This comes after the share price lost roughly half its value in the past year

The Aveng share price has been a rather sad and sorry tale. They’ve been struggling with the Australian business McConnell Dowell (haven’t we heard that story many times before on the JSE?) and they went through a strategic process of figuring out how to separate it out from the group. After investors hoped for news of a value unlock, what they got instead was an update in December that Aveng would be hanging onto McConnell Dowell.

There’s also a potential sale of the South African business (Moolmans) on the cards. They recently appointed a new managing director in that business, which is an unusual step when you’re trying to sell something.

I don’t know what else has happened in the background, but it seems as though there’s unhappiness and disagreement in the system as the CEO has decided to part ways with the company. Scott Cummins will step down with effect from 30 January 2026 – that’s just one step short of an immediate change.

David Simpson will be appointed as the interim group CEO. Although the announcement gives lots of vague commentary about his previous roles, it neglects to indicate which companies he has led before.

The company has also begun the search for a permanent CEO. Interim appointments often become permanent after due process has been followed, but not always.

Results for the six months to December are expected around 24th February. That’s going to be rather interesting.

The share price fell 6% on the day of the announcement.

Ninety One’s share price is up by well over 50% in the past year. It closed 7% higher on Friday based on the assets under management (AUM) update. For a company like this, AUM is the lifeblood of revenue, as it is the basis upon which fees are earned. When AUM is heading in the right direction, the share price tends to do the same.

The AUM figure at 31 December 2025 of £159.8 billion is a meaty 22.7% higher than it was at 31 December 2024. The amplified impact on the share price is thanks to better sentiment towards the business and the positive impact on margins of achieving growth like this.

Recent momentum is also encouraging, as AUM is 5% higher than it was at the end of September 2025.

Shareholders will want to see more of this as Ninety One closes out their financial year in the next quarter.

Nibbles:

Director dealings:

Several executives at Life Healthcare (JSE: LHC) received share awards and took different courses of action. Encouragingly, it looks like the CEO hasn’t even sold the taxable portion, choosing instead to keep the full R3.3 million in shares. Two other directors sold only the taxable portion (the usual approach). Also, there were two senior execs who sold previously vested shares worth a total of roughly R10 million.

A senior exec at Investec (JSE: INL | JSE: INP) sold shares worth around R7.7 million.

Remgro (JSE: REM) has renewed the cautionary announcement related to a potential restructuring of the Mediclinic investment. You may recall that the intention here is for Remgro to take full ownership of Mediclinic Southern Africa, while the Swiss partners would then take full ownership of the Swiss business. Negotiations are still underway. It’s lovely to see an intention to increase exposure to South Africa rather than a desire to deploy more capital offshore!

After a long, painful and rather worrying process to get the deal done, Shuka Minerals (JSE: SKA) must be thrilled to announce that the acquisition of Leopard Exploration and Mining has now closed. This means they have 100% ownership of the Kabwe Zinc Mine. This is of course only the beginning – like all junior mining projects, it will be a capital hungry process.

Both are footnotes in a much older human habit: wanting something most when we’re told it’s off-limits.

Humans are curious creatures. Tell us something is forbidden and suddenly it’s the only thing we want to see. Hide information and we’ll dig for it. Try to erase something and we’ll screenshot it, repost it, remix it, and turn it into a meme before the PR company has finished drafting the apology statement.

Psychologists have a term for this tendency. The internet does too. And Barbra Streisand, somewhat unwillingly, gave it a name and a face.

A photo nobody cared about (until everybody did)

The year was 2003, and photographer Kenneth Adelman was flying over the Californian coastline in a helicopter. His goal wasn’t voyeurism. Adelman was working on the California Coastal Records Project, a nonprofit initiative designed to document coastal erosion. The series of photographs that he was taking were publicly available, free for non-commercial use, and frequently accessed by researchers and government bodies.

Among the more than 12,000 images that Adelman uploaded was one that happened to include Barbra Streisand’s Malibu mansion. At the time, almost no one noticed. But somehow, Streisand got wind of this and decided to sue.

Citing privacy concerns and legitimate fears around harassment and stalking, she filed a $50 million lawsuit against Adelman, arguing that the photograph exposed details of her residence and therefore endangered her safety. From her perspective, the move made sense. Remove the image, reduce the risk, regain control. It’s worth noting that at the time of the lawsuit the image in question had been downloaded only six times, and two of those downloads were by Streisand’s own legal team.

Streisand and her lawyers hoped that the photograph would quietly disappear and the world would be none the wiser. Instead, the lawsuit did something remarkable: it turned a mostly ignored aerial photograph into one of the most famous celebrity property images on the internet.

Within a month of the filing, the photo had been viewed more than 400,000 times. News outlets republished it. Blogs dissected it. People who had never heard a single Barbra Streisand song suddenly knew where she lived and what her house looked like from above. As if that wasn’t bad enough, Streisand also lost the case and was ordered to pay Adelman’s legal fees. The photo remains online to this day.

Years later, in her 2023 autobiography My Name Is Barbra, Streisand reflected on the episode with candour. Her issue, she explained, was never the photo itself – it was the attachment of her name to it. She believed she was standing up for a principle. In retrospect, she admitted, it was a mistake.

Why suppression so often backfires

The phenomenon now commonly known as the Streisand effect describes what happens when attempts to suppress, censor, or remove information end up amplifying it instead. In other words, the harder someone tries to make something disappear, the more attention it attracts.

This isn’t just an internet quirk. It’s a deeply human one. Attempts to control information have existed for as long as information itself. Books have been banned, artworks destroyed, speeches silenced. What’s changed since the advent of the internet is the speed and scale with which information can be accessed and shared. Online suppression doesn’t just fail quietly – it fails spectacularly.

Cease-and-desist letters are a common starting point. A polite but firm “please remove this content” lands in someone’s inbox. Sometimes it works. But often, especially when the request feels heavy-handed or unjustified, the result is the opposite. The letter gets shared, screenshots circulate, and in no time at all, the story becomes news.

Seeking an injunction to remove content can trigger the same effect. The legal action itself becomes a story, and the content you hoped to bury gets a second, louder life in headlines, think pieces, and social feeds.

When banning makes things more popular

One of the clearest demonstrations of the Streisand effect comes from an unlikely place: libraries. A study examining banned books in the United States found that titles on the banned list saw their circulation increased by an average of 12% compared to similar, non-banned books. It makes sense if you think about it – the act of banning signals scandal. If this book was dangerous, controversial, or forbidden, then it must be worth reading. It turns out the best thing an author can do to sell books in the US is to write something so controversial that it ends up on the banned list, but not so controversial that it alienates readers completely!

It’s not just the contents of forbidden books that get us salivating – we even go crazy for illegal numbers. This is what happened in 2007, when companies using Advanced Access Content System (AACS) encryption attempted to suppress a 128-bit numerical key that could be used to decrypt HD DVDs.

Not exactly a salacious or particularly interesting piece of information on its own, is it? The companies issued cease-and-desist letters demanding the key be removed from high-profile sites like Digg. What followed was internet folklore: the number spread everywhere. It appeared in forum signatures, chat rooms, blog posts, and comment sections. It was printed on T-shirts, tattooed onto bodies, and turned into songs on YouTube.

By the afternoon of Tuesday 1 May 2007, the number was still relatively contained. A Google search for the encryption key returned just over 9,000 results. By the following morning, that figure had exploded to nearly 300,000. By Friday of the same week, the BBC reported that almost 700,000 webpages were hosting the key. This was despite – or rather, because of – the fact that two weeks earlier the AACS Licensing Authority had sent Google a DMCA notice demanding that the search engine stop returning results for it.

A few years later, the same dynamic played out on a much larger, messier stage. In 2012, a UK high court ordered five major internet service providers to block access to The Pirate Bay, the Swedish file-sharing site that had long irritated copyright holders and governments alike. The ruling was meant to curb piracy by making the site harder to reach, effectively cutting it off at the source. Instead, it functioned as a global publicity campaign.

News outlets around the world reported on the ban, often explaining in detail what The Pirate Bay was and why authorities were so eager to shut it down. Curious users who had no idea that it was possible to (illegally) download films off the internet went looking for the site. Seasoned users shared workarounds, mirror links, and VPN tutorials with missionary zeal. Within days, traffic to the site had surged, increasing by more than 12 million visits.

