In terms of section 36(1)(d) of the Companies Act, No 71 of 2008 (Companies Act), the creation of “blank shares” in a company’s memorandum of incorporation (MOI) is not unusual. However, practical and legal uncertainties often arise in respect of the timing of the determination of the associated preferences, rights, limitations or other terms of those shares, the issuance of the shares, and the filing of the amendment to the MOI with the Companies and Intellectual Property Commission (CIPC).

Relevant provisions

S36(1)(d) of the Companies Act provides that the MOI may set out a class of shares which does not specify the associated preferences, rights, limitations or other terms of that class (Share Terms). The section empowers the board of the company to determine the Share Terms, and states that the shares must not be issued until the board has made such determination.

In terms of s36(4), if the board acts in terms of s36(1)(d), it is required to file a Notice of Amendment of its MOI with CIPC, which sets out the changes effected by the board (Board Amendment Notice). We also see that this constitutes an amendment of the MOI by the board in s16(1)(b) of the Companies Act.

An amendment to a MOI, as set out in s16(9)(b) of the Companies Act, takes effect (i) 10 business days after receipt of the Notice of Amendment by CIPC, unless endorsed or rejected with reasons by CIPC prior to the expiry of such period; or (ii) such later date, if any, as set out in the Notice.

Analysis of relevant provisions

Once a board has determined the Share Terms, the question often arises as to when such shares can be issued. Given that the most common habitat in which blank shares are encountered is the preference share funding environment, more often than not, time is of the absolute essence, and every day counts. Particularly, the question is whether:–

• these shares can only be validly issued after the Board Amendment Notice has been “registered” by CIPC; or

• the company is able to proceed forthwith with the issuance of the shares after the board resolution has been passed, and only thereafter file the Board Amendment Notice with CIPC.

The question has become even more important and relevant pursuant to the Companies Act amendments which took effect in December last year. Those amendments effectively clarify that CIPC performs a similar reviewing and registration role which it had under the previous Companies Act – it now has 10 business days within which to accept or reject the resolution. A rejection can sometimes occur on extremely technical, administrative grounds, or due to an inadvertent mismatch between the company’s and CIPC’s respective records of what the share capital of the company is (there could be historical issues in this regard). This makes it vitally important to know when exactly the parties can go ahead and close the section 36(1)(d) issuance.

The Companies Act is regrettably ambiguous when it comes to addressing this question. A strong argument exists that the company is able to issue the shares once the Share Terms have been determined by the board, with an ex post facto CIPC filing. This argument is based on the grounds discussed below.

S16(9)(b)(i) of the Companies Act refers to an amendment of a company’s MOI taking effect “after receipt of the Notice”. Considering s16 of the Companies Act as a whole, we note the Notice of Amendment is referred to in s16(7) and 16(9) only. S16(7)(b) of the Companies Act refers to the filing of a Notice of Amendment if a new MOI will substitute the existing MOI in terms of s16(5)(a), or the existing MOI is altered in terms of s16(5)(b). When we consider s16(5), we see that this section refers to amendments that were effected under s16(1)(c), which requires a special resolution of the shareholders, and not s16(1)(b), which deals with a board amendment. Consequently, s16 does not deal with the filing of the Board Amendment Notice where the MOI was amended by way of board resolution. Thus, a textual argument (albeit a tenuous one) may be made that (i) s16(9) only deals with the filing of a Notice of Amendment for amendments in terms of s16(1)(c) (special resolutions of shareholders), and that (ii) s36(4) is a different procedure that applies for amendments by the board as contemplated in s36(3).

Consideration of the language in s36(4) of the Companies Act, specifically that the Board Amendment Notice must set out “the changes effected by the board”, implies that once the board resolution to determine the Share Terms is passed, the changes to the MOI are in law, “effected”. Therefore, the filing of the Board Amendment Notice is merely a formality for record purposes – much like the return a company files with CIPC, recording changes to its directorship. From a contextual and purposive perspective, this interpretation is also logical as the board’s powers are limited to an amendment which relates only to share capital, with one of the obvious purposes of enabling the company to raise equity finance. Companies would normally require equity finance to be raised as quickly as possible, and without being delayed by CIPC’s processes. Therefore, given the context and purpose of s36(3) of the Companies Act, it is sensible and businesslike to interpret s36(4) as allowing the board to issue shares immediately upon determining the Share Terms.

The point above also garners support from s36(1)(d)(iii) of the Companies Act, which prohibits the issuance of the shares until the board has determined the Share Terms. This section does not require that the determination by the board be filed with CIPC and, thus, the only requirement prior to issuance of these shares is that the Share Terms be determined by the board.

However, it must be noted that regulation 15(3) of the Companies Regulations, 2011 requires the Notice to be filed together with any required supporting documentation and the filing fee within 10 business days after an amendment to the MOI has been effected in any manner contemplated in s16(1) of the Companies Act. As this regulation covers s16(1)(b) as well, the Notice with the board resolution which determines the Share Terms should be filed with CIPC within the prescribed time period.

Conclusion

S36(1)(d) of the Companies Act has given companies the flexibility to create “blank shares”. However, the Companies Act remains ambiguous with regard to the timing of the determination of the Share Terms, the issuance of the shares, and the filing of the MOI amendment with CIPC. While a strong case exists for the issuance of the shares the moment that the board determines the Share Terms, to mitigate any potential legal and compliance risks, we recommend that companies proceed with caution and only issue such shares after they have “registered” the board resolution with CIPC. Alternatively, if the parties really cannot wait, then the special resolution of the shareholders approving the initial MOI amendment should, in anticipation, include a specific reference to s38(2) which allows the retroactive authorisation of shares that were issued before their creation in law.

Ian Hayes is Practice Head and Storm Arends is an Associate in Corporate & Commercial | Cliffe Dekker Hofmeyr

This article first appeared in DealMakers, SA’s quarterly M&A publication.

BALANCING GEOPOLITICS, REGIONAL INTEGRATION AND VALUE ADDITION

As the global economy undergoes a profound transformation towards low-carbon energy systems and digital technologies, critical minerals such as lithium, cobalt, platinum group metals (PGMs), rare earth elements (REEs) and graphite have emerged as key enablers of this transition. These minerals underpin everything from electric vehicles (EVs) and renewable energy to semiconductors and hydrogen fuel systems.

Rising demand has elevated these minerals from mere commodities to strategic assets that define national security, industrial competitiveness and geopolitical alignment. The Southern African Development Community (SADC), richly endowed with many of these resources, finds itself at the epicentre of this global shift.

While Southern Africa’s mineral wealth presents a generational opportunity, resource abundance alone does not guarantee economic transformation. To fully leverage its position, the region must transition from being a raw material supplier to a strategic industrial partner, anchored in coherent policies, regional cooperation and value chain development.

THE GLOBAL RACE FOR CRITICAL MINERALS: Opportunity and risk

Southern Africa’s strategic positioning must be understood within the broader context of intensifying global competition over critical mineral supply chains. China’s dominance in processing key inputs, particularly rare earths, lithium and graphite, has prompted countries like the United States (US) and the European Union (EU) to ‘de-risk’ their supply chains by diversifying sources. This has translated into a wave of new trade policies, strategic partnerships and investment frameworks increasingly focused on Africa.

Bilateralism and fragmentation risks

The US, for example, has signed separate critical minerals agree-ments with Zambia and the Democratic Republic of Congo (DRC), marking a shift from multilateral co-operation to bi- lateral engagement. While these partnerships signal increased interest in the region, they also risk fragmenting regional cohesion. Country-by-country deals reduce the collective bargaining power of African nations and complicate efforts to coordinate regional industrial strategies, particularly in downstream beneficiation and infrastructure planning.

The rise of resource nationalism

At the same time, growing resource nationalism across the Global South, manifested through export restrictions, local content mandates and beneficiation requirements, signals a shift in approach. African countries increasingly recognise that controlling their mineral endowments and capturing more value domestically is not only a matter of economic benefit, but also essential to long-term development and strategic autonomy.

DEFINING CRITICALITY: A continental mosaic of priorities

Despite the shared importance of critical minerals, SADC countries define ‘criticality’ differently, reflecting diverse economic structures, industrial capacities and development goals. For instance, South Africa prioritises PGMs, manganese, vanadium and iron ore due to their economic contributions, while placing less emphasis on lithium and copper. Zambia, Zimbabwe and Namibia, in contrast, consider lithium, copper and rare earths as top priorities.

