")

Accelerate Property Fund is ready to raise the next R100 million in equity (JSE: APF)

This addresses an overhang in the share price

Accelerate Property Fund told the market in 2023 that they would need to raise up to R300 million in fresh equity. This created a clear overhang in the share price, as many punters will quite wisely wait for the dust to settle on this kind of thing. Well, the dust is now settling.

After raising R200 million in June 2024, they are now moving forward with the remaining R100 million. They will use R50 million for capex at Fourways Mall and the remaining R45 million (net of costs) for working capital.

The price is 40 cents per share. That’s an 18.48% discount to the 30-day VWAP, which is actually a pretty fair discount. Shareholders who don’t want to take up their rights will be able to try and sell their letters of allocation. Shareholders won’t be allowed to apply for excess allocations, so this tells you that the underwriter is only too happy to take up shares.

The offer is fully spoken for between Investec Bank and the underwriter, K2016336084 (South Africa) (Pty) Ltd – a name that just rolls off the tongue. If you trace it, it looks like this company relates to the controlling shareholder of Castleview Property Fund.

A fully committed and underwritten rights offer means that there’s significant backing for Accelerate Property Fund at 40 cents per share, which is an interesting “price floor” for punters who want to get involved here. You can’t treat the price floor as a guarantee of course, but it’s a strong positive signal.

It will be interesting to see what the uptake is from the broader shareholder base. The share price has been stuck at roughly the 50 cents mark for a year now, so perhaps this will also catalyse some action.

Of course, it’s then all to play for with Fourways Mall. I doubt they would approve additional capex at the property if they weren’t happy with the numbers they are seeing.

Capital Appreciation got the market excited (JSE: CTA)

The share price closed 10.9% higher after a trading statement

Capital Appreciation Limited did that thing that you’ll often see on the JSE, where they’ve given the bare minimum disclosure under trading statement rules. For the year ended March 2025, they expect HEPS to be at least 20% higher than in the comparable period. Now, this could mean just about anything, as the words “at least” sometimes work very hard.

If we go back to the interim period ended September 2024, we find a decrease in HEPS of 8.3%. This means that they had an exceptional second half to the year, with a business update in March suggesting that the payments business was doing well and the software division was having a better time of things.

Although the software division is still below where it needs to be, the payments division seems to be doing enough to achieve solid growth numbers.

The share price is up 43% over 12 months and is now 6.5% higher year-to-date, with the latest jump doing wonders for these numbers.

Copper 360’s losses have at least doubled (JSE: CPR)

Welcome to the broken hearts club

When it comes to junior mining, investors already approach everything with a great deal of caution. This is warranted, as these are high-risk businesses with immense uncertainty. This also means that there is limited margin for error in terms of missed deadlines and disappointments.

Copper 360’s share price has lost over half its value in the past 12 months. This makes it so much harder for them to raise capital or be taken seriously in the market. With the headline loss for the year ended 28 February 2025 being at least 100% worse (in other words, the loss has at least doubled), there’s very little to stem the bleeding.

They blame operating losses at the SXEW plant due to lower-than-expected feed grade, with that plant now in care and maintenance. The new Modular Floatation Plant at Nama Copper only reached operating capacity in the second half of the year, so the full benefit of it isn’t being felt in the full-year results. Finally, planned revenue at the Rietberg mine wasn’t achieved due to construction and production delays, so they incurred the costs and didn’t enjoy the benefits.

This update came out after market close on Friday, so don’t be fooled by the share price being 8.1% higher on the day. For the market response to these numbers, rather watch it on Monday.

Junior mining is the toughest sector of the lot. I hope that they start to find some success at the company.

I’m not sure what the market didn’t like at Dis-Chem (JSE: DCP)

The share price dropped despite 20% growth in HEPS

The market can sometimes do rather odd things. Dis-Chem’s share price fell 6.3% on Friday after they released results for the year ended February 2025. There was clearly something that investors didn’t like, although there’s also a chance that this was due to profit-taking by large punters. In reality, it was probably a mix of the two.

Either way, the underlying numbers look fine to me. Revenue was up 8%, HEPS increased 20% and the total dividend for the year was up 19.9%, so cash quality of earnings is strong. Those numbers are hard to fault.

The retail side of the business saw comparable pharmacy store revenue growth of 4.1%. Store openings took total revenue growth up to 5.9%. Notably, they reported net closures in the baby store offering, so one wonders how that is really going – the birth rate isn’t exactly providing much support right now.

Wholesale revenue increased by 9.9%, with a bright spot being sales to independent pharmacies and TLC franchises, up 22.1%. This has been core to the growth strategy at Dis-Chem and it has worked well, as they don’t want to rely purely on their own stores for growth.

