Before there was Las Vegas, there was Port Royal: a city of pirates, plunder, and peril clinging to the southern edge of Jamaica. The 17th-century hotspot was once the beating, drunken heart of the Caribbean, until one Sunday in 1692, when the earth opened up and swallowed it whole (quite literally). There’s more truth to Disney’s tales of Captain Jack Sparrow than you might realise.

By the late 1600s, Port Royal was considered to be the crown jewel of the Caribbean – although on second thoughts, “crown” may be a bit too generous a description. In reality, Port Royal was probably more like a golden tooth: gleaming, ostentatious, and clearly quite rotten.

Founded by the Spanish in 1494, Port Royal officially became a British outpost after the Brits wrestled Jamaica from Spanish hands. Its location at the mouth of Kingston Harbour, smack in the middle of Spanish-controlled seas, made it the perfect launchpad for privateers.

Privateers were essentially pirates on the British payroll. They were legally allowed to rob Spanish ships on behalf of the British Crown, which made them both criminals and civil servants, depending on the week’s foreign policy. When England and Spain were at war, the privateers were “heroic seamen”. When peace between the two countries returned, they were downgraded back to pirates, or simply thieves with boats.

Still, privateering was a profitable arrangement. Gold and silver from Spanish galleons poured into Port Royal like rain, and soon the place was booming. In its absolute heyday, it had a population of almost 8,000, and that population sure liked to party. In July 1661 alone, 40 licenses were granted to open new taverns. By 1662, Port Royal was recorded as having one tavern for every ten residents.

Sin City by the sea

If you squinted, Port Royal looked a bit like London, with its narrow cobble streets, brick-and-wood houses, busy merchants, and the occasional pickpocket. But the similarities stopped there.

This was the kind of town where morality was the exception, not the norm. Public drunkenness was normal, gambling was a civic pastime, and prostitution wasn’t just tolerated, it was practically part of the tourism industry. Sailors fresh off the high seas filled the taverns, flinging coins and curses in equal measure. There were carpenters and cobblers, shipwrights and blacksmiths, all feeding off the booming pirate economy. Money sloshed through the streets as freely as the rum, and few cared to question where it all came from.

The key to Port Royal’s popularity was its exceptionally deep harbour, which allowed up to 500 ships to dock at once. This meant constant trade and an equally constant influx of trouble. The city was built, quite literally, on sand – a fragile spit of land that jutted out into the Caribbean. Geographically, it was a risky position, but no one seemed to worry about geology when the economy was this good. As the population grew, more land was laid dry to make space for new buildings. The pirates were essentially stealing territory from the sea itself.

To the devout back in England, Port Royal was less a colony and more a cautionary tale; a sun-drenched Babylon in the tropics. Clergymen called it “the wickedest city on earth.” And like any good biblical story, the ending would be apocalyptic.

June 7, 1692

It was a Sunday morning, just before noon. The markets were busy, the taverns already humming, and the church bells likely ringing with irony. Then the ground began to shake.

At first, people thought it was a passing tremor. But within seconds, the shaking turned violent. Brick walls cracked, the church tower crumbled, and the harbour churned like a pot of boiling stew.

Modern geologists estimate it was a magnitude 7.7 earthquake that struck not just Port Royal, but the whole of Jamaica. That’s an enormous force unleashed directly beneath a city built on sand. And that sand was about to betray them.

When earthquakes hit sandy soil, an eerie process called liquefaction happens. The solid ground suddenly behaves like water, and everything sitting on it begins to sink. The ground that Port Royal was built on didn’t crack or heave during the earthquake – it essentially liquified. Two-thirds of the city slid straight down into the sea. Buildings vanished whole. Streets folded in on themselves. People, animals, and homes were all pulled under in a matter of minutes.

For a city long accused of sin, it was the most literal form of damnation imaginable. But the earthquake was just Act One.

Moments after the ground stopped shaking, the sea struck back. The shifting seabed had triggered a tsunami, or more precisely, what scientists call a “seiche wave”. The harbour turned into a giant sloshing bowl, with water surging back and forth, smashing ships against each other and flinging them inland. One British vessel, the HMS Swan, was hurled across the city and deposited inside a house. This impossible image was confirmed by archaeologists centuries later when they found the ship’s hull still lodged in the building’s ruins.

In the space of minutes, Port Royal was unmade through an almost biblical trifecta of earthquake, liquefaction, and tsunami.

A city cursed twice

The survivors, which numbered around 4,000 immediately after the earthquake, stumbled through a landscape that barely resembled the city they knew. Half of Port Royal was at the bottom of the sea, and what was left on land was reduced to rubble.

Wells were contaminated, food quickly ran out, and disease swept through the survivors. Within weeks, another 2,000 had died from injuries, infection, or thirst. To the British back home, the disaster was divine justice. Pamphlets declared the city’s destruction proof of God’s wrath. It was a convenient narrative – sin, punishment, lesson learned – but it ignored the geological explanation. The city had been built in exactly the wrong place, on a sandbar barely holding itself together. And when nature pushed back, there was nothing man, government or pirate could do to stop it.

When money trumps sense

Today, Port Royal is a treasure trove for archaeologists, a kind of Caribbean Atlantis that tells its story brick by perfectly preserved brick.

Modern dives have mapped entire blocks of the old city, revealing homes, shops, and even the remnants of Fort James. Artifacts like coins, pipes, pottery and even sealed bottles of wine can be found in the remnants of eerie underwater buildings. The city that once epitomised greed and excess now lies in perfect silence, inhabited only by fish. Above it, ships still glide into Kingston Harbour, probably unaware that beneath their hulls lies a city once called “the richest and wickedest on earth.”

If there’s a lesson in Port Royal’s story, it’s not the one preached by the moralists of 1692. It’s simpler and far more human. Every civilisation has its Port Royal moment – that point where success turns into overconfidence and growth outpaces good sense. The pirates in this story just happened to build theirs on sand.

Three hundred years later, as coastal cities expand into floodplains and developers pave over wetlands, Port Royal’s story feels less like ancient history and more like a prophecy. As modern skylines rise higher, it’s worth remembering that nature has never needed a sermon to deliver a reckoning.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Deneb is acquiring 80% in Dawning Filters (JSE: DNB)

This is a very good example of the types of deals and pricing you see locally

Deneb is involved in the manufacturing and distribution of industrial products. As is typical for companies in this space, they are open to acquisitions to expand the overall product offering.

As the name suggests, Dawning Filters supplies all kinds of filtration products to customers across multiple industries. The company has distribution offices in Joburg, Durban and Cape Town, with manufacturing done in Durban.

Deneb is paying R80 million for an 80% stake in the company, so you don’t need to get the calculator out to know that the implied value of the entire company is R100 million. Profit after tax for the year ended February 2025 was R15.7 million, so the earnings multiple is 6.4x.

Importantly, there’s a pathway to a 100% stake in the form of a put option that becomes exercisable after four years for a six-month window period. But there’s no call option, so Deneb cannot force the issue to get to 100% – the sale of the final 20% is at the option of the sellers of the business. The maximum consideration that could be payable to the sellers is R120 million, so Deneb has wisely included a cap on the option. The basis of the calculation for the put option price is 6x average annual profit.

This is a category 2 transaction, so Deneb shareholders won’t be voting on it. There are various other conditions though, so it will no doubt take a few months to close the deal.