This lack of standardisation presents a challenge for regional alignment. Moreover, while producer countries focus on domestic benefits like jobs, revenues and industrialisation, consumer countries define criticality based on supply chain security, scarcity and import risks.

A shared, science-based and forward-looking regional framework is therefore essential. It must respect national priorities, while aligning with global trends in clean energy, digital infrastructure and advanced manufacturing. This framework should also promote inclusive industrial growth, especially by integrating artisanal and small-scale mining (ASM), which often plays an outsized role in supplying niche minerals.

NATIONAL STRATEGIES IN MOTION: Parallel paths, shared aspirations

Across SADC, countries are advancing domestic strategies to increase value capture from critical minerals.

Zimbabwe has implemented a phased approach to restricting lithium exports, beginning with a ban on raw ore and extending to a planned ban on lithium concentrate exports by 2027, to promote domestic value addition and battery-related manufacturing.

Namibia is enhancing rare earth processing capacity, supported by strategic partnerships and investment facilitation from the EU.

Zambia and the DRC are collaborating to develop copper and EV battery value chains, supported by US-backed agreements and infrastructure initiatives, most notably the Lobito Corridor railway project.

Botswana is diversifying beyond diamonds by developing projects to process minerals like manganese into battery-grade materials, while expanding renewable energy infrastructure to support its clean energy ambitions.

However, these national approaches, while promising, also risk duplicating efforts and diluting investment. Without coordination, multiple countries could build similar infrastructure (e.g. smelters, refineries), leading to suboptimal returns and missed synergies.

There is an urgent need for value chain rationalisation. Instead of each country building all components of the beneficiation chain, the region should strategically allocate functions across borders, based on competitive advantage. For example, Botswana – with its central location, access to the Kalahari Copper Belt, and vast salt pans – could serve as a processing and logistics hub, linking copper from Zambia and lithium from Zimbabwe.

Such coordination could form the foundation of a regional industrial strategy that maximises shared benefits while avoiding inefficient competition. Examples such as regional gold refining in Germiston (which services multiple SADC states under existing Rules of Origin provisions) illustrate that practical cross-border beneficiation is possible when regulatory frameworks are aligned and infrastructure is leveraged.

INFRASTRUCTURE AND INTEGRATION: Building the backbone of value chains

Value chain coordination cannot occur in isolation; it must be supported by physical and regulatory infrastructure. This includes transport, energy, water and digital systems. Equally important are trade-enabling legal instruments such as the SADC and AfCFTA Rules of Origin, which, through provisions like ‘cumulation’, allow components sourced across member states to be treated as local inputs, facilitating integrated processing and manufacturing.

Projects like the Lobito Corridor, linking the DRC and Zambia to Angola’s ports, are a positive step. But more corridors, such as Nacala, Walvis Bay and Beira, are needed. These routes should not merely facilitate mineral exports, but evolve into industrial development corridors, fostering downstream beneficiation and local economic ecosystems along their paths.

Botswana, strategically located at the crossroads of Southern and Central Africa, could emerge as a regional transport and processing hub. With deliberate planning, corridors can become economic arteries, enabling integrated clusters of processing, manufacturing and technology development, ranging from battery assembly to hydrogen electrolyser production.

Crucially, these corridors must complement rather than compete. Each offers unique advantages based on geography, resource type and trade routes. A coordinated approach would ensure that corridor development supports regional scale and resilience, rather than creating redundant infrastructure.

THE COST OF FRAGMENTATION: Missed opportunities and market failure

The cost of failing to act collectively is significant, as illustrated by several examples:

Despite Southern Africa’s global dominance in platinum, the industry remains largely a price taker, exporting predominantly unrefined concentrate. This persists even as the region leads in fuel cell research and development, missing opportunities to capture greater value through downstream processing.

Zimbabwe exports significant volumes of spodumene concentrate, a lithium precursor, but without domestic battery manufacturing capacity, much of the economic value is realised offshore, limiting local industrial development and job creation.

Botswana hosts Africa’s largest salt pan system, the Makgadikgadi Pans, which is under active exploration for lithium brines. However, the country currently lacks operational lithium extraction or value addition facilities, leaving it disconnected from the regional lithium and EV battery value chains.

Without coordinated, integrated regional planning, Southern Africa remains vulnerable to commodity price volatility, and reliant on foreign actors for downstream processing and value addition. These structural inefficiencies constrain economic growth and undermine the region’s capacity to influence and benefit from global mineral supply chains.

VALUE ADDITION: Transforming mineral potential into industrial power

To change this trajectory, beneficiation must be at the heart of the region’s strategy. With nearly 70% of global PGMs sourced from South Africa and Zimbabwe, SADC holds sufficient market power to demand downstream investment, just as Indonesia did with nickel.

The growing prominence of the hydrogen economy enhances this leverage, given the importance of PGMs in fuel cells and electrolysers. Regional efforts to develop R&D capabilities, supply chain infrastructure and technology transfer should focus on moving beyond raw exports to high-value industrial outputs.

Countries are already moving in this direction:

Zimbabwe is implementing a beneficiation roadmap for lithium and chrome.

Namibia is attracting REE and hydrogen investment.

Botswana is expanding processing beyond diamonds.

Zambia and the DRC are deepening cross-border copper value chains.

Yet energy constraints, limited capital and weak digital infrastructure remain major bottlenecks. Among all infrastructure categories, power access and affordability stand out as the most pressing and potentially transformative investment areas.

ENABLING INVESTMENT THROUGH LEGAL COHERENCE AND ESG ALIGNMENT

The legal landscape across SADC is evolving, with countries updating mining codes, export regimes and local content rules. However, the lack of harmonisation remains a source of uncertainty and delays, particularly for junior and ESG-focused investors.

Existing instruments like the SADC Protocol on Trade in Goods and its Rules of Origin (RoO) provide preferential access to intra-regional markets, often recognising minerals as wholly originating goods. Value-added products also qualify, provided they meet moderate RoO thresholds. The AfCFTA Protocol on Trade in Goods offers a continental framework closely aligned with SADC’s RoO principles and includes provisions for cumulation, broadening opportunities for cross-border beneficiation chains.

Establishing a regional engagement platform within SADC could facilitate legal alignment, streamline permitting, and promote coordinated investment planning, enhancing the region’s appeal to responsible investors while respecting national sovereignty.

Equally critical is adherence to Environmental, Social and Governance (ESG) standards, now essential for access to global markets. Embedding digital traceability, environmental certification and community inclusion into policy and practice is vital. Formalising ASM, ensuring transparent licensing, and introducing ESG incentives can strengthen the region’s reputation and competitiveness.

Together, these trade instruments create important enablers for cross-border industrialisation. The key challenge now is to translate these frameworks from legal availability into practical accessibility through coordinated customs enforcement, institutional capacity building, and increased awareness among public and private stakeholders.

GLOBAL ALIGNMENT: SADC’s strategic moment on the world stage

The launch of the G7 Critical Minerals Action Plan in 2025 presents a timely opportunity for Southern Africa to align its development priorities with growing global demand for responsibly sourced critical minerals. Many of the plan’s key focus areas – such as supporting local beneficiation, financing infrastructure projects, and harmonising ESG practices – already feature prominently in SADC’s regional strategies. This alignment positions the region to leverage global momentum to build resilient and transparent mineral supply chains.

A particularly important aspect of the G7 plan is its recognition of Artisanal and Small-Scale Mining (ASM), which remains a vital source of niche, high-value minerals, and a major employer across Africa. By formalising ASM, the region will not only improve livelihoods; it will increase transparency and address environmental and social challenges associated with informal mining activities.

To capitalise on global trends, SADC countries should actively engage with international initiatives that support critical mineral development and sustainable infrastructure investment, such as the:

Minerals Security Partnership, an international coalition focused on responsible sourcing and supply chain resilience.

Canada-led Critical Minerals Production Alliance, emphasising investment collaboration.

EU–Africa Global Gateway, the EU’s flagship infrastructure programme with a focus on green minerals and energy transition partnerships.

Green Hydrogen Alliance, promoting global hydrogen development, a sector where Southern Africa’s abundant renewable resources and mineral wealth could play a strategic role.

