At the midpoint of 2025, the global economy stands at a precarious intersection of cooling inflation on one side and rising geopolitical tensions on the other. In this episode of No Ordinary Wednesday, Jeremy Maggs speaks with Investec Chief Economists Annabel Bishop (South Africa) and Phil Shaw (UK) about the shocks and signals shaping markets, from the Strait of Hormuz and the US tariff clock to South Africa’s subdued growth and greylisting outlook.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Beneath the waves, a silent collapse is underway. As fish stocks dwindle, so do the jobs, meals and communities built around them. But it’s not too late for us to make a meaningful change.

Somewhere off the coast of West Africa, a trawler the length of a rugby field is scraping the seafloor with a net big enough to trap a blue whale. As it progresses, the heavy chain on the bottom lip of its net levels the terrain, smashing through rocks and corals and stirring up sediment from the ocean floor. It is fishing for one particular species of fish, but it will vacuum up everything in its path, from crustaceans to rays and even dolphins or small sharks. It is estimated that up to 75% of the creatures that die in this net will be tossed back into the ocean as by-catch – caught, but not sold or consumed. Even juveniles of the desired species, too young to breed and therefore illegal to sell, are raked up and discarded.

It is probably the most indiscriminate method of hunting that exists in our world today. To fully picture this level of destruction, you would have to imagine a reality where we burn down a hectare of bushveld in order to make it easier for us to shoot three springbok. It’s hard to think that we would tolerate this level of habitat demolition and waste if we could see it happening in front of us. But industrial bottom trawling happens where we can’t see it: far from shore, at the bottom of the ocean, concealed by water.

The trawler that I’ve just described to you is one of about 4 million fishing vessels currently ploughing the world’s oceans, chasing fish faster than nature can replace them. And depending on where you live in the world, your tax money might be helping it to do just that in the form of government subsidies that bail out struggling industrial fisheries.

Fishing, in theory, is a beautiful thing. It feeds half the planet. It provides jobs for61.8 million people around the world. It supports entire coastal economies. But that’s the story you hear when the camera pans over a quaint harbour and a smiling fisherman holds up the morning’s catch. The real story – the one playing out in deep waters – is darker, messier, and deeply unsustainable.

Something fishy in the data

In 2022, the global fisheries and aquaculture industry smashed records, hauling in 223.2 million tonnes of aquatic animals and algae. It was the first time in history that farmed fish (aquaculture) outpaced wild-caught ones (capture fisheries). That sounds like a win for sustainability – more farmed fish means fewer fish taken out of the ocean, and surely that can only be a good thing, right? But take a closer look at the stats, and you’ll see where the problem lies.

We’re turning to aquaculture because we can no longer meet the demand for fish by catching them wild in the ocean. Wild fish stocks have plummeted worldwide while aquatic food consumption has grown twice as fast as the world population since the 1960s. Today, estimates suggest that the average human eats over 20kg of fish a year. 89% of aquatic animals caught or farmed go straight into our stomachs. The rest get pulverised into fishmeal or oil to feed (ironically) more farmed fish, or livestock, or even pets.

Overfishing isn’t just a buzzword for marine biologists; it’s the reality of a third of the world’s assessed fish species, which are pushed beyond their biological limits and unable to replenish fast enough. And that’s just the assessed ones. We don’t even have a full view of what’s happening in vast parts of the ocean.

Some of this overfishing is legal. A lot of it isn’t. Experts estimate illegal, unreported, and unregulated (IUU) fishing nets up to $36.4 billion a year for those willing to look the other way. That’s nearly the GDP of Ecuador, vanishing into the murky supply chains of high-value tuna, snapper, and squid. Illegal fishing often goes hand-in-hand with human rights abuses, flag hopping (when vessels change countries to dodge rules), and what insiders grimly call “fish laundering.” But the big problem isn’t just the pirates. It’s the fact that the entire system is structurally tilted toward taking more than the ocean can give.

So what about conservation?

Marine Protected Areas (MPAs) exist, but they vary widely in terms of rules and enforcement. Some allow fishing, others allow tourism, many allow both. It’s not uncommon to find MPAs that operate more like lightly managed parks than true sanctuaries. The argument for these flex arrangements is that completely banning human activity is politically difficult, especially when fishing and shipping are so deeply woven into national economies.

As of 2020, only about7.5% to 8%of the world’s oceans are under some kind of conservation status. That’s roughly 27 million square kilometres, or about the size of Russia and Canada combined. When it comes to actual no-take zones, where all fishing and exploitation are completely off the table,just 1.89%of the ocean is covered by fully protected, no-take marine reserves. That means the overwhelming majority of the ocean (including most of the areas that have a ‘protected’ label) are still open to fishing, and in some cases, even trawling.

It’s tempting to think of overfishing as an environmental issue; something that affects coral reefs and endangered turtles. Something that sits in the realm of marine biologists and blue-planet documentaries. But that’s only half the story.

Where environment meets economy

The truth is, if we collapse fish stocks, we’re not just losing biodiversity – we’re pulling the plug on an industry that supports and feeds millions of people globally. When the fish go, so do the jobs, the incomes, and the communities built around them.

Back in December 2022, over 190 countries signed on to the Kunming-Montreal Global Biodiversity Framework. The framework includes 23 targets, all aimed at halting the rapid decline of the habitats, species, and ecosystems we rely on. One target in particular, helpfully nicknamed “30×30”, has become the headline act. It calls for 30% of the world’s land, freshwater, and oceans to be effectively protected and managed by the year 2030. Emphasis on effectively, because the goal isn’t just to draw neat little borders on a map. It’s to actually make those areas safe from destruction.

The default position, in this vision, is protection. You start with the idea that 30% of the ocean should be deemed no-take zones. If any fishing is allowed around these areas at all, it should be minimal, carefully managed, and in the hands of local communities, not massive industrial fleets vacuuming up entire ecosystems for export.

Why would we do this? Because when you give marine life space to recover (meaning no boats, no nets, no interruptions), fish populations tend to bounce back. This has been demonstrated and proven across multiple existing no-take zones. And since there are no borders or fences in the ocean, these growing populations don’t just stay in their protected no-take areas. Once fish are breeding and growing in peace, their offspring start to drift outward, spilling over into surrounding waters where fishing is allowed. So even if the total area where fishing is permitted shrinks, the amount of fish being caught can actually go up.

That’s the counterintuitive magic of doing less: when we stop chasing every last fish, we get more and better fish in return. Not to mention healthier oceans, stronger food systems, and coastal economies that don’t have to live or die by whatever the trawlers left behind.

Change on a plate

We can’t treat overfishing as a niche environmental concern for scientists and scuba divers. It’s an economic time bomb. And if we want to defuse it, we need to start with accountability.

That means pushing governments to phase out harmful subsidies that reward overcapacity and destructive fishing. It means following up on progress made towards 30×30 goals and putting pressure on decision-makers where possible. It means asking uncomfortable questions about where our seafood comes from, who benefits from its trade, and who’s left paying the price. And it means using our power as consumers to support the alternatives that already exist.

In South Africa, that includes home-grown initiatives like Abalobi, a brilliant local platform that connects small-scale fishers directly to consumers, restaurants, and chefs. Every fish is traceable, responsibly caught, and fairly priced, meaning you’re supporting sustainable livelihoods and healthier oceans in one swipe. These are the choices that matter. Not everyone can control government policy, but we can all control what lands on our plates. If we want a future with fish – and with jobs, and functioning coastal economies – we have to stop treating the ocean like a bottomless buffet.

Because it isn’t. And once we’ve trawled it bare, there’s no subsidy on earth that can bring it back.

For more on this topic, be sure to watch Sir David Attenborough’s brilliant documentary Ocean.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Absa’s trading update has a positive tone (JSE: ABG)

This is better than we’ve seen from the peer group

Absa released a voluntary update for the six months ending June. There’s quite a bit of good news actually, including the favourable recent trend in African currencies and how this benefits Absa’s reported earnings.