Clearly, blocking access didn’t eliminate demand. In fact, we could argue that getting sued was the best marketing result that The Pirate Bay team ever achieved. The attempt to close the door simply taught millions of people where the door was and how to slip through it.

The people will not be denied access

The Streisand effect isn’t really about celebrities, pirates, or encryption keys. It’s about control, and our instinctive resistance to losing it. The moment someone tries to decide what we’re allowed to see, know, or talk about, curiosity turns into defiance. Information becomes more than data; it becomes a symbol. And accessing it feels like reclaiming agency.

In a reality where information moves faster than authority ever can, silence is no longer enforced – it’s negotiated. And more often than not, the loudest thing you can do online is try to make something go away. Barbra Streisand didn’t invent human curiosity, and the Swedish founders of The Pirate Bay didn’t perfect it. They simply revealed an uncomfortable truth of the digital age: attention is stubborn, curiosity is contagious, and once the internet smells secrecy, it cannot look away.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

In July 2025, Hyprop announced the sale of a 50% undivided share in Hyde Park Corner, along with the option to dispose of the remaining 50%. The proposed purchaser was a wholly owned subsidiary of Millennium Equity Partners.

In my opinion at least, Hyde Park Corner is one of the more interesting and unusual retail spaces in Joburg. Genuinely iconic and with great positioning, the centre includes a solid mix of upmarket offerings. Perhaps I’m just biased because there’s an impressive bookstore. Either way, I think it’s a solid property to own that was made even better by the recent opening of a Checkers FreshX store.

That positive view on the centre is just as well, as the deal to sell the share in the property has fallen through due to lack of fulfilment of conditions precedent. The announcement doesn’t specify which conditions weren’t met. This means that Hyprop shareholders will continue to have exposure to this mall in the absence of any other offers coming through.

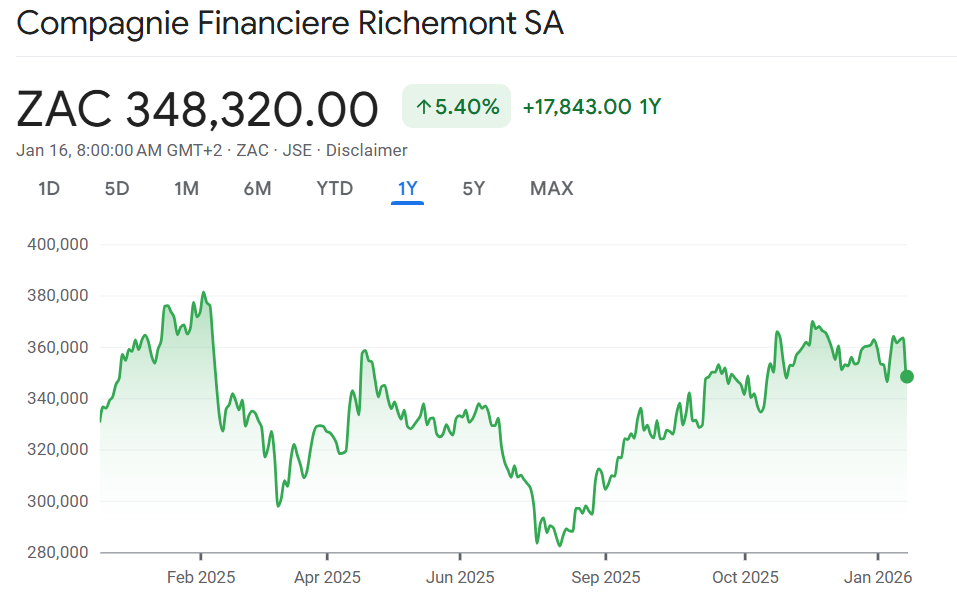

Currencies are having a huge effect on Richemont (JSE: CFR)

The dollar and yen are the worst offenders

Richemont released a sales update for the three months to December 2025, which is of course the all-important festive period. Sales were strong on a constant currency basis (up 11%), but this was diluted down to just 4% growth as reported in euros. Global geopolitical strain is having a serious effect on Richemont’s numbers.

Before we get to the currency effects, let’s deal with the momentum through the year. This quarter was slightly stronger than the nine-month results on a constant currency basis (11% Q3 vs. 10% YTD) and slightly lower as reported (4% Q3 vs. 5% YTD). This tells us that the the business itself is getting better, yet the geopolitical impacts are getting worse.

Breaking it down by region really tells the story. Asia Pacific remains the biggest region with sales of €1.87 billion, up 6% in constant currency but down 2% as reported. Within this region, it’s important to note that China, Hong Kong and Macau on a combined basis grew 2% in constant currencies. Seeing a positive growth trend in that part of the world is important to the investment case and a critical read-through for the entire luxury sector.

Next up is the Americas at €1.74 billion, up 14% in constant currency (a terrific result) but only up 6% as reported due to the weakened dollar. Europe is the third largest region at €1.55 billion, up 8% in constant currency and 6% as reported (part of the difference is the UK, which they say performed well).

Japan is much smaller (€632 million) and grew 17% in constant currency, or 7% as reported due to the pressure on the yen. Just to finish the regional summary, Middle East & Africa (€607 million) was up 20% in constant rates and 12% as reported.

The other popular way to slice and dice Richemont is by product segment. Jewellery Maisons (by far the largest at €4.8 billion) achieved sales growth of 14% in constant currency and 6% as reported. That’s a particularly impressive performance against a strong base. Specialist Watchmakers (€872 million) grew 7% in constant currency and 1% as reported. The Other bucket (a meaty €742 million that includes fashion and accessories) was flat in constant currency and down 5% as reported.

Finally, we can view the group through a distribution lens. Retail is the biggest (€4.6 billion) with a constant currency move of 12% and reported results up 5%. Wholesale and royalty income (€1.4 billion) grew 9% in constant currency and 3% as reported. Finally, online retail (€413 million) was up 5% in constant currency and down 1% as reported.

This deals with the sales story, but what about profits?

There’s a most unfortunate note in the announcement that I’ll repeat verbatim:

“Consistent investment to nurture Maisons’ growth prospects in a complex macroeconomic environment marked by weaker main trading currencies and rising material costs continuing to weigh on margins.”

Or, in simple terms, they have to keep spending money to stay competitive, but they are struggling to maintain margins. Combined with the currency concerns, this is why the share price fell over 4% on the day.

This is an interesting chart:

Nibbles:

If you’re keen to get up the curve on Southern Palladium’s (JSE: SDL) investment story, then a good way to do it would be to refer to the latest presentation delivered by the executive chairman at the Future Minerals Forum in Saudi Arabia. You’ll find it here.

The first Ghost Stories podcast in 2026 opens the door to global property investments with Satrix. In this lively and insightful discussion with Lauren Jacobs, Senior Portfolio Manager at Satrix, you’ll learn about how Satrix is broadening the range of property investment opportunities for investors.

Aside from a discussion on the various property strategies followed by investors (ranging from buy-to-let through to owning REITs and associated ETFs), this podcast gives you details on the existing suite of property ETFs and unit trusts offered by Satrix. This includes the Satrix Property ETF (JSE: STXPRO) that Ghost loves owning in his tax-free savings account.

And of course, there was much focus placed on the new ETF in the stable: the Satrix Global Property ETF (JSE: STXGLP). With rand-denominated exposure to offshore property, this ETF brings property asset classes that you won’t find anywhere else on the JSE (like senior housing and data centre funds).

Get ready to learn about how to broaden and diversify your equity exposure in property.

Satrix Investments (Pty) Ltd & Satrix Managers (RF) (Pty) Ltd is an authorised financial services provider. The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information. For more information, visit https://satrix.co.za/products

Full Transcript:

The Finance Ghost: Welcome to 2026. It’s a new year, and it’s another fantastic year of podcasts right here on Ghost Mail with your host, The Finance Ghost. I’m so looking forward to that, of course, and it’s another year with Satrix. I’m so happy to have you guys back.

I mean, this is year…I want to say three? It might even be four at this stage, I’m actually not sure. I think it’s three. It’s really been a fantastic journey with the Satrix team. Just understanding ETFs, but also getting to know the team and the nuts and bolts of how these things work, the investment ideas that come through.

