The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In just a few minutes, you can get the latest news and my views on Balwin, Quantum Foods, De Beers, Tiger Brands and Bidcorp. Use the podcast player above to listen to the show.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

At Alphamin, Mpama South is working as planned (JSE: APH)

Production to sales specification has been underway for two weeks now

Alphamin announced that Mpama South has been producing tin concentrate to sales specification since 14 May, so that means two weeks with no hiccups. Even more importantly, the tin grade of the feed ore was increased from 17 May, with the focus on consistent throughput and producing in line with the targeted recoveries for the processing plant.

The good news for shareholders is that the facility is doing what it is supposed to do: operating at targeted levels of processing recoveries and is producing high grade concentrate to sales specification.

Barloworld signs off on a tough period and renews the cautionary announcement (JSE: BAW)

A group with cyclical exposures can’t always go up

Barloworld has released results for the six months to March 2024. Although revenue fell by 7.7%, the highlight is that EBITDA margin was steady at 12.9%. It’s unusual to see margins stay consistent when revenue has fallen.

The consistency goes all the way down to HEPS which also fell by 8% for the period. This is despite finance costs moving 13.4% higher for the period. One of the key offsetting benefits was a much lower effective tax rate after restructuring the domicile of the equipment businesses. The share of profit from associates and joint ventures came in 22.4% higher and this also boosted HEPS.

You might assume that the same is true for the dividend, but the surprising outcome is that the interim dividend is 5% higher at 210 cents per share. This tells you that the balance sheet is in good shape, with net debt to EBITDA at 0.6x (giving plenty of headroom vs. covenants of 3x).

Return on invested capital (ROIC) was in line with the prior period at 14.3%.

As you might guess, the consistency in group level results isn’t because the underlying divisions were all in line with the prior year. In a diversified group like this, there will be good years and bad years at divisional level, with the hope being that the group result is smoother over time than the underlying divisional numbers. In this period, Barloworld Mongolia was the standout performance with a 43% revenue increase, whereas VT in Russia reported a drop of 24%. Between those extremes, we find Equipment Southern Africa with a drop of 10% and Ingrain with a decrease of 3%.

EBITDA movements at divisional level were more volatile than what we saw at revenue level, which is to be expected when a business has fixed costs. Equipment Mongolia led the way with an EBITDA jump of 78.8% and EBITDA margin of 24.7%. Disappointingly, Ingrain put in the worst EBITDA performance despite the modest dip in revenue, with EBITDA down 19.6% as margin contracted from 14.1% to 11.7%. Equipment Southern Africa saw EBITDA decrease by 8.5% and VT was down 16.1%.

For further context, Equipment Southern Africa is the largest EBITDA contributor at R1.4 billion. Barloworld Mongolia is next up at R479 million, followed by VT at R417 million and Ingrain at R372 million.

In a separate announcement, Barloworld renewed the cautionary announcement that was first issued on 15 April. They haven’t indicated what the potential opportunity on the table is. We don’t even know if they are looking to acquire or dispose of something in these discussions.

Collins Property isn’t shy of debt (JSE: CPP)

You won’t often see a target loan-to-value this high– but what’s the catch?

Collins Property Group is officially a REIT and they aren’t wasting any time in getting those dividends out the door, with a dividend for the year of 90 cents based on distributable income per share of 94 cents.

Of course, REITs are supposed to have very high payout ratios. That’s kind of the whole point of being a REIT. It’s easier said than done though, with many of them tripping up when debt is high.

There are no such issues at Collins it seems, despite a very high loan-to-value ratio of 54.3%. The target range is 45% to 55%. Total debt on the balance sheet comes in at R6.3 billion, with various banks lending to the group.

With bank covenants for a 55% loan-to-value as the maximum, Collins is sailing close to the wind and feeling just fine about it. Generally speaking, companies in the Wiese stable aren’t shy of taking a financial risk or two.

Note: an earlier version of this article noted a large outstanding balance of preference shares held by Christo Wiese’s Titan entity. I misread R1.3 million as R1.3 billion. My apologies for this. The loan-to-value ratio information was correct in the original article.

Datatec reports a massive jump in earnings (JSE: DTC)

This is what happens when a low margin EBITDA business goes the right way

In Datatec’s results for the year ended February 2024, you’ll find a 6.1% increase in revenue. That may not sound like much, until you see the 15.8% increase in gross profit and excellent 80.7% jump in EBITDA. The EBITDA increased from 1.9% to 3.3% and there’s an important lesson here about earnings volatility in low margin businesses. It takes just a small change further up the income statement (like a shift in gross margin) to drive big moves in EBITDA.

If you can believe it, the gross margin was 15.8% and the increase in gross profit was also 15.8%. At first I thought it was a typo in the SENS announcement!

The company announces various measures of earnings per share, not least of all because of Analysys Mason as a discontinued operation in the comparable year. The best measure is probably continuing underlying earnings per share, as this has the minimal level of distortion. Even then, it increased by 231.1% to 20.2 US cents!

The dividend was lower this year though, coming in at 130 cents vs. 195 cents in the prior period (a 33.3% drop).

Looking deeper, Westcon International is the largest contributor with EBITDA of $121 million, up by 150% thanks to significant improvement in gross margin. Logicalis International saw its EBITDA increase by 31.7% to $66.5 million, once again thanks to improved gross margin. Logicalis Latin America wasn’t so fortunate, with gross margin increasing but not enough to offset foreign exchange losses in Argentina that led to a drop in EBITDA from $21.2 million to $11.5 million.

In terms of prospects, the company highlights the opportunity of AI driving a new cycle of computing hardware investment. I’m hearing this more and more in the market and it certainly makes sense to me.

At Exemplar, the bankers are smiling more than shareholders (JSE: EXP)

Despite strong growth in net operating income, the distribution per share has dipped

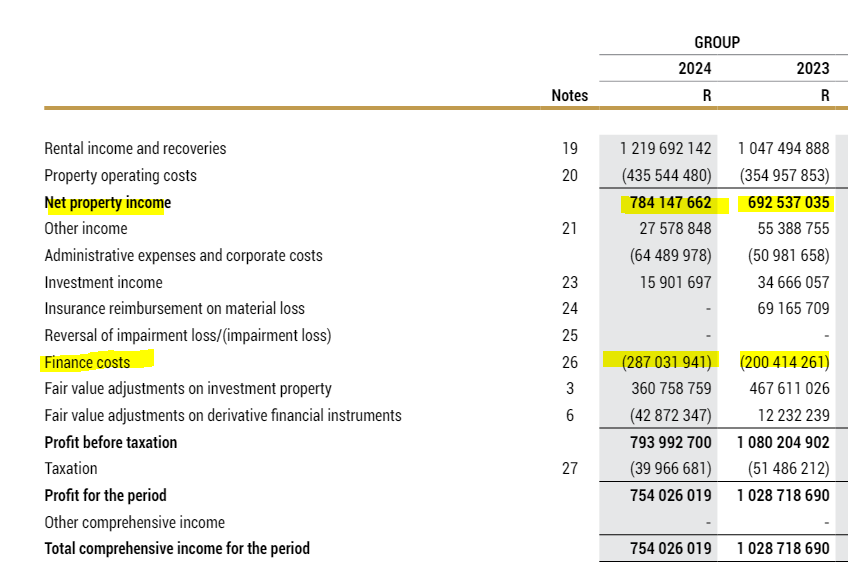

Exemplar’s portfolio is rather unusual in the modern South African context, in that it has absolutely no exposure to the Western Cape. The fund has 26 retail assets across five provinces with a particular focus on malls that service township areas. 86% of tenants are national and international tenants, or those with rental guarantees, featuring many large retailers who want to service lower income consumers who represent a high growth opportunity. If you’re building out a property portfolio, this is a good example of how you can diversify vs. many funds that are focused on properties in premium urban areas.

Despite a 16.4% increase in rental and recovery income, as well as a 13.2% increase in net property income, the total distribution per share for the year ended February 2024 fell by 1.5%.

The culprit? You guessed it: finance costs. They increased from R200 million to R287 million, completely offsetting the increase in net property income. This is what it looks like when you’re working hard so your bankers can have a better life:

Mantengu Mining is profitable (JSE: MTU)

The share price closed 32% higher on strong volumes (for a small cap)

Mantengu Mining released results for the year ended February 2024. This is the first year-end in production for the group, so the year-on-year movements look a bit silly (e.g. revenue up from R4.5 million to R109.9 million).

It’s probably better to just look at the results in isolation as opposed to comparing them to the prior year. Gross profit came in at R52.6 million and operating profit was R24.9 million. HEPS came in at R0.01 per share – positive by the smallest of margins. Even then, these results don’t tell much of the story, as there were only two months of steady state production at Langpan.

Aside from the a full production period at Langpan for FY25, the future looks interesting with the recent acquisition of 100% of Birca Copper and Metals that approximately doubles the existing chrome ore supply at Mantengu.

