Despite global economic challenges, the African fintech ecosystem continues to expand, with startup fintech investments proving a dominant source of venture capital deals. In 2022, over 100 startups in Africa obtained first-time funding above US$1 million, with fintech proving a strong source of investment. This reflects a steady course for growth in African fintech, with the industry making up more than 25% of all venture capital rounds in the last few years.

In such investment rounds, South Africa is joining other regional leaders, like Egypt, Nigeria and Kenya. Nigeria and Kenya have been two of the African fintech hotbeds garnering the most attention. Kenya’s fintech explosion occurred largely because the general African fintech wave followed the penetration of mobile phone technology and infrastructure. Kenya’s current mobile penetration surpasses the country’s entire population by 12%. Kenya’s fintech industry was originally focused on mobile money transfer services, and rode the wave of exponential market adoption between 2007 and today. Building on technology akin to GSM text messaging, major players in the market were able to expand their offering to users who did not have internet or data connections, but had access to cellular phone towers and basic mobile devices. In that same period, financial inclusion went from 26% in 2006 to 83% of the total population today. That activity created a market that many other fintech entrants were able to diversify within and, as a result, a large portion of GDP flowed through such services. This makes the regulators similarly fintech-friendly and creates interest in being cooperative towards innovation.

Nigeria’s rise has been similar, although perhaps more rapid in the last few years. Three of the largest African unicorns come from Nigeria, and the country is dominant in Africa in respect of fintech venture capital investments. This has followed some of the same drivers as Kenya on mobile penetration, but has also benefitted from a highly entrepreneurial technology sector and deep issues in respect of financial inclusion. About 38 million adults in Nigeria are completely financially excluded, particularly when it comes to credit access. This created the perfect conditions for dynamic fintechs to emerge, with a massive potential market if successful.

Out of the nine notable tech unicorns in Africa, seven are fintech companies. In terms of scaled fintech, mobile money, and third-party payment systems in particular, are segment leaders in the African fintech space, with more than half of the world’s mobile money customers now based in Africa. Many experts predict Mobile Network Operators (MNOs) will refine their fintech strategies in 2023 and 2024, taking more space out of the traditional banking industry, particularly as they begin to obtain mobile money licenses in new territories.

Nonetheless, the traditional banking industry has also seen some notable projects. In South Africa, for instance, the recent launch of the rapid payments system branded as ‘PayShap’ has been a particularly noteworthy development.

PayShap is the outcome of an industry-spanning collaboration, driven by BankservAfrica, the Payments Association of South Africa and the South African banking community, with the aim of modernising the national payments industry in the country. This development signals a progressive approach by local policymakers, together with the industry, and will hopefully lead to more dynamism in the sector and wider access to the country’s fintech products and investment opportunities, whilst keeping in step with the growing demands of international standards. It is also, however, a potential disruptor in the fintech sector, where some successful fintech ventures have built their payment products in the gaps of the traditional banking digital payments infrastructure. It remains to be seen whether the introduction of PayShap will influence any consolidation of players in an already saturated payments industry, and how this development may reshape or enhance African payments business models going forward.

Stagflation and the drying up of speculative capital remain some of the biggest challenges facing fintech globally, as investors are going to be more careful in their investment choices and selective in their risk-taking. Early venture figures in the first quarter of 2023 showed broader venture investment dropping to close to pre-pandemic levels, and this will have an impact on the types of fintech ventures that are able to survive. However, the African fintech space has shown incredible resilience to global market turmoil and there is still a lot more room for growth in segments such as alternative lending, digital investment and neobanking. African economies are buoyed by young populations that are increasingly entrepreneurial and driven by technology-led innovation. Digital infrastructure is also attracting investor interest; for example, there is an imbalance in the supply of data centres, compared to the growth expected from consumers that need more data and are spending more time online. There are also many other African countries that haven’t yet reached the heights achieved by the likes of Nigeria, Kenya, South Africa and others in their fintech development. The resilient rise of fintech in Africa appears to be far from over.

Ashlin Perumall is a Partner in Baker McKenzie’s Corporate/M&A Practice in Johannesburg

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

Constantia Risk and Insurance has attracted a buyer

Before you get confused, the subsidiary within Conduit Capital that suffered liquidation is Constantia Insurance Company. There were a couple of other businesses within the group that could be sold to help it at least realise some value.

One such entity is Constantia Risk and Insurance, which is being sold for R55 million. The buyer is TMM, a diversified pan-African investment group. Half of the purchase price will be held in escrow due to the liquidation process within the broader group and the potential for claims. This means that the money will be kept on one side to settle such claims if they arise. If the claims never come, the money will be released.

Negative Delta (JSE: DLT)

The property fund is struggling

In maths, delta is the symbol for change. The change in earnings at Delta Property Fund is unfortunately negative, with distributable earnings per share for the year ended February 2023 expected to be between 69% and 74% lower than the prior year.

This is a function of the issues plaguing the entire sector, ranging from negative reversions through to vacancies and higher interest rates.

“Distributable” is a relative term here, as there’s no dividend anyway for this period because of the challenges being faced.

Indluplace releases detailed results (JSE: ILU)

With 9,282 residential units, this is buy-to-let delivered at scale

Indluplace is more than just a residential fund, with a significant retail portfolio as well. The portfolio value is R3.4 billion and the company is currently under offer from SA Corporate Real Estate (JSE: SAC) for R3.40 per share. The price is now anchored to that number, trading at a slight discount to take into account the time value of money and what seems to be low deal risk.

There isn’t much for investors to think about here in terms of the share price because of the offer, but it’s interesting to note that residential occupancies improved from 89.7% to 94% over the past year and the student portfolio is back up to 98% from a dire level of 43% in March 2022.

The net asset value (NAV) per share is 5.5% lower at R6.5983, so the offer price is a discount to NAV of roughly 48.5%.

As highlighted previously by Indluplace, there is no distribution based on these interim numbers but there will be a clean-out distribution before the scheme is implemented, assuming all goes ahead.

MiX Telematics will have tricky results to work through (JSE: MIX)

A trading statement reveals a major impact on earnings from deferred tax

With detailed results due to be released on Thursday this week, MiX released a trading statement on Wednesday giving an indication of earnings. This is another great example of a company releasing a trading statement far too late in my view. It’s meant to be an early warning system, not something that comes out one day before results!

HEPS will be between 42% and 46% lower than the in year ended March 2022. This is mostly because of a deferred tax charge on forex movements linked to an intercompany loan. Investors will need to dig into this properly to understand it, with adjusted earnings per share (excluding the forex move and tax) actually increasing marginally.

Liberty Two Degrees’ pre-close update is worth a look (JSE: L2D)

There are useful insights here into the broader retail environment

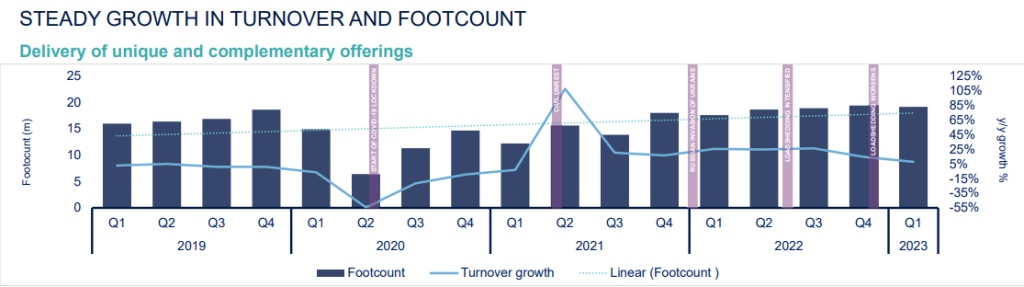

Liberty Two Degrees has exposure to some of the strongest properties in the country. This is a quality portfolio, yet it certainly hasn’t been immune to what has been going on out there. For example, office occupancy remains problematic at just 80.7% vs. retail occupancy of 97.7%.

But for me, the most interesting part of the update is the charts that give us an indication of the operating environment. For example, this chart from the update is pretty interesting, although that y-axis for growth is wild if you look closely:

It tells the story of the pandemic: wild volatility, huge pain in 2020 and then a strong recovery in 2021 driven by global stimulus. 2022 was a consolidation year, with 2023 growth taking a knock from load shedding.

