There’s a lot more to blockchain technology than just the latest Bitcoin or Ether price. After the boom of NFTs and all kinds of other things during the pandemic, things clearly cooled off in this space – and for the better. In the meantime, corporates and entrepreneurs are busy in the background on tokenisation of assets to create digital assets.

In a digital economy, digital assets are important.

The Fintech space is more widely understood. But again, it goes beyond just a payments solution on your wrist or your phone. As the world becomes increasingly cashless, there’s a lot of innovation in the financial space.

To unpack these areas in more detail and to understand how use cases are developing, I was joined by Wiehann Olivier (Partner and Head of Fintech & Digital Assets at Mazars) and Mia Pieterse (Partner and Fintech Specialist at Mazars).

Mazars is an internationally integrated partnership, specialising in audit, accountancy, advisory and tax services. Operating in over 100 countries and territories around the world, they draw on the expertise of more than 50,000 professionals – 33,000 in Mazars’ integrated partnership and 17,000 via the Mazars North America Alliance – to assist clients of all sizes at every stage in their development.

To find out more about Mazars in South Africa, visit:

In the latest episode of Investec’s No Ordinary Wednesday podcast, discover the sectors that have piqued the interest of award-winning fund managers, Barry Shamley and Peter Vogel, and the factors driving their local and international investment decisions.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Schroder European Real Estate refinances a major loan (JSE: SCD)

This is a useful way to see how a cost of debt can move higher

Schroder has refinanced a €8.6 million loan with existing lender Saar LB, secured against the Rennes logistics investment. The reason I think you should pay attention is that it shows how property funds see their cost of funding increase in an environment of higher rates.

The new five year facility is a margin of 1.6% above the reference rate, which is more expensive than the 1.4% margin on the outgoing facility. The total interest cost has been fixed at 4.3% (the five year euro swap rate of 2.7% plus a 1.6% margin).

The loan to value ratio is 33% gross of cash or 24% net of cash. This is well below the limit of 35% net of cash. Total third-party debt is €82.5 million.

But here’s the kicker: this refinancing takes the blended all-in cost of debt from 2.8% to 3.0%. The company describes this as “marginal” but I don’t think 20 basis points is all that marginal in a developed market context. It just shows how the narrative has changed as those markets have started to adjust to a “new normal” of higher rates.

Southern Palladium has advanced the pre-feasibility study (JSE: SDL)

Over 30,000m of drilling has been completed

The exploration phase in mining is all about taking an asset from a mystical area of land to an operating mine. To get there, you have to do a lot of drilling and reach a level of comfort around the extent of resources in the area and the plan to mine them. This allows for further funding to be raised and the mine to eventually be built. There are many important milestones along the way and the process takes a long time.

Southern Palladium is on this journey, with much drilling work having been completed as the company moves towards completing a pre-feasibility study. The company has cash reserves of $8.34 million and thus has sufficient funding to complete this study.

Things to look out for here are a long life of mine and indicative cash costs towards the low end of the global cost curve (i.e. relative to other mines focusing on the same commodity). After all, there’s no point in building an inefficient mine!

Based on the initial capital spend estimate of $408 million, the indicative post-tax internal rate of return is 21%. I must be honest, there are many private companies in far less risky industries in South Africa that offer similar returns. It’s obviously also not possible for large institutions to invest in small private companies, so I’m not comparing apples with apples. I’m just putting that IRR in context.

The company plans to complete the pre-feasibility study by roughly December 2024.

After announcing a major acquisition, Spear REIT has given an update for the financial year (JSE: SEA)

There is modest growth in distributable income per share vs. 2023

In case you missed the news earlier in the week, Spear has agreed to acquire a substantial Western Cape portfolio from Emira for R1.146 billion. That’s a very large transaction for the group and a major step towards being a scale player in the property sector.

Hot on the heels of that news comes this update, which confirms that distributable income per share has increased by between 0.75% and 1.5% for the year ended February 2024 vs. the comparable year. That may not sound like much, but most SA-focused property funds went backwards in their latest financial year. Where we have seen significant growth, it’s been in funds with offshore exposure.

Rental reversions rates have improved significantly from -3.69% in FY23 to -0.37% in FY24, so the huge pressure on lease renewals that we saw in the post-COVID period seems to be abating. The average portfolio in-force escalation rate was 7.52% in FY24, up from 7.40% in FY23. This is how property funds offer inflation protection to investors. The industrial portfolio is a highlight here, with reversions of 6.12% and in-force escalations of 7.72%. The retail portfolio sweeps away those reversions though, with positive reversions of 11.03% and in-force escalations of 7.47%. In case you’re wondering, Pick n Pay is 1.32% of the contractual rental income of Spear.

Of course, the reversion pressure has to come from somewhere, with the office portfolio as the only remaining place where it can be. Indeed, reversions were -4.67% and occupancy levels were only 84.37%. The fund believes that this situation will improve due to demand for space in Cape Town. Time will tell.

Interestingly, 96% of the cost of diesel supplied to operate generators has been recovered from clients. Landlords have been working hard to push the cost of load shedding onto tenant income statements. The fund isn’t sitting on its hands though when it comes to solar, with various installations currently being planned and an expectation that installed capacity within the next 12 to 18 months will generate 25% of Spear’s total electricity demand.

The loan-to-value ratio was 31.60% as at the end of February 2024. Fixed debt was just under 50% of total debt, which is below the strategic target of 65% to 75% of debt to be fixed. The disposal of the Liberty building will take this down by around 600 basis points. Although the group doesn’t provide the maths at this stage, the acquisition of the Emira portfolio will surely take it higher again.

The tangible net asset value per share is R11.79 and the share price is R8.03.

The WeBuyCars listing date has been finalised (JSE: TCP)

And so has Transaction Capital’s stake in the company just before the unbundling

Transaction Capital has released a finalisation announcement for the WeBuyCars unbundling. As a shareholder in Transaction Capital, I’m certainly looking forward to seeing how both the Transaction Capital and WeBuyCars share prices will behave.

The big day is Tuesday 16th April, as I’ll then see WeBuyCars in my brokerage account as a separately listed company.

Importantly, Transaction Capital has also announced that the stake in WeBuyCars after the various capital raising initiatives is 61.44%. They were hoping to raise some more capital from placing shares but I felt that their pricing was unrealistic and the market seemed to take the same view. This ship has sailed now, as the 61.44% holding will be unbundled to Transaction Capital shareholders.

