Within the banking sector, organisational resilience is becoming increasingly critical in South Africa, as highlighted in the SARB’s Annual Report.

The concept of organisational resilience encompasses a bank’s ability to withstand and adapt to internal and external disruptions while maintaining essential functions and safeguarding its reputation and long-term sustainability.

Moreover, the resilience of banks in South Africa is also being tested by regulatory changes, technological advancements, and shifts in consumer expectations towards ethical and transparent banking practices. As such, integrating organisational resilience into risk management frameworks becomes crucial for maintaining stability and competitiveness in the market. Banks that effectively navigate these challenges are better positioned to attract responsible investors, meet regulatory requirements, and build long-term value for shareholders and society.

These key trends align with the recently released report of the South African Reserve Bank (SARB) which highlighted focus areas for the coming year. As in previous years, the report issued by the Prudential Authority, the supervisory division of SARB, offers critical insights into the regulatory landscape.

It is crucial to dissect and understand this particular focus area, not only from the regulator’s perspective but also through the lens of our clients’ experiences.

From our interactions with clients, it is evident that many banks have been “thrown into the deep end” when dealing with sudden changes. These institutions often require substantial support to navigate these turbulent waters. The SARB’s feedback serves as both a warning and a guide, urging banks to adhere and to be ready for regulatory changes, to prioritise resilience and be prepared.

Our viewpoint aligns with this stance. We have observed that larger banks tend to have more sophisticated resilience mechanisms, while small to medium-sized banks often struggle with resource constraints. It is imperative for these smaller institutions to leverage technology and strategic partnerships to build their resilience. The role of foreign banks also cannot be ignored, although more reliance is placed at a group level, as they bring diverse perspectives and practices that can enhance local resilience strategies.

Our Banking team has been actively working with clients to navigate these complexities. We have found that banks that are forward looking proactively adopt organisational resilience practices often see long-term benefits, including improved risk management strategies, adherence to regulatory policies and procedures and enhanced reputation. However, the journey towards resilience is fraught with challenges, including the need for accurate, relevant and quality data, robust risk assessment models, and clear reporting standards.

While larger banks have well defined oversight structures, covering certain aspects of risk within the organisation, the challenge however remains to enhance organisational reliance by adequately mapping the interconnectedness and interdependencies with third party service providers. It is imperative that banks partner with service providers that have the capabilities and resources to assist with gathering quality and relative data used to inform principles, policies and procedures around organisational resilience.

Vulnerability of mutual banks

The Report highlights several critical concerns regarding mutual banks. It notes that many of these institutions fail to address organisational resilience in a comprehensive manner, leaving them vulnerable in various aspects of their operations. A significant issue identified is the inadequate management of third parties and supply chain risks. The resilience capabilities of these external partners are often not sufficiently integrated into their contractual agreements, leading to potential vulnerabilities.

Additionally, the report points out that mutual banks are lacking in their coverage of concentration risk, which could expose them to significant financial instability if not properly managed.

Market insight emphasised the need for continuous support and guidance. They noted that while the SARB’s report provides strategic direction, banks often require more detailed, practical advice to implement these strategies effectively. This underscores the importance of collaboration between regulators, banks, and advisory firms like ourselves.

As we move forward, commitment should be to helping banks interpret and implement the SARB’s recommendations.

The SARB’s 2023/24 report on organisational resilience provides a roadmap for banks to navigate the evolving regulatory landscape. By integrating resilience into their core operations, banks can better manage risks and contribute to a more resilient future. We are not only here to support our clients but we also challenge them every step of the way, helping them turn regulatory challenges into opportunities for growth and improvement.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Harmony Gold had a great year – but watch that guidance (JSE: HAR)

The next financial year may not be as delightful as this one

Harmony Gold has released results for the year to June 2024. It was a goodie, thanks to a higher gold price and a rough period for the company from which to recover. HEPS increased by 132% to R18.52, which means the share price is currently trading on a Price/Earnings multiple of 8.6x.

This period also saw record operating free cash flow of R12.7 billion, up by 111%. By all accounts, it was a strong year for Harmony and they took advantage of the gold price.

The concern (and perhaps the reason for a 3.5% drop in the share price) is actually around the guidance, with an expectation for FY25 of production of between 1,400,000 ounces and 1,500,000 ounces. They produced 1,561,815 ounces in FY24, so that’s an expected decrease. Then we get to All-In Sustaining Costs (AISC) of between R1,020,000/kg and R1,100,000/kg, which is well above R901,550 for this period. The drop in production would be a factor here in terms of efficiencies.

The group highlights that the FY24 performance benefitted from performance at certain mines that was well ahead of expectations in terms of recovered grades. This is the reason for what seems like conservative guidance. Either way, share prices are forward looking and the market didn’t love this guidance.

Metair’s balance sheet still needs loads of work (JSE: MTA)

I’m not convinced by the share price rally over the past three months

Metair is an incredibly unlucky company. Over the past couple of years, this group really has been through the most in both South Africa and Turkey. The market has jumped in recently, with the share price up by 38% in the past 90 days (but still down roughly 15% for the year). Based on the latest operational update, I’m not sure the GNU-phoria upswing is warranted for Metair.

For example, one of Metair’s key businesses is to supply the South African OEM vehicle production sector. Volumes for the first half of the year fell by 8%, with an expectation for volumes to only normalise in the final quarter of the year. That would be less of a big deal if Metair had a strong balance sheet, but alas the situation on the ground couldn’t be further from that. At the moment, Metair is focusing on bank covenants and a debt restructure plan, so there’s no room for error.

At least in the energy storage vertical, volumes in both Turkey and Romania improved considerably. The South African battery business experienced a dip in volumes, in line with the other businesses in the automotive components vertical.

Yes, there are green shoots, but goodness knows they need them. They need to refinance the South African balance sheet and “ensure a sustainable capital structure” – a process that is rarely painless for shareholders. The debt restructure programme is anticipated to launch in the fourth quarter and progress has already been made with raising bridging loans.

And if that isn’t enough of an overhang for you, Metair is also dealing with the European Commission and concerns around potential anti-trust violations by the Romanian business between 2004 and 2017.

Detailed results are due on 26 September, which will of course include an updated balance sheet and information on what earnings looked like for this period. That could lead to share price volatility, as there really is so much uncertainty here.

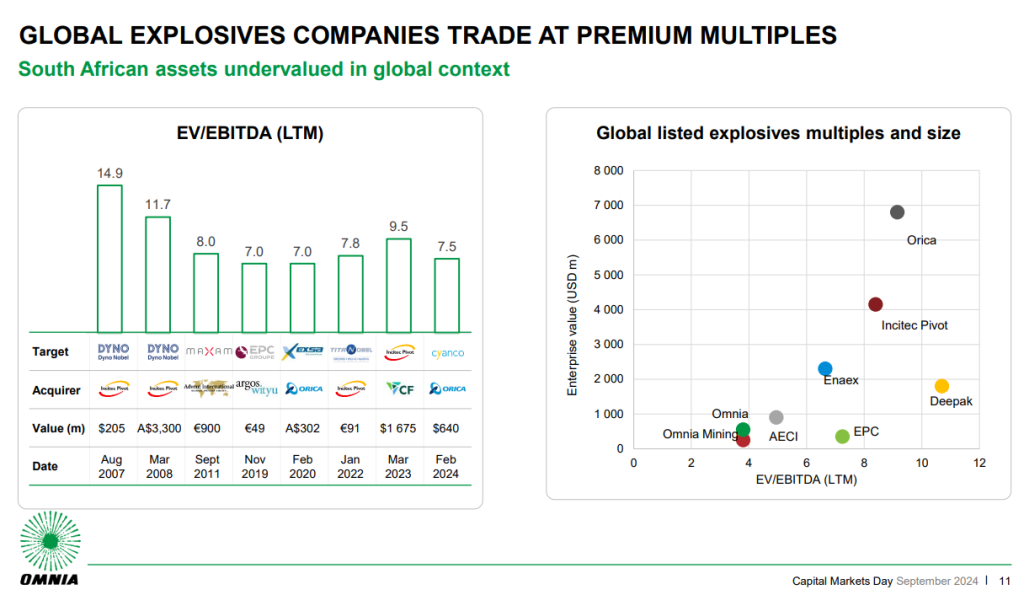

Omnia’s capital markets day shows the focus on the mining sector (JSE: OMN)

The contribution to group profits from this sector has increased drastically

A capital markets day is a great opportunity to learn about a listed company, especially when the full presentation has been made available -as is the case at Omnia. You’ll find it here.

