Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

In the 32nd edition of Unlock the Stock, we welcomed Bell Equipment back to the platform. With the share price up substantially in the past year and the market digesting the news of no dividend, there was much interest from investors in this discussion.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Copper 360 invokes the spirit of Steve Jobs (JSE: CPR)

As the genius told us: real artists ship

One of my favourite quotes is from Steve Jobs, who said that real artists ship. That’s it. Simple as that. It’s easy to sit on the couch and talk about other people’s success and what they do. Get off the couch and ship something to show everyone what you can do.

At Copper 360, they’ve shipped alright – in this case, the first copper concentrate from the Northern Cape in 21 years. It’s a cleverly written bit of hype and I’ll go with it as a proud South African who wants to see our country move forward.

The first concentrate plant was commissioned within the planned period and is forecast to be ahead of planned production within the first few months of operation. The second concentrate plant is scheduled to start production at the end of July 2024. The SX/EW plant that produces copper cathode is also ramping up.

Speaking of ramping up, the share price closed over 19% higher on the news. The company recently made allegations of suspected market manipulation. Whilst those allegations still need to be proven, I bet they aren’t complaining about being 19% up for the day.

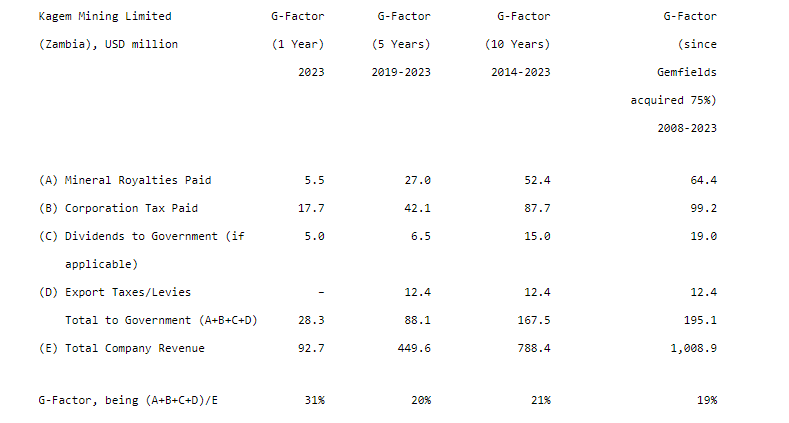

Gemfields and the G-Factor (JSE: GML)

The G is allegedly unrelated to Gemfields’ name

Before you get excited, I’m really just including this because I find it interesting. There’s no real news here about Gemfields as an investment.

The company releases a metric it calls the G-Factor, which apparently takes its name from government, governance and good practice. I’m quite sure the cute branding alongside Gemfields gave them some ideas on the name as well.

What makes this interesting is that it shows the value to a country of developing its mineral resources. It combines mineral royalties, corporate taxes, dividends to the government (if they are shareholders) and export taxes. It then divides this by revenue, showing what percentage of revenue is effectively going to the government.

Here’s the calculation they show for Kagem Mining:

It’s even higher at MRM in Mozambique, which might explain how they’ve managed to keep operating there despite security risks. Having the government on your side is of critical importance in Africa.

The company also notes that this measure isn’t perfect. It leaves out benefits to the country like taxes on employee salaries.

Long story short: driving the mining industry forward is good for any economy. Somebody please tell the South African government so that we fix our trains and ports.

Quilter’s distribution power shines through (JSE: QLT)

Muchlike at PSG Financial Services locally, it helps to have a sales force

I’ve commented a few times recently on how pure-play asset managers are struggling to meaningfully grow assets under management, while financial services groups with strong distribution networks are doing a solid job of attracting inflows. Of course, a sales team comes at a cost, so clearly they have to attract enough flows to make it a net positive strategy.

Quilter operates in the UK market and they make a big deal of their various distribution channel strategies. It’s working overall, with core net inflows in the first quarter coming in at almost double the comparable period. Gross Assets under Management and Administration were up 5% over the quarter i.e. between December 2023 and March 2024. These are impressive numbers.

It’s also great to see that productivity (measured as Quilter channel gross sales per advisor) was up 22% vs. the comparable period.

Quilter’s share price is up 30% in the past year, with all of that happening in the past six months. It trades at a high Price/Earnings multiple that is typical of a quality stock like this. Investors always have to be careful with such high multiples, even when the underlying company is strong.

RMH declares a special distribution (JSE: RMH)

This time, it’s funded by the exit from Divercity

If you’ve been following RMB Holdings, then you’ll know that the company has absolutely nothing to do with RMB anymore. In fact, it’s just a property holding company that is looking to achieve orderly exits of the portfolio, thereby returning capital to shareholders. That’s not the easiest thing to achieve in the current environment.

Step by step, it’s happening though. The exit from Divercity has now been completed, with RMB Holdings monetising its equity stake and loan claims in the company. This has led to the declaration of a special dividend of 3.5 cents per share (before withholding tax). The share price closed at 38 cents a share after the news.

Zeder: shareholders await news on Pome Investments and Zaad (JSE: ZED)

Patience will be needed, as these things take a long time

Zeder has released results for the year ended February 2024. It was an important period for the company, as it included the disposal of its stake in Capespan (except for Pome Investments) for proceeds of R511 million in cash. This led to the payment of a special dividend, with yet another special dividend of 10 cents per share declared as part of the year-end results.

The remaining assets are Pome Investments and Zaad, with Zeder having appointed PSG and Rabobank as co-advisors to consider any Zaad-specific approaches, given the size of that asset and the need to achieve the best possible exit – assuming such a deal materialises.

Based on management valuations in the sum-of-the-parts disclosure, Zaad is R2.34 billion of the total value of assets of R3.5 billion as at 10 April 2024. The reason for the strange date that doesn’t line up with the reporting period is that the company is trying to show the position after special dividends. On that basis, the value per share according to management is R2.29. Zeder currently trades at R1.75, with the discount due to many factors ranging from the costs of being listed through to the likelihood of a deal for Zaad and Pome coming through.

With Zaad having reported a decrease in recurring headline earnings of 38% for the six months to December 2023, investors should keep in mind that the farming industry and associated value chains remains a tough place to do business.

Little Bites:

Director dealings:

Two big-hitter directors at OUTsurance Group (JSE: OUT) bought shares in the company worth a total of R9.8 million.

At the group AGM, British American Tobacco (JSE: BTI) reminded the market that one of their values is “love our consumer” – a wonderful reminder of just how much ESG-washing goes on in that place. It’s like they just forget what products they produce each day. Anyway, the useful investment news is that the outlook for 2024 remains in line with guidance: low single digit growth in revenue and adjusted profit from operations. They expect performance to be weighted towards the second half, so don’t expect great news from the first half. By 2026, they expect organic growth of 3% to 5% in revenue and mid-single digits in adjusted profit.