In terms of revenue, they expect mid-single digit growth overall. As we’ve seen across the sector, non-interest revenue (NIR) is doing the heavy lifting (high single digit growth) at a time when net interest income (NII) is struggling with limited loan growth (mid-single digits) and pressure on net interest margin as rates have started coming down.

There’s a question mark around costs here, as operating expenses are up mid-single digits and the cost-to-income ratio is expected to move slightly higher. This tells us that there’s some margin pressure on pre-provision profit.

The best news in this update is that the credit loss ratio has improved from 123 basis points in the comparable period to the top end of the through-the-cycle target of 75 to 100 basis points. This has driven mid-teens earnings growth for Absa and a significant uptick in return on equity from 14.0% to 14.8%.

The balance sheet is in good shape overall and the payout ratio of around 55% is expected to be maintained.

In terms of other insights, I found it interesting that Absa noted a reduced risk appetite in personal loans. This once again speaks to the recent trend of retailers and BNPL players disrupting the banks and getting more credit into the system at point of sale. The big question is whether there’s a nasty outcome down the line in which the retailers and alternative credit providers find themselves on the wrong side of a credit bubble that the banks slowly stepped away from.

For Absa investors, as great as these numbers look, it’s important to recognise that the major growth is coming from the improvement in the credit loss ratio and they are now within their target range, so further improvements are likely to be limited.

Crookes is a reminder of how volatile the agri space is (JSE: CKS)

Bananas did the hard work here

You might find a more contentious issue in South African than “the land” – a favourite of politicians and comedians alike. The agriculture sector is an incredibly tough way to make money, with volatility based on factors that go way beyond the control of the farmers. Crookes Brothers is a rare example of this in the listed space, with a portfolio that includes sugar cane, bananas and macadamias as the major products.

Diversification is your friend here, as you’ll shortly see. Group revenue for the year ended March 2025 increased by 15% and HEPS grew by 27%. Lovely as that might sound, cash generated from operating activities fell by 28% and the dividend was 25% lower as well. This was no doubt influenced by a sharp increase in capital expenditure from R32.8 million to R81.6 million.

In sugar cane, revenue was just 1% higher and operating profit before biological asset movements was down 12%. In farming, these biological asset revaluations cause significant volatility in earnings and are an attempt to recognise what the future value of the existing crop might be. For example, the positive fair value change in sugar cane was 91% lower than the prior year! If you feel like you’ve heard of these fair value adjustments before, it might be from following a company like York Timber, where the fair value moves are always a major feature of earnings. To finish off on sugar cane, profit after the biological assets fair value move fell by 28%.

The second most important segment is bananas, where revenue was up 31% and operating profit before biological asset moves was up by a ridiculous 173%. The “going bananas” jokes write themselves. This is despite severe weather and bad storms in the Lowveld.

Over in macadamias, despite revenue increasing by 116%, there was still an operating loss before biological asset moves of -R36 million as they dealt with issues like heat damage to nuts in transit and severe damage to the macadamia factory from a storm. For context, the operating profit in bananas was around R50 million vs. sugar cane as the largest segment at R144 million.

Crookes also has a property business that grew revenue by 181% and swung from an operating loss of R8.8 million to an operating profit of R20.5 million. It says something about agriculture that the property division achieved the best margins in the group.

The outlook is negative for sugar cane prices in 2025, driven by weaker world sugar prices and higher imports into South Africa. The pricing of bananas is expected to remain favourable, so that’s bad news for anyone trying to coax their toddlers away from the sweets and towards the fruit.

Lesaka agrees to acquire Bank Zero in a major step for both companies (JSE: LSK)

Hopefully Lesaka’s stock liquidity will improve going forwards as well

Lesaka got plenty of attention on Friday morning with the announcement of the acquisition of Bank Zero. This is mostly a share-based deal, as the cash component is only R91 million and Bank Zero has been valued at R1.1 billion, so current Bank Zero shareholders will receive a stake worth around R1 billion in Lesaka (this will obviously fluctuate based on the Lesaka share price). In terms of shareholding, current Bank Zero shareholders will have 12% of the enlarged entity and will be subject to lock-ups ranging from 18 to 36 months post-completion.

Bank Zero was founded in 2018, so a vast amount of value has been created in just seven years. This is why fintech attracts so much attention, as businesses can scale quickly. As at the end of April 2025, Bank Zero had deposits of over R400 million and over 40,000 funded accounts in South Africa.

Critically, this puts a banking licence inside Lesaka’s broader fintech and distribution ecosystem. This is exciting, as Lesaka will be able to introduce new products and cross-sell across its divisions. They will also have access to cheaper funding in the form of customer deposits, thereby improving the economics of lending activities. In fact, as this is essentially a large injection of equity into the broader Lesaka group and an opportunity to significantly change the funding profile, they expect to achieve a R1 billion reduction in gross debt – and this does wonders for Lesaka’s balance sheet. Talk is cheap and implementation is what counts, but I can see why the parties are excited about this.

Importantly, Lesaka expects Bank Zero to be profitable in the first financial year after the transaction, so the deal should be accretive to shareholders from day one.

Michael Jordaan will join the Lesaka board, while Yatin Narsai will continue as CEO of Bank Zero. The full Bank Zero leadership team will remain in place.

Various regulatory conditions need to be met for the deal to be completed. In the meantime, further information will be made available when Lesaka releases results in early September. I think there will be plenty of focus on the valuation of Bank Zero, as the obvious risk here is overpaying for the asset. But if the numbers stack up, then this acquisition should improve Lesaka’s stock liquidity, as I suspect that more investors will take notice of their story.

Growth is hard to come by at PBT Group at the moment (JSE: PBG)

Can this share price regain some of its shine?

PBT Group was quite the story over the pandemic. The stock rallied from relative obscurity into the limelight, with a share price move from below R2 to over R10 (and a weird spike in the chart to over R12). Today, it’s at R5.65 and struggling to find any forward momentum, which is really just a reflection of how growth has tapered off for the company.

PBT has some of the best financial reporting you’ll find at any JSE small cap, so kudos to them for doing a great job of explaining the way in which the company makes money. Essentially, this is an IT consulting group that sells time. People are quick to dismiss this model, but there are many highly valuable consulting groups in the world. The challenge is that there is little operating leverage, with a mainly variable cost structure that is based on hiring consultants and then deploying them to clients. The key is to manage the utilisation rate in such a way that the correct margins are locked in.

The flurry of demand during the pandemic has settled down and created a challenge for PBT, with revenue growth of just 1.4% for the year ended March 2025. Operating profit was up 1.9%, but HEPS fell by 3.8% and normalised HEPS was down 0.6%. Although cash generated from operations decreased by 2.1%, the total dividend was 3.3% higher at 62 cents per share.

The business is sideways at the moment, but I must point out that the trailing dividend yield is now almost 11%, so shareholders are certainly getting paid while they wait for some capital growth.

Will Reinet let go of Pension Insurance Corporation? (JSE: RNI)

And if they do, what would they really have left?

Reinet no longer has any shares in British American Tobacco. This means that the company’s main exposure is the investment in Pension Insurance Corporation, with the rest of the investments spread across a number of funds and other assets.

We might be in for another massive move by the company, with Reinet responding to press speculation by confirming that they are in talks regarding a possible sale of Pension Insurance Corporation after being approached by a potential buyer. There’s absolutely no certainty at this point of a transaction happening, so you should treat this as a very low probability outcome at this stage.

If this does happen though, one really has to wonder whether Reinet would have a future as a listed entity. I think there would be significant shareholder pressure to just wind up the structure and return the value to investors. Ultimately, what Johann Rupert wants is what will happen. This is one to watch.

Remgro will unbundle its investment in eMedia’s subsidiary (JSE: REM | JSE: EMH)

As value unlock trades go, this one isn’t going to light up the markets – but it’s a start

Remgro trades at a persistently high discount to net asset value. As they would sooner give up their first-borns than stop paying dividends in favour of share buybacks, the only other meaningful way to try reduce the discount is to either dispose of assets and return cash to shareholders, or unbundle assets to shareholders.

