Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

This year, Unlock the Stock is delivered to you in proud association with A2X, a stock exchange playing an integral part in the progression of the South African marketplace. To find out more, visit the A2X website.

In this nineteenth edition of Unlock the Stock, Calgro M3 returned to the platform with a triumphant set of results and a clear strategy for the way forward.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions. Watch the recording here:

Is the value unlock at Adcorp finally working out? (JSE: ADR)

Revenue has grown for the first time since 2016

If ever you want to learn about the pain of a bid-offer spread in small caps, Adcorp is a great way to do it. The spread has come down a lot if there’s a busy trading day. On other days, you could park a bus in there. This makes it difficult to trade the stock and you have to patiently sit on the bid or offer at your desired price, hoping for a trade. You can’t just give an instruction to execute at the best available bid or offer at any given time as you’ll get a nasty surprise.

Looking at the results for the year ended February, the (rather shocking) news is that revenue from continuing operations has grown for the first time since 2016. Talk about a lost half-decade! Cash flow is also a lot better, with cash generated from operations up 45.2%. Operating profit from continuing operations is down 18.4% though, with the major culprit being a significant impairment of goodwill.

It’s a complicated result to try and work through, but cash is a language we all understand. With a share price at time of writing of R5.44, a special dividend of 91.3 cents and a final dividend of 16.5 cents have been declared.

Brikor warns of a headline loss per share (JSE: BIK)

The brick and coal group will release detailed results this week

Brikor released a trading statement noting a headline loss of between 0.09 cents and 0.11 cents per share for the year ended February 2022. This is a move from green to red over the past year, as the prior period reflected positive HEPS of 1.1 cents.

The current share price is 15 cents.

Exemplar enjoys a rebound in retail property (JSE: EXP)

Some of the malls could probably fit inside the bid-offer spread!

Exemplar REITail is a perfect example of the liquidity that investors complain about on the local market. This property fund is worth a few billion rand, so it’s certainly not a small cap. Despite this, bids are at R9.00 and offers at R12.00, which is a gigantic spread that makes trade very difficult.

Leaving that issue aside, let’s focus on results for the year ended February 2023. The 26 retail assets in the portfolio enjoyed a much better year, with revenue up by 18.4% and the total dividend per share by 20% to 141.12192 cents. I’m loathe to quote the current price of R9.00 in giving you a trailing yield, as the spread is huge and the yield will change drastically depending on the bid vs. offer. Perhaps that’s the point, with the huge spread reflecting a yield of between 15.7% and 11.8%.

At a yield of 15.7%, it’s not hard to see why some people are sitting on the bid at R9 and waiting to be hit.

The net asset value per share is R13.74, up 11.8% year-on-year.

Take a trip to Poland with Redefine (JSE: RDF)

After the takeover of EPP by Redefine, there’s a lot for shareholders to consider in Poland

Redefine announced that a property tour is being held in Poland over the next few days. Aside from being a lovely excuse for the fortunate few to travel and enjoy a country with electricity, this is a also useful opportunity for all Redefine investors to learn more about the EPP portfolio that Redefine acquired as part of that takeover and delisting.

EPP is the largest asset manager of retail real estate in Poland when measured by gross leasable area (GLA). There are 35 projects of which 29 are retail and 6 are offices. The portfolio is split across 23 Polish cities, absolutely none of which can be successfully pronounced by anyone whose surname doesn’t have a lot of Zs and Ws in it.

The presentation also deals with the ELI portfolio, a group incorporated in the Netherlands and held 48.5% by Redefine Europe. The portfolio is also based in Poland, with a strong slant towards logistics properties.

You can find the full presentation at this link if you want to really dig in.

Steinhoff might be forced by SdK Schutzgemeinschaft der Kapitalanleger to appoint a herstructureringsdeskundige (JSE: SNH)

Spare a thought for business radio presenters everywhere

Reading that sentence will either give you anxiety or make you want to order a beer. Or both.

I’m not going to pretend to be close to the details on this Steinhoff restructuring plan. Frankly, it’s good enough for me that management has said multiple times that the equity is likely worth nothing.

With the group trying to enter into the WHOA Restructuring Plan, it was the shareholders who said “whoa!” in the end. Unsurprisingly, the creditors who stand to receive some value all voted in favour of the plan and the shareholders left out in the cold didn’t.

From my understanding, the potential outcomes are that a court sanctions the WHOA plan regardless of the shareholder vote, or Steinhoff will end up in liquidation.

To celebrate the equity possibly being worth zero in an unexpected way rather than the communicated way, punters drove the share price around 3.8% higher in afternoon trade. No, I still don’t understand why anyone is buying here.

Transcend Residential Property has 97.4% occupancy (JSE: TPF)

People need somewhere to live

The latest results from Transcend Residential Property Fund cover the 15 months to 31 March 2023. The year end was changed, so the year-on-year growth numbers are pointless as we are comparing 15 months to 12 months. To make it worse, the base period had a whole lotta Covid in it.

Instead, I’ll just look at the latest facts, like an occupancy rate of 97.4% and a loan-to-value ratio of 37.1%, which is far more palatable than it used to be. This was achieved through the sale of 425 residential units to raise R390.7 million in cash, which was then used to reduce debt.

The company is taking full advantage of the availability of so-called “green” finance, comprising 68% of the total loan book and offering a rate benefit based on the underlying use of the funds and the ESG metrics.

The distribution per share is 72.34 cents which implies a yield of 11.3%. Again, I would caution that there are three extra months’ worth of profits in that number.

The net asset value per share is R8.40 and the share price is R6.40.

The market didn’t love the Zeda numbers (JSE: ZZD)

Car rental activities are still way below pre-pandemic levels, but the debt is the focus

It was rather interesting to see the Zeda share price come under pressure particularly in afternoon trade after releasing interim results early in the morning. On the face of it, they really didn’t look bad with revenue up 20%, EBITDA up 19% and operating profit up 25%.

Return on equity was up by 590 basis points to 28.3% and net debt to EBITDA improved by 60 basis points to 1.6x.

So, for the six months to March, it’s unlikely that the year-on-year numbers were the cause of concern in the market. I suspect that the balance sheet and the lack of dividend were to blame.

The trouble might be in some of the commentary, which touches on obvious pressures in the market. For example, margin on used cars reduced in the second quarter of the financial year as supply chain issues normalised. This is a worry for the second half of the year, as the used car side of the business is a critical part of the car rental value and leasing value chain. Those cars are eventually sold through the used car retail footprint and online auction platforms, so Zeda needs a robust used car environment.

Zeda owes a big chunk of money to Barloworld based on a loan from its old parent company. Now as a separately listed entity, Zeda’s balance sheet needs to be able to stand on its own feet. Some of the market jitters might be around this debt which is due by the end of the calendar year. Still, Zeda says that the company is on track to settle the debt.

Looking at the car rental business, the huge growth in inbound travel and corporate travel drove increases in revenue of 138.7% and 69.5% respectively vs. the prior period. If you read deeper into the results, you’ll see a comment that total car rental activities are still operating at only 26.8% of pre-pandemic levels. As always, bulls will see this as growth runway and bears will see this as a structural decline in demand.

I’m a bit on the fence with this. I think the adoption of video calling has removed a layer of business travel forever. I also think that the unreliability of Uber in South Africa is a major boost for car rental firms, with so many people on Twitter experiencing horrible service from Uber. I’ve also really struggled to get an Uber at times, which doesn’t build confidence in the platform.

