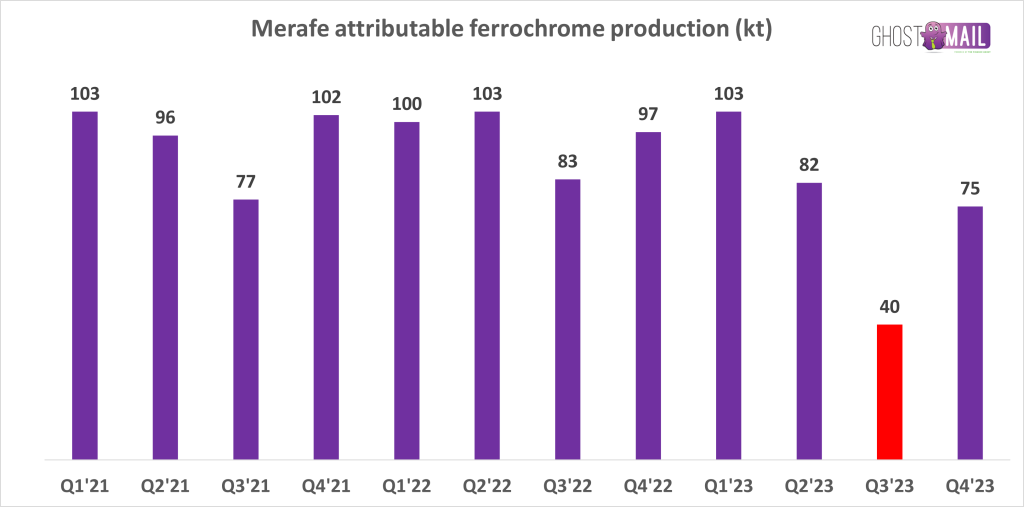

Despite what the name of their infamous reality TV series suggests, it’s actually quite hard to keep up with the Kardashians. With 280 episodes, a combined total of 1 billion followers and 15 businesses between them, this is clearly not the average family. Love them or hate them, you can’t deny that the Kardashians know how to monetise.

I remember reading a headline a while back that said something along the lines of “The Final Episode of Keeping Up With the Kardashians”. Turns out that wasn’t really the end of this reality TV dynasty (they rebranded to “The Kardashians” when they made the move from The E! Network to Hulu), but for a short moment, I still wondered what the world would be like without the so-called “first family” on our screens.

This led to me doing some digging into the Kardashian success story, and as per usual, I learned something that could be of use to business owners. As it turns out, there’s no better place to learn the power of personal branding than in the Kardashians’ stable of businesses.

“You’re doing great, sweetie!”

The question that often gets asked when people are discussing the Kardashians is how this family in particular managed to ingrain themselves so successfully in the global subconscious. I’ve broken it down for you with the help of this interview from the Los Angeles Times.

It all escalated in 2007, which was a big year for the Kardashian-Jenner family. After moving the family into a sprawling home in Hidden Hills, California, matriarch Kris Jenner entered into talks with Ryan Seacrest to create a television series documenting their “everyday” lives. The Kardashians already had a small amount of fame at this point; Kris had been married to Robert Kardashian, who became very visible as part of OJ Simpson’s legal team between 1994 and 1995.

Although Kris and Robert had separated in 1991 already, they had both been close friends with OJ and his wife, Nicole Brown Smith, and the Kardashian clan were often spotted in court during the famous trial. Kris married Olympic athlete and motivational speaker Bruce Jenner in 1991, shortly after her divorce was finalised. Bruce’s sports star status, the family’s combined wealth as well as the memorable surname Kardashian were the ingredients in a recipe for small-scale fame.

Ryan Seacrest sent a camera crew over to film a day’s worth of footage of the Kardashian-Jenners – a blended family made up of 5 daughters and 1 son – at home in their California mansion and was instantly enamoured with the results. Within 48 hours, the first season of the show was sold and Keeping Up With The Kardashians came into being.

But the show itself wasn’t the catalyst that led to superstardom. Those of you who know your internet history will also remember 2007 as the year that Kim Kardashian’s sex tape with her rapper boyfriend Ray J was leaked, making her a household name practically overnight. This helped to catapult the Kardashian family name even further into the spotlight, with Kim becoming the focus of public fascination.

While the Kardashian-Jenners have ardently denied that the leaked tape was a publicity stunt of their own design, that didn’t stop them from doubling down on Kim’s moment and milking it for everything that it was worth. As those who work in public relations will attest, there’s no such thing as bad press. In their TV show’s first season, Kris famously told Kim, “You’re doing great, sweetie!” as her daughter posed nude in a Playboy shoot.

While this seems like an odd course of action for a mother to take, from a business point of view, it makes perfect sense. As a brand, Kim was getting serious traction in 2007, and Kris was standing ready to fan those flames, doing exactly what anyone would expect a top-tier marketing executive to do.

If you’ve got it, flaunt it

The Kardashian business journey began with the establishment of retail stores, including Smooch, a children’s clothing store that operated for six years until its closure in 2009, and Dash, a women’s clothing store launched in California in 2006.