The stake held by Remgro’s Venfin in eMedia Investments is literally a drop in the ocean for Remgro, but this is where they’ve decided to show some intent in reducing the discount to NAV. eMedia Investments is currently a 67.69% held subsidiary of eMedia Holdings, the local media business that is part of the broader HCI stable and responsible for far more showings of Anaconda than was ever necessary.

This deal is actually far more interesting for eMedia than it is for Remgro. You see, Venfin will initially subscribe for eMedia Holdings N shares (currently listed as an additional share class in eMedia, but with no liquidity) worth R59.5 million, so there’s a cash injection into the group. Then, Venfin wiill swap its existing 32.31% stake in eMedia Investments for more eMedia Holdings N shares, thereby giving eMeda Holdings a 100% stake in its key subsidiary. Finally, Remgro will unbundle the N shares to its shareholders, in the hope that this creates more liquidity in the stock.

To give you an idea of size, the 32.31% stake is valued at R715 million. Add in the share subscription and you have value of roughly R775 million being unbundled to Remgro holders. That’s the size of a small-cap company when viewed in isolation, but it’s less than 1% of Remgro’s R82 billion market cap. As I said, this is a more important deal for eMedia in terms of scale and liquidity than it is for Remgro.

RMB Holdings has reached the hard part of the value unlock (JSE: RMH)

And the large discount to NAV reflects this

RMB Holdings has nothing whatsoever to do with the banking group or the broader FirstRand story anymore. It’s just a legacy structure with some property assets that need to be monetised over time. The challenge is that the “easy” part is behind them, with 91% of the portfolio being the stake in Atterbury. It’s been a strained relationship with Atterbury and RMH is only a minority shareholder there, so this is far from a lucrative position to be in.

The net asset value per share is 65.8 cents and the current RMB Holdings share price is 43 cents. At a discount of 35% to NAV, the market isn’t holding its breath for this big value unlock.

The six months to March 2025 saw a 3.5% increase in the underlying NAV of Atterbury, but also an additional expected loss on the Integer shareholders’ loan (Integer is the other asset in the group). RMB Holdings isn’t even generating enough of a yield on cash to cover its operating expenses as a listed company, so they are not-so-gently eating into their remaining cash balance.

Atterbury isn’t exactly set up to be a cash cow. This isn’t a REIT, so the loan-to-value (LTV) can be much higher than what you’re used to seeing in listed REITs. Atterbury’s LTV is 62.6%, so they are looking to juice up return on equity rather than spit out dividends. There are also problematic underlying exposures, like the Newtown Precinct in Joburg which has a large vacancy rate and an overall bearish tone.

In the outlook statement, the RMB Holdings board notes that they are “circumspect” on NAV growth for the foreseeable future. They are looking at ways to unlock value, but they are sitting on a portfolio of property investments that is going to be very difficult to sell to a third party buyer. The market isn’t putting much faith in the NAV and neither am I, as this strikes me as a portfolio that will end up being sold at a significant discount to NAV.

SA Corporate Real Estate’s pre-close update flags 4% to 5% growth (JSE: SAC)

But there are more interesting insights than that

SA Corporate Real Estate has released a pre-close update for the six months to June. Don’t let the name confuse you – this isn’t an office portfolio. Ironically, they have exposure to everything other than office properties, including a large residential portfolio!

The overall story is one of 5% growth in like-for-like net property income. The distribution for the interim period is expected to be between 4% and 5% higher than the comparable period, with a similar growth rate for the full year as well. So, this is the kind of typical, steady property performance that you hope to see in the sector. The performance across the different property types is remarkably consistent: industrial +4.1%, detail +4.7% and Afhco (mainly residential) +4.7%.

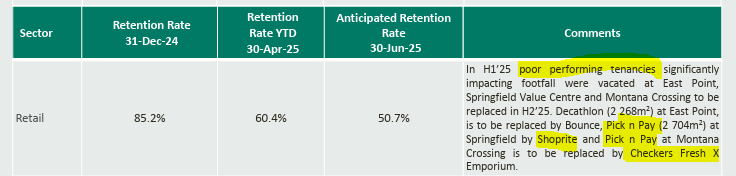

In the retail portfolio, they are running at positive reversions of 3.0% on renewals. But there’s a far more interesting insight that paints a pretty bearish picture (albeit with a very small sample size) of the turnaround at Pick n Pay:

Two “poor performing” Pick n Pays replaced by Shoprite group offerings, one in the lower income space and one as a flagship store? Good luck out there, Pick n Pay bulls. They also make reference to a Boxer replacing Pick n Pay at Umlazi Mega City and having a positive impact on trading densities. As a format, Pick n Pay just isn’t working.

The industrial portfolio is fully let and has a very small renewal base, so there isn’t much you can take from reversions that are anticipated to be 2.9% by the end of June.

The Afhco portfolio has residential and retail elements. The residential side is more interesting here, with vacancies in line with historical levels on a portfolio basis. Reversions are expected to be 2.8% for the period. They transferred 196 apartments from October 2024 to June 2025 and contracted to sell another 713 apartments. There are still 2,660 apartments that they want to sell.

The Zambian portfolio doesn’t get much attention, but I’ll just mention that the forecast is for positive reversions of 1.3% for the period (in USD).

The loan-to-value ratio has improved from 42% to 41%. Although that’s still higher than where most funds are comfortable operating, they are successfully refinancing debt and have received more favourable covenants. The weighted average debt margin has improved by 16.2 basis points vs. Decembeer 2024.

Sea Harvest is having a strong interim period (JSE: SHG)

That initial trading statement was very conservative vs. the performance they are really achieving

Whenever you see a trading statement come out with an expected increase in earnings of at least 20%, then you must keep in mind that this is the minimum level of disclosure required under JSE rules. In other words, the increase might be 20.1% or 200%, yet there is no need for the company to be more specific than “at least 20%”.

The good news is that most companies have better disclosure than that. The typical approach is to release the basic trading statement as soon as they are certain that the increase will exceed 20%, with a further trading statement released when the company has a better idea of the expected move.

This is exactly what we’ve now seen at Sea Harvest, where the initial trading statement came out on 29 May. An updated trading statement for the six months ending June reflects expected growth in HEPS of at least 60%, which is much more exciting than the initial trading statement. They attribute this to better sales price, improved catch rates and cost efficiencies in the South African business.

The words “at least” are still involved here, so the earnings increase may be even better than this trading statement has suggested. I wouldn’t assume a huge difference though, as they now have excellent visibility on this reporting period.

Nibbles:

Director dealings:

In settlement of a portion of a hedging and financing transaction, an associate of Michiel le Roux sold shares in Capitec (JSE: CPI) worth R74.8 million. The associated entity intends to implement another hedging and financing transaction, which would typically mean the use of shares as security and then a put/call structure to protect everyone involved.

Des de Beer has bought shares in Lighthouse (JSE: LTE) worth R3.2 million.

A director of a subsidiary of AVI (JSE: AVI) received share awards and sold the whole lot worth R575k.

To add to the recent selling by various ADvTECH (JSE: ADH) directors, we now have yet another example. This time, it’s a director of a tertiary education subsidiary. The sale is worth R248.5k. Either this is a lemmings off a cliff scenario, or bad news is coming.

Sean Riskowitz continues to fight a battle against illiquidity to get more Finbond (JSE: FGL) shares, with the latest purchase being for just R4.4k worth of shares.

Here’s some good news for Barloworld (JSE: BAW): they expect to meet the US Department of Commerce, Bureau of Industry and Security revised deadline of 2 September for the voluntary self-disclosure of “apparent US export control violations” – and the even better news is that investigations to date have not revealed any violations of sanctions.

The mandatory offer by Novus (JSE: NVS) to Mustek (JSE: MST) shareholders is currently open. Novus announced that they’ve picked up shares in Mustek that increased their holding from 38.60% to 39.92% (in both cases, excluding concert parties). These shares were paid for on a share-for-share basis, with Novus transferring treasury shares to the seller.