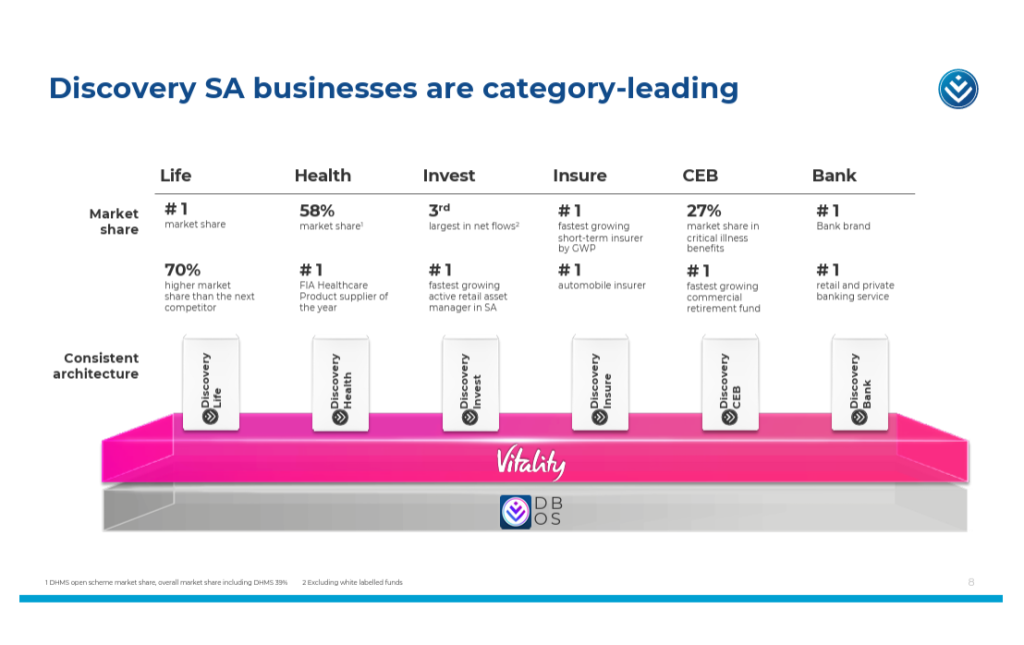

Discovery’s financial year is off to a good start (JSE: DSY)

The medium-term plan calls for mid-teens growth

Discovery presented at the UBS South Africa Financial Services Conference this week. Hylton Kallner, CEO of Discovery South Africa and Discovery Bank, led the presentation. I think it’s fairly obvious how the succession planning is shaping up at Discovery. You’ll find the presentation here.

The group had a very strong FY25 and took the opportunity to remind attendees that normalised headline earnings increased 30%. That’s always a nice way to set the scene!

There’s a very cheeky slide in which they talk about Discovery being number 1 in every category they play in locally. But the metric changes each time e.g. for Discovery Life they use market share and for Discovery Bank they use “number 1 bank brand” – market share is what counts, in which case they are very far from being number 1 across a couple of verticals. I’m not sure why they dilute such an objectively excellent year with such an obviously skewed way of explaining their market positioning:

There are also some very interesting slides on the data they have on things like sleep duration and how this affects health and overall risk of vehicle accidents etc. This is of course the Vitality data that they’ve been building for years now, with the AI era making it even more powerful (and valuable) than before.

The five-year growth ambition for the group is a CAGR of 15% to 20% in profit from operations. Although the South African business is the most mature part of the group, they expect it to achieve a CAGR of 12.5% to 17.5%. Yes, the ecosystem will need to work very well for this to be achieved, but they are firmly on that path.

The presentation also included an update on trading for the first quarter of the new financial year. They are calling it a strong start, with decent new business growth numbers and favourable claims and persistency experiences vs. embedded value expectations (that’s good for profits).

The share price went through a significant recent sell-off, but seems to have positive momentum once more.

Equites Property Fund remains far more bullish on SA than the UK (JSE: EQU)

That’s just as well, as they’ve taken significant steps to bring capital home

Equites Property Fund released results for the six months to August. The narrative tells a more positive story about South Africa, although they note that a “broad-based recovery has yet to take place” despite the recent optimism. That’s a lot better than the UK, with 10-year gilt yields (government bonds in the UK) at historically high levels and the UK logistics property market stuck in a state of low growth.

Equites has made it clear that they are reallocating capital from the UK to South Africa and they’ve already done some significant transactions to make that happen. The narrative simply confirms that nothing has changed regarding that strategy.

For the interim period, like-for-like portfolio rental growth was 5.1% and valuations were up 4.0%, so that’s a solid combination. The loan-to-value ratio did come in a bit higher at 37.2% (vs. 36.0% in February 2025), but the all-in cost of debt thankfully dropped by more than 50 basis points to 8.3%.

The dividend per share was 3.8% higher, while distribution guidance for the full year has been reaffirmed at growth of between 5% and 7%.

The net asset value (NAV) is R16.93 and shares are currently trading at R16.05. The entire sector has seen a reduction in discount to NAV as prospects have improved.

Hammerson is enjoying decent momentum (JSE: HMN)

A ratings agency upgrade does wonders for debt costs and availability

UK property fund Hammerson had no trouble with a €350 million bond issuance that was 5 times oversubscribed. This issuance is part of the refinancing of the €700 million bonds maturing in 2027. It helps that Fitch upgraded the company’s unsecured debt rating and Moody’s revised the rating to a positive outlook.

Due to the timing of the bond issuance, they now expect full year earnings to be £101 million, ever so slightly down from previous guidance of £102 million.

The announcement also includes a trading update based on the summer months, where UK and French footfall were up by mid-single digits. As one would hope, properties that went through significant redevelopment and repositioning did particularly well. Importantly, they are achieving a significant rent increase in long-term lease agreements.

Pick n Pay’s like-for-like momentum is encouraging, but the group is still making losses (JSE: PIK)

Retail turnarounds are hard

Pick n Pay released a trading statement for the 26 weeks to August 2025. The group is unfortunately still loss-making, so we may as well get that out of the way. The headline loss per share has improved by between 50% and 60%, but it’s still a loss of between -54.31 cents and -67.97 cents. In absolute terms, the headline loss is between -R399 million and -R479 million.

So, there’s a long way to go. The key metric to watch is like-for-like growth in Pick n Pay SA, where they came in at 4.3% for the interim period vs. 3.6% in the 17 weeks to 29 June 2025 (in other words there was a strong acceleration towards the end of the period). In the previous interim period, they only grew 1.1%, so this is a significant improvement.

The franchise supermarkets have been a tough story. They are still lagging, with growth of 1.7% vs. company-owned supermarkets at 4.8%. Franchise also had a really easy base in this period, as the comparable period was a like-for-like decrease of -1.4%!

Clothing standalone stores were up 7.5%, with a soft base effect here as well thanks to growth of just 0.2% in the comparable period.

Total turnover growth for Pick n Pay is below like-for-like growth as they’ve been reducing the store footprint to try and shrink into profitability. This has dire long-term consequences, with key rival Shoprite (JSE: SHP) happily mopping up those sites and increasing their footprint. It’s also clear that Boxer (JSE: BOX) is still by far the best business in the Pick n Pay group.

The Pick n Pay share price remains in the red this year, reflecting how hard a turnaround actually is.

Nibbles:

Director dealings:

Three directors of Hyprop (JSE: HYP) have sold shares worth a total of R14.6 million. The announcement notes that this is the first sale in several years and that this is to rebalance portfolio exposures. The company also has minimum shareholding requirements in place for executives. Fair enough then.

A director of a major subsidiary of AVI (JSE: AVI) received share awards and sold the whole lot to the value of just over R6 million. The company secretary of the listed holding company received awards and also sold all of them, with a total value of nearly R5.8 million.

The financial director of Pan African Resources (JSE: PAN) bought shares worth R425k. That’s interesting timing, as the gold price is looking pretty spicy at the moment!

Although Impala Platinum (JSE: IMP) announced dealings by many directors in relation to share awards, I don’t think there was enough of a pattern for us to really read anything into it. Thanks to the recent run in the PGM sector, the share awards ended up being worth meaty numbers for the execs!

Schroder European Real Estate (JSE: SCD) has had a rough year in its share price and the recent valuation trend won’t do much to improve that. In the quarter ended September, the total portfolio value was up just 0.1% quarter-on-quarter. As you would expect, there are bigger swings at individual property level, mostly driven by the passage of time on existing leases and thus the changes to lease terms.

After Silchester International Investors had lots to say in the media about the Barloworld (JSE: BAW) offer and the price they would be willing to accept, it turns out that they’ve now disposed of their entire holding in the company. So much for “at least R130 per share” then.

City Lodge (JSE: CLH) announced that Entertainment Holdings and Tsogo Sun Investments – part of Tsogo Sun (JSE: TSG) – sold shares in City Lodge such that they now hold just 3%. Tsogo had a stake of over 10% that was acquired in 2023, so that’s a particularly interesting move.

In August, Mahube Infrastructure (JSE: MHB) released a cautionary announcement regarding a potential buyout offer for the company by an existing shareholder. The company has renewed the cautionary announcement, as engagement between the independent board and the potential offeror is continuing. As this stage, there’s no firm intention to make an offer, so caution really is warranted here.

