Mergers and acquisitions (M&A) in Africa have traditionally presented complex challenges, including intricate regulatory landscapes, extensive due diligence requirements, and the need to navigate diverse legal systems. For foreign investors seeking opportunities within Africa’s expanding markets, these complexities have often resulted in increased costs, prolonged timelines, and heightened risks. However, the advent of legal technology is transforming M&A transactions across the continent, introducing efficiencies that mitigate these challenges and foster a more streamlined deal-making process.

From due diligence to post-transaction integration, legal technology is revolutionising core stages of M&A transactions, offering tools that enhance accuracy, reduce human error, and improve decision-making for stakeholders.

REVOLUTIONISING DUE DILIGENCE

Due diligence is one of the most critical phases of any M&A transaction, providing the foundation for informed decision-making. Historically, legal teams would manually review extensive documentation over several weeks or months, a time-consuming process susceptible to human error. Today, artificial intelligence (AI)-powered tools, employed by leading law firms such as DLA Piper, are automating this process with remarkable efficiency.

These tools leverage machine learning algorithms to review voluminous datasets, identify risks, and highlight key information in a fraction of the time required for manual analysis. By automating repetitive tasks, these technologies ensure comprehensive and accurate due diligence, enabling foreign investors to better assess potential risks and opportunities. This is particularly advantageous in Africa, where access to reliable data can be inconsistent.

STREAMLINING CONTRACT NEGOTIATION AND REVIEW

Contract negotiation and review are central to M&A transactions, which require meticulous scrutiny to ensure alignment with legal requirements and the interests of all parties. Legal technology now plays a pivotal role in this area, utilising AI-driven tools to analyse contracts, identify critical clauses, and detect discrepancies or risks.

These platforms not only expedite the contract review process but also assist legal professionals by suggesting edits and ensuring compliance with local laws and regulations. In Africa’s diverse legal environment, such tools are invaluable for tailoring contracts to address jurisdiction-specific challenges. Consequently, investors can approach transactions with greater confidence, knowing that agreements are both legally sound and strategically advantageous.

OPTIMISING DEAL STRUCTURING AND INTEGRATION

The structuring of M&A transactions often involves balancing complex considerations, including regulatory compliance, financial implications, and strategic goals.

Legal technology facilitates this process through predictive analytics and data-driven insights, allowing negotiators to evaluate various deal structures and simulate potential outcomes.

For transactions within Africa, where regulatory requirements can vary significantly between jurisdictions, these tools are instrumental in ensuring compliance and reducing the risk of post-transaction complications. Furthermore, legal technology supports post-deal integration by managing data, streamlining communication, and providing project tracking capabilities, thereby enhancing operational efficiency and long-term success.

ETHICAL CONSIDERATIONS AND EMERGING RISKS

While legal technology offers significant benefits, it raises ethical concerns, particularly around data privacy and AI reliability. AI tools rely on vast datasets, often containing sensitive financial and personal information, increasing the risk of data breaches. In Africa, where data protection laws are still evolving, companies must ensure compliance with local and international standards.

The reliability of AI-generated outputs depends on the quality of training data. Biases or inaccuracies can lead to misleading results, as seen in Mavundla v MEC: Department of Co-Operative Government and Traditional Affairs KwaZulu-Natal and Others (2025). In this case, a law firm faced scrutiny for citing fictitious case law, potentially AI-generated. The court dismissed the appeal after finding most references were non-existent, highlighting the need for rigorous oversight.

AI also has financial and environmental costs. Training large models requires vast computational resources, contributing to carbon emissions. The recent release of DeepSeek by China has intensified market competition, raising concerns about AI’s sustainability. Legal professionals must balance AI’s efficiencies with its ethical and environmental risks, ensuring it enhances rather than undermines legal integrity.

THE REGULATORY LANDSCAPE FOR AI IN AFRICA

As the adoption of AI accelerates, several African countries are developing frameworks to regulate its use. While no jurisdiction has enacted AI-specific legislation as of January 2025, notable advancements have been made:

Egypt: Released the Second Edition of its National Artificial Intelligence Strategy 2025–2030 in January 2025.

Ghana: Published the National Artificial Intelligence Strategy 2023–2033 in October 2022.

Kenya: Unveiled the Kenya National Artificial Intelligence Strategy 2025–2030 in January 2025.

Nigeria: Introduced a draft National Artificial Intelligence Strategy in August 2024.

South Africa: Released the National Artificial Intelligence Policy Framework in August 2024, emphasising ethical AI use, personal information protection, and enhanced government efficiency.

These initiatives reflect a growing recognition of AI’s transformative potential, coupled with the necessity of safeguarding ethical standards and data privacy.

The integration of legal technology into M&A transactions is reshaping the African deal-making landscape, offering tools that enhance efficiency, reduce risks, and ensure more successful outcomes. By automating labour-intensive processes such as due diligence, matter management, and contract review, and by providing actionable insights for deal structuring and post-transaction integration, legal technology is enabling investors and legal professionals to navigate the complexities of African markets with greater confidence.

Nevertheless, the adoption of these technologies must be approached with caution. The Mavundla case serves as a stark reminder of the potential pitfalls of uncritical reliance on AI, underscoring the need for human oversight and ethical diligence. As Africa continues to refine its regulatory frameworks for AI, legal practitioners must strike a balance between embracing innovation and safeguarding the principles of accountability and professionalism that underpin the legal profession.

Tevin Ramalu is an Associate Designate and Lemont Shondlani a Candidate Legal Practitioner in the Corporate Department. Supervised by Amy Eliason, a Director | DLA Piper Advisory Services

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

I’ve had the immense joy (quite recently, actually) of seeing the view from the top of the Portside building. It’s every bit as spectacular as you imagine it would be. In case you aren’t familiar with the Cape Town CBD (the only functional CBD in the country), Portside is the very tall glass building.

It’s been a painful trophy for Accelerate Property Fund, adding to the overall illusions of grandeur that got the fund into huge trouble in the first place. COVID was of course a disaster for office property, so owning the most impressive building of the lot just meant having bigger headaches. Accelerate is focused on turning the Fourways Mall around, so they can’t afford to have any other risks right now.

After making it pretty clear recently that the “For Sale” sign was outside the door of Portside, the Accelerate has now agreed a deal with Cavaleros Group Holdings for Accelerate’s proportionate ownership in the office tower. This means floors 9 – 18, along with 623 parking bays and the common areas. I checked the last annual report and based on the GLA that I found, this means a complete exit for Accelerate from the building.

The price? R580 million. The last valuation? R609 million. That’s a discount to net asset value (NAV) of just 4.7%. Meanwhile, Accelerate is trading at R0.50 per share and the NAV per share as at September 2024 was R2.60. Clearly, the discount achieved on the Portside sale is actually a massive premium to what the share price is implying.

This stock is looking more interesting by the day. They just need to keep the bankers at bay while continuing to deliver improvements at Fourways Mall.

Life Healthcare shareholders love the LMI deal (JSE: LHC)

You won’t often seen an approval rate this high

Life Healthcare recently announced a deal to sell Life Molecular Imaging (LMI) to Lantheus Holdings. The back story is that Lantheus is the counterparty to the sub-licensing agreement linked to LMI that was announced in mid-2024. During the due diligence process, Lantheus liked the asset so much that they wanted to buy the whole thing!

It’s an elegant deal for Life Healthcare. They expect to receive net proceeds of around R3.7 billion, most of which will hopefully be paid to shareholders as a special distribution within the next year. Importantly, they retain upside exposure to the LMI products, based on an earnout linked to US and global sales. The global rollout is therefore a pressure point for the Lantheus balance sheet rather than the Life Healthcare balance sheet, with Life still able to take a clip of the future economics.

I’m therefore not surprised to see that the deal got nearly unanimous approval at the Life Healthcare shareholders meeting. It’s a clever deal that has supported a 29% increase in the share price over the past 12 months.

Nibbles:

Director dealings:

A director of a major subsidiary of AVI (JSE: AVI) received share awards and sold the whole lot to the value of R874k.

