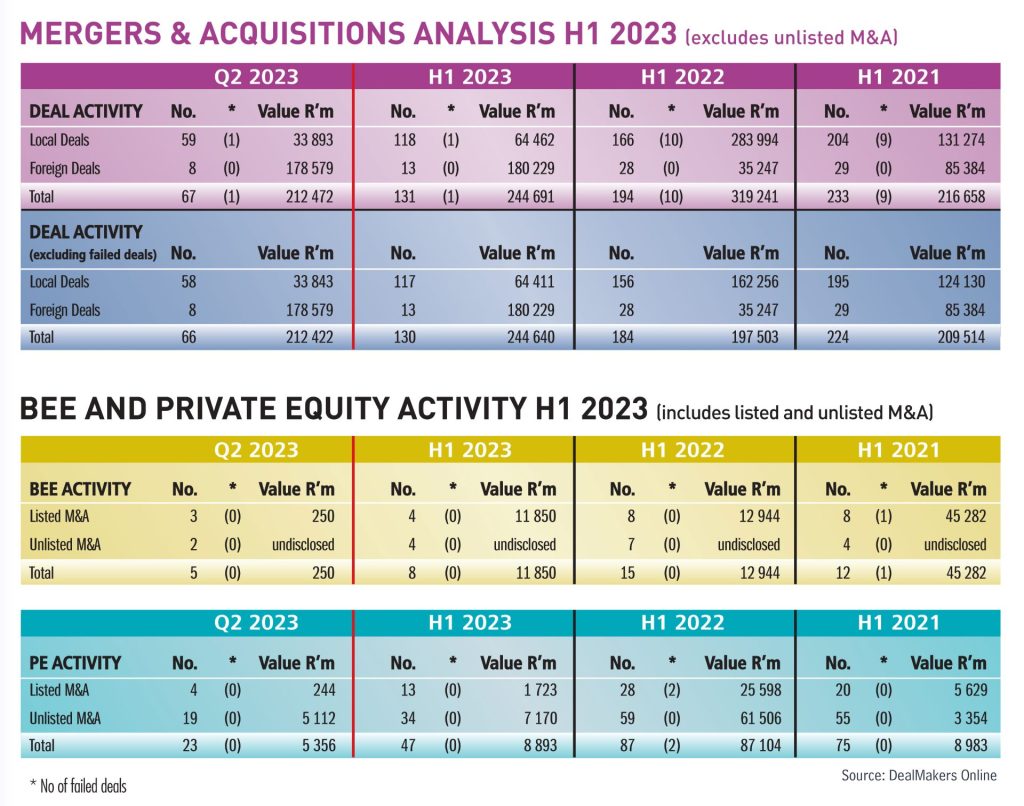

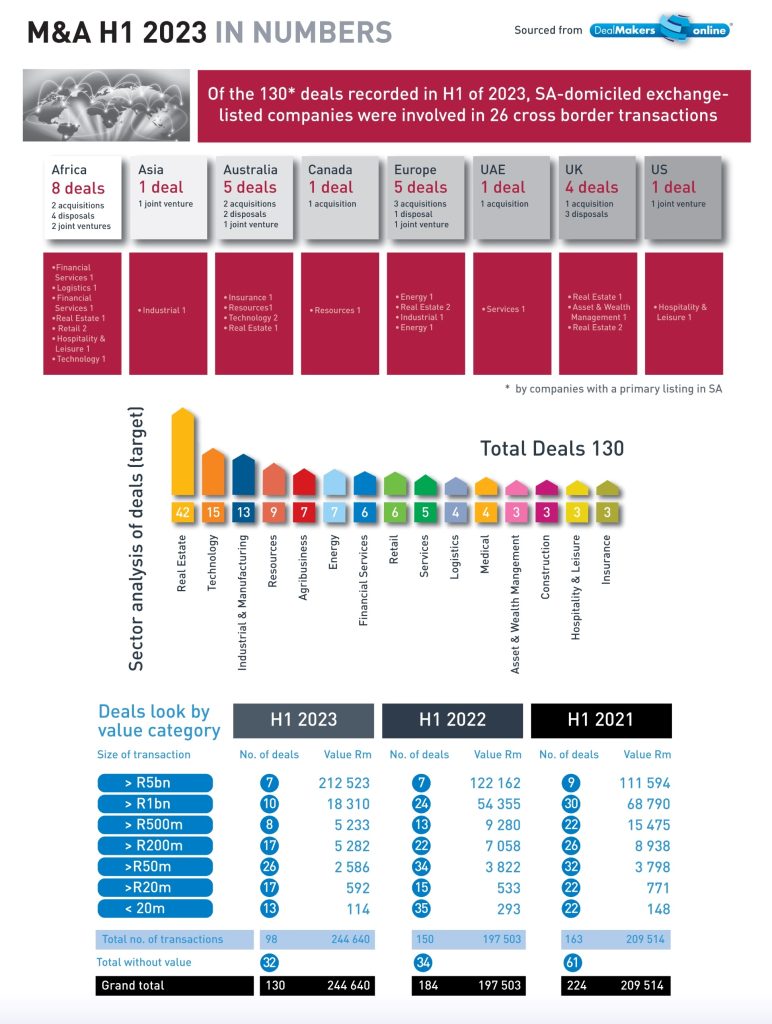

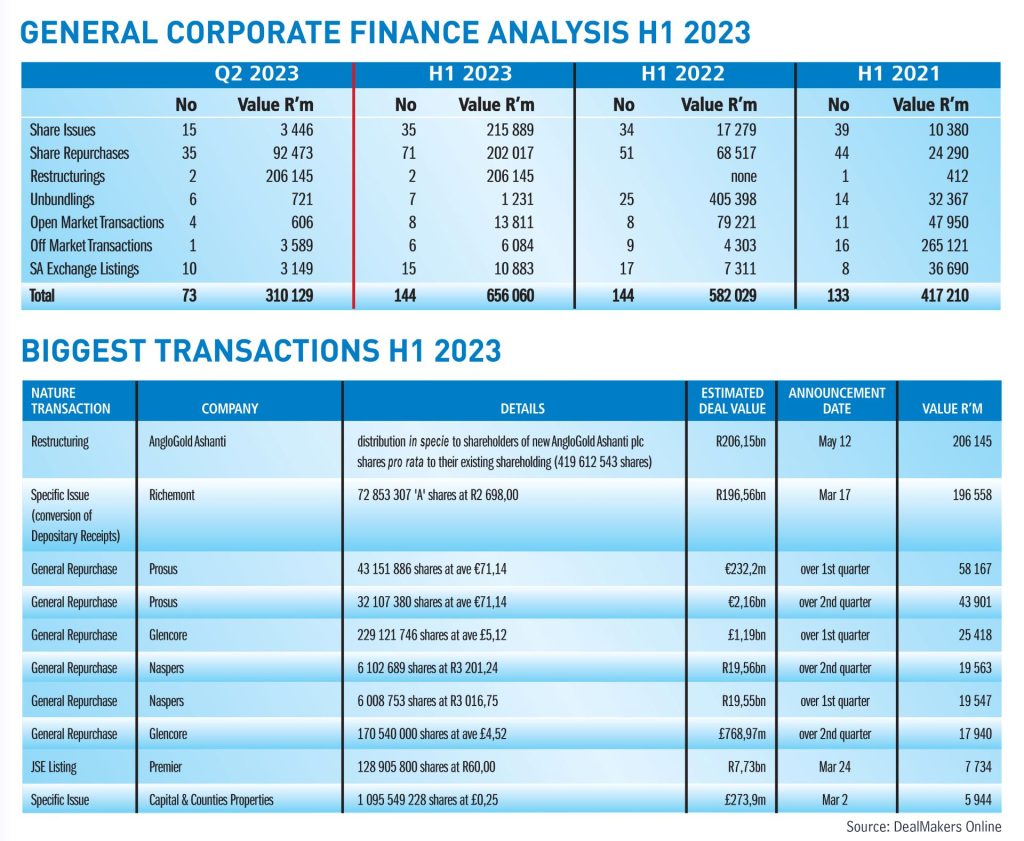

If a picture paints a thousand words, then so too do the M&A analysis tables below. The decline in merger and acquisition activity in South Africa began as far back as 2008, when the effect of the financial crisis hit home and the economy entered recession. In its hay day (2007), the industry reported 883 deals (listed and unlisted deals combined); an aggregate of some 405 for the half year. At the end of June 2023, the number was a meagre 242.

