There may have been many public holidays in April, but that didn’t stop the market from reacting to the broader geopolitical turmoil. With recession concerns as a key theme, which stocks did well and which ones delivered a nasty drop? This podcast is an overview of recent big share price moves among larger local companies on the JSE, revealing some interesting trends.

The Ghost Wrap podcast is proudly brought to you by Forvis Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Forvis Mazars website for more information.

Listen to the podcast here:

Transcript:

April may have been filled with public holidays, but that doesn’t mean that we didn’t see some meaningful moves on the local market. For this edition of Ghost Wrap, I decided to filter for share price moves in April of 10% or more in either direction.

This is rather different to looking at year-to-date moves, as some of the significant activity earlier in the year is still baked into those moves. For example, a number of the clothing sector names still haven’t recovered from the horrors of January, but there hasn’t been nearly as much action since then in those names. By looking at just April, we are looking at recent momentum.

It’s also important to note that I focused on companies with larger market caps in this analysis. Small-cap and even some mid-cap companies with large bid-offer spreads can show substantial percentage moves for reasons purely related to liquidity rather than underlying trends in sentiment and earnings. There may also be names that moved only slightly less than 10% over that period, which means they wouldn’t come up on the stock screener. You have to pick a cut-off at some kind of number! This episode is therefore meant to just give you a sense of where recent momentum has been, rather than an exhaustive list.

And with that, let’s start with the droppers before getting to the whoppers.

The droppers

Let’s just get Anglo American Platinum out of the way, as it bucks the positive trend we’ve seen in the broader platinum sector. The company is on the cusp of the demerger from Anglo American, so there’s just a ton of noise in this one and the share price has been all over the place. Given the strong performance of the platinum sector this year, I’m happy to chalk this up to an anomaly rather than a useful insight, so onwards we go.

As for Sasol, I’m afraid it’s a tragedy rather than an anomaly. Down around 16% in April, the market just cannot find any love in its heart whatsoever for Sasol, having further punished the stock on the basis of broader recessionary concerns and a production update that was filled with bad news about coal quality and the impact that it is having on Secunda Operations. Although the announcement did have some positivity in it regarding the recent performance of Transnet Freight Rail, this wasn’t enough to improve market sentiment towards the stock. And even when Sasol does seem to catch a break, like when the average sales basket price for the International Chemicals business moves higher, they suffer a knock to production that ruins the numbers anyway.

Sasol is a stock that I would not want to own in a recessionary environment filled with nervous punters. For large investors to get behind Sasol, we need to be in serious risk-on territory. Thanks to what’s going on in global politics right now, I don’t think we are in a risk-on environment. Whilst I completely understand that with cyclical stocks you are supposed to buy them when things look really bad, you do have to wonder what the catalyst for improvement will be at Sasol.

Much as Sasol is known to be a risky asset, we can’t really say the same about Aspen. They are in the pharmaceuticals game, particularly in manufacturing and distribution of drugs. Investors would see this as a blue-chip stock. In fact, they would probably be tempted to refer to it as defensive! Sadly, there’s a difference between being defensive and being a wide-moat business. You can be in a defensive sector, but if your market positioning is relatively weak e.g. because you don’t really hold the power in the value chain, then you can still end up having a bad time.

Aspen took a 24% dive in April based on the market panicking in response to an announcement of a material contractual dispute that could hit EBITDA by R2 billion – that’s a very big number. The broader issue is that Aspen’s business model is vulnerable to US tariffs, which are likely to impact global supply chains and where things are manufactured. If there’s any silver lining for Aspen right now, it’s that the share price at least found some support, bouncing off the 52-week low of R105.75 to reach a closing price for April at just over R124. As I mentioned, that’s unfortunately still a long way down for the month.

The whoppers

On we go to the winners, with a reminder that the local market loves quality stocks. Even though they tend to trade at demanding multiples, these are seen as relative safe havens on the local market. The multiples never seem to unwind, with the share price simply moving in response to earnings.

Capitec is a perfect example – and perhaps the best example, actually. Up 11% in April, the market simply adored the results for the year ended February 2025. And why not? Headline earnings increased by 30% and the dividend was up 34%. There were a number of other really encouraging metrics as well, like growth among high earners and the rather insane market share that they enjoy among the youth population. Sure, a major economic knock to South Africa wouldn’t do their impairments any favours, but this isn’t stopping the market from buying into this growth story. Capitec is a wonderful example of the power of winning market share in a lucrative profit pool, even if the broader economy isn’t growing by much. And yes, the multiple certainly suggests that this should all be priced in, but that’s just not how the local market seems to work. These quality stocks just stay expensive.

PSG Financial Services also came out of the PSG stable, just like Capitec. And just like the bank, this is seen as a high-quality business with a wide moat and great growth prospects. The trick at PSG is the distribution network, which helps gather assets that are subsequently managed or at least administered by the group – for a fee, of course. The recent results show that the model works, with the share price up more than 14% in April. Strong businesses get rewarded in tough markets and although PSG is exposed to overall levels of wealth and where the market levels are sitting, they have proven an ability to grow in almost any conditions. That’s important.

The third high quality business that got the market excited in April was Clicks, with a move of 16.7%. Like the aforementioned companies, this was a results-driven move based on Clicks seeing improved numbers in its wholesale business and ongoing solid numbers in the retail business. Diluted HEPS was up 13.2%. There are a lot of strong, defensive categories in the Clicks business model, supported by arguably the best rewards programme in the country.

To close off, it’s worth noting that market moves aren’t always explained by news flow. Although the three names above all had earnings releases, Woolworths for example was up more than 12% in April – admittedly after some heavy selling pressure towards the end of March that gave it a low base – but there wasn’t a single important SENS announcement from the company in April. The selling pressure continued into the first week of April before the stock caught a bid, so these movements are driven by other factors like portfolio rebalancing by major institutional holders, as well as general market liquidity and key levels that traders watch for. This is why you can never blindly use stock screeners in order to find trends, as there’s a big difference between a meaningful move based on fresh earnings news (or a deal announcement) vs. a move from general volatility. Redefine Properties is another great example by the way, with a 10.5% gain in April and not a single relevant SENS announcement.

So, aside from a couple of names that don’t have obvious explanations for the move, we can take a lesson from what we saw in April: the best names on the JSE (the high-quality companies) are entirely capable of staying expensive, even when there’s broader economic turmoil. In fact, that seems to be the case especially when there’s a risk-off environment! When these high quality companies release results, the market is just looking for confirmation that things are heading roughly in the right direction. These high multiples seem capable of staying expensive.

With the recent global markets turmoil, driven by US President Donald Trump’s tariffs policies, questions are being asked about the future of US exceptionalism. In this episode of the No Ordinary Wednesday podcast, Annelise Peers, Chief Investment Officer at Investec Switzerland, and Richard Cardo, Portfolio Manager and Head of Single Manager Investments at Investec, who oversees the Investec Global Leaders Fund, discuss the implications of US economic policies, the shifting investment landscape, and the potential for growth in alternative markets.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

AngloGold Ashanti announced that it will sell its stake in two gold projects in Côte d’Ivoire to Resolute Mining, a company with experience in West Africa. These projects were part of the Centamin plc acquisition in November 2024. AngloGold has been assessing what to do with them and the decision has obviously been made to let them go, specifically because of the need to focus capital and time elsewhere.

There are no conditions to the sale, so this is a done deal.

Interestingly, part of the deal will see AngloGold acquiring Toro Gold Guinée Sarlu, which owns the Mansala Project in Guinea. This project is adjacent to an existing AngloGold mine in Guinea and they expect to develop it over time. This acquisition does have conditions though, even though the abovementioned sales don’t.

The selling price for the main Côte d’Ivoire asset (the Doropo Project) is $175 million, of which at least $150 million is payable in cash. The remaining $25 million is settled either through the Toro Gold Guinée Sarlu deal, provided it can be completed within 18 months, or through a further payment of cash. The payments are made in three tranches over 30 months.

