When it comes to gold miners, Gold Fields has been the most impressive weed in a swamp of disappointment for me. My investment in this sector has been an epic fail, as the gold price has decided that war and inflation are no longer drivers of its price.

Nobody is quite sure what does drive the gold price now.

In dollar terms, gold is lower than it was a year ago. In rand terms, it is marginally higher. This doesn’t help when underlying mining costs are climbing sharply from inflationary pressures on wages and energy costs.

Gold Fields tanked more than 11% on Tuesday morning after the company announced a deal with Yamana Gold. It got even worse once the Americans woke up, eventually closing more than 20% down. The swamp has claimed another victim, this time self-inflicted by doing a gigantic deal to acquire a global player that is trading at a vastly higher multiple.

The first line of the announcement sounds rather exciting. The deal creates a top-4 gold player as measured globally, with operations in Canada, Australia, South America, Ghana and South Africa. The headquarters would be Johannesburg, which remains the City of Gold (and Potholes).

The deal structure is an all-share offer by Gold Fields based on an exchange ratio of 0.6 Gold Fields shares for each Yamana share, which implies a valuation of Yamana of $6.7 billion. The board of Yamana has unanimously approved the transaction and recommended to shareholders that they vote in favour of the deal, which makes me wonder whether Gold Fields has offered too much.

The reported value of net assets of Yamana is $5.25 billion and the profit after tax in the last quarter was $55.3 million. Even on an annualised basis, this is a forward Price/Earnings multiple of 30x! According to TIKR, Gold Fields is on a forward Price/Earnings multiple of 11.5x.

Can you say “earnings dilution”?

Yamana is currently listed in Toronto, New York and London, so the company moves faster between major cities than an oligarch’s yacht on a midnight escape route. The operations are in Canada, Brazil, Chile and Argentina and are focused on gold and silver production.

Gold Fields highlights the appeal of scale benefits from a larger portfolio, enhanced geographical diversification and complementary cash flow generation profiles. Both groups have healthy balance sheets and staggered capital investment cycles. The announcement also refers to an “industry-leading” growth pipeline.

Around $40 million worth of pre-tax synergies have been identified, mainly in operational integrations and financing synergies. A streamlining of overheads has also been highlighted. That’s not terrific news if your job at head office is to plug two systems into Excel and produce a pivot table.

No details are given of the triggers for the break fees. If they were to apply though, Gold Fields would have to pay $450 million or Yamana would have to pay $300 million, depending on which party is in breach.

So why has the market made its disgust clear with this deal? One reason might be the price – at a premium of 33.8% to the ten-day volume-weighted average price (VWAP) of Yamana, Gold Fields shareholders are paying up for this deal. Another might be the sheer size of the transaction and the risk that it brings, as existing Gold Fields shareholders will only own 61% of the combined group.

For this deal to go ahead, at least 75% approval is needed from Gold Fields shareholders. I’m not convinced that this is a dead rubber.

Your daily market overview delivered in bite-sized bullets:

Bidvest Group has released a voluntary trading update for the ten months to April 2022. The strong momentum has continued since the interim result, with “strong trading profit growth” and “excellent” cash generation. The business service operations are doing well, with a shrinking fleet and finance book as the blemish on the update. In trading and distribution, Bidvest has pointed to a strong performance even measured against a high base. Although working capital investment has been required in response to supply chain pressures and inflation, there is no concern over debtors. The group is looking abroad for growth opportunities, with several possible deals at various stages of progression. Results for the year ended June will be released in early September.

Adcorp Holdings has released results for the year ended February 2022. Although revenue from continuing operations fell by 1.7%, gross profit increased by 7.0% and operating profit jumped by 68.2%. Headline earnings per share (HEPS) jumped by 190.6% to 99.4 cents. Importantly, group interest-bearing debt (i.e. excluding leases) fell from R456 million to R133 million. Banking facilities of R350 million are being negotiated and the facility in Australia has already been extended. Adcorp’s bid-offer spread is wider than the smile of an investment banking analyst getting a first bonus, so be careful with this one. The share price is flat year-to-date but the chart has flapped around between R4.65 and R6.30 this year.

Momentum Metropolitan has released an operating update for the nine months ended March 2022. HEPS is up a meaty 59% as reported or 46% on a normalised basis. Although new business volumes were 16% higher, value of new business has fallen by 16% as new business margin has deteriorated from 1.1% to 0.8%. Return on equity has jumped from 11.7% to 18.2%. Momentum Corporate was the segment with the largest positive swing, as a normalised headline loss of R72 million in the prior period transformed into normalised headline earnings of R617 million in this period.

Asset management group Sygnia has released a trading statement for the six months ended March 2022. HEPS will be up by between 20% and 25%, coming in at 89.8 cents – 93.5 cents. The share price closed 3.7% higher at R17.

Novus Holdings has released a trading statement for the year ended March 2022. HEPS is expected to improve by at least 100% vs. the headline loss per share of 5.4 cents. I guess this means that the company will at least break even for the period. The announcement was called an “initial trading statement” so I don’t think the full story has been told here yet. Keep an eye on this one.

Oceana Group has more twists and turns than a school of fish escaping a seal. The latest news is that auditor PwC has resigned with immediate effect in respect of the audit for the year ended September 2022. There is a “strained relationship” and Oceana points out that a significant number of votes were exercised by shareholders against PwC’s reappointment. There’s been a lot of negative noise around Oceana, with investigations into accounting practices and departures of executives in recent months. The company needs to appoint auditors within 40 business days and is in discussion with a Big Four audit firm. Shareholders will be hoping for some stability going forward.

Huge Group has concluded a new debt package with RMB for R240 million in refinance and acquisition facilities, R15 million in general banking facilities and R12 million in asset based financing facilities. They are repayable in 20 equal quarterly tranches. R230 million of the refinance facility will be used to repay debt from Futuregrowth, leaving R10 million for potential acquisitions. The company notes that the repayments under the RMB facility are significantly less than the Futuregrowth facility. Let’s just hope that whatever strategy they follow with the money will be more successful than the Adapt IT debacle.

Grand Parade Investments is in the process of unbundling its steak in Spur. I mean, its stake. The SARB needs to give approval for the transaction and this hasn’t been obtained yet, so the company has noted that the dates of the unbundling will need to be amended.