By deepening engagement with these platforms, SADC can strengthen its position globally, attract responsible investment, and ensure that its critical minerals contribute meaningfully to both local development and the global clean energy transition.

From resource custodians to strategic co-creators

The global transition to green energy, digitalisation and strategic autonomy has placed critical minerals at the heart of economic and geopolitical realignment. With its vast mineral wealth, Southern Africa is no longer a peripheral player, but a pivotal force shaping global supply chains.

The region’s success hinges on collective, strategic action. The choice is clear: remain fragmented exporters of raw ore, or unite as industrial partners driving downstream industries, innovation and sustainable growth.

This transformation demands five core shifts:

From bilateral deals to coordinated regional strategy: SADC must strengthen collective bargaining through integrated policies and value chain coordination.

From export dependency to onshore value addition: Beneficiation and manufacturing must move from ambition to reality, supported by competitive infrastructure and energy access.

From siloed infrastructure to interconnected corridors: Strategic transport corridors like Lobito, Nacala and Walvis Bay should evolve into multi-country industrial belts, enabling regional value chains.

From legal complexity to investor confidence: Harmonised mining, energy and ESG frameworks will reduce barriers, attract finance, and empower junior miners and ASM actors.

From marginal voices to global rule-shapers: Active engagement in platforms like the G7 Minerals Security Partnership and African Union strategies is essential to embed Africa’s interests in the green transition.

Ultimately, vision must be matched by execution. Political will, institutional capacity and regional trust are vital. If SADC acts with unity and urgency, it can move beyond benefiting from the critical minerals boom to leading it.

Nomsa Mbere is a Partner | Webber Wentzel

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

Cell C has been on quite the adventure in its efforts to carve out a sustainable competitive position. The telcos space can be brutal, with historically high levels of capital investment required to compete.

This has thankfully changed, with Cell C having created a profitable business model that goes well beyond the MVNO operations that the market tends to focus on.

In this podcast, CEO Jorge Mendes joined me to explain Cell C’s business and how they plan to win across key verticals like Prepaid and Postpaid in addition to the exciting MVNO and other opportunities. We talked about why the turnaround is behind them and how Cell C plans to grow into the future.

As a separately listed company with a much simpler balance sheet, Cell C is on the radar of investors and worth understanding in more detail. This podcast is an excellent resource in your research process.

This podcast has been sponsored by Cell C. As always, I was given an opportunity to dig into the strategy and ask my own questions in my quest to learn more. You must always do your own research and speak to a financial advisor before making any decision to invest. This podcast should not be seen as an investment recommendation or an endorsement.

Full Transcript:

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast. Despite the very best efforts of Cloudflare, which took down Riverside, meaning we were scrambling for a solution here, I’m pleased to report that the Cell C technology stack is a whole lot more reliable than Cloudflare (which seems to run almost the entire internet; it’s kind of frightening, actually).

I’m very grateful that it did finally start working, because today I have the opportunity to chat to Cell C CEO, Jorge Mendes. And what a fantastically exciting time to be able to speak to you, Jorge. Obviously, now a separately listed company. I’m sure you’re quite excited about that.

Before I formally say hello to you, I do just want to get one thing out of the way. Obviously, the IPO has closed now – I mean, everyone could have seen the pricing for themselves. But because I’m chatting to you and not to the shareholders who were behind that whole transaction in Cell C, the focus today is on the Cell C business, not on the IPO and the pricing and all the stuff that the bankers would have worked on. It’s just an unhelpful conversation.

So, I’m personally very keen to chat to you about the Cell C business itself, and the market will figure out over time what the shares should be worth, of course. That’s the magic of a market. So, looking forward to that.

Jorge, welcome to the show! Thank you for making time for this. I’m keen to learn more.

Jorge Mendes: Thank you very much! Thank you for having me here. A great phase in our business, lots of excitement. I think we’re well-positioned for what we call ‘the telco of the future’. Perhaps, during our conversation, I can elaborate on that a little bit more. But, yes, we’re now at the beginning of the new journey.

The Finance Ghost: Absolutely. Yeah, it really is that, actually. Let’s dig into the story here. The Mobile Virtual Network Operator (MVNO) operations at Cell C do tend to get all of the focus from investors and from the media, but the reality is there’s actually a lot more to Cell C.

There’s a huge piece of your business that does have some stuff in common with the other telcos – for example, just over 8 million direct subscribers – and I think that part of the business doesn’t really get the attention that it should receive from the market.

So, let’s start with just a lay of the land of how Cell C actually makes its money. Set the scene for us here, for those who aren’t familiar with how the group looks today.

Jorge Mendes: Yeah, thanks very much. It’s a great question and a great starting point, because you’re quite right. I think it’s more than, dare I say, a one-trick pony. We’ve got a very strong set of growth engines.

But before we talk about the growth engines, I think what we’ve done extremely well is we’ve pivoted to a capex-light model. In essence, what that means is we’ve given up the steel structures, the steel towers, and we’ve got a Virtual Radio Access Network (vRAN) arrangement with MTN and with Vodacom. So, very good partners that build great quality infrastructure.

And we do know that the market will go through a level of consolidation as the market matures. We are making the sector a healthier sector by being a very good customer to both MTN and Vodacom, from a roaming point of view. The billions in revenue that they generate from us with a very high, healthy margin, they can reinvest into infrastructure, or simply bank it as profits.

We are a full Mobile Network Operator (MNO). We have our own spectrum, our own core, our own billing systems, our own everything. We’ve just given up the steel towers, and we’ve got the vRAN. So, that helps tremendously.

It also improves things from an ESG point of view, so we really are playing our part in terms of the planet. It doesn’t make sense to have four good base stations next to each other, with four good generators and security guards and diesel, and so on. So, that’s the foundation.

And then we’ve unlocked Multi-Operator Core Network (MOCN) roaming, which allows us to shift traffic between our roaming partners. So, we’ve gone from 5,500 of our own physical base stations to over 28,000, in terms of access to those 28,000 towers.

We really do have the best of the best when it comes to network quality – voice, data – and there are a number of accolades that support that. But more important than the accolades is the experience that our customers and business partners now enjoy in terms of good quality.

So, we get to market with very, very comparable voice quality and data. We’re providing significant revenues to our roaming partners. That creates a healthier sector, and that’s the foundation.

On top of that, we then call ourselves a platform for growth. If I take our engines, we have a Prepaid engine, a Postpaid Consumer engine, an Enterprise engine, and then a Wholesale MVNO engine.

If I take Prepaid, we now have a significant amount of revenue and customers still in Prepaid. We’re growing, so we’re coming off a lower base given our market share. But we’ve got new products, new distribution channels. We’ve got a great quality network.

We rebranded Cell C in August of last year, so we’ve got a brand-new look and feel. We’ve got taglines like “Nothing Should Stop You” and “Switch to See”, which is really an invitation for customers to try our network. All of these ingredients are boding well for making sure that we do grow in Prepaid.

Our consumer Postpaid business. We acquired Comm Equipment Company (CEC), which was a full subsidiary of Blu Label, and that was really postpaid handset financing. So that’s back in the Cell C fold, and we’re running our Postpaid Consumer business end to end.

And again, an introduction of new channels. We integrated into iStore, for example. We were the only network that was not integrated. High-value segment, there.

We’ve got 103 of our own stores. We’ve rebranded and refreshed – with a new look, feel, and experience – 72 of those, just in the last year alone. So, a massive task.

We’ve launched new tariff plans and propositions that are now very favourable in the market. And we’ve changed small things like credit vetting profiles and scoring, so that will be continuous improvement.

And then of course, given the financial constraints that we had in the past and largely that goes away now, we will be in a better position to compete in handset financing, hardware arranging, etcetera, when it comes to Consumer Postpaid.

Our Enterprise business is a small business, but a good growth engine, in terms of percentage growth. We’re partnering very deeply there. We’re not hiring a lot of staff. We’re hiring a handful of key account managers, if you like, and we’ve signed up more than 44 partners.

We’ve got Altron, Nashua and a whole bunch of other players that allow us to get to market with propositions that they need connectivity, or vice versa – where we have the connectivity and they have a solution – and that’s boding very well. So, it’s part of our ethos to partner very deeply.

