Thungela’s one year share price return is 750%. Those who bought shortly after the unbundling from Anglo American in early June 2021 have made an even bigger killing, sitting on a position that is over 10x more valuable than the entry price. Yes, just one week makes that much of a difference!

The coal mining group has released a pre-close update and trading statement for the six months ending June 2022. The share price fell 9.8% on the day, a significant drop even in the context of a horrible day in the markets.

Headline earnings per share (HEPS) for this period is expected to be at least R58.00, a massive increase vs. the comparable period of R3.05.

Thungela has benefitted from a high average benchmark coal price, part of the overall increase in energy costs that has swept the global market. Because doing business in South Africa is never easy, this benefit has been partially offset from the poor rail performance from Transnet Freight Rail. We can’t export coal if we can’t get it to the port.

The average benchmark coal price in this period has been $266/tonne vs. just $98/tonne in the comparable period. Thungela notes that prices have been extremely volatile with large daily fluctuations.

Export production is 14% lower than the comparable period, a direct result of a decision to curtail production in certain circumstances to mitigate the impact of an inconsistent rail performance. Dankie, Transnet.

The unit cost of production per tonne (excluding royalties) has jumped from R787 last year to R957 in this period, significantly higher than the full year 2022 guidance of R850 to R870. Guidance has not been restated as the increase in unit costs is largely due to the impact of lower export production.

The full year guidance assumes an improvement in export production in the second half of the year. This depends on Transnet improving its performance by around 9% over the remainder of 2022, which is right up there with believing in the Tooth Fairy as an adult.

I hope that I’ll be proven wrong.

Capital expenditure for this period is around R0.5 billion. The group has a net cash position of R15.3 billion, so there’s no shortage of money running around to fund this. A liquidity buffer at the upper end of the range of R5 billion to R6 billion is being maintained.

The resolution to authorise share buybacks was not passed at the AGM, so Thungela will return cash to shareholders via dividends. The targeted minimum pay-out ratio is 30% of adjusted operating free cash flow.

An interim dividend will be declared in August and there’s much speculation about how high it might be. I’ve seen guesses on Twitter of between R45 and R55 per share. With a closing price of R223 per share, that’s a rather gigantic potential dividend. Of course, we won’t know for sure until August.

For those who bought shares in Sirius Real Estate towards the end of 2021, it’s an excellent example of bad multiples happening to good people. When it comes to property funds, you need to tread carefully whenever the share price is at a premium to the net asset value (NAV) per share.

This year, Sirius has lost over 31% of its value. It’s worth showing a chart of what happens when the market gets carried away:

What goes up, sometimes comes down.

This isn’t a reflection of the underlying business, which achieved an accounting return in the year ended March 2022 of 20%. This is a great follow-on performance after achieving 19.5% in FY21. A primarily logistics and industrial property strategy has been lucrative during the pandemic, especially as retail and especially office properties faltered in comparison.

The issue for investors is that the share price ran too far ahead of the underlying assets. The reason why NAV per share should be your anchor for a property fund is that the properties are usually carried on the balance sheet at fair value, not historical cost. The NAV per share is a reasonable indication of what the outcome for shareholders would be if all the properties were sold and all the debts were settled.

Note: this isn’t the case for US property funds that report based on US GAAP, as we examined in Simon Property Group when we analysed it in Magic Markets Premium. For funds that report under IFRS though, NAV per share is important.

Sirius clearly achieves returns that are ahead of the market average, or the level that investors could reasonably expect from a property fund. This helps to justify a premium to NAV. The issue is the extent of the premium and the price action in the chart above clearly tells the story.

Stepping away from the share price and focusing on the core business reveals that Sirius made some big moves in this period. The fund committed €200 million for acquisitions in Germany and splashed out £380 million for the acquisition of BizSpace in the UK.

Sirius issued corporate bonds of €700 million and brought down the weighted average cost of debt to 1.4%. Tread carefully though, as the loan-to-value (LTV) has jumped from 31.4% to 41.6% which is on the high side.

There’s strong like-for-like growth in rent in Germany and UK, which investors will hope can continue. This has supported a juicy increase of 16.1% in the dividend this year to €0.0441 per share. This works out to around R0.75 per share, a trailing yield of 3.6%.

Investors should note that the fund’s policy is to pay 65% of Funds From Operations as a dividend.

The NAV per share increased by 15.5% to €1.0204, or R17.13 at the exchange rate at time of writing. After closing at R20.78 the share is still trading at a premium of over 21% to the NAV.

This is a far more reasonable premium than we saw in 2021. Still, a dividend yield of 3.6% is low (which means the share price is high) and Sirius is still trading at a demanding valuation. I don’t hold a position in this stock.

“Reduced losses in the Rest of Africa (RoA), a rebound in advertising revenues and a continued focus on cost containment enabled us to absorb the R1.1bn impact of a normalisation in content costs as live sport returned and we resumed our local content production post the COVID-19 lockdowns,” says Calvo Mawela, Chief Executive Officer.

“We continued to enhance our video entertainment offering and expanded the variety of services offered to our customers as we grow our entertainment ecosystem,” he added.

The group’s linear pay-TV subscriber base (measured on a 90-day active basis) increased by 0.9m to reach 21.8m households, comprising 9m in South Africa and 12.8m in the RoA. The 5% growth year-on-year (YoY) is subdued due to the tough economic environment and elevated subscriber growth during COVID-19 related lockdowns in the previous year.

Here are a few highlights:

Revenue: ZAR55.1bn up 3% (up 7% organic)

Trading profit: stable at R10.3bn (up 1% organic, due to absorbing cost normalisation)

Core headline earnings: R3.5bn (up 6% as Forex impact was less negative))

Free cash flow: R5.5bn (down 3%, due to one-off prepayments)

Dividend: R2.5bn 565 ZARc per share (±4% yield)

MCG continued to pursue its differentiation strategy through local content, stepping up its local content production by 32% YoY to 6 028 hours and bringing its local content library close to 70 000 hours. Local content accounted for 47% of total general entertainment content spend and the group remains on track to achieve a target of 50% by 2024.

Seven major new channels launched, including two Portuguese-focused channels in Angola and Mozambique. In South Africa, the group’s co-productions such as Reyka and Recipes for Love and Murder were broadcast to critical acclaim and international interest.

SuperSport delivered world class productions given a bumper calendar of major sporting events. A record number of viewers tuned into Euro 2020, the British and Irish Lions rugby tour and the Tokyo Olympics. SuperPicks, a free-to-play predictor game and the group’s first product collaboration with KingMakers, was launched in Nigeria in August 2021 and already has 0.5m registered users.

SuperSport Schools, now 100% owned by the group, continues to grow rapidly and broadcasted 5 249 live games of schools sport during FY22.