Exciting times ahead to see what happens here. We have a classic case of the market darling (WeBuyCars) and the ugly duckling left behind (Transaction Capital). This is where growth and value investors tend to sort themselves into two orderly queues on either side of the room.

Woolworths is ready for your furry friends (JSE: WHL)

The group is now the proud owner of Absolute Pets

People spend a lot of money on their pets. This we know to be true. Retailers want to tap into this of course, especially where consumers are buying from specialist pet stores rather than the pet food aisle at the local supermarket.

I don’t think it would make much sense for Woolworths to allocate a bigger portion of their already compact Woolworths Food stores to pet food. I think it makes a lot of sense to rather acquire a specialist, which is exactly what they’ve done with the acquisition of 93.45% of Absolute Pets.

In case you’re wondering, the remaining shares are held by management and can be acquired by Woolworths over an agreed period.

The deal was previously announced, so the latest news is that all suspensive conditions have been met (including Competition Tribunal approval) and the deal closed with effect from 1 April 2024.

Organic vegan dog biscuits, anyone?

Little Bites:

Director dealings:

A person associated with the CFO of Primary Health Properties (JSE: PHP) has bought shares worth just under £20k.

If I understand the announcement correctly, then Prosus (JSE: PRX) director Steve Pacak has sold shares worth around €14.5 million – half in his own name and half in a trust.

The MC Mining (JSE: MCZ) – Goldway battle rages on. The board of MC Mining has now responded to Goldway’s Fourth Supplementary Bidder’s Statement. For those who enjoy a robust debate (like I do), it’s quite a thing to have read all these announcements in detail. Goldway’s recent approach was to try and discredit the Independent Expert’s report and MC Mining has obviously hit back sternly against that strategy. There is also much fighting over the status of Vele Aluwani Colliery. The independent board remains steadfast in its view that shareholders should not accept the offer.

Salungano (JSE: SLG) has released an update on the business rescue application for Keaton Mining. The courts were having none of it, dismissing the application. Salungano plans to appeal the judgment. Keaton comprises the operations of Vanggatfontein Colliery (a most unfortunate name) and is unrelated to Salungano’s main revenue generated options at Moabsvelden Colliery.

Lighthouse Properties (JSE: LTE) announced that the acquisition of H2O Centro Comercial in Spain has been completed with an effective date of 3 April 2024.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

African Rainbow Minerals to take a 15% stake in Surge Copper Corp (JSE: ARI)

Surge Copper is listed on the TSX Venture Exchange

From time to time, listed companies invest in other listed companies. This can be for portfolio diversification or more strategic reasons. In this case, African Rainbow Minerals has invested in a 15% stake in Surge Copper Corp, which is listed on a couple of exchanges including the Venture Exchange on the TSX (Toronto).

The subscription price works to an 18% premium to the 20-day VWAP. Before you panic, this isn’t very unusual. To build a 15% stake through on-market buying would inevitably be even more expensive, as the price would run higher in the process.

This looks like an early-stage mining group that owns the Berg Project, which has a Preliminary Economic Assessment showing an IRR of 20% (that’s in Canadian Dollars) based on copper, molybdenum, silver and gold resources. The company also has a 100% interest in the Ootsa Property, an exploration project which has similar resources.

This gives African Rainbow Minerals exposure to low-carbon energy transition metals.

At BHP, Blackwater has been bought by Whitehaven (JSE: BHG)

Clearly, names related to colours are in!

BHP Group and Mitsubishi Development each owned a 50% stake in a joint venture that in turn held the Blackwater and Duania mines. Whitehaven Coal has now paid $2 billion in cash to acquire those mines. There’s a preliminary adjustment of a further $44.1 million to be received from the buyer. A $100 million deposit was already received in October 2023.

On top of this, $1.1 billion is payable by Whitehaven over three years, with a potential further $900 million in a price-linked earnout structure. The earn-out is a maximum of $350 million each year for three years, with a cap of $900 million overall.

The total cash consideration for the deal is thus up to $4.1 billion, plus the completion adjustment amount of an estimated $44.1 million. Half of the net proceeds would be attributable to BHP.

Calgro M3 locks in Bankenveld District City (JSE: CGR)

This is a major boost to the development pipeline

First off: where on earth is Bankenveld District City? I’m hoping this video I found on YouTube is an accurate representation of what they are actually building, but at the very least it gives you an idea:

Calgro M3 is entering into a joint venture with Eris Property Group to acquire a strategic land parcel that will deliver between 20,000 and 30,000 housing units alongside commercial, retail and industrial spaces. That’s a huge opportunity. Calgro M3 and Eris will share the cost of the infrastructure installation (34% of the land), whereafter Calgro M3 will do the residential development and Eris will develop the rest.

Clever, isn’t it?

As at August 2023, the project pipeline at Calgro M3 was 20,239 units. This deal therefore more than doubles the project pipeline, with more than R18 billion in potential revenue. Goodness knows it’s easier said than done to do developments like these, but it’s a very interesting strategic step.

One wonders what the impact will be on capital allocation, as Calgro M3 has been active with share buybacks at a time when the share price has been cheap. It’s still at a modest valuation multiple, but more capital will presumably be applied towards this development now.

The share price closed 3% higher on the day.

Emira sells a Western Cape portfolio to Spear REIT (JSE: EMI | JSE: SEA)

Emira is reducing debt and Spear is growing at pace

The beauty of a market is that there is a buyer and seller for every asset. This means that someone can think of reasons to sell it and someone else can find reasons to buy it. Sometimes, it’s because of different plans with the assets. Other times, it has more to do with the different stages of business and strategic priorities.

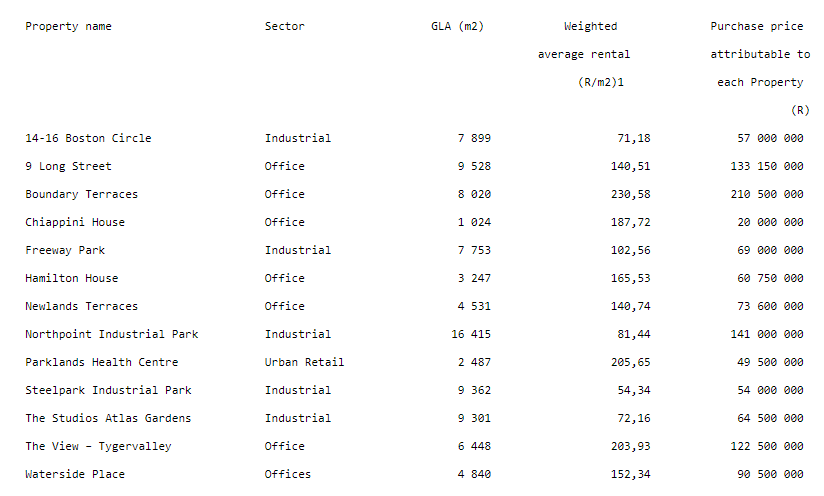

In this case, Emira is selling a portfolio of 13 properties in the Western Cape to Spear REIT for R1.146 billion. Spear is focused exclusively on the Western Cape and this is a pretty spectacular way to beef up the portfolio in one big deal. Emira is looking to recycle capital and reduce debt, which makes sense based on what I saw in their results last week.