Marshall Monteagle (JSE: MMP) has pretty limited liquidity in its stock, so it only gets a mention down here on an otherwise busy day of news. It’s an odd thing really, with exposure to listed international companies, industrial property in South Africa and global financing and trading companies. Sadly, a 2% drop in revenue for the year ended March 2025 drove a horrible 62% decrease in HEPS. The state of international trade is putting pressure on the business and although they comment in the results on how strong the balance sheet is, there’s also reference to an upcoming rights offer. Ouch.

Castleview (JSE: CVW) is an R8 billion property fund with excellent underlying assets and absolutely no liquidity in its stock. Whether or not that will meaningfully change over time is debatable, as it strikes me as a pooling of strategic assets rather than a fund designed to have many shareholders. In the year ended March 2025, the net asset value increased by 9.7% to 953.94 cents. The dividend has decreased by 27% though, with a significant subscription for shares in DL Invest having taken place in the period. The loan-to-value is 46.2%, down from 48.9% in March 2024.

4Sight saw a jump in profits – even against a 14-month base period (JSE: 4SI)

But where’s the dividend?

4Sight changed its year-end from December to February in 2024, which means that the base period is the 14 months to February 2024. It’s therefore unsurprising that revenue for the 12 months to February 2025 couldn’t quite match the 14-month period, although it got pretty close. Much more impressively though, operating profit came in well ahead of that comparable period, so there’s been a clear improvement in the underlying business.

The past few years have seen explosive growth at the company. Revenue has almost doubled since 2020 and headline profit has more than tripled. The tech buzzwords are all over this thing, but the numbers are coming through as well.

Margins remain too low though, with a net profit after tax margin of 4.0% and return on equity of 11.9%. Growth is great, but these numbers will need to see significant improvement for the company to attract a premium valuation.

The thing that I don’t understand is why there’s no dividend, despite an ordinary dividend having been paid last year. Flip-flopping on dividends won’t do their valuation any favours either, as investors like consistency. Despite all the growth in the underlying business, this small cap’s share price has been flat for the past year (aside from the usual bid-offer spread choppiness that plagues illiquid stocks).

Double-digit growth at Argent Industrial (JSE: ART)

When a business has operating leverage, it means that percentage moves in revenue lead to larger percentage moves in operating profit (up or down), due to the presence of fixed costs. When there is financial leverage, percentage moves in operating profit lead to larger percentage moves in net profit (again, up or down), due to the presence of debt. So when you have both, a modest change in revenue can lead to a significant move in profits.

At Argent Industrial, revenue for the year ended March 2025 only grew by 3.6%. Operating profit was up by 8.0% and profit for the year increased by 9.7%. This suggests that the usual suspects of operating leverage and financial leverage are doing the work. But if we dig deeper, we find that profit before tax grew by 7% and profit after tax grew by 9.7%. This means that a substantial decrease in the tax rate was a major driver of earnings as well – a more unusual case of tax leverage!

To further improve the numbers, there’s a 1.8% decrease in the weighted average number of shares outstanding. This means that HEPS growth came in at a meaty 12.5% – again, this has been driven by just a 3.6% increase in revenue! The total dividend was 10.4%, so the payout ratio came down slightly but shareholders got double-digit growth nonetheless.

Argent has been pretty focused on building up the group’s international business. The latest numbers certainly reflect that trend, with flat revenue in South Africa and a drop in profit before tax of 28.6%, whereas the “other regions” segment was good for revenue growth of 7.2% and profit before tax growth of 21.9%. As a further indication of relative profitability, revenue across the two major segments is very similar, yet South Africa generated profit before tax of R102 million and other regions generated R265 million.

Growthpoint is responding to major shifts in South Africa (JSE: GRT)

The Western Cape continues to be the oasis

Growthpoint’s update for the nine months to March 2025 is a reminder of how important this year is from a strategic perspective. But before we get into that, let’s deal with the most important news: guidance for distributable income per share growth for FY25 has been improved slightly. They originally expected 1% to 3% and now they expect 2% to 3%. So, it wasn’t as bad as they thought it might be, but it also wasn’t any better than they thought it could be.

The fund is making significant changes, including a R2.8 billion asset disposal target for the year ending June 2025 of office properties (primarily B and C grade offices), as well as older industrial and manufacturing assets and properties in deteriorating CBDs. They are also getting out of motor dealerships. Essentially, Growthpoint is on a mission to improve the quality of its portfolio, rather than having broad exposure.

R2.2 billion is the targeted investment for FY25 into the core portfolio, which includes mainly logistics, industrial and retail assets. Unsurprisingly, the Western Cape is a focus. I have no doubt that their positive experience with the V&A Waterfront has influenced this decision.

Similarly, the plan in the international businesses is to be more focused on a core portfolio, rather than having such broad exposure. They are “evaluating all options” related to Globalworth Real Estate Investments and NewRiver REIT (the latter being the stake they now hold after the disposal of Capital & Regional in a share-for-share deal).

So, how did they do against the targets?

At the nine-month mark, they’ve sold and transferred R1.1 billion in assets. Since the end of March, another R445 million in disposals have been transferred. A further R1.2 billion are in process, of which around R780 million is expected to be completed by the end of June. This would take them to around R2.3 billion, which means they are R500 million off their target. That’s a decent attempt, I think. Notably, of the R1.1 billion already transferred, the total pricing was a R29.6 million discount to book value. Again, not bad at all.

In terms of development and capex spend in South Africa, they’ve invested R1.2 billion thus far. That seems to be just over half their goal, with the announcement not giving further details on that gap.

In terms of performance in the South African portfolio, vacancies improved since June 2024 but ticked up slightly from December 2024 to March 2025, mainly due to the completion of a new speculative industrial development. The lease renewal success rate has been dropping, now at only 67.4% vs. 76.3% in FY24. They seem to be standing firmer on pricing, as reversions came in at -1.0% vs. -6.0% in the prior year. Rental escalations are stable at 6.9%.

Looking deeper, the retail portfolio saw an outperformance by community centres vs. regional malls, with the total portfolio reflecting growth in footfall of 2.6% and trading density growth of 5.5%. Notably, Edgars is either reducing space or exiting malls altogether, so there is once again an Edcon-flavoured headache for landlords. Reversions are at -0.8%, improved from -2.1% in FY24, but with a dip in the renewal success rate from 86.4% in FY24 to 84.6% currently. Again, lower quality retail assets are hurting them. Conversely, the redevelopment of Bayside Mall (and it looks good, I went the other day) has led to a turnover increase of 26% at the property. An interesting move is the installation of their own fibre backbone at Bayside as a source of non-rental income for the retail portfolio and improved data.

The office sector has seen some improvement, with vacancies down from 15.1% in FY24 (and 15.9% in December 2024) to 14.7%. It seems as though vacancies have stabilised at national level. The Western Cape and KwaZulu-Natal continue to outperform Gauteng as companies try desperately to respond to the trend of where people actually want to live. Negative reversions are -3.3%, which is vastly better than -14.8% in FY24. The Western Cape is the only positive region at 3.5%.

In logistics and industrial properties, vacancies improved to 4.4% from 5.2% in FY24, although speculative developments did drive an increase in vacancies vs. December 2024. It’s fascinating that although office and retail trends are so firmly in favour of the Western Cape, the Gauteng logistics properties continue to do very well. There are of course tons of people in Gauteng, but the overall deterioration of the place means that the way they can be serviced by the likes of Growthpoint is changing. Having said that, the Western Cape is once again the only region with positive reversions in this portfolio.

It’s always worth touching on the performance at the V&A Waterfront. EBIT grew by a whopping 23% for the nine months. Here’s the really interesting thing though: on a rolling 12-month basis, visitor numbers fell by 2%. They attribute this to the rise in online grocery sales. You ignore changing consumer behaviour at your own peril.

The various international operations are all separately listed and can be referred to directly for more details. I personally find it more interesting to focus on the South African insights in the Growthpoint announcement, as they tell us something about the entire property sector in our country as well as a look-through into retail trends (like online shopping).

