Orion Minerals has signed an exclusivity agreement (90-day exclusivity period) with Stratega Metals which will undertake a technical due diligence on its Jacomynspan Nickel-PGE Project in the Northern Cape. Orion has the exclusive right to enter into an earn-in agreement to earn a 75% interest in Stratega by funding construction of a demonstration-scale refinery.

Capital & Counties Properties released an announcement to shareholders following recent press comment, to confirm that it is in discussions with Shaftesbury plc for the possible £3,6 billion merger to create a REIT focused on the West End of London with a portfolio of c.2,9 million square feet of lettable space.

Unlisted Companies inq., a pan-African cloud and digital service provider, is to acquire Syrex, a local provider of hyper-converged cloud technology solutions for an undisclosed sum. The strategic acquisition comes at a time when Edge services are increasingly critical to digital transformation and fundamental to enterprises across the public and private sectors.

10X Investments is to acquire CoreShares in an undisclosed all-cash deal. The transaction will crate a full service South African indexing investment specialist with c.R31 billion in assets under management.

DealMakers is SA’s M&A publication www.dealmakerssouthafrica.com

Grand Parade Investments (GPI) has taken the decision to exit the restaurant business and will unbundle the company’s stake of 9.28% (8,447,731 shares) in Spur to shareholders by way of a pro rata distribution in specie in the ratio of 1 Spur share for every 63 GPI shares held. The stake is valued at R174 million, based on the current share price of Spur of R20.65 which is equivalent to 37c per GPI share. The company will be left with its stake in gaming businesses SunWest, Golden Valley Casino and Sun Slots.

Afristrat Investment has advised that in a move to address liquidity constraints, it will commence a capital raise process to raise R60 million in cash funding from its current shareholder base. The funds will be used to settle long standing debt of c.R25 million, provide R15 million in working capital to be used in the next 12 months and R20 million to support and provide a catalyst for growth of the remaining investments of the company.

Argent Industrial repurchased 40,032 ordinary shares during March for an aggregate value of R521,118.

Net1 Technologies, which is listed on the JSE and Nasdaq, has received shareholder approval to change its name to Lesaka Technologies.

Steenkampskraal, a rare earths project in the Western Cape, has announced it is to seek a secondary listing on the JSE through a pre-initial public offering. The company also intends to list on AIM. The company will produce and sell monazite concentrate initially and progress to producing and selling mixed rate earth concentrates and separated rare earth oxides.

A number of companies listed on one of South Africa’s Stock Exchanges have initiated share buyback programmes and each week update shareholders. They are:

Investec Ltd has completed its share buy-back programme announced in March repurchasing 1,537,823 preference shares at R96,37 per share for an aggregate R148,2 million. The preference shares will be de-listed from the exchange.

Pan African Resources announced the initiation of phase one of a share buyback programme to purchase up to R50 million (£2,6 million) worth of ordinary shares over one month commencing April 1, 2022. Purchases took place on the LSE and JSE. The company repurchased in aggregate 11,825,491 ordinary shares for a total consideration of R50,3 million. A total of 7,568,744 shares were acquired on the LSE at a volume weighted average price of 21.67 pence per share and 4,256,747 shares on the JSE at a VWAP of 418.21 cents per share. All shares purchased under the programme have been cancelled.

As part of the repurchase programme announced on March 24, 2022, Reinet Investments has repurchased a further 285,271 ordinary shares at an average price of R313.34 per share for a total consideration of R89,4 million (€5,4 million)

Glencore this week repurchased 2,530,842 shares for a total consideration of £12,1 million in terms of its existing buyback programme which is expected to end in August 2022.

This week British American Tobacco repurchased 2,143,612 shares for a total of £71,36 million. The purchased shares will be held in treasury with the number of shares permitted to be repurchased set at 229,400,000.

Two companies issued cautionary notices to shareholders this week. The companies were: Trustco and Afristrat Investment.

Wintershall Dea, a European independent natural gas and oil company, is to acquire an additional 11.25% participation interest in the Reggane Nord natural gas project in Algeria. The stake is to be acquired from Edison International for an undisclosed sum. The acquisition will increase Wintershall Dea’s stake to 30.75%. Other members of the consortium are Sonatrach (40%) and Repsol (29.25%).

