The Magic Markets team is two years into the Magic Markets Premium journey, having recently released the 100th podcast and research report on that platform. The Finance Ghost and Mohammed Nalla also have nearly 150 free weekly Magic Markets shows under their belts.

In short: there’s been a lot going on.

To celebrate the 100-show milestone, I asked the hosts to each pick a handful of insights from the various research activities. Demonstrating the breadth of research coverage and variety of industries, part 1 of this series includes insights from Swatch, TripAdvisor and John Deere.

Swatch: life comes at you fast

In business as in life, disruption can come at you at any time and from any direction. The quartz crisis, which affected Switzerland’s watch industry in the 1970s and 1980s, is a prime example. Swiss watchmakers (who prided themselves on aeons of mechanical expertise and craftsmanship) were blindsided by the rise of quartz technology, which made watches more accurate and affordable.

Suddenly, you didn’t need something expensive just to tell the time.

For context, the Swiss watch industry captured a staggering 50% share of the global watch market before the 1970s. By the late 1970s, quartz timepieces had overtaken mechanical watches in the market, and the Swiss watch industry’s 1,600 watchmakers at the start of that decade had dwindled to just 600.

The lesson here is that even well-established industries and companies can face unexpected challenges. Investors should always be vigilant and open to the possibility of disruption. It doesn’t happen often, but when it does, it can reshape entire markets.

Lab-grown vs. mined diamonds, we are looking at you.

Tripadvisor: the power of Google as a gatekeeper

Google is the go-to interface between internet users and countless businesses worldwide. Although Microsoft is trying hard to make headway with Bing as an alternative, nobody “Bings it” just yet. They Google it.

They don’t “Tripadvisor it” either, unfortunately. Despite this company being a household name, the lesson is clear: if you need to keep paying Google to reach consumers, your business has a structural flaw.

Tripadvisor’s business has been significantly impacted by changes in Google’s search algorithms and advertising practices, underscoring the importance of diversifying customer acquisition channels and not relying too heavily on a single platform. This is especially true when that platform is also one of your biggest competitors!

To make it worse for Tripadvisor, the unit economics are also weak. The share price has lost more than two-thirds of its value over the past five years and there’s no indication of things improving.

John Deere: tractors, but with internet?

The digitisation of industrial companies is a trend that has been reshaping traditional manufacturing and services. Companies like John Deere have been transitioning towards offering “as-a-service” models, where they provide not just equipment but ongoing services and data-driven insights.

This is the classic “internet of things” trend – and in this case, the tractors are the things.

Investors should recognise that even in traditional industries – and is there an industrial industry more traditional than agriculture? – digital transformation is driving innovation and new revenue streams. Companies that adapt to these changes can remain competitive and capture new growth opportunities. Those that don’t will sadly fall behind the curve.

And if you need a good example of why John Deere likes the combination of hardware and service revenue, look no further than the house that Apple built!

Investing in global stocks requires careful research, regular monitoring and an ability to spot changing market dynamics. That’s a lot to try do on your own, which is why Magic Markets Premium brings you a weekly research report and podcast on global stocks. At justR99/month, it’s a bargain. To celebrate the 100th report, you can use the coupon MAGIC100EPS on checkout to pay R899/annum instead of the usual R999/annum. Be quick! This deal is only valid until the end of October.

About the author:

Dominique Olivier is a fine arts graduate who recently learnt what HEPS means.Although she’s really enjoying learning about the markets, she still doesn’t regret studying art instead.

She brings her love of storytelling and trivia to Ghost Mail, with The Finance Ghost adding a sprinkling of investment knowledge to her work.

Unlock the Stock is a platform designed to let retail investors experience life as a sell-side analyst. Corporate management teams give a presentation and then we open the floor to an interactive Q&A session, facilitated by the hosts.

This year, Unlock the Stock is delivered to you in proud association with A2X, a stock exchange playing an integral part in the progression of the South African marketplace. To find out more, visit the A2X website.

In the 27th edition of Unlock the Stock, we welcomed Lesaka Technologies to the platform for the first time. The management team gave a presentation on the performance and strategy and took numerous questions from attendees.

As usual, I co-hosted the event with Mark Tobin of Coffee Microcaps and the team from Keyter Rech Investor Solutions. Watch the recording here:

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

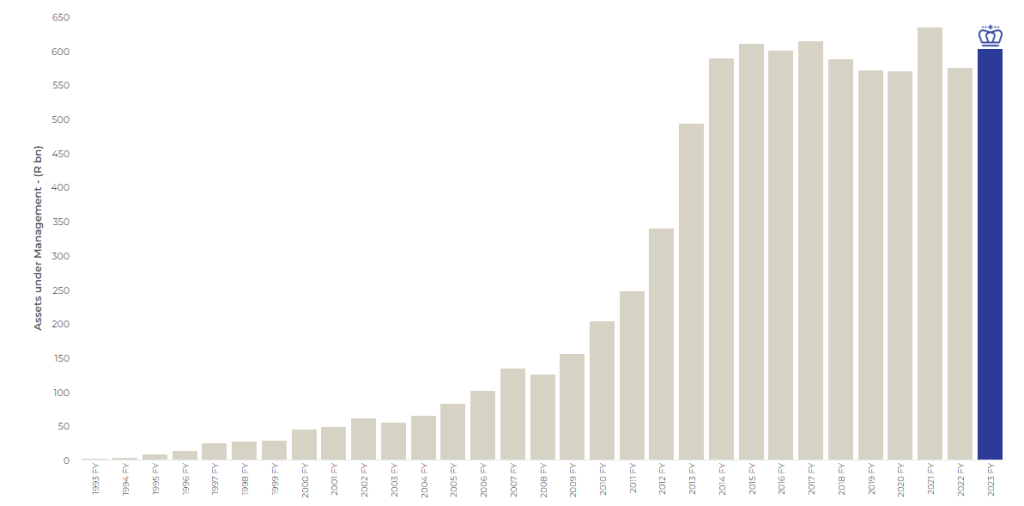

Coronation loves making us go look for historical AUM (JSE: CML)

This really frustrates me

Every time that Coronation announces its assets under management (AUM) on SENS, the company neglects to include comparable levels. This is irritating and it makes me want to highlight the reason why that might be the case.