Growth in Connected Video users on the DStv app and Showmax service is outpacing the market. Paying Showmax subscribers were up 68% YoY, whilst overall monthly online users of the group’s connected video services increased 28% YoY. A major driver has been the focus to localise by expanding local payment channels and enabling local billing in various markets. In addition, local content was stronger than ever with titles like DevilsDorp, the Real Housewives franchise and The Wife. Showmax Pro delivered an enhanced customer experience, which included the Tokyo Olympics, Euro 2020 and every English Premier League game.

On the product side, the announcement of DStv as official launch partner of Disney+ in South Africa is a further extension of the group’s aggregation strategy, which aims to bring customers more content, and convenient access in one central place via DStv’s connected devices.

DStv Internet, which was launched in September 2021, is growing strongly. The DStv Rewards program, which supports customer retention and has been successful in reducing dormancy, continues to gain traction with close to a million customers. Digital adoption continues to track well with around 75% of customer touch-points now being managed through the group’s self-service channels. Due to the ongoing global silicon chip shortage the DStv Streama launch has been delayed and is now expected to launch in the first half of the next financial year.

SEGMENTAL REVIEW

South Africa

The South African business faced an increasingly difficult consumer climate, with FY22 growth rates impacted by rising unemployment levels, intermittent loadshedding and a disruption caused by the July riots in Durban and Johannesburg.

Revenue increased 4% to ZAR35.6bn, supported by the rebound in advertising revenue and a 1% increase in subscription revenues, driven by subscriber growth in the mass market and the uplift from annual price increases. The return of live sport and other value adding initiatives contributed to reducing churn in the Premium base relative to the prior year. Trading profit declined 1% to ZAR11.0bn as the ongoing cost-optimisation programme only partially offset consumer pressure in the middle market and the normalisation of content costs and sales and marketing expenses.

Rest of Africa (RoA)

The Rest of Africa business benefited from the popularity of local content such as Big Brother Naija and live sporting events. Whilst revenue of ZAR17.9bn reflects a strong 14% organic increase, it is only 4% higher than the prior year due to the impact of translating Rest of Africa’s USD revenues at a stronger ZAR for reporting purposes. Trading losses amounted to ZAR1.2bn, which is a 24% improvement YoY on an organic basis. Local currencies held up better against the USD than prior years, resulting in an overall headwind on reported results of only ZAR0.1bn (FY21: ZAR1.2bn). Although liquidity challenges continued in Nigeria, the group successfully repatriated cash throughout the year, albeit at a premium to the official exchange rate.

Technology segment

Irdeto, was impacted by global silicon shortages affecting supply chains, as well as COVID-19 related disruptions in large markets such as India. Revenues of ZAR1.5bn, down 17% YoY (9% organic), were further depressed by the impact of a stronger ZAR upon translation from USD. The segment contributed ZAR0.5bn to group trading profit with margins strong at 33%. Irdeto gained additional market share in its core media security business by winning four new Tier-1 customer. It also grew its device security business, expanded its deployment of connected vehicles with Hyundai, and started new projects like providing security software to large logistics companies.

KingMakers

On 29 October 2021, the group increased its shareholding in KingMakers from 20% to 49.23%. KingMakers delivered USD136m (ZAR2.0bn) in revenues, representing robust growth of 74% YoY. It recorded a loss after tax amounting to USD19m (ZAR0.3bn) as increased revenues were offset by investment in people, product and technology to further scale the business. Although revenues are still primarily generated in Nigeria, the group is now also active in Kenya, Ghana and Ethiopia.

FUTURE PROSPECTS

In the year ahead, the group will continue to drive penetration of its video entertainment services across the African continent by offering customers an array of unique and rich media content delivered in a convenient and cost effective way. Local content and select sporting events such as the English Premier league, UEFA Champions League and the 2022 FIFA World Cup will contribute to the growth in linear and streaming services.

Returning the Rest of Africa business to profitability in FY23, maintaining strong cash flows to support a healthy balance sheet and pursuing innovative products and services remain key pillars for long term value creation.

“As a platform of choice, our group will look to further expand our entertainment ecosystem by identifying growth opportunities that leverage our scale and local capabilities,” says Mawela. “We will continue to strive to be a trusted partner for our customers’ ever-evolving needs, enriching their lives by delivering entertainment and relevant consumer services underpinned by technology.”

Note: this article has been placed by MultiChoice Group to provide information to market participants and does not reflect any analysis or views from The Finance Ghost.

Until fairly recently, investing in China via Naspers as a proxy for the underlying Tencent business was very profitable for South African investors. However, the Naspers share price has more than halved in the past 15 months in line with the falling value of Tencent (I won’t get into the byzantine debate about whether Naspers or Prosus is the greater or lesser of two evils). Now many people are wondering whether or not it is worth getting back into Tencent or Chinese tech stocks generally.

That question is probably best answered by acknowledging that the best returns from these stocks are probably over and although they may have some interesting trading opportunities ahead, the old adage of caveat emptor strictly applies to investment in China generally. It is not for the faint-hearted.

Many years ago, a captain of South African industry told me that if I could spot paradigm shifts taking place before they became common knowledge, then as an investment analyst I would steal a march on my competition. That was very sage advice and remains as relevant today as it was in the 1980s and 1990s. Arguably the largest paradigm shift in the global economy these past thirty years has been the inexorable rise of China from being a relatively insignificant, though vocal society under Mao Zhedong into the world’s second largest economy.

Conventional wisdom tells us that China will soon overtake the US as the leading global economy and that the world will shift from being a unipolar economy, dominated by the US to being something more akin to a bipolar or even multipolar situation with China being at the top of the pile. But that view of the world has been shaken to the core with the impact of the Sars-CoV-2 pandemic and the rapid de-globalization that has set in during the past three years. In this article, we examine how China may evolve in a low growth, de-globalized economy and where the Chinese population is actually declining for the first time in a generation.

Ever since the early 1990s. China has been seen as the great land of investment opportunity. Its strong, sustained economic growth initiated by Deng Xaio-Ping in 1979 has been hailed by many observers as nothing short of miraculous. The country has been transformed from a largely agrarian society into a modern, relatively developed state. And during this time, the Chinese Communist Party (CCP) has managed to hold onto power, with its rather unique brand of state capitalism, that allows a degree of free enterprise to co-exist. But global and local dynamics are changing rapidly and the conditions that helped create the world’s second-largest economy are disappearing rapidly.

The CCP knows this and is desperately trying to keep the Chinese economy moving at a rapid pace, but the odds are definitely against it. The combination of de-population and de-globalization coupled with the fact that the Chinese economy is maturing means that we should not expect to see Chinese GDP growth of much more than 2% to 3% on average in future.