The company secretary of Bidvest (JSE: BVT) sold shares worth R807k that were related to a share award. The announcement isn’t explicit on whether this is only the taxable portion.

A podcast that I recorded with Kingsley Williams will be released in the next few days. We covered a variety of concepts linked to diversification. In the meantime, you can enjoy this article by Kingsley to whet your appetite.It was first published here.

Over the last few weeks, I’ve been approached by various people seeking my perspective on the recent market turmoil, particularly in the US, where that market was down almost 6% since the end of 2024[1], and down 10% since its peak almost a month ago[2]. Investors seeing their portfolios decline in value may be questioning whether their current strategy is still right, or if a change is needed.

I always begin by asking what the investor is aiming for and how long they have to reach that goal. While other factors matter, this is the key determinant of whether their strategy is still appropriate.

At Satrix, we don’t predict short-term market movements. Markets can be highly unpredictable in the short term, and equities tend to have more volatility.

What we do know is that, over longer periods, markets behave more predictably. However, any prediction still carries a high degree of uncertainty due to unpredictable shifts in the investment, regulatory, inflation, and geopolitical landscapes. So, what can investors do to better reach their goals?

Match your investment term with the right mix of asset classes

Diversify your strategy – it’s one of the only free lunches in investing

Manage your costs

The principle is simple: riskier asset classes should be held for longer periods to pay off. In the short term, they are more volatile, but over time, their value should align more with fundamentals. Higher returns for taking on more risk make sense in the long run.

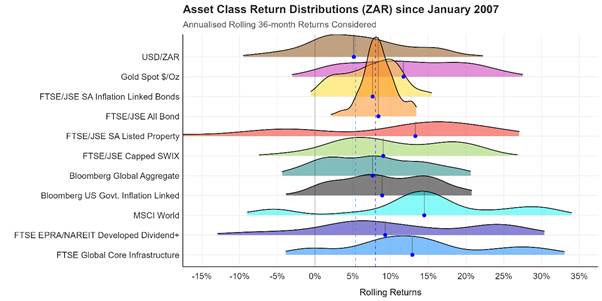

Charts comparing asset classes since January 2007 show that some, like local inflation-linked bonds (yellow) or nominal bonds (orange), have a narrower range of returns over all three-year periods, offering more certainty. In contrast, other asset classes show a much wider range of outcomes, providing less certainty over the same period.

Figure 1: Asset Class Return Distributions (ZAR), annualised rolling three-year periods. Source: Satrix, as at 28 February 2025.

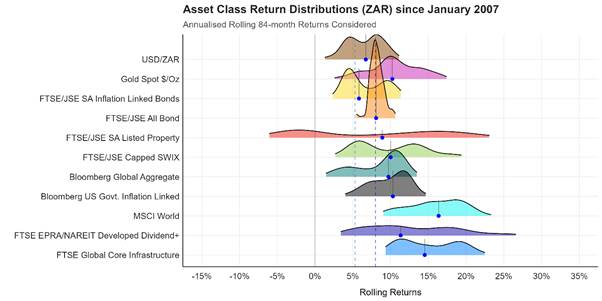

As the holding period is expanded to seven years, the return distributions of all asset classes narrow, although some narrow a lot more than others. All asset classes, except for local listed property (red), have delivered a positive return over all seven-year periods. Nominal bonds (orange) have never delivered a return below inflation. Local equities (FTSE/JSE Capped SWIX), in light green, have delivered a median CPI+5% outcome, albeit with a high degree of variability around this. What is also noticeable is how much higher the median return for developed market equities (MSCI World) has been as it has benefitted from a weakening rand and the strength of the US equity market after the global financial crisis.

Figure 2: Asset Class Return Distributions (ZAR), annualised rolling seven-year periods. Source: Satrix, as at 28 February 2025.

The purpose of showing these charts is not to provide an expectation of the return for each asset class – past performance is no guarantee of future results – but to show why more time is necessary when investing in riskier asset classes. It also shows that in most cases, but not always, more risk is generally compensated with higher returns.

Diversify Your Investment Strategy

Both within each asset class, and across asset classes, diversification allows you to reduce idiosyncratic risk to a minimum, so you’re only left with systemic risk. As one of my colleagues likes to say, “Volatility (or systemic risk), is a feature of investing, not a bug!” The only way to really manage this risk is to ensure you invest for a suitably sufficient time frame, which gives your investment time to reward you for your patience and for taking the risk.

An example of diversifying your risk would be not to hold only US equity exposure, but include broader developed market exposure in your portfolio, such as tracking the MSCI World Index. While this index is still heavily dominated by the US, it also includes exposure to Europe, Asia and Australasia. You could also consider investing beyond developed equity markets, by, for example tracking emerging market equities, which, over the same year-to-date period, are up over 3%[3]. Some of the performance delivered by indices outside of the US equity market year-to-date, over the relatively short period, show how differently markets can behave, and why you don’t want all your eggs in one basket[4]:

MSCI China: 16.7%

MSCI Europe: 12.2%

FTSE Global Core Infrastructure: 2.4%

Bloomberg Global Aggregate: 2.4%

Bloomberg US Government Inflation-Linked Bond: 2.9%

Another factor to carefully consider is currency exposure. The above global indices are all denominated in US dollars. When converted to rand, which has strengthened relative to the US dollar, these US dollar-denominated returns have faced headwinds, while our local equity market is up 3.6% in rands[5], or 5.3% in US dollars.

It is tempting to believe that what has worked for the last 10 years will continue to work for the next ten. However, markets do eventually respond to longer-term fundamentals, meaning expensive markets and asset classes are more likely to underperform their undervalued counterparts. We accounted for this when reviewing the Strategic Asset Allocation for our range of multi-asset funds. Our analysis indicated US equity markets were expensive, so instead of allocating more capital to the expensive US equity market, we increased our allocation to emerging markets during our September 2024 rebalance.

So far, this overweight tilt in favour of emerging markets relative to the MSCI All Country World Index (ACWI) – which includes exposure to both developed and emerging markets – has paid off well. As has our exposure to global listed infrastructure, which acts as a more defensive equity play. The global listed infrastructure index that we track selects companies that operate infrastructure assets, whose revenue is often directly linked to inflation, providing a highly predictable long-term revenue stream, regardless of market or economic conditions.

Similarly, our recently launched Satrix Global Balanced FoF ETF (ticker: STXGLB) – the first of its kind on the Johannesburg Stock Exchange – has overweight exposure to emerging markets and a material allocation (10%) to global listed infrastructure, which has helped soften the impact to the US sell-off.

Manage Your Costs

I think about investment costs in relation to the expected real return. A low-risk investment, like a money market fund, may outperform inflation slightly over one-three years. However, when investing for growth above inflation, costs should be considered relative to that goal. For instance, a high-equity balanced fund might be expected to deliver a 5% real return above inflation (before costs), but if it costs 1.5%, plus 0.5% for platform access, the total cost is 2%. This means the cost is 40% of the expected return. It’s no wonder investors are left disappointed when they achieve only 3% real growth, having expected 5%. The impact of compounding, especially the negative effect of fees, is significant over the long term, so managing costs is crucial.

A similar balanced fund with a cost structure of 0.50% and accessed through the same platform, would now only cost 1% or 20% of your expected return, leaving you with 4% real growth.

When investing for the long term, market corrections and drawdowns are inevitable. Staying the course and resisting the urge to make drastic changes to a well-thought-out strategy is more likely to help you reach your investment goals on time, rather than constantly realigning your entire portfolio. Eventually, the market smooths out, allowing you to reach your destination as planned. As it turns out, the S&P 500 has recovered somewhat since 13 March 2025, and is now only down 1.7% as at 24 March 2025. Avoiding the urge to act, often at the most inopportune time, is a discipline that has shown to serve investors well.

