RCL Foods delivers pleasing Interim Results in a challenging environment.

Muted demand persists in a challenging economic environment

Rainbow turnaround yields positive result

Continued good Sugar performance

Service levels restored in Pet Food and Pies

Load-shedding direct costs continue to impact earnings

Receipt of Vector Logistics sale proceeds improves cash position

We remain committed to our overarching business strategy as previously communicated, which includes improving shareholder returns as we seek to GROW WHAT MATTERS for all our stakeholders. I am pleased to say that we are on track with our strategy delivery plan for the 2024 financial year, supported by the rollout of our Purpose across our Value- Added Business.

RCL FOODS’ Chief Executive Officer, Paul Cruickshank

RCL FOODS is a deeply-rooted South African consumer goods business that produces some of the country’s most-loved brands: Yum Yum peanut butter, Nola mayonnaise, Ouma rusks, Pieman’s pies, Number 1 mageu, Sunbake and Sunshine bread, Supreme flour, Selati sugar, Simply Chicken, Rainbow chicken, Bobtail and Canine Cuisine dog food, Catmor and Feline Cuisine cat food, and Molatek and Epol animal feed, to name a few. It also produces a wide range of speciality and private label products.

Headquartered in Westville, Durban, the business employs over 16 000 people across 8 provinces in its Value-Added and Rainbow operations. At the heart of its culture and strategy is its Purpose – WE GROW WHAT MATTERS – which encapsulates its belief in collectively doing that little more to create a positive impact that matters.

By Nico Katzke, Head of Portfolio Solutions at Satrix*

Just over a year ago we were all enthralled by the emergence of a technology that promised to disrupt all facets of our lives.

What started as a live social experiment of opening large Natural Language Processing (NLP) algorithms, in the form of ChatGPT, to answer the public’s unscripted questions, soon proved so effective that most see it as a technology with the potential for hard-to-even-comprehend disruption.

Most of us are currently observing, with both interest and anxiety, the rapid rise of this technology, wondering how this will impact and reshape the industries we work in.

Many observers’ enthusiasm was somewhat curbed in recent months by the realisation that physical limitations exist in building larger and ever more capable training models. It turns out, when we ask ChatGPTa question online, somewhere a machine is whirring and crunching numbers. It is, after all, not magic. Nor is it a tireless sentient being answering our questions – it is simple a set of machines doing complex math. The more we ask of it, the bigger it needs to be.

Despite clear physical and hardware challenges, to many it seems the future domination of Artificial Intelligence (AI) through Large Language Models (LLMs) is inevitable. Others are more sceptical.

First, it is costly. Building, training and maintaining these models require incredible costs and expensive manpower, access to enormous datasets and advanced chip making infrastructure. In fact, Sam Altman, CEO of OpenAI, the creators of ChatGPT, is reportedly looking to raise up to $7 trillion to further boost GPU-chip supply, critical in building more capable algorithms able to power the truly disruptive promise of AI. That number is greater than Apple and Google’s market caps combined, and while other executives (notably the CEO of Nvidia, the leading chip maker) have been critical of these numbers, most estimates suggest a chip making industry worth several trillion dollars in the near future.

Apart from hardware limitations, other key drawbacks include the environmental costs associated with training and managing these energy hungry algorithms, the inherent biases that undocumented training could embed in model responses with limited recourse, the inability of modelers to reverse engineer parameters (making it a black-box process by design), as well as the lack of ethical scrutiny required to ensure it is safely deployed on society.

Proponents of AI’s unbridled growth might point to these being fixable problems; eggs broken in the pursuit of a sentient omelette.

But a bigger problem might lurk in its current design that should give even the most optimistic pause: the lack of Intelligence, or the “I” in AI. People are mesmerised by Generative AI’s output and the illusion of understanding that it possesses. It also doesn’t help that researchers and companies at the forefront of its development have strong incentives to feed this illusion with anthropomorphic language like learning, intelligence and reasoning.

But at its core, the models we interact with are simply computer algorithms trained on human supplied information (think all the public Reddit, Wikipedia, etc. pages), that take text as input and produce answers by predicting what word (or what pixel, when drawing) should come next.

It is, ultimately, super-efficient predictive text strung together in a way that, given its vast library of human conversational data for training, seem intelligent and human-like. But it is a parrot, not a mind.

A remarkable achievement in mimicry and information collation, but not sentient and completely void of understanding. It is simply pattern matching at unprecedented scale, meaning its current design will always scupper its ability to “think” outside the (very black) box. Even if a methodology is identified that can bring us to the holy grail of Artificial General Intelligence (AGI), that doesn’t mean that it will necessarily be achieved. Think the decades long pursuit of nuclear fusion which is theoretically possible.

While we believe the destination of broad-based adoption of some form of AI across industries is still a way off, we have been thrust upon a path to discover its full potential. But the path still needs to be paved, sidewalks erected and streetlamps put in.

The biggest current opportunities therefore are likely with companies able to harness their size and scale to access the best minds and computer hardware needed to build the foundation for tomorrow’s application. Small and nimble are not traits that help with securing trillion-dollar chip deals or access to enormous computing warehouses.

A sensible proxy for investing in the future of AI may very well be an index comprised of larger, more established tech companies, like the Nasdaq 100. Despite returning more than 50% in US$ in 2023, if the future is indeed broad-based adoption of AI, then which sentient being currently dares bet against the established tech giants in the Nasdaq?

*Satrix is a division of Sanlam Investment Management

Disclaimer Satrix Investments (Pty) Ltd is an approved FSP in terms of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. Satrix Managers is a registered Manager in terms of the Collective Investment Schemes Control Act, 2002.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSPs, their shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

Afrocentric is struggling to find growth (JSE: ACT)

This isn’t an easy way to make money

AfroCentric owns a portfolio of healthcare-related enterprises that are finding it tough going at the moment. Aside from the overall lack of economic activity to drive growth, the company has had to contend with contracts with low levels of profitability. In some cases, the company has walked away from such contracts.

After all the excitement of the deal with Sanlam last year, there isn’t any excitement at all in the financials. For the six months to December 2023, revenue grew by just 1.4% and HEPS dropped by 2.4%. If there are going to be any exciting synergies with Sanlam, we aren’t seeing them yet.

At least there is an interim dividend of 11 cents per share vs. no dividend in the comparable period.

Not much to write home about at Aspen (JSE: APN)

Revenue growth hasn’t translated into profits

The six months to December 2023 were filled with interesting strategic news at Aspen, like a distribution and promotion agreement with Lilly, as well as the product purchase agreement with Viatris for Latin America and the acquisition of the Sandoz business in China.

The benefits of these initiatives will hopefully come through in the second half of the financial year, as the first half hasn’t been exciting. Although revenue increased by 10% as reported, HEPS was down 6% as reported or up 1% on a normalised basis.

The highlight was the 44% growth in operating cash flow per share, with the cash conversion rate way up from 58% to 89%. A reduction of investment in heparin inventory was the key here. They call it a permanent shift, which is good news.

Net debt has increased considerably from R22.2 billion to R27.3 billion. Although overall debt levels are comfortable, debt isn’t a cheap source of growth right now.

Shareholders will pay very close attention to the second half of the year, which is when the benefits of recent strategic initiatives are expected to be realised.

AVI: masters of operating leverage (JSE: AVI)

The beverages and snacks businesses led the charge

AVI has released results for the six months to December 2023. They reflect an increase in revenue of 7.1%, which is decent by FMCG standards in this environment. More impressively, the company achieved growth in HEPS and the interim dividend of 17.4%.

At segmental level, Entyce Beverages is the second-largest revenue contributor and also grew the most, up by 16%. Snackworks is the bigger hero though, with the largest revenue and operating profit contribution and an excellent increase in profit of 35.1% off just a 9.8% increase in revenue. It turns out that biscuits really are good for you!

Fish? Not so much. I&J saw revenue fall 5.1% and operating profit plummet by 56.0% due to poor catch rates and loss of export sales.

The company has warned that growth in the second half of the year may not be as exciting as the first half, as they are lapping a strong fourth quarter in the comparable period.