The ABC Project, which is the other Côte d’Ivoire asset, is being sold for $10 million in cash plus a 2% net smelter royalty. The cash payment is triggered by the declaration of a mineral reserve.

Brait’s update was met with market approval (JSE: BAT)

Solid performance at Virgin Active and capital discipline were the themes

Brait’s share price is up 65% in the past 12 months, so this is a good example of where speculative plays can work out pretty well. And thanks to a positive 10% move in response to a trading update, the share price is slightly in the green year-to-date as well – a pretty resilient performance in a market with so much volatility.

In the latest update, Brait noted that Virgin Active is growing revenue at 13% year-on-year, with annualised March trading suggesting run rate EBITDA of £119 million. They neglected to give a comparison in the update, so I had to go digging for the run-rate EBITDA at the time of the interim results (September 2024). It was just £85 million, so that’s a great example of operating leverage (the benefit of additional revenue at the gyms without a major increase in costs).

Brait still has a stake in Premier, but the results of Premier aren’t a surprise because that company is separately listed these days. Premier is expecting HEPS growth of between 20% and 30% for the year ended March 2025, so that’s certainly helping the story.

And as a cherry on top, Brait decided not to participate in New Look’s £30 million capital raise to accelerate its digital strategy. Historically, New Look has been such a headache that investors are thrilled to see that Brait isn’t throwing good money after bad. Instead, they did things like repurchase convertible bonds at a discount to par value – and that’s what investors want to see from a capital allocation perspective.

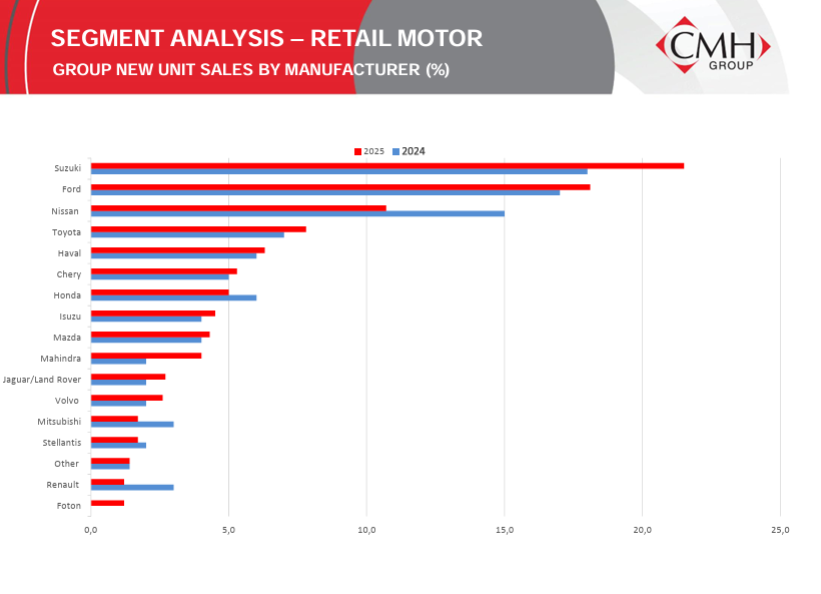

A brief additional note on CMH (JSE: CMH)

The analyst presentation caught my eye

Although I already wrote about CMH’s results in detail when they were released, the company subsequently made an analyst presentation available. It’s worth a read if you’re interested in all the details.

There’s one particular chart that I felt was worth highlighting, as it shows how severe the drop in sales was at Nissan and Honda in 2025. It also shows how important Suzuki is to the group story and how this is their best defence against the Chinese onslaught in passenger vehicles:

Although Ford did well, their focus is on the light commercial market. If quality Chinese bakkies make a mark, then those sales are also at risk.

More auction results from Gemfields, this time for emeralds (JSE: GML)

And once again, comparability is difficult

As we saw earlier in the week with the results of a rubies auction, Gemfields has released numbers that aren’t easy to interpret. At least this wasn’t a mini-auction, with total revenue of $16.4 million comparing favourably to the auction in November 2024 that raised $16.1 million.

The average price was $6.97/carat, which is once again a million miles below the recent results that varied from $15.90/carat to $167.51/carat. The mix of emeralds in any given auction can vary dramatically, leading to this range of prices and making it really hard to figure out whether this is good or bad news.

This means we have to rely on management commentary, with the company calling this a “notable improvement” on the November auction. They have all the details on how pricing played out for this specific mix of stones, so I have to assume that this is an accurate reflection of what happened.

The market didn’t like Glencore’s production update (JSE: GLN)

An 8.6% drop in the share price on the day took the year-to-date move to -29%

Glencore has released a production update for the first quarter of the year. At this stage, energy coal’s guided production range for the full year has been reduced by 5%, while other guidance is unchanged. So, not a fantastic start.

Copper is also causing some stress for investors, as it had a slow start to the year with Q1 production down 30% year-on-year. Although Q1 is a seasonally slower period for copper production, it does put pressure on the rest of the year and of course this heightens the risk of anything going wrong. They expect a 42/58 split for H1 vs. H2 copper production this year, so there’s a lot of uncertainty heading into the rest of 2025.

To add to the uncertainty, the Marketing side of the business is of course dealing with all the complexity created by the tariff environment and the recessions risks in the global economy. Volatility can also represent opportunity and you would probably back the smart people at Glencore to figure that out, as the company has quite the reputation. For now, they are taking a safe approach with their guidance, with an expectation for Marketing Adjusted EBIT to be in the middle of the long-term guided range of $2.2 – $3.2 billion for the year.

Glencore’s share price is down 44% in the past 12 months. Commodity cycles can be brutal things. There is a risk-off flavour to the market, which is why a disappointing Q1 production number caused this kind of sell-off.

The Gold Fields deal to acquire Gold Road may still have legs (JSE: GFI)

After an initial rebuttal by the Gold Road board, the parties are talking

On 24 March, Gold Fields announced that it had put in a non-binding, indicative proposal for Gold Road Resources. They want to acquire 100% of the company through a scheme, which is why the Gold Road board would need to be happy with the terms and would need to agree to propose them to shareholders.

The underlying asset that is driving the deal is Gruyere, a low-cost gold mine in Western Australia. Gold Fields is already operating the mine and Gold Road owns it, so the parties are joint venture partners.

The Gold Road board initially rejected the proposal, which isn’t unusual in an effort to get the price up. In response to press speculation, Gold Fields has confirmed that active discussions with Gold Road are underway, so the parties are clearly back at the negotiating table.

Again, this isn’t unusual and it doesn’t give any guarantees that a deal will go ahead.

Much, much better numbers at MTN Nigeria (JSE: MTN)

This compounds the good news story out of MTN Ghana

It feels good to be reading about better numbers from MTN’s African subsidiaries. MTN’s share price is up 32% this year, with the market putting a lot more belief in the growth story.

Thankfully, the numbers seem to be supporting that view. After releasing solid numbers from MTN Ghana, the group has now followed it up with a far more positive performance than I can recall seeing at MTN Nigeria.

Naturally, the macroeconomics are playing a major role here, just as they did when things were really tough. The exchange rate was fairly stable vs. the US$ and inflation was “only” 24.2% – you can’t apply developed and even emerging market standards to frontier markets like Nigeria. The trick is to compare revenue growth to inflation, with the goal always being to achieve meaningful real growth.

Sure enough, with service revenue growth of 40.5% and EBITDA up by 65.9%, there’s plenty of real growth. And because of the improved forex picture, they swung wildly from a loss of N392.7 billion to profit of N133.7 billion. There was positive free cash flow of N209.9 billion, despite a 159% increase in capex.

A source of uncertainty in the coming quarter is the implementation of the new tariff structure. Most of the adjustments only took place in March, so the full impact wasn’t in these numbers. For now, MTN Nigeria is seeing resilience among customers in response to the pricing change, so that’s encouraging.

With EBITDA margin up 720 basis points to 46.6%, there’s a lot more to smile about at MTN Nigeria – especially as they made plenty of progress in reducing their foreign debt exposure. With only 23% of total debt denominated in foreign currency and with the business currently generating free cash flow, they have a real chance of getting things on track here.