Be careful of the wide bid-offer spread in this stock, with the best bid currently at R1.07 and the best offer at R1.57. The share price closed 32% higher at R1.03 on strong volumes of roughly 8x the average trading volume.

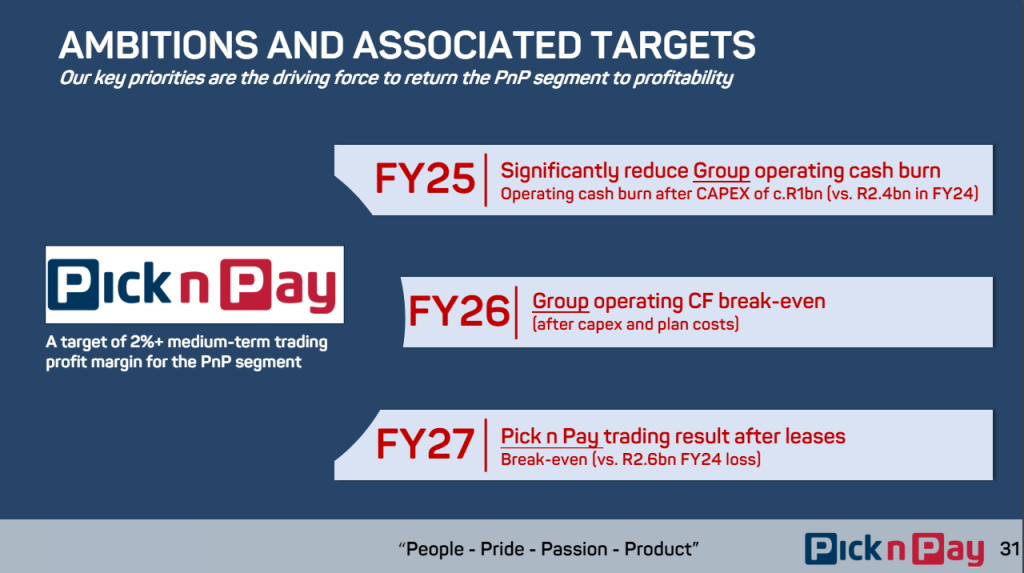

The Ackermans get out the way at Pick n Pay (JSE: PIK)

The financials are in disarray and the turnaround will be extremely tough

Pick n Pay has released results for the 52 weeks to 25 February. They reflect revenue growth of 5.4%, which is pretty poor, along with a particularly revolting decline in gross profit margin from 19.6% to 18.1%.

Trading profit collapsed from just over R3 billion to only R385 million, with a paltry trading profit margin of 0.3%. It only gets worse from there of course, with a loss after tax of nearly R3.2 billion. A vast increase in finance costs to just over R700 million was a major contributor here, along with impairments of R2.8 billion. The impairments are a non-cash item. The same cannot be said for the finance costs.

Unsurprisingly, there’s no dividend. This is what happens when the headline loss per share is -254.72 cents.

Net debt ballooned to R6.1 billion at the end of February vs. R3.7 billion the year before. What’s that old story about gradually and then suddenly?

Silver linings? Well, Boxer grew revenue 17.3% and they will need to get the market to pay a decent price for those shares when Boxer is set free from this mess, so that’s good news. Pick n Pay Clothing standlone stores were up 17%, a strong result that might bring some hope to the broken grocery business.

The SENS announcement claims that experienced leadership has re-energised the supermarkets business. I can hand on heart say that my last visit to a Pick n Pay was many things, but energetic wasn’t one of them. I’ve heard that some stores look much better, but it’s the inconsistency in the footprint that makes Pick n Pay so hard to believe in. Although like-for-like sales growth for the first 12 weeks of the year is up vs. FY24, that’s hardly saying much. They are in a different postal code to Shoprite these days in terms of in-store execution. Just ask your friends where they shop.

Part of the turnaround is to either close 100 loss-making supermarkets or convert them to Pick n Pay franchise or Boxer stores. I somehow doubt that franchisees will be queuing around the block for these.

Pick n Pay has a huge mountain to climb here and they will probably only have one shot at raising the equity capital required to get it right. People have a limit to how willing they are to throw good money after bad.

The big news at the top is that Gareth Ackerman is stepping down as chairman, getting out of the way after being there for a period of time during which Pick n Pay’s core supermarkets business was left for dead by Shoprite. In even bigger news, the Ackerman Family has agreed to let go of majority shareholder voting control. The SENS announcement puts a positive spin on this, calling it a vote of confidence in the current management team. Somehow, I suspect the boardroom discussions weren’t quite that simple.

Ackerman Investment Holdings will follow its rights in the recapitalisation up to a maximum of R1.025 billion. The offer is R4 billion in equity, with three banks (Absa, RMB and Standard Bank) coming in as underwriters in equal proportions. I can’t help but wonder just how exposed those banks are to Pick n Pay. At this point at least, perhaps it hurts less to underwrite the equity raise than to face facts around the debt.

Speaking of the debt, the R4 billion in equity will primarily be used to repay group debt. If they don’t achieve a proper turnaround quickly, the debt hole will be back before you know it.

Remember when property funds invested in Edcon to try and save a sinking ship? The jury is still out on Pick n Pay, but you would be incredibly naïve to think that Shoprite won’t try and deliver the death blow here. Pick n Pay better pray night and day that load shedding doesn’t come back after elections, as I think an environment devoid of load shedding is the best chance they have to emerge in a sustainable (albeit smaller) form.

Just take a look at how difficult this will be, based on this slide from the strategic turnaround presentation:

RH Bophelo grew its NAV by 19% this year (JSE: RHB)

They have moved through the R1 billion NAV mark

RH Bophelo is an investment holding company in the healthcare sector. The group now boasts a net asset value (NAV) of over R1 billion after growing NAV by 19%. NAV per share is now R15.99 and the share price is only R2.25, so the market clearly has a very different view on what the NAV is.

They do make some rather odd investments, like 29% in Ambit Health (a pathology company) for just over R1 million. How does this move the dial on a R1 billion NAV? Or even influence the dial?

If you can believe it, that was the biggest of three new investments in this period. Like I said, odd. The market doesn’t reward investment holding companies with vast portfolios of small investments. If they want to close the gap between the share price and NAV per share, this isn’t the way to do it.

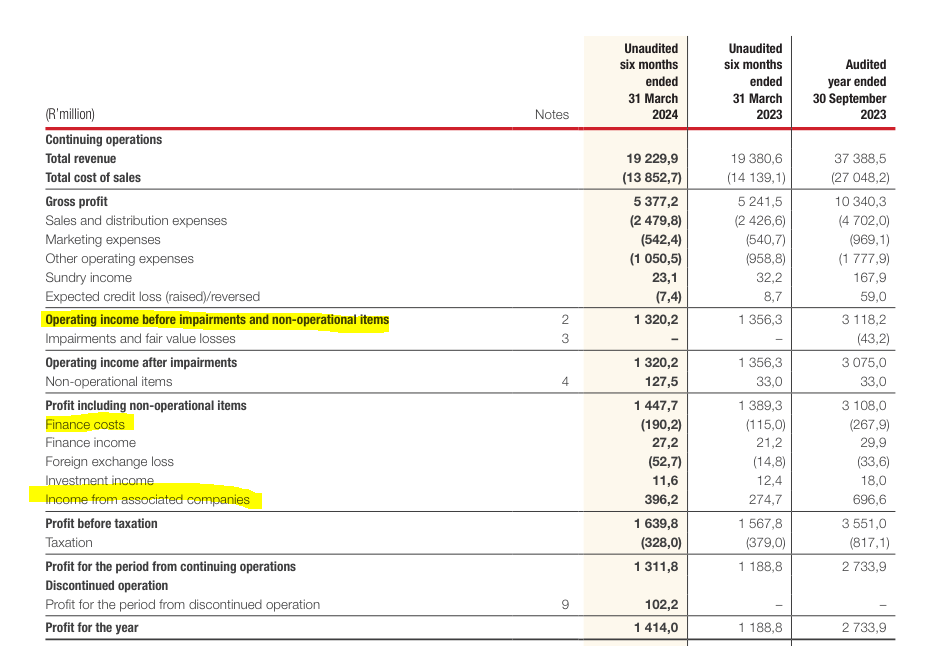

The road ahead won’t be easy at Tiger Brands (JSE: TBS)

Income from associates saved the growth as core operations went sideways

Tiger Brands is under new management, with a new CEO and CFO in place as well as managing directors for the six business units in the group. The new brooms need to sweep clean, as Tiger Brands is currently trading at levels that we also saw in 2011. There have been some encouraging rallies in the past year, but the price just can’t seem to sustainably break higher:

The results for the six months to March 2024 show why this might be the case, with revenue decreasing by 1%. Volumes fell by 9% and price inflation came in at 8%, with the loss in volumes being a deliberate strategy in some cases to improve pricing.

Group operating income fell by 3%, so the top half of the income statement clearly isn’t telling a positive story.