If you go digging on their website, there is a chart dealing with annual AUM going all the way back to 1993. I’m afraid that the last decade tells quite the story:

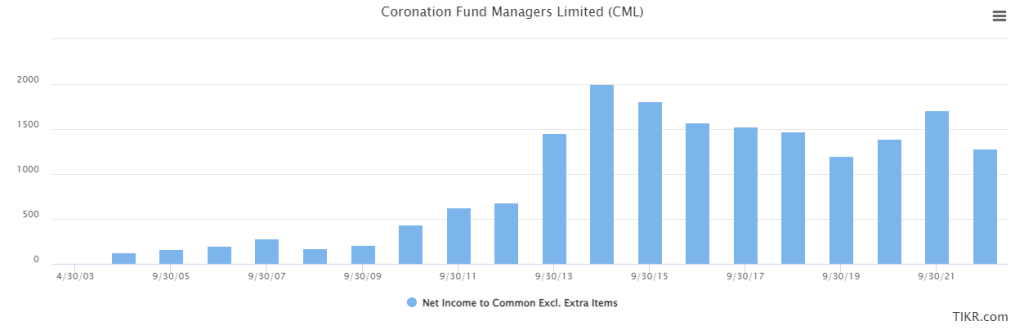

When AUM has essentially gone nowhere in 10 years and costs have been rising, it shouldn’t come as a shock to see a net income chart that looks like this:

I often hear the argument that Coronation is attractive as a dividend paying stock. Even if we ignore the recent tax problem, I’m afraid that this is a classic case of the dividend yield not even offsetting the share price decline, so the total return is practically non-existent.

The lesson here? Don’t invest in a stagnant business just because of the dividend. Different strokes for different folks I suppose, but I can’t get my head around taking equity risk on something that isn’t growing.

This historical performance is important context when looking at the results for the year ended September 2023. Although we only have a trading statement to work off at this stage, it’s detailed enough to get a good idea of what the performance looks like in this period.

The tax fight with SARS is heading to the Constitutional Court. It was worth 205 cents per share in this period, so this has been the driver of the drop in HEPS of between 164.8 cents and 201.4 cents. It’s also important to reference fund management earnings per share as a purer view on operational performance, with earnings down by between 212.8 cents and 251.5 cents per share. Through that lens, the tax issue is certainly the largest driver of the drop, but it’s not like the core business is going in the right direction either.

With South African investors under pressure from every angle, it’s hard to get excited about Coronation’s prospects.

Finbond is much closer to being profitable (JSE: FGL)

Core growth metrics are looking positive

Finbond has had a tough time, including in the US where regulatory changes in Illinois hurt the business. Things are looking considerably better for the six months ended August, although the group is still loss-making with a headline loss per share of -2.3 cents vs. a loss of -8.2 cents in the comparable period.

The value of loans advanced increased by 23.2% and total revenue was 14.3% higher. As encouraging as that is, the overhang of stimulus in the US is that US volumes are still only 75% of pre-COVID levels, as customer savings levels are 30% higher than pre-COVID.

One of the problems with higher growth is that the loans in the US are 18- to 24-month products, yet the expected credit loss must be recognised at the commencement of the loan. The interest is only earned over the period of the loan. This drives a substantial lag in profitability. Another issue for profitability is the fixed cost base, so scale is important and needs to improve.

It’s interesting to note that the average size of a retail deposit at Finbond Mutual Bank is over R356k, with a weighted average interest rate of 9.3% and weighted average deposit term of 27.9 months. The group has R583 million in retail deposits. This is still much smaller than the R2.4 billion in commercial paper in South Africa. The rest of the funding is in the US, worth R466 million. The balance sheet is built around a strategy of having long-term liabilities and short-term assets, which minimises liquidity risk.

And in case you’re wondering, the average consumer loan size in South Africa is just under R2k. The entire loan portfolio turns over approximately four times a year.

The net impairment is 21.7% of revenue.

Finbond is trading at 35 cents per share. It’s up around 30% in six months but has lost 90% of its value over five years. I must say, it’s looking kinda interesting as a more speculative play.

Gemfields gives a summary of its share buybacks (JSE: GML)

The company has repurchased 4.59% of its issued share capital since November 2022

Under JSE rules, a company must make an announcement once 3% of issued shares have been repurchased. Gemfields is operating under the general authority at the last AGM to repurchase shares and has reached 4.59% of the shares that were in issue at the date of that meeting.

This means that R176 million has been invested in share buybacks at an average price of R3.1751 per share. That’s practically the same as the current traded price.

Merafe reports on nine-month production figures (JSE: MRF)

There was a deliberate reduction in production over the winter months

Merafe has reported its attributable ferrochrome production from the Glencore Merafe Chrome Venture for the third quarter ended September. It came in at 40kt, way below the run-rate for the nine-month number of 225kt.

This is because of a pullback in production in response to market conditions, with only one smelter operating over the winter season when electricity was more expensive.

For the nine months, production is 21.4% lower year-on-year.

Reinet’s fund NAV dipped this quarter (JSE: RNI)

This is a precursor to the NAV of the listed company

The bulk of Reinet’s NAV is captured in Reinet Fund, which includes the investments in Pension Insurance Corporation, British American Tobacco and others. The group always releases the NAV of the fund before releasing the NAV of the group. The NAV itself is different at group level but the direction of travel is usually consistent.

As at 30 September, the NAV per share of Reinet Fund was €32.79. This has dipped by 0.6% in the past three months.