Bidvest reminds the market why it is so respected (JSE: BVT)

There’s a strong performance at trading profit level

Bidvest has released results for the six months to December 2023. Revenue grew by 8.8% and trading profit by 11.8%, showing solid operating leverage that shareholders love to see. Cash generated by operations almost doubled to R3.7 billion!

Five of the seven divisions reported double digit trading profit growth, so the group can be proud of that. Automotive took a significant knock, with trading profit down 11.4% due to oversupply of new vehicles and a resultant knock-on effect in the used market. The brand mix at McCarthy’s is problematic as Bidvest doesn’t have exposure to new brand entrants that are doing well.

These strong numbers were blunted somewhat at HEPS level, with HEPS up by 5.3% and normalised HEPS up by 6.9%. The final dividend followed suit, up 6.9%. It won’t surprise you to learn that net finance charges were to blame here, up 41.5% excluding IFRS 16 and other fair value adjustments (in other words: a pure view on the increase due to debt).

The jump in finance costs was driven by higher average gross debt (of which R3.2 billion was due to corporate actions) and an increase in average cost of funding from 5.2% to 6.1%.

Return on Invested Capital of 15.8% is down on 16.3% in the prior year but still ahead of the weighted cost of capital.

Hulamin was all about the cash in this period (JSE: HLM)

Despite normalised EBITDA dropping by 7%, cash flow from operations skyrocketed

It is critically important for companies to manage both the balance sheet and the income statement, particularly when they are serious about driving return on capital higher. If a company doesn’t focus on return metrics like those, run away as fast as you can. This is why looking at the change in working capital and the extent of capex is just as important as looking at the income statement.

In Hulamin’s numbers for the year ended December 2023, a drop in volumes and EBITDA didn’t set an encouraging scene. Thanks to a substantial effort in reducing working capital requirements and simplifying the business, cash flow from operations was 503% higher at R363 million. That’s still not a great conversion rate vs. EBITDA of R620 million, but it’s a lot better.

Capex was R311 million, so shareholders seem to get very little cash out of this thing. Investors also won’t be enthralled by the performance in HEPS, which fell by 11% as reported or 27% on a normalised basis.

MAS could have a tougher route forward than expected (JSE: MSP)

The balance sheet outlook is proving to be difficult to solve

In the six months to December 2023, MAS grew adjusted earnings per share by 6%. The tangible NAV per share was up 10% in euros. This is good stuff, so why has the share price dropped sharply in the past year?

Despite the best efforts of the company on the income statement and the management of the properties in the portfolio, the trouble lies in the EUR300 million Eurobond that was issued in 2021. The goal was to reach investment grade and refinance the debt by 2025 / 2026. Nothing ventured, nothing gained.

Sadly, it’s not going to happen due to various factors. The bond market for non-investment grade issuers has completely dried up, which means the refinancing of the debt in 2025 / 2026 will be much more difficult and more expensive than hoped.

To the company’s credit, they are trying hard to get ahead of this problem. They are raising secured debt on unencumbered properties and they suspended the dividend.

A further recent setback is that banks are viewing MAS and the joint venture with Prime Kapital as a single group from a credit perspective. This is hurting the ability to borrow for both MAS and the joint venture, due to credit exposure limits that banks place on groups.

The net result isn’t pretty. Either MAS will have to raise debt with dividend restrictions post the 2026 calendar year, or there might even be a rights issue. A sale of assets may also be needed, which takes the group even further from an investment grade rating.

When credit markets move against you, life becomes hard in property funds.

Higher earnings and cash at Merafe (JSE: MRF)

2023 was a decent year in the end

Like all local mining groups, Merafe has had to negotiate failing South African infrastructure and all the other challenges that come with being in this industry. Nonetheless, a trading statement tells us that HEPS for the year ended December 2023 increased by between 4% and 24%. That’s solid.

The other good news is that cash and cash equivalents increased by just over R50 million in the six months from June to December, now at R1.656 billion. Admittedly, a chunk of this is set aside for future environmental rehabilitation obligations.

Detailed results for the year are expected on 18 March.

Metrofile is growing far too slowly (JSE: MFL)

The bankers are getting more excitement here than shareholders

In a world of exotic cocktails and food, Metrofile is like ordering the cheese sandwich on white bread, with a glass of tap water. It will fill you, but you might die of boredom midway through eating it.

Revenue grew by 2% for the six months to December 2023 and EBITDA fell by 4%. Exciting, hey? Due to higher interest rates, HEPS sadly dropped by 13% as bankers got a proportionately larger share of the pie vs. the prior year. Net debt is up 3% to R507 million.

The interim dividend is down 22% to 7 cents per share.

In case your bull case is related to the United Arab Emirates and Oman, you should know that revenue increased 28% (yay) but operating profit fell by 48%. Oh man, indeed.

Each to their own, I guess. This one isn’t for me:

At Netcare, mental health activity remains above pre-pandemic levels (JSE: NTC)

And revenue has grown by 5% for the first quarter of the year

Netcare is participating in an investment conference this week, so the company has released a voluntary announcement for the benefit of the rest of us who aren’t invited to the cool kids party.

For the five months to 29 February 2024, total paid patient days grew 0.3%. The announcement gives all kinds of different periods unfortunately, but the crux here is that growth is coming from revenue per paid patient day. For the first quarter of the financial year, total group revenue increased by 5% and total operating costs have been “well contained” despite the inflationary environment.

It’s also worth highlighting that demand for mental health remains strong, which isn’t a shock for anyone dealing with adulting.

Raubex grows despite Beitbridge having been completed (JSE: RBX)

The company wasn’t expecting to grow against a tough base period

Thanks to an increase in tender activity, Raubex has done better than they thought they would. The order book is strong despite the macroeconomic conditions, which is great news for investors.

This is why the company expects HEPS to be between 0% and 10% higher for the year ended 29 February 2024. This may not sound like much of an achievement, but the Beitbridge Border Post Project was in the base period and not in this period. To be flat or slightly up from there is impressive.

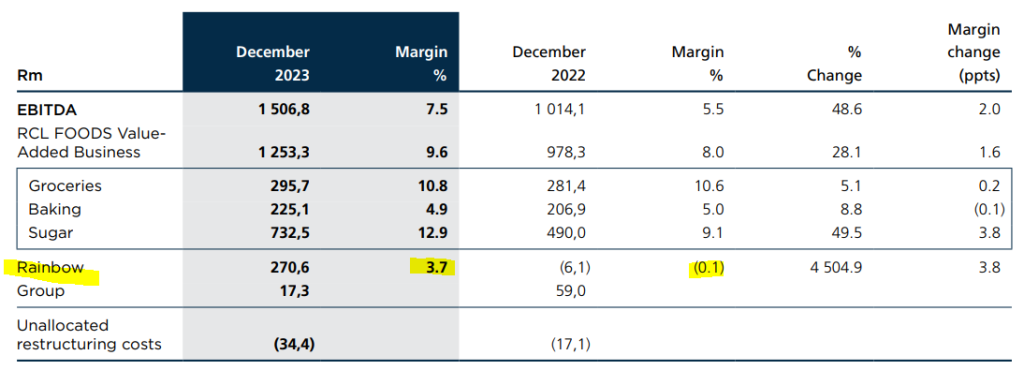

A pot of gold at the end of the RCL Foods rainbow (JSE: RCL)

There has been a sharp recovery

RCL Foods has released results for the six months ended December 2023 and they tell a great story. Revenue from continuing operations is up by 8.4% and EBITDA has jumped by 48.6%.

By the time we reach HEPS, we see growth of 52.6% in continuing operations and 43.3% overall. The discontinued operation in question is Vector Logistics, which was sold in August 2023.

Despite Avian Influenza in this period, Rainbow was one of the major areas of improvement for the period. It shows just how rough things were for poultry businesses in the comparable period.

Sugar also improved, with higher market prices that more than offset the impact of lower crop yields. Across the other food businesses, it looks like performance was mixed.

The Rainbow chicken business remains the lowest margin business in the group:

The big news here is that Rainbow is set for an unbundling and thus separate listing on the JSE. This will allow investors to take a pure view on either the poultry or other foods businesses. Currently, investors have to accept a very mixed exposure when buying shares in RCL Foods.

Due to the separation of Rainbow, RCL Foods has not declared an interim dividend.