The Lewis Turning Point

Much of China’s strong economic growth in the 1980s, 1990s and into the first few years of the new millennium was predicated upon the vast movement of people from the rural to urban areas. In a seminal working paper for the IMF in January 2013, authors Mitali Das and Papa N’Diaye postulated that China would reach the Lewis Turning Point and from there would experience a precipitous decline in GDP growth.

The following extract is from the executive summary:

“China’s large pool of surplus rural labour has played a key role in maintaining low inflation and supporting China’s extensive growth model. In many ways, China’s economic development echoes Sir Arthur Lewis’ model, which argues that in an economy with excess labour in a low productivity sector (agriculture in China’s case), wage increases in the industrial sector are limited by wages in agriculture, as labour moves from the farms to industry (Lewis, 1954). Productivity gains in the industrial sector, achieved through more investment, raise employment in the industrial sector and the overall economy. Productivity running ahead of wages in the industrial sector makes the industrial sector more profitable than if the economy was at full employment and promotes higher investment. As agriculture surplus labour is exhausted, industrial wages rise faster, industrial profits are squeezed, and investment falls. At that point, the economy is said to have crossed the Lewis Turning Point (LTP).”

Average wages in China have risen by around 12 times since 2000 but labour productivity has only risen by a factor of 2 to 3 times, suggesting that China has reached the LTP. The LTP is a well-known and documented economic phenomenon and has occurred in most developed countries at some point in time. In China’s specific case, it has been badly exacerbated by the impact on population of the disastrous one-child policy, also introduced by Deng in 1979.

De-population

The one-child policy persisted from 1979 until 2016, during which time it was ruthlessly prosecuted, especially in the urban areas. The CCP finally woke up in 2016 when the one-child policy was revised to allow two children and then again in May 2021 to the current situation that permits three children. But the damage has been done. Chinese couples are no longer interested in having large families. Their priorities lie elsewhere as they rapidly urbanise.

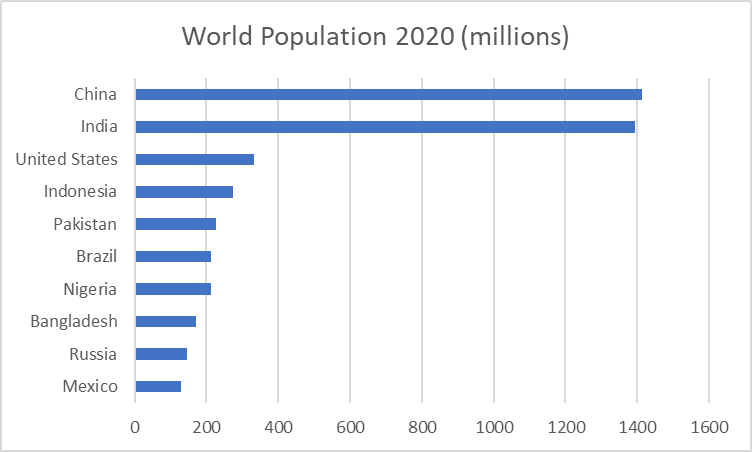

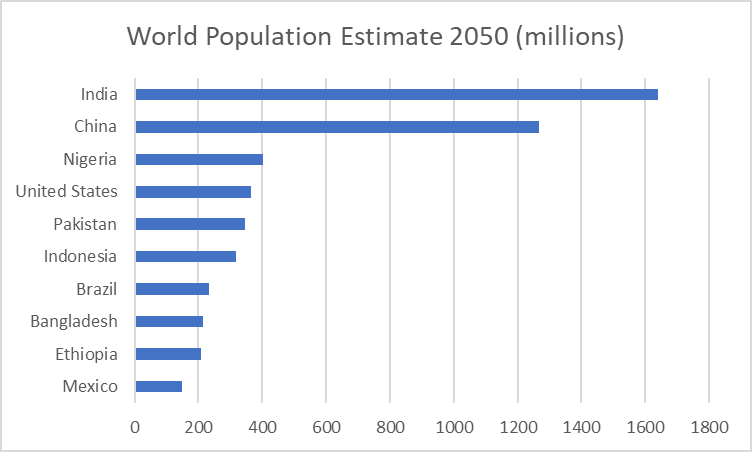

As can be seen from the two charts from the Population Reference Bureau below, China’s population is forecast to fall from just under 1.4 billion people in 2020 to just over 1.2 billion in 30 years’ time. By that time, India will have by far the greatest number of people. And this is probably a very conservative estimate. The Shanghai Academy of Social Sciences predicts an annual average decline of 1.1% after 2021, pushing China’s population down to 587 million in 2100, less than half of what it is today. Controversial billionaire Elon Musk recently tweeted that he believes China will lose around 40% of its population in a generation if present birth rates continue.

It is therefore no exaggeration to say that China has the world’s worst demographics.

Source: Population Reference BureauSource: Population Reference Bureau

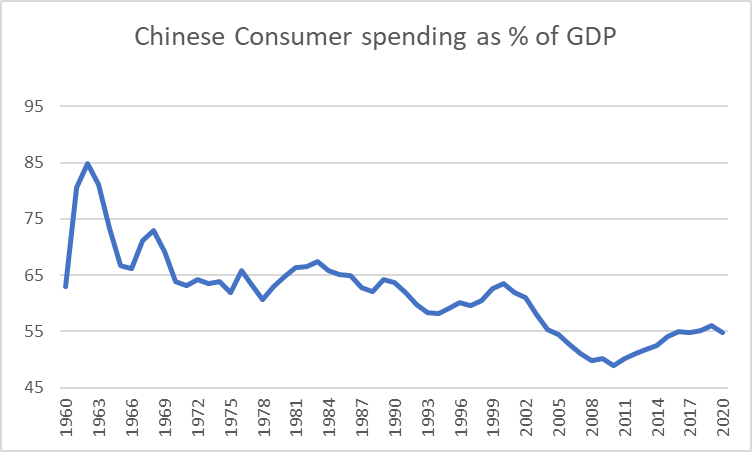

Normally this wouldn’t be a train smash as in most developed countries, the trend is a move away from heavy manufacturing and into services, with the emphasis being on consumer-related activities. But in China this is a problem, as China’s consumption to GDP ratio is probably the lowest of any large economy in the world. The reasons are many and varied but right near the top is a very high savings ratio due to huge uncertainty surrounding pensions, healthcare and education costs. So this cohort has had to put precautionary money aside over many decades just to feel secure in old age. In other words, they have deferred consumption in favour of personal welfare spending. And until the CCP takes concrete steps to greatly improve social welfare programmes, this phenomenon will likely persist.

The following graph shows that Chinese consumer spending as a percentage of GDP has been in secular decline since 1962 and shows no signs of reversing direction.

