Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Bidcorp goes from strength to strength (JSE: BID)

Double-digit growth is always good news

Bidcorp is one of the best businesses on the local market. Through a combination of organic and inorganic growth, they’ve built an exceptional global food service empire. As offshore exposure goes, this is one of the best choices on the JSE in my opinion.

The share price has been erratic though. This is a function of the rand, the COVID disruptions to the restaurant and hospitality industries, as well as Bidcorp’s demanding valuation that recognises the quality of the business:

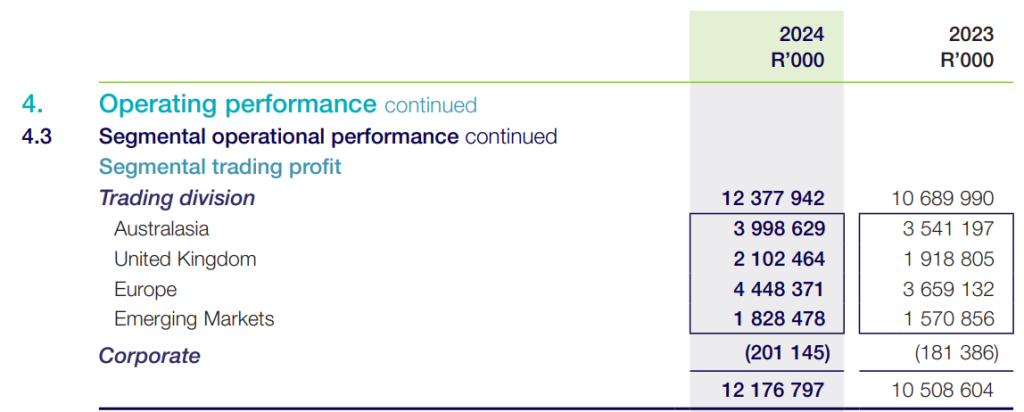

The management team is in control of the earnings, not the share price. They are doing a great job with those earnings, with the latest numbers from Bidcorp reflecting revenue growth of 15.1% for the year ended June. That translates beautifully to cash and profits, with EBITDA up by 14.4% and a cash conversion ratio of 102% of EBITDA. That’s hard to fault.

HEPS is up by 15.5%, so there are no weird once-offs driving that EBITDA performance. Thanks to the cash quality of earnings, the dividend is up 16%.

The segmental view gives a great idea of not just the diversification, but also the level of performance in Europe in particular in the latest period:

If ever you wanted to do a deep dive into the power of bolt-on acquisition strategies, Bidcorp would be a great place to do it.

Finbond makes two acquisitions in South Africa (JSE: FGL)

Buying short-term consumer lenders based in the Eastern Cape seems rather brave

Finbond is taking the rather interesting step of making acquisitions in two short-term consumer loan businesses that operate through a total of five branches in the Eastern Cape. The region is not exactly a hotbed of activity and has really struggled during the tough times in South Africa, so this is a big bet on the success of the GNU.

These businesses made a net profit before tax of R3.93 million for the year ended February 2024. This includes expenses of R4.85 million which apparently won’t be applicable after the acquisition, which isn’t uncommon for small businesses. The net asset value of the businesses is R6.75 million, so they generate a lot of profit off a small net asset base – typical of a short-term lender with constant churn in loans.

Finbond is paying R25.75 million for the deal, which seems like quite a lot even after that adjustment for expenses. Finbond’s market cap is worth R336 million, so it’s not an insignificant transaction.

Murray & Roberts is fighting hard, but there are still losses (JSE: MUR)

This has been an extremely rewarding speculative punt for those who were brave enough

The Murray & Roberts share price is up by a rather ridiculous 114% year-to-date, reflecting renewed enthusiasm around South African investment prospects and how much of this should hopefully flow into the construction industry.

For now, the share price is a much better story than the earnings. As a trading statement tells us, Murray & Roberts has certainly made improvements but is still loss-making.

Many of those improvements have come from cost-cutting exercises, with annualised savings of R100 million just in corporate costs. The full effect of those cost savings will be felt in the 2025 financial year.

The other good news is on the balance sheet, where South African debt has been reduced from R2 billion in April 2023 to R409 million as at the end of June 2024. Negotiations are underway to refinance the remaining debt. Importantly, at group level, they are now in a net cash position rather than a net debt position.

There’s still a lot of noise in the numbers, particularly due to deconsolidation of the Australian businesses. The best approach is to look at continuing operations, where the headline loss per share improved from -71 cents to a loss of between -19 cents and -29 cents.

Looking ahead, FY25 will be the first year where Murray & Roberts can really show us what the new and improved version of the group looks like. The recovery still has some way to go though, with a recovery to pre-pandemic levels of earnings only expected from 2027.

MC Mining has found itself a major investor (JSE: MCZ)

Kinetic Development Group will take a 51% stake in MC Mining

Here’s a big piece of news for MC Mining: the company has agreed that Hong Kong-listed Kinetic Development Group will subscribe for enough shares to take it to a 51% post-money stake. This will happen in two tranches.

Kinetic is a coal mining and trading group, so MC Mining’s Makhado steelmaking, hard coking coal project is of interest here and the capital will take that asset into production. There’s also enough capital on the table to help MC Mining develop other assets.

The first tranche is for a subscription of 13.04% in MC Mining for $12.97 million. It works out to around R3.72 per share, which is more than double the current share price. The second tranche for $77 million will come in after the various conditions precedent are met, which will include shareholder and regulator approvals. That is going to take a while. The parties have allowed for up to 270 days to achieve this. If it goes beyond that, Kinetic has the right to require the first tranche shares to be repurchased.

Let’s call this what this is: a great example of foreign direct investment flowing into our country. The winds of change are blowing for South Africa!

A special dividend at PPC (JSE: PPC)

PPC is paying out most of the proceeds from the sale of CIMERWA

Special dividends are interesting things. They are often rooted in disposals of major businesses, with the company’s management team showing the maturity to return the capital to shareholders rather than invest it in marginal products.

This is what is happening at PPC, with the group electing to pay a special dividend of 33.5 cents per share. Although the wording of the SENS is a bit confusing at first, this represents 66% of the cash that was obtained from the sale of CIMERWA in Rwanda.

Transpaco’s earnings and margins have dipped (JSE: TPC)

Both the plastic and paper divisions saw a drop in operating profit

Transpaco has released results for the 12 months to June and there aren’t really any highlights. There was plenty of load shedding for most of that period and very little of the GNU-inspired good stuff. For those reasons, a 4% drop in revenue and an unpleasant 15.7% decrease in operating profit isn’t the biggest shock around.

The group’s two major divisions, plastic products and paper and board products, are similarly sized – or at least, they are now. Operating profit in plastic products fell sharply from R134 million to R99 million, while paper and board products fell from R99 million to R87 million.

Group operating margin fell from 9.7% to 8.6%. A 110 basis points deterioration on what is already a fairly tight margin is significant.

By the time we reach HEPS level, the impact is slightly less severe. HEPS fell by 8.3% and the total dividend was down 7.7% as the payout ratio moved up slightly. The group is in a net cash positive position rather than a net debt position, which does wonders when earnings move lower. Share buybacks also helped improve the HEPS result relative to operating profit.

The group doesn’t exactly give the market much to hang onto in the results, with little or no commentary on the outlook. Transpaco is an illiquid counter with a wide bid-offer spread. Some additional management commentary might help address that over time, as investors would be armed with more information to help them make decisions.

Little Bites:

Director dealings:

There’s more selling of Investec (JSE: INL | JSE: INP) shares by Stephen Koseff, this time to the value of £1.2 million.

An associate of a director of Brait (JSE: BAT) – not Christo Wiese – bought shares worth R2.3 million. This is a follow up to another recent purchase by that director.

A director of Afrimat (JSE: AFT) has sold shares worth R535k.

There’s yet more selling by a director of a major subsidiary of RFG Foods (JSE: RFG), this time to the value of R453k.

For those interested in Powerfleet (JSE: PWR), the full 10Q report is now available to supplement the press release that recently came out. You can dig in here if you want all the details on the company. The US reporting style is very different and is worth checking out.

I have no idea why they are bothering, since the company is suspended from trading, but Chrometco (JSE: CMO) is going through the process of changing its name to Sail Mining Group.

The Trader’s Handbook is brought to you by IG Markets South Africa in collaboration with The Finance Ghost. This podcast series is designed to help you take your first step from investing into trading. Open a demo account at this link to start learning how the IG platform works.

Listen to the podcast using the podcast player below, or read the full transcript:

Note: examples used in this podcast should not be interpreted as advice. They are for informational purposes only.

