Centum Investment Company has entered into a binding agreement with Access Bank for the proposed purchase by Access Bank of Centum’s entire 83.4% equity stake in Sidian Bank for KES4,3 billion. In due course, Sidian will be merged with Access Bank’s subsidiary in Kenya. The transaction is subject to regulatory approvals in Nigeria and Kenya.

Montage Gold, the Canadian precious metals exploration and development company, is to acquire 100% interest in the Mankono-Sissédougou Joint Venture Project in Côte d’Ivoire. The deal, with Barrick and Endeavour Mining, is for a total purchase consideration of C$30 million involving cash and shares.

Swiss-based Holcim’s subsidiary Associated International Cement is to dispose of its 76.45% stake in Lafarge Cement Zimbabwe to resources firm Fossil Mines for an undisclosed sum.

Kuvimba Mining House, Zimbabwe’s state mining vehicle, is to acquire the 50% shareholding in Great Dyke Investments from Afromet JSC. Financial details were undisclosed.

Proparco, a development finance institution and the private sector financing arm of French AFD Group, is to make an equity investment of US$10 million into MUA, the SEM-listed insurer. The investment backs the Mauritian insurer’s regional growth ambitions by further strengthening its financial capacity to improve insurance overage and increase market share. MUA has operations in Mauritius, Kenya, Uganda, Rwanda, Tanzania and Seychelles.

GOMYCODE, a Tunisia-based edtech startup, has raised US$8 million in a Series A round led by Proparco and AfricaInvest. The funds will be used to scale tech education across the MEA region.

Nigerian multi-channel retail company ShopEX has received a US$400,000 investment from South African venture capital firm HAVAÍC. The retailer mobilises a combination of traditional and digital channels to market, sell and distribute successful and global brands in Nigeria and other African markets. The capital injection will allow ShopEX to scale its presence into new markets.

SparePap, a Kenyan digital after sales marketplace, has secured funding from Mobility 54, Toyota Tsusho Corporation’s venture capital arm. The app provides automobile owners with vetted, competent, and trusted mechanics on demand and the ability to purchase replacement parts.

Egypt-based fintech platform ADVA has raised an undisclosed sum in a seed round from Sawari Ventures. The six figure investment will be used to expand its product offering which provides customers with services in health, education and insurance among others.

Insurtech startup Nice Deer has raised US$1 million in a pre-seed funding round led by DisrupTech Ventures. The platform has developed a comprehensive integrated digital ecosystem for the healthcare industry in Egypt, facilitating insurance and repayment of insurance claims between healthcare providers, health insurance companies and beneficiaries.

Klash, the Nigerian cross-border African commerce platform provider, has raised an additional US$2 million in a total seed fund round worth US$4,5 million. The proceeds will be used to expand into a further five African countries in 2022 and relaunch its consumer app – renamed KlashaCart, an app that allows consumers to shop from participating international merchants online and in African currencies.

Nigerian digital lending platform Indicina, has raised US$3 million in a round led by Target Global with participation from Greycroft and RV Ventures. Indicina uses data to determine the financial status and potential loan eligibility of potential borrowers. The funds will be used to accelerate expansion into other African markets and develop new products for consumer credit recommendations.

WafR, a Morocco-based fintech and rewards startup, has raised US$455,000 in a funding round supported by Launch Africa Ventures, First Circle Capital and WeLoveBuzz among others. The application enables retail brands to broadcast smart promotions to retailers. The funds will be used to increase its network of retailers and expand its current team.

Over the last few years, amendments to the Competition Act which introduce national security considerations for foreign acquisitions have been pending enactment. Although there is no exact indication of when these amendments will come into effect, we are likely to see some movement on this front in 2022.

South Africa receives the largest amount of foreign direct investment (FDI) on the continent, followed by Morocco and Nigeria. Although South Africa saw a decline on FDI in 2020 (in line with the decline of FDI in the broader continent), there was an uptick in 2021, led by the financial services, technology, online retail and healthcare industries. The increase is likely to be sustained in 2022, with additional potential opportunities in renewable energy, agriculture and education sectors.

In line with the growing global trend towards protectionism, South Africa plans to introduce the long-awaited national security provisions by way of amendment to the Competition Act (in terms of section 18A) (FDI Amendments). Although the exact timing remains unclear, there is an expectation that these amendments could be enacted in 2022, and that they will result in FDI mergers facing an additional regulatory hurdle. Here is what FDI investors will need to know…

At a high level, the FDI Amendments introduce a mandatory regime which will consider FDI mergers from a national security perspective. The national security interests will be considered by a committee to be established by the President of South Africa (President), comprising cabinet members and other public officials. The mandate of the committee will be to determine whether the implementation of a merger involving a foreign acquiring firm may have an adverse effect on the national security interests of South Africa. Due to its mandate, the committee is likely to include the Ministers of Defence; Health; Agriculture and Land Reform; and Trade, Industry and Competition. The committee will be empowered to prohibit or impose conditions on mergers which may have an adverse effect on South Africa’s identified national security interests.

Although the FDI Amendments will involve an additional review process for FDI mergers, they do not expand the scope or nature of FDI mergers to be scrutinised, as the committee will only consider those mergers that meet the same thresholds already applicable under the Competition Act. Therefore, the committee will only have jurisdiction to assess a merger if the acquiring firm is a foreign entity, the merger relates to one or more national security interests, and satisfies the applicable financial thresholds for notifiable mergers. Applications for FDI approvals will need to be filed at the same time as applications for competition approvals, and are likely to follow a similar timeframe (currently, the proposed review period for the committee is 60 business days – which is the same as the maximum review period for an intermediate merger). However, considering that the anticipated members of the committee are officials in other capacities, there is a concern around their capacity to reach decisions timeously.

National security and public interest considerations

The list of national security interests to be considered by the committee is yet to be published. However, the draft FDI Amendments list several factors that the President must consider in determining national security interests. These include South Africa’s defence capabilities and interests, the use of sensitive technology or know-how outside South Africa, the security of infrastructure, and the supply of critical goods and services. The President must also publish a list of the markets, industries, goods and services or regions in respect of which mergers involving foreign acquiring firms would require the approval of the committee.

As part of their substantive assessment of mergers, the South African competition authorities are already required to assess the impact of mergers on certain public interest factors. This involves an assessment of the effect a merger may have on (i) a particular industry or region, (ii) employment, (iii) the ability of small/black owned firms to compete, (iv) the ability of national industries to compete internationally, and (v) the promotion of a greater spread of ownership, in particular to increase the levels of ownership by historically disadvantaged persons (HDP) and/or workers.