Finance costs also moved significantly higher, so the numbers at headline earnings level would’ve been pretty rough were it not for income from associated companies (Carozzi and National Foods in particular) that shot up from R274 million to R396 million.

I’ve included a screenshot of the income statement below to show you the shape of the financials and how it was the associates that came in right at the bottom to save the trajectory of profit before tax:

HEPS may have been up by 11% thanks to the associates, but not a cent in dividends was received from them in this interim period. In the context of such difficulties in the core businesses, as well as the levels of debt and associated finance costs, I therefore found it surprising that the interim dividend increased 9% to 350 cents per share.

Little Bites:

Director dealings:

A director of a major subsidiary of RFG (JSE: RFG) sold shares worth R248k and an associate of a director of the same major subsidiary sold shares worth just over R3 million.

The CEO of Quantum Foods (JSE: QFH) was willing to increase the price for a share purchase to R10.00 per share, with the value of the purchase being R354k.

Associates of the CEO and CFO of Spear REIT (JSE: SEA) bought shares in the company with a total value of R234k.

Not quite the standard type of update in this section, but a few non-executive directors of Orion Minerals (JSE: ORN) have elected to receive a portion of accrued director fees in shares in lieu of cash. This helps to preserve the company’s cash reserves.

MTN Uganda is one of the better African subsidiaries in the MTN (JSE: MTN) stable. MTN is taking advantage of the recent positive momentum by selling down a portion of the stake while the going is good. A substantial 7.03% stake in the company is being made available for sale to retail and professional investors, thereby broadening local ownership and unlocking value on the MTN balance sheet.

AYO Technology (JSE: AYO) released an updated circular dealing with the specific repurchase from the PIC. The independent expert has valued AYO’s shares at between R4.94 and R5.04. The repurchase is at R36 per share, so that’s clearly unfair to all other shareholders. The post-transaction fair value range is R3.30 to R3.40. The funny thing is that the current share price is R0.50, which is actually way below that fair value range. If you’re curious to read more, the circular is here.

Gemfields (JSE: GML) confirmed that the currency conversion rate for the final dividend for the 2024 financial year equates to a dividend of R0.1574624 per share, payable on 24th June.

Equites Property Fund (JSE: EQU) announced the dividend reinvestment price as being R12 per share, which is a 1.34% discount to the spot price per share on Friday 24th May, adjusted for the pending dividend. That’s not much of a discount to encourage investors to reinvest their dividends in the company.

In the incredibly unlikely event that you are a shareholder in Cafca Limited (JSE: CAC), you should note that the company has released results for the six months to March 2024. They are in Zimbabwean Dollars, so prepare yourself for some truly gigantic numbers. I also couldn’t get their website to work, unfortunately.

Every so often, I come across a story that I think would work well for this audience, only to find that it is actually just too light to justify a full article. Never one to deny you informative (and interesting) content, I’ve decided to alternate my usual long writing format with the occasional collection of short stories, tied together by a central thread but otherwise distinct from each other.

In v.01 of my Short Stories, I’m sharing five tales of AI to educate, captivate and horrify. Read them at your own peril.

The new world is (still) being built on African shoulders

When you picture the people who built ChatGPT, you probably envision a slick office in Silicon Valley, staffed with bespectacled tech virtuosos who spend their days and nights writing endless lines of code. The last thing that crosses your mind when you’re creating this image (I’m guessing) would be a building full of underpaid Kenyan data labellers.

For all its promise of changing the world as we know it back in 2022, the earliest versions of ChatGPT presented a significant stumbling block: its tendency to spit out racist, biassed and sexually suggestive answers. It makes sense if you consider that this is a large language model that was trained on that which already exists on the internet – and we all know what kind of stuff can be found on the web. From smut fiction to hate speech, this dicey content was poisoning the data pool and resulting in some seriously toxic responses.

The solution? To build a filter that would catch these kinds of responses before they made it past ChatGPT’s blinking cursor. Of course the building of this filter would require more human input than the usual data scraping that was used to train ChatGPT, because human beings would need to assess whether or not something was offensive. By identifying and labelling enough offensive inputs, they could feed ChatGPT a “guidebook” of topics, words and ideals that are not OK to use.

That’s where the Kenyans come in. In 2021, OpenAI (ChatGPT’s parent company) partnered with Sama, a data labelling partner based in San Francisco that claims to provide developing countries with “ethical” and “dignified digital work”. Sama recruited data labellers in Kenya to work on behalf of OpenAI, playing an essential role in making the chatbot safe for public usage. But despite their integral role in building ChatGPT, these workers faced gruelling conditions and low pay.

In order to obtain the labels it needed, OpenAI outsourced tens of thousands of text snippets to Sama, who then sent it to their Kenyan teams. Many of these texts seemed to originate from the darkest reaches of the internet, detailing graphic situations such as child sexual abuse, bestiality, murder, suicide, torture, self-harm and incest. Kenyan workers were expected to read and label between 150 and 250 passages of this text per nine-hour shift, with those passages ranging from around 100 words to well over 1,000. For this, they were paid a take-home wage of between around $1.32 and $2 per hour.

While the nature of this work eventually led to the cancellation of the contract between OpenAI and Sama, the harsh realities faced by these data labellers sheds light on a darker facet of the AI landscape. Beneath its techy allure lies a reliance on covert human labour in the Global South, often characterised by exploitation and harm. These unseen workers persist on the fringes, yet their contributions underpin billion-dollar industries.

Your dead granny wants you to sign up for premium

The digital world is brimming with personal remnants, from forgotten MySpace profiles to dormant social media pages, lingering online even after a person’s passing. But what if AI used these artefacts to recreate the presence of those we’ve lost?

It’s a reality unfolding before us as we speak – and one that AI ethicists caution could lead to a new phenomenon: “digital hauntings” by “deadbots.” With the ongoing advancements in generative artificial intelligence, there emerges a novel possibility for grieving individuals to interact with chatbot avatars trained on the digital footprint of the deceased, encompassing their voice, appearance and online persona.

Certain products from companies like Replika, HereAfter and Persona, marketed as “digital replicas”, are already pushing these boundaries, allowing users to simulate the departed. Amazon’s 2022 demonstration, wherein its Alexa assistant mimicked the voice of a deceased woman using just a brief audio clip, underscores the potential of this unsettling trend.

In their recent publication in Philosophy and Technology, AI ethicists Tomasz Hollanek and Katarzyna Nowaczyk-Basińska employed a technique known as “design fiction” to envisage various situations where fictional characters encounter challenges with different “postmortem presence” enterprises. The scenario that stuck with me the most is one where an adult user is impressed by the realism of their deceased grandparent’s chatbot, only to soon start receiving premium trial and food delivery service advertisements in their deceased relative’s voice.

“These services run the risk of causing huge distress to people if they are subjected to unwanted digital hauntings from alarmingly accurate AI recreations of those they have lost,” Hollanek added. “The potential psychological effect, particularly at an already difficult time, could be devastating.”

“We need to start thinking now about how we mitigate the social and psychological risks of digital immortality,” Nowaczyk-Basińska added.

No, that’s not really Katy Perry

Earlier this month, New York City saw a grand gathering of music, entertainment and fashion icons for the annual Met Gala, themed “Garden of Time”.

However, amidst the glamorous snapshots flooding social media, Katy Perry was notably absent. Or was she?

Despite the fact that Perry was in studio recording while the Met celebrations went on, two images of her (wearing two completely different dresses) seemingly posing for photographers at the Met started circulating on social media channels as other celebrities made their entrances.

While it’s unclear where these AI-generated images originated from, they were realistic enough that they were shared and liked thousands of times before sharp-eyed viewers cried foul. According to a screenshot shared by Perry herself, even her mother was fooled into commenting on her flowered ball gown.

Less amused by AI’s imitation of her is Scarlett Johansson, according to recent headlines.

The actress stated that she was left “shocked and angered” after OpenAI launched a chatbot this month with a voice that sounds “eerily similar” to hers.

This comes on the heels of Johansson turning down an offer from OpenAI to voice the chatbot, named Sky, in September last year. Two days before Sky went live, Sam Altman reached out to Johansson again, requesting that she rethink the offer. She declined, and the contested demo version of the chatbot went live days later.

In a statement shared with the BBC by OpenAI, Mr Altman denied that the company had sought to imitate Johansson’s voice. “The voice is not Scarlett Johansson’s, and it was never intended to resemble hers,” he wrote.

Johansson’s lawyers have retaliated by sending two letters to OpenAI, demanding insights into how the voice was created. While OpenAI continues to deny that the voice of its chatbot was designed to imitate Johansson, they have since suspended the use of that particular voice.

The AI train is running out of coal

As AI continues to soar in popularity, researchers have raised concerns that the industry could be facing a shortage of training data – the essential fuel powering advanced AI systems. This potential scarcity threatens to decelerate the development of AI models, particularly the expansive language models that rely heavily on vast datasets.

In other words: after scouring the world wide web for half a decade and scraping data from billions of sites (presumably both legally and slightly-less-than-legally), AI is running out of fresh data to learn from.