Intro: Welcome to The Trader’s Handbook, a limited podcast series brought to you by IG in partnership with your host, the Finance Ghost. Over the course of our upcoming episodes, we are delving deep into the world of trading, helping both novice and seasoned traders alike navigate this exciting field. Join us as we unravel the intricate strategies and insights that define this dynamic landscape and the beautiful puzzle that is the markets. IG Markets South Africa is an authorized financial services and over the counter derivatives product provider CFD. Losses can exceed your deposits.

The Finance Ghost: Welcome to Episode five of The Trader’s Handbook and what an awesome podcast series this is turning out to be. Really, really enjoying it, and so are you, it seems. We’re happy with the numbers. It looks like people are opening demo accounts and making their first trades in accounts where it’s not monopoly money anymore. So, well done to you if you’re one of those people! And if you aren’t, go and check out the demo accounts and start putting some of the stuff into practice, because of course that is what makes it so fun. And we are recording this week amidst an environment of all-time highs on the JSE. We’ve had a strong rebound for stocks in general. We’ve had the rand below R18 to the dollar. Things are good in South Africa right now. Sentiment is strong. Most local stocks are rallying. The sun is kind of starting to shine. Not so much in Cape Town. More on that to come.

But let me first welcome Shaun Murison from IG Markets South Africa, our regular source of knowledge on the world of CFD trading. Shaun, thanks so much as always for doing this with me.

Shaun Murison: Great to be here again. Exciting times in the market. Like you correctly said, rand at its best levels in more than a year, we’ve had the JSE Top 40 Index trading to new all-time highs. We’re on the cusp of this easing cycle in interest rates. So, things are cautiously optimistic. Well, actually not so cautiously – more like aggressively optimistic at this stage, but markets don’t move in a straight line. So exciting times ahead, expecting a little bit of volatility.

The Finance Ghost: They are quite aggressively optimistic. You see these South African mid-caps now trading at like low- to mid-teen P/Es, where they were languishing previously at like sevens and eights. It’s quite interesting.

I’m sitting with quite a lot of listed property exposure in my investment portfolio, hoping for these rates to come down and for all of this good stuff to flow into these property owners, ultimately, especially on the retail side. It’s going to be pretty interesting to see how the next year pans out.

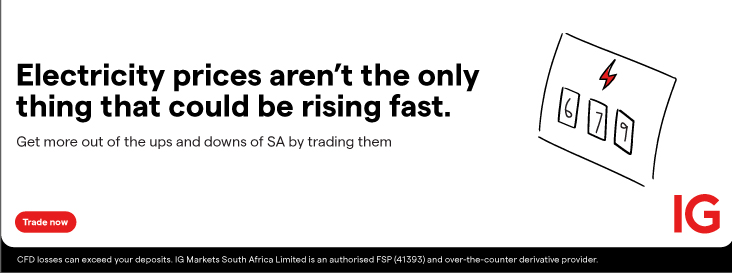

But of course, as I’ve learned in some cases the hard way, trading and investing are quite different animals. Now, listeners who have been following the shows thus far will know that one of the positions that I tried out in my demo account was to be short Mr Price.

Now this was very much based on my view that, well, I don’t think Mr Price is as strong as some of its competitors in that space. I think the valuation had gotten a little bit overcooked, and we’re going to reflect on that trade today and what I’ve learned from it, as well as perhaps a smarter way to actually go about things. But I think before we do that, for those who have perhaps made this their first podcast in the series, or still aren’t quite familiar with these terms, I think it’s always worth just spending literally a minute recapping the difference between long and short positions on a stock. The beauty of CFD trading is that you can go short. You can’t do that in your traditional brokerage account. You can only go long. So, Shaan, I’ll let you do the honours on a brief relook of long versus short.

Shaun Murison: Okay, so long, very simply, it’s the same as what you do if you’re investing. You want to buy low and sell high, obviously simplifying things. There’s a use of leverage in trading, and so we talked about the profits and losses being magnified. But when you talk about the short side of things, it’s taking a trade with a view that you expect that market to fall. When you’re going long, you want to buy low and sell high to make money. When you’re going short, you want to sell high and buy low, if that makes any sense. So essentially, in both scenarios, you need to pay less to buy something than you sell it for to make money. It’s just when you’re going short, you can do it the other way. If you think that market’s expensive, you can take a short position, you can sell it, basically borrowing shares if you’re looking at shares, you’re selling it and you’re hoping if it does come down, you can buy it back cheaper.

The Finance Ghost: So, back to the Mr Price trade. Now, I had what would best be described as a naked short – in some ways I lost my shorts, but we’ll talk about that now! And in other words, this is basically an unprotected position of being short Mr Price. I’m not long any other clothing retailers or South African general mid- to large-caps in case there’s a big rally in local stocks. I’m just sitting there short Mr Price, because I believe so strongly in that trade.

Easy with monopoly money, and that’s why I did it.

Now, it looked promising initially. Actually, I was in the green. I think we spoke about that on probably episode two, I can’t recall exactly. And at that point I should have said, thank you very much, I’ll take the profits and run. However, I didn’t. And on a naked short, I think you need to be in it pretty much for a good time rather than a long time. You can’t be too greedy because you are betting against a whole lot of things, like inflation, for example. I mean, this is such an important concept in long versus short, right? Shares are generally expected to go up over a long enough time horizon, so there’s actually no limit to how much you can lose on a short.

Whereas on a long position and if it goes wrong initially, you can kind of wait it out. But this is monopoly money in my demo account and I wanted to see how this trade would play out. Instead, as that share price moved higher and my short lost money, I added to the short and hoped that, okay, you know, I’ll get the right level, the thing will fall over and the trades will be in the money. That turned out to be a really bad call.

If you are naked short and it starts moving against you, I think you need to be very careful of fighting that momentum. The long positions, as I said, they sort themselves out over time, provided the stock is at least going up over the long term. But an ugly short that is going wrong has no limit to how much it can hurt you. So eventually I got out of the way of it. I locked in a loss in the process. So, a nice lesson learned there. I think the lessons I took from it were if you’re going to be contrarian, as I was, and as you pointed out at the time, one, you have to be nimble, which is exactly what you said. And two, don’t be stubborn and turn a small loss into a bigger loss. If you’re going to do something like that and it goes against you, then rather get out of the way. And I would definitely refer our listeners to the episode we did just before this. That would have been episode four in which we talked about what it means to have these different trading strategies to let your winners run, cut your losses, or not, as the case may be.

There may well be a smarter way to actually play these valuation dislocations. Because instead of a naked short, I could have done a pairs trade, which is quite an interesting way to play the market. And in one of your very recent newsletters, Shaun, you put out an idea for Mr Price vs. Truworths as a pairs trade. And I think before we get into the details of that exact trade, can you just explain for us what a pairs trade is? And then I think, yeah, maybe go into how that trade would actually work.

Shaun Murison: Just on the short side of what you were saying earlier on before going to the pairs stuff. You’re right. If you are short, there is no ceiling as to, you know, how far share can go up. So we have a saying, here we go: it’s better to be long and wrong than short and caught. And I think in your trade, you’re short and caught.

The Finance Ghost: Definitely short and caught. Definitely. That is precisely what happened.

Shaun Murison: Because, I mean, on the long side, a share can go to zero, but that means that if you’re on the wrong side of that, if you were long, your loss would be capped. But a way of protecting yourself in the market is basically a hedging strategy.

When we talk about pairs trading, we’re looking at taking two positions instead of one. We’re looking at taking a long position and a short position. And generally, we’ll do it with shares that are quite highly correlated. Shares within the same sector, like gold shares or platinum shares, banking counters etc. And looking at one that’s underperformed a little bit, and one that’s outperformed. The one that’s underperformed, you might look at a long position and then the one that’s outperformed, you look at a short position and you view the profit and loss from both those positions together. You’re trading one share against the other, rather than just the general macro market environment.

In my opinion, it’s a bit of a safer way to trade. You are essentially hedged in the market, and where the markets are going up or down, there’s an opportunity to make money in that pair. So, when we refer to that Mr Price trade, something that I was looking at in a Technical Tuesday newsletter which put out every Tuesday, and it is free for your subscribers if anyone is interested in that. The basic analysis there was saying that it looks like since the election time, we’ve seen quite an outperformance of Mr Price relative to Truworths. Now, they’ve both been positive, there’s been positive sentiment around both companies, both have rallied.