Given the nature of the interests to be considered by the committee when assessing FDI mergers, there are likely to be overlaps with respect to the public interest factors currently considered by the competition authorities. A merger may be prohibited on public interest grounds, even if it does not have an anti-competitive effect in the relevant market. This has the impact of propelling the importance of public interest considerations in FDI mergers.

Transparency and accountability

The decisions of the committee may have serious consequences for FDI mergers across the board, as the FDI Amendments prohibit the South African competition authorities from approving a merger that has been prohibited by the committee.

It would, therefore, be important for parties to have an avenue of recourse against decisions made by the committee. However, the provisions relating to the committee are brief, and do not include any provisions that deal with the accountability of the committee. The only requirement is for the Minister of Trade, Industry and Competition to publish the committee’s decisions in the Government Gazette and inform the National Assembly of the decision (in appropriate detail, although not necessarily the committee’s reasons).

Notably, the FDI Amendments in their current proposed form also do not provide a dispute resolution mechanism. Arguably, a foreign investor could use the South African Promotion and Protection of Investments Act, which provides for a dispute resolution mechanism for foreign investors (essentially entailing international arbitration). This process could be used to challenge decisions of the committee (although this approach is yet to be tested). Unlike the South African competition authorities, the committee is not an independent body. The broad nature of the factors to be considered by the committee also leaves room for interpretation and disputes. Greater clarity in the drafting and accountability in decision making is critical if South Africa hopes to remain an attractive destination for FDI. In 2020, Nigeria passed investor friendly legislation and experienced an uptick in FDI deal activities, especially in the technology, financial technology, automotive and construction industries. As a continent, we need to ensure an investor friendly regulatory environment if we are to retain the continent’s already low share of FDI (at just 4% on a global scale), and even more so to attract greater FDI and increase the investor base beyond developmental financial institutions.

Considerations for merger parties

Public interest has been considered by many jurisdictions in the merger application process, including the United Kingdom, Russia and India and, therefore, should not be a foreign concept to FDI investors. While a global trend, the national security provisions will add another layer of regulation that an investor must contend with and creates a level of uncertainty across a large number of FDI mergers. In the current climate of stringent merger control regulation in South Africa, and even more so when the national security provisions come into effect, merger parties have to carefully assess the potential impact of transactions on public interest (e.g. employment, dilutions in HDP ownership), as well as the potential national security concerns. Depending on the nature of transactions and timing, merger parties may want to deal with these issues upfront as part of their application for merger approval. In global transactions with timing sensitivities, the South African competition authorities could also be consulted on whether ring-fencing arrangements are possible. Such arrangements are not specifically provided for and are generally considered by the competition authorities on a case-by-case basis.

It would also be prudent to anticipate the nature of conditions that may be imposed from a public interest (and going forward, national security) perspective, so that they are priced into transactions, and the economic rationale for transactions is assessed. As has been seen in recent merger approvals, the competition authorities often seek to impose conditions in pursuance of its public interest mandate. Conditions range from establishing employee ownership schemes, introducing HDP shareholders, to undertakings relating to local procurement and/or supply. In some transactions, it may even be preferable to negotiate conditions upfront, rather than to seek approval without conditions, particularly in transactions where onerous conditions are likely to be imposed. Although the right time to engage with the competition authorities depends on the circumstances of each case, parties may want to consider the possibility of more formal, proactive engagements early in the process. The South African competition authorities are generally receptive to such engagements with parties.

Ziyanda Ntshona and Burton Phillips are Partners and Lwazi Mthembu a Trainee Attorney | Webber Wentzel.

This article first appeared in DealMakers, SA’s quarterly M&A publication

Baker McKenzie’s newly launched Africa Competition Report provides a detailed analysis and overview of recent developments in competition law enforcement and competition policy in 32 African jurisdictions and regional bodies. The Report considers not only recent developments in competition law enforcement and competition policy in each of the highlighted jurisdictions, but also provides an overview of regulatory and legislative dynamics and challenges in selected markets.

According to the Report, 29 of the 32 surveyed African jurisdictions have national competition laws in place, while only two have no national competition laws, but are members of a regional competition law body. Countries where competition laws exist include Kenya, South Africa, Tunisia, Côte d’Ivoire, Tanzania, Egypt, Nigeria and Rwanda, while Ghana and Uganda do not have national competition law, although they are part of a regional competition body.

The Report outlines how competition authorities in Africa play an important role as champions, advocates and enforcers of competition policy across economies, and view competition policy as a key driver of economic growth. Although over the past two years, African competition regulators have actively engaged in efforts to address pandemic-related challenges, there has also been a general upward trend in competition policy enforcement across the continent. The upward trend in enforcement is highlighted by a number of significant recent developments in competition law regulation around the continent.

NOTABLE DEVELOPMENTS IN AFRICAN COMPETITION LAW

Algeria In Algeria, a new competition legislation is being considered. A first draft of the legislation is currently being reviewed by the Secretariat General of the Prime Ministry.

Angola The Competition Regulatory Authority in Angola conducted market inquiries in two sectors, namely telecommunications and petroleum products. Further merger filing fees were introduced by Executive Decree No. 32/21 of 1 February 2021.

Botswana During the 2020/21 financial year, the Botswana Competition and Consumer Authority carried out market inquiries (mainly focusing on cartelistic conduct) in the following sectors: abattoirs, construction, waste management, government supplies and animal feed. The Competition and Consumer Authority also expressed concerns in relation to pyramid schemes, with the Authority opening an investigation in collaboration with the Botswana Police Service. The price gouging of essential products during the pandemic was also on the agenda, with the Authority receiving numerous excessive pricing complaints in relation to basic food stuffs, healthcare products and hygiene products. The Authority cautioned suppliers and has maintained continuous price monitoring in relation to these products. Vehicle repair garages were also on the Authority’s radar in 2021. It handled 175 cases concerning the use of sub-standard parts or defective spare parts in vehicles brought in for repair and/or service, resistance of garages to effect warranty terms, and unclear pricing practices.

Furthermore, the Authority, in collaboration with the Organisation for Economic Cooperation and Development (OECD), is currently undertaking an impact assessment analysis of the legislative framework in the agricultural grains sector to determine the effectiveness of the legislative framework, focusing on pricing and import restrictions.

Cameroon Cameroon recently signed a Memorandum of Understanding with the United Kingdom, which sets out the arrangements for applying the effects of the economic partnership agreement from 1 January 2021.