When I first read this headline, I was a bit surprised that we could be at this junction already. To me it feels as though OpenAI and its cousins have only really been a major part of our lives since 2022. Consider that the internet itself is over four decades old – that’s four decades worth of writing. It’s a bit astonishing to consider that these large language models have burned through this much fuel already.

Obviously, training powerful, accurate and high-quality AI algorithms requires an immense amount of data. For example, ChatGPT was trained on an extensive dataset encompassing 570 gigabytes of text data, equivalent to roughly 300 billion words.

In a similar vein, the stable diffusion algorithm, which powers many AI image-generating applications like DALL-E, Lensa and Midjourney, was trained on the LIAON-5B dataset. This dataset includes an impressive 5.8 billion image-text pairs.

High-quality AI models cannot be developed using low-quality data sources, such as social media posts or blurry photographs, despite their abundance and ease of access. These types of data do not provide the richness and precision needed to train high-performing AI systems. Therefore, ensuring both the quantity and quality of data is paramount for the advancement and reliability of AI technologies.

To further complicate the problem (although this writer in particular was quite gleeful to learn this fact), AI models cannot be trained on AI-generated content. All of those blogs and LinkedIn articles that are being churned out at pace by ChatGPT? Those are absolutely useless for training purposes – in fact, their inclusion in learning datasets can actually cause damage to the algorithm. By making ChatGPT so freely available to the masses, OpenAI has effectively contributed to its own training data shortage.

(For the record, I don’t usually subscribe to schadenfreude. But when something has messed with your industry and your ability to work as seemingly effortlessly as ChatGPT has, well… it does make you smile a little to see them struggle for once.)

So, what next? Innovation, of course. The people building AI models are way too smart to be held back by something as trivial as a data shortage. One promising avenue for AI developers is to enhance algorithms to utilise existing data more efficiently. By refining these algorithms, it is likely that, in the coming years, they will be able to train high-performing AI systems using less data and potentially less computational power. This optimisation would not only advance the capabilities of AI but also contribute to reducing its carbon footprint, addressing environmental concerns associated with large-scale data processing.

Another viable strategy is the use of specially-designed AI to generate synthetic data for training systems. In this approach, developers can create the specific data they require, tailored precisely to the needs of their particular AI model. Obviously, this kind of content differs from the break-the-algorithm type of AI-generated content I mentioned before. This synthetic data can mimic real-world data scenarios without the need for massive data collection efforts. It can fill gaps in datasets, provide diversity in training examples, and even help in creating rare or hard-to-obtain data instances.

By focusing on these strategies, the AI industry can overcome the challenges posed by data limitations, paving the way for more sustainable and efficient AI advancements.

Hooray for that, I guess. Or not.

About the author: Dominique Olivier, founder human.writer

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Balwin targets growth in the KZN market (JSE: BWN)

This deal also has an interesting funding mechanism

Balwin has agreed to acquire 13.41 hectares of land in Shongweni in KZN. The property is adjacent to Westown Square, which is a 50,000 square metre retail site due to be completed in 2025. The broader area includes plans for a hospital, hotels, warehousing, schools and all sorts of other things. I don’t know this particular area at all, but Balwin reckons its an LSM 8 – 10 opportunity that has strong population growth among 30-somethings in particular.

What makes this deal particularly interesting is the “pay-as-you-register” model that Balwin has put in place with the seller. Basically, a contracted amount per apartment is paid to the seller on the registration of each apartment. Balwin will acquire development rights once all infrastructure has been installed by the seller and the property is fully serviced.

The benefit here is obvious: Balwin can do this deal with far less strain on the balance sheet than would otherwise be the case. They will develop 1,260 residential apartments and pay for the development rights as each one is sold. The value of the development rights is R133.7 million.

The price paid to the seller will be R100k for a 1-bedroom, R110k for a 2-bedroom and R120k for a 3-bedroom apartment. Balwin must settle the full price within 6 years and expects to sell all the units within 4 years, so they’ve built in some fat. Importantly, there are no inflation escalations on the purchase price.

There’s a further R27 million payable to the landowner when apartments are sold to clients. This is based on 1.5% of the selling price of each apartment. The seller of the development rights must also pay 1.5% over to the landowner, so Balwin and the seller are sharing the cost equally.

Long story short, Balwin has found a way to defer the payment of the development rights and make this a less capital-hungry exercise. Importantly, the company must still fund the development of the apartments and of course takes the risk on the development being a success, as the development rights must be settled within 6 years regardless of how well the development performs.

This is a category 2 deal, so shareholders won’t be asked for an opinion or a vote on it. The share price closed 5.4% lower on the day but this announcement came out after market close, so keep an eye on share price action on Monday when trade reopens.

Brikor is back in the green (JSE: BIK)

The company has guided a return to profitability

Brikor has released a trading statement for the year ended February 2024. It’s an important one, as it reflects a move from a headline loss per share to positive headline earnings.

With full details due to be released before the end of May, we at least know in the meantime that HEPS will come in at between 1.2 cents and 1.4 cents per share vs. a headline loss of 0.1 cents per share in the comparable year.

The share price is trading at R0.15 and there is limited liquidity in this thing, with a market cap of just over R100 million.

Brimstone’s intrinsic NAV is heading the wrong way (JSE: BRT)

Sea Harvest is the source of pressure on intrinsic NAV in the past three months

Brimstone’s intrinsic net asset value (NAV) per share is the key metric to assess the performance of the business, as this is an investment holding company with a variety of investments ranging from very small stakes through to control.

The investments in Oceana (a 25.1% stake) and Sea Harvest (53.4% stake) contribute the bulk of the intrinsic NAV per share. These are valued based on the market value per share, so this can lead to significant swings in the Brimstone intrinsic NAV.

Between December 2023 and March 2024, intrinsic NAV fell by 6.7%. Pressure on the Sea Harvest share price is largely to blame, although some other investments also went the wrong way (like MTN Zakhele Futhi). A reduction in net debt helped limit the pain at least.

If we take a longer-term view, it’s easy to see that the intrinsic NAV per share has been a really disappointing story in recent years. On a fully diluted basis, it reduced from R12.827 per share as at December 2020 to R11.097 per share as at March 2024. The market has valued the share price at roughly a 55% discount to intrinsic NAV, with little sign of that discount closing.

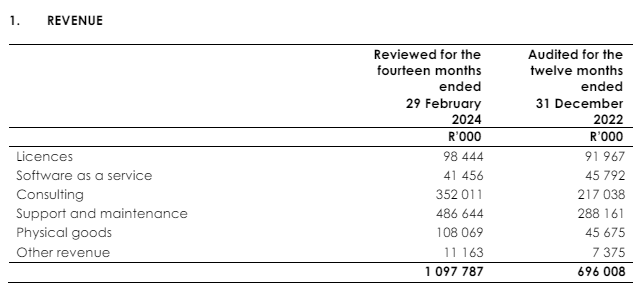

4Sight: full of buzzwords, but also growth (JSE: 4SI)

Revenue is up substantially

4Sight operates in the technology space and it really won’t take you long to figure that out, with words like digital transformation and artificial intelligence featuring prominently. Buzzwords aside, the growth in the business across Africa and the Middle East is significant. This table shows how they make money:

Total revenue is up by 57.7% and the increase in support and maintenance is particularly encouraging, as that sounds recurring in nature. Operating profit is up by 76.9%, so the revenue growth is being accompanied by an improvement in margins – a wonderful combination for investors. Gross margin did dip though, so the operating expense management was where the good stuff happened.

But here’s the trick: you need to read really carefully. The latest period is for the 14 months to February 2024 and the comparable period is the 12 months to December 2022. This is because of a change in year-end. Those growth rates are impressive regardless, but clearly that plays a role.

HEPS is up by 153.8%, coming in at 6.037 cents per share. The dividend is 5 cents per share vs. no dividend in the comparable period. Again, this is for 14 months, so you can’t use this in the normal way to calculate a dividend yield or P/E multiple. They did also release 12-month results which help, but there’s an odd situation here where January and February added plenty of revenue but not much profit. It’s not clear how much of this is seasonal.

Change in reporting period and other questions aside, there’s still a very high growth rate and the dividend is a high payout ratio vs. HEPS, suggesting that these are high quality earnings.

The share price is R0.84.

ISA Holdings is another tech small cap on a charge (JSE: ISA)

Revenue and profits are up strongly

ISA Holdings seems to be in the right place at the right time, with a business model focused on cybersecurity solutions. This is a major area of investment by corporates at the moment. ISA offers a consumption-based solution that is resonating with consumers.

Revenue is up by 33% and profit before tax is up 23% for the year ended February 2024. These are great growth rates, even if there is some margin contraction. They attribute the dip in margin (gross profit margin down from 53% to 49%) to product sales during the current period that excluded any of the higher margin services.

Share of profits from equity associate DataProof (another cybersecurity offering) increased by 63%. This helped drive HEPS higher by 35% to 18.9 cents.