Margins improved in both the retail and wholesale businesses, contributing to the much higher growth in earnings relative to revenue. An impressive decrease in like-for-like retail employee costs of 0.2% would’ve been a major contributor here.

The outlook statement also doesn’t really explain the share price drop. For 1 March to 27 May (essentially the first quarter of the new financial year), comparable pharmacy store revenue growth improved to 4.6%. The only negative is that wholesale revenue growth to external customers has slowed to “just” 13.6% – still a strong number.

Dis-Chem is trading on a P/E of 24x, so there are high expectations at that level. Too high, perhaps?

HCI’s financial director is going to run the Africa Energy Corp business (JSE: HCI)

Given its importance to the group, this seems reasonable

HCI and its various group companies all released updates earlier in the week. HCI itself is facing some challenges at the moment, particularly as the core gaming business is heading the wrong way. With the oil and gas prospecting business still incurring substantial losses at the moment, the group cannot afford any missteps.

Rob Nicolella has resigned as financial director of HCI and a director of the HCI board, as he will move into the CEO role at Africa Energy Corp (the oil and gas business). That’s certainly much closer to the action than his current role.

Cisco Pereira has been announced as his replacement, having been with the group since 2010 and played a role in various subsidiaries. The company also noted that Adhika Singh will join the board of HCI as a non-executive director, with particular expertise in risk and compliance.

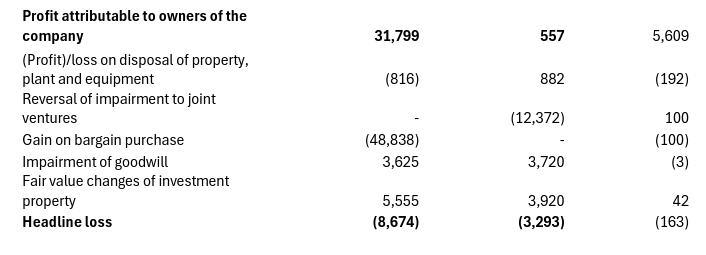

Huge Group value write-down is finally happening (JSE: HUG)

For as long a I can remember, I’ve been saying their assets are overvalued

Huge Group sees itself as an investment entity. This means that they carry their investments at fair value.

Now, within their total portfolio, one of the largest assets is a preference share into the Huge Connect business. Until FY24, they were valuing these prefs using a required rate of return of 10.75%. It’s hard to put into words how ridiculous this is, as it implies that the Huge Connect business has a similar risk profile to SA 10-year government bonds. Clearly, that’s just not true.

Lo and behold, in the freshly released FY25 numbers, they are now using a rate of 12% for those prefs. When the rate goes up, the value comes down. 12% is still nowhere near high enough in my opinion, yet just that change was enough to drive the fair value lower by R106 million.

The total portfolio fair value movement led to a drop in the net asset value per share of 3.7%. This took it down to 928.69 cents per share, which is still a huge premium to the current share price of R1.95.

The market is sending a very clear message here about how overvalued these assets still are. Although some of it is perhaps starting to sink in, it’s when I read a word salad like this in the integrated report that I remember why I’ve never held shares in this company:

Are they saying that they don’t have capital, or that their portfolio investment companies don’t have sufficient opportunities? Heaven knows.

A truly awful year at Insimbi Industrial Holdings (JSE: ISB)

There’s no dividend – and no profits either!

Insimbi has released earnings for the year ended February 2025. They aren’t good at all, with revenue down 11% and EBITDA tanking by 68%. It only gets worse further down the income statement, with the group slipping into a headline loss per share of -6.50 cents vs. HEPS of 12.54 cents in the comparable period.

Last year’s dividend of 2.5 cents is but a distant memory, as there’s no dividend this year.

Having just announced their lowest operating profit in the past five years, you would hope to see some decisive commentary about their plans. Instead, the SENS announcement is filled with generic comments about the broader economic environment and how they are expecting some benefits from growth in South Africa. They are of course beholden to global commodity prices in metals like copper, aluminium, nickel and steel, so that brings plenty of uncertainty to the earnings, but it’s hard to see a brighter future for them if they aren’t clearly articulating what they are doing about the challenges.

The share price has lost over a quarter of its value in the past year.

Mustek and Novus have released the combined mandatory offer circular (JSE: MST | JSE: NVS)

This comes after plenty of regulatory delays and debate

Usually, corporate transactions go smoothly with the regulator. They follow well-trodden paths and the lawyers involved have “seen this movie” and “get it across the line” with the regulators. Don’t worry, there are lots of other options for playing corporate advisor bingo if those two don’t interest you.