Cape Verde In Cape Verde, it has been noted that competence on competition matters will be vested in the Ministry of Finance in the short to medium term, as there is currently no effective competition regulatory body.

COMESA There were various developments with regards to the COMESA in 2021. In February 2021, the COMESA Competition Commission issued a Practice Note in which it amended the interpretation of the term “operate”. Prior to this, a party “operated” in a COMESA Member State if it had turnover or assets in that Member State in excess of USD 5 million. This requirement has now been removed, effective 11 February 2021, and a party will “operate” in a COMESA Member State merely if it is active in it (without a minimum turnover or asset threshold). The impact of this will be to make it easier for a transaction to fall within the scope of the COMESA merger control regime.

The COMESA Commission has also recently issued Draft Guidelines on Fines and Penalties, Draft Guidelines on Settlement Procedures, and Draft Guidelines on Hearing Procedures.

In September 2021, the COMESA Commission issued its first penalty for failure to notify a transaction within the prescribed time periods, which penalty amounted to 0,05% of the parties’ combined turnover in the Common Market in the 2020 financial year. This was imposed in relation to the proposed acquisition by Helios Towers Limited of the shares of Madagascar Towers SA and Malawi Towers Limited.

In December 2021, the COMESA Commission imposed a fine for failure to comply with a commitment contained in a merger clearance decision.

The COMESA Commission also conducted eight investigations into restrictive business practices in 2021.

Egypt There were numerous recent developments in Egypt, including in November 2020, when the Competition Authority announced that the Egyptian Prime Ministry had approved the Prime Minister’s draft law amending certain provisions of the Egyptian Competition Law 3/2005. In February 2021, the Egyptian parliament’s Economic Affairs Committee started the discussions on the new amendments. The Competition Authority has also recently initiated market inquiries in relation to multiple sectors including healthcare, food, electronic and electrical appliances, as well as the automotive, real estate, media and petroleum sectors.

In April 2021, the Economic Court of Cairo issued a ruling in a criminal case brought against five individual poultry brokers by the Competition Authority in March 2020, for colluding to fix the price of chicken to the detriment of consumers and chicken breeders. The court fined each broker 30 million Egyptian pounds (approx. US$1,6 million) for agreeing to fix the price of a kilogram of chicken.

In July 2021, the Competition Authority initiated a criminal case against two companies who agreed to submit identical offers in one of the practices of the General Authority for Veterinary Services, in violation of Egyptian competition law.

The head of the Competition Authority announced plans for the creation of an Arab Competition Network to enhance cross-border cooperation between antitrust enforcers in the Middle East. The ACN would be the first to provide Arab competition authorities with an official platform to meet and discuss prominent issues and impending changes to antitrust law. The network would be run by the 22 members of the League of Arab States, which includes Egypt, Syria, Lebanon, Iraq, Jordan and Saudi Arabia, among others.

Eswatini In Eswatini, the Competition Commission published a Draft Competition Bill, 2020, which is intended to be presented to the Minister of Commerce, Industry and Trade. The object of the Draft Bill is to increase effectiveness, consistency, predictability and transparency in the enforcement and administration of competition law in Eswatini. It also aims to give effect to regional frameworks, such as COMESA Competition Regulations and international best practices. The Draft Bill has yet to be signed into law. In April 2021, the Competition Commission published guidelines on market definition, which adopt international best practices.

Ethiopia In Ethiopia, the Trade Competition and Consumer Protection Authority is working on regulations to provide guidance on the application of the Trade Competition and Consumer Protection Proclamation (No 813/2013). Proclamation No. 1263/2021, which is expected to be enacted and come into force in 2022, transfers the powers of the Trade Competition and Consumer Protection Authority to the Ministry of Trade and Regional Integration.

The Gambia The Ministry of Information in The Gambia is currently reviewing a Merger Commission, which will be effective in maintaining and encouraging competition in markets, to promote and ensure fair and free competition, and to protect the welfare and interests of consumers. The Competition Commission has initiated the following market studies: Hajj Market Study; Rice and Sugar Market Study; Liquefied Petroleum Gas Market Study; Cement Market Study; Tourism Market Study; Banking Market Study; and Vehicle Procurement Market Study.

Ghana In Ghana, a draft Competition and Fair Trade Practices Bill is before parliament for consideration.

Kenya The Competition of Authority in Kenya finalised its study into the regulated and unregulated credit markets in the country and issued its report in May 2021. The Authority further developed the Retail Trade Code of Practice 2021, in consultation with stakeholders in the retail sector, to address the abuse of buyer power issues arising from the sector. Also in 2021, the Competition Authority conducted a dawn raid in the steel industry and issued draft joint venture guidelines, to clarify the rules and filing requirements of joint venture arrangements.

Malawi Notable developments in Malawi include amendments to the Competition and Fair Trading Act, with the regulations having been proposed and submitted to the Ministry of Justice. Furthermore, the Competition and Fair Trading Commission has drafted new guidelines on various topics, including abuse of dominance and collusive conduct, exclusive dealing arrangements and resale price maintenance, market definition, discriminatory and tying conduct, and public interest, amongst others. These guidelines have been circulated to various stakeholders for comment, but have yet to be published. The Competition and Fair Trading Commission recently concluded a market inquiry into the funeral services market, and is currently conducting a market study on digital markets.

Mauritius The Competition Commission in Mauritius concluded a market study in the pharmaceutical sector on 8 June 2021.

Mozambique There were numerous developments in competition law in Mozambique in 2021, including that the Competition Regulatory Authority became operational in January 2021. Regulations on Merger Notification Forms were enacted by means of Resolution No. 1/2021 of 22 April 2021. The Regulations prescribe the different forms to be completed for merger notifications, as well as the details of the information and documentation required. Regulations on Filing Fees were enacted by means of Ministerial Diploma No. 77/2021 of 16 August 2021. Filing fees are currently set at 0.11% of the turnover of the parties in the previous year, up to a maximum of MZN 2,250,000 (approx. US$35,000). Amendments to the Competition Regulations were enacted by means of Decree No. 101/2021 of 31 December 2021.

Namibia A Competition Bill is in progress in Namibia, and the Competition Commission expects to submit the final version of the Competition Bill to the Ministry of Industrialisation and Trade by the end of June 2022.

Nigeria On 2 August 2021, Nigeria adopted the Merger Review (Amended) Regulations 2021, which set out new fees applicable for merger filings. The Federal Competition and Consumer Protection Commission launched and publicised an investigation into the alleged anticompetitive conduct of five companies in the shipping and freight forwarding industry in October 2021.