And then lastly, to your point, you spoke about the MVNO business. The MVNO business has some really strong brands. We’re able to reach those segments very quickly and very effectively, as opposed to trying to do it ourselves by inventing products, marketing, spending time building the awareness and then trying to address it.

The last little piece is that we have a fibre ISP. So, we do still sell fibre – owning the home and family is very much a strategy – but we’re not laying fibre, we’re not laying physical infrastructure. We leave that to the guys who do it best.

The Finance Ghost: Thank you. That does a fabulous job of the lay of the land. That’s exactly my point. There’s way more to Cell C than just the MVNO business, even though that gets so much of the attention in the market.

I really want to try and not take the conversation away from that – because it’s a relatively unique element, and you’ve got such a good market position there – but I think people forget about everything else going on in Cell C, which is a pity.

I actually walked past one of your stores the other day, I think it was in Canal Walk, and it looks really good. Genuinely looks excellent. I love the new colours, etcetera. So, well done!

Jorge Mendes: Thank you.

The Finance Ghost: It looks exciting. It looks like a challenger brand. It looks like it should. It’s edgy, it’s fun, and it’s different.

Jorge Mendes: Yeah, thank you. And what we’ve done is what most people think is very obvious. We asked customers what they like. To be brutally honest, if I have permission to speak truly, I didn’t personally like the colour orange. It’s not about me. We asked the market.

We’ve been around for 24 years. We’ve gone through many phases. We’ve been black, we’ve been red, we’ve been blue – and that’s just the colour and the positioning. And I said, “It’s less about me as the CEO. It’s less about what we feel. It’s absolutely about our customers and partners. What do you like? What don’t you like? What would you like more of? What would you like less of?” And that’s what we’re trying to do.

We’ve looked at the headwinds in the market and said, “How do we address this? If I built another beautiful version of yellow or red, why would a consumer come to me and get the orange version of what already exists?” So, we had to do things differently. Not for the sake of being different, but for giving customers and partners what they really want. And that creates the real disruption.

So, the look and feel of the stores comes from what customers wanted – and I’ve fallen in love with them, quite clearly. Of course, I’m a little bit biased now, but we’ve really tried to take the elements that they’ve asked for – fresh, funky…

I mean, the word ‘howzit’ that greets everybody is just typically South African, across all of the diversity that we’ve got, and that was something that was just synonymous with a greeting. Small, little things like that actually go a long way, because we’ve done some deep research and analytics and listened properly to what customers have to say.

The Finance Ghost: Yeah, I love it. Well done. I think the colours look like something I want to get into and drive on a mountain road, so that works for me. Maybe that’s my own bias coming through, but I really like it. It’s very cool.

Let’s talk to a couple of the growth engines then, as you’ve highlighted. The one is Prepaid, and this is where things got super interesting in the media recently and some of the commentary coming through from the likes of Telkom, MTN.

It’s a very competitive space, obviously. We know that South Africans are extremely cost-sensitive. That’s just the reality of the South African consumer. So, lots of competition in Prepaid.

I’d love to get some comments here (to the extent you can speak about it), just around those Prepaid forces, what you’re really up against there. And to what extent do you face the risk of almost damaging competition, versus competition where you can actually win, and it’s economically lucrative?

Jorge Mendes: Yeah, absolutely. It’s a great question. We want to always add value to the sector. As you get into a more mature level of the sector, then typically what starts happening, the organic growth is not there in the same way that it was in years gone by. So, you end up taking share from one or the other, and you’ve got to reinvent yourself.

And I guess what we’ve done is we’ve said we had too much above-the-line pricing and not enough below-the-line and personalisation. So we’ve changed platforms.

We’ve spent a lot of money. Our capex – we’ve guided between R650 and R800 million in capex. And that’s all customer-facing, so billing systems, CVM platforms, cybersecurity posture that improves the cybersecurity and mitigating risk for customers. We built a new app. We’ve done 72 of the 100 stores – those are refreshed already.

And specifically, back to Prepaid, to your point. We’ve changed platforms in terms of CVM, so personalisation at a customer-level segment of one, and we’ve moved a lot of the above-the-line standard pricing to below-the-line personalised pricing. So that’s the one thing.

Two is we’ve created new distribution channels for inflow growth. So, how do we acquire new customers from different segments? We’ve unlocked different commercials and structures that we didn’t have before, with the Pepkor Group as an example. We’ve got Shoprite as another huge channel where we’ve made some differences. We’ve created six new Wholesale channels that we didn’t have.

We’ve got some call centres, the telesales that we’ve now got on board that also help with some of the migration journeys and uplifting revenue and value-added service sales, etcetera. We’ve enhanced our USSD channel.

We’ve built a new app, so that’s what we call the ‘minimum lovable products’ that we release every kind of month or so. It starts somewhere that’s neat, and customers love, and we just add products every other day and so that’s growing quite nicely.

Then we’ve launched a whole bunch of new products. We’ve got Supa Bonus – three times the value. It’s very simple to understand, nothing complicated. You load with x, and you get 3x that amount in terms of value. That’s boding well.

And again, as I say, it sounds like a small thing, but with very, very good quality of voice and data. The best and the second best, as rated by independent surveys. And that’s very different because two-and-a-half years ago we were fourth, and so you could have to play with price a lot because the quality wasn’t as great.

So, we do believe we’re now at the beginning. We’ve seen a little bit of growth coming through, and I think Telkom has done a fantastic job in being data-led and data-centric in that growth. Credit to Sarame and his team, and Lunga, for the great work that they’ve done over the last 12 quarters.

I think yellow and red are under a little bit of pressure in terms of hanging on to revenue growth, and there’s a bit of decline starting to happen there. That’s largely because they’ve got the biggest shares. And when the smaller players start growing, you normally eat into that share.

So, I have no doubt that the competition will accelerate, but I think we’re quite comfortable that, given the level playing fields now that we have on the quality of voice and data, the amazing distribution channels, our platforms, our capability. And we’ve built an incredible team in a short space of time. We really do have a strong team that understands this quite well. I think we’re very well-positioned for growth in Prepaid.

The Finance Ghost: ‘Minimum lovable products’ is great, I love that. Instead of ‘minimum viable product’. Very cool, that’s going to stay with me. I really enjoy that reference.

Let’s talk Postpaid, and then I’m going to bring it back to MVNOs. Because obviously, Prepaid and Postpaid are so linked, at the end of the day. It’s just a different way of selling connectivity to people. I guess the same is true for MVNOs, but you get what I mean.

So, you talked about handset financing channels, all the new tariff plans and propositions. These are the routes to win in that space. And something in your roadshow documentation for the IPO that I picked up is that Postpaid is an area where you believe you are underrepresented, which basically means you have less market share than you think you should have, as I understand it, which means you have space to grow.

So, do you think that you’ve got the building blocks in place now? The stuff you’ve talked about, the financing, the channels, etcetera. Is that now going to get you to the market share that you think you can get to in Postpaid?

Jorge Mendes: Yeah, absolutely. Again, at the beginning, and I hate to sound repetitive, but we’ve had to fix this business. We’ve had to come from difficult circumstances. We’ve been recapitalised twice, and you can figure that out. When you’re not in great shape, there are a lot of things that don’t happen the way they should happen.

We have now allocated an RFP and awarded an RFP for a Postpaid billing system. We did the Prepaid billing system in time, in budget, and that went live in August of last year. I got cracking on that immediately when I started, which was about two-and-a-half years ago. So we’ve done that, we’ve bedded that down, it’s working beautifully.

We’re now doing the same for Postpaid. That will still be a journey; that’ll be 18 to 24 months. So, the capability that we have today is good, but we want better, and we want to plan for the future. So that’s forward-looking stuff.

What we’ve done in Postpaid, for sure – in my previous life, I actually did the roaming deal between Cell C and Vodacom. At that stage, Cell C had 1.3 million customers on their consumer Postpaid business. Today we have under 800,000, at somewhere around 790,000. So, you can see that that’s been in decline. Had we not started managing that business directly this year (so, the last 8 to 10 months), it would have been even lower than the 790,000. That’s how we were bleeding customers.

So, there are a lot of things that you have to do in order to resolve this. First is the quality of network, again. Second (and this is not in sequence – it’s just the ingredients involved here), you need to have good distribution channels.

