Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

e>

A special distribution at enX (JSE: ENX)

This is being funded from the proceeds of the Eqstra disposal

enX announced that the disposal of Eqstra was completed and the gross proceeds of R1.14 billion (subject to some deductions and escrow amounts) have been received.

The net amount after those adjustments is R990 million. This has triggered the declaration of a distribution by the company of R5 per share.

The weather isn’t being kind to Gold Fields (JSE: GFI)

Salares Norte in Chile has been hit by the earlier onset of winter in Chile

Mining isn’t an easy gig at the best of times. It’s even worse when the weather doesn’t play ball. Gold Fields is the latest example of the weather giving a mining group a hard time, with an earlier-than-expected winter in Chile playing havoc with the commissioning and ramp-up phase at Salares Norte.

Long story short, calendar year 2024 production for the project has been revised down from 220koz – 240koz to 90koz – 180koz. This range is largely independent of weather events until late August.

The impact on group production guidance is a decrease from 2.33Moz – 2.43Moz to 2.20Moz – 2.30Moz. But when production is lower, all-in costs inevitably move higher. The previous range of $1,600/oz – $1,650/oz has been revised to $1,675/oz – $1,740/oz.

And to make it worse, Gold Fields can’t even use the disrupted winter months to capture and relocate chinchillas. If it’s not the weather, it’s the environmental considerations that make mining difficult.

The market didn’t love this obviously, with the share price down 11% for the day.

Mr Price looks to be struggling (JSE: MRP)

This doesn’t look nearly as strong as what we’ve seen from the likes of TFG

When a group has been active with acquisitions, you always have to be careful when interpreting their results. Buying earnings is one thing. Growing them on a comparable basis is quite another.

For the 52 weeks ended March 2024, Mr Price grew revenue by 15.5%. That sounds amazing of course, but it was only 5.8% if you exclude the Studio 88 acquisition. Now we are getting closer to the right lens on these numbers. Comparable store sales tell the real story, as this excludes the growth in the footprint. This metric only increased by 1.8% for the full year, with the silver lining of significant momentum into the second half of the year. The Home segment came under particular pressure, with a negative move in comparable sales.

Mr Price seems to have given up the online fight, especially when you compare it to Bash within The Foschini Group. At Mr Price, online sales decreased by 2.2% and now contribute only 2.1% of total sales. Without Studio88, online sales were down 3.7%. And yet despite this, they talk about how South Africans favour omni-channel shopping. It’s true, they do, hence why it isn’t good to see online sales moving in the wrong direction.

Unlike at Pepkor where the focus is on credit sales, Mr Price only saw growth of 1.7% in that metric. Cash sales excluding Studio88 were up 7.0%.

Gross margin was a tale of two halves. Although it was only 20 basis points higher for the full year, the second-half performance was an increase of 160 basis points to 40.6%.

Another worry for me is the cost growth. Excluding Studio88, it was up 7.8% – and that’s higher than revenue growth.

Profit from operating activities was up 7.9%. This includes Studio88. It’s important to note that operating profit margin contracted by 110 basis points to 14%.

At least inventory was down 4.2% at the end of the period, leading to a better working capital outcome and improved stock freshness.

HEPS for the year was up 6.7%. The second half momentum is what needs to continue, as earnings were up 17.4% in the second half of the year.

My overall feeling on Mr Price is that they find themselves in an awkward strategic position. Acquisitions for the sake of acquisitions make a group bigger, not necessarily better. They aren’t the credit sales powerhouse that Pepkor is becoming, nor have they tackled online in the way that TFG have. It’s hard to really pinpoint the Mr Price strategy and that’s a concern.

Novus updates its earnings range and has an update on the Bytefuse deal (JSE: NVS)

This is a strong period of profitability

For the year ended March 2024, Novus has guided that the range for HEPS is between 78.02 cents and 79.49 cents. That’s a huge improvement from the small headline loss per share in the prior period.

Separately, the group announced that the fairness opinion related to the acquisition of Bytefuse has been finalised. The independent expert has opined that the terms of the deal are fair.

Little Bites:

Director dealings:

A prescribed officer of ADvTECH (JSE: ADH) sold shares in the company worth nearly R950k.

A director of a major subsidiary of Shoprite (JSE: SHP) bought shares worth R297k.

Des de Beer has bought shares in Lighthouse (JSE: LTE) worth R200k.

If you are interested in Raubex (JSE: RBX), then check out the site visit presentation related to Bauba Resources. You’ll find it here.

Impala Platinum (JSE: IMP) announced that all conditions for the B-BBEE transaction have been met and the deal has been implemented.

Invicta (JSE: IVT) has announced the redemption of its preference shares in issue at a small premium. There has been a trend of preference share redemptions, as this asset class didn’t really work out on the JSE in the way that was intended.

Conduit Capital (JSE: CND) is going from bad to worse. The headline loss per share has worsened by between 24% and 64%. This is despite the group achieving its first net underwriting profit since 2016.

Premier Group has acquired a 30% shareholding in rice distributor Goldkeys International for a cash consideration of R313,6 million. The company, which imports rice, supplies branded Thai and Indian sourced rice under its brands Golden Delight, Golden Pride and Light & Right. The investment builds on the May 2023 relationship when Premier entered into a Sales, Merchandising and Route to Market Services agreement.

Nedbank Private Equity (Nedbank) has disposed of its stake in Entersekt to Pape Fund 3 for an undisclosed sum. Entersekt provides financial institutions with digital banking fraud prevention and payment security solutions through its cross-channel, Context Aware™ Authentication platform.

Heriot REIT is to acquire the shares in CTSE-listed Thibault REIT. Heriot will issue 63,886,124 consideration shares valued at c.R1,1 billion equating to an exchange ratio of 62 new Heriot shares for every 100 Thibault shares. In addition to its current retail, office and residential portfolio of 87 521.67m², Thibault holds a 10.02% interest in Safari REIT and a 19.33% interest in Texton REIT. Heriot Investments is a material shareholder of Heriot holding c.86.76% of the issued share capital and is also a material shareholder of Thibault, holding c.97.66% of the issued share capital of Thibault. Thibault will delist from the CTSE on 9 July 2024.