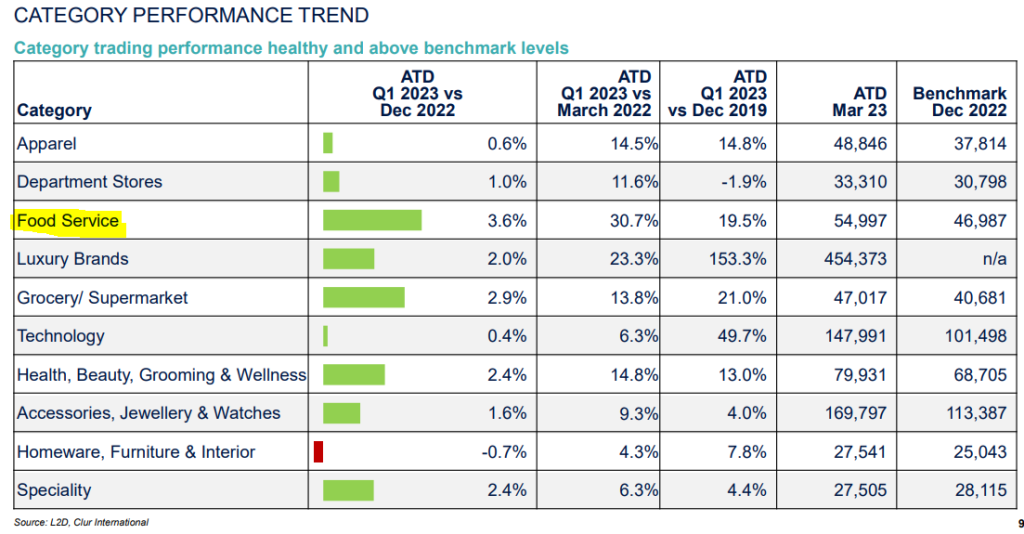

Here’s another interesting graphic, which supports my view that fast food businesses are doing very well in this environment (despite Famous Brands telling us otherwise):

And in hospitality, occupancies are up sharply and there were 67 events at the Sandton Convention Centre between January and April 2023 vs. 47 in the same period last year. Investors in hotel groups will also be pleased to know that RevPar (a measure of room pricing) has increased significantly vs. 2022.

Nampak calls 2023 a “defining year” – no kidding (JSE: NPK)

Interim CEO Phil Roux sounds believes in the future of the business at least

It is entirely possible that Nampak can emerge from this mess as a sustainable business. It’s also possible for shareholders to lose a ton of money along the way, despite a rally of 9% after the release of results on Wednesday. I would remind you that even over 3 years (which means the worst of the pandemic as a starting point), the share price is down 44%.

With revenue of R8.4 billion and trading profit of R899 million, this hardly sounds like a basket case. But once you include net forex losses of R571 million because of Angolan and Nigerian profits, the situation deteriorates rather quickly. Operating profit before impairment losses was R259 million for the six months ended March and net finance costs were R494 million (up by a whopping 77%), so not even the debts are being serviced by these assets, let alone the shareholders.

Even if we ignore the very large impairment losses, the headline loss for just the interim period is R342 million.

Is there any good news? Well, the originally envisaged rights offer of R1.5 billion has been reduced to a rights offer of R1 billion. A circular will be published at the end of May to this effect. With a market cap of under R500 million, this is still a massively dilutive rights offer.

In addition to the rights offer, there is an asset disposal plan that needs to be delivered before Nampak can breathe a sigh of relief on the balance sheet.

Finally, if you really want to understand how severe those forex losses are, take a look at this:

The tide went out on Premier Fishing’s profitability (JSE: PFB)

HEPS has more than halved

For the six months to February 2023, Premier Fishing and Brands suffered a significant drop in profitability. HEPS has tanked by between 51.56% and 71.56%, which means interim HEPS of between 0.87 and 1.49 cents per share.

That share price of R1.62 is looking very high relative to those earnings.

No further details behind the drop are given in the trading statement, but detailed results are due this week.

Reunert is on the right side of this environment (JSE: RLO)

When industrials businesses do well, they tend to do really well

Most industrials in South Africa are struggling at the moment, with load shedding as a major driver. But with significant export and renewable energy businesses, Reunert is about as well positioned as one can hope to be in this environment.

In the six months to March, revenue is up 21% and operating profit increased by 33%, so the joy of operating leverage is coming through here. We need to be careful though, as this period included a business interruption insurance payout of R44 million. Without that, operating profit would be 23.8% higher, so the positive operating leverage effect is far more muted than initially appears to be the case.

Major drivers of revenue growth were better cable volumes in the Electrical Engineering Segment and growth in sales in the Applied Electronics Segment thanks to demand for renewable energy products and the defence export business.

I must also note that the ICT Segment is acquiring IQbusiness, a management and technology consulting firm with revenues in excess of R1 billion. Remember this reference if someone says to you that “selling time” isn’t a business. It sure is one!

Although HEPS was 37% higher, the dividend per share is only up by 11%. This might be due to the R324 million increase in working capital across debtors and inventory.

RFG Holdings has been a beacon of hope (JSE: RFG)

There aren’t many local companies growing HEPS, let alone by 37.7%

Food producer RFG Holdings has put in a very strong performance in the six months ended 2 April 2023, with the international business operations as a major contributor. The rand has really helped here, particularly as the base period included a failed peach crop in Greece that was a temporary boost to RFG’s business.

Group revenue increased by 10.2% with price inflation of 14.8%, which means that volumes dropped. Ultimately, all that matters is total revenue, so it’s not a big deal if price increases more than make up for a drop in volumes. There are many companies out there suffering a drop in volumes even without price increases.

We do need to note foreign exchange gains and the Today acquisition that contributed 2.7% and 2% to revenue respectively. This means that the group volume decline was actually 8.5%, so RFG’s ability to still grow HEPS in this environment is very impressive.

Interestingly, the fruit juice category delivered the best market share gains for RFG. These food businesses are just a roll-up of a number of categories, which can make it very difficult for investors to forecast growth. A lot of it comes down to belief in the management team that they can keep doing the right things.

To give a sense of the effect of load shedding, operating profit in this period was R346 million and diesel costs were R37.8 million. This means that operating profit is roughly 10% lower than would be the case if dear Eskom was functioning.

Overall, HEPS increased by 37.7% and the group even managed to reduce net debt slightly despite net working capital increasing by 13.7%. Return on equity has increased from 9.9% to 14.1%.

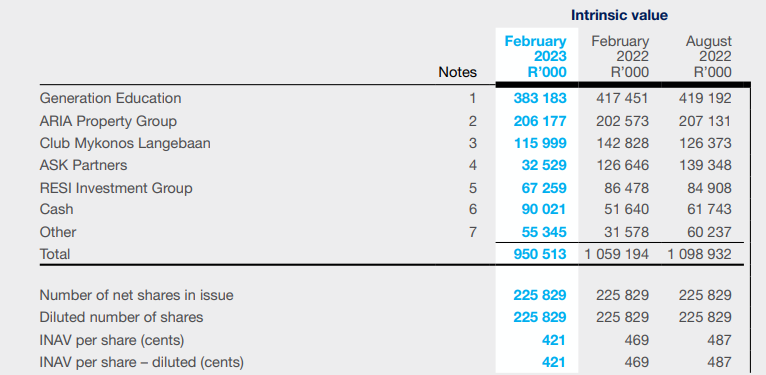

Trematon’s INAV is under pressure from Generation Education (JSE: TMT)

But the overall drop in INAV is also largely due to a capital distribution to shareholders

Trematon is an investment holding company, which means that intrinsic net asset value (INAV) per share is the key metric when assessing performance. This is based on director valuations of the underlying assets and is the market standard for a company like this.

When a capital distribution is made to shareholders, this reduces the size of the group and hence the INAV. The shareholders receive that cash, so it’s not a loss in value. Of the drop in INAV from 487 cents to 421 cents as at February 2023, 40 cents was because of the capital distribution. The remaining 26 cents is because of the assets.

The major pressure was in Generation Education, where profit from operations fell from R11.5 million to R4.7 million. This was driven by slower growth in student numbers and higher costs, so margins were squeezed. The ARIA property business also suffered a drop in profitability, yet the contribution to INAV has somehow remained flat. I’ll also touch on the Club Mykonos resort in Langebaan, which generated operating profit of R3 million vs. break-even in the prior interim period.

There are various business units that you could dig into with detailed analysis. Overall, the share price of R2.45 means that the group is trading at a discount to INAV of 42%. I must point out that INAV per share should always take into account deferred tax and I see no evidence of that here (happy to be corrected if I’m wrong). Investors also need to allow for centralised costs, so this discount often isn’t as high as it initially seems.

Vunani reports a drop in earnings and the dividend (JSE: VUN)

Asset administration saved this result from being a lot worse

Vunani has a variety of business units that really need to be considered separately in order to understand the group’s results for the year ended February 2023.

The largest contributor to profit is now asset administration, achieving profit of R33.7 million out of a group total of R61.7 million. It has jumped sharply from R19.8 million in the prior year, which is just as well because there have been major negative swings in some other business units.

The only other unit with a good news story for this period is insurance, with profit of R14.6 million vs. R11.8 million in the prior period.

Businesses linked to the markets have come under pressure, like fund management where profits dropped from R37.4 million to R21.2 million and institutional securities broking which slipped from a profit of R1.4 million to a loss of R9 million. Stockbroking really is one of the toughest business models around at the moment.

Finally, advisory services increased revenue by over R12 million but somehow only managed a flat profit performance of R1.3 million.

Overall, Vunani’s revenue increased by 10% but HEPS dropped by 14.4% to 29.7 cents. The dividend of 11 cents per share puts the trailing dividend yield on 3.9% based on the current share price of R2.80.

Little bites:

Director dealings:

Directors of Harmony Gold (JSE: HAR) have sent a pretty clear message about where they think we are in the cycle, with two directors selling a combined R10.2 million worth of shares.

An associate of a director of Ascendis (JSE: ASC) has bought shares worth over R373k. In a separate transaction, an associate of a different director of the company bought shares for R232k.

A director of Brimstone (JSE: BRT) and one of his associates bought a combination of ordinary shares and “N” shares worth R70.7k.