The leasing business is a useful part of the group, helped along by commercial vehicles and the higher interest rate environment that makes it more difficult to buy rather than lease. But with revenue only up by 6% and EBITDA down by 2% in that segment, this could be another area that caused concern in the market.

Interim HEPS was 189 cents per share, up just 4% because of the net interest costs increasing by 56%. There is no interim dividend per share, with the group presumably focused on the debt reduction. The share price slipped below R10 in afternoon trade, so the Price/Earnings multiple looks modest on an annualised basis. It all comes down to the debt.

Little Bites:

Director dealings:

Directors executed small additional purchases of Calgro M3 (JSE: CGR) shares to the value of R14.5k.

Holders of 70.75% of shares in AfroCentric (JSE: ACT) tendered their shares in the offer from Sanlam (JSE: SLM). Each participant can now choose the split between cash and Sanlam shares in line with the circular, with a value of R60 per Sanlam share being used in the formula as the 30-day VWAP came in at R54.

Buka Investments (JSE: BUK) has absolutely no bids and offers in the market, so the trading update only earns a spot in Little Bites. The headline loss per share is expected to be between -25 and -31 cents for the year ended February 2023. The share price is only 73 cents. In case you are wondering where you’ve heard this name before, Buka Investments is what became of the Imbalie Beauty listed shell. I would love to give you a website link but I can’t find one and got tired of looking – the company clearly isn’t bothered about anyone finding information.

In the land of sunshine and braais, where the woes of loadshedding have become a dishearteningly familiar refrain as Eskom’s troubles continue to cast a shadow over South Africa’s energy landscape, savvy investors may seek refuge in alternative energy.

As the sun sets on traditional power sources, we look at Renergen (JSE: REN) as this trailblazer harnesses the winds of change and captures the essence of possibility in a world where investing in the Green Wave gains significant traction.

Lights Out, Ideas On: Exploring Alternative Energy Amid Loadshedding

As South Africans come to terms with the dim reality that loadshedding is no temporary inconvenience but rather a permanent fixture in our everyday lives, alternative energy solutions may prevail as viable investment options for market players looking to safeguard their portfolios from the ongoing energy crisis.

According to the South African Reserve Bank, loadshedding is expected to increase by nearly 60% in 2023 from 2022, which could wreak havoc concerning economic growth and inflation. The persistent blackouts are predicted to inflate prices by a staggering 1.1% annually, and with South African inflation remaining stubbornly high, it is clear that loadshedding has economic consequences far more extreme than many could fathom. With headline consumer inflation ticking higher to 7.1% in March, up from 7% in February, further rate hikes may be in store for the already-struggling average South African consumer.

Amidst a landscape riddled with uncertainty, we direct our focus to Renergen. This innovative domestic alternative energy company holds the potential to illuminate some of the darkness cast by Eskom’s challenges. As a recent pioneer in the industry, Renergen offers a potential hedge to the Eskom woes and embodies the global trend towards reducing carbon emissions and investing in renewable energy solutions. The company’s operations align seamlessly with the quest for long-term sustainability, making it all that more topical. However, as the traditional saying goes, “Don’t count your chickens before they hatch,” market participants should understand there is still a long way to go before Renergen becomes a formidable force in the global helium and natural gas-producing industry.

Renergen Limited (JSE: REN)

In a world where innovation meets sustainable energy solutions like never before, Renergen, a trailblazing force in the energy sector, is making significant strides in unlocking a cleaner, greener future. With their pioneering technology, Renergen captures and liquefies natural gas from underground helium wells, taking a giant leap towards energy independence and reducing carbon footprints.

Through Renergen’s Virginia Gas Project, South Africa has joined a league of eight nations producing their own liquid helium, playing an indispensable role in numerous cutting-edge industries. From propelling space exploration and fuelling rocketry to empowering high-level scientific advancements, enhancing medical MRI machines, revolutionising fibre optics and telecommunications, enabling superconductivity, and empowering nuclear power stations, helium’s versatility knows no bounds. While helium is a precious resource known for its scarcity, the economic viability of its extraction is noteworthy. It becomes a financially viable pursuit even at concentrations as low as 0.1% within natural gas.

However, the Virginia Gas Project stands out with an impressive average helium concentration of 3.4%, which could open up unprecedented possibilities, potentially solidifying Renergen’s position as a valuable player in the helium extraction landscape.

Although the company aspires to become a global helium-producing powerhouse, significant work remains for Renergen to finalise the Virginia Gas Project before reaping such benefits.

Renergen has already successfully sourced liquefied natural gas (LNG) and liquid helium from the Phase 1 plant in its Virginia Gas Project, making it the world’s newest producer of liquid helium.

While the company’s Phase 1 liquefaction plant can produce approximately 50 tons of LNG daily, the subsequent phase is expected to produce the bulk of LNG and liquid helium. Renergen aims to increase its production capacity to around 680 tons daily, equivalent to approximately 940,000 litres of diesel per day, when it rolls out the Virginia Phase 2 liquefaction plant.

On that note, Renergen has outlined its strategic goal of establishing a series of LNG refuelling stations across South Africa in the coming three years. This initiative will be implemented once Phase 2 of the Virginia Gas Project becomes operational.

In a recent announcement, the company provided a glimpse into its endeavours through a collaboration with Time Link, a privately-owned transport and logistics company based in Cape Town.

Through its subsidiary, Tetra4, Renergen has entered into an agreement with Time Link to supply LNG for their long-haul fleet, facilitating the company’s transition from costlier diesel fuel.

According to Renergen CEO Stefano Marani, establishing LNG refuelling points along major highways in the country is expected to proceed smoothly. Marani emphasised that these fuelling points will primarily cater to the transportation of goods between cities. Using LNG instead of diesel during long-haul trips, such as from Cape Town to Johannesburg, offers substantial cost savings. Additionally, Time Link acknowledged the positive environmental impact of reducing diesel consumption in their fleets, saying, “As fleet operators, we are always looking to reduce our carbon footprint, enhance fuel efficiency and reduce costs. Introducing LNG to displace diesel in our fleet makes sense.”

While there is still a long road ahead before Renergen completes the second phase of its Virginia Gas Project, it appears the company already has an advantageous position nationally and globally in the energy and helium sectors.

South Africa’s daily helium consumption sits at a mere 200kg, while the United States has an average daily consumption of approximately 35,000kg. The Virginia Phase 1 liquefaction plant aims to steadily increase liquid helium production to around 350kg per day during 2024, while the second phase is expected to reach a production capacity of up to 4,200kg per day. Having said that, if Renergen can successfully roll out the completion of its second phase in its Virginia Gas Project timeously, the potential exists for the company to emerge as a global powerhouse in the liquid helium-producing industry.

Fundamental Analysis

In Renergen’s recently-released 2023 financial statements, the locally-based natural gas and helium producer reported an impressive 381% year-over-year surge in revenue, coming in at R12.69 million for the 2023 financial year. Despite not realising a profit, the company cut its net loss figure by more than 20% to -R26.73 million for the 2023 financial year, while its EBITDA figure improved by just over 23% to -R30.11 million.

These improved financial results align with Renergen emerging as a producer rather than an explorer.

Year-to-date (YTD), Renergen has seen its share price outperform fellow industry peer Montauk Renewables, as seen in the price chart below. Despite outperforming its alternative energy peer, Renergen has lost nearly 7.5% to shareholders (orange line) since the beginning of the year. Montauk Renewables has lost close to 35% to shareholders (green line).