It obviously goes into loads of detail about the broader group, with a key takeout being that the investment in the mining segment has been a huge focus area. The contribution to group earnings before interest and taxes (EBIT) from that segment increased from 30% to over 50% between FY18 and FY24.

As interesting as that is, I see we’ve now reached the point where local companies are again feeling brave enough to make reference to the traded multiples of global peers. There are many good reasons, theoretical and otherwise, why South African companies trade at a discount to global peers. And yet, here’s the slide:

It is completely correct by the way that the chart on the right shows that larger companies also trade at larger multiples. A size discount is a real thing, as smaller players are seen as risker and less resilient – and therefore less valuable per unit of profit generated. Omnia cannot make the argument that they should be trading at the same multiple as much larger global companies.

Still, the wind is clearly in the sails of South African management teams once more. That’s a good thing!

Solid double-digit growth at OUTsurance (JSE: OUT)

And the local businesses are where you’ll find the magic

OUTsurance Group is one of those companies that doesn’t seem to get much attention. I don’t think I’ve ever seen it mentioned as a stock pick, yet this is a R76 billion company that has delivered a 16% share price return this year. Not bad at all.

An interesting element of the group is that OUTsurance Group holds 90.5% in OUTsurance Holdings, with regular transactions to flip those minority shareholders up to the group company. It’s probably not a bad thing to have this structure though, as it incentivises those minority shareholders in the right place.

The local performance looks strong, assisted by a favourable claims experience in South Africa and macroeconomic elements like higher interest rates that boosted investment income. OUTsurance SA grew earnings by between 12% and 22%, coming in at nearly R1.9 billion. OUTsurance Life jumped by a lovely 38% to 58%, admittedly off a small base. That business generated R142 million in earnings.

Looking abroad, Youi Group (the Australian business) grew by between 8% and 18%, contributing R1.4 billion in earnings. This is a rare example of success in that market for a South African corporate, with the difference being that OUTsurance grew Youi Group organically from the ground up. This is a vastly better (but slower) approach than buying an existing business in that market and hoping for the best.

OUTsurance is doing it again, this time in Ireland. They are incurring startup losses at the moment, with a loss of R56 million for the period. A successful group like OUTsurance can easily incubate initiatives like these. Again, I far prefer seeing startup losses vs. large, risky transactions.

At overall group level, normalised earnings per share grew by between 15% and 25%. HEPS was up between 14% and 24%, so no concerns there in terms of the extent of normalisation adjustments. Detailed results are due on 17 September.

Pan African Resources has enjoyed the gold price (JSE: PAN)

This mining group has taken advantage of better commodity prices

If there’s one thing we’ve certainly learnt this year, it’s that gold miners don’t always do well when the gold price is up. Sadly, they inevitably all do badly when the price is down. This return profile is why some investors prefer buying the yellow stuff itself vs. the underlying miners.

Thankfully, with a year-to-date share price performance of around 68%, Pan African Resources sits on the right side of that analysis. HEPS will be up by between 27% and 37%, measured in dollars as the group’s presentation currency.

This was driven by a 16.8% increase in revenue, with volumes of gold sold up by 4.9% and the gold price up by 11.3%.

Sanlam signs off on an excellent interim period (JSE: SLM)

HEPS growth of 40% will do nicely

Sanlam has released results for the six months to June. The numbers look really strong, with the net result from financial services (the key measure) up by 14%. This is the best way to gauge performance at Sanlam, as it talks to the underlying businesses like insurance, investment management and structuring. There are a lot of encouraging signs in the numbers, like impressive new business volumes in life insurance and a significant jump in net client cash flows.

The next important measure on the income statement is net operational earnings, with the major difference being the inclusion of investment returns on shareholder capital. This is largely outside of the control of management, as this is where the macro factors like interest rates and equity markets start to affect the returns for financial services groups. The growth rate of 8% in net operational earnings reflects the lower (but still positive) investment returns this year vs. last year.

There are a lot of other complexities in the numbers, including the elements that are captured between net operational earnings and headline earnings. Thanks to higher underlying earnings and fewer shares in issue, HEPS increased by 40%.

Initially, the next bit of disclosure caught me out until I was kindly corrected on X, which is by far the best finance audience you’ll find online. Sanlam disclosed that the return on group equity value per share came in at 9.3%, or 10.7% on an adjusted basis. Their hurdle rate is disclosed as 7.5%, which seemed oddly low to me. I therefore expected to see the current share price of R85.44 representing a discount to the gross equity value per share of R73.41, but instead it trades at a premium. That’s when I should’ve clicked that the return hasn’t been annualised and neither has the hurdle rate, which is highly unusual.

If we just double them for simplicity, the hurdle rate is 15% (which makes far more sense) and Sanlam is achieving a return on group equity value per share that beats most of the banking groups. That’s a lot more believable.

Still, I’m always nervous of buying a financial services group at a premium to equity value. Sanlam is a great business for sure, but the market already knows that.

Little Bites:

Director dealings:

A director of a subsidiary of KAP (JSE: KAP) – PG Bison, for what it’s worth – sold shares worth R708k.

Something seems to be on the boil at Transaction Capital (JSE: TCP), with a cautionary announcement noting that the group has entered into a “series of negotiations” – with no further details given at this time. It’s surely more likely to be a disposal than an acquisition, but time will tell.

Metrofile (JSE: MFL) announced that Pfungwa Serima, the group CEO, will be stepping down with effect from 30 September 2024. He has been in the role since February 2016. Thabo Seopa, currently an independent non-executive director, will take over in the CEO role. It’s extremely unusual to see a non-executive taking the top job. Seopa does have loads of relevant experience though, so hopefully he will inject some more life into the digitalisation and evolution of the business.

Gemfields (JSE: GML) usually makes quite a song and dance of auction results, but the latest auction seems to have been a less important one as it focused on by-products of the mining process in the ruby business. Auction revenue came in at $2.3 million vs. $1.5 million for the comparable auction in the prior year. All the carets were sold, consisting of sapphire, corundum and a small amount of ruby.

Trustco (JSE: TTO) has issued shares to a public shareholder at 36 cents per share. The total raised was nearly R1.8 million, so it’s a modest issuance. The current share price is 40 cents.

In May 2022 Sanlam and Allianz announced a joint venture (SanlamAllianz) to house the merger of their African operations – Sanlam’s South African and Namibian subsidiaries were excluded. Sanlam and Allianz agreed on an initial shareholding split of 60:40, subject to post-closing adjustments and the inclusion of the Namibian operations. Sanlam has now integrated its Namibian business into SanlamAllianz, as reported in its interim results released this week, at an initial valuation of R6,2 billion. To maintain the split following the incorporation of the Namibian operations, for which it will receive a cash consideration of R2,5 billion, Sanlam will subscribe for additional shares in the joint venture. Allianz retains the option to raise its stake in SanlamAllianz to 49% within six months of the completion of the Namibian transaction.

In another corporate action Sanlam subsidiary Sanlam Life will acquire a 25% interest in African Rainbow Capital Financial Services (ARC FSH) for a cash consideration of R2,41 billion. The deal with ARC FSH, the investment holding company for all the financial services investments of the Ubuntu-Botho Investments Group and Sanlam’s strategic empowerment partner, will see Sanlam Life dispose of its 25% interest in ARC Financial Services Investments in exchange for the issue by ARC FSH of shares to the value of R1,49 billion. Sanlam will subscribe for further ARC FSH shares valued at R92 million in cash making up the 25% stake. Sanlam will pay African Rainbow Capital an outperformance fee based on the extent to which the value of ARC FSH’s investment in Tyme Investments Pte (Asia), as at 30 June 2028, exceeds an annual hurdle rate of 14.64%. This is capped at R70 million.

Pepkor has entered into an agreement with Shoprite to acquire Shoprite’s furniture business operating more than 400 stores in South Africa, Botswana, Lesotho, Namibia, Eswatini and Zambia. The stores will be combined with Pepkor Lifestyle (previously JD Group) which operates 900 stores in the same countries (except Zambia). The proposed transaction includes the Shoprite Furniture credit loan book and related insurance cell captive agreements as well as the OK Furniture and House & Home retail brands. The deal will enable key synergies and efficiencies to be unlocked within the supply chain, logistics and financial services operations. The purchase consideration which will be determined at the close date of the transaction represents c. 4% (c.R3 billion) of Pepkor’s market capitalisation and will be settled in cash.