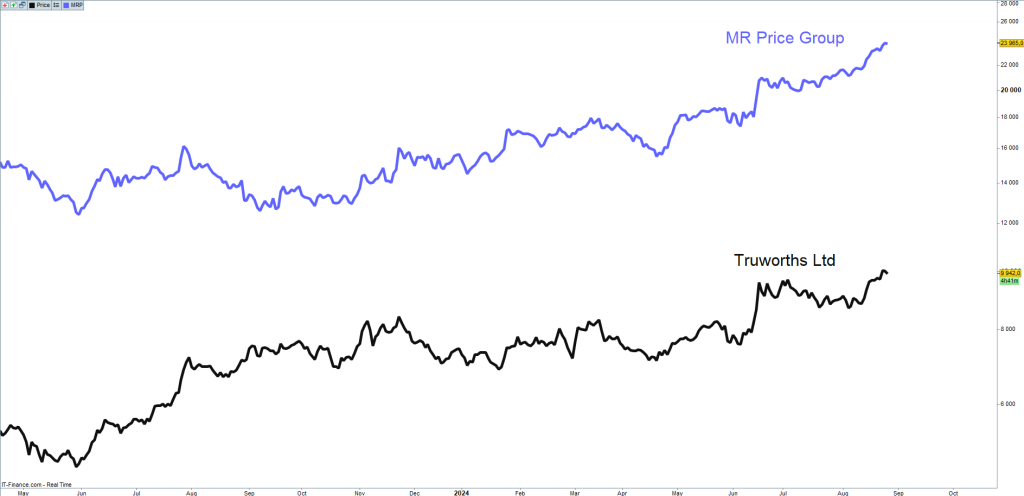

But perhaps, you know, the gains on Mr Price have gone a little bit too far relative to the gains in Truworths. We use a little technical indicator – yes, I’m using a technical analysis version for approach to the pairs trade – called the relative strength comparison. And all it is, is a ratio. It takes the share price of Truworths and it divides it by the share price of Mr Price.

And what that was telling me is that, well, Truworths has underperformed Mr Price a little bit too much over the short term. And maybe going forward, we can see now Truworths start to outperform Mr Price. It’s not saying that I think Mr Price has to come down and Truworths has to go up. It’s just saying their relationship needs to normalize, and if it does, then you’ll be making money. At the moment, that suggestion was maybe there was an underperformance of about 8% there. So, looking to make about 8% on that trade and it has started moving in the right direction, hasn’t hit the target just yet. That’s the basic premise of it.

The Finance Ghost: Yeah. And that’s very different to sitting naked short, right? Because if I think that there’s a company in the sector that is expensive, well, if the whole sector goes up, then that short can still lose money. Expensive things can get more expensive. But one of the ways to protect against that would be to go long one of the low valuation stocks in the same sector. So that if the sector gets the upswing, you would hope that the low valuation stock would get more of an upswing than the one that you’re sitting short and net net, you come out with a profit.

Would you say it’s also quite contrarian then, because you’re actually going short the winner and long the relative loser in the sector? It’s actually quite contrarian, which must be why I like it, right?

Shaun Murison: Maybe it is, it’s a bit of a mean reversion type strategy in technical analysis, there’s a lot of talk about trend following, and this is actually just deviating away from the trend following approach in trading. A mean reversion type strategy expects relationships to normalise over time. But yes, if we say there is a contrarian aspect to the type of trade, but we are still market neutral, we’re not worried about whether the shares are both going up or down. We’re trading the relationship between the two companies.

The Finance Ghost: For someone like me, who believes quite strongly in stuff like mean reversion in multiples and how important valuations are, I think pairs trading becomes really, really interesting and is a superior strategy, I think, to sitting naked short. The other mistake, of course, with that short was to just be naked short into immense South African sentiment.

And that was a good lesson learned as well: when you’re investing, which is my background and it’s long only and it’s longer term stuff, you are often rewarded by being against what the typical sentiment is. You’re buying the beaten down thing because you believe there are catalysts for it to improve at some point in the future. And then you look three, four years down the line and you’ve achieved a compound annual growth rate of 20% and you’ve beaten the market because you bought something at the right time when no one else wanted the thing.

Trading is just so different to that and it’s a lesson that you’ve got to learn by doing, which is why I’m so in favour of these demo accounts, because you’ve got to rather go and make these mistakes in a demo account than making them with real money. And a pairs trade would be a different outcome potentially for me.

I think, Shaun, let’s go into the costs of a pairs trade because this is obviously really, really important, right? You’ve got to look at your net return after costs because otherwise you might not be making any money at all. So, what are the costs of a pairs trade? There are actually two legs to this trade. Presumably it costs roughly double what it would cost you to just go with one leg of the trade. I think let’s run through that.

Shaun Murison: Yeah, so the costs don’t change in terms of how IG prices things. Entry level cost, commission on a position, you’re looking at 0.2% or R50 on a trade, and that’s each leg. Like you correctly said, when you start looking at a pair trade, you are essentially insuring yourself a little bit in the market and you’re doubling up on your position. Your cost does increase, which is, I suppose, the premium for, I would say, reducing your risk within the market, but so you’d pay that 0.2% on both legs. Let’s go back to that Truworths – Mr Price position. You’d be paying 0.2%, so on a R50,000 position you’d be paying R100 for the trade. But if you’ve got two of those, so now you’ve got two R50,000 positions, that’s another 0.2% and that would be another R100. And obviously you pay that when you enter the trade, and you’re going to pay that when you exit the trade. That’s your barrier to making a profit.

The Finance Ghost: Look, we definitely shouldn’t create the impression that a pairs trade is guaranteed to work, because of course, this is a trade with two legs. And that means technically, if you get both wrong, you can lose money twice as quickly if your short goes against you and your long goes against you.

In other words, if you believe that one share is expensive and one share is cheap, and that gap should close, but instead it opens – the winner keeps winning and the loser keeps losing – and you’ve now gotten the wrong way around, that gap can just keep widening. A great example on the international market would be something like Costco versus Walmart. I can imagine there were many times where someone looked at this and said, sure, Costco is crazy expensive, Walmart is looking cheap in relative terms, let me go long Walmart, short Costco. If you had been sitting short Costco at any point in that journey, you have been absolutely killed. That gap has just opened and opened and opened between the two. It’s actually now the biggest I think it’s ever really been in terms of the gap in valuation multiples.

That’s a very tempting one to say, okay, great, do the pairs trade, but it can just keep going. You just don’t know. So that’s obviously a challenge.

One of the ways to mitigate risk that we’ve talked about a lot in these podcasts is the use of stop losses. They’re probably a little bit more complicated in a pairs trade than they are in a normal trade. I think let’s just work through how stop losses work in the context of a pairs trade. Do they work? And is it something that you have to think about differently?

Shaun Murison: Okay, so when you’re trading, you’ve got to manage your downside risk. We’ve talked about that at length. And when we talk about a stop loss, it’s really about admitting when you’re wrong. We’re not going to get it right every time, especially when you’re trying to tell the future. That’s essentially what we’re doing with trading, aren’t we? We’re trying to tell the future. In a conventional trade, what you’re going to do is you’re going to have a look at what I want to buy here if it hopefully it moves in my favour and I’ll look to take profit there. But you know, if it goes against me, where am I prepared to accept that I’m wrong and take my loss? And that’s obviously what we refer to as a stop loss. Now when you’re trading on the IG platform, essentially you have the feature of being able to put in a stop loss into the system to automate that process. You don’t have to be in front of your computer the whole time. And if the market, you know, you’re at work and the market moves against you, it would pre-determine your loss and would kick you out of the trade. Now when you do look at something like a pairs trade, that does change a little bit. It does become a little bit more complicated because you don’t know how things are going to correlate. If you are taking two positions, you’ve got a long and a short in the market, in a perfect world, you want your long to go up and your short to come down. So you’re making money on the long and you’re making money on the short is what we call double alpha positive.

But quite often that’s not the case. It’s quite often you’ll find that both shares, because they are correlated and you know what’s happening in the macro environment, you might find that they both go up. And in that situation you want the position that you are long to go up quicker than the position that you’re short so that you make more money from the long than you’re losing from the short. And remember, we net those two positions off. Or alternatively you could have both share prices falling. In that situation to make money, you want the short to fall quicker than your long. So you make money on the short, you’d be losing money on the long, but when you net those positions together, hopefully you’d be profitable.

Now when we talk about a stop loss, we don’t know in pairs trading how that market’s going to correlate. For the example of Truworths vs. Mr Price, now that has started to work and has started to move in the right direction, but both of those shares have gone up. So, you’re losing a little bit on the Mr Price short, but you’re making on the Truworths long because you don’t know how that’s going to correlate. It’s hard to just put a stop loss in the system to try protect your risk.

You should still manage your risk, but I think in a pairs trade, you manually exit the trade. You might say to yourself, well, I’m prepared to lose, let’s say 3% in that trade, and then you just need to monitor that position and then say, okay, well, it’s breached my levels. And then you’d exit both trades at the same time. So still need to manage your risk, still need to manage that downside risk. And because if they do revert back to the mean, we don’t know how that’s going to happen. So, yeah, it’s a manual exercise of stop loss in that situation.