Sibanye-Stillwater has received the details of a claim from affiliates of Appian Capital Advisory LLP. This relates to the termination of the acquisition of the Santa Rita and Serrote mines in Brazil, a deal that Sibanye walked away from after a geotechnical event which Sibanye concluded would be material and adverse to the business. Sibanye will need to defend the claim in the High Court of England and Wales, so a few legal eagles will be making money shortly.

S&P has revised Telkom’s outlook from stable to positive, thereby confirming that nobody from S&P has ever tried to cancel a Telkom contract. Jokes aside, this is a result of the improved outlook on the South African government, which happens to own around 40% of Telkom. Many local companies have had their outlooks revised as a result of an improvement in the sovereign outlook.

AngloGold is the latest company to implement an additional listing on A2X. This exchange offers a trading platform rather than an issuer regulation platform. The JSE (or other primary exchange) still sets the rules that each company must abide by. A2X is simply a place for shares to trade in a more efficient manner, effectively stripping some income away from the JSE.

Renergen Limited has updated shareholders on the commissioning of the Phase 1 plant. If you have a deep and secret desire to be an engineer, you should read the full announcement for all the details. Investors will be interested to note that customer sites are being prepared in parallel to receive the liquefied natural gas (LNG), so the commercial operation date will be planned in such a way that the plant doesn’t need to be turned off again as part of providing customers with LNG. After a 32-month process, Renergen has had “no surprises” during hot commissioning and is nearly finished with the process. The announcement doesn’t give a completion date, though.

Fuel forecourt REIT Afine Investments listed in December 2021 and provided a profit forecast for the year ended February 2022 as part of the listing documentation. The trading statement released by the company is based on variance to that forecast as well as the prior reported period. The latter comparison is pointless, as the listed entity only existed for one month of the comparable period. The important thing is that HEPS will be approximately 8% lower than the guidance in the profit forecast of 50.14 cents.

UK property funds Shaftesbury and Capital & Counties are in discussions regarding a possible merger. The initial deadline was that by 4th June, JSE-listed Capital & Counties is supposed to either announce a firm intention to make an offer or confirm that it will not make an offer. That has now been extended to 17th June at Shaftesbury’s request, which the Takeover Panel has consented to. Further extensions are possible by Shaftesbury, once again with regulatory consent. Take note that as these are UK-based companies, those company laws apply even though Capital & Counties is listed on the JSE. Don’t confuse the domicile of the company with the exchange on which it trades.

Kibo Energy has done a deal with Hasta Trust. This immediately put Arnold Schwarzenegger one-liners into my head, so I hope it does the same to yours. The deal is to develop a portfolio of long duration energy storage projects held by National Broadband Solutions (NBS) in South Africa, which is 100% owned by Hasta. This is linked to the distribution deal with CellCube for long duration energy storage solutions in Southern Africa. Under this transaction, Kibo will acquire a 51% interest in NBS.

If you are a Textainer shareholder, you’ll be interested to know that the exchange rate for the dividend has now been set. The $0.25 dividend will be converted at R15.60/$, so a dividend of R3.90 will be paid on 15th June.

If you are unfortunate enough to be a shareholder in PSV Holdings, you should take note that the company is still in business rescue. If the group is not recapitalised, it will likely face liquidation with no prospect of any payment to shareholders. I’m afraid there isn’t even a website for me to link to for this company.

Pepkor has released results for the six months ended March 2022. Revenue increased by 3.3%, or 3.7% if you adjust for the disposal of John Craig, which represents a gain in market share of 189 basis points. Operating profit jumped by 19.1%, so margins have improved considerably. HEPS increased by 28.3% or 12.1% on a normalised basis (excluding the Steinhoff global settlement). Cash generated from operations was R4.1 billion. The group points out that revenue is up 15.4% over two years, representing substantial market share gains over the pandemic. Pepkor is still growing, opening 144 stores in this period (total footprint now 5,708 stores) and acquiring an 87% interest in Brazilian value retailer, Grupo Avenida. Avenida has 130 stores and Pepkor is happy with performance since February when the deal closed. Perhaps the most important insight in the announcement was this: “While global supply chain uncertainties persist, it seems that shipping costs have stabilised and may trend downwards.”

After an incredibly busy week of results for listed companies controlled by Hosken Consolidated Investments (HCI), the mothership released its results for the year ended March 2022. Revenue increased 31% and EBITDA doubled that growth rate with a 62% increase. At headline earnings per share (HEPS) level, the increase is a rather daft 359%. The percentages become silly at that level. To make it easier to see the jump, HEPS increased from 287.7 cents to 1,321.3 cents. When viewed per underlying sector, the biggest swing was in gaming with a R20.5 million headline loss in the prior period swinging into headline earnings of R622 million in this period. The other sector worth noting is hotels, which still made a loss of R35.2 million. That’s a whole lot better than the loss of R318 million in the comparative period. HCI’s share price has been exceptional this year, up 138%!

Gemfields is such an interesting business. With a market cap of over R3.8 billion, it’s also a substantial company that is still off the radar for most investors. The share price has doubled in the past year, so the lack of market knowledge on this company is a pity. Gemfields owns 75% of the Kagem mine in Zambia and has achieved a record-breaking emerald auction in May. Across 38 lots, revenue of $43.4 million was achieved. The price per carat was also a new record for Kagem auctions. Gemfields also mines rubies in Mozambique and has other gemstone prospecting licences in several African countries. As a final tidbit on this interesting group, Gemfields also owns premium jewellery business Fabergé.

Nedbank released a voluntary update for the four months ended April 2022. There’s plenty of fluffy language and not many hard numbers in the update. I was hoping to see strong commentary around growth in corporate balance sheets and how the banks are getting a piece of the action. Instead, Nedbank talks about “moderate credit growth” and “robust consumer spending” which suggests that corporates are using internally generated cash flows to fund growth in this environment and that retail consumers are still driving growth. Net interest margin has “increased” and interest earning assets increased by “low-to-mid single digits” with “selective growth” in the corporate book. Impairments are within the 80bps to 100bps guided range for FY22. Non-interest revenue growth is up by double digits without adjusting for fair value adjustments and mid-single digits when taking a normalised view. Although expense growth is mid-single digits, JAWS (revenue and associate income growth less cost growth) is positive. That associate line is important, with income from Ecobank (ETI) expected to be up 74% year-on-year in the first half.