South Africa There were various developments in South Africa in 2021, including in May 2021, when the Competition Commission launched the Online Intermediation Platforms Market Inquiry, focusing on four broad online intermediation platforms and market dynamics that specifically affect business users – eCommerce marketplaces, online classified marketplaces, software app stores and intermediated services (such as accommodation, travel, transport and food delivery). The inquiry is ongoing, with a provisional report scheduled for release on 10 June 2022, and the final report scheduled for release in November 2022.

In April 2021, the Commission released its market inquiry reports on Land Based Public Transport. Furthermore, in April 2021, the Commission published its final report on an impact assessment study it conducted in relation to COVID-19. The report sets out the findings of the Competition Commission regarding the impact of the COVID-19 block exemptions and the enforcement work done by the Competition Commission during the pandemic. The Competition Commission’s fifth Essential Food Pricing Monitoring Report, which is released quarterly, focused on tracking the impact of the COVID-19 pandemic and consequent economic crisis on food markets.

In May 2021, the Commission issued, for comment, draft guidelines on Small Merger Notifications, which contain specific guidance applicable to the assessment of digital mergers.

Notably, 2021 was the year that the Commission prohibited a merger solely on public interest grounds, making it the first transaction to be prohibited on non-competitive grounds. Ultimately, however, the merger was conditionally approved before the Competition Tribunal.

In November 2021, the Commission released its Economic Concentration Report, which highlighted patterns of concentration and participation in the South African economy. The report includes details on the Commission’s power to launch market inquiries into highly concentrated industries, as well as its increased authority to impose structural remedies on businesses in these sectors.

In March 2022, the Commission issued Guidelines on Collaboration between Competitors on Localisation Initiatives, which are aimed at providing guidance to industry and government on how industry players may collaborate in identifying opportunities for localisation and implementing commitments related to localisation initiatives in a manner that does not raise competition concerns.

In March 2022, the Commission launched a market inquiry into the South African fresh produce market, which will examine whether there are any features in the fresh produce value chain which lessen, prevent or distort the competitiveness of the market.

The Commission concluded various settlement agreements with market players (e.g., grocery retailers and laboratories) to reduce the prices of goods and services.

Zimbabwe In March 2021, the Competition and Tariff Commission in Zimbabwe published draft guidelines on Horizontal Agreements for comment.

Lerisha Naidu is a Partner, Angelo Tzarevski an Associate Director and Sphesihle Nxumalo and Zareenah Rasool are Associates in the Competition & Antitrust Practice | Baker McKenzie Johannesburg

This article first appeared in DealMakers, SA’s quarterly M&A publication

Mr Price has released its results for the 52 weeks ended 2 April 2022. I know that this is an odd-sounding reporting period, but with retailers you need to remember that most of them report based on trading weeks rather than calendar years.

There’s another important nuance that you need to be aware of: because of the reporting calendar being based on weeks rather than calendar years, those retailers need to report a 53-week period every few years. Mr Price did this in FY21, which means you need to be careful when comparing FY22 to FY21 because the prior period has an extra week of trading.

To make it possible to do meaningful year-on-year comparison, retailers typically give commentary on a “comparable basis” where they only focus on the first 52 weeks of the comparable year.

I appreciate that these aren’t the most exciting concepts in the world, but you can’t properly understand retail results without knowing about this. Onward to the numbers!

Mr Price is a proper business

On a comparable basis (and now you know what that means), headline earnings per share (HEPS) grew by 25.9%. If you don’t adjust for the extra trading week, the growth rate is 20.1%. This is why it is so important to understand these periods.

One of the things you want to see in a retailer is growing market share, which Mr Price achieved with 140 basis points growth. Another important metric to look out for is operating margin, which has increased to 17.7%.

It’s worth highlighting that online sales grew by 48.2% and contributed 2.9% of total sales. This is much lower than we see in markets like the UK, which creates a strong argument that South Africa’s online shopping channel still has plenty of runway.

Mr Price has been on the acquisition trail, with Power Fashion (1 April 2021) and Yuppiechef (1 August 2021) both included in this result and described as being “earnings accretive” – there’s a difference between being earnings accretive and offering attractive returns on capital though. Investors will be keeping an eye on these acquisitions, as Mr Price did pay top dollar for them. Or top rand, even.

Mr Price is retaining a portion of earnings for future growth, as is common in listed companies. The final dividend is up 25.9% and the pay-out ratio of 63% has been maintained.

A closer look at the numbers

Revenue increased by 25.9% on a comparable basis and 14.1% using comparable stores, which is strong like-for-like growth. Other income grew by 37.5% but this included a once-off SASRIA claim of R296.1 million related to the civil unrest. A business interruption claim is still under assessment and should be finalised in the new financial year.

Here’s the most important metric for me: on a two-year basis and excluding acquisitions, sales grew by 12.5%. Consumers have shifted to value clothing in a time of economic pressure and Mr Price has been waiting with open arms.

Cash sales are 86.1% of the group total but it should be noted that Power Fashion and Yuppiechef are entirely cash based. If you exclude them, cash sales grew 14.3% and credit sales grew 23.6%, with account applications up by 54%. Mr Price notes that the account approval rate of 33.1% remains well within risk tolerance.

Selling price inflation was 5.5% excluding Power Fashion. Including that acquisition totally breaks the internal inflation number as the items are at a much lower average price point. Volumes were up 10% excluding acquisitions.

Moving on to margins, gross profit margin decreased by 150bps to 41%. There were some once-offs in the numbers, with Mr Price noting that on a comparable basis gross margin was in line with the previous period at 42.4%.

Total expenses grew 16.4%, a number well in excess of inflation. That is to be expected when a footprint is growing, as it includes new stores and inflationary costs on the old cost base. The important point is that sales growth is higher than expenses growth, so operating margins have expanded.

This is called “operating leverage” – the joy of revenues growing faster than inflation on fixed store costs.

When it comes to working capital, inventory increased by 6.1% excluding acquisitions and higher goods in transit. This is reasonable in the context of group growth and global pressures.

Capital expenditure was R734 million this year and is expected to be R900 million next year, including 180 – 200 new stores. With return on equity of 28.9% and return on assets of 23.2%, shareholders won’t complain about the group investing capital in growth.

Segments

The Apparel segment achieved record market share and saw operating profit increase by 33.7%, with operating margin up 40bps to 18.9%.