Source: World Bank

De-globalisation

Globalisation – that process by which the world became increasingly interconnected due to greatly increased trade and cultural exchange – is under threat and soon may no longer exist as we currently understand the term. On balance, globalisation has been a force for good over many years and has helped over a billion people pull themselves out of poverty. Additionally, improved trade and information links with the growing middle classes in autocracies such as China and Russia have sustained the cause of liberalism, thanks mainly to globalisation.

If globalisation were to retreat into something more akin to what we endured during the Cold War period between 1945 and 1990, it would indeed be tragic. But unless the free world starts changing its attitudes to autocracies intelligently, that could be the outcome in a few years’ time.

Globalisation has been happening for hundreds of years, but has quickened dramatically in the last half-century, notably with the extermination of communism in eastern Europe and the USSR from the late 1980s and the Chinese economic miracle since the late 1970s. The most noticeable impacts have been in the areas of greatly enhanced international trade, the emergence of a plethora of true multinational companies, freer movement of capital, goods, services & people (as in the case of the European Union), a greater dependence of the global economy in terms of outsourcing and insourcing and recognition of companies such as Amazon, Facebook, Twitter, McDonald’s, Google and others in less economically-developed countries.

Globalization’s heyday was 30 years from the mid-1980s onwards, when outsourcing of manufacturing to less developed countries in far east Asia, especially China, really took off. But that is now evaporating and the trend has been exacerbated by the impact of the coronavirus pandemic, as progressively more and more developed countries begin on-shoring and moving away from these formerly low-cost manufacturing jurisdictions.

The impact of globalization on China is nicely encapsulated by the Chinese journalist Ma Jun who said:

“Globalisation has powered economic growth in developing countries such as China. Global logistics, low domestic production costs, and strong consumer demand have let the country develop strong export-based manufacturing, making the country the workshop of the world.”

The Cult of the Personality

The most successful era of Chinese economic growth has been under collective leadership. But the current leader, Xi Jinping wants to consolidate power under his authority alone and to that end is seeking a third term in office at the 20th CCP Congress in October this year. Xi wants his legacy to rival that of Mao Zhedong, the founder of the People’s Republic of China. And while Mao’s reign, if viewed dispassionately, was hardly a roaring economic success, Mao is still held in extremely high regard. Xi knows this and is keen to preserve a legacy that matches Mao’s, regardless of the economic realities.

Under Xi’s leadership, China has effectively been under stop/start lockdowns in various parts of the country for over two years. It has adopted a slavish adherence to a so-called “Zero-Covid” policy that common sense dictates cannot be won. In the early stages of the pandemic, Chinese vaccines were relatively effective against the original Wuhan strain of the virus but against Delta and especially Omicron, they are largely useless. So the CCP has resorted to ordering massive lockdowns of entire cities such as Shanghai to attempt to eliminate the virus, to little or now avail.

Meanwhile, Chinese industry is suffering, as Chinese supply chains take the strain as more and more countries start on-shoring away from China. The solution to this problem is glaringly obvious to anyone not blinded by political dogma: import the required western vaccines (probably mRNA ones from Pfizer or Moderna). That would be regarded as failure on the part of the Chinese state. Xi is personally identified with the Zero-Covid policy and any criticism of the policy is seen as criticism of him and that is not acceptable in the totalitarian Chinese state.

Another area where Xi has fallen is in his so-called “Common Prosperity” and “Dual Circulation” visions, which have mainly arisen since the start of the US trade wars. In a nutshell, these policies aim to tackle inequality, monopolies and debt and to turn China into a type of fortress against any further possible trade tariffs or sanctions. All of these will be dictated from a central government level, with all the accompanying bureaucracy and red tape.

Until very recently, China had a flourishing tech sector that was about to overtake that of the acknowledged leader, Silicon Valley in the US. But Xi has changed all that with his ruthless crackdowns on this sector, using all sorts of flimsy excuses for clipping its wings. In a re-worked state capitalist system with a demagogue at the helm, there can be only one voice and that voice is Xi’s.

And then to top it off, Xi wants to increase the role of state-owned enterprises in the economy and use more debt to expand its already large footprint. Bottom line is that under Xi’s envisaged third term in office, he will ensure that ideology trumps good business sense. Meanwhile investors have voted with their feet. The CSI 300, a broad measure of stocks listed on the Shanghai Stock Exchange, is deep in bear territory, having fallen some 28% from its February 2021 peak. This is substantially worse than the Nasdaq or S&P 500 and the decline set in much sooner.

Investors may be making a gradual return to China but it is likely to be a slow process and it still remains unclear how much autonomy, if any, will be available to Chinese tech companies when it comes to running their businesses. What is clear is that there is an inexorable move to the left in Chinese politics and a much greater role for the state in future. But, that in itself doesn’t necessarily make China un-investable.

However, what it does mean is that investors should not expect that same degree of return that they have experienced in the past and that they should also view Chinese investment with a high degree of healthy skepticism.

Taiwan

Following Russia’s disastrous invasion of Ukraine, many observers have begun speculating about the possibility of China doing a similar thing with Ukraine. But there are major obstacles, both physical and financial, that China would need to overcome if it was to be assured of victory in a Taiwan invasion.

The first point to note is that China was probably watching the west’s reaction to Russia’s invasion of Ukraine to see if it could pull off a similar exercise against Taiwan and not get heavily sanctioned for it. China must have been incredibly surprised at a) the cohesive sanctions applied by the west against Russia in response and b) the degree to which the Russian military failed to gain a decisive victory in Ukraine.

Taiwan is altogether different to Ukraine from many angles.

Firstly, while Ukraine has only been preparing for war since 2014, Taiwan has effectively been on a war footing with China since 1949. Secondly, while Russia was able to literally drive its tanks and heavy weaponry straight into Ukraine, a Chinese invasion of Taiwan would be considerably more difficult from a logistical perspective. And then finally, an armed invasion of Taiwan by China would be met by stiff sanctions from the west, if the Russia/Ukraine conflict is anything to go by.

While most countries respect China’s One-China policy with regards to Taiwan, they would expect a peaceful, negotiated conclusion to this policy and would have no truck with an aggressive invasion of the island. Sanctions against China would likely be far more effective than those currently deployed against Russia. While Russia is self-sufficient in fuel and food, China is certainly not and has to import around 85% of its food requirements. Energy, too, is largely imported.

So, China could be crippled quite quickly in the event of comprehensive sanctions being applied. China also desperately needs to be part of the global community, regardless of Xi’s efforts at Dual Circulation. If access to the outside world were cut off, China’s balance of payments would deteriorate rapidly.

The Foschini Group (TFG) is a retailer on a mission. With a strong push into local supply chains and encouraging growth in the business, it seems like TFG just can’t put a foot wrong. The group has now released its results for the year ended March 2022, reflecting group revenue growth of 29.7% and HEPS growth of a ridiculous 409.9%. Of course, when you see a number like that, you need to look at prior years as well. I provide that analysis and far more in this feature article on TFG’s latest results.