Coromandel International headquartered in Hyderabad, India, is set to acquire a 45% equity stake in Baobab Mining and Chemicals, a rock phosphate mining company based in Senegal. Coromandel will pay US$19,6 million for the stake in Baobab plus a loan of US$9,7 million. The investment will strengthen Coromandel’s backward integration and will ensure long term supply security of the raw material.

The International Finance Corporation (IFC) has acquired a 6.71% stake in Equity Group, a financial services holding company headquartered in Nairobi. The IFC will inject US$164 million towards Equity’s programme which aims to finance c.5 million MSMEs and c.25 million households.

Private equity firm SPE Capital has, as part of a consortium with Amethis and the European Bank for Reconstruction and Development, acquired Global Corp for Financial Services S.A.E, an Egyptian non-banking financial services company. Financial details were undisclosed.

Badili, a Kenyan online smartphone buy-back platform, has raised US$850,000 in a pre-seed funding round. Badili acquires old mobile phones, refurbishes them and on sells them to consumers looking for a cheaper alternative. The funds raised will be used to acquire inventory, tech enhancement and establish an offline presence through brick-and-mortar stores across Kenya.

Nigerian identity verification startup Identitypass, has raised US$2,8 million in seed funding in a round led by MaC Venture Capital. The funds will be used to roll out new verticals around compliance, security and data collection with the aim of expanding into other African countries.

Mylerz, an Egyptian-based last-mile delivery startup, has closed a US$9,6 million round led by private equity firm Lorax Capital Partners. The funds will be used to scale the startup’s presence in North Africa and support the construction, by year-end, of a new AI-enabled, automated cross-docking fulfilment centre in Cairo.

Interswitch, an African-focused integrated digital payments and commerce company facilitating the electronic circulation of money between individuals and organisations, has secured a US$110 million joint investment from LeapFrog Investments and Tana Africa Capital. The investment will be used to drive Interswitch’s pan-African strategy which will include growing the customer base and building new products to support a financial inclusion strategy.

Kaltani, a Nigerian clan-tech plastic waste recycling company, has raised US$4 million in seed funding to be used to scale the business by increasing the number of collection and aggregation centres across Nigeria.

Nigerian fintech startup Kwaba, has secured an undisclosed sum in a pre-seed round of funding led by Co-Creation Hub. Kwaba assists low- and middle-income earners manage monthly rent payments, bridging the gap between property and finance. The funds will be used to increase its footprint across the continent.

Paymob, an Egyptian fintech, has raised US$50 million in Series B funding in a round led by PayPal Ventures, Kora Capital and Clay Point. Paymob enables merchants to accept digital payments online and in-store. Funds will be used to scale the business in Egypt and across the MENA region.

On an otherwise revolting day in the markets, Sappi put its best foot forward with an excellent quarterly update for the period ended March 2022.The share price closed 3.8% higher.

On a quarterly and six-month basis, revenue is up 45% year-on-year. EBITDA is flying, up 201% on a quarterly basis and 175% on a six-month basis (both numbers year-on-year).

As you might have guessed, there is a Covid-impacted base effect here. In the six months to March 2021, Sappi recorded a net loss of $40 million. In the latest six months, Sappi achieved net profit of $311 million. Take note that Sappi reports in USD.

The balance sheet also looks better, with net debt 13% lower at $1.79 billion. This was achieved by a major positive swing in net cash generation (+$105 million vs. -$53 million in the prior year). As I keep seeing across the board, working capital increased due to inflation and the resultant increase in inventories and accounts receivable.

Headline Earnings Per Share (HEPS) for six months of $0.58 per share equates to around R9.40 at current exchange rates. The share is trading at around R62, so this is an annualised Price/Earnings multiple of around 3.3x. That may sound incredibly cheap at first blush, but you need to remember that this is a cyclical stock, so you always have to be careful with multiples.

For example, “tight global paper markets” were a major contributor to this result, giving Sappi pricing power in a time of high inflation. Volumes in the pulp segment were up 9%, so the company responded well to the opportunity in the market. The graphic paper segment recorded 12% volume growth and ran at full capacity, implementing a series of selling price increases along the way. The packaging and speciality paper segment grew volumes 13% and achieved some margin expansion, but certain contractual commitments limited the ability to restore margins to normalised levels.