It’s lovely to see a censure on a director of a listed company for trading in a closed period without permission. It’s grossly unfair that these types of things happen in the market and the rules are there to protect minority shareholders who don’t sit on the inside of these companies. With many years of experience, Dipula Income Fund (JSE: DIB) director Brian Azizollahoff should’ve known better when he sold shares worth R108k in a closed period without clearance. He earned himself an embarrassing public censure and a fine of R50k. Having been in top executive roles for a long time, I doubt the fine stung very much but the censure probably did. Hopefully the public censure sends a message to directors across the JSE.

Choppies (JSE: CHP) announced that the charge against the company by the Botswana accounting authorities for alleged non-compliance in 2017 – 2020 has been withdrawn.

Mustek (JSE: MST) announced that its Chairperson would be stepping down at the AGM in November, with Reverend Vukile Mehana having served in that role since 2016. The board has commenced a process to find a successor.

Alexander Forbes shows the benefit of its strategy (JSE: AFH)

Growth in HEPS from continuing operations is encouraging

Alexander Forbes has been a group on a mission to execute major strategic changes. Aside from the sale of the life insurance business, the group also sold the client administration business to Sanlam Life.

The correct measure to assess performance is thus HEPS from continuing operations, as it splits out the gain on sale of the businesses and the improved performance in discontinued operations for the portion of the year for which they were held. Continuing operations, as the name suggests, are what the shareholders will be exposed to going forward.

On that measure, HEPS increased by between 20% and 25% for the year ended March 2023. Things have definitely improved at this company, with the share price up roughly 20% in the past year.

Bytes reports impressive numbers (JSE: BYI)

Demand for the group’s services remains strong

Cybersecurity. Cloud. Hybrid datacentres. These are high-growth service offerings and Bytes has all of them, which is why revenue increased by 26.5% in the year ended February 2023. I feel compelled to point out that this is growth in British pounds, a real currency.

Although gross margin came down from 73.7% to 70.3%, we can all agree that this is still a pretty juicy margin. Operating profit increased by 20.6%, a similar percentage increase to gross profit. Operating profit margin was 27.6%.

HEPS increased by 23% and the dividend nearly followed suit.

Strategically, bolt-on acquisitions are clearly still in play here, with a 25.1% investment in AWS partner Cloud Bridge Technologies. This is a business that has worked with Bytes for a long time, which is always encouraging when you see deals like these.

I remain a happy Bytes shareholder.

Coronation has troubles beyond the tax (JSE: CML)

Outflows of 5% of average AUM are not helpful to shareholders

With R623 billion under management, Coronation is absolutely enormous. It hasn’t been a good period for the company, with the jokes writing themselves about the “Trust is Earned” slogan in light of major fights with SARS and a huge tax bill.

That fight is ongoing, with Coronation having applied for the right to appeal the ruling of the Supreme Court of Appeal in the Constitutional Court. It’s a worthwhile exercise, as the tax bill is a cool R716 million. This was the major driver of HEPS being obliterated by 97% to just 6.2 cents in the interim period.

There’s a potential sting in the tail though, with SARS lodging a cross-appeal to the Constitutional Court to appeal the Supreme Court of Appeal decision to dismiss the penalties. The tax problem could get worse rather than better!

Even without SARS, there are reasons to be concerned about these results. Although closing assets under management (AUM) increased by 9%, outflows were 5% of average AUM and that reflects the lack of ability for many South Africans to meaningfully save and invest.

Worryingly, the 11% increase in fixed expenses was impacted by the weakening of the rand, with Coronation clearly having many technology expenses that are denominated in dollars or at least linked to the currency.

Between the outflows and the increase in costs, Coronation seems to be getting squeezed by macroeconomic issues that go a lot further than just the value of the equity markets. Profit before tax fell by 8% year-on-year and that obviously excludes the huge SARS problem.

As a closing comment, I must note that the entire SARS expense (excluding a potential further issue related to penalties) has been recognised in the interim period. In other words, although interim earnings have been crushed, the second half of the year should see a normalised profit performance and so the impact on the full year numbers will be a lot less severe than the impact on the interim numbers.

Datatec has discovered “adjusted EBITDA” (JSE: DTC)

The scourge of this reporting style continues

Another soldier has fallen. Datatec has been reading earnings reports from international peers and has decided that adjusted EBITDA is the way forward.

And guess what? The adjusted numbers look better than the reported numbers. Isn’t that a massive surprise?

Continuing adjusted EBITDA margin was 3.5% for the year ended February 2023, identical to the prior year. Continuing EBITDA margin as reported properly actually fell from 3.2% to 1.9%. We shouldn’t let this minor inconvenience ruin everyone’s snacks after the results presentation.

I don’t actually mind when the adjustments relate to genuine once-off costs, like restructuring costs. I mind a lot when they involve share-based payments. Tech companies love falling into the trap of paying staff big chunks of their bonuses in shares rather than cash, proudly showing a strong adjusted EBITDA number when in reality, shareholders are constantly being diluted.

Adjusted EBITDA is generally like Pringles – once management teams start, they just can’t stop.

If we lift our heads to the overall performance, continuing revenue grew by 13.1% and continuing gross profit grew by only 2%, so the margin pressures are clear and dollar strength in the first half was the major culprit. Continuing EBITDA fell by 31.5%.

With Analysys Mason having been sold, the remaining businesses are Westcon International, Logicalis International and Logicalis Latin America. EBITDA decreased across the board.

The share price closed 5.9% higher, so clearly reporting all these adjusted numbers has worked.

HCI flags a substantial jump in earnings (JSE: HCI)

Another 5% jump in the share price takes the year-to-date increase to nearly 33%

It’s been a tough year for South Africa and many investors, yet your money would be smiling back at you if it had been invested in Hosken Consolidated Investments (HCI) shares at the beginning of the year.

To back up the juicy share price gains, a trading statement for the year ended March reflects expected growth in HEPS of between 50.2% and 60.2%. With so many different businesses in the stable, investors will look forward to digging into the group company updates to see what the key drivers were.

Indluplace shows decent growth in income (JSE: ILU)

There is no dividend at this stage while the scheme of arrangement is in progress

You may recall that Indluplace is the target of an acquisition by SA Corporate Real Estate (JSE: SAC), with one of the terms being that no dividend is payable on the interim profits at this stage. Instead, Indluplace would pay a clean-out dividend prior to the scheme being implemented. I’ve seen this called a “clean price” in the property sector before, designed to ensure that current shareholders get their dividend in a process that has uncertain timing.

Excluding interest on loans earned from participants of the Indluplace share purchase and option scheme, distributable income has grown by 7.3% year-on-year for the six months to March.

Will MultiChoice shareholders be alright this year? (JSE: MCG)

With the business under pressure, MultiChoice held a capital markets day

Eskom isn’t doing MultiChoice any favours whatsoever, with load shedding making it increasingly difficult for families to justify a monthly spend on entertainment on TV. This also has a negative impact on advertising, something that eMedia Holdings (JSE: EMH) has consistently flagged in periods of bad load shedding. And of top of all of this, MultiChoice’s customer base has discovered the joy of streaming instead.

Without a doubt, Eskom cannot be blamed for all of MultiChoice’s challenges. Every time I see an advert on Facebook for DSTV, the comments section is filled with people begging for a SuperSport-only bouquet. I currently pay MultiChoice absolutely nothing. I would love to pay them a couple of hundred bucks a month for sport.

MultiChoice’s strategy is to look beyond South Africa’s borders. The focus is on Africa, with the company also seeking out major global partners. In my view, the biggest strength is the regional content, which is a genuine competitive advantage against the likes of Netflix. I would also caution that Netflix is equally focused on creating regional content, so MultiChoice doesn’t operate in a competitive vacuum even in that space.

Another competitive advantage held by MultiChoice is the ability to receive payments across Africa. That sounds so silly if you’ve never run a business that receives payments, but there are around 200 payment partner integrations and receiving money in Africa isn’t as easy as you might think. Of course, the problem lies in getting the money back from the African subsidiaries to group level.

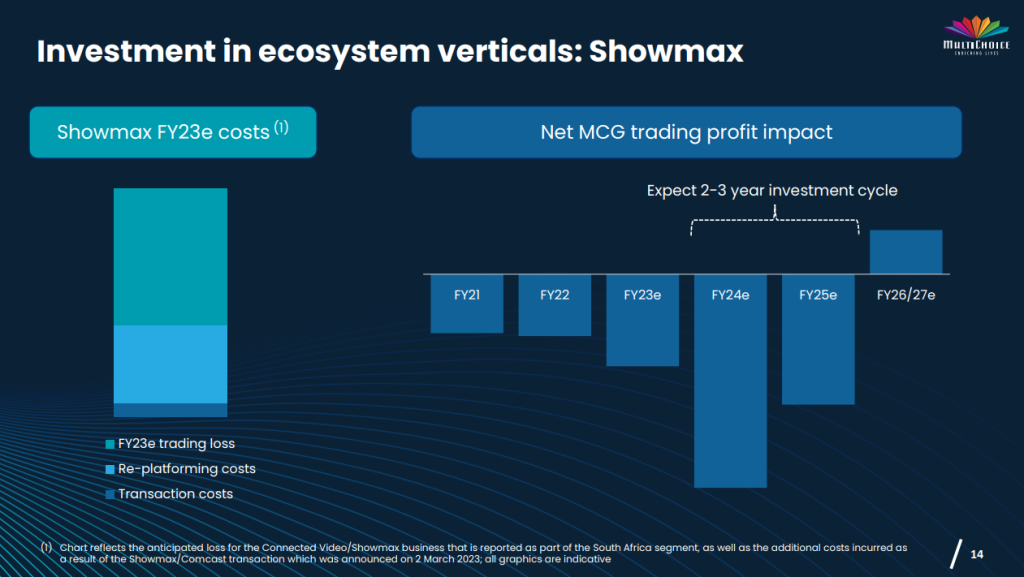

MultiChoice is responding to growth in access to broadband on the continent by putting in place key streaming partnerships, like the recently announced deal to partner with Comcast on Showmax. It will be Showmax powered by Peacock, the streaming technology that underpins Comcast’s streaming offering. MultiChoice will own 70% in that business and perhaps the most important element is the access to Comcast’s content like English Premier League football and HBO.