The mandatory offer by Novus to shareholders of Mustek has been very different, with a fight in the High Court with the Takeover Regulation Panel (TRP). This means that the lawyers had to do some original drafting this time rather than sticking to a template, with a full page disclaimer in the circular related to the TRP’s position.

The TL;DR is that the TRP is currently considering its legal options after the High Court set aside the TRP’s prior ruling. This means that an appeal could still happen, which could then lead to this circular being amended. There’s a lot of “could” here, unfortunately.

The intention here isn’t for Mustek to be delisted. Novus has moved through the 35% ownership threshold in Mustek, hence a mandatory offer is triggered. Those who would like to accept the offer can either accept R13 per share in cash, or R7 per share plus 1 Novus share, or 2 Novus shares per Mustek share.

Mustek is currently trading at R13.08 and Novus is at R7.15 per share. At current values, taking two Novus shares would theoretically offer the best value, but of course the Novus share price is changing all the time.

Valeo Capital has acted as independent expert and has provided a fair value range per Mustek share of between R16.39 and R19.60 per share, with a likely value of R18. They indicate a fair value per Novus share of R7.27.

On this basis, they have opined that the cash offer of R13 is unfair and unreasonable to Mustek shareholders. The cash plus share offer is unfair, but reasonable, with the reasonability test being based on Mustek’s traded price. The share-only offer is also unfair and reasonable. In all three cases, the fairness test is based on the fair value of the two shares.

Again, as this isn’t a scheme of arrangement, so anyone can simply decline the mandatory offer and be left with their shares. This is why an “unfair and unreasonable” offer can be put to shareholders, as there’s actually no choice in the matter – it is, after all, a mandatory offer!

Santova is acquiring an interesting group in Europe (JSE: SNV)

They are targeting the eCommerce sector here, an obvious growth area

Santova has been trading under cautionary since early February. The market took that caution seriously, with no obvious direction to the share price (aside from the usual bid-offer choppiness of a mid-cap). But the message from the market was very clear on Friday after Santova announced the details of this transaction: the share price closed 9.3% higher on strong volumes.

I don’t blame the market, as Santova has found something interesting here. The Seabourne Group has been around 1962 and is based in the UK and Europe. They’ve positioned themselves for the eCommerce market, which means strategically located fulfilment centres and a design built around elements like fast picking and packing rather than bulk storage and long-term inventory holding. The fact that one of their specialities is mailing niche subscription magazines tells you a lot.

I think that this is clever stuff. eCommerce is only getting bigger from here, not smaller. The variety of things to buy online will only increase, not decrease. This is going to drive more demand for specialist supply chain services over time.

In terms of price, they are paying £17 million for this asset. £13.6 million is payable on completion, along with an amount of roughly £1.7 million that is subject to adjustment for movement in the net asset value. The remaining £1.7 million is structured as deferred payments over two years, subject to the profit warranty.

This bring us to the meat of the story: the valuation. The profit warranty is for a minimum EBIT of £3.7 million per year. This is the key, as the net assets of Seabourne are only worth £1.9 million and hence they are buying a lot of goodwill here rather than identifiable assets.

If we just apply the UK corporate tax rate of 25%, the warranty EBIT translates to roughly £2.8 million of post-tax profits (assuming there’s no interest expense). This implies an unlevered forward P/E of around 6x for the business. That doesn’t seem unreasonable for a European business.

If the profits for the two warranty periods exceed £7.4 million in aggregate, then 35% of the excess will be payable to the sellers. The cap for the purchase price is £19 million, so Santova isn’t sitting with unlimited potential liability here. Putting a cap on this exposure is a very important dealmaking tool.

Santova will pay for this from internal cash and a R60 million five-year debt facility. It’s an amortising loan, so the bankers must be comfortable with the local cash flows to service this debt. Banks and corporates have learnt many hard lessons about funding foreign investments with local debt.

Kudos to Santova – this is an interesting deal!

Sirius Real Estate continues to actively manage its portfolio with acquisitions and disposals (JSE: SRE)

It’s all about buying low and selling high, like any good trading strategy

Sirius Real Estate isn’t a fund that sits on its hands. They’ve announced the acquisition of a multi-let business park in Germany for €12.7 million, representing a net initial yield of 7.9%. They also announced the sale of a German business park for €30 million on a net initial yield of 6.8%. Remember, the lower the yield, the higher the price. The sale was achieved at a 9% premium to book value, which is impressive.

As is is usually the case for a deal by Sirius, the acquired property has room for improvement. Acquired with an occupancy rate of 88%, Sirius has already locked in a lease to take it to 95%. A further catalyst for growth is the overall development of the area, including significant government infrastructure projects.

The property that they’ve sold was acquired in July 2008 for €14.5 million. This works out to a compound annual growth rate of around 4.4%, excluding dividends.