Dr Leila Fourie is retiring as CEO of the JSE (JSE: JSE) at the end of March 2026, having been in the role since 2019. Valdene Reddy, currently the Director of Capital Markets at the JSE, has been named as Fourie’s successor.

BHP (JSE: BHG) investors didn’t exactly form an orderly queue for the dividend reinvestment plan. Holders of less than 4% of total shares in issue elected to participate, with the rest happy to receive cash.

Metrofile (JSE: MFL) announced that there are no longer any put or call option arrangements between Sabvest (JSE: SBP) and an associate of director Phumzile Langeni in relation to the company’s shares. It doesn’t seem like any dealings in shares happened as part of this.

Labat (JSE: LAB) renewed the cautionary announcement regarding the potential disposal of certain subsidiaries to All Trading. Negotiations are ongoing.

Growthpoint Properties subsidiary, Growthpoint Healthcare Properties (GHPH), which is managed by Growthpoint Investment Partners, is to acquire the properties and operations of Auria Senior Living, a developer, owner and operator of senior living communities in South Africa. The property assets are valued at R2,4 billion and would initially add four Auria senior living communities to the portfolio. Auria will continue to operate under its current leadership team and brand. Auria’s pipeline of developments include Coral Cove in Salt Rock, KZN in addition to brownfield opportunities which GHPH intends to commence. The acquisition will take GHPH’s assets under management to c.R6,2 billion.

Kibo Energy has announced it will potentially acquire Carbon Resilience, a utility-scale industrial decarbonisation and renewable energy company for US$135 million (R2,3 billion) from FA SPC Real Asset Income, part of the institutional asset management platform of the ARIA Commodities’ group. Following the completion of a due diligence process, the company will be required to undertake a fundraising in connection with the transaction. Kibo will issue c.966 million ordinary shares at an issue price of 10.4 pence per share and will seek shareholder approval for a 1,600:1 share consolidation. The transaction will result in a reverse takeover of the company.

SA Corporate Real Estate (SAC) through its wholly-owned subsidiary SA Retail Properties, has entered into an agreement with Tinos Consulting and Advisory to dispose of Bluff Towers Shopping Centre in Durban for a cash consideration of R544,65 million. The disposal aligns with SAC’s strategy of reducing its retail exposure to KZN.

Vunani’s 78% held subsidiary Vunani Fund Manager has acquired the remaining shares in Sentio Capital Management – a black-owned and managed fund manager. Prior to the merger, Investment Managers Group (IMG) held a 30.05% stake in Sentio. Due to the dilution of its stake as a result of the merger, IMG opted to exit its stake as part of concluding the merger. Sentio will be merged with VFM to form Vunani Sentio Fund Managers. VFM will issue 44,754 shares to Sentio’s shareholders and a cash consideration.

Deneb Investments will acquire 80% of issued share capital of Dawning Filters from vendors MG Dain and the Dibb Family Trust. The R80 million purchase consideration will be paid in cash to the sellers in a 50:50 ratio. The deal is a category 2 transaction and as such does not require shareholder approval.

On 1 October 2025, the parties to the Barloworld transaction agreed to waive the Standby Offer Condition relating to the receipt of competition regulatory approval by COMESA. As at 6 October 2025, NewCo had received valid acceptances of the Standby Offer in respect of 108,25 million shares equating to c.58% of shares in issue. This combined with the Consortium’s and Barloworld Foundation shares equates to 81.8% of the shares in issue. Shareholders who still wish to accept the Standby Offer have until Friday, 7 November 2025 to do so. Results will be announced on 10 November 2025.

Unlisted Companies

36ONE Asset Management has concluded a BEE transaction with a consortium led by MI Capital and including 36ONE staff members and youth communities represented through the Invincible Empowerment Trust. The consortium will acquire a 22% stake in the company. Financial details were not disclosed.

Dibber International Preschools has acquired the South African LittleHill Montessori group of schools, which include five campuses in Kikuyu, The Polofields, Fynbos, Thaba-Eco, and The Huntsman. The five schools will now operate under the Dibber Montessori name, continuing their strong Montessori focus while incorporating Dibber’s Nordic pedagogy, which emphasises play-based learning and holistic child development. Financial details undisclosed.

EduLife, a South African network of private schools, has acquired Arrow Academy, marking the scaling of it footprint into Gauteng. The expansion was supported by Sanari Capital’s 3S Growth Fund, under which EduLife is a portfolio company. Financial details were undisclosed.

Optasia, a fintech company in which Ethos Capital holds an indirect interest, has announced plans to list on the JSE, raising up to R6,3 billion by selling a combination of new and existing shares. Optasia’s AI-driven platform makes credit-vetting decisions by analysing various unstructured data sets. It works closely with mobile network operators, mobile wallet operators and financial institutions thereby unlocking financial opportunities for the underbanked across emerging markets. Optasia has c. 121 million monthly active users, processing over 32 million loan transactions per day with access to over 860 million mobile subscribers though its distribution partners and financial institutions.

Orion Minerals has again increased the size of its capital raise this time to A$8,6 million (R99 million) – initially the company announced a A$5 million capital raising exercise but increased this to A$7,7 million due to level of demand. The private placement now comprises the issue of c. 574 million shares at an issue price of 1,5 cents (R0.17) per share.

Visual International has launched an equity raise of up to R2 million though the issue of new ordinary shares implemented through an accelerated bookbuild process. Funds will be used to assist with the company’s working capital requirements.

Marshall Monteagle plc will launch the renounceable Rights Offer to raise up to US$10,7 million from shareholders in terms of which a total of 8,964,377 Rights Offer shares will be offered at an issue price or $1.20 per share in the ratio of one Rights Offer share for every four Marshall shares. The maximum number of shares that can be issued in terms of the Warrants is 4,482,188 and the maximum amount raised $5,3 million.

BHP has purchased 3,997,199 shares, valued at c. R11,86 billion, in terms of its Dividend Reinvestment Plan for those shareholders electing to have shares allocated to them in lieu of the final 2025 cash dividend.

Remgro has received South African Reserve Bank approval for the payment of a gross special dividend to shareholders of 200c per ordinary share.

Last week, the JSE informed Labat Africa shareholders that the company had failed to submit its annual report timeously and its shares were under threat of suspension. Labat has advised that new accountants have been appointed and that it will publish the annual financial statements for the year ended May 2025 by 15 October 2025.

This week the following companies announced the repurchase of shares:

Old Mutual is the latest company to implement a share repurchase programme. It will repurchase c.220 million ordinary shares for a total consideration of R3 billion. The repurchase will take place on the JSE only and the shares will be cancelled reverting to authorised but unissued ordinary share capital.

Over the period 30 September to 3 October 2025, eMedia repurchased 15,327,677 N ordinary shares representing 3.44% of the companies issued share capital. The shares were repurchased for an aggregate R27,77 million using cash resources.

City Lodge Hotels repurchased 42,729,300 shares over the period 10 March 2025 to 3 October 2025. The shares, which have been delisted and cancelled, were acquired at an average price of R3.99 per share for an aggregate value of R170,29 million. The general repurchase was funded from available cash resources and debt facilities.

South32 continued with its US$200 million repurchase programme announced in August 2024. The shares will be repurchased over the period 12 September 2025 to 11 September 2026. This week 784,611 shares were repurchased for an aggregate cost of A$2,23 million.

On March 6, 2025, Ninety One plc announced that it would undertake a repurchase programme of up to £30 million. The shares will be purchased on the open market and cancelled to reduce the Company’s ordinary share capital. This week the company repurchased a further 31,526 ordinary shares at an average price 204 pence for an aggregate £64,398.

The purpose of Bytes Technology’s share repurchase programme, of up to a maximum aggregate consideration of £25 million, is to reduce Bytes’ share capital. This week 489,711 shares were repurchased at an average price per share of £3.98 for an aggregate £1,95 million.

Glencore plc’s current share buy-back programme plans to acquire shares of an aggregate value of up to US$1 billion. The shares will be repurchased on the LSE, BATS, Chi-X and Aquis exchanges and is expected to be completed in February 2026. This week 7,200,000 shares were repurchased at an average price of £3.44 per share for an aggregate £24,79 million.