The cycle seems to be turning against Santova (JSE: SNV)

This had to happen eventually

Logistics group Santova has been a darling of the local small cap universe, with the share price up 133% over five years. If you bought in the depths of COVID, you’re up 277% over three years.

The group was a net beneficiary of supply chain pressures across the world, assisted by a solid expansion strategy. At some point though, the cyclical nature of logistics had to play a role.

In a trading statement dealing with the six months to August 2023, HEPS is down by between 20.9% and 25.9%. The actual guided range is 57.87 cents to 61.78 cents vs. 78.11 cents in the comparable period.

The share price closed 3% lower on the day of the announcement at R7.61.

Noel Doyle is on his way out at Tiger Brands (JSE: TBS)

It won’t do much for his self-esteem that the market rallied in response

Markets are cruel things. They well and truly don’t care about your feelings. Noel Doyle has “jointly agreed” to part ways with Tiger Brands, with the company saying that “new leadership was required to respond to the challenges currently facing the company” – in other words, he was asked to leave after over 20 years of service with the company. The market responded with the share price closing 11% higher.

If you ever want to know what the challenges are, just walk to the baked beans aisle at your local grocery store. There, you will see Koo beans priced at a premium to various other competitors because of the supposed strength of the brand. I am quite sure that consumers eating baked beans don’t really care about the strength of the brand at a time when prices have basically doubled over the past couple of years. Ditto for Albany Bread, which is more expensive than competitors.

Doyle’s replacement is Tjaart Kruger. He is no stranger to Tiger Brands, having worked in the group from 2001 to 2007. He then ran Premier Foods from 2011 to 2021. Kruger has signed a 26-month contract with Tiger Brands, which is a weirdly specific tenure. It also means that this a transitionary period in leadership, as the group will be looking for a CEO to take over from Kruger. Doyle will remain available to Tiger Brands until March 2024 to help with the handover.

In case you still don’t believe me about the baked beans, perhaps a trading statement for the year ended September 2023 will convince you. The performance at segmental level varies considerably (as one might expect), with HEPS from total operations expected to differ by between -5% and 2% vs. the comparable period. Notably, the Groceries and Snacks & Treats businesses are experiencing overall volume declines.

KOO sometimes isn’t the best you can do.

Little Bites:

Director dealings:

The CEO of Equites (JSE: EQU) has sold shares worth R26 million. This represents around 18% of his stake in the company. The share price is down 28% this year and this sale won’t do the trajectory any favours.

A director of a major subsidiary of Woolworths (JSE: WHL) sold shares worth R5.1 million. The Woolworths share price is down 16% in 90 days, so I wouldn’t ignore that.

A prescribed officer at ADvTECH (JSE: ADH) has sold shares worth R2.6 million.

Des de Beer has bought another R1.75 million worth of shares in Lighthouse Properties (JSE: LTE)

There have been various recent off-market purchases of shares in DRA Global (JSE: DRA) by Apex Partners, an associate of director Charles Pettit.

As part of the buyout and delisting of Transcend Residential Property Fund (JSE: TPF) by Emira Property Fund (JSE: EMI), there is a “clean-out dividend” to be paid to Transcend shareholders to cover the period from 1 April 2023 until the date of the implementation of the deal. The board has determined that this dividend is 29.44 cents per share.

CORRECTION: The Quilter (JSE: QLT) odd-lot offer doesn’t follow the usual approach at all. It applies to 200 shares rather than 100, but more importantly you needed to be on the register on 28 April to qualify.

The weirdness around aReit Prop (JSE: APO) never seems to end. In an announcement dealing with a special resolution for financial assistance, I learnt that aReit Prop can’t collect the rentals directly on a property because it hasn’t been able to finalise a VAT registration since March 2022. The company hopes to finalise this in October 2023. Even more hilariously, the website doesn’t work (or at least not when I tried to access it).

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

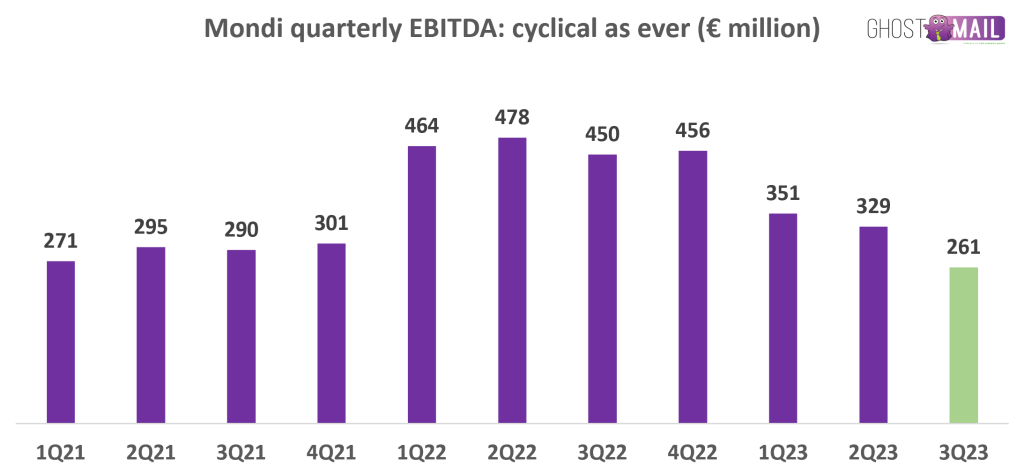

The market expected more from Mondi (JSE: MNP)

The share price didn’t enjoy the quarterly earnings release

Mondi closed 6.8% lower after providing a quarterly trading update dealing with the three months ended September. Market demand was “soft” and selling prices came under pressure, a combination that investors never want to see.