Since the release of a damaging report on state capture by the outgoing Public Protector Thuli Madonsela in 2016, and particularly in the last two years since emerging from the COVID-19 pandemic, the extent and reach of the malaise throughout the organs of government have become all too clear. This, together with uncertainties created by the war in Ukraine, inflation rates, looming recession, a weakening domestic exchange rate, foreign policy blunders, and the recent ‘greylisting’ of South Africa have forced investors to place more scrutiny on their investment domiciling decisions.

The most active sectors during H1 were Real Estate (32% of the quarter’s deals) followed by the tech sector. Deal size fell typically in the R50m to R200m bracket reflecting a third of deals recorded for the period. SA-domiciled companies were involved in 26 cross border transactions, notably within Africa (8), Australia (5) and Europe (5).

Share issues and repurchases characterised the general corporate finance activity for the first six months of 2023, with R215,89 billion raised from the issue of shares and R202 billion the value of shares repurchased. The repurchase programmes of Prosus, Naspers and Glencore account for most of this value, while the aggregate value of Richemont’s issue of A shares (conversion of depositary receipts) was R196,56 billion.

Although ratings agency, Fitch recently held SA’s credit rating at BB- (three steps below investment grade), it warned that further big increases in government’s debt-to-GDP ratio could lead to a further downgrade. The IMF is forecasting GDP growth of 0.3% in 2023, against 1.9% in 2022, due to severe power shortages – lagging far behind the 4% average at which the IMF sees emerging markets and developing economies growing in 2023. The Reserve Bank estimates that power cuts trimmed between 0.7% and 3.2% off the GDP growth rate in 2022, and that supply disruptions will cut 2% off output growth in 2023.

Looking ahead, the local equities and the SA bond markets offer value to potential investors relative to their international counterparts – but investors will continue to be circumspect, with much depending on SA’s ability to extract itself from the quagmire in the months ahead.