We had some good distribution channels. We now have very good distribution channels, and also a unique way of how we gain access to those channels, in terms of the commercial construct and how we finance hardware. We’ve created some interesting stuff that I really think will start unlocking value in the next few months. So this, again, is forward looking.

For example, if you don’t qualify for creditworthiness, you press a button, and you give us access to six months of your bank statements. We have an AI tool that looks at various algorithms and will say, “You are good for R370 between the 14th and the 15th of the month. Do you accept the debit order on that time frame?” And we’ll approve you.

So that’s kind of forward-looking stuff that we think we’ll start adding value to, because Postpaid is really about hardware financing. The value that you get on Prepaid is very good. Hardware financing is what makes it attractive for contracts on consumer, and that’s normally 12, 24, 30 or 36-month contracts.

I do also believe, by the way, that, forward-looking, the banks will do the hardware financing better than the telcos. And I think that, given our relationships with MVNOs that are also significantly in the financial services sector, that relationship will bridge nicely in terms of handset financing at a P&L level. You can do this on-balance sheet and off-balance sheet. We will be exercising both options.

So, we do have a better balance sheet and better liquidity to now range hardware better. And then we have some interesting ideas which I’m not going to share with you because they unfortunately are very competitive. But we’ve looked at the market again differently. So, are customers who are in-contract out of range for us? In other words, is the whole market available as an opportunity to gain share from, or only those that are out of contract? And we’ve come up with some really interesting ideas that say the whole market is available to us. So even those that are in-contract, we have some interesting propositions that say we’ll give you really some serious room for thought around, “Hmm, maybe I should switch to Cell C and see what’s going on there.”

So channels, tariff plans. Obviously, credit vetting profile, liquidity and financial position on hardware ranging, etcetera.

We’ve got some new channels that we didn’t have before – I’ve mentioned iStore, but we’ve also just gone with Incredible and HiFi Corp. Those are new channels. We have our own footprint. And then we’ll look at the physical footprint. So, we could have a situation where a Cell C customer could collect hardware at an FNB Connect or at a Capitec Connect or vice versa. So, we’ll use the full footprint to leverage each other’s capabilities and not just keep them as individual silos.

The Finance Ghost: Very cool. Some exciting stuff coming from orange, so we’ll see what happens there. I like it. And yeah, you’re right. The banks have such a low cost of funding. They are a pretty obvious partner in that space. That’s very cool.

I guess that leads us nicely into the MVNO piece, where obviously you have got these banking partners. And it’s quite interesting, the part of Cell C that actually deals with this whole MVNO piece launched all the way back in 2006, if I’m not mistaken? Which was before the world had the iPhone!

I always reference that 2007 was the first iPhone. I remember, because I was first year varsity and there was like one really lucky kid in the class who had an iPhone brought from overseas. People forget how quickly the world has changed. 18 years of the smartphone. Before that, it was BlackBerrys.

And those who have bearish views on Cell C might point out that, at the end of the day, you’re really the middleman. You’re the switch between telcos and retailers like Shoprite, banks like Capitec.

What is the moat here? Why can’t they just disintermediate you? I hear this a lot when I hear people speaking about Cell C, so let’s deal with the meat of that argument. Now, having set the scene around the rest of Cell C’s offering, why does Capitec have a moat in this MVNO space?

Why can you defend your position – your market-leading position, I might add – there?

Jorge Mendes: It’s a great question. I think it’s a strategy that again requires deep thought and analytics around, “How do you make this successful in a sustainable way?” So, given our market share – that’s one of the ingredients that allows you to go very hard at the segment. If there isn’t significant organic growth, those with the larger market share have the most to lose. That’s the first thing.

And so, in spite of certain articles that may appear or not, I’m quite clear that both my larger competitors do not really want MVNOs. They’ve said as much in interviews. “Too many chefs spoil the mobile broth,” I think has been quoted on the red side. Yellow has said the same, that we could have another Netherlands, and the MVNOs could collapse the market. A correction there is that it was not the MVNOs, but rather the MNOs, that led with unlimited tariff plans. And once you go to unlimited, you can’t price up, so there’s no more value to be extracted. So, there are nuances.

We’re very clear that if we wanted to go after mass retail banking customers, we’d have to create a brand, market the brand, create distribution and all of that, which costs a lot of money. So what we do, rather, is partner very deeply with someone who does it very well.

And so if you look at how the economics work, given our market share of let’s call it ‘roaming traffic’ that we buy and that’s got a certain amount of capacity. If I use that traffic for myself, I add costs like sales, distribution, ongoing revenue commissions, marketing, etcetera. And I get to a contribution margin of x.

If I sell that traffic to my MVNO partners, I remove all of those costs. And because they largely have those costs sunk already into their business, they can get to a similar contribution margin.

Take Cell C. If I sell a Cell C prepaid starter pack, and I make a contribution margin of x, or even an inflow revenue of R30, as an example, I largely make the same contribution margin and inflow revenue from an MVNO partner. So, left pocket, right pocket, no difference economically from a P&L point of view and we have to look at the construct.

When you look at our partners that we have, the following ingredients I do believe will give them a higher probability of success. And that’s probably why some of the MVNOs of the past were not successful. So, very strong brands like Red Bull Mobile, Virgin Mobile, Trace TV – even Lyca Mobile, the world’s largest MVNO – did not succeed in South Africa.

And the reason, in our belief, is the following (and I think we’re more right than wrong): you need a high utility product. So, voice data, banking, electricity, food is a high utility product. I don’t believe a clothing retailer will be very successful in MVNO. I don’t believe a cutlery and crockery retailer will be very successful in MVNO. There’s not enough in the utility of the product that will give you enough of a reason to switch.

So, a high utility product. Physical distribution, you need physical distribution. These guys have all got a massive number of branches. You need digital distribution. So an app of sorts that gives you that reach and the high level of engagement, and preferably the combination of the two.

And then lastly, a customer base. If you have a large customer base, you already have that level of engagement. And when you have those ingredients, your probability of success in a partner like Cell C (because we truly partner, we make it a win-win), there are very interesting commercials for them. We keep them competitive.

And what we do is we kind of reverse engineer the structure. We say, “What would an FNB Connect customer need to have to compete favourably out there? What would a Capitec Connect customer need? A Shoprite Connect customer? An Old Mutual Connect customer? What would a Mr Price Mobile Connect customer need?” And then you reverse engineer the commercials that allow the organisation itself to make a significant amount of revenue. And then, what revenue is acceptable to us? So, it’s a true partnership model that allows us to unlock that.

Why do we have a moat? It’s quite clear that the regulator and the CompCom want more competition. They’ve been trying for years to break up a duopoly that has existed. In the last round of spectrum in ’22, they actually insisted that each MNO have one MVNO that they launch and make successful for a period of three years.

That’s why it feels a little bit like MVNO season. We’re doing it very deliberately and intentionally, and others, dare I say, might be doing it to comply (and so with no real intention of success, but we’ve given it a bash). For us, it’s a very deliberate, intentional strategy.

So that’s the first, the breaking up of competition, which gives you the support of the regulator and of the CompCom.

The second is that, given the pricing that we have and the levels of margin that are acceptable to us – so, I’ve now gone capex-light. I’m only 900 staff on my payroll compared to 4,000, 4,500, 5,000 of other competitors. So I can live with acceptable margins that are fundamentally different, and I can price into a position that’s acceptable to me, with acceptable margins, and still make the MVNO partners very successful in their own right.

We align very deeply on their strategy. So one partner may want the rewards programme, the other partner may want a reduction in costs in data fees, as an example, when customers are using the app. So, that alignment of strategy is very good.

We’re also the only network operator that hasn’t signalled to any of the financial services players that we want to be a financial services player. So the others, strategically, are not aligned because they’re holding up a flashing light that says, “We’re coming for your banking customers! We’re coming to eat your lunch, because we have these financial services products.” Whether they’re MoMo or VodaPay, etcetera. We’re not. We’re partnering deeply, so it’s all lining up.

And then, probably lastly, is that if one of the bigger players did want to go to our MVNOs, they could. They’d have to come in and price right below where we are, and if they did that, then two things would happen.