The Homeware segment achieved sales growth of 15.6% which is really impressive vs. a strong base. Operating margin did come under some pressure, down from a record 21.3% to 20.6%, a decrease of 70bps.

The Telecoms segment grew revenue by 34.4% to R1.2 billion. This is still a small contributor (Apparel is R19.5 billion for example) but growth prospects are exciting.

The Financial Services segment grew revenue by 6.2%, including insurance premium income up by 6.4%. The impairment provision adequately covers net bad debts.

Growth prospects

Mr Price is on a rampage. It opened 130 new stores this year, a much higher rate of growth than the 5-year average of 80 new stores a year. Power Fashion has increased its footprint by 20.6% since being acquired, which is quite something considering most people had never even heard of the group before Mr Price bought it.

Surprisingly, openings were lower than Mr Price had hoped, as the group had to direct a lot of its energy towards reopening looted stores.

Beyond bricks and mortar, Mr Price is doing very well in the online space. Online traffic market share is second only to Takealot among pure-play retailers and social media followers grew by double digits. The Mr Price mobile app is the highest ranked South African fashion app on Google Play, with usage up 27.3%.

Of the R4.6 billion available in cash, R3.3 billion is needed for the Studio 88 acquisition once regulatory approvals have been achieved. This will cap off a strong period of acquisitive growth for Mr Price, so the management team will need to focus on integrating the businesses and delivering the strategies.

The important thing is that there isn’t any debt on the balance sheet, so Mr Price isn’t under pressure to service payments to banks.

Am I trading it?

The share price is down around 2.5% this year and is trading at similar levels to May 2021. As great at these numbers look, it all comes down to what was priced into the stock. I must say, I’m tempted to punt at a move from R200 to R220.

There is an important point in the results presentation that gives some balance to all the good news: “May 2022 sales growth below expectations – details to follow at next trading update” – this means that inflation is starting to bite.

Decisions, decisions.

As always, you need to do your own research and arrive at your own conclusion!

Your daily market overview delivered in bite-sized bullets:

Spar Group released interim earnings for the six months to March 2022. This is the one I’ve been waiting for, as I took a rather speculative position in the company in the hopes of a strong result. In some places, I got it right. There were some negative surprises though. At group level, turnover was up 5.2%, operating profit increased by 7.1% and diluted headline earnings per share (HEPS) was uninspiring with 3.7% growth. I’ve written a feature article on this result, including details on why I took the long position and how it performed in relation to that. Spoiler alert: the trade didn’t work out.

Sanlam has released an operational update for the four months to April 2022 that includes some rather scary numbers. The floods have caused great pain in the insurance business, causing a drop in headline earnings for this short period of 31%! I cover this in more detail in this feature article.

Etion Limited intends to sell 100% of the shares in Etion Create to Reunert, a listed electronics business. This is such a large deal for Etion that it triggers the need for a special resolution (75% approval), as it is the “greater part of the assets or undertaking of the company” – simply, this is triggered under s112 of the Companies Act when over 50% of the group’s assets are being sold. Etion Create specialises in customised electronic subsystems, so the fit with Reunert is clear. Etion is following a value unlock strategy with great success, as it has historically traded at a significant discount to the underlying intrinsic value. The purchase price is around R197 million and isn’t allowed to exceed R210 million after all adjustments. The net assets of Etion Create as at 30 September 2021 were R159.4 million. Etion intends to distribute the net proceeds to shareholders. There are many steps to be completed in this deal and Etion shareholders can expect to receive a circular on approximately 1 August 2022 with full details.

Afrocentric holds a 71.3% stake in AfroCentric Health. That subsidiary has entered into an agreement to acquire the remaining 49% in AfroCentric Distribution Services for R75 million. This is a small related party transaction under the JSE listings requirements. This is part of AfroCentric’s strategy to build distribution capability to market the new generation products of AfroCentric and its other partners. In the six months to December 2021, this business generated profit before tax of R11.6 million. As this is a small related party deal, shareholders don’t need to vote on it but an independent expert does need to sign off that the deal is fair and reasonable. Mazars Corporate Finance has been appointed to provide an opinion.

The JSE probably had to take a lot of dust off the podium and screens for a new listing event, but today Southern Palladium celebrated its dual listing on the Australian Stock Exchange (ASX) and the JSE. With a successful initial public offering (IPO) that raised $19 million, the company will focus on developing its Bengwenyama PGM project in the Bushveld Complex. Southern Palladium holds a 70% stake in the project.

If you are a shareholder in MAS Real Estate, you should note that the company has released the circular for its proposed acquisition of six commercial retail centres in Romania. The counterparty happens to be the fund’s joint venture partner in the country, so this is a related party deal which means there are special JSE rules. The circular also deals with an extension to the joint venture. You can find the circular at this link.

I don’t pay a lot of attention to shareholding changes related to local funds, as they trim and increase their positions regularly and are often restricted to the South African market. Global investment giant BlackRock has no such restrictions, so it is notable that the fund has increased its stake in The Foschini Group to 5.375%.

If you are interested in Orion Minerals, then you can listen to a presentation at an investor conference in Australia at this link.

If you’ve always wondered how bank balance sheets are managed, or if you simply feel the desire to stare at many numbers on your screen, you could check out Sasfin’s Pillar III Risk Management Report.