Capital expenditure is expected to be $395 million for FY22.

In terms of outlook, pricing conditions largely remain favourable. Due to scheduled maintenance and damage to infrastructure in KZN that has impacted access to the Port of Durban, volumes will come under pressure in the second half of the year. Overall, the company has guided underlying EBITDA for the third quarter that is in line with the second quarter.

Sappi is up nearly 32% this year and more than 40% over the past twelve months.

South Africa’s State of Disaster was officially lifted by President Ramaphosa on Monday, 4 April 2022. Most South African investors and dealmakers would say it was a two-year period that they would hope never to repeat. But if the ongoing global uncertainty and flux has revealed anything, it’s never to say never.

The following article offers insight into what happened on the ground in dealmaking during South Africa’s State of Disaster, and what it takes to implement deals under significant economic challenges.

Following Ramaphosa’s announcement of the country’s “hard lockdown” on 23 March 2020, most sectors adopted a wait-and-see approach. Many companies focused internally, taking stock of their current situation, and looking at responsive risk-mitigation strategies. Hindsight indicates that this period of contemplation was valuable time lost, as Corporate South Africa immediately stopped payments during the hard lockdown to preserve their bottom lines. Some companies were never to recover. By the first half of 2021, almost 1000 South African business liquidations were recorded.

Dealmaking hit a massive ten-year low around the world in 2020, as deals were swiftly put on hold. But 2021 saw a massive improvement. According to PriceWaterhouseCoopers, the deals that were announced globally in 2021 exceeded 62 000, up an unprecedented 24% from 2020. Africa had its fair share in what was a “stellar year”, with deal value exceeding $85 billion (R1.3 trillion) and volume reaching nearly 1000 deals. Deals in new technologies emerged as having the most exciting potential.

Although statistics provide a broad overview of the pandemic’s impact on dealmaking, it is also important to understand what happened “on the ground” during this time. Practices that are successful in times of constraint and uncertainty can provide a valuable roadmap from which to navigate the next market shock.

During the State of Disaster, corporate financiers and dealmakers who responded differently to the mainstream were able to reap benefits. At investment banking firm Bravura, an immediate and intensive analysis of the market was undertaken in order to identify six or seven key focus areas where opportunities might exist.

Following their identification, these areas were tested among existing and prospective clients. Those areas that had no immediate traction were quickly discarded, while the remainder were proactively presented to the firm’s network and put through further rigorous desktop research. The strong combination of driving relevant angles with an elaborate network of entrepreneurs, listed companies and capital providers yielded the initiation and implementation of several transactions.

As people became accustomed to the new operating conditions in “lockdown”, following the first two months of near-total economic standstill, the market began to recognise that there were opportunities for transacting. For many dealmakers, there was an expectation that companies would be responding to distressed situations. However, the inundation of distressed equity or debt raises and asset sell-offs actually did not materialise. Other interesting opportunities emerged.

Such an opportunity came through listed companies on the Johannesburg Stock Exchange (JSE) that were sitting with valuations that were dropping to all-time lows. Prior to 2020, the JSE was already under-priced, with share prices rarely reflecting fair value. But the pandemic saw discounts (particularly for small and mid-caps) becoming deeper and valuations further depressing. Responding to the financial challenges wrought by the lockdown, investors began to consider alternative strategies such as share buybacks or taking businesses private in order to optimise value for stakeholders.

Contrary to the state of play on the JSE, global markets were hitting all-time highs, with debt cheaper and more accessible than ever before. This created interesting opportunities for local private equity firms that were sitting on portfolio companies which, due to end-of-life, required divestment. With international financial and strategic parties seeking yield, the environment was flush with potential. This further enabled parties to successfully re-engage on previous deals that had run aground.

During the pandemic, certain sectors grew disproportionally. IT, fintech, ecommerce and financial services developed intrinsic growth and solid fundamentals, both in South Africa and Africa. This growth has created an ongoing need for continued capital raising.

In 2021, a year into the State of Disaster, the market was ablaze with activity as dealmakers who were actively in-tune took advantage of market opportunities. Although 2022 continues to hold good prospects for dealmakers, this will be tempered by geopolitical tensions, run-away inflation and increasing interest rates.