The first is that they would cannibalise their own revenue fastest. Because today, factually, 10% of the MVNO customers port from Cell C. The other 90% port from all the other networks. So, out of 10 customers, we lose one to ourselves. And as I said earlier, the contribution margin and economics – I’m perfectly okay with that. The other nine are net gainers.

And so it stands to reason that if a yellow or a red wanted to go in this direction, they would lose a significant amount of their own customers to the MVNO, and they would lose their retail revenue. So, it’s a decision they would have to make, to compromise their retail revenue quite significantly in favour of wholesale revenue.

It’s not a bad strategy. I just think it’s one that’s difficult to make, given how much revenue is sitting in this and how much pressure you’ve now seen just on Prepaid alone, in the last couple of quarters in the declining space there. So we really do believe that we have a moat.

So, I said the first thing is that they will erode the retail revenue. The other thing is that it could then, depending on where the price points reach, compromise the wholesale pricing. And if your retail pricing then breaches your wholesale pricing, you have margin squeeze. And then you have, again, competition and regulatory matters that would kick in to say, “Well, this is not the way that things should work.”

So, we really do believe that the way we’ve priced ourselves (and we keep repricing to the MVNOs, to keep them competitive) does not allow the bigger players to come and play in that space, because the cannibalisation of their own revenue is far too high.

The Finance Ghost: Jorge, thank you. That’s super interesting, and you’ve really given me a lot more insight into the MVNO space. Some great points there.

I’d like to talk now about some of the growth prospects for Cell C and some of the drivers of that. So, the one thing you mentioned there, it sounds like there are specific conditions for your partners to work. You need digital distribution, high utility, etcetera. Maybe there’s a limit then to the number of potential partners in South Africa? I guess there is a practical limit.

So the growth drivers there, I guess, would be maybe winning more of those over time, but there’s probably a practical limit to that. So what would help you in South Africa would be overarching macroeconomic growth, right? And the wonderful news is that, at the moment, South Africa is looking better than it has in quite some time.

So I’d like to understand from you, for a few minutes, the big growth drivers. If you could really sit down, what’s the wish list of what you wish was happening to actually hit those growth flywheels that underpin not just your medium-term targets in the IPO documentation, but allow you to even beat those over time?

What would it be? It would be a macro story in South Africa, I’m sure, but what else?

Jorge Mendes: Yeah, absolutely. In my mind, the role of government is to cultivate the land, to make the soil conducive to really good economic growth. So, what’s a little bit more optimistic than in the past is that I think the GNU is delivering a fair amount of competition between ministers. And that’s stacking up quite well. That’s creating a bit of a healthy competition there.

I think Mteto and Dan at Eskom have done an incredible job there to turn around the electricity grid. That was hampering growth, for sure. In the telco space alone, I know there were billions in investment that were going into batteries just to ‘keep the lights on’, so to speak. And that’s wasteful, because nothing else has happened other than just having what you had before. Very, very wasteful.

It has unlocked solar, so I think there is a lot more green energy that will come from that. But I think the energy grid is a very important part. I think the political climate’s better. The fact that we’re off the grey list is fundamentally different, so we’ll be viewed a little bit more seriously. I think those are good things.

There’s still economic pressure, there’s no doubt about it. The unemployment rate is still too high. Education levels are not where they should be, in terms of pass rates and equality and so on.

But I think what’s starting to happen is a lot of movement going into the township economy. You’re seeing fibre players coming up. R5 a day for unlimited Internet access. That is going to unlock economic activity, no doubt about it.

So we want to be in that space, we want to play in that geography all day long. We want to make sure that we participate in inclusion through a digital economy for everyone. We take it too flippantly, sometimes. If you can get someone who for R5 can connect to the internet, suddenly there’s a little bit of a job creation opportunity. Whether it’s from influencing or just putting themselves out there, from a basic painter job or gardening or a car guard today can get paid through a QR code.

These things are starting to change. Shoprite has this programme now, where you buy a QR code inside for R5, you then pay the car guard with it, and they redeem that for groceries. So those kinds of things are starting to add some tremendous value.

When the economic activity has optimism – and I think this is what the Cell C brand has now brought back into the telco space, is hope, optimism, a fresh energy. And I’m not trying to sound like the messiah of the industry. We’re the smallest player; we know our position right now. But we do have lots of hope, lots of opportunity and lots of credibility that’s now come back in.

I think when you put those ingredients together, and you partner deeply with Cell C, we can share in growth, we can share in the aligning of the strategy. And that’s a different approach. It’s not just meant to sound like fancy words.

So, economic outlook is more positive. Conducive environment. That’s looking a lot more optimistic. I think prices will always come down. You want connectivity to become more and more affordable. You’re seeing handset financing, you’re seeing better hardware coming into the country.

So, the availability of a great device that today, if you look at your device, you don’t know if it’s a phone, a calculator, a camera, a diary, a calendar, a trading platform, and the list goes on. It’s an all-in-one that unlocks a lot. We want to be right at the forefront.

And then there’s also a lot of opportunity in enterprise and public sector that we haven’t participated in. I think that’s quite interesting for us. We haven’t played in that space at all.

The Finance Ghost: Yeah, it’s speaking my language 100%. I absolutely share that view with you that access to internet is a game changer. That is the number one thing that marginalised communities desperately need in this country, so that’s excellent. I’d love to see anything in that space.

I’ve only got you for a few minutes still. Jorge, let me ask you the last question, which is – and it’s just so fascinating to follow the whole Cell C Story, right? It’s been around for so long, but in so many different iterations. It’s felt like a startup almost throughout. It’s like a pivot, and then, “Oh, it doesn’t work.” Recap. Pivot. “Oh, it doesn’t work.” Recap. Pivot. “Oh, it’s working.”

So, as you look back now. One of the investment highlights in the IPO deck talks about ‘turnaround delivered’, which is strong wording. That means, “We’ve done it, we’ve done the turnaround, we’re ready for growth.” Now, as you look at the balance sheet, as you look at what’s happened, as you look at now being distinct from Blu Label, etcetera.

If you could just spend a couple of minutes on what gives you the confidence to say that? Why do you believe it’s now behind you, this turnaround, and you’ve got this platform for growth?

Jorge Mendes: Yeah, thanks. That’s a very good question. And firstly, I’m very honoured and privileged to be able to be in this position. I think a lot of great names have come before me. Strategies are easy to assess looking backwards – “That was clearly the wrong thing” – but clearly, no one goes into a strategy upfront saying, “I hope I fail so that someone can write a story about it.” So, there have been great names that have come before me.

It’s a household brand. It’s 24 years old. Why I say turnaround delivered, certainly in the two-and-a-half years I’ve been in the role, I know what we inherited in terms of the organisation. So, that’s balance sheet, financials, creditor stretch, the type of organisation, the strategy, what we had in systems and people and all of that.

We’re up to date on everything in terms of payments, the creditor stretch is down to nothing. That was in the billions. We’ve removed costs – that was not there. We had all sorts of things happening in the organisation – that’s completely clean. Our balance sheet is now just trading debt, so that’s a fantastic position. We’ve been ‘unshackled’, so to speak.

And I think an important part of getting to a listing is that it gives credibility when you meet the JSE requirements. And we did. I think it’s called the section 144A, which is the US listing. It’s a very stringent process. So, what it does is suddenly, as a listed entity, you have a different level of credibility.

So, where perhaps it was murky, and “We’re not sure those guys are still going to be around, what’s their financial position? Will they survive?” That starts changing immediately because the level of scrutiny and governance (and I’ve always operated personally in environments this way), it changes overnight. So, our financial position is fundamentally different.

The execution over the last two years has been nothing short of remarkable and relentless in what we’ve done in a very short space of time. With systems, with the brand, with the financial position, with clearing debt, with changing the balance sheet, it’s done.

It’s not happening. It’s not “possibly” – it is done. It is behind us, and now it allows us to compete favourably. So we were like a Mvela Golden League team that arrived to play a Premiership team. We had different-coloured socks. We had borrowed boots. We made a plan on transport and how to get to the game, and somehow we delivered a result.

And now we’ve been promoted to the Premiership. And we’re at the beginning of this new journey, and the resilience and the scars on our back that we’ve learned. And we have to remain humble, we have to remain professional, we have to remain accessible, and we have to remain a win-win organisation.