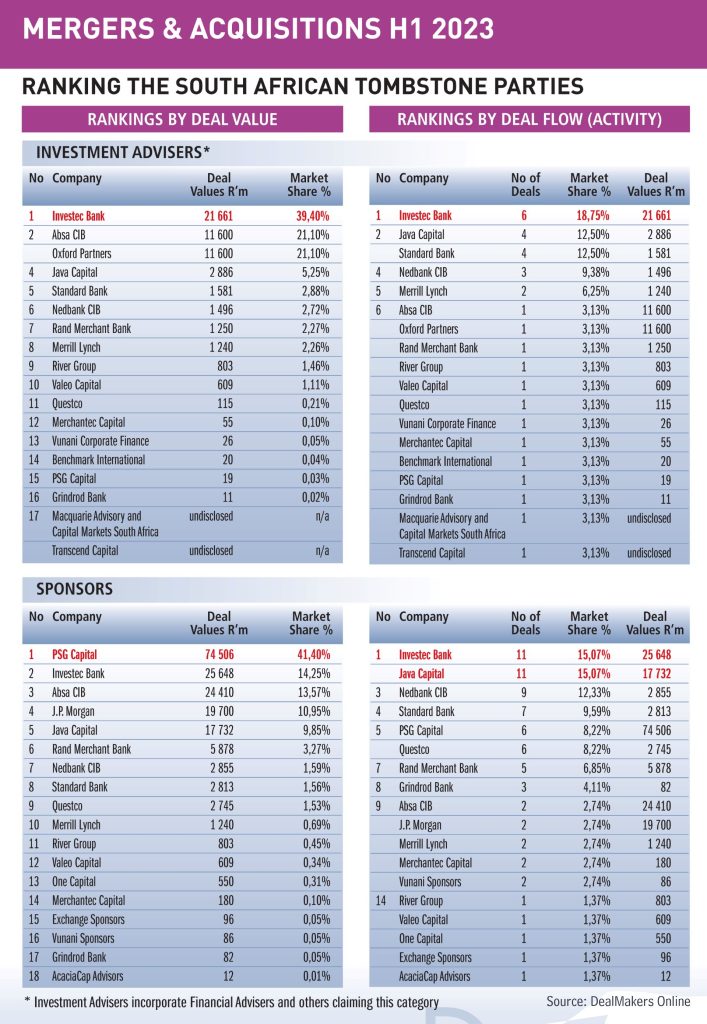

DealMakers H1 League Table – M&A activity by the top South African advisory firms (in relation to exchange-listed companies).

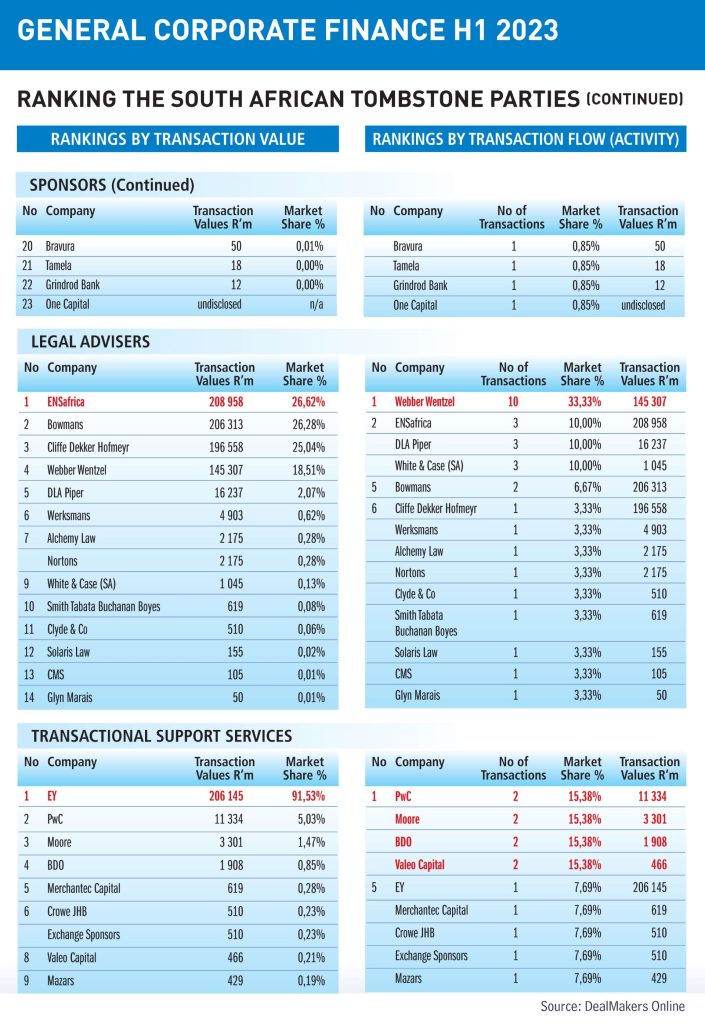

DealMakers H1 League Table – General Corporate Finance activity by the top South African advisory firms (in relation to exchange-listed companies).

Capital & Regional is to acquire The Gyle Shopping Centre in Edinburgh, Scotland for a total acquisition consideration of £40 million. The acquisition will be financed through existing funds held by the company, a new debt facility of £16 million and c. £25 million from proceeds to be received from a fully underwritten (by Growthpoint) capital raise. The capital raise is being implemented by way of an open offer of 46,278,681 open offer shares. The issue price of 54 pence/R13,03 per share represents 4 open offer shares for every 15 existing ordinary shares. Approximately £1,6 million of the proceeds will be used to pay fees and expenses incurred in connection with the proposed transactions.

STANLIB Asset Management (Standard Bank) through its Infrastructure Fund II, has acquired a controlling interest in renewable energy solutions specialist Solareff and its subsidiary, GridCars. Solareff is a commercial and industrial solar and battery platform with over 500 projects to date and a total of over 190MW of installed capacity. GridCars is the owner, operator, and supplier of charge-network infrastructure with related network software for South Africa electric vehicles. Financial details were undisclosed.