Oceana has given tighter earnings guidance (JSE: OCE)

Things certainly could’ve been worse

In February 2025, Oceana noted that HEPS for the six months ending 31 March 2025 would be at least 40% lower than in the comparable period. One of the reasons was the previous record-breaking production by Daybrook that created an incredibly tough base for comparison.

Now, as any experienced investor will know, the words “at least” sometimes work very hard in trading statements. The subsequent move can be much worse than initially guided, so be careful whenever you see that wording. Thankfully, Oceana’s initial guidance was on point, as the updated guidance is for a decrease in HEPS of between 40% and 48%.

Although fish oil prices didn’t do Daybrook any favours in this period, there were other positives to help offset the impact. This included the performance in segments like Lucky Star and Wild Caught Seafood, with full details to be included when the group releases interim earnings.

The fishing sector depends on a large number of external factors, so variability in earnings is a feature rather than a bug. The share price is down 23% in the past 12 months.

Renergen is on a cash flow treadmill (JSE: REN)

Litigation costs aren’t helping

Renergen has released its financials for the year ended February 2025. As I’ve written before, there’s no expectation of profits at this stage in the company’s journey. Still, seeing the loss increase from R110.3 million to R236.1 million is rather scary.

LNG sales volumes and prices both moved higher, so revenue was R52.1 million. Although that obviously helped, the reality is that they are still firmly in cash burn phase. Getting liquid helium production off the ground cost a fortune and there were many delays. On top of this, they had significant increases in interest costs (up from R22.7 million to R81.1 million) and operating costs, including cash and non-cash costs. Seeing a high depreciation expense is one thing, but noting negative cash from operations of R150.6 million is quite another.

Cash on the balance sheet fell from R471 million to R28.3 million. To help support the next phase of cash burn, AIRSOL subscribed for a second tranche of convertible debentures to the value of $4 million in March. That won’t get them far at the current level of expenses, so I’m quite sure we will see more share issuances in the coming year.

It also doesn’t help that Renergen has been involved in a great deal of litigation, with legal and professional fees of R12.1 million for the year. Although they landed a blow against Springbok Solar through a challenge to the Section 53 consent, the court still hasn’t delivered its ruling. There are other fights underway as well, including a claim and counterclaim situation with the contractor for the process plant, as well as Molopo’s attempt to cancel the loan agreement for alleged breach of a condition. Renergen notes that the soonest hearing date in the High Court in Gauteng is 4 years and 9 months away, which is absolutely ridiculous and a reflection of how bad things have gotten in our courts. Molopo will have to be patient, it seems.

Renergen’s share price is down 46% over 12 months. Although it more than doubled from the recent 52-week low, it remains a highly speculative stock.

Supermarket Income REIT refinanced £90m in debt (JSE: SRI)

This is a useful indicator of UK funding costs

Property funds operate with a targeted loan-to-value (LTV) ratio, or at least a range. This debt is needed to juice up the returns from the properties, as these funds can access debt at attractive rates. Unlike most companies where debt comes and goes, the concept of having debt is baked into the REIT model. This is why you will frequently see them refinancing debt that is about to mature.

The latest such example is Supermarket Income REIT, which refinanced £90 million in debt through a new unsecured debt facility with Barclays. This will refinance existing facilities with Wells Fargo and Bayerische Landesbank of £30 million and £55.4 million respectively, which were due to mature in the next 12 months.

The new facility is an interest-only facility, which means that the capital is only repayable when it matures after three years. The lender has the discretion to extend it by two years. The loan is priced at a margin of 1.55% above SONIA. At current rates, SONIA is 4.46% and thus the current floating rate is 6.01%.

But here’s the good news: there are existing interest rate hedges on the maturing facilities that will cap the rate at 5% at no additional cost to the company. This gives them certainty over the cost of debt, with the potential for it to move lower if SONIA drops significantly.

The company’s expected pro-forma LTV after the refinancing is 31%, which is a healthy level.

Nibbles:

Director dealings:

A non-executive director of Dis-Chem (JSE: DCP) sold shares worth R38.6 million.

Gerrie Fourie is retiring as the CEO of Capitec (JSE: CPI) in July this year. In such a case, it’s not uncommon to see a sale of shares as the outgoing executive looks to diversify exposure. Fourie has sold shares worth R26.2 million.

Here’s another example of yet more sales of Standard Bank (JSE: SBK) shares, this time by the CFO. He sold shares worth R30 million.

A director of Italtile (JSE: ITE) sold pledged shares worth R384k.

Anglo American (JSE: AGL) enjoyed strong shareholder support for the demerger of Anglo American Platinum (JSE: AMS), with 99.94% of votes being in support of the deal. There are still some conditions precedent to be met, with the demerger expected to become effective on 31 May. At the AGM for Anglo, the address to shareholders also included this nugget about De Beers that I felt was worth including in full (and you can decide for yourself if the challenges are only in the “near-term” market):

MTN (JSE: MTN) is still dealing with the aftermath of its decision to operate in Iran. Turkcell is suing MTN in the South African courts, claiming damages related to allegations of impropriety in how the private licence was awarded in Iran. This goes back more than a decade, when an MTN special committee investigated this and found that MTN was not in the wrong. The latest court development is that the Supreme Court of Appeal has upheld an appeal by Turkcell regarding court jurisdiction. There are also some elements of Iranian Law that apply to the dispute. This has no bearing at all on the merits of Turkcell’s case, but it does mean that the legal process can move forwards.

MC Mining (JSE: MCZ) released a quarterly update that reflects a 13% drop in run-of-mine production at Uitkomst on a year-on-year basis. This obviously had a significant negative impact on sales volumes. Coal prices were also under pressure. But of course, what really mattered was the approval by shareholders of the next tranche of the Kinetic Development Group deal that will see them holding a 51% interest in MC Mining.

Jubilee Metals (JSE: JBL) is in the process of finalising the trials of the processing of various high grade copper ores at the Roan Concentrator. This is quite a complex process, as they need to adjust the circuit at Roan for each material. The results have therefore been delayed, with further trials expected over the next couple of weeks.

enX (JSE: ENX) recently announced a deal with Trichem South Africa for West African International Proprietary Limited (WAI). This business is in South Africa by the way, not in West Africa! The deal sees Trichem subscribe for 25% in WAI, with an option to acquire the remaining 75%. The subscription step has been completed, with gross proceeds of R107.3 million flowing into WAI.

Remgro (JSE: REM) and Vodacom (JSE: VOD) have received the reasons for the Competition Tribunal’s decision to prohibit the fibre deal. They tend to submit an updated notice of intention to appeal on 2nd May, with the Competition Appeal Court having reserved 22 to 24 July 2025 for the hearing. Although the transaction long-stop date has now been extended to 23 May 2025, they will clearly need to extend it several more times if they hope to get the deal done.

Super Group (JSE: SPG) announced that the SG Fleet scheme of arrangement in Australia has been implemented. This deal couldn’t have come at a better time for the group, as they are wrestling with the broader disruption to the automotive industry.

Southern Palladium (JSE: SDL) is still in exploration phase, so the quarterly update just gets a mention down here in the Nibbles as it serves of more of a reminder of progress than anything else. The company’s pre-feasibility study for the Bengwenyama PGM project has an expected IRR of 28%, which is solid. Looking ahead, they expect a decision by the DMRE on their mining right application in the coming quarter.

At Kore Potash (JSE: KP2), the quarterly report doesn’t give us much in the way of new information. They expect an 18% IRR from the Kola Project on an ungeared post-tax basis, which will hopefully be enough to get investors across the line. The funding structure is going to be crucial, as any funding sources that come in at a lower cost than the ungeared IRR would significantly boost the geared IRR (i.e. the returns to equity holders). The quarterly update didn’t have any additional information on the Summit Consortium proposal. A separate announcement about the suspension of trading did have reference to the proposal though, with the ASX now imposing a suspension and the JSE lifting its trading halt. This is a really complex situation in which there are multiple exchanges involved that have different rules. Kore Potash is sticking to their guns about not disclosing any details of the funding proposal while they are negotiating it, which seems perfectly reasonable to me. If that leads to short-term trading suspensions, then so be it.