In a particularly interesting twist, Emira is paying a transaction fee of R22.5 million to Spear that the latter can use at its discretion. Another fun term is that if Emira wants to incur capital expenditure on any of the properties prior to transfer, this can be done with Spear’s consent and with the understanding that Spear will refund Emira up to R15 million for such expenditure.

As you can imagine, there are many other property-specific terms in a deal like this, not all of which are worth highlighting here.

Here’s the portfolio:

The companies have confirmed that these values are in line with the fair market value as determined by the directors.

In the Spear announcement (which is a Category 1 deal announcement), the company notes that the acquisition price is a net operating income yield of 9.46% excluding the transaction fee payable by Emira to Spear. Including this amount would take the net initial yield to 10.1%. Given that’s a once-off amount, I would personally focus on the former number, not least of all because Spear will also incur once-off expenses for the deal.

One of the conditions to the deal is that at least 50% of the purchase price will be funded by mortgage bonds that can be raised over the properties. These approvals have been granted in principle.

If you are a shareholder in Castleview (JSE: CVW) then remember this deal is also relevant to you, as Castleview is the 59.3% shareholder in Emira.

Salares Norte commences production at Gold Fields (JSE: GFI)

This has been a 13-year journey

Gold Fields announced that Salares Norte has commenced production and delivered first gold, in line with the updated project schedule that was shared with the market in December 2023. The payback period is less than three years at current gold prices, which would be a wonderful return on investment if the good times continue.

The journey from discovery through to exploration, development and now commencement of production took a whopping 13 years. Mining isn’t a quick process, although companies obviously choose to delay or accelerate projects based on market conditions and availability of capital.

The all-in cost of gold production is $1,790 to $1,850 for 2024 and expected production volumes are 580koz. This gives it one of the industry’s lower cost profiles. The total capital cost was between $1.18 billion and $1.2 billion.

The rest of the group has a less enjoyable story to tell, with group production for the first quarter of 2024 coming in lower than planned. This was impacted by operational challenges at South Deep (a fatality on 2 January 2024 and many other far less serious issues) as well as severe weather conditions in Australia and Peru.

For now though, the company has left production and cost guidance unchanged for 2024.

Invicta: getting its bearings (JSE: IVT)

Or more bearings, I should say – as this is a familiar product category for the industrials group

Invicta has agreed to acquire 100% of Nationwide Bearing Company (NWB) in Doncaster, South Yorkshire in the United Kingdom. Invicta has tons of experience with bearings in South Africa, so this feels like a good fit.

NWB has been around since 1992 and has its own developed brand as well, with the products developed internally and manufactured by outsourced partners across the world. Invicta believes that it can add value in the supply chain here, using its scale to help source inventory.

The effective date was on 1 April. No, this isn’t a joke, especially not when R293 million is changing hands. There is the potential for the final price to be adjusted based on how the net asset value of NWB changes, to a maximum adjustment of £34,000 (and thus small in the greater scheme of the deal).

The purchase consideration is heavily front-loaded (£9.9 million), with two major deferred payments 6 months and 12 months after completion of the deal. The adjustment amount is payable 55 business days after the completion date.

The total purchase consideration is £12.355 million and the net asset value (NAV) of the entity was £8.7 million as at March 2023. Based on the adjustment for net asset value, it seems the NAV may be up to £10.2 million by completion date. Either way, it’s a premium to NAV. Profit for the year ended March 2023 (which is now a full year out of date) was £1.395 million. It’s a pity that profits for the year ended March 2024 aren’t given in the announcement.

Little Bites:

Director dealings:

The CEO of Trellidor (JSE: TRL) has bought shares worth R137k. With a share price down 42% over the past year, that’s interesting.

Fortress Real Estate (JSE: FFB) announced that the scrip distribution will be at a 5% discount to the 5-day VWAP, which means a shareholder can elect to receive 5.77205 new Fortress B shares for every 100 shares held. The cash dividend is 81.44308 cents.

Lighthouse Properties (JSE: LTE) has announced a scrip distribution reference price that is a 3% discount to the closing spot price on 28 March 2024. Shareholders can either receive a gross cash dividend of 27.69614 ZAR cents per share, or 3.67803 new Lighthouse shares for every 100 Lighthouse shares held.

After a review of Pepkor’s (JSE: PPH) credit rating, Moody’s has left the credit ratings and stable outlook unchanged. This is based on Pepkor’s resilient business model, while recognising the risks of South Africa. I must remind you that a credit assessment is a completely different lens to an equity investment, so see this more as some downside reassurance rather than upside potential.

MultiChoice (JSE: MCG) has agreed with Imtiaz Patel that he will extend his tenure as Chair until the conclusion of the Canal+ transaction, or a sooner date depending on how the deal goes. Elias Masilela will become the Deputy Chair.

Trustco (JSE: TTO) has withdrawn the announcements previously released about the terms of the related party transaction with Next. This is because material terms have changed in subsequent negotiations. The company will release a further announcement when appropriate.

aReit (JSE: APO) has declared a dividend of 33 cents per share for the year ended December 2023. I just can’t help but wonder where the financial results are, as I can’t recall seeing another example of a dividend announcement without the accompanying results.

Oando (JSE: OAO) has been suspended from trading on the JSE based on the inability to meet the extended deadline to publish the 2022 year-end results. The company believes that it is close to completion on these, with the board scheduled to approve before 15 April.

Nico Katzke of Satrix* returns to Ghost Stories to talk about the latest buzzword of the moment: Artificial Intelligence (AI). This topic has been dominating market headlines for a while now and it poses both opportunities and risks.

In this podcast, we discuss:

The way in which some people run towards hype and others run in the opposite direction – talking to the different investor personalities in the market.

Whether the development of cloud computing and SaaS can teach us anything about the risk of being too sceptical about AI.