PPC has concluded an equity transaction with a newly formed PPC Employee Share Ownership Trust which has acquired 10% of PPC South Africa for a purchase consideration of R380 million. All employees not currently participating in PPC’s long-term incentive programme will be eligible and participation will be weighted in favour of the historically disadvantaged. The company will provide the Trust with a loan of R380 million which will be repaid from 75% of the dividends that it will receive from it shareholding in PPC SA, with the remaining 25% distributed to the beneficiaries.

Remgro and Vodacom have advised that the Competition Commission has recommended to the Competition Tribunal to prohibit the proposed acquisition by Vodacom of a 30% interest in Maziv. The deal, first announced in November 2021, proposed that Maziv, a newly formed entity, would house the assets owned by Community Investment Ventures which included Vumatel and Dark Fibre Africa as well as certain fibre assets of Vodacom.

Unlisted Companies

Fledge Capital, a local private equity firm, has invested an undisclosed sum in Luxury Time, an online business selling high-end watches at discounted prices. The new investment will be used to scale its inventory and enhance its online presence and customer service capabilities.

FinMeUp, a community-based platform dedicated to fostering a collaborative environment and offering a range of solutions including financial advisory, investments, insurance and credit solutions, has raised an undisclosed sum. The funding round was led by SAAD and Blue Sky Investments. The startup will use the funds to scale operations and enhance its user experience.

ADvTECH schools the market on how to grow (JSE: ADH)

All divisions have been strong contributors to this result

We will need to wait until 28 August to get all the details, but we do know that ADvTECH put in a very strong earnings performance over the six months to June.

The education group has indicated growth in HEPS of between 21% and 26%, which suggests a range of 82.3 cents to 85.7 cents. The share price closed more than 4% higher at R19.42.

CA Sales Holdings drives earnings forwards (JSE: CAA)

This really is an interesting business

CA Sales Holdings isn’t on the radar of most investors, yet the company has a fascinating business model and it is clearly working. In a trading statement for the six months ended June, the company has highlighted growth in HEPS of between 19% and 24%. This implies a range of 35.69 cents to 37.19 cents, with a current share price of around R7.15 for context. Remember, those are half-year earnings.

This news was accompanied by the release of interim results

Capital & Regional isn’t a company that you’ll regularly see in the news. This property fund is focused on community shopping centres in the UK and has announced the acquisition of The Gyle Shopping Centre in Edinburgh for £40 million.

To finance the deal, the company is raising £16 million in new debt and around £25 million in equity, so that’s a very rare thing these days: an equity raise on the JSE! There’s zero chance of the capital raise failing, as Growthpoint is underwriting the offer in full at a price of 54 pence per share. In London, the share price closed at 56.40 pence, so that’s a slight discount.

The debt is being provided by Morgan Stanley at a fixed cost of 6.5% for 5 years. The days of cheap debt in the UK (and everywhere, really) are over. The asset is being acquired at a net initial yield of 13.51%, so the days of property owners selling on a low yield also seem to be over! At that purchase price and with strong anchor tenants in place, I can see why Growthpoint is happily to put up all the capital if other shareholders don’t support the capital raise.

You have to start asking some tough questions about valuations in the local market if a mall in Scotland (a land of electricity and service delivery) is priced on a yield of 13.51%.

Alongside the news of this transaction, Capital & Regional also announced its results for the six months to June 2023. Occupancy improved, rent collections were good and like-for-like rental income increased by 13%, driving a 17% increase in adjusted earnings per share.

Net asset value increased by 2.3% as valuations finally started to stabilise.

The interim dividend has been increased by 10% to 2.75 pence per share. That’s a lower payout ratio than the prior year based on adjusted earnings per share, perhaps in response to the loan-to-value increasing from 41% to 42% and a general increase in average cost of debt in the market.