Through deep partnerships, I think we will unlock tremendous value. So, I’m less interested about the share price. We didn’t talk about it that much and you said right up-front that it’s about the IPO. The value is the value. It doesn’t really matter because I am very confident.

I’ve never been more convicted in my life that the value and the growth in this organisation is there. It’s a strong growth story, it’s a strong cash-generative business. But it’s only because we will do all the right things, and then those KPIs will follow.

So, normally, if you focus on the share price, you don’t run a business that well. But if you focus on running a business that well, normally you get rewarded in the share price over time. And I think that’s the consistency we’re looking for and the credibility that we have to bring. Hopefully, we can make all stakeholders and shareholders proud of this organisation in future.

The Finance Ghost: Yeah, I love that. And just to be clear for the listeners, it wasn’t that I was asked not to ask you about the share price. I said I don’t want to because I personally get nervous when CEOs start talking about the share price. The share price is a function of a million things, and all you should be worrying about is running the business. So, I love that you think that way, because it’s the right way.

So, Jorge, this has been amazing. I did note you started as a call centre agent in the 1990s. So, you’re well versed in doing podcasts, which explains why you’re so good at this.

Thank you so much for your time, and just, good luck. I certainly hope this won’t be our last podcast. I look forward to following the Cell C story and writing about it in Ghost Mail. And yeah, really, all the best.

It’s exciting to see these new listings on the JSE. It’s exciting to see some growth in South Africa, some excitement and more competition in the telco space. The winners there are the South African consumers, which is obviously great for everyone. So, congratulations and thank you.

Jorge Mendes: Thank you very much. Really appreciate it. Thanks for the time today.

Anglo American and Teck Resources shareholders approve the merger (JSE: AGL)

Hopefully, the “merger of equals” spam will soon leave us on SENS

If there’s one thing that Anglo American has tried very hard to convince us of, it’s that the deal with Teck Resources is a “merger of equals” – and the problem is that it actually isn’t. If it was a merger of companies of similar value, they wouldn’t need to shout at us constantly about it!

Anyway, the merger of not-really-equals has been approved by the shareholders of both Anglo American and Teck Resources. The combined group will have more than 70% of its exposure in copper. It’s incredible to see the focus on copper among the mining giants. They better all hope that demand doesn’t disappoint.

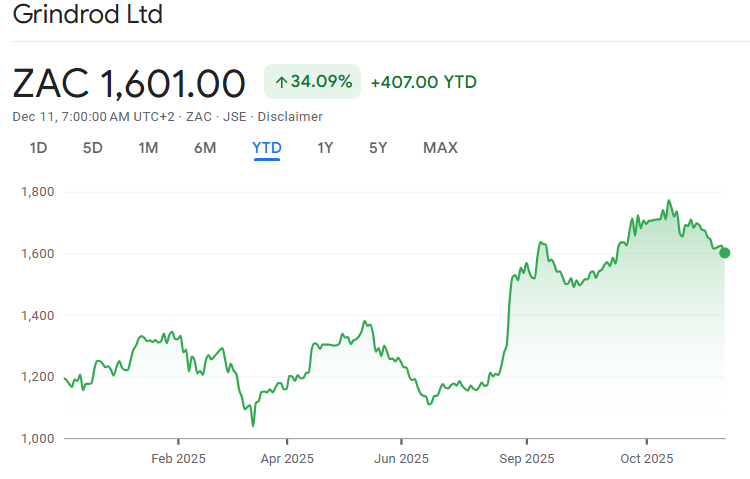

Grindrod releases a sobering update after a strong share price run (JSE: GND)

This chart looks vulnerableto me

Grindrod is up 34% year-to-date. The share price made it all the way up to R18 before falling to the current level of R16. It looks less stable than your favourite uncle after his 8th drink at the family Christmas jol:

The pre-close update is a mixed bag, so that makes this chart even more interesting. As you’ll shortly see, volumes are weak but margins are strong.

Mining commodity markets have had a tough year once you go beyond gold and platinum. Grindrod’s dry-bulk commodities experienced a 12% decline in the period. Demand for iron ore and chrome was thankfully resilient, but the reality is that Grindrod makes more money when its mining clients are making more money and shipping more products.

The dry-bulk terminal at the Port of Maputo exported 13.9 Mt for the period vs. 13.2 Mt in 2024. Grindrod’s dry-bulk terminals were good for 15.2 Mt vs. 15.5 Mt last year. Elsewhere in the business, the ship agency and clearing/forwarding operations were described as “resilient” and the recovery in the container and graphite handling businesses is slow. Low deployment of locomotives impacted their rail performance. Overall, other than Port of Maputo, volumes look tough.

The saving grace is the margin story. In the Port and Terminals segment, EBITDA margin increased from 35% to 39%. The Logistics EBITDA margin, excluding transport brokering, is down from 27% to 25%. Thankfully, Port and Terminals is the most profitable part of the business (headline earnings of R448 million in the interim period vs. R140 million in Logistics). And at Port of Maputo, the share of earnings increased by 5.6% to R338.3 million.

Although gross debt increased from R2.9 billion to R3.7 billion, the group actually improved from net debt of R0.4 billion to net cash of R0.2 billion.

There are some good news stories in here, but is it enough to support such a sharp increase in the share price this year?

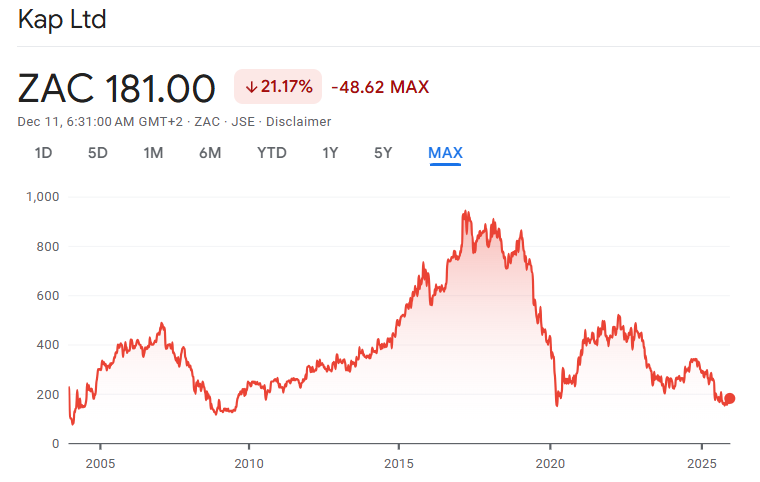

Has KAP finally found the bottom and turned higher? (JSE: KAP)

This update is strong and the market liked it

KAP closed a casual 13% higher on Wednesday on strong trading volumes. The share price is still very ill, as this long-term chart shows:

You can’t see it on this chart, but the share price is down 38% year-to-date even after the rally on Wednesday. If the bottom is indeed in, then there’s a long runway for a turnaround.

The results for the year ended June were poor. They were hit by major pressure points, including lower OEM vehicle production that impacted the Feltex business, as well as the ramp-up costs of the PG Bison MDF line that was commissioned during a period of weak demand. It’s a low base for comparison, so take that into account when you consider the trading statement for the six months to December 2025 that reflects an increase in HEPS of more than 20%.

Here’s another thing to keep in mind: the concept of “at least 20%” is the bare minimum disclosure for a trading statement. It could be only slightly higher, or it could be much higher. In all likelihood, a further trading statement will be released in January.

Where has the improvement come from? Well, PG Bison has increased its volumes and seen a better performance in revenue and operating profit. Unitrans managed to improve margins despite a decline in revenue, as the transport company is focusing on higher margin work. Feltex enjoyed higher domestic vehicle assembly volumes.

Of course, as we are accustomed to at KAP, there are one or two divisions that are still having a bad time. Safripol is the most worrying one, as this is a core division that is struggling with overcapacity in the market. It’s so bad that they stopped production at the PET plant in Durban for five weeks to rather work their way through elevated inventory levels! Both revenue and profit were down vs. the prior period at Safripol.

Finally, obscure startup Optix suffered a decline in profit. It’s long overdue that KAP got out of this one.

The scary capex cycle is behind them, with spend over the next three to five years focused on higher capacity at PG Bison and improving the average fleet age at Unitrans.

Aside from a target like R700 million annual operating profit at Unitrans over the medium term, the group is targeting a net debt reduction of R500 million in FY26. That will certainly help.