To add to this pressure on EBITDA, there was a far lower forestry fair value gain in this quarter. The fair value gains sit in EBITDA, which is part of why the earnings can be this volatile:

It’s difficult for cyclical companies to make long-term decisions, but Mondi still believes in the structural growth in the packaging markets that it serves. For this reason, the €1.2 billion expansionary projects pipeline remains in place and is running within budget.

Sasol asks shareholders to give it flexibility on the convertible bonds (JSE: SOL)

If shareholders give the green light, the convertible bonds can be equity settled

In November 2022, Sasol announced that $750 million had been raised through the issuance of convertible bonds. The conversion is currently cash-settled, with Sasol wanting shareholders to give the company the flexibility to settle any future conversion by issuing ordinary shares instead.

The problem for Sasol is that if the only way to settle the conversion is through cash rather than shares, then the company constantly has this potential conversion hanging over its head. If shares can be issued instead, it frees up cash for other corporate purposes.

Of course, for shareholders, the prospect of equity settlement is dilutionary and technically puts an overhang on the share price instead of on the management team.

For this reason, Sasol is asking shareholders extra nicely to say yes. In case you’re interested, the circular can be found here.

Vunani’s earnings drop but the divi is steady (JSE: VUN)

If you read carefully, the insurance business is carrying the team

Vunani reported a 4% increase in revenue and premiums and a 7% drop in profit after tax for the six months ended August. There are many things that happen between those two numbers, including fair value movements.

We therefore need to dig deeper into the business. The largest revenue contributor is the insurance business, responsible for 36.5% of group revenue. It’s also the major growth driver in the group, up roughly 25%.

The next largest segment is asset administration, with revenue up by 6.8%. This segment contributes over 30% of group revenue.

Fund management is up next, with this segment heading in the wrong direction. It’s down roughly 12.5% in revenue. Because of the operating leverage in that business, profit is down 47%.

Within the smaller investment banking business, advisory revenue fell to R14.8 million but at least that business turned positive at profit level, so costs were presumably cut. No such luck in institutional securities broking, with that race-to-the-bottom business reporting yet another loss. Revenue was flat and the loss has worsened from R940k to R3.4 million.

Overall, HEPS fell by 10.8% to 18.2 cents and the dividend was steady at 9 cents per share.

Little Bites:

Director dealings:

You’ll never believe it, but Des de Beer bought R352k worth of shares in Lighthouse Properties (JSE: LTE)

I’ve seen some views in the market that the extensive sales of shares by the CEO of Truworths (JSE: TRU), Michael Mark, is a strong sell signal. These sales related to share options issued many years ago. Given that information and Michael Mark’s age, I’m still not sure these are such a strong signal, especially as many shares are also being retained when the options are being exercised.

The CFO of Mpact (JSE: MPT) and his associates have sold shares in the company worth R67k.

Primeserv (JSE: PMV) announced the acquisition of a business back in May 2023 for almost R11 million. The resolutive conditions have now been fulfilled. A resolutive condition is different to a suspensive condition in that the deal actually closes when there are resolutive conditions, with an attempt made to subsequently unscramble the egg if a resolutive condition isn’t met. It’s rare to see this in practice because it can be a practical nightmare.

BHP along with its joint venture partner Mitsubishi Development, are to disinvest from the Australian Blackwater and Daunia mines. Two wholly owned subsidiaries of Whitehaven Coal will acquire the mines for a cash consideration of up to US$4,1 billion. Completion of the transaction is expected to occur in the June 2024 quarter.

Omnia has taken a minority stake in Swedish-based Hypex Bio Explosive Technology. Omnia sees the deal as a strategic partnership; one that will enhance the ongoing development and commercial rollout of Hypex’s HP emulsion technology in key markets and will provide BME, Omnia’s provider of blasting solutions subsidiary, with access to state-of-the-art technology. Financial details were undisclosed.

Hyprop Investments has concluded a sale agreement to acquire Table Bay Mall for R1,6 billion. The company notes that an additional R23,3 million will be paid in respect of the cost of the solar panels currently being installed at the mall – a sign of our times. The addition of this asset to its portfolio is consistent with the company’s strategy to increase its exposure to the Western Cape. The acquisition is classified as a category 2 transaction, so shareholder approval is not required.

In another property transaction announced this week Accelerate Property Fund has disposed of two office properties in the Eastgate area – Pri-movie Park situated at 185 Katherine Street and 1 Charles Crescent. The purchaser, Micawber 832, will pay a combined R117 million. Accelerate shareholders are not required to approve this transaction.

Concert parties African Equity Empowerment Investments (AEEI) and Sekunjalo Investment Holdings (SIH) have made an offer to AEEI shareholders to acquire their shares for R1.15 per share. The offer price is a 28% premium on the share price of R0.90 prior to the announcement. The offer is for a maximum 144,336,812 shares (SIH holds a 70.6% stake in AEEI which is excluded from the offer) for a maximum offer consideration of c.R166 million. At the time of the announcement 47.27% of shares held by eligible shareholders had undertaken to vote in favour of the delisting resolution.

Following a strategic review of its businesses against a backdrop of the current economic, political and competitive landscape, Sasfin has announced the disposal of its Capital Equipment Finance and Commercial Property Finance businesses to African Bank for an aggregate consideration of c. R3,26 billion. Post the transaction, Sasfin will retain its Wealth, Rental Finance and focused Banking businesses which it aims to strengthen and scale.

Boland Rugby has announced a transformative equity partnership with Stellenbosch Academy of Sport, a subsidiary of Remgro, and a consortium comprising companies controlled by the Motsepe family. Remgro and African Rainbow Capital Investments will each own a 37% of the Boland Rugby Union – with the union retaining the remaining 26%.

Deneb Investments via its subsidiary Sargas, has disposed of properties considered non-core to its growth strategy. The properties, situated at 40 Leicester Road, Mobeni West in Durban, are to be sold to Groforce Investments for a cash consideration of R65 million. The disposal consideration will be used to settle outstanding debt.