Cashbuild got hammered, but perhaps by less than expected? (JSE: CSB)

HEPS has dropped sharply, yet the share price had a good day

Cashbuild isn’t exactly an illiquid counter, so a 3.7% increase for the day isn’t just because of the spread. Yes, the broader market was also in the green today, so Cashbuild’s outperformance after the market had the entire day to consider the trading statement says something about how bad the expectations were.

For the year ended June 2023, HEPS is down by between 35% and 40%.

Although I don’t usually focus on earnings per share (EPS), I will note that the P&L Hardware business has had its goodwill impaired in response to ongoing pressure on that business.

The HEPS range for the year is R11.576 to R12.541. The share price is R168, so that still feels like a big Price/Earnings multiple for something that is struggling so much.

Life Healthcare is still exploring a deal for AMG (JSE: LHC)

Unsolicited proposals received this year are being taken seriously

Life Healthcare has been trading under cautionary since February 2023 based on unsolicited proposals received from third parties for the group’s stake in Alliance Medical Group in Europe.

Although there is still no guarantee of a sale of the stake, these are clearly serious proposals because the group has “narrowed the scope off its evaluation” and is working to see if a transaction is possible.

A big drop in the Lighthouse dividend (JSE: LTE)

Details will be released next week

You may recognise Lighthouse Properties as the company that Des de Beer always seems to be buying shares in. If you followed his strategy in the hope of happy news on the dividend, you’ll be disappointed.

The company has noted that the interim dividend is 1.35 EUR cents per share, a decrease of 16.92% year-on-year. Detailed results are due on 14 August.