Finbond Group has released results for the year ended February 2022. There’s a substantial increase in loans advanced, up by 25.9% to just over R5 billion. Despite this, turnover fell by 13.7%. The first reason is that there is a lag effect in revenue in the Illinois business in the US where loans are for 24 months, so the book needs to build up. The second reason is that Finbond now equity accounts for C1 Holdings (brings in the net income further down the income statement) vs. the base year where it accounted for all the revenue and then took out minority interest further down. As always, the sensible number to look at is HEPS, which improved by 25.3% but is still a significant loss of 17.9 cents per share. No dividend has been declared. Sean Riskowitz of Protea Asset Management LLC has joined the board.

PBT Group is a company on the move. With a market cap of around R960 million, the business operates in the exciting and growing world of data science and related analytics. The share price has gained around 135% in the past 12 months. A special distribution of 30 cents per share has been declared, which sent the share price 7% higher on Friday.

Murray & Roberts jumped 6.7% on Friday after announcing that the Clough Saipem 50/50 joint venture had been awarded the engineering, procurement and construction (EPC) contract by Perdaman Industries for the multi-billion Australian dollar urea plant. This is a huge contract with extensive work involved, of which Clough’s share is around R22 billion. This increases the group’s order book to an all-time high of around R80 billion. The share price is still down 21.5% this year.

Huge Group has been rather quiet since the company’s disastrous attempt to acquire Adapt IT. I’ve missed the comic relief of that process. Shareholders will be pleased to note that HEPS for the year ended February 2022 will be more than double than prior year, coming in at between 56.01 cents and 58.81 cents. I strongly caution against making any decisions based on this trading statement, as Huge changed its accounting approach completely on 1 March 2021 and now sees itself as an “investment entity” – which makes the Adapt IT debacle even funnier – so underlying businesses are now recognised at fair value rather than consolidated. Full results are due this week and the share price closed on Friday at R3.69. This announcement came out after market close, so look out for any share price action on Monday.

ISA Holdings is a company you’ve possibly never heard of. With a market cap of around R180 million, this small cap provides information security solutions and boasts nearly 80% of revenue being of a recurring nature. The share price is up over 57% in the past year, so plucky shareholders in this business have done well. Revenue for the year ended February 2022 was up 11% and HEPS increased by 26% to 10.5 cents, thanks mainly to a decrease in operating expenditure. A final dividend of 6.2 cents and a special dividend of 10.0 cents have been declared, adding to the 4.3 cents interim dividend. The illiquid share price closed 5.9% higher at R1.07 and now has an incredible trailing dividend yield. Be careful of assuming that the special dividend will be repeated. This is exactly why companies distinguish between ordinary and special dividends.

NEPI Rockcastle has confirmed permanent executive appointments after operating with an interim CEO and CFO. Rudiger Dany and Eliza Predoiu have been permanently appointed to those respective roles. They have also appointed a COO in the form of Marek Noetzel. The useful thing about buildings is that they tend to withstand wholesale leadership changes with far more ease than operational companies. Shopping centres don’t complain about culture.

Brimstone Investment Corporation has released a quarterly update on its intrinsic net asset value (NAV), which is based on the directors’ valuations of the underlying investments. Between December 2021 and March 2022, the intrinsic NAV is up 3.7% on a per-share basis. That’s a solid performance over three months in this environment. The fully diluted intrinsic NAV is R13.399 and the share price is trading at R7.09, a discount of 47%. Welcome to the frustrations of investment holding companies on the JSE! The largest contributors to the value are Sea Harvest (39.9%), Ocean (33.2%), Equites (5.7%), Phuthuma Nathi (4.8%) and FPG Property Fund (4.1%). Stadio also deserves a mention, contributing 3.1% to the intrinsic NAV.

The Implats – Royal Bafokeng Platinum deal has taken another twist, with Northam Platinum intervening in the proceedings before the Competition Tribunal. You may recall that Northam Platinum also owns a significant stake in Royal Bafokeng that it acquired from Royal Bafokeng Investment Holdings. The Competition Commission recommended the approval of the deal, but the Tribunal is what really counts. Based on this issue, Implats has extended the “longstop date” (the legal term for the date by which all conditions precedent must be fulfilled) to 8 August 2022.

Quantum Foods is a poultry group that includes Nulaid, the largest egg producer in South Africa. The share price jumped 22% on Friday after the company released results for the six months to March 2021. Revenue increased by 7% and HEPS fell by 41%. A dividend of 8 cents per share has been declared. The share price jump happened right at the end of the day and could well have been finger trouble, as I can’t imagine why people would react so favourably to an update like this.

Rebosis Property Fund is in the process of selling a R3.35 billion portfolio of assets to a special purpose vehicle being put together by Vunani. Rebosis shareholders are holding their breath as well as their shares here, as the disposal is critical and the deal hasn’t gone through yet. In the six months ended February 2022, Rebosis’ net property income fell by 6%. The group has breached loan covenants, so all debt has been disclosed as short-term debt and a loan from RMB of R242.9 million is being renegotiated, with no certainty that this can be achieved. Rebosis is a highly speculative play and there are two classes of shares, so anyone considering a punt at Rebosis needs to do very detailed research first (even more so than normal).

Kibo Energy has announced the termination of its intended acquisition of the Victoria Falls Solar Project. The deal didn’t pass the due diligence process. Kibo has other exciting things underway, like a waste-to-energy project in South Africa and its partnership with CellCube to deploy long duration energy storage solutions. The group is also busy investigating substitutions for coal in projects in Tanzania, Botswana and Mozambique. If you are bullish on renewable energy, this is a company that you could spend some time researching.

Brikor (a brick manufacturing and coal business) released results for the year ended February 2022. Revenue is up 5.7% but EBITDA is down 64%. HEPS has fallen by 47.6%. The bricks segment had its best revenue result in the past five years. The coal segment had the opposite result, with revenue down 31.3% to its worst result in the past five years, attributed to excessive rainfall in the last quarter of the year. The brick business has performed “exceptionally” in April and May, with the coal business showing “significant improvement” in those months. The stock has low liquidity and has lost a third of its value this year.