On the debt side, the weighted average rand cost of funding has decreased from 9.6% in FY24 to 9.1%. If you include cross-currency interest rate swaps and foreign-denominated loans, the improvement is from 7.2% to 7.1%. The swaps are the reason for a more modest improvement on that basis.

If you can believe it, this was just a summary of the insights in what was a very long and detailed nine-month update.

Hyprop enjoying higher retail sales, but footfall is flat in South Africa (JSE: HYP)

Here’s another example of the effect of eCommerce adoption

Hyprop has released an operational update for the five months to May 2025. The announcement goes into tons of detail about specific tenants, with the only really interesting point being that the reduction of space by Edgars comes up again (as it did with Growthpoint). But the good news for Hyprop is that the major reduction at Canal Walk was replaced by a premium Jet store, so all is well from a landlord perspective in that particular case.

The South African portfolio saw a 7% increase in tenant turnover for the five months to May, thanks to trading density being up 10.2%. Footfall was just 0.1% higher, with a clear trend of shoppers adopting eCommerce as an alternative. This doesn’t mean that Hyprop and its tenants can’t make money – it just means that I can’t see why footfall would grow from here.

In Eastern Europe, tenant turnover for the five months was up 3.5% and the footfall impact is even more stark, with a drop of -3.3%. Trading density rose by 4.0%. Vacancies are almost non-existent at a 0.1% vacancy rate, but I don’t like that footfall trend.

The loan-to-value ratio improved from 36.3% in December 2024 to 34.2% thanks to the capital raise in June. Note that in this case, they are quoting a metric that goes beyond the end of May. Of course, the real question is around whether they are going to have a crack at an acquisition of MAS. At this stage, they are still playing it coy, with fluffy paragraphs about why they like the idea of making a bid for MAS. At this stage though, there’s nothing concrete.

Overall, they expect to achieve the guidance for distributable income for the year ended June 2025 (an increase of 4% to 7%). But of course, having now raised loads of new capital, the growth on a per-share basis has plummeted to a range of -1% to 2%. When you’re putting out numbers like that, you can’t be out there making will-they won’t-they statements about a deal forever. There’s now a genuine cash drag on the balance sheet and a negative impact on shareholders. If they are going to do something with MAS, it needs to become clear sooner rather than later.

Schroder European Real Estate is still struggling with valuation pressures (JSE: SCD)

European office properties aren’t doing well right now

Schroder European Real Estate released its results for the six months to March 2025. It gives you a sense of how tough things are that the company is crowing about a positive total return. In other words, if you offset the dividend against the drop in the net asset value (NAV) per share, you come out slightly positive. How exciting.

Share buybacks helped achieve that outcome, so at least they are reducing the number of shares in issue at a time when capital values for the underlying properties are going the wrong way. The exception to this is the industrial portfolio, which saw an uptick in the valuation.

Another way of seeing this is that EPRA earnings before exceptional items fell from €4.3 million to €3.9 million – and if you then account for the negative valuation movements, you get to a small IFRS loss.

A further challenge they are dealing with is a fight with the French Tax Authority. Schroder has taken advice and hasn’t raised a provision at all, which is a pretty aggressive approach. We don’t often see European tax fights on the South African market, but it feels pretty unlikely that the exposure is truly zero.

Their outlook for the market isn’t exactly the most bullish thing you’ll read all day. They expect only gradual improvements in 2025, with a hope for better conditions in 2026. Their balance sheet is at least in good shape to navigate this, with the loan-to-value ratio at 18%.

Sirius wasted no time in announcing another acquisition – and a disposal! (JSE: SRE)

This comes off the back of a fresh debt facility having been raised

As I wrote when Sirius Real Estate announced a new revolving credit facility this week, you can expect plenty of deals from the group as they look to deploy equity and debt capital. The latest such example is the acquisition of a light industrial property in Geilenkirchen, Germany, for €12.9 million.

This is a sale-and-leaseback transaction with an engineering firm that entered into a triple net lease on the property, which is a structure that means that Sirius isn’t taking the risk of operating cost overruns on the property. The net initial yield on the deal is 9.3%.

Despite having so much capital that they need to deploy, Sirius couldn’t say no to the opportunity to dispose of a small non-core asset in the UK for £1.55 million. This price is a 7% premium to the most recent book value and reflects a disposal yield of 8.1%. It may be a small disposal, but this is the kind of dealmaking that gives Sirius a strong reputation among investors.

Try not to fall off your chair: Thungela has noted an improved Transnet Freight Rail performance (JSE: TGA)

It helps greatly if they can actually get their products to port

Thungela has released a pre-close update for the six months to June 2025. The most exciting news is surely the 17% year-on-year improvement in rail performance at Transnet Freight Rail. They expect further improvement in 2026. Before you get too excited about government progress here, I must remind you that industry collaborative initiatives are largely to thank for this, with the private sector stepping in to try and solve public sector problems – how utterly unusual in South Africa.

In Australia, where Thungela acquired the remaining stake in Ensham from co-investors, production and sales were negatively impacted by “challenging geology” in the first half of the year. Presumably after talking to the rocks and asking them nicely to do better, Thungela expects better production in the second half.

Coal prices unfortunately have a very bearish story to tell in 2025. Benchmark prices are sharply down in both South Africa and Australia for the five months to May 2025 vs. FY24, with decreases of 12.9% and 24.6% respectively. On top of this, the discount to the Richards Bay benchmark coal price has increased based on weak markets, so the average realised export price has actually fallen by 14.5%. In Australia, the discount has been consistent, but the benefit of fixed price contracts has meant that the average realised export price has only decreased by 11.4%. The challenge is that a portion of the price is subject to adjustments, so the final decrease will likely be slightly worse.

It really is so typical that when coal prices were high, Transnet couldn’t deliver. Now that coal prices are falling off, Transnet has improved and export saleable production increased from 6.2Mt to 6.4Mt. In terms of FOB cost per export tonne in South Africa, they expect to be marginally above the upper end of guidance for the year, as production was impacted by higher rainfall.

Those geological issues in Australia were no joke, with production at Ensham down from 2.1Mt to 1.6Mt (both on a 100% basis to avoid the effective shareholding change distorting these numbers). Unsurprisingly, lower production means that the cost per tonne will be above guidance, as fixed cost overhead recoveries take a serious knock when production decreases.

In terms of capital expenditure, they’ve put R1.1 billion into the South African business (a fairly even split of sustaining and expansionary capex), while Ensham’s capex is expected to be R127 million for the half year, with the majority of the spend coming in the second half.

With net cash of between R5.9 billion and R6.1 billion, Thungela’s balance sheet remains very strong. They need it, as the drop in coal prices has led to the share price shedding a quarter of its value over 12 months and a third over 6 months. You need a strong stomach for cyclicals:

Nibbles:

Director dealings:

Adrian Gore has put another huge hedge in place over his position in Discovery (JSE: DSY). Firstly, he had to sell shares worth R10.5 million as early settlement of the previous collar. Then, he bought puts at a strike of R215.07 per share worth R446 million and sold calls at a strike price of R297.52 per share worth R617 million. The expiry dates are in 2031. For reference, the current spot price is R211, so the puts are approximately at the money. In simpler terms, he’s locking in the current level and giving away upside above the call strike price 6 years from now.

The CEO of Pan African Resources (JSE: PAN) sold shares worth around R5 million. It’s interesting to see some profit-taking in the gold space.

A director of Vodacom’s (JSE: VOD) South African subsidiary sold shares worth almost R1.4 million.

Non-executive directors in Anglo American (JSE: AGL) were happy to receive shares in lieu of fees to the value of around R750k.

After a significant rally in Santova (JSE: SNV) and recent director buying, it’s certainly worth noting that a director of a major subsidiary of Santova has sold shares worth nearly R330k.

The chairman of Sasol (JSE: SOL) bought shares worth R82k.

Barely worth mentioning, but the size is likely due to lack of volumes rather than anything else – Sean Riskowitz has bought just R416 worth of shares in Finbond (JSE: FGL). Not R416k – R416, as in the price of grabbing some food for the family at your local burger joint.