Earlier in March this year, Takealot, Naspers’ e-commerce business in South Africa, announced it was looking to offload its fashion retailer Superbalist amid growing concerns of increased competition from Shein and Temu. This week Takealot sold the business to a consortium of retail and private equity investors led by Blank Canvas Capital for an undisclosed sum. The deal will support Suberbalist’s ongoing growth while allowing the group to focus efforts on expanding Takealot and Mr D. Takealot will however, continue to provide warehousing and logistics services to Superbalist through a multi-year service agreement.

Burstone has entered a strategic partnership in Europe with Blackstone, an American alternative investment management company which will see a scaling of the group’s international fund and investment management strategy. Blackstone will acquire, at a 3.1% discount to gross asset value (11.7% discount to NAV), an 80% stake in Burstone’s pan-European Logistics platform for a €1,02 billion (R20 billion) purchase consideration. Burstone will reduce its stake by 63% (valued at €644m/R12,69 billion), retaining a 20% stake and will continue to manage the portfolio. The balance of 17% will be acquired from unrelated parties. Together the groups will expand the portfolio, targeting industrial and logistics properties across Europe. In addition, Burstone’s Australian Irongate joint venture has announced a new industrial joint venture in Queensland with a global alternative asset management firm (the name of which was not disclosed) backed by an initial A$200 million (R2,4 billion) equity commitment. Burstone is also currently negotiating to acquire a 25% co-investment stake in a €170 million (R3,4 billion) German light industrial platform. Post the successful implementation of these transactions, Burstone’s assets under management are expected to increase 32% and its loan-to-value ratio decrease 12.5% to 33.5%. Burstone will also increase its dividend payout ratio from 75% to between 85% and 90%.

The SPAR will exit the loss-making Polish business, the assets of which include 200 retail stores, three distribution centres and one production facility. The exit will be at great expense to the company, which will recapitalise operations at a cost of R2,7billion (c.12% of Spar’s current market capitalisation), the majority of which will be for the settling of funding debt. The buyer, Specjal, a Polish retailer is, according to the company statement, better placed to turn the business around and will pay Spar R185 million for the assets.

Nampak has disposed of the businesses of manufacturing, selling and supplying of plastic drums and of HDPE and PET bottles and jars. The disposal of the Drums Business and Liquid Business is in line with the implementation of Nampak’s asset disposal plan announced in August 2023. Financial details of the transactions were not disclosed.

Trustco has issued 4,936,193 shares to an unnamed public shareholder at 36 cents per share – representing the 30-day VWAP of 6 August 2024. The shares, valued at R1,78 million, were issued under the general authority granted to the company by shareholders at the 2023 Annual General Meeting. Following the listing of the new shares Trustco has 992,174,774 shares in issue.

The week was all about the repurchase of shares:

During the period January to end-June 2024, Shoprite has repurchased 215,172 shares at an average price of R229.23 per share for an aggregate R49,5 million. Since the inception of the Group’s share buy-back programme in 2021, a total of 8,6 million shares have been repurchased to the value of R1,6 billion.

In line with its share buyback programme announced in March, British American Tobacco this week repurchased a further 433,413 shares at an average price of £28.48 per share for an aggregate £12,34 million.

In terms of its US$5 million general share repurchase programme announced in March 2024, Tharisa has repurchased a further 10,000 ordinary shares on the JSE at an average price of R19.41 per share and 136,570 ordinary shares on the LSE at an average price of 80.78 pence. The shares were repurchased during the period 26 – 30 August 2024.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 26 – 30 August 2024, a further 2,246,844 Prosus shares were repurchased for an aggregate €74,56 million and a further 188,720 Naspers shares for a total consideration of R687,18 million.

Two companies issued profit warnings this week: Truworths International and Sibanye Stillwater.

During the week, five companies issued cautionary notices: Finbond, Burstone, The Spar, Conduit Capital and Transaction Capital.

South Africa is often referred to as the business gateway to the African continent due to its strategic location, advanced infrastructure, diverse economy, regulatory environment and skilled workforce. Parties looking to set up an investment structure in South Africa to tap into this market generally have a choice between: (i) incorporating a limited liability private company; or (ii) setting up a partnership, with the latter rising in prominence over the past decade.

The two main categories of partnerships are general (en nom collectif) and extraordinary partnerships. Extraordinary partnerships can further be divided into anonymous and en commandite partnerships (ECPs), with both sub-categories possessing unique characteristics, and catering to different business needs and strategic goals. This article will focus on the role ECPs can play in unlocking capital in South Africa for deployment into Africa.

En Commandite Partnerships

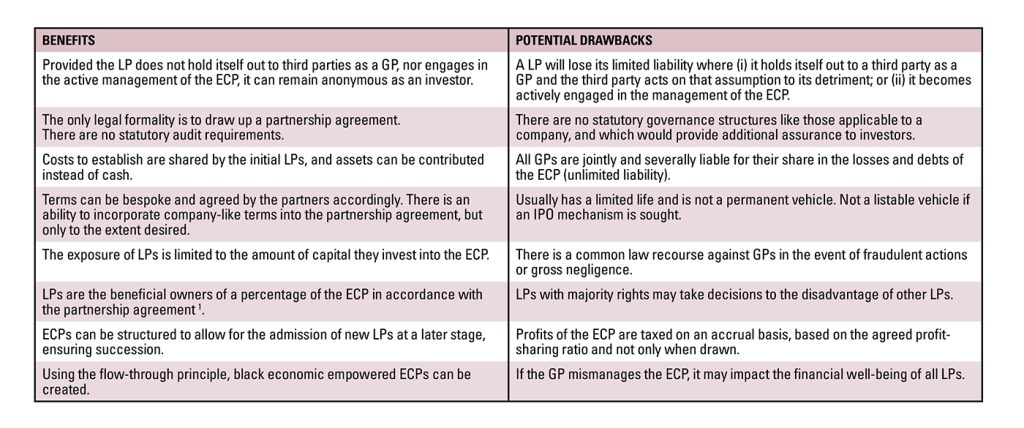

ECPs are carried on by two or more partners, comprising (i) a general or managing partner (GP) which is the named partner, responsible for the management of the partnership; and (ii) one or more limited partners (also known as commanditarian or en commandite partners), whose name(s) is/are not disclosed (LPs). LPs are, generally, silent partners who contribute a fixed sum of money to the partnership, on condition that they receive a share of the profit (to the extent that there is a profit); but in the event of loss, they are liable to their co-partners only to the extent of the fixed amount of their agreed capital contribution.

ECPs are widely used in South Africa, due to their unique ability to combine the expertise and management skill of GPs with the capital and limited liability of LPs. Entrepreneurs can utilise ECPs to attract passive investors looking to generate returns without being actively involved in the management of the business, and who wish to remain anonymous. In return for their investment, the passive investors can leverage off the expertise of the general or managing partner to help generate economic returns.

Considerations before creating an ECP

While offering numerous benefits, ECPs also pose some potential drawbacks. Understanding these differentiators is crucial for investors when deciding on the appropriate structure to pursue. The table below highlights some of the benefits and potential drawbacks associated with ECPs.