Over the last three months, Renergen has returned approximately 3.5% to shareholders (orange line), while Montauk Renewables has lost 32% over the same three-month period (green line).

Technical Analysis

Analysing the weekly price chart of Renergen, it is clear that its share price has been consistently declining for just over a year, indicating a prevailing downtrend, with the 50-day moving average remaining above the candlesticks. Last week saw positive market sentiment push Renergen’s share price significantly higher, but this week has seen the share price retrace and tick down somewhat.

Looking at the daily chart analysis of Renergen, we can see that the company’s share price broke above its consolidation phase, exhibiting a pronounced upward trend. This week has seen some of that upward trajectory reverse as the share price retraces downward.

For the bull case, if positive sentiment persists around Renergen and if the local natural gas and helium producer rolls out the second phase of its Virginia Gas Project as expected, market participants could anticipate the share price to rise and potentially test the R26.40 resistance level (horizontal black dotted line). The R26.40 level could be watched closely by market participants as a potential entry point for bullish investors or a point at which the bears may expect a retracement toward lower levels.

For the bear case, if negative sentiment emerges as it has done in the past, Renergen’s share price could potentially fall lower and decline towards the primary support level at R17.00 (solid red line). Should there be a delay in rolling out the completion of Renergen’s second phase in its Virginia Gas Project, for example, market participants could potentially drag the share price lower.

Welcome to Ghost Wrap. It’s fast. It’s fun. It’s informative.

In this week’s episode of Ghost Wrap, we cover:

Pan African Resources shareholders are licking their wounds, with a major sell-off in the share price after a reduction in production guidance.

The Hosken Consolidated Investments (HCI) group of companies reported this week, with a vastly different picture at the mothership vs. underlying listed companies Deneb, eMedia and Frontier Transport.

Southern Sun’s earnings tell an interesting story vs. pre-Covid levels, particularly when assessed against occupancy levels.

Datatec has unfortunately found the “adjusted EBITDA” button, a metric that global technology groups just love using.

The poultry sector is in disarray, with Astral and Quantum Foods both reporting horrific drops in profitability despite increasing revenue – and that’s before the impact of the avian flu outbreak in April!

Lewis Group can’t rely on share buybacks forever, with the trend in cash sales vs. credit sales being cause for concern.

Trematon’s intrinsic net asset value per share is under pressure from Generation Education in particular, with worrying metrics in that business.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

When reading about a small financial services group listed on the JSE, it’s easy to assume that any troubles must be related to the local economy. In Finbond’s case, you would need a passport to go and find the problems.

Of all places, Illinois in the US has been the biggest headache for the group. Finbond needs to lend money to lower income customers and those customers were the beneficiaries of incredible levels of stimulus in the US. In a perverse irony of note, the US economy is too strong for Finbond to be doing well there.

To add to the difficulties, there were major regulatory changes in March 2021 in Illinois that caused problems for the business model, with a revised longer-term product leading to a lag effect in profitability. Simply, accounting rules require interest revenue to be earned over the period of the loan and credit loss provisions to be recognised upfront, so a period of strong growth in lending would actually have a negative impact on short-term profitability!

Now that your mind has been blown by good things that are actually bad things for Finbond, I can highlight the financial performance for the year ended February 2023. Revenue increased by 21%, gross loans and advances increased by 25.6% and the headline loss per share decreased from -17.9 cents to -15.1 cents.

There is yet again no dividend, which makes sense in the context of the headline losses.

I was surprised to see that no mention is made of net asset value per share anywhere in the announcement, especially as this is generally seen as a key input for valuations of financial services groups. Based on a very quick look at the market cap and equity on the balance sheet, it looks like a price/book of roughly 0.3x.

ISA Holdings displays resilience, if not growth (JSE: ISA)

The digital security group could only increase revenue by 1%

If you dig into the numbers of this technology small cap, you’ll see that ISA Holdings managed to tread water on the top line. The same can’t be said for operating expenses, which jumped by 22.5% largely due to payroll expenses. The company is clearly hiring, but the benefit hasn’t come through on the revenue line yet.

The net profit result was saved for the year ended February 2023 by a major increase in share of profits from associate DataProof, which increased from R1.6 million to R7.7 million. This made all the difference in profit before tax growing from R22.8 million to R26.4 million.

With all said and done, HEPS grew by 34% to 14 cents per share. At R1.35 per share, the business trades on a sizable valuation for a company with a market cap of just R230 million. The core business needs to show a much better margin story to justify that multiple.

They may tug at the heartstrings, but renewable energy projects aren’t guarantees of success

Mahube Infrastructure (JSE: MHB) has investments in a variety of wind and solar farms. It’s a small listed group, with a market cap of just over R300 million.

In a trading statement for the year ended February 2023, some of the challenges in this sector were laid bare. The fair value of the assets went the wrong way based on macroeconomic variables (like discount rates) and the adverse revision of long-term assumptions on the amount of electricity generated. I was surprised by the latter issue, as that is not good news for these types of projects.

The results were also impacted by a drop in dividend income, including from the wind investments that experienced adverse wind conditions during the reporting period.

Pan African Resources shareholders get a 21% hiding (JSE: PAN)

Production guidance has been revised sharply downwards

You won’t often see a significant local company receive a 21% smack from the market in a single day. Then again, you won’t often see a gold miner reduce its full-year production guidance by roughly 12.5% with just over a month to go until the end of the period.

If we compare the latest guidance from Pan African Resources to the midpoint of the previous guidance range, there’s a drop of 25,000oz. Approximately 10,000oz has been attributed to Eskom’s electricity supply, with the rest due to a slower ramp-up at Barberton Mines and lower than expected production at Evander Mines.

Renewable energy projects are underway, but these take time of course. The company also noted that the issues at Barberton have improved towards the end of this financial period. The problems at Evander Mines were due to geological challenges that take longer to deal with.

The only good news is that the Mintails project is expected to receive the last remaining approval imminently, which means plant construction can commence within the next month. Steady state production is expected by December 2024.

Thanks to strong gold prices, the group is still in a decent financial position and net senior debt could be reduced by as much as 50% since December 2022.

This period really is a case of what might have been, with production issues at a really unfortunate time when the gold price finally gave miners an opportunity to generate substantial cash flows.

Even looking ahead to the 2024 financial year, we see production guidance of 178,000oz to 190,000oz, which is still lower than the guidance of 195,000oz to 205,000oz that was on the table for the 2023 financial year before being reduced to 175,000oz.

The underperformance relative to peers is severe this year:

Quantum Foods is a lesson in margins (JSE: QFH)

Revenue growth doesn’t matter if costs have gone ballistic

The poultry industry is a wild place. I cannot think of another sector that is so volatile at net earnings level, with skinny margins that can vary for reasons far beyond the control of the companies in this industry.

In the latest interim period, revenue at Quantum Foods increased by 22.0%. It was cold comfort, as gross profit only increased by 6.6% and operating expenses grew by 8.4%. With such tiny margins in this sector on a good day, that was enough to smash operating profit by 57.4% and HEPS by 82%.

Quantum Foods describes the six months to March 2023 as the most challenging conditions since listing in October 2014. Across record high feed raw material costs, outrageous levels of load shedding and consumer pressure that makes it impossible to recover the costs through pricing increases on eggs, this has been a perfect storm for poultry.