Stefanutti Stocks (JSE: SSK) announced that the timeline for fulfilment of the conditions precedent for the disposal of SS-Construções (Moçambique) Limitada has been extended out to 31 May 2025. Also, the lenders have agreed to extend the capital repayment profile of the loan as well as its duration out to 30 June 2026. It’s all about creating breathing room on the balance sheet as part of the broader capital restructuring.

In an effort to get more international investors, Datatec (JSE: DTC) is now trading on the OTCQX platform. This is focused on giving US investors a way to buy the shares quoted in US dollars. This isn’t the same as having a listing on one of the major US exchanges, but it is a step in that direction for many companies.

Kibo Energy (JSE: KBO) announced that its financials for the period ended December 2024 are unlikely to be published by June 2025, which means that they will miss the deadline under AIM rules (the development board on the London Stock Exchange). This is because they are looking at potential acquisitions under a reverse takeover transaction. If they can’t find one, then I suspect that it would affect whether the audit is conducted on a going concern basis.

London Finance & Investment Group (JSE: LNF) has confirmed that the suspension of its shares from trading will be from 7 May, with the delisting scheduled for 9 May.

I don’t usually comment on non-executive director appointments, but I thought it was worth noting the appointment of Lisa Seftel to the board of Frontier Transport Holdings (JSE: FTH). What caught my eye is that she has loads of experience in various spheres of the South African government. Given Frontier’s business model and the level of collaboration required with government around transport systems, this seems like a sensible appointment to me.

Here’s another interesting director appointment for you: KAP (JSE: KAP) has appointed Samara Totaram to the board as an independent non-executive director. Her most recent role was as STADIO’s CFO. She brings loads of corporate finance experience, which will be helpful to KAP from a dealmaking perspective. Is the company preparing for corporate activity?

Absa sent out a circular to its preference shareholders (JSE: ABSP) regarding the repurchase of the shares at 930 cents per share. Be sure to read it if you are a preference shareholder.

I strongly believe that we are nowhere near the bottom

Remember how I warned you about lab-grown diamonds and the disruptive force that they seemed to be? De Beers (and by extension, Murray & Roberts) bore the brunt of that impact. I believe that the Chinese car disruption to the automotive sector is just as strong as that of lab-grown diamonds.

After all, the recipe is exactly the same: consumers just love a much more affordable option that gets the job done. If perceived quality is the same or at least roughly the same, yet the price is two-thirds cheaper, then consumers will form an orderly queue. And frankly, why shouldn’t they?

CMH has a proud history and represents a number of impressive legacy brands in its dealer network. The problem is that these are the brands that are struggling. Although revenue was up 3.2% for the year ended February 2025, operating profit fell 18.1% and HEPS tanked by 25.6%. It won’t surprise you that the dividend to be paid in June 2025 followed suit, down 22.3%.

If you’re wondering why profits fell so sharply despite revenue increasing, the answer lies in margins. There has been massive pricing pressure on the legacy brands thanks to the Chinese competitors. Every day, my Facebook feed is filled with specials by legacy brands (not just from CMH, either).

Of course, the company can react to the change in consumer trends by reworking its dealership base. This is a very expensive process that I’m sure is a contractual minefield of note, but it is possible at least. If you look at the list of dealers in the group, you’ll see that more Chinese names are starting to come through. You’ll also see that they are sitting on around 11 Proton dealerships, an unmitigated disaster and a complete misread of what South African consumers are looking for.

They are looking to sell off all Proton inventory and then “decide on the way forward” – I literally would not buy a Proton for my worst enemy. The chances of being left high and dry if they leave the country seem to be very strong. Here it is, straight from the CMH report:

As for electric vehicles, the decision by Volvo to focus on EVs has transformed it into even more of a niche player in South Africa. The dealer network is dropping from 25 dealers to just 7 dealers, with CMH operating 4 of the 7 dealers.

There are 10 million South Africans who can afford a car. This number doesn’t grow, mainly because our economy doesn’t grow. WeBuyCars (see earnings update further down) is brand agnostic and helps these 10 million people churn through vehicles, which is why I’m a shareholder there. CMH (and others) are attached to certain brands and are hoping on those people being able to afford new, shiny cars, which is why I’m not a shareholder.

If you’re waiting for a chance to point out that the car hire business at CMH represents diversification that could see them through the storm, then I have bad news for you. Although this is certainly a useful contributor, car hire is a hugely competitive market. Not only are there are number of options for car hire at airports, but there’s always the option of taking an Uber. Instead of participating in what CMH calls a pricing war, they decided to restructure and defleet.

The net impact? Profit before tax in the car hire segment fell by a nasty 45%. That’s much worse than the 12.4% drop in motor retail, a result that was further mitigated by a flat performance in financial services (also a major profit contributor).

In other words, car hire was a detractor from results in this period, let alone a source of diversification. It is anything but defensive.

And yet the market continues to believe in this stock, with wild volatility this year based on the broader macroeconomic picture:

Still, I’m not unhappy with my choice in this sector:

I firmly believe that were will still see some major scalps in this environment, possibly even of a German variety. There are huge issues facing brands that once enjoyed strong market positions.

Gemfields released ruby auction results (JSE: GML)

It’s not easy to compare auction results

Gemfields could really do with some positivity at the moment. The share price has lost around 60% of its value over 12 months and the company now needs to do a rights issue to keep things going. Above all, they need prices for rubies and emeralds to head in the right direction.

The company announced the results of a mini-auction of rubies in which revenue of $7.2 million was generated. They aren’t joking about it being a small auction, as the latest ruby auction in December 2024 generated $46.2 million in revenue – and that was the smallest of the five most recent auctions at the time.

Now, it’s difficult to actually compare the USD price per carat, as the grades of rubies can vary dramatically. To give you an idea, the five preceding auctions saw prices range from $154.84/carat to $321.94/carat. The latest auction was just $39.47/carat, so either the underlying rubies were very different, or the market has truly collapsed.

As the company talks about “very healthy results” from this auction, I’m inclined to believe that this was simply a different underlying profile vs. previous auctions. The announcement isn’t explicit enough on this though, which is disappointing.

HCI’s Namibian oil update is disappointing (JSE: HCI)

The latest drilling was dry

HCI is the 51% shareholder in Impact Oil and Gas, which in turn has a 9.5% interest in certain blocks offshore Namibia. The results for the third drilling campaign have now been announced.

The bad news is that the Deepsea Mira rig didn’t find any hydrocarbons in the Marula-1X well, which is a fancy way of saying that they drove the Chevy to the levee and the levee was dry. They will therefore demobilise the rig.

Although this is clearly disappointing for the Marula prospect, Impact has noted that they will integrated the data into the evaluation of the block’s full potential. Such is life in the world of energy exploration!

Finally, there’s a funding term sheet on the desk at Kore Potash (JSE: KP2)

The Summit Consortium has delivered a proposed funding structure

If you’ve been following the Kore Potash story, you’ll know that it took an incredibly long time to finally get the EPC contract from PowerChina for the construction work in the Republic of Congo. Throughout that process, Kore Potash kept reminding us that the Summit Consortium was simmering on the stove, ready to dish up a term sheet for funding for the project as soon as the EPC was concluded.

Although there was an awkward and somewhat worrying delay along the way, the Summit Consortium has indeed come through with a funding proposal. It includes royalty and project finance components and would fund the entire project.

Now, this doesn’t mean that there terms are acceptable yet or economically fair; it just means that the Summit Consortium has played its hand and put terms on the table. Kore Potash now needs to consider the terms and negotiate them, with the potential to explore other sourced of funding if required.

Pending the announcement of the terms, trading has been halted on the Australia Stock Exchange and the JSE. Due to different rules, trading is allowed to continue on AIM on London. I’ve honestly never understood how it helps anyone or creates a fairer market to have suspensions only in certain places. This is one of the anomalies that comes with listings on more than one exchange.