For Corporate South Africa, the past two years have been a tough lesson in how to react to market shocks. In 2020, market uncertainty created a static response. Hindsight reveals that it might be better for companies to think swiftly and take action rather than sitting tight. When there is uncertainty, the market itself is unsure of the next steps – thus it is not always wise to follow what the market does. Flexibility and innovation should be harnessed when engaging with what may seem like insurmountable obstacles. If companies are unsure of their next steps, turn to experts who have an ear to the ground and understand the environment; they may see what is yet to be visible.

Rob Bergman is a Corporate Finance Principal | Bravura

This article first appeared in DealMakers, SA’s quarterly M&A publication DealMakers is SA’s M&A publication www.dealmakerssouthafrica.com

Sappi has released a great quarterly update, with revenue for the last six months up 45% year-on-year and EBITDA up a whopping 175%. There’s a base effect here from Covid of course, but the company has risen to the occasion with strong production numbers when it has really mattered. I’ve written a feature article on these numbers here.

Harmony Gold is under pressure. The Hidden Valley mine in Papua New Guinea knocked production numbers heavily and there are underlying challenges in the South African operations as well. On the plus side, net debt has been reduced over the past nine months and the group has reiterated full year guidance. Get all the important details in this feature article.

Deutsche Konsum REIT is a specialist property fund focused on regional retail centres in Germany. In the first half of the current financial year, rental income increased 10% and net profit increased 13%. Funds From Operations (FFO – a key measure in this sector) increased by 4%. More than 80% of income is inflation-linked which is obviously great in this environment. The fund has executed acquisitions of 15 retail centres for a total of EUR49.4 million in this six-month period. The net loan-to-value (LTV) ratio is 53.9% which is above the target of 50%, so the fund may look to deleverage i.e. pay down some debt. Guidance of FFO for the full year of between EUR40 million and EUR44 million has been reiterated.

Redefine Properties released a trading statement noting that distributable income per share for the first half of 2022 should be 26.33 cents per share, an increase of 0.6% year-on-year. This doesn’t warrant a trading statement as the percentage change is so low. The reason for the update is that the interim dividend is back in action, with a dividend per share for this period of 23.69 cents per share vs. no dividend in the comparable interim period.

Spear REIThas finalised the acquisition of 27 Junction Road, Parow for R65 million. Pepkor has been signed as a tenant for 10 years and 9 months. This is in line with the fund’s industrial strategy in the Western Cape.

enX Group has released a trading statement for the six months to February 2022. HEPS from continuing operations is between 79% and 100% higher than the prior comparable period. Total earnings (i.e. including discontinued operations) is difficult to work with for this period as there were disposals in both this period and the comparable period. Continuing operations give a better sense of how the group is performing, with revenue up 17% and operating profit up between 55% and 59%.

Afristrat Investment Holdings has lost a fortune on MyBucks – around R1.5 billion! In a detailed announcement, the company set out how amounts in the company were used inappropriately or in a manner not approved by the board. There are numerous examples of alleged control failures. Afristrat has instituted a civil claim of R250 million against the former executives and R800 million against MyBucks. Afristrat also confirmed that it cannot make any payments of interest or capital to noteholders. The company will propose to noteholders and preference shareholders that they convert to ordinary shares in Afristrat. The company will try raise R60 million in equity, of which R25 million is for long outstanding creditors, R15 million is for legal fees and R20 million is for growth in the underlying investments of the company. Afristrat’s largest shareholder (MHMK Group Limited) will underwrite R15 million of the R60 million. This is a perfect example of how things can go badly wrong for a listed company.

Pan African Resources has completed Phase 1 of its share buyback programme. The company dipped its toes in the water with a R50 million buyback vs. a current market cap of around R8.75 billion. With the share price down nearly 14% in the last month, the average price for the buyback is higher than the current traded price.

ISA Holdings, an IT security business, has updated its trading statement for the year ended February 2022. HEPS is expected to be between 10.06 cents and 10.89 cents, an increase of between 21.2% and 31.2% vs. the prior year. The share price is at R1.10 and has very low liquidity.