The Finance Ghost: And of course, position size is the other great risk management tool, right? It’s one thing to have stop losses, but if you go and put in this big position relative to not just your portfolio, but also your own ability to potentially lose money, and I think that’s maybe a concept that we don’t talk about enough. It’s not just relative to the size of your portfolio, it’s your value at risk. And you talked on the previous podcast about looking at stuff like the volatility in each stock, the average moves that it can make. It’s a very nice way to go and assess the risk. Look at those two charts and say to yourself, okay, how much do they typically each move? What is my risk in this trade? And then get the sizing right. I mean, that’s got to be another important risk mitigation tool here?

Shaun Murison: Yeah, so exactly what you’re saying. Position size is a function of stop loss. So, you always look at how much we’re going to risk per share, but you also need to determine the total risk of your account that you prepare to risk in any one trade. General guidelines, you know, between 1% and 5% of your account size in any one trade, but it really is up to you. You have to predetermine that, obviously, if you’re going too big into the market, your position sizes are too big, then you don’t give yourself that much breathing room. Now, when you’re looking at peer trades, you look at more or less equal position size. You’ve got a 100,000 position on the long, 100,000 position on the short. And I think if you are getting started out there, I always suggest taking smaller positions and having maybe slightly wider stops just so that we can actually give those trades a little bit of breathing room. Because quite often they don’t move immediately in the right direction. Sometimes they go against you before they move in the right direction, if they do move in the right direction, which is obviously the goal.

The Finance Ghost: Speaking of the sort of mistakes that can be made, and me getting it wrong in my Mr Price short, here’s another fun mistake. Always good to learn. So, I wanted to do a pairs trade in the last week of short Italtile, long Cashbuild, going and picking the downtrodden one. Italtile and Cashbuild, there are a lot of good reasons why they should move together as South African consumer discretionary spending improves, etc. I’m actually long Cashbuild in my vanilla equities account for what it’s worth. But obviously to do pairs you need CFDs, but also you need both of those instruments to be available. So instead of checking that they are both there, I just assumed they both would be. I put on the short for Italtile and then I was rather horrified to find that Cashbuild was not available on the system. This left me, guess what, naked short Italtile! Yay, me! The joy of a demo account and practicing.

So why is that the case sometimes, where you actually just don’t have a stock on the system? Obviously a pairs trade kind of requires two, as the name suggests. The lesson here being to check both legs of a trade before pulling the trigger. But I think it’s good to understand why sometimes there just isn’t availability on the platform.

Shaun Murison: Okay, so when you start trading leverage instruments, you want shares to have high levels of liquidity. And so generally shares that have lower level of liquidity, we won’t offer, just because they become a lot more volatile when you’re crossing the spread. You can see sharp sudden movements and it’s just a higher risk to the client and obviously higher risk to our books.

We offer the most liquid stocks. I don’t have the exact figure here, but it’s at least 200 of the more liquid stocks on the JSE, if you’re looking at the local market, ones that we think are suitable for short-term trading, and it’s gauged by risk and liquidity. There are some securities that won’t be available and they would be those smaller cap shares.

The Finance Ghost: Yeah, that does make sense. The lesson in this is always check, especially if you’re going to do a pairs trade. Don’t go and do one instrument and then potentially not the other.

I think, Shaun, this brings us to the end of episode five. I think it’s been another goodie in what is really a great series. I think pairs trading is just a great way to go and express your views on relative valuations and to actually look for the opportunities out there. And you can’t do it without being able to go short. And that, of course, means CFDs. So, the only way to see this for yourself, honestly, is to get that demo account open. You might think, oh, you know, I don’t want to try it or I’m going to go straight into the real deal. Just look at some of the silly mistakes I’ve made in my demo account. I can almost guarantee you’ll make other silly mistakes or different ones. You know, maybe you won’t, in which case you’re lucky. But why take the risk? Go and try it out. Go and get used to the system. Go and make those mistakes without real money. And then you’ll know for sure if this is something you want to dabble in, and then you can do it with the stuff that actually counts.

I would also put out there that if you are listening to this series and you’ve got questions that come up or you wish we covered something, send it through to us. You can contact me on X, which used to be Twitter, or you can contact me through Ghost Mail. You can reach out to Shaun on the various social platforms or the team at IG. Let us know what you’d love us to cover. There are still several podcasts in this series, and we would love to be responsive to your questions and sort of build them into what we’re going to cover.

Thank you for listening. We look forward to having you here on the next one, Shaun. And to the listeners, we look forward to welcoming you back for episode six when that launches. This has been episode five. Go check out the others that we have. Thank you.

Shaun Murison: Awesome. Thanks.

Outro: CFD losses can exceed your deposits. In our gorgeously diverse country, there really is a new reason to trade every day. Current affairs to political news can make the markets move and cause volatility, which can be advantageous to a trader. Diversify your portfolio by opening a trading account with IG and explore the possibilities of CFD trading or practice your trading skills on an IG demo account.

The Ghost Wrap podcast is proudly brought to you by Forvis Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Forvis Mazars website for more information.

This episode covers:

Italtile had a better second half as expected, but new risks have emerged.

ADvTECH and STADIO have shown us that private education can be lucrative, provided the business model is right.

Harmony got its gold production sorted at exactly the right time.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

BHP is such a good example of how mining cycles play out (JSE: BHG)

The bumper profits of 2022 are now a distant memory

Mining cycles are wild things. We can see this quite clearly at BHP, where diluted headline earnings fell from $22.2 billion in 2022 to $13 billion in 2023 and then $9.9 billion in 2024. That’s quite the drop, which is why mining cycles are only for those with strong stomachs.

The shape for EBITDA is similar other than in the latest year, with underlying EBITDA decreasing from $40.6 billion to $28 billion and then up to $29 billion in the latest period. You can see that the EBITDA vs. headline earnings disconnect happened in 2024. One of the reasons for the gap is that net debt has increased from $333 million in 2022 to $9.1 billion in 2024, at a time when interest rates are much higher. Remember, EBITDA is a measure of earnings before interest costs – in fact, that’s where the first part of the acronym comes from!

Looking at free cash flow for total operations, this dropped from $25 billion in 2022 to $5.6 billion in 2023 and then increased to $11.9 billion in 2024. In a capex-heavy business model, free cash flow tends to have far more volatility than earnings.

In a group as diversified as BHP, we need to look deeper to see what’s really going on in the major commodities produced by the group.

In the copper operations, we find a promising story of EBITDA up by 29% and underlying return on capital employed of 13%. They expect to deliver 4% growth in production in the coming year after two years of 9% growth.

In iron ore, EBITDA was up 13% and return on capital employed was a meaty 61%. This is the joy of owning the lowest cost major iron ore producer globally in the form of Western Australia Iron Ore.

Coal EBITDA was down 54% but is thankfully a smaller part of the group. Return on capital employed was 19%, which is still decent.

In terms of outlook, BHP flags major uncertainty around China – no surprise there. They also note India as a bright spot for commodities, with significant growth there.

Brimstone’s intrinsic NAV has gone backwards since December (JSE: BRT)

In an investment holding company, this is the key metric

Investment holding companies tend to recognise some investments as associates and others as subsidiaries, leading to all kinds of weirdness in the accounting. I prefer to look past all of that and focus on net asset value (NAV) per share, as this tells you whether the investment portfolio went up or down in value.

Looking on a per share basis is also important as it takes into account any share repurchasing activity, which is value accretive when the share price trades below NAV – as it literally always does. It’s therefore good to see that Brimstone reduced debt and executed share repurchases in this period.

Still, the intrinsic NAV per share fell 5.7% from December 2023 to June 2024, coming in at R11.436 per share. Brimstone trades at R5.70, so there’s the discount I was talking about. The biggest problem has been Sea Harvest, where the share price has been under pressure. You’ll find the results from that company further down, as Sea Harvest is also listed.

Master Drilling has flat profits – but watch those impairments (JSE: MDI)

You can’t always ignore the stuff in EPS rather than HEPS

The most common difference between Earnings Per Share (EPS) and Headline Earnings Per Share (HEPS) is that EPS is net of impairments and HEPS is not. An impairment is based on an assessment of the value that can still be derived from an asset. If that value is lower than the carrying amount on the balance sheet, an impairment or write-down must be recognised.

Sometimes, impairments aren’t very important. They often relate to assets that probably should’ve already been impaired a while ago. At Master Drilling though, the impairments in this period caught my eye as they relate to reverse circulation and mobile tunnelboring equipment – assets that are important sources of revenue. Due to uncertainty in the broader market, they’ve recognised a vast impairment in this period of $13.3 million.

Above all else, this is a reminder of the technological and market risks facing Master Drilling. If these impairments become a regular feature at the company, then it negatively impacts the business case. With 55% of capex on expansion and 45% on sustaining the existing fleet, they are constantly adding to the equipment and taking a view on what the demand for it might be.

The company reports in US dollars and revenue is up 17.3% in that currency, so it was a strong period aside from the impairments. Alas, increases in operating expenses ate up pretty much all the uplift in gross profit, with higher finance costs adding to the pain. Measured in US dollars, HEPS fell by 3.2%. Measured in rand, HEPS fell only 0.5%.