Delta Property Fund has disposed of the property situated at 215 Peter Mokaba Road in Morningside, Durban. The Lexis Nexis Building was sold to Icebolethu Funerals for a cash consideration of R37,38 million.

Exemplar REITail has concluded an agreement to acquire Eerste River Mall in Stellenbosch from the Klein Welmoed Trust for a cash payment of R282 million.

The R60 million sale of Cherry Lane Shopping Centre by Accelerate Property Fund to Cadastral Assets announced in March has been terminated. Accelerate has entered into another sale agreement to dispose of the property, this time with QSPACE for a cash consideration of R57 million.

Visual International has cancelled its related party acquisition of a 20% stake in Tuin Huis. The terms of the deal, announced in March 2023, were that Visual would be responsible to build and project-manage all development projects undertaken by Tuin Huis at cost, with the intention to complete at least three Infill Housing Projects per year. However, due to the Infill Housing project running at a loss due to the weaker property sector over the past year and a change in strategic vision by the company, the parties have agreed to the cancellation of the transaction.

Unlisted Companies

Admaius Capital Partners, headquartered in Rwanda, has acquired a stake in Johannesburg-based The Particle Group (TPG), a manufacturer and retailer of specialist chemical products used in mining processes. Admaius is investing alongside TPG’s senior management via an exit by the Synerlytic Group. Financial details were undisclosed.

Accelerate Property Fund has announced the results of its R200 million capital raise by way of a fully underwritten renounceable rights offer. Of the 500 million shares offered at 40 cents per Rights Offer share, the underwriter took up 135 million shares for R54 million.

Omnia is to pay shareholders a special gross dividend of 325 cents per share, payable in cash from income in respect of the year ended 31 March 2024. The aggregate R537 million is in addition to a final gross ordinary dividend of 375 cents per share.

Equites Property Fund will issue 28,111,564 new shares at an issue price of R12.00 per share in lieu of a final dividend resulting in retained profits of R337,34 million.

Shareholders holding 4.5% of Oasis Crescent Property Fund units qualifying to receive a distribution opted to reinvest the distribution. A total of 56,201 new units were issued amounting to R1,69 million.

enX is to make a special distribution of R5.00 to shareholders following the divestment of Eqstra Investments and receipt of R990,5 million net of retention and escrow amounts. The special distribution is deemed to be a dividend for tax purposes.

Trustco will issue 1,26 billion conversion shares and 2,52 billion shares settlement shares to lenders of the company (Q van Rooyen and Next Capital, both related parties to the company) to convert the company’s indebtedness. The shares will be issued at N$1.17 per share. To facilitate the transaction, the company will increase the authorised share capital from 2,5 billion ordinary shares to 7,5 billion ordinary shares. As this is a category 1 transaction, a circular will be distributed to shareholders who will vote on the transaction.

Invicta is to redeem 6,857,757 outstanding preference shares in issue at R102.50 per preference share.

Scheme conditions have been fulfilled with the result that the offer to buy out Ibex Investment (formerly Steinhoff Investment) preference shareholders has become unconditional. The termination of the listing of the preference shares from the JSE will be on 25 June 2024.

Cilo Cybin, an entity formed to list on the JSE as a SPAC (Special Purpose Acquisition Company) will list 71,017,906 ordinary shares on AltX, commencing trading on 25 June 2024. The company will pursue the acquisition of, and investments in, commercial enterprises operating in the Biotech, Biohacking or Pharmaceutical sector that will enable it to develop and expand methodologies by utilising Artificial Intelligence to deliver holistic and individualised solutions to better health, performance and longevity.

A number of companies announced the repurchase of shares:

In terms of its US$5 million general share repurchase programme announced in March 2024, Tharisa has repurchased 18,577 ordinary shares on the JSE at an average price of R18.12 per share and 510,372 ordinary shares on the LSE at an average price of 76.72 pence. The shares were repurchased during the period June 3 – 7, 2024.

In line with its share buyback programme announced in March, British American Tobacco this week repurchased a further 211,835 shares at an average price of £24.04 per share for an aggregate £5,1 million.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 3 – 7 June 2024, a further 3,109,646 Prosus shares were repurchased for an aggregate €105,72 million and a further 291,362 Naspers shares for a total consideration of R1,12 billion.

Four companies issued profit warnings this week: Efora Energy, Vunani, Motus and Conduit Capital

Three companies issued cautionary notices this week: Trustco, Conduit Capital and The Spar Group.

Diageo has announced that it will sell its 58.02% stake in Guiness Nigeria PLC to Tolaram for NGN81.60 per share. The Nigerian firm will remain listed on the NGX following completion of the deal and Tolaram intends to launch a mandatory takeover offer. Diageo will retain ownership of the Guinness brand which will be licensed to Guinness Nigeria for the long-term.

Renew Capital Angels has invested in Zuri, a tech-enabled beauty company headquartered in the DRC. Zuri, founded in 2016 by Gisèla Van Houcke, aims to empower women through beauty, with products specifically designed to highlight and celebrate black women’s beauty.

British International Investment has sold its 10.1% stake in East African banking group, I&M Group to AfricInvest. Financial terms were not disclosed.

Development Partners International (DPI) has announced its second exit for the year – the investment firm has sold 100% of International Facilities Services (IFS) to a consortium comprised of ES-KO, Phatisa and IFS management. DPI first invested in the integrated facilities management business back in 2019. Financial terms were not disclosed.

African Export-Import Bank has disbursed US$40 milion in the form of an Intra-Africa Investment facility to Fidelity Bank Nigeria to support the bank acquisition and recapitalisation of Union Bank UK. The facility was provided in two tranches – the first $20 million was used to part-finance the acquisition and the second will support the recapitalisation.

Egyptian fintech Sahel has raised US$6 million in Serie A and seed funding. The Series A was led by Egyptian investment firm, Ayady for Investment and Development who joined existing investors Egypt Pay, Delta Electronic Systems and E-Finance.