Raubex CEO Rudolf Fourie will retire at the end of July. Felicia Msiza has been appointed as the new CEO and the company has used this opportunity to also create a COO role which will be filled by Dirk Lourens, another internal appointment. Fourie has been with Raubex for 25 years and it is encouraging to see an internal succession plan playing out.

DRA Global has announced a sudden change of CFO. There’s an internal appointment as Acting CFO which gives some stability, but a seemingly unplanned change at executive director level is always a red flag for governance.

The Chair of Quilter Plc, Glyn Jones, has stepped down. Ruth Markland has been appointed into the role. In case you aren’t familiar with the company, Quilter was separately listed as part of the Old Mutual restructure (or “managed separation” according to the corporate PR specialists). Quilter is essentially a rebrand of Old Mutual’s UK wealth management business. The business operates in two segments (Affluent and High Net Worth) and has performed well in the past year financially.

If you are familiar with the JSE Listings Requirements (or just curious about them), then you may be interested in the consultation paper issued by the JSE with amendments designed to “cut red tape” for listed companies. You can find it at this link.

Not much has changed overnight, with the rand and other EM’s still trading sideways ahead of today’s US CPI print which is expected to read 8.1% YoY. We open this morning with our local currency trading at R16.08 against the dollar, R16.95 against the euro, and R19.83 against the pound. Earlier this morning, we saw that China’s inflation surged by 2.1% during April as higher energy costs and a pick-up in demand for fresh produce led to rising food prices. Equity markets in the east have all closed higher this morning, with the Shanghai Composite and Hang Seng closing around 1.7% higher.

Commodity update

A rampant dollar and higher US Treasury yields are still impacting gold’s price, and we see the yellow metal trading at $1,838 this morning. Platinum is quoted at $977, while palladium is still flat from yesterday and hovering around $2,070. Base metals are still under pressure, with lower demand from China keeping the prices under pressure. A recovery in demand could be on the cards, with Shanghai reporting a 51% drop in its infection rate. Copper has bounced from the lows we saw yesterday to currently trading at $9,344.

Oil prices are up this morning, with OPEC+ agreeing to another modest increase in production but warns that the globe is short on oil producing capacity. This, coupled with the anticipation of an increase in demand for fuel in China in the coming weeks, has led to Brent Crude rising 2.35% already this morning, up from $101.30 earlier on.

International update

The dollar is still up this morning, quoted at 1.0545 against the euro and 1.2335 against the pound. We could see the dollar trading range-bound with a slightly stronger bias ahead of the CPI print around 14:30 this afternoon. US treasury yields at 2.98% for the 10yr, 2.91% for the 5yr, and 2.62% for the 2yr. The Nasdaq has gained back some of the losses over the past few days closing just under 1% higher earlier this morning. This follows the aggressive sell-off in tech stocks we have seen since Friday.

Net 1 UEPS Technologies (or just Net1 for my sanity) has released results for the third quarter of 2022. The company is changing its name to Lesaka Technologies, which at least rolls off the tongue more effectively. Shareholders have already approved the change. The thinking behind this new name is that Lesaka means “kraal” (the “social and economic heart of a village”) in Setswana and Sesotho. Now you know why the feature image for this article used cattle.

With that in mind, you may be surprised that the company reports in dollars. This is because the group is listed on the Nasdaq, so results are issued quarterly and denominated in the world’s ultimate currency. The operations are in South Africa and the acquisition of Connect Group (which closed in April) cements that strategy. Connect Group brings an enormous base of micro, small and medium enterprises, of which around 35,000 are informal.

The service offering includes a prepaid value-added services platform called Kazang, a digitised cash management platform called Cash Connect, a merchant lending platform called Capital Connect and a merchant acquiring solutions business called Kazang Pay and Card Connect. The business generated around R1.1 billion in net revenue in FY21 and targeted EBITDA of R375 million for FY22 at the time the deal was announced in November 2021. Learn more about the business by visiting the website.

Revenue is up 22% in dollar terms (27% in rand terms) and Segment Adjusted EBITDA swung into the green. This excludes any corporate costs, so it isn’t a good indication of group profitability. This adjusted EBITDA number improved from a $10.7 million loss in Q3’21 to a $0.3 million profit in this quarter.