And of course, to end off 2025, there was a wonderful discussion with René Basson, where we talked about the 25 years to get to this point. Highly recommend you go back and listen to that if you want to give yourself some context as to just how amazing this journey was, to get to these ETFs that we now just take for granted.

We just take for granted the fact that you can own the market with just a single investment every month, for example. It really is quite amazing, and it’s quite a journey.

Today, we will be talking about a new product that’s coming out from Satrix, so that’s going to be quite exciting because the team is always innovating, they’re always bringing new stuff to the fore.

To do that, we have Lauren Jacobs. She is a Senior Portfolio Manager at Satrix. She is also no stranger to the Ghost Stories podcast. Lauren, you’ve done a couple of these now – I think you’ve done two – so, welcome to the podcast. Happy New Year, and thanks for doing this with me.

Lauren Jacobs: And Happy New Year to you, Ghost. Thanks for having me again, and all the best for 2026. It’s been an interesting time up until 2025, but yeah, onwards and upwards for the new year.

The Finance Ghost: Yeah, absolutely. It’s going to be quite a year. It’s gotten off to quite a start from a geopolitical perspective, so it’s not going to be boring, I think. That much we know for sure.

But what we’re talking about today is not geopolitics. We are talking about property. And actually, what makes that so interesting is that property sits somewhere between your sort of traditional equity exposure and then your debt exposure. So, quite an interesting place in a portfolio.

But before we even get to that, I think property remains an asset class that people are just very drawn to. It’s a very contentious issue, the cost of property. Because, of course, it directly affects your cost of living.

I think the conventional wisdom, from our parents’ generation especially, is to own the house you live in and then, as soon as you can, go and buy an apartment and rent it out. The classic advice was, “Well, buy your first apartment and then, when you’re ready to move on, you can rent that one out. Then you buy the next place.”

This was kind of the dream that many of our parents put onto us – with the best intentions, I think. Unfortunately, that hasn’t necessarily worked out super well in South Africa, depending on where you bought. Just the reality, unfortunately.

So, I don’t do any of those things. I, at this stage, don’t own the house I live in. I certainly don’t have any investment properties. I prefer to have listed property stocks.

But before we dig into the ETF, I was curious where you fall on that spectrum, Lauren, in terms of your approach to property and how you think about it. Do you prefer the listed stuff or a bit of bricks and mortar and the admin that comes with it?

Lauren Jacobs: I’m in the bucket where I fall into all three – we own a home, we own a rental property, and we own property stocks. So, it’s a very interesting time just in terms of how things are shaping up around property (not only in South Africa, but also around the world).

But for us – for me – I think I’m more of a conservative investor. I like to know my house is going to be my house forever, but maybe it’s just because I’m a little bit older. I still subscribe to that kind of thought. And also, unintentionally, the investment property came up.

But again, like you said – the admin around it and the taxes. People don’t understand that when they go into buying a property – the transfer duty, then if it’s your own property, there might be a capital gains tax. And the constant cost of a property if something goes wrong (and there’s always something going wrong).

You need to make provision to have cash available for that. To fix whatever’s gone wrong, or for your levies and your taxes and so on. I think when you saw your parents, they had a property, and you just lived on the property. You didn’t know all of those costs that came with it.

So, that’s just something – if you are buying a bricks-and-mortar property or even an investment property – to keep in mind. Just around how many costs are included in the lifespan of that property.

And then again, in the olden days, your parents were like, “Oh, but I’m keeping it for you, and you’re going to get this when I die.” But then there’s also that estate duty tax at the end that you’re not aware of, so there’s a lot of hidden costs around that.

Yes, there is the security of knowing it’s mine, I can go home every day. But yeah, it’s just – there’s always that double-edged sword around having that, but also the implied cost of it. It’s an interesting ride, and that’s my view on it.

The Finance Ghost: Yeah, I like that. Thank you. So, I guess where I am on the spectrum is I would, at some point, probably have what I would call our ‘forever home’. But that’s more around stability for family and children and proximity to schools. Because the rental market can sometimes be very cruel around timing and what’s available at the time you need to move. It’s not a financial decision, definitely not.

And I quite enjoyed your comment around how you take for granted the costs your parents might have had. I’ve experienced that now. So, the place we’re in now has a swimming pool. It’s the first time I’ve been responsible for a swimming pool. Young kids love it, obviously, but I think back and I’m like, “Wow, my parents went through a lot to make this thing work.” It costs you money all the time.

I grew up in Joburg, where the weather’s good a lot, so we used it all the time. Down in Cape Town, it’s like every few days, depending on how windy your suburb is. But anyway, this is just adulting of course.

The one thing I personally won’t do is have an investment property, just because of the admin you talk about. Because it’s not passive income. People think it’s passive income. I’ll tell you what is passive income: owning a property ETF. Because out there are a whole bunch of professional people sending rental invoices, kicking people out who don’t pay, getting new tenants in, getting the leases done. That is passive income.

So, I’m a big fan of having property exposure in my equity portfolio primarily. It’s a very good inflation hedge. It also (I like to think) gives me a little bit of a hedge against residential property prices absolutely running away while I’m not actually a residential property owner. Because chances are very, very good that if residential property is cooking in South Africa, the best shopping centres, the best industrial properties, and maybe even offices are probably also actually doing kind of well.

So, there’s a pretty decent hedge there. At least, I like to think. Hopefully, that will work out for me. I guess time will tell.

And of course, you can have this property exposure in your tax-free savings account, which is fantastic. So, we’ll talk about that as well.

But maybe let’s talk about some of Satrix’s existing products in the space, and then we’ll get to the new stuff. And the property sector on the JSE really is vibrant. It’s super active. It’s actually one of the sectors where historically we’ve had the most listings as opposed to delistings. There’s tons of capital raising all the time, and it’s because institutional investors are big supporters of the property sector.

And so, billions of rands (literally billions) flow into these companies, and they can go and deploy it into properties. So, very, very interesting space. Of course, that means that there’s an index for it. Satrix tracks the index. So, maybe we could just start there.

You could give us a quick overview of some of Satrix’s existing property products that investors might already be familiar with. As I said, it’s something I already have in my tax-free savings account, so I get that beautiful REIT dividend without any tax whatsoever, which is fun.

So yeah, give us the lay of the land, literally, in terms of the current Satrix offering around property.

Lauren Jacobs: So, in the local property space, currently Satrix has two offerings – one on the ETF side and one in unit trust form.

On the ETF side, that property ETF tracks the S&P SA Property Capped Index. That’s a little bit different to the way the JSE does it. They’ve obviously got a broader composite that they choose the property stocks from – not maybe a JSE All Share, it’s kind of a different broad-market index that they start from.

So, what you’ll find is that there’ll be some stocks in there that are not maybe specifically in the SAPY (the SA Listed Property Index, the FTSE/JSE one) or the weightings will be different.

It’s also got a capping factor, so the stocks are capped at 10% at each quarterly index review, and so, although it will move in line with the property sector because of some of the weightings of the underlying constituents, you won’t get the same as you would in the SAPY.

And of course, in the SAPY, the number of constituents there is capped at 20. Only 20 constituents in the SAPY, and that one also does a quarterly review.

So, on the unit trust side, we’ve got the SAPY – where we’re tracking the SAPY in the unit trust – and then on the ETF side, we’re tracking the S&P SA Property Capped Index.

Again, we’ll move sort of in line with the property sector, but you will find the differences just in terms of the underlying constituents and how those constituents move. For example, in the ETF, we have Hammerson (JSE: HMN) at 3%, whereas it’s not in SAPY. So, there you’ll get a difference in returns, depending on what that constituent does.

The Finance Ghost: Yeah, that’s interesting, and that’s why the fact sheets are obviously so important. You actually need to go in and just see exactly what is being tracked. What’s actually in there, what you are getting. And go and check out those weightings as well, because that makes a big difference.

And of course, the other thing in the property sector, specifically in South Africa, is a lot of these funds have offshore exposure. So, it’s all good and well to say, “Well, I love the South African property story and I’m trying to maybe hedge against residential property going up, etcetera, etcetera.”