Little Bites:

Director dealings:

The CEO of RH Bophelo (JSE: RHB) bought shares worth just under R20k.

Canal+ has been granted an extension by the TRP until 8 April 2024 to make the mandatory offer that is required under local takeover law to the shareholders of MultiChoice (JSE: MCG).

MC Mining (JSE: MCZ) has formally responded to the takeover bid by Goldway Capital Investment, priced at A$0.16 per share. The independent board’s advice to shareholders is to not accept the offer. There is a substantial document released to substantiate this view, which you can accessat this link. In summary, the independent board sees it an opportunistic offer that is between 20% and 30% below the pricing guidance in the initial non-binding takeover proposal.

Hyprop (JSE: HYP) announced that the acquisition of Table Bay Mall has been approved by the Competition Tribunal without any conditions being imposed on any party. The remaining condition precedent for the deal is the transfer of the property to Hyprop, anticipated to take place this month.

Kibo Energy (JSE: KBO) has sold shares in Mast Energy Developments (MED) to the value of £29k, with the proceeds being applied to reduce the outstanding balance on the RiverFort bridge loan facility.

Buka Investments (JSE: BKI) got off to a very slow start as a listed company, but has made some new director appointments that might be a precursor to some action.

No, this is not another fluff piece about the importance of humanity in creativity, designed to placate those who have lost their jobs to the heartless algorithm. This is the story of how creators around the world are standing up for their IP in unsurprisingly creative ways. Should artificial intelligence be quaking in its boots? Maybe a little.

Picture the following scenario: you’re using an image generator like Midjourney or Dall-E to create a visual for a campaign marketing fashion accessories. You type in the prompt “woman carrying a handbag”. The image generator spits out an image of a fashionable young woman carrying a toaster. Perplexed, you retype the prompt: “woman carrying a HANDBAG” – and receive another image of a woman holding a toaster. Unsure why this prompt isn’t working, you decide to try something else. You type in “woman wearing a hat” instead. The AI happily returns an image of a woman with a three-tier cake stacked on top of her head.

What is going on here?

What I’ve described is the future of AI, as seen through the eyes of its would-be disruptors. But why would anyone want to make artificial intelligence less effective? The answer to that question starts with how artificial intelligence became so smart in the first place.

The ethics of data scraping

The New York Times. Elon Musk. John Grisham, George R.R Martin and Jodi Picoult. These are just a few of the big names that have filed lawsuits against OpenAI since the launch of its deep learning model, ChatGPT, in 2020.

Generative AI systems, such as ChatGPT, work by interpreting user prompts through sophisticated algorithms. These algorithms are trained on extensive datasets, which are accessed by “scraping” and analysing billions of pieces of online text. At the heart of many of the lawsuits that OpenAI is facing is the question of who gave the company permission to access copyrighted materials for the training of its AI models.

It all sounds very vague when we talk about the IP attached to written words or images, so let me illustrate the problem for you with a more tangible example.

Imagine that you owned a bakery renowned for making a particular type of bread. One day, you come into your bakery to find a man in the corner who stands there all day, watching as you work. You did not give the man permission to be in your bakery and he won’t leave when you ask him to. The next day, he goes to the bakery around the corner and does the same thing there. And the day after that, he goes to a bakery two streets down and repeats the performance.

At the end of the week, the man opens a stall in the town square and starts giving free lessons on how to bake bread, incorporating signature techniques that he saw in your bakery and the others he visited. The enthralled public flock to his stall, and many of them go home and start baking their own bread. Next week, your bread sales are halved.

The authors who are filing lawsuits against OpenAI are making the case that the company is using material that they hold the copyright to without their permission (and, most importantly, without compensating them). Since OpenAI has been notoriously unforthcoming about where it sources its datasets from (remember, we’re talking about billions and billions of samples of text here), there is almost certainly a chance that they are drawing on copyrighted material from ebooks, scripts and online newspapers. Open AI has thus far neither denied nor confirmed whether this is the truth.

Instead, OpenAI is countering these arguments using a very open-ended exception to copyright protection known as “fair use”, which allows for the limited reproduction of text for uses like commentary or criticism. If you apply that argument back to our bakery example, that would be the man in the bakery claiming that anyone in the bakery (customers included) could look over the counter at any time and see the methods you are using to bake your bread.

It’s a tough argument to win and a bitter pill for creatives to swallow. While writers at the top of the bestseller lists are unlikely to be too affected by the rise in AI-generated writing, writers who work on a humbler scale (yours truly included) are working tirelessly to convince clients that their work is worth paying for. It’s hard not to feel that the whole situation is unfair.

It seems highly unlikely that the man with the stall in town square will be going away anytime soon. Fortunately, creatives never encountered a problem they couldn’t find an interesting solution for.

Define “sabotage”

While writers are taking AI to court, creatives in visual media are showing that they aren’t afraid to get hands-on when it comes to protecting what’s theirs.

In the same way that ChatGPT has disrupted the writing industry, AI-powered image generators have wreaked havoc in the art and design industries. The method for training these image generators also involves data scraping – and therein lies the crux of what might be AI’s undoing.

It started with Glaze, a tool developed by a team at the University of Chicago under the leadership of professor Ben Zhao. Glaze allows artists to “mask” their own personal style by changing the pixels of images in subtle ways. These changes are invisible to the human eye, but are powerful enough to manipulate machine-learning models to interpret an image as something different from what it actually shows. You can think of Glaze as a set of curtains in front of a window, obscuring a clear view of what’s inside.

While Glaze was designed as a countermeasure to IP theft, its sibling, Nightshade, takes a far more aggressive approach.

Developed by the same team at UC, Nightshade is a data poisoning tool that has the potential to break deep learning models by feeding them incorrect data. This tool strikes at the heart of AI’s biggest weakness – it needs to access vast amounts of data in order to learn. When the data is manipulated, the machine doesn’t know the difference; it simply absorbs the information that it is given without questioning whether that information is right or wrong. If you tell an image generating tool enough times that hats are synonymous with cakes, pretty soon it will believe you.

Just like many of the image generative tools that are out there, Nightshade is open source, which means that others are able to tinker with it, make their own versions, and distribute at scale. There’s a reason for this, according to team leader Zhao: the more people use it and make their own versions of it, the more powerful the tool becomes. The data sets for large AI models can consist of billions of images, so the more poisoned images can be scraped into the model, the more damage the technique will cause.

When an image generator starts spitting out images of weird animals with six legs and three eyes when prompted with “dog”, getting to the root of the problem is anything but simple. The poisoned data is very difficult to remove, as it requires tech companies to painstakingly find and delete each corrupted sample, of which there could be thousands.

As an artist who has always had a penchant for the surreal, I’d be lying if I said I wasn’t a little bit excited about the strange and twisted versions of reality that a poisoned image generator could produce. But I’m guessing the folks who are developing Google Gemini (and all the other models out there) are less excited about that prospect.

About the author:

Dominique Olivier is a fine arts graduate who recently learnt what HEPS means.Although she’s really enjoying learning about the markets, she still doesn’t regret studying art instead.

She brings her love of storytelling and trivia to Ghost Mail, with The Finance Ghost adding a sprinkling of investment knowledge to her work.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

MTN’s profits have been decimated (JSE: MTN)

The depreciation of the nairahas ruined the numbers

There really is no respite for MTN and the experience that the company has had in Nigeria. In a trading statement for the year ended December 2023, MTN announced that group numbers have been well and truly ruined by the naira. There are vast forex losses that have been a disaster for MTN as a whole, not just the Nigerian business.

HEPS is expected to be between -60% and -80% lower, which means a range of 231 cents to 462 cents vs. 1,154 cents in 2022. The company notes that 889 cents of the problem (i.e. all of it) was attributed to non-operational items, like hyperinflation adjustments of 151 cents and forex losses of 715 cents. The naira depreciation was a problem worth 593 cents per share.

As you might expect, the EPS result is even worse thanks to the impact of impairments, with that number expected to be between -70% and -90% lower.

Separately, MTN Nigeria released its results for the latest quarter. The top-line revenue growth isn’t the problem, with 22.7% growth in FY23 in local currency service revenue and an acceleration in Q4 (up 25%). Sadly, much of the cost exposure (operating costs and finance costs) is dollar denominated, so the devaluation of the naira severely impacts the company. MTN Nigeria reported a loss after tax of N137 billion vs. a profit of N348.7 billion in 2022.