To add to the difficulties in interpreting this result, net cash from operating activities more than doubled from $12.2 million to $27.7 million. Master Drilling doesn’t pay an interim dividend, so we will have to wait for the full year results to see how the cash picture translates into distributions to shareholders.

Some signs of life at Pick n Pay (JSE: PIK)

Oddly, the franchise stores are now underperforming corporate-owned stores

Pick n Pay has raised capital from the market and now needs to deliver the turnaround strategy. They have their work cut out for them, especially with a gorilla like Shoprite in the room. Still, there are some signs of improvement coming through.

You won’t see much good news in the 26 weeks to 25 August unfortunately, with a trading statement noting that HEPS will be at least 20% lower for the period. The benefit to the balance sheet of the rights issue will only start to be felt in the second half of the year, as the capital was raised recently. This is why net finance charges are R180 million higher year-on-year. As expected, Boxer has grown headline earnings for the period and the troubles at Pick n Pay have more than offset that growth.

One of the problems is that gross margin is under pressure, as they’ve had to be aggressive on price to win shoppers back and compete against the likes of Shoprite. The diesel savings from lack of load shedding have been reinvested in price. I’ve written a few times this year that Eskom gave Pick n Pay a get-out-of-jail card this year. Had load shedding still been in place, I genuinely am not sure how they would save this thing.

To deliver a better full year result, they are expecting a much better performance from Pick n Pay. In the 21 weeks to 21 July 2024, they could only manage like-for-like growth in PnP SA Supermarkets of 2.0%. This excludes standalone clothing stores. Company-owned supermarkets grew 3.6% and franchise supermarkets were down 0.8%, a surprising underperformance from the franchise business. These are still really poor numbers, especially vs. a weak base. Boxer grew 13.5% overall and 9.5% on a like-for-like basis, showing us what a successful retail format can do.

In case you’re curious, standalone clothing stores grew 10.3% overall but only 0.7% on a like-for-like basis.

I think that a turnaround of Pick n Pay, if it ever really happens, will be harder and take longer than most people expect. It’s extremely tough to get this right.

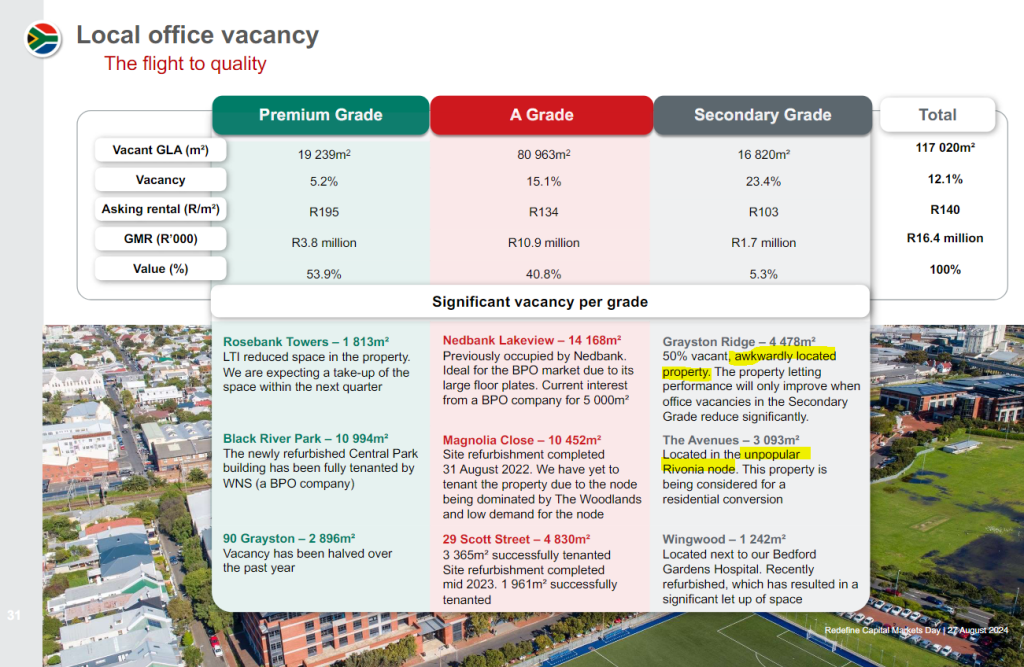

Redefine has made the capital markets day presentation available (JSE: RDF)

If you’re interested in the property sector, this is a great document to work through

I always enjoy it when a listed company hosts a capital markets day and makes the presentation available to everyone. The Redefine presentation is incredibly detailed and tells the story of the evolution of the portfolio over the past few years.

It also has gems like this slide, which surely wins an honesty award (and gives great insight into the office market):

If you can make the time to just flick through the presentation, I guarantee you’ll learn something new. You’ll find it here.

Sasfin has managed to pull off the acceptances condition (JSE: SFN)

The biggest hurdle to the deal is now out the way

The offer of R30 per share to Sasfin shareholders came with an unusual condition that holders of no more than 10% of shares in Sasfin can accept the offer in order for it to be valid. In other words, holders of 90% need to agree to hold the shares into a private environment.

Sasfin managed to get it right, with irrevocable undertakings from holders of more than 90% of shares that they will not accept the offer, thereby meeting the condition and allowing the deal to continue.

The next step is that Unitas and Wipfin as the take-private partners will subscribe for shares in Sasfin Wealth. This will allow Sasfin Wealth to fund the offer being made to shareholders in Sasfin.

A circular will be distributed to shareholders in due course.

Also, the international revenue mix is considerably higher

Sea Harvest has released results for the six months to June 2024. Revenue was only 3% higher, so that’s not a great start. International revenue is now 53% of the total, up significantly from 45% in the comparable period.

Thankfully, gross profit was up 22% as gross margin moved from 24% to 29%. Operating profit was up 23%, yet earnings before interest and tax (EBIT) was only 6% higher.

We then get to the uncomfortable numbers, dragged down by higher net finance costs (up from R104 million to R128 million) and taxes (up from R48.5 million to R60.7 million). This resulted in attributable profit after tax dropping by 17% and headline earnings decreasing by 32%.

To add to the negative move for shareholders, Sea Harvest has more shares in issue than before and hence HEPS fell by 36%. Not a great outcome at all.

Looking ahead, the acquisition of 100% of Terrasan’s pelagics business and 63.07% of Terrasan’s abalone business closed on 14 May, so that should be a major contributor to the coming year provided things improve in the abalone market in particular. They need it, as catch volumes in the hake business in South Africa have been under pressure, leading to the relatively higher contribution from international sources than before.

The share price is down 15.9% over the past year.

Stor-Age still has a growth story to tell (JSE: SSS)

If only the valuation wasn’t so demanding

Stor-Age is a solid REIT and the market knows it, which is why it trades on a yield of just 8.4%. On such a fully priced yield (remember that a low yield means a higher share price), there hasn’t been much share price growth for investors. Over three years, the price is only up 2%!

There’s not much growth in the mature side of the business, but things are still in the green. In the owned portfolio, occupancies are up 2.8% year-on-year for the four months to July. Although the South African portfolio has seen occupancies fall since March i.e. a year-to-date view, this is largely due to seasonality and they expect things to pick up after winter. This is why the year-on-year view is so important. In the UK, occupancies were up 4.7% year-on-year vs. 2.3% in South Africa, so they are growing quickly in that market.

We do need to dig deeper though, as there are other important metrics. In same-store occupancy in the UK joint venture portfolio for example, occupancies are down 1.2% year-on-year. They have huge room for ongoing expansion of the footprint though, as we can see in the total growth in occupancies in the UK joint venture portfolio of 13.7%.

All of these occupancy growth rates are based on square metres i.e. actual metres occupied, not occupancy as a percentage of total space.

Of critical importance is the growth in rental rates. This is the other part of the growth algorithm along with the amount of occupied space. They have achieved 8.4% growth year-on-year in South Africa and 1.9% in the UK on the same basis. You can see how inflation has started calming down in the UK.

Another crucial part of the investment thesis is that the acquisition and development pipeline remains extensive.

In South Africa, they recently acquired Extra Attic in Airport Industria, Cape Town for R73 million. The developments of the Kramerville and Century City properties were recently completed. In Sunningdale in Cape Town, they are enjoying the explosive growth in the area and the property that was completed in 2021 has delivered a predictably strong performance. To squeeze more juice out of the area, they’ve agreed with Garden Cities to acquire another hectare of land adjacent to the existing property. Development on that land in only in the planning phase at this stage.

In the UK, there are two major developments underway with the joint venture partners. Interestingly, Stor-Age reduced its shareholding in one of the developments by selling shares and using the proceeds to fund the proportionate share of the development. In other words, they opted not to send further capital to the UK to fund the development.