In May 2025, British American Tobacco plc extended its share buyback programme by a further £200 million, taking the total amount to be repurchased by 31 December 2025 to £1,1 billion. The extended programme is being funded using the net proceeds of the block trade of shares in ITC to institutional investors. This week the company repurchased a further 912,826 shares at an average price of £38.34 per share for an aggregate £35 million.

During the period 29 September to 3 October 2025, Prosus repurchased a further 1,479,279 Prosus shares for an aggregate €89,55 million and Naspers, a further 247,516 Naspers shares for a total consideration of R319,78 million.

Two companies issued profit warnings this week: Newpark REIT and Pick n Pay.

During the week five companies issued or withdrew a cautionary notice: MTN Zakhele Futhi, Vunani, Conduit Capital, Mahube Infrastructure and Labat Africa.

DealMakers is SA’s M&A publication. www.dealmakerssouthafrica.com

Gabonese startup, POZI, has closed a €650,000 fundraising round led by Saviu Ventures, with participation by Emsy Capital and Chazai Wamba. POZI specialises in telematics and fleet management. Using data and artificial intelligence, the platform provides managers, insurers, and institutions with predictive analytics to anticipate breakdowns and incidents, real-time performance indicators to manage their operations, and risk management solutions tailored to African realities.

Barrick Gold, a Canadian-based global mining company, has announced the sale of its interests in the Tongon gold mine and certain of its exploration properties in Côte d’lvoire to the Atlantic Group for total consideration of up to US$305 million. Owned by an Ivorian entrepreneur, Atlantic is a leading privately held multisectoral Pan-African Group with diversified interests in financial services, agriculture, and industry, and a strong footprint across 15 countries in Africa.

Inspired Evolution’s Evolution III Fund, a fund dedicated to next-generation energy transition, has committed US$20 million to Cold Solutions East Africa Holdings (CSEAHL), a temperature-controlled warehousing and logistics platform operating across Kenya, Uganda, Rwanda, and Tanzania. The investment will support the development and construction of modern cold-chain infrastructure throughout East Africa, helping to reduce post-harvest losses, strengthen food systems, enhance food security, and drive energy and resource-efficient growth in the region.

To help improve access to clean and affordable water in Sierra Leone, Zvilo Africa, a working capital lender, has partnered with So Pure to support the scale of treatment and distribution of safe drinking water across the West African country. So Pure targets low-income and middle-class households across Sierra Leone with clean water, handling every step of the supply chain: purifying the water, packaging it into half-litre sachets or large dispenser 20-litre bottles, and then distributing it to mom-and-pop kiosk shops across the Freetown region. Since 2019, the company has focused on water purification and filling up sachets sourced from a range of local packaging suppliers. An expansion phase aims to distribute 10-12 million litres of purified drinking water monthly by year-end, helping provide clean, safe and affordable drinking water to over 500,000 people.

French long-term infrastructure and impact investor, STOA, has made a US$27 million equity investment into Atlas Tower Kenya (ATK). Backed by Kalahari Capital, Atlas Tower Kenya owns and operates more than 450 telecom towers nationwide, providing critical digital infrastructure that enables mobile network operators to deliver reliable and ubiquitous connectivity. ATK has been operating in Kenya since 2019 with a blended mix of sites in urban, rural, and underserved communities.

Zambian integrated poultry producer, Hybrid, has received a debt investment from specialist impact investors, AgDevCo. The investment, a US$10 million senior debt loan, will enable Hybrid to increase its processing capacity by building a modern abattoir which will create 270 jobs and support the company’s growth.

Tagaddod, an Egyptian tech-powered renewable feedstocks platform, has closed a US$26,3 million Series A led by The Arab Energy Fund, with support from existing investors FMO, Verod-Kepple Africa Ventures and A15 Ventures. Tagaddod has developed a proprietary, tech-powered platform that collects, aggregates, and traces renewable waste-based feedstocks from thousands of suppliers, including households, restaurants, food manufacturers, and collectors across its operating markets.

Ellah Lakes an integrated agro-industrial company in Nigeria,has announced that it has entered into an agreement for the acquisition of 100% of Agro-Allied Resources & Processing from ARPN PTE, Singapore. ARPN PTE. is equally owned by Tolaram Africa PTE Ltd and Valuestar Holdings PTE. The acquired assets comprise 11,783 hectares of cultivated land (planting over 6,280 hectares of oil palm plantations and associated infrastructure), 2,093 hectares of cassava plantations land and an additional 10,393 hectares of uncultivated land. Financial terms were not disclosed.

Artificial intelligence (AI) is rapidly transforming our everyday lives, including merger and acquisition (M&A) transactions.

Currently, 77% of businesses use AI or plan to implement it.1 Most of these businesses believe that AI will increase their productivity, leading to higher revenue.

This trend has increased the number of businesses undergoing M&A processes that either use or have developed AI tools across various business areas. The growing use of AI necessitates bespoke considerations for M&A transactions, both in evaluating the business and conducting due diligence investigations.

Considerations for M&A transactions

When undertaking a due diligence, first consider whether and to what extent the business utilises AI, and how this AI is deployed. A strategic assessment must be undertaken to determine whether AI usage adds value to the business, and whether it will continue after the M&A transaction. Some general aspects for consideration include:

AI development and maintenance in businesses

Strict restraint of trade, confidentiality and intellectual property provisions in employment contracts for AI development and maintenance

Ownership of intellectual property rights in relation to strategic AI inputs and outputs

Costs of in-house AI updates and maintenance

Consideration of off-the-shelf AI solutions for cost-effectiveness over bespoke solutions

Quality of training data which affects the AI system’s value

The difficulty with assessing the value of the AI system during M&A transactions

Almost every AI model processes personal information, requiring compliance with data protection laws during M&A processes. These laws prescribe strict conditions for processing personal information, and often limit automated processing. AI models’ lack of transparency makes it nearly impossible to comply with data subject requests for deletion or correction of processed personal information. M&A transactions may identify this as a risk, potentially decreasing business value or resulting in warranties and/or indemnities against potential sanctions from data protection non-compliance.

Risk assessments

As demonstrated above, AI can add immense value to businesses, but it also introduces risks – many unknown – associated with its use. Businesses must balance AI’s added value against these risks. This balance makes it extremely difficult to accurately value businesses that have developed bespoke AI, or which rely heavily on AI systems.

Standardised risk-based approach Foreign jurisdictions have developed AI risk management frameworks to manage AI-associated risks. For example, the US Department of Commerce classifies generative AI risks into the following categories: technical/model risks (risks of malfunction), human misuse (malicious use), and ecosystem/societal risks (systemic risks).2 Additionally, the European Union’s high-level expert group on AI has developed assessment tools, including ethics guidelines for trustworthy AI, policy and investment recommendations, assessment lists, and sectoral considerations.3 This development raises questions about whether due diligence investigations should apply a standardised approach when assessing AI systems. Evaluations aligned with these frameworks could provide in-depth and uniform AI system assessments. However, these remain recommendations, and many businesses are likely to avoid applying these frameworks due to their onerous obligations.

Contractual risks Most contracts reviewed during a M&A due diligence predate widespread AI adoption and, therefore, inadequately address AI-related considerations. This gap becomes particularly critical when examining agreements with key business partners, including suppliers and customers, where AI usage creates unforeseen legal and commercial implications. Since AI systems generate novel outputs and creative works, contracts must clearly delineate intellectual property ownership rights in any content, data or innovations produced by the AI systems.

Cybersecurity risks Integrating AI technologies into business operations introduces substantial cybersecurity vulnerabilities requiring careful evaluation during M&A processes. These elevated security risks necessitate comprehensive incident management frameworks and robust response protocols to address potential cybersecurity incidents. AI systems significantly alter a target company’s risk profile, often compelling buyers to seek additional contractual protections through specialised indemnities and/or warranties designed to mitigate emerging technological threats. This creates challenges for sellers, as businesses now face exponentially higher probabilities of cyber incidents. The prevalence of cyber incidents makes sellers reluctant to accept expansive liability provisions that could materially impact M&A transactions.