Brimstone (JSE: BRT) issues shares to employees and executive directors as part of their remuneration. With such limited liquidity in the stock (both ordinary and N shares), it’s very hard for the staff to realise the value. Brimstone therefore likes to conduct a specific repurchase to help the staff members and executives monetise the stakes at a price equal to the 30-day VWAP. The value is going to be roughly R7.9 million in ordinary and R3.9 million in N shares. There are a bunch of minority holders who I’m sure would also love to monetise their stakes, but alas.

Conduit Capital (JSE: CND) is still trying to sell off CRIH and CLL to TMM Holdings. There have been multiple extensions to the fulfilment date, as the Prudential Authority hasn’t approved the transaction yet. It’s now gone on so long that a further extension to 31 May comes with new conditions giving the purchaser the right to cancel the agreement if the Conduit liquidator issues high court proceedings against CRIH before the effective date. There are also some amendments to how and where the money for the deal would be paid, assuming it goes ahead.

In the highly unlikely event that you are a shareholder in Eastern European property fund Globe Trade Centre (JSE: GTC), you will want to know that the company has released results for the year ended December 2023. Rental revenues were up 10% and funds from operations also moved higher. So did debt, with the loan-to-value ratio up from 44.5% to 49.3%. There is no, and I mean no trade in this stock.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Amplats: refined production is flat, but on track for full year guidance (JSE: AMS)

PGM basket prices are still way down on a year ago though

There seems to be more talk of a potential bull market for PGMs this year, although you would be forgiven for asking how on earth that is possible when Anglo American Platinum is down 27% this year. This takes the 12-month view to a 37% drop. The share price is languishing, with the desperation of investors in the sector perhaps driving the calls for a recovery.

If things are going to improve, it’s going to be because basket prices have moved higher and so have production volumes. Neither of those conditions are in place at Amplats, at least not on a year-on-year view for the latest quarter.

Production was the highlight, with refined PGM production at similar levels to the comparable period despite own-managed mines production being down. Sales volumes were also broadly flat. That’s where the good news ends unfortunately, as the ZAR realised basket price is down by a hideous 26% year-on-year. It’s up 8% sequentially (i.e. vs. the preceding three months), which is what has given support to calls for a bull market, but there’s a very long way to go.

There isn’t anything that the company can do about PGM prices. They can only manage their production, with guidance for 2024 unchanged at this stage. The potential for Eskom load curtailment is an ever-present risk in this sector as well.

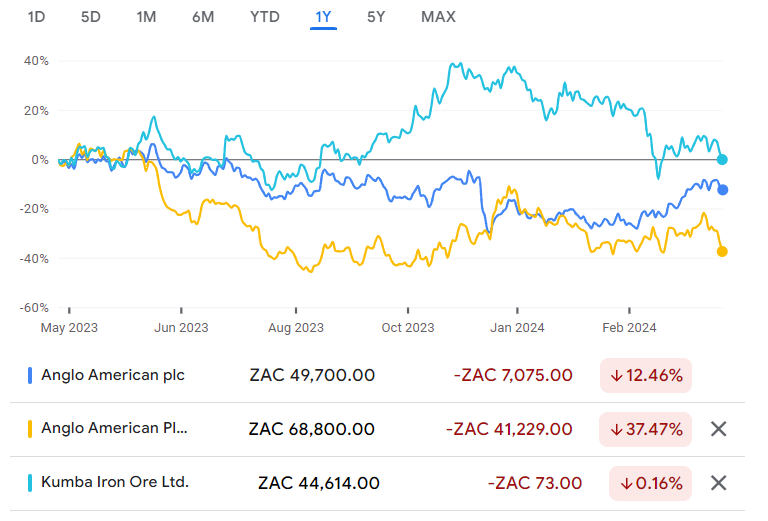

The Anglo American mothership has a good copper story to tell (JSE: AGL)

While the listed South African subsidiaries battle away with poor infrastructure

As you’ll read elsewhere in this edition of Ghost Bites, Anglo American Platinum and Kumba Iron Ore are struggling. Infrastructure is failing them. This obviously affects Anglo American as the ultimate controlling company, but shareholders in the mothership at least have other things to smile about, like the copper exposure.

Before we get to that, I want to touch on De Beers. Diamond production has been lowered in response to market inventory levels, which is a fancy way of saying that had to cut supply because demand was poor. The company has generally blamed macroeconomic conditions. I still believe that lab-grown diamonds are playing at the very least a supporting role here. Rough diamonds production was down 23% for the quarter and full year guidance has been lowered. On the plus side, diamond prices increased by 23%.

Let’s move onto the highlight now, which is copper production up by 11% thanks to higher throughput at Quellaveco and the operations in Chile. Operating in South America must seem like a breeze at the moment compared to South Africa.

Steelmaking coal production was up 7% thanks primarily to the Aquila and Capcoal operations. Iron ore was flat, with a strong performance at Minas-Rio offset by the challenges at Kumba. PGM production was 7% lower. Nickel is 2% lower and manganese ore is 7% lower.

There isn’t much to feel happy about in this quarter beyond the copper story. That really is where the focus is, with copper now representing 30% of total production at Anglo American.

In this share price chart of Anglo American vs. Anglo American Platinum and Kumba Iron Ore, you can see that none of them have exactly given shareholders a great time over the past year:

Ascendis shareholders approve the delisting application (JSE: ASC)

The company has also commented on the TRP news

Ascendis held the rescheduled general meeting on Tuesday and achieved strong support for the resolutions related to the independent board fee, the management agreement and perhaps most importantly, the authority to apply for the delisting of the company from the JSE.

The company also took the opportunity to comment on the announcement published by the Takeover Regulation Panel (TRP), clarifying that the TRP isn’t launching a new investigation. Instead, the regulator is drawing a line in the sand for any new complaints to be submitted, while also setting the timelines for them to be addressed.

Mid-teens growth at Capitec (JSE: CPI)

The market liked it, despite plenty of growth already priced in

By now, you should know that initial market reactions are based on the narrative and direction of news rather than well informed views on the underlying numbers. Capitec is clearly already priced for growth, yet the share price closed 7.8% higher on the news of 16% growth in HEPS for the year ended 29 February 2024.

The total dividend for the year was also up 16% and the net asset value increased by 15%, so it’s a mid-teens performance all round.

There’s a great chart in the report that shows the five-year performance in the business. Given the craziness of 2020 in general and the inclusion of the business banking business for only part of that year, taking a four-year view is perhaps more sensible (i.e. 2021 to 2024, four years of data and three years of growth). Over that period, it’s worth noting that net interest income grew by a total of 42%. In contrast, non-interest income increased by 71%, so it’s not hard to see where the focus has been.

If we include credit impairments, then income from operations after credit impairments is up 80%. That’s a 21.6% compound annual growth rate (CAGR) on this line. With that knowledge, you can see that 16.6% growth in the past year is actually a slowdown from the post-pandemic growth.

Capitec is known for its efficiency and expense management. If we look at operating expenses, that line has grown by 47% over three years, or a CAGR of 13.8%. The cost-to-income ratio has improved from 41% to 39% over the period, with investors latching onto the operating leverage and buying up the shares accordingly.