Tongaat Hulett needs to recapitalise the business and the planned investment from Magister Investments has been forced by regulators to hit the brakes. The Takeover Regulation Panel (TRP) has ruled that a previous waiver for a mandatory offer is a nullity. In simple terms, this means that Magister would have to be in a position to acquire the entire company if it supports the recapitalisation in the way currently envisaged. Magister has applied to the Takeover Special Committee for a hearing regarding the TRP’s ruling. Tongaat itself has decided not to appeal the ruling and will abide by the decision pursuant to Magister’s request for a ruling. Tongaat also notes that it is engaging with a “range of stakeholders on a sustainable capital structure” – exactly what the directors should be doing. As a final potential twist, there’s also no guarantee that Magister would walk away if the hearing doesn’t go well. Anything is possible here.

Industrials REIT has released results for the year ended March 2022. With a portfolio of industrial property assets (obviously) and a loan-to-value of just 25.6%, this fund is sitting in a great position. Occupancy is 93.6% and the portfolio valuation increased by 19.4% on a like-for-like basis. Although the accounting return was a record 25%, the full year dividend of 6.85 pence per share is only slightly higher than 6.75 pence in the prior year. This puts the fund on a trailing yield of 3.9%. The share price is down 11% this year and is trading at almost exactly the EPRA NTA per share, which is a European methodology for measuring Net Tangible Assets per share.

BHP shareholders (like me) can expect to receive the dividend related to the sale of Woodside Energy shares on 20 June. As a quick reminder, BHP sold its petroleum business to Woodside in exchange for shares which were then unbundled to those shareholders who qualify to hold the Woodside shares. As Woodside isn’t listed on the JSE, most South Africans will be paid out in cash generated from the sale of Woodside shares on their behalf.

Since November 2021, Motus has repurchased 6.1448% of shares in issue at an average price of R104.2951 per share. The share price is currently R110.90 so this seems to have been a successful strategy. The total value of the share repurchases is over R1.2 billion.

RECM and Calibre has released a trading statement based on change in net asset value (NAV) per share rather than earnings, which is how investment holding companies measure performance. The NAV per share will decrease by between 30% and 35% but this is due to the unbundling of shares in listed company Astoria Investments. When measuring based on NAV, any unbundlings to shareholders will reduce the size of the company and hence the NAV.

The managing director of a division at Mpact has sold shares in the company worth around R1.15 million. Given the current boxing match underway between Mpact and Caxton, I felt that this deserved a mention.

Property development group Acsion Limited has released results for the year ended February 2022. Revenue increased by 29% and HEPS jumped by 47.91%. A dividend of 18 cents per share has been declared. There is very little trade in this stock and the share price is down nearly 20% this year, though a drop like that can often close just through the bid-offer spread when the stock trades again. It is very difficult to invest in illiquid stocks like these because of the bid-offer spreads.

Tradehold has extended the maturity date of its floating rate preference shares from 20 June 2022 to 31 August 2023. This helps the company meet medium-term working capital requirements.

An independent director of NEPI Rockcastle has acquired nearly R3.4 million worth of shares in the company. That’s a chunky investment.

Healthcare investment group RH Bophelo has released results for the year ended February 2022. The net asset value (NAV) per share increased by 5% and a maiden dividend of R0.15 has been declared. The share price is down 30% this year and is yet another example of an illiquid stock on the JSE.

Southern Palladium is hosting an investor webinar on Wednesday 15th June. If you are interested, you’ll find the registration details here. Someone got very excited with the trigger finger on Friday, buying 858 shares for R100 when the previous close was R25. You can see some crazy things in illiquid stocks.

Orion Minerals requested a trading halt on its shares ahead of an announcement before 15th June regarding a capital raising. This is an Australian Stock Exchange (ASX) rule, which is where Orion’s primary listing sits.

It was a busy week for retailers, with results out from Spar and Mr Price in addition to this result from The Foschini Group. Be sure to refer to those feature articles as well to get yourself up to date with the local retail environment.

The Foschini Group is famous for two things: stealing my future stock market ticker (JSE: TFG) and investing heavily in its local supply chain. The former makes zero difference to anyone except me and the latter has made all the difference to TFG shareholders in a time of incredible global supply chain pressures.

The numbers included in this update were known to the market before Friday, as TFG released a detailed trading update in May. This is important context to assessing the market reaction to the announcement.

An overview of the numbers

In the year ended March 2022, group revenue increased by 29.7% to R46.2 billion, supported by retail turnover up 31.6% to R43.4 billion. Online revenue is now 10.2% of retail turnover and increased by 11.7%, coming off a really high base in the pandemic.

Cash turnover is 79,9% of the group total. Everyone always talks about Mr Price being the cash-focused retailer with 86.1% of group sales being in cash, but TFG isn’t exactly far behind. TFG’s impairment allowance on its credit book has improved slightly from 20.7% to 19.1%.

The highlight for me in this result is the improvement in gross margin from 45.5% to 48.5%. That’s a substantial move, which the company attributes to lower inventory markdowns due to strong consumer demand and an increasingly efficient, local supply chain. At this rate, the local supply chain is becoming a significant competitive advantage in a sector that is fiercely competitive.

By the end of March, TFG traded out of 4,351 outlets. It was very interesting to see that 377 outlets were opened and 310 were closed, demonstrating a significant reshuffle of the store portfolio. The UK business now has a much smaller footprint, down from 801 outlets to 688.

Headline earnings per share (HEPS) has increased by 409.9%, which isn’t a number you’ll see often. At 1,009 cents per share, it is still below the FY20 number of 1,174.4 cents and the similar FY19 number of 1,187.1 cents. Whenever you see a ridiculous increase like 409%, you have to go back to older periods to see what the through-the-pandemic growth looks like.

Cash generated from operations of R8.2 billion means that around 17.7% of revenue is converted into cash that is then available for capital expenditure, debt reduction and dividends. This was assisted by a reduction in inventory days from 169 days to 153 days, further evidence of an efficient inventory management and procurement function.

Net debt of R1 billion is an historic low levels. After adjusting for the stupidity of IFRS 16 that ruins financial statements of companies that have many leases, the debt : EBITDA ratio is 1.3x.

A final dividend of 330 cents per share has been declared, adding to the 170 cents per share interim dividend. This puts the group on a trailing dividend yield of 3.75% based on Friday’s closing price.

Taking a deeper look at the operations

TFG operates in Africa, Australia and the UK. It hasn’t been easy to do business anywhere in the world in the past year.