In case you think streaming will be good news for MultiChoice’s profits in the next two years, think again:

Another strategic driver that possibly makes sense is sports betting, an obvious opportunity alongside SuperSport. Will that be the catalyst for a sports-only bouquet? I wouldn’t bet on it just yet.

It gets patchy after that, with other initiatives like FinTech and Home Services. Yes friends, DSTV Internet is coming. If you can’t beat ’em, join ’em?

The Rest of Africa business is on track for trading profit breakeven in FY23. That’s a nice way of saying it would be profitable without forex headwinds. Sadly, those headwinds tend to be a feature of doing business in Africa.

Finally, for Phuthuma Nathi shareholders, the good news is that MultiChoice will need a lot of capital at group level and the biggest source of that cash flow by far is MultiChoice South Africa. Phuthuma Nathi holds shares alongside MultiChoice in MultiChoice South Africa, so the movement of cash to group level for investment purposes means that Phuthuma Nathi gets its slice of the pie.

Of course, this makes it even more important for MultiChoice to look after the South African business properly. I’ll say it again for employees reading this: give us a SuperSport bouquet! My money is waiting.

Zeda is growing HEPS, albeit only slightly (JSE: ZZD)

The traded multiple is looking very modest at this stage

Mobility business Zeda was unbundled by Barloworld (JSE: BAW) in December. It’s been one-way traffic since then unfortunately, with the share price down nearly 40% since initial trade.

When you consider earnings drivers like growth in leasing and an increase in inbound and corporate travel, it’s not obvious why the company is trading at such a light multiple. The results are seasonal in line with what you might expect, with HEPS for the year ended September 2022 of 325 cents vs. HEPS for the six months to March 2022 of 182.3 cents. You therefore can’t just double the interim guidance to work out a forward Price/Earnings (P/E) multiple on this stock.

But with Zeda closing at R10.14, the P/E is just 3.1x on the full-year numbers. The guidance for HEPS for the six months to March 2023 is between 187.8 and 191.4 cents, representing growth of 3% to 5%. Although that is modest growth, it still makes Zeda sound cheap at this price point.

Is the market missing a trick here?

Little Bites:

Director dealings:

A director of Gemfields (JSE: GML) locked in the gain on share options, selling shares worth R8.1 million that were acquired at a discount of up to 35% on the current market price.

The CFO of Discovery Life (a subsidiary of Discovery – JSE: DSY) has sold shares worth R201k.

GMB Liquidity continues to live up to its name, with the new CEO of Grand Parade Investments (JSE: GPL) mopping up another R172k worth of shares via his investment vehicle.

The CEO of Spear REIT (JSE: SEA) has bought more shares for his kids and family worth nearly R72k.

A director of Sea Harvest Group (JSE: SHG) has acquired shares worth over R46k.

Value Capital Partners has reduced its stake in Novus Holdings (JSE: NVS) to 6.42%. The stake was over 10% previously.

Orion Minerals (JSE: ORN) has issued a large number of shares in line with previous announcements. Other than to directors and managers, as well as Tembo Capital as repayment of a convertible loan, the latest issuance includes the first tranche of the capital raising activities that bring Clover Alloys (SA) onto the register as a strategic partner.

Investors have been well primed on the benefits of compound returns. What is underappreciated, though, is that not all compounding is equal. In this article we discuss two key pillars of compounding that is understated in importance, but critical to make it work in your favour.

First, the source of compounding determines the rate of compounding. We all know that to earn the proverbial biscuit, you have to risk it. Casinos take a calculated risk with each spin of the Roulette wheel. Many spins make uncertain outcomes near certain. Similarly, diversified exposure to risk assets in financial markets, given enough time, has shown to pay off with high consistency – and at a superior compounding rate.

Second, know your enemy. The anti-matter to compounded returns is compounded costs. A sure way to reduce the exponential benefits of compounding is to tolerate a counter-compounding effect through high fees, costs, and inefficient re-allocations. The sheer impact might surprise you.

First Pillar: Source of Compounding

To understand why the source of compounding matters so greatly, we need to first understand the difference between Saving and Investing.

Saving means spending less than you earn – storing seeds safely to be consumed later.

Investing means sowing those seeds for greater harvests in the future.

We need both – but only investing truly benefits from compounding.

Why is that? The evergreen adage of higher risk, higher reward gives us a clue. Risk’s reward crucially relies on differences in our perception and temporal tolerance of it. Savers and short-term investors have less appetite for risking the seeds they intend consuming tomorrow. They thus pay a premium to investors willing and able to bear the possible short-term pain of sowing seeds for the long-term gain they seek. Harvesting risk premiums to truly compound one’s efforts requires time, not timing.

But how much does taking some risk truly matter? The answer may surprise you. To show just how important harnessing the right source of compounding is, we use a simple illustration.

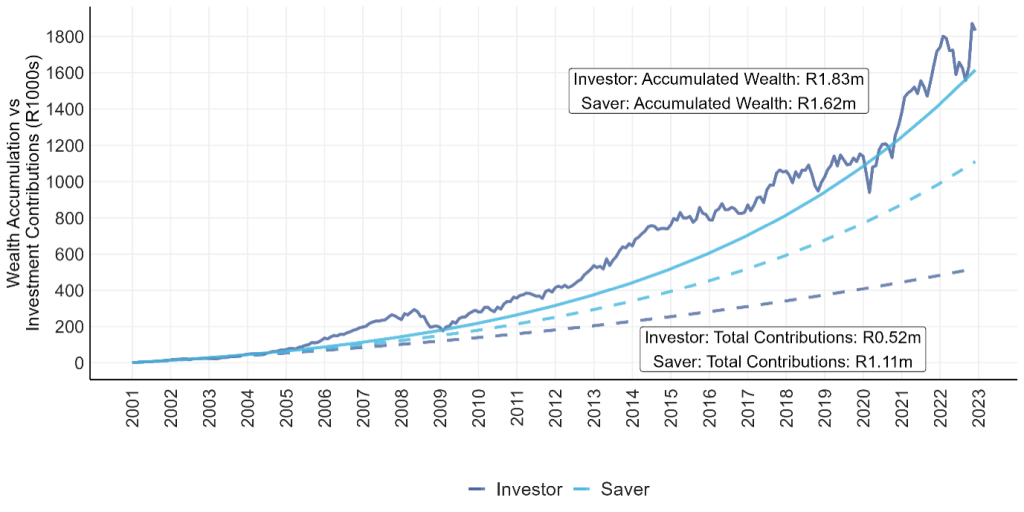

Suppose you have two individuals, Saver and Investor. Both studied the same degree and started earning the same salary 20 years ago. Saver worked long hours and occasionally weekends. Saver is all work, no play. And it shows. Saver earns a whopping 12% salary increase every year.

Investor likes to pursue other hobbies, has a great work/life balance, and works far shorter hours. And it shows. Investor earns a basic 6% salary increase each year in line with inflation.

Both have one thing in common – they diligently set aside 10% of their income. What they do with their saving contributions differ though. Saver dislikes risk & prefers certainty and earns a fixed 5% annualised return on a savings deposit account. Investor embraces risk and earns the equity market risk-premium over time by investing in the Satrix Top 40 ETF. Suppose we left them to work 22 years and then reviewed their wealth in 2023. Note the below:

Source & Calculation: Satrix. December 2000 – December 2022.

At the end of 22 years, the hard-working Saver had a final salary more than 3 times that of Investor. He contributed R1.1m to his savings pool (dotted light blue line) and reached an accumulated R1.62m capital (solid light blue line, earning 45.9% on total contributions). Investor put aside half this amount (dark blue dotted line) yet grew her total capital by more than 15% that of Saver (netting a return on total contributions of 252%).

By setting aside capital every month, both enjoyed the benefits of compounding. One just did so significantly more than the other. Saver focused on growing income; Investor focused on what she did with hers. And this made a very big difference. It turns out that being intentional about what you do with your earnings matter far more than simply working to grow it. Very few apply this principle in life though; we are mostly conditioned to become income maximisers, not wealth creators.

The lesson is clear, but some might not be convinced. In fact, many would argue that “this time is different”, or TTID. Considering all the turmoil, currency uncertainty and all that, earning equity market risk premiums today might seem too risky and so choosing safer, less rewarded alternatives seem prudent. But if history has taught us anything, it is that TTID is only right in the short-term and can be the enemy of long-term wealth creation.