The energy demands of AI and what this could mean for renewable energy.

What AI technology is and what it is not – and why the term may well be an example of great marketing more than anything else.

Our preferred ways to get exposure to this theme in our portfolios.

There’s so much in here, underpinned by Satrix’s commitment to South African investor education. To find out more about SatrixNOW, visit this link>>>

*Satrix is a division of Sanlam Investment Management

(this article was first published on Satrix’s podcast platform here)

Disclosure

Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this podcast (“the information”), the FSP’s, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

No, you’re not imagining it: Taylor Swift really is everywhere right now. From radio airwaves to streaming services, social media to news outlets and now even the sidelines of football fields, there genuinely is no escaping her presence. But with one artist dominating public attention (and spending) to this degree, is there space left for anyone else?

You don’t have to like Taylor Swift or her music to be able to appreciate that she is currently the poster child for winner-takes-most economics. To give you some perspective on her dominance, consider this stat: in 2023, 1 in every 78 US-based audio streams was a Taylor Swift song. Keep in mind that streaming is based on the choice of the listener, not the radio DJ forced to play the latest pop.

She claimed 1.28% of the US streaming market in 2023, which doesn’t sound that impressive until you consider that entire genres of music like Classical and Jazz only made up 0.8% and 0.9% respectively. Even the Children’s streaming genre, fueled by parents having to play Baby Shark 15 times a day to placate their demanding toddlers, could only claim 1.1% of the total streaming market.

So yes, Tay-Tay is doing just fine, thank you very much. But what is it about her and her music that has singled her out from millions of professional musicians worldwide – not to mention every amateur garage-band, viral talent-show contestant and high-school virtuoso in the world? Why do some musicians get a minute in the limelight, while Taylor Swift gets almost two decades?

What makes her the Microsoft of Musicians?

One of a million girls next door

Almost anything or anyone has the potential to evolve into a brand – like a blonde, guitar-playing American girl. Just like household brands Nike and Google, Taylor Swift’s brand strength is the result of smart marketing and knowing how to sell a product.

To be fair, her backstory definitely helped to shape the lore: after growing up on a Christmas tree farm (yes, really) in Pennsylvania, a 13-year-old Swift expressed an interest in country music and subsequently became the catalyst for her entire family moving to Nashville to get her closer to the wellspring of the genre. She describes one of her earliest introductions to music as hearing her opera-singer grandmother singing in church (cue the beam of golden light coming through the stained glass window). The fact that her entire childhood sounds like a Hallmark movie waiting to happen is only underlined by the fact that Taylor Alison Swift is her real name, even though it sounds exactly like the kind of pretty pseudonym a pop princess would choose.

So she’s pretty, talented and she has an interesting backstory – but then again, so do hundreds of other musicians. This brings us back to the original question of Taylor’s rocket-fuelled career.

Taylor currently occupies one of the top positions in music, which is a career avenue notorious for its winner-takes-most approach. In a winner-takes-most market, the top performers seize a significant portion of the available rewards, leaving little for the rest of the competitors. This dynamic exacerbates wealth disparities, as a small elite accrues a growing share of income that would otherwise benefit a broader segment of the population.

Then there’s also the Matthew Effect to consider. No, Matthew isn’t one of Taylor’s many prominent exes – the Matthew Effect is the tendency of individuals to accrue social or economic success in proportion to their initial level of popularity, friends, and wealth. The term was coined by sociologists Robert K. Merton and Harriet Zuckerman in 1968. This phenomenon can be primarily attributed to preferential attachment, where wealth or credit is allocated based on existing holdings.

In other words, according to the Matthew Effect, lower-ranked individuals face escalating challenges in augmenting their assets due to limited resources to invest over time. Conversely, higher-ranked individuals find it easier to maintain their substantial holdings because they possess greater resources to invest.

That sounds a bit like Taylor’s reign, doesn’t it? She accumulates new fans through a fiercely loyal existing fanbase, and she is able to pour almost endless resources into extravagant tours, album launches and more. Newer or lesser-known musicians face a much steeper uphill battle to getting an album sold than Taylor does, in the same way that a locally-made sport shoe brand would have a hard time competing with Nike.

In her money Era

As of October 2023, Taylor Swift is the first billionaire in history to have accumulated their fortune solely from a career as a musician.

She has released a new album every two years since 2006 (with the exception of Reputation, which was released three years after its predecessor, 1989). She doubled down during the pandemic, which is why 2020 saw the release of two “sister albums”, Folklore and Evermore, in the same year.

This excludes the “Taylor’s Version” albums, which are four of her early albums that she re-recorded between 2021 and 2023 in order to own her masters, following a dispute over ownership with record label Big Machine Records in 2019. Six of her 14 albums have opened with over one million sales in the first week. What’s that quote from Steve Jobs about real artists shipping?

With that much material to draw from, it makes sense that Taylor was able to create one of the biggest retrospective shows in the history of live performance in the form of her Eras Tour. Spanning 152 shows across five continents, the tour kicked off on March 17, 2023, in Glendale, Arizona, United States, and is scheduled to wrap up on December 8, 2024, in Vancouver, Canada. Though currently only halfway, the Eras Tour has already left an indelible mark on global culture, achieving the milestone of surpassing $1 billion in revenue, thus solidifying its status as the highest-grossing tour in history.

The Microsoft of Musicians

When we see a business like Nike at the top of its industry, we are quick to recall its humble beginnings in Phil Knight’s garage, and just as quick to applaud the hard work, strategic prowess and marketing successes that allowed it to ascend to its position. When we talk about Microsoft, we are impressed by the consistent evolution of the company to stay at the very top of its game. But for some reason, when we see remarkable success in a single person, we want to start talking about luck, chance and having “it”.

The key to understanding Taylor Swift’s success is to think of her as a business, not a person. There is no magic stick that selected Taylor Swift as the artist of the century, thereby distinguishing her from every other guitar-playing girl to ever come out of Nashville. Just like Phil Knight took a risk when he imported that first batch of Onitsuka Tigers into the United States, Taylor’s parents took a risk by moving their family to another state in order to support her interest in music. Just as the team at Nike grew their operation through smart partnerships with suppliers and distributors, Taylor connected with agents, record labels, writers and engineers who aligned with her vision and the unique sound she wanted to produce.

Yes, it may be true that there isn’t much space at the top of the music market, and Taylor’s massive success thus far is certainly helping to bring in new opportunities on a regular basis. But let’s not gloss over the fact that she climbed this ladder through regular album releases, clever marketing, and an extremely well-managed brand.