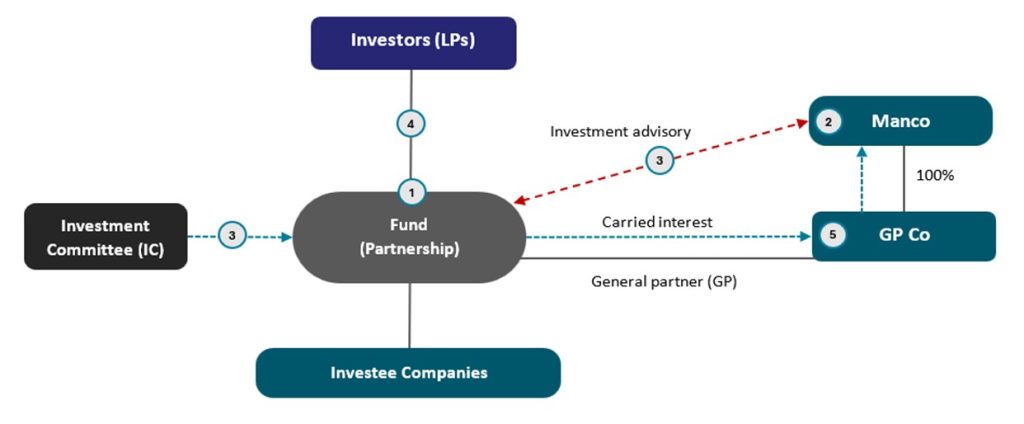

Typical example of an ECP structure used for an investment fund

Each of the individual parties outlined in the diagram below play an integral part in the successful implementation of an ECP structure for a fund:

1.Fund set up as a limited liability partnership (ECP), but can also be set up as a trust. 2.GP Co sets up the fund (with GP Co having potential empowerment credentials if required to benefit using flow-through principle). 3.Manco appointed by the GP Co as the investment adviser to the Fund. LP appoints an investment committee (IC) to approve investment decisions. 4.Investors are LPs to the Fund. Investors contribute capital or assets to the Fund. 5.GP Co is the GP, and the vehicle earns the carried interest (which is essentially the profit share for the GP’s performance). The carried interest is then distributed to Manco, to the extent that Manco is a shareholder in GP Co.

ECPs play a key role in corporate finance by providing a flexible structure for capital raising, profit-sharing and risk management, with a reduced administrative burden. In practice, it has been seen that some investors have recently favoured the conversion of partnerships into permanent capital vehicles (PCVs), allowing an unlimited time horizon for investment and realisation without pressure to realise assets within a certain period.

In the current landscape, LPs continue to benefit from tax efficiency, risk mitigation, and access to specialised expertise. This makes ECPs a valuable tool for businesses seeking capital for strategic initiatives and growth.

By leveraging the advantages of ECPs effectively, businesses can navigate the complexities and demands of the modern business environment while generating value for various stakeholders.

A trusted advisor with relevant practical experience is a crucial link in helping entrepreneurs and investors navigate the permutations of an ECP structure to ultimately maximise utility for all parties involved.

1 Comprehensive Guide To Dividends Tax (Issue 4), p 50, SARS.

James Moody and Mikayla Barker are Corporate Financiers | PSG Capital

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

“The 2030 Agenda for Sustainable Development1, adopted by all United Nations (UN) Member States in 2015, provides a shared blueprint for peace and prosperity for people and the planet, now and into the future. At its heart are the 17 Sustainable Development Goals (SDGs), which are an urgent call for action by all countries – developed and developing – in a global partnership. They recognise that ending poverty and other deprivations must go hand-in-hand with strategies that improve health and education, reduce inequality, and spur economic growth – all while tackling climate change and working to preserve our oceans and forests.”

This is the opening paragraph about SDGs on the UN’s website. What captures one here is the fact that social welfare and looking after the environment can go hand in hand with economic growth, which is exactly why SDG funding might be the next frontier for merger and acquisition (M&A) financing in South Africa.

Let us look at some of the benefits of Sustainable Development Funding:

Low interest rates Similar to an impact fund, a sustainable development fund’s mandate is to leave the world a better place; therefore, the interest asked on the capital deployed is very competitive – more than that of traditional banks and PE firms. Interest can be between five to 10 percent, with appetising incentives, such as the reduction of the interest when certain sustainable development goals are met.

Longer payment holidays In the pursuit of reducing carbon emissions, projects usually targeted by sustainable development funds are often green energy projects. Most green energy projects are normally greenfield projects and, therefore, capital raised for these projects may enjoy longer payment holiday periods. The holiday ranges from 24 months to 60 months, depending on the project. This will assist the entity to invest their earnings back into the project, to improve the chances of success.

Incentives for repaying the funds quickly Because sustainable development funds need to support as many projects as possible, recycling money as quickly as possible is imperative, which is why they offer an incentive to projects that can return the capital raised in a shorter period than agreed. Such incentives include reducing or removing the interest from the capital asked.

This type of funding removes the traditional capital raising barriers that banks and PE firms struggle with. With the Government of National Unity (GNU) now in place, it will be interesting to see how the Democratic Alliance (DA) will use this position to promote sustainable development goals without rattling the African National Congress (ANC)’s cage on redress policies such as Broad-Based Black Economic Empowerment (B-BBEE) and Affirmative Action. The DA has always hailed the narrative that sustainable development goals should replace redress policies, so perhaps the marriage between the two parties can produce a merged initiative to promote sustainable development goals and broad-based black economic empowerment alike.

Sustainable development funding can revolutionise the mergers and acquisitions landscape by aligning financial returns with positive social and environmental impacts. Integrating SDG funding into M&A strategies in South Africa can attract international investors seeking ethical investments, enhance corporate reputation, and foster long-term sustainability. Embracing SDG principles can drive innovation, create jobs, and build resilient communities, ultimately contributing to a more inclusive and prosperous economy.

1 https://sdgs.un.org/2030agenda

Thulisile Buthelezi serves as Secretary of the Policy & Research Committee and Provincial Chairperson (KZN) and Ayavuya Madolo is the National Deputy Chair | BMF Young Professionals.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

The worst should now be over at Cashbuild – I think (JSE: CSB)

I’m keeping my long position in the hope that interest rate cuts will be a further boost

After the market recently dished out an absolute gift in the form of a sell-off in Cashbuild down to R142 per share, it has recovered to trade at R160 per share. I bought that dip and I’m obviously thrilled with how it turned out, with the decision now being whether to hold on for more. I think that an easing of local interest rates will do wonders for Cashbuild’s business, with the numbers for the year ended June hopefully reflecting the end of the bad times for the group.

It was another tough period, with HEPS down 22% despite revenue growing by 5%. The final dividend fell by 29%, so that’s a nasty year-on-year trend.

Importantly, this is a 53-week result compared to a 52-week period. If the extra week is stripped out, revenue was up just 3% and HEPS fell by 38%. That’s the best way to look at this result.

Although sales volumes were up 3%, with a small boost from inflation to take like-for-like sales growth to 4%, this is again on a 53-week basis. With that stripped out, volumes would likely be slightly positive. My thesis is that lower inflation and hopefully a drop in rates will improve sales volumes.

Gross profit margin is a concern, having dropped from 25.4% to 24.7%. That trend needs to improve, obviously. The drop in margin is why operating profit fell by 16% (excluding impairments) despite operating expenses only increasing by 4%.

This is an important lesson in comparing the growth in operating expenses to the growth in revenue. The growth rates might look similar, but major changes in gross profit margin will have a big impact on operating profit.

Looking at the balance sheet, the 37% decrease in cash and cash equivalents is largely due to a cut-off issue, with June supplier payments reflecting in this period vs. the comparable period when the suppliers were paid after year-end. In retailers, cut-off is an important point that makes working capital ratios difficult to work with.

The group helpfully highlights that stock levels increased by 5%, which seems reasonable relative to revenue.

For the first six weeks of the new financial year, sales revenue is up by 5%. Although that may sound like there’s no real improvement vs. the full year, you have to remember that the 5% growth in FY24 included an extra week of trading. I’m therefore not unhappy with the recent growth rate, although it obviously needs to move higher for this investment to work out well.

Management’s narrative is one of caution, with an expectation for trading conditions to remain challenging.

SPAR finds a buyer for SPAR Poland – but it comes at a cost (JSE: SPP)

Add this one to the list of failed international moves by local retailers

When it comes to SPAR Poland, I guess it’s fair to say that they got unlucky with COVID. Although I don’t think many people would gush over the previous SPAR management team, it’s also true that a risky international deal becomes an impossible task when an unforeseeable pandemic arrives.

Thankfully, this nightmare is always over, thanks to the incredibly named Przedsiebiorstwo Produkcyjno Handlowo Uslugowe Specja Spólka z o.o. coming in as the acquirer of SPAR Poland. If it’s ok with you, I’ll just refer to that company as the buyer.

The buyer is Polish (in case that wasn’t super obvious) and has been in operation since 1990. They will need all that experience, since SPAR Poland lost R813 million in the six months to March and has a negative net asset value.

At first blush, it looks incredible that Spar managed to secure a wonderful price of R185 million for the business, though it does have the potential to be adjusted downwards if more partner stores leave the network. Then, as you read further, you get to the bad news: Spar first needs to recapitalise the company to bring the net asset value to zero, plus they must contribute well over R1 billion to cover expected operating losses.