The bigger issue is that there is no obvious improvement to any of these problems. The weak rand has a significant impact on raw material costs. We all know that Eskom has no solutions for any of us. Finally, it’s not like the situation is getting any better for South African consumers.

To give you an idea of how much more expensive it has become to raise chickens, the cost of layer and broiler feed increased by 30.3% and 27.4% respectively, while the selling prices for eggs only increased by 7.5% and volumes fell by 9%. There is a crisis brewing for South Africa’s core sources of protein.

If you’re hoping that Quantum has an exciting energy solution on the cards, you’ll be disappointed. The company is only at the point of having generators installed at its major sites, which of course only helps with availability of power rather than the cost thereof.

It gets worse before it gets better. Although this period wasn’t affected by avian flu, there was an HPAI outbreak in April 2023 at the Lemoenkloof layer farm in the Western Cape. Just this outbreak carries a cost of R34 million, which is frightening when headline earnings for the six months to March was just R6 million.

Unsurprisingly, there was no interim dividend for this period.

Texton moves ahead with the GEPF repurchase (JSE: TEX)

If you see a rights offer down the line, remember this day

This certainly isn’t the first time that Texton has had me scratching my head. The company isn’t exactly the gold standard in capital allocation track record, evidenced by a share price that is down roughly 60% over 5 years.

The latest unusual step is a massive specific repurchase of 19.8% of the shares from the Government Employees Pension Fund (GEPF), managed by the PIC. At a price of R2.15, this is a discount of 11% to the current traded price. That’s great for Texton shareholders and strange for the GEPF, as the net tangible value per share before the repurchase is a much higher R6.11.

It would make a lot more sense for the PIC to rather put pressure on the company to recycle capital and return it to shareholders, particularly with the price at such a high discount to the tangible NAV. I’m grateful that I have precisely none of my own money in the GEPF.

If Texton can actually afford this, it’s really good for remaining shareholders as they are getting rid of a big chunk of shares from someone else at a discount. My bigger concern is that the initial announcement around this deal mentioned a potential equity raise in future, which could then negate any benefit from this deal.

If you see a rights offer from Texton at any stage in the near future, just remember this repurchase price of R2.15 and compare it to whatever price the rights offer will be executed at.

Shareholders of Texton will need to approve the deal with a 75% approval required. It helps that Heriot Investments (with a 64.7%) holding has already agreed to vote in favour.

Will Tradehold regret its UK exit? (JSE: TDH)

Although losses were realised on disposal in the UK, things aren’t easy at home either

In November 2022, Tradehold sold its operations in the UK for just over R2 billion, realising a loss of R164 million after releasing forex reserves on the disposal. The proceeds were used to redeem preference shares held by RMB and pay a special dividend of R4.34 per share to shareholders in November.

This makes Tradehold a primarily South African group (73% of assets) so the reporting currency is now the rand.

Net asset value (NAV) per share has dropped from R19.47 to R12.40 over the year ended February 2022, of which R4.34 is due to the special dividend. This means that R2.73 is simply due to losses on the disposal of the UK assets and the general performance of the portfolio.

The highlight here is Collins Group, with a portfolio of mainly industrial buildings and large distribution centres. Net profit grew by 9% in this period, although the average increase on renewals was just 3% in this period.

Solar projects are obviously top of mind for distribution centres with huge roof areas. Collins is using a rental based model to roll out solar projects, so there is no capital expenditure outlay.

As a sign of the times, the group plans to increase its exposure to the Western Cape to 17% of the total portfolio, which still seems pretty low vs. 42% in KwaZulu-Natal and 39% in Gauteng.

A final dividend of 30 cents per share has been declared. At R7.99 per share, the discount to NAV is just over 35%.

Transcend Residential Property Fund flags higher earnings (JSE: TPF)

You need to read very carefully to spot the change in reporting period

In a trading statement released by the company, Transcend Residential Property Fund noted an increase of 28.29% in its dividend per share. That sounds extraordinary, until you realise that this covers the 15 months to March 2023 vs. the 12 months to December 2021.

So not only has the financial period been changed, leading to a once-off longer period, but the base period included plenty of Covid issues.

The growth rate is irrelevant here. Instead, the helpful information is that the dividend per share is 72.34 cents, so the trailing yield is 11.3% based on the current share price.

Little Bites:

Director dealings:

There is more selling in the gold sector, this time a prescribed officer of AngloGold Ashanti (JSE: ANG) selling R1.94 million worth of shares.

A name you won’t see in this section very often is Sea Harvest Group (JSE: SHG), so take note of an associate of an independent director buying R1.33 million worth of shares.

A director of Calgro M3 (JSE: CGR) has bought shares worth R92.8k.

Choppies Enterprises (JSE: CHP) has renewed the cautionary announcement related to the potential acquisition of 76% in the Kamoso Group, an FMCG business in Botswana. The negotiations were originally for a 100% stake.

With all said and done on the Sanlam (JSE: SLM) – AfroCentric (JSE: ACT) transaction, Sanlam will hold 60% of the shares in AfroCentric. It will be interesting to see how successfully the strategy is delivered going forward, as substantial promises were made to AfroCentric shareholders about the benefits of this deal.

The odd-lot offer by CA Sales Holdings (JSE: CAA) lives up to its name in my books. After considerable effort to attract a wide base of shareholders, the company is moving ahead with an odd-lot offer to try and mop up the 5,073 shareholders who each hold less than 100 shares. It’s also possible that this base was inherited from PSG as part of the unbundling. This is just 0.02% of the company, so I can understand the administrative burden vs. the total shareholding. What I can’t understand is that the total value of those shares is roughly R860k and the cost of executing the odd-lot offer is R680k! I’m sure the maths has been done, but I find it surprising that the company is a net winner on this basis. It shows how expensive it is to have a retail shareholder base in South Africa’s regulatory environment, though I must point out that an odd-lot means fewer than 100 shares and that’s a value of just R700 at the current share price.

Hillie Meyer will retire from the top job at Momentum Metropolitan (JSE: MTM) on 30 September 2023. His replacement is Jeanette Marais, who has been Deputy Group CEO since 1 March 2018. This seems like a solid example of succession planning.

2023 marks the 30th birthday of one of the most significant financial innovations of modern times – The Exchange Traded Fund (ETF). In this time, ETFs have championed the cause of democratising investing, levelling the playing field by making it simple and accessible for all.

Three decades on, these powerhouses continue to offer flexibility and diversity, drawing in the most inexperienced of investors while maintaining a strong performance – currently boasting an impressive $US10 trillion in assets under management (AUM).

After record inflows in recent years, it is no surprise that it’s predicted that ETFs will hold over $US20 trillion by 2026, representing a compound annual growth rate of 17% over the next five years. This makes ETFs more popular than ever and this can also be attributed to their accessibility and the rise in digital investment platforms.

Satrix introduced the first ETF to South Africa in 2000, and investors have never looked back. ETFs have seen an increase in fund inflows in South Africa due to their resilience, making them an attractive option for investors looking to weather the pandemic storm and current tough economic times. Currently, ETFs have an AUM of R129 billion in South Africa.

A true revolutionary of the investing world, ETFs are arguably the single-most disruptive and game-changing product the market has ever seen.

Prior to the advent of ETFs, investing was expensive, could be confusing to beginners, and offered fewer options for portfolio diversification. ETFs changed all that, providing a basket of securities that trade on an exchange, like a stock, allowing investors to access a wide array of different exposures at minimal cost.