A nice name and a cute backstory will get you a head start in the music industry. But just like everywhere else, the ones right at the top are the ones who work the hardest off the initial platform of luck.

About the author:

Dominique Olivier is a fine arts graduate who recently learnt what HEPS means.Although she’s really enjoying learning about the markets, she still doesn’t regret studying art instead.

She brings her love of storytelling and trivia to Ghost Mail, with The Finance Ghost adding a sprinkling of investment knowledge to her work.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Ascendis swings sharply into the green (JSE: ASC)

You do need to read carefully for the once-offs though

Revenue at Ascendis may be down 5% for the six months to December 2023, but that’s where the bad news stops. Gross profit margin increased by 150 basis points to 40.9% and significant cost-cutting efforts have paid off, with a substantial drop in operating costs across the board. Without adjusting for once-offs, operating profit came in at R47.6 million vs. a loss of R122 million in the comparable period.

That’s quite the swing, isn’t it?

The group goes on to explain that there were major line items like a VAT provision reversal of R43.1 million and an accounting gain of R27.1 million. There were also various transaction costs and impairments. On an adjusted basis, operating profit was R8.9 million vs. a loss of R47 million in the comparative period.

Interest paid was R5.1 million, vastly less than R50.5 million in the comparable period after all the progress was made in reducing debt on the balance sheet.

Remember, Ascendis is currently at the centre of what became a controversial potential take-private transaction. This is being spearheaded by the current CEO, which is relevant information when there’s commentary in the announcement that the company may look to raise further equity from shareholders to enable growth. This suggests that if the take-private doesn’t go ahead, the group may look to equity funding mechanisms on the public market. Some will heed this warning and others may see it as a strategy to encourage the delisting.

Either way, aside from the extensive noise around the potential deal, it’s clear that things have improved significantly at Ascendis from an operational standpoint. The group is profitable, albeit not by much once you look at the adjustments.

Dividend disappointment at Bell Equipment (JSE: BEL)

HEPS up strongly, yet the dividend has disappeared

After a couple of trading statements, there’s been much excitement around Bell Equipment. With the release of annual results though and the disappointing news of no dividend at all, the share price closed around 10% lower on the day.

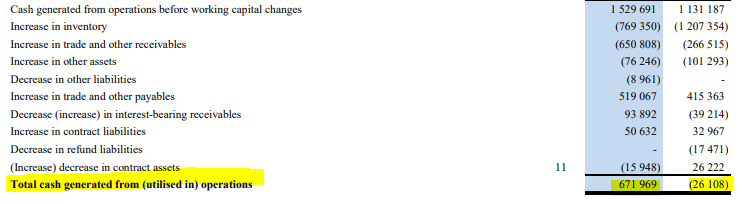

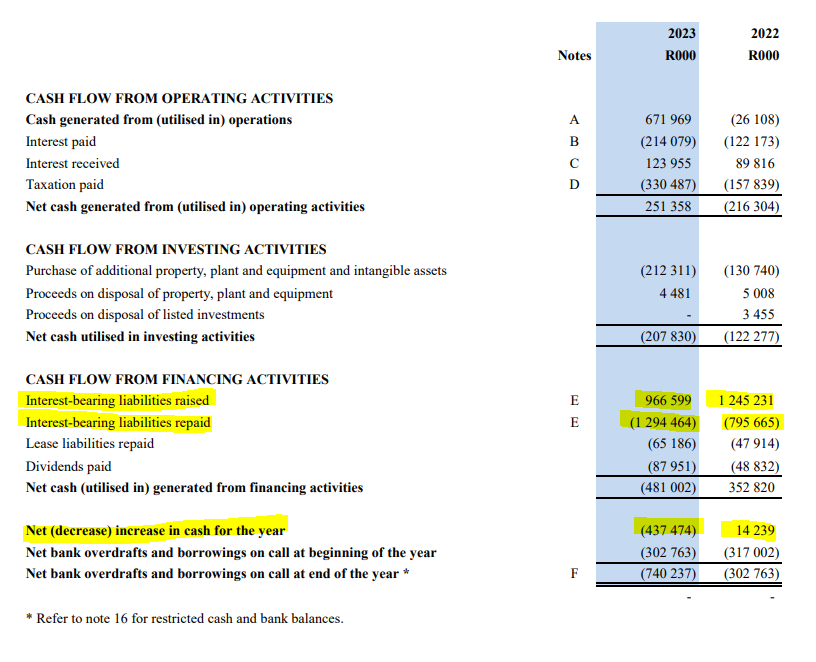

A revenue increase of 32% drove a HEPS improvement of 69%. The cash flow tells an incredibly different story though, with a massive cash outflow of R437 million for the year vs. an inflow of R14 million in the prior year.

You may assume that this is related to working capital, but a deeper look reveals that this isn’t the case. You’ll find that cash generated from operations actually looked just fine thanks (with 2023 in dark blue):

The biggest swing in cash actually happened in financing activities, shown here:

The company notes that working capital investment across inventory and receivables is the primary reason why the dividend is gone. That’s a forward looking view of where the cash might go in the coming year. Based on the financials, a contributing factor to why the dividend disappeared seems to be more related to the longer term debt on the balance sheet rather than working capital.

Emira sells two properties (JSE: EMI)

Makro Crown Mines and Market Square in Plett have been sold in separate deals

Emira has decided to recycle capital by selling two properties. The first is Makro Crown Mines, disposed of for R337.5 million. The second is Market Square in Plettenberg Bay, sold for R354 million. These are two separate deals with different buyers.

The net operating income for Makro Crown Mines for the six months ended September 2023 was R14.98 million. On an annualised basis, the property has been sold on a yield of 8.9%. Market Square’s net operating income over the same period is R12.4 million, implying an annualised yield of just under 7%.

The net proceeds will be used to reduce Emira’s debt and fund new acquisitions once opportunities are identified.

In a separate update, Emira gave investors a pre-close view for the 11 months to February 2024. The overall story is that the local commercial portfolio is performing in line with expectations. It’s rather interesting to note that retail vacancies increase from 3.2% at September 2023 to 4.1% at the end of February, whereas office vacancies actually improved from 12.0% to 11.3%! For completeness, the industrial portfolio improved marginally from 0.7% to 0.6%.

Moving on to residential, this was an important period for the company as the takeover of Transcend was completed. 486 units in the residential portfolio have been disposed of during the period at a small premium to book value. A further 74 units should transfer by the end of March.