It’s great to see some positivity at KAP. But time has taught me that this diversified industrials group always has a headache somewhere, so I’m approaching it with caution. The market really loved it though, as evidenced by the share price jump.

Libstar exits fresh mushrooms and is still in talks with potential acquirers for the whole group (JSE: LBR)

The share price has been volatilein anticipation of a potential deal

As you can see on this chart, Libstar’s share price was deep in a hole earlier this year. Like the fresh mushrooms that it is now disposing of, the chart managed to spring up overnight in response to news of a potential acquirer swooping in for Libstar. Since then, it’s been choppy:

The good news is that Libstar is still engaging with the potential acquirers regarding the expressions of interest that were received. There’s no guarantee of a deal going ahead, but there’s still a good chance.

The other good news is that the company is moving ahead with cleaning up the group. For example, they’ve announced the disposal of the fresh mushroom business, other than the property in the Western Cape and the Denny brand itself which Libstar will license to the purchaser. This is because Libstar wants to keep producing certain Denny-branded products. The disposal will trigger a loss on sale of between R45 million and R55 million. This is an accounting measure of the difference between the book value of the assets and the selling price. It isn’t a reflection of whether the sale is the right decision or not.

Libstar is also assessing non-binding expressions of interest regarding the remaining Household and Personal Care business. They need to get out of that space and simplify the group as soon as practically possible.

To give a sense of trading performance, they’ve delivered a pre-close trading update for the 47 weeks to 21 November. They’ve excluded the fresh mushrooms business that is being sold anyway.

Revenue increased by 6.7%. There were some significant extraordinary items due to bulk sales, inventory clearances and business closures. If you adjust for this, then volumes were up 3.1% and price/mix contributed 3.6%. Encouragingly, gross margins were up for the year, so that speaks to an improved trading performance overall.

They are also on track to deliver the year-end debt guidance, with net debt to normalised EBITDA improving from the 1.3x reported for the interim period.

Looking at the segments, Ambient Products looks fine, with revenue up 5.6%. Volumes were down 0.4% (or up 4.5% on an adjusted basis) and price/mix contributed 5.9%. But then we get to Perishables where things went rather mad, with revenue growth of 8.1% thanks to wild swings of positive 23.2% in volumes and a price/mix reduction of 15.0%. The adjusted volumes growth is 1.4%. You can see why they’ve disclosed the adjusted numbers to try and give investors a better idea of the true performance.

Results are due for release on 17 March. The big question is whether some kind of deal announcement will happen before then.

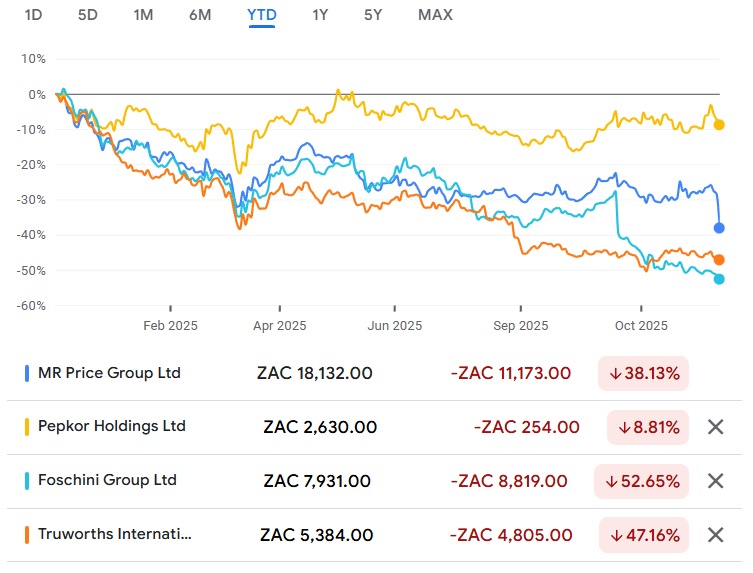

Mr Price throws a stick of dynamite at its investment thesis – and share price (JSE: MRP)

The share price tanked 13.7% in response to this inability to read the room

Until Wednesday, there were two types of FMCG companies on the local market right now: those who are executing turnarounds, cleaning up after a decade of dicey deal making and reaping the rewards, and those who haven’t figured out yet that the market is tired of ownership of non-core assets.

But now we have a third type: Mr Price. 2014 called and wants its dumb offshore strategy back, please.

In an announcement of a deal that feels like a fever dream, Mr Price announced the acquisition of 100% (first problem) of European (second problem) value retailer NKD Group GmbH from a private equity seller (third problem).

Let’s just deal with the three immediate issues.

Firstly, offshore acquisitions should always be a smaller stake with a pathway to control and eventually 100% once the business is fully understood. Running straight into a 100% stake is such poor structuring that I can’t believe the board signed off on this.

The second issue is that this business is in Europe. How many more South African retailers are going to try and get it right in Europe? NKD may be an apparel and homeware retailer in Central and Eastern Europe and thus Mr Price feels like they understand that model, but we have endless examples of local management teams who made similar mistakes in faraway lands.

Thirdly, the seller is a private equity house. Buying from private equity is rarely a great idea. These people are experts at packaging a business with a big shiny bow on it, even if the underlying business has issues. They are also focused on maximising the exit price. Negotiating with private equity houses is a dance with wolves. You might get it right, but there’s a good chance of getting bitten.

We then get to the biggest issue of all: instead of dipping their toes overseas, Mr Price has dived headfirst into a rip current near the rocks. They are paying a whopping R9.66 billion for the group, or roughly a fifth of the Mr Price market cap after the obliteration of the share price (down 13.7% on the day) in response to this news.

Mr Price notes that NKD achieved sales of nearly R14.2 billion in 2024. They are therefore paying nearly 0.7x sales for the acquisition. Yes, that’s less than the 1.2x that Mr Price trades at, but it’s not cheap.

With NKD expected to be roughly 25% of group sales after the acquisition, they are literally baking in a substantial drag on the group valuation until they rebuild trust in the market. The old days of roll-up strategies where you buy something “cheap” and the market magically re-rates those earnings once you own them are far behind us.

As a sign of just how significant the shift in sentiment in response to offshore deals has been, most of the deal value was wiped off the Mr Price market cap a short while after the announcement. The market has declared this acquisition to be almost worthless. That might be an opportunity for those willing to trust the Mr Price management team in the hope that they won’t do any more bonkers deals.

NKD did generate a significant net loss in the 6 months to June 2025, but that was because of debt refinancing and hedging derivative valuation charges. If you remove those, profit after tax was roughly R129 million for the six months. How exciting. If you go back to December 2024, the annual profit was R261 million. This means that Mr Price is paying a Price/Earnings multiple of 37x for this asset.

What on earth are they thinking?

They describe NKD as a “high performing business with a strong track record” and they talk about how value retailing is growing in popularity in Europe. They also talk about “limited distraction for both management teams” – goodness knows nobody is going to take that seriously. No amount of perfume can possibly be put on this valuation pig.

As the final nail in the coffin, they have to fund this with a mix of existing cash and debt.

This is a Category 2 transaction, so shareholders won’t be asked to vote on the transaction. They voted with their feet though, as shown on the share price chart. Unsurprisingly, Mr Price’s share price has now dived down towards where Foschini Group (JSE: TFG) and Truworths (JSE: TRU) find themselves:

The biggest irritation is that my entire investment thesis here was based on Mr Price being a simpler group than peers with more focused exposure. It was working, with Mr Price having stabilised at my in-price and looking good for a recovery towards where Pepkor (JSE: PPH) is trading. Mr Price has now thrown a stick of dynamite at that thesis and people are quite rightfully angry.

Nibbles:

Director dealings:

Now here’s a share purchase worth paying attention to: two entities associated with Johnny Copelyn, the CEO of Hosken Consolidated Investments (JSE: HCI), bought shares worth almost R119 million! That’s a serious show of faith.

Nampak (JSE: NPL) CEO Phil Roux’s hedging transaction has been closed out and the underlying shares have been sold in the market. The value of the transaction that was unwound is R49 million.

An associate of a director of Lewis Group (JSE: LEW) bought shares worth R41k.

African Rainbow Minerals (JSE: ARI) announced that they have received R1.5 billion from Assmang in respect of the year ended June 2025.