But here’s the real kicker: the dividend payout ratio is 100%. The interim dividend was 7.7 cents and the final dividend is 11.2 cents. This adds up to 18.9%, which is equal to HEPS for the year. As cash quality of earnings goes, you won’t find better than that.

And in case you think it’s a fluke, they did exactly the same thing in the comparable period with a 100% payout ratio.

A chance for MC Mining shareholders to sell to Goldway (JSE: MCZ)

There is no compulsory squeeze-out envisaged

Goldway is giving the remaining shareholders in MC Mining another chance to sell their shares on the same terms and conditions as the recent buy-out offer. This means a cash price of A$0.16 per share.

This gives remaining shareholders until 25th June to accept the offer. Those who do not accept it will then sit with a highly illiquid stake in the listed company. There’s no guarantee whatsoever of being able to sell those shares to Goldway or anyone else.

Goldway intends to delist the shares from the ASX and the JSE but has not commenced the process yet. The listing on the AIM in London is being cancelled, though.

A most unusual situation at Pan African Resources (JSE: PAN)

The company needs to rectify a technical problem with previously paid dividends

Here’s one that you won’t see every day! Pan African Resources has released a circular that seems to reclassify the share premium account on the balance sheet as a distributable reserve. The reason is that dividends paid from 2019 to 2023 met the net assets test on a ZAR basis, but not on a USD basis which is the presentation currency for the group.

The substantial depreciation in the rand over the past few years led to a Foreign Currency Translation Reserve with a negative equity balance of $171 million. It gets deemed as a distributable reserve under the rules for assessing whether a dividend can be paid, leaving the group with a serious problem. Even though the ZAR numbers look perfectly capable of supporting a dividend, the USD balance sheet tells a different story.

Share buybacks over the same period suffer from the same problem.

The company has no intention of trying to recover the past dividends from shareholders. Instead, the goal is to get shareholders to agree to remedial resolutions that take the form of a capital reduction, which means reclassifying some equity as distributable reserves.

What isn’t clear at this stage is how the company fixes this problem going forward. They note that a number of accounting strategies are being considered to ensure adequate distributable income going forward. Changing the presentation currency to ZAR is presumably one way to do it, although this goes against the company’s attempts to appeal to a global shareholder base.

Like I said: you won’t see this every day.

Revenue dropped at Quantum but HEPS is way up (JSE: QFH)

This was a period of margin improvement

Revenue at Quantum Foods fell by 13% for the six months to March 2024. That doesn’t sound like the start of a great highlights package, yet operating profit was up a ridiculous 327% and HEPS jumped by an even sillier 653%.

To put more sensible numbers to it, headline earnings increased from R6 million to R43 million. This is a good reminder of how touch-and-go the base period was.

Although there was an impact from avian flu outbreaks in this period, the real win came in higher egg prices and a drop in input costs in the form of raw materials for feed (yellow maize and soya meal). This is despite the weaker rand, as international prices thankfully fell by enough that the rand couldn’t offset the benefit. And of course, less load shedding took some strain off the system in terms of diesel costs etc.

In summary, despite the pressure on revenue from a drop in egg volumes, the unit economics improved so much that profitability went firmly in the right direction. This is a great reminder that margins matter more than revenue. It doesn’t help to sell more of something that is barely profitable.

Of course, first prize would be a recovery in egg volumes along with these improved margins.

As this paragraph in the outlook section shows, Quantum isn’t buying the story that load shedding is gone for good:

No interim dividend has been declared despite the improved results.

Little Bites:

Director dealings:

A director of a major subsidiary of Shoprite (JSE: SHP) sold shares worth R1 million.

Telkom (JSE: TKG) shareholders have approved the category 1 transaction to dispose of Swiftnet to an infrastructure investment consortium that includes Actis and Royal Bafokeng Holdings. In fact, the deal achieved 100% approval from shareholders in attendance at the meeting, which is an unusual level of support.

Afine Investments (JSE: ANI) released a trading statement noting that earnings per share will be 94.70 cents for the year ended February 2024. This is because of upward revaluations of properties. They haven’t given a specific number for HEPS but they have noted that it will be within 20% of the prior comparative period, so cash earnings aren’t as exciting as the property revaluations.

Accelerate Property Fund (JSE: APF) released an announcement correcting an error in the circular regarding the directors’ intention to subscribe for the rights offer shares. The circular initially noted that it is likely that the directors won’t subscribe for them. The correct position is that directors have disclosed an intention to participate, which makes sense given how discounted the rights offer is price is.

Hammerson (JSE: HMN) announced the results of the dividend reinvestment plan alternative. It had very little uptake, which isn’t a great show of faith in the company. Holders of 1.57% of shares on the UK register and 0.58% of shares on the SA register elected to receive shares in lieu of a cash dividend.

Momentum Metropolitan Holdings (JSE: MTM) is looking to do all of us a favour by shortening the name to Momentum Group. This requires the issuance of a circular to shareholders – admittedly a very small one. In case you’re curious, you can find it here.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Anglo American reports a further drop in diamond sales (JSE: AGL)

Thelatest De Beers sales numbers are in

In and amongst all the noise around potential offers for the group, Anglo American has released the latest sales cycle numbers for De Beers. With $380 million in sales for cycle 4, the trend is firmly negative. Cycle 4 2023 was much higher at $479 million. Cycle 3 2024 was also significantly higher at $446 million.

Apart from the obvious issues of macroeconomic pressures, there was a quieter period of trading in India during the elections. The next sales event is in the US – and in Las Vegas, no less. The company has already tried to temper expectations by referencing macroeconomic issues and hoping for a recovery in coming years.

As a reminder, Anglo American’s current proposal to shareholders to unlock value involves a disposal of some kind of De Beers. Selling a business with falling sales isn’t straightforward – at least not for a decent price.

Bidcorp is still growing despite much lower inflation (JSE: BID)

This is one of the best rand hedges on the JSE

Bidcorp has updated the market on performance for the ten months to April. In case you aren’t familiar with the group, this is a global food services giant that is one of the genuine rand hedges on the JSE, as very little of its revenue is generated here.

A key feature of this result is that food inflation has come all the way down to 2.6% vs. 15.2% in the comparable period. They point out that food inflation is lower than core inflation for the first time in two years. Another important point is that rand weakness has delivered a 9% positive impact on the reported numbers, as much of the revenue is generated elsewhere.

The performance across Australasia, Europe and the United Kingdom looks solid, with sales growth and stable or improving margins. Emerging markets are more of a mixed bag, with China and Brazil of particular concern. South Africa is actually performing well despite the challenges here, with other highlights being Malaysia, Chile and the Middle East.

Group sales for the ten months increased by 8.8%, with the UK as the standout at 15.9% (rand weakness helps here). Gross margins are slightly ahead of the previous year, which is just as well because operating costs as a percentage of revenue deteriorated by 40 basis points to 18.9%.

The EBITDA before IFRS 16 margin of 5.6% of net revenue is in line with 2023 which was a strong year. This is a period of working capital absorption for the group, with the good news being that working capital is in line with management expectations and slightly better than the comparable period.

R4.4 billion has been invested by the group, which is well up on R2.0 billion in the comparable period. Aside from two bolt-on acquisitions (a small bakery in Germany and a seafood wholesaler in South Africa), the focus has been on vehicles. They are busy with a “couple” of potential deals in the UK and one in Europe, all expected to close early in the new financial year.

Bidcorp is a powerhouse of note. Like most of the really high quality businesses on the JSE, the multiple reflects that. Based on last reported earnings, the Price/Earnings multiple is roughly 19x.

Bytes is growing strongly, despite the ex-CEO mess (JSE: BYI)

If you bought the panic selling around the departure of Neil Murphy, you’re smiling

Disgraced ex-CEO Neil Murphy is no longer involved at Bytes, after it came out that he had executed many, many undisclosed trades over a few years. The share price reflected panic when the news broke and those who were smart enough to buy the panic have already locked in a roughly 20% return in the past month.

This is because the group is still doing well, although margin compression in the IT services industry continues. Gross invoiced income increased by 26.7% and revenue was up 12.3%, so they are having to work harder and harder for that revenue. Gross profit increased 12.5% and operating profit was up 11.4%. By the time we reach HEPS, growth has been leveraged up to 15.4% – a very presentable result, especially in GBP.

The final dividend is 17.6% and the board has decided to pay another special dividend like last year, with a 16% growth rate in the special dividend as well. The only reason why they call it a special dividend is because they don’t want to commit to the higher payout ratio forever, just in case they need the capital for something else.

Plenty of activity around Capital & Regional (JSE: CRP)

And a 19.7% increase in the share price on the day

Capital & Regional is suddenly the talk of the town, confirming that on 19 April it received a non-binding indicative proposal from Vukile Property Fund (JSE: VKE) regarding a possible cash and share offer for the share capital of the company. I’m surprised it was kept under wraps for this long.