In the US-based portfolio, vacancies increased from 3.6% to 4.7%. There are some larger tenant failures that have negatively impacted results.

The loan-to-value ratio of 43.7% as at the end of February is up from 41.2% at the end of September, with the increase driven by the acquisition of the remaining shares in Transcend. That does feel a bit high to me in this environment, with the firm continuing to recycle capital and diversify the fund. Perhaps some of that capital will be used to bring debt down.

Heriot took a knock from financing costs (JSE: HET)

The distribution per share has fallen for the interim period

Property fund Heriot reported a 4.2% decrease in the distribution per share for the six months to December 2023. This is despite a 12.9% increase in net property operating income. Property funds have been hit hard by the rising interest rates, with Heriot as just one of many examples.

The retail portfolio has been the biggest source of growth, with net operating income up by a very impressive 21.2%. The Industrial property increased by 9.9%. Office and residential assets have a less pleasing story to tell. Luckily, 71% of the portfolio is retail and 19% is industrial.

Heriot is looking to increase exposure to Safari Investments, with a 48.7% direct interest and a further 10.1% held by a concert party, Thibault REIT.

The net asset value per share at Heriot increased by 21.3% from R13.02 to R15.78. The share price is R13.50.

Renergen gives a quarterly update (JSE: REN)

There’s nothing new here, but it’s still a useful summary of the past three months

Renergen releases a quarterly update to give investors a summary on the latest strategic news and the state of the financials. The fourth quarter of the 2024 financial year can count the Mahlako Gas Energy investment as the major highlight, with that party putting in R550 million for a 5.5% equity stake in the South African operating entity. The investment by Airsol has also been completed.

Although LNG deliveries resumed in February, it’s the production of helium that investors are really waiting for. The helium system integration is nearly complete, with no significant issues detected. The OEM supplier is busy with pre-checks ahead of the final performance test.

Whatever the outcome of that test, I would expect a pretty big share price move either up or down, depending on the results.

RMB Holdings finds a way to exit Divercity Urban (JSE: RMH)

The group is trying to turn assets into cash – and some aren’t as easy as others

Trying to sell a tiny stake in a private company really isn’t easy. This is generally why listed groups avoid holding such stakes in the first place. RMB Holdings is trying to turn assets into cash as part of the strategy to return value to shareholders. On more strategic holdings, it’s a lot easier. For the 7.15% stake in Divercity Urban, there probably weren’t many buyers in town.

This is why RMB Holdings has agreed to the company repurchasing shares and shareholder loan claims held in and against Divercity. The company is loss-making, so RMB Holdings didn’t get a great price here. The carrying value of Divercity in RMB Holdings’ accounts as at 30 September 2023 was R87 million. In that period, there was a fair value loss of R9.8 million. The price for this repurchase is only R50 million, so that’s a long way down from the September carrying value.

This will in all likelihood lead to another special dividend to RMB Holdings shareholders once the deal is completed.

Workforce suffered major headline losses (JSE: WKF)

This is despite an increase in revenue

Revenue at Workforce Holdings increased by 4% for the year ended December 2023. Despite this, EBITDA came down sharply from R201.1 million to R151.3 million off a revenue base of R4.5 billion. Those are very skinny margins indeed.

It looks much worse at HEPS level, with a drop from 46.8 cents to a headline loss of 13.3 cents per share. There’s no final dividend, which is to be expected when there are losses.

The revenue increase was simply no match for margin erosion and increases in overheads. The company put steps in place to reduce costs, but they were only completed by September 2023. This suggests that a more palatable 2024 may be on the cards.

In general, a low margin company in a volatile market like South Africa is always going to be a rollercoaster.

At York, the assets go up in value and HEPS comes down (JSE: YRK)

The share price has been on a steady slide since 2022

York Timber has released results for the six months to December 2023. Revenue fell 2% and cash generated from operations was down R111 million, so it was another difficult period for the group. HEPS fell sharply from 13.27 cents to 4.67 cents. Core earnings per share deteriorated from a loss of 2.62 cents to 10.06 cents.

Despite the financial performance dropping faster than the trees being cut down for processing, the biological asset value increased by 5%. It strikes me as such a theoretical concept, as we can quite clearly see that extracting value from the trees is far harder than the valuation would otherwise suggest.

There’s no dividend for this interim period, just like in the last period as well.

The outlook isn’t a source of encouragement either, with York noting that the lumber market is expected to remain weak in terms of demand and pricing.

Little Bites:

Director dealings:

With the share price at Quantum Foods (JSE: QFH) continuing to run amok from speculation (now up to R13.50), the company announced that director Hendrik Lourens has agreed to buy shares worth R1.26 million for either R9.00 or R10.00 depending on which tranche you look at. Director Wouter Hanekom, acting through an associate, bought R1.7 million worth of shares at R10 per share.

Following the release of the annual results, the chairman of Kore Potash (JSE: KP2) will subscribe for shares worth $150k. In those results, the company confirmed that it is still targeting the signing of full EPC documentation in Q2 2024, with funding required to help the company reach that point.

If you’re closely following the MC Mining (JSE: MCZ) offer by Goldway and all the to-and-fro with the independent board, then you’ll want to check out the fourth supplementary bidder’s statement released by Goldway. They are focusing on trying to discredit the work of the independent expert here, which of course underpins the board’s decision to recommend that shareholders do not accept the offer. There’s far too much detail to go into here. If you hold shares in MC Mining, you need to read everything carefully.

Jubilee Metals (JSE: JBL) released an update on its copper projects and expansion of chrome operations. On the copper side, International Resources Holding in Abu Dhabi has exercised its right to proceed with the formation of the joint venture for the implementation of the Waste Rock Project. At the Roan Project, ramp-up is expected to commence in April 2024. At Project Munkoyo, initial deliveries of copper ore to the Sable Refinery are expected in September 2024. Moving to local chrome and PGMs, the chrome tolling agreements have been extended to February 2027 and the construction of Thutse’s second chrome processing module is on track to commence in August 2024.

Zeder (JSE: ZED) has appointed PSG Capital and Rabobank as co-advisors to consider any approaches from third parties regarding the investment in Zaad Holdings. This may or may not lead to a formal process to find a buyer. Zeder also confirmed that third parties have made approaches regarding the Pome Division that was excluded from the disposal of Capespan.

enX (JSE: ENX) announced that the urgent application by Inhlanhla Ventures to try and interdict the general meeting for the disposal of Eqstra has been withdrawn. This means that the meeting will go ahead on 3 April as planned.