AI in the M&A process

Businesses can use AI at nearly every stage of the M&A transaction, including:

Target identification and screening

Due diligence investigations

Report editing

Transaction document drafting

Post-merger integration monitoring

AI’s ability to process large volumes of data quickly makes it ideal for due diligence processes. Legal-specific AI can review multiple documents simultaneously and provide outputs in user-defined categories.

But while AI expedites due diligence processes, it can also hallucinate outputs. AI hallucination refers to the phenomenon where AI systems, particularly large language models, generate outputs that are incorrect, nonsensical, or lack factual basis, while presenting them as accurate.

The consequences of hallucinations in due diligence processes, where AI fails to identify risks in M&A transactions, could prove ruinous. Thus, dedicated human oversight must ensure factually accurate AI outputs. To mitigate this risk, practitioners can adopt a sampling approach, manually reviewing a sample of AI-reviewed agreements and comparing results to AI outputs. These samples should come from different document categories of varying complexities and importance.

M&A practitioners must also consider potential confidentiality breaches resulting from AI tool use. When uploading confidential M&A transaction documents to AI tools, this information generally becomes available to AI service providers, who may store it on their servers or use it to train their models. This creates significant risks, as sensitive commercial information, financial data, strategic plans, and proprietary business details could be inadvertently disclosed to third parties or accessed by unauthorised persons. M&A transactions require strict information security protocols due to their confidential nature, yet AI systems’ ability to process large data volumes quickly makes them attractive despite these confidentiality risks. Organisations must carefully evaluate AI providers’ data handling practices, security measures and privacy policies before uploading sensitive M&A documentation to AI systems.

In summary

AI integration into business operations fundamentally transforms the M&A landscape in two critical ways. First, the proliferation of AI-enabled businesses creates new complexities in transaction evaluation and execution that require specialised expertise and risk assessment frameworks. Second, AI tools revolutionise how businesses conduct M&A processes, offering unprecedented efficiency gains while introducing novel risks requiring careful management.

Moving forward, successful M&A practitioners must master both the evaluation of AI as a business asset, and the strategic deployment of AI as a transaction tool. This dual competency, combined with robust risk management frameworks and stakeholder transparency, will prove essential for navigating the AI-transformed M&A environment.

1 AI in Business Statistics 2025 [Worldwide Data] by T Benson accessed at https://aistatistics.ai/business/ (on 8 July 2025). 2 National Institute of Standards Technology, Artificial Intelligence Risk Management Framework: Generative Artificial Intelligence Profile accessed at https://nvlpubs.nist.gov/nistpubs/ai/NIST.AI.600-1.pdf on 8 July 2025. 3 European Union accessed at https://digital-strategy.ec.europa.eu/en/policies/expert-group-ai on 8 July 2025.

Tayyibah Suliman is a Director and Izabella Balkovic an Associate in Corporate and Commercial | Cliffe Dekker Hofmeyr

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Private capital investors in Africa are successfully navigating a turbulent investment environment – shaped by global economic challenges and rapidly evolving regulations – and in the process, seizing exciting opportunities in the continent’s energy and infrastructure space.

According to a recent AVCA report, Understanding the Context – Africa’s Infrastructure Financing Gap (Report), Africa receives only 5% of global infrastructure investment, despite hosting 18% of the world’s population.

The report notes that between 2012 and 2023, private capital investors demonstrated a growing confidence in African infrastructure, deploying US$47,3 billion across 847 reported deals, and establishing new models for sustainable development across the continent.

The sector leading the way is Energy, which has attracted significant private sector investment to date, particularly in South Africa, with open access energy regimes evolving across the continent. The aim of such regimes is to open up private investment opportunities, increase grid reliability, and offer energy consumers greater value and more choice.

Other sectors necessary for economic growth, and in which there has historically been underinvestment, such as transport and logistics, and water infrastructure, are also beginning to attract private sector solutions to encourage the pace of development.

Energy

South Africa stands out for the rapid growth in private sector involvement in the energy space since the introduction of the Renewable Energy Independent Power Producer Programme in 2012. Growing investor confidence, market deregulation and a demand that exceeds available supply have led to the emergence of a competitive private power and trading market which has reshaped the way investors and heavy industry users participate in these sectors.

The South African government’s commitment to private sector participation and the liberalisation of the energy market has unlocked substantial foreign direct investment in the renewable energy sector. The UN Conference on Trade and Development noted in 2024 that South Africa’s renewable energy sector attracted US$16 billion in investments between 2020 and 2023 alone.

Over and above the rapidly growing bilateral power market – which was unlocked in recent years through the changes in licensing legislation – the Draft Market Code (Code), issued by the National Transmission Company South Africa (a subsidiary of Eskom) in April 2024, will assist in establishing a transparent, non-discriminatory trading platform based on a multi-market structure under the Electricity Regulation Amendment Act, which became effective in January 2025. The target commencement date of the Code is April 2026, with an open and competitive electricity market expected to be operational by 2031.

The increasing integration of renewable energy into the grid has led to substantial constraints, creating further opportunities for private sector involvement in electricity transmission. The recently announced invitation by the South African government – seeking private sector investment in electricity infrastructure – is expected to result in further private sector participation at the same time as reforms are being introduced.

Across Africa, governments are following suit and launching initiatives to harness private sector participation in the energy sector. This has resulted in private sector-driven, business-to-business power solutions that assist businesses to meet their decarbonisation goals and ensure a stable energy supply.

In Kenya, the country’s National Energy Policy 2025-2034, published in February 2025, focuses on developing the country’s ability to produce sustainable energy, and on improving energy access, affordability and security. A big part of this plan is the implementation of an open energy regime.

The Energy (Electricity Market, Bulk Supply and Open Access) Regulations 2024 were published last year to facilitate the opening of the electricity market, and to enable private sector investors to participate in the generation, transmission and distribution of electricity.

The emergence of private transmission opportunities has resulted in the first transaction of its kind on the continent, a public-private partnership involving the development of two power transmission lines: the 400 kV Loosuk-Lessos line and the 220 kV Kisumu-Musaga line.

Zambia also recently adopted an open access regime, which enables IPPs and large power consumers to engage in electricity trading by connecting to and utilising the electricity transmission and distribution networks, irrespective of the network’s ownership or operation. This new regime is anchored by the Electricity Act of 2019 and the Electricity (Open Access) Regulations 2024.

Transport and logistics infrastructure

Historic underinvestment in the maintenance of South Africa’s ports and rail has led to increased use of road transport for bulk logistics, which in turn has led to increased transportation costs and roads that are buckling under the strain. According to reports, as of 2024, these challenges are estimated to cost the South African economy approximately R1 billion per day in lost economic activity.

The South African government is turning to the private sector to fund the infrastructure development, which is desperately needed.

For example, South Africa’s state-owned freight logistics company, Transnet’s PSP programme represents a significant opportunity for private participation in the country’s rail, port and logistics sectors. Opportunities for investment include those in port modernisation and efficiency. For example, the Durban Port Master Plan aims to attract R100 billion in private investments over the next ten years. Further opportunities exist in the rail network and rolling stock, large container development, and supply chain management.

Private sector participation is also being sought for the development of logistics corridors to enhance regional connectivity across Africa.

In both Kenya and Zambia, private participation in the public sectors is being pursued through legislative frameworks such as the Public

Private Partnerships (PPP) Act 2021, in Kenya and the Public-Private Partnership Act, 2023 in Zambia, to progress and develop complex infrastructure projects by addressing the enforcement of legal compliance and swifter project implementation.

There are growing numbers of infrastructure funds that are playing a significant role in driving the growth and development of infrastructure across Africa. These funds include African Infrastructure Investment Managers (AIIM), Helios Investment Partners, and Afri Fund Capital.

Water infrastructure

In South Africa, government-procured water projects, as well as private sector solutions to water infrastructure needs, are emerging. At the forefront are new bulk water projects, including the construction of infrastructure such as pipelines, and privately procured water treatment facilities. The potential for private investment in this space is significant, offering investors the chance to contribute to the development and management of critical infrastructure.

Across Africa, governments are implementing measures to facilitate private investment in the water sector through the PPPs model. For example, Kenya recently introduced the Water (Amendment) Bill, 2023, and Zambia published the National Water Policy in 2024, with both outlining plans to harness private investment to finance water sector projects.