Accelerate Property Fund (JSE: APF) is moving its listing to the General Segment of the Main Board of the JSE, giving themselves a regulatory framework that is more appropriate for where the company is in its journey. They also used this as an opportunity to remind the market that much progress has been made in the past 18 months, including a significant drop in vacancies at Fourways Mall.

Oando (JSE: OAO) has released more details on its results for the three months to March 2025. They increased volumes by 72% and have made progress on other growth projects. Margins were the story of the period though, with gross profit up 172% despite an increase in revenue of just 2%.

Mantengu Mining (JSE: MTU) issued shares worth R9.4 million to Disruptioncapital as part of the broader equity facility in place with GEM Global Yield LLC.

Eastern Trading, the majority shareholder of AH-Vest holding a 95.7% stake in the company, has made a firm intention offer to acquire the remaining ordinary share capital of AH-Vest. The consideration terms of the offer is 55 cents per share payable in cash with the aggregate consideration of R2,42 million. Prior to the offer, the share traded at 3 cents per share.

Master Drilling has increased its stake in A&R Group by a further 15% to 66% for a purchase consideration of R50,3 million to be settled in 60 equal monthly instalments. The acquisition deepens its investment in technology-enabled mining solutions. The acquisition of additional shares became effective on 1 May 2025.

Sirius Real Estate has acquired a light industrial property in Geilenkirchen, Germany, for €12,9 million, strengthening its footprint in the Euregio Maas-Rhine industrial region. As part of its ongoing UK portfolio optimisation strategy Sirius also disposed of a small non-core asset in Huddersfield to a private individual for £1,55 million.

This week Assura recommended to its shareholders to accept the revised offer from Primary Health Properties (PHP) which is higher than KKR-Stonepeak’s best and final offer of 52.1 pence. In terms of the revised offer, Assura shareholders will receive 0.3865 new PHP shares, 12.5 pence in cash, 1.68 pence in quarterly dividends and a special dividend of up to a maximum of 0.84 pence per share if the offer becomes unconditional. This implies a total value of 55 pence for each Assura share and values the group at £1,79 billion (c.R43 billion).

Unlisted Companies

Oslo-headquartered Link Mobility, a cloud communications platform has announced the acquisition of SMSPortal, a local A2P (Application-to-Person) provider. The purchase consideration of US$115 million is before conditional payment. The transaction will be settled through an upfront cash payment of $100 million, financed with cash and an equity consideration of $15 million implying a multiple of 4.6x cash EBITDA. The equity component will be settled with 5,9 million shares issued at a price of NOK26 per share.

MTN has advised shareholders of further progress made in the MTN Zakhele Futhi structure unwind. MTN has repurchased 50,590,890 shares, representing c.2.68% of the group’s issued share capital from MTNZF in full settlement of the outstanding balance of the notional vendor funding of R6,43 million. Following this c.2,48m MTN shares will remain in the structure and will be sold on the open market in due course.

The JSE has approved the transfer of the listing of Accelerate Property Fund to the General Segment of Main Board with effect from commencement of trade on 27 June 2025. The listing requirements in this segment are less onerous for the smaller cap firms.

This week the following companies announced the repurchase of shares:

In the period 21 November 2024 to 20 June 2025 Momentum repurchased 42,403,434 shares in terms of the general authority granted by shareholders in November 2024. The shares were repurchased at an average price of R31.22 at a total value of R1,32 billion.

African Rainbow Minerals has repurchased and cancelled 3,239,681 ordinary shares in a series of unrelated transactions. The average price per share paid was R154.27, representing a total consideration of R499,8 million.

In its annual financial statements released in August 2024, South32 announced that it would increase its capital management programme by US$200 million, to be returned via an on-market share buy-back. This week 720,860 shares were repurchased at an aggregate cost of A$2,07 million.

In October 2024, Anheuser-Busch InBev announced a US$2 billion share buy-back programme to be executed within the next 12 months which will result in the repurchase of c.31,7 million shares. The shares acquired will be kept as treasury shares to fulfil future share delivery commitments under the group’s stock ownership plans. During the period 16 to 20 June 2025, the group repurchased 125,000 shares for €7,71 million.

Hammerson plc continued with its programme to purchase its ordinary shares up to a maximum consideration of £140 million. The sole purpose of the buyback programme is to reduce the company’s share capital. This week the company repurchased 304,548 shares at an average price per share of 295 pence for an aggregate £897,303.

In line with its share buyback programme announced in March 2024, British American Tobacco plc this week repurchased a further 347,783 shares at an average price of £35.93 per share for an aggregate £12,49 million.

During the period 17 to 20 June 2025, Prosus repurchased a further 3,853,134 Prosus shares for an aggregate €178,62 million and Naspers, a further 321,556 Naspers shares for a total consideration of R1,69 billion.

Three companies issued profit warnings this week: Castleview Property Fund, Marshall Monteagle and Cilo Cybin.

During the week three companies issued or withdrew cautionary notices: AH-Vest, Ayo Technology Solutions and TeleMasters.

Nigerian on-demand delivery platform, Chowdeck, has acquired Mira, a point-of-sale platform specifically built for the food and hospitality industry in Africa. Terms of the deal were not disclosed.

Serengeti Energy and Kwama Energy together with four impact-oriented financiers, have partnered to develop the Ilute Solar Project located in Zambia’s Sesheke District in Western Province. Led by FMO – the Dutch Entrepreneurial Development Bank – with a US$26,5 million package, the project brings together a mix of funding from FMO, the Sustainable Energy Fund for Africa (SEFA) managed by the African Development Bank (AfDB), Triodos Investment Management and EDFI Management Company, through the EU funded Electrification Financing Initiative – Electrifi. The blended finance model weaves together commercial, development, and concessional capital to mitigate investment risks, unlocking a new way of financing renewable energy in Africa.

In May 2022, Amazon entered into an Option Agreement with EFG Holding, acquiring US$10 million of EFG Holding GDRs, with the option to convert the GDRs into a direct stake in Valu (U Consumer Finance S.A.E), equivalent to 4.255% of its share capital, upon a qualified liquidity event. Amazon has exercised the option, based on the terms and conditions of the Agreement, which will result in Amazon owning approximately 3.95% of Valu, which listed on the Egyptian Stock Exchange on 21 May 2025.

Desert Gold Ventures has entered into an option agreement with Flower Holdings SARLU to acquire a 90% interest in the Tiegba Gold Project in Côte d’Ivoire. Desert Gold will pay Flower a total of US$450,000 over the term of the agreement plus issue 1,500,000 common shares in three equal instalments.

The European Union-funded AgriFI facility, managed by EDFI Management Company, is investing c.€2,2 million (US$2,5 million) in Complete Farmer, a Ghanaian agritech company working to improve market access and productivity for smallholder farmers. The financing will contribute to the construction of six new fulfilment centres – hubs for aggregation, quality control, and logistics – with a focus on the country’s northern regions.

Shoptreo, a Nigerian e-commerce startup has secured an undisclosed round of funding from Rebel Seed Capital. Shoptreo equips local artisans with digital storefronts, integrated logistics, payments and inventory tools to efficiently meet global demand.

The Republic of Angola has become the latest sovereign shareholder in Africa Finance Corporation (AFC) with a US$184,8 million equity investment in the infrastructure solutions provider. Angola now becomes the second Lusophone African nation, after Cape Verde, to join the growing list of equity investors in AFC.

Egyptian logistics startup, Nowlun has raised an additional US$600,000 in a seed extension round led by Ingressive Capital. This follows $1,7 million raised in December 2024.

Following the 2024 disposal by Air Liquide of 12 subsidiaries across Africa [Benin, Burkina Faso, Cameroon, Congo, Ivory Coast, Gabon, Ghana, Madagascar, Mali, Democratic Republic of Congo, Senegal and Togo]to Adenia IV, Air Liquide has disposed of its Nigerian subsidiary to Oak Heir Ltd, a Nigerian family trust founded and managed by Gbotemi Kuti.