Consider that if we were to randomly select a day in the past and invest R1 in the All-Share index since 1995 – the odds of returning more than 5% annualised are 74%, 82% and 93.9% respectively over 1, 3 and 5 years (this is in line with other global equity indexes too). Similar to the casino relying on multiple spins of the wheel to make uncertain outcomes near certain – time & patience places the odds firmly in your favour to earn the equity premium.

Second Pillar: Know Your Enemy

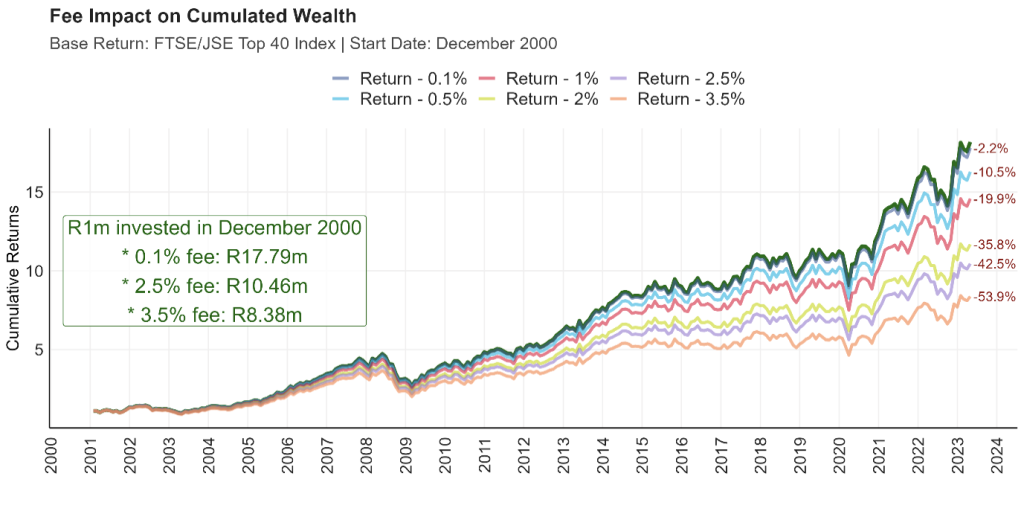

The second pillar to making compounding work for you is avoiding its archenemy: costs. If we were to take Investor’s success above and apply a cost layer to it – her nest egg fast erodes. As before, the scale is more surprising than the statement: R1m invested in the Top 40 since 2000 would’ve been worth less than half if it had an annualized fee of 3.5%. The compounding impact of fees is crystal clear when you see it. Below we show different fee scales and show at the end how much total return were lost accordingly.

Source: FTSE/JSE. Calculation: Satrix. December 2000 – April 2023.

Conclusion

We often hear that compounding is the 8th wonder of the world and that it is a powerful force for wealth creation. In this short piece we argue that to truly harness the wealth creating potential of compounding, we need to know what the source is of compounding, and also, what is working against it.

Compounding works best if you harvest well-diversified and fairly rewarded risk premiums (such as those earned in equity markets) while limiting investment costs. Only then will this wonder truly work its magic in your portfolio.

Disclosure Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

There’s a juicy jump in HEPS at Adcorp – if you ignore one of the Aussie businesses

Adcorp closed 17% higher on Monday, which sounds incredible unless you try to actually sell your shares, at which point you’ll learn about the pain of a bid-offer spread. The spread at Adcorp is approximately the size of Jupiter, with the associated drops being your tears as you try to cross the double and trade at anything close to the “price” shown to you on your friendly local data provider like Google Finance.

Stock illiquidity aside, the company has put in a solid performance for the year ended February 2023. Revenue is up by between 5.2% and 7.7% and HEPS from continuing operations has jumped by between 38% and 58%.

The “continuing operations” point is critical here, as including allaboutXpert Australia in the numbers takes the group into a very different position. HEPS from total operations is down by between 29% and 49%. This business has been classified as a discontinued operation as the company is being placed in voluntary administration.

Importantly, the balance sheet is ungeared, which is a fancy way of saying that there is no debt. The group is in a net cash position of R312 million.

Although these are somewhat encouraging numbers, the share price is down nearly 19% this year even after the latest rally.

Astral says “no dividend down 100%” (JSE: ARL)

They really wanted to drive the point home about this dividend – and the pain of load shedding

If you want to draw a direct line from governmental failures to the impact on the poor of South Africa, look no further than Astral Foods.

Despite a 5.7% increase in revenue for the six months to March, higher feed prices and of course load shedding drove an 88% reduction in group operating profit to R98 million. To be clear on the role that load shedding played, profits in the prior period were R785 million and the group notes load shedding costs of R741 million incurred during the period that couldn’t be recovered from the market.

Is this sustainable? Absolutely not. The Poultry Division (which produces South Africa’s staple protein) made a loss of R283 million. The group was saved by the Feed Division, which reported a profit of R381 million thanks to decent recovery of raw material costs.

To add insult to injury, net working capital increased by R705 million at a time when profits collapsed. This means that strain was put on the balance sheet, with a net cash outflow of R1.2 billion for the period.

The group has moved from a net cash position of R701 million at the end of September 2022 to an overdraft of R506 million at the end of March.

Unsurprisingly, all capex that doesn’t relate to emergency maintenance or measures related to electricity and water supply has been put on hold. In line with what we are seeing everywhere, private balance sheets are being used to do exactly what government should be doing with our corporate taxes.

Semigration is clear at Balwin (JSE: BWN)

Gauteng is becoming a smaller proportion of group volumes over time

At this stage, Gauteng is still the largest contributor to apartment volumes at Balwin. This is shifting quickly, with the percentage dropping from 61% last year to 48% this year. The Western Cape jumped from 32% to 40% and KwaZulu-Natal increased from 7% to 12%.

For the year ended February, revenue increased by 6% and HEPS jumped by 21% as the group’s focus on margin paid off. There is a healthy cash position of R607.4 million as at the end of February, which is lucky as I think that tougher times are ahead.

The number of pre-sold apartments has dropped sharply from 1,551 apartments at the end of August 2022 to 870 apartments at the end of February 2023. The company puts a positive angle on this number, noting that apartments were rolled out at pace to respond to semigration. That’s great, but what about demand in the coming period?

Another concern I have is the monthly rental guarantee at some developments, where Balwin is basically encouraging buy-to-let by derisking some of the economics for the buyer. In other words, Balwin is having to absorb more risk to drive sales.

Here’s another metric that tells a story: there were 1,648 mortgages originated by Balwin this period vs. 2,824 in the comparable period.

With a net asset value (NAV) per share of 824.38 cents vs. a traded price of 290 cents, the discount to NAV is a whopping 65%. The total dividend for the year was 24 cents, so the market has put Balwin on a dividend yield of 8.3%. With what is primarily a property development business rather than rental business being valued on such a high yield, the market is sending a clear message around its skepticism of the Balwin growth story.

I have shared this skepticism since I started writing publicly about the markets and I haven’t been proven wrong yet on this stock.

The good news story at Barloworld continues (JSE: BAW)

Key metrics have all gone in the right direction

Barloworld’s revenue from continuing operations increased by 12.9% in the six months to March, with solid contributions across the board. If you look at HEPS from total operations, you’ll see a drop because of the unbundling of Zeda. The correct metric is HEPS from continuing operations, which increased by 29.4% to 578.1 cents.

At EBITDA level, the performance was a mixed bag across the divisions.

Equipment Southern Africa managed to grow EBITDA by 22.7%, a juicy number despite a contraction in EBITDA margin from 12.9% to 11.4%. This was attributed to a change in sales mix, with machine revenue being higher in the current period vs. the prior period. It’s always important to remember that the mix effect can have a big impact on margins even if revenue seems to be doing well. This is simply because different products and services achieve different margins.

Looking abroad, Equipment Mongolia more than doubled EBITDA, with margin expanding from 16.7% to 19.8%. Equipment Russia suffered a 24.6% drop in EBITDA, even though margins were much higher at 17.8% vs. 11.9%. This was because of demand for aftermarket products in Russia, which carry higher margins.

Finally, food ingredients business Ingrain reported a 7.5% drop in EBITDA, with a margin of 14.1% vs. 17.6% in the comparable period. There were production issues in this part of the business, with unplanned breakdowns and other troubles.

The banks continue to do well, with net finance costs up by 49.4% because of an increase in working capital and obviously higher average interest rates. Net debt jumped from R2.5 billion in September 2022 to R7.1 billion in March 2023, with Barloworld noting that the first six months of the financial year traditionally see an increase in working capital.

Debt covenants are comfortable, with EBITDA : interest cover of 5.2x (needs to be over 3x) and net debt : EBITDA cover of 1x (needs to be lower than 3x).

Famous Brands thinks load shedding hurts its revenue (JSE: FBR)

I remain convinced that Eskom is helping these fast food joints out

When my power is off from 6pm to 8:30pm and I need to eat something, I don’t mess around. As a bachelor these days, it’s vastly easier to get takeout rather than something from the grocery story. Although my weapon of choice is Kauai (Brait (JSE: BAT) is sitting on a gem there), there’s little doubt in my mind that Famous Brands is a beneficiary of load shedding. Whether this means families getting burger specials for dinner or people going to coffee shops for a warm drink and wi-fi during the day, I just can’t see how this environment is bad for top-line growth in the industry.

With revenue up 15% and HEPS up 37% in the year ended February 2023, there seems to be some truth to my view, Covid-affected base period notwithstanding.