Bridging the gap

Amid challenging market conditions, private investors are stepping up to bridge critical funding gaps, channelling much-needed capital into initiatives that fuel growth and deliver significant social and economic benefits for the continent.

Angela Simpson and Alexandra Clüver are Partners | Bowmans

This article first appeared in Catalyst, DealMakers’ quarterly private equity publication.

Key metrics are up and so is guidance for the full year

Alphamin has released numbers for the third quarter of 2025, reflecting contained tin production that was 26% higher than the previous quarter. Best of all, guidance for the full year is up from 17,500 tonnes to between 18,000 and 18,500 tonnes.

Contained tin sales came in 12% higher than the prior period. The average tin price achieved was up 4% and all-in sustaining costs (AISC) per tonne was 3% lower. When you consider all these metrics, it won’t surprise you that EBITDA was up by a juicy 28% vs. the preceding quarter.

These are quarter-on-quarter numbers, not year-on-year. Before you get too excited though, the important context is that there were security issues early in the preceding quarter that made it a soft base for comparison. The security risks are never zero when you’re operating in regions like the DRC. The company has noted a recent increase in security events on a key border line that is about 200kms away from the mine. At this stage there are no disruptions to operations, but the risk is clearly there.

On the exploration side, the company has continued with drilling at Mpama North and Mpama South to increase the resource base and life of mine. They also plan to discover the next tin deposit near the Bisie mine, as well as any remote tin deposits on the land package. Those are long-term plans, with the focus right now on the drilling results at Mpama North and Mpama South.

Anglo American’s Teck Resources era isn’t off to a great start (JSE: AGL)

Teck has cut production guidance at two of its copper assets

The trouble with large corporate deals is that when you assure the market that a particular mega-merger is a great idea (despite a zillion historical examples of dicey shareholder value outcomes in these types of deals), you really can’t afford for any bad news to come through. Anglo American’s reputation for deal timing just won’t leave them alone, with now-demerged Valterra Platinum (JSE: VAL) rallying like crazy and future dance partner Teck Resources releasing a tough announcement.

If you would like to read the detailed Teck announcement, you’ll find it here. The TL;DR is that due to project challenges at Quebrada Blanca, they now have an expectation of increased downtime in both 2025 and 2026. Mining projects are incredibly complicated and dangerous things, so it’s critical to do them properly and make the tough decisions when required. But this doesn’t mean that shareholders are happy to see this stuff, particularly Anglo American shareholders who need to believe that the Teck merger is the right decision for the group.

Guidance for 2025 copper production at Teck has been cut by over 11% if you use the midpoint of guidance. That’s particularly frustrating for the company at a time when copper prices are strong. Teck’s guidance for zinc is unchanged at least.

Unfortunately, as is always the case when production comes in lower than expected, the unit cost of the commodity has increased significantly. They expect a 20% increase in the net cash costs per pound at problematic Quebrada Blanca for 2025.

Of course, if this is just a temporary wobbly, then it isn’t the end of the world. The problem is that if you read Teck’s 2026 – 2028 outlook, the issues just get worse as time goes on. The mid-point of copper production guidance at Quebrada Blanca for 2027 and 2028 has dropped by approximately 13% and 17% respectively. At Highland Valley Copper, they expect some pressure on 2026 production and then a significant improvement in 2027 ahead of prior guidance. At Red Dog zinc, guidance for 2027 and 2028 is below previous guidance.

You get the idea. These numbers are fluid and will be updated as time goes on, but the theme is clearly one of a disappointing production outlook vs. previous guidance. Anglo American’s response is that their independent due diligence led to an expectation that is “broadly consistent” with Teck’s latest numbers. This suggests that Anglo did a better job of understanding these assets through the due diligence process than Teck management did by living with them every day. You’ll forgive my skepticism here.

Investors tend to be nervous of large deals as a default setting. Deals that involve a deterioration in expectations at the target asset are even scarier.

Exciting news for Ethos Capital and the market: Optasia intends to float (JSE: EPE)

New listingsare always fun

When a company announces an intention to float, this has nothing to do with their December holiday plans. Instead, it means that they will be coming to market through a listing process, with Optasia (a name you’ll recognise as being the most important investment in the Ethos Capital stable) looking to do exactly that on the JSE.

New listings are the lifeblood of the market, so they always lead to excitement, particularly when it’s a proper listing with a company that has put in the work. Check out the Optasia IPO website and you’ll see what I mean.

What does Optasia do? Well, you have to look through a lot of buzzwords (including AI) to arrive at the understanding that this fintech focuses on providing access to credit and airtime in underbanked markets. In other words, this is a classic African fintech story, although they have a presence in Asia, the Middle East and even some parts of Europe!

Optasia has been around since 2012 and has 350 employees across 15 offices, so they are a scale player. There are 121 million monthly active customers. Revenue for the first half of 2025 was up more than 90% year-on-year, so this is a beautiful example of the J-curve in action. They are very profitable at adjusted EBITDA level with a margin of 46%, although the adjustments always need to be treated with caution. The company is certainly profitable though, with a substantial jump in net profit from $7.6 million to $23.3 million in the six months to June 2025.

The width of the moat comes from the extent to which Optasia has managed to build an ecosystem with multiple touchpoints. It’s a complex marketplace, with financial institutions on one side and distribution partners in the middle, all before reaching consumers on the other side who become more familiar with the offering over time. That’s a very hard thing to build, especially across multiple geographies.

As for the listing, they are looking to raise R1.3 billion, so this is decently sized raise in the local market. It looks like it will be done through institutional investors only (rather than an offer to the public). Certain existing shareholders are also going to sell R5 billion in shares to institutional investors.

As for Ethos Capital, they haven’t specifically said whether they are one of the selling shareholders. Given their stated approach of returning value to investors, it seems like that they intend to either fully or at least partially exit the Optasia stake.

FirstRand’s battle in the UK motor finance industry isn’t over (JSE: FSR)

The company is unhappy with the proposed redress scheme

FirstRand (along with other financial services companies operating in the UK vehicle finance market) is dealing with a difficult regulatory situation related to commission practices around vehicle finance. It looked as though the worst of the uncertainty was behind them after the UK Supreme Court ruling that gave legal clarity to the situation, but that joy was short-lived.

The UK’s Financial Conduct Authority (FCA) has proposed a redress scheme that FirstRand describes as being “beyond expectations of what can be considered proportionate or reasonable” – and that’s not good for FirstRand shareholders. They haven’t indicated what the amounts would be at this stage, but FirstRand wouldn’t have released an announcement with that wording if they felt that their existing provision was adequate to cover it.

As part of pushing back against this, they’ve flagged their disagreement with the lack of application of the recent UK Supreme Court ruling to the redress scheme.

There will now be a period of six weeks of consultation with the UK FCA. FirstRand has undertaken to keep the market informed of any developments that might happen before the end of that period as they consult with the regulator.

Nibbles:

Director dealings:

A director of Woolworths (JSE: WHL) sold shares worth R23.2 million and a director of a major subsidiary sold shares worth R7.2 million. With the share price down 16% year-to-date, that’s not exactly a bullish signal about the chances of a near-term recovery.

A non-executive director of Mondi (JSE: MNP) bought around R508k worth of shares. The price was R203.30, so the purchase must have been after the initial drop in response to earnings. The price has subsequently kept sliding, now at R195.

City Lodge Hotels (JSE: CLH) announced that they’ve repurchased R170 million worth of shares since March 2025 at an average price of below R4.00. The share price is currently R4.20. This represents 7.14% of shares that were in issue as at the date of the AGM last year, so this should be a very helpful boost to HEPS going forwards.

Wesizwe Platinum (JSE: WEZ) announced that the ramp-up of underground operations is ahead of schedule. They are negotiating key development contracts and will keep investors informed of further milestones.

Kibo Energy (JSE: KBO) is suddenly back on our screens, with news of a potential acquisition of a decarbonisation and renewable energy company called Carbon Resilience. I’ve gotta tell you, carbon resilience is the kind of resilience that investors needed to get to this point, as Kibo has been a story of one corporate disappointment after the next. Perhaps the new chapter will be different, with Kibo looking to acquire the asset for $135 million, settled through the issuance of shares after a planned 1600:1 share consolidation. Just to add to the dilution of value of current shareholders, the company has also issued a convertible note to an institutional investors to provide funding of up to £150k. As part of lifting the suspension of the listing on AIM, the company needs to get the accounts for the year ended December 2024 out the door.