In further news on the balance sheet and dividend strategy, Stor-Age has received strong shareholder support to reduce the dividend payout ratio from 100% to between 90% and 95% of distributable income.

I would love to hold shares in Stor-Age again, but not at these yields. It’s literally priced for perfection and that’s why total returns over the past three years have been underwhelming. Great company, wrong price for me.

WBHO expects an improvement in HEPS (JSE: WBO)

The trading statement is light on details, but at least earnings are up

Construction group WBHO has released a trading statement for the year ended June. The great news is that HEPS is up by between 10% and 20% for continuing operations, coming in at between R18.73 and R20.44 per share. For total operations, it’s up by between 25% and 35% at a range of R18.94 to R20.45.

They haven’t given any further details at this stage, other than confirmation that results are due on 10 September.

Little Bites:

Director dealings:

Stephen Koseff has sold more shares in Investec (JSE: INL | JSE: INP), this time to the value of £544k.

An associate of a director of Brait (JSE: BAT) bought shares in the company worth nearly R2.2 million. Separately, Titan Premier Investments (the vehicle linked to Christo Wiese) bought shares worth just over R2 million.

Andre van der Veer (not Andre van der Veen of A2X fame as I initially thought) and his wife bought shares in NEPI Rockcastle (JSE: NRP) worth R368k.

A non-executive director of Hammerson (JSE: HMN) bought shares worth £8.5k.

The family trust of a director of a major subsidiary of RFG Foods (JSE: RFG) sold shares in the company worth R37k.

Vodacom’s (JSE: VOD) court battle around the Please Call Me matter continues, with the Constitutional Court agreeing to hear the company’s application for leave to appeal in the matter in tandem with its appeal against the Supreme Court of Appeal judgment. It all comes back to the amount that should be paid to Kenneth Nkosana Makate, with the Vodacom CEO having offered R47 million and Makate fighting for more in court.

Lighthouse Properties (JSE: LTE) has confirmed that the scrip distribution reference price is a 3% discount to the spot price on 26 August, so they are providing a small incentive to shareholders who choose to receive shares rather than cash.

Insimbi Industrial Holdings (JSE: ISB) released a trading statement noting that HEPS will be down by at least 20%. That’s the bare minimum disclosure required by the JSE, so it’s anyone’s guess how bad it could be. This is for the six months to August, so the period isn’t even over yet. Buckle up!

There’s a significant recovery at Workforce Holdings (JSE: WKF), where HEPS has jumped from 1.7 cents to between 12.43 cents and 12.77 cents for the six months to June. We don’t need to bother with noting the percentage move on a jump like that! It’s more important to go back and compare this to previous years. Sure enough, HEPS for the six months to June 2022 was 14.6 cents, so this performance is still not a full recovery to previous levels after a terrible time in 2023.

Jubilee Metals (JSE: JBL) has secured a private power purchase agreement in Zambia. The counterparty is independent solar and hydro power producer Lunsemfwa Hydro Power Company, with the deal designed to meet the total power needs of Roan and Sable. There’s also room for expansion, with discounted rates locked in for a further 10MW of solar power if Jubilee needs it. Roan has previously been impacted by power shortages, so they are taking advantage of a decision by the Zambian government to allow the private sector to provide power.

Southern Palladium (JSE: SDL) has announced that the combined UG2 and Merensky Reef Mineral Resource is now 35% up from the previous estimate. Two separate independent consultants have audited the mineral resources data. The pre-feasibility study is underway and scheduled for release in Q4 of this year.

Vunani (JSE: VUN) renewed its cautionary announcement regarding the potential disposal of a minority shareholding in a subsidiary. They haven’t indicated which subsidiary and there’s still no guarantee that a deal will go ahead.

There’s truly never a dull moment at Trustco (JSE: TTO), with the latest being the discovery of an “exceptional diamond” by Meya Mining, in which Trustco has a 19.5% interest. Long story short, they found a 391.45 carat diamond, which isn’t the biggest ever found in the region (that honour belongs to a 770-carat diamond found in 1945), but is certainly a large and very economically helpful diamond. Trustco flags that in its valuation of the asset going forward, they may look to take into account the number of exceptional finds in the area. Like I said: never a dull moment.

Reinet Investments (JSE: RNI) announced that the proposed dividend of €0.35 per share was approved by shareholders. The exchange rate to rand will be announced in due course.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

ADvTECH signs off on another strong period (JSE: ADH)

These numbers look great

ADvTECH has released results for the six months to June 2024 and there’s a lot to feel good about. Revenue is up 9%, operating profit increased by 15% and HEPS put in a 16% increase. When you’re looking for your equity investments to deliver real growth i.e. ahead of inflation, these are the types of numbers you want to see.

The interim dividend of 38 cents per share is 26.7% up on the prior year, so there’s a bump in the payout ratio as well.

Perhaps best of all, operating margins have increased in each of the underlying divisions. Schools Rest of Africa is quite the story, with operating margin up 400 basis points to 28.7%. That’s higher than Tertiary at 25.8%, Schools South Africa at 20.3% and the relative ugly duckling in the group, Resourcing at 6.3%.

I think they would unlock an even better valuation multiple if they sold the Resourcing business and made themselves a pure-play education business.

Harmony expects HEPS to more than double (JSE: HAR)

Some of this is a weak base, but well done to them for improving when it mattered

The gold sector has dished up remarkable variability in earnings performance this year. If you haven’t seen it before, this has been a great time to learn that the miners and the commodity don’t always perform equally. In fact, they rarely do.

Harmony has released a trading statement for the year ended June that reflects an expected increase in HEPS of at least 100%. In other words, it will at least double!

We will only get full details when results are released on 5 September. The delay is due to auditors needing to complete their work related to an undeveloped property. In the meantime, we know that production was 6% higher and ahead of guidance, supported by higher recovered grades. All-in sustaining costs increased by 1%, so you can quickly see how margins opened up and profitability jumped.

It’s not all perfect harmony though, with an impairment of R2.8 billion at Target North based on mineral resource estimates that suggest a lower recoverable amount vs. the carrying amount in Harmony’s books.

With a market cap of R117 billion and a share price that is up nearly 150% in the past 12 months, I don’t think investors will pay too much attention to that impairment.

Italtile has flagged a dangerous competitive environment (JSE: ITE)

The market doesn’t seem to care, based on recent share price momentum

With GNU-phoria having found its way into Italtile along with many other local stocks, the share price is up 36% over 90 days. Despite Italtile releasing some tough numbers and even tougher commentary early in the morning on Monday, there was no stopping the positive momentum.

With flat system-wide turnover, trading profit down 11% and HEPS down 7%, there’s not much to feel good about here. The ordinary dividend is down 8% for the year to June as well.

The market seems to be clinging to the second half performance at Italtile, which was better than the first half but by no means good yet. Trading profit for the second half was still slightly down year-on-year.

I would be cautious here, as Italtile has noted the emergence of aggressive new competitors and a situation where manufacturing capacity far exceeds demand. Manufacturing businesses have high fixed overhead structures, so depressed volumes lead to higher overhead absorption per unit and a substantial negative impact on profitability. Although I’m now sitting long Cashbuild in my portfolio, they don’t have the same manufacturing exposure that Italtile does. Also, perhaps even more importantly, the Cashbuild share price had been sold off sharply before I climbed in, having now made a full recovery and delivered me a delightful little return.

Based on how much cash there is on the balance sheet (up 76%), Italtile has declared a special dividend of 78 cents, which works out to 6% of the current share price. The total dividend is thus 127 cents. That’s clearly not the sustainable yield though. It’s interesting to note the confidence to pay this dividend when there is still so much uncertainty in the market. On one hand they are telling the market to be careful of lost market share and essentially a price war in the local market, while on the other they are paying out excess cash.

There’s also an interesting note around the energy requirements at the Ceramic business. Currently, 70% of energy requirements are provided by Sasol as the primary supplier of imported piped natural gas. Sasol will only be able to supply this energy until June 2027, so Italtile is looking for alternatives like natural gas and coal-based synthetic gas.

STADIO’s numbers are heading the right way (JSE: SDO)

The shape of the income statement looks good as well

STADIO has released results for the six months to June and they look strong. Right at the top, we find that student numbers increased 10%, revenue was up 16% (so pricing increased were also achieved) and EBITDA grew by 12%. Although there’s a bit of EBITDA margin pressure there (as the percentage growth is lower than revenue growth), core HEPS was up 20% and there’s much to celebrate.

Within these numbers, the acquisition of an additional 15.4% in Milpark Education is relevant. The non-controlling interest there is down from 31.5% to 16.14%, so STADIO is close to owning the entire thing now.

STADIO doesn’t pay an interim dividend, so don’t be shocked to see that there isn’t one this year either. With these numbers, there is seemingly a strong probability of an annual dividend. With no external debt at all, the strength of the balance sheet would certainly support a dividend.