Unlisted Companies

The Hollard Group, a mass-market life insurance company, has announced a strategic investment in SA-based insurtech, Simply Financial Services, a registered FSP and insurance software developer. The undisclosed investment by Hollard will enable the insurance disruptor to scale the business and target a larger pool of individuals and businesses.

Licensed open-access fibre infrastructure provider, Frogfoot Networks, has acquired Garden Route Networks and Route Networks as it expands its connectivity capabilities in parts of South Africa’s coastal region. Financial details were not disclosed.

Global financial services provider Apex Group has announced the sale by its BEE partner Ditikeni Trust of a minority stake in the South African subsidiary Apex Fund Services to a B-BBEE consortium. The stake has been sold to a consortium led by Ntiso Investment Holdings and Akhona Group. Financial details were undisclosed. In addition, Apex announced the successful close of the acquisition of Boutique Collective Investments (BCI) and Boutique Investment Partners (BIP). BCI is a collective investments scheme manager with a core business focus on third-party branded portfolios while BIP is an independent investment management and consulting firm providing multi-manager and consulting services to South African independent financial advisers and their retail and institutional clients.

Belgium headquartered P95, a provider of clinical and observational services to vaccine developers, is to merge with local clinical research organisation OnQ Research. Post the transaction P95-OnQ will have a physical presence in 30 countries with offices in Europe, Latin America, Asia and Africa with services covering both regulatory-grade real-world evidence and full-service interventional clinical trial research.

South African owner and operator of serviced last-mile logistic parks, Inospace, has acquired a landmark A-grade industrial facility in Paarden Eiland from the liquidators of shipbuilder Nautic Africa. The vacant property was purchased at a rate of R8,900/m² and has a gross lettable area of 8,400m² under a 22-metre-high roof.

Knife Capital, the Cape-based venture capital investment manager, has led a Series A funding round by Outsized. The talent-on-demand platform enables large enterprise clients and consulting firms in Asia-Pacific, Africa and the Middle East to implement flexible workforce models.

Zeder has declared an ad-hoc gross special dividend of 10 cents per share (R154 million) in its interim results. This is the second special dividend to shareholders; earlier this year the company announced a special dividend of 5 cents per share (R77 million) which was paid out in August.

Exemplar REITail is proposing an equity raise by issuing up to 99,687,204 shares for cash in a private placing via a bookbuild process. The raise is intended to create the headroom for debt-funded growth.

Shareholders of Prosus N shares are to receive a capital repayment of €0.07 (R1.41) per share. Those shareholders not wishing to receive a capital repayment can instead elect to receive a dividend.

Several listed companies reported repurchasing shares this week. They were:

Gemfields has repurchased an additional 40,062,001 ordinary shares for a total consideration of R126,19 million. The repurchased shares will be held as treasury shares.

Prosus and Naspers continued with their open-ended share repurchase programmes. During the period 9 – 13 October 2023, a further 3,525,732 Prosus shares were repurchased for an aggregate €99,47 million and a further 337,605 Naspers shares for a total consideration of R1,05 billion.

Glencore intends to complete its programme to repurchase the company’s ordinary shares on the open market for an aggregate value of $1,2 billion by February 2024. This week the company repurchased a further 9,65,000 shares for a total consideration of £44,53 million.

South32 continued with its programme of repurchasing shares in the open market. This week a further 2,019,525 shares were acquired at an aggregate cost of A$7,04 million.

Primary Health Properties plc is to take a secondary inward listing on the Health Care REIT sector of the JSE. The UK-based company, an investor in modern primary healthcare premises across the UK and Ireland, has a primary listing on the LSE and is included on the FTSE 250 Index. The REIT will commence trading on the main board of the JSE on 24 October 2023.

With effect from 26 October 2023, Vodacom’s shares will trade on A2X. The company will retain its primary listing on the JSE and its issued share capital will be unaffected by the additional listing.

The JSE has warned shareholders of aReit Prop, AH-Vest and Sasfin that the companies may face suspension and possible removal of their listings from the bourse if the companies fail to release financial statements before 31 October 2023.

One company issued a profit warning this week: Pick n Pay (update).

Three companies issued or withdrew a cautionary notice: Ellies, enX and Afristrat Investment.

Afreximbank’s impact investment subsidiary, The Fund for Export Development in Africa (FEDA) has invested in the Cabinda Oil Refinery in Angola. Financial terms were not disclosed. The 60,000 barrel per day refinery is an integrated modular oil refining platform being developed by joint venture partners Gemcorp and Sonangol.

Verod Capital and AfricInvest have acquired a majority stake in ICT solutions provider, iSON Xperiences. The companies did not disclose the value or size of the stake, but this is a follow-on investment for AfricInvest who first invested back in 2018. iSON operates in 19 countries, 16 of which are in Africa and serves more than 500 million end-users across multiple sectors.

Oasis Capital Ghana has announced its first complete exit from the Oasis Africa Fund 1, through the successful exit of its holdings in Legacy Girls College in Ghana.

Orosur Mining, a minerals explorer and developer operating in Columbia, Argentina and Brazil, has expanded into Africa with the announcement of a joint venture with Nigeria’s Jurassic Mines. The 70%:30% joint venture partners have agreed to explore a number of exploration licences across Nigeria, considered to be highly prospective for lithium mineralisation. The 70% stake is structured as a two-phase earn-in of US$3 million expenditure for a 51% stake and $2 million for the remaining 19%.

Shell and Saudi Aramco have partnered up to join the bidding for Wataniya Petroleum, a subsidiary of the Egyptian military-owned, National Service Products Organization. Other contenders include ADNOC, North Petroleum International Company, Emirates National Oil Company and TAQA Arabia.

Crafty Workshop, an Egyptian edtech founded in 2019, has raised US$400,00 in seed funding from EdVentures. This is a follow-on investment for the edtech investor who first invested in 2019. The e-learning platform specialises in the creative industries and also serves as a vocational training provider.