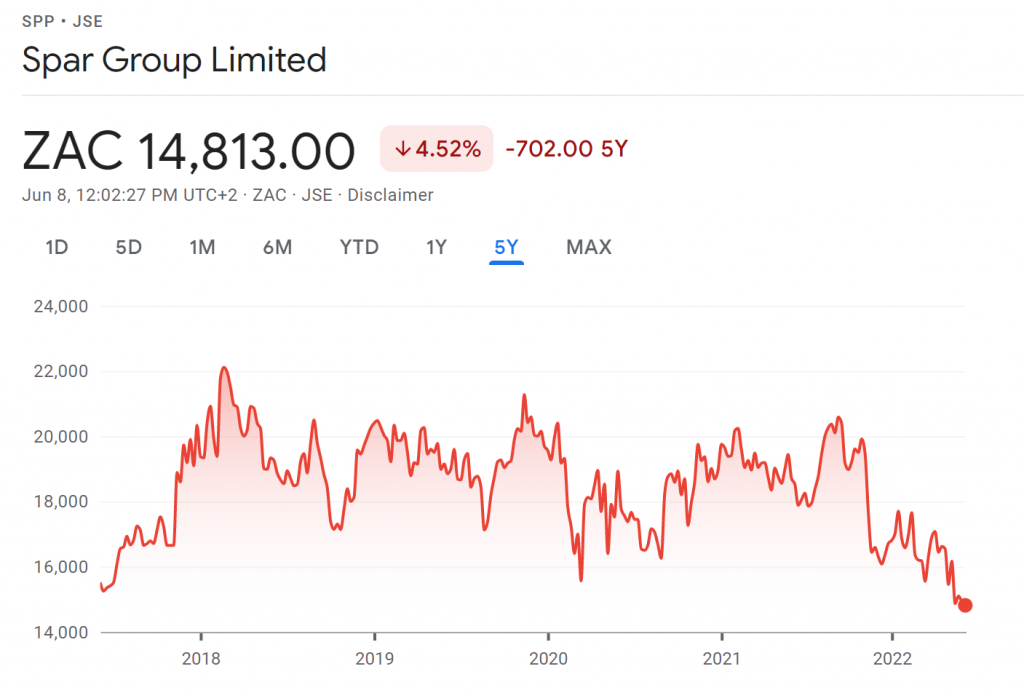

Spar’s slogan these days is “Under the Tree” – I had to Google it to check. Gone are the days of “Good for You”, which may be apt considering recent share price performance.

Spar has traded in a channel for years. Check out this chart and take note of how the stock has swung up and down in a clearly visible range:

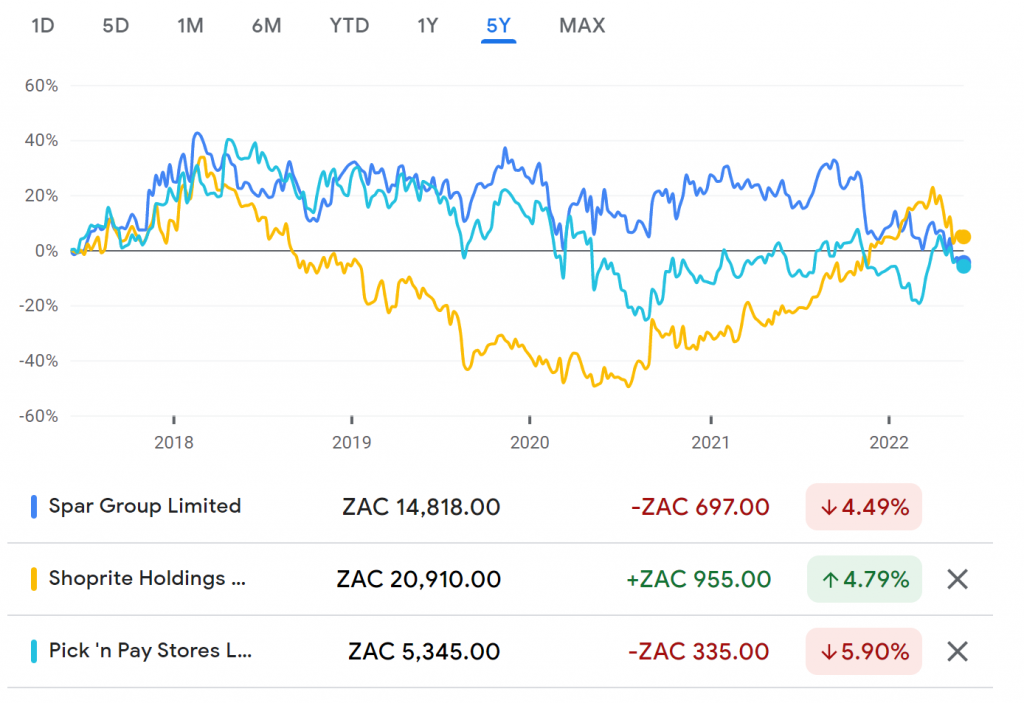

This means that Spar has been a poor choice in a buy and hold strategy. Before you get carried away in thinking Shoprite and Pick n Pay were any different, here’s a 5-year relative performance chart of all three of them:

Clearly, this isn’t a sector where you can buy and forget. For fans of swing trading and pairs trading (long one and short the other), the grocery retail sector does offer plenty of fun. I think part of the reason is that this sector is hyper-competitive, so success at one retailer is often at the expense of another.

I took a punt on Spar ahead of the latest earnings. The stock sold off sharply at the end of 2021 based on issues in integrating the acquired business in Poland and the guidance given to the market that the dividend would be significantly lower for the next couple of years. This is to give the balance sheet breathing room for a large SAP implementation project.

To be fair to Spar, substantial investment in IT infrastructure is part of what drove Shoprite’s recent run of form. The process is painful but it should be worth it.

I bought after the big sell-off and my long thesis was based on the following expectations for this result:

Poland to be doing better, not least of all with so many Ukrainians to feed (sad but true)

The food service businesses in Ireland and England to perform well as restaurants have recovered

Local grocery retail to lose further ground to Shoprite and Pick n Pay but nothing major

TOPS to put in a huge recovery performance as people were allowed to buy alcohol and have braais

Build it to experience slightly negative turnover growth in line with the broader pressures in DIY and building materials vs. a really strong base year

I didn’t have a firm view on Switzerland but didn’t expect it to cause fireworks in either direction (sigh)

So, what happened?

I’ll start with Poland, where turnover was +6.5% in local currency (a good result). Retailer loyalty (the percentage of goods that franchisees acquire from Spar group as the wholesaler) only increased marginally to 31%, which isn’t great. The issue seems to be in the south of the country. Expenses were -3.3% which is really good as corporate stores were closed and the footprint rationalised. There’s still a loss of R187.5 million but it’s a lot better than it used to be. So, expectations partially met.

Moving on to Ireland and Southwest England, turnover +8.3% in local currency so that ties in with what I hoped to see. Here’s the bad news: operating expenses jumped by +16.9%, driven by labour shortages and distribution costs. This caused a nasty impact on margins that I didn’t see coming.

I’ll deal with Switzerland before bringing it home. Turnover was -1.6% in local currency and operating expenses increased by 10% in local currency, so this business’ margins also got hammered as operating profit fell by 13.7%. Ouch.

The improvements in Poland were effectively offset by the pressures in the other businesses. This is a major disappointment.

Within South Africa, TOPS shot the lights out with turnover +41.6%. TOPS revenue of R5.5 billion in this period is much higher than R4 billion in the six months to March 2019 before the world became a less enjoyable place.

Build it did well I think to achieve turnover growth of +1.4%. Inflation was +5.8% so volume growth was approximately -4.4% (assuming no major change to the footprint).