The introduction of ETFs has transformed the investing landscape, making investing accessible to everyone, and allowing individuals to make their money work harder for them at minimal expense. The market has transitioned from being predominantly composed of wealth managers buying shares, to a more diverse investment market accessible to all. The impact of ETFs has been seismic, and their significance in democratising investing, particularly in South Africa, and helping retail investors ‘own the market’ cannot be understated.

Major milestones for the world’s greatest financial innovation

Here is a timeline of ETFs’ greatest hits so far:

The ETF is born: There were a few ‘prototype’ ETFs, from Wells Fargo’s efforts, to the Toronto 35 Index Participation units. Then, 30 years ago, in 1993, State Street Global Advisors launched the Standard & Poor’s Depositary Receipt (SPY), the first US-based Exchange Traded Fund (ETF), which tracked the S&P 500. It’s known as SPDR today, pronounced ‘Spider’. It’s still the largest ETF in the world, with over $370 billion in assets under management, consistently trading over 80 million shares daily. It was physicist-cum-submarine-specialist Nathan Most’s ‘baby’, and it took him about six years to launch.

Dotcom changed everything: The Dotcom boom catapulted ETFs into public consciousness, thanks to the proliferation of the internet, which fueled S&P 500 growth of 28% a year, on average, between 1995 and 1999. This catalysed growing awareness of the power of indexing to ‘own the market’, versus stock picking.

A big Millennium moment: In 2000, European ETFs launched for the first time, following approval from the Undertakings for Collective Investment in Transferable Securities (UCITS) directive from the European Union. In 2000, ETFs had $65 billion in assets. By 2010, this grew to $991 billion. 2000 also saw the first factor-based ETF come into existence in the US.

Satrix brings ETFs to South Africa: Satrix pioneered its flagship Satrix 40 ETF, the first-ever South African ETF in November 2000, the same year the product launched in Europe. Kingsley Williams, our CIO, says, “We pioneered index tracking in South Africa to disrupt the status quo. Today, the power of investing belongs to everyone.”

The Dotcom bust (2000-2002): The Dotcom bust showed many investors that trying to beat the market was incredibly difficult to do with any degree of consistency. A low-cost, well-diversified fund, with low turnover and tax advantages was an attractive option in a time of total upheaval, so ETF uptake grew considerably.

Bonds arrive: Bond ETFs were launched in 2002, giving investors more opportunity to build diversified portfolios at low cost. It took close to 20 years for bond ETFs to surpass $1 trillion in global assets. BlackRock predicts they’ll hit $2 trillion by 2024. Commodity ETFs came shortly after bonds. All these different asset classes helped further democratise investing.

Active ETFs arrive: 2008 saw the first actively-managed ETFs launch, combining the traditional benefits of ETFs like low fees and tax efficiency, while capturing an active investment strategy. South Africa was only to see the Active ETF landscape materialise in 2023.

ETFs ramp up in retail: ETFs started to gain traction in the retail market (non-professional) during the 2010s, driven by education and awareness, and people’s cost sensitivity and desire for transparency. They offered a plethora of interesting products at excellent price points. They also allowed astute investors to stay ahead of the curve, without having to wait for forward pricing for trust and mutual funds.

The $1 trillion milestone is met: ETFs hit the trillion mark in assets under management in 2009.

Sustainable ETFs take off: There’s been growing demand for sustainable and ESG-linked ETFs that allow investors to align their values with their investments. Satrix was the first to launch an ESG ETF in South Africa in 2019, with its Diversity and Inclusion ETF. Global ESG ETFs have had a 90% compound annual growth rate from 2015 to 2020. In 2020, ESG ETFs took approximately 10% of overall ETF flows globally. Sustainable assets are expected to double by 2025.

No more minimums: In 2015, South Africa had another major ETF milestone when Satrix removed all minimums, making investing more accessible than ever before, with the launch of SatrixNOW.

Invest more, offshore: ETFs also gained a lot of traction in South Africa because they allow for 100% offshore exposure, without people having to lose their foreign allowance capacity. Satrix’s partnership with iShares, for example, has been a major game changer for accessing foreign markets.

Covid-19 caused major adoption: Counterintuitively, during the pandemic Satrix saw record investing inflows to ETFs. ‘Locked’ at home, many people had some disposable income available, and ETFs presented a safer option, in a time of serious distress. In 2019, the total AUM in the SA investment market was about R6 trillion, of which 5.3% was made up of indexed assets. This rose to R6.7 trillion (6.7%) by the end of 2021. Globally, the pattern was the same, with the pandemic pushing major money into index products, like those tied to the S&P 500.

The first crypto ETF arrives: 2021 saw the first ever Bitcoin ETF launch in the US.

Passive surpasses active: In 2022, the AUM of equity indexed funds surpassed active funds in the US for the first time. Research shows global net inflows into indexed strategies have been far more consistent, relative to active funds, attracting 59% of new net flows from 2009 to 2019.

🎈 Happy 30th birthday to ETFs! 🎂 We’re proud to be a part of this industry that brought about an evolution in portfolio construction with greater choice, more features, reduced costs, and a consistently compelling performance. And their next chapter promises greater growth than ever before.

Disclosure Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

African Media Entertainment rides a radio recovery (JSE: AME)

The trading statement is highly encouraging

Covid wasn’t great for the radio industry. That statement may not make sense at first blush, but the live events and music festivals held under the radio station banners are highly lucrative and nobody wanted to attend them as masked balls.

Things are better now, with African Media Entertainment guiding growth in HEPS for the year ended March of between 21% and 40%.

AYO Technology flags a large loss (JSE: AYO)

The headline loss per share has more than doubled

For the six months to February, AYO Technology has guided for a headline loss per share of between -75.63 cents and -82.49 cents. That’s huge when the share price is only R3.05! The headline loss per share in the comparable period was -35.90 cents.

The company has attributed this to lower gross margin, restructuring costs and fair value adjustments on options.

Finance costs hurt Deneb in this period (JSE: DNB)

And if you split out insurance proceeds, it’s worse

Deneb is part of the HCI stable and the company holds some interesting assets, though you would be forgiven for thinking otherwise based on the absolute lack of commentary on the underlying operations in the result.

Although revenue at Deneb managed to grow 14%, gross margin pressure meant that the increase in gross profit was unexciting.

With the usual inflationary pressures factored in alongside higher net finance costs, HEPS fell by 15%. If you exclude the business interruption proceeds insurance in this period, it fell by 45%!

eMedia: from Anaconda to Afrikaans Turkish telenovelas (JSE: EMH)

Diversification has helped at a time when advertising revenue is dropping

eMedia owns not just e.tv, but also other assets like YFM (the radio station) and local film studios. This diversification has been helpful in a period of extended load shedding, with the company believing that Eskom has cost the TV advertising industry a whopping R500 million in revenue.

I think it’s pretty good that group revenue only fell by 0.6% in this environment, with profit down by 10.3%. The market clearly didn’t see it coming, with the share price dropping 9.7% on the day. A 20% drop in the dividend (and hence a lower payout ratio) may have been a driver here.

I found myself thoroughly intrigued by a note that Afrikaans Turkish telenovelas have been a major audience generator in the eVOD platform. This is the local version of a Netflix Originals strategy!