Nigerian insurtech startup Haba has announced a US$75,000 pre-seed funding raise from undisclosed investors. The funding will be used to enhance the company’s service capabilities, strengthen its technical team and increase its marketing reach to grow its individual customer base.

Access Afya, a Kenyan healthcare operating system, has raised a significant investment from the Philips Foundation and the UBS Optimus Foundation. The exact size of the funding was not disclosed.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Accelerate sells off two difficult office buildings (JSE: APF)

The purchasers no doubt have interesting plans for these buildings

Accelerate Property Fund needs to reduce debt and doesn’t have the time to focus on particularly difficult buildings. Two such buildings are the Pri-movie Park office and warehouse and the 1 Charles Crescent office building, both in Eastgate. The fund has sold both buildings at a combined price of R117 million.

The vacancy levels are gigantic. The purchaser (a consortium of four family trusts including a couple of guys I knew at university) must have something different planned for the properties, as a condition to the deal is that Accelerate must sign the required resolutions for the re-zoning of the properties.

BHP disposes of two coal assets in Australia (JSE: BHG)

Two mines in the BHP Mitsubishi Alliance are being sold to WhitehavenCoal

The Blackwater and Daunia mines are being sold for a combined cash consideration of up to $4.1 billion. BHP holds 50% in these assets through the BHP Mitsubishi Alliance metallurgical coal joint venture in Australia.

$2.1 billion in cash is payable on completion, with $1.1 billion payable in cash over three years. The remaining $0.9 billion is structured as an earn-out over 3 years. It’s interesting to note that $100 million is payable as a deposit, which would act as a break fee in certain circumstances i.e. the sellers will retain this amount if the buyers walk away.

The net proceeds of the deal will be used to reduce debt.

In a separate announcement dealing with an operational review for the quarter ended September, BHP noted that it is on track to achieve full-year production and unit cost guidance at all its assets. The highlight in this quarter was an 11% increase in copper production year-on-year.

Of course, meeting guidance doesn’t mean that all production has moved higher. It just means that performance is in line with expectations. For example, iron ore and metallurgical coal are both down year-on-year, as is nickel. When looking at quarterly numbers, the timing of maintenance programmes at individual assets can have a big impact.

The bigger concern is that average realised prices have fallen in this quarter vs. the second half of 2023 for literally every single commodity in the group.

EOH’s operating profit is 35% higher, but is that enough? (JSE: EOH)

Even after the rights issue, there’s a lot of debt here

EOH’s revenue from continuing operations could only increase by 3.3% for the year ended July. That’s pedestrian at best, although the good news is that operating profit from continuing operations increased by 35%. A very important number is adjusted EBITDA from continuing operations, as this is a proxy for cash profits. It decreased by 11.5% to R322 million.

The adjusted EBITDA margin for the continuing operations is only 5.2%, which really isn’t anything to get excited about. This remains a low margin, unexciting business. It just happens to have a rollercoaster of a corporate history.

There is still a headline loss per share from continuing operations, but that’s because of the level of debt in this financial year. R678 million was repaid during the year, the bulk of which came from the R555 million equity raise. The problem is that the balance at the end of July 2023 is R683 million just in interest-bearing bank loans, so that’s still a whole lotta debt in this environment. If you include bank overdrafts and the ring-fenced project finance loan from the IDC, it’s up to R833 million.

Stephen van Coller as extended his contract as CEO by six months until March 2024. He did his job in terms of saving the existence of EOH and helping it achieve a stable balance sheet. There’s also a change to the CFO role, with Marialet Greeff an an internal appointment to replace Megan Pydigadu.

It may be steady, but is it now a good investment? With such a modest EBITDA margin and this much debt still on the balance sheet, I’m not excited by this story. Neither are the outgoing execs, it seems.

Pick n Pay laid bare just how bad it is (JSE: PIK)

If you had been paying attention to the stores around you, this wasn’t a surprise

You know those green scooters that you keep seeing literally everywhere? The ones with the Checkers Sixty60 branding? That also counts as stock research. Common sense would’ve gotten you a long way this year with avoiding being on the wrong side of this chart:

The 12.5% drop on Wednesday after the release of results could’ve been avoided just by reading the trading statement, which made it clear that Pick n Pay is now loss-making even before considering diesel costs.

The reason for this starts very high up the income statement, with turnover up by just 5.4% and gross profit margin dropping from 19.4% to 18.5%. Trading expenses jumped by 13.7%. That’s a disaster, driving a decrease in trading profit of 97.5%.

The group made just R31.8 million in trading profit in the 26 weeks to 27 August, with a loss before tax of R837.2 million because of a huge increase in net finance charges. Unsurprisingly, the interim dividend is a thing of the past.

Of course, the announcement raises the R396 million spent on load shedding and blames this for Pick n Pay’s inability to respond to a more promotional environment. What it doesn’t say is that Shoprite (and others) are operating in exactly the same conditions, so it’s all relative. The reality for Pick n Pay is that years of strategic misstep chickens have now come home to roost.

If we are going to scratch around like chickens for the positives, then Boxer grew 16.1% and Pick n Pay Clothing (in my opinion the best business in the group) grew 13.8%. Online sales growth was 76.3%, although one would expect to see a big number there. Value-added services income grew by 13.5%.

Sean Summers has one hell of a task on his hands.

Quilter achieved a mixed result in the third quarter (JSE: QLT)

Net inflows in the core business are only slightly positive

When measuring the performance of an asset or wealth management business, assets under management and administration (AuMA) is a metric that only tells part of the story. These companies cannot control the movements in global asset values, with this factor having the biggest impact on AuMA. To really measure the performance of the company, you need to look at net flows and whether the manager is attracting new clients or not.