Oikocredit has provided AfricInvest Private Credit (APC) with a US$10 million loan to support small and medium enterprises (SME’s) in Africa. APC is a non-bank financial institution, providing structured debt financing solutions to SME’s.

Disruptech Ventures, OneStop Capital, Axian Investment CVC, Egypt Ventures and other investors have participated in a pre-Series A funding round in Egyptian B2B medtech, i’SUPPLY, bringing the firm’s total funding to US$2,5 million since its inception in 2022.

The International Finance Corporation (IFC) has provided Johnvents Industries with a US$23,3 million financing package to help fortify the Nigeria agricultural sector and provide support to farmers in the West Africa country. The financing package includes an $8,5 million loan from IFC’s own account, a $6,3 million loan equivalent in Nigerian Naira with support from the local currency facility of the International Development Association’s Private Sector Window, and a $8,5 million loan by the Private Sector Window of the Global Agriculture and Food Security Program (GAFSP).

The Sovereign Fund of Egypt (SFE), via its healthcare sub-fund, has acquired a 20% stake in Care Pharmacies for EGP75 million. Under the terms of the transaction SFE will take control of 45 of the 220 branches run by Care Pharmacies.

Forget bidding wars and boardroom battles – the new frontier of mergers and acquisitions (M&A) is a data-driven battlefield. Success in today’s fast-paced market depends more on the smart use of legal technology and artificial intelligence (AI) than it does on having million-dollar muscles.

M&A has always been a high-stakes game, but the emergence of these new dealmakers is changing the game by turning tiresome due diligence procedures into opportunities to find hidden treasures and spot potential hazards. However, this is certainly not an attempt to replace legal experts. AI is becoming the ideal sidekick, allowing legal teams to put less effort into the details, and freeing them up to concentrate on what really counts – providing outstanding value, developing winning strategies, and assisting clients with unmatched accuracy and insight as they navigate the maze of intricate transactions.

Historically, M&A lawyers often found themselves balancing strategic thinking with time-consuming, process-driven work. Technology is changing that dynamic. By streamlining contract drafting and editing, accelerating document review, and centralising communication and transaction management, legal technology unlocks crucial lawyer time. This enables lawyers to focus on strategic considerations and value-adding activities like deal negotiation and structuring, opportunity identification, risk identification and mitigation, proactive issue resolution, and solution design.

AI and legal technology tools amplify the abilities of exceptional lawyers to achieve excellent client outcomes.

Consider the due diligence phase, which is a crucial information-gathering exercise in any deal. In the past, lawyers would spend countless hours manually reviewing contracts, financial statements, and other critical documents. Now, AI-powered tools can accelerate this process, enabling faster identification of potential risks, deviations, red flags, or missing information. AI may even surface potential deal synergies or hidden liabilities that might otherwise be missed. This frees legal teams to focus on analysing the discovered findings, rather than the raw data itself.

Beyond due diligence, secure collaboration portals streamline the M&A process. These portals enable lawyers to communicate and engage with clients and the other side for due diligence and contract negotiations, all from a central place. This secure exchange of documents and real-time communication enhances efficiency and transparency.

Smart drafting tools move beyond static templates, offering dynamic clause libraries that capture a firm’s accumulated knowledge and best practices. AI-powered drafting assistance enables lawyers to review and edit their drafts faster. Some tools can also analyse contracts to ensure consistency with the negotiated deal terms or playbooks, reducing risk and streamlining the overall process. By streamlining foundational work, lawyers can focus their deep experience and human judgment on the high-priority, complex and nuanced issues of greatest concern to their clients.

Centralised transaction management platforms serve as the mission control for deals, facilitating faster closings. Transaction dashboards offer at-a-glance views of deal progress, highlighting milestones and proactively surfacing potential bottlenecks. Dynamic closing checklists prevent critical steps from being overlooked, and integrated eSignature capabilities expedite the signing process. By keeping tasks organised and streamlined, lawyers regain precious time for strategic planning and decision-making. Beyond efficient execution, this focus on data transparency and workflow management can offer valuable post-deal analysis, aiding firms to refine future M&A processes.

The rise of technology in M&A is accelerating. Innovative legal technology not only enhances efficiency and accuracy, but also allows lawyers to offer more personalised and nuanced advice. By automating, analysing and collaborating more effectively, legal teams can leverage powerful tools to provide clients with the tailored, insightful and strategic guidance they expect in the dynamic and complex world of M&A. Those unwilling to adapt may find themselves outpaced, unable to compete with the enhanced value that technology enables.

Safiyya Patel is a Partner and Aalia Manie Head of Webber Wentzel Fusion | Webber Wentzel.

This article first appeared in DealMakers, SA’s quarterly M&A publication.

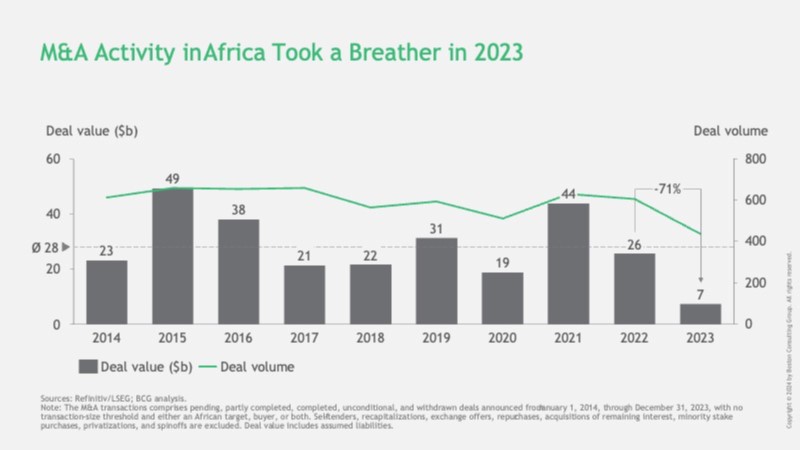

After a post COVID-19 lull, mergers and acquisitions (M&A) activity on the African continent is set for an exciting new phase, as investors see opportunities to deploy capital.