MTN Ghana kicks off a new reporting season for the African subsidiaries (JSE: MTN)

And things are off to a good start!

Regular readers will be aware that MTN’s African subsidiaries are volatile things. The macroeconomics in the region are the main reason of course, with potentially wild swings in inflation and currencies. In fact, in the last round of reporting by the African subsidiaries, plucky Uganda stuck its hand up as the highlight!

In Ghana, the first quarter of 2025 was once again a rollercoaster ride of economic indicators: the currency was 17.1% weaker vs. the USD on a year-on-year basis and inflation was 22.4% at the end of March. The good news is that inflation was down slightly from the levels seen at the end of 2024.

But the really good news is that service revenue at MTN Ghana was up 39.6%, which is well in excess of inflation. EBITDA margin went the right way, up 220 basis points to 58.1%. This means that EBITDA increased by 45%, which in turn drove an improvement in earnings per share of 53.7%.

Profit after tax was GHS1.7 billion and capex (excluding leases) was GHS 0.8 billion, so there’s even some free cash flow there. And just when you thought that things couldn’t possibly look any brighter, the government in Ghana abolished the e-levy tax on Mobile Money transactions, effective from 2 April 2025.

Although it’s very early days in 2025 and this is obviously just one country out of many, at least we are off to a positive start for the Africa story this year.

A bloody nose for the TRP on the Novus – Mustek transaction (JSE: NVS | JSE: MST)

The High Court has dismissed the recent TRP ruling

It’s been quite a regulatory journey to get the mandatory offer by Novus to shareholders of Mustek across the line. A mandatory offer isn’t even the most technical part of takeover law, yet a bunch of interesting and complicated issues have come up.

At the end of March though, we saw a particularly surprising outcome in the form of the TRP unilaterally withdrawing its approval of the Firm Intention Announcement that went out in November. Understandably, Novus was less than impressed with this approach. An appeal to the High Court has led to the court agreeing with Novus, which means that the ruling of the TRP has been set aside. In fact, the TRP was even ordered to pay the costs of the court action!

The court has directed Novus to post the offer circular and supplementary firm attention announcement within 5 days of the date of this order, or a longer period as determined by the TRP in consultation with Novus.

Interestingly, the TRP is evaluation the decision in the context of its “regulatory authority” – while acknowledging that they need to comply to avoid further delays.

Regulators should always be a balancing act. Too little regulation is a problem. Regulators behaving badly is also a problem. The reason why we have a legal system is to create potential remedies, which is what has happened here.

Quantum Foods: even better than they expected (JSE: QFH)

A revised trading statement has further increased the earnings range

Quantum Foods released an initial trading statement in mid-April that guided a vast jump in HEPS from 21.7 cents to at least 68 cents. The percentage change isn’t meaningful when earnings are more than tripling!

An updated trading statement reveals that things are even better than they initially expected, with a revised range for HEPS of between 72.6 cents and 77.0 cents. The volatility in poultry sector earnings will never cease to amaze me.

Reinet seems to have had a flat quarter (JSE: RNI)

The direction of travel for the NAV of Reinet Fund is usually a good indicator of the group NAV

Reinet released the net asset value (NAV) for Reinet Fund. Although this isn’t a perfect proxy for the NAV of the listed company, as there’s a layer of balance sheet items on top of the fund that listed shareholders are exposed to, it’s usually a very good indicator of the direction of travel of the group NAV.

That direction was rather flat between December 2024 and March 2025, with the NAV of €6.92 billion representing a decrease of €13 million over three months.

The NAV for the listed company will be announced in due course.

Over R500 million in interim core headline earnings at WeBuyCars (JSE: WBC)

It’s just a pity about all those extra shares in issue

Despite having more than doubled over 12 months, the WeBuyCars share price has been remarkably resilient this year. It’s only down 3% year-to-date, despite all the noise out there and the large P/E multiple that it trades on.

In a trading statement for the six months to March, support for the multiple was provided by core headline earnings increasing by between 24% and 28%, coming in above the R500 million mark for the interim period. That’s obviously extremely impressive.

Unfortunately, due to the vast number of additional shares that were issued before the listing, HEPS was up by between 0% and 4%. The pie may be bigger, but there are many more people trying to eat it.

As the listing itself becomes smaller in the rear-view mirror, headline earnings and HEPS growth should converge. The market is counting on juicy ongoing growth, something that I also believe is possible as a shareholder in the business.

Nibbles:

Director dealings:

In yet another example of a Standard Bank (JSE: SBK) executive selling shares, the CEO of Personal and Private Banking offloaded R10 million worth of shares. This is despite the group maintaining earnings guidance for the year and reporting a solid first quarter.

The company secretary of Sun International (JSE: SUI) sold shares worth R2.64 million. They relate to share-based incentives and it’s not clear whether this is only the taxable portion. So, as usual, I assume that it isn’t.

Prosus (JSE: PRX) and Naspers (JSE: NPN) announced the appointment of Nico Marais as CFO. He’s been serving as interim CFO since December 2024, so it’s nice to see this confirmation of a permanent appointment. Having been with the group for over two decades, this is strong support for Fabricio Bloisi and the rest of the executive team.

Astoria (JSE: ARA) released results for the quarter ended March 2025. The diamond market is a major headache here, with a downward move in the valuation of the Trans Hex businesses. As a result, the NAV per share of the group was down 8.7% in ZAR for the three months from December 2024 to March 2025.

In a quarterly activities report, Orion Minerals (JSE: ORN) reminded the market that this was a really important quarter: the Definitive Feasibility Studies (DFS) for both the Prieska Copper Zinc Mine and the Okiep Copper Project were released at the end of the quarter. The Prieska project is the juicier of the two, with an expected IRR of 26.2%. This is the project that they intend to develop first. With an expected IRR of 23% at Okiep, that’s hardly a bad supporting act. Also, new CEO Tony Lennox is in place, with Errol Smart having stepped down as CEO in early April. The focus is on putting together the right project financing package for the development of the project.

Both Nedbank (JSE: NED) and Capital Appreciation Limited (JSE: CTA) announced the sad news of the passing of Errol Kruger, who served as a non-executive director on both boards. He had a long and impressive career in the banking industry.

If you are a Clientèle (JSE: CLI) shareholder, then be aware that the circular dealing with the amendment to the funding structure and MOI in relation to the Emerald Life acquisition has now been sent out. As you may recall, a change was required after engagement with the Prudential Authority.

After successfully playing catch-up on its financial reporting, AYO Technology (JSE: AYO) has had its listing suspension lifted by the JSE. Trading resumed from the afternoon of 29 April.

In the unlikely event that you are a shareholder in Globe Trade Centre (JSE: GTC), then be aware that results for the year ended December 2024 were released. Funds from operations came in flat and the loan-to-value ratio ticked up from 49.3% to 52.7%.

London Finance & Investment Group (JSE: LNF) announced that the court has sanctioned the capital reduction, which means the distribution of £0.7153 per share has been agreed. The effective date is unclear though though, as there is some kind of delay at Companies House in the UK. The date for the distribution and delisting of the company will be communicated in due course.

It’s been a really bad few days at Harmony Gold (JSE: HAR), with the company announcing its second loss-of-life incident. This time, it happened at the surface operations at the Saaiplaas Reclamation Dam. This is unrelated to the first incident that happened at Moab Khotsong.

In this piece, Nico Katzke (Head of Portfolio Solutions at Satrix*) covers some of the key investment themes that are playing out in this geopolitical environment.

The global investment landscape is undergoing a seismic shift, shaped by geopolitical tensions, trade frictions, and policy uncertainty. The post-war economic order, once a symbol of stability, now appears fragile. Investors face the challenge of navigating a world where traditional assumptions about safety and opportunity are being disrupted.

The key question arises: How can investors future-proof their portfolios in such a world? As uncertainty abounds, the value of sensible, risk-conscious diversification remains as certain as ever.