Disclaimer

*Satrix is a division of Sanlam Investment Management

Satrix Managers (RF) (Pty) Ltd is an approved financial service provider in terms of the Financial Advisory and Intermediary Services Act, No 37 of 2002 (“FAIS”). The information above does not constitute financial advice in terms of FAIS. Consult your financial adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Satrix Managers (RF) (Pty) Ltd (Satrix) is a registered and approved Manager in Collective Investment Schemes in Securities. Collective investment schemes are generally medium- to long-term investments. With Unit Trusts and ETFs, the investor essentially owns a “proportionate share” (in proportion to the participatory interest held in the fund) of the underlying investments held by the fund. With Unit Trusts, the investor holds participatory units issued by the fund while in the case of an ETF, the participatory interest, while issued by the fund, comprises a listed security traded on the stock exchange. ETFs are index tracking funds, registered as a Collective Investment and can be traded by any stockbroker on the stock exchange or via Investment Plans and online trading platforms. ETFs may incur additional costs due to being listed on the JSE. Past performance is not necessarily a guide to future performance and the value of investments / units may go up or down. A schedule of fees and charges, and maximum commissions are available on the Minimum Disclosure Document or upon request from the Manager. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Should the respective portfolio engage in scrip lending, the utility percentage and related counterparties can be viewed on the ETF Minimum Disclosure Document. A fund of funds portfolio is a portfolio that invests in portfolios of collective investment schemes that levy their own charges, which could result in a higher fee structure for the fund of funds. International investments or investments in foreign securities could be accompanied by additional risks such as potential constraints on liquidity and repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk, settlement risk as well as potential limitations on the availability of market information.

iOCO has been focusing on margins – and with great success (JSE: IOC)

Life-after-EOH is showing positive momentum

In case you’ve forgotten or haven’t really kept up with this story, iOCO is the renamed EOH. What is in a name, you ask? Well, in this case, quite a bit. Instead of focusing on legacy issues and getting tons of bad press, the company is working on getting its profits to head in the right direction.

This is working, despite a drop in revenue of 6.4% for the six months to January 2025. With gross margin up 300 basis points to 30%, gross profit increased by 2.8%. The real highlight is on the EBITDA level, which improved by a massive 159%. EBITDA margin increased from just 3.1% to 9.2%!

This is the joy of coming off a really low base for margins. Below the EBITDA line, there’s further room for improvement thanks to a reduction in net finance costs. These factors are why HEPS swung wildly from a loss of 11 cents to profit of 19 cents per share.

The share price is up 176% over 12 months, which is obviously immense. At the current share price of R3.16, simply annualising the interim result to get to earnings of 38 cents per share would imply a P/E of 8.3x. This isn’t exactly a demanding valuation, but isn’t a bargain either. To really push the share price beyond this level, they would ideally need to show the market that iOCO can become a revenue growth story, not just a margin story.

With plenty of narrative in the results around plans for revenue growth, they just might get it right!

A wobbly at Kore Potash (JSE: KP2)

There’s a delay to the Summit Consortium term sheet

Oh boy. So it begins. Despite the Summit Consortium having an incredibly long lead time to think about how to finance the Kola project that Kore Potash is putting together, the consortium has missed the communicated deadline to submit a non-binding financing term sheet.

Kore Potash expected to receive it by the end of March. With various excuses linked to religious holidays, the consortium has now asked for more time. They expected to deliver it before the end of April and “hopefully” by the middle of the month.

Hope isn’t what investors want to see here. They want to see a funding deal for the project. Although it’s entirely possible that everything is still on track, this is the kind of wobbly that gets people concerned.

Renergen’s quarterly update comes after a period of extreme price volatility (JSE: REN)

The share price is up 96% over one month and just 2% year-to-date

The latest Renergen quarterly update is certainly one of the more interesting ones. As usual, there’s good news and bad news.

An example of bad news is that Renergen still doesn’t know how to fill large iso-containers at the extremely cool temperatures needed. The good news is that they’ve figured out a plan B with smaller containers. They did at least fill a smaller container during this quarter, which is why the share price went nuts.

Quietly in the background, LNG production increased 22% quarter-on-quarter. That’s clearly good news. It just has little bearing on the long-term investment case.

Speaking of the investment case, we now get to the scary stuff. The dispute between Tetra4 (Renergen’s South African subsidiary) and Springbok Solar was heard in the High Court on 20 February. Judgment has been reserved, which means that the court is taking its time to deliver a ruling. In the meantime, Tetra4 has filed an appeal with the Department of Mineral Resources regarding the approval that the solar developer obtained. The fight continues, with potentially severe consequences if the court rules against Renergen.

Despite the uncertainty, the show must go on in terms of finding funding for the development of the helium asset. Renergen included some commentary in the announcement about working on a liquidity solution to enable the completion of Phase 1, with negotiations expected to be concluded in the coming weeks. That could mean anything, to be honest.

On the exploration side, there was no drilling during this period. Instead, the focus was on analysing previously obtained data.

Never a dull moment then, with all eyes on the court case.

Nibbles:

Director dealings:

The founders of Discovery (JSE: DSY) are fans of putting hedges in place over their shareholdings. This strategy seems to have rubbed off on the CEO of Discovery Bank, who has put a collar in place over R20 million worth of shares. The call strike price is R248.86 and the put strike price is R200.63. For reference, the current price is R205, so this collar is strongly focused on protecting against downside risk from this level. The expiration date is March 2027.

A non-executive director of Shaftesbury Capital (JSE: SHC) bought shares worth R450k.

An entity related to the chairman of Stor-Age (JSE: SSS) bought shares worth R434k.

In the recent Fortress Real Estate (JSE: FFB) dividend election, a number of directors of Fortress and/or NEPI Rockcastle (JSE: NRP) elected to receive shares in NEPI instead of a cash dividend. Remember, Fortress holds a substantial investment in NEPI and has been using that stake strategically for capital structure purposes. Receiving the NEPI shares was the popular choice, with holders of 90.57% of Fortress B shares making that election.

In one of the smallest director dealings I’m sure you’ll see for a while, a director of Cilo Cybin (JSE: CCC) bought shares worth just R2k.

Sibanye-Stillwater (JSE: SSW) hasn’t had much in the way of good news lately, although the share price is up a meaty 40% year-to-date based on a run in platinum prices. Although I don’t think the latest announcement is the kind of news that can move the share price, it’s still good news for renewable energy enthusiasts that the Castle wind farm has achieved commercial operation. This is the largest private offtake wind farm in the country, located near De Aar in the Northern Cape and providing power to Sibanye’s operations via a wheeling agreement with Eskom. This is a prime example of Eskom’s infrastructure being used for transmission rather than power generation. This project is expected to supply 5.5% of Sibanye’s energy needs in South Africa at a significant discount to what Eskom power would cost.

Shaftesbury Capital (JSE: SHC) didn’t waste any time in getting the deal to sell a 25% stake in Covent Garden across the line. It’s all done and dusted, which means that Norges Bank Investment Management is now the proud owner of a minority stake in this excellent London property.

In similar deal news, Mondi (JSE: MNP) has completed the acquisition of the Western Europe packaging assets of Schumacher Packaging. This adds to Mondi’s existing European network of corrugated solutions plants. Despite the name of the asset being acquired, this deal wasn’t that quick to get across the line, with the initial announcement having been made in October 2024.

Lighthouse Properties (JSE: LTE) has finalised the price for the scrip dividend. Those who elect to receive a scrip dividend (i.e. more shares in Lighthouse) in lieu of a cash dividend will receive shares based on a calculation that is takes into account a 2% discount to the Lighthouse price on the JSE on 31 March (adjusted for the amount of the cash dividend). In other words, there’s a minor discount.

The CFO of MAS (JSE: MSP), Nadine Bird, has resigned with effect from 30 June 2025, having been in the role since February 2023. After much was achieved around the debt management strategy, this was a successful, albeit short stint. A replacement has not been named as of yet.

Accelerate Property Fund needs another rights offer – but there are positive signs (JSE: APF)

This is a good example of a company that is shrinking into prosperity

Bigger isn’t always better. In some business models, scale is your friend and is practically a necessity for survival. In others, scale adds limited benefit and can quickly become a disaster if the building blocks aren’t in place.

Accelerate Property Fund falls into the latter bucket, with the fund having gotten itself into all kinds of trouble under previous management. This has led to significant property sales (R700 million done and R1.2 billion still to go) to reduce debt and get the balance sheet under control. There was also a R200 million rights offer recently. The company has just announced the need for another R100 million rights offer, so the equity injections aren’t over yet.