According to our research over the last 10 years, deal activity in Africa has averaged around US$28 billion in value, and there have been approximately 600 deals per year. Apart from bumper years, activity in most years fluctuated around these averages. In 2021, for example, the continent saw significant transactions by BP and Eni, which pushed the deal value up. Another exception was in 2023, when we saw only $7 billion in deal value across 440 deals – a 71% drop in deal value compared to 2022.

When looking at the geographic locations of these transactions, we observe that most deals target South African companies. But other economies like Morocco, Egypt, Nigeria and Kenya are catching up, and becoming increasingly attractive for acquirers.

We believe that there are several catalysts that may align to reverse the trend of below-average activity in recent years, and push M&A activity on the African continent to new heights.

Firstly, a look at global trends in M&A suggests that companies have strengthened their balance sheets, have excess cash on hand to invest, and are forecasting a more stable interest rate environment. While this should be seen in the context of increased geo-political uncertainty, companies may also utilise this period to look at cross-industry transactions to help them meet their digitisation and sustainability-linked goals.

The second trend is that there remains robust demand for African assets, with roughly half of the 2023 deal value being inbound activity – these are classified as non-African acquirers buying African assets. In 2023, we saw the second-highest share in the last 10 years with 57% of deal value from such deals. One connected trend is the increasing presence of Chinese buyers on the continent. Their share in deal value increased from 2% in 2014 to 7% in 2023, with a tendency to be involved in larger deals.

Sector-wise, we saw most of the transactions take place in the materials and energy and power industries, with 27% and 25% respectively in 2023. This is a shift compared to 2014, where these two sectors combined accounted for only about a quarter of aggregate African deal value.

This trend is expected to continue into 2024. Transactions in the energy and power clusters will be fuelled by major international oil companies optimising their portfolios through divestments of non-core assets, particularly in Africa. These companies, acting as the main sellers, are shifting away from non-strategic assets, driving interest not only in fossil fuels, but also in renewable energy sources and infrastructure development.

As African economies aim for energy diversification and independence, the focus on renewable resources and sustainability is increasing, indicating a move towards more self-sufficient and environmentally friendly energy production.

On the materials front, the rise of the green economy and the so-called “metals of the future” cluster – cobalt, manganese, copper and lithium – are expected to attract investor attention, especially in Africa.

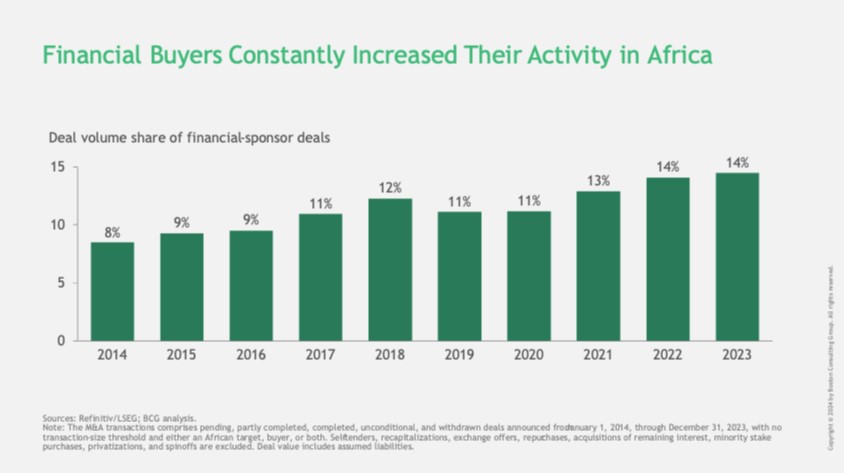

A third trend which is expected to contribute to higher M&A activity in Africa is the increasing activity of financial buyers – classic private equity investors, or a slightly newer class of financial sponsors in the form of Sovereign Wealth Funds (SWFs). With African markets maturing, these buyers have almost doubled their share of total deal-making from 8% in 2014 to 14% in 2023. One of the drivers of these transactions is the increased participation of Middle Eastern SWFs, looking to diversify their investments outside their home markets. An example is the Eastern Co, a tobacco company based in Egypt, which was acquired by UAE’s Global Investments for approximately US$625 million.

The fourth trend on the African continent is more structural, where increased optimism around deal-making is supported by game-changing initiatives like the African Continental Free Trade Area (AfCFTA), which is expected to enhance intra-African trade and M&A activity.

Should the increased M&A activity materialise through these trends, we believe that there are several opportunities for businesses to benefit. However, it’s not guaranteed that the companies which participate in deal-making create value from it. To do so, companies must follow a clear set of rules, which have proven to drive success in other regions already. Our research has shown that the following factors, among others, are pivotal for success:

• Be prepared and systematic: Have the right team, tools and processes in place to act on M&A opportunities. • Acknowledge the risk: Doing M&A in lesser-developed economies comes with an additional risk to the already challenging odds of creating value from transactions. • Build experience: Experience matters in M&A, as our research has shown. • Master the art of timing: In M&A, as in many other areas of business, timing is half the battle. • Double down on integration design and execution: The importance of execution for successful deal outcomes cannot be overstated.

Rich in mineral resources, with a youthful population and maturing financial markets, and strategically positioned between key trade routes, the African continent represents an exciting frontier market for investors. We anticipate that these trends will contribute toward a healthy M&A environment.

Historically, acquirers in Africa have created slightly more value from their deals, compared with the global average; however, the odds of creating value are, at the same time, lower. Companies that keep an eye on the trends shaping the M&A market in Africa and prepare for successful deal-making are sure to be presented with an historic opportunity.

Jens Kengelbach is Managing Director and Senior Partner; Global Head of M&A | Boston Consulting Group

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

e>

Earnings take a dive at Motus (JSE: MTH)

Consumer pressures are hurting themat this point in the cycle

If there’s one thing my current trip to London has highlighted, it’s just how poor South Africans have become in the global context. I don’t think I’ve seen a single Chinese car on the road here. Meanwhile, back home, they are selling much better than European brands at the moment. I don’t think it’s a trend that is going to improve.