The Fragile Global Economic Framework

The post-war economic structure, long considered stable, is under strain. Trade negotiations have exposed vulnerabilities, and the Trump administration’s protectionist “America First” policy has created great uncertainty. Historically, US Treasuries were considered a safe haven due to their liquidity and security. However, Trump-inspired protectionist policies aimed at both allies and adversaries alike may serve to severely undermine this perceived stability.

This may, in turn, drive investors to continue allocating to other assets like gold, which offers both safety and liquidity. This reallocation could very well become reinforcing – pushing up yields and US debt servicing costs, making US treasuries riskier. This then creates ripple effects across equity markets, inflation, and consumer demand. It turns out that policy does not happen in a silo, even if set by the world’s largest economy – and weaponising one’s policy framework may do more harm than good.

The Rise of Scarce Assets

In this context, scarce assets like gold are gaining prominence, with rising prices reflecting investor anxiety. Gold’s ability to hedge against inflation and geopolitical risk is becoming more apparent. The demand for a safe-haven alternative to US treasuries has seen the price of gold reach all-time highs this year – with few analysts willing to bet that we’ve seen the ceiling reached just yet.

Growth Potential in Tech

Meanwhile, AI (Artificial Intelligence) has emerged as a key disruptor for traditional views on corporate earnings, efficiency and economic growth. As AI adoption accelerates, broader economic efficiency increases, making US tech equities attractive despite caution about valuations.

One often overlooked factor is the growth potential of tech companies. Unlike the dot-com bubble that many are trying to draw parallels to, companies at the forefront of AI development are mostly well-established with vast cash reserves. Even if only partially achieving some of the loftier earnings projections, their current valuations may appear undervalued in hindsight, even though their price-to-earnings ratios seem high today. Our broadly accepted models for valuations today are arguably incapable of measuring the true valuation of an industry still in its adoptive phase – making the argument for stretched valuations less convincing than would otherwise be the case.

Fixed Income Outlook in a Volatile World

The global fixed-income outlook is characterised by a persistent fear of returning inflation, with duration risk remaining stubbornly high. Policy uncertainty, which is the order of the day, further makes this asset class seem like a risk not worth taking. The US Federal Reserve’s cautious stance suggests that rates will likely remain somewhat elevated. This favours short- and mid-duration bonds, particularly higher yielding high-quality corporate credit. However, the traditional role of bonds as portfolio stabilisers is being challenged, as high and positive stock-bond correlations force investors to look beyond conventional fixed income instruments for diversification.

This shift is driving interest in alternatives such as gold, inflation-linked bonds, and market-neutral strategies.

Don’t write off the US… yet

Much noise has been made about the havoc wreaked this year by unclear and erratic policy decision making in the world’s largest economy. The Trump administration has confidently embarked on a dangerous game of rhetorical improvisation when it comes to trade policy, economic growth and even delicate geopolitical matters – virtually all with little to no clear wins so far. Yet one cannot write-off the (often labelled expensive) US equity market just yet. While Trump’s dealmaking capability and negotiating leverage may not be as decidedly powerful as his ardent supporters believed, the current US administration makes policy decisions very much with the market in mind.

While the Fed has failed to bow to political pressure (up to now), the government still has considerable fiscal and regulatory stimuli that it can fall back on – especially considering the blind obedience both houses of congress show to Trump. You can be sure that the administration will do whatever it can to buoy up equity markets by providing stimulus to get runs on the board, without much regard for the long-term impact of such measures. In fact, one might argue that getting a W for T arguably matters more than the long-term viability of anything done by this administration.

Emerging Markets: A Tactical Opportunity

Emerging markets (EM) present both risks and opportunities in this uncertain environment. While EM assets have lagged developed markets consistently for over a decade, there are compelling reasons for tactical allocations to this cohort currently. Regions like Latin America, the Middle East, and India are benefitting from shifting global supply chains and geopolitical tensions. For example, Mexico has surpassed China as the US’s largest trading partner.

In Asia, China’s growth is stabilising at 4.5 – 5%, presenting opportunities, especially in the tech sector. The risk remains, of course, that the perennial bridesmaid to developed market regions underperforms; but with a resetting of the global order, a well-diversified regional positioning on global equities seems a logical choice.

Re-Globalisation and Trade Frictions

Trade frictions are accelerating trends of global supply chain fragmentation, leading to a re-globalisation of trade. This creates both winners and losers. Countries like India and the UK are poised to benefit from more resilient supply chains. For investors, this means focusing on assets that can withstand inflation, like US Treasury Inflation-Protected Securities (TIPS), and identifying regions and sectors that are less vulnerable to tariff pressures but are thriving in a fragmented global economy.

Building a Future-Proof Portfolio

Constructing a future-proof portfolio requires a nuanced approach, balancing safety with growth opportunities. After all, even in uncertain times, the greatest risk that a long-term investor can take is not taking enough well-rewarded risk. Risk-conscious investors could consider diversifying beyond traditional stock-bond allocations to include scarce assets, inflation-linked bonds, and alternative diversifiers. The choice, however, could be a daunting one.

An easy and cost-effective solution could be global balanced funds, like the Satrix Global Balanced Fund of Funds ETF, which offers diversified exposure to global assets in a low-cost portfolio, simplifying portfolio construction in today’s complex market environment.

The Rise of the Sophisticated Index Investor

The rise of exchange traded funds (ETFs) has been driven by their cost-effectiveness and diversification benefits. However, a notable trend is the emergence of the “sophisticated index investor.”

These investors use ETFs not only as index-tracking instruments but also as precise building blocks to express market views and enhance portfolio efficiency. Much like Lego blocks – while simple and transparent in their design, ETFs placed together in the right combination can produce a sophisticated portfolio. The main benefit is that investors know what they get and, crucially what they pay as well.

Embracing Uncertainty

While the investment landscape is uncertain, it also presents opportunities for those that remain invested. Understanding the structural forces – such as the rise of AI, the fragmentation of global supply chains, and the shifting role of traditional safe havens – can position investors for success. Periodic risk is what explains the payoff for investing in risky assets – if there was no risk, there’d be limited reward. The key is to diversify thoughtfully and embrace strategies that help navigate the complexities of the market.

As we move into 2025 and beyond, consistency will define successful investing. Though the world may be topsy-turvy today, a well-balanced approach will allow investors to turn uncertainty into opportunity. By leveraging low-cost index strategies, investors stack the odds in their favour by building resilient portfolios poised for growth.

**Based on the recent Satrix IndexMore Discussion on Navigating Investment Trends

*Satrix is a division of Sanlam Investment Management

Disclaimer

Satrix Investments (Pty) Ltd is an approved financial service provider in terms of the Financial Advisory and Intermediary Services Act, No 37 of 2002 (“FAIS”). The information above does not constitute financial advice in terms of FAIS. Consult your financial adviser before making an investment decision. While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSP, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaim all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Satrix Managers (RF) (Pty) Ltd (Satrix) is a registered and approved Manager in Collective Investment Schemes in Securities and an authorised financial services provider in terms of the FAIS. Collective investment schemes are generally medium- to long-term investments. With Unit Trusts and ETFs, the investor essentially owns a “proportionate share” (in proportion to the participatory interest held in the fund) of the underlying investments held by the fund. With Unit Trusts, the investor holds participatory units issued by the fund while in the case of an ETF, the participatory interest, while issued by the fund, comprises a listed security traded on the stock exchange. ETFs are index tracking funds, registered as a Collective Investment and can be traded by any stockbroker on the stock exchange or via Investment Plans and online trading platforms. ETFs may incur additional costs due to being listed on the JSE. Past performance is not necessarily a guide to future performance and the value of investments / units may go up or down. Performance is based on NAV to NAV calculations with income reinvestments done on the ex-div date. Performance is calculated for the portfolio and the individual investor performance may differ as a result of initial fees, actual investment date, date of reinvestment and dividend withholding tax. A schedule of fees and charges, and maximum commissions are available on the Minimum Disclosure Document or upon request from the Manager. Collective investments are traded at ruling prices and can engage in borrowing and scrip lending. Should the respective portfolio engage in scrip lending, the utility percentage and related counterparties can be viewed on the ETF Minimum Disclosure Document. A fund of funds portfolio is a portfolio that invests in portfolios of collective investment schemes that levy their own charges, which could result in a higher fee structure for the fund of funds. International investments or investments in foreign securities could be accompanied by additional risks such as potential constraints on liquidity and repatriation of funds, macroeconomic risk, political risk, foreign exchange risk, tax risk, settlement risk as well as potential limitations on the availability of market information.