Were it not for the forex losses, profit would have been N344.5 billion i.e. down by 14.3%. Free cash flow was up 11.6% to N631.6 billion. Sadly, we cannot simply ignore the impact of the naira.

The MTN share price is down 41% in the past 12 months. Considering it peaked at over R200 in February 2022, the ride down to the current level of R84 has been painful.

Despite earnings collapsing at Northam, there’s a dividend for this period (JSE: NPH)

Profit margins sharply deteriorated in 2023

This was an action-packed period for Northam Platinum, with the six months to December 2023 including some major corporate activity and the ugliness of a drop in PGM prices.

Dealing with the former, Northam Platinum accepted the mandatory offer from Impala Platinum for Royal Bafokeng Platinum and obtained R9 billion in cash and a whole lot of Impala Platinum shares. This was because Northam effectively gave up on the bidding war for Royal Bafokeng. Northam subsequently disposed of the shares in Implats for R3.1 billion and recognised a R800 million loss. All in all, shareholders won’t look back on the Royal Bafokeng gamble with any joy.

Moving on to the operational stuff, it’s never going to end well when the PGM basket price drops by 42.3% in a given period in ZAR. The pressure on the palladium price has been driven by lower demand for catalytic converters in internal combustion engine vehicles. The rhodium price has dropped because of substitution for platinum in the fibreglass industry, which sounds to me like a more permanent problem.

Northam gives a bearish outlook that notes a depressed pricing environment for the next 12 to 24 months. They are therefore fully focused on preserving liquidity, which is why they got out of the Royal Bafokeng / Implats situation as quickly as they could, taking the tried and tested approach in the markets of the first loss being the best loss.

Despite the focus on liquidity, the company declared an interim dividend of 100 cents per share despite HEPS collapsing by 92.5% to 121.4 cents. That’s a pretty high payout ratio for such a tough environment. The decision to declare this dividend would’ve been supported by the cash position of R11.8 billion in the group, with undrawn banking facilities of R11 billion.

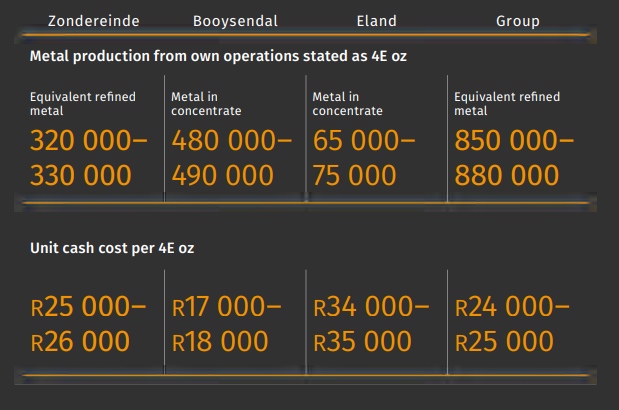

The real concern for Northam is the cash cost of the various operations vs. the current PGM price. Bearing in mind that the ZAR 4E basket price was R24,269 for the six months to December 2023, this unit cash cost guidance for 2024 is not encouraging:

At these commodity pricing levels, only Booysendal is profitable. Eland is losing money at an alarming rate and Zondereinde is marginal. The group as a whole is therefore marginal as well.

The Northam share price is down 30% in the past 12 months and unless there is a meaningful improvement in PGM basket prices, things won’t get better from here. The light at the end of this tunnel could be the world realising that EVs may not be the answer, with plenty of headlines suggesting that the EV-or-nothing silliness of global automotive manufacturers is being toned down significantly. This would be supportive of PGM prices.

Little Bites:

Director dealings:

Johan Holtzhausen is a non-executive director of KAP (JSE: KAP) and has vast experience in corporate finance, so I would pay attention to the fact that an associate entity of Holtzhausen bought shares in battered and bruised KAP worth R750k. The average price was R2.21.

An associate of a director of Huge Group (JSE: HUG) bought shares worth R107k.

Stefanutti Stocks (JSE: SSK) has reached an in-principle agreement with lenders to extend the capital repayment profile of the loan out to June 2025. They are busy amending the current facility agreement, with a short-term extension given until 27 March 2024 to conclude the amendments.

Salungano Group (JSE: SLG) is going through a tough time at the moment and is suspended from trading. In positive news, the company has announced the appointment of three new independent non-executive directors, all of whom are highly experienced in various commercial roles.

London Finance & Investment Group (JSE: LNF) is one of those completely off-the-radar listed companies on the local market. For the six months ended December 2023, HEPS fell by 51.6% (measured in GBP) and the dividend increased by 9.1% to 0.60 pence per share.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

AB InBev’s Q4 profits dip despite revenue growth (JSE: ANH)

Volumes fell in 2023, with pricing taking revenue growth into the green

It was a lot more expensive to drink in 2023 than the year before. We know this because although full-year volumes at AB InBev fell by 1.7%, revenue was up by 7.8%. This can only be because of pricing increases.

This makes things tricky for AB InBev, as manufacturing companies need volumes to keep growing in order for efficiencies to be realised. Normalised EBITDA margin for the full year contracted by 23 basis points to 33.6%. At least the fourth quarter impact was minor, down 2 basis points to 33.7%.

Profits for the full year came in at $6,158 million vs. $6,093 million in the prior year, so there’s a small uptick there. For the fourth quarter though, they fell from $1,739 million to $1,661 million.

Net debt to normalised EBITDA was 3.38x at 31 December 2023, an improvement from 3.51x at the end of 2022.

Choppies has a good story to tell, but not at HEPS level (JSE: CHP)

This is what happens when you issue lots of new shares under a rights offer

Choppies has announced an interim dividend of 1.6 thebe per share. In case you didn’t know, the thebe is the cents currency of Botswana (i.e. 100 thebe equals 1 pula), which is where Choppies has its primary listing! This is compared to no interim dividend being paid last year, so there’s some good news for shareholders.

This is because the company seems to be doing a lot better, with revenue up 21% and operating profit up 28%. Despite profit being up 41%, HEPS could only move 2% higher. This is because there are many more shares in issue after the recent rights issue.

To give you a sense of the dividend payout ratio, HEPS was 5.3 thebe and the dividend was 1.6 thebe per share as mentioned, so they are still retaining a lot of earnings.

Ellies is now technically insolvent (JSE: ELI)

The tangible net asset value per share is negative

At Ellies, the results for the six months ended October 2023 probably signal the death of the company, at least in its current form. Revenue is down 30.6%, the headline loss per share was a massive 13.27 cents and the net tangible asset value per share has moved from 12.3 cents to -7.3 cents.

The group is now in business rescue. Good luck to Standard Bank getting their money back on the term facilities and general banking facility. Hopefully the notarial bond over moveable assets will work out well for them.

As for equity holders, you can perhaps ask for the share certificates and frame them on the wall to remind you not to invest in basket cases.

FirstRand: only keeping up with inflation (JSE: FSR)

The dividend is up by 6%

It’s tough for the large banking groups in South Africa, as there is practically no economic growth to help them. What does help of course is inflation and higher interest rates, offset to varying extents by impairments. A group like Standard Bank is growing strongly in Africa at least, whereas the others are reporting far more pedestrian numbers.

FirstRand is the perfect example, with the ordinary dividend up by only 6% per share. Normalised return on equity has fallen from 21.6% to 20.6% for the six months to December. The highlight here is a 14% increase in normalised NAV per share, which is one of the key valuation inputs for the share price.

Looking at top-line growth, it was all about net interest income (up 14%) rather than non-interest revenue (up just 4%). Operating expenses increased 9% and impairments were 28% higher, hence why normalised earnings were only up by 6%. The credit loss ratio has increased from 0.74% to 0.83%.

The share price is down 3% over the past 12 months. In contrast, Standard Bank is up 8.9%. In both cases, this excludes dividends.

Fortress expects to start paying dividends (JSE: FFB)

This is thanks to the deal that sorted out the share structure by using NEPI Rockcastle shares

After a long journey to try and sort out the dual-class share structure into something sustainable, Fortress must be feeling chuffed to announce that distributions are expected for the first half of the 2024 financial year. Distributable earnings themselves are up 19%, but the share structure has changed completely, so reflecting this on a per-share basis isn’t useful for comparability.