There are some fascinating trends vs. pre-Covid behaviours. The evening sit-down trade hasn’t recovered to pre-pandemic levels, with consumers making earlier bookings at the group’s restaurants. I can only assume that lockdown babies are taking their toll here, as any parent of a little one will know. The restaurant fun ends at 6pm when you have a small human with you.

The other trend is growth in food delivery, making this a sustainable channel in which Famous Brands can focus on its own delivery alongside third-party aggregators.

We might see more of an impact of load shedding in the next financial period, with franchise partner financial relief implemented from March 2023. In practice, this means a lower royalty and marketing percentage to help franchisees with sales generated during load shedding hours. In other words, Famous Brands needs to subsidise those hours a bit to retain its appeal to consumers.

With HEPS for the year of 488 cents and a total dividend of 363 cents, the share price of R64.30 represents a trailing Price/Earnings multiple of 13.2x and a trailing dividend yield of 5.6%.

In the six months to March 2023, Netcare’s revenue has increased by 11.9% and normalised EBITDA improved by 220 basis points to 19.1%.

Here’s the outrageous part: one of the normalisation adjustments is the exclusion of diesel costs! I mean, really now? Is load shedding just a casual once-off bump in the road? How we all wish it were true!

To quantify the diesel impact, we have to consider normalised EBITDA of R2.015 billion vs. diesel costs of R67 million. In other words, including diesel costs would decrease EBITDA by 3.3%. This would mean an EBITDA margin of 16.9%, which is higher than the prior period but not as good as management would’ve liked us to focus on.

Netcare needs to deal with the reality we are all facing: load shedding isn’t about to disappear and nor are the diesel costs, at least not in the foreseeable future.

The good news for shareholders is that management is confident enough to increase the interim dividend by 50%, which means a higher payout ratio as HEPS increased by 40.4%. Thankfully, HEPS includes diesel costs!

A Premier performance (JSE: PMR)

Shareholders are being given their daily bread here

Premier has only been separately listed for a couple of months, having been split out from Brait after a long period of preparing the group to stand on its own feet. So far, so good, with a reasonably flat share price since listing (despite the negative sentiment around SA Inc.) and a trading statement for the year ended March 2023 that tells a great story.

HEPS will be up by between 32% and 42% on a reported basis, or 17% and 27% on a normalised basis. The adjustments to arrive at a normalised number include forex gains on cash and loans and a reversal of accrued withholding tax. Those are indeed unusual items, so I would go with the normalised growth rather than reported growth.

This is an impressive outcome under the economic circumstances, which of course gets the market wondering what Tiger Brands (JSE: TBS) might be managing to achieve in this environment.

Stefanutti Stocks lands an arbitration victory (JSE: SSK)

The share price closed 8.6% higher in a show of appreciation

It feels like construction companies are permanently in some form of dispute. Thankfully, this one has gone the way of Stefanutti Stocks and its shareholders, with an arbitration process leading to an award of R90.7 million excluding legal fees.

On that note, legal fees have also been awarded, so the other side is really hurting on this one.

With a market cap of under R200 million, this is big news for the company.

Spear REIT shows the value of focus (JSE: SEA)

No frills and no fuss – the way a property fund should be

As you would’ve picked up from the Balwin numbers further up, the Western Cape is the place to be right now. As a semigrant myself, I don’t for a second believe that the semigration trend will reverse anytime soon.

This is good news for Spear, with a portfolio focused exclusively on the Western Cape. Along with a sensible management style that delivers unspectacular but dependable results to investors, this has generated growth in the distribution per share of 11.31%. The loan to value ratio also decreased from 39.05% at 28 February 2022 to 36.30%, as the group has recycled capital and repaid debt at the right time.

Based on a full year distribution of 75.97 cents, the share price is trading on a trailing yield of 10.6%.

Little Bites:

Director dealings:

A director of FirstRand (JSE: FSR) has bought shares worth R3.8 million.

The Chairman of WBHO (JSE: WBO) has sold shares worth R2.5 million.

The Chief Strategy Officer at Investec (JSE: INL) has sold shares worth £329k.

A director of Thungela Resources (JSE: TGA) has bought shares worth R196k.

A director of Quilter (JSE: QLT) bought shares worth nearly £16.7k.

After Mast Energy Developments issued new shares to lenders who converted to equity, Kibo Energy (JSE: KBO) has seen its stake in the company drop from 57.86% to 54.91%.

At Jasco Electronics (JSE: JSC), the offer was accepted by holders of 19.08% of Jasco’s shares, taking CIH and the offeror to a combined stake of 74.42% in the company. With the listing being terminated on 23 May, this means that a significant minority stake is being taken into the private environment.

Conduit Capital (JSE: CND) is in the process of selling Constantia Life and Health Assurance Company to Affinity Financial Services for R20 million. The date for fulfilment of suspensive conditions has been extended to 30 June 2023.

Finbond (JSE: FGL) has renewed the cautionary announcement related to potential acquisitions in Southern Africa. Yes, the announcement references acquisitions i.e. plural.

Primeserv (JSE: PMV) has also renewed its cautionary announcement regarding a potential acquisition in the staffing services sector.

In one of the most incredible announcements I think I’ve seen on the JSE, Afristrat (JSE: ATI) distanced itself from a website called afristratpumpanddump.co.za – of course, all this did was alert basically the entire market to the existence of this website (and yes, it’s real). People out there are angry with the company.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Dis-Chem’s latest numbers, including a very concerning second half of the financial year.

The cyclicality of the shipping industry, with the most recent quarterly performance of Grindrod Shipping as a perfect example.

The appeal of property in Eastern Europe, with NEPI Rockcastle generating strong income growth in a country far away from load shedding.

Telkom’s gigantic impairments as this technological dinosaur tries hard to avoid an asteroid.

The broken balance sheet at Nampak as the company moves towards what will surely be a very painful rights offer.

At the other end of the rights offer spectrum, the growth story at Purple Group and Sanlam’s underwriting of the rights offer.

Investec’s powerful performance in the year ended March 2023, particularly in the UK.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

The share price is trying to tell us something – but what?

Dis-Chem is a quality retailer in my books. There are elements of the strategy that make a lot of sense to me, like the investment in baby categories (and associated acquisitions). The problem is that the share sense has been expensive since the IPO, which is why Dis-Chem hasn’t been a good investment for those who got carried away in the IPO hype back in 2016. A share price return of around 9% in roughly 6.5 years isn’t a happy outcome!

The performance this year has been very interesting compared to Clicks, with a major sell-off in the price:

This isn’t what you expect to see from a company that just reported HEPS growth of 17.4% after growing revenue by 7.4%. There’s clearly something here that the market is worried about.

The likely culprit is the performance in the second half (H2) of the year. In the first half (H1), HEPS increased from 48.7 cents to 70.3 cents, or 64.3 cents if we exclude a property gain. The full-year number includes the gain as well, so in my view we can just subtract the H1 number from the full-year number to isolate the second half of the year that didn’t include the property gain anyway.

In other words, the H2 performance this year is 116.5 – 70.3 = 46.2 cents. In the comparable H2, the performance was 99.2 (FY22 result) – 48.7 = 50.5 cents.

Hang on. What happened here? HEPS fell by approximately 8.5% in the second half of the year after growing by 31.9% in the first half (excluding the property gain)!

Read that again if it all went over your head. Remember, companies report on the first six months and the full-year result. If you subtract interim numbers from final numbers, you can isolate second half profits. This does not work for the balance sheet, as the balance sheet is a snapshot at a point in time rather than a measure of performance over a period of time (like an income statement).

With slow like-for-like growth and all the inflationary pressures on expenses that we can imagine, this truly is a tale of two halves for Dis-Chem. If separate financial statements were required for the second half of the year vs. the first half, that story would be very obvious. In the absence of that information, we have to dig into the numbers.

The clue to take a deeper look was the share price movement, which doesn’t make sense vs. the HEPS performance even if the valuation was a bit expensive.

As an aside, I enjoyed this chart from the slide pack:

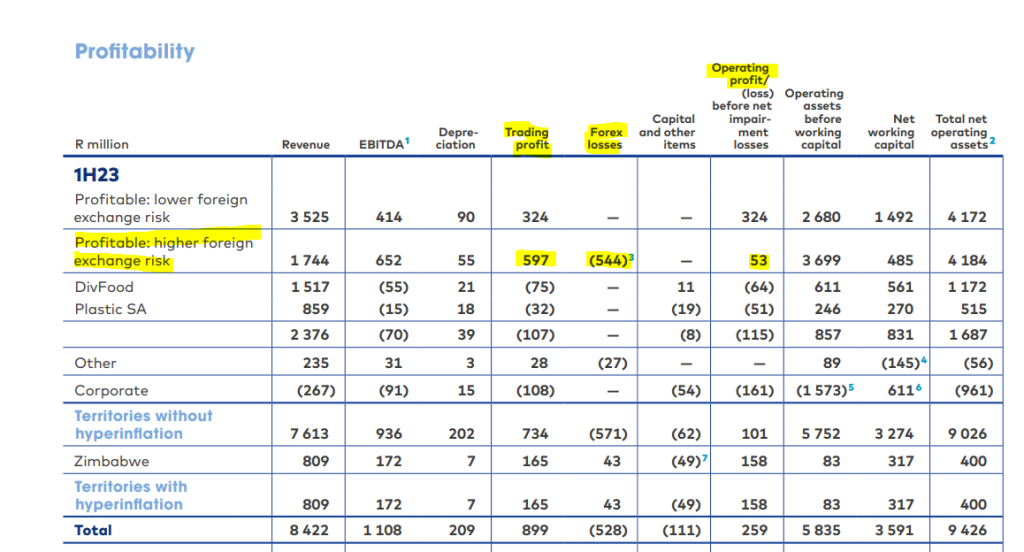

Nampak sheds another 11% (JSE: NPK)

A trading statement has laid bare the extent of the pain

Nampak has lost well over a third of its value this year. Over 5 years, the share price is down around 96%. In summary: it hasn’t been great.