Here’s something you won’t see every day in the local market: a new listing! It’s not even a spin-off of something that is already in a listed group, as we saw with the likes of Boxer and WeBuyCars. No, this is something brand new to our market.

ASP Isotopes has been listed on the Nasdaq since 2022 and has a market cap of $400 million. That’s small by US standards, but would make it a decently-sized mid-cap on the JSE.

So, why the JSE? Simply, because 97% of the employees and operating assets are right here in South Africa. This clearly gives the company the ability to use local shares for incentivisation as well as for any potential deals.

Here’s a rather astonishing statistic: 19% of the staff at the company hold PhDs. Talk about a daunting place for a water cooler chat! All these clever people are focused on producing and enriching natural isotopes at three production facilities in Pretoria. They use processes that you can reference at the dinner table to sound impressive, like Aerodynamic Separation Process (hence the name ASP Isotopes I presume) and Quantum Enrichment. Then you have to hope that nobody asks you for further details.

The client base for these products can be found in the medical, semiconductor and nuclear energy markets. With Russia currently producing 85% of stable isotopes in the world, I can already see why this company is in such a juicy geopolitical position at the moment.

Subject to approvals, the listing is expected to take place on the Main Board of the JSE later this year. Exciting!

Delta Property Fund announces another disposal (JSE: DLT)

Slowly but surely, they are making progress

The old joke about eating an elephant one bite at a time is certainly applicable to the debt on the Delta Property Fund balance sheet. They continue to dispose of properties as often as possible, with the intention being to reduce debt. Sadly, these aren’t exactly premium properties, so getting them sold isn’t so easy.

The latest sale is the Chambers of Change building in the Johannesburg CBD. The purchaser is not a related party and the price that they got is R25 million, which is well below the valuation as at the end of February 2024 of R37.7 million. To be fair, with a vacancy rate of 76.2% in this office building, the “value” is a relative term.

The purchaser is paying a non-refundable deposit of R1.25 million and has to come up with the remaining R23.75 million within 45 business days.

Finbond wants to tap the market for capital (JSE: FGL)

Preference shares are the preferred mechanism

Finbond has issued a circular to shareholders that proposes the creation of 1,000,000,000 unlisted preference shares. They are looking to raise capital for “operating capital” – and they aren’t messing around, with a proposed maximum raise of R2 billion.

Although Finbond claims that this is non-dilutive for ordinary shareholders, this really is a sugar-coated view. Sure, issuing preference shares won’t dilute voting rights, but the word “preference” is there for a reason. These shares rank ahead of ordinary shares for things like dividends, or in a liquidation situation.

Finbond’s market cap is just R370 million, so the quantum of the raise is also relevant here. If they get the full raise away (or even a meaningful portion of it), such an issuance would dwarf the existing ordinary equity value.

If you’re a shareholder, I suggest that you very carefully consider this circular.

Implats maintains guidance despite a tough quarter (JSE: IMP)

Production was under pressure, but sales were slightly up

In a production update dealing with the quarter and nine months ended March, Implats noted that they faced production challenges that included maintenance in the South African operations. Despite this, full-year guidance for volumes and unit costs has been maintained, so that’s a decent outcome.

For the nine months, 6E refined and saleable production was up 1% to 2.5 million ounces and 6E sales volumes also increased 1% to 2.55 million ounces. They therefore dug into finished stock in this period, as they sold slightly more than they produced. Notably, although refined and saleable production was slightly higher, group production volumes actually fell by 5%.

Another important point to note is that the momentum in the third quarter was concerning, with sales volumes down 6%. Refined and saleable production was flat for the quarter. If that carries on into the fourth quarter, it will further impact the full-year numbers.

Merafe and Glencore are pulling back on ferrochrome production (JSE: MRF | JSE GLN)

This is far more important to Merafe than it is to Glencore

Glencore operates a vast group across numerous commodities, so a few ferrochrome smelters in South Africa won’t exactly move the dial for them. As for Merafe though, these assets represent their entire business. This is why you’ll find an announcement by Merafe and not by Glencore regarding the decision to suspend operations at two smelters.

The ferrochrome market just isn’t playing nicely at the moment, with Merafe having responded to these issues by initiating a business review process. The outcome of this process is that the Boshoek and Wonderkop smelters will be suspended during May 2025. There is no intended date for lifting of the suspension, unless ferrochrome prices improve.

The Lion smelter will continue with production for the remainder of 2025.

Merafe is one of those stocks that has always been trading on a “cheap” P/E multiple. Cheap is often cheap for a reason, particularly in mining houses with exposure to a single commodity.

Losses widen at Renergen (JSE: REN)

At this stage in the company’s journey, losses are to be expected

Renergen is still in its relative infancy when you consider how much development work still needs to happen to bring the helium dreams to life. Even without the many bumps in the road that we’ve seen in the past couple of years, it’s likely that the company would still be loss-making at the moment.

Those who are bullish on the company are focused on the long-term prospects, not the near-term earnings. Still, it’s never nice to see that the headline loss per share has more than doubled.

The expected range in the trading statement is -R1.52 to -R1.67 per share for the year ended February 2025. The comparable period was -R0.7507 per share.

The Vodacom share price boosted YeboYethu (JSE: YYLBEE)

The earnings in the structure are as volatile as the share price

B-BBEE investment structures like YeboYethu have only one investment, so their earnings (and thus value) are volatile based on how that underlying investment moves. In the case of YeboYethu, the underlying investment is Vodacom.

This volatility comes through clearly in the trading statement for the year ended March 2025, in which YeboYethu expects HEPS to be between R40 and R48, which is a wild swing from a loss of -R40.04 in the comparable period!

The net asset value (NAV) per share has also increased dramatically, up from R31.51 to between R71 and R77.

This has been driven by a 27% increase in the Vodacom share price between March 2024 and March 2025. The reason why this percentage change causes a much larger percentage change in the value of YeboYethu is because of leverage (debt) in the structure. In good times, leverage is your friend. In bad times, it can kill you.

Nibbles:

Director dealings:

A director of Italtile (JSE: ITE) sold pledged shares in on-market trades to the value of over R1.5 million.

It was a smaller trade than usual for Des de Beer this time, with a purchase of Lighthouse Properties (JSE: LTE) shares worth R53k.

Caxton and CTP Publishers and Printers (JSE: CAT) is proposing an odd lot offer. We regularly see this on the local market, as companies with a long tail of retail shareholders carry a significant cost of compliance and administration for the sake of a small percentage of the overall economics of the company. At Caxton, shareholders with fewer than 100 shares represent 32.3% of total shareholders, yet hold just 0.27% of share capital in aggregate. Credit to Caxton – they are at least executing the odd lot offer at a decent price, being a 20% premium to the 30-day VWAP calculated up to 23rd May. Note that this is being structured as a dividend, so dividend withholding tax of 20% would apply to individual shareholders. Still, I’ve seen a number of companies structure this as a dividend without paying a premium, so this is a much fairer approach to shareholders.

As a reminder that the mining industry is still a dangerous place for workers, Harmony Gold (JSE: HAR) announced a loss of life incident at Moab Khotsong mine. This happened in a locomotive-related accident. It’s always very sad to read these updates.

Trustco (JSE: TTO) is still working towards a delisting of the company and has renewed the cautionary announcement in this regard.

Science doesn’t just progress in laboratories. It unfolds in the margins, shaped by the people, politics, and institutions around it. The story of IVF, when told in full, reminds us that breakthroughs are often born twice: once in the petri dish, and again in the public imagination.