Is there light at the end of the tunnel? There might be, provided that Fourways Mall makes the shift from white elephant to prize beast. The fund brought in Flanagan & Gerard and the Moolman Group in a last-ditch attempt to address the large vacancy rate in the mall. It’s down from 19.0% to 13.4%, so the strategy seems to be working. The mall had a decent increase in sales at the end of last year. R144 million in capital expenditure has gone into improving the mall, with further projects including a roof on the upper level parking deck and a new solar plant.

The headroom for these projects has been created by a reduction in debt from R4.4 billion to R3.7 billion, along with asset disposals that are in process and the rights offer of R100 million that will take place soon. As a show of support for the strategy, the commercial lenders have renewed Accelerate’s entire debt book for two years.

Once all is said and done, they expect the loan-to-value to be below 40%. If they can get the metrics at Fourways Mall right, then this could be a pretty lucrative deep value play in the local property sector. Is this dog finally going to have its day?

AECI is looking to sell its public water division (JSE: AFE)

The deal is too small to be categorisable under JSE rules

AECI has entered into a binding memorandum of agreement to sell Improchem’s public water business. Improchem is a wholly-owned subsidiary of AECI. The buyer is a B-BBEE investment entity owned by Nsukutech and Tanzanian group Junaco Limited. Junaco supplies water treatment chemicals and equipment across Eastern and Southern Africa and has partnered with AECI for 15 years, so the parties know each other well.

There are various regulatory hurdles that need to be overcome. You won’t see much more in the way of detail on this transaction, as it falls below the categorisation thresholds in JSE rules. These are the thresholds that trigger more detailed disclosure. AECI technically didn’t need to announce anything at all, so at least they gave the market a few details on a voluntary basis.

This disposal is part of the strategy to focus on core businesses at AECI.

Separately, the company announced that the disposal of Much Asphalt has now been completed. The final price was in line with the guidance of R1.1 billion. Remember, many deal structures allow for the final price to vary based on changes to working capital in the business while the deal is being implemented.

ArcelorMittal is deferring the decision to shut the Long business (JSE: ACL)

The IDC is coughing up to kick the can down the road

ArcelorMittal is in a difficult position. Viewed purely through a profit lens, the Long business should’ve been gone ages ago. Viewed through a social lens, it would be a complete disaster for the small towns that rely on this business. ArcelorMittal needs to try and manage being a good corporate citizen and not letting its shareholders down.

After extensive engagement with government (and I suspect plenty of examples of calling each other’s bluff), we finally have an update that sees the Long business stay open for at least another 6 months. This is being made possible by the IDC putting in a R1.68 billion facility. Government has also provided a Temporary Employee Relief Scheme (TERS) grant. ArcelorMittal hasn’t disclosed the value thereof.

Now, if this sounds to you like good money being thrown after bad, you’re on the right track and I share your sentiment. Our country has plenty of examples of people living off the taxpayers and we don’t need to create corporate examples as well. The good news is that these relief measures are accompanied by promises for structural changes, like the preferential pricing system and tariffs. My understanding is that cheap steel being exported by China is the problem, so government also isn’t in an easy situation right now. We aren’t exactly making friends and influencing people in the West right now, so upsetting our biggest partner in the East isn’t a great approach either.

For shareholders in ArcelorMittal, it’s hard to say for sure whether this is good news or not. The IDC facility is debt, so what is essentially happening here is that operating losses are being funded by a debt package that would never be provided by commercial banks due to the risks involved. Will any structural improvements in the industry more than offset these costs?

ArcelorMittal is about as speculative a play as you’ll find anywhere.

Emira seems happy with performance thus far this year (JSE: EMI)

A pre-close update indicates that they are on track internally

Emira Property Fund released a pre-close update based on numbers for the 10 months to 31 January 2025. There are still challenges for landlords out there, evidenced by ongoing negative reversions on leases – albeit to a lesser extent than before. This has improved from -6.8% to -4.2%.

The retail portfolio has almost gotten rid of negative reversions, coming in at -0.9% vs. -4.0% by the end of the interim period (September 2024). The office portfolio can’t say the same, but at least reversions are headed in the right direction, improving from -9.6% to -5.8%. This is despite the office portfolio being strongly skewed towards high quality properties. As for the industrial portfolio, there’s a nasty trend in reversions that saw them deteriorate from -7.9% to -10.8%.

The residential portfolio is spread across 3,389 units, with a low vacancy rate and high collections vs. billings. They sold 386 units in this period, unlocking disposal proceeds of R312.9 million.

Looking at other capital allocation strategies, the US portfolio is down from 12 properties to 11 and saw an uptick in the vacancy rate based on the bankruptcy of a retailer. Over in Poland, Emira’s shareholders recently approved the tranche 2 subscription option that will take Emira’s stake to 45% in DL Invest. The Polish portfolio is mainly logistics or industrial in nature (67% by value).

The loan-to-value ratio has decreased to 34.1% as at February 2025. That’s a meaningful improvement from 42.0% as at the end of September 2024. They expect to finish at between 36% and 37% as at the end of March.

Although it’s clear that there are still difficulties in the market, Emira is making progress and is pleased with how the financial year has gone.

enX sells West African International (JSE: ENX)

Don’t be fooled by the name – this is the Southern African chemicals business

As confusing names go, this one has to take the cake. West African International is the chemicals segment of enX and it operates in South Africa. West of what, exactly? Australia?

Either way, enX has found a suitor for the business. Trichem South Africa will subscribe for a 25% stake in West African International and will have the option to acquire the remaining 75%. If they don’t, they have the right to sell the 25% to enX (this takes the form of a put option).

Assuming the deal goes ahead and the put option isn’t exercised, enX would look to return surplus cash to shareholders. The initial subscription for shares is based on the NAV of West African International and that money would stay in the business going forwards, so that’s a red herring. The bit that enX shareholders care most about is the price for what would be the remaining 75% in the enlarged company. This will be calculated as 95% of net asset value, plus 75% of profits over the period between the first subscription for shares and the exercise of the ownership option.

The deal value for the initial subscription for shares and the subsequent purchase of 75% is capped at R450 million. I doubt it will get anywhere close to that number, as the NAV of the segment was R283 million as at August 2024. Profit after tax was R84 million for that year.

Unless the business is busy falling over or had an unusually great time in 2024, I’m not sure why they would want to sell it at what looks like a P/E multiple of under 4x.

Ethos Capital sold down a portion of Optasia (JSE: EPE)

This does wonders to prove the valuation

Ethos Capital’s largest and arguably most impressive asset is Optasia, a fintech group that contributed 48% of Ethos’ net asset value (NAV) per share as at 31 December 2024. Optasia is focused on under-banked individuals and SMEs in frontier markets, so that’s the kind of growth opportunity that gets venture capitalists excited.

An existing shareholder in Optasia has bought a further 13% in the group. Ethos Capital sold 0.81%, or approximately 11.1% of its 7.3% economic interest. This valued Optasia at an enterprise value of $1 billion, which is a 12.8x EV/EBITDA multiple. Welcome to startup valuations!

A valuation on paper is one thing. A valuation based on an arm’s length deal is quite another. This deal is a 13% premium to the value at which Optasia was recognised in the financials at the end of December. That’s great news for Ethos. Further positive news for shareholders comes from management’s intention to either reduce debt or return the proceeds to shareholders, rather than deploy it into new opportunities.

Jubilee Metals blames lower chrome prices for the latest results – but is that right? (JSE: JBL)

The interim results aren’t good news for shareholders

Jubilee Metals released its interim financials for the six months to December 2024. Although revenue was up 51%, EBITDA fell by 6.8% as it was “impacted by softer chrome prices” in this period. Well, that’s what the highlights section of the SENS announcement says.

In reality, the chrome business in South Africa improved its revenue per tonne of chrome concentrate, so I don’t know what they are getting at here. In the section dealing with PGMs, they even talk about how they focused on chrome recoverability in the first quarter to capitalise on those market conditions.