Interestingly, there’s a resurgence in contact learning as things have truly normalised after the pandemic. Contact learning numbers grew by 9%, having grown just 3% in the prior year.

Little Bites:

Director dealings:

The family trust of a director of a major subsidiary of RFG Foods (JSE: RFG) sold shares worth R1.33 million.

A director of a major subsidiary of Vodacom (JSE: VOD) sold shares worth R564k.

Burstone Group (JSE: BTN) has renewed its cautionary announcement around a potential strategic partnership with funds advised by Blackstone Europe. There is still no certainty at this stage that a transaction will be concluded, hence the need for caution.

Lighthouse (JSE: LTE) has disposed of another R1.45 billion worth of shares in Hammerson (JSE: HMN)

Gold Fields (JSE: GFI) announced that Phillip Murnane has been appointed as CFO. He takes over from Alex Dall, who has been interim CFO since 1 May 2024 after the departure of Paul Schmidt.

Salungano Group (JSE: SLG) renewed the cautionary announcement related to Keaton Mining, where the hearing date for the application for leave to appeal against the judgment that dismissed the business rescue application is still being awaited.

Chrometco (JSE: CMO) has renewed its cautionary announcement regarding a material subsidiary. The stock is suspended from trading, so it’s not like anyone has the temptation to trade it anyway.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

African Rainbow Minerals suffers a sharp drop in earnings (JSE: ARI)

PGM and thermal coal prices dragged earnings lower

African Rainbow Minerals has released a trading statement for the year ended June 2024. HEPS took a proper knock, down by between 40% and 50%. A drop of this extent isn’t unusual in the mining sector at the moment, as some commodities have come off severely in price.

PGMs and thermal coal were the culprits for African Rainbow Minerals, with higher average realised iron ore export prices helping to mitigate some of the pain. Detailed results are due on 6 September, so we will get all the insights soon.

Despite the decline in earnings, the share price is surprisingly flat over 1 year – admittedly with plenty of volatility along the way.

Alphamin has released its detailed interim financials (JSE: APH)

We already knew from previous announcements that Q2 was a record for tin production

With Alphamin on such a growth path, it’s not surprising to see that the management team includes quarter-on-quarter comparisons as well as year-on-year. Typically only high growth companies will compare quarters sequentially, rather than just year-on-year.

The growth rate over the past year is immense, with revenue up 37% year-on-year for the second quarter and operating profit up 63%. Net profit over that period increased by 27%.

If we compare the second quarter to the first quarter, then revenue dipped 5% but operating profit was up 5%. After various other moves, including some major tax line items, net profit was down 10% quarter-on-quarter. It may be high growth, but very few companies can grow every single quarter.

With Q2 as a record for production, it might puzzle you that revenue dipped from Q1 to Q2. The clue is in the word “production” which isn’t the same as tin sold. They actually experienced a 21% drop in sales vs. a 28% increase in production, so they will need to play catch-up there. If they are lucky, tin prices will stay elevated, as the average tin price was up 20% quarter-on-quarter and 26% year-on-year.

The company expects tin sales in Q3 to exceed tin production by around 500 tonnes, which would recover more than half of the differential between production and sales in Q2.

Alphamin’s share price is up 15% over the past 12 months and 23% year-to-date.

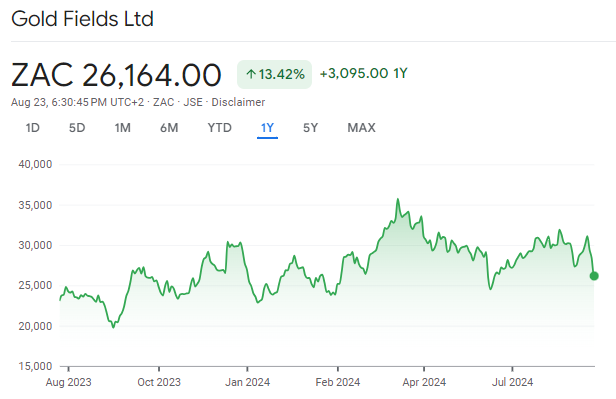

A rough day for Gold Fields shareholders (JSE: GFI)

An upward move in the dividend payout ratio couldn’t stop the bleeding in the share price

The gold miners have been such a mixed bag recently, despite the more appealing gold price. This is a good lesson on the volatility when you buy the miners rather than the commodity itself, as plenty can go wrong on the production side. We’ve seen that play out at Gold Fields, where production for the six months to June 2024 is down by 20% year-on-year. Ouch.

When volumes drop like this, even for reasons outside of the company’s control (like the weather), there’s inevitably a major knock-on impact for unit costs. Mining has substantial fixed costs, so lower production volumes mean higher overhead absorption on a per-unit basis. All-in costs were up 47% to $2,060/oz, so the 14.7% increase in the dollar gold price was ruined by the jump in costs of production.

The net impact is that HEPS from continuing operations fell by a rather ugly 26.5%, which certainly isn’t what you expect to see when the gold price has moved higher. The interim dividend per share is only 7.7% lower as the payout ratio has been moved from 30% of normalised earnings to 40% of normalised earnings. This is a classic example of a company trying to use the headroom in the payout ratio to soften the blow of poor earnings. The market is usually smarter than that.

The balance sheet also has an unfortunate story to tell, with a free cash outflow for the period of $58 million vs. an inflow of $140 million in the comparable period. Net debt has increased by $129 million, admittedly including lease liabilities. If we exclude them, then net debt increased by $91 million, or 14.5%.

The first half of the year was so disappointing that full year guidance is being reduced, which is probably what gave the market a reason to take the share price 7.8% lower on the day. Although guidance has been moderated, they do still expect the second half to be much better than the first half. There are some uncertainties around this though, like the ramp-up at Salares Norte and the potential for further delays.

Despite these numbers, the share price is still up 13.4% over the past 12 months. Traders may find some interesting volatility in this chart to consider:

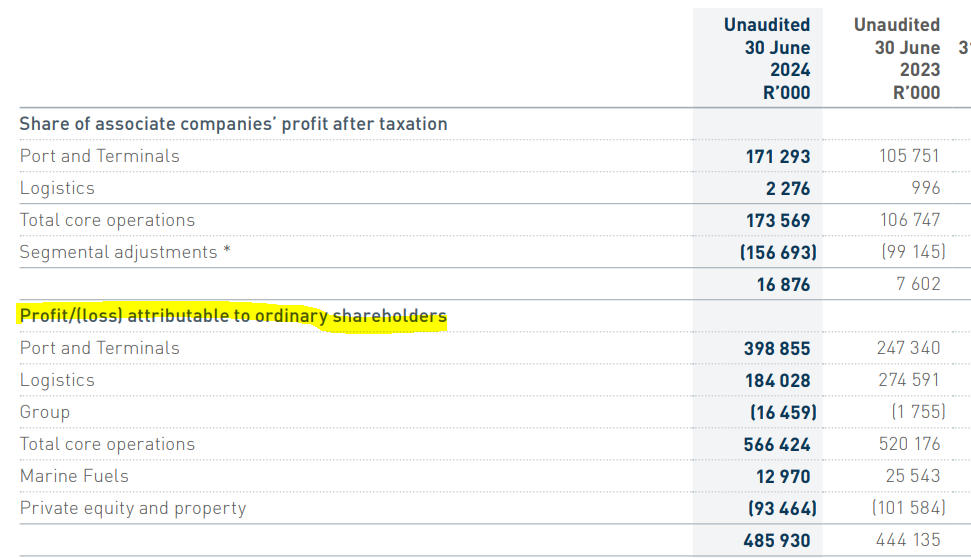

Port volumes are up, but Grindrod’s results are flat (JSE: GND)

The Port and Terminals segment is just one part of the group

The Grindrod investment case gets a lot of positive attention based on the Port and Terminals segment, with a 22% compound annual growth rate (CAGR) in port volumes over three years and a 12% CAGR in terminal volumes. In the latest period being the six months to June, Richards Bay bounced back with 20% growth in volumes, adding to another 18% growth from the Port of Maputo. This has driven substantial growth in profit attributable to ordinary shareholders from the Port and Terminals segment of 61.5%.

As you can see from this table, the Port and Terminals business is unfortunately just one part of the group story and was certainly the highlight in this period:

The Logistics segment struggled in this period, although there was a bright spot in the form of the ships agency and clearing and forwarding businesses. As for container handing, that was impacted by broader logistical constraints in the market. The rail business has also been through quite a bit, with that structural reorganisation now complete. The less said about the private equity and property segment, the better.

When it comes to HEPS, Grindrod went backwards slightly from 73 cents to 72.1 cents. The interim dividend took far more of a knock, down from 34.4 cents to 23.0 cents as the payout ratio was decreased.

The share price fell 4% on the day of this news. That’s just a minor blip in the recent growth trajectory though, with the share price up a substantial 45% in the past 12 months.