In Australia and the UK, Covid-related restrictions continued to hit the group in this period. In South Africa, the group had to contend with the civil unrest which impacted 198 stores. 176 of these stores had been reopened by May 2022. SASRIA payments of R541 million have been received and the business interruption claim is still in progress.

In Australia, TFG’s revenue increased by 24% in local currency. This business now contributes 15.8% to group turnover. The UK business grew 57.3% in local currency and contributes 14.4% to group turnover. TFG Africa is just under 70% of group turnover and is therefore still the most important segment.

In TFG Africa (which includes South Africa), clothing is the most important category with a contribution of over 75% to turnover. Cellphones contributed 9.5% and homeware 7.4%. It’s interesting to note that cosmetics only increased by 8.2% for the full year, perhaps a function of ongoing hybrid work environments. People simply don’t spend as much money on “looking good” when they are staying home for the day!

Looking ahead: a differentiated model

TFG is excited about its acquisition of Tapestry Home Brands, the holding company for Coricraft, Volpes, Dial-a-Bed and The Bed Store. This ties in perfectly with TFG’s strategy to have a localised supply chain for TFG Africa and gain exposure to new product categories. The deal is currently going through regulatory approval processes.

The group thinks that supply chain disruptions will continue for most of the 2022 calendar year. With a strong balance sheet and the localised supply chain, TFG is well-positioned to cope with that.

It feels like TFG just can’t put a foot wrong, regardless of the tough conditions. Despite this, the share price is down nearly 13.5% over the past 12 months and is up just 8% this year. The share price closed 3.8% lower on Friday on a red day for the market.

With a closing share price of R133.24 on Friday, the trailing Price/Earnings multiple is 13.2x. A cursory glance at TIKR suggests that this is similar to pre-pandemic averages. There’s a lot of macroeconomic pressure but TFG has made huge strides in strengthening its business.I don’t hold a position in the stock.

African Rainbow Capital Investments (ARC Investments for our collective sanity) holds a highly diversified portfolio of investments. It’s notoriously confusing to know what is going on, as there is also a private investment holding capital called African Rainbow Capital and in some cases they are invested alongside each other. The same key decision-makers sit behind both groups.

In the past 12 months, the ARC Investments share price is up 57.6%. Before you get carried away with excitement, it is 23.5% down since listing in 2017. I don’t know how many more times I need to warn people about the risks of investing in a brand new listing. They inevitably happen at the top of a market cycle and patience is almost always rewarded.

One of the irritations for investors has been the rather lucrative incentivisation structure for the executives. When the company listed, it noted that this would be reviewed after five years. A new structure will be reviewed at the AGM in November 2022 and the share price performance since listing isn’t a great way to tee up that conversation.

The company has released an “investment update” to let the market know what has happened since interim results for the period ended December 2021 were released.

Believing in yourself

Before we move into the underlying investments, it’s worth noting that ARC Investments is effectively investing in itself by purchasing its own shares. Between December 2021 and March 2022, R24.1 million worth of shares were acquired for R6.85 per share. That’s above the current price of R6.43 per share. Since inception though, total purchases of R353.8 million have been executed at an average price of just R3.59 per share, which looks much better.

A rain dance (and other interesting businesses)

It starts off with rain, the company that is big on internet and low on capital letters. No self-respecting tech startup ever uses capital letters, in case you haven’t noticed. The company invested R1.43 billion in spectrum in the recent spectrum auction, a major step that ARC believes will positively impact the valuation that will be prepared for the June 2022 reporting date. The update also notes that demand for 4G and 5G services remains strong.

Not all internet businesses are created equal, of course. ARC chose to dispose of its investment in Metrofibre for a total price of R275 million, achieving a gain of R37 million in the process. R244 million has already been received and the remaining R31 million is receivable in June 2022.

Afrimat needs no introduction, as this mining and construction materials group has one of the finest track records on the JSE. ARC sells down this stake to raise capital for other purposes. Between December and March, R244 million worth of Afrimat shares were sold for a profit of R132 million. ARC still holds a 7.3% shareholding in Afrimat.

ARC is invested in the Elandsfontein phosphate mine via Kropz Plc, which is listed on the Alternative Investment Market (AIM) in London. The AIM is like the local AltX on steroids, offering a place for smaller and less developed groups to list and raise capital. With slower-than-expected progress in commissioning the mine, ARC has extended further funding for working capital purposes. ARC is committed to seeing this one through to completion, based on strong market demand for phosphate and fertilizer.

An unsolicited offer has been received by ARC for the 11.1% stake in Humanstate and the 43.2% stake in Payprop SA. ARC seems to be taking the offer seriously, noting that it is “considering a potential divestment” of these stakes.

ARC holds a stake in Bluespec, which offers a number of IT and logistics solutions. ARC highlights that financial performance has improved after the pandemic hurt the business. It is “materially reducing” its debt, which is always a clue that a company has been through several rounds with a heavyweight boxer. Bluespec’s investment in digital vehicle bidding platform Weelee is gaining traction.

By being invested in Fledge Capital, ARC benefits from having another team running around finding deals. Fledge invested in WeBuyCars (now held by Transaction Capital) and has cash to invest. It has acquired 20% in sports nutrition manufacturer USN already. Boet.

Right idea, wrong Tyme?

The listed ARC entity holds 49.9% in the financial services portfolio. The remainder is held by the unlisted ARC entity.

In the financial services portfolio, TymeBank is embarking on an international growth strategy. The group plans to launch in the Philippines with a digital bank called GOtyme. I feel like there were many discussions around how to use capital letters in this one.

As an aside, the Philippines is where Purple Group is planning to expand EasyEquities, so it is fascinating to see both financial services disruptors identifying an opportunity in this market. To be clear, Purple Group has nothing to do with ARC.

Tyme is acquiring 130,000 customers per month in South Africa. That’s lovely, provided they actually use the accounts. The group is focused on increasing the number of active accounts, which is proving to be challenging in this economic environment. It doesn’t help to grow accounts that lie dormant.

Another very important investment in ARC is the stake in Alexander Forbes Group Holdings. The business has rebranded to Alexforbes and is a far more focused business these days. ARC Financial Services Investments holds 41.47% in the company. The ARC fund has an effective 20.7% stake in Alexander Forbes.

Rand Mutual Holdings may sound like the lovechild of leading financial institutions, but it has nothing to do with Rand Merchant Bank or Old Mutual. Rand Mutual is an insurance business that is implementing a five-year growth strategy and ARC seems to be happy with the progress.

After years of disappointing the market, performance over the past year has been strong. I personally find it difficult to invest in such a diversified group, as it becomes tricky to really form a view on underlying prospects. In these cases, the main question to answer is whether you are happy to back this management team to continue the recent run of form.