Accelerate Property Fund has finally released the Portside disposal circular (JSE: APF)

Turning the Portside stake into cold, hard cash is crucial for the fund

If you’re familiar with the Cape Town CBD skyline, then you already know the Portside building. It’s the gigantic glass building in town that towers above everything else. When Accelerate originally bought it from Old Mutual Life Insurance Company in 2016, they paid R755 million for it. That was then and this is now, with the latest valuation being R610 million and Accelerate achieving a selling price of R580 million.

Before you get out the torches and pitchforks, I must tell you that many property deals done around 2014 – 2016 in South Africa were concluded at ridiculously high prices. Property certainly isn’t immune to bubble risks, with the level of equity capital raising activity among listed property funds as a great indication of whether things are overcooked or not. During those years, the pot was boiling over with capital being thrown at every property company in the market.

The relevance of this deal isn’t the return (or lack thereof) over the past decade, but rather the critical importance of this disposal to the recovery of Accelerate. With a bruised and broken balance sheet (and share price), Accelerate simply cannot afford any further missteps. They are dealing with very tough related party risks, as well as the difficulty in transforming Fourways Mall from a white elephant into a cash cow. There are also other assets that need to be disposed of, including several that aren’t nearly as impressive as the Portside silhouette.

This disposal reduces Accelerate’s total debt from R3.85 billion to R3.27 billion. The total asset value after the disposal will be just over R7 billion. The net asset value (NAV) of the company is barely impacted vs. the March 2025 level, as they’ve sold the property at the carrying value as at that date. In other words, one type of asset is being turned into another. That’s not the point though – you see, when a share is trading at a vast discount to NAV, it creates a lot of value for investors (punters?) if that NAV evolves from illiquid fixed assets to liquid cash.

The net asset value per share as at March 2025 was R2.03. The dilutive rights offer took that down to R1.83. The pro forma number after this deal is R1.82. And the share price? Just R0.39 per share, reflecting a discount to NAV of 79%!

This is why existing shareholders should feel very good about every single example of Accelerate turning an asset into cash at or near the carrying value.

Accelerate shareholders will vote on this deal on 6th November. The other remaining condition for the disposal is a Competition Commission approval without any onerous conditions attached to it. I can’t see why that would be a problem in a property deal like this.

Is Afrimat primed for a big positive swing? (JSE: AFT)

The latest update shows a remarkable turnaround in the business

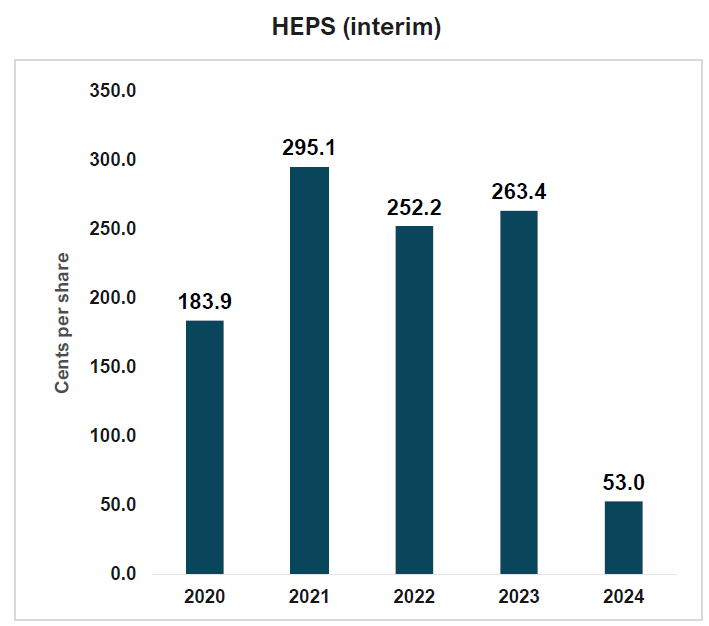

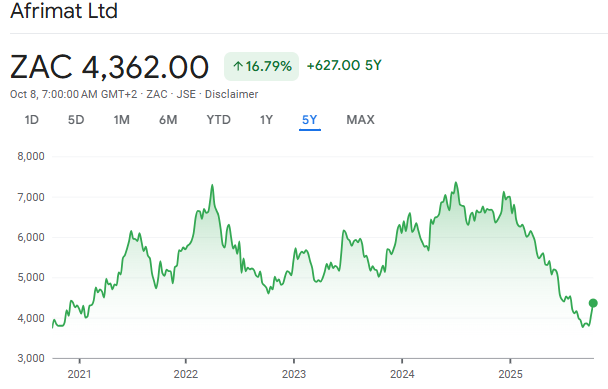

Afrimat has released a trading statement for the six months to August. With the share price having lost well over 40% of its value year-to-date, they desperately needed to show some positive momentum in the group.

The good news is that they’ve done exactly that, with an expectation for HEPS of between 100.7 cents and 103.4 cents. That’s an increase of between 90% and 95% vs. the comparable period! When you see moves like these, it’s very useful to go back a bit further and example the multi-year performance. In the six months to August 2023, HEPS was 263.4 cents. In fact, if you go back to the results presentation for the six months to August 2024, you’ll find this excellent chart:

The key point here is that HEPS was incredibly depressed in 2024, so the year-on-year move of between 90% and 95% doesn’t mean much. The guided range is still way off the pandemic levels and even the pre-pandemic levels.

It therefore makes sense that the share price is also still miles off those levels:

Of course, the real question is whether this will be enough to stop the slide and perhaps drive a rally back up to the R50 level. Afrimat closed 10.7% higher in response to this announcement, so that’s a sharp improvement in momentum.

The fundamental drivers of the improved performance in this period look good overall, although there’s still a long way to go.

In Construction Materials for example, there was a slow start to the first quarter and then a much better second quarter. The fly ash business had its best ever month in July in terms of volumes. But the cement business remains loss-making overall for the first half, showing just how difficult it is to make that business work.

The Bulk Commodities business enjoyed a massive increase in iron ore sales, with local volumes more than doubling vs. the comparable period. International volumes posted a more modest increase of 13.5%. Don’t get too excited though, as planned maintenance shutdowns of the Saldanha export line during the second half should lead to a situation where full year volumes are flat vs. the prior year. Another concern is the anthracite mining operation, which is suffering with decreased demand from ferrochrome smelters that have been forced to temporarily shut down in South Africa due to harsh economic realities in that sector. Afrimat is exporting anthracite via Mozambique to try and mitigate this lack of demand.

The Industrial Minerals business is a small part of the group, but had a weak half due to delayed demand from the agricultural sector based on the timing of rainfall.

The Future Materials and Minerals business is an early-stage business, with the economics expected to be three years away. Thankfully, no additional capital investment is expected to get them there. The Glenover project is selling phosphate material and is decreasing its operating losses.

Detailed interim results are expected to be released on 23 October.

Datatec has taken some inspiration from how global tech companies report numbers (JSE: DTC)

The goodnews is that they are firmly in the green either way

Datatec has released a trading statement for the six months ended 31 August 2025. The underlying story is great, with Westcon achieving stronger margins and both Logicalis International and Logicalis Latin America achieving much better numbers than before.

This has driven a juicy increase in HEPS of more than 100%, with expected earnings of between 21 and 23 US cents for the period.

Datatec has decided to present underlying earnings excluding share-based payments (and with various other adjustments). This will sound familiar to anyone who regularly reads the reports of global technology companies. I’m not a fan of this approach, as US companies use it as a great excuse to ramp up share-based payments and then conveniently adjust earnings accordingly. I’m hoping that Datatec won’t behave in that way and that they are rather doing this to improve comparability of their earnings to global peers.

On this adjusted basis, underlying earnings will be between 18 and 20 US cents, or between 33.3% and 48.1% higher than the prior year. This seems to be a decent indication of the year-on-year growth that the company achieved.

Either way, it’s excellent.

Finbond is back in the green (JSE: FGL)

The share price has been strong this year

Finbond is one of those companies that always seems to be bubbling under the surface. They have some interesting elements to their business model, yet it rarely seems to all come together for them in a way that rewards investors. But in the latest period, they’ve at least swung back into profitability.