Look, I’m sure your mom and dad were really pleased when you were born, but let’s be honest: not everyone’s birth is lauded as one of the most important medical breakthroughs of the 20th century. That distinct honour went to one Louise Joy Brown in 1978, when she became the first human being in history to be born following conception by in vitro fertilisation.

Louise was the first in her family (in the world), and just four years later, the birth of her sister Natalie marked the 40th IVF baby. And when Natalie went on to have her own baby (conceived without IVF) in 1999, she became the first human conceived by IVF to give birth, proving that IVF babies could grow up to be perfectly “normal” reproductive adults (much to the relief of a watching world). That’s a whole lot of firsts for the Brown family!

Fast forward to today, andmore than 10 million IVF babies have been born around the world. Estimates suggest that between 1% and 6% of all babies born since 2020 have arrived courtesy of a petri dish.

But there’s a side to this story that most people don’t know. Just 67 days after Louise Brown’s birth, another IVF baby was born – this time in India. Her name is Kanupriya Agarwal, and the man who made her birth possible, Dr. Subhash Mukherjee, used a method entirely different from Edwards’ team, working with far fewer resources and in near-total isolation.

So why wasn’t his name in the newspaper headlines? Well, that’s a question for the Bengal government.

The creation of Louise Brown

The science that brought Louise Brown into the world in 1978 might’ve felt revolutionary, but it had actually been simmering on the scientific back burner for over a century.

Let’s rewind to 1878. While most people were still trying to figure out electricity and internal plumbing, a Viennese embryologist named Samuel Leopold Schenk was already experimenting with fertilising mammalian eggsoutside the body. Using rabbits and guinea pigs (science’s most patient test subjects), Schenk mixed sperm with ova in a dish and noted signs of cell division. It was early, imperfect, and not quite a pregnancy, but it was the first whisper of what IVF could one day be.

In 1934, two researchers named Gregory Pincus and Ernst Vinzenz Enzmann made headlines for reportedly achieving the first IVF pregnancy in rabbits. But later scrutiny revealed an important technicality: their fertilisation didn’t happen in vitro (Latin for “in glass”) but in vivo – inside the body. They’d reimplanted their eggs too soon, before they had matured, and nature took over from there. Promising, but not quite the scientific mic-drop they thought it was. In 1959, US scientist Min Chueh Chang successfully used IVF to impregnate a rabbit, officially marking the technique’s first true success in mammals.

In the late 1960s, gynaecologist Patrick Steptoe and reproductive biologist Robert Edwards joined forces after a fateful lecture on laparoscopy. Steptoe had been pioneering this minimally invasive technique to retrieve eggs, while Edwards was obsessed with understanding human fertilisation. Together, they cracked one problem after another: how to mature eggs with hormonal stimulation, how to retrieve them safely, how to fertilise them in a petri dish, and (critically), when to reimplant the fertilised embryo.

By 1976, the duo began working with a couple from Bristol who had spent nearly a decade trying to conceive: Lesley and John Brown. Lesley had blocked fallopian tubes, a hurdle that IVF was uniquely poised to bypass. On 10 November 1977, Steptoe and Edwards tried a new approach: no fertility drugs, just a natural cycle IVF procedure, fertilisation in a humble petri dish, and then implantation.

Nine months later, Louise Joy Brown was born. The media called her a test tube baby. The scientists knew better – it was a petri dish that did the trick. But either way, the world had changed.

The creation of Kanupriya Agarwal

In 2010, at the age of 85, Robert Edwards finally got the nod he’d long deserved: the Nobel Prize in Medicine. His collaborator Patrick Steptoe, sadly, couldn’t be honoured. Nobel rules don’t allow posthumous awards, and Steptoe had passed away in 1988.

The timing of the award felt almost poetic. It landed close to the anniversary of another quiet revolution in reproductive science – one that had unfolded not in Cambridge or Oldham, but in Kolkata. In October of 1978, Indian reproductive scientist Subhas Mukherjee announced the birth of Kanupriya Agarwal – nicknamed Durga – the world’s second and India’s first IVF baby. Headlines at the time, however, only mentioned Edwards’ team and the birth of Louise Brown.

While Edwards’ method involved fertilising an egg outside the body and then implanting it in the uterus, Mukherjee had independently worked out other key pieces of the IVF puzzle. As early as the late 1970s, he had become the first in the world to use hormone treatments to coax ovaries into producing more eggs, the first to harvest those eggs through a far less invasive transvaginal route, and the first to successfully freeze and thaw embryos before implantation.

In a 1997 article in Current Science, reproductive biologist TC Anand Kumar – the man responsible for the birth of India’s second documented IVF baby – told the world that Mukherjee and his colleagues were “ridiculed by the medical fraternity and victimised by bureaucracy”. At the time of Mukherjee’s discovery, the state of West Bengal was barely a year into Left Front governance and had little patience for maverick science. Instead of peer review, Mukherjee got a panel led by a radiophysicist (yes, really) and staffed by scientists unfamiliar with reproductive medicine. Unsurprisingly, they dismissed his work.

It only got worse. By late 1978, Mukherjee was banned by the Bengal government from presenting his findings at scientific conferences. An invitation from Kyoto University was similarly denied. In 1981, he was abruptly transferred to an eye hospital and expected to work in an area of medicine completely outside his field. That July, at just 50 years old, Subhas Mukherjee tragically died by suicide.

The world was led to believe that India’s first IVF baby was born 5 years later in 1986, under the care of the aforementioned Anand Kumar. But in a twist worthy of a detective novel, Kumar later unearthed Mukherjee’s handwritten lab notes, personal correspondence, and experimental logs. After cross-checking with Durga’s parents and scrutinising every technical detail, he reached an unavoidable conclusion: Mukherjee had done it first. Putting his personal accomplishment aside, Kumar vowed to make sure that the world knew that the birth of India’s first test tube baby was the result of Mukherjee’s work, not his own.

It took nearly two decades, but thanks to Kumar’s dogged determination, Mukherjee’s name was finally restored to the record. The Indian Council of Medical Research acknowledged him as the true pioneer behind India’s first successful IVF birth. And Durga herself, who now works as a marketing executive in Delhi, came forward on her 25th birthday to tell the world who she was, and to pay tribute to the man who made her birth possible.

Remembering Subhas Mukherjee

Thanks to the integrity of Anand Kumar, Mukherjee’s work is now recognised in the Dictionary of Medical Biography. It’s no Nobel Prize, but it’s a small, overdue nod in a history that very nearly erased him.

The story of IVF is often told as a tale of science defying biology to offer hope where there was none. But it’s also a story about who gets remembered and why. For every name etched in textbooks, there are others – like Subhas Mukherjee – whose brilliance are buried under bureaucracy, politics, or prejudice. That his legacy now lives on, not only in Durga but in the millions born through techniques he helped pioneer, is a quiet kind of justice. History may be slow to correct itself, but sometimes, it does.

About the author: Dominique Olivier

Dominique Olivier is the founder of human.writer, where she uses her love of storytelling and ideation to help brands solve problems.

She is a weekly columnist in Ghost Mail and collaborates with The Finance Ghost on Ghost Mail Weekender, a Sunday publication designed to help you be more interesting.She now also writes a regular column for Daily Maverick.

Where are investors seeking refuge amid uncertainty? And will the recent rebound in global stocks last? In this episode of No Ordinary Wednesday, Investec Wealth and Investment International’s Chief Investment Strategist Chris Holdsworth, and investment strategist Osa Mazwai explore the ongoing impact of US President Donald Trump’s tariff policies.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Anglo American can be thankful for iron ore (JSE: AGL)

And yes, diamonds are still in trouble

2025 is a major transitional year for Anglo American. They will be demerging Anglo American Platinum (see further down) in the next month or so. They are in the process of selling the Steelmaking Coal business to Peabody Energy and the Nickel business to MMG Singapore. And although they have a new long-term diamond sales agreement in place with the Government of Botswana, they would love to sell De Beers.