There’s nothing binding at this stage, with Vukile facing a PUSU (Put Up or Shut Up) deadline of 20 June 2024. As the juicy name suggests, they need to announce a firm intention to make an offer by that date or they need to confirm that they won’t make an offer.

On top of all this, Capital & Regional announced that Growthpoint (JSE: GRT) (which holds 68.13% in the company) received a non-binding expression of interest from NewRiver REIT in relation to a potential offer for Capital & Regional. The board of Capital & Regional hasn’t received a proposal from NewRiver at this stage.

Of course, the outcome of all this was a significant jump in the Capital & Regional share price as punters hit the buy button in the hope of a juicy offer coming in.

The growth rate at Emira isn’t useful (JSE: EMI)

But the range for the distribution certainly is

Emira Property Fund released a trading statement for the year ended March. The challenge here is that the comparable period is only nine months long as there was a change of year-end, so the increase in distribution per share of between 19.86% and 21.93% isn’t a valid growth rate as the comparable period was shorter.

It does tell us that the range is 116 to 118 cents per share and that’s the useful bit of information. This puts the fund on a trailing yield of 11.7%.

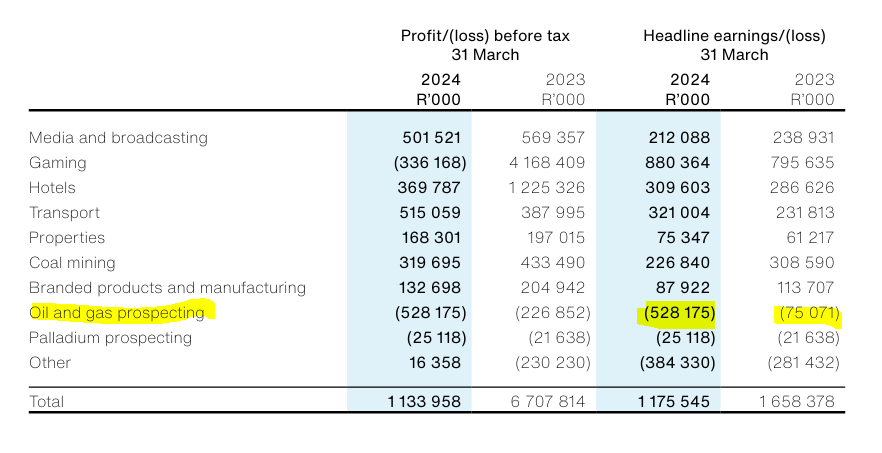

These HCI group companies all released numbers: HCI, eMedia and Frontier Transport (JSE: HCI | JSE: EMH | JSE: FTH)

I’ll deal with them all in one place – and Tsogo Sun separately as it is much bigger

I’ll start with eMedia, which reported for the year ended March 2024. Load shedding doesn’t help TV viewership at all, with advertising down 1%. It’s worth highlighting that e.tv spends R600 million per year on local drama series. Media Film Service got hurt badly by the writer’s strike in Hollywood, with profit down R31.5 million year-on-year. They also spent R8.8 million in legal battles with MultiChoice related to channels being carried on that bouquet. Revenue in eMedia fell 2.1% and HEPS was down 11.7%. The dividend of 16 cents per share was 20% lower.

Moving on to Frontier Transport, a wonderful example of how to make money in an unsexy industry, revenue increased by 8.9% and HEPS was up 37.8%. This is because operating costs increased 6.3%, with the resultant margin expansion driving that juicy improvement in HEPS. In addition to the ordinary dividend of 48.4 cents, there was a special dividend in January of 137.38 cents.

We now get to the mothership, Hosken Consolidated Investments (or HCI for short). We have an interesting scenario here where HEPS fell 29% and the dividend per share doubled to 100 cents. The major negative move was in oil and gas prospecting, where the headline loss jumped from R75 million to R528 million. That’s a very big move when total headline earnings came in at R1.18 billion. The reason why we can see negative moves of this side and yet a higher dividend is that the negative moves are non-cash in nature, with downward fair value adjustments recognised on the investment held by Africa Energy Corp.

Here’s what the total group looks like:

Although HCI controls Tsogo Sun, I’ve dealt with that company further down as the market cap is much larger than the likes of eMedia and Frontier. And in case you’re wondering, Deneb reported earlier in the week.

Investec’s earnings moved higher in GBP – and thus much higher in ZAR (JSE: INL | JSE: INP)

Key metrics like Return on Equity (ROE) also moved higher

Investec has released results for the year ended March 2024. This was a period of significant corporate activity, like the major deal in the UK to combine Investec Wealth & Investment UK with the Rathbones Group. They also sold the property management company to Burstone Group for a small fortune.

To make the numbers more comparable, Investec has presented adjusted operating profit as though the abovementioned transactions took place at the start of the period. On that basis, adjusted operating profit is up 8% in GBP or 24.6% in ZAR. Return on Equity has moved higher, up from 13.7% to 14.6%.

The cost to income ratio improved from 54.7% to 53.8% as total operating costs increased by only 3.2%, an impressive show of discipline.

The full-year dividend increased by 11.1% to 34.5 pence for the year.

It’s interesting to note the revised through-the-cycle targets for the credit loss ratio. In Southern Africa, where the book is mainly high income private clients and large corporates, the range is 15 to 35 basis points. In the UK with more of a mid-market positioning, the range is 35 to 55 basis points. This tells you something about the economic resilience of the different books.

The share price closed 4.5% on the day of these results, taking the 12-month gain to 19%. Those who enjoy range trading strategies might want to take a look at this chart:

Kore Potash’s share price took off on a rocket (JSE: KP2)

The ASX has even queried the recent price action

The Australian Stock Exchange sent Kore Potash a price query, which means they noticed an unusual uptick in price and volume in the stock and wanted to understand if there is any information that should’ve been disclosed that could have leaked into the market.

Here’s the chart – and it’s not hard to see why the ASX took notice:

The company reiterated that no formal legal agreements have been entered into with PowerChina re: the all-important EPC contract for the development of the Kola Project. In other words, the last release from the company is still the latest news.

Speculators seem to be lining up for a release of good news and what that might do to the share price.

Winds of change at Mahube Infrastructure (JSE: MHB)

As in, literally

Mahube Infrastructure released a trading statement dealing with the year ended February 2024. There’s a huge swing in profitability and in the right direction. Compared to a headline loss per share of 53.68 cents, HEPS will come in at between 91.05 cents and 100.64 cents.

Aside from dividends received from investee companies (including special dividends), the earnings were driven by a favourable change in the fair value of financial assets due to a revision of wind forecasts an improvement in the macroeconomic indicators.

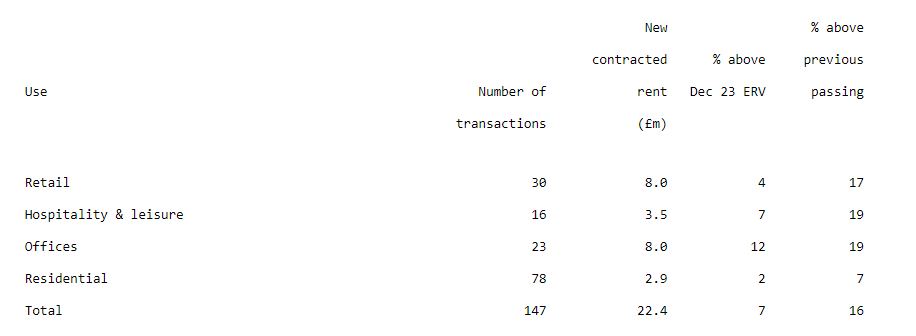

Strong momentum at Shaftesbury (JSE: SHC)

Things seem to be going well in this London-focused fund

Shaftesbury has released a trading update that was presented at the company’s AGM. The highlight is that leasing demand is producing rents that are 7% ahead of 2023 numbers, with the company also enjoying the recycling of capital at a premium to the values at which the properties are held on the balance sheet.

They have completed £213 million in asset sales since the merger that created Shaftesbury as we know it today, with a premium of 3% to the valuation on the books. They have reinvested £83 million in target acquisitions.

The loan to value is at 30% which is a very healthy level for a property fund. The current weighted average cash cost of drawn debt is 4%.

Perhaps most interesting, the office portfolio is showing the best increase in contracted rent vs. 2023 levels, with the return to office trend gaining momentum:

Never a dull moment at Stefanutti Stocks (JSE: SSK)

The group is hoping that the Eskom claim will be finalised in Q3

Stefanutti Stocks is in the midst of a turnaround plan. If you aren’t sure why, a quick look at the balance sheet where liabilities exceed assets will dispel that uncertainty for you. The financials are still prepared on a going concern basis due to the expected cash flows under the restructuring plan.

For those punters willing to take a speculative position here, the key is the dispute with Eskom that is now with the Dispute Adjudication Board (DAB). This relates to contractual claims and compensation events at Kusile Power Project. Independent experts evaluate the delays and related numbers and the DAB then makes a decision that is binding on the parties. Stefanutti Stocks submitted a total claim of R1.6 billion to the experts and will now wait to see how much it gets. It is hoped that a binding decision will be issued in Q3 2024.