To give context to the results, group profit was R377 million and within that number, we find smaller subsidiaries like Media Film Services with net profit of R45 million and YFM on R15.9 million.

Frontier Transport Holdings – are you on the bus? (JSE: FTH)

You may not even be aware that these businesses are listed

Frontier Transport Holdingsis one of those companies that only a close market watcher will likely know about. Part of the Hosken Consolidated Investments (JSE: HCI) stable, it includes businesses like Golden Arrow Bus Services.

For the year ended March, revenue increased by 15.1% but operating expenses increased by 18.9% over the same period. This margin pressure was driven by issues like fuel costs, with EBITDA only 2% higher as a result.

Thanks to a reduction in debt and thus finance costs, HEPS was up 5.9%. The full year dividend of 57 cents is a 9.6% increase on the prior year.

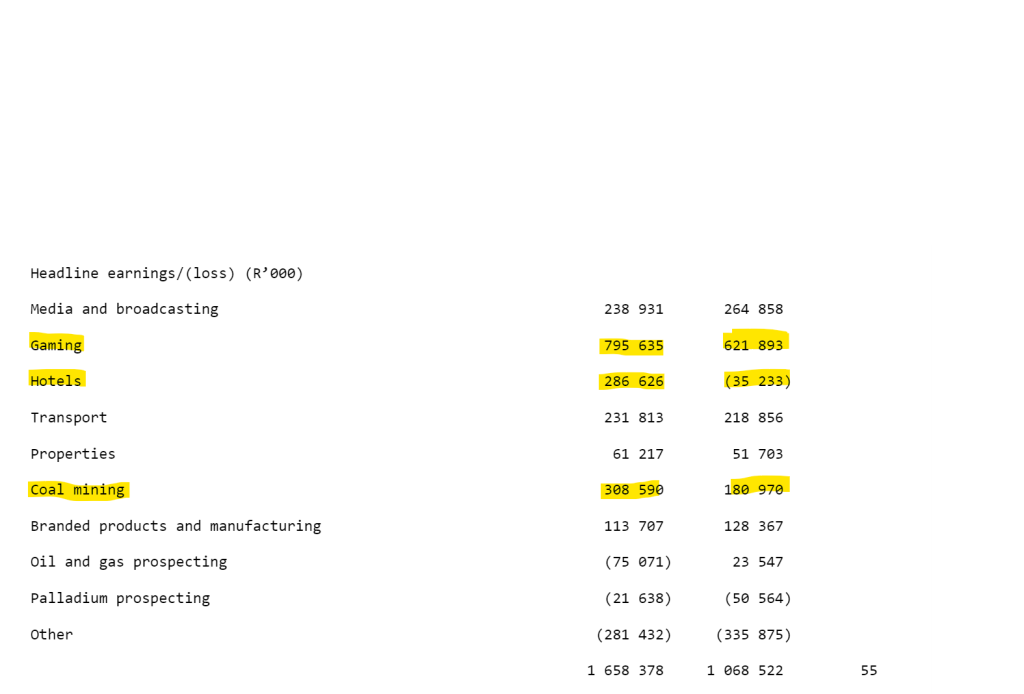

HCI’s solid result is underpinned by gaming and hotels (JSE: HCI)

A helpful contribution from coal doesn’t hurt, either

Hosken Consolidated Investments (HCI) is a fascinating group. It’s always a busy time on SENS when the company reports, as the reporting cycle is the same as the other listed companies that are part of the HCI group, like eMedia, Deneb and Frontier Transport Holdings. Those have all been covered separately today.

The easiest way to get a quick sense of the group is to use this table directly from the earnings release for the year ended March 2023:

The headings are cut off, but the latest period is on the left. You can immediately see the improvement in gaming and hotels, with coal also a lot higher. Note the pressure in media and broadcasting, particularly the television assets that don’t perform well during load shedding.

Your eyes aren’t deceiving you. In the bottom right, that is indeed a 55% jump in headline earnings.

With an investment focus on oil and gas prospects in Namibia, the group decided not to declare a final dividend. Watch this space.

Lewis feels the bite of economic pressure in SA (JSE: LEW)

Thanks to the ongoing share buybacks, HEPS managed to inch higher

Furniture retail group Lewisis well known among investors for a share buyback approach that has produced far better results for shareholders than would otherwise have been the case. Lewis trades at stubbornly low multiples, so share buybacks tend to be lucrative.

Share buybacks only get you so far, though. Lewis is facing considerable pressure in its operations, driven by broader challenges in South Africa.

Perhaps the biggest concern is that cash sales are moving sharply in the wrong direction. Cash retailer UFO suffered a sales drop of 12.5%. Group credit sales grew by 18.1% while cash sales fell by 16.3%. Ouch. It does at least help that the quality of the book has improved year-on-year, with the impairment provision improving from 40.4% of the book to 36.2%.

Total group revenue increased by 3.1% and gross margin improved by 10 basis points to 40.6%. Lower shipping rates have been helpful here. Despite this, operating profit fell by 8.3% as inflationary pressures in the cost base were too much to bear.

Here’s where the magic of share buybacks comes in: although headline earnings fell by 9.8%, headline earnings per share (HEPS) was actually up by 1%!

Life’s core business is performing strongly (JSE: LHC)

A VAT dispute settlement overshadowed the latest results

For the six months ended March 2023, Life Healthcare grew revenue by 12.9% and normalised EBITDA by 13.9%. That sounds great, until you read about normalised earnings per share only increasing by 1.1%. You can largely thank the tax dispute with SARS for that, with Life having paid R246 million in VAT of which R199 million was provided for in the prior period. This was despite Life having “strong legal and tax opinions” on this.

Something we aren’t reading about very often at the moment is margin expansion in Southern Africa, yet Life has managed to enjoy the right side of operating leverage in the land of load shedding. Revenue was up 11.6% and normalised EBITDA increased by 13.5%. In the AMG business in Europe and the UK, revenue grew by 15.5% and normalised EBITDA by 10.8%.

Net debt to EBITDA at 2.17x is higher than the comparable period at 2.03x, but remains manageable.

Strategic focus areas at the company include further investment in molecular imaging in South Africa and renal dialysis clinics, also in the local market. The hospitals have always had to be able to function with emergency electricity, so this is one of the few industries where capital expenditure is still going into the core business rather than into power backup solutions. Capex in Southern Africa was R514 million in this period, of which R418 million was on refurbishment and “portfolio optimisation” – classic boardroom terminology.

Despite the decent core results and a 13.3% increase in the dividend per share, the share price closed 7% lower.

Importantly, Life is still in discussions with various parties regarding unsolicited offers received for the AMG business in Europe.

Margins under pressure at MiX Telematics (JSE: MIX)

The impact on HEPS from a tax charge was severe

In the year ended March 2023, MiX Telematicsmanaged to grow revenue by 15.7% or 10.3% on a constant currency basis. The acquisition of FSM was a positive contributor here, responsible for 4.5% of the 11.9% constant currency growth in the subscription revenue line specifically.

Margins went the wrong way though, with gross margin down 110 basis points and operating margin down 190 basis points. The additional pressure in operating margins was due to restructuring costs, the benefits of which should start coming through.

Because of a massive deferred tax charge on intercompany loans, HEPS fell by 46%. On an adjusted basis excluding restructuring costs and the deferred tax charge, it was slightly up year-on-year.