Your daily market overview delivered in bite-sized bullets:

Mr Price kicked off the day on SENS by releasing its FY22 results. Frankly, they were excellent. Value fashion (aimed at cost-conscious consumers) has been a great place to play in the past year. Mr Price has executed two major acquisitions (Power Fashion and Yuppiechef) with the deal to buy Studio88 in progress. I decided to take a detailed look at the numbers and the share price chart, whilst making a final decision on whether to have a punt at Mr Price.

There was much excitement around Mediclinic, with the share price closing 4.7% higher. The catalyst was Remgro (owned of 44.6% of Mediclinic) releasing an announcement before the market opened, responding to press speculation that it would be making an offer alongside MSC Mediterranean Shipping Company for Mediclinic. Apart from much head-scratching about why a cruiseliner wants to own a hospital group, the focus was on the price of 463 pence per share (inclusive of the 3 pence per share final dividend) that was put forward to the board of Mediclinic on 26 May and rejected as being too low. I had to look up the ticker of the London listing (LON: MDC) to compare this to the current price. Mediclinic closed at 441.7 pence, well below the rejected price. There is no guarantee that a higher offer will be made, so be careful speculating in the stock. Considering the long-standing relationship between Remgro and Mediclinic, it’s quite odd to see things playing out like this in public. The press speculation must’ve triggered this outcome.

Steinhoff subsidiary Pepco Group has released interim results for the six months ended March 2022. Revenue grew 18.9% and profit before tax jumped by 28.5%. Like-for-like sales growth was 5.3% for the period and 12.1% in Q2, so the cadence is strong. With record store openings, the group is pushing hard for growth. The market does note that Western European markets are experiencing an “acute spike in inflation in a stagnant wage growth environment” which has “quickly resulted in absolute lower spending by consumers” – not good news. Overall, the group’s like-for-like sales have risen above pre-Covid levels. To access the full result, download it here on the Pepco website.

Vukile Property Fund has released results for the year ended March 2022. The share price was trading 6% higher in late afternoon trade, which tells you what the market thought. In South Africa, like-for-like normalised operating income grew 3.9%, retail vacancies reduced to 2.6% and the like-for-like retail valuation increased by 4.6%. In Castellana (Vukile’s investment vehicle in Spain), there were positive reversions of 3.12% which is big news. This means that new leases are being concluded at higher rates than the leases being replaced. With a loan-to-value (LTV) ratio of 43%, debt is still on the high side for my liking, but the underlying story looks solid and the company describes the debt as being “well hedged” which helps in a rising rate environment. Of total funds from operations this year of 136.3 cents, the dividend was 105.8 cents. The net asset value (NAV) per share is R17.92. Trading at R14.44 at time of writing, the discount to NAV is 19.4% and the trailing yield is 7.3%.

British American Tobacco has delivered a pre-close trading update dealing with the first half of the 2022 financial year. The group knows that it probably can’t sell cigarettes forever, so the plan is to build the “New Categories” business up to GBP5 billion revenue by 2025. Simultaneously, the group is cutting GBP1.5 billion in costs out of the “combustibles” business i.e. cigarettes. This is a value stock of note, with FY22 guidance of revenue growth of 2% to 4%, some operating leverage bringing mid-single figure adjusted diluted earnings per share growth and cash conversion of over 90% of adjusted profit from operations. The group invested GBP1 billion in the New Categories business in the first half of the year, a segment that is still loss-making and is expected to stay that way for a few more years. One of my particular joys about the modern world is that British American Tobacco is a shining light when it comes to ESG metrics. It’s clearly not about where you’ve come from or what you even do to generate profits, but rather the progress you are making in being less harmful to people. Repent, sinner, and you’ll be included in our ESG Index.

Motus traded at nearly R117 immediately after releasing a trading statement, before the share price fell away over the day to trade at around R112 by close of play. The update shows growth in attributable profit of between 45% and 55%, with HEPS increasing by between 50% and 60% for the year ended June 2021. Improved availability of vehicles helped drive passenger vehicle market share of 23.6% for the period. The imported brands performed well, which has a knock-on benefit for workshop activity and parts sales. An important and related point is that higher usage of cars by owners as they return to work also drives increased demand for the workshops. On the car rental side, vehicle utilisation increased to 72%. Motus expects inventory supplies to normalise in the second half of the FY23 calendar year i.e. first half of next year. The group is well within banking covenants with a net debt : forecasted EBITDA ratio of 1.2x. The share price is 3.9% higher this year and is up more than 15% in the past 12 months.

MultiChoice Group released results for the year ended March 2022. Group subscribers increased by 5% year-on-year, with Rest of Africa growing 7%. There are 21.8 million subscribers in total and the South African business has 9 million subscribers, so Rest of Africa is larger with 12.8 million subscribers. Growth in South Africa was hit by consumers “prioritising video entertainment” which is a nice way of saying that people are cancelling DSTV and streaming instead. Subscription revenue increased by 5% and advertising revenue rebounded strongly, up 37%. Irdeto experienced a 9% reduction in revenue. Trading profit grew by just 1% as content costs from the prior year were deferred into this year, driven by the return of major sporting events. Consolidated free cash flow of R5.5 million was 3% lower year-on-year. It’s interesting to note that 47% of entertainment spend is on local content, which is a sensible strategy to compete against the streaming platforms. The dividend for the year was R5.65 per share, so the share price around R130 is a dividend yield of 4.3%.

Anglo American has signed a $100 million 10-year loan agreement with the International Finance Corporation (IFC) linked to sustainability goals. This is IFC’s first such loan in the mining sector and is also believed to be a global first in the mining sector that focuses only on social development indicators. Examples of targets include schools in the local communities performing well vs. national peers and the creation of three offsite jobs for every onsite job at Anglo American’s operations by 2025. If Anglo falls short of targets, it has committed to contributing additional funds to agreed social causes. You see, this is the kind of ESG that I can get behind.

As noted yesterday, Southern Palladium has officially listed on the JSE. The bid-offer spread of R30.00 – R90.00 isn’t a great start, but I can’t say that I was expecting much liquidity here. I suspect that most of the (limited) trading will happen on the Australian Stock Exchange, at least for now. After raising $19 million in the IPO, the company has appointing a drilling contractor with a two-phase program scheduled to commence in coming weeks at its 70%-owned Bengwenyama project. The local community holds 30% in the project and 12.3% in Southern Palladium as well.

Imbalie Beauty has released results for the year ended February 2022. Revenue was almost identical to the prior year and the headline loss per share improved by 83% (but was still a loss). A loan to survive Covid was provided by Absa but resulted in the company selling most of its assets, a process that was finalised in January 2022. Imbalie is going to change its name to Buka Investments and will be repositioning itself in the fashion industry.