The group is loss-making overall, with a target of $19.2 million in annualised cost savings targeted in the 2023 financial year. The Connect Group acquisition closed in April (after the end of this quarter) and will be critical to the strategy going forward.

In the nine months to March 2022, the group’s operating loss was $30 million vs. a loss of $40 million in the comparable period.

At the end of the quarter, the group had $183.7 million in cash of which $169.9 million (R2.5 billion) is held in rands.

The name change will be official on 18th May. Shareholders will expect a far greater change to come in the financial performance, with all eyes on the Connect Group acquisition.

Net1 is about to change its name to Lesaka Technologies, reinforcing the group’s South African strategy despite being listed on the Nasdaq in addition to the JSE (and reporting in dollars). The operating loss over the past nine months is more than $30 million, so all eyes will be on the acquisition of Connect Group to drive a group turnaround. I’ve written a feature article that you can read here.

Ascendis Health is probably our closest corporate equivalent to Game of Thrones at the moment. With six directors on the ballot for the Special General Meeting, it was the trio of Amaresh Chetty, Bharti Harie and Carl Neethling that were voted onto the board with support of around 61% of shareholders. The lenders have now applied a 4% ratchet to the debt (which means the rate on the R550 million facility will retrospectively increase to JIBAR plus 12.33%) based on a request for the annual financial statements for the Medical Devices business that could not be met in time. There’s plenty of gamesmanship going on around here. Netflix should consider this as a low-budget thriller to help improve its cash flows and attract some more local subscribers.

Famous Brands has released a trading statement for the year ended February 2022. Even if we ignore the prior year loss from discontinued operations of R1.1 billion, the percentage growth looks ridiculous. After selling many burgers and pizzas, headline earnings per share (HEPS) from continuing operations is up between 504% and 639%. A far more useful approach is to consider the earnings vs. pre-pandemic levels. The guidance for this period is 320 to 392 cents vs. 319 cents in FY19 and 393 cents in FY18. This means that Famous Brands has made a full recovery to pre-pandemic levels. The share price closed 1.7% higher yesterday at R59.00, a Price/Earnings multiple of around 16.5x at the midpoint. The share price is down 23.6% this year. It seems my efforts to help local wine producers with cash flow this winter will need to be extended to help Famous Brands with selling more food to prop up the share price. It’s tough out there but I’m here to help.

In a time of high corporate profits in mining and manufacturing businesses and considerable inflationary pressure on our most vulnerable people, the stage is set for labour unrest. With Sibanye already dealing with this, the next company on the list is ArcelorMittal. NUMSA has issued the company with a strike notice, as the union isn’t accepting a final offer of a 7% increase (5% on all remuneration elements and another 2% cash equivalent on those elements). NUMSA is demanding 15%, a number that I think we can all agree is silly. The share price has lost around 13.4% this year. I can’t explain why it rallied over 5% yesterday after this news though!

International ICT company Datatec has released a trading statement for the year ended February 2022. Despite supply chain issues that have plagued this sector in particular (like shortages of chips), group divisions performed well. The sales backlog also increased significantly year-on-year as a result of these constraints. HEPS will be between 15.5 and 16.5 US cents, a massive increase vs. 1.8 US cents in FY21. This puts Datatec on a Price/Earnings multiple of around 15x in round numbers, with a flat share price performance this year.

Trematon Capital Investments owns a variety of assets. To give you an idea of the diversification here, the group owns Club Mykonos in Langebaan and Generation schools among other businesses. I feel that I can comfortably speculate that liquidity in the stock is far lower than in the bars at Club Mykonos. For the six months to February 2022, revenue is up 18% and profit after tax is up 35%, with Generation as a major contributor (R8.1 million operating profit vs. R0.3 million operating loss in the comparable period). HEPS is only up 5% though at 2.2 cents. Intrinsic net asset value per share is R4.69 and yesterday’s closing share price was R3.84.

Investment holding company Universal Partners has released quarterly results. The net asset value (NAV) per share is similar to June 2021 levels after a dividend was paid in November. This UK-focused group owns a fascinating portfolio of investments including a dental consolidation group (yes, really), a contractor payroll solutions business, a financial group focused on high yield and distressed debt investing, a global recruitment business and a business called Propelair, which manufactures toilets. Ahem. The share price is R20.43 and the NAV per share is R28.85 at current exchange rates. There is currently a mandatory offer on the table from Glenrock for R18.63 per share, which I can’t see many shareholders taking unless they have large blocks of shares they want to sell in this illiquid company.