But in the past year, operating expenses increased by 17.4%, so the operating leverage actually went the wrong way.

In summary: Capitec is still performing very well, but seems to be slowing down vs. the post-pandemic performance.

Return on equity took a knock in 2021 due to impairments on investments, so comparing to that year isn’t very helpful. Instead, I would rather point out that return on equity (ROE) has been 25% – 26% in each of the past three financial years. That’s impressive.

I don’t think anyone believes that Capitec is anything other than an excellent business. The problem has always been the valuation. With a net asset value per share of R376.11, the current share price of R2,174 is a price/book of 5.8x. If we compare this to the ROE of 26%, the effective ROE is around 4.5%. That is a very low return by South African standards, which is why value investors continue to feel frustrated by Capitec’s share price performance. The share price is trading 35% higher over 12 months, though I must point out that the five-year gain (with a nasty pandemic during that period) is only 60% in total, which isn’t an exciting annual growth rate.

Capitec has spent the past few years building a diversified financial services groups. They have focused on winning more fully banked clients, thereby increasing their share of wallet per client. They are encouraging value-added services. They’ve repositioned the business bank in such a way that it aligns to the retail bank strategy in terms of fees. They are building out the insurance business, having sold credit life insurance policies since May 2023.

There has been a lot of noise around this story in terms of the quality of the book and the credit loss ratios. As things have settled in a post-pandemic environment, I think Capitec has clearly shown the sustainability of the model.

Having said that, the share price remains incredibly expensive in my view, even for such a quality stock.

Kumba continues to be hamstrung by Transnet (JSE: KIO)

Production and sales numbers are lower

Kumba Iron Ore, which is part of the Anglo American stable, has released its production and sales report for the first quarter ended March.

Sadly, the business had to cut back in order to try and get closer to the capacity that Transnet is actually capable of dealing with. There really is no point in mining loads of iron ore that just gets stuck at the mines instead of railed to the ports and exported. Of course, this is terrible for GDP, job creation and tax revenue, but that’s the country we live in right now.

The Saldanha Bay Port is where the export issue is being felt, with Transnet apparently undertaking maintenance programmes. Whether this will help or not remains to be seen. In this quarter, ore railed to port by Transnet was flat year on year, with equipment failures and a derailment in March leading to lack of any improvement.

For the quarter, total production fell by 2% year-on-year (in line with the plan to reduce production) and total sales decreased 10% due to port performance problems, which really is disappointing.

Although Transnet issues are out of Kumba’s hands, guidance has been left unchanged for the full year.

Orion Minerals releases its quarterly activities report (JSE: ORN)

The word “spectacular” is back

I couldn’t help myself: when I saw this announcement came out, I hit ctrl-F for “spectacular” and wasn’t disappointed. At least they are consistent in describing the recent development in the copper exploration.

These quarterly reports are important for junior mining houses, as they need to give the markets detailed updates on progress being made. In Orion’s case, they now have a complete site-based operating team at Prieska Copper Zinc Mine and trial mining is delivering results that they are happy with, as they work to de-risk the process.

Another important step was the acquisition of surface rights that allowed drilling to commence to provide additional mineral resource information. This is intended to enhance the all-important Bankable Feasibility Study (BFS).

The Sasol hole: a bottomless pit? (JSE: SOL)

Shareholders had to stomach a drop of nearly 11% on Tuesday

Sasol was a rags to riches story from the depths of the pandemic until mid-2022, by which time the share price was basically a twenty bagger! If you bought right at the bottom in 2020 and sold right at the top in 2022, you made approximately 20x your money.

Sadly, the days of trading at over $400 have become a distant memory, with the share price down at $135. What went up has certainly come down:

Plagued by South African infrastructure and a few other things, the company has proven to be a poor proxy for the oil price. It hasn’t been a hedge against inflation, either. The only thing it has really hedged against is a feeling of happiness, helping shareholders remember that there’s always something in life to feel upset about.

The reason for the latest share price knock (almost 11% in a single day) is that Sasol’s performance isn’t good and neither is the outlook, based on the production update for the nine months to March 2024.

Production guidance at Secunda Operations has been reduced. In Chemicals, the average sales basket price year-to-date is down 20% vs. the prior period, leading to a 17% drop in revenue as volume growth couldn’t possibly offset this. Sure there are some highlights, including the recent regulatory victory around how emissions at Secunda are measured, but the overall direction of travel is clearly down.

If you were hoping to play a game of Eskom and Transnet bingo, then you won’t be disappointed. Sasol makes sure we know that the infrastructure in South Africa is a major part of the problem. This is despite an improved Transnet Freight Rail performance (albeit off a low base) that helped export coal sales increase by 9%.

Trustco increases its stake in Legal Shield Holdings (JSE: TTO)

This is a share-based deal with Riskowitz Value Fund as the sellers

Trustco already holds an 80% stake in Legal Shield Holdings, which is turn holds Trustco Insurance, Trustco Life and Trustco’s real estate portfolio. They seem to be particularly excited about the property portfolio, with a surprising comment that Namibia is experiencing an “acute shortage of serviced land” – Namibia may be sparsely populated, but I guess most of it is the desert. Gorgeous place, by the way. I hope to visit again one day.

Back to the deal, Trustco will issue 400 million shares at R1.17 each to Riskowitz Value Fund, which is a price vastly in excess of the current listed share price. Irritatingly, the announcement talks about the number of shares being acquired in Legal Shield, without indicating the percentage of the company that the shares represent.

Now, this is where it gets even more complicated. You see, the market cap of Trustco is only R247 million, so they are issuing shares worth much more than the current market cap. To avoid this being a takeover, Riskowitz Value Fund has given the chairperson of Trustco an irrevocable instruction regarding voting of the shares. And then for further confusion, there’s a put and call option structure between Trustco and Riskowitz Value Fund for 100 million shares at R1.17 per share.

You know what I like to invest in? Straightforward companies that do simple, logical, understandable things without unusual commercial terms. Trustco is usually the opposite of that, with the share price down 97% over five years.

Little Bites:

Director dealings:

An associate of a director of Workforce Holdings (JSE: WKF) has bought R19.6 million shares in an off-market deal. With average daily traded value of roughly R60k, there’s no way to buy a stake that size in on-market deals.

A prescribed officer of ADvTECH (JSE: ADH) sold shares worth R2.8 million.

The boardroom drama continues at MultiChoice (JSE: MCG), with a major change in direction around Imtiaz Patel sticking around as chairman. At the start of April, MultiChoice announced that Patel would be deferring his retirement as chairman in order to assist with the Canal+ deal. Fast forward a few Chasing the Sun episodes later and he’s on his way, with Elias Masilela taking over as chairman. Despite all of this, Patel will remain involved in assisting the group on a consultancy basis. Sometimes the only consistency in this world is inconsistency.