But if all of your money is sitting in a fund (and this is not something that would happen in an ETF), but if you go single stocks and you go and buy a fund that is focused on Poland, that’s not going to hedge you against South Africa in any way, shape or form. It’s just not going to.

So, that’s rather interesting and certainly something to take into account. And it’s the old story, right, Lauren? Go and read the fact sheet, go and understand what it is that you are actually buying, because that is the only way to do it when it comes to ETFs. Go and do the research. It’s the old cliche, right?

Lauren Jacobs: Correct. And again, ETFs (or at least, index-tracking ETFs) are quite transparent. All the information is there. The constituents are on the website every day.

So you almost don’t have an excuse to say, “Oh, I didn’t know that was what I was tracking.” All the information is there for investors to find.

The Finance Ghost: Stuff like the capping really does make a big difference. So, genuinely go and have a look. There’s always a sort of ‘Top 10 Constituents’ list that shows you a lot of information in these fact sheets.

Don’t think that just because you’re buying ETFs, you don’t have to do research. You do have to do research. It’s just different research to how you would do a single stock, for example, and it is also much easier. ETF research is much simpler than going and digging into all these companies, definitely.

So, having set the scene of the excellent current offering and a couple of the options there for different kinds of investors – in December, Satrix capped off the year by talking about a global property feeder ETF. Very interesting. That will be under the code STXGLP.

This now delivers international property opportunities to investors looking for further diversification. So again, if you’re trying to hedge residential property in Cape Town, this one is not going to do it. But it will bring some excellent other exposure into your portfolio – some offshore exposure property specifically, obviously.

But before we even get into the details of the actual fund, this word ‘feeder’ – can you tell us (because I know you’re super involved in the operational side of the ETFs, we’ve done a show on that before) what a feeder ETF is, for those who have seen this term before and always wondered what that is?

Lauren Jacobs: So, if we take a step back and just think about global indices, for example. Your MSCI World, your S&P 500 – there are hundreds (and then in the MSCI World, thousands) of stocks in those indices.

As a local index-tracking house, it isn’t viable for us to now go and buy every single stock in that index and hold it and rebalance it every quarter. The cost, first of all, will be high. And secondly, sometimes we can’t get all the markets, or there’s the currency efficiencies that we wouldn’t be able to get.

So what a feeder structure does is it says instead of us going to hold every single stock underlying, we find a global ETF (or foreign ETF, whichever one you want to call it). Maybe it’s in the iShare range, maybe it’s in one of the other index provider ranges, and we go and just buy that ETF.

So, there’s only one holding in a feeder fund structure, and that holding is holding this ‘master fund’ or this larger, main parent fund – the wording’s interchangeable, but it’s one fund that we are holding, and that fund is then tracking the index.

So, we would get a return of the fund, which is in turn tracking the index underlying. And that also reduces the cost, because now we’re only holding one instrument. We’re not having to go and trade all of these underlying stocks.

It’s just an efficiency in terms of how we can give global exposure, but in rands. So, we buy the underlying in whatever currency it is, but we offer it to investors in rands. And that is really efficient, in terms of currency, in terms of pricing for the end investor.

The Finance Ghost: Yeah, it’s super interesting. And that’s exactly the point, right? It’s a currency efficiency. So technically speaking, someone could go and buy this ETF overseas with their offshore money.

So, if you’ve already taken money out of South Africa (you’ve got, I don’t know, a dollar-based brokerage account or whatever it is), you can go and buy this ETF right now.

Lauren Jacobs: That’s correct, yes.

The Finance Ghost: You can do it. But with the Satrix product, you can now do it without having to first take your money into dollars, for example. So that helps, because every time you’re going into dollars, there are inevitably some pretty ugly fees around switching currency. That bid-offer spread gets pretty wide.

And also, you’re using up your allowance. So, that’s more of a consideration for big investors who… I mean, this is the lifelong dream for many of us, right? May I please get to the point where I feel irritated about only taking, what is it, R11 million out of the country every year?

Lauren Jacobs: Exactly [laughing].

The Finance Ghost: Like, “Oh no, today in first world problems.” But jokes aside, the currency, the bid-offer spread – that’s a big one.

And now, just the ability to see it on your rand-based brokerage account – because the reality is most South Africans, much as they like to complain (well, actually these days we complain a lot less – the rand is looking good, things are looking much better, you go back to the depths of load shedding and no one wanted anything to do with the JSE), even then, familiarity bias kicks in. South Africans just love seeing things quoted in rand, things on the JSE.

I see it with my own work – if I write about a South African stock versus a global stock, there’s no competition here around what people are more interested in. So, these are all of the factors that come in, right? Just making it easier for people to actually get access to the stuff.

Lauren Jacobs: And it’s a huge plus to be able to use your rands to buy an offshore investment. Who wouldn’t want to do that? And also with Satrix, the way we offer it, you can do it on a monthly basis with a debit order. Who would have thought that you can get offshore exposure?

And also, if we go back to our conversation around your bricks and mortar – your house, your investment property – a lot of our assets sit locally, and we want to diversify and improve our exposure. And here you can improve that, but still using your rands. So, it’s a great concept for us to be able to offer this to investors.

On the flip side, though, we must also be aware. Like you mentioned, the rand is doing really well at the moment, but there’s always that currency risk in terms of offering it to you in rands, even though the underlying investment is in dollars or euros. That’s another thing that investors must really be aware of.

You might see, “Oh, the S&P did 10%,” but you must think, “Okay, is that in dollars or in rands?” If I now look at the Satrix S&P 500, which is rand-denominated, and that did maybe 5%, you must remember that the rand strengthened.

So, it’s just something to be aware of. That currency risk is there, and also to be conscious that you can’t just say, “Oh, but Satrix is underperforming because the S&P is doing this.” Also just remember – in what currency is it performing?

The Finance Ghost: Yeah, absolutely. And this is the thing with offshore, right? You’ve got to have a currency decision, and then you’ve got to decide where your money is going, because you want to take the rands out of the country when the rand is strong.

Unfortunately, it’s just human nature. People panic at the worst time for them to panic. It’s always when the rand is like flirting with R20 to the dollar that everyone is taking their money offshore.

Like, “Oh no, this thing is going to R30. It’s over, it’s done. We are Zimbabwe. Oh my goodness!” And the money’s gone.

And then it comes back down to like R18, and now that wonderful advisor who told you that we are basically going to become a basket case is gone. They’re nowhere to be found, you know. They’ve made their money.

Lauren Jacobs: Exactly.

The Finance Ghost: So, yeah, this is the thing. When the rand is doing really well like this, it’s the time to think, “Okay, what international exposure would I like to pick up?”

Because the rand had a fantastic year. Look, I think it might have another pretty decent year, but we’ll see what happens. It’s off to a very good start…

Lauren Jacobs: It really is, yeah.

The Finance Ghost: …and in the last few weeks, it really has been quite something to watch!

[both laugh]

The Finance Ghost: So, yeah. This is the benefit of diversification. There’s no way to call these things on an individual basis. And you certainly shouldn’t be holding one investment so that you sit there and cry yourself to sleep over, you know, “Oh no, the rand strengthened!”

Then you’re doing it wrong. Then your portfolio is not being managed as a portfolio.

Lauren Jacobs: Definitely.

The Finance Ghost: So, these things are considerations – currency, etcetera. But they should always be seen in the context of the broader portfolio.

Lauren Jacobs: Exactly.

The Finance Ghost: So, speaking of ‘broader portfolio’ and these exposures, let’s talk about the types of properties you’ll actually find in here.

Because, as South Africans, when we look at REITs, we are very accustomed to big shopping centres (that’s always in there), logistics properties these days (so that’s big warehouses, etcetera, etcetera, and also small ones, actually), and then offices.

Offices, people try not to talk about too much, because that’s still a little bit of a mess. Lots of offices got converted to residential. Vacancies are still not great, negative reversions are still a problem.

And we have a sprinkling of specialist funds in South Africa, but we’re very light on specialist property funds in South Africa. There are like a couple, literally. Stor-Age is a very good example (which is, as their name suggests, storage).

But offshore, it’s different. There are lots of specialists, right? So, how much of that comes through in this ETF?