When you sell cars, like Motus does, you need consumers with disposable income. The South African market is a tough place for Motus right now, which is why the group is also looking to the likes of the UK and Australia for growth opportunities. There’s no getting away from the importance of the South African market, though.

There’s a smack back down to earth for the numbers in the latest period. There was always going to be a cyclical downturn at some point for this group and it happened in the year ended June 2024, with a trading statement revealing a drop in HEPS of between 25% and 35%.

The good news is that the oversupply of vehicles is moderating. The reduction in stock levels is coming at the cost of discounts to consumers and thus lower gross margins, but it has taken pressure off the balance sheet and has reduced net debt in the process.

Results are due to be published on 3 September.

In a separate announcement, Motus noted that Brenda Baijnath has been appointed as CFO designate. She joins from September and takes the full CFO role from November.

MultiChoice’s financial performance has tanked (JSE: MCG)

The timing of the Canal+ deal is fortuitous to say the least

The content delivery game is no joke. With streaming growing in popularity by the minute, there’s a real push among the smaller players to consolidate their offerings to take the fight to the likes of Netflix. I am a big fan of the Canal+ tie-up with MultiChoice and I think that the latest MultiChoice numbers show exactly why it is important.

Subscriber growth is in trouble. Well, the growth isn’t in trouble, as that would imply that there is any growth at all. Instead, there’s a 9% decline in active subscribers at group level. Rest of Africa fell by a nasty 13% as consumers had to prioritise other expenses over their content subscriptions. South Africa was down 5%. In both cases, that’s worrying.

Showmax is growing really well after its relaunch but that’s still a relatively small component of the group. You also need to keep in mind the early-stage losses in streaming, as it takes a long time for these businesses to be profitable. Along with several other contributing factors, the level of investment in Showmax has had a significant negative impact on trading profit, which fell by 21%.

Core adjusted HEPS was down 38%. Free cash flow was down a whopping 79%. And on top of all this, there’s now a negative net asset value because of non-cash charges and accounting adjustments.

If I held MultiChoice shares, it would take me about 2 nanoseconds to say yes to the Canal+ offer.

PPC swung into profits for the year ended March (JSE: PPC)

There’s a big change to the prior period figures to exclude CIMERWA

PPC has released a trading statement for the year ended March 2024. It reflects a massive move from losses to profits, with the prior period having been restated to recognise CIMERWA (the business in Rwanda) as a discontinued operation.

This means that the focus is on continuing HEPS, which reflects the positive impact of the performance in Zimbabwe in this period vs. the prior period which was impacted by the kiln shutdown. This period was also positively impacted by the functional currency of PPC Zimbabwe being changed to the US dollar.

HEPS from continuing operations will be between 16.5 cents and 20.0 cents vs. a loss of 20 cents in the comparable period.

The only silver lining at Spar is that they may have sold Poland (JSE: SPP)

But no final deal has been announced yet

Spar closed more than 11% up after the release of results. I think it had less to do with the numbers and more to do with the announcement that there’s a deal to dispose of Spar Poland that seems to be far down the line. There’s a binding offer and they have aligned on key terms. Spar hasn’t named the buyer or disclosed any of those terms, but that didn’t stop the market from getting excited.

I can’t think that the results for the six months to March 2024 were much of the excitement, with turnover up 7.9% but HEPS down 7.6%. Operating profit was only 0.2% higher. The significant difference between operating profit and HEPS can largely be explained by higher finance costs.

Growth in turnover in South Africa was 4.8%. Volumes were down in grocery, with growth of 4.0% vs. price inflation of 7.0%. TOPS did well in this period, with wholesale turnover up 12.8%. Build it reported a flat sales performance as the construction industry continued to go nowhere slowly. Conversely, the pharmacy business (S Buys Pharmacy) achieved 15% turnover growth.

The South African business continues to struggle with the disastrous SAP implementation at the KZN distribution centre. It’s so bad that they have spent a fortune to put in a system that leads to warehouse inefficiencies and less visibility for buyers, with margin then impacted. There’s a very open-ended comment in the announcement that “the decision has also been made to implement a more cost-effective warehouse management system that is better suited for our business.” It seems as though they are only partially moving away from SAP rather than laughing it off, but what a mess either way.

BWG Group in Ireland and South West England achieved turnover growth of 5.7% in local currency, which translated into 16% growth in rands. Spar Switzerland saw turnover drop 4.6% in local currency. It was up 8.7% in rands as our currency weakness gave Spar a helping hand. In both overseas businesses, the challenge is that consumers are struggling to afford what they need and are in search of discounts rather than convenience.

Spar is not intending to seek additional funding from shareholders and still has the support of lenders to execute a proper optimisation of the balance sheet. Unsurprisingly, there’s still no dividend.

In terms of outlook, South Africa is expected to remain challenging. Spar hopes for a better performance in the offshore businesses over the summer period, which does make sense. What would certainly help them is interest rate decreases that give consumers some relief.

The CFO of Spar is retiring after 29 years with the group. A replacement hasn’t been named as of yet.

There’s strong positive momentum at Telkom (JSE: TKG)

I still laugh at the description of “next generation” revenue

Telkom’s performance in the year ended March 2024 was a vast improvement on the prior year. Normalised HEPS (the best measure to look at) increased by between 195% and 205%! This measure excludes the substantial once-off restructuring costs in the prior year. It also reflects the restated HEPS for the prior period after they found a mistake in how they did the tax.

I can’t help but chuckle when Telkom talks about “next-generation revenues” – next generation in comparison to an old home phone, maybe. This isn’t exactly the cutting edge of AI technology. Either way, the “next-generation revenues” now comprise 80% of group revenue, having grown 7% in this period.

Although reported EBITDA for the group grew 18%, normalised EBITDA was only up by 5%. Depreciation and write-offs were lower this year, but net finance costs were higher and there were negative forex and fair value movements. Still, the net impact was a major jump in HEPS.

Detailed results are due for release on 18 June.