A trading statement for the six months to August 2025 suggests HEPS of between 0.88 cents and 1.28 cents, which is much better than a loss of 2 cents in the comparable period. But it’s also nowhere near high enough to justify the current price of R1.05 per share, so the market is clearly pricing in much more upside in earnings. The share price is up more than 65% year-to-date.

Newpark REIT has released updated earnings guidance (JSE: NRL)

The large negative reversion at the JSE has hurt the year-on-year performance

Newpark is a particularly unusual property fund on the JSE. They have a very focused portfolio with literally only a handful of buildings. This means that any negative changes to the leases have a significant impact on the numbers.

Exhibit A: the large negative reversion in the lease for the JSE building. Much as I’m sure the JSE really wants to be where they are, the truth will always be that it’s easier to move a business than a building. In a market with oversupply, like in Sandton offices, this creates a recipe for negative reversions i.e. the renewed lease being at a lower rate than the old lease.

This is why Newpark guided for a nasty year-on-year decrease in earnings this year of between 38.1% and 47.1%. This is actually updated guidance that is slightly better than before, with Newpark trying to mitigate the negative impact through strategies like decreasing the operating costs at the properties. They also have escalations at the other properties to offset some of the impact of the JSE building.

For the six months to August, they expect funds from operations per share to decrease by 24.5%. The dividend for the period is expected to be 13.3% lower. It looks like they are front-loading the interim dividend when you compare it to the guidance for the full year.

SA Corporate Real Estate to sell Bluff Towers (JSE: SAC)

The fund is reducing its retail exposure to KZN

SA Corporate Real Estate announced the disposal of Bluff Towers Shopping Centre for R544.6 million. The price is very similar to the June 2025 independent valuation of R545.1 million. With net property income of R44.7 million for the year ended December 2024, that’s a trailing yield of 8.2%. The recent income would hopefully be higher due to the benefit of inflation, but it gives you an idea of the yields at which large retail properties are changing hands.

SA Corporate Real Estate has disclosed that the net asset value attributable to the property was R358 million as at the end of December 2024. I assume that this is net of debt, as that’s way below both the recent valuation and the selling price.

This deal is effectively a disposal of an asset that has been redeveloped to maturity, something that is reflected in the attractive price that SA Corporate Real Estate has achieved here. The fund will probably look to reallocate the capital to opportunities with higher potential returns. This is a Category 2 transaction, so shareholders won’t be asked to vote on the deal.

Nibbles:

Director dealings:

The CEO of Fortress Real Estate (JSE: FFB) increased the number of shares pledged for a loan facility, as the facility limit has increased from R26 million to R34 million. This is nothing unusual in the property sector, with many executives entering into leveraged trades to acquire shares in the funds that they run.

MAS (JSE: MSP) recently announced a tender offer to reduce its debt in the market. That’s a big deal if you’ve followed the fund over the past few years, as full focus has been on trying to prepare the balance sheet for debt redemptions. The tender offer was made to holders of €300 million in notes due 2026. Almost €120 million was tendered under the offer, with holders of the remaining notes clearly keen to keep them until expiration.

Barloworld (JSE: BAW) announced that the standby offer closing date has been extended from 15 October to 7 November. They are obviously trying to get as many acceptances as possible.

Salungano Group (JSE: SLG) is catching up on its financial reporting. They’ve now released financials for the year ended March 2024, with the auditors flagging a material uncertainty about the group as a going concern. The headline loss per share increased from 58.65 cents to 111.91 cents. It’s a mess.

Southern Palladium (JSE: SDL) has lodged the environment guarantee in relation to the Bengwenyama PGM project, which is an important milestone related to the mining right application with the Department of Mineral and Petroleum Resources. The mine development plan for the Definitive Feasibility Study is on schedule. In junior mining, it’s all about ticking the milestones off the list.

The Saltzman family continues to reduce their influence on the group that they founded, with Saul Saltzman (son of the founders) resigning as an executive director of Dis-Chem (JSE: DCP). He will stay on the board as a non-independent, non-executive director. Dis-Chem has been an incredible example of founders creating a legacy business and then trusting professional managers with it.

The digital generation has access to more information and tools than ever before. But the more things change, the more they stay the same: one of the most powerful tools of all remains the benefit of starting young and entrenching the right money habits from as early as possible in your life.

And yes, this includes investing on behalf of your children!

In this episode of Ghost Stories, Lauren Jacobs (Senior Portfolio Manager at Satrix) joined me for a candid discussion about her approach to entrenching the right financial behaviours from early in her career and the journey of investing for her family.

We also talked about the value of learning by doing, which means testing out the market and banking the hard lessons sooner rather than later!

The concept of “time in the market” is one of the most powerful wealth creation strategies of them all. If you are looking for the inspiration to just start, or a refresher on why those tough-to-form habits are so worthwhile, then you’ll love this discussion.

Disclaimer: Satrix Investments (Pty) Ltd & Satrix Managers (RF) (Pty) Ltd is an authorised financial services provider. The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information. Consult your financial advisor before making an investment decision. Tax Free Savings Accounts: Annual limit of R36000, lifetime limit of R500 000, 40% tax penalty applicable for contributions above the limit, per individual.

Full Transcript:

The Finance Ghost: Welcome to this episode of the Ghost Stories podcast featuring the team from Satrix and this time around I get to speak with Lauren Jacobs again. She is a Senior Portfolio Manager at Satrix.

Lauren and I had a fantastic discussion earlier this year where we really got to understand so much about the nuts and bolts of Exchange Traded Funds or ETFs. I think the TL;DR of that conversation was that it might be a nice passive buy-and-hold investment for investors, but there’s nothing passive about what happens in the back-end for Lauren and her team – there is a lot to do all the time.

Fresh from another index balancing, Lauren, thank you for making time for doing this podcast. I know it’s been a busy time for you.

Lauren Jacobs: It’s good to be back again, Ghost. Thanks for having me. Yeah, we did have quite a hectic week last week, but we’re back in action on all the other things. So yeah, happy to be here.

The Finance Ghost: Yeah, fantastic. Another one under your belt there. Today we’re going to be talking about a couple of things, but the overarching principle of this podcast is around the importance of digital tools, not just for younger investors, but also for any investor, really. It’s just obviously younger generations of investors tend to be a little bit more familiar with some of the digital tools that are out there.

We’ll also just be talking about the importance of an early start and some of that as well.

And I think, Lauren, what’s going to make it extra fun is we’ll kind of be asking each other a few questions because I think you’re probably going to ask me a few about some of the tools that I use as well. So I’m looking forward to a nice dynamic conversation.

I think let’s jump straight into it and start with really the key principle here, which is that old story of: is it ever too early to start or is it always good to just start as early as possible in the market and why?

Lauren Jacobs: Yeah, Ghost, I think it’s really important to just start and whenever that is, whether it’s as a parent for your kids or as a young person, if you have a job but you earn some money and want to put some money away, it really is important to start early. And the really powerful concept here that we want to keep in mind is compound interest. Because when you invest, your money earns returns and then those returns earn returns and those returns earn returns, and it just snowballs. And obviously the longer you have to earn those returns, the larger your investment could be over time. It’s not just about the numbers – it’s also the fact that when you are young, you can take more risks, you have more time to recover from market dips and also you learn from an early point in your life, whether that’s age or just in terms of point in your life, you really learn to build financial discipline, which is important for anybody to learn.

The Finance Ghost: Yeah, absolutely. I mean, the benefit of doing this younger is that a market crash – maybe that sounds a bit harsh – but a market dip, whatever the case may be, almost becomes an opportunity rather than something else. You only have to look historically, long-term returns on the big market indices, the big equity indices specifically, it recovers every time, it takes time – not at individual stock level – but at market level.

And that’s the benefit of ETFs, right?

Lauren Jacobs: So when you’re young, you have this major advantage of time. And time allows you to take on more financial risk because you have these years, even decades, to recover from those market downturns. And markets go up and down, like you said, I mean, it’s normal. One day it’s up, one day it’s down. Maybe it’s down for a significant number of months.

But if you start investing early, you can ride out those dips. You don’t need to panic when the market drops 10%, 20% because you’re not planning to take your cash out next year. You’re investing for the long-term.