Lauren Jacobs: So, it’s such an interesting sector, this global property sector, because things are changing every day for us. Like you say, moving from that bricks and mortar (office blocks, retail malls) to where, in developed markets, the universe includes so many different properties.

And when I talk about that, it’s from your traditional bricks to digital infrastructure. So, for example, data centres fall within these properties now.

These are the backbone of cloud computing, and AI, and digital services. They house the servers and the network equipment for these large tech companies. I mean, who would have thought, “One day, that’s a property stock”?

Healthcare facilities, those are also now being rented out – senior housing, hospitals, medical offices. We’ve got this ageing population, and we’re outsourcing this healthcare infrastructure. It’s a huge global property play.

And then again, another sector that we look at here is the telecom towers and speciality REITS that we spoke about. These towers are now also being constructed and seen as property, and this is supporting mobile connectivity and digital transformation around the world.

So, it’s a very interesting time. It offers such huge diversification from what we’re seeing in South Africa and what’s offered in South Africa. And it looks at the structural growth of domestic economies and what is going to be required in the future – from property, from what is available to investors in terms of property.

The Finance Ghost: The reason why a lot of these funds and these specialist funds have been spun out of traditional industries – you spoke about stuff like telecom towers, that’s a really good example – is because property is just a very different asset to the operations of a business, and it attracts a very different kind of investor.

So, if you split out the operations of a business from something like its infrastructure, then you can actually reduce the cost of funding for the entire group. Because suddenly, infrastructure investors who see their particular assets as lower risk jump in and say, “Okay, we’re prepared to fund the towers at a lower cost of capital than the actual operations of the tenant of those towers.”

Now, I’ve always wondered about that, to be honest, because in specialist funds, is the risk really so different? At the end of the day, what happens if that telco goes under? It’s not like another one is going to jump in and immediately pick up all those leases.

Lauren Jacobs: Exactly.

The Finance Ghost: So obviously, the more specialised the properties, the riskier it is. But there’s an entire industry of people who have dedicated their careers to quantifying that risk and actually taking a view on capital.

And obviously, CFOs of these groups then say, “Well, how do we optimise our cost of capital? Let’s try to get different investors in. Let’s split out the properties from the operations, etcetera.” And there are still a lot of big corporates that have massive property portfolios sitting on their balance sheet that they haven’t actually split out or done anything with.

One of the really interesting local examples is actually Shoprite. They have a massive property holding. There’ve been many calls over the years for them to actually split that out and separately list as a REIT, bring down their cost of capital, but it’s not something that they’ve done.

And I guess the corporate consideration there is you’ve got to wonder about loss of control of your properties, etcetera. And all of those decisions in boardrooms around the world eventually lead to the creation of these property funds, which then land in an index like this. So, some very interesting stuff.

And, as you’ve mentioned, there are some real growth areas like data centres, etcetera. Lots of debate around: Are there too many data centres at the moment? Are there not enough?

But this is the joy of investing, right? Risk and reward. You’ve got to figure these things out for yourself, right?

Lauren Jacobs: Yes. I think the change in the way business does business is consistent, and that’s also something we want to see going forward – the digital transformation. You want to see that businesses are being mindful of that.

And, like you said, taking your property out of your business and finding different ways to essentially leverage what you can out of those properties. We’re seeing that globally now, so it’s a good direction we’re going in.

And I think, because it’s been in businesses before, a lot of them are now spinning it off and out of their business. It’s not that it’s a new thing, so there is some trust there, and some history there that we can look at and say, “Okay, yes. This is a good thing, going forward.”

The Finance Ghost: The other nuance here is the tax, and we should definitely talk about that, because the tax in this particular fund is quite interesting. There’s a withholding tax benefit in the way that the fund is structured.

So I guess, as simply as possible for investors – let’s call it individual investors specifically, who are sitting there going, “Okay, that’s cool, that’s interesting. What’s in it for me from a tax perspective, versus going and investing in the local ETF?”

What does the tax benefit really mean for investors in the ETF, and how do they see it coming through? Is this something that just comes through in the return of the ETF itself? Does the tax happen layers up, and you just see it in your return? How does that actually work?

Lauren Jacobs: So, as we spoke about earlier, this is a feeder fund. The feeder structure calls for us holding a specific underlying foreign ETF, and the one that we have invested in is the HSBC FTSE EPRA NAREIT Developed UCITS ETF.

So a UCITS ETF is a specific legal structure. It’s seen in Ireland as like a CIS in South Africa; it’s very similar to that. But in the same breath, that fund is Irish-domiciled – that means that HSBC has set up a company in Ireland, and the fund itself is Irish-domiciled.

The compelling thing about that is that there’s a double taxation treaty between Ireland and the US. What that means is that an Irish-domiciled fund will not pay the full dividends withholding tax on US equities.

And as we spoke about, listed property is like an equity, right? So, what happens with this double taxation treaty is that these Irish-domiciled funds only pay 15% withholding tax on US stocks, not the 30%. And the fund, or let’s say the index itself, 62% of that index sits in US stocks.

So if you think about it, on 62% of your fund, you’re now only paying 15% on your withholding tax, not 30%. But the index itself assumes a 30% withholding tax.

This creates a structural benefit where the fund would consistently outperform the benchmark, because of the fact that you’re paying 15% less on your tax. That means, net of fees, you’re kind of getting that gain over and above your index, for all time periods.

And effectively, what it does is it subsidises the cost of the underlying fund. So, because of the fact that you are now getting an outperformance of the index, you’re actually gaining back the cost of your fund.

And also, that tax saving effectively offsets your fee, and that’s a gain to the investor because you are “not paying a fee”, because the fund has essentially gained that through that withholding tax benefit.

So yeah, for me, that would mean that you are effectively in line with the index. And everybody complains, “Oh, ETFs are always behind the index.” But that’s because of costs.

In this instance, you’re going to see that the fund should essentially be in line with the index, because of that gain from that withholding tax benefit.

The Finance Ghost: Super interesting!

So, I’m looking at the top holdings in the underlying index once you go all the way down to what this thing is actually tracking. Just to give you an idea of diversification, the biggest holding (and hopefully I’m looking at the right thing here) is Welltower?

Lauren Jacobs: Yes.

The Finance Ghost: So if you go and have a look at Welltower (and it’s actually super fun), if you look at their About Us, they talk about being “positioned at the centre of the silver economy”.

Now, before you panic and you think that this is a mining company that’s pretending to be a property company, what they’re talking about is senior citizens in places like the US, the UK and Canada.

These are developed markets which have, I will remind you, a serious birth rate problem, an ageing population, lots and lots of older people who are getting older all the time (again, on average, not individually) because of better healthcare.

And that is interesting. That is an interesting long-term fundamental underpin. There is nothing like that on the JSE. There is not a single property company on the JSE that is anything like that. So, that’s just one example.

Then, Prologis is second. That’s basically the GOAT of logistics plays. That’s the big one. That is the big one.

Lauren Jacobs: Yeah [laughing]

The Finance Ghost: Also in the top five are Equinix and Digital Realty Trust. Those are both data centre-type plays.

Lauren Jacobs: Correct.

The Finance Ghost: And then in fourth place is Simon Property Group (something I’ve researched on Magic Markets Premium a couple of times), which is, again, the GOAT of retail malls in the US.

And again, in the US, if you actually have a look, there’s this horrible long tail of crummy malls that no one wants – it’s a bit like their banks…

Lauren Jacobs: [laughing]

The Finace Ghost: …but the best ones are fantastic, and Simon plays among the best ones. So, that is a really interesting way to go and get that kind of exposure.

Almost 8% sits in Welltower – that’s the senior citizen residential stuff. Prologis, seven-and-a-bit percent. If you combine Equinix and Digital Realty Trust, you’re looking at like 7.7% – that’s the data centres, among those two. There are probably some more further down. And Simon, at like 3.5%.

That’s just your top five holdings. It’s very interesting. I see there’s a storage name down there. There are a couple of storage names down there, actually.

So, again: diversification. For anyone who thinks that diversification is not important, go back and listen to some of the podcasts we’ve done on this series with people like Kingsley, with people like Nico. Just go and have a listen, it’s something we’ve spoken about.

The whole team, really. Siya, Duma. It’s come up over and over again. It’s come up in conversations with professionals way beyond Satrix, because everyone understands that diversification is important.