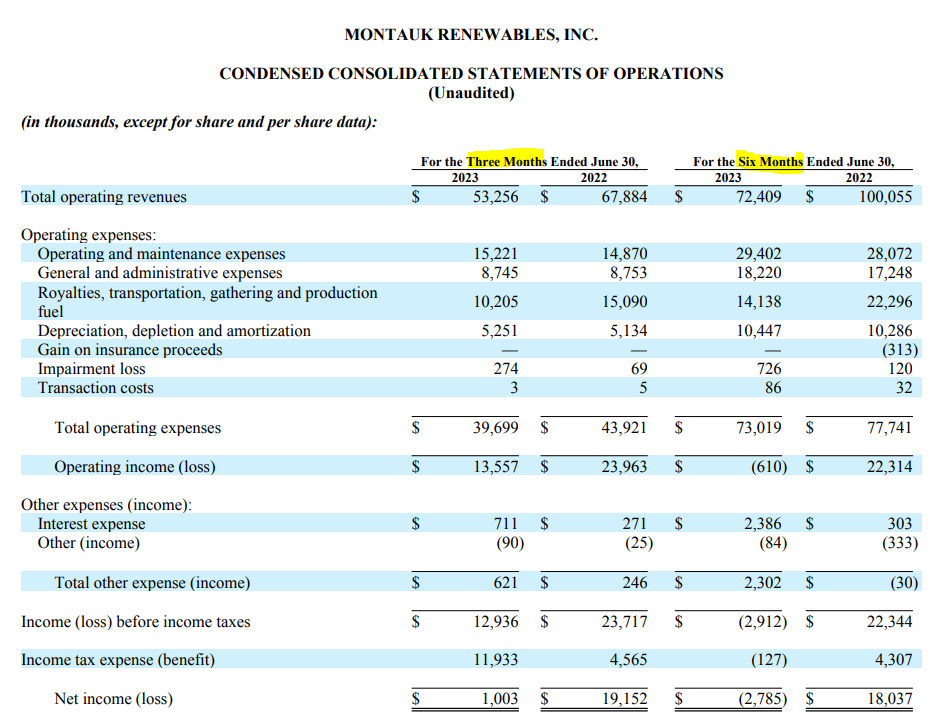

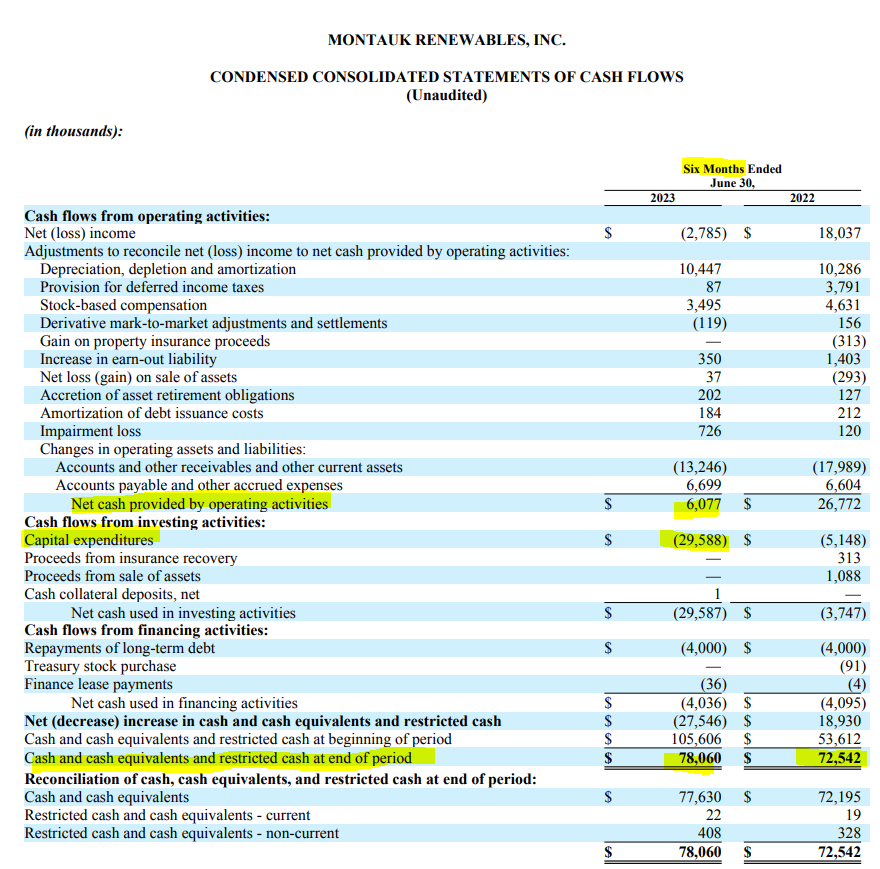

An interim loss at Montauk, but a better quarter (JSE: MKR)

There has also been extensive capex in this period

Montauk Renewables is listed on the NASDAQ in addition to the JSE, so the company reports earnings every quarter. When you see a huge swing in interim headline earnings from $0.13 to -$0.01, you can dig into the quarterly results to figure out why.

In there, you’ll find an income statement in this format:

As you can see, this lets you see the latest quarter as well as the six-month period. Although this quarter was profitable, it wasn’t enough for the performance over six months to be in the green.

This business is very much in growth phase, which is why capital expenditure was $29.6 million in this interim period despite cash from operations being only $6 million. As the group came into this period with a lot of cash on the balance sheet, this brought the net cash balance down to where it was a year ago. Here’s how to spot the information that I just gave you:

Unsurprisingly, there’s no dividend.

In other news, Montauk continues to develop its project pipeline. The latest is an agreement with Duke Energy for a waste-to-renewable energy facility in North Carolina, with Duke agreeing to buy electricity for 15 years. The electricity is being converted from swine waste of all things! Renewable electricity and renewable natural gas is an interesting space.

Little Bites:

Director dealings:

The CEO of Argent Industrial (JSE: ART) sold shares worth nearly R18k.

For completeness, it’s worth noting that Remgro (JSE: REM) told us what we already know thanks to Vodacom (JSE: VOD) on Tuesday – that the Competition Commission doesn’t like the transaction to combine Vodacom’s fibre assets with Vumatel and Dark Fibre in a new joint venture. Remgro sits on the other side of the deal to Vodacom, so a prohibition (if decreed by the Competition Tribunal) would hurt both companies.

In rather interesting news, Orion Minerals (JSE: ORN) managed to settle R5.3 million worth of advisory fees to advisor Webb Street Capital through the issue of shares at 18 cents per share. That’s a pretty big discount to the current price of 27 cents but it does say something about their belief in the company as its advisor.