It is useful for shareholders to see the anticipated dividend per share being 81.44 cents. The forecast for the second half of 2024 is 60.44 to 65.57 cents, with full year distributable earnings expected to be between 10.9% and 14.0% lower. This is due to the impact of the group having used a big chunk of the NEPI Rockcastle investment to settle shareholders.

Grindrod Shipping reports a loss for the year (JSE: GSH)

If you want a steady investment, stay far away from shipping

All cyclical industries are painful, but some are more painful than others. After shipping made an absolute fortune during and immediately after the pandemic, the cycle turned with a vengeance and Grindrod Shipping generated a loss for the six months to December of $9.2 million as shipping rates dropped further.

After modest profits in the first half of the year, the full-year loss was $7.9 million.

The focus at this point in the cycle has been to reduce debt, with $56.9 million worth of debt cleared in 2023. Cost efficiencies across the fleet are also a priority, especially with shipping rates under pressure.

The dividends continue at Hammerson (JSE: HMN)

Key metrics are looking better for the group

In its full year 2023 results, Hammerson has highlighted like-for-like gross rental income growth of 6% and a reduction in administrative costs of 14%. Adjusted earnings were up 11% thanks to these efforts.

Importantly, net debt was down 23%. The loan-to-value came in at 34% after a disposal programme strengthened the balance sheet.

After reinstating dividends at the half-year mark, the company has recommended a final dividend that brings the full-year dividend to 1.50p per share. The policy is to pay between 60% and 70% of annual adjusted earnings, so don’t expect a cash cow here like you’ll find in most SA REITs.

Impala Platinum’s detailed interims are now available (JSE: IMP)

As we already knew, they aren’t pretty

The recent performance of PGM miners is no secret. We’ve had a few updates from the sector as a pre-cursor to the release of detailed numbers. It therefore might upset you, but shouldn’t shock you that HEPS at Impala Platinum is down by 77.9% for the six months to December 2023.

With revenue down by 24.9% as PGM prices plummeted, the rest of the income statement never really stood a chance.

There is no dividend for this period, with a free cash outflow of R4.76 billion vs. an inflow of R11 billion in the comparable period.

With group unit costs expected to increase by between 6% and 10% for the full year, they really need PGM prices to go the right way.

Murray & Roberts is still making losses (JSE: MUR)

Yes, even from continuing operations

Murray & Roberts is in esteemed company, as one of the many South African businesses that got a klap in Australia. We shouldn’t play cricket there and in most cases, we shouldn’t do business there either. Send the Bokke to represent us and be done with it.

With the company’s Aussie subsidiaries having been placed into voluntary administration in December 2022, the size of the group has been significantly reduced. The balance sheet needed to get smaller too, with debt down to R400 million from R2 billion in April 2023. They need to refinance the remaining debt by June 2024.

For the six months ended December 2023, the headline loss per share from total operations (i.e. including the loss from the deconsolidation of various entities) was between -29 cents and -24 cents. It’s a vast improvement from -322 cents in the prior period, but it’s still a loss.

From continuing operations only, the group has improved slightly from a headline loss per share of -27 cents to an expected range of -19 to – 14 cents.

And this, dear friends, is why the share price looks like an exciting thing to try on a snowboard in the winter:

Pepkor says goodbye to The Building Company (JSE: PPH)

Private equity buyers have swooped in to give Pepkor an exit from this asset

The building materials sector hasn’t exactly been a great place to play recently, with Pepkor deciding to exit its investment in The Building Company. The main brands here are BUCO, Timbercity and Tiletoria.

The buyer is Capitalworks Private Equity and selected members of management, so this is a classic management buyout deal. The price is R1.2 billion. This isn’t a categorisable transaction, so we aren’t getting any further details than that.

A dig through the Pepkor financials reveals revenue for the building materials segment of R8.4 billion for the year ended September 2023. The disclosure is quite light in 2023, but I found a profit number for 2022 (off much the same revenue) of R462 million.

I would guess that the profit multiple for this deal is around 3x, which tells us that Pepkor was just happy to get rid of the thing. Good luck to management and the new buyers!

Sanlam’s HEPS has moved much higher (JSE: SLM)

A solid result in the financial services business helped drive this outcome

Ahead of the release of detailed 2023 results on 7 March, Sanlam released a trading statement noting a beautiful jump of between 44% and 54% in HEPS for the year ended December 2023.

This was driven by a strong improvement in the cash result from financial services, which increased by between 15% and 25% on a per-share basis. Overall growth in the book and an improved risk experience in the life insurance business were helpful here, amongst other things.

Net operational earnings per share was up by between 23% and 33%, with higher investment returns on the shareholder capital portfolio.

Sanlam’s share price is up 20% in the past 12 months.

The weather – and general life in South Africa – are making short-term insurance a tricky game

For the year ended December 2023, Santam’s group insurance revenue increased by 9%. HEPS was up by 27%, with the vast gap between those numbers explained by a major uptick in the return on shareholders’ funds rather than by great underlying results in the insurance business.

In fact, conventional insurance net underwriting margin deteriorated from 5.1% in 2022 to 3.5% in 2023. This is why underwriting profit fell by 26%, impacted by all kinds of weather-related problems and even the earthquake in Turkey!

Importantly, the investments in India and Malaysia reflected revenue growth of 31%, with the Indian business as the major driver here.

The dividend is 7% higher at 905 cents per share.

Shaftesbury grows the dividend (JSE: SHC)

The London-based portfolio is delivering growth

In the year ended December 2023, Shaftesbury grew gross income by 10.4% on a like-for-like basis. Still, the environment of higher rates meant that the wholly-owned portfolio saw its valuation drop by 0.8%.

Notably, the loan-to-value has increased from 28% to 31% over the past year. Anything in the 30s is pretty normal for a property fund.

The final dividend of 1.65 pence per share takes the full-year dividend to 3.15 pence per share.

The medium-term growth prospect is 5% to 7% per annum. Of course, the total return to investors will depend greatly on property valuations and the cap rates being applied.

At this valuation, I’m not surprised they’ve agreed to sell

South32 has agreed to sell Illawarra Metallurgical Coal in Australia to Golden Energy and Resources and M Resources. The buyer is a lot less important than the price, with the deal being worth up to $1.65 billion, of which $1.05 billion is payable at completion. $250 million is payable in 2030 as deferred consideration and there’s a contingent amount of up to $350 million as well.

Assuming the total is received, that’s a multiple of 7.2x average annual free cash flow. Although the deferred amount is years away and should be present valued at a suitable discount rate, thereby reducing the effective multiple being received, it’s still a strong price.

Aside from unlocking the capital, the deal simplifies South32’s business and reduced its capital intensity.

Spur reports impressive momentum (JSE: SUR)

This was a positive surprise for me

Spur has been doing really well lately, with restaurant brands that resonate with customers looking for value offerings and somewhere for the kids to have a jol. The fact that Spur is doing well in general isn’t a surprise for me. The results for the six months to December 2023 are a surprise though, as retail mall commentary for the period was that quick-service restaurants didn’t have a great time.

So if Spur did well, are we in for a famous disappointment elsewhere? Time will tell.

Sticking to those with a taste for life, turnover was up 10.4% in total and 9.0% excluding the Doppio Collection. There’s no debt on the balance sheet, so shareholders get the juicy benefits of a 16.4% increase in HEPS.

The interim dividend is up by 15.8% to 95 cents per share.

The group has highlighted the benefit of tourism numbers for the Western Cape (and to a lesser extent, KZN) restaurants in December.

Spur’s share price is up 22% in the past year, which is an exceptional outcome relative to other consumer plays.

Not much to write home about at Truworths (JSE: TRU)

But at least earnings have moved higher, so that’s something

Truworths has released results for the 26 weeks ended 31 December 2023. Apparel retailers had a pretty decent end to 2023, with Truworths reflecting 8.5% growth in sales of merchandise. Gross profit margins were steady at 53.6% vs. 53.5% in the comparable period. Operating margins unfortunately fell slightly by 20 basis points to 24.5%.