So, my favourite thing about this ETF is that now there is a way on the JSE to actually go and get this exposure with a single investment and, like you say, a debit order. I would encourage listeners to listen to the discussion I had with René at the end of last year about how far things have come.

It’s absolutely incredible that you can set up a monthly debit order, and a portion of your wealth every month will flow into assets like US senior-citizen housing. Just contemplate how interesting that is, compared to going and hacking your way through that buy-to-let flat that you’ve owned since you were 25 and has gone nowhere in its value.

I mean, I’m being slightly facetious, but go and speak to enough people who have done that, and they all have pain in their eyes – especially, I’m afraid, if it’s places like Joburg. There hasn’t been much property growth over the past, like, 10 years.

I actually went and looked, just for fun, at the apartment in Lonehill where I lived during my articles – which I bought because I articled at a bank and you could get access to this super-cheap funding. And obviously, I had my parents in my ears like, “Well, go and buy property. This is the thing to do.”

That would have been almost 15 years ago now. Whatever it is, I promise you (and I wish I was joking), those apartments are selling for the same price today.

The Finance Ghost: The same price. That’s horrific! It’s so bad [laughing]. So, you know, you’ve got to be careful with this stuff.

Lauren Jacobs: Yeah, I think it’s…okay, maybe my experience is a bit different. In Cape Town, obviously, it’s a little bit different.

The Finance Ghost: Yeah, it’s very regional.

Lauren Jacobs: But then you get to a point where you also have to take the tax into consideration. Because now, your return is higher than what you’re paying in terms of your bond payment and your interest. That’s also an important thing to think about.

And if we go back to having a Satrix investment and putting it in your tax-free savings account, the dividends that you get from this listed property ETF – those are not taxable. So, it’s a win-win situation if you now buy the ETF through Satrix and also put it in your tax-free savings account, it’s like a no-brainer to really put a lot of those income-generating ETFs into your tax-free savings account, and just gain in terms of the tax there.

The Finance Ghost: And people often use the argument, “Well, if you go and buy the physical property yourself, then you are getting the full upside on the capital, and you’ve leveraged the thing.”

That’s great, now go take off your costs on the way in (which is your transfer duty, etcetera), and now your cost on the way out (of an estate agent) and give me your average holding period.

And, unfortunately, the other argument that always happens is, “Yeah, but I made money.” And that’s always how people… Unfortunately, when they haven’t really been exposed to proper investment thinking, where you look at the world as an annual return, like a compound annual return over time.

Lauren Jacobs: Yes.

The Finance Ghost: The test is not, “Did you make a profit?” If you made R1,000 on R1 million over 10 years – yes, you made a profit, but you also didn’t. Because your friend, who went and bought shares, is definitely not sitting on R1,000 from his R1 million, or her R1 million.

So anyway, the point is: always speak to your financial advisor. Look at these things as a portfolio, etcetera. But personally, I’m a strong proponent of property ETFs, whether local or offshore.

That comes down to your personal decisions, what you want to own. I mean, that’s where it gets really interesting. But I’m a big proponent of property ETFs, rather than a buy-to-let investment.

Owning the home you live in and you raise your kids in and it’s close to the schools, that’s a lifestyle decision where you have a lot of other things you need to take into account, but certainly buy-to-let, Lauren, I would say the ETFs are more interesting, hey?

Lauren Jacobs: [laughing]

The Finance Ghost: So, when are you selling your apartment and buying ETFs? That’s the big question.

Lauren Jacobs: Let’s not go there right now. Let’s not go there right now. [laughing]

The Finance Ghost: The pain trade. [laughing]

Lauren Jacobs: [laughing] Yeah. And again, going back to diversification. It’s not only what assets you have in your pension fund or in your other portfolios. You need to consider across all the bands.

If you think of your pension fund. Yes, they’re allowed to go with 45% now, but if you look at it, most of the funds are sitting at like 35%, 38%. It’s not that full offshore exposure as yet. So there’s an opportunity there to increase your offshore exposure with this global property fund.

So it’s really looking at the spectrum of what your assets are, whether it’s your house, your pension fund, or your investment property (we may not call it an investment property, but that other property that you rent out).

It’s just thinking around, “What does my total portfolio look like? And how can I improve that, in terms of a) the dividends I’m getting out of it, and the return and the tax efficiency of the total portfolio.”

The Finance Ghost: Just a final comment from my side. If you do invest in this thing now (let’s say the rand strengthens over the next six months and property overseas doesn’t keep up with the level of the rand strengthening), don’t be surprised if it doesn’t give you an initial fantastic return, because your rand-based assets have probably done better.

Again, it’s part of a portfolio. You should never just have one ETF. And I would say if you are going to have one ETF, it shouldn’t be offshore, because your life is in South Africa.

So, if you’re going to have just one – which you should never do – you should be matching it to the currency that you spend in. That would be my two cents’ worth, I suppose.

But as a part of a portfolio, I think it’s super interesting. It’s listed currently, so you can go and search it. The code is JSE: STXGLP, and that is the Satrix Global Property Feeder ETF. Very, very cool.

Final question from my side, Lauren. How long does it actually take to get one of these things off the ground?

Like, from when the team starts saying, “Hey, this is what we want to do,” until we see this on our screens, how long does that actually take? Because I’m sure it’s a lot. It looks simple from the outside – I’m sure it’s anything but simple on the inside.

Lauren Jacobs: We go with about six months. It also depends, because remember, you need your approvals via the FSCA, from your trustees, from the JSE. So, those processes take quite long.

And then, if there are any questions from the FSCA, from the JSE, from trustees. It’s the back and forth. So, I’d say this one took a little bit more than six months, but yeah.

And then, once all those approvals come through, there’s obviously a JSE timeline in terms of creating that on the JSE. So, yeah, it takes quite long, from the inception of the idea.

And I must say that this idea has been around for a long time in terms of Satrix wanting to offer this global property offering to investors. It’s just that, at the time, we couldn’t find an underlying fund that we wanted to buy into, and that also gave us this Irish domicile.

So, it’s taken us a while to get to that point, where we’ve actually found an investment that we wanted to offer to local investors. It’s been a long time coming. I think if you look at our Satrix Balanced and Satrix Low Equity Balanced Index funds on the unit trust side, you’ll see that we were already investing in global property now, I think, since 2022.

So, it’s already part of Satrix. It’s one of our investment views to invest in global property. We’ve been trying to bring this option to local investors outside of our Balanced funds for a while, and this year – sorry, in 2025, not this year – it came to fruition in December.

The Finance Ghost: Fantastic. Congrats. Don’t worry, my brain is still a little bit in 2025 as well. It’s very early in 2026, but off to a good start for the team.

Thank you, Lauren. Great start to the year. I really enjoyed this podcast. I look forward to a whole year of goodies with the Satrix team, obviously. And to you, again, just Happy New Year. To the listeners as well. Let’s get this year off to a strong start.

Lauren, I’m sure we’ll be welcoming you back before too long to talk about something else, so thank you and may your year get off to an excellent start.

Lauren Jacobs: Thanks so much for having me again, Ghost! I’m looking forward to chatting to you again this year.

And if Glencore and Rio Tinto do tie the knot, what will be excluded?

We are firmly in an environment of mining mega-mergers. We’ve seen it with Anglo American (JSE: AGL) and Teck Resources – you know, the “merger of equals” that we keep hearing about. We are potentially going to see it in Glencore (JSE: GLN) and global giant Rio Tinto as well.

And based on their market caps, if a deal does go ahead between Glencore and Rio Tinto (and assuming that not too much is carved out of the merged group and spun off), it would create the world’s most valuable mining group. That probably stings for BHP (JSE: BHG) who tried to cement their position at the top of the pile by making an unsuccessful play for Anglo.

There’s a lot going on in the sector, with the big guns all making moves to distinguish the transition metals from the “dirty” fossil fuels like coal.

Nothing is guaranteed at this stage, but Glencore’s share price is roughly 10% higher than it was before the announcement. This story will be in the headlines for a long time to come, regardless of whether it goes ahead or not. The intent for more huge mergers is clearly there.