Europa Metals (JSE: EUZ) released results for the six months to December 2023. As this is a resource development company, it shouldn’t really shock you that there are net losses. They came in at A$248k, which is a lot better than A$1.2 million in the comparable period. The company is developing the Toral project in Spain. Of critical important is the funding arrangement with Denarius, which gives that company the option to acquire up to 80% in the Toral project. If you’re investing in junior mining, you need to understand that massive dilution of your equity interest is par for the course, unless you have very deep pockets to help fund the development.

DRA Global (JSE: DRA) released its annual report and announced a dividend of A$0.11 per share for the year ended December 2023. This is the company’s first dividend since listing. It works out to 136.35 cents per share. For reference, the share price is R22 at time of writing.

The Foschini Group (JSE: TFG) has announced the appointment of Ralph Buddle as CFO, which relieves Anthony Thunström from the role as executive financial director in addition to being CEO. Buddle was previously interim CFO at Oceana Group and has been in an executive role at The Foschini Group since September 2023.

Stefanutti Stocks (JSE: SSK) has reached agreement with its lenders to extend the capital repayments profile of the loan as well as its duration to 30 June 2025. This is part of the group’s restructuring plan.

Sanlam (JSE: SLM) implemented a B-BBEE deal in 2019 that ended up being badly impacted by COVID. These highly leveraged structures depend on dividends and significant share price growth to be successful. When those things don’t happen, they end up underwater. This is what has happened here, with Sanlam looking to buy the shares back from that structure at a nominal value. It’s even worse than that really, as Sanlam had to step in to buy the preference shares from Standard Bank that funded the deal. It’s an expensive outcome for Sanlam shareholders.

Wesizwe Platinum (JSE: WEZ) does not have any revenue at the moment. The auditors have also made it clear that there are uncertainties around the company’s ability to continue as a going concern, with the group’s existence dependent on ongoing support from the majority shareholder and a willingness not to call the current shareholder loans. Although the loss per tax for the year came down significantly from R134 million in the prior period to R25.2 million in 2023, it was still a substantial loss.

Randgold & Exploration Company (JSE: RNG) is focused pursuing legal claims and limiting operational costs. It’s not the most inspiring company vision in the world, but somebody has gotta do it. The company reported an operating loss of R30.6 million for the year ended December 2023, worse than R22 million in the prior year.

SAB Zenzele Kabili (JSE: SZK) released its annual report. The net asset value has increased from R2.26 billion to R2.67 billion, a direct result of a strong finish to the year for the AB InBev share price.

In order to meet B-BBEE requirements under ICASA licensing provisions, Telemasters (JSE: TLM) is disposing of 30% in major subsidiary Catalytic Connections to the Sebenza Education and Empowerment Trust. This is a Category 2 transaction, so there is no shareholder vote on this. A more detailed announcement with terms of the deal will be released in due course.

Chrometco (JSE: CMO) is an absolute mess that is suspended from trading. The reporting is running behind schedule and the company is struggling to appoint auditors because subsidiaries are in business rescue. On top of all this, the business rescue practitioner in on subsidiary is even suing another subsidiary! It sounds like only the lawyers are making money here, with the creditors meeting for the business rescue plan to be held on 11 April 2024.

Afristrat Investment Holdings (JSE: ATI), perhaps the most broken company of all on the JSE, would really like to voluntarily liquidate itself. It can’t though, as a creditor is trying to liquidate it first. Yes, really.

Deutsche Konsum (JSE: DKR) has basically zero liquidity on the JSE and has announced an intention to drop this listing. Still, in case you are one of the few local shareholders, it’s important for you to know that the company has sold off a large portfolio of properties to try reduce debt and is negotiating with bondholders to extend debt maturities.

Deutsche Konsum REIT-AG has disposed of a sub-portfolio of 14 retail properties with an annual rent of c. €5,5 million. The properties were sold at a discount of 3.8% on current carrying amounts. The funds will be used in full to repay bank and bond liabilities.

Sirius Real Estate is to expand its UK portfolio with the acquisition of Vantage Point Business Village, a multi-let business park in Gloucestershire for a total acquisition of £48,24 million. Through the purchase, Sirius will add more than 1,5 million square feet of space to its BizSpace portfolio, of which 1 million square feet is industrial space. The acquisition has been made using the proceeds of the company’s £147 million capital raise achieved in November 2023.

MTN has accepted an offer from Africa-focused telecommunications company, Telecel, to acquire its units in Guinea-Bissau and Guinea-Conakry. The disposals are part of MTN’s portfolio optimisation strategy and investment in digital platforms and fintech offerings. Financial details were undisclosed.

Following the failure to get the deal with Alma Trading CC across the line, Accelerate Property Fund has announced the sale of Cherry Lane Shopping Centre in Pretoria to Cadastral Assets for a cash consideration of R60 million. Accelerate purchased the property as part of a retail portfolio acquired in 2014.

CA Sales, through its wholly owned subsidiary CA Sales Investments, is to acquire a 49% stake in Roots Sales from Mass Market Distribution Holdings. The acquisition is part of the company’s channel broadening strategy and has the option to increase its shareholding in the future. Roots has an integrated market offering that combines all commercial requirements, including sales, merchandising, auditing and delivery solutions into a single interlocking and dynamic service enterprise specialising in the main market. Financial details were undisclosed.

In August last year Nampak announced it would undertake to implement various turnaround initiatives including an asset disposal plan to raise c.R2,6 billion. This week the group announced the disposal of its liquid cartons business in South Africa and its businesses in Zambia and Malawi for a total consideration of R450 million. The assets have been acquired by a consortium represented by RMB Corvest (FirstRand) and Dlondlobala Captial.

After several months of cautionary announcements and speculation around Telkom’s sale of its mast and towers business Swiftnet, the company has finally released further details. Towerco Bidco, a consortium comprising an infrastructure fund managed by a subsidiary of Actis and a vehicle owned by Royal Bafokeng Holdings (RBH) will acquire Swifnet. As its BEE partner, RBH will hold at least a 30% of the acquiring entity. The aggregate consideration to be paid to Telkom will be calculated with reference to an enterprise value of R6,75 billion.

Hot on the heels of the release of details on the listing of WeBuyCars, Transaction Capital has announced the disposal of Nutun Australia (NAH) for A$58,3 million. The sale, to Australian alternative investments company Allegro Funds, is in line with Transaction Capital’s announcement that it was reviewing its operations to reposition or dispose of non-core assets. Nutun International has entered into a strategic partnership with NAH and its new shareholder, through the on-going provision of customer and debtor engagement support services and associated technologies to NAH clients from South Africa.