In other words, they aren’t just giving it away – they are actually paying someone to take it! Incredible. The maximum exposure for SPAR is nearly R3.5 billion. The final amount will vary obviously depending on all sorts of things, with the plan being to bring nearly R2.0 billion of Polish debt back to South Africa and refinance it here (!) and for R566 million to be funded from existing sources into the Polish business.

Unsurprisingly, the share price took a knock of 6.8% on the day.

What. A. Disaster.

A step forward for Telkom’s disposal of Swiftnet (JSE: TKG)

The Competition Tribunal has given the green light

In corporate dealmaking, a deal is never done until the money changes hands. When conditions precedent are still outstanding, anything is still possible – especially when it comes to regulators, who can be unpredictable.

There would therefore have been a collective sigh of relief at the news that the Competition Tribunal has approved the disposal of Swiftnet. Telkom is selling the business to a consortium of an Actis infrastructure fund and Royal Bafokeng Holdings.

Although there are further remaining conditions, this is a big milestone for the deal.

The Foschini Group is fully focused on margins (JSE: TFG)

When capital is expensive, retailers tend to avoid chasing market share at all costs

The Foschini Group has released a trading update dealing with the 21 weeks to 24 August. When the highlights section talks about gross margin as the first few points and completely ignores sales growth, you know what’s coming.

Group sales fell by 3.5%, with TFG London as the major laggard with a 12.7% decline. TFG Australia fell 5.5% and TFG Africa was down 1%. Those percentages are based on the offshore businesses measured in rands. Bash was the sales highlight, with turnover up 42.7%.

That sounds poor of course, with the saving grace being that group gross margin expanded by over 100 basis points, with a 200 basis points expansion in TFG Africa and record gross profit in that business, up 4% on the prior period. Despite the sales pressure in TFG London and TFG Australia, they even managed to grow gross margin there.

To further explain the trend, the announcement notes that the base period included a major inventory clearance initiative. That would’ve boosted sales and impacted gross margin, so that explains some of the move in this financial year on both those lines.

We will have to wait until 8 November to get the detailed interim results. Given the gross profit performance and some of the expense control we’ve seen at other retailers, it probably won’t be a shocker at profit level. Still, this isn’t what shareholders want to see, as lack of sales growth is always a worry.

Woolworths Food is carrying the team (JSE: WHL)

After much initial progress, the rest of the business has stalled

The Woolworths share price is down more than 15% this year, a particularly unfortunate performance compared to how “SA Inc.” has performed in the new political landscape. Sentiment is great and everything, but a company needs to deliver growth in order to see the share price go the right way. With HEPS from continuing operations on a 52-week basis down by 16.8% and the dividend down 15.2%, growth isn’t the theme here. The increase in net debt from R2.5 billion to R5.6 billion isn’t good news either.

Ironically, more positive sentiment towards South Africa over the past decade or so might have saved Woolworths a lot of heartache in Australia and New Zealand. Just when investors thought the worst was over with David Jones out of the system once and for all, things have gotten bad for Country Road Group. This is the business that Woolworths deliberately held onto in the region, yet sales have dropped 8% for the year on a comparable 52-week basis. In comparable stores, sales fell by 13.1%. They point to the high base to help explain this, but the two-year growth stack is disappointing anyway. And on top of this, gross margin deteriorated by 230 basis points to 60.3%. Despite best efforts to control expenses, operating profit margin collapsed from 12.4% to 4.6% and profits were down 66%. Ouch.

Focusing now on the local businesses, it was Woolworths Food that tried to save the day. When you’re looking at the 11.2% growth in sales for Woolworths Food, remember that this includes the 53rd week of trading as well as the acquisition of Absolute Pets in the second half. On a 52-week basis, sales grew 9% overall and 6.9% in comparable stores. Price inflation was 7.9%, suggesting that volumes remained a struggle for the full year. Woolworths goes on to confirm that the volumes trend turned positive in the second half, so that’s encouraging at least. Another encouraging element is that Woolworths Dash grew 71.2%, so they are clawing back some lost ground in on-demand shopping. Perhaps more importantly, gross margin increased by 30 basis points to 24.7%, which I think is impressive given how much more competitive they have needed to become on price. Operating profit margin increased from 6.9% to 7.1% and adjusted operating profit grew by 12.3%.

We now arrive at Fashion, Beauty and Home (FBH), the part of the business that showed great promise under new leadership. Things have gone wrong with that recovery, with sales down 0.4% for the 52 weeks and 1.3% on a comparable store basis. With price inflation of 8.9%, this means that volumes were firmly in the red. They managed to maintain gross margin at 48.5% at least. They also kept expense growth to just 2.6%, but the reality is that a business cannot succeed through efficiencies alone. The lack of top line performance meant a 9.9% drop in adjusted operating profit, with operating profit down from 13.2% to 12.0%.

It’s a bit sad when one of the major highlights is Woolworths Financial Services, where profit after tax jumped by 69.3%. Although the book was a bit smaller, there was an improvement in the impairment rate.

Unfortunately, the outlook section of the announcement doesn’t suggest that a quick recovery is around the corner. By afternoon trade, Woolworths was down 4.7%.

Little Bites:

Director dealings:

Michael Georgiou of Accelerate Property Fund (JSE: APF) sold shares worth nearly R81 million in an off-market trade that was part of a lending arrangement. I suspect that hurts.

Titan Premier Investments (of the Christo Wiese stable) has unwound its collateral arrangement on certain funding positions and now has 5.34% in Pepkor (JSE: PPH) once more.

The Ghost Wrap podcast is proudly brought to you by Forvis Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Forvis Mazars website for more information.

This episode covers:

CA Sales Holdings has a great business model that is still working beautifully.

RCL Foods and Rainbow Chicken have reported numbers together for the last time, which gives us an opportunity to reflect on exactly why the unbundling made sense.

Motus is struggling at the moment and the market doesn’t seem to be punishing the share price, presumably because of the expectation of interest rate cuts.

Bidvest reminds us of the value of diversification, with five out of seven divisions in the green and a reasonable overall result at group level.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

AfroCentric didn’t escape the red day on the JSE despite growing earnings (JSE: ACT)

Earnings may be up, but revenue growth is modest

AfroCentric has released its earnings for the year ended June 2024. Revenue only increased by 0.4%, with this mainly due to the discontinuation of the surgical business. Still, headline earnings increased by 54.1%, so there’s an unusually shaped income statement for you. On a HEPS basis, the increase of just 11%, as the number of shares in issue has increased substantially after the deal with Sanlam.

The synergies from the Sanlam deal will be felt mainly in the Corporate Solutions Cluster, where AfroCentric has made progress in selling into Sanlam channels. Lovely as that is, it’s still small in the group context. The biggest operation is the Services Cluster, where you’ll find the medical scheme administration businesses and a revenue growth rate of 6% in the past year. The Pharmaceutical Cluster is also important and is facing challenges in profitability, with operating profit growth of 7.3% but some major underperformers within the cluster that are stopping this from being better.

Hopefully, the synergies with Sanlam will start to pick up steam.

Ascendis is finally profitable – well, mostly (JSE: ASC)

With the delisting off the table for now, it’s unclear what the future will hold

Ascendis has been the topic of quite the regulatory tussle this year, with the Takeover Regulation Panel at the centre of the debate. The potential delisting seems to be dead for now, so there’s no offer left to fight over. Instead, investors have to focus on the underlying business and whether they want to own it.

Despite a decrease in revenue, Ascendis managed to swing from losses to an operating profit of R46.4 million. Although HEPS from total operations came in at 1.1 cents, HEPS from continuing operations was a loss of 1.4 cents (admittedly a much better situation than a loss of 41.5 cents in the comparable period).

The company is now switching to an investment holding company structure, with ACN Capital (the Carl Neethling entity) appointed as the investment manager. The tangible net asset value per share of 91 cents is likely to be the important metric going forward, with the share price currently at 71 cents.

Apart from some strong words aimed at the regulators and activist shareholders, the announcement also raises a concern around group cash flow. Although they have no external debt, the cash position of the group deteriorated during the year.

The market hated the Aspen numbers (JSE: APN)

Watching a >R100bn market cap company take a 13% bath is quite something

The year-to-date Aspen share price now looks like the elevation profile of someone jumping off the side of a mountain:

As they say, the bulls take the stairs up and the bears take the elevator down. That’s a huge one-day move of 13%, with this large cap being thrown around like a rag doll on the market.