Copper 360 (JSE: CPR) released an unusual announcement about suspected market manipulation. They talk about unusual and uncommercial trades in its shares, continuing for a period of several weeks. I guess we will find out if there’s any merit to these claims, or if the significant drop in the share price really is just the result of more sellers than buyers. It will be very embarrassing if nothing comes from these claims. In a separate update, the company noted that shareholders voted in favour of the share subscription facility with GEM Global Yield of up to R650 million.

Kibo Energy (JSE: KBO) continues to sell shares in Mast Energy Developments (MED) to reduce the balance on the loan facility with RiverFort Global Opportunities PCC. This is literally the sale of assets to pay debt, which is just one of Kibo’s many challenges. The latest sale is worth just over £22k.

Oando Plc (JSE: OAO) is playing catch-up on its financials, with results for the 12 months to December 2021 and December 2022 now released.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In just a few minutes, you can get the latest news and my views on Sirius Real Estate, Afrimat, Oceana and PSG Financial Services. Use the podcast player above to listen to the show.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

At Anglo American, Kabwe raises its head once more (JSE: AGL)

This is despite the High Court previously dismissing the claimants’ application

If you would like to read a particularly interesting sequence of events, then check out this link on the Anglo American website that sets out the company’s position on the Kabwe lead mine and the associated class action.

I quite enjoyed this paragraph:

“We strongly encourage careful consideration of the commercial motives of law firms and their funders in bringing a case like this, in singling out AASA as part of a major reputable mining company while completely ignoring the evidence and clear culpability of the actual responsible parties.”

The High Court previously dismissed the application by the claimants. They took almost a year to make that decision, highlighting multiple legal and factual flaws.

The High Court has now granted the claimants the right to appeal the judgment. Anglo American will obviously oppose any appeal that may now follow.

Cashbuild: is this finally the bottom? (JSE: CSB)

Volumes have finally stopped falling

Cashbuild has been really struggling to find any growth at all in this difficult environment in South Africa. Thanks to issues like load shedding and higher interest rates, it’s hard to find South Africans will to invest in their properties.

Perhaps assisted by the lack of load shedding, there are finally signs of life in the latest quarter. It really didn’t come a moment too soon, as the share price has seen a lot of pain:

Revenue for the third quarter of the year was up by 2% for existing stores. Importantly, sales volumes were flat in existing stores, which means that Cashbuild may finally have bottomed. Goodness knows 3% group revenue growth isn’t nearly enough to be exciting, but at least it’s heading in the right direction again. Selling inflation was 2.4% higher year-on-year.

Cashbuild South Africa (over 80% of group sales) was positive in terms of existing growth. Even P&L Hardware, which has really been suffering, managed to achieve a flat performance for the quarter. Pressure was mainly felt in Botswana and Malawi, which is the smallest segment in the group.

Merafe’s production was down sharply this quarter (JSE: MRF)

This is probably doing a few favours for Eskom as well

Merafe released its production report for the quarter ended March 2024. It reflects a 26% decrease in attributable ferrochrome production from the Glencore Merafe Chrome Venture in the period.

This is because of the Rustenburg smelter not operating in response to market conditions. Smelters use a lot of electricity, so Eskom is the one company in South Africa that probably didn’t mind Merafe allowing the smelter to get a few cobwebs.

A win for Murray & Roberts in Latin America (JSE: MUR)

This is a helpful shift in momentum for materials handling contracts

Murray & Roberts announced that Terra Nova Technologies has a 51% share in a joint venture that has been awarded an engineering, procurement and construction (EPC) contract with a large copper producer for a mine in South America. The total contract value is around $200 million.

Over 27 months, starting this month, the scope of work will include a primary crushing facility, an overland conveyor, a power transmission system and associated infrastructure.

This is great for Terra Nova, as the order book has been a struggle since the end of COVID. The business was acquired by Cementation Americas in 2019 and was a decent contributor to earnings in the year before COVID.

With a share price down 92% over five years, Murray & Roberts needs all the good news it can get.

Dear, oh dear – not the “hype” language at Orion Minerals (JSE: ORN)

Words like “spectacular” get me worried

Orion Minerals closed 26% higher on Monday as the market jumped at the headline of the SENS announcement, which talked about a “spectacular high-grade copper intercept” at the Okiep Copper Project. This is clearly exciting news, but I get worried as a matter of principle when I see stuff like this. When companies are trying to hype up a share price, investors are in danger of nasty corrections in value.

The saving grace here is that the findings are spectacular, with the CEO noting that this is one of the highest grade intercepts reported in South Africa for the past 40 years, adding significantly to Orion’s early production plan for the Okiep Copper Project.

The proud South African in me loves seeing news like this and of course I wish them nothing but success. I just hope they don’t get drawn into the trap of using flowery language and then disappointing investors down the line when something goes wrong or gets delayed. Having a highly volatile share price isn’t a good thing.

South32: all on track, other than Tropical Cyclone Megan (JSE: S32)

FY24 production and operating cost guidance is unchanged, other than Australia Manganese

There are a lot of variables when it comes to mining. Management can do their best, but there’s not much they can do about angry weather. At South32, Tropical Cyclone Megan negatively impacted the performance at Australia Manganese. Operations there were suspended in March, with a recovery plan underway.

For an indication of why diversification is helpful in this sector, South Africa Manganese (same metal, different weather) achieved record production for the quarter ended March.

The overall story is that FY24 production and operating cost guidance is unchanged for the full year, except for Australia Manganese due to the weather. Important strategic steps included the approval of the development of the Taylor zinc-lead-silver deposit at Hermosa, as well as the decision to sell Illawarra Metallurgical Coal for up to $1.65 billion. That deal is expected to be completed in H1 FY25.

Net debt decreased by $154 million to $937 million in the quarter, thanks to the operating performance and partial release of working capital tied up in inventory.

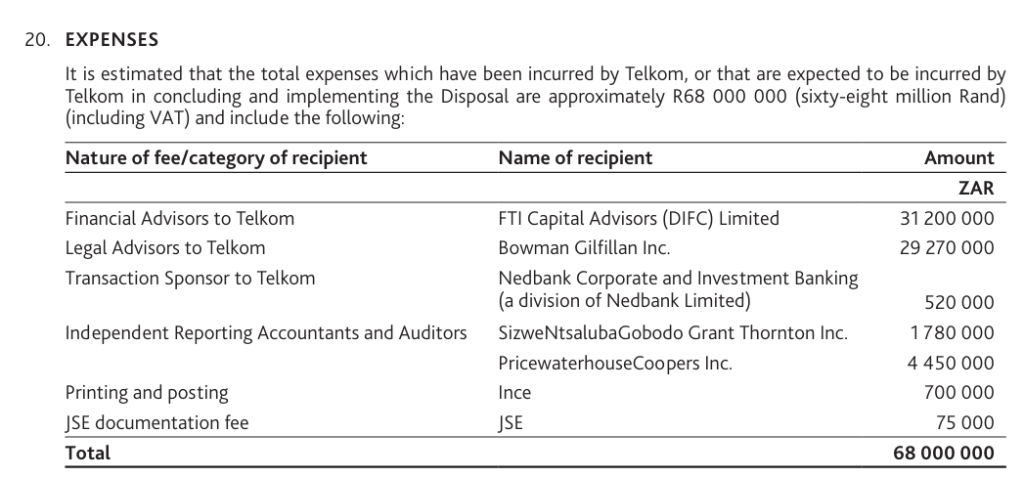

Telkom releases the Swiftnet disposal circular (JSE: TKG)

And the advisors on the deal must be itching to spend their fortunes

The Swiftnet deal is very important for Telkom. They have the opportunity to sell the business for a base purchase price of R6.75 billion. The terms make allowance for balance sheet adjustments up until the effective date of the deal.