Old Mutual was a mixed bag this quarter (JSE: OMU)

A group this size usually has winners and losers in any given period

In an update for the three months to March, Old Mutual reported a 1% drop in Life APE sales mainly because of China, without which the sales number would’ve been 7% higher. Persistency is under pressure, which means that Old Mutual’s clients aren’t necessarily hanging on to life policies.

Gross flows increased by 22%, with Futuregrowth as a strong contributor here. Unfortunately, outflows in wealth management across all platforms was a partial mitigator of that good news story around flows.

Loans and advances were flat year-on-year, which tells me that Old Mutual is being cautious in this environment.

On the insurance side, gross written premiums increased by 19%.

Squid games at Premier Fishing and Brands (JSE: PFB)

There’s a tasty jump in operating profits at the company– but no dividend

For the six months to February, Premier Fishing and Brandsreported a 15% jump in revenue, with the squid sector as the major driver of the strong jump in revenue. Lobster and hake deep sea also did well.

The problem is that shareholders of Premier didn’t get the lion’s share here, with a large part of profits attributable to minorities. This led to a drop in HEPS of 61.6%.

There’s also trouble on the balance sheet, with profits not flowing through into cash in the way that the company would’ve liked. There is no interim dividend.

Reinet flags a 2.9% drop in NAV year-on-year (JSE: RNI)

The compound growth rate since 2009 is 8.8% in euros

The drop in NAV at Reinetover the past year is mostly attributable to the stake in British American Tobacco (JSE: BTI), a company which I don’t believe is as defensive as the market likes to think it is.

The private equity investments had a good year, up by 26%. Although everyone only ever talks about the stakes in British American Tobacco and Pension Corporation, Reinet actively reinvests dividends in new opportunities that can be quite exciting, like technology funds.

The proposed dividend of €0.30 per share is 7% higher than the comparable period.

Southern Sun’s profits beat FY20 (JSE: SSU)

This is despite a lower occupancy rate than pre-pandemic

There are two ways to think about the occupancy rate. If you’re bearish, you might argue that a full recovery in occupancy isn’t coming for a long time, with a structural decrease in business travel and economic pressures on leisure travel. If you’re bullish, you could argue that there is runway for further improvement in this story.

Or, you could simply read the Southern Sun announcement, in which case you’ll see commentary around a normalisation of travel patterns except for the Sandton node. Structurally lower activity in Sandton has been a theme of the post-pandemic world, with devastating effects on office property owners in the area.

Welcome to the markets, where people can look at the same piece of information and form completely different views.

The year-on-year performance is a little silly, with EBITDAR (that’s not a typo – it’s the standard measure in hotel groups for operating profit) more than doubling from R590 million to R1.4 billion. The more interesting approach is to compare it to FY20 (where only one month was impacted by Covid), in which case EBITDAR is 6.2% higher despite occupancy of 51.5% vs. 59.3% in FY20.

In a great demonstration of how sensitive profitability is to occupancy above the point where fixed costs are covered, occupancy was only 30.6% in FY22. So, occupancy increased by roughly 68% (51.5% vs. 30.6%) and profits increased by approximately 140%. Welcome to hotel economics.

Winter is coming. The group notes the uncertainty around demand over this period, particularly with load shedding. The good news is that the balance sheet is in good shape to weather this storm.

The share price has made a full recovery vs. pre-Covid levels but seems to have run out of steam in 2023:

Stefanutti Stocks: under construction (JSE: SSK)

Valuation is everything – as evidenced by this share price move

The markets can be confusing. A company can release seemingly solid results and watch its share price drop. Stefanutti Stocks can release a headline loss per share of -38.73 cents for the year ended February 2023 and watch its share price close 9.6% higher.

It all comes down to what the market was pricing in. When it comes to Stefanutti Stocks and its broken business that is being restructured, this bruised and battered fighter isn’t exactly priced for great expectations.

The restructuring plan is being implemented over the year ended February 2024. It includes everything from the sale of non-core assets through to a potential equity capital raise.

This is a perfect example of a speculative punt on a turnaround story. With an operating profit from continuing operations of over R100 million but a total loss from continuing operations of -R37.5 million, there is something to save here underneath layers of difficulty.

Texton looks to take the PIC out at a good price (JSE: TEX)

A large specific repurchase is on the cards

Textonis proposing a repurchase of approximately 19.8% of its share capital from the PIC at a price of R2.15 per share, a substantial discount to the current traded price of R2.41. That may sound strange, but there’s absolutely no chance the PIC could sell a stake that size on the open market without smashing the price into oblivion.

Here’s the funny part: the repurchase will come out of existing cash resources, but Texton may then require a rights offer for its strategy. At what price does the management team think a rights offer can be achieved?!?

Assuming a rights offer goes ahead, is there really a saving here for shareholders net of transaction costs on the buyback and the rights offer?

Little Bites:

Tsogo Sun Gaming(JSE: TSG) has built a 10% stake in City Lodge (JSE: CLH) very quickly, which obviously has gotten the market talking about potential takeout activity. The City Lodge announcement doesn’t specifically mention Tsogo Sun Gaming, but the companies that own the 10% stake were figured out by financial media houses to be part of the Tsogo Sun Gaming group.

With the scheme of arrangement for the take-private of Mediclinic (JSE: MEI) sanctioned by the UK court, the listing on the JSE will be terminated on 7 June.

It won’t make much of a dent, but every bit helps – Nampak (JSE: NPK) has sold a property in Tanzania for $5.5 million, payable over four instalments until August.

Capital & Regional Plc (JSE: CRP) will issue shares equivalent to 2.6% of share capital under the scrip dividend.

Altvest has garnered a lot of attention in a short space of time. This financial services group is building in public, which is a very difficult thing to do as start-up losses are scrutinised by the market and pivots are a matter of public discussion rather than private decisions in a boardroom.

With a controversial approach at times to its public persona, much of the Altvest story has been lost in the noise.

Warren Wheatley approached me for a fireside chat to dig into the vision at Altvest and to address some of the historical matters on social media.

This is a raw, unedited discussion that lasted just over an hour. If you want to understand a lot more about the Altvest business and the challenges of building in public, then this is for you.

Note:

An appearance on the Ghost Stories podcast is never an endorsement by me of a company’s investment case, business model or share price. Always do your own research and arrive at your own decision. At the time of the release of this podcast, I do not currently own shares in Altvest or any related entity.