Grindrod’s Port of Maputo investment is looking good (JSE: GND)

They handled record volumes in 2025

Grindrod highlighted a press release by the Maputo Port Development Company that paints a rosy picture. Grindrod holds a 24.7% stake in this company as part of its core logistics business.

The Port of Maputo enjoyed an all-time high in volumes in 2025, with a 3.4% increase in total tons processed. The growth rate is actually more important than whether it’s a record, but it still makes for a nice story.

Some other highlights include 6.4% growth in direct operations, as well as a 17% increase in rail volumes.

There have been important infrastructure products at the facility, including expansion to both the bulk terminal and the container terminal. Along with improvements to the logistics corridor, momentum is positive for the business.

Keeping the government happy is always an important consideration in frontier markets like Mozambique. With concession fees up by 4.5% to $48.9 million (excluding any taxes and dividends), all the port’s stakeholders are winning.

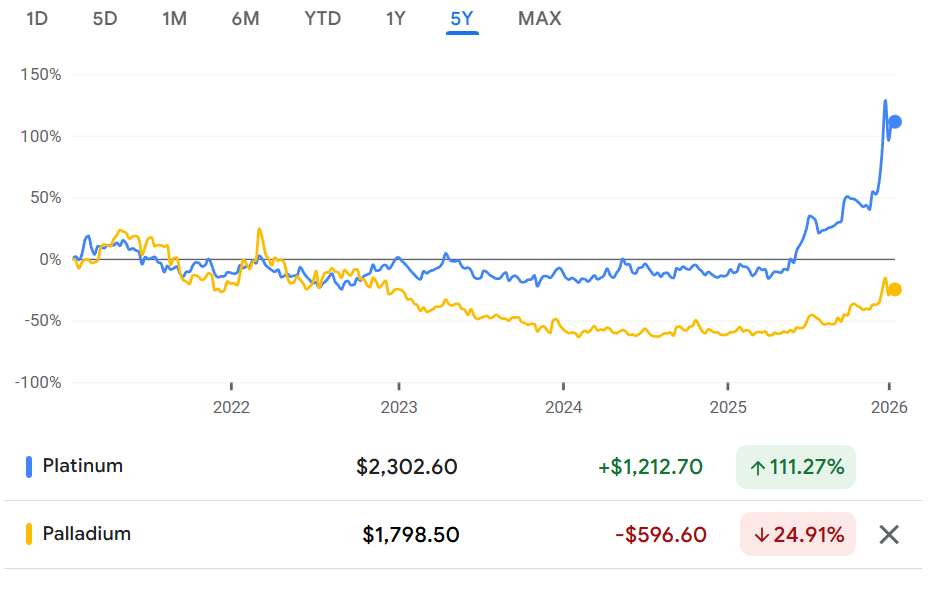

Northam Platinum produced more PGMs when it counted (JSE: NPH)

This is what you wantto see when prices are moving higher

Northam Platinum released a production update for the six months to December 2025. They achieved a 3.7% uplift in total equivalent refined PGMs, as well as an increase of 14.8% in chrome concentrate production.

Eland was the star of the show, with a 19.6% increase in PGM concentrate production and a 44.7% jump in chrome production. The only negative move across the board was a 0.4% decline in chrome production at Zondereinde.

Equivalent refined PGMs from third parties increased by 39.7%.

There are a number of projects in progress at the various mines. With prices looking more favourable, it’s a lot easier to justify capex. In fact, the market will demand that capex takes place to support production!

If you’ve ever wondered how important the PGM basket impact is (i.e. the performance over the underlying metals), check out this five-year chart of platinum vs. palladium:

You can also clearly see why the PGM names spiked so strongly towards the end of 2025!

Primary Health Properties celebrates 30 years of dividend growth (JSE: PHP)

It’s a clickbaity milestone, but an impressive one nonetheless

Primary Health Properties kept the headlines busy in 2025 with the Assura deal. The transaction created a much larger healthcare REIT that is still focused on the UK and Ireland. For South African investors looking to diversify their exposure, it’s good to have stuff like this locally available on the JSE.

The focus of a company like this will always be on paying a dependable, growing dividend. This is why it’s a big deal that they’ve just achieved their 30th year of consecutive dividend growth. Naturally, the growth rate is what really counts, as a tiny increase each year just for the sake of that milestone wouldn’t be helpful.

Thankfully, the dividend is up 2.8% on a per-share basis despite such a large acquisition having taken place. This was supported by rent reviews up 3.2% on an annualised basis, so the group is doing a good job of managing inflation. Remember that this is a hard currency play that needs to be seen in the context of developed market inflation and the trajectory of the GBP/ZAR. The cost of debt is also much lower in that market, with a weighted average cost of debt of 3.7% for the company. You therefore can’t compare these percentages to South African property funds without making allowance for the structurally different regions.

The aftermath of the combination with Assura seems to be going well. They’ve already delivered 60% of the total annualised synergies of £9 million, mainly through reducing duplicate roles and professional fees. I’m sure that the remaining 40% won’t be quite as easy.

The other challenge is to get the balance sheet back to the stage where they are within the targeted leverage range of 40% to 50%. A temporary increase in debt ratios is normal in the wake of an acquisition, with strategic asset disposals as a likely strategy in bringing debt levels back to where they want them. They’ve also already refinanced £225 million of the £1.225 billion acquisition facility, so they don’t waste any time at this place in getting things done.

Fitch currently has the company on BBB- with a negative outlook. This is based on execution risk around asset disposals, so any progress made in addressing that risk will do wonders for the credit rating and cost of debt.

Looking deeper at the performance for the year ended December 2025, rental growth on a like-for-like basis was up by 2.7%. The contributions were similar: PHP at 2.6% and Assura at 2.8%.

There is a significant development pipeline across the enlarged group. With completion dates in 2026 and 2027, the pipeline has a remaining cost to complete of £39.5 million and a yield on cost of 5.4%.

Other than a strange spike in early September 2025, the share price has been range bound for the past six months. There is some positive recent momentum though. The market tends to be cautious in the period immediately after an acquisition, although I think that this announcement will do wonders to calm those nerves.

Shuka Minerals is finally ready to move forward with its acquisition (JSE: SKA)

It’s certainly taken long enough to raise the money

You have to feel for Shuka Minerals. They’ve been put through a horrible experience by their funder, Gathoni Muchai Investments. I’ve lost count of how many announcements I’ve seen about delayed funding, despite numerous promises that it would come. The fact that the acquisition of Leopard Exploration and Mining didn’t fall through is nothing short of a miracle.

There were four announcements over the just the past few days, which tells you how closely the situation was being monitored by Shuka’s management team and the company’s stakeholders.

Thankfully, a further payment of £815k was received by the company from its funder, with teeth having been pulled to reach a paltry balance of just £1.115 million (this really is a tiny number in a corporate funding context). A further £385k is undrawn under the facility.

The other big news from a capital raising perspective is that £1 million has been raised through a share placement at 4 pence per share. That’s well below the current (illiquid) share price of R1.07, although it traded as high as R1.50 just yesterday. The bid-offer spread is wide enough that you could park all the recent SENS announcements in that gap and still have space.

There’s also an issuance of share warrants to the equity investors that could raise an additional £2 million at 8 pence per share (valid for 3 years).

What is the prize at the end of all this? Well, acquisition target Leopard Exploration and Mining brings them Kabwe, which they describe as “one of the world’s richest and most notable zinc mines” – and with a production track record going back to 1904! The mine was closed in 1994 as it had become uneconomical to run based on commodity prices at the time.

The zinc and lead resources at Kabwe are estimated to have value of over $2 billion. Naturally, you still have to get the stuff out the ground, with work having been done to establish positive expected returns.

With the funding for the acquisition in place and now additional funding raised, the company will look to undertake drilling work and associated studies (including technology that wasn’t used before at Kabwe, like gravity and magnetic studies). They also need to upgrade infrastructure. The goal is to update the resource estimate later in 2026. This will be key to securing further funding.

Shuka also owns the far less exciting Rukwa coal project in Tanzania. They reckon they can invest just $150k to achieve a staged ramp up to 5,000 tonnes per month in washed coal. This implies an IRR of 80%. $150k is literally pocket change in any corporate context and that IRR is huge. If those numbers are true, they should have no problem raising the money.