Capitec announced that S&P has revised the outlook for Capitec Bank’s issuer rating from stable to positive, in line with the change made to South Africa’s sovereign outlook. Capitec’s issuer ratings were also reaffirmed by S&P. The ratings agency noted that Capitec’s funding and liquidity profile compares well with the sector and forecasts that the risk adjusted capital ratio will remain strong.

African Equity Empowerment Investments (AEEI) released interim results for the six months ended February 2022. Revenue fell by 8.9% and the headline loss got worse, deteriorating from R32.6 million to R69 million. AEEI reports a normalised headline loss number which looks even worse in percentage terms, coming in at R39.7 million vs. R6.4 million last year. No interim dividend has been declared.

Buffalo Coal Corp has barely any trade on the JSE, so I’ll just give it a passing mention here. In the three months ended March 2022, revenue increased 12% and the operating loss more than halved from R52.7 million to R24 million.

Imbalie Beauty has a market cap of R27 million, which possibly makes it the smallest company on the JSE. The headline loss for the year ended February was between 0.06 and 0.08 cents.

Prior to Advanced Health listing on the JSE, the CEO of Presmed Australia (Mark Resnik) was granted an option to subscribe for shares in the Australian business. Resnik has exercised that option through an investment company, with the effect that Advanced Health’s interest in Presmed has been diluted from 60.57% to 56.44%.

In case you feel bad about your life this morning, remember that Pembury Lifestyle Group is busy negotiating a reappointment of its auditors because it can’t even afford to pay outstanding audit fees. On the plus side, the Northriding property (initially a school) has been converted to a commercial building and leases have been concluded. Pembury is currently suspended from trading on the JSE.

Chris Gilmour writes weekly for Ghost Mail, sharing his international perspectives and on-the-ground insights into what the global investment community is focusing on.

South Africa’s infrastructure used to be highly regarded globally. Its road system in particular was world-class, as was its electrical utility company Eskom. Its water reticulation systems were easily the best in Africa. The rail system, though based on the quaint so-called “Cape gauge” track width of three foot six inches, nevertheless worked well.

But that’s all changed now.

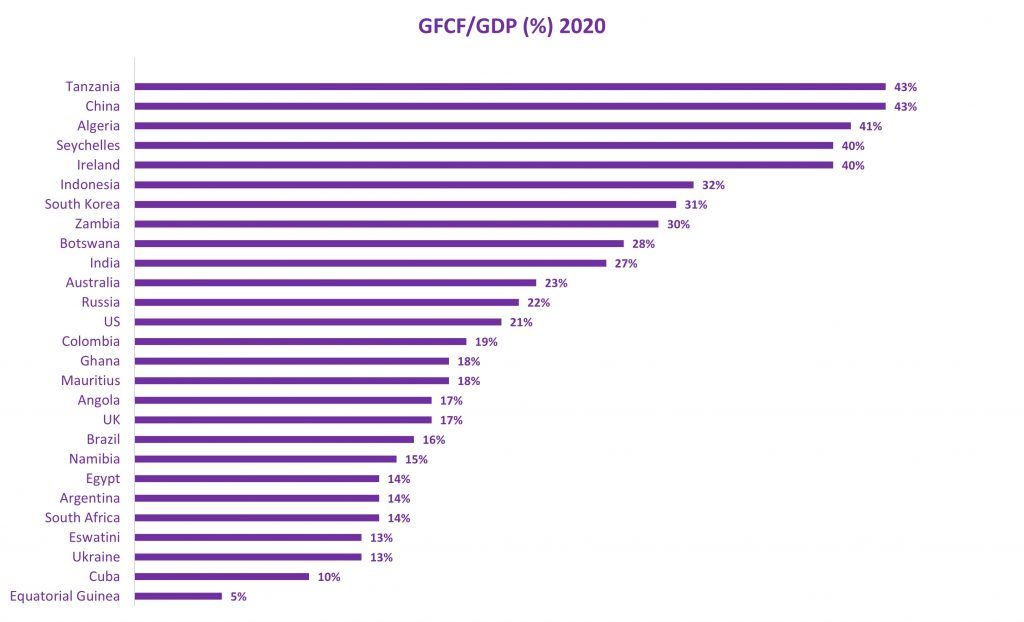

As a percentage of GDP, gross fixed capital formation (GFCF) reached a peak of 32% in 1976 and with the exception of the blip in the noughties associated with the FIFA World Cup stadium construction and the Gautrain, that percentage has been in secular decline ever since. At 14% in 2020, it was the lowest it had been since 1960. The average for all countries covered by the World Bank is 26%, so South Africa is a little over half the global average. In an IMF report on infrastructure earlier this year, it was reported that SA’s GFCF to GDP had reached an all-time low of 12.2% in 2021.

The net results can be seen in the badly potholed road system (apart from the arterial trunk roads, which still seem to be in reasonable condition), the fact that Eskom has now been indulging in rotational power cuts (loadshedding in Eskom-speak) for 15 years and the fact that many of the waterways are heavily polluted with raw sewage. Additionally, the rail tracks are literally being stolen from under our noses on an industrial scale.

It should come as no surprise that South Africa ranks extremely poorly in the World Bank’s ranking table of GFCF to GDP. Only Equatorial Guinea, a basket-case, Cuba (a failed state where little or no material infrastructure spend has occurred since the late 1950s), Ukraine and Eswatini have lower GFCF to GDP ratios.

Source: World Bank

But there may be light at the end of the tunnel, at least in certain areas of infrastructure development. The good news is that President Ramaphosa unveiled plans to materially boost SA’s infrastructure spend in late 2020. The bad news, according to a report released by Standard Bank on May 25 this year, is that a quarter of South Africa’s R340 billion worth of strategic infrastructure projects have been delayed or put on hold.

A recent article by Antoinette Oosthuizen from Futuregrowth Asset Management dimensions the impending water crisis in South Africa and offers practical solutions to that crisis:

“The challenges that confront the country are varied. Old/aging, poor quality and poorly maintained infrastructure is contributing to high levels of water wastage and the pollution of rivers and groundwater with sewage. Climate change is driving the country towards a warmer and drier future, with longer, more extreme droughts and more intense floods predicted.”

This is especially apparent given the tragedy of the recent widespread flooding in KZN, the worst natural disaster in South African history.