Sure, market prices for chrome may have dipped, but they still sold chrome at a more favourable price than before. Clearly, the EBITDA pressure didn’t come from the chrome business.

So, what was to blame? The average cost per tonne of chrome concentrate was up 30.3%, so the strategy to get the stuff out the door is putting margins under pressure.

They also had a tough time in the copper business, although this wasn’t based on market conditions. Revenue was up 5.1% and gross profit fell 88%, with the stoppage of the Roan operations due to power interruptions not helping at all. They’ve now addressed the power issues. Major changes have been made at Roan that are showing promising signs.

Jubilee is planning to update the market in April regarding guidance. Perhaps by that stage, they will have a better one-liner to explain the results than “impacted by softer chrome prices” – as this clearly doesn’t tell the story at all.

Phil Roux bids Nampak adieu (JSE: NPK)

This comes as a surprise– well, to me at least

Phil Roux was appointed as the CEO of Nampak in April 2023. That’s only two years ago. Having made plenty of progress, he’s decided to step down with six months’ notice.

This feels like a surprise. Roux will retain some involvement in the group at least, remaining on the board in a non-executive capacity and as the chair of a new Strategic Planning and Oversight Committee. The committee has some pretty granular stuff in its mandate, so this doesn’t feel like a traditional non-executive role.

Andrew Hood will take over as CEO from 1 October 2025. He is described as having “extensive experience” within Nampak and he will be appointed as COO from 1 April 2025 so that he can work closely with Roux for the next six months. This makes it even clearer to me that this came as a surprise, as that’s an odd succession structure.

Another solid period for PSG Financial Services (JSE: KST)

This business model really gets the job done

PSG Financial Services operates a strong business that is built around a combination of distribution power and management of assets. The companies on the market that have focused only on the latter have found it really difficult to grow assets. Those with a distribution capability have been doing far better.

The good times have continued for them, with a trading statement for the year ended February 2025 reflecting expected growth in recurring HEPS of between 22% and 25%.

Despite this underlying performance, the PSG share price is down 8% year-to-date. It’s up nearly 18% in 12 months.

Sephaku had a tough end to its year (JSE: SEP)

The GNU has been a disappointment for the cement industry

After much excitement related to the GNU, there’s been very little follow-through for the construction industry. Data suggests that there is limited improvement in demand for building materials and the underlying results of companies in the sector support this view.

Sephaku Holdings has reported that Sephaku Cement experienced a minor increase in profits for the 12 months to December 2024, which is a decent outcome in the context of a 4% dip in sales volumes and an 11.2% decrease in EBITDA. Sephaku Cement had gotten off to a great start in the interim period that was subsequently ruined in the second half by unplanned repairs and an associated drop in production levels. They were lucky to have lower financing costs and depreciation, leading to profit coming out slightly up despite the drop in EBITDA.

At the Metier business, which has a different year-end to Sephaku Cement, volumes are down for the 11 months to February. EBITDA is up at least, benefitting from higher selling prices and cost savings.

Vukile Property Fund has confirmed guidance for the year ended March 2025 (JSE: VKE)

This was a busy period for Iberian acquisitions

Portugal and Spain are the talk of the town in the local property sector. It seems as though this is the new Poland for local investors. Luckily for Vukile, they’ve been early adopters here, with a portfolio in that region that has been a feature of the group for several years now.

Despite all the excitement on that side of things, the South African portfolio generated growth in net operating income of 6.4% in the year ended March 2025. The township and rural segments are doing particularly well, capturing the trend of informal-into-formal retail. Rental reversions are positive, so that’s clearly a highlight that speaks to demand for the space from tenants.

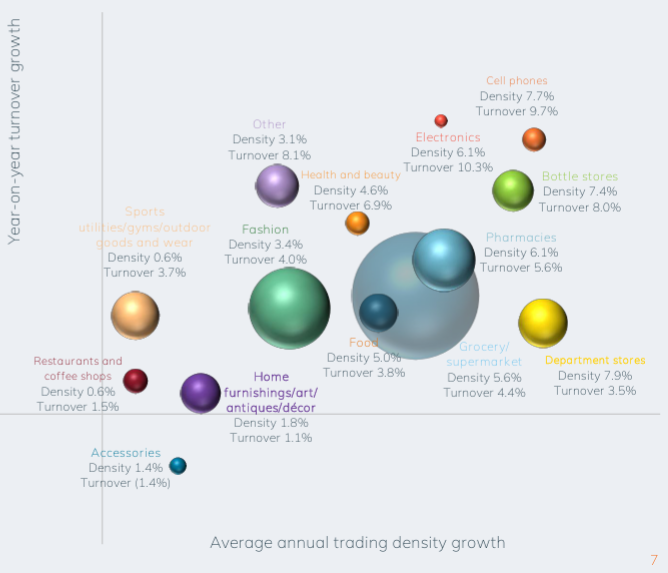

As this excellent chart from the deck shows, shoppers are drinking – just not at restaurants:

Over in Spain, economic growth was well ahead of forecasts in 2024. As South Africans, we can only dream of such things. Portugal also had decent economic growth and both countries achieved record tourist numbers. Still, like-for-like growth in Spanish subsidiary Castellana was only 2%, which is well below what the South African portfolio managed in the past year. Personally, I wouldn’t extrapolate that – the fundamentals in Iberia are clearly better at the moment.

After a busy period of dealmaking, Vukile is now calming down with no planned acquisitions, equity capital raises or dividend reinvestment programmes. That’s good news in my books. They expect to achieve 6% growth in the dividend per share for the 2026 financial year. No further share issuances will certainly help with this.

And as for the year that just ended, being the 12 months to March 2025, they also expect the dividend per share to be up by 6%. That’s solid.

York Timber had a stronger interim period (JSE: YRK)

But there’s still no interim dividend

York Timber had a much better time of things in the six months to December 2024. Revenue was up 18% and adjusted EBITDA (which excludes the fair value adjustment on biological assets) increased dramatically from R8.3 million to R84.3 million. HEPS jumped from 4.67 cents to 14.31 cents, so at this point you must be wondering if there’s an interim dividend.

The answer is no, there isn’t. HEPS was boosted by the biological asset value increase of 5%, which isn’t a cash inflow. Core earnings per share excluding the fair value movement still reflected a loss, albeit a much smaller one at 0.09 cents vs. a loss of 10.06 cents in the comparable period. And although cash generated from operations achieved a massive swing from negative R7.8 million to positive R45.7 million, it’s also true that debt in the group increased (thanks to the Pine-Valley acquisition) and so did working capital requirements.

This company has always felt to me like a really hard way to make money.

Nibbles:

Director dealings:

Among sales by directors of Impala Platinum (JSE: IMP) that were mainly to cover the tax on share awards, it looks like there was one director that sold R5.6 million worth of shares that represented an entire award, not just the taxable portion.

The CEO of Sirius Real Estate (JSE: SRE) sold shares worth R2.8 million. The company has been on a roll recently with acquisitions, so that comes as a surprise.

A director of HomeChoice (JSE: HIL) sold shares worth R1.4 million.

A non-executive director of Shaftesbury Capital (JSE: SHC) bought shares worth R1.2 million.

A director of Remgro (JSE: REM) bought shares worth R249k.

Lesaka Technologies (JSE: LSK) hosted an investor day and released four detailed presentations that take you through the business. It took me a little while to find them on the website. You can enjoy the presentations and the webcast at this link.

OUTsurance Group (JSE: OUT) announced that its Australian business Youi is making some changes to its distribution strategy. They are moving away from a broker distribution channel and will instead focus on direct distribution. This means the end of the distribution relationship with Blue Zebra Insurance, in which Youi holds a 36.9% interest that will be sold to other shareholders. Separately, the company announced that losses from Cyclone Alfred are expected to mostly be within the reinsurance claim window. They do expect residual losses though, coming in at between A$10 million and A$15 million – a reminder of the risks sitting on insurance books when it comes to natural disasters.

Eastern Platinum (JSE: EPS) has very little liquidity in its stock. They also have a lot less revenue than before, with results for the year ended December 2024 reflecting a 41.5% drop in revenue and a swing into operating losses. The company has a large working capital deficit. There are obviously going concern risks here, with the company clinging to the upside potential of the Zandfontein operations that are being ramped up.