Copper 360 has entered into a memorandum of understanding with Far West Gold Recoveries (FWGR) in terms of which the DRDGold subsidiary will conduct a due diligence (DD) on Copper 360’s copper tailings dams over a 12-month period. The DD will determine the viability of the copper dumps which may result in the parties entering into a joint venture agreement, with FWGR acquiring a 50% interest and becoming the operator of the dumps.

Telemedia, a subsidiary of the Rex Trueform Group, is to acquire a number of properties from Telelet, a company owned by The Bretherick Family Trust. The R51,5 million acquisition of the properties is seen as a strategic opportunity for Telemedia which currently partially occupies the properties for operational purposes. Additional rental revenue from remaining portions will diversify Rex Trueform’s existing portfolio of properties.

Actis has exited its investment in Octotel and RSAweb to a consortium led by African Infrastructure Investment Managers (Old Mutual). AIIM is investing alongside STOA, an impact fund in infrastructure and energy and Thebe Investment Corporation. Octotel is a key player in the fibre-to-the-home and business markets in the Western Cape.

Zeder Investments has received several approaches from third parties regarding the company’s portfolio investments, namely the Pome Division, previously in the Capespan Group and Zaad Holdings. Zeder will consider these approaches and will, it says, embark on formal processes where appropriate though this may take several months.

Unlisted Companies

Medu Capital has acquired a majority stake in Optron Group, a distributor, supporter and integrator of cutting-edge technology brands. The strategic partnership, through its Medu IV fund, will aim to foster innovation, drive market expansion and deliver value to both customers and stakeholders.

RH Managers, a local private equity firm headquartered in Johannesburg, has invested R270 million, split evenly between debt and private equity, into Herolim Private Hospital, a healthcare facility in Mthatha.

Adcorp has repurchased 73,701 shares for a consideration of R295,798 in terms of its Odd-lot Offer, representing 0.07% of the company’s total issued share capital.

Kore Potash plc has advised on the conversion of Convertible Loan Notes into 109,865,053 new ordinary shares in the company at a price of 0.38 pence per new ordinary share. Following the issue of the new shares, the total issued share capital of the company will consist of 4,229,532,173 ordinary shares.

Deutsche Konsum REIT-AG has announced it is to withdraw its secondary listing on the JSE. The company, which has a primary listed on the Frankfurt Stock Exchange, listed on the JSE in March 2021. The intention was to attract interested South African investors. However, despite various initiatives, engagements with investors have not yielded the desired results from a local market perspective. Further details will be announced in due course.

Oando plc, which has a secondary listing on the JSE, has had the trading of its shares suspended. This follows the company’s failure to comply with the JSE Listings Requirements by not publishing its year-end results for 2022 and the interim results for 2022 and 2023.

A number of companies announced the repurchase of shares.

British American Tobacco has commenced its programme to buyback ordinary shares using the £1,57 billion net proceeds from its sale of ITC shares. The company will buy back £1,60 billion of its ordinary shares – £700 million in 2024 and the remaining £900 million in 2025. This week the company repurchased a further 1,76 million shares at an average price of £23.71 per share for an aggregate £4,17 million.

Tharisa plc, dual listed on the JSE and London Stock Exchange, is to undertake a US$5 million general share repurchase programme during the period 26 March to 21 February 2025. The repurchase will represent up to 10% of the ordinary shares in issue.

Hammersonplc has, in accordance with the terms of its share repurchase programme announced on 12 March 2024, this week purchased a further 857,634 shares at a volume weighted average price of 26,92 pence, for an aggregate £232,393.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 18 to 22 March 2024, a further 3,994,681 Prosus shares were repurchased for an aggregate €109,8 million and a further 315,210 Naspers shares for a total consideration of R976,9 million.

Five companies issued profit warnings this week: Gemfields, Wesizwe Platinum, Salungano, Randgold & Exploration and Balwin Properties.

Three company either issued, renewed, or withdrew cautionary notices this week: Telkom SA SOC, Pick n Pay Stores and AYO Technology.

Altona Rare Earths has entered into an agreement with Sustineri Group and other shareholders to acquire the entire issued share capital of Phelps Dodge Mining (Zambia), the registered holder of Large Scale Exploration Licence 21403-HQ-LEL located in the Mufumbe District in Zambia. The consideration will be settled as follows – US$40,000 on completion and US$150,000 12 months after completion payable in Altona shares.

AI-powered edtech Sprints.ai, has raised US$3 million in bridge funding in a round led by Disruptech Ventures and includes EdVentures, CFYE and others. The Eqyptian startup, launched in 2020, is looking to use the funding to scale its end-to-end platform that bridges the tech talent gap.

The COMESA Competition Commission has approved the 100% acquisition of Kenyan dairy company Highland Creamers by Uganda’s Lato.

Kenya’s BasiGo announced a US$3 million equity investment by Toyota Tsusho Corporation’s CFAO to accelerate the production and delivery of electric buses in Kenya and Rwanda.

British International Investment has provided a US$100 million finance facility to the Eastern and Southern African Trade & Development Bank (TDB Group) which will assist the group with providing financial support to local businesses and financial institutions in several key African markets.

Flour Mills of Ghana has acquired a stake in Ghana’s oldest animal feed producer, Agricare, from Injaro Agriculture Capital Holdings for an undisclosed sum. The sale represents a full exit from Agricare for the fund which is managed by Injaro Investments.

The International Finance Corporation and other lenders, including African Development Bank, Bangkok Bank, British International Investment, Citibank, DEG, DZ Bank, Emerging Africa Infrastructure Fund (EAIF), Rand Merchant Bank, FMO, Export-Import Bank of India (India Exim Bank), Export-Import Bank of Korea (KEXIM), the Standard Bank Group, Standard Chartered Bank, and the United States International Development Finance Corporation (DFC) have announced a US$1,25 billion financing package to Indorama Eleme Fertilizer and Chemicals in Nigeria to ramp up its fertilizer production and develop a port terminal for exports.

CANAL+ Group has acquired a stake in Marodi TV, a Senegalese production company. Financial terms were not disclosed.

Many Peaks has announced an agreement to acquire a 100% interest in the Turaco Gold and Predictive Discovery Ltd joint venture [CDI Holdings] which holds the right to acquire an 85% interest in four mineral permits in Côte d’Ivoire (including the Ferke Gold Project). The purchase will be settled through the issue of 5,617,978 fully paid ordinary shares in Many Peaks.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")