According to Oosthuizen, capital expenditure on the second phase of the Lesotho Highlands Water Project (LHWP-2) is expected to increase substantially from 2022/23, as construction ramps up. The combined debt of the augmentation schemes in the Vaal River System must be repaid within 20 years after completion of LHWP-2, with estimated water delivery in 2027.

Eskom appears to be an altogether more intractable problem, with a massive debt burden of just less than R400 billion compounding a host of operational issues. In addition, sabotage at the Tutuka and other power stations is causing a far greater incidence of rotational power cuts.

But even here, there are signs that things may be improving, at least from a broad perspective. Industry and the mines were recently given the authority to generate up to 100 megawatts of power internally. An increasing number of people who can afford it are migrating off the Eskom electricity grid via installation of rooftop solar panels and battery arrays. Even if Eskom is unable to put in new capacity, a far higher commitment to renewable energy development should help boost infrastructure spend.

According to the Standard Bank report, the rollout of one project – a plan worth billions of dollars to build 2,000 megawatts of new power-generation as quickly as possible – has been held up by court cases and Eskom. This couldn’t have happened at a worse time, as South Africa heads for a record year of disruptive rotational power cuts as Eskom is incapable of meeting even the current diminished demand for electricity.

The national road network is a SANRAL competency which it appears to be executing reasonably well, with a few exceptions. A new funding model will need to be found for the Gauteng Highway Improvement Project, as motorists have made it very clear that they are not prepared to pay via electronic gantries on a user-pays basis. The worst examples of potholes and other road degradation are to be found in the urban areas, where municipalities have been failing dismally to keep roads in good shape. As long as municipalities are regarded by certain political parties as an easy way to make money, this poor road situation is likely to persist.

Having said that, Raubex recently posted strong results and made mention of the SA government’s higher level of infrastructure spend.

This just leaves the national rail network. During the depths of the pandemic, a great deal of metal in the stations and on overhead power cables was stolen. It is only very gradually being replaced. Railtrack has been stolen and in certain areas, shacks have been built on the tracks. It is difficult to think of anywhere in Africa where a similar situation persists.

And for over a decade now, the Chinese have been making plans to establish a high-speed rail link between Johannesburg and Durban that would carry both passengers and freight. This would be constructed on international gauge track – the same width of track as Gautrain – but as yet is only really seen as a possibility in the minds of politicians.

This is a pity, as this is the stuff that dreams are made of. If a high-speed rail link could be established between Johannesburg and Durban that could cut the journey time from the current approximately 14 hours to nearer 4 hours, it could compete head-on with the airlines, when all-in logistics are taken into consideration. And for a developing economy such as South Africa, that is precisely what is required. Also, putting more freight back onto the railways and taking it off the roads would result in far less damage being done to the road network.

Considering how far South Africa has fallen on the global infrastructure ranking, even if only a few new big projects get commissioned in the next few years, the effect could be profound, albeit from a low base.It’s quite conceivable that SA’s GFCF/GDP could double in five years if everything manages to align. Here’s hoping.

I‘ve been a guest on the Honest Money podcast on two prior occasions. Warren Ingram and his team work hard to bring excellent insights on personal finance and investments to a wide audience. This is ultimately my passion as well, so I always welcome the opportunity to be on the show.

In my third appearance, Warren wanted to talk about my thoughts on active vs. passive investing. This is so important, as any wealth creation journey needs to at the very least include passive exposure to equities i.e. index tracking ETFs. The strategies can go far beyond that of course, with juicy ETFs that give exposure to interesting themes and the use of stock-picking strategies to add an active element to a portfolio.

As you know, I do all my investing through the EasyEquities platform. The great thing is that active and passive investments can be executed through an EasyEquities account. A tax free savings account is a no-brainer for all investors and only passive investments are allowed in that ring-fenced account. Again, this can be done through EasyEquities.

In this episode, we also touch on single stock portfolio diversification, rebalancing, the psychology behind risk trading and great tips and insights on how to maximize on your returns.

Listen to the show using the podcast player below:

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Companies do a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

I co-host these events with Mark Tobin, a highly experienced markets analyst who combines an Irish accent with deep knowledge in the Australian market (I know, right?) and the team from Keyter Rech Investor Solutions.

You can find all the previous events on the YouTube channel at this link.

The latest event saw Calgro M3’s executives presenting their business after posting an excellent set of results. For easy reference and more context to the session, you can refer to this article I wrote on the results.

Sit back, relax and enjoy this video recording of our session with Calgro M3:

In the current market environment, investing is incredibly complicated. As the longest bull market run in history comes to an end and inflation continues to rise steeply, investors are faced with the prospect of becoming poorer in real terms.

The increasingly difficult task of extracting alpha (excess returns in relation to the market) in traditional 60/40 (equities/bonds) portfolios is likely to further drive the popularity of alternative investments. According to Prequin research, the alternative investments industry is predicted to continue its surge from $13 trillion in assets under management today, to more than $23 trillion by 2026.

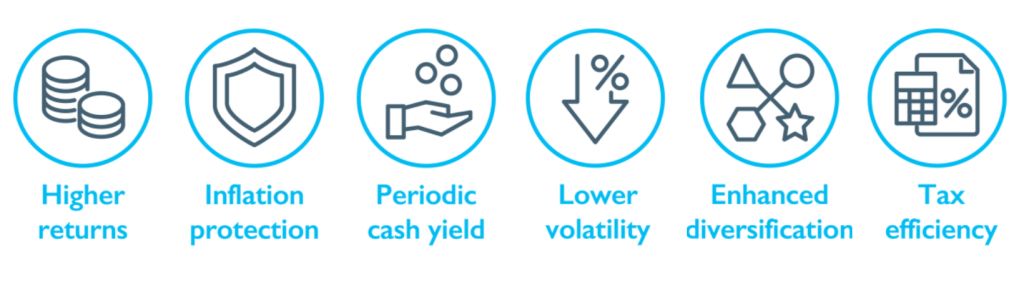

One of the world’s fastest growing alternative asset classes is private debt. When compared to traditional fixed income, private debt offers investors:

Investors are able to gain exposure to the asset class through Westbrooke’s local and offshore private debt funds (click here to find out more). In the offshore space, Westbrooke’s Yield Plus private debt fund is currently generating a trailing 12-month cash yield of 6.7% in GBP (net of fees and costs).