DRA Global has released an unpleasant trading update that guides a loss for the first half of FY22. Revenue for the full year is expected to be as much as 25% lower than FY21 and underlying EBIT (Earnings Before Interest and Taxes) is expected to be between $15m and $25m (vs. $56.5m in FY21). An impairment charge takes the first half into a loss. The company is losing money on some fixed-price construction contracts and has decided not to declare a dividend in respect of FY21. It’s never good news for shareholders when a dividend isn’t declared after a profitable year based on concerns about the subsequent year.

There’s some progress on the buyout of Long4Life by Old Mutual Private Equity for R6.20 per share. Other than finality on some financial conditions, the important news is that the Competition Commission has recommended that the deal be approved without conditions. The Tribunal needs to make the final decision on a merger of this size and will meet on 12th May to finalise this application.

Directors of education businesses Curro and Stadio are buying shares in the company. The year-to-date performance of those share prices is -20.7% and +13.3% respectively. I must be honest that I expected it to be the other way around, so I bought Curro earlier this year. I’m in no hurry to sell.

At EOH’s shareholder meeting to vote on the disposal of the Information Services Group, 99.93% of votes were cast in favour. No surprises there, as the company desperately needs to reduce its debt through a disposal process.

Property fund Rebosis is in the process of selling an enormous portfolio to Ulricraft, an entity backed by Vunani Capital Partners. Funding is taking longer than expected to be finalised, which is a nice way of saying that Ulricraft’s backers are running around in the market trying to find enough co-investors to make the deal work. Rebosis will only issue a circular to shareholders once the funding is secured, which the company hopes will be achieved by the end of June.

Blackrock (the world’s largest asset manager) now holds a 5% stake in Woolworths. I hope that the portfolio manager was sent one of those incredibly overpriced Chuckles shopping bags as a gift, as I’m not sure how else the retailer gets rid of them.

Salungano Group (previously called Wescoal Holdings) has announced the early retirement of CEO Michael Berry due to ill health. It always saddens me to read news like this. He has been with the company for 25 years. Thivhafuni Tshithavhane has been appointed as acting CEO.

Grand Parade Investments has changed auditor. After significant changes to the portfolio, EY (the previous auditor) found itself in a position where it would not be auditing the majority of GPI’s earnings, as subsidiaries can have different auditors to the group company. Deloitte & Touche has been appointed to replace EY.

Investec has invested nearly R150 million in buying back around 5% of its issued preference shares. We’ve seen this trend across local banks recently, as preference shares lost their shine as a source of capital when banking regulations changed and the liquidity in this asset class has been disappointing on the JSE. Some of the banks previously made offers to buy back all of their preference shares vs. just a share buyback programme. In Investec’s case, only 5% has been bought back under this programme.

A director of MAS Real Estate has bought a casual R16.9 million in shares in the company.

Andre Botha, Senior Dealer at TreasuryONE, shares the latest with us on inflation in the US:

In the last week or so, we have seen the fascinating side of markets, with data and events coming thick and fast from all over the globe. However, the underlying narrative that most of the data and events are telling us is that:

1) inflation is not as transitory as initially thought; 2) Central Banks are talking a big game on their monetary policy with Central Banks looking to hike aggressively; and 3) there is a notion of risk-off in the market, especially from the demand side.

Interest rate hike

Last week, we saw the US Fed hiking their interest rate by 50 basis points, as many in the market expected. The market did a peculiar thing after the announcement: the US dollar lost ground, and risky assets were on the front foot. The reason for this is the Fed eliminated the potential of a 75-basis-point raise, indicating a dovish stance.

But, hang on a minute? The Fed alluded to more 50 basis point hikes going forward, which is hawkish, come to think of it. It took the market a trading session or so to figure that out, and we saw risky assets like the rand give back all of its gains post-Fed back in the following trading session.