At Quilter, Old Mutual’s old wealth management business in the UK, some parts of the business are showing decent growth. This includes the Quilter distribution channel, with net inflows year-to-date of 16% of opening AuMA in the High Net Worth segment and 11% in the Affluent segment. In contrast, the independent financial advisor (IFA) channel on the Quilter platform experienced a net outflow. Another useful metric to consider is sales per Quilter advisor as a measure of productivity, up 23% year-on-year.

The non-core business experienced outflows consistent with the run-rate in the first half, after adjusting for once-off fund closures.

With all said and done, AuMA of £101.4 billion as at the end of September was very similar to the £101.7 billion level reported at the end of June.

Little Bites:

Director dealings:

Des de Beer has bought another R1.7 million worth of shares in Lighthouse Properties (JSE: LTE). That’s not all folks, because he’s also bought R2.67 million worth of shares in Resilient REIT (JSE: RES).

If you are a shareholder in Caxton and CTP Publishers and Printers (JSE: CAT), look out for an investor presentation that should become available on the website on Monday 23 October.

Impala Platinum (JSE: IMP) released an announcement clarifying the broader scope of the financial assistance resolution put forward in the AGM notice. The reason for the increased scope vs. previous years is because of the need to implement a B-BBEE transaction as part of the acquisition of Royal Bafokeng Platinum.

Following his investment in Apex Group, Mcebisi Jonas has resigned as a non-executive director of Sygnia (JSE: SYG) as this is a competing business interest.

Transcend Residential Property Fund (JSE: TPF) announced that the offer by Emira Property Fund (JSE: EMI) has become unconditional. A further announcement will be made about the clean-out dividend and the finalisation information.

Languishing at below R5 per share, Transaction Capital (JSE: TCP) announced that Coronation is at least buying the dip of all dips, increasing its stake in the company from 19.85% to 20.15%.

In 2022, Sasol (JSE: SOL) announced the appointment of Andreas Schierenbeck as a non-executive director, with much hype around the contribution he would make to decarbonisation efforts. He didn’t stick around for long, now resigning from the board based on increasing demands on his time away from Sasol and the risk of conflict of interests based on energy sector opportunities being pursued by the group.

Listen to the latest episode of Ghost Wrap here, brought to you by Mazars:

Exemplar REITail wants to raise capital via a bookbuild (JSE: EXP)

A capital raise has become a rare sight on the JSE

Exemplar REITail wants to reduce its loan-to-value ratio and try to improve the spread of institutional holders. The problem is that the net asset value (NAV) per share was R14.10 at the end of February 2023 and the share price is R10.10, so any share issuance would be at a discount to NAV.

In this case, the company doesn’t seem too bothered by this. Minority shareholders won’t be thrilled, as the planned capital raise is a bookbuild process rather than a rights issue, so not every shareholder would be able to participate. I think it’s even worse when the raise is simply to reduce debt, especially when the current loan-to-value ratio of 36.3% isn’t even very high!

It’s not a small raise either, with a plan to issue up to 99,687,204 shares – a very precise indication indeed, especially since the circular doesn’t give an intended rand value! The issue price for the bookbuild is a discount of up to 10% to the 30-day VWAP calculated at a future point in time. If we just use the current price for simplicity, this is a raise of roughly R900 million by a company with a market cap of R3.4 billion. Shareholders who don’t get to participate in the bookbuild likely aren’t going to be happy about this.

The loan-to-value will be under 25% after this deal. The company doesn’t plan to stay there, as the headroom on the balance sheet would be used for further acquisitions.

In other words, instead of raising equity capital for a specific purpose, the management team wants to issue shares at a discount and effectively be given a blank cheque for further acquisitions. I’m quite happy to not be invested here.

Hyprop is acquiring Table Bay Mall (JSE: HYP)

This mall perfectly captures the semigration trend

Table Bay Mall is in Sunningdale, which is in the part of Cape Town that is growing really quickly and attracting many families from Gauteng. I have shopped there multiple times and I can tell you with confidence that this is a good asset.

I was less pleased to read in the Hyprop acquisition announcement that there are 5,000 to 7,500 residential units in the pipeline for the area over the next 5 – 10 years. The traffic simply isn’t going to cope.

Practical worries aside, Hyprop is investing in the right area and relatively early in the life cycle of this particular property. The deal is worth R1.625 billion and it will be settled in cash. Hyprop will use existing undrawn borrowing facilities and might use some of the proceeds from the pending dividend reinvestment programme.

After this deal, Hyprop’s loan-to-value ratio is expected to be around 40.3%.

Interestingly, the solar installation has been noted separately in the transaction, with a value of R23.3 million.

By now, you must be itching to know what the acquisition yield was. The net property income for the mall was R108.6 million for the year ended February 2023 and the projection for the next 12 months (i.e. 1 November 2023 to 31 October 2024) is R125.7 million. This puts it on a forward yield of 7.7%, so this was anything but a cheap transaction.

The price may seem high, but I do like the strategic nature of this property.

Separately, Hyprop announced that GCR Ratings has upgraded the credit rating on the Domestic Medium-Term Note Programme. The outlook for Hyprop is Stable according to the agency.

Jubilee Metals is awarded a slag project in Zambia (JSE: JBL)

This isa joint venture with Mopani Copper Mines

The large Mufulira Slag Project has been awarded to Jubilee Metals in the form of a joint venture with Mopani Copper Mines. There are 13 million tonnes of historical slag to be processed, estimated to contain 0.7% copper and 0.27% cobalt in addition to slag arisings. The copper grades within the slag are believed to be double those of standard tailings, so Jubilee is rather excited.

This is quite the project, as it requires the development of the processing solution and the raising of capital as well. At this stage, no numbers regarding future potential profits or returns have been provided.