The rest of the group still has all the usual uncertainty and difficulty that seems to follow construction companies around. For example, Hyvec JV was previously shown as a discontinued operation. A change of plan means that it is back in continuing operations. Delays in on-boarding labour due to legislative changes led to the recognition of an onerous contract provision and a loss for the year there of R78 million.

Although the year-on-year swing in continuing and discontinued operations is rather wild, the combined operations managed to show what looks like a smooth result: growth in profit for the year of 9%.

HEPS tells a different story though, deteriorating by 44% to a loss of 55.73 cents.

Revenue up and HEPS down at Tharisa (JSE: THA)

Chrome prices helped mitigate the fall in PGM prices

Tharisa has announced results for the six months to March. They reflect a 9.9% increase in chrome production and a 7.7% decrease in PGM production. Chrome prices were 16.9% higher and PGM prices were 39.3% lower.

The net effect is that revenue was actually up 10.1%, with EBITDA slightly down and EBITDA margin contracting from 24.2% to 21.6%. Due to higher finance costs, HEPS fell sharply, down 25% to US 13.2 cents.

The interim dividend of US 1.5 cents per share is 50% lower than the prior year.

Tsogo Sun is facing pressure at casinos (JSE: TSG)

Adjusted HEPS has dipped

Tsogo Sun has released results for the year ended March 2024. Income is up 2% and operating costs increased 3%, with load shedding having an impact on both those metrics. This led to adjusted EBITDA decreasing by 2%.

When operating profits are going the wrong way, it’s hard for HEPS to avoid following suit. Due to the termination of hotel management contracts in the base year, it’s important to look at adjusted HEPS to see the impact of operational performance. This is down 5%.

Perhaps the final dividend tells the best story, down a substantial 30% after the interim dividend was flat year-on-year. There’s clearly uncertainty in this space and the group has also had to recognise impairments based on the financial performance.

It might help matters if exposure to the Western Cape can be increased. The casino footprint is heavily geared towards the northern parts of the country. The group notes a plan to develop a new casino and hotel precinct in Somerset West, as well as upgrades to the Caledon site.

Little Bites:

Director dealings:

Des de Beer has bought shares in Lighthouse Properties (JSE: LTE) worth R15.8 million.

A non-executive director of WeBuyCars (JSE: WBC) bought shares in the company worth R506k.

Spear REIT (JSE: SEA) is due to release the circular for the substantial acquisition of a Western Cape portfolio from Emira (EMI) by no later than 2 July. In the meantime, Spear has released the forecast financial information for the target portfolio on the assumption that the transfer date for the properties is 1 December 2024. It shows that the expected distributable income from the portfolio for the year ending February 2026 (the first full year) is R8.1 million, with net property income of R118.9 million and finance costs of R104 million due to the level of leverage. The release of the circular will give far more detail.

Mondi (JSE: MNP) has launched a €500 million 8-year Eurobond. The issue will close on 31 May and the proceeds are for general corporate purposes. The bonds are due in 2032 and have a coupon of 3.75%, so that gives you an idea of where investment grade corporate credit in London is trading. The debt is rated Baa1 by Moody’s and A- by Standard and Poor’s.

Ibex Investment Holdings (JSE: IBX) (formerly Steinhoff Investment Holdings) received almost unanimous approval from shareholders for the repurchase of the preference shares at R93.50 per share plus pro-rate preference dividends from 1 January 2024 until the scheme operative date. This isn’t a surprise, as there’s no other way for major holders to realise their investments.

Chrometco (JSE: CMO) announced that the CEO is stepping down and will be replaced by William Yang. Greg Hunter will be appointed executive chairman of the company. The share price is still suspended from trading.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

BHP increases its Anglo offer one more time – and Anglo says no (JSE: BHG | JSE: AGL)

The revised proposed exchange ratio is 24.8% higher than the initial proposal

The initial deadline for BHP to “put up or shut up” (that is the actual term – also called PUSU) was 22nd May. Anglo American requested an extension of the deadline, which was granted under UK law with a revised date of 29 May. This leaves a week for BHP to decide whether to put in a binding offer or not.

In the meantime, BHP keeps testing the waters with price and gets rejected every single time. The “final” exchange ratio is 0.8860 BHP shares for every Anglo share, plus the shares in Anglo Platinum and Kumba, as BHP is standing firm on a requirement for Anglo to demerge those assets. The revised ratio means that in addition to the Anglo Platinum and Kumba shares, Anglo shareholders would have 17.8% in the combined BHP and Anglo American group.

This proposal is 24.8% higher than the initial proposal put in by BHP. It represents a 47% premium to the undisturbed Anglo American share price (i.e. before the press speculation about the deal) and a much larger premium to the unlisted assets if you work out the Anglo Platinum and Kumba contributions.

BHP says that it won’t increase the offer further, unless a third party sticks in an offer or Anglo indicates that a higher price might be acceptable. In other words, they probably would increase the offer further if it gets the deal done.

Anglo has rejected this proposal once more, citing the complexities around the demergers as a major concern. I continue to enjoy the irony of this argument, as one of Anglo’s own strategic plans is to demerge Anglo Platinum!

Anglo American’s share price is up more than 21% in 30 days. If BHP walks away from this and nobody else puts up their hand, the pressure on the Anglo board to unlock value will be immense.

Burstone will look to reduce its debt (JSE: BTN)

The loan-to-value ratio is on the high side after the manco internalisation

Burstone (previously Investec Property Fund) paid a lot of money to internalise its management company. Although this has obviously saved on management fees, it required a significant capital investment that has contributed to the loan-to-value ratio moving from 42% at March 2023 to 44% at March 2024.

This is above the group’s comfortable range of 37% to 40%, so you can expect to see some recycling of assets to get it back down there. They have a disposal pipeline in South Africa and Europe and have generally managed to get the sales done at or above book value.

On the asset side of the balance sheet, the South African portfolio value was fairly stable, but the European portfolio fell by around 1% in value after valuation yields expended further. Along with some moves in derivatives, this caused the net asset value to fall 4.5% to R15.45 per share.

The share price at R7.19 (up 6.4% for the day) is a significant discount to that value.

The dividend payout ratio was 85%, down from 95% in the comparable period. This seems to be another place where the increase in debt has bitten.

Strong cost control drives earnings at Deneb (JSE: DNB)

When growth is hard to come by, you have to be disciplined

Deneb’s revenue growth of 7% makes it sound like things were quite easy for the group, yet the underlying story is that the automotive parts manufacturing business was up 26% and the rest of the group was pretty much flat. This is why diversification is important, especially in the industrials space.

Lower volumes make it difficult to maintain margins, so Deneb did pretty well to keep gross margin contraction to only 30 basis points. The magic was that costs only increased by 1% overall. Fixed costs were down 1%. This was good enough for operating profit to grow by 21%, provided we adjust for the insurance claims received in the base period.

Such an adjustment is warranted, as those claims were clearly a once-off benefit that skew the year-on-year performance if not removed.

Net finance costs were up 45%, with around half the increase coming from rate hikes and the other half from debt balances increasing. This is a perfect example of why banks do well in a combination of inflation and higher rates. The debt has come down sharply in the final quarter of the year, thanks to a 47% uptick in cash generated from operations. This will do good things for the income statement in the new financial year.

Adjusted HEPS (which is the right metric because of the insurance claim) increased by 25% to 23 cents per share. At R2.30 per share, you shouldn’t need to get the calculator out to work out that Price/Earnings multiple!

Double-digit dividend growth at Life Healthcare (JSE: LHC)

They expect a“lengthy implementation journey of NHI”

Life Healthcare has reported growth in revenue from continuing operations of 7.8%, as well as 8.4% growth in normalised earnings per share. The interim dividend is up by 11.8%, so the payout ratio has moved higher which is usually a good sign of confidence.

Paid patient days grew by 2.3%, so there was “volume” growth as well as pricing growth in the business.

Life Molecular Imaging (LMI) grew revenue by 77.5%, driven by the sales of NeuraCeq in the US. This business still makes a small loss at normalised EBITDA level as it is an early-stage operation. This loss is expected to reduce after this year.

Thanks to further growth in paid patient days as well as inflationary increases and growth in the South African imaging business, the group expects to see revenue growth of 6% to 7% for the full year. This outlook explains the higher payout ratio.

As for NHI, I’ll repeat the commentary verbatim:

“However, the approval of the Bill without addressing concerns raised during the parliamentary process, is a regrettable missed opportunity to expand sustainable access to healthcare. We, therefore, expect a lengthy implementation journey of NHI due to operational and legislative changes required, as well as the current fiscal constraints.”