It’s worth noting that up to R225 million of the existing R360 million shareholder loan may remain outstanding, with interest payable at a rate equal to the rate paid by the purchasing consortium to its bankers for the deal, plus 200 basis points. It would need to be fully settled within a 30 month period.

The buyer is a private equity consortium led by Actis and including Royal Bafokeng Infrastructure, with the latter holding not less than 30% of the shares. Those buyers will be getting their hands on a business that owns 4,000 commercially viable masts and towers in South Africa.

This deal is part of Telkom’s value unlocking strategy. We can’t be sure yet whether Telkom will deliver on that strategy, but we can certainly see the value unlocked by the financial and legal advisors in this deal:

If you ever wondered why corporate M&A is so lucrative for the advisors, it’s because percentage-based fees are accepted as the market norm. This is “only” 1% of deal value (roughly), but is still a vast sum overall.

Assuming Swiftnet will be sold, Telkom will primarily be left with Telkom Consumer, Openserve and Business Connexion. To give context to how big Swiftnet is within the group, the pro-forma financials for the six months to September 2023 (assuming Swiftnet had been sold at the start of the interim period) would’ve reflected HEPS that was 33% lower due to that business no longer being in the group.

Little Bites:

I don’t usually bother with non-executive director changes in listed companies, but it’s worth noting that Warren Chapman has resigned as a non-executive director of enX (JSE: ENX).

Ellies (JSE: ELI) has applied to the JSE for a voluntary suspension of trading of shares. There is no prospect of Ellies meeting the listings requirements given its current status. Interestingly, subsidiary Ellies Electronics (Pty) Limited continues to operate and the business rescue practitioner believes that it has a reasonable prospect of being saved. Perhaps only the listed structure will collapse and the Ellies name might live on. Only time will tell.

I worry about how many shareholders actually read the odd-lot offer documentation at Coronation (JSE: CML) and considered the tax implications. Either way, holders of 65,699 shares sold their shares in the odd-lot offer and holders of 13,496 shares retained their shares. There were a further 141,105 shares sold in the specific offer. In total, Coronation mopped up 206,804 shares for a total investment of nearly R7 million. This is 0.05% of shares in issue.

If you’re curious about how Anglo American (JSE: AGL) is thinking about sustainability and the projects they are delivering, then you’ll find the latest presentation on this topic at this link.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Ascendis will be investigated by the TRP (JSE: ASC)

After loads of mud-slinging on social media, the regulator is going to take a detailed look

The Takeover Regulation Panel (TRP) has many responsibilities. One of them is to investigate any complaints regarding affected transactions and offers. The potential take-private of Ascendis clearly falls within that ambit.

There has been a lot of noise and accusations around this deal, thrown in just about every direction you can think of on social media. There are defamation lawsuits. There are posts ranging from sensible to downright ridiculous. At some point, it needed a regulator to come in and actually take a proper look to see if any regulations have been breached.

The TRP notes that it has received approximately 20 complaints related to this transaction, with Ascendis having already taken remedial action on a “considerable number of them” in the form of issuing a supplementary circular with corrected disclosure of concert parties. They also had to reconstitute the independent board.

The regulator is planning to move quickly it seems, with a deadline of 10 calendar days for any further complaints to be submitted. This period ends at noon on 29 April 2024. The parties against whom complaints have been lodged will then have 20 business days to respond once they have received the collated complaints. The TRP will take 3 business days between the deadline for submissions and the presentation of the collated complaints to the impugned parties.

And finally, the complainants will then have 10 calendar days to respond to the responses by the impugned parties. No, I’m not sure why it’s business days in some cases and calendar days in others.

Whatever the outcome, this is exactly what needed to happen – the regulator investigating the complaints, rather than ongoing damaging interactions on social media that call the functioning of the entire market and regulatory system into question.

The clock is now ticking and the lawyers are billing.

Mondi walks away from DS Smith (JSE: MNP)

This is a useful reminder that deals fall over regularly

A deal isn’t a deal until all suspensive conditions have been met. This means that there’s a risk of failure right up until the 11th hour. When a transaction is little more than an early-stage investigation into whether a deal might make sense, the failure risk is even higher. This is why investors should always be cautious of getting too excited when they see news of potential deals.

In a perfect example of this, Mondi has decided not to proceed with the all-share merger with DS Smith. This is after conducting a due diligence and considering the value of the merger. The market responded positively to the corporate discipline, sending the Mondi share price 9% higher on the day.

What the Mondi announcement neglects to mention is that US rival International Paper came in as a competing bidder for DS Smith. Mondi chose to step out of the way of a bidding war, which isn’t quite the same thing as doing a due diligence after a deal announcement and then walking away. Same outcome, but based on the pricing of the deal rather than the quality of the DS Smith business.

Moving from deodorants to banks, Old Mutual has finally received Section 17 approval to establish a bank. The Prudential Authority has given the all-important nod to Old Mutual’s plans. This is a big deal, as you don’t just rock up at the offices and fill in a three-page form to get clearance.

For shareholders, the spending really starts now. As we’ve seen at Discovery, it’s not cheap to start a bank. In fact, it costs an absolute fortune if you’re going with the full-service model – even without having a branch network. And whilst Capitec has proven that success is possible in this game, it was achieved through strong differentiation from competitors and excellent strategic execution. I think it’s quite tough to argue that Discovery’s banking efforts have truly made waves in the market.

As for Old Mutual, we will have to see what they build here. Another me-too bank doesn’t make a great deal of sense in the South African market. You may also recall that Old Mutual walked away from its investment in Nedbank, so this is a slightly odd full-circle moment.

There’s already a green bank in the market. I can’t help but wonder what colours Old Mutual will go with. In my experience, purple is quite fun!

Little Bites:

Director dealings:

A director of Italtile (JSE: ITE) has sold shares worth R185k.

All conditions for the disposal of Eqstra Investment Holdings by enX (JSE: ENX) have been met, with the Takeover Regulation Panel having issued a compliance certificate. The transaction will be implemented during June 2024. You may recall that the buyer here is Nedbank (JSE: NED) and I think it’s a pretty interesting strategic move.