Gadaa Bank S.C. has officially listed on the Ethiopian Stock Exchange (ESX). The bank’s prospectus was approved by the Ethiopian Capital Markets Authority on 17 June 2025, and the shares were listed on 23 June. Gadaa becomes the second bank to list on the ESX.

Nigerian diversified financial services group, BAS Group, has acquired a majority stake in local fintech startup, Zuvy for an undisclosed sum.

AfricInvest has announced its successful exit from AFG Holdings, a pan-African banking group headquartered in Côte d’Ivoire. AfricInvest first invested in the group in October 2022.

BURN, a Kenyan clean cookstove manufacturer and carbon project developer, has signed an agreement with the Trade and Development Bank Group to scale access to clean cooking in Mozambique, the DRC and Zambia.

Over the past year, a wave of legislative reform has begun to reshape the legal landscape in which businesses operate. From enhanced transparency requirements and stricter compliance obligations to more streamlined regulations, these legal developments have ushered in a new era of corporate accountability, transparency and operational efficiency.

Companies Amendment Acts

In July 2024, President Cyril Ramaphosa signed the First and Second Companies Amendment Bills into law, now known as the Companies Amendment Act, 2024 (Companies Amendment Act) and the Companies Second Amendment Act, 2024 (Second Companies Amendment Act), which amend the Companies Act, 2008 (Companies Act). The most material changes introduced are those pertaining to remuneration disclosures and, from an M&A transaction perspective, the new thresholds that will trigger the requirement for private companies to comply with the Takeover Regulations and the scrutiny of the Takeover Regulation Panel (TRP) when implementing affected transactions.

Certain sections of the Companies Amendment Act and the entire Second Companies Amendment Act became effective as of 27 December 2024. Amendments that are now in force and effect include updates to AGM requirements for public and state-owned companies in terms of mandating the presentation of a social and ethics committee (SEC) report and a remuneration report, alongside SEC appointment approvals. Amendments have also been made to SEC exemption applications and membership requirements.

Further changes include adjusted timelines for amending a company’s Memorandum of Incorporation, while also addressing delayed consideration and stakeholder shareholding issues. Additionally, the legislation introduces a relaxation of approval requirements for financial assistance to subsidiaries, share buybacks and auditor appointments. Other key amendments comprise clarified definitions for employee share schemes and securities, changes to business rescue post-commencement finance, revised timelines for initiating director liability claims, and streamlined procedures for company name changes.

Sections not yet in force include those on remuneration disclosures for public and private companies; access to private company financials; removal of the right of ‘accredited entities’ to perform dispute resolution functions in favour of using the Tribunal; provisions enabling the validation of irregular share issues; obligations to publish where records are kept; and new M&A transaction thresholds requiring TRP scrutiny. It is anticipated that these changes will take effect this year.

General Laws (Anti-Money Laundering and Combating Terrorism Financing) Amendment Bill, 2024 (GLA)

The GLA proposes further amendments to the Companies Act (among other Acts), aimed at strengthening South Africa’s framework for combating financial crime and addressing the deficiencies identified by the Financial Action Task Force (FATF) as part of efforts to secure the country’s removal from the FATF grey list.

These changes propose increasing the maximum penalty for administrative fines to R10 million (up from R1 million) and empowering the Companies and Intellectual Property Commission (CIPC) to deregister a company for non-compliance with beneficial ownership, beneficial interest, security register and annual return filing requirements for any consecutive year, coupled with the imposition of administrative fines.

The GLA was published for public comment on 13 December 2024, with a submission deadline of 6 February 2025. Following public consultations, the revised GLA will be submitted to Cabinet and then to Parliament for consideration.

CIPC guidelines and opinions

The CIPC has made it clear that compliance with the new beneficial ownership, beneficial interest, and security register filing requirements – as well as annual return submissions – is of critical importance. Under pressure from the FATF, the CIPC has repeatedly warned that it will be taking a hardline stance on non-compliance. The extended deadline for meeting these filing obligations was 30 November 2024. On 31 January 2025, the CIPC began the process of deregistering non-compliant companies.

Companies that have been deregistered by the CIPC are, from a legal standpoint, prohibited from trading. Deregistration may trigger the freezing of bank accounts, potential personal liability of directors, and result in significant operational disruption. In extreme cases, the state may even absorb the deregistered company’s assets.

The scale of the CIPC’s enforcement is significant: approximately 800,000 non-compliant companies were earmarked for deregistration. Rectifying the consequences of deregistration and re-registering a company can take up to 30 working days. As a result of the widespread deregistrations, the CIPC has relaxed certain reinstatement rules. Companies in this position are strongly encouraged to seek legal advice without delay.

Other notable developments from the CIPC include new guidelines on electronic AGMs, aimed at promoting effective and meaningful shareholder participation and engagement, as well as a practice note that strengthens the qualifications and responsibilities of business rescue practitioners.

King V Code of Corporate Governance (King V Code)

The King Committee has released the draft King V Code for public comment, marking an evolution from King IV. Building on its predecessor, King V aligns more closely with recent amendments to the Companies Act and places greater emphasis on sustainability, stakeholder inclusivity and integrated thinking — anchored in values like Ubuntu.

While the King Code is not legislation, many of its practices have been incorporated into the JSE Listings Requirements, making them binding on listed companies.

South African courts have also recognised the persuasive value of King’s principles, frequently referring to them in judgments involving corporate misconduct.

Beyond the courtroom, King has influenced legislative reform and empowered civil society and activists in holding companies accountable.

King V introduces a streamlined set of principles, a stronger framework for technology and AI governance, a standardised disclosure template, and an expanded ethical mandate. As the global and local business landscapes shift in response to climate change, technological disruption, and growing demands for social equity, King V responds by reinforcing outcomes-based governance with clearer guidance — balancing prescriptiveness with the flexibility of proportionality.

JSE modernisation

The Johannesburg Stock Exchange has recently undertaken several significant initiatives aimed at modernising its regulatory framework and enhancing market accessibility. These developments reflect the JSE’s commitment to fostering a robust and investor-friendly market environment while aligning with global best practices and local legislative requirements.

New Service Issue 32 The JSE has released a revised Service Issue 32 of the JSE Listings Requirements in February 2025, incorporating consolidations of the most recent effected changes (including those pertaining to market segmentation, the rejuvenation project, the new specialist securities rules and the B-BBEE segment, each detailed below).

Dual listings The amended section 18 on Dual Listings has, among other things, collapsed the approved exchanges lists, provided for a fast track for qualification, simplified the dual listing company structure, and made provision for companies with a secondary listing – in certain circumstances – to follow compliance of a company’s primary exchange (rather than the more onerous regime) subject to new requirements.

Depository receipts (DRs) Also dealt with in the Dual Listings section, the amendments have introduced provisions differentiating between sponsored and unsponsored DRs (i.e. issuers of unsponsored DRs must be regulated under the Banks Act or an equivalent, and must demonstrate expertise. Depository responsibilities and the entity’s financial data will also need to be published).

Alignment with legislative changes The JSE is aligning its Listings Requirements with the Companies Amendment Act and the Second Companies Amendment Act. Proposed changes focus on corporate governance and remuneration policies. For example, proposed changes will remove non-binding advisory vote requirements for a company’s remuneration policy from the Listings Requirements for companies governed by the Companies Act. They also contemplate deleting aspects of schedule 14 on share incentive schemes since remuneration will be adequately covered elsewhere.

For foreign issuers, amendments propose that the non-binding advisory vote will remain, but the percentage of negative votes that trigger shareholder engagement will change. The JSE has announced that it will align the effective date of these changes with those of the corresponding provisions in the Companies Amendment Acts.

Simplification project advancements

The near final consolidated version of the new Listings Requirements pursuant to the JSE Simplification Project has now been released, with a final public consultation process currently being undertaken by the Financial Sector Conduct Authority. The last few phases of the Simplification Project have focused on streamlining pre-listing statements for Main Board issuers, while maintaining disclosure for AltX issuers and aligning with the Companies Act; and new listing criteria, simplifications for dual listings and hybrid securities clarifications. The JSE is aiming to finalise and bring the Simplification Project changes into effect in 2025.