With a four year track record of successfully delivering returns within the target range of Cash + 5% – 7% in GBP, Westbrooke Yield Plus provides investors with a high yielding, fixed income alternative investment, through a diversified portfolio of 45 private debt transactions predominantly in the UK. The Fund delivers an asymmetric risk / return profile, by focusing on providing loans to lower and middle-market UK companies and real estate sponsors, a significantly under served UK market segment. Importantly, more than 70% of loans are floating rate in nature, providing investors with much needed inflation protection in the current environment.

It is our pleasure to invite clients to an exclusive offshore private debt overview webinar, in which we will be discussing the UK private debt industry, the Westbrooke Yield Plus offering and how you can gain exposure ahead of the 24 June investment deadline.

You can RSVP for the webinar by clicking on the image below.

The rand managed to claw back yesterday afternoon’s losses and eventually closed firmer on the day at R15.68 as the euro and pound both bounced against the dollar. The local currency touched an intraday weakest level of R15.86 before the turnaround by the dollar.

The rand is trading a touch firmer at R15.67 this morning on the back of a lower dollar. Yesterday’s local PPI data showed prices at the factory gate increasing at a faster pace. The YoY number grew by 13.1% vs. market estimates of 12.3%.

The Russian central bank slashed interest rates by 3.0%, from 14.0% to 11.0%, in an effort to slow the sharp rally in the Ruble.

Commodity update

Gold ended flat yesterday while there were small gains for both Platinum and Palladium. This morning we have Gold and Platinum trading unchanged at $1,852 and $949, respectively, while Palladium is up 0.8% at $2,022. Tight supply continues to push the Oil price higher, with Brent quoted at $117.60 and WTI at 114.20.

International update

The DXY index has slipped to 101.5 as the dollar falls to 1.0758 against the euro and to 1.2650 against the pound. Traders are starting to lower their expectations for more aggressive rate hikes by the Fed as US economic growth starts to slow.

US treasury yields are consolidating below recent 20-year highs, and there have been some investors exiting their long Dollar positions. Wall Street rallied again yesterday, with the Nasdaq leading the way. The Nasdaq gained 2.68% and the Dow ended 1.61% higher. Asian stocks are following the positive move on Wall Street with all markets in the green, while US futures have opened largely flat this morning.

Lewis Group released results for the year ended March 2022. This business has been so disciplined in recent years, focusing on its core business and using share buybacks to take advantage of stubbornly low valuation multiples. Since 2017, Lewis has bought back 26 million shares at an average price of R31.82 per share, far below the current share price of around R51. This has the impact of supercharging HEPS growth, as the denominator shrinks over time (provided the share buybacks were done when the shares were cheap). Revenue in this period increased by 7.9% and HEPS grew by 37.7%. The cash flows look strong (with metrics in the debtors book going the right way), allowing the dividend to be increased by 25.9% to 413 cents per share (so Lewis offers the kind of yield usually reserved for REITs). A point worth noting is that credit sales grew by 16.7% and cash sales only increased by 6.4%. The gross margin performance was impressive at 40.5% vs. 41.8% the prior year, a low decrease considering the supply chain and inflationary pressures.

Nampak has released results for the six months ended March 2022. Revenue is up 24%, operating profit is 26% higher and HEPS has approximately doubled to 35.6 cents per share. As I keep pointing out in many company results, balance sheets are growing because of inflation, with Nampak investing R653 million in working capital. Covenants have been complied with.

Spear REIT has released results for the year ended February 2022. This is a solid little REIT with a portfolio focused on the Western Cape, which helps it trade at a yield that would normally be seen at bigger funds. The distribution per share has increased by 16.26% this year, with an average pay-out ratio of 88% vs. 80% in the prior year. This is a sign of increased confidence in the overall environment. There are still negative reversions at play (average of 5.57% excluding hospitality which had a positive reversion) but Spear looks to be in good shape. The loan-to-value at 39.05% (down sharply from 45.81% in February 2021) is still a bit high for my liking but has moved in the right direction. The net asset value (NAV) per share is R11.30 (down 2% this year) and the share price is trading at around R7.95. This is a discount to NAV of around 30% and a trailing dividend yield of 8.6%.

Although Barloworld is facing great uncertainty in its Russian business, the group’s balance sheet is strong and they want to take advantage of the depressed share price. Barloworld will buy back up to 10% of its issued shares, which will give huge support to the share price. In addition, the CEO has bought R2.3 million worth of shares through his trust. As they say – there are many reasons why directors sell shares, but only one reason why they buy.

Grindrod’s share price closed 9.8% higher after an announcement that Grindrod Bank will be sold to African Bank. The African Bank curatorship story has been a success, as the bank is now on a stable footing. Its shareholders are the South African Reserve Bank (50%), the Government Employees Pension Fund (25%) and a consortium of local banks (25%). This deal will allow Grindrod to focus on its freight businesses and will give African Bank an entry into the business banking market. This is a R1.5 billion deal that will give a solid boost to Grindod’s balance sheet and investment war chest. The net asset value for the bank as at 31 December 2021 was R1.67 billion and profit after tax was R109.4 million. The transaction will take a while to close, as this is a Category 1 deal for Grindrod (requires >50% shareholder approval) and a number of regulators will need to approve the deal.

Mr Price has released a trading statement for the year ended 2nd April 2022. Retailers often have reporting periods that end on strange dates, as they report based on weeks rather than calendar months. Every few years we see a 53-week reporting period instead of the usual 52-week period. FY21 was one such period, so comparisons need to be made on a 52-week basis or the numbers are skewed by an extra week of trading in the base. On that basis, diluted HEPS is up between 22% and 27%. This period included the acquisitions of Power Fashion (1 April 2021) and Yuppiechef (1 August 2021) which were bought for cash. This has a positive impact on HEPS as the earnings are added to the group but no new shares are issued.

Net 1 UEPS Technologies has changed its name to Lesaka Technologies, which is far less of a mouthful and reflects the African strategy going forward. The ticker has changed to JSE: LSK. The share price rallied 9%, so perhaps the best strategy is to just keep changing the name. If the company updated its website from a design that looks like it came from the 90s, it might rally another 9%.