Kore Potash (JSE: KP2) has released results for the year ended December 2024. They are in the process of raising funding for the Kola project, so the focus at the moment isn’t on what you’ll find in the financial statements. This is common for junior mining companies that are still in project phase. The cash burn in the latest year was $3 million and the group had $1.3 million in cash as at the end of December. They need to raise money this year to meet the going concern test, as they have large payments to make in relation to the development.

If you are following Merafe (JSE: MRF) closely, you’ll be interested to know that the company has broken down its revenue in Asia in more detail. This is part of the JSE’s proactive monitoring review process. As Asia is the largest contributor to revenue, I guess they wanted to see more disaggregation to give investors granular detail.

Gold Fields (JSE: GFI) is considering a bond offering. They are looking at issuing 10-year bonds to repay outstanding amounts under the $750 million bridge facilities that were used to fund the acquisition of Osisko Mining in 2024. Global coordinators and bookrunners have been appointed to drum up interest among fixed income investors.

AYO Technology (JSE: AYO) finally released financials for the year ended August 2024. The headline loss per share jumped from 71.81 cents to 177.09 cents. To give you context to just how bad the income statement is, gross profit was R347 million and operating expenses came in at R648 million.

Finbond (JSE: FGL) announced that holders of 71.27% of shares in issue (less exclusions) elected to receive cash dividends rather than scrip dividends.

Curry. Con carne. Arrabbiata. Peri-peri. In almost every corner of this world, you’ll find a dish that’s been given the signature bite of the chilli pepper. As strong as they are small, these pungent peppers have achieved the culinary equivalent of world domination, when all they really wanted to do was to get us to stop eating them.

The other day, I came across a headline that seemed innocent enough: Campbell’s is spicing up its range of iconic soups.

Harmless, right? Just a classic American brand keeping up with the times, rolling out a few new flavours to keep things fresh. Except, the deeper I dug into this story, the weirder it got.

Campbell’s isn’t just playing around with new flavours – it’s diving headfirst into the spice pool. The New Jersey-based food giant has launched four new varieties: Spicy Chicken Noodle, Spicy Tomato, Spicy Buffalo-Style Cream of Chicken, and (I can’t believe I’m typing this) Spicy Nacho Cheese Soup. It’s a weirdly hot twist for a brand strongly associated with comfort and nostalgia, don’t you think? After all, for most of us, soup is the kind of thing we eat when we’re cold or sick, not when we’re actively trying to break a sweat.

And yet, this isn’t just Campbell’s throwing stuff at the wall to see what sticks. The numbers back them up: spicy flavours account for a quarter of soup category growth, according to industry data. Younger consumers in particular are driving the demand for spicier flavours (if you were looking for concrete proof that Gen Z are all secretly masochists, this may be as close as you get). A 2022 survey of over 6,000 consumers found that nearly three-quarters believe that most foods taste better with some level of heat.

Spicy food isn’t new. What is new is the way it’s seeping into everything, not just the traditionally mild and soothing world of canned soup. It’s the Hot Ones YouTube series, where celebrities sweat through Scoville-induced existential crises. It’s the viral challenges where people voluntarily eat chips so spicy they require a legal disclaimer. It’s the fact that there are entire festivals dedicated to hot sauce, where attendees gleefully burn their taste buds off like it’s a competitive sport.

Most species avoid pain as a survival mechanism. But humans? We chase it down and put it on the menu.

How does a chilli pepper make a living?

Let’s kick things off with a little biology. Ever wonder why chilli peppers burn in the first place? It all comes down to something called an antifeedant. Sounds fancy, but in plain terms, it’s nature’s way of saying, “Hey, maybe don’t eat me” to the world. Some plants develop foul-smelling fruits (looking at you, durian) in order to scare off would-be grazers, while others cultivate bitter-tasting leaves or roots (thanks a lot, kale).

The fiery antifeedant at play in chillies is called capsaicin, and it works in cahoots with sidekicks known as capsaicinoids. When ingested, these chemicals actually trigger pain receptors in your mouth and throat, sending off an SOS signal straight to your brainstem and thalamus, which process heat and discomfort. Essentially, your body thinks you’ve eaten something like a hot coal, hence the sweating, the gasping, and the urge to chug milk like your life depends on it.

But why would a plant want to make eating it a miserable experience? Most fruiting plants rely on animals to eat their fruits and then, um, distribute their seeds elsewhere as a method of reproduction. So why go full sadist? As it turns out, chillies aren’t actually waging war on all creatures indiscriminately. They’re just picky about their seed couriers.

Mammals (like us) have capsaicin receptors, which means we feel the burn. Birds, on the other hand, get a VIP pass. They don’t have capsaicin receptors, which means they can munch on chillies without so much as a flinch. As a result, they became nature’s top-tier chilli seed couriers, spreading them far and wide.

So, in a way, chillies pulled off an evolutionary masterstroke. They deter land-based mammals who might distribute their seeds in a narrow radius while enlisting far-flying (and far-pooping) birds as their personal delivery service. It seems like a faultless plan on paper, if only human beings didn’t decide to not only tolerate the burn but actively seek it out. The question is, why are we like this?

Some like it hot

One school of thought among evolutionary biologists suggests that our fondness for spice started as a survival tactic. Peppers (along with other spicy foods like wasabi and mustard) come packed with natural antimicrobial properties, meaning they help kill off the bacteria that can turn a meal from delicious to disastrous. This theory makes particular sense when you consider that spicier cuisines tend to dominate in warmer climates, where food spoils more easily. The thinking goes that those who developed a taste (and tolerance) for chilli were less likely to get sick from rotten food, and over time, that preference became ingrained.

But biology is only one piece of the puzzle. Psychology has also thrown its hat into the ring with a different perspective, one that paints spice lovers as thrill-seekers. Back in 1980, psychologists Paul Rozin and Deborah Schiller put this to the test by feeding people progressively hotter doses of chilli. Their conclusion was that the attraction to spice is similar to the rush people get from riding roller coasters or taking scalding hot baths. It’s all about “constrained risks”, in other words, situations where we can experience a little bit of danger (or at least perceived danger) in a controlled, safe environment. More recent studies have taken this further, linking a preference for spice to personality traits like sensation seeking and sensitivity to reward. In other words, if you’re the kind of person who enjoys skydiving, gambling, or cranking the shower dial up to magma, odds are you’re also the one ordering the spiciest thing on the menu.

And then, of course, there’s culture to take into consideration. Remember, humans don’t just eat for survival – we eat for meaning. Our food choices reflect tradition, identity, and the way we want to be perceived. Anthropologists have found that in many cultures, spice is less about flavour and more about who you are. Take Mexico, for instance. In some regions, spiciness is deeply tied to national and regional identity. Cultural historian Esther Katzreferences a phrase from Indigenous Mixtec people in Oaxaca: “Somos fuertes porque comemos puro chile”, which translates to “We are strong because we eat nothing but pepper”. The implication is that handling heat isn’t just a preference, but a mark of resilience, toughness, and even pride. Similar associations pop up across multiple cultures, where eating spicy food is linked to bravery, masculinity, or just good old-fashioned toughness.

And so, the humble chilli, a fruit that evolved to keep us at bay, has instead become the object of our obsession. We’ve taken its fiery defence mechanism and turned it into a badge of honour, a source of pleasure, and a billion-dollar industry. Whether we’re sweating over a bowl of soup, braving a Carolina Reaper for internet glory, or simply dousing our eggs in Tobasco, one thing is clear: pain, in small, edible doses, is something we’re more than willing to pay for. Maybe that’s the real human enigma – while most creatures avoid suffering, we’ve found a way to season it, bottle it, and ask for seconds.

Humans 1, chillies 0.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Bell Equipment reminds us what a cyclical business looks like (JSE: BEL)

That previous offer price of R53 per share just feels further and further away

I’ve said it many times and I’ll say it again: I think that Bell shareholders who blocked the take private deal were too greedy. The share price is now just below R38 and the offer price was R53. Sure, if the cycle was in Bell’s favour, then perhaps the price might get back there without an accompanying offer to boost it. Alas, the opposite is true.