It’s exceptionally difficult to get money back to the mothership where it is so desperately needed, with Nampak recognising profits in its African countries and then suffering huge forex losses to get the money back to South Africa at just about whatever rate is available.

A cocktail of forex losses and higher interest rates is deadly for a company in Nampak’s position. This is why the headline loss per share for the six months to March has come in at between -53 and -58 cents per share vs. headline earnings per share of 35.6 cents in the comparable period. Remember, headline numbers exclude the impact of any asset impairments.

If we take the impairments into account by using earnings per share instead, we find a loss of between -380 cents and -420 cents per share vs. earnings per share of 34.9 cents in the comparable period.

When the share price is just 65 cents per share, this means that the company is a dead man walking unless a substantial amount of equity is injected and the balance sheet is rectified. For existing shareholders, any rights offer would most likely be intensely dilutive and would wipe out a big chunk of the remaining value. The size of the required rights offer will be “announced in due course” by the company based on negotiations with lenders and progress made on the restructuring plan.

Tharisa’s operating profit fell by 29% (JSE: THA)

But HEPS is up andyou need to assess this result very carefully

The Tharisa results need to be read carefully, as revenue is up by 0.4% and operating profit is down by 29.0%. That isn’t very unusual in this environment sadly, as inflationary pressures are causing difficulties for many companies.

The eyebrow-raiser is that HEPS is up 13.5% despite the drop in operating profit. The interim dividend is flat year-on-year despite the jump in HEPS, which is the final clue that a deeper look is required here.

When you see a big swing in HEPS vs. operating profit, the usual reason is that there have been substantial changes to the balance sheet. A classic example is debt, with net finance costs impacting HEPS but not operating profit, as the latter tries to isolate the results of the underlying businesses regardless of how they are funded.

Although net finance cost did move year-on-year, the quantum is nowhere near enough to explain the swing in HEPS.

Now you need to really go digging, particularly for the note that reconciles headline earnings to profits. Here’s what that looks like:

In this case, the comparable period included massive accounting gains on an acquisition of a subsidiary. These are reversed out for a HEPS calculation but they also don’t sit in operating profit, so that was a red herring to try and understand the HEPS move vs. the operating profit move.

Back to the income statement we go, with important highlights below:

The gain on acquisition of a subsidiary was already dealt with in the HEPS note, so that’s crossed out in red. The other yellow highlights are important. In summary, HEPS looks far better than operating profit because the share of losses from an associate are gone and the fair value changes in financial assets and liabilities went sharply in the right direction. The single biggest swing is in the value of the option held by the Republic of Zimbabwe to increase its shareholding in Karo Platinum, with the fair value of the option more than halving. I had to go digging in the notes to find that, but I didn’t want you to panic with another screenshot.

Long story short: the fall in operating profit is what I would focus on rather than the increase in HEPS. The fall was driven by a 61.4% decrease in gross profit in the PGM operations (with production and basket prices well down), mitigated to some extent by a 66.9% increase in gross profit in the chrome operations.

And there you were, thinking that can always just blindly rely on headline earnings as a measure of performance! You often can, but sometimes you can’t.

Tradehold gives guidance on net asset value per share (JSE: TDH)

There are good explanations for the large decrease

Companies that are judged based on net asset value (NAV) per share are susceptible to big negative moves that may not necessarily mean something bad for shareholders.

In particular, if assets are unbundled to shareholders or if there is a large disposal and subsequent special dividend, then the company has deliberately made itself smaller and NAV per share drops. The trick is that shareholders are holding another asset somewhere (either an unbundled company or the special dividend in cash), so the combined picture is fine.

Having said that, a disposal at a price below the value that shareholders were banking on would reduce NAV per share because the value of that asset was actually too high in the NAV calculation.

Tradehold is a perfect example of these issues, with NAV per share expected to be between R6.97 and R7.97 lower. If you adjust for the special dividend related to the Moorgarth disposal of R4.34, the drop is less nasty. Aside from the dividend, the disposal of Moorgarth hit NAV per share by R3.80. With a total impact from those two issues of R8.14 on NAV per share, this means that the ongoing operations have been a positive contributor to NAV per share in the year ended February 2023.

If you just read the NAV per share headline and nothing further, you would never pick that up.

The latest NAV per share is between R11.50 and R12.50, with the share price trading at R7.49.

Tongaat releases a business rescue plan – for a subsidiary (JSE: TON)

Creditors are set to receive 7 cents in the rand from Tongaat Hulett Developments

Read very carefully here: this business rescue plan is for a subsidiary of Tongaat Hulett, not the group company. The all-important plan at group level is due at the end of May, along with plans for two other subsidiaries.

The plan released on Friday is for Tongaat Hulett Developments, the property company that owns a substantial amount of land in KwaZulu-Natal.

Not only is the equity in this subsidiary worthless, but even unsecured creditors have lost everything. “Secured” creditors hardly do any better, expected to receive 7 cents in the rand. In other words, they lose 93% of the debt owed by the company. If the company had gone into liquidation instead of business rescue, secured creditors were estimated to only receive 2.5 cents in the rand.

The important lesson here is that “rescue” is a relative term. Some companies emerge from a business rescue with the brands in one piece and a new owner. Other processes are simply a better outcome for creditors than would’ve otherwise been possible in a liquidation. Either way, you don’t ever want to be an equity holder when a company goes into business rescue.

Little Bites

Director dealings:

In a rather unusual announcement, Michiel le Roux (ex-CEO and chairman) has bought shares in Capitec (JSE: CPI) worth nearly R4.5 million and a prescribed officer in the bank sold shares worth R1.39 million. I have no position in Capitec, but when the incredibly wealthy director is buying a position that is small as a percentage of total wealth vs. an officer in the bank selling a chunk amount, I tend to maintain my bearish view on Capitec in the context of its valuation and broader SA pressures right now.

Although an associate of a director of Santova (JSE: SNV) bought shares worth nearly R93k, the much more important news was a sale of shares by a director worth nearly R4.3 million,

In an encouraging sign for Transaction Capital (JSE: TCP) shareholders, Sabvest Capital (JSE: SBP) – the investment vehicle of director Chris Seabrooke – has bought another R1.4 million worth of shares at a volume-weighted average price of R7.09. I would ideally like to see more director buying from other directors as well before I add further to my position.

For the budding geologists among you, Europa Metals (JSE: EUZ) has released drilling results at the Toral project. This is the 2023 drilling campaign being run by Europa Metals and Denarius Metals Corp. You’ll be thrilled to know that Hole TOD-043 is both thick and well-mineralised. That’s about all I can tell you really, other than a comment that the CEO sounds happy with the “robust” nature of the resource.

Utterly obscure company CAFCA Limited (JSE: CAC) released results on Friday. With a market cap of R43 million and almost no trade in the stock, you haven’t been missing out if you’ve never heard of this cable manufacturer based in Zimbabwe. The company reports in Zimbabwean dollars, so there are numbers on the balance sheet running into the billions. Sadly, the paper in the annual report is worth more than the currency.

A slowdown in economic activity hits Afrimat (JSE: AFT)

HEPS came under pressure from the industrial minerals and construction materials segments

Although Afrimat’s group revenue increased by 4.9%, operating profit fell by 13.3% and operating margin declined from 23.7% to 19.6%.

Some of this is due to increased operating activity and associated costs at Jenkins and Nkomati, with those mines expected to reach steady state in the coming year. With a drop in iron ore prices and those ramp-up pressures on margin, the Bulk Commodities segment reported a drop in operating profit of 15.6%.

There isn’t much that Afrimat can do about iron ore prices, or the reality of starting up new operations. Sadly, there also isn’t much that the company can do about broader South African economic activity. With electricity supply disruptions and a slowdown in economic activity, Industrial Minerals saw operating profit fall by 41.9% and Construction Materials dropped by 17.7%.

The Future Materials and Metals division is interesting but still very small, with revenue of R25.2 million and start-up losses of R11.4 million.

The total dividend for the year of 150 cents per share is 19.4% lower than the prior year. This is a larger drop than the decrease in HEPS of 15.7%.

Even Afrimat, with all its diversification and track record of excellent management, isn’t immune from the pressures out there.

Coronation flags a loss based on its key metric (JSE: CML)

The tax troubles are temporary, but painful

Some coronations are full of pomp, ceremony and old-fashioned traditions that surprisingly still manage to draw huge crowds in the UK. Others are full of tax troubles and disappointing numbers, at least for now.

Coronation’s internal metric used to measure performance is fund management earnings per share. It excludes mark-to-market impacts and forex effects on investment securities held. On that measure, Coronation expects a decrease of between 102% and 112% in the six months ended March. This is a loss of between 4.3 and 25.8 cents per share.