Life Healthcarehas released interim results for the six months ended March 2022. Revenue from continuing operations increased by 4.2% but normalised EBITDA fell by 1.9%. This is unusual in the sector, as the likes of Mediclinic are seeing an increase in margins. The negative impact on Life’s margins was from the ending of Covid-related support services in the international operations. In South Africa, normalised EBITDA increased by 7.5%. HEPS has decreased by 12.7%. Net debt to EBITDA has improved to 2.03x from 2.78x a year ago. The good news for investors is that the interim dividend per share is back, with a 15 cents per share dividend declared. The share price was trading nearly 2% higher in afternoon trade at around R18.70.

Stefanutti Stocks released results for the year to February 2022. Contract revenue is higher and so are the losses, which isn’t great news. The loss from operations is R415 million of which R263.7 million is from continuing operations. Clearly, this group needs to achieve a turnaround or it will cease to exist. The group is focused on restructuring the balance sheet, which means renegotiating debt terms and extending facilities to try create some headroom. The problem is that there have been delays in sales of operations and delays in resolving certain issues. The company simply doesn’t have enough margin for error for more issues to crop up. To call this R110 million market cap group a “speculative” play would be an understatement.

Old Mutual has released a voluntary operating update for the period ended March 2022. Life insurance sales were up 19% and the value of new business was 53% higher with a 70 basis points improvement in margin. Funds under management fell by 3% though. There are strong growth numbers coming out of Africa. The really good news is that no additional provisions have been raised for Covid mortality claims, with the latest wave tracking well within provisions. The net impact (i.e. after reinsurance) on Old Mutual Insure from the KZN floods is between R100 million to R150 million.

African Media Entertainment (AME) has released a trading statement for the year ended March 2022. Radio assets had a terrible time in the pandemic, with a huge drop-off in advertising and no live events to generate extra revenue. In this period, HEPS is expected to be between 350 cents and 390 cents, way up from 112.7 cents in the prior year. This illiquid stock is trading on a Price/Earnings multiple of around 8x based on the mid-point of the guidance.

Hosken Consolidated Investments, the JSE-listed investment entity led by Johnny Copelyn, has released a further trading statement confirming a substantial improvement in fortunes. HEPS for the year ended March 2022 has jumped to between 1,292.5 and 1,350 cents. It was just 287.7 cents in the prior year, so the percentage jump isn’t relevant. What is relevant is that the share price closed 6.6% higher and that was before this announcement even came out, so there may be more action in the stock on Friday.

Deneb Investments has released results for the year ended March 2022. Revenue increased by 13.3% and HEPS jumped 43% to 33 cents per share. The dividend is 29% higher at 9 cents per share. Deneb is involved in property, branded product distribution (including toys and stationery) and manufacturing businesses. The controlling shareholder of Deneb is Hosken Consolidated Investments (HCI).

eMedia Holdings, which owns e.tv, YFM and other media businesses, has released results for the year ended March 2022. The commentary managed to say “resounding bounce back” twice in the opening lines, which gives you an idea of how happy they are. Profits are much higher than in 2020 and 2021, driven by a record revenue performance and a 39% year-on-year increase in TV advertising revenue. I guess that taking a position in eMedia means you are betting against the SABC, which isn’t exactly difficult to justify. Overall, it’s great to see traditional media making a comeback after social media platforms dominated during the pandemic. The controlling shareholder of eMedia is Hosken Consolidated Investments (HCI).

Frontier Transport Holdings has released results for the year ended March 2022 and they look great – revenue is up 26.8%, HEPS is up 29.6% to 90.75 cents and a dividend of 52 cents per share has been declared. This company is best known for owning Golden Arrow Bus Services. Over 80% of shares are held by Hosken Consolidated Investments.

ArcelorMittal has reached a speedy resolution to its wage dispute. It only took two weeks to sort out, with ArcelorMittal agreeing to a 6.5% increase in all remuneration elements, a R5,000 once-off ex-gratia payment and a backdate of the remuneration increase to 1 April 2022.

Platinum group metals (PGM) and chrome miner Tharisa has released interim results for the six months ended March 2022. Production numbers for PGMs and chrome are higher which is important. Revenue increased by 6.5% and EBITDA fell by 10.4% as the group came under cost pressures, especially from diesel costs. This drove a 29.2% decrease in HEPS. An interim dividend of $0.03 per share has been declared. Tharisa is busy with some major investments (including a controlling interest in Karo Mining Holdings) and is focused on maximising production to try and minimise the impact of cost pressures.

In related mining wage news, Anglo American Platinum has signed a five-year wage deal with three of the four unions. This covers 90% of unionised employees. The total labour cost-to-company will increase on average by 6.6% per annum over the period.

Tsogo Sun Hotels and Tsogo Sun Gaming are taking a big step away from each other. After Tsogo Sun Hotels unbundled Tsogo Sun Gaming, the former was appointed to manage seventeen hotels belonging to the gaming group. Tsogo Sun Gaming wants to terminate the agreements, which Tsogo Sun Hotels agreed to for fifteen hotels in return for a payment of R398.8 million. Tsogo Sun Hotels will buy the remaining two hotels for R141.6 million. This is a net cash inflow of around R257 million for Tsogo Sun Hotels. As Hosken Consolidated Investments (yes, them again) is involved in both companies, this is a related party transaction that will require a fairness opinion. Thankfully, Tsogo Sun Hotels is in the process of changing its name to Southern Sun Limited.

Separately, Tsogo Sun Hotels is selling a 75.55% stake in a hotel in Nigeria for $30.4 million. The rationale behind the deal is to get rid of USD-denominated debt in the group. The hotels only contributed $0.7 million in attributable headline profit in FY22.

In the final update for the day from a Tsogo company, Tsogo Sun Gaming released financial results for the year ended March 2022. Against a Covid-infested base, income increased 57%, operating costs increased 47% (as the group started operating again) and EBITDA (the one that counts) was 80% higher. Most importantly, a headline loss of R32 million has swung into a R1.15 billion headline profit. HEPS is 110.2 cents, which puts the group on a Price/Earnings multiple of 10.9x. Debt to adjusted EBITDA is 2.89x, which is only slightly better than the covenant of 3.0x. The group doesn’t expect to have a problem meeting these covenants as the group is generating cash.