Once we get to HEPS level, the increase is only 3.6%, with a 36.7% increase in finance costs playing a major role here. The interim dividend is 3.8% higher. It’s positive at least, but not by much.

The highlight is probably cash generated from operations, which increased from R1.7 billion to R2.7 billion. Net debt is down from R854 million to R124 million, so the balance sheet looks better.

At segmental level, the star of the show was the Office business in the UK, achieving growth of 33.1% in rands (and 15.6% in GBP). Truworths Africa was down 0.3%, so the group was a relative loser vs. some of its peers in South Africa.

In terms of outlook, sales for the first seven weeks of the new period increased by 3.8%. South Africa is down 0.5% and Office is up 1.3% in GBP. On this basis, I would be careful of Truworths this year, as the UK carried it through 2023 and the growth there seems to have moderated.

Little Bites:

Director dealings:

Sean Riskowitz, seemingly acting in his personal capacity for once, bought shares in Finbond (JSE: FGL) worth R5.34 million.

The wife of the CEO of Shaftesbury Capital (JSE: SHC) bought shares in the company worth £110k.

An executive of BHP (JSE: BHG) has bought shares worth A$70k.

A non-executive director of Primary Health Properties (JSE: PHP) has bought shares in the company worth £25k.

Equites (JSE: EQU) released a pre-close presentation that is worth digging into if you’re a shareholder. The loan-to-value ratio is down from 42.3% at August 2023 to an estimated 41.5% at February 2024, with disposals in the UK as the major positive driver and various acquisitions in South Africa limiting the decrease. The cost of debt in South Africa is up from 8.58% to 9.11% in the past year. In the UK, the cost of debt is down from 4.15% to 3.62% over the same time period. Dividend per share guidance of 130 – 140 cents per share for FY24 is unchanged.

MTN Ghana, part of MTN (JSE: MTN), released results for the year ended December 2023. Service revenue was up 34.6% in local currency and EBITDA margin increased by 230 basis points to 58.4%. Total capex was up 90.3% though, so the same story keeps applying around lack of cash coming from these businesses. With macroeconomic issues continuing, the African subsidiaries are focusing on in-country investments.

EOH (JSE: EOH) announced that the PAYE dispute between SARS and EOH Abantu has been settled, with the company owing R112 million to SARS before 1 March 2024. The company had already provided for this. EOH Abantu must also forfeit a tax receivable credit of R6.9 million, which hadn’t been provided for. The assessed loss of R34.5 million is also gone, with no impact to the financials as no deferred tax asset had been raised anyway. Standard Bank has increased the debt facility by R63 million, which is the shortfall for EOH Abantu to settle the tax.

Sirius Real Estate (JSE: SRE) has acquired a German business park for €13.75 million, marking the third German acquisition this year. The deal has been funded from the proceeds of November’s capital raise. For some reason, the announcement doesn’t mention the acquisition yield.

DRA Global (JSE: DRA) has released results for the year ended December 2023. Revenue may be down by 1% but profits are up by 190% to $19.7 million. No dividends have been paid for this period, despite the turnaround in financial performance. The group has noted a strong project pipeline and the share price closed 17.42% higher, admittedly on low volumes as usual.

Salungano Group (JSE: SLG) is currently suspended from trading and thus needs to release a quarterly update. The reason for the suspension is that FY23 results haven’t been released, with business rescue of yet another subsidiary causing further complications. They expect to release FY23 results by mid-April and interim 2024 results as soon as possible thereafter.

The listing of Collins Property Group (JSE: CPP) will be transferred to the Industrial REITs subsector of the JSE with effect from 18 March 2024. This is important in terms of index funds and even actively managed funds being able to hold the shares, as mandates of even actively managed funds can be quite narrow.

Earlier this week, Anglo American (JSE: AGL) and some of its subsidiaries announced good news regarding a renewable energy deal with Envusa Energy, in which Anglo American holds a 50% stake. The latest news is that Envusa has completed the project financing for its first three wind and solar projects in South Africa, collectively called the Koruson 2 cluster of projects. This is a wind and solar operation located on the border of the Northern and Eastern Cape. Anglo American Platinum, Kumba Iron Ore and De Beers have committed to 20-year offtake agreements.

Capitalworks Private Equity has acquired The Building Company (TBCo) from Pepkor for R1,2 billion. Select members of TBCo’s management team are investing alongside the private equity company. The disposal will streamline Pepkor’s portfolio of businesses, while for TBCo the deal will position it strategically and operationally to pursue future growth.

South32 has entered into an agreement with Golden Energy and Resources Pte and M Resource to dispose of Illawarra Metallurgical Coal. South32 will receive an upfront cash consideration of US$1,05 billion, a deferred cash consideration of $250 million and a contingent price-linked cash consideration of up to $350 million. The deal is in line with the company’s strategy to unlock value for shareholders.

Sirius Real Estate is to acquire its third German business park this year for €13,75 million. The business park is situated in Klipphausen, near Dresden.

Hammerson plc has disposed of Union Square, a 52,000m² shopping centre in Aberdeen, Scotland to US-headquartered Lone Star Real Estate Fund VI for £111 million in cash. The proceeds of the disposal will be used to strengthen the balance sheet. The sale of Union Square concludes the company’s £500 million non-core disposal programme initiated in early 2022.

Kibo Energy has finally parted ways with the institutional investor-led consortium led by Proventure Holdings (UK) and announced a funding agreement with new strategic partner RiverFort Global Opportunities. The initial funding facility is up to £4 million. The funds will predominantly be used to fund the Pyebridge 9MW flexible power generation asset out of care and maintenance.

Life Healthcare has declared a gross special dividend of 600 cents per ordinary share. The dividend is payable from income reserves and is the distribution of the net proceeds received following the disposal of the Group’s interest in Alliance Medical Group. Payment date is expected on 8 April 2024.

Trustco reminded shareholders in its cautionary announcement that the company is in the process of concluding several pivotal transactions with key shareholders. There is a planned equity investment in the amount of c. N$950 million by Riskowitz Value Fund by way of a fresh issue of Trustco shares to RVF. In addition, Trustco is also considering increasing its equity stake in Legal Shield to 91.35% by acquiring 11.35% from RVF. To top this off, the company is also considering a Rights Offer to minority shareholders – so to enable them the opportunity to participate in the company’s growth and to minimise the dilutionary effect.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 19 – 23 February 2024, a further 3,510,037 Prosus shares were repurchased for an aggregate €99,24 million and a further 237,724 Naspers shares, for a total consideration of R780,48 million.

AB InBev has repurchased a further 224,067 shares at an average price of €58.37 per share for an aggregate €13,08 million. The shares were repurchased over the period 19 – 23 February 2024.

Santova has advised that it has applied to the JSE for the cancellation of 4,328,877 shares which were repurchased by the company at an average price of 743,50 cents per share. Following the cancellation of the Treasury Shares, the share capital of the company will comprise 129,609,951 ordinary shares of no par value.

Collins Property Group was granted REIT status by the JSE with effect from 21 December 2023. The company’s shares will now be transferred from the Real Estate Holding and Development subsector to the Industrial REITs’ subsector with effect from the commencement of trade on 18 March 2024.

Six companies issued profit warnings this week: Mustek, Thungela Resources, Ellies, Putprop, African Rainbow Minerals and Murray & Roberts.

Five companies either issued, renewed, or withdrew cautionary notices this week: Afristrat Investment, Salungano, Trustco, Chrometco and PSV.

Creating value from environmental, social and governance (ESG) considerations has gained importance in M&A1. Companies are examining how they can leverage a target’s ESG strengths to promote revenues, profits and balance sheet efficiencies for the combined business. Such synergies often feature prominently in the equity story presented to investors, and can play a major role in boosting total shareholder returns.

Acquirers face numerous challenges, however. Although the quality of ESG reporting has improved among large companies over the past five years, the use of multiple standards and frameworks complicates efforts to understand and compare their ESG performance. Additionally, relatively few middle-market companies fully report their ESG performance. This makes it difficult to pinpoint ideal targets for bolt-on acquisitions, both from an immediate standpoint and with regard to long-term ESG-related value drivers, such as talent retention and brand visibility.