Core grocery turnover was +4.6%. Price inflation for the SA business as a whole was 5%, so it is likely that volumes dropped slightly in grocery. As a wholesaler, Spar runs at much tighter margins than Shoprite and Pick n Pay, so the impact of fuel cost increases etc. have to be passed on to franchisees. It’s worth noting that whilst employee costs only increased by 3%, fuel jumped by 40% and the period ended March only includes a few weeks of the petrol price jumps we have suffered with. Watch out for this in the next period.

Spar’s private label turnover was only +4.1%, with riots severely impacting major suppliers and thus Spar’s range of house brands. This is an important source of gross margin uplift and I would hope to see this tracking ahead of revenue growth in future.

My idea hasn’t worked out

By the time you roll this up to group level, turnover was +5.2% and operating profit was +7.1%. An unfavourable tax contributed to profit after tax +4.1% and headline earnings per share (HEPS) +3.5%.

It’s also very important to note that HEPS of 642.6 cents is much higher than the interim dividend of 175 cents per share. Spar is retaining cash for the R1.8 billion SAP implementation. The interim dividend is 37.5% lower than the prior year.

If we simply double the interim dividend for the purposes of working out a forward yield, we have a yield of around 2.4% at the current share price. The risk for investors is the share price dropping to around R125, which is where support is found at a share price level going back to 2015!

The worry for me is that there’s also a fundamental argument that the share price could get to R125. Investors in a rising yield environment may not have the patience required to sit on the stock at this dividend yield and the share price may drift lower as a result.

I bought Spar with a swing trading outlook and swings don’t always go in the direction you want them to. If they did, everyone would be a stock market millionaire!

The share price jumped in the opening auction and then traded down rather quickly, eventually closing 0.8% lower for the day.

Having considered the reasons why I bought the stock and what the outlook is from here, including critical macroeconomic considerations like inflation, I’m now looking to exit my position.

Around a week ago, Santam released an operational update for the four months to April 2022, which I wrote a feature article on. Sanlam has now done the same, giving us insights into the mothership.

Sanlam is a genuinely impressive business. If you have a look at the dividend history of the company, this is a very good example of a business that you can buy and forget about. The share price isn’t going to shoot the lights out, but it should give decent returns over an extended period with a significant dividend yield. Having said that, the last few months have been really challenging for the group.

Sanlam is taking a big step in Africa with the Allianz deal. I wrote about the deal in detail in early May, which you can find here. As a quick synopsis, Sanlam wants to combine its African operations with those of Allianz, creating a vast footprint on the continent. Sanlam would hold 60% of the joint venture, which means it would effectively be taking control of Allianz’s assets. This is a significant deal.

The group has positioned itself firmly as an emerging markets business, with only a focused international asset management business remaining in the UK.

Strategically, the story is great. The latest earnings are an unfortunate reminder of the risks faces by insurance groups.

As a sign of the times, Sanlam has significantly increased its buffer of discretionary capital. This means that more money is being kept in reserve, a direct result of ongoing market pressures and uncertainties. Discretionary capital increased from R2.9 billion on 31 December 2021 to R6.5 billion on 30 April 2022, including GBP153 million in proceeds from the UK asset sales.

The downside of the increased buffer is that it negatively impacts returns to shareholders. The nature of a buffer is that it would be invested conservatively, which doesn’t provide equity-level returns to Sanlam investors.

The net result from financial services has decreased by 7%. Digging deeper into this, we find that the Life Insurance business performed well, up 14% thanks to lower Covid-related mortality claims. The Investment Management business enjoyed higher average assets under management than a year ago, as inflows throughout 2021 were strong.

Earnings in the General Insurance business fell by a whopping 62%, a direct result of the catastrophe claims and lower returns on insurance funds. As insurance reserves are invested in the market, buying a business like Sanlam means you are taking exposure to the rest of the equity market as well.

In terms of new business volumes, Life Insurance was a solid contributor with volumes up 8%. General Insurance volumes were up 4%. Investment flows were down by 8% though, with Sanlam pointing out the high 2021 base. The net margin on new business declined from 2.82% in 2021 to 2.34%, mainly due to product mix changes.

Group net cash inflows of R26.7 billion were down by 5% because of the lower investment flows.

The effect on net earnings of a weak result from financial services was magnified by group project expenses. It’s never pretty when overheads are growing quickly and the underlying business has had a tough time. The impact on headline earnings is substantial, with a decrease of 31%!

With a drop in the share price of around 1.5% by late afternoon trading, it seems to have been mostly priced in. This year, the share price is slightly up.

Property fund Attacq has released a pre-close update presentation. This is a way to bring the market up to speed with how the fund has performed in recent months, with the current financial period closing at the end of June. Hence, a “pre-close” update.

I always appreciate and applaud any efforts by companies to go above and beyond minimum disclosure requirements to investors. I must also note that I am a shareholder in Attacq.

Gross interest-bearing debt has decreased since December 2021, reducing from R8.6 billion to R8.1 billion. The gearing percentage (net debt as a percentage of assets, with some adjustments) has stayed at 38%.

Attacq has applied the marketing brush to the names it uses for different types of properties. You’ll shortly see what I mean.

Collaboration hubs (what everyone else would just call office properties) saw vacancies improve slightly since December, with occupancy at 82.9% vs. 82.7%. I was quite surprised to note that the Waterfall City offices have a lower occupancy rate than offices in the rest of South Africa (81.8% vs. 85.7% respectively).

“Retail-experience hub” (shopping centre) occupancies also increased slightly from 96.2% to 96.4%. The logistics and hotel properties are fully let.

Trading densities in certain malls have grown significantly year-on-year. Trading density is a measure of tenant turnover divided by gross lettable area. Mall of Africa trading density grew 18.1%, Garden Route Mall grew by 13.3% and Eikestad Mall is 12.2% higher. Other malls have only managed low single digits.

From a dividend perspective, Attacq wants to retain its REIT status and needs to declare a dividend by the end of October to do so.

Beyond the rental income and related dividends, Attacq has numerous developments underway. Recently completed developments include the Cotton On head office and distribution centre as well as a Courtyard Hotel in Waterfall. A corporate campus, data centre, distribution centre and residential tower are all under development.

Attacq plans to hang on to its 6.46% stake in MAS Real Estate, giving strategic exposure to European property. Retail assets in the rest of Africa are considered non-core and will be disposed of.