It looks like Silverbridge Holdings may be sticking around on the JSE. Although there is an offer underway by ROX Equity Partners for R2.00 per share, the offer condition of a delisting has been dropped. This means that the company will stay listed provided not all shareholders accept the offer (as it then wouldn’t meet the spread requirements for a listed company with a minimum number of shareholders.

Texton Property Fund has a 50% held joint venture called Inception Reading, which has agreed to sell Broad Street Mall for GBP57.5 million (around R1.1 billion). The deal should close in June. Texton hasn’t given an indication at this stage what it will use the cash for.

The Chairman of the Board of York Timbers has resigned after 15 years in the role. He would’ve seen many things over that period, including the recent shareholder activism. A successor will be announced in due course.

Mahube Infrastructure is restructuring its wholly-owned subsidiary Mahube Capital Fund. A Black Fund Manager (as defined) will be created, which will then attempt to raise up to R2 billion for Mahube by the end of 2025. There are many more details in the announcement, so you should read it on the Mahube website if you are a shareholder.

In May, a consortium comprising Remgro and MSC Mediterranean Shipping Company proposed to the Board of Mediclinic International a possible cash offer to acquire the Mediclinic shares not already held by Remgro at a price of 463 pence (R88,43) per share. The proposal was rejected by the Board of Directors as it believed that the offer significantly undervalued Mediclinic and its future prospects. Remgro, which currently holds a 44.6% stake in Mediclinic, released an announcement this week following press speculation saying that following the rejection of the proposal the Consortium was considering its position and may make a further offer but reserved the right to do so at a lower value or on less favourable terms.

AfroCentric Investment subsidiary, AfroCentric Health, has acquired the remaining 49% stake in AfroCentric Distribution Services from WAD. The decision to bring the specialised marketing and sales company in-house stems from the critical role it performs in the Group’s growth strategy for medical schemes and the new generation products. The stake will be acquired for an aggregate purchase consideration of R75 million.

Heriot Properties, a wholly owned subsidiary of Heriot REIT, together with concert parties Heriot Investments and Reya Gola Investments, have made a general offer to Safari Investment RSA shareholders to acquire Safari shares. Together the concert parties hold 33.1% stake in Safari and are offering shareholders R5.60 per share. The Takeover Regulation Panel has confirmed that should acceptance exceed the 35% threshold, as a result of the general offer, the parties are not required to make a mandatory offer to Safari shareholders.

Santam has acquired the remaining 49% stake in JaSure, an app-based insurance provider for an undisclosed sum. JaSure has a younger market reach which Santam intends to leverage with its efficiencies and wider distribution capability.

The announcement in April by ROX Equity Partners of its intention to acquire all the issued shares in Silverbridge at R2,00 per share, has been amended to waiver certain of the offer conditions following the release of the independent expert report which concluded that the offer was unfair but reasonable. Delisting of the company will not be pursued and following the implementation of the general offer, the shares will remain listed on the JSE.

The mandatory offer by MCC Contracts and African Phoenix to acquire the remaining 62.23% of the shares in enX at an offer consideration of R5.60 per share closed on June 3, 2022. Only 103,371 enX shares were tendered representing 0.06% of the issued share capital. Following the transaction, the offerors will collectively hold 37.83% of the listed company.

Unlisted Companies

Crossfin Technology, a South African fintech group, has acquired a significant stake in payments and technology company Vantage Africa for an undisclosed sum. Trading as VantagePay, the cloud-based platform provides payment solutions to address the massive latent demand for access to trusted financial services in Africa.

Sonnedix Power, a global independent power producer, has disposed of its South African solar business which owns a 60% interest in the 75MW solar farm known as the Prieska Project in the Northern Cape. Financial details of the disposal to pan-African BTE Renewables were not disclosed.

Franc, a local fintech app, has raised R8 million in a seed extension round led by 4DX Ventures and has announced a B2B offering Franc Business, a low cost and easy way to invest app. The funds will, in part, fund this initiative.

Cape Town venture capital firm HAVAÍC has invested US$400,000 in Nigerian multi-channel retail company ShopEX. The retailer mobilises a combination of traditional and digital channels to market, sell and distribute successful and global brands in Nigeria and other African markets. The capital injection will allow ShopEX to scale its presence into new markets.

MFS Africa, a pan-African digital payment company, headquartered in Johannesburg, has, for an undisclosed sum, acquired US Global Technology Partners (GTP) in a deal which will scale the business to the next growth stage; widening its offering to Africa’s gig economy, the business travel market and millions of individuals through card credentials linked to mobile money wallets for secure online purchases. In addition, the deal will be used by MFS to leverage off GTP’s presence in the US to expand its activities in North America.

Tongaat Hulett’s recapitalisation bid suffered a setback this week with the Takeover Regulation Panel (TRP) retracting the exemption given for Tongaat to make a mandatory offer to shareholders. In mid-January the company announced its intention to raise R4 billion via a rights issue to reduce its massive debt. The transaction was to be underwritten by major shareholder Magister Investments and would likely have pushed its stake above the 35% threshold, triggering a mandatory offer to minorities. The waiver of the mandatory offer was a condition precedent to the Magister deal. Following an investigation by the TRP after a complaint, the changed ruling means the company/Magister would need to be able to acquire the entire company.

Oasis Crescent has issued a total of 725,159 new units in terms of its scrip distribution alternative amounting to R18,1 million.

Another miner has announced its intention to take a secondary listing on A2X, with Impala Platinum set to list on June 13, 2022.

The JSE welcomed the inward bound listing of Southern Palladium on June 8, 2022, after an initial delay. The company, which has also listed on the ASX, raised A$19 million in an initial public offering (IPO) which closed on May 6. The company floated 89.75 million ordinary shares of which 39.63 million will move onto the SA register. The share price closed its first day of trade on the JSE at R25,00 per share. Towards the end of the month, June 27, CA Sales will list 461,432,502 ordinary shares on the Main Board in the Diversified Retailers sector. The company will delist from the CTSE on June 24.

Lewis has repurchased 4,326,696 of its own ordinary shares, being 6.6% of its issued share capital at the onset of the repurchase programme. The shares were repurchased as price ranging from R42.69 to R52.00 for an aggregate R215,8 million.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

This week British American Tobacco repurchased 2,110,000 shares for a total of £75,19 million. The purchased shares will be held in treasury with the number of shares permitted to be repurchased set at 229,400,000.

Glencore this week repurchased 3,441,117 shares for a total consideration of £18,2 million in terms of its existing buyback programme which is expected to end in August 2022.

This week two companies issued profit warnings. The companies were: Multichoice and Nictus.

Three companies issued or withdrew cautionary notices to shareholders this week. The companies were: Hulamin, Safari Investments RSA and Nutritional Holdings.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

, Africa’s leading entertainment company, delivered steady margins for the year ended 31 March 2022 (FY22)")

")