Vunani suffers a significant drop in earnings (JSE: VUN)

Detailed results are due to be released later this week

Vunani has released a trading statement for the year ended February. HEPS is expected to fall by between 63% and 83%, which is a substantial negative movement.

They expect to release full results on 14 June i.e. at the end of this week. It will be important to properly unpack where the HEPS pressure has come from.

Little Bites:

Director dealings:

Many associates within the Mouton family have bought shares in Curro (JSE: COH) with a total value of R18.5 million.

Des de Beer has bought another R765k worth of shares in Lighthouse Properties (JSE: LTE).

A director of AVI (JSE: AVI) bought shares in the market worth R494k.

A prescribed officer of Old Mutual (JSE: OMU) has bought shares worth nearly R200k.

An associate of the controlling shareholder of Workforce Holdings (JSE: WKF) has bought shares worth R150k.

Cilo Cybin (JSE: CCC) is a name you might have seen before. At one stage, they were sniffing around a potential listing. That day has finally come, with the structure being that of a SPAC – Special Purpose Acquisition Company. This isn’t an IPO, but rather a listing of a structure that meets the requirements for minimum shareholder spread and level of investment. A major Malaysian investor has come on board. If you would like to read the pre-listing statement, you’ll find it here.

GCR Ratings as reaffirmed Curro’s (JSE: COH) credit rating with a stable outlook. Although equity holders should always be careful about putting too much focus on credit ratings, it does always help to see it either stable or improving.

Kibo Energy (JSE: KBO) is becoming a comedy show. Despite announcing a plan for an extensive corporate restructuring and change of management, there’s now another announcement reversing that entire thing. The latest idea is to transition Kibo into a broader energy company, including potential interests in oil and gas. Someone wake me up when they aren’t at R0.01 per share and writing long SENS announcements about exciting plans.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

e>

Accelerate has concluded the rights offer (JSE: APF)

And they had to find a new buyer for Cherry Lane

Accelerate Property Fund successfully raised R200 million in equity in its rights offer. This isn’t a shock, as the offer was underwritten. The more interesting update is the extent to which the underwriter had to get involved i.e. the level of support received from other shareholders.

In the end, the underwriter took up R54 million worth of shares. We can only hope that this will be the last time that Accelerate taps the market at this deeply discounted share price.

And in other news, the sale of Cherry Lane to Cadastral Assets fell through. They have a new deal on the table already though, with an entity belonging to Herman Zolty (not a related party) stepping in to buy the centre. The price is R57 million vs. the indicative market valuation of R60 million, so the buyer has put in a slightly cheeky bid but nothing crazy. Cadastral was going to pay R60 million, so the bigger irritation for shareholders is that the deal has taken longer than expected and is for R3 million less.

A due diligence still needs to be done by the buyer on the property, so this transaction isn’t guaranteed either.

Delta Property Fund to sell the Lexis Nexis building (JSE: DLT)

This is part of the broader asset disposal strategy to sort out the balance sheet

Delta Property Fund has agreed to sell the Lexis Nexis building in KZN for R37.375 million. The purchaser is Icebolethu Funerals Proprietary Limited, which isn’t a related party.

The net proceeds are R32.5 million and Delta will use them to reduce debt. The loan-to-value ratio will dip slightly by 20 basis points to 60.7%. This is like digging a big hole with a spoon, but they simply have to make progress wherever they can.

The buyer needs to deliver funding guarantees within 45 days of signature date. These deals are never done until the money is in the bank. Getting the guarantees in place is a good step towards that.

Heriot to take Thibault REIT private (JSE: HET)

The Cape Town Stock Exchange is very light on listings and now one is about to disappear

Heriot has announced that it will acquire 100% of the shares in Thibault REIT, which is listed on the Cape Town Stock Exchange, in return for the issuance of shares in Heriot. Thibault was established by the founder of Heriot, so there was always a chance of this happening.

Thibault owns various properties as well as a 10.02% interest in Safari REIT and a 19.33% interest in Texton REIT. The extent to which listed funds hold stakes in other funds on the JSE never ceases to amaze me.

The deal value is roughly R1.1 billion, which is similar to Thibault’s net asset value. This is a small related party transaction which means that an independent expert needed to opine on the deal. Given the pricing in relation to the net asset value, it’s not a surprise that it was signed off as fair.

Thibault will delist from the Cape Town Stock Exchange as part of this.

Premier Group drives strong earnings growth off modest revenue growth (JSE: PMR)

This is the joy of operating leverage working with you rather than against you

For the year ended March, Premier Group delivered revenue growth of 3.6%. That certainly won’t blow your socks off, but the HEPS growth of 34.8% just might.

Revenue growth doesn’t tell you much about performance in a company. If expenses are running out of control, then great revenue growth doesn’t help. Conversely, if a group has a high proportion of fixed costs and is ready to take advantage of operating leverage, then modest revenue growth can do wonderful things. Premier is obviously in the latter bucket.

Group EBITDA was up 18.6%, with Millbake as the major contributor there. It achieved EBITDA growth of 20.6% off revenue growth of 3.7%. The Grocery and International categories don’t have much operating leverage, with revenue up 3.3% and EBITDA up 3.7%.

EBITDA margin was up 140 basis points to 11%. Operating profit margin expanded by 160 basis points to 8.8%.

And to put icing on this cake, cash generated from operations was up by 54.8%. This has driven group leverage to levels below historical averages, which gives management the confidence to undertake transactions like the acquisition of 30% of Goldkeys International in KZN, one of the largest rice importers in South Africa. The deal was settled in cash and the investment will be accounted for as an associate.

This is a very strong result overall.

Renergen is close to the all-important performance test (JSE: REN)

Either way, the share price is going to react sharply to the results of that test

After many issues with the helium plant and plenty of chatter online about whether Renergen will ever achieve what they have promised, we have finally reached the point where the company is about to undertake the critical performance test. This is where the rubber hits the road – or the bulls hit the bears! Either way, I expect to see either a significant positive or negative share price response to the results of the test.

Liquid helium production resumed on 4 June. That’s good, but the focus now is on showing that the entire plant can be operated as designed. If that goes well, then the performance test takes place – a 7-day process of much clenching of you-know-what cheeks while they put the plant through its paces.