When the first quartz-powered watch made its debut at the end of the 1960s, it inspired both excitement and existential fear in watchmakers around the world.

Isn’t it interesting how people can look at the same event from different angles? Japanese brand Seiko’s debut of their first quartz-powered watch in 1969 is often referred to as the start of the “Quartz Crisis” for the Swiss watchmaking industry – a time of great upheaval and financial woes. But every now and then, you’ll hear whispers of the “Quartz Revolution”, suggesting Seiko actually sparked a horological breakthrough. They pulled off what many thought was impossible, and they did it flawlessly (as Seiko tends to do).

Those who label it a crisis likely see it from one perspective, while others view it as revolutionary. So, why do some see it as a crisis? After all, change and innovation are part of the game in everything we do. Let’s dive into that discussion, starting with the Swiss.

Make watches, not war

Our story begins with the circumstances of Switzerland’s neutrality during World War II.

While other nations redirected their industries to churn out military hardware like tanks and bomb timing devices, Switzerland remained steadfast in its watchmaking tradition. One could say that while the rest of the world was going tick-tick-boom, the Swiss preferred to stick to tick-tick-tick.

This choice proved pivotal, catapulting the Swiss watch industry to dizzying heights. In the early 20th century and well into the aftermath of World War II, Switzerland dominated the global market for mechanical watches, accounting for a staggering 95% of all sales. With virtually no competition, Switzerland held an unparalleled lead in technical expertise and craftsmanship.

Production was primarily conducted in small, state-controlled enterprises, where the majority of the work was executed by skilled hands using reliable yet straightforward machinery. Even in those days, Swiss watches epitomised perfection, exquisite craftsmanship and uncompromising quality. The watch industry employed approximately 90,000 individuals either directly or indirectly.

However, in the 1950s and 60s, as the race to develop the first quartz wristwatch heated up, the Swiss encountered formidable competition. Quartz technology tantalised with the promise of cheaper and more accurate timepieces than their mechanical counterparts. Despite these advantages (and the fact that one of the world’s first quartz movements was manufactured by a Swiss watchmaker consortium during the early seventies), Swiss watchmakers hesitated to fully embrace quartz. They cherished the intricate artistry of mechanical watches, a unique feature that remains prized to this day.

Yet, the growing popularity of quartz watches became undeniable. By the late 1970s, quartz timepieces had eclipsed mechanical ones in the market, sending Swiss watchmaking into a tailspin. Of the 1,600 Swiss watch brands in existence in 1970 (just a year after Seiko’s quartz watch debut), approximately one thousand failed to survive the following decade. Employment within the Swiss watch industry plummeted by two-thirds during the same timeframe.

The democratisation of horology

Who might champion the Quartz Revolution over the Quartz Crisis? Well, naturally, the Japanese stand at the forefront, alongside those who harbour a fervent enthusiasm for technology and the belief in the ever-changing nature of industry.

The revolutionary impact of the Astron – Seiko’s debut quartz watch – cannot be overstated: boasting an accuracy of +/- 5 seconds per month, a feat no Swiss movement of its era could rival. Swiss counterparts struggled to match this precision over a 24-hour cycle, let alone sustaining it for an entire month.

The Japanese approached their watch presentations with a youthful, vibrant and playful flair. Leveraging cutting-edge production techniques, they ensured their watches boasted solid quality. The once prestigious “Swiss made” label lost its lustre, becoming obsolete and antiquated practically overnight. Seiko outlets proliferated, overshadowing Swiss-made mechanical watches, which were soon deemed inaccurate and overpriced.

An often overlooked aspect of this transformative era is Seiko’s democratisation of horology on a global scale. While the Swiss, Americans, French and Germans may have produced more accessible versions of mechanical watches, none could match the accessibility of Seiko’s quartz-powered timepieces. The affordable watch brands that are flourishing worldwide today are a direct outcome of the Quartz Revolution, a paradigm shift that ultimately proved immensely beneficial for many.

One of those beneficiaries, if you can believe it, actually ended up being a Swiss watch brand.

Second breath, second watch

In the early 1980s, Swiss banks enlisted the expertise of management consultant Nicolas George Hayek to assess their dire predicament. Hayek devised two strategies to navigate the crisis. His vision involved consolidating the brands of the two major watch groups, ASUAG and SSIH, under a single powerful umbrella brand and introducing a new watch line that combined Swiss quality with affordability.

Thus, the birth of the Swatch Group was realised through a banking agreement, with Nicolas G. Hayek leading the charge.

Swatch, an abbreviation for “Second Watch” (not Swiss Watch) signified an ingenious concept – to offer affordable, everyday watches that complemented a mechanical collection rather than replacing it entirely. The quartz-powered Swatch watch was pitched as an everyday-about-town kind of timepiece, while its mechanical counterpart would be the special-occasion, important-meeting watch. This way, the Swiss could hold on to their legacy of mechanical prowess while benefiting from the quartz trend.

Hayek adopted a bold marketing approach, highly unconventional for the Swiss watchmaking sphere at the time. Swatch timepieces boasted a distinctive profile: flat, lightweight, bright and audacious. Hayek personally curated the designs chosen for production. Positioned in the affordable price bracket, Swatch watches directly challenged their Japanese counterparts. In an unexpected turn, Swatch swiftly became a ubiquitous accessory in global pop culture, reigniting the allure of “Swiss made.” It was a stroke of genius, arriving literally at the eleventh hour.

Competition: the great motivator

Seiko’s impact on the Swiss watch industry was profound, acting as a catalyst for transformative change. By introducing new technologies, innovative designs, and competitive pricing strategies, Seiko disrupted the status quo that had long characterised Swiss watchmaking. The traditional Swiss watchmakers, accustomed to their dominance in the market, were forced to reevaluate their approach and adapt to the evolving landscape. Fortunately, Swatch was born, rising like a phoenix from the ashes of a dormant watchmaking industry.

Change is an inevitable part of life and history is a testament to its continuous evolution. Just as horse-drawn carriages gave way to cars, every aspect of our world undergoes transformation. Those who embrace these shifts and adapt accordingly are the ones who not only survive, but thrive.

Lab-grown vs. mined diamonds, anyone?

About the author:

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.

Companies around the world are leveraging advanced technology to drive innovation and enhance efficiency in the workplace.

Optimism about Artificial Intelligence (AI) has been high ever since the launch of ChatGPT by OpenAI in November 2022. In the first quarter of 2024; companies in the AI sector raised over US$11 billion in funding for companies like Moonshot AI, Minimax (China) and Humanoid Robot (US).

The backbone of AI applications is the processing units made by chipmakers, and this is where the most market action is. As the leading manufacturer of chips for generative AI, NVIDIA – with a massive 80% of the semiconductor chip market dwarfing companies like Advanced Micro Devices inc. (AMD) – has clocked in returns north of 200% in the last 12 months.