Ninety One’s AUM continues to drop (JSE: N91)

This isn’t encouraging news ahead of the release of interim results

Ninety One has announced its assets under management (AUM) as at 30 September 2023. This has come in at £123.1 billion, below £124.8 billion at the end of June and £129.3 billion at the end of March this year. For a 12-month view, AUM was £132.3 billion as at the end of September 2022.

Results for the six months to September will be released on 15 November.

The JSE is getting a new listing (and this isn’t a typo) (JSE: PHP)

Primary Health Properties joins us from the UK

Brace yourself: there’s a new listing on the JSE. It’s an offshore REIT, which is perhaps predictable given the popularity of REITs on the JSE. Primary Health Properties (or PHP) is a healthcare REIT that derives 89% of its income from government bodies in the UK and Ireland. Unlike in South Africa, it’s likely that the government actually pays the rent in those countries.

Goodness knows that this isn’t the most exciting way to make money, but the dividend has increased for 27 consecutive years. The annual rent roll is £147.4 million off a property portfolio worth £2.783 billion, so that’s a yield of 5.3% before expenses and debt. Net overheads come to around 10.1% of gross rental income.

97% of the company’s debt is fixed or hedged for a weighted average period of just under seven years, so there’s some protection against this high interest rate environment. Still, low yielding European funds haven’t exactly been having fun, as this chart of the share price in London shows:

There is no capital raise as part of this listing, so this is simply the implementation of a secondary listing to try tap into the South African investor market to drive interest in the shares. It will be interesting to see whether local investors put much value on the defensive tenant base and the hard currency earnings, as this interest rate cycle isn’t finished dishing out pain.

Standard Bank keeps waving its flag (JSE: SBK)

The latest quarter is another strong result

Standard Bank releases a quarterly update to the market because the group needs to provide high level numbers to the Industrial and Commercial Bank of China (ICBC) to enable that entity to equity account its investment in Standard Bank.

This is great because we get more regular updates than would otherwise be the case.

For the first nine months of the year, earnings are up by 30% year-on-year. Both income and cost growth was slower in Q3 than the first six months, but the group still achieved positive JAWS (higher operating margin). The credit loss ratio for the nine months remains within the group’s target range of 70 to 100 basis points.

Over the nine months, the Africa regions contributed 44% to group headline earnings.

Chrome numbs the pain at Tharisa (JSE: THA)

The PGM numbers look really tough

For the year ended September 2023, chrome production was essentially flat at Tharisa and 6E PGM production fell sharply by 19.3%. That’s only the first part of the story. The other part, of course, is commodity pricing. Average chrome prices increased by 25.8% and average PGM prices fell 26.2%. The divergence between the commodities couldn’t be more stark.

This divergence has driven a decision to slow down the Karo Platinum Project, with the commissioning date pushed out 12 months to June 2025. The timeline can be accelerated if markets become more favourable for PGMs.

Production guidance for FY24 is for a flat or slightly higher production number for 6E PGMs, with chrome production expected to increase by as much as 14%.

The net cash position has decreased from $141.5 million at the end of June 2023 to $126.6 million.

The share price closed 5% lower after this update.

Zeder releases results and declares another dividend (JSE: ZED)

This dividend is the starter, with the future proceeds from Capespan as the main course

Zeder has been on a classic “value unlock” journey, which means selling off assets and returning cash to shareholders. This works when the share price is trading at a discount to net asset value (NAV) per share. Based on the results for the six months to August, the NAV per share is R2.62 and the share price closed 5.4% higher at R1.72. So, there’s still a gap.

To help close that gap, a special dividend of 10 cents per share has been declared. This is just a teaser for what is to come, as the company is selling Capespan (excluding the Pome Farming Unit) to 3 Sisters. Zeder holds 92.98% in Capespan and will receive R511 million in proceeds. On a market cap of R2.5 billion, that’s a decent chunk of money that has mostly been earmarked for a future distribution to shareholders.

Along with the Pome Farming Unit that is being retained, Zeder will then focus on growing the remaining investee companies. This makes it sound like much of the value unlock strategy has already played out, so it’s by no means a guarantee that the remaining discount to NAV will close.

Little Bites:

Director dealings:

Guess what? Des de Beer has bought R2.7 million worth of shares in Lighthouse Properties (JSE: LTE).

The spouse of the CEO of Calgro M3 (JSE: CGR) has bought shares worth R270k.

To assist with the successful implementation of the deal with the Government Employees Pension Fund, two non-executive directors of Attacq (JSE: ATT) will no longer be retiring this year as was previously communicated.

enX Group (JSE: ENX) has renewed the cautionary announcement related to the possible disposal of the interest in Eqstra Investment Holdings. Negotiations are ongoing.

The yield is tiny, but it’s still worth noting that holders of N shares in Prosus (JSE: PRX) will receive a 7 euro cents distribution in the form of a capital repayment. It is possible to elect to receive a dividend rather than a capital repayment instead, with different tax considerations.

Delta Property Fund (JSE: DLT) is still in a fight for survival. It’s therefore good to see something positive out of the company, with Alex Phakati (who has loads of experience in the property sector) joining the board.

The Ghost Wrap podcast is proudly brought to you by Mazars, a leading international audit, tax and advisory firm with a national footprint within South Africa. Visit the Mazars website for more information.

In this episode of Ghost Wrap, I recapped a week’s worth of news across a variety of sectors:

PSG Financial Services is making a strong case for itself as an attractive option on the local market.

MiX Telematics has attracted an international suitor and the merged entity would be listed on the JSE, so that’s exciting news.

Karooooo will be sticking to its knitting going forward and that’s a good thing.

CMH is on the wrong side of a car market that is finally cracking, with the car hire business doing a lot better than automotive retail.

Sasfin has managed to offload two business units off to African Bank at a juicy price, leading to a major rally in the Sasfin share price.

Cashbuild continues to struggle, with revenue flat year-on-year.

Calgro M3 released solid results that also show the benefit of share buybacks when used properly.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

")

")

")

")

")