Pick n Pay – or is that Pick n Pray? (JSE: PIK)

Things still look terrible there

Pick n Pay has released a sales update and trading statement for the 52 weeks ended 25 February 2024. It really only takes a visit to your local Pick n Pay grocery store to figure out what the problem is here. The numbers firmly reflect the in-store experiences and lack of consumer resonance, with sales down -0.2% for Pick n Pay in South Africa (or up +0.2% on a like-for-like basis). Internal selling price inflation for the period was 7.3%, so this means a heavy drop in volumes.

The Pick n Pay number includes Pick n Pay Clothing, which grew 17.0% or 7.7% on a like-for-like basis. This means the core grocery business is doing particularly horribly, offsetting all the good stuff in the clothing business.

Boxer continues to do incredibly well, with sales up 17.5% overall or 8.1% on a like-for-like basis. This implies some positive volumes growth along with the benefit of inflation and the ongoing store rollouts.

Although still firmly a poor cousin of Shoprite’s dominance in this space, Pick n Pay Online (which includes asap! and the Mr D partnership) grew sales by 74.4%.

Rest of Africa is in the highlights package for this period, with sales up 10.1% overall and 12.5% on a constant currency basis.

Armed with this knowledge, you won’t be surprised that Pick n Pay recognised a R2.8 billion impairment on the supermarkets. This is a non-cash charge of course, but it sends a message. It also includes another little nugget of information: loss-making company-owned stores will be closed or converted to either Pick n Pay franchises or Boxer stores. A long tail of problematic stores can be a matter of life or death for a retailer.

Other issues that hurt the numbers include once-off costs of R423 million across supply chain changes and employee restructuring, a roughly R400 million trade receivables provision (this implies that franchisees are also struggling), an additional R467 million in net debt service costs and R698 million in diesel for generators.

For the year, the headline loss per share was huge, coming in at between -228.99 cents and -177.14 cents. It’s even worse if you use comparable HEPS as their preferred metric, with a loss of -281.13 cents to -228.31 cents.

The group is working towards a rights offer of up to R4 billion, along with a separate listing of Boxer on the JSE. This is very similar to how Transaction Capital had to spin out WeBuyCars, leaving behind an ugly rump that will need a great deal of fixing.

Group net debt at the end of February was R6.1 billion, which was better than the guidance of R6.7 billion. A debt restructuring agreement has been concluded with lenders, securing funding up to 1 September 2025.

Most importantly, the strategic plan going forward will be presented by Sean Summers as part of the FY24 results presentation, expected on 27 May.

Reunert’s Electrical Engineering segment leads the way (JSE: RLO)

There are some less appealing trends elsewhere in the group

Reunert has reported results for the six months to March 2024. Revenue increased 7% and HEPS was up 8%, with the interim dividend also up 8%. This is real growth (ahead of inflation), so that’s something at least.

There were certainly some challenges in this period, like Nashua struggling with logistics challenges that led to shortfalls in products and a resultant knock to sales and operating profit. The other headache is in residential and small commercial batteries, where the market has become saturated and demand has fallen away. That situation would presumably be even worse after year-end, as there’s been no load shedding for weeks now.

The Electrical Engineering segment was the highlight, with revenue growth of 7% and operating profit growth of a meaty 12%. Both the power cable and circuit breaker sides of the business did well.

In the ICT segment, IQbusiness was successfully integrated into the ICT segment and this led to a 38% increase in revenue, yet operating profit was flat year-on-year. The Nashua issues sit in this segment.

Applied Electronics saw a 10% drop in revenue, but operating profit also remained flat year-on-year. It’s amazing to see two segments report steady profits despite revenue moving sharply in either direction!

The outlook for the full-year numbers is positive overall, with IQbusiness to be included for a full 12 months and encouraging signs in Electrical Engineering and the Defence Cluster (part of Applied Electronics).

RFG Holdings looks just peachy in these numbers (JSE: RFG)

Practically every metric has gone the right way

RFG Holdings has had to deal with a weak domestic consumer environment that led to a decline in volumes. You would never know that by looking at the numbers though, with price inflation taking revenue growth into the green and margins improving across the income statement.

Group revenue grew by 3.2%, with regional revenue up 5.8% and international volumes down 8.6%. The price vs. inflation mix was quite something, like in the regional business with price up 10.0% and volume down 5.5%. Internationally, price fell 6.5% and volumes 8.9% (port challenges in Cape Town did them no favours here), with forex benefits of 5.5% mitigating the pain. Mix effects make up the balancing numbers.

Long life foods increased revenue by 7.5% and fresh foods increased by 2.9%. Ready meals seem to have also done well. Consumers are craving convenience, a logical outcome of really busy households.

Operating profit margin expanded by 100 basis points to 10.2% despite these challenges, with operating profit growth of 15.2%. Reduced diesel costs vs. the prior year helped. Margins in the regional segment were up from 8.9% to 10.0%, with the international segment managing to increase from 10.4% to 11.5%.

Group EBITDA margin was up 140 basis points, with EBITDA growing 14.6%. Combined with a reduction in the net interest expense, this drove a 20.7% increase in headline earnings per share.

The group is focusing on working capital management, with a lower outflow for this period than in the prior year. Seasonality is important here. The bulk of the capital expenditure at the moment is at the Tulbagh fruit products factory and the group is achieving a return on equity of 15.7% at the moment, so shareholders shouldn’t feel upset about reinvestment of profits.

The cost of debt has blunted Spear’s growth (JSE: SEA)

Still, the fund is in the green at a time when many others aren’t

Spear REIT is respected on the JSE as one of the most focused, well-run property funds on the market. They can control a bunch of things, but not the prevailing level of interest rates. Property funds make extensive use of debt and this leaves them vulnerable to higher rates.

For the year ended February 2024, distributable income per share increased by 1%. The distribution per share is up 3.80%, which means the payout ratio has moved to over 95%. A payout ratio that high tells you a lot about the quality of the business.

The average reversion for the year was -0.37%, which is a pretty solid outcome in this environment. This speaks to demand in the Western Cape.

The loan-to-value has decreased from 36.30% to 31.60%, so the balance sheet is in a good place. The reduction in debt helped limit the impact of higher rates on distributable earnings.

The net asset value per share is up 2.8% to R11.80. The share price is trading at R7.90, which implies a trailing yield just under 10%. Next time you consider a buy-to-let property, remember that you can buy a solid REIT with instant liquidity, some underlying growth and a yield of 10% without you having any headaches with tenants.

Southern Sun shines brightly (JSE: SSU)

A record year of profitability

Southern Sun has a lovely story to tell for the year ended March 2024. 19% growth in income and 32% growth in EBITDAR (not a typo – this is a standard metric in the hotel game) drove a massive 77% increase in adjusted HEPS.

And yet, HEPS without the adjustment only grew by 7%. Should we be worried?

Not in this case, as the base period included once-off income from Tsogo Sun in the form of a separation payment of R399 million. Excluding that from the base is a much better way to view underlying performance, so adjusted HEPS is the right approach.

One of the encouraging signs in these results is the increase in average room rate of 9%. If your hotels aren’t well positioned and appealing, you can’t increase pricing. Food and beverage revenue is up 15%, so they are doing a great job on share of wallet as well.

It’s interesting to see how they allocated funds. Free cash flow of R970 million went towards share buybacks (R670 million), expansion capex (R180 million) and the reduction of net debt, with a comfortable net debt to EBITDA range being enjoyed.

The group’s exposure to Cape Town has been a major benefit here, with a strong year for tourism, business travel and events. Group occupancy levels came in at 58.6% for the year, which is 710 basis points up on 2023 but still below 59.3% achieved before the pandemic.

Given the improved outlook and level of performance, the final dividend is 12.50 cents. There was no final dividend in 2023.

Little Bites:

Director dealings:

Des de Beer has acquired shares in Lighthouse (JSE: LTE) worth R7.7 million.

One of the highly experienced directors of Santova (JSE: SNV) has sold shares worth R3m. Given the recent concerns around where we are in the shipping cycle, I would look at that quite carefully if I held shares here.

An associate of a executive director at Calgro M3 (JSE: CGR) has sold shares worth just under R2 million.

Harmony Gold (JSE: HAR) has reported yet another loss-of-life incident this month, this time at Phakisa mine in a blasting incident. All blasting operations have been temporarily suspended.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Double-digit growth in earnings at Alexander Forbes (JSE: ADR)

The strategic focus in recent years is paying off

Alexander Forbes has released a trading statement for the year ended March 2024. It has happy news for shareholders, with HEPS from continuing operations up by between 10% and 20%. In this environment, double-digit growth is admirable.

Including discontinued operations i.e. if we look at total operations, HEPS is up by between 23% and 33%. Although that’s no indication of the go-forward position, it’s always better when discontinued operations were a positive contributor rather than a mess as we so often see in large corporates.

In this case, the discontinued operations reflect the impact of the close-out of insurance liabilities and assets relating to the sale of the AF Life business to Sanlam, with remaining reserves released as well.

Detailed results are due on 10th June and the market will watch them closely, especially with the share price having been stuck in a stubborn range this year:

Collins Property Group now reports as a REIT (JSE: CPP)

And the distribution per share is much higher