The share price is down around 17% this year and is volatile between R6 and R8 a share, with a clearly visible trading range that creates great opportunities for swing traders. It’s just a pity that the stock is quite illiquid with a wide spread.

Your daily market overview delivered in bite-sized bullets:

Sygnia has released interim results and they look to be a rock solid set of numbers. I was particularly impressed by net inflows in the retail business over the six months to March, a tough period in the market. I wrote in detail about the results at this link.

Attacq has released a pre-close update in which the property fund has disclosed movements in debt, growth in trading densities, a slight improvement in vacancies and an update on properties under construction. I’ve written on the numbers in more detail at this link.

Sirius Real Estate is a industrials-focused fund that achieved excellent share price gains during the pandemic. Things have cooled off substantially in 2022, something I warned about during 2021. THis is a great example of a momentum trading strategy and the importance of getting out of the way once the momentum turns against you. The underlying results are still good, with the fund announcing that its dividend for the year ended March 2022 is going to be 15.5% to 16.5% higher than the prior year. Importantly, this is mainly driven by an increase in funds from operations, so there is high “cash quality of earnings” – this is what investors want to see vs. fair value gains which are a paper return rather than an improvement to the bank account. Sirius is down around 28% this year.

Omnia Holdings has released a trading statement for the year ended March 2022. Headline earnings per share (HEPS) is expected to be between 70% and 90% higher, coming in at between 639 cents and 714 cents. There’s noise in the numbers from hyperinflation in Zimbabwe and the disposal of Umongo Petroleum and Oro Agri over the past two financial reporting periods. Omnia has a strong balance sheet and has said that a “decision regarding dividends” will be communicated with results. Is another special dividend on the way?

Sabvest Capital has been a great story for investors over the past year, proving that there is value to be found among JSE-listed investment holding companies. The company is also proof that even with a truly terrible website, excellent returns can be achieved. The share price is up almost 40% in the past year and the latest update is that the CFO has bought over R1 million worth of shares.

Oando Plc has signed a Memorandum of Understanding with the Lagos Metropolitan Area Transport Authority for a rollout of electric mass transit buses, the necessary supporting infrastructure and related service centres. Lagos has 25 million residents and the city is clearly concerned about the impact on air quality of a growing population that needs to move around the city. Oanda is an energy company that is trying to transition away from fossil fuels. The stock has very little liquidity on the JSE.

Nutritional Holdings is back at it with colourful and unusual SENS announcements. A former shareholder and director has taken steps to apply for a provisional liquidation of both the holding company and a subsidiary to recover a shareholder loan. The matter for the subsidiary has been postponed to July 2022 and the holding company judgment is pending. The new board is investigating the matter and notes that there may have been Companies Act breaches related to the loan. The soap opera continues and I’m glad that I am watching from a distance, as I never have and never will own shares in this company.

Safari Investments RSA has responded to Heriot REIT’s firm intention announcement relating to a general offer to be made to Safari shareholders. At this stage, the independent board is not expressing a view on the offer of R5.60 per share. The immediate next step is for Heriot REIT to issue a circular with details of the offer. Safari then needs to issue a response circular, which will include the opinion of an independent expert on whether the offer is fair and reasonable.

There’s been another loss-of-life incident at Harmony Gold’s Kusasalethu mine, near Carletonville. In the strongly-worded announcement, the company notes that there have been too many incidents at this mine and that safety messages to staff have been re-emphasised. Harmony will conduct a comprehensive investigation into the incident.

Nictus Limited is one of the smallest companies on the JSE, with a market cap of under R37 million. This obscure listed company is a retailer of furniture and electrical appliances. In a trading statement, Nictus updated the market that for the year ended March 2022, HEPS is between 39% and 59% lower than the prior period.

A director in WBHO has bought a small number of shares, with a transaction value of almost R55,000.

It’s always fun tracking the progress of a disruptor. In the asset management industry, Sygnia fits that description. The share price has nearly doubled over the past 3 years and is up almost 20% in the past month after drifting lower for the first few months of 2022. Can the growth continue?

Before digging into Sygnia’s latest results, let’s give the numbers some context. By the end of March, Coronation had assets under management (AUM) of R625 billion. Sygnia has assets under management and administration of R295.3 billion.

Now, there’s an important nuance there. AUM attracts the best fee, with assets under administration attracting a lower fee as there isn’t discretion over the asset allocation decision. Sygnia has built its business around passive investments, with the differentiator being clever marketing around products that track interesting underlying indices.

Sygnia is the second-largest provider of ETFs in South Africa and the largest provider of international ETFs on the JSE. I mean really, who hasn’t heard of the Sygnia 4th Industrial Revolution fund?

Another relevant nugget of information is that Sygnia operates the sixth-largest commercial umbrella fund in South Africa, with around R12.5 billion under management.

In the six months to March, Sygnia generated revenue of R397.4 million. Over the same period, Coronation generated R1,934 million in revenue, 4.87x higher than Sygnia off an asset base that is only 2.12x larger. This is the impact of the AUM vs. assets under administration strategy.

This isn’t a criticism of Sygnia at all. It’s just very important as an investor to understand the business model.

At first blush, it looks like revenue grew faster than assets, which suggests a positive change in mix. A more detailed read shows that average assets under management and administration increased by 15.3% and revenue linked to assets increased by 10.6%, so that reveals quite the opposite. A promising story on the revenue line is that treasury, securities lending and brokerage income increased by 24.5%. The blended outcome is 13.4% growth in revenue.

An increase in value of assets under management and administration of R4.5 billion helped offset most of the R5.6 billion net outflow in this period, compared to net inflows of R3.8 billion in the prior comparative period. It’s important to highlight that R241.2 billion of assets are institutional and this business experienced a R9.2 billion net outflow, of which R7.2 billion relates to a mutually agreed termination of a low margin client.

Looking through this noise, R3.6 billion in net inflows in the retail business shows how the South African retail investor community is maturing. They are buying market weakness rather than running away from it.

The revenue growth in this period was strong enough to drive headline earnings per share (HEPS) growth of 23.8% as benefits of scale were achieved. HEPS came in at 92.6 cents.

The interim dividend is 80 cents per share, up from 55 cents a year ago.

Sygnia’s share price of around R18.50 suggests an annualised Price/Earnings multiple of around 10x. Sygnia isn’t trading at a bargain price, so punters may want to watch it carefully for any pullback to the traded channel of around R15.50 to R17.00.Those happy to take a longer-term view on Sygnia would need to believe in continued disruption of the establishment by this group, with a track record to back that up.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")