For the year ended December 2024, Bell Equipment’s revenue fell by 13% and operating profit was down 37%. It just gets worse as you head further down the income statement, with HEPS down by 42%. At least there’s a dividend of 160 cents per share, representing a payout ratio of almost 35% of HEPS. Hardly a growth asset right now and not exactly a cash cow, either.

The issue is that Bell’s customer base is primarily in industries like mining. This is a hugely cyclical game where investment in capital goods (like the products that Bell sells) will only happen when the miners feel good about commodity prices. This wasn’t the case for the majority of commodities in 2024 (gold really was the exception), hence the impact on Bell’s numbers.

This takes us back to the issue I had with minority shareholders who blocked the deal: I felt that the offer was more than decent, particularly as it was being made based on earnings that were at a favourable point in the cycle. If Bell does ever get back to R53 per share, I suspect it will be a few years away. Time value of money, anyone?

Personally, I think much the same story of regret awaits the Barloworld shareholders who blocked that deal as well. Time will tell.

The decline in the birth rate in developed countries and particularly among higher income families in emerging markets is becoming an increasingly concerning reality. This could lead to a demographic profile in years to come that is highly problematic, as we’ve seen in places like Japan and China. It’s not just an anecdotal thing of having fewer friends with kids than in prior generations – it’s an observable trend confirmed by numerous data points like declining maternity cases at Netcare.

The other trend that I always note is the level of demand for mental health services. Combined with the maternity trend, these are just some of the reasons why Netcare is experiencing a change in revenue mix where medical cases are growing faster than surgical cases. Interestingly, mental health demand may be coming off its peak though, with paid patient days 1.9% lower in this particular period in that area.

The underlying revenue mix may be changing over time, but at least the direction of travel is up. At group level, paid patient days are up 1.1% for the first half of the year. Revenue per paid patient day has increased roughly in line with inflation, which means that the group expects full-year revenue to be up by between 5% and 6%.

To help boost shareholder returns, the group has been busy with an extensive share buyback programme. This does indicate a degree of capital allocation discipline in the group, particularly as many hospital projects do struggle to generate sufficient returns on capital.

Interim results are due for release on 19 May.

Novus and the TRP just aren’t friends at the moment (JSE: NVS)

The mandatory offer to Mustek shareholders continues to be a headache

Novus hasn’t been on the right side of the Takeover Regulation Panel (TRP) recently. After raising their ire around concert party definitions in the offer made to Mustek shareholders, it looked as though things were sorted out. The Firm Intention Announcement (FIA) was released and the ball was rolling.

The latest development is that the TRP has now withdrawn its approval for the FIA, which means that Novus has to publish a new one within 20 business days. Presumably the clock will then be reset for the deal process to be followed. In the meantime, Novus will appeal against the ruling on an urgent basis.

This is a messy situation.

Orion Minerals really put the SENS systems to the test (JSE: ORN)

There was so much news that they needed four announcements in one day!

Orion Minerals certainly kept the market appraised of their plan to release major news on the underlying projects during March. In a flurry of announcements on Friday, they did exactly that.

A lot of it is very technical in nature, as is typical for a junior mining company. I’ll just focus on the high level stuff.

First up, the Definitive Feasibility Study (DFS) for the Prieska Copper Zinc Mine. The initial phase needs capex of R560 million and would achieve first production 13 months after the start of construction. This near-surface asset would run for 4.3 years. To get the life of mine up, there is a second phase that will be implemented roughly halfway through the initial phase. The total life of mine then increases to 13.2 years, with an expected post-tax internal rate of return (IRR) of 26%.

Then, we can deal with the DFS for the Flat Mines Project at Okiep Copper. This is less lucrative but still worthwhile, with a post-tax IRR of 19%. The expected capex bill is R1.6 billion. They have also planned a phased approach here, making it easier to raise funding along the way.

These DFS reports will allow the company to negotiate project funding, plan the implementation and negotiate offtake deals, among other workstreams.

Separately, the company announced a mineral resources update for the Flat Mines Area, informed by recent drilling activity. Junior mining is all about de-risking the project and getting closer to numbers that have higher confidence. This is what gets investors across the line.

And guess what? They did the same thing for Prieska, with a mineral resource update based on the recent data that was gathered in the DFS study.

Overall, the rubber now hits the road for Orion Minerals. This is where things hopefully get exciting for them, as they will need to raise capital for these projects. The market cap is R1.2 billion, so it’s likely that there will be significant dilution of shareholders along the way. This isn’t necessarily a problem, provided the valuation of Orion keeps improving over time and capital can be raised at higher share prices over time.

MultiChoice has pulled the rug on Phuthuma Nathi – and it’s disgusting (JSE: MCG)

The Canal+ transaction is starting to look like a matter of life and death

I’ve been writing and mentioning on radio interviews for a while now that MultiChoice looks to me like it was built for sale, not for sustainability. They threw everything at building out the African operations, hoping that South Africa would be able to fund it. This is as risky a strategy as you’ll find, appealing only to a buyer who wants major African exposure in one shot – much like Canal+.

The deal has gone from a nice-to-have to practically a life-or-death situation for MultiChoice. The recent results have been shocking at group level and the latest announcement shows that even Phuthuma Nathi shareholders aren’t safe. This is a disaster for B-BBEE investors, with the Phuthuma Nathi share price crashing by 56% on Friday.

The issue lies in MultiChoice South Africa, which is the level at which Phuthuma Nathi is invested. Sure, there’s a difficult environment being faced by the company, but MultiChoice has been messing around in Africa instead of getting the basics right at home. When there are endless complaints about the quality of the smart TV streaming app and nothing is done about it, you know that management is focusing on all the wrong stuff. If you add the African pressures to this, you now have a situation where MultiChoice has flagged that the dividend at MultiChoice South Africa is likely to be “significantly lower” going forwards.

So, in summary, lots of qualifying Black investors (including some major groups) trusted MultiChoice to run a decent business in South Africa that could keep paying dividends. Instead, they dropped the ball completely and now they need to preserve cash at SA level to help with the Rest of Africa. Worst of all, the Rest of Africa is a set of businesses that Phuthuma Nathi doesn’t even get any upside exposure to!

This is a disaster for many B-BBEE investment groups that saw Phuthuma Nathi as a reliable source of dividends and cash flow. Frankly, the board of MultiChoice should be looking for new jobs, but alas there is so little true corporate accountability in South Africa that it probably won’t happen.

But maybe, just maybe, there are enough angry B-BBEE investors out there with sufficient capital behind them to put pressure in the right places. I live in hope.

Safari Investments is exiting Namibia (JSE: SAR)

They found a Namibian buyer for their property assets

Safari Investments has decided to sell 100% of its interests in Safari Namibia for R290 million. The group wants to focus on rural and township shopping centres in South Africa instead, a rather interesting growth area. Unlocking capital from non-core assets obviously helps with this.

Safari Namibia is the owner and manager of the Platz am Meer Shopping Centre in Swakopmund. Having had the immense pleasure of visiting Swakopmund once before, I do wish I could go see the deal for myself! It’s a beautiful little place.

Travel memories aside, the deal also comes with an “agterskot” (a potential future payment) if Safari Namibia achieves a targeted net operating income yield during the 12 months after the disposal. This could add between R1 million and R10 million to the price for the deal.

The fair value of the property is R303 million, so even if the agterskot is triggered, they would have sold this at a price below fair value. Still, I agree that exposure to retail properties in lower income areas in South Africa is a better bet for the long term than having a shopping centre in Swakopmund.

Telkom’s earnings are trending higher, but HEPS is the right metric to use – as usual (JSE: TKG)

This is a great example of how badly EPS can be distorted

Telkom has released a trading statement dealing with the year ended March 2025. The good news for investors continues to flow at the group, with HEPS up by at least 10%. The telecoms sector has been enjoying strong market support lately and Telkom is no different, with the share price up more than 40% over six months.