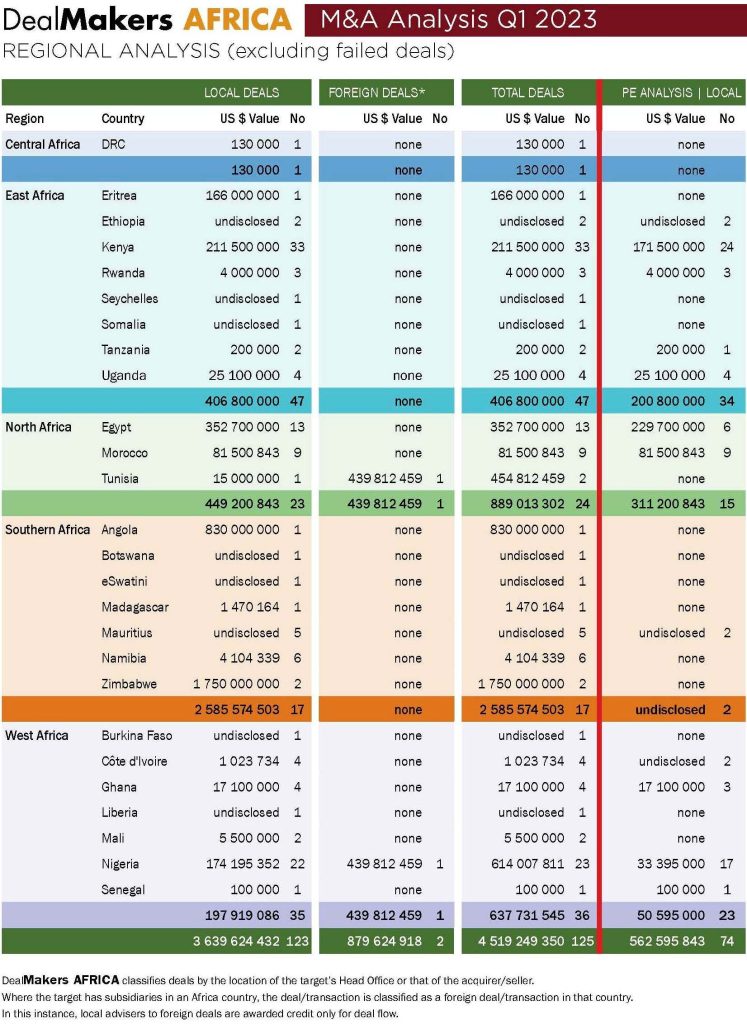

The total value of deals captured (excluding South Africa) for Q1 2023 was US$3,63 billion, almost a third of the value of that reported for the same period in 2022. Of the 123 deals captured, 38% of activity was recorded in East Africa – specifically, in Kenya – followed by West Africa, led by Nigeria with 28% of the Q1 M&A activity.

The increasing importance of private equity (PE) investment on the continent has been highlighted for some time, and the decrease in M&A activity for the first quarter of 2023 is directly aligned with the fall off in PE investment for the period. There were 74 PE deals captured for Q1 2023, with a reportable value of $562,6 million (reportable because the value of many of these deals is undisclosed), constituting 60% of all M&A activity for the quarter. This is compared with $1,34 billion (139 deals) over the same period, a year ago. According to Africa: The Big Deal, the amount raised by start-ups in the first four months of 2023 is less than half of what it was at the same time back in 2022, with healthcare being the only sector recording positive year-on-year growth, contrasting with the steep decline almost everywhere else. If the continent’s economies are to return to the unprecedented growth seen in the two decades leading up to COVID, then focus should be on ensuring that start-ups have the support and conditions needed to help fuel the next wave of growth. Africa, with 60% of its population under the age of 25, is ripe to embrace new technologies, particularly if they address the socio-economic problems faced.

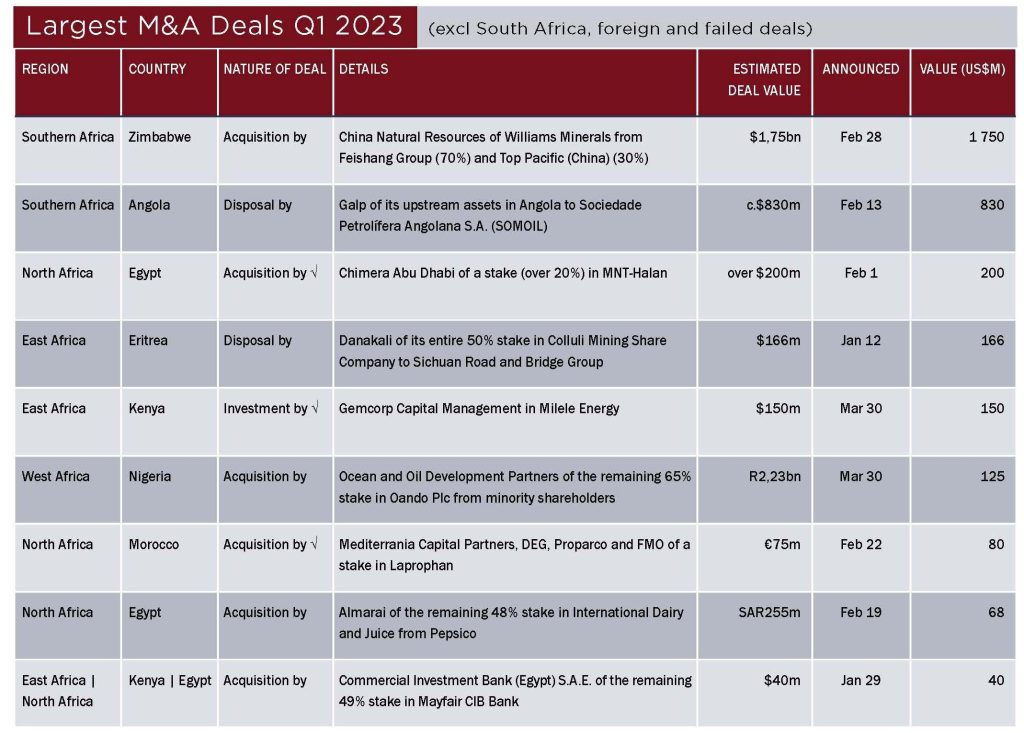

The largest deal by value was the acquisition by China Natural Resources (CNR) of the Williams Minerals lithium mine in Zimbabwe for US$1,75 billion from Chinese investment company Feishang Group and Top Pacific (China). The deal is a strategic move by CNR to meet the rising demand for a safe and reliable resource of lithium in a global market where the appetite for renewable energy continues to grow. Unsurprisingly, with the world focused on goals to reduce carbon emissions toward a clean energy future, five of the top six deals by value for the quarter fall into the Energy/Resources sector.

Life Healthcare is to acquire the renal dialysis clinics in southern Africa belonging to German dialysis specialist Fresenius Medical Care. The 51 clinics located in Namibia, Eswatini and South Africa will become part of Life Healthcare’s renal care programme.

With the liquidation of Conduit Capital’s largest insurance business, Constantia Insurance Company, the Group does not have the scale and capital to grow its remaining insurance businesses. For this reason, Conduit Capital is to dispose of Constantia Risk and Insurance to TMM for an aggregate cash price of R55 million. Part of the disposal payment will be kept in escrow to cover sales claims against Constantia Life should they arise.

The offer by Community Holdings to Jasco Electronics’ minority shareholders has been accepted in respect of 70,097,576 Jasco shares representing 19.08% of the total shares in issue, increasing the equity stake to 74.42%. The shares were acquired for a consideration of 16 cents per Jasco ordinary share, representing a 4% premium on the 30-day weighted average traded price of Jasco shares on 2 December 2022, the trading day preceding announcement. The delisting of Jasco was terminated this week on 23 May 2023.

Nampak has disposed of the property in Dar es Salaam which housed its Tanzanian manufacturing business prior to being wound down and closed. The property was sold to Canda (T) Investment Company for US$5,55 million.

Unlisted Companies

Edtech startup Play Sense, has secured an undisclosed funding from Grindstone Ventures. The preschool offers play-based learning through its micro-schools online platform. The funds will be used to enhance its franchise model and accelerate growth.

TSX-listed Dye & Durham, one of the world’s largest providers of cloud-based legal practice management software, has acquired Cape Town-headquartered GhostPractice in a deal in which the financial terms were undisclosed. GhostPractice is the largest provider of legal practice management software in South Africa and also serves law firms in Canada.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

| Lewis Group | Trematon)")

")

")

")