Labat Africa has upgraded its cultivation facility in Kenton-on-Sea, known as Sweetwaters. This cannabis business has secured offtake agreements in Europe and Australia for cannabis products. The first harvest of 1.2 tons in wet weight product has yielded 100kgs in dry weight. The plan is to increase production capacity from 500kgs to 1.8 tons per year in dry weight. A EU-compliant manufacturing facility will also be set up at the site with the assistance of a German pharmaceutical company. The share price jumped 10% based on this update.

A director of Raubex has acquired shares in the company worth R682k. Investors always see buying by directors as a positive sign.

MiX Telematics has reported its full year IFRS results (as the group is also listed on the New York Stock Exchange and that requires US GAAP). The accounting rules can be incredibly different in certain aspects. Annual recurring revenue is up 9.1% and the group now has 815,200 subscribers. Adjusted EBITDA of R513 million represents a 24.1% margin. Free cash flow is one to watch here, as the group generated R323.9 million in net cash from operating activities and invested R409.6 million in capex, so there was negative free cash flow of R85.7 million. The CFO is moving on from the company after joining in 2019, which isn’t a long stint at all. An internal replacement has been announced. After HEPS fell from 0.44 cents to 0.24 cents, there will be a lot of work ahead.

Back in 2012, Italtile lent an interest-free loan to the Ceramic Foundation Trust for R120.6 million. This is a typical B-BBEE deal structure. The loan should be repayable in August 2022, but only R30 million has been repaid to date. Normally, the trust would sell enough Italtile shares to cover the loan. Italtile doesn’t want this to happen or its B-BBEE score will diminish, so the loan has been extended by a further 10 years. Most of these fully leveraged B-BBEE structures don’t manage to pay the debt and end up selling shares to settle whatever is left. It’s unusual to see an extension like this but it makes sense for all concerned.

There’s a new Chairman at Jubilee Metals and some changes at executive level, as the company puts the building blocks in place for its global development plan.

Northam Platinum has raised R2.06 billion in new domestic medium term notes under the R15 billion debt programme. It has also extended the maturity of notes to the value of R1.17 billion by more than 2 years. When combined with previous issuances, the nominal value of notes in issue under the programme is R11.36 billion. R102 million will mature in this financial year, with the rest spread out across 2023 – 2026.

Altron’s disposal of Altron Document Solutions was scheduled to close by 31 May 2022. As regulatory approvals are outstanding in certain jurisdictions, the deadline to fulfil all conditions precedent has been extended to 31 August 2022.

African Equity Empowerment Investments has released a trading statement for the six months ended February 2022. The headline loss per share has deteriorated significantly from -6.64 cents in the prior period to between -13.39 and -14.71 cents in this period.

Mahube Infrastructure expects HEPS to be between 117.85 cents and 120.02 cents for the year ended February 2022. This is a massive jump from 21.71 cents the prior year.

Etion has disposed of its Original Design Manufacturing company, Etion Create, to Reunert subsidiary Reunert Applied Electronics for an estimated R197 million. Etion Create manufactures customised electronic subsystems and products across a range of sectors including Mining and Industrial; Defence and Aerospace; Internet of Things and Sensors; and Cyber Security.

Capital & Regional plc, the UK convenience shopping centre REIT, has exchanged contracts for the sale of The Mall, Blackburn to the retail arm of Adhan Group of Companies in a cash deal of £40 million. The net proceeds will be used to repay debt secured on the property.

Deneb Investments’ sale of its property in Worcester, Breede Valley, Western Cape to GS Prospects for R43,5 million will not proceed as the transaction was conditional on the purchaser obtaining a loan against the registration of a first mortgage bond over the property. The condition precedent was not fulfilled by the stipulated date.

Tradehold is to implement a disposal which will reduce the complexity of its current corporate structure. The company will dispose of its entire shareholding in Moorgarth Holdings (Luxembourg) which holds all the group’s interests in the UK. The disposal to newly incorporated Moorgarth Holdings for £102,5 million is a related party transaction as certain directors of Tradehold are shareholders in the purchaser.

As part of its strategic initiative to expand on its rental portfolio, Balwin Properties is to repurchase the 75% equity stake in Balwin Rentals from Yieldex Trading 2 for a purchase price of R18 million.

Raubex and Bauba Resources have announced the extension of the closing date of the mandatory offer to shareholders to June 10, 2022. Raubex, acting in concert with Pelagic made an offer to shareholders of R0.42 in February.

Sable Exploration and Mining has updated shareholders on its proposed deal with Magni Investment and Lurco Metals announced in Q4 2021. Due to non-fulfilment of certain conditions precedent, the transaction will not proceed.

Unlisted Companies

Ironweed plc, a UK exploration and development company incorporated in England and Wales is to acquire Ferrochrome Furnaces, located in Rustenburg, out of business rescue for a nominal fee (R980) and the purchase of outstanding debt (R115 million) from the sole creditor. Upon completion, a further R100 million will be paid over 10 years based on a share of profits from the smelter facility capped at 13.5% per annum.

Imvelo Ventures has made a follow-on investment in Acumen Software. The undisclosed Series B funding has been used to expand the services of the My Smart City platform.

Energy giant Électricité de France (EDF) has announced the planned acquisition of a 50% stake in Cassava Technologies business Distributed Power Africa. The partnership will develop hybrid energy solutions for businesses in SA. EDF is already active locally in the low-carbon generation, transmission, distribution and energy efficiency services. Financial details were undisclosed.

Phatisa, the African private equity fund manager, is in the news again this week, this time as part of a consortium of leading development finance institutions to acquire a significant minority stake in South Africa-based citrus and fresh-produce exporter Lona Group. The other parties to the undisclosed investment were British International Investment, Norfund and Finnfund. The funds will be used for expansion capital to drive growth and investment into cutting-edge sustainable food production.

Edtech and entrepreneur education company Genius Group has acquired E-Squared Education Enterprises, an Eastern Cape-based entrepreneur-focused primary and secondary school and vocational college. Financial details were undisclosed.

South African edtech startup FoondaMate has raised US$2 million seed funding in a round led by UK venture capital firm Local Globe. Other participants include Emerge Education, FirstCheck Africa, LoftyInc Capital Management and Future Africa. The startup targets high school students in emerging markets where WhatsApp is used as cheaper to use or free to access. The funds will be used to scale its WhatsApp and Facebook-based learning chatbot across the globe.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.