Although I’m simply picking on Spar (JSE: SPP) here because it’s a fresh example, I really do wonder how a fee like R2.76 million to the Chairman of the Board can be justified. The cost of running a corporate board is just extraordinary and it’s very debatable whether there is a net benefit to the company or its stakeholders from such bloated boards full of committees and independent directors. Of course, the counterargument is that directors carry a lot of risk, so they need to be paid accordingly. The system just feels inefficient to me.

African Equity Empowerment Investments (JSE: AEE) has been in dispute for a while with BT Limited. The dispute went to arbitration hearing in July and the parties are now working towards a settlement.

After PKF Octagon was not reappointed by shareholders as the auditor of Acsion Limited (JSE: ACS), the company will need to propose a new auditor. We don’t yet know who that will be.

Kore Potash has raised $0,8 million through the issue of 124,384,000 new ordinary shares. The proceeds will form part of its US$5 million commitment as per the Engineering, Procurement and Construction (EPC) contract for the construction of the Kola Potash Project.

Orion Minerals has issued 29,652,776 shares for a total consideration of A$444,792. The shares were issued to Webb Street Capital in lieu of fees owed by Orion for services provided.

Invicta announced the results of the odd-lot offer to the 1,510 ordinary shareholders on the share register holding less than 100 Invicta ordinary shares. The company repurchased 37,501 shares for a total consideration of R1,12 million.

Calgro M3 has repurchased 4,024,601 shares during the period 29 June 2023 to 7 August 2023. The shares, representing 3.30% of the issued ordinary share capital of the company, were repurchased for an aggregate R12,97 million. The shares will be delisted and cancelled.

Glencore has announced the commencement of another programme to repurchase the company’s ordinary shares on the open market for an aggregate value of $1,2 billion with the intended completion by February 2024. The company repurchased a further 1,930,000 shares for a total consideration of £8,79 million this week. In its half year report, Glencore advised it would distribute c.$1 billion ($0.08 per share) by way of a special cash distribution to shareholders.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 31 July – 4 August 2023, a further 2,269,254 Prosus shares were repurchased for an aggregate €159,6 million and a further 473,244 Naspers shares for a total consideration of R1,65 billion.

Reunert shares will be admitted to trade on A2X as a secondary listing with effect from 15 August 2023.

Four companies issued profit warnings this week: Impala Platinum, Cashbuild, Glencore and Lighthouse Properties.

Two companies issued or withdrew a cautionary notice: African Equity Empowerment Investments and Life Healthcare.

DealMakers is SA’s M&A publication. www.dealmakerssouthafrica.com

Egypt’s B2B digital pharmacy marketplace, Grinta, has announced the acquisition of Auto-Cure. Financial details of the deal were not disclosed. Since launching in 2021, Grinta has made two acquisitions (PH Store and EME) and has raised US$8 million in seed funding (November 2022).

AI recruitment company, Talents Arena, has raised US$750,000 in pre-seed funding from UI Investments and several angel investors. The Egypt-based firm is a Flat6Labs portfolio company and an alumnus of the Plug and Play startup accelerator programme. The funds will be used to accelerate the AI hiring engine and expand its footprint in the Saudi market, which already makes up 25% of its client base.

Moove, the mobility fintech founded in Nigeria, has announced that it has raised additional funding to help with its global expansion plans. The US$76 million raised comprises $28 million in equity from new and existing investors, $10 million in debt and $38 million raised in the last year (not previously disclosed).

A15 has led a seed funding round with participation from group of angel investors, in Egypt’s Buguard. The US$500,000 investment will help the cybersecurity startup grow its team – this is the company’s first external fundraise.

Rwanda’s SOUK Farms has received an undisclosed investment from Goodwell Investments’ uMunthu II fund. The funding will provide SOUK, a grower and exporter of fresh horticultural produce from Rwanda, the capital it needs to scale up its operations.

Airtel Africa announced that its wholly owned subsidiary, Airtel Uganda intends to list on the Main Investment Market Segment of the Uganda Securities Exchange. The initial public offer will consist of 8,000,000,000 ordinary shares, representing 20% of the company.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")