Ahead of that test, Renergen has appointed two independent helium consultants to its team with experience in commissioning and running liquid helium plants around the world. They have indicated that no fundamental issues are likely to exist within the plant. The performance test will tell us for sure.

As someone who wants to see South Africa grow, I certainly hope that the test will go well.

Little Bites:

Director dealings:

Des de Beer is back at it, buying R2.9 million worth of shares in Lighthouse (JSE: LTE).

Trustco (JSE: TTO) is converting N$4.4 billion worth of debt from Quinton van Rooyen and Next Capital into shares. The price for the conversion is N$1.14 per share, which is the NAV as per the latest financials. This is way above the current traded price of N$0.44 but is still highly dilutive for shareholders.

Just a few months after joining EOH (JSE: EOH), CFO Marialet Greeff has now resigned with effect from the end of September to pursue other interests. When a key role like CFO is a revolving door like this, it sends a really poor message to the group.

I don’t usually focus on changes to non-executive directors, but it’s unusual to see three changes at once. This is the case at Gemfields (JSE: GML), where Bruce Cleaver, the ex-CEO of De Beers, is joining the Gemfields board as chairman. This isn’t the only new board appointment, with the ex-CFO of Lonmin Platinum (Simon Scott) also joining in an independent non-executive capacity. Assore International Holdings, which holds over 29% in Gemfields, has appointed its managing director to the board in a non-executive role as well.

Didier Oesch, the CFO of ADvTECH (JSE: ADH) ,will be stepping down as CFO and as a director at the end of April 2025. He’s been there for a long time and will make himself available for consulting requirements for a smooth handover. The group hasn’t announced a successor yet.

Quantum Foods (JSE: QFH) announced that in an accident at the Malmesbury feed mill, one individual has tragically passed away and two others were injured but are in a stable condition. The cause of the explosion is unknown at this point. In terms of damage to the property, only the raw material intake area has been damaged and operating activities outside of that area can continue.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

e>

The cash is raining down at Alexander Forbes (JSE: AFH)

Management is rewarding shareholders with fat dividends

Alexander Forbes has released results for the year ended March 2024. The last couple of years have been intense for the group, with major corporate activity to reshape the group into a more desirable financial services operation.

The acquisitions have a significant impact on the growth rates in income and expenses, as the group has effectively bought earnings. They’ve acquired six businesses in the past three years, with OUTvest and TSA Administration highlighted by the group as performing well. It’s hard to get every acquisition right, with an impairment recognised for EBS International.

Operating income increased by 12% overall (including acquisitions, while operating expenses jumped by 16%. The cost-to-income ratio has moved from 77.4% to 79.5%, which isn’t entirely unexpected in a period with corporate activity and related integration expenses. Alexander Forbes will look to reduce this over time.

The growth in expenses obviously blunted the benefit of top-line growth, with profit from operations up just 2%. Cash generated from operations was flat during the prior year.

HEPS tells a different story though, driven by an uptick in investment income. This led to HEPS from continuing operations increasing by 16% and normalised HEPS up by 31%. This would’ve driven the decision to not just increase the total annual dividend by 19% to 50 cents per share, but to add on a special dividend of 60 cents per share as well. On the current share price of R6.88 at time of writing, that’s a meaty return of cash to shareholders.

More than just Lucky Stars at Oceana (JSE: OCE)

HEPS is up dramatically in the latest period

Oceana has reported numbers for the six months to March and they look excellent. Revenue increased by 12.1% and this set the tone for the rest of the income statement, with operating profit up 57.1% and HEPS up 84.6%. The interim dividend is up by a juicy 50%.

It wasn’t just Lucky Star that did well here, although their second quarter benefitted from improved canned food sales volumes. Daybrook in the US was the star of the show, with record earnings. They had strong inventory levels coming into this period and this allowed them to take advantage of record prices for fish oil.

And of course, the weaker rand made the translation of those US-based earnings even more appealing.

Thanks to the stronger pricing in the market, gross margin from continuing operations was up 700 basis points to 34.1%. Although there were some offsetting factors like lower wild caught volumes and the impact on margins, this was clearly a great period.

The substantial jump in profits relative to revenue was achieved through overheads only increasing by 3.5% in continuing operations. This is the joy of operating leverage when it works with you, rather than against you.

The loss from joint ventures and associates of R25 million was mainly due to the Westbank Fishing operation, which was in its off-season for most of this period. That didn’t dampen the overall group earnings party.

The bigger negative in the result was the wild caught seafood business, which saw operating profit fall substantially from R108 million to R17 million. The business suffered various operational issues that plagued the results.

The finance costs line bucked the broader trend in the market and decreased by R3 million to R93 million. This also did wonders for the HEPS jump relative to the revenue increase. Net debt ended the period 16.7% lower and the net debt to EBITDA ratio improved from 1.6 times to 1.2 times.

The group is investing in future growth. Cash from operations was up 12.6%, giving the group confidence to ramp up capital expenditure by 44.9% to R297 million. R132 million of this was to upgrade the West Coast plants and the rest of the capex was replacement in nature.

And here’s an interesting one: Lucky Star is acquiring a 75% stake in a canned chicken liver business in Graaff-Reinet that supplies school feeding schemes in the Eastern Cape and Gauteng. This is interesting diversification.

Oceana will be presenting on Unlock the Stock on 13th June at midday. You can register to attend this online event for free at this link.

Omnia feels confident to pay a much higher dividend (JSE: OMN)

This is despite a decline in earnings

At first blush, it hasn’t been a good year for Omnia. Revenue fell 16% for the year ended March 2024 and operating profit was down 10%. Adjusted HEPS was roughly flat at 737 cents.

This isn’t the typical precursor to a dividend increase of 87%, yet here we are.

As you might have guessed based on that percentage increase, there’s a special dividend for this period. It comes in at 325 cents vs. the ordinary dividend of 375 cents. Management is feeling a lot more confident about the outlook, notwithstanding the recent results. I’m sure a 15% decrease in net working capital helped with the cash flow outlook.