Regular readers will be aware that trading statements are triggered by an earnings move of at least 20%, so why did this get released for a HEPS move of 10%? The answer lies in the Earnings Per Share or EPS line, which is impacted by the profit made on the disposal of Swiftnet. Including that profit means there’s a 300% increase in EPS!

Clearly, that’s not an indication of recurring earnings growth, hence why HEPS is the better metric to use.

Nibbles:

Director dealings:

An executive at Investec (JSE: INL | JSE: INP) sold shares worth R4.3 million.

A director of the main operating subsidiary at Mpact (JSE: MPT) sold shares worth R1.49 million.

A couple of directors at Cilo Cybin (JSE: CCC) bought shares worth R17k.

There’s a changing of the guard at Capitec (JSE: CPI). Gerrie Fourie is retiring as CEO, having been part of the executive management team for the past 25 years. He’s a founding member of the bank and can certainly look back on a career that genuinely changed the banking landscape in South Africa. His successor is Graham Lee, who has been on the group executive team since 2022. He joined Capitec in 2003, so this is a great example of a succession plan in action.

Rex Trueform (JSE: RTO) released results for the six months to December 2024. There’s practically no liquidity in this stock, so it just gets a passing mention. Although revenue fell by 4.5%, gross profit margin was up and operating profit increased by 9.6%. Despite this, HEPS fell by 3%. African and Overseas Enterprises (JSE: AOO) is a related entity that also released results, reflecting HEPS up by 0.5%.

AH-Vest (JSE: AHL) released results for the six months ended December. This is a tiny company, hence it only gets a mention in the Nibbles. Revenue fell 12.8% and HEPS crashed by an ugly 93%, so the company is barely profitable. It made a profit of R178k off revenue of R100.6 million. I’ve seen thin margins before, but this quite possibly takes the cake.

The chairperson of Labat Africa (JSE: LAB) has resigned with immediate effect, which is odd after 12 years on the board. Separately, a new director with IT experience has been appointed to the board, so this points to the new direction being taken by the company. N Bodirwa has been appointed as interim chairperson.

Europa Metals (JSE: EUZ) released results for the six months to December 2024. This was the period in which the Toral Project was disposed of to Denarius Metals Corp in exchange for shares. They also announced the planned Viridian Metals deal in this period, which they subsequently decided not to pursue. They will need to figure out the way forward, as the assets on the balance sheet almost entirely consist of the stake in Denarius.

Cilo Cybin (JSE: CCC) updated the market on the process for the proposed acquisition of Cilo Cybin Pharmaceutical. Due to the timing of the audit, the intention is to have the latest pro forma financial information in the circular. To achieve this, the company is approaching the JSE for a dispensation for a further extension of the circular distribution date.

Salungano Group (JSE: SLG) is dealing with a change in CFO during the finalisation of results that are now terribly late. They need to get the March 2024 annuals out, as well as the September 2024 interims. With another delay announced on Friday and an expectation of only releasing these reports by June 2025, the March 2025 annuals might be late by then as well!

Stefanutti Stocks (JSE: SSK) announced that the disposal of SS-Construções (Moçambique) Limitada is still suffering delays. The fulfilment date for the conditions to the deal has been extended to 30 April 2025.

Conduit Capital (JSE: CND) released its quarterly progress report. The company has to do this as it is suspended from trading. Aside from the provisional liquidation issues, the more important updates are: (1) the sale of CRIH and CLL to TMM, which was once again blocked by the Prudential Authority, has had its fulfilment date extended to 16 May to allow for time to engage with the regulator, and (2) the company is taking steps to enforce the arbitration award against Trustco Properties.

London Finance & Investment Group (JSE: LNF) had no problem in getting the approval from shareholders to delist and return capital to shareholders, with an almost unanimous vote in favour of the plan.

Randgold & Exploration Company (JSE: RNG) released results for the year ended December 2024. This is little more than a cash shell these days that is busy pursuing legal claims. There is no revenue other than finance income. The operating loss for the year ended December 2024 improved by 44% to a loss of R17.2 million.

Comparability is limited in Ascendis’ numbers (JSE: ASC)

The change to investment entity accounting is a big one

As flagged when Ascendis recently released a trading update, the shift to investment entity accounting makes a big difference to the numbers. They will now be focusing on metrics like net asset value (NAV) per share, rather than consolidated HEPS.

There’s nothing wrong with this approach, but it makes things difficult in the first year of its application. This is because the changes aren’t applied retrospectively, so the comparatives are now practically meaningless in the context of the latest numbers.

To give us a starting point for this new chapter of the company’s life, NAV per share was 105 cents as at December 2024. The Medical portfolio is 35% of the value and the Consumer portfolio is 65%.

The Consumer business is slow, with almost no growth at the moment in the face of subdued demand and pressure on pricing. The balance sheet is strong enough to allow them to launch new products to the market, which may be facilitated through acquisitions, like in the case of a new weight management product. Still, this feels to me like the narrow moat side of things, so it’s a pity that it forms the bulk of the portfolio.

The more interesting side is surely the Medical portfolio, with five entities providing a variety of devices to the private and government sectors. One of those entities is Surgical Innovations, which exited business rescue in 2023 and has been fighting for its life ever since. Thanks to the overall improvement to the balance sheet though, Ascendis could support one of its other investees making an acquisition of two strategic agencies. I’m no expert in this sector, but this sounds like a higher quality business than the Consumer portfolio in the South African context.

You may recall that there was an offer at 80 cents a share to take Ascendis private in late 2023 / early 2024. The NAV is now a fair bit higher than that number and the share price is at 83 cents.

Capital Appreciation’s payments division is doing well (JSE: CTA)

Importantly, the software division is no longer making losses

Capital Appreciation’s best business is undoubtedly the payments division. It continues to grow revenue at double digits and has a strong annuity flavour to its business model with multi-year contracts. Annuity revenue is more than half of total revenue and that obviously does great things for visibility and thus the valuation over time.

The ongoing growth of digital payments vs. cash will help them here, with innovations focused on providing solutions to micro-enterprise customers in Africa. There are good reasons to believe in the positive outlook for this division.

The recent drag on the story has been the software division. When work was slow to come in, Capital Appreciation tried to retain key staff in the hope that things would improve. At some point though, you simply have to restructure the business to respond to slower demand. This has now taken place, which is why the division returned to profitability in the second half of the year. Although the revenue prospects seem to be weak, they are no longer bleeding there.

Results for the year ended March will be released in early June. The share price is up 17.7% over 12 months. It’s well off the 52-week high of R1.90 though, currently trading at R1.40.

CA Sales just can’t stop growing (JSE: CAA)

This remains one of the most impressive local growth stories

If you’ve been paying attention to Unlock the Stock, you would’ve had the chance to engage with the management team of CA Sales Holdings on multiple occasions by now. In doing so, you would probably have reached the conclusion that they are a humble bunch who know what they are doing. Their next appearance on the platform is on 10 April (register for free here), so you have a chance to get to know them if you haven’t done so before.

When you consider that HEPS just grew by 25.3% in the year ended December 2024, it’s important to pay attention to this story. Sure, they are facing risk from exposure to the economy in Botswana and thus the look-through impact of diamond prices, but they’ve also done a fantastic job of diversifying beyond their home market. Management feels confident about the Southern and East African portfolio of businesses in the group, hence why the final dividend increased by 24.9%. This implies strong cash quality of earnings.

One of the things I appreciate most about the group is the bolt-on acquisition strategy. Instead of betting the farm on huge transactions, they go step-by-step in adding businesses to the portfolio. It’s like building a house out of lots of little Lego blocks rather than one or two big ones. If you’ve ever unleashed a toddler on a Lego house, you’ll know that small blocks are more resilient. African trading conditions and toddlers aren’t all that different.

The market has certainly taken notice of the company, with the P/E multiple at over 13x. The share price is up 48% over 12 months. Even more impressively, they are up slightly year-to-date, bucking the trend we’ve seen in consumer businesses on the JSE.

The company greatly values the Ghost Mail audience and they have placed their results at this link on the site, along with great visual summaries and the investor presentation. Don’t miss it!

Datatec is managing mid-single digit growth (JSE: DTC)

The company wants you to focus on gross profit as the right metric