If the impact on investment securities is included, then HEPS will drop by between 89% and 99% to between 2.0 and 21.9 cents per share. In this case, the market moves went the right way. It’s just a real pity about the tax.

IFRS 2 charges take Datatec into the red (JSE: DTC)

The share-based remuneration costs have severely hurt the numbers

Datatec reported a headline loss of 9.3 US cents per share for the year ended February, a number that bears little resemblance to the story at operational level.

The performance of Westcon International has been very strong in recent years, leading to a significantly higher valuation for that division and a large IFRS 2 charge based on share-based remuneration plans. So large, in fact, that it is responsible for the group reporting a loss. Yes, this is highly unusual.

Looking at numbers that are perhaps a better reflection of underlying performance, revenue from continuing operations increased by 13% for the year in dollars. That’s more like it. This excludes Analysis Mason, which was sold during the year for a profit on sale of $109.9 million.

Aside from the performance at Westcon, Logicalis International also did well with a much better second half in the Latin America business.

If the IFRS 2 charge conveniently wasn’t there, underlying earnings per share would be 29.5 US cents per share. This is the metric that the board will use in considering a cash dividend for the year.

If you needed further proof that shipping is cyclical…

During the pandemic, shipping companies made more money than they could count. In the latest quarter, Grindrod Shipping just reported a loss. Here’s what that journey looks like on a share price chart:

If we dig into the details, we find that revenue fell year-on-year from $110.3 million to $76.8 million. That isn’t quite the entire story, as vessel revenue fell from $110.2 million to $52.8 million. This is because the sale of vessels is recognised as revenue, so you need to strip that out in my opinion to see what is really going on.

To give a better sense of just how significant the drop in shipping rates has been, Handysize TCE (the way of measuring daily rates in this industry) was $9,491 per day in this quarter vs. $22,201 per day in the comparable quarter. The trend is similar in other shipping sizes.

When you combine this with pressure on operating costs from the likes of lubricating oil, the profits disappear as quickly as they arrived. Gross profit fell from $40.7 million in Q1 2022 to $7 million in this quarter.

The company fell from a profit of $29 million to a loss of $4.3 million in this quarter.

Investec achieved a juicy increase in HEPS (JSE: INL)

This is a case study in the joy of positive JAWS

For some reason, I’ve not really seen the JAWS ratio make its way outside of banking. Even Investec doesn’t seem to use the term in the SENS announcement dealing with results for the year ended March 2023. Having spent time working in a different local bank, I can tell you that JAWS is a major focus area for the traditional South African banks.

It’s simple, really. JAWS measures the difference between the growth rates of income and expenses. If those JAWS are pointing the right way, then margins go up. If expense growth is outpacing income growth, margins go down.

At Investec, the latest period reflects revenue growth of 14.6% and operating cost growth of just 9.5%. The net result? A 28% increase in pre-provision adjusted operating profit. Although the credit loss ratio increased to 23 basis points (still below the through-the-cycle range of 25 basis points to 35 basis points), HEPS was 25.3% higher.

With a geographical lens, Southern Africa grew adjusted operating profit by 14.6% and the UK business grew by 30.5%.

Return on equity has increased from 11.4% to 13.7% and the net asset value has remained flat despite the distribution to shareholders of the 15% stake in Ninety One, along with other dividends and share buybacks.

Strategically, the group will hope that combining Investec Wealth & Investment UK with Rathbones plc will create a stronger franchise in the UK in the wealth management space.

The dividend payout ratio is largely consistent year-on-year, so the dividend per share is 24% higher.

The share price is up more than 18% in the past year.

Investec Property Fund is a lot less juicy than the bank (JSE: IPF)

Thedecline in distributable income per share is in line with guidance

These results are further proof of my irritation with property “ManCos” and how they are little more than a glorified way to rip off shareholders. The management teams of property companies obviously play a substantial role in results, but they are ultimately managing a stream of cash flows and they are beholden to macroeconomic challenges that are always blamed for tough results.

Do they deserve an asset management fee for this rather than a salary and bonuses? Do they really behave like fund managers with a broad mandate, or do they behave like operational managers in the same way as executives in other sectors do? I think my view on it is obvious.

For the year ended March, Investec Property Fund reported a drop in distributable income per share of 2.8%. The weighted average cost of funding in Europe was part of the problem, with rates now capped and limited further risk over the next 2.5 years. Those hedges don’t come for free, I might add.

The loan-to-value ratio of 43.4% looks high. The target is 35%, so capital will need to be recycled to lower debt.

The guidance for FY24 is low single digit growth in distributable income per share. It’s far more exciting to be in the ManCo than on the shareholder register, I’ll tell you that much.

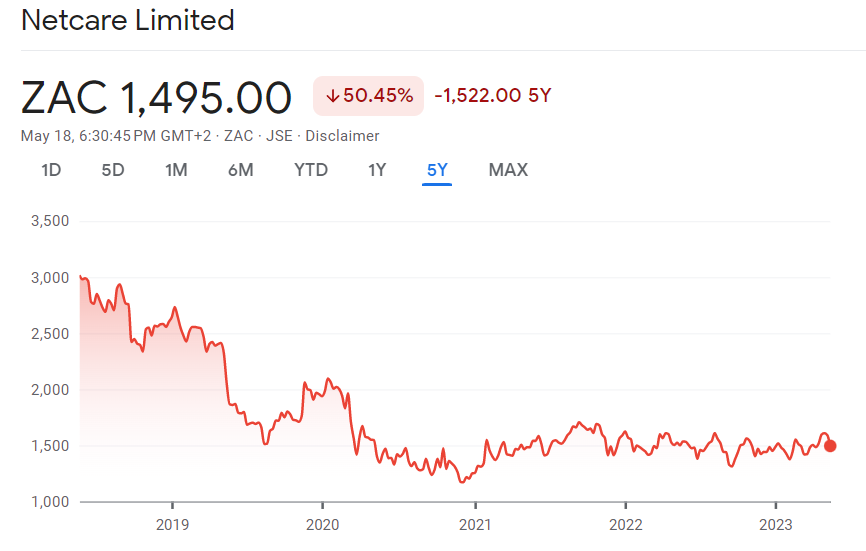

Netcare reports a significant jump in earnings (JSE: NTC)

The post-COVID normalisation continues

For the six months to March 2023, Netcare expects to report HEPS that will be between 39.8% and 41.4% higher. The management team likes to use adjusted HEPS to measure performance, with that metric up by between 31.0% and 32.4% – a lower growth number but still substantial.

In absolute terms, adjusted HEPS will be between 46.1 cents and 46.6 cents.

The last interim results that had no COVID impact were for the six months to March 2019. Sadly, that was before the implementation of IFRS 16, which arguably had an even larger impact than the onset of COVID right at the end of the 2020 interim period.

To give you context, I’ll thus mention the interim 2020 HEPS of 79.0 cents. As you can see, we are still running well below those levels. This explains the share price:

Purple Group confirms the terms of the rights offer (JSE: PPE)

Sanlam is underwriting the offer at Purple level and following its rights in EasyEquities

As the management team has been saying for a while, Purple Group needs to raise capital for the growth ambitions of EasyEquities. The company wants to replicate its model in other markets where the metrics look appealing in terms of potential user numbers, like Kenya. Efforts in the Philippines have already been underway for a while now.

The pricing for the offer has been announced as 81 cents per share, a discount of 31.87% to the 7-day VWAP. This rights offer will increase the number of shares in issue by 9.25%.

With Sanlam willing to underwrite the offer at that price, it gives a good idea of where an institution on the inside sees value in the shares. It also gives final evidence of just how ridiculous things had gotten at nearly R3.50 per share at the start of 2022.

Aside from Sanlam’s underwriting, shareholders with 27.12% of shares in issue have provided irrevocable commitments to follow their rights in full.

Sanlam will earn a 2% underwriting fee for the pleasure. This is standard market practice, as the reward for Purple Group is that the capital raise has effectively been derisked. The money will be raised – it just depends from who.

PLEASE NOTE: if you are a Purple shareholder, you will receive letters of allocation in your brokerage account on 29 May. If you don’t want to follow your rights and put in more money, you would be very silly not to try and sell the letters, as they will be worth something on the open market (likely close to the prevailing market price less the rights offer price). In other words, if you do nothing at all, you are likely to suffer a loss in value.

Across almost the entire business, Sanlam is stronger (JSE: SLM)

It’s little wonder that they are being such a supportive partner to Purple Group

In the first quarter of 2023, Sanlam reported a 25% improvement in the net result from financial services and a 38% jump in operational earnings. New business volumes are up at group level and even where there are pressures on volumes (like in the life business), value of new business margin has improved.

It was only the Investment Management business that reported a year-on-year drop in profits, down 2% as reported and 8% in constant currency. Sanlam notes a substantial once-off in the base, without which the result would’ve been 11% higher. At the other end of the spectrum, we find the Credit and Structuring segment as the biggest winner, up 45% as reported and 37% in constant currency.

As noted in the Santam update earlier in the week, the Allianz transaction is expected to close in the second half of 2023. It’s been a busy period of corporate finance for Sanlam (including deals with Absa and AlexForbes in the past couple of years), underpinned by solid numbers.

Little Bites:

Director dealings:

A number of associates of Piet Mouton have bought shares in Curro (JSE: COH) worth nearly R6.6 million.