Speaking of money being raised, remember that capital raises are going to happen frequently for a company like this. Junior mining is all about reaching milestones and raising capital accordingly. Volatility is really the only guarantee.

Better production yields gave Tharisa a year-on-year boost (JSE: THA)

But the quarter-on-quarter comparison is less favourable

Mining is a difficult game. Not only do you have to navigate commodity prices that can be highly volatile, but you also have to actually produce the commodities in question! Only the latter is within the control of management, so mining houses tend to be judged on their production numbers.

Tharisa has released their production report for the quarter ended December 2025. This marks the first quarter of the 2026 financial year.

The main highlight is a substantial improvement in recovery rates (i.e. the production of PGMs and chrome relative to the reef they processed). This is important, as it can make up for a period in which total material processed was lower.

On a year-on-year basis, PGM production was up nearly 30% and chrome was down 6.7%. It would obviously be nice if both were positive, but PGMs are what counted in that quarter based on a delicious spike in the commodity price.

If you compare the December quarter results to the September quarter results (i.e. a sequential quarter-on-quarter view), you’ll find that PGM production fell 6.1% and chrome was down 14.2%. That’s obviously far from ideal, with weather and other impacts this quarter. It’s also worth noting that the net cash position fell from $68.6 million as at September 2025 to $47 million as at December 2025.

Full year guidance is for PGM production of between 145 koz and 165 koz. Although production is rarely a straight-line thing, guidance can be assessed in the context of Q1 delivering 38.8 koz. On the chrome side, guidance is for 1.50 to 1.65 Mt, with Q1 having delivered 0.35 Mt.

Nibbles:

Director dealings:

An entity associated with Johnny Copelyn, CEO of Hosken Consolidated Investments (JSE: HCI) bought shares worth R31.6 million. That’s a substantial purchase!

Prosus CEO Fabricio Bloisi’s wife bought shares in the company (JSE: PRX) worth a cool R19 million. That’s a solid show of faith in her partner!

A non-executive director of MTN (JSE: MTN) bought shares and sold them within roughly a month for a profit. The total value of the sale was roughly R1.75 million. Concerningly, clearance to deal does not appear to have been obtained.

An associate of a non-executive director of Afrimat (JSE: AFT) sold shares worth R440k.

Acting through Titan Premier Investments, Christo Wiese is back on the bid for Brait (JSE: BAT). He bought shares worth over R260k across various trades.

The CEO of Spear REIT (JSE: SEA) bought shares in his family investment vehicles worth over R121k.

Jan van Niekerk and Piet Viljoen are using Maximus Corporation as their primary investment vehicle to hold their stake in Goldrush (JSE: GRSP). A number of CFD transactions were entered into to effect this restructure. Maximus has direct and indirect exposure to 18.61% in Goldrush.

Trustco (JSE: TTO) has been trading under cautionary for ages now in relation to the company potentially going private. They’ve noted that based on the simplified listing requirements that have been released, they might rethink this decision. As always, there’s never a dull moment with them.

Labat Africa (JSE: LAB) has renewed the cautionary announcement regarding a potential AI and technology company with operations and a significant footprint within the SADC region. As for who it is, we have no idea at this stage. Remember, there’s no guarantee of a deal going ahead here, hence the need to exercise caution.

Live TV is always fun. I get a particular kick from seeing a purple ghost alongside one of the most recognised brands in finance media: CNBC.

In this interview that took place on 13th January with CNBC Africa, I spoke through the pockets of performance on the JSE in the past 12 months and some of the areas that were left behind.

Investing is always forward-looking, so it really comes down to one big question: can the JSE’s momentum in 2025 filter down into JSE mid-caps? And what should investors look out for?

I had a lot of fun doing this interview and I hope you’ll enjoy it too:

The world’s richest people aren’t always building apps or chasing disruption. Here are three stories that reveal how unglamorous industries keep minting billionaires.

If you had to guess where the majority of today’s billionaires are being made, you’d probably point to Silicon Valley, Shenzhen, or some airless room full of servers humming away on renewable energy. We’ve gotten very used to the idea that tech founders dominate the rich lists these days, usually accompanied by language about disruption, scale, and changing the world via algorithm.

But there’s another kind of billionaire building wealth far from the spotlight. These fortunes are being made in industries that are often described (perhaps a little dismissively) as “boring”. These aren’t the kinds of businesses that trend on X, yet they seem to print cash with a reliability that most tech startups would kill for. And, in many cases, they’ve been doing so for decades.

The common thread isn’t glamour or innovation in the Silicon Valley sense. It’s patience. Infrastructure. Control. And a deep understanding of problems that most people don’t find interesting enough to try and solve.

Advertising that throws its wait around

Jean-Claude Decaux was the son of a shoe salesman, which feels like the sort of detail biographers include when they’re hinting at a rags-to-riches origin story. In Decaux’s case, it mattered. At 18, he got into an argument with his father about how the family shoe store’s window display should look. Instead of backing down, he started his own business making roadside billboards.

That first venture didn’t last. In 1963, French legislation clamped down on billboard advertising, effectively killing the business overnight. Many people would have taken the loss as a sign to try something else. Decaux treated it as a design problem. If you couldn’t put advertising on roads, where could you put it?

His answer arrived in 1964. Decaux approached the city of Lyon with a proposal that now seems obvious, but at the time was quietly radical: he would build and maintain bus shelters at his own cost. In return, he’d be allowed to sell advertising space on them. And so, JCDecaux was born.

If you’re finding it hard to believe that bus shelters were only invented in the 1960s (yes, before that people really just stood outside in the elements, waiting for their bus), it just shows how well Decaux’s invention cemented itself into our daily lives. Decaux’s idea was a win-win: the city got clean, well-lit shelters without spending taxpayer money, advertisers got captive audiences, and Decaux got a business model that was hard to copy and even harder to dislodge.

This was the invention of “street furniture” advertising: bus shelters, kiosks, public toilets, an approach that later expanded into airports and transit hubs. It wasn’t flashy, but it was embedded. Once a city signed a long-term contract, JCDecaux became part of the urban fabric.

By the time Jean-Claude Decaux died in 2016, his net worth was estimated at around $7 billion. JCDecaux had grown into the largest outdoor advertising company in the world, with ads on roughly 140,000 bus stops and 145 airports. In 2023, the company reported revenue of €3.57 billion and net income of just over €209 million.

The business is still majority-owned by the Decaux family. Two of Jean-Claude’s sons, Jean-François and Jean-Charles, alternate annually as CEOs. We have to wonder whether son number three (presumably also a Jean-something) followed in his father’s footsteps and got into a fight with his old man before he could take over the family business!

The world’s richest farmer

If outdoor advertising sounds a bit dull, pig farming sounds even less promising as a route to billionaire status. And yet Qin Yinglin, chairman and president of Muyuan Foodstuff, is the richest farmer on Earth.

Qin was born in 1965 in the rural Henan province and grew up poor. When he was in high school, his father scraped together enough money to buy 20 pigs. All but one died. For most families, that would have been the end of the experiment. For Qin, it became the beginning of an obsession.

He decided to study pig farming properly, enrolling at Henan Agricultural University to study animal husbandry. After graduating, he took a stable job at a state-owned food company, an “iron rice bowl” position that promised security for life. Despite the promise of stability, he quit after three years. In 1992, Qin and his wife, Qian Ying, who had trained as a veterinarian, moved back to his hometown and started raising pigs themselves. They began with 22. Within two years, they had 2,000. By 1997, that number had grown to 10,000.

In 2000, Qin founded what would become Muyuan Foodstuff. Unlike many competitors, Muyuan invested heavily in owning and controlling its own facilities. That decision would prove decisive in the long run. When African swine fever tore through China’s pork industry in 2019, killing millions of pigs and driving prices through the roof, weaker operators collapsed. Muyuan survived (and thrived) because it controlled its breeding, feeding, and processing environments more tightly than most.

Qin was blunt about the situation. The epidemic, he said, brought “both benefit and harm”. It would wipe out small players, but it would also create opportunities for stronger enterprises to grow. Muyuan increased automation, expanded capacity, and consolidated its position. By 2023, the company was slaughtering around 65 million pigs a year. Qin’s net worth goes up and down with the pork price, but is currently sitting at a tidy $21.9 billion.