As the corporate law framework evolves, businesses transacting in South Africa have an opportunity to address the challenges and embrace these legal and regulatory shifts. Doing so will ensure business operations and transactions are navigated in a way that is sustainable and aligned with global best practice.

Cathy Truter is Head of Knowledge Management, Ricci Hackner and Mili Soni are Knowledge and Learning Lawyers | Bowmans

This article first appeared in DealMakers, SA’s quarterly M&A publication.

Kenya’s financial landscape has long been dominated by traditional banking institutions. However, with the rise of cryptocurrencies, regulatory bodies have gradually shifted their stance. In 2015, the Central Bank of Kenya (CBK) issued a public notice warning against the use of virtual currencies, citing their unregulated status and lack of government backing. This position was echoed by the Capital Markets Authority (CMA) in 2018, which cautioned against participating in initial coin offerings (ICOs) due to the high risk of fraud and lack of investor protection. The CBK reaffirmed its position in a further notice issued in 2020.

Despite these warnings, cryptocurrency adoption among Kenyans has grown. The Kenya Revenue Authority (KRA) reported that between 2021 and 2022, cryptocurrency transactions amounted to approximately KES2,4 trillion – nearly 20% of the country’s GDP – demonstrating widespread public engagement with cryptocurrencies. The government’s recognition and acceptance of virtual currencies followed suit in 2023 when it introduced the Digital Asset Tax (DAT), imposing a 3% tax on income derived from the transfer or exchange of digital assets. This marked Kenya’s first formal approach to regulation, signalling a shift from caution to structured oversight.

However, the regulatory framework for crypto assets in Kenya remains uncertain due to the absence of specific definitions or classifications of digital assets. The CMA provides the legal foundation for securities regulation, but its definition of securities does not explicitly cover cryptocurrencies. Kenyan courts have interpreted the law more broadly in the Wiseman Talent Ventures case, where Wiseman attempted to conduct an initial coin offering of its token, KeniCoin. The court applied the U.S.-developed ‘Howey Test’ 1 to classify the offering as an investment contract, thus bringing it under the jurisdiction of the CMA. The decision emphasised consumer protection and recognised the potential mandate for the CMA to regulate the digital asset space in the absence of a legal regime.

Despite this, the Wiseman ruling did not establish a definitive classification framework for cryptocurrencies, as the court refrained from providing abstract criteria for determining when a digital token should be regulated under the CMA Act. The court also noted that the KeniCoin token bore characteristics of a currency, which would ordinarily fall under the purview of the CBK, which has an exclusive mandate over issues related to currency and payment systems. This overlapping consideration further illustrated the lack of clear boundaries between the CMA and CBK’s regulatory mandates in relation to cryptocurrency. While the judgment highlighted the court’s prioritisation of consumer protection, it also highlighted the urgent need for a clear regulatory framework for digital assets in Kenya.

IMF MARKET ANALYSIS

In December 2024, at the request of the CMA, the International Monetary Fund (IMF) conducted an analysis of cryptocurrency activity in Kenya. It highlighted the absence of cryptocurrency specific regulations, with oversight based on existing CBK and CMA mandates – an approach that was limited and not legally binding, as outlined in the Wiseman case. This regulatory gap has contributed to the rise of crypto-related scams and criminal activity. The IMF gave various recommendations, including:

Conduct a comprehensive market analysis on the state of Kenya’s crypto market and identify financial, market and consumer protection risks;

Develop crypto-specific regulations aligned with international standards through collaboration with foreign regulators, to manage risks associated with international exchanges while accommodating Kenya’s unique context to maintain financial stability; and

Strengthen cooperation across the relevant authorities, and invest in adequate technical and human resources to ensure effective oversight.

VIRTUAL ASSET SERVICE PROVIDER BILL 2025 (VASP BILL)

The Kenyan government has since embraced the sector, as seen in the draft National Policy on Virtual Assets and the VASP Bill, introduced by the Blockchain Association of Kenya in March 2024.

The VASP Bill proposes a comprehensive regulatory framework to promote financial stability, market integrity and consumer protection while addressing anti-money laundering (AML) / combating the financing of terrorism (CFT) risks. It designates the CBK and CMA as the key regulators responsible for the licensing and oversight of VASPs. Key provisions include licensing based on eligibility, financial health, cybersecurity and public interest; mandatory Know Your Client (KYC) procedures, reporting of suspicious transactions, a local presence, robust governance structures; and severe penalties for non-compliance, including up to KES10,000,000 for individuals and KES20,000,000 for entities, or ten (10) years imprisonment.

Public participation concluded on 29 January 2025, with the following feedback:

The 3% tax on the transaction amount should instead be on gains or transfer fees;

Introduce tiered licensing to accommodate multi-service providers and eliminate regulatory duplication; and

Harmonisation with international standards is required, to support cross border transactions and global competitiveness.

THE BENEFITS OF CRYPTOCURRENCY ADOPTION AND REGULATION

Regulatory oversight plays a key role in protecting investors and ensuring market integrity. The VASP Bill aims to enhance consumer protection, prevent fraud, and align Kenya with international standards. If effectively enforced, the framework could boost investor confidence, attract innovation, and position Kenya as a leading crypto investment hub.

The VASP Bill will formalise tax compliance by requiring licensed entities to report and remit the DAT, replacing the current reliance on voluntary contributions. In the financial year ending June 2024, the KRA collected KES10 billion in DAT from just 384 cryptocurrency users, highlighting the significant capacity for revenue generation for the government.

In 2024, Kenya was grey-listed by the Financial Action Task Force for inadequate measures against money laundering, terrorist financing, and unaddressed crypto-related risks. The implementation of the VASP Bill demonstrates Kenya’s commitment to strengthening its AML/CFT framework, as it provides comprehensive provisions to address these concerns.

Stablecoins are cryptocurrencies pegged to fiat currencies or commodities and offer price stability compared to traditional cryptocurrencies. A survey by Emurgo Africa revealed the growing adoption of stablecoins in sub-Saharan Africa, driven by local currency volatility and limited banking access. In Kenya, factors like inflation, currency depreciation, a strong fintech ecosystem, and widespread internet access have accelerated stablecoin use. Platforms like Binance have leveraged M-Pesa to enable stablecoin-fiat exchanges, expanding financial access in remote areas. Stablecoins are increasingly viewed as a cost-effective, reliable alternative for value storage and currency conversion, offering protection against inflation and currency instability.

IN SUMMARY

Just as M-Pesa transformed the way in which Kenyans interact with money, cryptocurrencies are set to further revolutionise the financial sector by offering decentralised, borderless and digital alternatives. With Kenya’s history of embracing technological advancements and its large, digitally literate population, the country is well-positioned to become a key player in the global cryptocurrency market. As fintech startups focused on cryptocurrency continue to penetrate the market, future collaborations between traditional banks and blockchain companies are likely, fostering a more inclusive and efficient financial ecosystem.

1.A contract which involves the investment of money or other property with the expectation of profit or gain based on the expertise, management or effort of others.

Njeri Wagacha is a Director and Wambui Kimamo a Trainee Lawyer | CDH Kenya

This article first appeared in DealMakers AFRICA, the continent’s quarterly M&A publication.

At the halfway mark in 2025, we’ve lived through some huge geopolitical shifts. The world’s gaze has shifted beyond just the US market. This opens up new opportunities of course, but finding those gems isn’t easy.

Many investors choose to stick with what they know in times like these. This means homegrown favourites on the JSE. But which stocks have been the big winners thus far this year, and what do they have in common?

In this episode, I explain how the key themes of gold, platinum and telcos have proven to be the rising tide that lifts all boats in those industries. There have also been rewards for stock-pickers beyond those sectors, with the examples of Naspers/Prosus, OUTsurance and WeBuyCars all being interesting.