Getting a Slice of AI

Without having to create your own basket of shares, the Satrix NASDAQ 100 ETF is one of the most convenient ways for South African investors to get a slice of the AI action. NVIDIA is among the top three holdings in the fund, accounting for 6.3% of its weighting, while AMD makes up 2.1%. Another big AI player in the fund is CrowdStrike, making up 0.5% of the fund, which uses AI to proactively identify and address digital security threats. Broadcom makes up 4.6% of the fund, a company in the semiconductor and infrastructure software industries.

Almost 50% of the fund is made up of the “Magnificent Seven” stocks – Microsoft, Apple, Alphabet, Amazon, Nvidia, Tesla and Meta which are leading innovations in the AI space.

Though historical returns cannot guarantee future returns, the NASDAQ index that this ETF tracks has pulled in 48.6% in the last 12 months to March and 12.5% year-to-date in rand terms.

For more on the AI topic, listen to the recent podcast featuring Nico Katzke of Satrix:

The Rest of the International Scene

AI is not an isolated sector and many of the technological advances also apply to other industries. In the US this has further helped grow Large Cap stocks with Info-Tech stocks raking in US$18 million in inflows for the first quarter of the year, according to Bank of America. In March, the MSCI US Index was up 3.1%, while the MSCI UK and MSCI Euro indices were up 4.5% and 3.7% respectively, in dollar terms. The MSCI World and the S&P 500 indices were both up 3.2% during the month, while the NASDAQ Index was up 1.2% and the MSCI Emerging Markets Index was up 2.5%.

Locally it has Been a Gold Rush

Local markets held strong for the month, with the FTSE/JSE All Share Index up 3.2%, recovering from two negative months that began the year. Propped up by the mining sector, particularly gold stocks (Harmony up 40.4% and Gold Fields up 22.5%), the Resource Index was up 15.4% for the month, while the Industrials index was up 2.9%, and Financials were down 3.5%. Listed Property slowed in March after a strong start to the year, with the FTSE/JSE SA Listed Property Index (SAPY) down 1.0%. With the South African Reserve Bank (SARB) putting the rate cut on ice for the moment, the bond market dragged during the month with the FTSE/JSE All Bond Index (ALBI) down 1.9% while Cash was up 0.6%.

The rand ended February at R19.18 to the dollar and strengthened to R18.94 by the end of March, a 1.3% appreciation.

SatrixNOW is a no-minimum online investing platform from Satrix that allows you to buy and sell ETFs directly.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Copper, iron ore and energy coal are on track at BHP (JSE: BHG)

The latest update covers the nine months year-to-date

Each quarter, BHP Group releases an operational review that goes into great detail on each of the operations in the group. If you want to really dig in, I suggest referring to the full announcement.

The key takeout is that copper, iron ore and energy coal production is on track for the year. Notably, copper volumes are up 10% thanks to strong production within the group. In iron ore, production has been consistent despite heavy rainfall. Of course, things can’t be good everywhere, with the metallurgical coal operations in Queensland not managing to offset the impact of wet weather (including two cyclones), leading to revised guidance. Energy coal has had a better time of things, with production expected to be at the upper end of the guidance range.

Over in Canada, the Jansen Stage 1 project is ahead of schedule with a 44% completion status. The group also notes that a decision on the future of the nickel business in Western Australia will be made in coming months, as the group responds to difficult realities in that sector.

Record chrome production at Jubilee, but pressure on copper (JSE: JBL)

Chrome and PGM production guidance is unchanged and copper has been lowered

Jubilee Metals released an operational update for the third quarter of the 2024 financial year. This covers the three months to March.

The good news is that chrome production achieved a quarterly record despite being a seasonally lower quarter due to the holiday period in January. On a year-to-date basis, chrome production is up 19.2%. There’s more to come, with a second chrome processing module due to be completed in August 2024 and fixed margin tolling agreements extended to 2027.

The same can’t be said for PGMs, where reduced stock of lower grade feed material led to a decline in quarter-on-quarter production. Over nine months, PGM production is 3.6% lower than the comparative period.

In Zambia, construction activities at the Roan concentrator and Sable refinery impacted production. Project Roan has experienced a six week delay in delivery of final electrical components, which will push commissioning out to May 2024. This has led to a reduction in guidance for the year, although this is really just a short-term wobbly. The long-term picture is much better, with partnership agreements being negotiated that could delivery substantial copper units.

As further upside optionality in this story, don’t forget the partnership with International Resources Holding in Abu Dhabi regarding the large surface copper Waste Rock Project. Jubilee is busy with a detailed resource definition to confirm the material reclamation strategy and location of targeted processing units.

Mantengu will tap into GEM Global Yield’s facility “in due course” (JSE: MTU)

The company has reminded the market of the terms of the facility

Mantengu previously released a circular detailing the terms of the R500 million facility made available by GEM Global Yield to the company. Although there’s nothing new in the latest announcement, Mantengu has reminded the market of some key terms related to the capital injection, as the company plans to drawdown on the facility in due course.

Essentially, Mantengu will alert GEM Global Yield that it wants to raise capital. A floor price must be given with each notice, which is the lowest price at which the company is willing to issue the shares. The investor has to subscribe for at least 50% of the shares and can subscribe for up to 200% of them, subject to some conditions. There are also some calculations around the subscription price, along with other terms that are necessary for a share price that isn’t very liquid.

At this point, we don’t know exactly how much Mantengu is planning to raise or when. We just know that it’s coming soon.

The tide comes in for Oceana shareholders (JSE: OCE)

HEPS growth is significantly higher than the initial trading statement suggested

Here’s another great example of the words “at least” or “more than” working hard in a trading statement. When Oceana released an initial trading statement in March, the indication was HEPS growth of “more than” 60% for the six months to March 2024. The good news is that it’s a lot higher than that, coming in at between 89% and 99%.

This implies HEPS of between 565 cents and 595 cents for the interim period vs. 299.1 cents in the comparable period.

The driver of this result was Daybrook’s higher fishmeal and fish oil sales volumes at a time when US dollar fish oil pricing is at record highs. Closer to home, Lucky Star managed to improve its volumes in March. The drag on the numbers was lower Wild Caught Seafood sales volumes, but there’s very little chance of every segment in a group like this doing well at the same time.

A trading halt at Orion Minerals (JSE: ORN)

The Australian market is an interesting place

Orion Minerals is listed in Australia, so we see rather interesting nuances from that market coming through from time to time. One such rule relates to trading halts ahead of major announcements, with Orion Minerals requesting a halt until the commencement of trade on Monday 22 April. This is because the company intends updating the market on exploration results at the Okiep Copper Project, with an investor webinar also scheduled for 22 April.

These rules exist to avoid any information finding its way into the market before the announcement, so it protects all investors equally.

PSG Financial Services (previously PSG Konsult) shows the power of distribution (JSE: KST)

When you have a sales force, AUM tends to head in the right direction

PSG Financial Services is one of the better companies on the local market, evidenced by an 11% increase in recurring HEPS for the year ended 29 February 2024. Better yet, the dividend is up by 17%, so management is feeling confident.