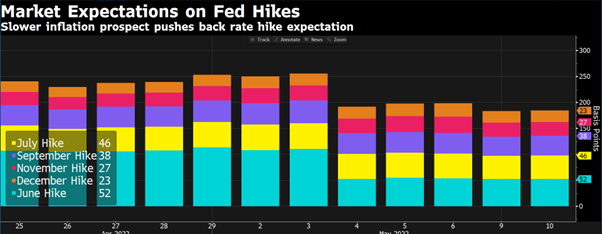

See below the interest rate expectations in the US for the rest of 2022. Despite the fact that it has dropped since the last FOMC, it is still pricing in nearly another 200bps of raises, with 50bps hike expected in June and July.

Interest rate hikes, at what cost?

Speaking of Central Banks, we also saw the Bank of England hiking interest rates by 25 basis points last week. Again, the Central Bank emphasised fighting inflation – and fighting inflation will cause certain hardships along the way for the economy.

This would ring true for most economies in their bid to fight inflation where there will be interest rate hikes, but at what cost? The delicate balancing act is determining where the sweet spot is between raising interest rates to combat inflation, and driving oneself into a recession.

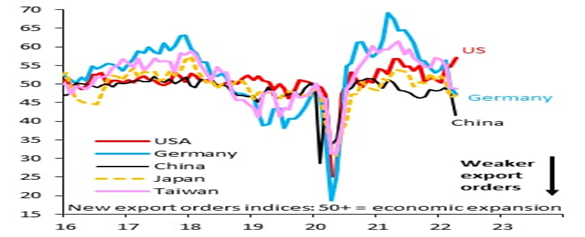

We have already seen economies like China and Germany declining in their new export numbers, which suggests that a recession is on its way. It is also curious to see that the US is the only country at the moment showing growth in its export numbers.

And the last point leads to the final issue of global demand weakening. The slowdown in demand was a given, as China went into lockdown over renewed fears of COVID. We have seen commodity prices falling by the wayside as demand from China slows. If inflation continues to rise, demand will be reduced even further as purchasing power declines around the world, which is negative for the global economy. The global picture in the short term is not a rosy one.

US inflation rate out this week

Looking at this week in data terms, we have the US inflation rate coming out tomorrow, and the market will be eager to see if inflation is still running hard or if there is some respite in the number. Expect markets to be quite volatile around the release of the number as this will significantly impact the forward view of interest rates and the view of the market regarding them.

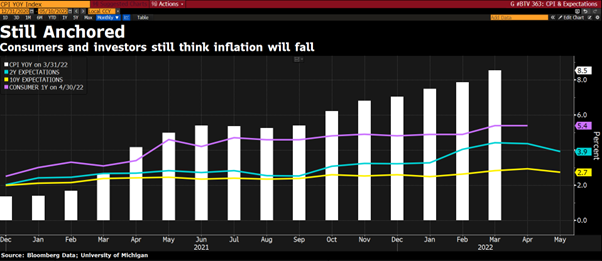

The expectation is for an 8.1% rise in inflation for April 2022. See below the inflation expectations in the US continue to fall. The 2-year (green) and 10-year (yellow) is pointing to lower inflation in the coming months.

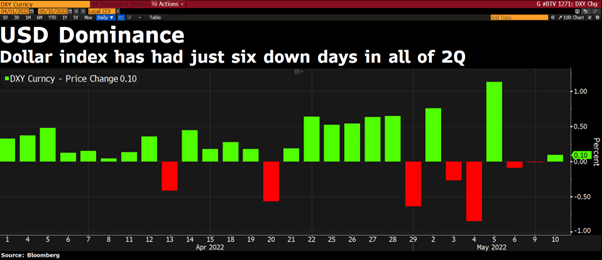

We have seen the rand push past the R16.20 level on the local front but have since retraced back to R16.10. The dollar has been a wrecking ball so far in Q2 of 2022, with the dollar index only having 6 down days so far for the quarter. This has been the telling story of the weakness in the rand and the rest of the currency market.

We expect the rand to be under pressure with the global sentiment skewing more to the “risk-off” side than taking any risk. We have seen the US dollar being the “safe haven” of choice, and any move in the US dollar will feed through to the rand.

We do believe that some correction is warranted, but that depends on the inflation number out on Wednesday from the US. For now, we still believe the rand is testing the upper end of our R15.00 to R16.00 for the rest of 2022.

See below the support line for the rand around R15.00.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.