The market didn’t care much about Aspen’s news of its highest-ever normalised EBITDA for H2 in the second half of the year. The market also didn’t focus on the cash conversion ratio of over 100%, or the news of manufacturing contracts exceeding guidance.

No, the market was only interested in normalised HEPS being flat for the year, with HEPS down 3% without those adjustments. Even the dividend increasing by 5% couldn’t save the story, as investors panicked about lack of growth in earnings.

Pressure on gross profit margin didn’t help, with revenue up by 10% and gross profit up by just 4%, impacted by sales mix with more focus on manufacturing revenue. This was enough to help Aspen tread water based on growth in expenses and a flat move in net financing costs, but the market wanted more than that.

Investors do seem to have glossed over the impact on margin of the Heparin inventory being cleared. They unlocked a lot of operating cash flow through this process (up 13%) and managed to do so without causing a negative year-on-year move in earnings. The manufacturing segment saw gross margin decrease from 11.4% to 9.2% and this will clearly be a focal point for the market going forward.

On normalised HEPS of 1,492.1 cents, the share price of R206 is a Price/Earnings multiple of 13.8x. It feels like this drop might have been overdone, so keep an eye on this for short-term long opportunities to play the closing of the gap.

Motus is a tale of thin margins and expensive debt costs (JSE: MTH)

The combination isn’t going well at the moment

Motus has released its financials for the year ended June 2024. With revenue up 7%, you would hope that the rest of the income statement looks decent. Alas, operating profit fell 4% and HEPS was down by a rather ugly 28%, leading to the dividend for the year dropping from 710 cents in 2023 to 520 cents in 2024.

The Retail and Rental division is over 80% of group revenue before eliminations and that business saw operating margin decline from 3.0% to 2.8%. A 20 basis points move on such tiny margins is material. Import and Distribution is the next largest division in terms of revenue and margins there fell from 5.8% to 4.0%. The 20 basis points improvement in Aftermarket Parts from 8.4% to 8.6% wasn’t enough to offset this.

Sadly, operating profit is only one part of the story in a business that runs with structurally high levels of debt. Finance costs jumped significantly from R1.4 billion to R2.3 billion, which is a very large number when operating profit was R5.5 billion. More importantly, operating profit dipped from R5.7 billion to R5.5 billion, so finance costs increased substantially at a time when operating profit fell.

The impact was most severe in Import and Distribution, which saw profit before tax plummet spectacularly from R1.14 billion to just R95 million.

Automotive groups are pretty desperate for interest rates to drop. Not only does it improve customer affordability and thus put less pressure on gross margins, but it helps reduce the costs of their own debt.

I genuinely don’t know how the share price has managed to behave like this despite the negative move in the cycle:

Pepkor: less building materials, more furniture (JSE: PPH)

The group clearly sees value in Shoprite’s furniture business

Pepkor has taken a couple of major steps in changing the shape of its group.

One of them we’ve known about for a while, which is the disposal of The Building Company to Capitalworks and the company’s management in a deal worth R1.2 billion. This is a classic management buyout structure in which a private equity player puts in the balance sheet for the deal.

The other is hot off the press, with further details below.

Before we get to the new deal, the news on the disposal of The Building Company is that the Competition Tribunal has approved the transaction, so the closing date is 30 September and Pepkor can get its hands on the money.

That’s just as well, because Pepkor is buying the furniture business out of Shoprite. As I cover further down in the Shoprite section, the business isn’t exactly a fast growing operation. With sales growth of 2.3%, Pepkor will need to really sweat this furniture asset to get real benefits for shareholders. The good news is that they are buying it for its net asset value, so Shoprite is happy to pass the baton to Pepkor without asking for any goodwill on top.

The deal will be settled in cash and represents around 4% of Pepkor’s market cap, so they aren’t exactly betting the farm. That’s just as well, because I don’t think this is the most lucrative deal around. Pepkor reckons that they can integrate the business with other Pepkor businesses focused on complementary categories.

With a 2.6% drop in the Pepkor share price, the market didn’t exactly pop the champagne at this news.

A strong top-line result at Shoprite didn’t quite convert this time (JSE: SHP)

And on a red day for the broad market, Shoprite’s share price was punished

A 5.9% decline in Shoprite’s share price is a big move, especially in one day. Although the JSE was down 1.6% for the day (and this is important context), it still tells us that the market didn’t love the results from Shoprite.

The problem wasn’t in sales growth, with group sales up by 12%. Supermarkets RSA grew 12.3%, Supermarkets non-RSA managed 6.1% and other operating segments grew by a significant 21.1%. Furniture could only achieve 2.3%, with more on that later.

We need to look deeper into Supermarkets RSA, with Checkers and Checkers Hyper up by 12.3%, Shoprite by 10.3% and Usave by 13.2%. Once again, the group has done a lovely job of resonating with customers of all income levels. This is yet another warning to those who are bullish on the Pick n Pay turnaround: it’s going to be really tough when you’re in the same market as Shoprite’s businesses.

And in case you’re curious, which you probably are, the turquoise scooter army delivered sales growth of 58.1% in Sixty60.

Despite the great sales growth, Shoprite’s full-year dividend only increased by 7.4%. This is in line with the increase in diluted HEPS from continuing operations, which excludes losses in various underlying African businesses that were recognised as discontinued operations in this period. On such a demanding Price/Earnings multiple, this wasn’t enough for the market and the share price took a knock as growth expectations were moderated.

There’s a much more important discontinued operation coming, with Shoprite finally making the decision to sell the furniture business. I think this is absolutely the right decision, as this is a slow-growth business in an industry that is all about credit sales rather than pushing high volumes, so it’s a poor strategic fit with the rest of the Shoprite group. OK Furniture and House & Home will be sold to Pepkor at a price equal to net asset value. I’ve covered this in more detail in the Pepkor section in this edition of Ghost Bites.

Back to the broader Shoprite group, the store footprint increased by 343 stores to 3,639 stores. This intensive expansion programme is another reason why the furniture business had to go, as they need the capital elsewhere to earn better returns. As mentioned earlier, the furniture division grew sales by just 2.3% in this period, so Shoprite shareholders won’t be sad to see it go.

Due to the mix effect of underlying divisional growth, gross margin decreased by 10 basis points to 24.0%. Importantly, Supermarkets RSA achieved a small increase in gross margin.

Trading profit increased by 12.4% and trading profit margin moved slightly higher from 5.5% to 5.6%. At this point, you’re probably wondering where the catch was that saw such subdued growth in the dividend vs. trading profits.

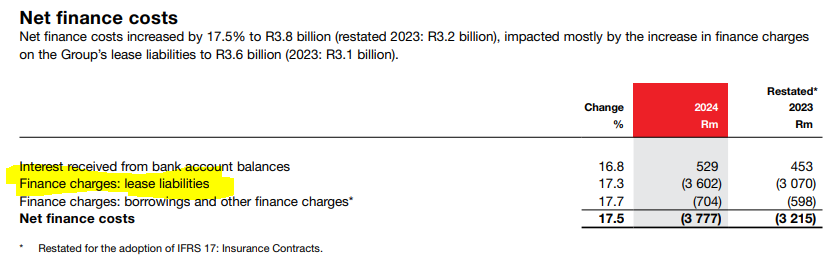

The problem is that in their infinite wisdom, IFRS accounting standard setters decided that lease costs should be in net finance costs rather than operating costs. With an increase of 17.3% in this metric (and 17.7% in finance charges on borrowings), this is what went wrong between trading profit and HEPS:

What this really shows is the inflationary pressure in the cost base, as well as how expensive money is at the moment. A drop in interest rates will help here, as will an even slicker group that allocates capital into the best opportunities.

HEPS for the period was 1,250.2 cents, so the share price after the sell-off reflects a Price/Earnings multiple of 23.6x. Shoprite is a terrific business, but at some point this multiple is simply too high for the realities of growth in South Africa.

Little Bites:

Director dealings:

An associate of a director of Afrimat (JSE: AFT) sold shares worth R6.7 million.

Two directors of different associates of Blue Label Telecoms (JSE: BLU) sold shares in the company worth a total of R330k.

An associate of the CEO of Sirius Real Estate (JSE: SRE) bought shares in the company worth £7.9k.