To overcome the challenges of unlocking ESG synergies, acquirers need to integrate ESG considerations throughout the M&A process, from pre-deal due diligence to post-merger integration.2

ESG synergies are often significant

Traditionally, acquirers have mainly addressed ESG during the risk assessment in their due diligence efforts, in order to mitigate the risks and preserve the target’s value. ESG risk mitigation continues to be a fundamental aspect of the pre-deal assessment. An acquirer needs to integrate targets into its ESG compliance and reporting standards, and avoid potential downgrades of the combined entity’s ESG score. It also must assess the impact on integration costs if the target does not comply with its ESG objectives.

But ESG synergies go beyond risk mitigation. They encompass the ways in which an acquirer can generate value for the combined entity by utilising its own ESG practices and those of the target, as well as by implementing new operating models and generating scale effects. This value can be quantifiable or nonquantifiable.

Quantifiable value is created by ESG synergies that directly affect the income statement. These include, for example: • Driving recurring cost savings through measures such as enhancing operational efficiency in conjunction with decarbonisation,3 and implementing more sustainable procurement and supply chains. • Increasing revenue, such as by overcoming regulatory barriers to access new markets, increasing customer engagement or raising prices. • Improving the cost of capital, such as by mitigating risks, gaining access to alternative funding, or optimising capital expenditures, investments and assets.

Nonquantifiable value arises from the impact of ESG synergies on the acquirer’s equity story and total shareholder return (TSR). A BCG study4 found that deals emphasising ESG considerations tend to outperform other deals, in terms of cumulative abnormal returns upon announcement and two-year relative TSR.

For example, enhanced ESG scores and ratings may lead to higher valuations by reducing the cost of capital and facilitating better access to capital markets. Moreover, if an acquirer materially improves its ESG performance by integrating a target, it may attract new types of investors and broaden the investor base, leading to further capital-raising opportunities and long-term growth.

Addressing ESG synergies in three phases

Acquirers can extract maximum value from their ESG investments by utilising a traditional approach to synergies. The following steps serve as a guide for unlocking ESG synergies.

Conduct ESG due diligence before signing the deal

Before the due diligence phase or the initial stages of public takeovers, it is vital to pinpoint the most significant ESG factors for both the target company and the potential combined entity. Utilise publicly accessible data to perform an outside-in assessment of material ESG-related risks and opportunities. Gain a clear understanding of the most important sustainability issues in the industry, along with the trends and technologies that should be prioritised and accelerated. If ESG presents substantial risks or is central to value creation, leverage data from the target during the due diligence process to evaluate risk exposure, identify mitigation opportunities, and formulate preliminary synergy hypotheses.

Validate ESG risks and opportunities between signing and closing

After signing the deal, use the additional information available to validate the assessment of ESG-related risks and opportunities, describe the synergies in detail, and develop an implementation plan. Support from a “clean team” composed of third-party personnel is valuable during this stage. Although antitrust laws prohibit merging companies from sharing sensitive information before the closing, the clean team can analyse data from both companies and share sanitised, interim results with both integration teams.

The validation process includes collecting data, harmonising ESG metrics and taxonomies, consolidating ESG baselines, and synthesising hypotheses. The output is a prioritisation of material ESG factors, along with initial estimates of savings potential. Substantiate synergies by having the clean team conduct initial analyses, and refine top-down synergy targets derived during due diligence. This phase also includes prioritising ESG initiatives by materiality, assigning and communicating targets, and refining integration costs.

Finally, plan the execution of ESG synergies. Start by validating bottom-up synergy targets with functional teams from, for example, finance, procurement, sales, marketing and HR. This provides the basis for prioritising longer-term opportunities and aligning on new or renewed ESG priorities and ambitions to include in detailed implementation plans.

Implement ESG Synergies from Day 1

After the deal closes, start implementing ESG synergies right away. To obtain comprehensive data about the acquired company, engage in open-book discussions, town hall meetings or small group sessions. Use this detailed information to validate targets and plans developed in earlier phases, execute risk management and savings initiatives and, if necessary, reprioritise longer-term opportunities. The execution phase is also the time to fine-tune the new or renewed ESG priorities and ambitions for the combined entity, as well as to define a roadmap for capturing the value. Finally, create a culture of collaboration among teams from acquirer and acquiree so that they can pursue shared goals aimed at enhancing the combined entity’s ESG performance and unlocking further value.

As ESG topics gain importance as motivations for M&A, acquirers should determine the forward-looking actions that the combined entity can take to generate value through ESG synergies. Acquirers that succeed will promote sustainability goals and ensure that the combined entity’s performance is more than the sum of its parts.

Get the latest recap of JSE news in the Ghost Wrap podcast, brought to you by Mazars:

AECI calls this a “year of transition” – and shareholders will hope that’s the case (JSE: AFE)

Nobody likes to see a final cash dividend drop by 79%

AECI has released results for the year ended December 2023. They reflect revenue up 5.4% and EBITDA up just 3.2%. Once you factor in the nasty things below EBITDA at this stage in the interest rate cycle, you end up with HEPS down 11.7%.

Despite unlocking some working capital in this period (and cash from operations increasing by 4.3%), the final cash dividend has dropped by 79% to 119 cents.

AECI is celebrating its 100th anniversary in 2024 and is calling it a year of transition, with the goal of doubling profitability of the core businesses (mining and chemicals) by 2026. It’s interesting that both are referenced here, as the mining business did really well in 2023 (EBIT was a record, having grown 18.2%) and chemicals had a tough year (EBIT down 8.5%).

And in case you’re wondering about the problematic AECI Schirm business, it sits in AECI Agri Health. This segment grew revenue by 8% to R7.6 billion but reported an EBIT loss of R192 million.

There aren’t a lot of highlights in the 2023 numbers as the pre-cursor to the centenary year, but at least net debt improved from R5.345 billion to R4.338 billion coming into 2024.

African Rainbow Minerals flags a big drop in HEPS (JSE: ARI)

A drop in PGM and thermal coal prices are to blame here

African Rainbow Minerals released a trading statement for the six months to December 2023. HEPS is expected to be roughly 40% to 50% lower, coming in at between 1,319 cents and 1,583 cents for the period. This is because of a 43% decline in the PGM basket price (in dollars) and lower thermal coal prices. The weaker rand couldn’t offset these impacts.

Due to substantial impairments, EPS will be between 70% and 80% lower.

Cashbuild drops another 8% after releasing results (JSE: CSB)

This is despite a previously released trading statement

I’ve been writing extensively on the challenges faced by South African retailers, particularly in the home improvement and DIY sector. Cashbuild is a great way to see how bad it has been, with Italtile added to this chart for further context:

Things didn’t get any better in the six months ended 24 December 2023, with Cashbuild’s revenue up only 2% and HEPS down by 20%. The dividend of 325 cents is down 19%, tracking HEPS lower.

The metrics simply don’t work right now. Gross profit margin deteriorated from 25.3% to 24.7% and operating expenses increased by 5% in existing stores, so the profits never really stood a chance.

If you include the impairment of R137 million, then basic EPS decreased by 98%. I’m not usually one to mention EPS, but that’s a particularly nasty outcome that talks to value destruction in this environment.

To make things worse, stock levels increased by 10% despite the asthmatic performance in revenue, so that’s not good for the working capital cycle either.

There’s no sign of improvement, with revenue for the six weeks subsequent to period end showing a flat performance vs. the comparative period.

Harmony signs off on an excellent period (JSE: HAR)

You won’t often see HEPS growth of 226%

Harmony has released results for the six months ended December 2023. As we already knew, they are excellent.

HEPS is up by a whopping 226% to R9.56 per share and there’s a record interim dividend of R1.47 per share. Operating free cash flow? That was also a record, up 265% to R7.1 billion.

No matter where you look, the numbers are great year-on-year. Not only did Harmony enjoy higher gold prices, but they took advantage of them with a strong jump in production and a 5% decrease in all-in sustaining costs.

It all looks good for the full-year numbers, with annual production and grade expected to be at the upper end of guidance and costs well below the guided level.

When gold mines do well, they do really well. The share price has nearly doubled in the past 12 months.