Nibbles:

- Director dealings:

- Adrian Gore of Discovery (JSE: DSY) usually has a collar position in place over at least a portion of his shareholding in the company that he built. When the share price does well, it can end up at a price above the strike price of the call options when they expire. In such a case, he is a forced seller of the shares related to that derivative. The latest such sales are to the value of R33 million. He’s put another hedge in place now that this tranche has expired, buying put options with a strike price of R214.61 and selling calls at a strike of R457.12. The options expire in 2031 and the current Discovery share price is R218.

- In and amongst the trades by many Investec (JSE: INL | JSE: INP) execs in relation to share-based awards, there was also a sale by the CEO to the value of around R6.2 million and the CFO to the value of R2.5 million. The announcement doesn’t specify that these sales are to cover taxes.

- Here’s an interesting one for you: Nampak (JSE: NPK) CEO Phil Roux has put in a place a collar hedge over 91,000 shares in the company. The put strike price is R480 and the call strike price is R533. The spot price is R485, so the idea here is to protect against downside risk from the current level. The options expire in May 2026.

- The CFO of Altron (JSE: AEL) bought shares in the open market worth R841.5k.

- A director of Stefanutti Stocks (JSE: SSK) bought shares to the value of R100k.

- There were several results from smaller companies on Friday. I can’t cover them all in detail or it will be too much for you to read in Ghost Bites, so several of them are just being noted in the Nibbles section. The first example is RH Bophelo (JSE: RHB), with growth of 4% in the net asset value (NAV) per share for the year ended February 2025. This may be a positive move, but there’s a significant decrease in investment income and no dividend has been declared to shareholders. I also have to note that the NAV per share is R16.67 and the share price is just R1.81, so that tells you what the market thinks of the NAV.

- Onwards to Mahube Infrastructure (JSE: MHB), where we see a similar story in terms of a modest uptick in NAV per share for the year ended February 2025 (in this case by 2%) and a significant slowdown in earnings. Revenue fell from R68.2 million to R49.8 million. Notably, the dividend income from underlying solar projects was boosted in the prior period from a refinancing of those projects (i.e. raising debt and paying out a dividend), so that was always going to be a very tough base for comparison. With the share price at just R3.90 vs. the NAV per share of R10.73, this is another example of a huge discount to NAV.

- Next up is AYO Technology (JSE: AYO), the company that Sekunjalo is taking private. For the six months to February 2025, revenue fell by 23% and the headline loss per share worsened by 36%. They call this a “resilient” performance – I guess that word means different things to different people. I don’t think there are too many people who will shed tears over the delisting of this company.

- The final results update in this section is Mantengu Mining (JSE: MTU), the company that has been in the headlines for wild reasons based on making allegations of share price manipulation. The cease and desist letter that the JSE sent Mantengu seems to have sunk in, with the announcement making no mention of these allegations. We will have to wait and see if anything comes of that mess. In the meantime, a jump in expenses and a debt write-off more than offset the improvement in gross profit. Finance costs then finished this ugly job, with a headline loss per share of 23 cents (vs. 1 cent in the comparable period). They recorded a massive R350 million gain on bargain purchase of Sublime Technologies, a deal that I still can’t understand the pricing of. They literally paid nothing for the deal, suggesting that the US sellers just wanted to get rid of it as quickly as possible. Too good to be true? This gain doesn’t get included in the headline numbers, hence the huge gap between the headline loss per share and earnings per share.

- Mondi (JSE: MNP) shareholders didn’t exactly fight over the ability to reinvest their dividends. Holders of just 0.83% of shares on the UK register and 2.84% of shares on the South African register elected to reinvest their dividends.

- Tharisa (JSE: THA) is undertaking a share buyback programme of up to $5 million. The timing is pretty good, as there has been a fair bit of share price weakness. Although shareholders have given authority for repurchases of up to 10% of the shares in issue, the market cap is close to R5 billion and so a $5 million programme won’t get anywhere near the 10% limit.

- Salungano Group (JSE: SLG) has updated the market on the expected timing of release of the results for the year to March 2024 and the six months to September 2024. They are on track to get both out by the end of June 2025. The March 2025 results are expected to be published by the end of September 2025. They then need to sort out their annual report, with the overall goal being for the listing suspension to be lifted by November 2025.

- Efora Energy (JSE: EEL) announced a delay to the release of its financials for the year ended February 2025. They needed to be released by 31 May and instead will only be published by 30 June.

- Wendy Luhabe has stepped down as chairman of Libstar (JSE: LIB). JP Landman has been appointed as the new chairman. This came into effect immediately after the AGM held on 30 May.

")

")

")

")

")