These numbers have been driven by a 15% increase in assets under management, as well as a 13% increase in gross written premium. With return on equity of 23.4%, there’s much to feel good about in this result. I would keep an eye on expenses though, with technology and infrastructure costs up by 13% and fixed remuneration up 12%.

Performance fees constituted 2.8% of headline earnings vs. 6.5% in the comparable period. This talks to the resilient underlying nature of the business model.

At divisional level, PSG Insure saw its recurring headline earnings fall by 6%, so that’s another thing to watch going forward. PSG Asset Management was down 1%. The star of the show, PSG Wealth, also happens to be the biggest division. It grew earnings 17%, with overall divisional earnings up 9%. A reduction in shares outstanding is the final piece to the puzzle that saw recurring HEPS grow 11%.

The market isn’t blind to how good this business is, with a share price of just under R15 vs. HEPS of 81.1 cents. Quality assets in South Africa trade at premium valuations, leaving earnings growth as the key driver of returns (vs. margin expansion).

Even more retrenchments at Sibanye-Stillwater (JSE: SSW)

At least there’s a silver lining at the Siphumelele shaft

Despite all the chaos at Sibanye, my recent decision to significantly reduce my average in-price has worked nicely so far. The stock is up 30% in the past 30 days. Sadly, there’s still some way to go before I can smile about this one.

Mining is a tough gig, but Sibanye seems to soak up enough bad luck for an entire industry. If it isn’t dealing with unprofitable operations or floods, the company is trying to repair damaged infrastructure.

I’ll start with the slightly good news, which is that the Siphumelele shaft damage in February 2024 has been repaired. Staff are back and are busy with start-up procedures. Production is expected to resume in May. Thankfully, there were no injuries from this incident. This shaft was set to produce 3.5% of SA PGM production this year. That may not sound like much, but every delay is problematic when PGMs prices have shown some green shoots.

We now move to the sad news, which is that the PGM price increases haven’t been enough to save the 4B shaft at the Marikana operation. It hasn’t met the profitability requirements of the s189A process that was announced in October 2023, so the shaft will be closed. The initial proposal to close the shaft was made in 2019, with subsequent initiatives keeping it going to mine more economically extractable reserves.

Many employees were set to be impacted, with the net effect reduced thanks to efforts to transfer employees. Natural attrition (employees leaving by choice) also helped. In the end, 643 employees accepted voluntary separation packages. 65 employees were retrenched. A number of contractors have also been impacted.

Sun International sells off a hotel in Lagos – well, almost (JSE: SUI)

Oddly, Sun International is left with a 6% stake in the hotel

Sun International currently owns 49.3% of TCN in Nigeria, which trades as the Federal Palace Hotel in Lagos. Sun International also manages the hotel under an operating management agreement. Nigeria isn’t a fun place to do business these days thanks to currency and other challenges, so Sun International is trying to exit the country.

There are some Hotel California vibes here, as Sun International can check out but cannot leave. Only 43.3% is being sold to Rutum Finance Company (RFC), leaving Sun International with a very odd 6% stake. I don’t think that will be easy to sell. The deal also includes 100% of the loan to TCN being sold to RFC. The real value sits in the loan ($12.675 million) vs. the equity ($1.875 million).

Sun International will receive R275 million from this transaction, with the proceeds used to reduce group debt.

TCN made an attributable adjusted headline loss of R10 million in the year ended December 2023. Sun International will no longer need to consolidate those losses (or any profits) after this deal. Not only will the proceeds be used to reduce group debt, but the change in accounting approach will take another R800 million of debt within TCN off the Sun International balance sheet.

This sounds to me like a fantastic way forward for Sun International, even if they never manage to get rid of the 6%.

Little Bites:

Share repurchases continue at Lewis (JSE: LEW), with 3.2% of share capital having been acquired since the general authority granted in October 2023. That percentage is calculated with reference to the share capital in place at the time of the general authority. The average price paid is R42.23 and the current price is R43.68.

Canal+ now holds 40.83% of the issued shares in MultiChoice (JSE: MCG), with Canal+ continuing to mop up liquidity in the market at current prices of R116 – R117.5 per share. The mandatory offer price is R125.

I don’t usually make reference to changes in institutional holdings of companies, as asset managers can adjust their positions for many different reasons. As WeBuyCars (JSE: WBC) is still new to the market though, I thought it’s worth highlighting examples of institutional support. We now know that Coronation holds a 29.75% stake in the company and Aylett & Company holds 5%, with both funds having acquired shares to reach those points.

Keep an eye on changes to JSE regulations, with the stock exchange considering a change to the current two-tiered equities market structure of the Main Board and AltX. Instead, there would be two segments called Prime and General. This would change the regulatory environment depending on size and liquidity of the issuer, which could bring more balance to the current challenges that are facing smaller listed companies.

Sun International is to dispose of 43.3% of its 49.3% equity stake and 100% of its loan account in Tourist Company of Nigeria (t/a Federal Palace Hotel) to Nigerian Rutam Finance for an aggregate cash consideration of R275 million ($14,55 million). The remaining 6% equity interest held by Sun International will be sold in due course. The transaction is in accordance with the company’s stated intention and strategy to exit its investment in Nigeria.

Following the joint announcement by Canal+ and MultiChoice which set out the terms of the mandatory offer, Canal+ has notified shareholders that it has, this week, acquired a further 18,578,131 MultiChoice shares in open/off market transactions. Canal+ now holds an aggregate of c.40.83% of the MultiChoice shares in issue. The price at which these shares have been acquired have ranged from R115.95 to R119.92, below the mandatory offer price of R125.00 per share.

Goldway Capital Investment has reminded shareholders of MC Mining in its sixth Supplementary Bidder’s Statement that its offer to acquire outstanding shares will close on 22 April 2024. Results of the offer will be announced on 29 April 2024.

Unlisted Companies

Global financial services provider Apex Group has acquired IP Management Company (IPMC). The South African unit trust management company is a collaboration between established financial services businesses which have operated unit trust funds independently for more than fifteen years, but which co-exist in a synergistic relationship within IPMC. Clients of IPMC will benefit from access to the Group’s global single-source solution which includs digital banking, fund raising, distribution and administration solutions as well as ESG rating, reporting and advisory services. In March 2023 Apex acquired Boutique Collective Investments when it announced the acquisition of local Efficient Group.

South African private equity investor Vuna Partners has acquired a 40% stake in Ferreira Fresh, a family-run fresh and frozen produce provider of fruit and vegetables with a delivery footprint covering Gauteng and extending into neighbouring provinces. Financial details were undisclosed.

M&C Saatchi Abel and the South Africa Group management is to acquire the shares owned by the UK-based global group in the local operations in a deal mooted to be in the region of £5,6 million. M&C Saatchi Plc will continue to collaborate with the South African operations, partnering with them on the African continent. Seen as a vote of confidence the deal will further accelerate the group’s transformation ownership agenda whereby the BEE shareholding value will increase by 40% in the new structure.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")