The hard times continue at KAP (JSE: KAP)

The share price has lost over 70% of its value over 5 years and profits have plummeted

KAP has reported on a period that the company will want to forget. For the six months to December, revenue was down 2% and operating profit fell by 17% as operating leverage worked against the company (a larger percentage decrease in profits than in revenue due to fixed costs). HEPS fell by 36%!

If you’re looking for silver linings, you could consider the R914 million improvement in net working capital, or the R708 million reduction in net interest-bearing debt. Much as this helped to mitigate some of the pain of the finance costs, a 20% increase in net finance costs is why the HEPS performance looks so ugly.

KAP is really just the outcome of various businesses mixed together, so it’s critical to look at the segments.

PG Bison grew revenue by 9% to nearly R2.9 billion, while operating profit increased by 18% to R575 million. This is one of the good news stories. Safripol is at the other end of the spectrum, with revenue down 8% and operating profit down 67% to R178 million as raw material margins deteriorated. Unitrans is another tough story, with revenue down 7% and operating profit down 21% to R264 million, with non-recurring restructuring costs of R30 million playing a significant role there.

Moving into the smaller segments, Feltex enjoyed an improvement in South African vehicle assembly volumes, growing revenue by 24% and operating profit by 31%. Restonic saw revenue increase 8% and operating profit almost triple from R34 million to R99 million. Restonic’s operating profit margin of 10.2% is still below the long-term guidance of 13% to 15%.

Finally, Optix could only manage a flat revenue performance and break-even at operating profit level, down from profits of R10 million a year ago. Let this be an ongoing lesson in how hard it is to scale a business.

Don’t get your hopes up for much improvement in the latter half of the year, as the company expects elevated levels of debt due to the extent of capital projects. One of the biggest and most exciting is PG Bison’s MDF project, which will increase the division’s total production capacity by 33%. Perhaps most of all, KAP needs the supply and demand situation to improve in the polymer business, with no immediate improvement expected.

Kibo has finally laughed off the Proventure joint venture (JSE: KBO)

It’s been pretty obvious to everyone else for a while that it wasn’t going to happen

When the smell of nonsense starts to emanate from a transaction, it’s usually because there are layers of the brown stuff hidden underneath. As soon as you see things like a payment that couldn’t be made due to an administrative issue, or a banking problem, the red flags should be going up in your brain.

Kibo Energy hasn’t exactly had many alternatives for funding in subsidiary Mast Energy Developments (MED), so they had to flog this delightfully dead horse for a long time just in case it came back from the dead. Thankfully, due to an alternative deal with RiverFort, the Proventure joint venture is now dead and the company will try and claim damages etc. from Proventure under the terms of the joint venture agreement. Good luck to them.

Onto the new deal then, which will see RiverFort provide an initial funding facility of up to £4 million. The goal here is to lift MED’s Pyebridge 9MW flexible power generation asset out of care and maintenance and into a revenue generating state during April 2024. Make no mistake here: RiverFort will get its pound of flesh, with the facility being convertible into preference shares in Pyebridge.

The market doesn’t seem to care, with the Kibo share price not budging off R0.01 per share. There are so few bids in the market for this thing and there are many offers at R0.02, so it will take a lot to lift this share price off the lowest possible level.

Life confirms the quantum of the special dividend (JSE: LHC)

Investors have been waiting to see what they will get from the Alliance Medical disposal

After quite a wait, shareholders of Life Healthcare now know that the special distribution will be 600 cents per share. This means that R8.8 billion is being distributed to shareholders, which is higher than the estimation of R8.4 billion that was provided in the circular.

To give more context to this amount, the company received £845.9 million for the disposal of Alliance Medical (roughly R20.5 billion) and repaid R10.2 billion to the South African holding company after settling international debt, as well as transaction and hedging costs. Life Healthcare is retaining R1.4 billion to partly fund the acquisition of the renal businesses of Fresenius Medical Care and to support growth opportunities at Life Molecular Imaging.

After the distribution, the level of gearing will be 0.8x net debt to EBITDA.

On a share price of R17.44, a special dividend of R6 per share is material.

Canal+ must make a mandatory offer for MultiChoice (JSE: MCG)

The Takeover Regulation Panel (TRP) has also flexed its muscles here

MultiChoice didn’t win any friends at the TRP recently by making rather unusual announcements related to the Canal+ saga. The TRP needs to approve announcements when a takeover process has been triggered, so a compliance notice has been issued against MultiChoice due to that breach in process. MultiChoice is taking that on appeal.

The more important news is that the TRP has also ruled on whether Canal+ needs to make a mandatory offer to shareholders of MultiChoice, having breached the 35% ownership threshold that triggers a mandatory offer.

The debate here was how to apply the provisions of the Memorandum of Incorporation that limit voting rights of a foreign shareholder to 20%, regardless of how many shares they hold. The TRP didn’t accept that this avoids a mandatory offer, as there are circumstances where the 20% voting restriction wouldn’t apply and Canal+ would have more than 35% voting rights on such matters.

If you’re terribly bored (or very keen on the law) and want to read the entire TRP ruling, you’ll find it here.

We don’t know for sure what the mandatory offer price will be, but we can be very confident that it is below the R105/share that Canal+ was happy to offer shareholders (and which the MultiChoice board gave a resounding “no” to). In other words, I think Canal+ would be very happy to pick up shares at the mandatory offer price.

The dividend is higher at Primary Health Properties (JSE: PHP)

But the share price hasn’t gotten off to a good start on our market

South African investors don’t have much love in their hearts for UK-based property funds that achieve limited growth in rental income. This is why many local property funds have looked to higher inflation regions, like Poland or Spain, as this is seen as friendly territory for South Africans.

Still, it’s not bad going that Primary Health Properties grew net rental income by 5.5% and the dividend per share by 3.1% to 6.7 pence. Goodness knows that the rand does a good job of driving a larger increase when expressed in ZAR.

With a loan to value ratio that has moved from 45.1% at the end of December 2022 to 47.0% at the end of December 2023, along with the average cost of debt going from 3.2% to 3.3%, there are reasons to be cautious about this property fund. Although it is true that debt may be fixed rate in nature, the reality is that any refinancing of debt in the near-term is likely to increase the weighted average cost of debt even further.

It’s rather interesting to note that Ireland is the focus area for investment, with the goal being to grow the portfolio there to 15% of total group exposure from the current level of 9%.

The share price is down 27% just this year. It has more than halved since listing.

Standard Bank keeps waving its flag (JSE: SBK)

It’s a good time to be a bank – especially a good bank

This is a point in the cycle where banks should be doing very well, as interest rates are high and companies have to keep borrowing to fund balance sheets that need to get bigger due to inflation. Not every bank is taking advantage of this properly, but Standard Bank certainly is.

HEPS is up by between 23% and 28% for the year ended December 2023, coming in at between R25.22 and R26.24. The market seems to have priced this in, with the share price closing 0.5% lower at just under R204.

Texton reports a sharp drop in distributable earnings (JSE: TEX)

And there’s no dividend for the interim period

Texton is a short story about a company that doesn’t understand what to do when the share price is trading miles below the NAV per share. Instead of doing buybacks at R2.51 on a NAV per share of R7.12, they choose to keep investing in properties.

This tells you that minority shareholders probably aren’t going to experience a great outcome here. If that doesn’t convince you, then perhaps a 17.1% decrease in distributable earnings will.

The only highlight is that the NAV per share is up 16.8%, with the share price up 23% over 12 months. This means that the discount to NAV has closed slightly. Now just imagine what a few share buybacks would do!

Even Woolworths can’t do well in this environment (JSE: WHL)

Stock availability challenges plagued the FBH business– but was it an own goal?

It’s tough out there. Really it is. Woolworths could only manage 5.4% growth in turnover and concession sales from continuing operations (i.e. excluding David Jones from the prior period) for the 26 weeks ended 24 December 2023, which sadly led to a drop in adjusted diluted HEPS of 5.6%.

And if you aren’t sure about whether to use adjusted numbers, then you could just consider the 6.6% decrease in the interim dividend per share as a way to gauge performance.

With group return on capital employed of 22.3%, I am not sure why the company retained the Bourke Street property in Melbourne as an investment asset after the disposal of David Jones. Woolworths needs to be generating returns way in excess of what property can deliver. When times are tough, having drags on the balance sheet doesn’t make a whole lot of sense.