Little Bites:

Director dealings:

There’s yet more selling by a member of the founding family of Famous Brands (JSE: FBR), this time to the value of R11.4 million.

Aside from some selling related to share awards by executives at Investec (JSE: INL | JSE: INP), there’s a sale by Stephen Koseff of £530k that is worth taking note of.

A Dis-Chem (JSE: DCP) prescribed officer has been selling shares for a while now and the selling has continued, with R4.9 million as the latest tranche.

A director of Sasol (JSE: SOL) bought shares worth R286k.

Property group Putprop (JSE: PPR) released a trading statement reflecting a drop in HEPS of between 40.5% and 60.5%. They didn’t give any further details, with results expected to be released on 30 August.

There’s an unusual shuffling of chairs at Texton (JSE: TEX), with current CEO Pienaar Welleman moving into the CFO role and current COO Jonathan Rens taking the CEO role.

Trustco (JSE: TTO) has decided to walk away from its commercial banking business, with a decision to return its banking licence to Bank of Namibia for cancellation. This is less than 1% of Trustco’s total investments, so the operations are probably more of a pain than they are worth.

For all things, from share price performances to TikTok trends, there is a universal truth: the pendulum swings. After the self-indulgent lunacy of “Brat Summer” in July, August was marked by the counterpointing “demure” trend, with everyone from influencers to brands expounding how they keep things “very cutesy, very mindful”. Got no clue what I’m talking about? Keep reading, I’ll take you through it.

And before you panic about whether this is just a tabloid post, my point here is that brands are no longer setting the trends out there. As this piece will hopefully show you, brands are now reacting to trends rather than driving them. Things have changed.

Choose your fighter

Love it or hate it, there’s no denying the truth that social media (TikTok in particular) is the petri-dish from which the world’s trends emerge. Despite being relatively new compared to other platforms, TikTok’s growth has been nothing short of extraordinary, achieving in six short years the kind of reach that Facebook and Instagram only saw after a decade. At present, the app has just over a billion regular users – meaning one in every eight people on earth. That’s not an audience to be sniffed at.

As cost per acquisition rises and consumer attention gets more scattered, brands are facing a real challenge in reaching the right decision-makers. Remember that old marketing adage about consumers needing an average of seven interactions with a brand before a purchase is made? I think we can safely assume that that average has continued to move up with every new social media platform’s introduction.

Millennials, who make up a significant chunk of the TikTok community (60% of the platform’s audience, in fact), are a key group to target. Most millennial TikTok users are now juggling adult responsibilities like household grocery shopping, making them the main decision-makers in many households.

With an estimated $360 billion in global disposable income, Gen Z is another must-win audience. The “born on the internet” generation, Gen Z users are 1.4x more likely to discover new brands and products on TikTok and 1.7x more likely to create tutorials about a product after buying it. This makes TikTok a golden opportunity for brands to tap into Gen Z’s love for discovering, participating, and influencing, driving both product awareness and consideration.

With all these stats considered, it seems like a no-brainer for any brand worth their salt to be chasing TikTok fame – but of course it can’t be that easy. TikTok isn’t your typical social media platform. Its quirky, trend-driven, fast-paced nature means that traditional ads or sponsored content might not cut it. But those who lean into what works on TikTok stand to win eyeballs and brand clout for their efforts.

Consider Unilever as a case study. #CleanTok – the TikTok community for cleaning content – is thriving. With over 97 billion views, it’s become the go-to place for sharing life hacks, learning pro tips, and discovering proven product recommendations. Unilever, whose homecare category tends to make up over half of annual turnover, recognised the potential of this engaged community. Partnering with TikTok, they launched #CleanTok content to make cleaning feel more like entertainment than a chore. And it’s working: 54% of users have purchased a household product after seeing it on the platform.

That’s the kind of ROI that gets marketers salivating, which explains why everyone is trying to get a slice of this pie.

In the blue corner: Charlie XCX

Although it was a thing in the middle of South Africa’s cold season, Brat Summer is an idea that transcends mere weather. It all started with the release of pop singer Charli XCX’s latest album, Brat, which has taken the charts by storm. The album, with its lime green cover and sans serif font – design elements that you’ve no doubt seen everywhere lately and wondered why – is best described as an embrace of a hot-mess aesthetic. It prioritises club culture at its core but still hides introspective lyrics on ageing, womanhood, grief, and anxiety between the beats. Taking its cues from the album, Brat Summer mixes the carefree, grungy, and hedonistic vibes of the 80s and 90s with that millennial and Gen Z edge (and angst). Brat Summer is about knowing that the world is a messed up place and we’re all a little traumatised but we’re doing our best and we’re managing to have fun. As Charli herself puts it, “It’s very honest, it’s very blunt, it’s a little bit volatile… It’s brat, you’re brat, that’s brat.”

Editor’s note: having never even heard of Charli XCX before reading this article, our resident ghost is now feeling old.

Unsurprisingly, Brat Summer became the trend to chase for about eight weeks. Perhaps my favourite moment in this whole crazy ride was when presidential contender Kamala Harris’s PR team decided to “brat-code” her official X account with a neon-green cover image and that unmistakable font. This of course followed on the heels of Charli XCX stating that Kamala Harris “IS brat” – high praise that was no doubt met with cheers of joy by the young left.

But Harris isn’t the only one who got a piece of Brat Summer. AirBaltic acted quickly and went all-in by temporarily rebranding themselves as AirBrat, playing off their already-existing signature lime green look. The move paid off, with over 400,000 views on TikTok. In case this TikTok player confuses you, you have to click the replay button in the bottom left:

And just as Brat Summer apparently reached its climax, it was ushered out by a new contender: the word “demure”. It all started with this video by creator Jules Lebron, which went live in the first week of August:

While the jury is still out about what exactly the secret ingredient is that led to its rapid rise in popularity, Jules’ video went viral seemingly overnight. Less than a month later, she’s now made dozens of viral TikToks about being demure – with the most-watched one sitting at a cool 10.7 million views.

Jules talks about being “mindful,” “cutesy,” “sweetsy,” and “considerate,” but her videos are far from serious critiques. Instead, she often makes fun of herself. For example, she once went to work wearing bold green-glitter makeup – not exactly “demure.” In another video, she claims she doesn’t drink or party, only to follow it with footage of herself, clearly tipsy, muttering “very demure” while searching for her hotel room after a wild night in Las Vegas.

Making its way to celebrities’ social media feeds, the trend has since prompted big names and brands to showcase their demureness and hop on the “demure” bandwagon.

For me, the key takeaway is that the days of brands and celebrities being the tastemakers in the world are nearing their end. With so many creators contributing original content to social media platforms like TikTok every day, and each one of their ideas having the potential to go viral any minute, it almost doesn’t make sense for a brand to try to swim against the current of attention. It may well be far easier, and – when done right – far more rewarding to incorporate what’s already trending, instead of trying to set the trend.

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Margins under pressure at Adcock, but HEPS looks alright (JSE: AIP)

The final dividend per share has also shown some growth

In Adcock Ingram’s business, margins aren’t easy to manage. Apart from margin mix and how growth in different categories can lead to structural changes in group margin, there are also other issues like regulated prices for medicine. Even where revenue shows growth, gross profit may not follow suit.

This has been the case for the year ended June, where revenue was up 6% and gross profit was just 1% higher, which means gross profit margin fell. Despite a 6% drop in operating profit, they still managed to show 10% growth in HEPS to 616.6 cents. This is the power of share repurchases, particularly when a share trades at low multiples. Headline earnings was only up by 3.5%, yet on a per-share basis this jumps to 10% thanks to the sheer number of shares repurchased in the past year.

The same positive effect is seen on the dividend per share. The total dividend for the year is 275 cents, up 10% from 250 cents last year. The full benefit of the growth in the annual dividend is being felt in the final dividend, which jumped from 125 cents to 150 cents.

Looking at the segments, it was the Hospital segment where profit dislocated from revenue to the greatest extent. Revenue was up 8% in that segment, yet trading profit fell by 16%. As an example of a different shape elsewhere, Prescription saw revenue up 4% and trading profit up 10%. This is my point about how the mix effect can really impact the group numbers.

The market liked what it saw, with the share price ending the day 9% higher.

The bottom is hopefully in at Cashbuild (JSE: CSB)

I strongly believe that things will improve from here

After watching the Cashbuild share price come off sharply for no obvious reason in the past month, I pulled the trigger and got in at R143.65. So far, so good. I’m up around 14% in the space of a week – and that’s even after the drop in the share price after these earnings came out! Sometimes, the market gives you a gift.

You won’t understand my investment thesis on Cashbuild purely by looking at the trading statement for the 52 weeks to 25 June. HEPS will be down by between 20% and 30%, which by all accounts is awful. The point is that share prices (and thus investment returns) are based on what will happen in future, not what already happened.