It feels like it’s been a while, but Des de Beer is buying more shares in Lighthouse Properties (JSE: LTE) – this time it’s a small purchase though (by his standards), coming in at R74k.

There’s a buzz in the market around potential corporate activity at Caxton (JSE: CAT), with Peregrine announcing that it has acquired shares and now has a 9.61% stake in the company.

Orion Minerals (JSE: ORN) has completed the confirming drilling programme at Okiep Copper Project, confirming the quality of the drilling database that was inherited from Newmont and Gold Fields. The next step is to update the Mineral Resource estimate.

Coronation (JSE: CML) has received SARB approval for the special dividend, with a payment date of Monday 16th September to shareholders who are on the register as at Friday 13th September. It’s quite funny that Friday the 13th effectively brings the entire SARS fight to a close, with the missed dividend being paid.

Shareholders in NEPI Rockcastle (JSE: NRP) should note that the circular for the scrip distribution alternative has been made available at this link.

Omnia (JSE: OMN) announced that Global Credit Rating Company has affirmed the long-term issuer rating of A+(ZA) and short-term issuer rating at A1(ZA). Importantly, there is a stable outlook as well.

Insimbi Industrial Holdings (JSE: ISB) announced that the clever reverse asset-for-sale transaction has now been completed. Basically, they sold off businesses and executed share buybacks to help the buyers pay for them.

Oando PLC (JSE: OAO) released some very angry SENS announcements presumably aimed at the Nigerian press and speculation around various allegations related to the company. I don’t think I’ve ever seen such a strongly worded statement, so there’s either a genuine smear campaign out there against the company or there really is something to worry about. Given the wording of the announcement, I lean towards the former.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Some challenges at Bidvest, but earnings are still up (JSE: BVT)

Five of the seven divisions reported profit growth

For the year ended June 2024, Bidvest achieved revenue growth of 6.7%, trading profit growth of 8.5% and HEPS growth of 6.6%. That’s not going to go down as their best period in history, but the direction of travel remains the right one. Note that normalised HEPS was only up by 4.3%, so this was a rare example of Bidvest not delivering an inflation-beating return for the year. The total dividend for the year was also up by 4.3%.

At least cash generated from operations has a double-digit story to tell, up 15.3%. With Return on Funds Employed of 37.3%, you can still feel pretty good about Bidvest management allocating that cash into the business.

With five out of seven divisions reporting profit growth and four of them achieving double digits, the immediate thought is of course where the problems were. Commercial Products faced a high base effect in the renewables market and Automotive dealt with a declining vehicle market.

This gives you an idea of the level of diversification in the group, both geographically and in terms of segments:

Burstone moves ahead with the Blackstone deal (JSE: BTN)

The partnership is focused on the European logistics portfolio

Burstone has announced a rather interesting deal related to the Pan-European Logistics portfolio. At a price that implies a 5.6% net initial yield, global investment group Blackstone will take an 80% stake in the portfolio. The key here is that Burstone will continue to manage the portfolio, so this flicks them neatly into more of a capital-light strategy.

Blackstone is getting it at a good price, representing an 11.7% discount to the FY24 net asset value. In return, Burstone shareholders will see the loan-to-value of the fund drop to 33.5% thanks to immediate cash proceeds to be received by Burstone. With the balance sheet in better shape, the dividend payout ratio will increase from 75% to between 85% and 90%.

This approach of managing portfolios with co-investors is now the focus at Burstone, with initiatives underway to do much the same thing in Australia and South Africa. They are also looking at another opportunity in Germany, so it doesn’t look like Blackstone has exclusivity over that region with Burstone.

Combining balance sheet exposure and management fees is a way to juice up the return on equity over time for Burstone shareholders. You also see this strategy playing out at Stor-Age, another JSE-listed REIT, as well as hotel groups internationally.

The market seemed to like it, with the share price closing 5.5% higher.

CA Sales Holdings marches on (JSE: CAA)

The business model is working

CA Sales Holdings is up 27% this year and 63% in the past year, with the market paying an increasing amount of attention to this story. Through a combination of organic growth strategies and bolt-on acquisitions, CA Sales Holdings is doing a great job of participating in the African growth story across various markets.

For the six months to June, revenue increased by 9.2% and HEPS was up by 19.2%, so that’s a great outcome. Although operating profit fell by 21.1%, a closer read reveals that this was due to a bargain purchase gain in the previous year (the opposite of goodwill – i.e. buying a business at a price below its net identifiable assets) that didn’t repeat in this year. If you strip that out, operating profit growth was roughly in line with HEPS growth.

The key demographic trend here is not just urbanisation of populations in Africa, but also growth in rural areas and demand for FMCG products. CA Sales specialises in taking brands to people and they do it well, with no other business on the JSE playing in this space.

The company only pays an annual dividend, so there’s no interim dividend.

MAS still has work to do on the balance sheet, but underlying retail exposure is helping (JSE: MSP)

Central and Eastern Europe remains a hotbed of activity for retail property landlords

MAS has released results for the year ended June. If you adjust for the impairments in the DJV joint venture, then they came in at 9.19 euro cents per share of adjusted distributable earnings. That’s within the guidance that was provided in March 2024.

These earnings are being supported by strong footfall and tenant sales growth metrics in Central and Eastern Europe (CEE), where retail property owners have been thoroughly enjoying themselves in recent years. The same can’t be said for MAS’ exposure to the residential market through DJV, with a net loss for the period.

The big story at MAS in the past couple of years has been one of balance sheet challenges, with the company taking a highly proactive approach to managing the debt maturities in coming years. MAS cut their dividend to retain cash for balance sheet flexibility, with the worry being around capital availability and costs of debt for a sub-investment grade property fund. Recent progress has been encouraging though, particularly as they have found way to raise further debt funding from an existing noteholder.

The net asset value per share at MAS is 157.9 euro cents, or roughly R31.20 per share. The current share price is R17.15, with the discount reflecting the local market’s distaste for property companies that aren’t paying dividends. With the tangible net asset value at MAS growing by 8.1% between December 2023 and June 2024, that’s a pity.

Nampak makes more progress on its restructuring (JSE: NPK)

These deals are part of the broader asset disposal plan

Nampak has been busy with deals to try and save its balance sheet. One of them is the disposal of Liquid Cartons, a deal which has now closed – and that means that Nampak has received the selling price.

On the Bevcan Nigeria disposal, the merger application has gone to the competition authorities in Nigeria. At this stage they can’t give any guidance on the timing.

In further transactions, Nampak has sold the drums business and liquid business, as part of the broader asset disposal plan that was announced in August 2023. These are small deals, so no further details have been announced.

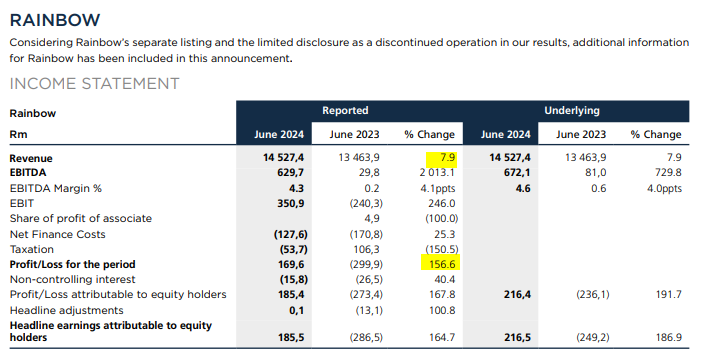

RCL Foods has released results – and Rainbow Chicken shareholders also need to read them (JSE: RCL | JSE: RBO)

Rainbow is separately listed now, but the results came out together one last time

RCL Foods has released results for the year ended June 2024. As Rainbow Chicken was only unbundled on 1 July (and this is no coincidence relative to year-end), the results for RCL include results for Rainbow. We therefore have an unusual situation in which the results for two listed companies are in one set of numbers.

In this case, the term “continuing operations” is doing the heavy lifting. It excludes Vector (sold in August 2023) and Rainbow, so isolating the RCL Foods result is made possible by looking at earnings from continuing operations. On that basis, revenue was up 6.8% and underlying EBITDA was up 15.5%, with HEPS up 8.3%.

RCL Foods is therefore doing decently at the moment, although there are input cost pressures that need to be passed through to consumers in the form of pricing increases. In a group this size, there will always be positive and negative stories as you dig deeper. For example, the pet food business enjoyed better operating conditions this year with less load shedding, yet the baking business had a tough time in bread where there was intense competition. Notably, the sugar business performed well.