While the family has seen remarkable success with current ventures like Kim’s Skims shapewear brand (valued at a cool $3.2 billion), and Khloe’s size-inclusive denim brand Good American (boasting $200 million in sales), their entrepreneurial path has not been without its share of setbacks. Notable among these are the short-lived PerfectSkin skincare line and the Kardashian Kard prepaid debit card, both lasting only one year in 2010. Additionally, joint business ventures, such as the Kardashian Kollection at Sears (2011-2015) and Kardashian Beauty (2012-2016), reflect a mix of both triumphs and challenges in the Kardashian business portfolio.

Kim is probably the one who has done the most dabbling in various businesses over the last two decades, including the “Kim Kardashian: Hollywood” video game (2014 – present), which was acquired by Glu Mobile in a $2.4 billion deal in 2021. Additionally, her emoticons, known as “Kimojis” (2015 – 2018), achieved notable success, reportedly generating $1 million per minute on the day of launch! In addition to overseeing her shapewear and skincare brands, Kim is now delving into the realm of venture capital with her latest initiative, the private equity firm SKKY Partners. Launched in September 2022, this venture aims to invest in and develop projects within the realms of hospitality, media, and luxury businesses.

Another member of the clan who is well-known for her business ventures is the youngest Jenner. At the age of 18, Kylie Jenner ventured into the makeup industry. The inception of her makeup brand, Kylie Cosmetics, was triggered by the media frenzy surrounding her use of lip filler. In response, Kylie strategically embraced the attention and launched the brand with an initial focus on three “lip kits,” each comprising a liquid lipstick paired with a lip liner. The demand for these products was unprecedented, resulting in immediate sell-outs and launching Kylie Cosmetics into the spotlight.

The success story continued as the brand diversified its offerings, expanding beyond lip kits to include a range of makeup products, such as eyeshadow palettes. Kylie’s entrepreneurial spirit further led her to enter the skincare and baby markets with the introduction of Kylie Skin and Kylie Baby. The financial impact was substantial, with Kylie Cosmetics achieving a remarkable $420 million in revenue within its first 18 months of operation. Surpassing expectations, the brand reached the coveted $1 billion milestone in 2019, accomplishing this feat three years earlier than initially estimated.

The secret to success may be Grede

While Emma Grede may not have the same level of celebrity status as the Kardashian-Jenner family, her behind-the-scenes brilliance has played a pivotal role in launching billion-dollar enterprises with the famous clan.

At 41, this London-born entrepreneur serves as the co-founder and CEO of Good American, the successful clothing line created in collaboration with Khloé Kardashian. Additionally, Emma is the founding partner of Skims. Her diverse portfolio extends to her role as the co-founder of Safely, a cleaning supplies company launched in 2021 in collaboration with Kris Jenner.

Emma’s journey with the Kardashian-Jenners began in 2013 when she first connected with Kris. The two discussed the ambitions of the Kardashian sisters, and Kris, known for her forthrightness, expressed a desire for meaningful participation in their ventures beyond mere endorsements. This sparked Emma’s idea of developing a size-inclusive clothing line, leading to the creation of Good American. The launch was a remarkable success, with $1 million worth of jeans sold on the first day.

In 2017, Emma and her partner Jens relocated to Los Angeles to be closer to the Kardashian-Jenner family and tap into the lucrative US market. Two years later, Emma was approached by Kim Kardashian to collaborate on Skims. Jens oversees the day-to-day operations of the range, while Emma focuses on design, production, planning, and merchandising.

Emma acknowledges the unique storytelling capabilities that each member of the Kardashian-Jenner family brings to the table, describing Kris, Khloé, and Kim as “incredible business partners.” Their partnership exemplifies the fusion of fame and entrepreneurial prowess, demonstrating that, in the world of business, fame can indeed be a powerful accelerator.

Monetise like a Kardashian

You know how each Kardashian has their own “thing”? Kim is the sexy one, Kourtney is the more private one, Khloe is the tall one, etc. It’s like they’ve turned their personal stories – the ups, the downs, and everything in between – into this relatable brand narrative. It’s not just about products; it’s about personalities and connections.

The Kardashians have effectively built and leveraged their personal brands, creating a strong and distinctive identity for each family member that has resulted in massive followings on social media. This individual branding strategy has allowed them to connect with diverse audiences, fostering a sense of authenticity and – dare I say it – relatability.

In my opinion, the main lesson that businesses can learn from the Kardashians is that showing a bit of personality (even if that personality is flawed) and crafting a unique brand story can really make customers feel connected. Having a massive social media following and partnering with the right people are equally important ingredients in the recipe, but they aren’t the secret to success in this instance. For businesses to get a taste of Kardashian success, it’s about creating a brand that people don’t just buy into; they want to be a part of the story.

The question is: can anyone else really keep up with the Kardashians?

About the author:

Dominique Olivier is a fine arts graduate who recently learnt what HEPS means. Although she’s really enjoying learning about the markets, she still doesn’t regret studying art instead.

She brings her love of storytelling and trivia to Ghost Mail, with The Finance Ghost adding a sprinkling of investment knowledge to her work.

Dominique is a freelance writer at Wordy Girl Writes and can be reached on LinkedIn here.

")

")

")

")

")

")