It’s important to look at the segmental performance in a diversified group like Omnia. Starting with agriculture (excluding Zimbabwe), revenue fell by 22% and operating profit decreased by 21%. This means the operating margin increased every so slightly. South Africa had decent sales volumes, so the worst pressure was felt in Africa. They are reviewing their business models in the region in response to these challenges.

Moving on to mining, revenue fell by 3% but operating profit increased by 26%. This means that operating margin expanded significantly. They managed to grow volumes in a difficult market in South Africa, but it seems like the international operations delivered the big uptick in this segment. Markets like Canada, Indonesia and West Africa are key here.

In the chemicals segment, revenue was down 23% and operating profit collapsed by 92% to just R11 million, so this was a disastrous outcome with operating margin of just 0.5%. It sounds like just about everything went wrong in the local market, with macroeconomic conditions giving them plenty of headaches.

The fight with SARS regarding the 2014 to 2016 years of assessment is ongoing, with the Alternative Dispute Resolution (ADR) proceedings underway. Other avenues may be possible if needed, like court adjudication.

So, it was a rather odd year in which the mining division did the heavy lifting. The special dividend will be seen as a positive outlook for the group, with the share price up 11% by late afternoon trade in response.

And to help shareholders further, there’s an independent research report

The Rainbow Chicken business isn’t new to investors, as it has been part of RCL Foods throughout. This means that the market is already fairly familiar with Rainbow. Of course, with the pre-listing statement now published as part of the plan to unbundle the business to shareholders, there’s more public information than ever before on Rainbow.

With 165 farms, there are a lot of chickens at Rainbow. The group is dividend into three segments though: chicken (self-explanatory), animal feed and Matzonox (a waste-to-value operation based at the Chicken division’s Worcester and Rustenburg chicken processing sites which processes wastewater from chicken processing plants and poultry manure from chicken farms to generate electricity, heat and recycled water). Talk about vertical integration.

This excerpt from the pre-listing statement gives you a good idea of how volatile this industry can be, especially with all the craziness over the past few years of avian flu, load shedding and wild macroeconomic swings:

If you want steady profitability, the chicken business isn’t for you. If you enjoy opportunities that require a more active approach to managing the position, then this sector might appeal.

The independent research report will only be published on 11th June, the day after the pre-listing statement. In the meantime, you can read the pre-listing statement here.

Little Bites:

Director dealings:

MTN (JSE: MTN) made a pretty bad mistake in its SENS announcement last week. I must say, I was surprised to see the announcement of a director of a major subsidiary buying over R4 million worth of shares. That surprise was warranted in the end, as he actually sold the shares rather than purchased them.

Finbond (JSE: FGL) announced that Protea Asset Management, managed by director Sean Riskowitz, bought shares worth R1.7 million.

Two directors of OUTsurance (JSE: OUT) have acquired shares worth a total of R1.09 million.

The CEO of Capital Appreciation (JSE: CTA) has purchased R900k worth of shares on the market. This is a positive signal after the recent release of excellent numbers.

A director of Hyprop (JSE: HYP) bought shares worth R374k.

Exemplar REITail (JSE: EXP) announced the acquisition of Eerste Rivier Mall in Stellenbosch, marking its first steps into the Western Cape. The purchase price is R282 million.

Primeserv (JSE: PMV) released a trading statement for the year ended March 2024. There’s a juicy jump in HEPS of between 31% and 41%, coming in at between 30.70 cents and 33.10 cents. On a share price of R1.39 at time of writing, this low single digit Price/Earnings multiple is typical of what we see on small caps.

There has been decent uptake of the Equites Property Fund (JSE: EQU) dividend reinvestment alternative, with holders of 65.91% of shares in issue electing to reinvest their dividends in the shares at R12 per share. This helps with retaining equity on the balance sheet and many property funds take this approach.

Labat Africa (JSE: LAB) is currently suspended from trading and in the process of appointing new auditors. The business continues regardless. It takes on new meaning when they say that the “group is continuing to grow” as Labat is focused on medical cannabis. Retail division CannAfrica has opened more than 20 franchises in the past year.

Visual International (JSE: VIS) announced that the proposed related party acquisition of a 20% stake in Tuin Huis has been cancelled due to weak performance in the residential property sector in the past year. The acquisition of the Stellandale Gardens land has also been pushed out until after February 2025 to allow the company to focus on Stellandale Junction.

Powerfleet (JSE: PWR) is certainly playing the listed game, announcing that the company will be joining the small-cap Russell 2000 Index with effect from 1 July when the index is reconstituted. Being included in an index is helpful not just for visibility, but for ETFs and unit trusts who have a specific mandate related to that index. This does good things for liquidity in the stock. The much more exotic part of the announcement is Powerfleet calling itself an “artificial intelligence of things (AIoT) software-as-a-service (SaaS) provider” – a wonderful example of buzzword bingo. To drive that message home, the stock ticker for the Nasdaq listing will change to AIOT. It doesn’t look like the JSE listing ticker will change.

Oasis Crescent Property Fund (JSE: OAO) is unusual for a few reasons, not least of all the lack of debt in the fund to meet Shari’ah requirements. One of the other nuances is that the default for the recent distribution was for shareholders to reinvest the distribution in the fund. Investors have to specifically elect to receive cash. Unitholders of 95.5% of units in the fund elected to receive cash, so maybe they should give the default a rethink.

Efora Energy (JSE: EEL), which is suspended from trading, is in the process of catching up on its financial reporting. We know this because the company released a trading statement for the six months to August 2023. I have no idea why suspended companies need to release trading statements, as you can’t trade in the stock anyway and an early warning of major movements isn’t necessary. They should just release results once finalised.

If you hold preference shares in Ibex Investment Holdings (JSE: IBX), then check out the finalisation announcement related to the scheme to repurchase the shares. Their listing will be terminated on 25 June.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In just a few minutes, you can get the latest news and my views on Capital Appreciation, MultiChoice, Spar and The Foschini Group. Use the podcast player above to listen to the podcast.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")