Moving on to Rainbow, they describe the turnaround as being “well advanced” with “every component of the process yielding positive results” – great news indeed. Load shedding was an absolute catastrophe for the chicken business, so it’s great to see improvement there. You have to dig a bit to find the Rainbow numbers, with this table showing just how strong the turnaround has been:

Note that a 7.9% revenue increase is all that was needed for Rainbow to swing from losses to profits. The EBITDA margin is only 4.3% for the period, with these incredibly thin margins driving highly volatile earnings. It also helped the net profit story that net finance costs were far less severe than in the prior year. There’s still a long way to go for Rainbow to be considered lucrative, as Return on Invested Capital was only 8.6% in this period.

When there are lots of corporate actions, there is money to be made for advisors. Advisory costs were R58.8 million in the current year for the Rainbow and Vector deals and R25.6 million in the prior year for Vector.

Sanlam gets even closer to African Rainbow Capital (JSE: SLM)

Sanlam wants a bigger slice of the action in the ARC portfolio– especially Tyme Bank

The relationship between Sanlam and African Rainbow Capital is already incredibly close, as it was a B-BBEE investment in Sanlam that provided the capital base off which ARC was ultimately started. Key executives at ARC are ex-Sanlam senior management, so the parties are very familiar with each other. They are about to get even more familiar, as Sanlam is looking to take a 25% stake in African Rainbow Capital Financial Services Holdings (ARC FSH), which means a cash subscription for shares as well as a restructuring of Sanlam’s existing investment in the ARC stable.

ARC FSH is an important holding company in the ARC group but is not the listed company, so Sanlam will hold further down in the structure than the listed shares. They currently have a 25% stake in ARC Financial Services Investments (ARC FSI) which they will exchange for exposure in ARC FSH. That share swap covers R1.492 billion of the investment. That’s only part of it, with a cash subscription worth R2.413 billion to make up the rest.

The net effect here is that Sanlam is pumping cash into ARC’s financial services portfolio and moving further up in the structure, which means they like the look of investments like TymeBank, which will be held entirely by ARC FSH as part of the implementation of the transaction.

Speaking of that asset, it’s interesting to note the outperformance fee structure that will see Sanlam Life pay ARC an outperformance fee based on the extent to which the investment in Tyme Investments Asia as at 30 June 2028 exceeds an annual hurdle rate of 14.64%. That’s not a very demanding hurdle rate for what is essentially a startup, so ARC has a good chance here of earning the fee. It will be capped at R70 million.

Sibanye-Stillwater is now barely profitable (JSE: SSW)

Welcome to new all-time lows since the company relisted in 2020

There really doesn’t seem to be much relief on the horizon for battered Sibanye-Stillwater investors. In a trading statement for the six months to June, HEPS has dropped down to almost nothing. A decrease of between 97% and 98% takes them to between 4.6 cents and 5.0 cents per share vs. 208 cents in the comparable period, which is horrific.

The results were ruined by not just the decline in PGM prices, but also production issues in both the platinum and especially gold businesses. The increase in the gold price got nowhere close to making up for this. Although production for PGMs overall was higher, it would’ve been better if not for production challenges and related pressure on unit costs. As for gold, production was down 21%.

The rats and mice stuff in the group, like Reldan in the US, zinc in Australia and nickel from the Sandouville refinery are just noise compared to how critical the PGM performance is to the group.

This is not pretty:

Sun International continues to grow (JSE: SUI)

By no means a rocketship, but the trajectory is up

Sun International has released a trading statement dealing with the six months to June. Adjusted HEPS is their preferred metric and is up by between 4.5% and 11.6% to between 206 and 220 cents. If you want to stick to HEPS, that metric is up by between 5.4% to 12.4%, with a range of 182 to 194 cents. The differences between the two related to the SunWest put option liabilities and the transaction costs for the Peermont acquisition.

Looking at the underlying businesses, it sounds like Sunbet is the most exciting story at the moment, exceeding its targets with an “exceptional” growth trajectory – and that’s what investors like to hear. Casinos are focused on protecting margins right now and urban hotels and resorts achieved growth in the EBITDA margin. A word that is less exciting is “resilience” which is how they describe Sun Slots, so there’s clearly pressure there.

Despite paying a dividend and executing share buybacks, debt in South Africa (excluding IFRS 16 – i.e. on the right basis for our purposes here) is down from R5.7 billion to R5.4 billion. They are firmly on the right side of debt covenants and generating cash.

Trellidor locks in a strong earnings recovery (JSE: TRL)

To understand these numbers, we need to look further back

Trellidor has been through a pretty torrid time recently, with the share price having shed half its value over 3 years. They initially bounced back strongly in the pandemic as everyone took “stay home and stay safe” very literally, but then there were labour problems and other challenges that ruined the party.

In a trading statement dealing with the year ended June, Trellidor can happily say that HEPS has jumped from 4.2 cents in the comparable period to at least 22.4 cents for this period. The percentage increase isn’t relevant when you’re talking about a 5x increase. Far more relevant is to work backwards and see what the earnings used to be, as FY23 isn’t exactly a demanding base.

It won’t help us to go back to FY22, which was even more awful at just 0.4 cents in HEPS. Like I said, times have been tougher than the doors themselves.

In FY21, HEPS was 40.8 cents. Now we are getting somewhere. Sadly, this means that the recovery in FY24 has only taken them back to around half of FY21 levels. With the share price down over 50% since those levels, it feels like this recovery was largely priced into the stock already.

Hopefully, things will only improve for Trellidor from here.

Little Bites:

Director dealings:

A prescribed officer of Standard Bank (JSE: SBK) has sold shares worth R5 million. There’s been quite a bit of selling from Standard Bank directors and prescribed officers recently and I wouldn’t ignore this.

Two directors of a major subsidiary of Stefanutti Stocks (JSE: SSK) bought shares worth R278k.

Directors of Astoria (JSE: ARA) entered into CFDs over the shares worth nearly R83k.

I’m not going to pretend to be close to the details on what is going on at Quantum Foods (JSE: QFH), where there’s a major fight between different groups of shareholders and the board. An unusual director dealings announcement came out that shows a transaction by various directors with a third party related to call options over their shares. There’s still plenty of stuff going on there.

Harmony Gold (JSE: HAR) released a further trading statement for the year ended June 2024. They are able to almost pinpoint HEPS now, coming in at between 1,852.0 and 1,852.4 cents vs. 800 cents in the comparable period, a jump of around 131.5%.

Anglo American (JSE: AGL) seems to be putting the steps in place for the potential demerger of the stake in Anglo American Platinum (JSE: AMS). Although Anglo American still holds 78.56% in Amplats for now, they’ve restructured that stake through a couple of steps into a new subsidiary within the group. This is typical of the preparation steps required for a major corporate action, so watch out for this in the near future.

Renergen (JSE: REN) has appointed Standard Bank as Joint Underwriter for the Nasdaq IPO and has secured a funding facility with the bank ahead of the IPO. Key directors are having to take on risk here, with associates Stefano Marani and Nick Mitchell pledging their shares in Renergen as security for the loan. This is an unusual situation, as minority shareholders benefit from the loan but aren’t exposed to the security for it.

Trustco (JSE: TTO) announced that Meya Mining (in which Trustco holds 19.5%) has released a technical report prepared at a Preliminary Economic Assessment level. It evaluates the viability of underground mining for the diamonds and suggests a post-tax net present value of $95.1 million discounted at 10% over seven years life of mine. A 10% discount rate is woefully inadequate in my view, so I went digging to see what the post-tax IRR was. The report suggests 65%, which is a much more respectable return for the risk. I have no idea why they bothered showing the NPV based on a 10% discount rate.

If you are a shareholder in MTN Zakhele Futhi (JSE: MTNZF), then be aware that the financial statements for the scheme have been released. Due to the underperformance of MTN’s share price, they are having to extend the structure to 2027 to avoid it expiring underwater i.e. with no value for the B-BBEE shreholders.

Salungano (JSE: SLG) is suspended from trading and thus has to release a quarterly update on the state of affairs. Due to delays in the handover process from KPMG to SNG Grant Thornton, the results for the six months to September 2023 will only be published by 31 October, not 31 July as previously advised. They still need to get the FY24 results done thereafter. At best, the board expects the suspension to be lifted by 31 January 2025.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")